Exhibit 13.1

ANNUAL REPORT

CONTENTS

| 1 | ||||

| 4 | ||||

| 4 | ||||

| 5 | ||||

| 19 | ||||

| Financial Statements |

||||

| 24 | ||||

| 25 | ||||

| 27 | ||||

| 30 | ||||

| 31 | ||||

| 32 | ||||

| 33 | ||||

| 34 | ||||

| 36 | ||||

This page left blank intentionally.

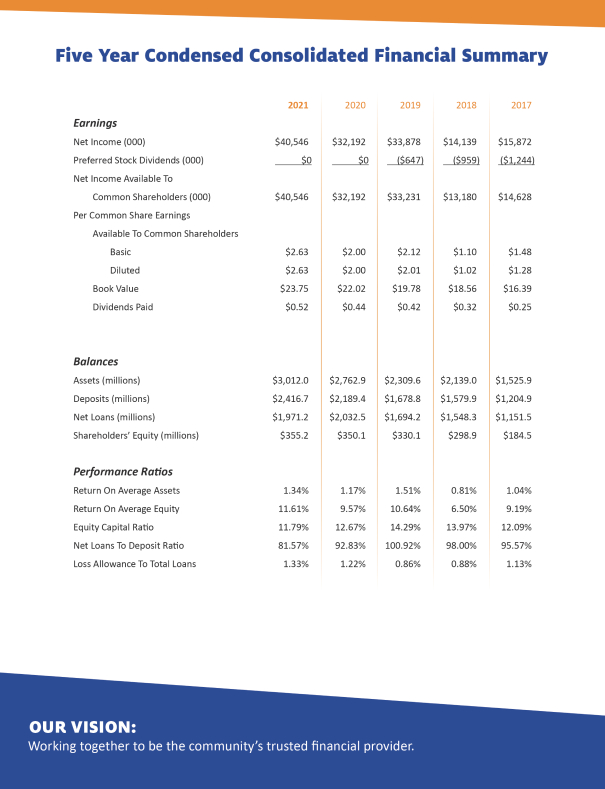

Five-Year Selected Consolidated Financial Data

(Amounts in thousands, except per share data)

Year ended December 31, |

||||||||||||||||||||

2021 |

2020 |

2019 |

2018 |

2017 |

||||||||||||||||

| Statements of income: |

||||||||||||||||||||

| Total interest and dividend income |

$ | 101,742 | $ | 99,865 | $ | 98,054 | $ | 73,677 | $ | 58,594 | ||||||||||

| Total interest expense |

6,317 | 10,138 | 12,954 | 7,570 | 4,092 | |||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|||||||||||

| Net interest income |

95,425 | 89,727 | 85,100 | 66,107 | 54,502 | |||||||||||||||

| Provision for loan losses |

830 | 10,112 | 1,035 | 780 | — | |||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|||||||||||

| Net interest income after provision for loan losses |

94,595 | 79,615 | 84,065 | 65,327 | 54,502 | |||||||||||||||

| Net gain (loss) on sale of securities |

1,786 | 94 | 32 | (413 | ) | 12 | ||||||||||||||

| Other noninterest income |

29,666 | 28,088 | 22,411 | 18,544 | 16,322 | |||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|||||||||||

| Total noninterest income |

31,452 | 28,182 | 22,443 | 18,131 | 16,334 | |||||||||||||||

| Total noninterest expense |

78,484 | 70,665 | 66,947 | 66,679 | 48,604 | |||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|||||||||||

| Income before federal income taxes |

47,563 | 37,132 | 39,561 | 16,779 | 22,232 | |||||||||||||||

| Federal income tax expense |

7,017 | 4,940 | 5,683 | 2,640 | 6,360 | |||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income |

$ | 40,546 | $ | 32,192 | $ | 33,878 | $ | 14,139 | $ | 15,872 | ||||||||||

| |

|

|

|

|

|

|

|

|

|

|||||||||||

| Preferred stock dividends and discount accretion |

— | — | 647 | 959 | 1,244 | |||||||||||||||

| Allocation of earnings and dividends to participating securities |

173 | 98 | 87 | — | — | |||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|||||||||||

| Net income available to common shareholders |

$ | 40,373 | $ | 32,094 | $ | 33,144 | $ | 13,180 | $ | 14,628 | ||||||||||

| |

|

|

|

|

|

|

|

|

|

|||||||||||

| Per common share: |

||||||||||||||||||||

| Net income available to common shareholders (basic) |

2.63 | 2.00 | 2.12 | 1.10 | 1.48 | |||||||||||||||

| Net income available to common shareholders (diluted) |

2.63 | 2.00 | 2.01 | 1.02 | 1.28 | |||||||||||||||

| Dividends declared |

0.52 | 0.44 | 0.42 | 0.32 | 0.25 | |||||||||||||||

| Book value |

23.75 | 22.02 | 19.78 | 18.56 | 16.39 | |||||||||||||||

| Average common shares outstanding: |

||||||||||||||||||||

| Basic |

15,353,215 | 16,080,863 | 15,612,868 | 11,971,786 | 9,906,856 | |||||||||||||||

| Diluted |

15,343,215 | 16,080,863 | 16,851,740 | 13,855,706 | 12,352,616 | |||||||||||||||

| Year-end balances: |

||||||||||||||||||||

| Loans, net |

$ | 1,971,238 | $ | 2,032,474 | $ | 1,694,203 | $ | 1,548,262 | $ | 1,151,527 | ||||||||||

| Securities |

577,957 | 384,887 | 379,970 | 368,385 | 245,309 | |||||||||||||||

| Total assets |

3,011,983 | 2,762,918 | 2,309,557 | 2,138,954 | 1,525,857 | |||||||||||||||

| Deposits |

2,416,701 | 2,189,398 | 1,678,764 | 1,579,893 | 1,204,923 | |||||||||||||||

| Borrowings |

203,308 | 183,341 | 274,601 | 245,226 | 123,082 | |||||||||||||||

| Shareholders’ equity |

355,212 | 350,108 | 330,126 | 298,898 | 184,461 | |||||||||||||||

| Average balances: |

||||||||||||||||||||

| Loans, net |

$ | 2,026,907 | $ | 1,953,472 | $ | 1,598,991 | $ | 1,261,568 | $ | 1,095,956 | ||||||||||

| Securities |

450,599 | 386,703 | 372,886 | 273,998 | 234,249 | |||||||||||||||

| Total assets |

3,032,382 | 2,754,708 | 2,241,111 | 1,742,823 | 1,526,387 | |||||||||||||||

| Deposits |

2,422,938 | 2,078,454 | 1,689,801 | 1,341,860 | 1,236,663 | |||||||||||||||

| Borrowings |

156,206 | 288,551 | 208,932 | 167,752 | 101,880 | |||||||||||||||

| Shareholders’ equity |

349,203 | 336,461 | 318,306 | 217,371 | 172,763 | |||||||||||||||

1

Five-Year Selected Ratios

Year ended December 31, |

||||||||||||||||||||

2021 |

2020 |

2019 |

2018 |

2017 |

||||||||||||||||

| Net interest margin (1) |

3.47 | % | 3.70 | % | 4.31 | % | 4.21 | % | 4.01 | % | ||||||||||

| Return on average total assets |

1.34 | 1.17 | 1.51 | 0.81 | 1.04 | |||||||||||||||

| Return on average shareholders’ equity |

11.61 | 9.57 | 10.64 | 6.50 | 9.19 | |||||||||||||||

| Dividend payout ratio |

19.77 | 22.00 | 19.81 | 29.09 | 16.89 | |||||||||||||||

| Average shareholders’ equity as a percent of average total assets |

11.52 | 12.21 | 14.20 | 12.47 | 11.32 | |||||||||||||||

| Net loan charge-offs (recoveries) as a percent of average total loans |

(0.04 | ) | (0.01 | ) | (0.00 | ) | 0.02 | 0.02 | ||||||||||||

| Allowance for loan losses as a percent of loans at year-end |

1.33 | 1.22 | 0.86 | 0.88 | 1.13 | |||||||||||||||

| Shareholders’ equity as a percent of total year-end assets |

11.79 | 12.67 | 14.29 | 13.97 | 12.09 | |||||||||||||||

| (1) | Calculated on a tax-equivalent basis using an effective tax rate of 21% for 2021, 2020, 2019 and 2018 and 35% for 2017. |

Shareholder Return Performance

Set forth below is a line graph comparing the five-year cumulative return of the common shares of Civista Bancshares, Inc. (ticker symbol CIVB), based on an initial investment of $100 on December 31, 2016 and assuming reinvestment of dividends, with the cumulative return of the Standard & Poor’s 500 Index, the NASDAQ Bank Index and the S&P U.S. BMI Banks Index. The comparative indices were obtained from SNL Securities and NASDAQ.

