ndm_ex997

EXHIBIT 99.7

ANNUAL INFORMATION FORM

FOR THE YEAR ENDED DECEMBER 31, 2020

This annual information form ("AIF") is as of March 31,

2021

Item

1. Table of Contents

Page

|

Item 1.

|

Table Of Contents

|

2

|

|

Item 2.

|

Preliminary Notes

|

3

|

|

Item 3.

|

Corporate Structure

|

11

|

|

Item 4.

|

General Development Of The Business

|

11

|

|

Item 5.

|

Description Of Business

|

16

|

|

Item 6.

|

Dividends

|

44

|

|

Item 7.

|

Description Of Capital Structure

|

44

|

|

Item 8.

|

Market For Securities

|

44

|

|

Item 9.

|

Escrowed Securities

|

45

|

|

Item 10

|

Directors And Officers

|

45

|

|

Item 11.

|

Promoters

|

53

|

|

Item 12.

|

Legal Proceedings

|

53

|

|

Item 13.

|

Interest Of Management And Others In Material

Transactions

|

56

|

|

Item 14.

|

Transfer Agent And Registrar

|

56

|

|

Item 15.

|

Material Contracts

|

56

|

|

Item 16.

|

Interests Of Experts

|

56

|

|

Item 17.

|

Additional Information

|

57

|

|

Item 18.

|

Disclosure For Companies Not Sending Information

Circulars

|

57

|

|

Item 19.

|

Audit And Risk Committee, Auditor Fees, Exemptions, Code Of

Ethics

|

57

|

|

Appendix A - Audit And Risk Committee Charter

|

60

|

Item

2.

Preliminary Notes

This

AIF contains "forward-looking information" within the meaning of

applicable Canadian securities legislation. Wherever possible,

words such as "plans", "expects", or "does not expect", "budget",

"scheduled", "estimates", "forecasts", "anticipate" or "does not

anticipate", "believe", "intend" and similar expressions or

statements that

certain actions, events or results "may", "could", "would", "might"

or "will" be taken, occur or be achieved, have been used to

identify forward-looking information.

Forward-looking

information in this AIF include, without limitation, statements

regarding:

● our

expectations regarding the potential for securing the necessary

permits for a mine at the Pebble Project and our ability to

establish that such a permitted mine can be economically

developed;

● the success

of our appeal of the record of decision (“ROD”) of the United States Army

Corps of Engineers (the "USACE") denying the issuance of certain

permits required for the Pebble Project ROD;

● our ability

to successfully apply for and obtain the federal and state permits

required for the Pebble Project under the Clean Water Act

("CWA"), the National

Environmental Policy Act ("NEPA"), and relevant

legislation;

● the outcome

of the US government investigations involving the

Company;

● our ability

to successfully defend against purported class action lawsuits that

have been commenced against us;

● our plan of

operations, including our plans to carry out and finance

exploration and development activities;

● our ability

to raise capital for exploration and development activities and

meet our working capital requirements;

● our

expected financial performance in future periods;

● our

expectations regarding the exploration and development potential of

the Pebble Project;

● the outcome

of the legal proceedings in which we are engaged;

● the

uncertainties with respect to the effects of COVID-19;

and

● factors

relating to our investment decisions.

Forward-looking

information is based on the reasonable assumptions, estimates,

analysis and opinions of management made in light of its experience

and its perception of trends, current conditions and expected

developments, as well as other factors that management believes to

be relevant and reasonable in the circumstances at the date that

such statements are made, but which may prove to be incorrect. We

believe that the assumptions and expectations reflected in such

forward-looking information are reasonable.

Key

assumptions upon which the Company’s forward-looking

information are based include:

● our appeal

of the ROD of the USACE will be successful;

● that we

will ultimately be able to demonstrate that a mine at the Pebble

Project can be economically developed and operated in an

environmentally sound and socially responsible manner, meeting all

relevant federal, state and local regulatory requirements so that

we will be ultimately able to obtain permits authorizing

construction of a mine at the Pebble Project;

● that we

will be able to secure sufficient capital necessary for continued

environmental assessment and permitting activities and engineering

work which must be completed prior to any potential development of

the Pebble Project which would then require engineering and

financing in order to advance to ultimate

construction;

● that the

COVID-19 outbreak will not materially impact or delay our ability

to obtain permitting for a mine at the Pebble Project;

|

2020

Annual Information Form

|

Page | 3

|

● that we

will ultimately be able to demonstrate that a mine at the Pebble

Project will be economically feasible based on a mine plan for

which permitting can be secured;

● that the

market prices of copper, gold, molybdenum, rhenium and silver will

not decline significantly or stay depressed for a lengthy period of

time;

● that key

personnel will continue their employment with us; and

● that we

will continue to be able to secure adequate financing on acceptable

terms.

Readers

are cautioned that the foregoing list is not exhaustive of all

factors and assumptions, which may have been used. Forward looking

statements are also subject to risks and uncertainties facing our

business, any of which could have a material impact on our

outlook.

Some of

the risks and uncertainties that could cause actual results to

differ materially from those expressed in the forward-looking

statements include:

● we may be

unsuccessful in our appeal of the ROD with respect to the decision

to deny the issuance of many of the permits which we require to

operate a mine at the Pebble Project;

● an

inability to ultimately obtain permitting for a mine at the Pebble

Project;

● an

inability to establish that the Pebble Project may be economically

developed and mined or contain commercially viable deposits of ore

based on a mine plan for which government authorities are prepared

to grant permits;

● we may not

be successful in defending shareholder securities litigation claims

that have been filed against us in the US and in

Canada;

● the

uncertainty of the outcome of current or future government

investigations and inquiries, including but not limited to, matters

before the U.S. Department of Justice and the Securities and

Exchange Commission;

● government

efforts to curtail the COVID-19 pandemic may delay the Company in

completion of its work relating to this permitting

process;

● our ability

to obtain funding for working capital and other corporate purposes

associated with advancement of the Pebble Project

● an

inability to continue to fund exploration and development

activities and other operating costs;

● our actual

operating expenses may be higher than projected;

● the highly

cyclical nature of the mineral resource exploration

business;

● the

pre-development stage economic viability and technical

uncertainties of the Pebble Project and the lack of known reserves

on the Pebble Project;

● an

inability to recover even the financial statement carrying values

of the Pebble Project if we cease to continue on a going concern

basis;

● the

potential for loss of the services of key executive

officers;

● a history

of, and expectation of further, financial losses from operations

impacting our ability to continue on a going concern

basis;

● the

volatility of gold, copper, molybdenum, silver and rhenium prices

and the share prices of mining companies;

● the

inherent risk involved in the exploration, development and

production of minerals, and the presence of unknown geological and

other physical and environmental hazards at the Pebble

Project;

|

2020

Annual Information Form

|

Page | 4

|

● the

potential for changes in, or the introduction of new, government

regulations relating to mining, including laws and regulations

relating to the protection of the environment and project legal

titles;

● potential

claims by third parties to titles or rights involving the Pebble

Project;

● the

uncertainty of the outcome of current or future litigation

including but not limited to, the appeal of the ROD denying the

issuance of permits required to operate a mine at the Pebble

Project;

● the

possible inability to insure our operations against all

risks;

● the highly

competitive nature of the mining business;

● the

potential equity dilution to current shareholders due to any future

equity financings or from the exercise of share purchase options

and warrants to purchase the Company’s shares;

● that we

have never paid dividends and will not do so in the foreseeable

future.

This

list is not exhaustive of the factors that may affect any of the

Company’s forward-looking statements or information.

Forward-looking statements or information are statements about the

future and are inherently uncertain, and actual achievements of the

Company or other future events or conditions may differ materially

from those reflected in the forward-looking statements or

information due to a variety of risks, uncertainties and other

factors, including, without limitation, the risks and uncertainties

described above. See "Risk

Factors" on page 35.

