Management's Discussion and Analysis of

Results of Operations and Financial Condition

For the three and six months ended

June 30, 2022

August 8, 2022

INTRODUCTION

This Management's Discussion and Analysis ("MD&A") dated August 8, 2022 is intended to supplement Hudbay Minerals Inc.'s unaudited condensed consolidated interim financial statements and related notes for the three and six months ended June 30, 2022 (the "consolidated interim financial statements"). The consolidated interim financial statements have been prepared in accordance with International Financial Reporting Standards ("IFRS"), including International Accounting Standard 34, Interim Financial Reporting, as issued by the International Accounting Standards Board ("IASB").

References to "Hudbay", the "Company", "we", "us", "our" or similar terms refer to Hudbay Minerals Inc. and its direct and indirect subsidiaries as at June 30, 2022.

Readers should be aware that:

- This MD&A contains certain "forward-looking statements" and "forward-looking information" (collectively, "forward-looking information") that are subject to risk factors set out in a cautionary note contained in our MD&A.

- This MD&A has been prepared in accordance with the requirements of the securities laws in effect in Canada, which may differ materially from the requirements of United States securities laws applicable to US issuers.

- We use a number of non-IFRS financial performance measures in our MD&A.

- This MD&A includes a discussion of the results of a preliminary economic assessment of the Copper World Complex. The preliminary economic assessment is preliminary in nature, includes inferred resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves and there is no certainty the preliminary economic assessment will be realized.

- The technical and scientific information in this MD&A has been approved by qualified persons based on a variety of assumptions and estimates.

For a discussion of each of the above matters, readers are urged to review the "Notes to Reader" discussion beginning on page 56 of this MD&A.

Additional information regarding Hudbay, including the risks related to our business and those that are reasonably likely to affect our consolidated financial statements in the future, is contained in our continuous disclosure materials, including our most recent Annual Information Form ("AIF"), consolidated interim financial statements and Management Information Circular available on SEDAR at www.sedar.com and on EDGAR at www.sec.gov.

All amounts are in US dollars unless otherwise noted.

OUR BUSINESS

We are a diversified mining company with long-life assets in North and South America. Our operations in Cusco (Peru) produce copper with gold, silver and molybdenum by-products. Our operations in Manitoba (Canada) produce gold with copper, zinc and silver by-products. We have an organic pipeline that includes copper development projects in Arizona and Nevada (United States), and our growth strategy is focused on the exploration, development, operation, and optimization of properties we already control, as well as other mineral assets we may acquire that fit our strategic criteria. We are governed by the Canada Business Corporations Act and our shares are listed under the symbol "HBM" on the Toronto Stock Exchange, New York Stock Exchange and Bolsa de Valores de Lima.

SUMMARY

Strong Operating and Financial Results

- Full year 2022 production and operating cost guidance is reaffirmed as second quarter production was in line with expectations and Hudbay achieved strong unit operating cost performance despite inflationary pressures from higher input prices for many services and consumables.

- Second quarter net earnings and earnings per share were $32.1 million and $0.12, respectively. After adjusting for a non-cash gain of $60.7 million primarily related to a quarterly revaluation of our Flin Flon environmental provision given higher long-term risk-free discount rates, and a $95.0 million pre-tax impairment loss related to certain specific capitalized costs and assets associated with the previous stand-alone development plan for the Rosemont deposit, among other items, second quarter adjusted net earnings1 per share were $0.12.

- Operating cash flow before change in non-cash working capital was $123.9 million and adjusted EBITDA1 was $141.4 million in the second quarter of 2022, benefiting from strong realized zinc prices and higher gold sales volumes, compared to the same period in 2021.

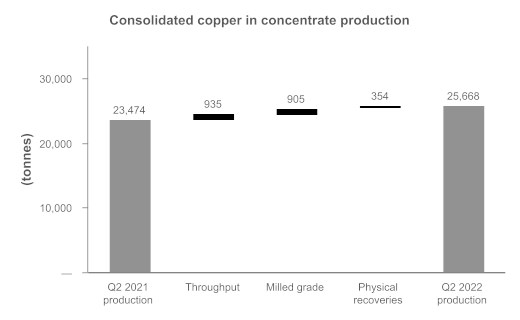

- Consolidated production in the second quarter included 25,668 tonnes of copper and 58,645 ounces of gold, an increase from the first quarter of 2022. Consolidated cash cost and all-in sustaining cash cost per pound of copper produced, net of by-product credits1, were $0.65 and $1.93, respectively, a significant decrease from the first quarter of 2022.

- Peru delivered strong operating performance in the second quarter with copper production of 20,880 tonnes as mill throughput and copper grades improved over the first quarter of 2022.

- Manitoba achieved second quarter gold production of 44,787 ounces at a cash cost per ounce of gold produced, net of by-product credits1, of negative $207 as New Britannia achieved higher than targeted throughput rates and gold recoveries continue to improve.

- After 18 years of steady production at our 777 mine in Manitoba, the final reserves were depleted in June 2022, consistent with the mine plan. Closure activities to safely decommission the 777 mine, the Flin Flon concentrator and the zinc plant commenced in the second quarter and are advancing ahead of schedule.

- Cash increased by $45.2 million during the second quarter to $258.6 million, as at June 30, 2022, mainly as a result of $165.6 million of cash generated from operations, partially offset by $78.9 million of mostly sustaining capital investments, an $18.6 million payment toward the gold prepayment liability and a $10.0 million scheduled deferred payment related to the acquisition of the former minority partner's interest in Rosemont.

Executing on Growth Initiatives

- Recently released the results of the Copper World Complex preliminary economic assessment ("PEA") which entails a two-phase mine plan that has an after-tax net present value (10%) of $1,296 million and generates an 18% internal rate of return at $3.50 per pound copper.2

- Advancing a pre-feasibility study for Phase I of the Copper World Complex, which will focus on converting the remaining inferred mineral resources to measured and indicated and evaluating many of the project optimization and upside opportunities.

- Exploration agreement on the Maria Reyna and Caballito satellite properties in Peru is nearing completion.

- Released our 19th Annual Sustainability Report in June 2022 discussing our key accomplishments and initiatives in 2021, and the Company is currently working toward specific emission reduction targets to align with the global 2030 and 2050 climate change goals.

1 Adjusted net earnings (loss) and adjusted net earnings (loss) per share, adjusted EBITDA, cash cost, sustaining cash cost, all-in sustaining cash cost per pound of copper produced, net of by-product credits, cash cost, sustaining cash cost per ounce of gold produced, net of by-product credits, and net debt are non-IFRS financial performance measures with no standardized definition under IFRS. For further information and a detailed reconciliation, please see the discussion under the "Non-IFRS Financial Reporting Measures" section of this MD&A.

2 The preliminary economic assessment for the Copper World Complex is preliminary in nature, includes inferred resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves and there is no certainty the preliminary economic assessment will be realized.

Summary of Second Quarter Results

Cash generated from operating activities in the second quarter of 2022 increased to $165.6 million compared to $96.4 million in the same quarter of 2021. The increase is primarily the result of an increase in our non-cash working capital, higher realized zinc metal prices and higher gold sales volumes partially offset by lower base metal sales volumes, higher mine operating costs due to inflationary pressures and higher profit sharing. Operating cash flow before change in non-cash working capital was $123.9 million during the second quarter of 2022, reflecting a decrease of $8.9 million compared to the same period of 2021. The lower operating cash flow before changes in non-cash working capital in the second quarter of 2022 was largely due to higher mine operating costs and higher profit sharing partially offset by higher zinc prices.

Consolidated copper production in the second quarter of 2022 increased by 9% compared to the same period in 2021 primarily as a result of higher throughput, grades and recoveries in Peru and Manitoba. Consolidated gold production in the second quarter of 2022 increased by 47% compared to the second quarter of 2021, due to higher gold grades from Pampacancha and higher gold grades at Lalor coupled with significantly higher gold recoveries at New Britannia. Consolidated zinc production in the quarter decreased by 21%, versus the comparative quarter in 2021, primarily due to the continued transition toward mining the gold lenses at Lalor and a corresponding decrease of production from the base metal zones. Consolidated silver production in the second quarter increased by 26% compared to the same period in 2021, as a result of higher grades from Lalor and Constancia offset by lower recoveries in Peru.

Net earnings and earnings per share in the second quarter of 2022 were $32.1 million and $0.12, respectively, compared to a net loss and loss per share of $3.4 million and $0.01, respectively, in the second quarter of 2021. Second quarter earnings benefited from a non-cash gain of $60.7 million mostly related to the quarterly revaluation of our Flin Flon environmental provision, which was impacted by rising long-term risk-free discount rates. Given the long term nature of the reclamation cash flows, the related environmental provision is highly sensitive to changes in long-term risk-free discount rates and, as such, we may continue to experience quarterly environmental provision revaluations. The quarterly financial results were also negatively impacted by a $95.0 million pre-tax impairment loss related to certain specific capitalized costs and assets associated with the previous stand-alone development plan for the Rosemont deposit, which were determined to no longer be recoverable.

Adjusted net earnings1 and adjusted net earnings per share1 in the second quarter of 2022 were $30.5 million and $0.12 per share, respectively, after adjusting for the non-cash gain related to the revaluation of our environmental provision and the specific asset impairment loss, among other items. This compares to an adjusted net earnings and adjusted net earnings per share of $5.4 million, and $0.02 in the same period of 2021. Second quarter adjusted EBITDA1 was $141.4 million, compared to $143.2 million in the same period of 2021.