Annual Report on Form 10-K

A copy of the Company’s Annual Report on Form 10-K, as filed with the Securities and Exchange Commission, will be furnished, free of charge, to shareholders, upon written request to Lance A. Morrison, Secretary of Civista Bancshares, Inc., 100 East Water Street, Sandusky, Ohio 44870.

2

This page left blank intentionally.

3

Common Shares and Shareholder Matters

The common shares of Civista Bancshares, Inc. (“CBI”) trade on The NASDAQ Capital Market under the symbol “CIVB”. As of February 24, 2022, there were

14,888,915

common shares outstanding and held by approximately 1,502 shareholders of record (not including the number of persons or entities holding stock in nominee or street name through various brokerage firms).

CBI paid quarterly dividends on its common shares in the aggregate amounts of $0.52 per share and $0.44 per share in 2021 and 2020, respectively. The Company presently anticipates continuing to pay quarterly dividends in the future at similar levels, subject to compliance with applicable restrictions on the payment of dividends as discussed in the “Liquidity and Capital Resources” section of the Management’s Discussion and Analysis of Financial Condition and Results of Operations and in Note 18 to the Consolidated Financial Statements.

General Development of Business

(Amounts in thousands)

CBI was organized under the laws of the State of Ohio on February 19, 1987 and is a registered financial holding company under the Gramm-Leach-Bliley Financial Modernization Act of 1999, as amended. CBI and its subsidiaries are sometimes referred to together as the “Company”. The Company’s office is located at 100 East Water Street, Sandusky, Ohio. The Company had total consolidated assets of $3,011,983 at December 31, 2021.

CIVISTA BANK (“Civista”), owned by CBI since 1987, opened for business in 1884 as The Citizens National Bank. In 1898, Civista was reorganized under Ohio banking law and was known as The Citizens Bank and Trust Company. In 1908, Civista surrendered its trust charter and began operation as The Citizens Banking Company. The name Civista Bank was introduced during the first quarter of 2015 to solidify our dual Citizens/Champaign brand and distinguish ourselves from the many other banks using the “Citizens” name in our existing and prospective markets. Civista maintains its main office at 100 East Water Street, Sandusky, Ohio and operates branch banking offices in the following Ohio communities: Sandusky (2), Norwalk (2), Berlin Heights, Huron, Port Clinton, Castalia, New Washington, Shelby (2), Willard, Greenwich, Plymouth, Shiloh, Akron, Dublin, Plain City, Russells Point, Urbana (2), West Liberty, Quincy, Dayton (3), Beachwood, and in the following Indiana communities: Lawrenceburg (3), Aurora, West Harrison, Milan, Osgood and Versailles. Civista also operates loan production offices in Westlake, Ohio and Fort Mitchell, Kentucky. Civista accounted for 99.8% of the Company’s consolidated assets at December 31, 2021.

FIRST CITIZENS INSURANCE AGENCY INC. (“FCIA”) was formed to allow the Company to participate in commission revenue generated through its third party insurance agreement. Assets of FCIA were less than one percent of the Company’s consolidated assets as of December 31, 2021.

WATER STREET PROPERTIES, INC. (“WSP”) was formed to hold properties repossessed by CBI subsidiaries. WSP accounted for less than one percent of the Company’s consolidated assets as of December 31, 2021.

FC REFUND SOLUTIONS, INC. (“FCRS”) was formed during 2012 to facilitate payment of individual state and federal income tax refunds. The operations of FCRS were discontinued June 30, 2019 as a result of inactivity due to FCRS no longer being necessary to facilitate the Company’s continuing participation in the tax refund processing program.

FIRST CITIZENS INVESTMENTS, INC. (“FCI”) is wholly-owned by Civista and holds and manages its securities portfolio. The operations of FCI are located in Wilmington, Delaware.

FIRST CITIZENS CAPITAL LLC (“FCC”) is wholly-owned by Civista and holds inter-company debt that is eliminated in consolidation. The operations of FCC were discontinued December 31, 2021 as a result of inactivity.

CIVB RISK MANAGEMENT, INC. (“CRMI”) is a wholly-owned captive insurance company formed in 2017 which insures against certain risks unique to the operations of the Company and its subsidiaries and for which insurance may not be currently available or economically feasible in today’s insurance marketplace. Assets of CRMI were less than one percent of the Company’s consolidated assets as of December 31, 2021.

4

Management’s Discussion and Analysis of Financial Condition and Results of Operations—As of December 31, 2021 and December 31, 2020 and for the Years Ended December 31, 2021, 2020 and 2019

(Amounts in thousands, except per share data)

General

The following paragraphs more fully discuss the significant highlights, changes and trends as they relate to the Company’s financial condition, results of operations, liquidity and capital resources as of December 31, 2021 and 2020, and during the three-year period ended December 31, 2021. This discussion should be read in conjunction with the Consolidated Financial Statements and Notes to the Consolidated Financial Statements, which are included elsewhere in this report.

Forward-Looking Statements

This report may contain “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”), and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), relating to such matters as financial condition, anticipated operating results, cash flows, business line results, credit quality expectations, prospects for new lines of business, economic trends (including interest rates) and similar matters. Forward-looking statements reflect our expectations, estimates or projections concerning future results or events. These statements are generally identified by the use of forward-looking words or phrases such as “believe,” “belief,” “expect,” “anticipate,” “may,” “could,” “intend,” “intent,” “estimate,” “plan,” “foresee,” “likely,” “will,” “should” or other similar words or phrases. Forward-looking statements are not guarantees of performance and are inherently subject to known and unknown risks, uncertainties and assumptions that are difficult to predict and could cause our actual results, performance or achievements to differ materially from those expressed in or implied by the forward-looking statements. Factors that could cause actual results, performance or achievements to differ from those discussed in the forward-looking statements include, but are not limited to, impacts on our business, financial condition and results of operations resulting from the ongoing COVID-19 pandemic, including government regulations and stimulus programs related thereto; changes in financial markets or national or local economic or political conditions; adverse changes in the real estate market; volatility and direction of market interest rates; the transition away from LIBOR as a reference rate for financial contracts; credit risks of lending activities; operational risks; changes in the allowance for loan losses; legislation or regulatory changes or actions; increases in FDIC insurance premiums and assessments; changes in tax laws or examinations or challenges by tax authorities; accounting changes; inability to raise additional capital if and when needed in the future; unexpected losses of key management; failure, interruption or breach of security of our communications and information systems or those of our third party service providers; unforeseen litigation; increased competition in our market area; failures to manage growth and/or effectively integrate acquisitions; fluctuations in the market price of our common shares; future revenues of our tax refund processing program; climate change, natural disasters, acts of war or terrorism, and other external events; and other risks identified from time-to-time in the Company’s other public documents on file with the Securities and Exchange Commission.

The forward-looking statements included in this report are only made as of the date of this report, and we disclaim any obligation to publicly update any forward-looking statement to reflect subsequent events or circumstances, except as required by law.

The Private Securities Litigation Reform Act of 1995 provides a safe harbor for forward-looking statements, and the purpose of this section is to secure the use of the safe harbor provisions.

Financial Condition

At December 31, 2021, the Company’s total assets were $3,011,983, compared to $2,768,862 at December 31, 2020. The increase in assets is primarily the result of increases in cash and due from financial institutions and securities available for sale, offset by decreases in loans held for sale, loans and swap assets. Other factors contributing to the change in assets are discussed in the following sections.

5

Loans held for sale decreased $5,029, or 71.8%, from $7,001 at December 31, 2020 to $1,972 at December 31, 2021. The decrease is due to a decrease in refinances, resulting in lower volume. At December 31, 2021, 14 loans totaling $1,972 were held for sale as compared to 29 loans totaling $7,001 at December 31, 2020.

At December 31, 2021, the Company’s net loans totaled $1,971,238 and decreased by 3.0% from $2,032,474 at December 31, 2020. The decrease in net loans was spread across most segments. Commercial & Agriculture loans decreased $163,374, Residential Real Estate loans decreased $12,528, Real Estate Construction loans decreased $18,482, Farm Real Estate loans decreased $4,683 and Consumer and Other loans decreased $1,833. The decrease in Commercial & Agriculture loans is the result of forgiveness of Paycheck Protection Program (“PPP”) loans totaling $177,035 at December 31, 2021. The decreases in the foregoing loan segments were offset by increases in Commercial Real Estate – Owner Occupied loans of $17,039 and Commercial Real Estate - Non-Owner Occupied loans of $124,238.