Our

forward-looking statements are based on the reasonable beliefs,

expectations and opinions of management on the date of this AIF.

Although we have attempted to identify important factors that could

cause actual results to differ materially from those contained in

forward-looking information, there may be other factors that cause

results not to be as anticipated, estimated or intended. There is

no assurance that such information will prove to be accurate, as

actual results and future events could differ materially from those

anticipated in such information. Accordingly, readers should

appreciate the inherent uncertainty of, and not place undue

reliance on, forward-looking information. We do not undertake to

update any forward-looking information, except as, and to the

extent required by, applicable securities laws.

Incorporation of Continuous Disclosure Documents by

Reference

In this

AIF, the "Company" or "Northern Dynasty" refers to Northern Dynasty

Minerals Ltd. and all its subsidiaries and affiliated partnerships

together unless the context states otherwise.

Currency and Metric Equivalents

All

dollar amounts are expressed in Canadian dollars unless otherwise

indicated. The Company’s accounts are maintained in Canadian

dollars. The daily rate of exchange on December 31, 2020,

as reported by the Bank of Canada for the conversion of one

Canadian dollar into one United States dollar ("U.S. dollar"),

was $1.2732.

On

March 30, 2021,

the rate of exchange of the Canadian Dollar, based on the daily

rate in Canada as published by the Bank of Canada, was US$1.00 =

$1.2631. Exchange

rates published by the Bank of Canada, available on its website

www.bankofcanada.ca,

are nominal quotations - not buying or selling rates - and intended

for statistical or analytical purposes.

|

2020

Annual Information Form

|

Page | 5

|

The

following tables set out the exchange rates, based on the daily

rates in Canada as published by the Bank of Canada for the

conversion of Canadian Dollars into U.S. dollars.

|

|

Year

Ended December 31

(Canadian

Dollars per U.S. Dollar)

|

|

|

2020

|

2019

|

2018

|

2017

|

|

Rate at

end of year

|

$1.2732

|

$1.2988

|

$1.3642

|

$1.2545

|

|

Average

rate for year

|

$1.3415

|

$1.3269

|

$1.2957

|

$1.2986

|

|

High

for year

|

$1.4496

|

$1.3600

|

$1.3642

|

$1.3743

|

|

Low for

year

|

$1.2718

|

$1.2988

|

$1.2288

|

$1.2128

|

|

Monthly

High and Low Daily Exchange Rate (Canadian Dollar per U.S.

Dollar)

|

|

Month or Period

|

High

|

Low

|

|

March

2021 (to March 30, 2021)

|

$1.2668

|

$1.2455

|

|

February

2021

|

$1.2828

|

$1.2530

|

|

January

2021

|

$1.2824

|

$1.2627

|

|

December

2020

|

$1.2952

|

$1.2718

|

|

November

2020

|

$1.3318

|

$1.2965

|

For

ease of reference, the following factors for converting metric

measurements into Imperial equivalents are as follows:

|

Metric Units

|

Multiply by

|

Imperial Units

|

|

hectares

|

2.471

|

=

acres

|

|

metres

|

3.281

|

=

feet

|

|

kilometres

|

0.621

|

= miles

(5,280 feet)

|

|

grams

|

0.032

|

=

ounces (troy)

|

|

tonnes

|

1.102

|

= tons

(short) (2,000 pounds)

|

|

grams/tonne

|

0.029

|

=

ounces (troy)/ton

|

|

2020

Annual Information Form

|

Page | 6

|

Glossary

In this

AIF the following terms have the meanings set forth

herein:

Regulatory Terms:

|

Term

|

Meaning

|

|

CWA

|

United

States Clean Water Act

|

|

CWA 404

Permit Application

|

The

permit application filed by the Pebble Partnership with the USACE

pursuant to Section 404 of the CWA

|

|

EPA

|

United

States Environmental Protection Agency

|

|

LEDPA

|

The

"least environmentally damaging practicable

alternative" under the CWA

|

|

NEPA

|

National

Environmental Policy Act

|

|

Pebble

EIS

|

The

final environmental impact statement for the Pebble Project

published by the USACE on July 24, 2020

|

|

Record

of Decision

|

The

record of decision of the USACE in respect of the Pebble Project

issued by the USACE on November 25, 2020

|

|

USACE

|

United

States Army Corps of Engineers

|

Technical Terms:

|

Term

|

Meaning

|

|

Alkalic

|

Igneous

rock containing a relatively high percentage of sodium and

potassium feldspar; alteration can also introduce alkali

minerals.

|

|

Argillic

|

Hydrothermal

alteration of wall rock that forms clay minerals including

kaolinite, smectite, illite and other species.

|

|

CuEQ

|

Copper

Equivalent

|

|

Comminution

|

Reduction

of solid materials from one average particle size to a smaller

average particle size by crushing, grinding, cutting, vibrating, or

other means.

|

|

Deportment

|

Assessment

of how minerals contribute to grade, as each mineral is likely to

behave differently to comminution, flotation or

leaching.

|

|

Diorite

|

Grey to

dark-grey igneous intrusive rock of intermediate composition,

composed principally of plagioclase feldspar along with biotite,

hornblende and/or pyroxene.

|

|

Element

Abbreviations

|

Au -

Gold; Ag - Silver; Al - Aluminum; Cu - Copper; Fe - Iron; Mo -

Molybdenum; Na - Sodium; O - Oxygen; Pb - Lead; Re - Rhenium; S -

Sulphur; Zn - Zinc.

|

|

Geometallurgy

|

Practice

of combining geology and/or geostatistics with

metallurgy.

|

|

Graben

|

Down-dropped

block of land bordered by faults.

|

|

Granodiorite

|

Medium-

to coarse-grained acid igneous rock with quartz (>20%),

plagioclase and alkali feldspar, commonly with minor hornblende

and/or biotite.

|

|

Hypogene

|

Processes

below the earth's surface which, in mineral deposits, result in

precipitation of primary minerals like sulphides.

|

|

Hydrothermal

mineral deposit

|

Any

concentration of metallic minerals formed by the precipitation of

solids from hot waters (hydrothermal solution). The solutions may

be sourced from a magma or from deeply circulating water heated by

magma.

|

|

Illite

Pyrite

|

Alteration

zone with significant amounts of illite – a clay mineral and

pyrite – an iron sulphide mineral.

|

|

Intrusion

(batholith, dyke, pluton)

|

Medium

to coarse grained igneous bodies that crystallized at depth within

the Earth's crust. Large intrusive bodies are called batholiths;

smaller bodies are plutons and linear bodies are

dykes.

|

|

Leached

Cap

|

Rock

that originally contained mineralization that was subsequently

removed due to weathering processes.

|

|

Locked

Cycle Test

|

A

repetitive batch flotation test used in mineral processing

laboratories while developing a metallurgical

flowsheet.

|

|

Monzonite

|

Igneous

intrusive rock with approximately equal amounts of plagioclase and

alkali feldspar, and less than 5% quartz by volume.

|

|

National

Instrument 43-101 ("NI 43-101")

|

The

Canadian securities instrument which establishes disclosure

standards for mineral projects held by Canadian publicly-traded

resource companies.

|

|

K

Silicate

|

Alteration

zone with significant potassium (K) bearing silicate

minerals.

|

|

Kriging

|

A

method of estimation of a variable value (such as metal grade) at

an unmeasured location from measured values, weighted by distance

and orientation, at nearby locations.

|

|

Porphyry

deposit

|

A type

of mineral deposit genetically related to igneous intrusions in

which ore minerals are widely distributed, generally of low grade

but commonly of large tonnage.

|

|

Potassic

|

Hydrothermal

alteration that results in the production of potassium-bearing

minerals such as biotite, muscovite or sericite, and/or

orthoclase.

