Exhibit 99.1

Mercantile Bank Corporation Reports Strong Third Quarter 2021 Results

Sustained strength in core commercial loan originations, asset quality metrics, and operating performance highlight quarter

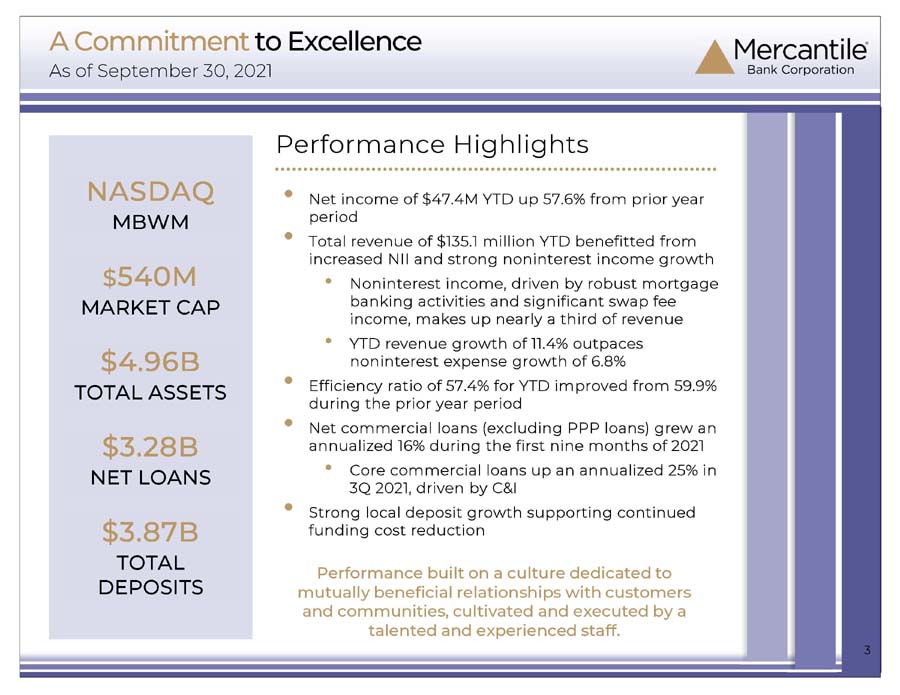

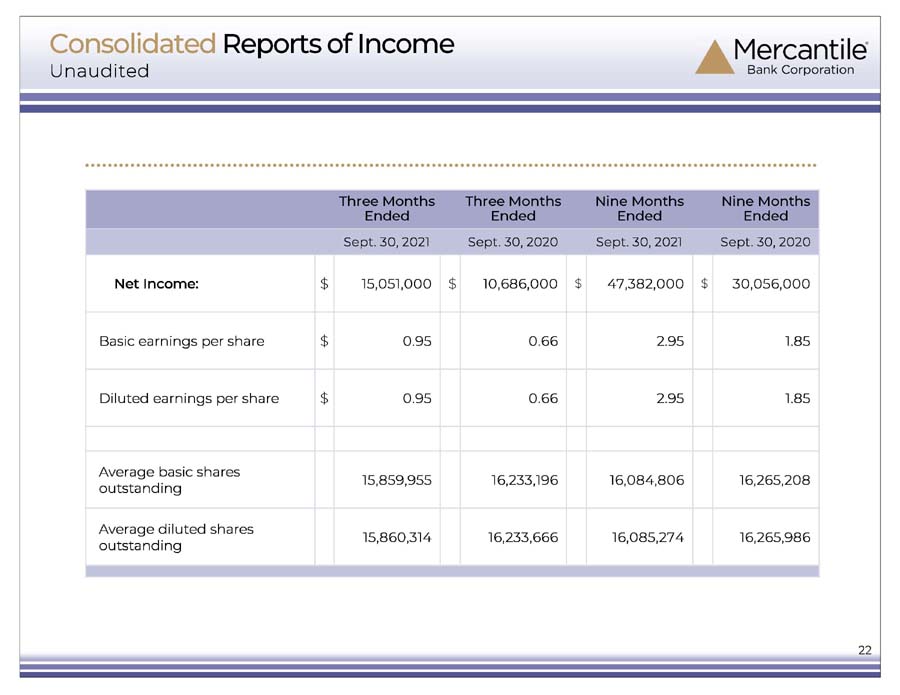

GRAND RAPIDS, Mich., October 19, 2021 – Mercantile Bank Corporation (NASDAQ: MBWM) ("Mercantile") reported net income of $15.1 million, or $0.95 per diluted share, for the third quarter of 2021, up 40.8 percent from $10.7 million, or $0.66 per diluted share, for the respective prior-year period. Net income during the first nine months of 2021 totaled $47.4 million, or $2.95 per diluted share, up 57.6 percent from $30.1 million, or $1.85 per diluted share, during the first nine months of 2020.