Securities available for sale increased by $196,410, or 54.0%, from $363,464 at December 31, 2020 to $559,874 at December 31, 2021. U.S. Treasury securities and obligations of U.S. government agencies increased $26,197, or 120.8% from $21,693 at December 31, 2020 to $47,890 at December 31, 2021. Obligations of states and political subdivisions available for sale increased by $69,824 from 2020 to 2021. Mortgage-backed securities increased by $100,389 to total $213,148 at December 31, 2021. The Company continues to utilize letters of credit from the Federal Home Loan Bank (FHLB) to replace maturing securities that were pledged for public entities. As of December 31, 2021, the Company was in compliance with all applicable pledging requirements.

Mortgage-backed securities totaled $213,148 at December 31, 2021 and none were considered unusual or “high risk” securities as defined by regulatory authorities. Of this total, $208,289 consisted of pass-through securities issued by the Federal National Mortgage Association (“FNMA”), Federal Home Loan Mortgage Corporation (“FHLMC”), and Government National Mortgage Association (“GNMA”), and $4,859 of these securities were collateralized by mortgage-backed securities issued or guaranteed by FNMA, FHLMC, or GNMA. The average interest rate of the mortgage-backed securities portfolio at December 31, 2021 was 2.4%. The average maturity at December 31, 2021 was approximately 7.8 years.

Securities available for sale had a fair value at December 31, 2021 of $559,874. This fair value includes unrealized gains of approximately $20,664 and unrealized losses of approximately $2,087. Net unrealized gains totaled $18,577 on December 31, 2021 compared to net unrealized gains of $27,148 on December 31, 2020. The change in unrealized gains is primarily due to changes in market interest rates. Note 2 to the Consolidated Financial Statements provides additional information on unrealized gains and losses.

Premises and equipment, net of accumulated depreciation, decreased $135 from December 31, 2020 to December 31, 2021. The decrease is the result of new purchases of $1,927, offset by disposals of $13, depreciation of $1,976 and transfers to available for sale of $73.

Accrued interest receivable decreased $2,036, or 21.6% from December 31, 2020 to December 31, 2021. The decrease is the result of COVID-19 pandemic related loan modifications returning to principal and/or interest payments.

Swap assets decreased $10,628 from December 31, 2020 to December 31, 2021. The decrease is primarily the result of decreases in the fair value of swap assets as compared to December 31, 2020.

Bank owned life insurance (BOLI) increased $665 from December 31, 2020 to December 31, 2021. The difference is the result of increases in the cash surrender value of the underlying insurance policies, offset by a redemption of $535 from death benefits.

Other assets increased $2,497 from December 31, 2020 to December 31, 2021. The increase is primarily the result of the recording of receivables with respect to $1,000 of AMT tax credits as a result of amending prior year tax returns and $535 for BOLI death claims receivable.

6

Year-end deposit balances totaled $2,416,701 in 2021 compared to $2,189,398 in 2020, an increase of $277,303, or 10.4%. Overall, the increase in deposits at December 31, 2021 compared to December 31, 2020 included increases in noninterest bearing demand deposits of $68,097, or 9.4%, interest bearing demand accounts of $127,371, or 31.1%, and savings and money market accounts of $72,225, or 9.4%, offset by decreases in certificate of deposit accounts of $35,910, or 14.9%, and individual retirement accounts of $4,480, or 9.7%. Average deposit balances for 2021 were $2,488,105 compared to $2,078,454 for 2020, an increase of 19.7%. Noninterest bearing deposits averaged $907,591 for 2021, compared to $739,648 for 2020, increasing $167,943, or 22.7%. Savings, NOW, and MMDA accounts averaged $1,315,220 for 2021 compared to $1,050,544 for 2020. Average certificates of deposit decreased $22,968 to total an average balance of $265,294 for 2021. The increase in year over year average balances was impacted by the COVID-19 pandemic as the Company’s participation in originating PPP loans resulted in loan proceeds being deposited by borrowers into deposit accounts at Civista and customer deposits of stimulus checks and unemployment benefits also increased average deposit balances in 2021.

Borrowings from the FHLB of Cincinnati were $75,000 at December 31, 2021 compared to $125,000 at December 31, 2020, a decrease of $50,000. During the second quarter of 2021, the Company prepaid a $50,000 advance with a rate of 2.05% and a remaining maturity of approximately 8 years at a pre-tax loss of approximately $3,717. The prepayment penalty of $3,717 was recorded in other operating expenses on the Consolidated Statements of Operations. Additional detail regarding these borrowings can be found in Note 9 and Note 10 to the Consolidated Financial Statements.

Civista offers repurchase agreements in the form of sweep accounts to commercial checking account customers. These repurchase agreements totaled $25,495 at December 31, 2021 compared to $28,914 at December 31, 2020. U.S. Treasury securities and obligations of U.S. government agencies maintained under Civista’s control are pledged as collateral for the repurchase agreements. Additional detail related to these repurchase agreements can be found in Note 11 to the Consolidated Financial Statements.

Subordinated debentures were $102,813 at December 31, 2021 compared to $29,427 at December 31, 2020, an increase of $73,386. During the fourth quarter of 2021, the Company sold and issued $75,000 aggregate principal amount of its 3.25% Fixed-to-Floating Rate Subordinated Notes due 2031. Net proceeds from the sale of these subordinated notes was $73,386. Additional detail regarding the subordinated notes can be found in Note 12 to the Consolidated Financial Statements.

Swap liabilities decreased $10,692 from December 31, 2020 to December 31, 2021. The decrease is primarily the result of decreases in the fair value of swap liabilities as compared to December 31, 2020.

Total shareholders’ equity increased $5,104, or 1.5%, during 2021 to $355,212. The change in shareholders’ equity resulted from net income of $40,546, an increase in the Company’s pension liability, net of tax, of $973, a decrease in the fair value of securities available for sale, net of tax, of $6,772 and decreases due to the purchase of treasury shares and dividends on common shares of $22,309 and $8,036, respectively. Additionally, $702 was recognized as stock-based compensation in 2021 in connection with the grant of restricted common shares. For further explanation of these items, see Note 1, Note 14 and Note 15 to the Consolidated Financial Statements. The Company paid $0.52 per common share in dividends in 2021 compared to $0.44 per common share in dividends in 2020. Total outstanding common shares at December 31, 2021 were 14,954,200.

Total outstanding common shares at December 31, 2020 were 15,898,032. The decrease in common shares outstanding is the result of the repurchase of 988,465 common shares at an average repurchase price of $22.57. The Company repurchased 239,536 common shares pursuant to a stock repurchase program announced on May 4, 2020, which authorized the Company to repurchase a maximum aggregate value of $13,500 of the Company’s common shares until April 20, 2021. The Company repurchased 562,489 common shares pursuant to a stock repurchase program announced on April 20, 2021, which authorized the Company to repurchase a maximum aggregate value of $13,500 of the Company’s common shares until April 19, 2022. Finally, the

7

Company repurchased 181,375 common shares pursuant to a stock repurchase program announced August 12, 2021, which replaced the April 20, 2021 repurchase program and authorizes the Company to repurchase up to a maximum of $13,500 of the Company’s common shares until August 10, 2022. An additional 5,065 common shares were surrendered by officers in 2021 to pay taxes upon vesting of restricted shares, and 3,298 restricted common shares were forfeited during the period. The decrease in common shares outstanding was offset by the grant of 39,139 restricted common shares to certain officers under the Company’s 2014 Incentive Plan and the grant of 8,792 common shares to directors of Civista as a retainer for their service. The ratio of total shareholders’ equity to total assets was 11.8% and 12.7%, at December 31, 2021 and 2020, respectively.

Results of Operations

The operating results of the Company are affected by general economic conditions, the monetary and fiscal policies of federal agencies and the regulatory policies of agencies that regulate financial institutions. The Company’s cost of funds is influenced by interest rates on competing investments and general market rates of interest. Lending activities are influenced by the demand for real estate loans and other types of loans, which in turn is affected by the interest rates at which such loans are made, general economic conditions and the availability of funds for lending activities.

The Company’s net income primarily depends on its net interest income, which is the difference between the interest income earned on interest-earning assets, such as loans and securities, and interest expense incurred on interest-bearing liabilities, such as deposits and borrowings. The level of net interest income is dependent on the interest rate environment and the volume and composition of interest-earning assets and interest-bearing liabilities. Net income is also affected by provisions for loan losses, service charges, gains on the sale of assets, other non-interest income, noninterest expense and income taxes.

Comparison of Results of Operations for the Years Ended December 31, 2021 and December 31, 2020

Net Income

The Company’s net income for the year ended December 31, 2021 was $40,546, compared to $32,192 for the year ended December 31, 2020. The change in net income was the result of the items discussed in the following sections.

Net Interest Income

Net interest income for 2021 was $95,425, an increase of $5,698, or 6.4%, from 2020. From 2020 to 2021, average earning assets increased 13.2%, interest income increased $1,877, and interest expense on interest-bearing liabilities decreased $3,821. The Company continually examines its rate structure to ensure that its interest rates are competitive and reflective of the current rate environment in which it competes.