|

|

Preliminary

Economic Assessment

|

A study

that includes an economic analysis of the potential viability of

mineral resources but that does not meet the definition of either a

“pre-feasibility study” or a “feasibility

study”, as such terms are defined under Canadian Institute of

Mining and Metallurgy ("CIM") Definitions below. It is a

term defined under NI 43-101.

|

|

Pyrophyllite

|

Aluminosilicate

hydroxide mineral that forms as a result of hydrothermal alteration

or low grade metamorphism.

|

|

QSP

|

Quartz

Sericite Pyrite; an alteration zone.

|

|

Sericite

|

Alteration

zone with significant sericite, a fine-grained version of the mica

mineral muscovite.

|

|

Sodic

Potassic

|

Alteration

zone with significant sodium (Na) and potassium (K) bearing

minerals

|

|

2020

Annual Information Form

|

Page | 7

|

|

Term

|

Meaning

|

|

Sodic

|

In this

report, refers to a type of hydrothermal alteration that contains

sodium-bearing minerals, most commonly albite

feldspar.

|

|

Subduction

|

Process

by which one tectonic plate moves under another tectonic

plate.

|

|

Supergene

|

Refers

to processes that occur relatively near the surface of the earth

which modify or destroy original (hypogene) minerals by oxidation

and chemical weathering.

|

|

Superterrane

|

A group

of physically connected and related geological terranes (group of

related rock units).

|

Canadian Mineral Property Disclosure Standards and Resource

Estimates

The

discussion of mineral deposit classifications in this AIF uses the

certain technical terms presented below as they are defined in

accordance with the CIM Definition Standards on mineral resources

and reserves (the "CIM Definition

Standards") adopted by the Canadian Institute of Mining,

Metallurgy and Petroleum (the "CIM

Council"), as required by NI 43-101. The following

definitions are reproduced from the latest version of the CIM

Standards, which were adopted by the CIM Council on May 10, 2014

(the "CIM Definitions").

Estimated mineral resources fall into two broad categories

dependent on whether the economic viability of them has been

established and these are namely "resources" (potential for

economic viability) and "reserves" (viable economic production is

feasible). Resources are sub-divided into categories depending on

the confidence level of the estimate based on level of detail of

sampling and geological understanding of the deposit. The

categories, from lowest confidence to highest confidence, are

inferred resource, indicated resource and measured resource. The

Company does not claim to have any reserves at this time. The CIM

definitions are as follows:

|

Term

|

Definition

|

|

Mineral

Resource

|

A

concentration or occurrence of solid material of economic interest

in or on the Earth’s crust in such form, grade or quality and

quantity that there are reasonable prospects for eventual economic

extraction. The location, quantity, grade or quality, continuity

and other geological characteristics of a mineral resource are

known, estimated or interpreted from specific geological evidence

and knowledge, including sampling.

|

|

Measured

Mineral Resource

|

That

part of a mineral resource for which quantity, grade or quality,

densities, shape, and physical characteristics are estimated with

confidence sufficient to allow the application of modifying factors

to support detailed mine planning and final evaluation of the

economic viability of the deposit. Geological evidence is derived

from detailed and reliable exploration, sampling and testing and is

sufficient to confirm geological and grade or quality continuity

between points of observation. A measured mineral resource has a

higher level of confidence than that applying to either an

Indicated mineral resource or an inferred mineral resource. It may

be converted to a proven mineral reserve or to a probable mineral

reserve.

|

|

Indicated

Mineral Resource

|

That

part of a mineral resource for which quantity, grade or quality,

densities, shape and physical characteristics are estimated with

sufficient confidence to allow the application of modifying factors

in sufficient detail to support mine planning and evaluation of the

economic viability of the deposit. Geological evidence is derived

from adequately detailed and reliable exploration, sampling and

testing and is sufficient to assume geological and grade or quality

continuity between points of observation. An indicated mineral

resource has a lower level of confidence than that applying to a

measured mineral resource and may only be converted to a probable

mineral reserve.

|

|

2020

Annual Information Form

|

Page | 8

|

|

Term

|

Definition

|

|

Inferred

Mineral Resource

|

That

part of a mineral resource for which quantity and grade or quality

are estimated on the basis of limited geological evidence and

sampling. Geological evidence is sufficient to imply but not verify

geological and grade or quality continuity. An inferred mineral

resource has a lower level of confidence than that applying to an

indicated mineral resource and may not be converted to a mineral

reserve. It is reasonably expected that the majority of inferred

mineral resources could be upgraded to indicated mineral resources

with continued exploration.

|

|

Mineral

Reserve

|

The

economically mineable part of a measured and/or indicated mineral

resource. It includes diluting materials and allowances for losses,

which may occur when the material is mined or extracted and is

defined by studies at pre-feasibility or feasibility level as

appropriate that include application of modifying factors. Such

studies demonstrate that, at the time of reporting, extraction

could reasonably be justified. The reference point at which mineral

reserves are defined, usually the point where the ore is delivered

to the processing plant, must be stated. It is important that, in

all situations where the reference point is different, such as for

a saleable product, a clarifying statement is included to ensure

that the reader is fully informed as to what is being reported. The

public disclosure of a mineral reserve must be demonstrated by a

pre-feasibility study or feasibility study.

|

|

Proven

Mineral Reserve

|

The

economically mineable part of a measured mineral resource. A proven

mineral reserve implies a high degree of confidence in the

modifying factors.

|

|

Probable

Mineral Reserve

|

The

economically mineable part of an indicated, and in some

circumstances, a measured mineral resource. The confidence in the

modifying factors applying to a probable mineral reserve is lower

than that applying to a proven mineral reserve.

|

|

Modifying

Factors

|

Considerations used

to convert mineral resources to mineral reserves. These include,

but are not restricted to, mining, processing, metallurgical,

infrastructure, economic, marketing, legal, environmental, social

and governmental factors.

|

|

Feasibility

Study

|

A

comprehensive technical and economic study of the selected

development option for a mineral project that includes

appropriately detailed assessments of applicable modifying factors

together with any other relevant operational factors and detailed

financial analysis that are necessary to demonstrate, at the time

of reporting, that extraction is reasonably justified (economically

mineable). The results of the study may reasonably serve as the

basis for a final decision by a proponent or financial institution

to proceed with, or finance, the development of the project. The

confidence level of the study will be higher than that of a

pre-feasibility study.

|

|

Pre-feasibility

Study

|

A

comprehensive study of a range of options for the technical and

economic viability of a mineral project that has advanced to a

stage where a preferred mining method, in the case of underground

mining, or the pit configuration, in the case of an open pit, is

established and an effective method of mineral processing is

determined. It includes a financial analysis based on reasonable

assumptions on the modifying factors and the evaluation of any

other relevant factors which are sufficient for a qualified person,

acting reasonably, to determine if all or part of the mineral

resource may be converted to a mineral reserve at the time of

reporting. A pre-feasibility study is at a lower confidence level

than a feasibility study.

|

|

2020

Annual Information Form

|

Page | 9

|

Cautionary Notes to United States Investors Concerning Canadian

Mineral Property Disclosure Standards

As a

Canadian issuer, Northern Dynasty is required to comply with

reporting standards in Canada that require that we make disclosure

regarding our mineral properties, including any estimates of

mineral reserves and resources, in accordance with NI 43-101.

NI 43-101 is a rule developed by the Canadian Securities

Administrators that establishes standards for all public disclosure

an issuer makes of scientific and technical information concerning

mineral projects. In accordance with

NI 43-101, the Company uses the terms mineral reserves and

resources as they are defined in accordance with the CIM Definition

Standards on mineral reserves and resources adopted by the Canadian

Institute of Mining, Metallurgy and Petroleum.