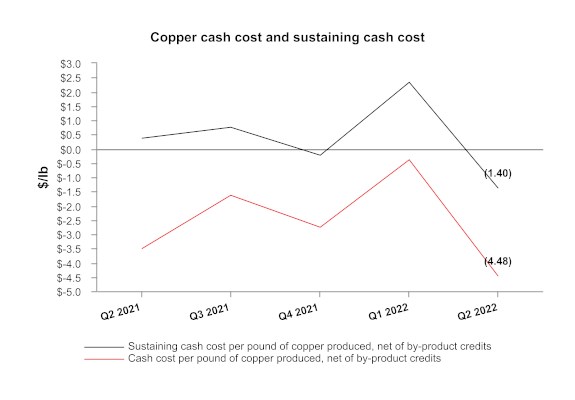

In the second quarter of 2022, consolidated cash cost per pound of copper produced, net of by-product credits1, was $0.65, compared to $0.84 in the same period in 2021. This decrease was a result of higher zinc and precious metal by-product credits and higher copper production, partially offset by higher milling and profit sharing costs. Consolidated sustaining cash cost per pound of copper produced, net of by-product credits1, was $1.87 in the second quarter of 2022 compared to $2.25 in the same period in 2021. This decrease was primarily due to the same reasons outlined above along with lower cash sustaining capital expenditures in Manitoba. Both measures were within our 2022 guidance ranges and we are reaffirming our full year consolidated cash cost guidance.

Consolidated all-in sustaining cash cost per pound of copper produced, net of by-product credits1, was $1.93 in the second quarter of 2022, lower than $2.48 in the same period in 2021, due to the same reasons outlined above along with lower corporate selling and administrative expenses.

As at June 30, 2022, our liquidity includes $258.6 million in cash as well as undrawn availability of $363.6 million under our revolving credit facilities. We expect that our current liquidity combined with cash flow from operations, particularly in the fourth quarter when production in Peru is expected to benefit from higher grades, will be sufficient to meet our liquidity needs for the foreseeable future. As such, we are well positioned to weather the volatility in commodity prices experienced during the second quarter.

1 Adjusted net earnings (loss) and adjusted net earnings (loss) per share, adjusted EBITDA, cash cost, sustaining cash cost, all-in sustaining cash cost per pound of copper produced, net of by-product credits, cash cost, sustaining cash cost per ounce of gold produced, net of by-product credits, and net debt are non-IFRS financial performance measures with no standardized definition under IFRS. For further information and a detailed reconciliation, please see the discussion under the "Non-IFRS Financial Reporting Measures" section of this MD&A.

KEY FINANCIAL RESULTS

| Financial Condition | Jun. 30, 2022 | Dec. 31, 2021 | ||||

| (in $ thousands) | ||||||

| Cash | $ | 258,556 | $ | 270,989 | ||

| Total long-term debt | 1,182,143 | 1,180,274 | ||||

| Net debt1 | 923,587 | 909,285 | ||||

| Working capital2 | 180,371 | 147,512 | ||||

| Total assets | 4,382,727 | 4,616,231 | ||||

| Equity | 1,601,123 | 1,476,828 | ||||

| 1 Net debt is a non-IFRS financial performance measure with no standardized definition under IFRS. For further information and a detailed reconciliation, please see discussion under the "Non-IFRS Financial Reporting Measures" section of this MD&A. | ||||||

| 2 Working capital is determined as total current assets less total current liabilities as defined under IFRS and disclosed on the consolidated financial statements. | ||||||

| Financial Performance | Three months ended | Six months ended | ||||||||||

| (in $ thousands, except per share amounts) | Jun. 30, 2022 | Jun. 30, 2021 | Jun. 30, 2022 | Jun. 30, 2021 | ||||||||

| Revenue | $ | 415,454 | $ | 404,242 | $ | 794,073 | $ | 717,866 | ||||

| Cost of sales | 325,940 | 322,060 | 619,291 | 583,173 | ||||||||

| Earnings (loss) before tax | 21,504 | 14,819 | 110,365 | (54,773 | ) | |||||||

| Net earnings (loss) | 32,143 | (3,395 | ) | 95,958 | (63,497 | ) | ||||||

| Basic and diluted earnings (loss) per share | 0.12 | (0.01 | ) | 0.37 | (0.24 | ) | ||||||

| Adjusted earnings (loss) per share1 | 0.12 | 0.02 | 0.14 | (0.04 | ) | |||||||

| Operating cash flow before changes in non-cash working capital2 | 123.9 | 132.8 | 201.0 | 223.4 | ||||||||

| Adjusted EBITDA1,2 | 141.4 | 143.2 | 251.9 | 247.7 | ||||||||

| 1 Adjusted earnings (loss) per share and adjusted EBITDA are non-IFRS financial performance measures with no standardized definition under IFRS. For further information and a detailed reconciliation, please see discussion under the "Non-IFRS Financial Reporting Measures" section of this MD&A. | ||||||||||||

| 2 In millions. | ||||||||||||

KEY PRODUCTION RESULTS

| Three months ended | Three months ended | ||||||||||||||||||

| Jun. 30, 2022 | Jun. 30, 2021 | ||||||||||||||||||

| Peru | Manitoba | Total | Peru | Manitoba | Total | ||||||||||||||

| Contained metal in concentrate and doré produced 1 | |||||||||||||||||||

| Copper | tonnes | 20,880 | 4,788 | 25,668 | 19,058 | 4,416 | 23,474 | ||||||||||||

| Gold | oz | 13,858 | 44,787 | 58,645 | 10,220 | 29,628 | 39,848 | ||||||||||||

| Silver | oz | 584,228 | 280,625 | 864,853 | 468,057 | 217,859 | 685,916 | ||||||||||||

| Zinc | tonnes | - | 17,053 | 17,053 | - | 21,538 | 21,538 | ||||||||||||

| Molybdenum | tonnes | 390 | - | 390 | 295 | - | 295 | ||||||||||||

| Payable metal sold | |||||||||||||||||||

| Copper | tonnes | 18,473 | 5,177 | 23,650 | 19,946 | 5,230 | 25,176 | ||||||||||||

| Gold2 | oz | 8,430 | 42,454 | 50,884 | 5,638 | 32,567 | 38,205 | ||||||||||||

| Silver2 | oz | 484,946 | 253,225 | 738,171 | 315,064 | 262,443 | 577,507 | ||||||||||||

| Zinc3 | tonnes | - | 20,793 | 20,793 | - | 25,361 | 25,361 | ||||||||||||

| Molybdenum | tonnes | 208 | - | 208 | 265 | - | 265 | ||||||||||||

| 1 Metal reported in concentrate is prior to deductions associated with smelter contract terms. | |||||||||||||||||||

| 2 Includes total payable gold and silver in concentrate and in doré sold. | |||||||||||||||||||

| 3 Includes refined zinc metal and payable zinc in concentrate sold. | |||||||||||||||||||

| Six months ended | Six months ended | ||||||||||||||||||

| Jun. 30, 2022 | Jun. 30, 2021 | ||||||||||||||||||

| Peru | Manitoba | Total | Peru | Manitoba | Total | ||||||||||||||

| Contained metal in concentrate produced 1 | |||||||||||||||||||

| Copper | tonnes | 40,046 | 10,324 | 50,370 | 36,885 | 11,142 | 48,027 | ||||||||||||

| Gold | oz | 24,647 | 87,954 | 112,601 | 14,858 | 60,490 | 75,348 | ||||||||||||

| Silver | oz | 1,089,796 | 559,414 | 1,649,210 | 873,771 | 508,818 | 1,382,589 | ||||||||||||

| Zinc | tonnes | - | 39,305 | 39,305 | - | 49,478 | 49,478 | ||||||||||||

| Molybdenum | tonnes | 596 | - | 596 | 589 | - | 589 | ||||||||||||

| Payable metal sold | |||||||||||||||||||

| Copper | tonnes | 35,298 | 8,961 | 44,259 | 34,782 | 11,323 | 46,105 | ||||||||||||

| Gold | oz | 22,882 | 76,345 | 99,227 | 8,601 | 54,987 | 63,588 | ||||||||||||

| Silver | oz | 1,121,079 | 481,684 | 1,602,763 | 652,676 | 434,591 | 1,087,267 | ||||||||||||

| Zinc 2 | tonnes | - | 38,099 | 38,099 | - | 53,704 | 53,704 | ||||||||||||

| Molybdenum | tonnes | 421 | - | 421 | 549 | - | 549 | ||||||||||||

| 1 Metal reported in concentrate is prior to deductions associated with smelter contract terms. | |||||||||||||||||||

| 2 Includes refined zinc metal sold and payable zinc in concentrate sold. | |||||||||||||||||||

KEY COST RESULTS

| Three months ended | Six months ended | Guidance | ||||||||||||||

| Jun. 30, 2022 |

Jun. 30, 2021 |

Jun. 30, 2022 |

Jun. 30, 2021 |

Annual 2022 |

||||||||||||

| Consolidated copper cash cost per pound of copper produced | ||||||||||||||||

| Cash cost 1 | $/lb | 0.65 | 0.84 | 0.87 | 0.94 | 0.60 - 1.05 | ||||||||||

| Peru | $/lb | 1.82 | 1.85 | 1.69 | 1.84 | 1.10 - 1.40 | ||||||||||

| Manitoba | $/lb | (4.48 | ) | (3.51 | ) | (2.29 | ) | (2.02 | ) | - | ||||||

| Sustaining cash cost 1 | $/lb | 1.87 | 2.25 | 2.07 | 2.20 | 1.60 - 2.25 | ||||||||||

| Peru | $/lb | 2.62 | 2.69 | 2.45 | 2.53 | |||||||||||

| Manitoba | $/lb | (1.40 | ) | 0.36 | 0.60 | 1.12 | ||||||||||

| All-in sustaining cash cost1 | $/lb | 1.93 | 2.48 | 2.23 | 2.42 | |||||||||||

| Manitoba gold cash cost per ounce of gold produced | ||||||||||||||||

| Cash cost 1,4 | $/oz | (207 | ) | - | 99 | - | 300 - 550 | |||||||||

| Sustaining cash cost 1,4 | $/oz | 519 | - | 847 | - | |||||||||||

| Combined mine/mill unit operating cost per tonne of copper processed 1,2 | ||||||||||||||||

| Peru 3 | $/tonne | 12.02 | 10.40 | 12.19 | 11.02 | 10.10 - 12.90 | 5 | |||||||||

| Manitoba | C$/tonne | 168 | 148 | 172 | 150 | 170 - 185 | ||||||||||

| 1 Cash cost, sustaining cash cost, all-in sustaining cash cost per pound of copper produced, net of by-product credits, gold cash cost, sustaining cash cost per ounce of gold produced, net of by-product credits, and unit operating cost are non-IFRS financial performance measures with no standardized definition under IFRS. For further information and a detailed reconciliation, please see the discussion under the "Non-IFRS Financial Reporting Measures" section of this MD&A. | ||||||||||||||||

| 2 Reflects combined mine, mill and G&A costs per tonne of milled ore. Peru costs reflect the deduction of expected capitalized stripping costs. | ||||||||||||||||

| 3 Excludes approximately $1.3 million, or $0.16 per tonne and $3.6 million, or $0.24 per tonne, of COVID-related costs during the three and six months ended June 30, 2022, respectively and $6.3 million, or $0.85 and $10.9 million or $0.79 per tonne during the three and six months ended June 30, 2021. | ||||||||||||||||

| 4 Cash cost and sustaining cash cost per ounce of gold produced, net of by-product credits were introduced in 2022 and do not have a published comparative. | ||||||||||||||||

| 5 Combined unit cost guidance for 2022 excludes COVID-19 related costs. | ||||||||||||||||