Total interest income increased $1,877 to $101,742 for the year ended December 31, 2021, which is attributable to an increase of $1,793 in interest and fees on loans. This change was the result of an increase in the average balance of loans, accompanied by a slightly lower yield on the portfolio. The average balance of loans increased by $73,435, or 3.8%, to $2,026,907 for the year ended December 31, 2021, as compared to $1,953,472 for the year ended December 31, 2020. The loan yield decreased to 4.42% for 2021, from 4.49% in 2020.

Interest on taxable securities increased $114 to $5,473 for the year ended December 31, 2021, compared to $5,359 for the same period in 2020. The average balance of taxable securities increased $49,092 to $232,813 for the year ended December 31, 2021, as compared to $183,721 for the year ended December 31, 2020. The yield on taxable securities decreased 62 basis points to 2.41% for 2021, compared to 3.03% for 2020. Interest on tax-exempt securities increased $127 to $6,250 for the year ended December 31, 2021, compared to $6,123 for the same period in 2020. The average balance of tax-exempt securities increased $14,804 to $217,786 for the year ended December 31, 2021 as compared to $202,982 for the year ended December 31, 2020. The yield on tax-exempt securities decreased 19 basis points to 3.96% for 2021, compared to 4.15% for 2020.

8

Total interest expense decreased $3,821 or 37.7% to $6,317 for the year ended December 31, 2021, compared with $10,138 for the same period in 2020. The decrease in interest expense can be attributed to a decrease in the average rate paid, partially offset by an increase in the average balance of interest-bearing liabilities. For the year ended December 31, 2021, the average balance of interest-bearing liabilities increased $109,363 to $1,736,720, as compared to $1,627,357 for the year ended December 31, 2020. Interest incurred on deposits decreased by $2,706 to $4,175 for the year ended December 31, 2021, compared to $6,881 for the same period in 2020. The decrease in deposit expense was due to a decrease in the average rate paid, as the average rate paid on demand and savings accounts decreased from 0.17% in 2020 to 0.09% in 2021 and the average rate paid on time deposits decreased from 1.76% to 1.11% in 2021, which was partially offset by an increase in the average balance of interest-bearing deposits of $241,708 for the year ended December 31, 2021 as compared to the same period in 2020. Interest expense incurred on FHLB advances and subordinated debentures decreased 26.4% from 2020. The decrease was due to a $32,674 decrease in average balance from 2020 and a decrease in rate from 2020. The average balance of other borrowings decreased $101,295 for the period ended December 31, 2021 as compared to the same period in 2020 as a result of the Company’s repayment of amounts borrowed under the Paycheck Protection Program Liquidity Facility (“PPPLF”) to fund PPP loans.

Refer to “Distribution of Assets, Liabilities and Shareholders’ Equity; Interest Rates and Interest Differential” and “Changes in Interest Income and Interest Expense Resulting from Changes in Volume and Changes in Rate” on pages 14 through 16 for further analysis of the impact of changes in interest-bearing assets and liabilities on the Company’s net interest income.

Provision and Allowance for Loan Losses

The following table contains information relating to the provision for loan losses, activity in and analysis of the allowance for loan losses as of and for each of the three years in the period ended December 31.

As of and for year ended December 31, |

||||||||||||

2021 |

2020 |

2019 |

||||||||||

| Net loan charge-offs (recoveries) |

$ | (783 | ) | $ | (149 | ) | $ | (53 | ) | |||

| Provision for loan losses charged to expense |

830 | 10,112 | 1,035 | |||||||||

| Net loan charge-offs (recoveries) as a percent of average outstanding loans |

(0.04 | )% | (0.01 | )% | (0.00 | )% | ||||||

| Allowance for loan losses |

$ | 26,641 | $ | 25,028 | $ | 14,767 | ||||||

| Allowance for loan losses as a percent of year-end outstanding loans |

1.33 | % | 1.22 | % | 0.86 | % | ||||||

| Impaired loans, excluding purchase credit impaired loans (PCI) |

$ | 1,222 | $ | 2,666 | $ | 3,597 | ||||||

| Impaired loans as a percent of gross year-end loans (1) |

0.06 | % | 0.13 | % | 0.21 | % | ||||||

| Nonaccrual and 90 days or more past due loans, excluding PCI |

$ | 3,673 | $ | 5,125 | $ | 5,599 | ||||||

| Nonaccrual and 90 days or more past due loans, excluding PCI as a percent of gross year-end loans (1) |

0.18 | % | 0.25 | % | 0.33 | % | ||||||

| (1) | Nonaccrual loans and impaired loans are defined differently. Some loans may be included in both categories, whereas other loans may only be included in one category. A loan is considered nonaccrual if it is maintained on a cash basis because of deterioration in the borrower’s financial condition, where payment in full of principal or interest is not expected and where the principal and interest have been in default for 90 days, unless the asset is both well-secured and in process of collection. A loan is considered impaired when it is probable that all of the interest and principal due will not be collected according to the terms of the original contractual agreement. |

9

The Company’s policy is to maintain the allowance for loan losses at a level sufficient to provide for probable losses incurred in the current portfolio. Management believes the analysis of the allowance for loan losses supported a reserve of $26,641 at December 31, 2021. The Company provides for loan losses through regular provisions to the allowance for loan losses as necessary. The amount of the provision is affected by loan charge-offs, recoveries and changes in specific and general allocations required for the allowance for loan losses. A number of factors impact the provisions for loan losses, such as the level of higher risk loans in the portfolio, changes in practices related to loans, changes in collateral values and other factors. We continue to actively manage this process and have provided to maintain the reserve at a level that assures adequate coverage ratios.

Provisions for loan losses totaled $830, $10,112 and $1,035 in 2021, 2020 and 2019, respectively. The Company’s provision for loan losses decreased $9,282 during 2021, as compared to 2020. The decrease in the provision was due to the stability of our credit quality metrics coupled with the stabilization and, in some cases, improvement of international, national, regional and local economic conditions that were adversely impacted by the 2020 economic shutdown and restrictions in response to the ongoing COVID-19 pandemic. While vaccinations and booster shots in 2021 have created some level of optimism in the business community, there remains uncertainty due to the continued concern over increased infections from the Delta and Omicron variants of COVID. We remain cautious given the level of classified loans in the portfolio, particularly loans to borrowers in the hotel industry as well as the challenges businesses face in today’s environment. The lingering economic impacts related to the COVID-19 pandemic have included the loss of revenue experienced by our business clients, disruption of supply chains, higher employee wages coupled with workforce shortages and increased costs of materials and services. While some of the pressures have eased, ongoing supply chain and staffing challenges, as well as inflationary pressures remain. Our Commercial and Commercial Real Estate portfolios have been, and are expected to continue to be, impacted the most.

Efforts are continually made to analyze each segment of the loan portfolio and quantify risk to assure that reserves are appropriate for each segment and the overall portfolio. Management specifically evaluates loans that are impaired, which includes restructured loans, to estimate potential loss. This analysis includes a review of the loss migration calculation for all loan categories as well as fluctuations and trends in various risk factors that have occurred within the portfolios’ economic life cycle. The analysis also includes assessment of qualitative factors such as credit trends, unemployment trends, vacancy trends and loan growth. The composition and overall level of the loan portfolio and charge-off activity are also factors used to determine the amount of the allowance for loan losses.

Management analyzes each impaired commercial and commercial real estate loan relationship with a balance of $350 or larger, on an individual basis and when it is in nonaccrual status or when an analysis of the borrower’s operating results and financial condition indicates that underlying cash flows are not adequate to meet its debt service requirements. Loans held for sale and leases are excluded from consideration as impaired. Loans are generally moved to nonaccrual status when 90 days or more past due. Impaired loans or portions thereof are charged-off when deemed uncollectible.

Noninterest Income

Noninterest income increased $3,270, or 11.6%, to $31,452 for the year ended December 31, 2021, from $28,182 for the comparable 2020 period. The increase was primarily due to increases in service charges of $617, net gain on sale of securities of $1,692, net gain (loss) on equity securities of $243, ATM/Interchange fees of $971, wealth management fees of $876, BOLI income of $223 and other noninterest income of $498, which were partially offset by decreases in net gain on sale of loans of $521 and swap fees of $1,252.