The

United States Securities and Exchange Commission (the "SEC") has adopted amendments to its

disclosure rules to modernize the mineral property disclosure

requirements for issuers whose securities are registered with the

SEC under the US Exchange Act (the "SEC Modernization Rules") with compliance required

for the first fiscal year on or after January 1, 2021. The SEC

Modernization Rules have replaced the historical property

disclosure requirements for mining registrants that were included

in SEC Industry Guide 7 ("Guide 7").

The SEC

Modernization Rules include the adoption of definitions of the

following terms, which are substantially similar to the

corresponding terms under the CIM Definition Standards that are

presented above under "Canadian

Mineral Property Disclosure Standards and Resource

Estimates":

●

mineral resource;

●

indicated mineral resource;

●

inferred mineral resource;

●

mineral reserve;

●

proven mineral reserve;

●

probable mineral reserve;

●

modifying factors;

●

feasibility study; and

●

preliminary feasibility study (or "pre-feasibility study").

As a

result of the adoption of the SEC Modernization Rules, the SEC will

now recognize estimates of "measured mineral resources", "indicated

mineral resources" and "inferred mineral resources". In addition,

the SEC has amended its definitions of "proven mineral reserves"

and "probable mineral reserves" to be substantially similar to the

corresponding CIM Definitions.

Northern

Dynasty is not required to provide disclosure on our mineral

properties, including the Pebble Project, under the SEC

Modernization Rules as we are presently a "foreign issuer" under the US Exchange Act

and entitled to file continuous disclosure reports with the SEC

under the Multi-Jurisdictional Disclosure System ("MJDS") between Canada and the

United States. Accordingly, we anticipate that we will be entitled

to continue to provide disclosure on our mineral properties,

including the Pebble Project, in accordance with NI 43-101

disclosure standards and CIM Definition Standards. However, if we

either cease to be a "foreign issuer" or cease to be entitled to

file reports under the MJDS, then we will be required to provide

disclosure on our mineral properties under the SEC Modernization

Rules. Accordingly, United States investors are cautioned that the

disclosure that we provide on our mineral properties, including the

Pebble Project, in the AIF and under our continuous disclosure

obligations under the US Exchange Act may be different from the

disclosure that we would otherwise be required to provide as a US

domestic issuer or a non-MJDS foreign issuer under the SEC

Modernization Rules.

|

2020

Annual Information Form

|

Page | 10

|

United

States investors are cautioned that while the above terms are

substantially similar to CIM Definitions, there are differences in

the definitions under the SEC Modernization Rules and the CIM

Definition Standards. Accordingly, there is no assurance any

mineral resources that we may report as "measured mineral

resources", "indicated mineral resources" and "inferred mineral

resources" under NI 43-101 would be the same had we prepared

the resource estimates under the standards adopted under the SEC

Modernization Rules.

Investors

are cautioned not to assume that any "measured mineral resources",

"indicated mineral resources", or "inferred mineral resources" that

we report in this AIF are or will be economically or legally

mineable.

Further,

"inferred resources" have a great amount of uncertainty as to

whether they can be mined legally or economically. In accordance

with Canadian securities laws, estimates of "inferred mineral

resources" cannot form the basis of feasibility or other economic

studies, except in limited circumstances where permitted under

NI 43-101.

For the

above reasons, information contained in this AIF and the documents

incorporated by reference herein containing descriptions of our

mineral deposits may not be comparable to similar information made

public by United States companies subject to the reporting and

disclosure requirements under the United States federal securities

laws and the rules and regulations thereunder.

Item

3. Corporate Structure

Northern

Dynasty is a mineral exploration company incorporated on

May 11, 1983 pursuant to the Company Act of the Province

of British Columbia (predecessor statute to the British Columbia

Corporations Act in force since 2004), under the name "Dynasty

Resources Inc." On November 30, 1983, the Company changed its

name to "Northern Dynasty Explorations Ltd." and subsequently, on

October 11, 1997, changed its name to Northern Dynasty Minerals

Ltd. Northern Dynasty became a reporting company in the Province of

British Columbia on April 10, 1984 and was listed on the

Vancouver Stock Exchange (now absorbed by the TSX Venture Exchange

and herein generally "TSX-V") from 1984-1987, listed on the

Toronto Stock Exchange ("TSX") from 1987-1993, and delisted from

trading but continued to comply with its continuous disclosure

obligations from 1993 to 1994, and thereafter listed on TSX-V from

1994 to October 30, 2007, when it again began trading on the TSX.

In November 2004, the common shares of Northern Dynasty were also

listed on the American Stock Exchange ("AMEX"). AMEX was purchased by the New

York Stock Exchange ("NYSE")

and the Company now trades on the NYSE American Exchange

("NYSE

American").

The

head office of Northern Dynasty is located at 1040 West Georgia

Street, 15th floor, Vancouver, British Columbia, Canada

V6E 4H1, telephone (604) 684-6365, facsimile (604) 684-8092.

The Company’s legal registered office is in care of its

Canadian attorneys, McMillan LLP, Barristers & Solicitors, at

Suite 1500, 1055 West Georgia Street, Vancouver, British Columbia,

Canada V6E 4N7, telephone (604) 689-9111, facsimile

(604) 685-7084.

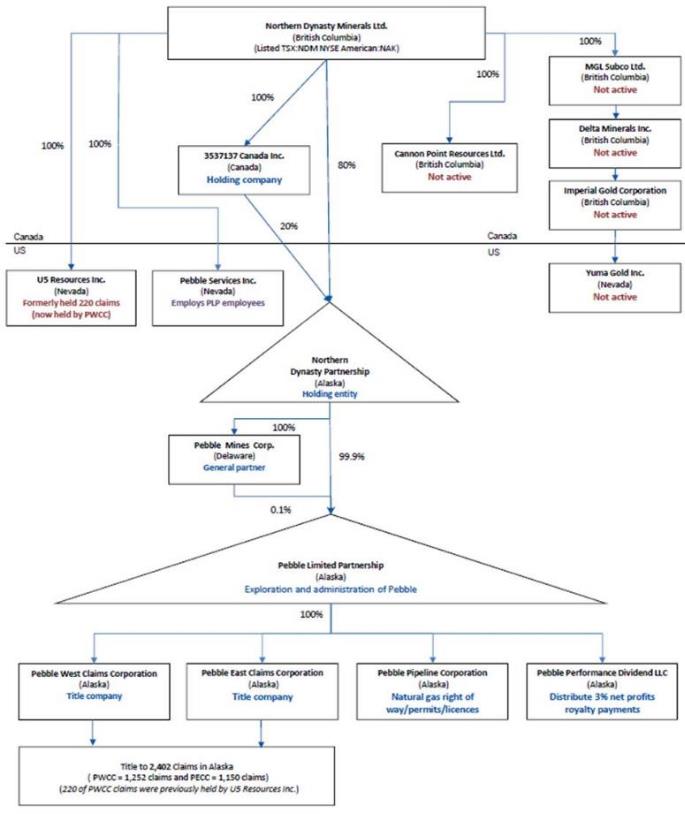

The

Company’s Alaska mineral resource exploration business is

operated through a wholly-owned Alaskan registered limited

partnership, the Pebble Limited Partnership (the "Pebble Partnership" or "PLP"), in which the Company owns a 100%

interest through an Alaskan general partnership, the Northern

Dynasty Partnership, which is a partnership formed by two of its

subsidiaries. An indirectly wholly-owned subsidiary of the Company,

Pebble Mines Corp. is the general partner of the Pebble Partnership

and responsible for its day-to-day operations. The business address

of the Northern Dynasty Partnership is Suite 505, 3201 C Street,

Anchorage, Alaska, USA, 99503.