RECENT DEVELOPMENTS

Robust Preliminary Economic Assessment Released for Copper World Complex

In June, we released the results of the PEA of our 100%-owned Copper World Complex in Arizona, which includes the recently discovered Copper World deposits along with the Rosemont deposit. Highlights of the PEA include:

- Two-phase mine plan has an after-tax net present value (10%) of $1,296 million and generates an 18% internal rate of return at $3.50 per pound copper1.

- The processing facilities are planned to have annual production capacity of 100,000 tonnes of copper cathode during Phase I and 125,000 tonnes of copper cathode during Phase II, and have been designed to reduce the project's carbon footprint to produce "Made in America" copper.

- Supports U.S. copper supply through onshore production of copper cathode expected to be sold entirely to domestic customers and eliminates greenhouse gas ("GHG") and sulfur emissions associated with overseas shipping and processing.

- Phase I reflects a stand-alone operation on private land and patented mining claims over a 16-year mine life with average annual copper production of approximately 86,000 tonnes from mined resources at cash costs and sustaining cash costs of $1.15 and $1.44 per pound of copper2, respectively, generating an after-tax net present value (10%) of $741 million and an internal rate of return of 17%1.

- Phase I of the Copper World Complex includes a 60,000 ton per day sulfide concentrator, a 20,000 ton per day oxide heap leach, an SX/EW facility and a concentrate leach facility with an initial capital cost estimate of approximately $1.9 billion. The concentrator is intended to expand to 90,000 tons per day in Phase II.

- Phase II expands mining activities onto federal land and extends the mine life to 44 years with average annual copper production of approximately 101,000 tonnes from mined resources at cash costs and sustaining cash costs of $1.11 and $1.42 per pound of copper2, respectively. Phase II provides additional optionality with an after-tax net present value (10%) of $555 million and an internal rate of return of 49% (and a projected after-tax net present value (10%) of $2,806 million at the time of Phase II sanctioning)1.

- Significant increase in copper contained in all mineral resource categories.

- Hudbay is evaluating several opportunities to optimize the project, including processing and initial capital optimizations, the potential to expand Phase I beyond 16 years with additions to the Company's private land package for tailings and waste rock storage and the potential to accelerate Phase II if federal permits are received earlier than as outlined in the PEA.

The preliminary economic assessment for the Copper World Complex is preliminary in nature, includes inferred resources that are considered too speculative geologically to have the economic considerations applied to them that would enable them to be categorized as mineral reserves and there is no certainty the preliminary economic assessment will be realized. For additional details on the Copper World Complex PEA, please refer to the news release dated June 8, 2022 and the NI 43-101 technical report filed on July 14, 2022.

Hudbay is advancing a pre-feasibility study for Phase I of the Copper World Complex during the second half of 2022, which will focus on converting the remaining inferred mineral resources to measured and indicated and evaluating many of the project optimization and upside opportunities.

____________________________________________

1 The valuation metrics are based on a preliminary economic assessment that includes an economic analysis of the potential viability of mineral resources. Mineral resources that are not mineral reserves do not have demonstrated economic viability.

2 Cash cost and sustaining cash cost are non-IFRS financial performance measures with no standardized definition under IFRS. For further details on why Hudbay believes cash costs are a useful performance indicator, please refer to the section titled "Non-IFRS Financial Performance Measures".

Arizona Permitting and Litigation Update

The permitting process for the Copper World Complex is expected to require state and local permits for Phase I and federal permits for Phase II. On May 23, 2022, the U.S. District Court for the District of Arizona issued a favourable ruling effectively stating that there is no obligation for the Army Corps of Engineers ("ACOE") to include Phase I of the project as part its NEPA federal review of the previous stand-alone Rosemont project design. Furthermore, on May 12, 2022, a decision from the 9th Circuit Court of Appeals clarified the permitting path for Phase II, including the requirements to receive federal permits for the second phase under existing mining regulations. Hudbay expects it will be able to pursue and obtain federal permits for Phase II within the constraints imposed by the Court's decision.

On July 27, 2022, Hudbay received approval from the Arizona State Mine Inspector for its amended Mined Land Reclamation Plan ("MLRP") for the Copper World Complex. The MLRP was initially approved in October 2021 and was subsequently amended to reflect a larger private land project footprint. Hudbay expects to submit applications for the other key state-level permits for Phase I of the Copper World Complex in the second half of 2022.

777 Mine Closure

On June 17, 2022, mining activities at our 777 mine in Flin Flon, Manitoba concluded after the reserves were depleted following 18 years of steady production. The 777 deposit was a large and rich orebody and for many years was the flagship mine of Hudbay's Manitoba operations. The mine commenced production in 2004 with an initial ten-year mine life, operated steadily and successfully expanded reserves by an additional eight years. After extensive drilling in and around the mine in recent years, no new deposits were identified. Our hydrometallurgical zinc facility in Flin Flon will also be closed after more than 25 years of successful operations. The 777 mine and the zinc plant are scheduled to be safely decommissioned by September 2022. The Flin Flon concentrator and tailings impoundment area will be shifted to care and maintenance to provide optionality should another mineral discovery occur in the Flin Flon area. Hudbay strives to achieve closure practices that align with leading standards and has developed stringent and detailed environmental plans to manage water and the remaining infrastructure and processing plants in Flin Flon.

Closure activities at the 777 mine and zinc plant have commenced and employees and equipment are transitioning to our operations in Snow Lake, Manitoba as part of our Lalor mine ramp-up strategy.

19th Annual Sustainability Report

In June, we released our annual sustainability report, which provides transparency and progress on key accomplishments and initiatives in 2021 along with goals for the upcoming year and long-term future. Hudbay believes global demand for the metals that we mine will continue to rise alongside the need for green technology that will play an essential role in meeting the challenge of climate change.

We are committed to a reduced GHG emissions future. We are currently working toward specific emissions reduction targets to align with the global 2030 and 2050 climate change goals. We are also designing the Copper World Complex in Arizona in compliance with 2030 and 2050 GHG objectives. In 2021, to better understand the nature of our GHG footprint and the best options for approaching and achieving sustainable GHG reductions, we began work on a 10-year Greenhouse Gas Reduction Roadmap. The roadmap will identify key sources of emissions, including Scope 3 emissions, and the nature of the changes - operational or technical - that will be required to make full or significant changes in each source area.

As a member of the Mining Association of Canada, we implement the Towards Sustainable Mining ("TSM") Protocols at all of our operations, with the goal to maintain a score of "A" or higher for all protocols. In 2021, we achieved a rating of "AA" across all TSM tailings management protocol indicators in both Manitoba and Peru. We also saw a 7% decrease in energy intensity per tonne of ore processed, and over 50% of our indirect energy consumption was from renewable sources.

Exploration Update

Peru Regional Exploration

Hudbay controls a large, contiguous block of mineral rights with the potential to host mineral deposits within trucking distance of the Constancia processing facility, including the past producing Caballito property and the highly prospective Maria Reyna property. Discussions with the community of Uchucarcco related to a surface rights exploration agreement on the Maria Reyna and Caballito properties are progressing well. The Company expects to finalize an agreement in the coming weeks before commencing field exploration activities. Finalization of the Uchucarcco agreement is expected to increase community investment costs in the second half of 2022.

The Company is compiling results from recent drilling at the Llaguen copper porphyry target in northern Peru and remains on track to complete an initial inferred mineral resource estimate in the third quarter of 2022.

Manitoba Regional Exploration

We have been actively conducting drilling activities in the Manitoba area with success in identifying extensions of the copper-gold rich feeder zone at the 1901 deposit and compiling results from ongoing infill drilling at Lalor.

Arizona Regional Exploration

A majority of the infill drilling to support the pre-feasibility study for the Copper World Complex has been completed, and in July, we reduced the number of drill rigs at site to three. Ongoing drilling will focus on continued confirmatory drilling in support of future feasibility studies.

Nevada Regional Exploration

A conductivity-resistivity IP ground survey will be conducted in the second half of 2022 at the Mason Valley properties located on private land claims near the Mason project. This work, in combination with a re-interpretation of geological data from past operating mines and previous exploration data, will be used to finalize a drill plan to test high grade skarn targets. The drilling program initially planned for late 2022 has been postponed to a later date considering the recent changes in the metal price environment.

Dividend Declared

A semi-annual dividend of C$0.01 per share was declared on August 8, 2022. The dividend will be paid out on September 23, 2022 to shareholders of record as of September 2, 2022.