Service charges increased due to increased account service charges and overdraft fees of $510 and $107, respectively. Net gain on sale of securities increased due to the sale of Visa Class B shares, which resulted in a gain of $1,785. Management, from time to time, will reposition the investment portfolio to match liquidity needs of the Company. Net gain (loss) on equity securities increased as a result of market value increases. Net gain on sale of loans decreased primarily as a result of a decrease in volume of loans sold. During the twelve-months

10

ended December 31, 2021, 1,341 loans were sold, totaling $260,294. During the twelve-months ended December 31, 2020, 1,575 loans were sold, totaling $304,026. ATM/Interchange fees increased as a result of increased transaction fees and MasterCard fees. Wealth management fees increased primarily as a result of an increase in trust and brokerage fees of $633 and $243, respectively. Trust income increased as a result of new accounts and market conditions while brokerage income increased due to volume of business. BOLI income increased due to death benefits paid. Swap fees decreased due to the volume of swaps performed during the twelve-months ended December 31, 2021 as compared to the same period of 2020. Other noninterest income increased due to increases in wire transfer fees, the amortization of mortgage servicing rights, merchant credit card fees and gains on the sale of OREO properties.

Noninterest Expense

Noninterest expense increased $7,819, or 11.1%, to $78,484 for the year ended December 31, 2021, from $70,665 for the comparable 2020 period. The increase was primarily due to increases in compensation expense of $2,210, FDIC assessments of $328, state franchise tax of $271, ATM/Interchange expense of $446, software maintenance expense of $922 and other operating expense of $3,905.

The increase in compensation expense was due to increased payroll, payroll taxes, employee insurance and employer savings contributions, offset by a decrease in commission and incentive based costs. The year-to-date average full time equivalent (FTE) employees were 451.8 at December 31, 2021, a decrease of 1.6 FTEs over 2020. Payroll and payroll related expenses increased due to annual pay increases. The year-over-year increase in FDIC assessments was attributable to small bank assessment credits applied to the 2020 assessment charges. The state franchise tax increase is related to $172 of additional taxes paid on the Company’s 2019 franchise tax return as a result of findings from a State of Ohio audit. The increase in ATM/Interchange expense is primarily due to increased transaction fees and a settlement received in the second quarter of 2020. The increase in software maintenance expense is due to a general increase in legacy software maintenance contracts and the implementation of our new digital banking. The increase in other operating expense is primarily due to the prepayment expense of $3,717 related to the early payoff of an FHLB long-term advance.

Income Tax Expense

Income tax expense was $7,017 in 2021 compared to $4,940 in 2020. Income tax expense as a percentage of pre-tax income was 14.8% in 2021 compared to 13.3% in 2020. A lower federal effective tax rate than the statutory rate of 21% in 2021 and 2020 is primarily due to tax-exempt interest income from state and municipal investments, municipal loans, income from BOLI and low income housing credits.

Comparison of Results of Operations for the Years Ended December 31, 2020 and December 31, 2019

Net Income

The Company’s net income for the year ended December 31, 2020 was $32,192, compared to $33,878 for the year ended December 31, 2019. The change in net income was the result of the items discussed in the following sections.

Net Interest Income

Net interest income for 2020 was $89,727, an increase of $4,627, or 5.4%, from 2019. From 2019 to 2020, average earning assets increased 23.3%, interest income increased $1,811, and interest expense on interest-bearing liabilities decreased $2,816.

Total interest income increased $1,811 to $99,865 for the year ended December 31, 2020, which is attributable to an increase of $2,805 in interest and fees on loans. This change was the result of an increase in the average balance of loans, accompanied by a lower yield on the portfolio. The average balance of loans increased by $340,497 or 21.1% to $1,953,472 for the year ended December 31, 2020, as compared to $1,612,975 for the year ended December 31, 2019. The loan yield decreased to 4.49% for 2020, from 5.27% in 2019.

11

Interest on taxable securities decreased $1,225 to $5,359 for the year ended December 31, 2020, compared to $6,584 for the same period in 2019. The average balance of taxable securities decreased $16,353 to $183,721 for the year ended December 31, 2020, as compared to $200,074 for the year ended December 31, 2019. The yield on taxable securities decreased 32 basis points to 3.03% for 2020, compared to 3.35% for 2019. Interest on tax-exempt securities increased $476 to $6,123 for the year ended December 31, 2020, compared to $5,647 for the same period in 2019. The average balance of tax-exempt securities increased $30,170 to $202,982 for the year ended December 31, 2020 as compared to $172,812 for the year ended December 31, 2019. The yield on tax-exempt securities decreased 21 basis points to 4.15% for 2020, compared to 4.36% for 2019.

Total interest expense decreased $2,816 or 21.7% to $10,138 for the year ended December 31, 2020, compared with $12,954 for the same period in 2019. The decrease in interest expense can be attributed to a decrease in the average rate paid, partially offset by an increase in the average balance of interest-bearing liabilities. For the year ended December 31, 2020, the average balance of interest-bearing liabilities increased $279,262 to $1,627,357, as compared to $1,348,095 for the year ended December 31, 2019. Interest incurred on deposits decreased by $1,176 to $6,881 for the year ended December 31, 2020, compared to $8,057 for the same period in 2019. The decrease in deposit expense was due to a decrease in the average rate paid, as the average rate paid on demand and savings accounts decreased from 0.33% in 2019 to 0.17% in 2020 and the average rate paid on time deposits decreased from 1.92% to 1.76% in 2020, partially offset by an increase in the average balance of interest-bearing deposits of $199,643 for the year ended December 31, 2020 as compared to the same period in 2019. Interest expense incurred on FHLB advances and subordinated debentures decreased 41.0% from 2019. The decrease was due to a $27,896 decrease in average balance from 2019 and a decrease in rate from 2019. The average balance of other borrowings increased $101,295 for the period ended December 31, 2020 as compared to the same period in 2019 as a result of the Company’s borrowings under the PPPLF to fund PPP loans.

Refer to “Distribution of Assets, Liabilities and Shareholders’ Equity; Interest Rates and Interest Differential” and “Changes in Interest Income and Interest Expense Resulting from Changes in Volume and Changes in Rate” on pages 14 through 16 for further analysis of the impact of changes in interest-bearing assets and liabilities on the Company’s net interest income.

Provision and Allowance for Loan Losses

Management believes the analysis of the allowance for loan losses supported a reserve of $25,028 at December 31, 2020.

Provisions for loan losses totaled $10,112 and, $1,035 in 2020 and 2019, respectively. The Company’s provision for loan losses increased $9,077 during 2020. The increase in the provision was due to an increase in Civista’s qualitative factors, primarily changes in international, national, regional and local conditions, related to the economic shutdown driven by COVID-19 and the ongoing payment deferrals on loans modified under the Coronavirus Aid Relief, and Economic Security Act (“CARES Act”).

Noninterest Income

Noninterest income increased $5,739, or 25.6%, to $28,182 for the year ended December 31, 2020, from $22,443 for the comparable 2019 period. The increase was primarily due to increases in net gain on sale of securities of $62, net gain on sale of loans of $5,856, ATM/Interchange fees of $416 and swap fees of $943, which were partially offset by decreases in service charges of $1,107, net gain (loss) on equity securities of $178 and tax refund processing fees of $375.

Net gain on sale of securities increased due to security sales. Management, from time to time, will reposition the investment portfolio to match liquidity needs of the Company. Net gain on sale of loans increased primarily as a result of an increase in volume of loans sold. During the twelve-months ended December 31, 2020, 1,575 loans were sold, totaling $304,026. During the twelve-months ended December 31, 2019, 709 loans were sold, totaling $125,796. ATM/Interchange fees increased as a result of increased transaction volume. Swap fees increased due

12

to the volume of swaps originated during the twelve-months ended December 31, 2020 as compared to the same period of 2019. Service charges decreased due to Civista waiving $93 of service fees on deposit accounts related to the COVID-19 pandemic. In addition, overdraft fees decreased during 2020. Net gain (loss) on equity securities decreased as a result of market value decreases. Additionally, the Company processes state and federal income tax refund payments for customers of third-party income tax preparation vendors for which we receive a fee for processing the refund payments. These tax refund processing fees decreased as a result of a decrease in the volume of transactions processed during 2020 as compared to 2019.

Noninterest Expense

Noninterest expense increased $3,718, or 5.6%, to $70,665 for the year ended December 31, 2020, from $66,947 for the comparable 2019 period. The increase was primarily due to increases in compensation expense of $3,324, FDIC assessments of $590 and software maintenance expense of $310, which were partially offset by decreases in equipment expense of $240 and marketing expense of $337.

The increase in compensation expense was due to increased payroll, overtime pay, 401k expenses, payroll taxes and commission and incentive based costs, offset by decreases in employee insurance costs and unemployment taxes. The year-to-date average full time equivalent (FTE) employees were 453.4 at December 31, 2020, an increase of 8.6 FTEs over 2019, which increased payroll and payroll related expenses. Payroll and payroll related expenses also increased due to annual pay increases and increases in commission based costs as the result of increased loan activity. The year-over-year increase in FDIC assessments was attributable to small bank assessment credits applied to the 2019 assessment charges. The increase in software maintenance expense is due to a general increase in software maintenance contracts. The decrease in equipment expense is due to lower equipment repair and maintenance cost. The decrease in marketing expense is due to decreases in both advertising and business promotion expenses, primarily related to the COVID-19 pandemic. Event cancellations and postponed outreach efforts contributed to the decrease as our focus was on communicating changes in operations, safety protocols, alternative delivery channels, and economic relief programs with the safety and financial wellness of our employees and customers in mind.