In this

AIF, a reference to the "Company" or "Northern Dynasty" includes a

reference to PLP and the Company’s wholly-owned subsidiaries

and other consolidated interests and entities, unless the context

clearly indicates otherwise. Certain terms used herein are defined

in the text and others are included in the glossary of this

AIF.

Item

4. General Development of the Business

Company Development

Northern

Dynasty is a mineral exploration company focused on the exploration and advancement

towards feasibility, permitting and ultimately development

of the Pebble Project, a copper-gold-molybdenum-silver-rhenium

mineral project located in southwest Alaska (the "Pebble Project" or the "Project"). The Pebble Project is

comprised of mineral claims that are held by subsidiaries of the

Pebble Partnership, which is a 100% wholly-owned subsidiary of

Northern Dynasty.

|

2020

Annual Information Form

|

Page | 11

|

Northern

Dynasty acquired a 100% interest the Pebble Project from an Alaskan

subsidiary of Teck Resources Limited ("Teck") in a series of transactions from

October 2001 through to June 2006. Teck has retained certain

royalties in the Pebble Project, as described in detail below under

Item 5

– Description

of Business.

The

Pebble Partnership was converted into a limited partnership in July

2007 in connection with a joint venture for the Pebble Project

entered into between the Company and an affiliate of Anglo American

plc ("Anglo American"). From

July 2007 to December 2013, approximately US$573 million was

provided to the Pebble Partnership by the affiliate of Anglo

American, largely spent on exploration programs, resource

estimates, environmental data collection and technical studies,

with a significant portion spent on engineering of various possible

mine development models and related infrastructure, power and

transportation systems. The technical and engineering studies that

were completed relating to mine-site and infrastructure development

are not considered to be current or necessarily representative of

management’s current understanding of the most likely

development scenario for the Project. Accordingly, the Company is

uncertain whether it can realize significant value from this prior

work. Environmental baseline studies and data, as well as

geological information from exploration, remain important

information available to the Company from this period in continuing

its advancement of the Project. Anglo American withdrew from the

Pebble Partnership effective December 10, 2013.

In

December 2017, Northern Dynasty and First Quantum Minerals Ltd.

("First Quantum" or

collectively, the "parties")

entered into a framework agreement, which contemplated that the

parties would execute an option agreement whereby First Quantum

could earn a 50% interest in the Pebble Partnership. First Quantum

also made a non-refundable early option payment of US$37.5 million

to be applied solely for the purpose of progressing permitting of

the Pebble Project. On May 25, 2018, the Company announced that the

parties had been unable to reach agreement on the option and

partnership transaction contemplated in the December 2017 framework

agreement, and it was terminated in accordance with its

terms.

Northern

Dynasty holds a 100% interest in the Pebble Partnership and the

Pebble Project. Northern Dynasty continues its efforts to secure a

partner for the project.

To

December 31, 2020, approximately $979 million (US$883 million) in

expenditures have been incurred on the Pebble Project. In addition,

Northern Dynasty has spent approximately $106 million in

acquisition costs on the Pebble Project.

Northern

Dynasty does not have any operating revenue, although currently and

historically it has had non-material annual interest revenue as a

consequence of investing its surplus funds, and has received

consideration for the sale of a net proceeds interest royalty held

on a non-core property that was carried at nominal

value.

Three Year History

In

February 2014, the US Environmental Protection Agency

("EPA") announced a

pre-emptive regulatory action under Section 404(c) the CWA to

consider restriction or a prohibition of mining activities

associated with the Pebble deposit. From 2014-2017, Northern

Dynasty and the Pebble Partnership focused on a multi-dimensional

strategy, including legal and other initiatives to ward off this

action. These efforts were successful, resulting in the legal

agreement with the EPA announced on May 12, 2017, enabling Pebble

to enter normal course permitting under the NEPA. On December 22, 2017, the

Pebble Partnership filed its 404 wetlands permit application (the

“CWA 404 Permit

Application”) under the CWA with the USACE, which was

“receipted” as complete by USACE on January 5,

2018 and initiated the

federal Environmental Impact Statement ("EIS") permitting process for the Pebble

Project under NEPA. The permit application included a project

description (the "Project

Description") that was based on a smaller mine concept

developed for the Pebble Project in the latter part of 2017 (see

further details in B.

Technical Summary - Introduction). The Project Description in

the permit application envisages the project developed as an open

pit mine and processing facility with supporting

infrastructure.

The

Pebble Project has completed the US NEPA Environmental Impact

Statement ("Pebble EIS")

process with the final Pebble EIS being published by the USACE on

July 24, 2021. The Pebble EIS process required a comprehensive

"alternatives assessment" be undertaken to consider a broad range

of development alternatives, such that the final project design and

operating parameters for the Pebble Project and associated

infrastructure may vary significantly from that being advanced. As

a result, the Company will continue to consider various development

options and no final project design has been selected at this

time.

|

2020

Annual Information Form

|

Page | 12

|

On

March 26, 2020, in accordance with the order of the Governor of

Alaska, the Pebble Partnership, along with all other nonessential

offices in Alaska, closed its offices for the health and safety of

its personnel. Notwithstanding the closure, the Company has

maintained its staff and employees to help ensure that the project

schedule announced by the USACE for the final EIS remained on

track. Technical review meetings were completed before the

implementation of the Governor’s order in response to

COVID-19.

On

April 17, 2020, a US federal district court judge in Alaska ruled

in favour of the EPA by granting a motion to dismiss a case brought

by a collection of litigants opposed to the Pebble Mine that

challenged the EPA’s July 2019 decision to formally withdraw

its prior regulatory action under Section 404(c) of the CWA. The

ruling was based on a determination that the litigants had failed

to state a claim upon which relief can be granted. This dismissal

has been appealed to the Ninth Circuit Court of

Appeals.

On May

22, 2020, the USACE announced a development alternative for the

Pebble Project as the ‘least environmentally damaging

practicable alternative’ or LEDPA for the transportation

corridor for the proposed Pebble mine. The LEDPA transportation

corridor includes an all land-based transportation route to connect

the proposed mine site to a port site on Cook Inlet via an

approximate 85-mile road north of Lake Iliamna, thereby avoiding

the need for ferry transport across the lake. The transportation

corridor, which is referred to as the ‘northern

transportation corridor’ and otherwise known and evaluated in

the Pebble EIS as ‘Alternative 3’, has been extensively

studied by the Pebble Partnership, and the Company believes that

this transportation corridor presents several compelling benefits

over the alternative lake ferry transportation corridor options.

The EPA, in a letter to the USACE dated May 28, 2020, confirmed its

view that the northern corridor transportation route was the least

environmentally damaging practicable alternative under the

EPA’s guidelines.

The

USACE published the final EIS for the Pebble Project on July 24,

2020. Led by the USACE, the Pebble EIS also involved eight federal

cooperating agencies (including the US EPA and US Fish &

Wildlife Service), three state cooperating agencies (including the

Alaska Department of Natural Resources and the Alaska Department of

Environmental Conservation), the Lake & Peninsula Borough and

federally recognized tribes.

The

final Pebble EIS was viewed by the Company as positive in that it

found impacts to fish and wildlife would not be expected to affect

harvest levels, there would be no measurable change to the

commercial fishing industry including prices and there would be a

number of positive socioeconomic impacts on local

communities.

|

2020

Annual Information Form

|

Page | 13

|

The CWA

404 Permit Application was submitted in December 2017, and the

permitting process over the next three years involved the Pebble

Partnership being actively engaged with the USACE on the evaluation

of the Pebble Project. There were numerous meetings between

representatives of the USACE and the Pebble Partnership regarding,

among other things, compensatory mitigation for the Pebble Project.