“Mercantile’s talented and dedicated people, commitment to local decision making, and longstanding investments in technology all contributed to the bank’s growth in commercial and residential mortgage loans, earnings, net interest income, and fee income, all while maintaining strong asset quality metrics and operating expense discipline,” said Robert B. Kaminski, Jr., President and Chief Executive Officer of Mercantile. “The significant growth in core commercial loans during the quarter, especially when considering the current economic and operating environments, is a noteworthy feat and reflects our commercial lending team’s ongoing concerted effort to meet existing customers’ credit needs and to foster new relationships. Based on our current loan pipeline, we believe core commercial loan originations will remain robust during the fourth quarter and into 2022.”

Third quarter highlights include:

|

● |

Strong growth in core commercial loans and residential mortgage loans |

|

● |

Sustained strength in commercial loan and residential mortgage loan pipelines |

|

● |

Ongoing strength in asset quality metrics |

|

● |

Solid earnings and capital position |

|

● |

Growth in key fee income categories |

|

● |

Additional growth in local deposits |

Operating Results

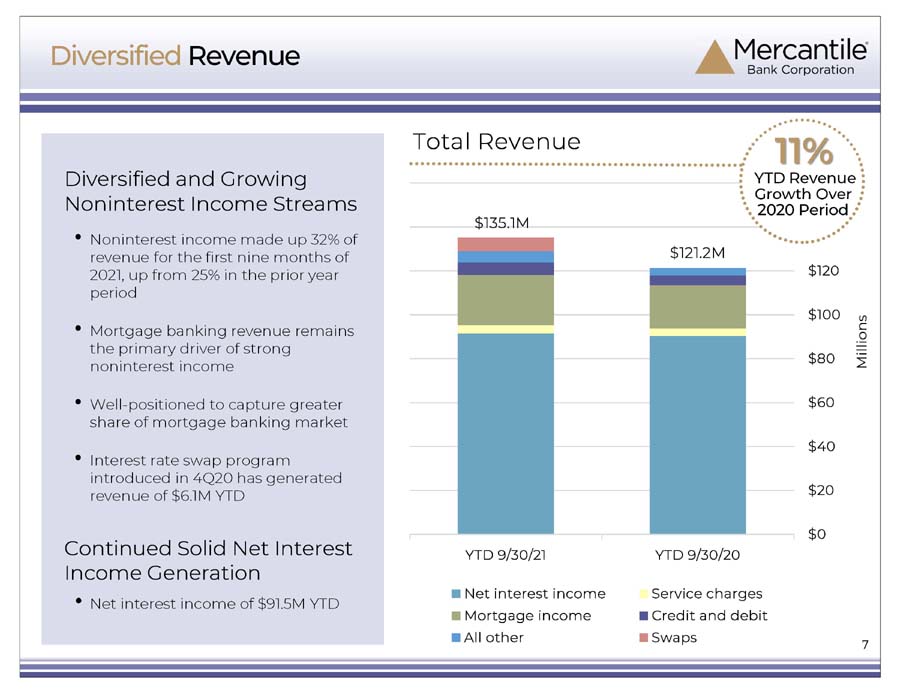

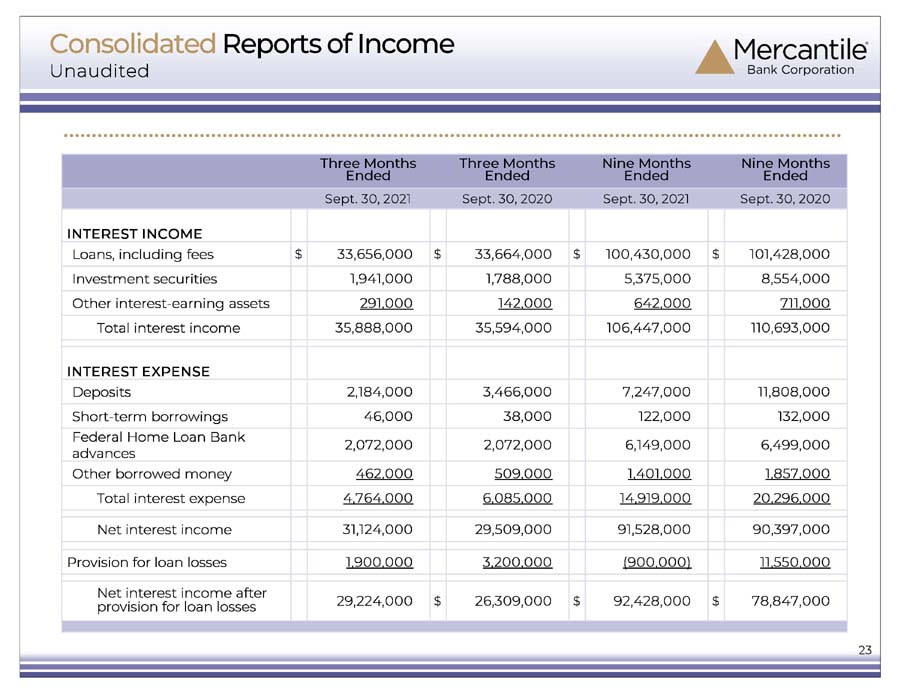

Total revenue, which consists of net interest income and noninterest income, was $46.7 million during the third quarter of 2021, up $3.9 million, or 9.1 percent, from the prior-year third quarter. Net interest income during the third quarter of 2021 was $31.1 million, up from $29.5 million during the respective 2020 period due to the positive impact of earning asset growth, which more than offset a lower net interest margin. Noninterest income totaled $15.6 million during the third quarter of 2021, up $2.3 million from the third quarter of 2020, mainly due to revenue associated with an interest rate swap program that was introduced during the fourth quarter of 2020. The net interest margin was 2.71 percent in the third quarter of 2021, down from 2.86 percent in the prior-year third quarter, reflecting excess liquidity and a lower yield on securities.