Income Tax Expense

Income tax expense was $4,940 in 2020 compared to $5,683 in 2019. Income tax expense as a percentage of pre-tax income was 13.3% in 2020 compared to 14.4% in 2019. A lower federal effective tax rate than the statutory rate of 21% in 2020 and 2019 is primarily due to tax-exempt interest income from state and municipal investments, municipal loans, income from BOLI and low income housing credits.

13

Distribution of Assets, Liabilities and Shareholders’ Equity;

Interest Rates and Interest Differential

The following table sets forth, for the years ended December 31, 2021, 2020 and 2019, the distribution of assets, including interest amounts and average rates of major categories of interest-earning assets and noninterest-earning assets (Amounts in thousands):

2021 |

2020 |

2019 |

||||||||||||||||||||||||||||||||||

| Assets |

Average balance |

Interest |

Yield/ rate |

Average balance |

Interest |

Yield/ rate |

Average balance |

Interest |

Yield/ rate |

|||||||||||||||||||||||||||

| Interest-earning assets: |

||||||||||||||||||||||||||||||||||||

| Loans (1)(2)(3)(5) |

$ | 2,026,907 | $ | 89,570 | 4.42 | % | $ | 1,953,472 | $ | 87,777 | 4.49 | % | $ | 1,612,975 | $ | 84,972 | 5.27 | % | ||||||||||||||||||

| Taxable securities (4) |

232,813 | 5,473 | 2.41 | % | 183,721 | 5,359 | 3.03 | % | 200,074 | 6,584 | 3.35 | % | ||||||||||||||||||||||||

| Non-taxable securities (4)(5) |

217,786 | 6,250 | 3.96 | % | 202,982 | 6,123 | 4.15 | % | 172,812 | 5,647 | 4.36 | % | ||||||||||||||||||||||||

| Interest-bearing deposits in other banks |

347,573 | 449 | 0.13 | % | 155,960 | 606 | 0.39 | % | 38,359 | 851 | 2.22 | % | ||||||||||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| Total interest earning assets |

2,825,079 | 101,742 | 3.69 | % | 2,496,135 | 99,865 | 4.10 | % | 2,024,220 | 98,054 | 4.95 | % | ||||||||||||||||||||||||

| Noninterest-earning assets: |

||||||||||||||||||||||||||||||||||||

| Cash and due from financial institutions |

35,404 | 77,848 | 47,472 | |||||||||||||||||||||||||||||||||

| Premises and equipment, net |

22,617 | 22,831 | 21,946 | |||||||||||||||||||||||||||||||||

| Accrued interest receivable |

8,010 | 9,043 | 7,088 | |||||||||||||||||||||||||||||||||

| Intangible assets |

84,747 | 84,953 | 85,744 | |||||||||||||||||||||||||||||||||

| Other assets |

36,456 | 37,675 | 24,273 | |||||||||||||||||||||||||||||||||

| Bank owned life insurance |

46,435 | 45,454 | 44,352 | |||||||||||||||||||||||||||||||||

| Less allowance for loan losses |

(26,366 | ) | (19,231 | ) | (13,984 | ) | ||||||||||||||||||||||||||||||

| |

|

|

|

|

|

|||||||||||||||||||||||||||||||

| Total |

$ | 3,032,382 | $ | 2,754,708 | $ | 2,241,111 | ||||||||||||||||||||||||||||||

| |

|

|

|

|

|

|||||||||||||||||||||||||||||||

| (1) | For purposes of these computations, the daily average loan amounts outstanding are net of unearned income and include loans held for sale. |

| (2) | Included in loan interest income are loan fees of $1,661 in 2021, $1,025 in 2020 and $1,227 in 2019. |

| (3) | Non-accrual loans are included in loan totals and do not have a material impact on the analysis presented. |

| (4) | Average balance is computed using the carrying value of securities. The average yield has been computed using the historical amortized cost average balance for available for sale securities. |

| (5) | Yield/Rate is calculated using the tax-equivalent adjustment of 21% for 2020, 2019 and 2018. |

14

Distribution of Assets, Liabilities and Shareholders’ Equity;

Interest Rates and Interest Differential (Continued)

The following table sets forth, for the years ended December 31, 2021, 2020 and 2019, the distribution of liabilities, including interest amounts and average rates of major categories of interest-bearing liabilities and shareholders’ equity (Amounts in thousands):

2021 |

2020 |

2019 |

||||||||||||||||||||||||||||||||||

| Liabilities and Shareholders’ Equity |

Average balance |

Interest |

Yield/ rate |

Average balance |

Interest |

Yield/ rate |

Average balance |

Interest |

Yield/ rate |

|||||||||||||||||||||||||||

| Interest-bearing liabilities: |

||||||||||||||||||||||||||||||||||||

| Savings and interest-bearing demand accounts |

$ | 1,315,220 | $ | 1,219 | 0.09 | % | $ | 1,050,544 | $ | 1,813 | 0.17 | % | $ | 869,340 | $ | 2,871 | 0.33 | % | ||||||||||||||||||

| Certificates of deposit |

265,294 | 2,956 | 1.11 | % | 288,262 | 5,068 | 1.76 | % | 269,823 | 5,186 | 1.92 | % | ||||||||||||||||||||||||

| Short-term Federal Home Loan Bank advances |

— | — | — | 8,151 | 134 | 1.64 | % | 112,088 | 2,600 | 2.32 | % | |||||||||||||||||||||||||

| Long-term Federal Home Loan Bank advances |

94,041 | 1,163 | 1.24 | % | 125,000 | 1,798 | 1.44 | % | 48,959 | 852 | 1.74 | % | ||||||||||||||||||||||||

| Other borrowings |

— | — | — | 101,295 | 354 | 0.35 | % | — | — | — | ||||||||||||||||||||||||||

| Securities sold under repurchase agreements |

26,165 | 23 | 0.09 | % | 24,390 | 25 | 0.10 | % | 18,321 | 19 | 0.10 | % | ||||||||||||||||||||||||

| Federal funds purchased |

137 | 1 | 0.73 | % | 288 | 1 | 0.35 | % | 137 | 3 | 2.19 | % | ||||||||||||||||||||||||

| Subordinated debentures |

35,863 | 955 | 2.66 | % | 29,427 | 945 | 3.21 | % | 29,427 | 1,423 | 4.84 | % | ||||||||||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| Total interest-bearing liabilities |

1,736,720 | 6,317 | 0.36 | % | 1,627,357 | 10,138 | 0.62 | % | 1,348,095 | 12,954 | 0.96 | % | ||||||||||||||||||||||||

| Noninterest-bearing liabilities: |

||||||||||||||||||||||||||||||||||||

| Demand deposits |

907,591 | 739,648 | 550,638 | |||||||||||||||||||||||||||||||||

| Other liabilities |

38,868 | 51,242 | 24,072 | |||||||||||||||||||||||||||||||||

| |

|

|

|

|

|

|||||||||||||||||||||||||||||||

| 946,459 | 790,890 | 574,710 | ||||||||||||||||||||||||||||||||||

| Shareholders’ equity |

349,203 | 336,461 | 318,306 | |||||||||||||||||||||||||||||||||

| |

|

|

|

|

|

|||||||||||||||||||||||||||||||

| Total |

$ | 3,032,382 | $ | 2,754,708 | $ | 2,241,111 | ||||||||||||||||||||||||||||||

| |

|

|

|

|

|

|||||||||||||||||||||||||||||||

| Net interest income and interest rate spread (1) |

$ | 95,425 | 3.33 | % | $ | 89,727 | 3.48 | % | $ | 85,100 | 3.99 | % | ||||||||||||||||||||||||

| |

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||||||

| Net interest margin (2) |

3.47 | % | 3.70 | % | 4.31 | % | ||||||||||||||||||||||||||||||

| |

|

|

|

|

|

|||||||||||||||||||||||||||||||

| (1) | Interest rate spread is calculated by subtracting the rate on average interest-bearing liabilities from the yield on average interest-earning assets. |

| (2) | Net interest margin is calculated by dividing tax-equivalent adjusted net interest income by average interest-earning assets. |

15

Changes in Interest Income and Interest Expense

Resulting from Changes in Volume and Changes in Rate

The following table sets forth, for the periods indicated, a summary of the changes in interest income and interest expense resulting from changes in volume and changes in rate (Amounts in thousands):