The Pebble Partnership submitted several draft compensatory

mitigation plans to the USACE, each refined to address comments

from the USACE and that the Pebble Partnership believed were

consistent with mitigation proposed and approved for other major

development projects in Alaska. In late June 2020, USACE verbally

identified the “significant degradation” of certain

aquatic resources, with the requirement of new compensatory

mitigation. The Pebble Partnership understood from these

discussions that the new compensatory mitigation plan for the

Pebble Project would include in-kind, in-watershed mitigation and

continued its work to meet these new USACE

requirements.

The

USACE formally advised the Pebble Partnership by letter dated

August 20, 2020 that it had made preliminary factual determinations

under Section 404(b)(1) of the CWA that the Pebble Project as

proposed would result in significant degradation to aquatic

resources. In connection with this preliminary finding of

significant degradation, the USACE formally informed the Pebble

Partnership that in-kind compensatory mitigation within the Koktuli

River watershed would be required to compensate for all direct and

indirect impacts caused by discharges into aquatic resources at the

mine site. The USACE requested the submission of a new compensatory

mitigation plan to address this finding within 90 days of its

letter.

Based on these requirements, the Pebble Partnership continued with

its efforts to develop the new compensatory mitigation plan

(the "CMP") to align with the requirements outlined by the

USACE as conveyed to the Pebble Partnership. This plan envisioned

creation of an 112,445-acre Koktuli Conservation Area on land

belonging to the State of Alaska in the Koktuli River watershed

downstream of the Project. During the period in which this CMP was

developed, the Pebble Partnership continued to confer with the

USACE regarding its proposed approach to

mitigation.

An initial draft of the CMP was

submitted to the USACE for an interim review by the USACE in

September 2020. The Pebble Partnership then revised the CMP based

on the input from the USACE. The objective of the preservation of

the Koktuli Conservation Area was to allow the long-term protection

of a large and contiguous ecosystem that contains valuable aquatic

and upland habitats. If adopted, the Koktuli Conservation Area

would preserve 31,026 acres of aquatic resources (wetlands) within

the aquatic resource of national importance-designated Koktuli

River watershed. The protected resources were designed to address

the physical, chemical, and biological functions highlighted by the

EPA and US Fish & Wildlife Service. Preservation of the Koktuli

Conservation Area was proposed with the objective of minimizing the

threat to, and preventing the decline of, aquatic resources in the

Koktuli River watershed from potential future actions, and

sustaining the fish and wildlife species that depend on these

aquatic resources, while protecting the subsistence lifestyle of

the residents of Bristol Bay and commercial and recreational sport

fisheries. The revised plan was submitted to the USACE on November

4, 2020.

On

November 25, 2020, the USACE issued the ROD. The ROD rejected the

compensatory mitigation plan as “noncompliant” and

determined the project would cause “significant

degradation” and was contrary to the public interest. Based

on this finding, the USACE rejected Pebble Partnership’s

permit application under the Clean Water Act.

The

Pebble Partnership submitted its request for appeal of the ROD (the

"RFA") to the USACE Pacific

Division on January 19, 2021. The RFA reflects the Pebble

Partnership’s position that the USACE's Record of Decision

and permitting decision – including its “significant

degradation” finding, its ‘public interest review'

findings, and its perfunctory rejection of the Pebble Partnership's

CMP – are contrary to law, unprecedented in Alaska, and

fundamentally unsupported by the administrative record, including

the Pebble EIS. The specific reasons for appeal asserted by the

Pebble Partnership in the RFA include (i) the finding of

“significant degradation” by the USACE is contrary to

law and unsupported by the record, (ii) the USACE’s rejection

of the compensatory mitigation plan is contrary to the USACE

regulations and guidance, including the failure to provide the

Pebble Partnership with an opportunity to correct the alleged

deficiencies, and (iii) the determination by the USACE that the

Pebble Project is not in the public interest is contrary to law and

unsupported by the public record.

In a

letter dated February 24, the USACE confirmed the Pebble

Partnership’s RFA is “complete and meets the criteria

for appeal.” The USACE has appointed a Review Officer to

oversee the administrative appeal process. The appeal process will

now move to consideration by the USACE of the merits of the appeal.

The appeal will be reviewed by the USACE based on the

administrative record and any clarifying information provided, and

the Pebble Partnership will be provided with a written decision on

the merits of the appeal at the conclusion of the process. The

appeal is governed by the policies and procedures of the USACE

administrative appeal regulations. While federal guidelines suggest

the appeal should conclude within 90 days, the USACE has indicated

the complexity of issues and volume of materials associated with

Pebble’s case means the review will likely take additional

time. There is no assurance that the Company’s appeal of the

ROD will be successful or that the required permits for the Pebble

Project will ultimately be issued. The permits are required in

order that the Pebble Project can be developed as proposed by the

Company. If the Pebble Partnership’s administrative appeal of

the ROD is successful, then we anticipate that the permitting

decision would be remanded back to the USACE’s Alaska

District in order that the permitting process would then continue

based on the administrative record and the findings and

determinations made by the USACE Pacific Division in its appeal

decision. There is no assurance that a successful appeal will

ultimately result in the issuance of a positive ROD by the USACE

Alaska District. If the Pebble Partnership’s administrative

appeal is not successful, the Company may seek judicial review of

the ROD in the appropriate US District Court. There is no assurance

that any judicial review would be successful in overturning an

unsuccessful appellate decision.

On

January 22, 2021, the State of Alaska, acting in its role as owner

of the Pebble lands and subsurface mineral estate, announced that

it had also filed a request for appeal. That appeal was rejected on

the basis that the State did not have standing to pursue an

administrative appeal with the USACE.

|

2020

Annual Information Form

|

Page | 14

|

Much of

the work by the Company through the Pebble Partnership in 2020, and

since 2017 has focused on facilitating and providing support to the

federal EIS permitting process. The Company also continued to

actively engage and consult with project stakeholders to share

information and gather feedback on the Pebble Project, its

potential effects and proposed mitigation. In 2018, 2019 and 2020,

right-of-way agreements were secured with Alaska Native village

corporations and other landowners whose lands cover portions of

several proposed transportation and infrastructure routes for the

Pebble Project. Opportunities for additional community benefits

from development of the project have also been explored, including

the Pebble Performance Dividend revenue sharing program for

full-time adult residents of Bristol Bay communities, and a

Memorandum of Understanding with Alaska Peninsula Corporation

announced in July 2020.

Corporate

activities have been directed toward raising capital to support the

EIS process and

discussions directed toward securing a partner with which to

advance the overall development of the project. Northern Dynasty

has completed the following financings and/or raised funds within

the past three years in order to fund its business

operations:

● In December

2017, the Company received a non-refundable early option payment of

US$37.5 million as a result of a framework agreement with First

Quantum, which was terminated in May 2018.

● In December

2018, the Company completed a private placement of 10,150,322

special warrants (the "Special

Warrants") at a price of $0.83 (US$0.62) per Special Warrant

for aggregate gross proceeds of approximately $8.4 million (US$6.3

million). The Special Warrants

converted into common shares on a one-for-one basis without payment

of any additional consideration on February 19,

2019.

● In 2019 and

2020, the Company completed four two-part financings.

● in March

2019, the Company completed:

o a bought deal

offering of 17,968,750 common shares at US$0.64 per common share

for gross proceeds of US$11.5 million ($15.3 million),

which included the exercise of an over-allotment option of

2,343,750 common shares for additional gross proceeds of

US$1.5 million. The offering was completed pursuant to an

underwriting agreement, among the Company and Cantor Fitzgerald

Canada Corporation, as lead underwriter and sole bookrunner, and a

syndicate of underwriters including BMO Nesbitt Burns Inc., H.C.

Wainwright & Co., LLC. and TD Securities Inc. (collectively,

the "Underwriters");

and

o a private

placement of 3,769,476 common shares at $0.86 (US$0.64) per common

share for gross proceeds of approximately $3.2 million

(US$2.4 million).