The yield on average earning assets declined from 3.45 percent during the third quarter of 2020 to 3.13 percent during the respective 2021 period due to a change in earning asset mix and a decreased yield on securities. A significant volume of excess on-balance sheet liquidity, which initially surfaced in the second quarter of 2020 as a result of the COVID-19 environment and persisted during the remainder of 2020 and first nine months of 2021, negatively impacted both the yield on average earning assets and the net interest margin by 40 basis points to 50 basis points during the third quarter and first nine months of 2021. The excess funds, consisting primarily of low-yielding deposits with the Federal Reserve Bank of Chicago, are mainly a product of federal government stimulus programs, lower business and consumer investing and spending, and Paycheck Protection Program loan forgiveness activities. The decreased yield on securities mainly depicted lower yields on newly purchased bonds, reflecting the declining interest rate environment, and a reduced level of accelerated discount accretion on called U.S. Government agency bonds.

The cost of funds decreased from 0.59 percent during the third quarter of 2020 to 0.42 percent during the current-year third quarter, primarily due to a change in funding mix, consisting of an increase in lower-costing non-time deposits as a percentage of total funding sources, and lower rates paid on local time deposits, reflecting the declining interest rate environment.

Mercantile recorded provision expense of $1.9 million and $3.2 million during the third quarters of 2021 and 2020, respectively. The provision expense recorded during the current-year third quarter mainly reflected net commercial loan growth, while the provision expense recorded during the prior-year third quarter was primarily comprised of increased allocations associated with the downgrading of certain non-impaired commercial loan relationships to reflect stressed economic conditions stemming from the COVID-19 environment.