PERU OPERATIONS REVIEW

| Three months ended | Six months ended | Guidance | ||||||||||||||

| Jun. 30, 2022 |

Jun. 30, 2021 |

Jun. 30, 2022 |

Jun. 30, 2021 |

Annual | ||||||||||||

| 2022 | ||||||||||||||||

| Constancia ore mined 1 | tonnes | 7,017,114 | 8,016,373 | 13,925,265 | 15,763,839 | |||||||||||

| Copper | % | 0.33 | 0.30 | 0.32 | 0.30 | |||||||||||

| Gold | g/tonne | 0.04 | 0.04 | 0.04 | 0.04 | |||||||||||

| Silver | g/tonne | 3.53 | 3.02 | 3.37 | 2.96 | |||||||||||

| Molybdenum | % | 0.01 | 0.01 | 0.01 | 0.01 | |||||||||||

| Pampacancha ore mined 1 | tonnes | 1,211,387 | 982,992 | 2,058,693 | 982,992 | |||||||||||

| Copper | % | 0.29 | 0.26 | 0.28 | 0.26 | |||||||||||

| Gold | g/tonne | 0.28 | 0.27 | 0.35 | 0.27 | |||||||||||

| Silver | g/tonne | 4.25 | 4.43 | 4.17 | 4.43 | |||||||||||

| Molybdenum | % | 0.01 | 0.01 | 0.01 | 0.01 | |||||||||||

| Total ore mined | tonnes | 8,228,501 | 8,999,365 | 15,983,958 | 16,746,831 | |||||||||||

| Strip ratio 2 | 1.22 | 0.83 | 1.16 | 0.83 | ||||||||||||

| Ore milled | tonnes | 7,770,706 | 7,413,043 | 14,984,539 | 13,775,795 | |||||||||||

| Copper | % | 0.32 | 0.31 | 0.31 | 0.32 | |||||||||||

| Gold | g/tonne | 0.09 | 0.07 | 0.09 | 0.06 | |||||||||||

| Silver | g/tonne | 3.64 | 2.88 | 3.46 | 2.86 | |||||||||||

| Molybdenum | % | 0.01 | 0.01 | 0.01 | 0.01 | |||||||||||

| Copper concentrate | tonnes | 93,122 | 82,696 | 174,730 | 160,656 | |||||||||||

| Concentrate grade | % Cu | 22.42 | 23.05 | 22.92 | 22.96 | |||||||||||

| Copper recovery | % | 85.0 | 83.3 | 85.2 | 83.7 | |||||||||||

| Gold recovery | % | 60.3 | 62.2 | 60.1 | 58.6 | |||||||||||

| Silver recovery | % | 64.2 | 68.2 | 65.4 | 69.0 | |||||||||||

| Molybdenum recovery | % | 38.8 | 33.3 | 30.1 | 33.3 | |||||||||||

| Combined unit operating costs 3,4,5 | $/tonne | 12.02 | 10.40 | 12.19 | 11.02 | 10.10 - 12.90 6 | ||||||||||

| 1 Reported tonnes and grade for ore mined are estimates based on mine plan assumptions and may not reconcile fully to ore milled. | ||||||||||||||||

| 2 Strip ratio is calculated as waste mined divided by ore mined. | ||||||||||||||||

| 3 Reflects combined mine, mill and general and administrative ("G&A") costs per tonne of ore milled. Reflects the deduction of expected capitalized stripping costs. | ||||||||||||||||

| 4 Combined unit costs is a non-IFRS financial performance measure with no standardized definition under IFRS. For further information and a detailed reconciliation, please see the discussion under the "Non-IFRS Financial Reporting Measures" section of this MD&A. | ||||||||||||||||

| 5 Excludes approximately $1.3 million, or $0.16 per tonne and $3.6 million, or $0.24 per tonne , of COVID-19 related costs during the three and six months ended June 30, 2022 respectively and $6.3 million, or $0.85 per tonne and $10.9 million or $0.79 per tonne, of COVID-19 related costs during the three and six months ended June 30, 2021. | ||||||||||||||||

| 6 Combined unit cost guidance for 2022 excludes COVID-19 related costs. | ||||||||||||||||

Total ore mined declined by 9% in the second quarter of 2022 compared to the same period in 2021 due to higher amounts of waste being mined. Ore milled during the second quarter of 2022 was 5% higher than the same period in 2021. Milled copper grades increased in the second quarter of 2022 in comparison to the same period in 2021 due to higher head grades from both Constancia and Pampacancha. Milled gold grades increased significantly in the second quarter of 2022 mainly due to higher volumes and gold grades from Pampacancha.

Copper recoveries in the second quarter increased marginally over the comparative 2021 period due to operational improvements in the cleaning circuit and lower oxide levels of the Constancia ore. Gold recoveries in the second quarter of 2022 were 3% lower than the comparative 2021 period and silver recoveries decreased by 6% over the same time frame due to higher levels of contaminants impacting the metallurgy of the Pampacancha ores.

Year-to-date ore mined was 5% lower than the same period in 2021 due to the same factors as the quarterly variance. Recoveries of copper and gold in the first half of 2022 were marginally higher than the same period in 2021. Recoveries of copper increased due to the same factors as described above for the quarter-over-quarter variance. Recoveries of gold increased due to higher gold grades at Pampacancha.

Combined mine, mill and G&A unit operating costs in the second quarter of 2022 were 16% higher than the same period in 2021 primarily due to inflationary pressures on fuel, consumables and energy costs, partially offset by additional tonnes milled. Combined mine, mill and G&A unit operating costs in the first half of 2022 were 11% higher than the same period in 2021 due to the same factors as the quarterly variance. As a result of inflationary cost pressures, full year unit operating costs in Peru are expected to be closer to the top end of the 2022 guidance range.

| Contained metal in concentrate produced |

Three months ended | Six months ended | Guidance | |||||||||||||

| Jun. 30, 2022 |

Jun. 30, 2021 |

Jun. 30, 2022 |

Jun. 30, 2021 |

Annual | ||||||||||||

| 2022 | ||||||||||||||||

| Copper | tonnes | 20,880 | 19,058 | 40,046 | 36,885 | 89,000 - 115,000 | ||||||||||

| Gold | oz | 13,858 | 10,220 | 24,647 | 14,858 | 70,000 - 90,000 | ||||||||||

| Silver | oz | 584,228 | 468,057 | 1,089,796 | 873,771 | 1,620,000 - 2,100,000 | ||||||||||

| Molybdenum | tonnes | 390 | 295 | 596 | 589 | 1,100 - 1,400 | ||||||||||

Production of all metals, and especially gold and silver, was higher in the second quarter of 2022 and year-to-date compared to the same periods in 2021 due to an increase in throughput, grade and recovery in the case of copper and molybdenum, and, in the case of gold and silver, due to increases in grade and throughput. As previously disclosed, full year production in Peru is expected to benefit from higher grades in the fourth quarter of 2022. As such, full year production of all metals in Peru remains on track to achieve the guidance ranges for 2022.

Peru Cash Cost and Sustaining Cash Cost

| Three months ended | Six months ended | Guidance | ||||||||||||||

| Jun. 30, 2022 |

Jun. 30, 2021 |

Jun. 30, 2022 |

Jun. 30, 2021 |

Annual 2022 |

||||||||||||

| Cash cost per pound of copper produced, net of by-product credits1 | $/lb | 1.82 | 1.85 | 1.69 | 1.84 | 1.10 - 1.40 | ||||||||||

| Sustaining cash cost per pound of copper produced, net of by-product credits1 | $/lb | 2.62 | 2.69 | 2.45 | 2.53 | |||||||||||

| 1 Cash cost and sustaining cash costs per pound of copper produced, net of by-product credits, are not recognized under IFRS. For more detail on these non-IFRS financial performance measures, please see the discussion under the "Non-IFRS Financial Performance Measures" section of this MD&A. | ||||||||||||||||

Cash cost per pound of copper produced, net of by-product credits, in the second quarter of 2022 was $1.82, a slight decrease compared to the same period in 2021 due to higher copper production and higher precious metal by-product credits, partially offset by higher overall mining, milling and general and administrative costs. Cash cost per pound of copper produced, net of by-product credits, is expected to decline with higher expected copper production and contributions from precious metal by-product in the fourth quarter. However, full year cash cost is expected to trend towards the upper end of the 2022 guidance range, reflecting the current inflationary cost environment. Cash cost per pound of copper produced, net of by-product credits, for the first half of 2022 was $1.69, a decrease of 8% compared to the same period in 2021 due to the same factors as outlined above.

Sustaining cash cost per pound of copper produced, net of by-product credits, for the second quarter and for the first half of 2022 both decreased by 3% compared to the same period of 2021 mainly due to the same factors affecting cash costs noted above, partially offset by higher sustaining capital expenditures.

Metal Sold

| Three months ended | Six months ended | ||||||||||||

| Jun. 30, 2022 | Jun. 30, 2021 | Jun. 30, 2022 | Jun. 30, 2021 | ||||||||||

| Payable metal in concentrate | |||||||||||||

| Copper | tonnes | 18,473 | 19,946 | 35,298 | 34,782 | ||||||||

| Gold | oz | 8,430 | 5,638 | 22,882 | 8,601 | ||||||||

| Silver | oz | 484,946 | 315,064 | 1,121,079 | 652,676 | ||||||||

| Molybdenum | tonnes | 208 | 265 | 421 | 549 | ||||||||

Quantities of payable metal sold for the three and six months ended June 30, 2022 were primarily affected by the same factors as contained metal production but were negatively impacted by elevated closing copper and molybdenum concentrate inventories at the end of June 2022.