● in June

2019, the Company completed:

o a bought deal

offering of 12,200,000 common shares at US$0.41 per common share

for gross proceeds of approximately US$5.0 million

($6.6 million). The offering was made through the Underwriters

described above. The Underwriters received 244,000 non-transferable

common share warrants, each warrant exercisable into one common

share of the Company at an exercise price of US$0.41 per common

share until June 24, 2020, which were all exercised;

and

o a private

placement of 3,660,000 common shares of the Company at US$0.41 per

common share for gross proceeds of approximately

US$1.5 million ($2.0 million).

● in August

2019, the Company completed:

o a bought deal

offering of 15,333,334 common shares of the Company at the price of

US$0.75 per Offered Share for aggregate gross proceeds of

approximately US$11.5 million ($15.3 million);

and

o a non-brokered

private placement to investors outside of the United States of

2,866,665 common shares of the Company at the Issue Price for gross

proceeds to the Company of US$2.15 million

($2.8 million).

|

2020

Annual Information Form

|

Page | 15

|

● in December

2019 and January 2020, the Company completed:

o an underwritten

public offering of 41,975,000 common shares at a price of US$0.37

per common share for gross proceeds of approximately US$15.5

million ($20.6 million, completed in December 2019);

and

o a non-brokered

private placement of 13,688,823 common shares of the Company at a

price of US$0.37 per common share for gross proceeds of

approximately US$5.1 million ($6.7 million, completed in

January 2020).

● in May

2020, the Company completed:

o an underwritten

public offering of 14,375,000 common shares at a price of $0.70 per

common share for gross proceeds of approximately

$10.1 million; and

o a non-brokered

private placement of 10,357,143 common shares of the Company at a

price of $0.70 per common share for gross proceeds of approximately

$7.3 million.

● in July and

August 2020, the Company completed:

o an underwritten

public offering of 24,150,000 common shares at a price of US$1.46

per common share for gross proceeds of approximately

US$35.3 million ($47.6 million, completed in August

2020); and

o a non-brokered

private placement of 5,807,534 common shares of the Company at a

price of US$1.46 per common share for gross proceeds of

approximately US$8.6 million ($11.7 million, completed in

two tranches in July and August 2020).

Item 5. Description of

Business

A.

The Pebble Project

The

Company’s business is the exploration and advancement towards

feasibility, permitting and ultimately development of the Pebble

Project.

The Pebble Project Is Subject To State and Federal

Laws

The

Pebble Partnership and its subsidiaries are required to comply with

all Alaska statutes in connection with the Pebble Project. These

statutes govern titles, operations, environmental, development,

operating and generally all aspects of exploration, development and

operation of a mine in Alaska.

Alaska

Statute 38.05.185, among others, establishes the rights to mining

claims and mineral leases on lands owned by the State of Alaska and

open to mineral entry. This group of statutes also cover annual

labor and rental requirements, and royalties.

Operations

on claims or leases on state owned land must be permitted under a

plan of operations as set out in Title 11 of the Alaska

Administrative Code, Chapter 86, Section 800. This

regulation generally provides that the State Division of Mining can

be the lead agency in coordinating the comments of all agencies,

which must consent to the issuance of a plan of operations, and

sets the requirements for the approval of a plan of

operations.

Environmental

conditions are controlled by Alaska Statute 46.08 (which prohibits

release of oil and hazardous substances), Alaska Statute 46.03.060

(which sets water quality standards), and Alaska Statute 46.14

(which sets air quality standards).

Once a

decision is made to enter permitting, the Pebble Project will be

required to satisfy permitting requirements at three levels:

federal, state and local (borough). The process takes approximately

3-4 years to complete and involves 11 regulatory agencies, 60+

categories of permits and significant ongoing opportunities for

public involvement. The Alaska Department of Natural Resources

Large Mine Permitting Team is responsible for coordinating

permitting activities for large mine projects.

|

2020

Annual Information Form

|

Page | 16

|

To

satisfy permitting requirements under NEPA and other regulatory

statutes, a project must provide a comprehensive project design and

operating plan for mine-site and infrastructure facilities;

documentation of development alternatives investigated; mitigation

and compensation strategies, and identification of residual

effects; and environmental monitoring, reclamation and closure

plans. The first step is to provide the required information

(including a Project Description and Environmental Baseline

Document) for an EIS under NEPA, prepared by a third-party

contractor under the direction of a lead federal agency. The EIS

determines whether sufficient evaluation of the project's

environmental effects and development alternatives has been

undertaken. It also provides the basis for federal, state and local

government agencies to make individual permitting

decisions.

Under

the CWA, Section 404(c), the Administrator of the EPA is given the

right to disallow the specification (including the withdrawal of

specification) of any defined area as a disposal site if he or she

determines that the release of material at the disposal site will

have an unacceptable adverse effect on municipal water supplies,

local wildlife, spawning and breeding areas of fisheries, shellfish

beds, and/or recreational areas. Such decisions made by the

Administrator require notice and opportunity for public hearings,

and consultation with the Secretary of the Army. The Administrator

shall set forth in writing and make public his or her findings and

reasons for making any determination under this

subsection.

B.

Technical Summary

The

following disclosure is mainly summarized from the "2021

Technical Report on the Pebble

Project, Southwest Alaska, USA" by J. David Gaunt, P.Geo.,

James Lang, P.Geo., Eric Titley, P.Geo., Hassan Ghaffari, P.Eng.,

and Stephen Hodgson, P.Eng., effective date February 24, 2021

("2021 Technical Report"),

and updated by Company staff. J. David Gaunt, P.Geo., James Lang,

P.Geo., Eric Titley, P.Geo., Hassan Ghaffari, P.Eng., and Stephen

Hodgson, P.Eng., are the qualified persons for the 2018 Technical

Report and have reviewed and approved the content derived from that

report. All qualified persons, other than Hassan Ghaffari, P.Eng.,

are not independent of Northern Dynasty.

The

Pebble deposit was originally discovered in 1989 and was acquired

by Northern Dynasty in 2001. Since that time, Northern Dynasty and

subsequently the Pebble Partnership have conducted significant

mineral exploration, environmental baseline data collection, and

engineering work on the Pebble Project to advance it towards

development.

Since

the acquisition by Northern Dynasty, work at Pebble has led to an

overall expansion of the Pebble deposit, as well as the discovery

of several other mineralized occurrences along an extensive

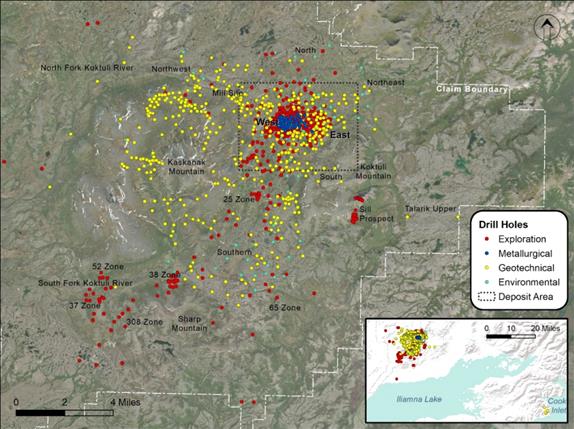

northeast-trending mineralized system underlying the property. Over

1 million feet of drilling has been completed on the property, a

large proportion of which has been focused on the Pebble

deposit.

Comprehensive

deposit delineation, environmental, socioeconomic and engineering

studies of the Pebble deposit began in 2004 and continued through

2013.

Northern

Dynasty completed a Preliminary Assessment (now known as a

Preliminary Economic

Assessment or PEA)

on the Pebble Project in February 2011 (“2011 PEA”). After considering

stakeholder feedback, Northern Dynasty initiated a broad review of

the Pebble Project that took place in 2016 and 2017 to consider ,

among other things, a smaller project footprint and improved

environmental and safety enhancements, and incorporated these and

other improvements into a new proposed development concept for the

Pebble Project.