Increase (decrease) due to: |

||||||||||||

Volume (1) |

Rate (1) |

Net |

||||||||||

| 2021 compared to 2020 |

||||||||||||

| Interest income: |

||||||||||||

| Loans |

$ | 3,262 | $ | (1,469 | ) | $ | 1,793 | |||||

| Taxable securities |

1,360 | (1,246 | ) | 114 | ||||||||

| Nontaxable securities |

439 | (312 | ) | 127 | ||||||||

| Interest-bearing deposits in other banks |

422 | (579 | ) | (157 | ) | |||||||

| |

|

|

|

|

|

|||||||

| Total interest income |

$ | 5,483 | $ | (3,606 | ) | $ | 1,877 | |||||

| |

|

|

|

|

|

|||||||

| Interest expense: |

||||||||||||

| Savings and interest-bearing demand accounts |

$ | 382 | $ | (976 | ) | $ | (594 | ) | ||||

| Certificates of deposit |

(377 | ) | (1,735 | ) | (2,112 | ) | ||||||

| Short-term Federal Home Loan Bank advances |

(134 | ) | — | (134 | ) | |||||||

| Long-term Federal Home Loan Bank advances |

(405 | ) | (230 | ) | (635 | ) | ||||||

| Securities sold under repurchase agreements |

2 | (4 | ) | (2 | ) | |||||||

| Federal funds purchased |

(1 | ) | 1 | — | ||||||||

| Other borrowings |

(354 | ) | — | (354 | ) | |||||||

| Subordinated debentures |

187 | (177 | ) | 10 | ||||||||

| |

|

|

|

|

|

|||||||

| Total interest expense |

$ | (700 | ) | $ | (3,121 | ) | $ | (3,821 | ) | |||

| |

|

|

|

|

|

|||||||

| Net interest income |

$ | 6,183 | $ | (485 | ) | $ | 5,698 | |||||

| |

|

|

|

|

|

|||||||

| 2020 compared to 2019 |

||||||||||||

| Interest income: |

||||||||||||

| Loans |

$ | 16,383 | $ | (13,578 | ) | $ | 2,805 | |||||

| Taxable securities |

(633 | ) | (592 | ) | (1,225 | ) | ||||||

| Nontaxable securities |

761 | (285 | ) | 476 | ||||||||

| Interest-bearing deposits in other banks |

913 | (1,158 | ) | (245 | ) | |||||||

| |

|

|

|

|

|

|||||||

| Total interest income |

$ | 17,424 | $ | (15,613 | ) | $ | 1,811 | |||||

| |

|

|

|

|

|

|||||||

| Interest expense: |

||||||||||||

| Savings and interest-bearing demand accounts |

$ | 512 | $ | (1,570 | ) | $ | (1,058 | ) | ||||

| Certificates of deposit |

341 | (459 | ) | (118 | ) | |||||||

| Short-term Federal Home Loan Bank advances |

(1,877 | ) | (589 | ) | (2,466 | ) | ||||||

| Long-term Federal Home Loan Bank advances |

1,117 | (171 | ) | 946 | ||||||||

| Securities sold under repurchase agreements |

6 | — | 6 | |||||||||

| Federal funds purchased |

2 | (4 | ) | (2 | ) | |||||||

| Other borrowings |

354 | — | 354 | |||||||||

| Subordinated debentures |

— | (478 | ) | (478 | ) | |||||||

| |

|

|

|

|

|

|||||||

| Total interest expense |

$ | 455 | $ | (3,271 | ) | $ | (2,816 | ) | ||||

| |

|

|

|

|

|

|||||||

| Net interest income |

$ | 16,969 | $ | (12,342 | ) | $ | 4,627 | |||||

| |

|

|

|

|

|

|||||||

| (1) | The change in interest income and interest expense due to changes in both volume and rate, which cannot be segregated, has been allocated proportionately to the change due to volume and the change due to rate. |

Liquidity and Capital Resources

Civista maintains a conservative liquidity position. All securities are classified as available for sale. At December 31, 2021, securities with maturities of one year or less totaled $3,789, or 0.7% of the total securities portfolio. The available for sale portfolio helps to provide Civista with the ability to meet its funding needs. The Consolidated Statements of Cash Flows contained in the Consolidated Financial Statements detail the Company’s cash flows from operating activities resulting from net earnings.

16

Net cash provided by operating activities for 2021, 2020 and 2019 was $40,761, $32,654 and $38,801, respectively. The primary additions to cash from operating activities are from net income, adjusted for amortization of intangible assets, amortization of securities net of accretion, the provision for loan losses, depreciation and proceeds from sale of loans. The primary use of cash from operating activities is from loans originated for sale. Net cash used for investing activities was $130,496, $340,982 and $150,764 in 2021, 2020 and 2019, respectively, principally reflecting our loan and investment security activities. Deposits and borrowings comprised most of our financing activities, which resulted in net cash provided of $216,925, $398,802 and $116,739 for 2021, 2020 and 2019, respectively.

Future loan demand of Civista can be funded by increases in deposit accounts, proceeds from payments on existing loans, the maturity of securities and the sale of securities classified as available for sale. Additional sources of funds may also come from borrowing in the Federal Funds market and/or borrowing from the FHLB. As of December 31, 2021, Civista had total credit availability with the FHLB of $677,834, of which $96,300 was outstanding, including standby letters of credit of $21,300.

On a separate entity basis, CBI’s primary source of funds is dividends paid by its subsidiaries, primarily by Civista. Generally, subject to applicable minimum capital requirements, Civista may declare and pay a dividend without the approval of the Federal Reserve Bank of Cleveland (the “Federal Reserve Bank”) and the State of Ohio Department of Commerce, Division of Financial Institutions, provided the total dividends in a calendar year do not exceed the total of its profits for that year combined with its retained profits for the two preceding years. At December 31, 2021, Civista was able to pay approximately $59,772 of dividends to CBI without obtaining regulatory approval. During 2021, Civista paid dividends totaling $19,900 to CBI. This represented approximately 49 percent of Civista’s earnings for the year.

The Company manages its liquidity and capital through quarterly Asset/Liability Management Committee (ALCO) meetings. The ALCO discusses issues like those in the above paragraphs as well as others that may affect the future liquidity and capital position of the Company. The ALCO also examines interest rate risk and the effect that changes in rates will have on the Company. For more information about interest rate risk, please refer to the “Quantitative and Qualitative Disclosures about Market Risk” section.

Capital Adequacy

Shareholders’ equity totaled $355,212 at December 31, 2021 compared to $350,108 at December 31, 2020. The increase in shareholders’ equity resulted primarily from net income of $40,546, a $973 net increase in the Company’s pension liability and a decrease in the fair value of securities available for sale, net of tax, of $6,772, which was offset by dividends on common shares of $8,036. In addition, the Company repurchased common shares pursuant to its publicly-announced share purchase programs totaling $22,309 during 2021.

During the first quarter of 2015, the Company adopted the new BASEL III regulatory capital framework as approved by the federal banking agencies. In addition to the other required capital ratios, the BASEL III rules also require the Company to maintain minimum amounts and ratios of Common Equity Tier 1 (“CET1”) Capital to risk-weighted assets (as these terms are defined in the BASEL III rules). Under the BASEL III rules, the Company elected to opt-out of including accumulated other comprehensive income in regulatory capital. All of the Company’s capital ratios exceeded the regulatory minimum guidelines as of December 31, 2021 and 2020 as identified in the following table:

Total Risk Based Capital |

Tier I Risk Based Capital |

CET1 Risk Based Capital |

Leverage Ratio |

|||||||||||||

| Company Ratios—December 31, 2021 |

19.2 | % | 14.3 | % | 12.9 | % | 10.2 | % | ||||||||

| Company Ratios—December 31, 2020 |

16.0 | % | 14.7 | % | 13.2 | % | 10.8 | % | ||||||||

| For Capital Adequacy Purposes |

8.0 | % | 6.0 | % | 4.5 | % | 4.0 | % | ||||||||

| To Be Well Capitalized Under Prompt Corrective Action Provisions |

10.0 | % | 8.0 | % | 6.5 | % | 5.0 | % | ||||||||

17

Common equity for the CET1 risk-based capital ratio includes common stock (plus related surplus) and retained earnings, plus limited amounts of minority interests in the form of common stock, less the majority of certain regulatory deductions.

Tier 1 capital includes common equity as defined for the CET1 risk-based capital ratio, plus certain non-cumulative preferred stock and related surplus, cumulative preferred stock and related surplus and trust preferred securities that have been grandfathered (but which are not permitted going forward), and limited amounts of minority interests in the form of additional Tier 1 capital instruments, less certain deductions.

Tier 2 capital, which can be included in the total capital ratio, includes certain capital instruments (such as subordinated debt) and limited amounts of the allowance for loan and lease losses, subject to new eligibility criteria, less applicable deductions.