MANITOBA OPERATIONS REVIEW

Mines

| Three months ended | Six months ended | ||||||||||||

| Jun. 30, 2022 | Jun. 30, 2021 | Jun. 30, 2022 | Jun. 30, 2021 | ||||||||||

| Lalor | |||||||||||||

| Ore | tonnes | 412,653 | 356,951 | 799,405 | 778,553 | ||||||||

| Copper | % | 0.70 | 0.64 | 0.75 | 0.60 | ||||||||

| Zinc | % | 3.06 | 3.81 | 3.54 | 4.56 | ||||||||

| Gold | g/tonne | 3.73 | 3.19 | 3.74 | 2.91 | ||||||||

| Silver | g/tonne | 23.95 | 22.98 | 23.46 | 22.86 | ||||||||

| 777 | |||||||||||||

| Ore | tonnes | 226,286 | 255,170 | 484,355 | 530,430 | ||||||||

| Copper | % | 1.03 | 0.82 | 1.12 | 1.46 | ||||||||

| Zinc | % | 3.51 | 3.57 | 3.83 | 3.79 | ||||||||

| Gold | g/tonne | 1.62 | 1.97 | 1.66 | 2.18 | ||||||||

| Silver | g/tonne | 20.63 | 23.35 | 20.85 | 26.45 | ||||||||

| Total Mines | |||||||||||||

| Ore | tonnes | 638,939 | 612,121 | 1,283,760 | 1,308,983 | ||||||||

| Copper | % | 0.82 | 0.72 | 0.89 | 0.95 | ||||||||

| Zinc | % | 3.22 | 3.71 | 3.65 | 4.25 | ||||||||

| Gold | g/tonne | 2.98 | 2.68 | 2.95 | 2.63 | ||||||||

| Silver | g/tonne | 22.77 | 23.14 | 22.48 | 24.31 | ||||||||

| Unit Operating Costs 1,2 | Three months ended | Six months ended | |||||||||||

| Jun. 30, 2022 | Jun. 30, 2021 | Jun. 30, 2022 | Jun. 30, 2021 | ||||||||||

| Mines | |||||||||||||

| Lalor | C$/tonne | 129.74 | 123.44 | 128.14 | 115.92 | ||||||||

| 777 | C$/tonne | 70.78 | 90.61 | 87.50 | 86.45 | ||||||||

| Total Mines | C$/tonne | 108.86 | 109.75 | 112.81 | 103.98 | ||||||||

| 1 Reflects costs per tonne of ore mined. | |||||||||||||

| 2 Unit costs is a non-IFRS financial performance measure with no standardized definition under IFRS. For further information and a detailed reconciliation, please see the discussion under the "Non-IFRS Financial Reporting Measures" section of this MD&A. |

|||||||||||||

After 18 years of steady production at our 777 mine in Manitoba, the final reserves were depleted with the last ore hoisted on June 17, 2022, consistent with the mine plan. Closure activities to safely decommission the mine commenced in the second quarter and are advancing ahead of schedule. As 777 mining activities wound down, our employees and equipment transitioned from 777 to Lalor to support Lalor's ramp-up strategy.

We continued to advance the Lalor ramp-up strategy and remain on track to achieve 5,300 tonnes per day by the end of 2022. We also further refined the processes to separate gold and base metal ores from Lalor to optimize feed for the New Britannia and Stall mills. Metal grades form the basis of separating higher gold content ore for processing at New Britannia from base metal ore which is directed towards Stall. Lalor successfully completed planned maintenance in the second quarter to allow for increased availability in the third quarter.

Ore mined at our Manitoba operations during the second quarter of 2022 was 4% higher than the same period in 2021 due to increased Lalor production, partially offset by lower production at 777 as it approached closure in June 2022. Copper, gold and silver grades mined at Lalor during the second quarter of 2022 were 9%, 17% and 4% higher, respectively, compared to the same period in 2021, mainly due to increased mining of gold and copper-gold stopes. Zinc grades mined during the second quarter of 2022 were 20% lower than the same period in 2021, in line with the mine plan. Zinc, gold and silver grades at 777 were 2%, 18% and 12% lower, respectively, than the same period in 2021, while copper grades were 26% higher consistent with expectations of remnant mining of final stopes.

Ore mined at our Manitoba operations during the first half of 2022 was 2% lower than the same period in 2021 due to lower production at 777, offset by increased Lalor production for the reasons listed above. Copper, gold and silver grades mined at Lalor during the first half of 2022 were 25%, 29% and 3% higher, respectively, compared to the same period in 2021, mainly due to increased mining of gold and copper-gold stopes. Zinc grades mined at Lalor during the first half of 2022 were 22% lower than the same period in 2021, in line with the mine plan. Copper, gold and silver grades at 777 were 23%, 24% and 21% lower than the same period in 2021 as challenging ground conditions resulted in excessive dilution during remnant stope mining as the mine approached the end of life. Zinc grades mined at 777 during the first half of 2022 were 1% higher than the same period in 2021.

Total mine unit operating costs during the second quarter of 2022 decreased by 1% compared to the same period in 2021 mainly due to lower costs at 777 as the mine ceased operations during the quarter, partially offset by higher inflationary cost pressures for bulk commodities, fuel, and Lalor contractor costs.

Total mine unit operating costs during the first half of 2022 increased by 8% compared to the same period in 2021 due to higher propane usage early in the year caused by a colder winter coupled with inflationary cost pressures for bulk commodities, fuel, and Lalor contractor costs.

Processing Facilities

| Three months ended | Six months ended | ||||||||||||

| Jun. 30, 2022 | Jun. 30, 2021 | Jun. 30, 2022 | Jun. 30, 2021 | ||||||||||

| Stall & New Britannia Concentrator Combined | |||||||||||||

| Ore | tonnes | 406,006 | 317,484 | 803,307 | 678,828 | ||||||||

| Copper | % | 0.73 | 0.68 | 0.78 | 0.64 | ||||||||

| Zinc | % | 3.20 | 4.06 | 3.71 | 4.84 | ||||||||

| Gold | g/tonne | 3.93 | 3.19 | 3.90 | 2.86 | ||||||||

| Silver | g/tonne | 23.98 | 22.02 | 23.57 | 22.76 | ||||||||

| Copper concentrate | tonnes | 15,384 | 11,028 | 31,664 | 21,375 | ||||||||

| Concentrate grade | % Cu | 17.26 | 17.40 | 17.44 | 17.74 | ||||||||

| Zinc concentrate | tonnes | 19,189 | 22,575 | 45,658 | 58,269 | ||||||||

| Concentrate grade | % Zn | 51.08 | 50.29 | 51.07 | 50.71 | ||||||||

| Copper recovery - concentrate | % | 89.5 | 88.8 | 88.5 | 87.3 | ||||||||

| Zinc recovery - concentrate (Stall) | % | 84.3 | 88.1 | 85.1 | 89.9 | ||||||||

| Gold recovery - concentrate | % | 58.8 | 55.5 | 58.6 | 56.5 | ||||||||

| Silver recovery - concentrate | % | 58.1 | 55.1 | 59.0 | 55.7 | ||||||||

| Contained metal in concentrate produced | |||||||||||||

| Copper | tonnes | 2,656 | 1,919 | 5,523 | 3,791 | ||||||||

| Zinc | tonnes | 9,803 | 11,352 | 23,319 | 29,548 | ||||||||

| Gold | oz | 30,113 | 18,078 | 58,995 | 35,285 | ||||||||

| Silver | oz | 181,786 | 123,844 | 359,431 | 276,750 | ||||||||

| Metal in doré produced | |||||||||||||

| Gold | oz | 7,441 | - | 13,721 | - | ||||||||

| Silver | oz | 15,974 | - | 26,020 | - | ||||||||

| Flin Flon Concentrator | |||||||||||||

| Ore | tonnes | 243,312 | 329,503 | 497,344 | 612,889 | ||||||||

| Copper | % | 1.02 | 0.89 | 1.11 | 1.35 | ||||||||

| Zinc | % | 3.60 | 3.65 | 3.87 | 3.90 | ||||||||

| Gold | g/tonne | 1.64 | 2.06 | 1.67 | 2.19 | ||||||||

| Silver | g/tonne | 20.76 | 23.65 | 21.00 | 25.67 | ||||||||

| Copper concentrate | tonnes | 9,498 | 11,504 | 22,602 | 33,816 | ||||||||

| Concentrate grade | % Cu | 22.44 | 21.70 | 21.24 | 21.74 | ||||||||

| Zinc concentrate | tonnes | 14,335 | 20,096 | 31,602 | 39,209 | ||||||||

| Concentrate grade | % Zn | 50.58 | 50.69 | 50.59 | 50.83 | ||||||||

| Copper recovery | % | 85.5 | 84.8 | 86.7 | 89.0 | ||||||||

| Zinc recovery | % | 82.9 | 84.8 | 83.0 | 83.3 | ||||||||

| Gold recovery | % | 56.4 | 52.9 | 57.1 | 58.4 | ||||||||

| Silver recovery | % | 51.0 | 37.5 | 51.8 | 45.9 | ||||||||

| Contained metal in concentrate produced | |||||||||||||

| Copper | tonnes | 2,132 | 2,497 | 4,801 | 7,351 | ||||||||

| Zinc | tonnes | 7,250 | 10,186 | 15,986 | 19,930 | ||||||||

| Gold | oz | 7,233 | 11,550 | 15,238 | 25,205 | ||||||||

| Silver | oz | 82,865 | 94,015 | 173,963 | 232,068 | ||||||||

| Unit Operating Costs 1 | Three months ended | Six months ended | Guidance | |||||||||||||

| Jun. 30, 2022 |

Jun. 30, 2021 |

Jun. 30, 2022 |

Jun. 30, 2021 |

Annual | ||||||||||||

| 2022 | ||||||||||||||||

| Concentrators | ||||||||||||||||

| Stall & New Britannia | C$/tonne | 49.46 | 24.80 | 49.76 | 23.90 | |||||||||||

| Flin Flon | C$/tonne | 27.36 | 26.95 | 28.14 | 27.01 | |||||||||||

| Combined mine/mill unit operating costs 2,3 | ||||||||||||||||

| Manitoba | C$/tonne | 168 | 148 | 172 | 150 | 170 - 185 | ||||||||||

| 1 Reflects costs per tonne of milled ore. | ||||||||||||||||

| 2 Reflects combined mine, mill and G&A costs per tonne of milled ore. | ||||||||||||||||

| 3 Combined unit costs is a non-IFRS financial performance measure with no standardized definition under IFRS. For further information and a detailed reconciliation, please see the discussion under the "Non-IFRS Financial Reporting Measures" section of this MD&A. | ||||||||||||||||

The combined Snow Lake mills processed 28% more ore in the second quarter of 2022 compared to the same period in 2021, tracking the increase in Lalor's production over the same period. Stall recoveries were consistent with the metallurgical model for the head grades delivered. Compared to the same period in 2021, unit operating costs at the Snow Lake mills were higher in the second quarter of 2022 as a result of the higher costs at New Britannia.