The

Pebble Partnership submitted an application for a CWA 404 permit in

December 2017 for the Pebble Project on the basis of a

substantially smaller mine facility footprint and with other

material revisions than what was envisaged in the 2011 PEA. As a

result, the economic analysis included in the 2011 PEA is

considered by Northern Dynasty to be out of date such that it can

no longer be relied upon. In light of the foregoing, the Pebble

Project is no longer an advanced property for the purposes of NI

43-101, as the potential economic viability of the Pebble Project

is not currently supported by a preliminary economic assessment,

pre-feasibility study or feasibility study.

|

2020

Annual Information Form

|

Page | 17

|

The

permit application under Section 404 of the CWA and Section 10 of

the Rivers and Harbors Act (RHA) was submitted to the USACE by the

Pebble Partnership on December 22, 2017. On January 8, 2018, USACE

accepted the permitting documentation and confirmed that an EIS

level of analysis was required to comply with its NEPA review of

the Pebble Project. The EIS process progressed through the scoping

phase in 2018. The USACE delivered the draft EIS in the first

quarter of 2019 and completed a public comment period from March to

July 2019. In the latter part of 2019 and early 2020, the USACE and

its consultants advanced toward a final EIS. The preliminary final

EIS was circulated to co-operating agencies for review in February

2020. As part of the EIS preparation process, the USACE and its

consultants had undertaken a comprehensive alternatives assessment

to consider a broad range of development alternatives and announced

the conclusions of the draft LEDPA in May 2020. The USACE published

the final Pebble EIS on July 24, 2020.

The

Pebble Partnership developed the CMP (further described in the

Company’s Three Year History above) to align with the

requirements outlined by the USACE. The CMP was submitted on

November 4, 2021.

On

November 25, 2020, the USACE issued a ROD rejecting the Pebble

Partnership’s permit application. The Pebble Partnership

submitted a RFA of the ROD on January 19, 2021. In a letter dated

February 24, 2021, the USACE confirmed the Pebble

Partnership’s RFA is “complete and meets the criteria

for appeal.”

Several

estimates of the mineral resources in the Pebble Deposit have been

done since Northern Dynasty acquired the project in 2001,

indicating that the deposit contains significant amounts of copper,

gold, molybdenum and silver. In September 2020, Northern Dynasty

published a Technical Report on the Pebble Project documenting

recent studies of the occurrence of rhenium and an estimate of the

rhenium mineral resources in the Pebble deposit. Although previous

work also determined significant amounts of palladium are present,

at least in parts of the deposit, insufficient analyses have

been completed to date to undertake an estimate of the palladium

resource. The report also summarized the proposed plan for the

project as documented in the June 2020 Project Description and

final Pebble EIS.

The

purpose of the 2021 Technical Report that will be filed with this

AIF is to update the current status of the EIS process for the

Pebble Project, given the decisions of the USACE. No changes were

made to the resource estimate from the September 2020 Technical

Report. Information on closure was also added to the Project

Description and Permitting section of the 2021 Technical

Report.

Property Description and Location

The

Pebble Project is located in southwest Alaska, approximately 200

miles southwest of Anchorage, 17 miles northwest of the village of

Iliamna, and approximately 60 miles west of Cook

Inlet.

|

2020

Annual Information Form

|

Page | 18

|

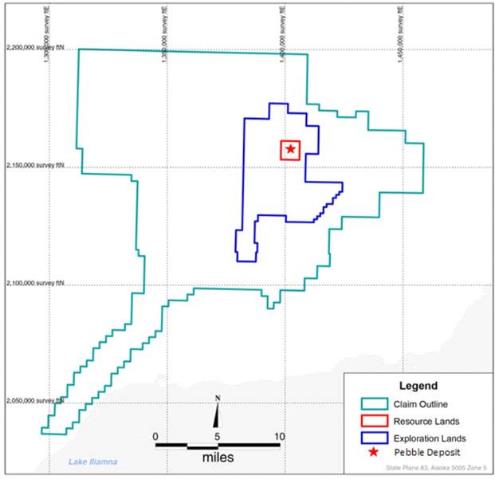

Figure

1

Property Location – Pebble Project

Source:

2018 Technical Report

Northern

Dynasty holds, indirectly through wholly-owned subsidiaries of the

wholly-owned Pebble Partnership, Pebble East Claims Corporation and

Pebble West Claims Corporation, a 100% interest in a contiguous

block of 2,402 mineral claims covering approximately 417 square

miles (which includes the Pebble Deposit) (Figure 2).

State

mineral claims in Alaska are kept in good standing by performing

annual assessment work or in lieu of assessment work by paying $100

per year per 40 acre (0.06 square mile) mineral claim, and by

paying annual escalating state

rentals. All of the assessment work payment obligations come due

annually on or before September 1. Credit for excess work can be

banked for a maximum of four years, and can be applied as necessary

to continue to hold the claims in good standing. The Project claims

have a variable amount of work credit available that can be applied

in this way1. State rentals for

2021 are approximately US$1,375,910 and are payable no later than

90 days after the assessment work is due (approximately December

1).

The

Pebble Partnership currently does not own surface rights associated

with the mineral claims that comprise the Pebble property. All

lands are held by the State of Alaska, and surface rights may be

acquired from the state government once areas required for mine

development have been determined and permits awarded. Permits

necessary for exploration drilling and other field programs

associated with pre-development assessment of the Pebble Project

are applied for each year. Environmental liabilities associated

with the Pebble Project include removal of structures, closing

monitoring wells, and removal of piezometers. The State of Alaska

holds a $2 million bond associated with removal and

reclamation of these liabilities.

__________________

1 Annual assessment work obligations for the claims

that are part of the current property of US$667,700 are due in

2021.

|

2020

Annual Information Form

|

Page | 19

|

Figure

2

Mineral Claims – Pebble Project

Source:

2021 Technical Report

Northern

Dynasty acquired the Pebble property by way of a two-part (Resource

Lands and Exploration Lands) purchase option from an Alaskan

subsidiary of Teck Cominco Limited (now Teck), which still retains

a 4% pre-payback advance net profits royalty interest (after debt

service) and 5% after-payback net profits royalty interest in any

mine production from the Exploration Lands portion of the Pebble

property, as shown on the figure above.

In June

2020, the Pebble Partnership established the Pebble Performance

Dividend LLP to distribute a 3% Net Profits Royalty Interest in the

Pebble Project to adult residents of Bristol Bay villages that have

subscribed as participants. The Pebble Performance Dividend will

distribute a guaranteed minimum annual payment of US$3 million each

year the Pebble mine operates beginning at the outset of project

construction.

Accessibility, climate, local resources, infrastructure and

physiography

The

Pebble property is located in southwest Alaska. The map shows a

proposed infrastructure corridor for the project, as further

described as the LEDPA in the Final EIS and the 2021 Technical

Report.

|

2020

Annual Information Form

|

Page | 20

|

Source:

2021 Technical Report

Access

to the property is typically via air travel from the city of

Anchorage, which is situated at the northeastern end of Cook Inlet

and is connected to the national road network via Interstate

Highway 1 through Canada to the USA. Anchorage is serviced daily by

several regularly scheduled flights to major airport hubs in the

USA. From Anchorage, there are regular flights to Iliamna through

Iliamna Air Taxi. Charter flights may also be arranged from

Anchorage. From Iliamna, access to the Pebble property is by

helicopter.

There

are paved roads that connect the villages of Iliamna and Newhalen

to the airport and to each other, and a partly paved, partly gravel

road that extends to a proposed Newhalen River crossing near

Nondalton. The property is currently not connected to any of these