The deductions from CET1 capital include goodwill and other intangibles, certain deferred tax assets, mortgage-servicing assets above certain levels, gains on sale in connection with a securitization, investments in a banking organization’s own capital instruments and investments in the capital of unconsolidated financial institutions (above certain levels). These deductions were phased in from 2015 through 2019.

Under applicable regulatory guidelines, capital is compared to the relative risk related to the balance sheet. To derive the risk included in the balance sheet, one of several risk weights is applied to different balance sheet and off-balance sheet assets, primarily based on the relative credit risk of the counterparty. The capital amounts and classification are also subject to qualitative judgments by the regulators about components, risk weightings and other factors.

The BASEL III regulatory capital rules and regulations also place restrictions on the payment of capital distributions, including dividends, and certain discretionary bonus payments to executive officers if the company does not hold a capital conservation buffer of greater than 2.5 percent composed of CET1 capital above its minimum risk-based capital requirements, or if its eligible retained income is negative in that quarter and its capital conservation buffer ratio was less than 2.5 percent at the beginning of the quarter. The capital conservation buffer began to phase in starting on January 1, 2016, at 0.625%, and was fully phased in effective January 1, 2019, at 2.5%. The implementation of Basel III did not have a material impact on CBI’s or Civista’ capital ratios.

Effects of Inflation

The Company’s balance sheet is typical of financial institutions and reflects a net positive monetary position whereby monetary assets exceed monetary liabilities. Monetary assets and liabilities are those which can be converted to a fixed number of dollars and include cash assets, securities, loans, money market instruments, deposits and borrowed funds.

During periods of inflation, a net positive monetary position may result in an overall decline in purchasing power of an entity. However, no clear evidence exists of a relationship between the purchasing power of an entity’s net positive monetary position and its future earnings. Moreover, the Company’s ability to preserve the purchasing power of its net positive monetary position will be partly influenced by the effectiveness of its asset/liability management program. As part of the asset/liability management process, management reviews and monitors information and projections on inflation as published by the Federal Reserve Board and other sources. This information speaks to inflation as determined by its impact on consumer prices and also the correlation of inflation and interest rates. This information is but one component in an asset/liability management process designed to limit the impact of inflation on the Company. Management does not believe that the effect of inflation on its nonmonetary assets (primarily bank premises and equipment) is material as such assets are not held for resale and significant disposals are not anticipated.

Fair Value of Financial Instruments

The Company has disclosed the fair value of its financial instruments at December 31, 2021 and 2020 in Note 16 to the Consolidated Financial Statements. The fair value of loans at December 31, 2021 was 100.7% of the carrying value compared to 101.5% at December 31, 2020. The fair value of deposits at December 31, 2021 was

18

100.0% of the carrying value compared to 100.1% at December 31, 2020. Changes in fair value were primarily due to changes in the discount values used to measure fair value.

Contractual Obligations

The following table represents significant fixed and determinable contractual obligations of the Company as of December 31, 2021.

| Contractual Obligations |

One year or less |

One to three years |

Three to five years |

Over five years |

Total |

|||||||||||||||

| Deposits without a stated maturity |

$ | 2,170,253 | $ | — | $ | — | $ | — | $ | 2,170,253 | ||||||||||

| Certificates of deposit and IRAs |

174,022 | 64,005 | 7,425 | 996 | 246,448 | |||||||||||||||

| FHLB advances, securities sold under agreements to repurchase and U.S. Treasury interest-bearing demand note |

— | — | — | 75,000 | 75,000 | |||||||||||||||

| Subordinated debentures (1) |

— | — | — | 102,813 | 102,813 | |||||||||||||||

| Operating leases |

569 | 613 | 417 | 491 | 2,090 | |||||||||||||||

| (1) | The subordinated debentures consist of $2,000, $2,500, $5,000, $7,500, and $12,500 debentures. |

The Company has retail repurchase agreements with clients within its local market areas. These borrowings are collateralized with securities owned by the Company. See Note 11 to the Consolidated Financial Statements for further detail. The Company also has a cash management advance line of credit and outstanding letters of credit with the FHLB. For further discussion, refer to Note 9 and Note 10 to the Consolidated Financial Statements.

Quantitative and Qualitative Disclosures about Market Risk

The Company’s primary market risk exposure is interest-rate risk and, to a lesser extent, liquidity risk. All of the Company’s transactions are denominated in U.S. dollars with no specific foreign exchange exposure.

Interest-rate risk is the exposure of a banking organization’s financial condition to adverse movements in interest rates. Accepting this risk can be an important source of profitability and shareholder value. However, excessive levels of interest-rate risk can pose a significant threat to the Company’s earnings and capital base. Accordingly, effective risk management that maintains interest-rate risk at prudent levels is essential to the Company’s safety and soundness.

Evaluating a financial institution’s exposure to changes in interest rates includes assessing both the adequacy of the management process used to control interest-rate risk and the organization’s quantitative level of exposure. When assessing the interest-rate risk management process, the Company seeks to ensure that appropriate policies, procedures, management information systems and internal controls are in place to maintain interest-rate risk at prudent levels with consistency and continuity. Evaluating the quantitative level of interest rate risk exposure requires the Company to assess the existing and potential future effects of changes in interest rates on its consolidated financial condition, including capital adequacy, earnings, liquidity and, where appropriate, asset quality.

The Federal Reserve Board, together with the Office of the Comptroller of the Currency and the Federal Deposit Insurance Corporation, adopted a Joint Agency Policy Statement on interest-rate risk, effective June 26, 1996. The policy statement provides guidance to examiners and bankers on sound practices for managing interest-rate risk, which will form the basis for ongoing evaluation of the adequacy of interest-rate risk management at supervised institutions. The policy statement also outlines fundamental elements of sound management that have been identified in prior Federal Reserve guidance and discusses the importance of these elements in the context of managing interest-rate risk. Specifically, the guidance emphasizes the need for active board of director and senior management oversight and a comprehensive risk-management process that effectively identifies, measures, and controls interest-rate risk. Financial institutions derive their income primarily from the excess of

19

interest collected over interest paid. The rates of interest an institution earns on its assets and owes on its liabilities generally are established contractually for a period of time. Since market interest rates change over time, an institution is exposed to lower profit margins (or losses) if it cannot adapt to interest-rate changes. For example, assume that an institution’s assets carry intermediate- or long-term fixed rates and that those assets were funded with short-term liabilities. If market interest rates rise by the time the short-term liabilities must be refinanced, the increase in the institution’s interest expense on its liabilities may not be sufficiently offset if assets continue to earn at the long-term fixed rates. Accordingly, an institution’s profits could decrease on existing assets because the institution will have either lower net interest income or, possibly, net interest expense. Similar risks exist when assets are subject to contractual interest-rate ceilings, or rate sensitive assets are funded by longer-term, fixed-rate liabilities in a decreasing-rate environment.

Several techniques may be used by an institution to minimize interest-rate risk. One approach used by the Company is to periodically analyze its assets and liabilities and make future financing and investment decisions based on payment streams, interest rates, contractual maturities, and estimated sensitivity to actual or potential changes in market interest rates. Such activities fall under the broad definition of asset/liability management. The Company’s primary asset/liability management technique is the measurement of the Company’s asset/liability gap, that is, the difference between the cash flow amounts of interest sensitive assets and liabilities that will be refinanced (or repriced) during a given period. For example, if the asset amount to be repriced exceeds the corresponding liability amount for a certain day, month, year, or longer period, the institution is in an asset sensitive gap position. In this situation, net interest income would increase if market interest rates rose or decrease if market interest rates fell.

If, alternatively, more liabilities than assets will reprice, the institution is in a liability sensitive position. Accordingly, net interest income would decline when rates rose and increase when rates fell. Also, these examples assume that interest rate changes for assets and liabilities are of the same magnitude, whereas actual interest rate changes generally differ in magnitude for assets and liabilities.

Several ways an institution can manage interest-rate risk include selling existing assets or repaying certain liabilities and matching repricing periods for new assets and liabilities, for example, by shortening terms of new loans or securities. Financial institutions are also subject to prepayment risk in falling rate environments. For example, mortgage loans and other financial assets may be prepaid by a debtor so that the debtor may refinance its obligations at new, lower rates. The Company does not have significant derivative financial instruments and does not intend to purchase a significant amount of such instruments in the near future. Prepayments of assets carrying higher rates reduce the Company’s interest income and overall asset yields. A large portion of an institution’s liabilities may be short term or due on demand, while most of its assets may be invested in long term loans or securities. Accordingly, the Company seeks to have in place sources of cash to meet short-term demands. These funds can be obtained by increasing deposits, borrowing, or selling assets. Also, FHLB advances and wholesale borrowings may be used as important sources of liquidity for the Company.