The combined Snow Lake mills processed 18% more ore in the first half of 2022 compared to the same period in 2021. Stall recoveries were consistent with the metallurgical model for the head grades delivered. Compared to the same period in 2021, unit operating costs at the Snow Lake mills were higher in first six months of 2022 for the same reasons outlined in the second quarter variance as well as scheduled mill maintenance at New Britannia early in the year.

The New Britannia mill achieved higher than targeted throughput in the second quarter of 2022 averaging approximately 1,590 tonnes per day, due to a number of improvement initiatives aimed at increasing throughput and further improving recoveries. With the inclusion of doré, the gold and silver recoveries at the New Britannia mill have also improved significantly in relation to previous quarters. Additional improvement initiatives will continue to be advanced in the second half of 2022 to further improve gold and silver recoveries.

The Flin Flon concentrator consumed all available ore feed from the 777 mine in the second quarter of 2022. Last ore from 777 was processed on June 21, 2022 and closure activities to safely place the concentrator on long-term care and maintenance are ahead of schedule. Recoveries at the Flin Flon concentrator were consistent with the metallurgical model for the head grades delivered. Unit operating costs at the Flin Flon concentrator increased by 2% during the second quarter compared to the same period in 2021 primarily as a result of increased grinding media used to fulfill paste requirements at the 777 mine.

Unit costs at the Snow Lake mills increased by 108% in the first six months of 2022 compared to the same period in 2021 due to higher than expected milling costs at New Britannia, baseline effects as New Britannia was not yet operational in the comparative period, as well as higher inflationary cost pressures. Flin Flon concentrator unit costs increased by 4% over the same timeframe.

Combined unit operating costs in the second quarter of 2022 and year-to-date increased by 14% and 15%, respectively, compared to the same periods in 2021 for the same reasons as outlined above. Looking ahead to the second half of 2022, we expect combined unit operating costs to increase due to ongoing inflationary cost pressures and the removal of the lower-cost Flin Flon operations. As such, we expect the full year combined unit costs to trend towards the upper end of the 2022 guidance range.

| Three months ended | Six months ended | Guidance | ||||||||||||||

| Contained metal in concentrate produced 1 | Jun. 30, 2022 |

Jun. 30, 2021 |

Jun. 30, 2022 |

Jun. 30, 2021 |

Annual | |||||||||||

| 2022 | ||||||||||||||||

| Copper | tonnes | 4,788 | 4,416 | 10,324 | 11,142 | 12,000 - 16,000 | ||||||||||

| Gold 2 | oz | 37,346 | 29,628 | 74,233 | 60,490 | - | ||||||||||

| Silver 3 | oz | 264,651 | 217,859 | 533,394 | 508,818 | - | ||||||||||

| Zinc | tonnes | 17,053 | 21,538 | 39,305 | 49,478 | 50,000 - 70,000 | ||||||||||

| Metal in doré produced 1 | ||||||||||||||||

| Gold 2 | oz | 7,441 | - | 13,721 | - | - | ||||||||||

| Silver 3 | oz | 15,974 | - | 26,020 | - | - | ||||||||||

| Contained metal in concentrate and doré produced | ||||||||||||||||

| Gold 2 | oz | 44,787 | 29,628 | 87,954 | 60,490 | 150,000 - 185,000 | ||||||||||

| Silver 3 | oz | 280,625 | 217,859 | 559,414 | 508,818 | 800,000 - 1,100,000 | ||||||||||

| 1 Metal reported in concentrate is prior to deductions associated with smelter terms. | ||||||||||||||||

| 2 Gold production guidance includes gold contained in concentrate produced and gold in doré. | ||||||||||||||||

| 3 Silver production guidance includes silver contained in concentrate produced and silver in doré. | ||||||||||||||||

Compared to the same period in 2021, gold and silver production in the second quarter of 2022 increased by 51% and 29%, respectively. This increase is primarily due to the processing of higher volumes of gold ore from Lalor at the New Britannia mill, offset by lower gold and silver grades at the 777 mine. Copper production increased by 8% in the second quarter of 2022 compared to the same period in 2021 due to significantly higher copper grades at 777 from the mining of remnant stopes, partially offset by lower volume of 777 ore mined. Zinc production in the second quarter decreased by 21% primarily due to lower head grades at Lalor consistent with the mine plan.

Compared to the same period in 2021, gold and silver production in the first half of 2022 increased by 45% and 10%, respectively. This increase is primarily due to the same reasons noted above. Copper and zinc production decreased by 8% and 21%, respectively, in the first half of 2022 due to lower zinc head grades at Lalor and lower 777 volumes as the mine fully depleted its reserves and ceased production in June 2022.

Full year production of all metals are on track to achieve guidance ranges for 2022.

Zinc Plant

| Zinc Production | Three months ended | Six months ended | |||||||||||

| Jun. 30, 2022 |

Jun. 30, 2021 |

Jun. 30, 2022 |

Jun. 30, 2021 |

||||||||||

| Zinc Concentrate Treated | |||||||||||||

| Domestic | tonnes | 34,500 | 47,376 | 76,223 | 101,865 | ||||||||

| Refined Metal Produced | |||||||||||||

| Domestic | tonnes | 17,831 | 22,419 | 37,894 | 48,927 | ||||||||

| Unit Operating Costs | Three months ended | Six months ended | |||||||||||

| Jun. 30, 2022 |

Jun. 30, 2021 |

Jun. 30, 2022 |

Jun. 30, 2021 |

||||||||||

| Zinc Plant 1,2 | C$/lb | 0.57 | 0.54 | 0.60 | 0.52 | ||||||||

| 1 Zinc unit operating costs include G&A costs. 2 Zinc unit costs is a non-IFRS financial performance measure with no standardized definition under IFRS. For further information and a detailed reconciliation, please see the discussion under the "Non-IFRS Financial Reporting Measures" section of this MD&A. |

|||||||||||||

The zinc plant production remained constrained by the availability of concentrate for processing through to its last day of operation on June 30, 2022. Closure activities to safely decommission the zinc plant are underway and are advancing ahead of schedule.

Manitoba Cash Cost and Sustaining Cash Cost

| Three months ended | Six months ended | Guidance | ||||||||||||||

| Jun. 30, 2022 |

Jun. 30, 2021 |

Jun. 30, 2022 |

Jun. 30, 2021 |

Annual 2022 |

||||||||||||

| Cost per pound of copper produced | ||||||||||||||||

| Cash cost per pound of copper produced, net of by-product credits 1 | $/lb | (4.48 | ) | (3.51 | ) | (2.29 | ) | (2.02 | ) | |||||||

| Sustaining cash cost per pound of copper produced, net of by-product credits 1 | $/lb | (1.40 | ) | 0.36 | 0.60 | 1.12 | ||||||||||

| Cost per ounce of gold produced | ||||||||||||||||

| Cash cost per ounce of gold produced, net of by-product credits 1 | $/oz | (207 | ) | - | 99 | - | 300 - 550 | |||||||||

| Sustaining cash cost per ounce of gold produced, net of by-product credits 1 | $/oz | 519 | - | 847 | - | |||||||||||

| 1 Cash cost and sustaining cash cost per pound of copper and per ounce of gold produced, net of by-product credits, are not recognized under IFRS. For more detail on this non-IFRS financial performance measure, please see the discussion under the "Non-IFRS Financial Performance Measures" section of this MD&A. | ||||||||||||||||

| 2 Cash cost and sustaining cash cost per ounce of gold produced, net of by-product credits were introduced in 2022 and do not have a published comparative. | ||||||||||||||||

Cash cost per pound of copper produced, net of by-product credits, in the second quarter of 2022 was negative $4.48. These costs were lower compared to the same period in 2021, as a result of higher zinc and gold by-product revenues offset by higher milling and profit sharing costs and slightly higher copper production.

Sustaining cash cost per pound of copper produced, net of by-product credits, in the second quarter of 2022 was negative $1.40. These costs were lower compared to the same period in 2021, primarily due to the reasons listed above and lower cash sustaining capital expenditures compared to the same period in 2021.

Cash cost per pound of copper produced, net of by-product credits, in the first half of 2022 was negative $2.29. These costs were lower compared to the same period in 2021, as a result of higher gold by-product revenues and slightly lower copper production offset by higher mining, milling and profit sharing costs.

Sustaining cash cost per pound of copper produced, net of by-product credits, in the first half of 2022 was $0.60. These costs were lower compared to the same period in 2021, due to the same reasons provided above and lower cash sustaining capital expenditures compared to the same period in 2021.

Cash cost per ounce of gold produced, net of by-product credits, in the second quarter and for the first half of 2022 were well below our 2022 guidance range.

Metal Sold

| Three months ended | Six months ended | ||||||||||||

| Jun. 30, 2022 |

Jun. 30, 2021 |

Jun. 30, 2022 |

Jun. 30, 2021 |

||||||||||

| Payable metal in concentrate and doré | |||||||||||||

| Copper | tonnes | 5,177 | 5,230 | 8,961 | 11,323 | ||||||||

| Gold | oz | 42,454 | 32,567 | 76,345 | 54,987 | ||||||||

| Silver | oz | 253,225 | 262,443 | 481,684 | 434,591 | ||||||||

| Zinc 1 | tonnes | 20,793 | 25,361 | 38,099 | 53,704 | ||||||||

| 1 Includes refined zinc metal and payable zinc in concentrate sold. | |||||||||||||

Sales of copper and silver in the second quarter of 2022 were lower than the comparable period in 2021 but higher than the first quarter of 2022 as approximately 60% excess copper concentrate inventory from the first quarter of 2022 has been drawn down during the second quarter of 2022 with improving railcar availability. Quantities of payable gold and zinc sold for the three and six months ended June 30, 2022 were primarily affected by the same factors as contained metal production.

FINANCIAL REVIEW

Financial Results

In the second quarter of 2022, we recorded a net profit of $32.1 million compared to a net loss of $3.4 million in the second quarter of 2021. Year-to-date in 2022, we recorded a net profit of $95.9 million compared to a net loss of $63.5 million for the same period in 2021, representing an increase in profit of $159.4 million.

The following table provides further details on these variances:

| (in $ millions) | Three months ended June 30, 2022 |

Six months ended June 30, 2022 |

||||

| Increase (decrease) in components of profit or loss: | ||||||

| Revenues | 11.3 | 76.2 | ||||

| Cost of sales | ||||||

| Mine operating costs | (15.9 | ) | (49.7 | ) | ||

| Depreciation and amortization | 12.0 | 13.7 | ||||

| Selling and administrative expenses | 8.4 | 6.5 | ||||

| Exploration expenses | 3.5 | (8.3 | ) | |||

| Environmental obligation adjustment | 60.2 | 135.5 | ||||

| Other expenses | 2.8 | (4.8 | ) | |||

| Impairment loss | (95.0 | ) | (95.0 | ) | ||

| Net finance expense | 19.3 | 91.0 | ||||

| Tax | 28.9 | (5.7 | ) | |||

| Decrease in loss for the period | 35.5 | 159.4 |

Revenue

Revenue for the second quarter of 2022 was $415.5 million, $11.3 million higher than the same period in 2021, primarily as a result of higher zinc prices and higher gold sales volumes, partially offset by lower copper and zinc sales volumes and lower copper prices. We continue to see higher sales volumes of gold as a result of the commencement of operations at the high-grade Pampacancha deposit in Peru and the copper-gold circuit at New Britannia mill in Manitoba. Copper sales volumes declined in the second quarter of 2022, relative to the prior year, despite higher copper production, primarily due to general timing of shipments. Lower zinc sales volumes are a result of a reduction in overall zinc production due to the closure of the 777 mine in Manitoba in June of 2022, as well as lower zinc grades from Lalor as we continue to transition to mining of the gold lenses and away from base metal zones.

Revenue for the first half of 2022 was $794.1 million, $76.2 million higher than the same period in 2021, mainly due to higher realized base metal prices as well as higher precious metal sales volumes. Offsetting these increases were lower zinc sales, due to the same reasons as the quarter-to-date variances described above.

The following table provides further details on these variances:

| (in $ millions) | Three months ended June 30, 2022 |

Six months ended June 30, 2022 |

||||

| Metals prices1 | ||||||

| (Lower) higher copper prices | (5.9 | ) | 31.2 | |||

| Higher zinc prices | 25.3 | 42.5 | ||||

| Lower gold prices | (0.4 | ) | (2.4 | ) | ||

| Lower silver prices | (1.8 | ) | (8.5 | ) | ||

| Sales volumes | ||||||

| Lower copper sales volumes | (14.8 | ) | (16.6 | ) | ||

| Lower zinc sales volumes | (14.0 | ) | (46.5 | ) | ||

| Higher gold sales volumes | 22.9 | 63.9 | ||||

| Higher silver sales volumes | 4.3 | 14.6 | ||||

| Other | ||||||

| Change in derivative mark-to-market on zinc | (0.5 | ) | (0.3 | ) | ||

| Molybdenum and other volume and pricing differences | (4.0 | ) | (3.4 | ) | ||

| Variable consideration adjustments | - | 1.6 | ||||

| Effect of lower treatment and refining charges | 0.2 | 0.1 | ||||

| Increase in revenue in 2022 compared to 2021 | 11.3 | 76.2 | ||||

| 1 See discussion below for further information regarding metals prices. | ||||||

Our revenue by significant product type is summarized below:

| Three months ended | Six months ended | |||||||||||

| (in $ millions) | Jun. 30, 2022 | Jun. 30, 2021 | Jun. 30, 2022 | Jun. 30, 2021 | ||||||||

| Copper | 230.8 | 250.2 | 439.7 | 423.9 | ||||||||

| Zinc | 88.7 | 77.4 | 155.2 | 159.5 | ||||||||

| Gold | 90.3 | 57.9 | 157.9 | 100.1 | ||||||||

| Silver | 8.9 | 7.2 | 15.5 | 13.6 | ||||||||

| Molybdenum | 9.0 | 7.1 | 18.2 | 14.2 | ||||||||

| Other metals | 2.0 | 2.6 | 4.4 | 4.2 | ||||||||

| Revenue from contracts | 429.7 | 402.4 | 790.9 | 715.5 | ||||||||

| Amortization of deferred revenue - gold | 10.0 | 9.2 | 23.2 | 14.1 | ||||||||

| Amortization of deferred revenue - silver | 9.2 | 7.9 | 21.0 | 16.6 | ||||||||

| Amortization of deferred revenue - variable consideration adjustments - prior periods | - | - | 3.2 | 1.6 | ||||||||

| Pricing and volume adjustments1 | (18.4 | ) | (0.1 | ) | (17.1 | ) | (2.7 | ) | ||||

| Treatment and refining charges | (15.0 | ) | (15.2 | ) | (27.1 | ) | (27.2 | ) | ||||

| Revenue | 415.5 | 404.2 | 794.1 | 717.9 | ||||||||

| 1 Pricing and volume adjustments represents mark-to-market adjustments on provisionally prices sales, realized and unrealized changes to fair value for non-hedge derivative contracts and adjustments to originally invoiced weights and assays. | ||||||||||||

For further detail on variable consideration adjustments, refer to note 16 of our consolidated interim financial statements.

Realized sales prices

This measure is intended to enable management and investors to understand the average realized price of metals sold to third parties in each reporting period. The average realized price per unit sold does not have any standardized meaning prescribed by IFRS, is unlikely to be comparable to similar measures presented by other issuers and should not be considered in isolation or a substitute for measures of performance prepared in accordance with IFRS.

For sales of copper, gold and silver we may enter into non-hedge derivatives ("QP hedges") which are intended to manage the provisional pricing risk arising from quotational period terms in concentrate sales agreements. The QP hedges are not removed from the calculation of realized prices. We expect that gains and losses on QP hedges will offset provisional pricing adjustments on concentrate sales contracts.

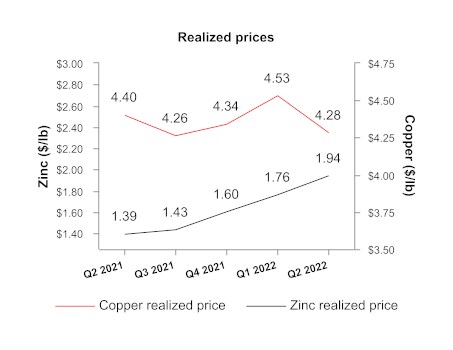

Our realized prices for the second quarter of 2022 and 2021, respectively, are summarized below:

| Realized prices1 for the | LME YTD 20222 |

Realized prices1 for the | |||||||||||||||||

| LME QTD 20222 |

Three months ended | Six months ended | |||||||||||||||||

| Jun. 30, 2022 |

Jun. 30, 2021 |

Jun. 30, 2022 |

Jun. 30, 2021 |

||||||||||||||||

| Prices | |||||||||||||||||||

| Copper | $/lb | 4.31 | 4.28 | 4.40 | 4.42 | 4.40 | 4.08 | ||||||||||||

| Zinc3 | $/lb | 1.78 | 1.94 | 1.39 | 1.74 | 1.86 | 1.35 | ||||||||||||

| Gold4 | $/oz | 1,795 | 1,803 | 1,769 | 1,793 | ||||||||||||||

| Silver4 | $/oz | 24.32 | 26.74 | 22.83 | 28.12 | ||||||||||||||

| 1 Realized prices exclude refining and treatment charges and are on the sale of finished metal or metal in concentrate. Realized prices include the effect of provisional pricing adjustments on prior period sales. | |||||||||||||||||||

| 2 London Metal Exchange average for copper and zinc prices. | |||||||||||||||||||

| 3 All sales for the three and six months ended June 30, 2022 and 2021 were cast zinc metal. Zinc realized prices include premiums paid by customers for delivery of refined zinc metal, but exclude unrealized gains and losses related to non-hedge derivative contracts that are included in zinc revenues. | |||||||||||||||||||

| 4 Sales of gold and silver from our 777 and Constancia mines are subject to our precious metals stream agreement with Wheaton, pursuant to which we recognize deferred revenue for precious metals deliveries and also receive cash payments. Stream sales are included within realized prices and their respective deferred revenue and cash payment rates can be found on page 29. | |||||||||||||||||||

The following tables provide a reconciliation of average realized price per unit sold, by metal, to revenues as shown in the consolidated financial statements.

| Three months ended June 30, 2022 | |||||||||||||||||||||

| (in $ millions) 1 | Copper | Zinc | Gold | Silver | Molybdenum | Other | Total | ||||||||||||||

| Revenue from contracts 2 | 230.8 | 88.7 | 90.3 | 8.9 | 9.0 | 2.0 | 429.7 | ||||||||||||||

| Amortization of deferred revenue | - | - | 10.0 | 9.2 | - | - | 19.2 | ||||||||||||||

| Pricing and volume adjustments 3 | (7.5 | ) | (0.2 | ) | (8.9 | ) | (0.2 | ) | (1.6 | ) | - | (18.4 | ) | ||||||||

| By-product credits 4 | 223.3 | 88.5 | 91.4 | 17.9 | 7.4 | 2.0 | 430.5 | ||||||||||||||

| Derivative mark-to-market 5 | - | 0.5 | - | - | - | - | 0.5 | ||||||||||||||

| Revenue, excluding mark-to-market on non-QP hedges | 223.3 | 89.0 | 91.4 | 17.9 | 7.4 | 2.0 | 431.0 | ||||||||||||||

| Payable metal in concentrate sold 6 | 23,650 | 20,793 | 50,884 | 738,171 | 208 | - | - | ||||||||||||||

| Realized price 7 | 9,442 | 4,282 | 1,795 | 24.32 | - | - | - | ||||||||||||||

| Realized price 8 | 4.28 | 1.94 | - | - | - | - | - | ||||||||||||||

| Six months ended June 30, 2022 | |||||||||||||||||||||

| (in $ millions) 1 | Copper | Zinc | Gold | Silver | Molybdenum | Other | Total | ||||||||||||||

| Revenue from contracts 2 | 439.7 | 155.2 | 157.9 | 15.5 | 18.2 | 4.4 | 790.9 | ||||||||||||||

| Amortization of deferred revenue | - | - | 23.2 | 21.0 | - | - | 44.2 | ||||||||||||||

| Pricing and volume adjustments 3 | (10.7 | ) | 0.5 | (5.6 | ) | 0.1 | (1.4 | ) | - | (17.1 | ) | ||||||||||

| By-product credits 4 | 429.0 | 155.7 | 175.5 | 36.6 | 16.8 | 4.4 | 818.0 | ||||||||||||||

| Derivative mark-to-market 5 | - | 0.4 | - | - | - | - | 0.4 | ||||||||||||||

| Revenue, excluding mark-to-market on non-QP hedges | 429.0 | 156.1 | 175.5 | 36.6 | 16.8 | 4.4 | 818.4 | ||||||||||||||

| Payable metal in concentrate sold 6 | 44,259 | 38,099 | 99,227 | 1,602,763 | 421 | - | - | ||||||||||||||

| Realized price 7 | 9,695 | 4,097 | 1,769 | 22.83 | - | - | - | ||||||||||||||

| Realized price 8 | 4.40 | 1.86 | - | - | - | - | - | ||||||||||||||

| 1 Average realized price per unit sold may not calculate based on amounts presented in this table due to rounding. | |||||||||||||||||||||

| 2 As per financial statements. | |||||||||||||||||||||

| 3 Pricing and volume adjustments represents mark-to-market adjustments on provisionally priced sales, realized and unrealized changes to fair value for non-hedge derivative contracts and adjustments to originally invoiced weights and assays. | |||||||||||||||||||||

| 4 By-product credits subtotal is used in the calculated of cash cost per pound of copper and zinc produced, net of by-product credits. Cash cost per pound of copper and per ounce of gold produced, net of by-product credits, are non-IFRS financial performance measures with no standardized definition under IFRS. For further information and a detailed reconciliation, please see the discussion under the "Non-IFRS Financial Reporting Measures" section of this MD&A. | |||||||||||||||||||||

| 5 Derivative mark-to-market excludes mark-to-market on QP hedges. | |||||||||||||||||||||

| 6 Copper, zinc and molybdenum shown in metric tonnes and gold and silver shown in ounces. | |||||||||||||||||||||

| 7 Realized price for copper, zinc and molybdenum in $/metric tonne and realized price for gold and silver in $/oz. | |||||||||||||||||||||

| 8 Realized price for copper and zinc in $/lb. | |||||||||||||||||||||

The price, quantity and mix of metals sold, affect our revenue, operating cash flow and profit. Revenue from metals sales can vary from quarter to quarter due to production levels, shipping volumes and transfer of risk and title to customers.

| Three months ended June 30, 2021 | |||||||||||||||||||||

| (in $ millions) 1 | Copper | Zinc | Gold | Silver | Molybdenum | Other | Total | ||||||||||||||

| Revenue from contracts 2 | 250.2 | 77.4 | 57.9 | 7.2 | 7.1 | 2.6 | 402.4 | ||||||||||||||

| Amortization of deferred revenue | - | - | 9.2 | 7.9 | - | - | 17.1 | ||||||||||||||

| Pricing and volume adjustments 3 | (6.2 | ) | 0.3 | 1.8 | 0.3 | 3.7 | - | (0.1 | ) | ||||||||||||

| By-product credits 4 | 244.0 | 77.7 | 68.9 | 15.4 | 10.8 | 2.6 | 419.4 | ||||||||||||||

| Derivative mark-to-market 5 | - | - | - | - | - | - | - | ||||||||||||||

| Revenue, excluding mark-to-market on non-QP hedges | 244.0 | 77.7 | 68.9 | 15.4 | 10.8 | 2.6 | 419.4 | ||||||||||||||

| Payable metal in concentrate sold 6 | 25,176 | 25,361 | 38,205 | 577,507 | 265 | - | - | ||||||||||||||

| Realized price 7 | 9,692 | 3,063 | 1,803 | 26.74 | - | - | - | ||||||||||||||

| Realized price 8 | 4.40 | 1.39 | - | - | - | - | - | ||||||||||||||

| Six months ended June 30, 2021 | |||||||||||||||||||||

| (in $ millions) 1 | Copper | Zinc | Gold | Silver | Molybdenum | Other | Total | ||||||||||||||

| Revenue from contracts 2 | 423.9 | 159.5 | 100.1 | 13.6 | 14.2 | 4.2 | 715.5 | ||||||||||||||

| Amortization of deferred revenue | - | - | 14.1 | 16.6 | - | - | 30.7 | ||||||||||||||

| Pricing and volume adjustments 3 | (9.5 | ) | 0.5 | (0.2 | ) | 0.3 | 6.2 | - | (2.7 | ) | |||||||||||

| By-product credits 4 | 414.4 | 160.0 | 114.0 | 30.5 | 20.4 | 4.2 | 743.5 | ||||||||||||||

| Derivative mark-to-market 5 | - | 0.1 | - | - | - | - | 0.1 | ||||||||||||||

| Revenue, excluding mark-to-market on non-QP hedges | 414.4 | 160.1 | 114.0 | 30.5 | 20.4 | 4.2 | 743.6 | ||||||||||||||

| Payable metal in concentrate sold 6 | 46,105 | 53,704 | 63,588 | 1,087,267 | 549 | - | - | ||||||||||||||

| Realized price 7 | 8,989 | 2,982 | 1,793 | 28.12 | - | - | - | ||||||||||||||

| Realized price 8 | 4.08 | 1.35 | - | - | - | - | - | ||||||||||||||

| 1 Average realized price per unit sold may not calculate based on amounts presented in this table due to rounding. | |||||||||||||||||||||

| 2 As per financial statements. | |||||||||||||||||||||

| 3 Pricing and volume adjustments represents mark-to-market adjustments on provisionally priced sales, realized and unrealized changes to fair value for non-hedge derivative contracts and adjustments to originally invoiced weights and assays. | |||||||||||||||||||||

| 4 By-product credits subtotal is used in the calculated of cash cost per pound of copper and zinc produced, net of by-product credits. Cash cost per pound of copper and per ounce of gold produced, net of by-product credits, are non-IFRS financial performance measures with no standardized definition under IFRS. For further information and a detailed reconciliation, please see the discussion under the "Non-IFRS Financial Reporting Measures" section of this MD&A. | |||||||||||||||||||||

| 5 Derivative mark-to-market excludes mark-to-market on QP hedges. | |||||||||||||||||||||

| 6 Copper, zinc and molybdenum shown in metric tonnes and gold and silver shown in ounces. | |||||||||||||||||||||

| 7 Realized price for copper, zinc and molybdenum in $/metric tonne and realized price for gold and silver in $/oz. | |||||||||||||||||||||

| 8 Realized price for copper and zinc in $/lb. | |||||||||||||||||||||

Stream Sales

The following table shows stream sales included within realized prices and their respective deferred revenue and cash payment rates:

| Three months ended | Six months ended | ||||||||||||

| Jun. 30, 2022 | Jun. 30, 2022 | ||||||||||||

| Manitoba | Peru 4 | Manitoba | Peru 4 | ||||||||||

| Gold | oz | 3,629 | 7,431 | 8,017 | 17,926 | ||||||||

| Silver | oz | 75,367 | 494,029 | 162,279 | 1,137,665 | ||||||||

| Gold deferred revenue drawdown rate1,2 | $/oz | 1,241 | 734 | 1,247 | 734 | ||||||||

| Gold cash rate3 | $/oz | 429 | 412 | 429 | 412 | ||||||||

| Total gold stream realized price | $/oz | 1,670 | 1,146 | 1,676 | 1,146 | ||||||||

| Silver deferred revenue drawdown rate1,2 | $/oz | 24.49 | 14.95 | 24.62 | 14.95 | ||||||||

| Silver cash rate3 | $/oz | 6.33 | 6.08 | 6.33 | 6.08 | ||||||||

| Total silver stream realized price | $/oz | 30.82 | 21.03 | 30.95 | 21.03 | ||||||||

| Three months ended | Six months ended | ||||||||||||

| Jun. 30, 2021 | Jun. 30, 2021 | ||||||||||||

| Manitoba | Peru | Manitoba | Peru | ||||||||||

| Gold | oz | 5,694 | 2,321 | 8,271 | 3,997 | ||||||||

| Silver | oz | 109,381 | 295,116 | 158,143 | 641,254 | ||||||||

| Gold deferred revenue drawdown rate1,2 | $/oz | 1,284 | 824 | 1,273 | 894 | ||||||||

| Gold cash rate 3 | $/oz | 425 | 408 | 425 | 408 | ||||||||

| Total gold stream realized price | $/oz | 1,709 | 1,232 | 1,698 | 1,302 | ||||||||

| Silver deferred revenue drawdown rate1,2 | $/oz | 24.73 | 17.54 | 24.50 | 19.87 | ||||||||

| Silver cash rate 3 | $/oz | 6.26 | 6.02 | 6.26 | 6.02 | ||||||||

| Total silver stream realized price | $/oz | 30.99 | 23.56 | 30.76 | 25.89 | ||||||||

| 1Subsequent to the variable consideration adjustment recorded on January 1, 2022, the deferred revenue amortization is recorded in Manitoba at C$1,584/oz gold and C$31.28/oz silver (June 30, 2021 - C$1,578/oz gold and C$30.38/oz silver) and converted to US dollars at the exchange rate in effect at the time of revenue recognition. | |||||||||||||

| 2 Deferred revenue drawdown rates for gold and silver do not include variable consideration adjustments. | |||||||||||||

| 3 The gold and silver cash rate for Manitoba increased by 1% from $400/oz and $5.90/oz effective August 1, 2015. Subsequently every year, on August 1, the cash rate will increase by 1% compounded. The weighted average cash rate is disclosed. The gold and silver cash rate for Peru increased by 1% from $400/oz and $5.90/oz effective August 4, 2019. Subsequently every year, on August 4, the cash rate will increase by 1% compounded. The weighted average cash rate is disclosed. | |||||||||||||