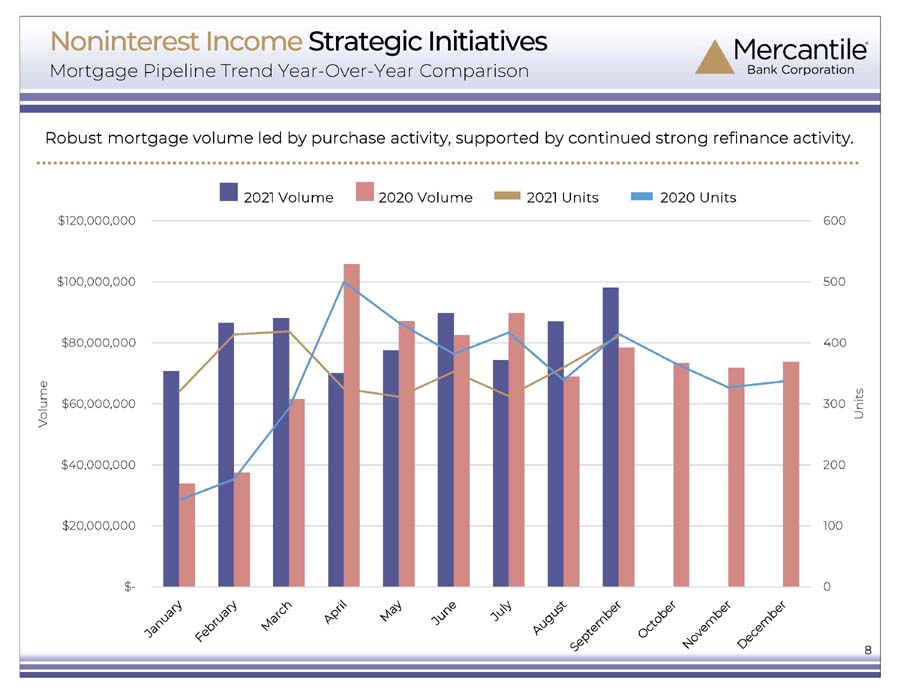

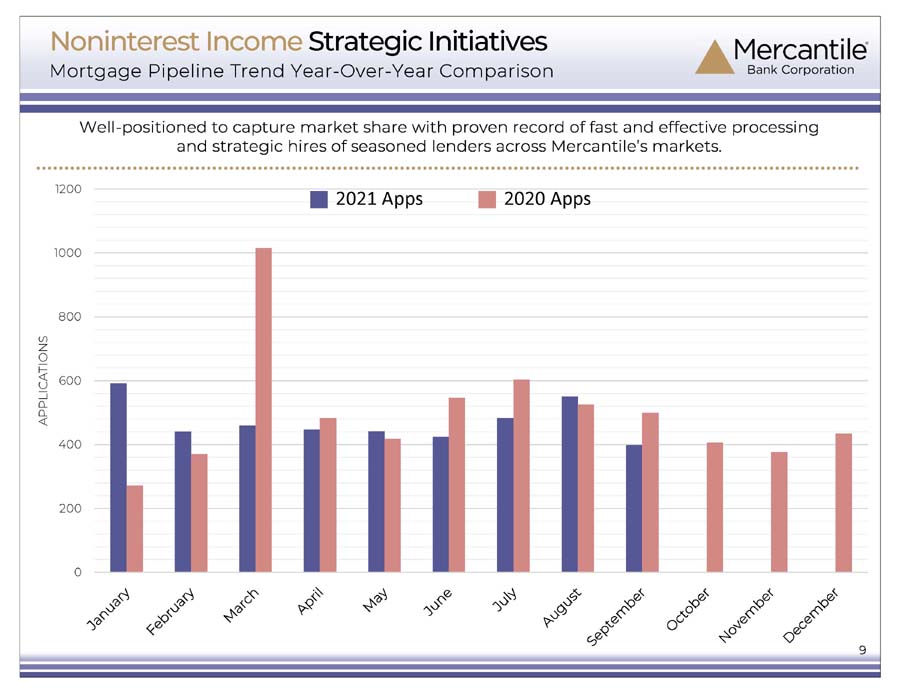

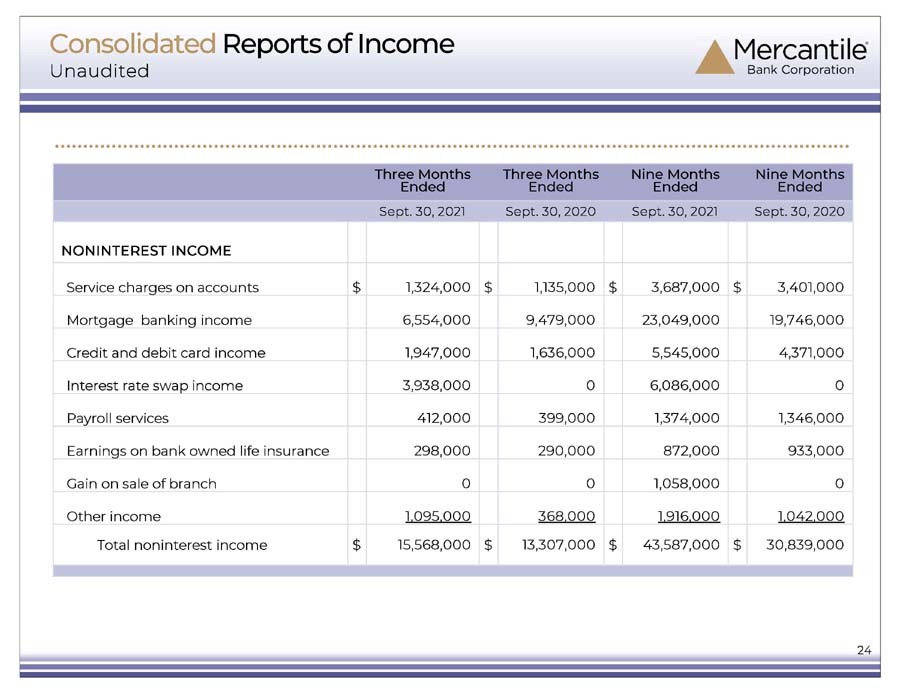

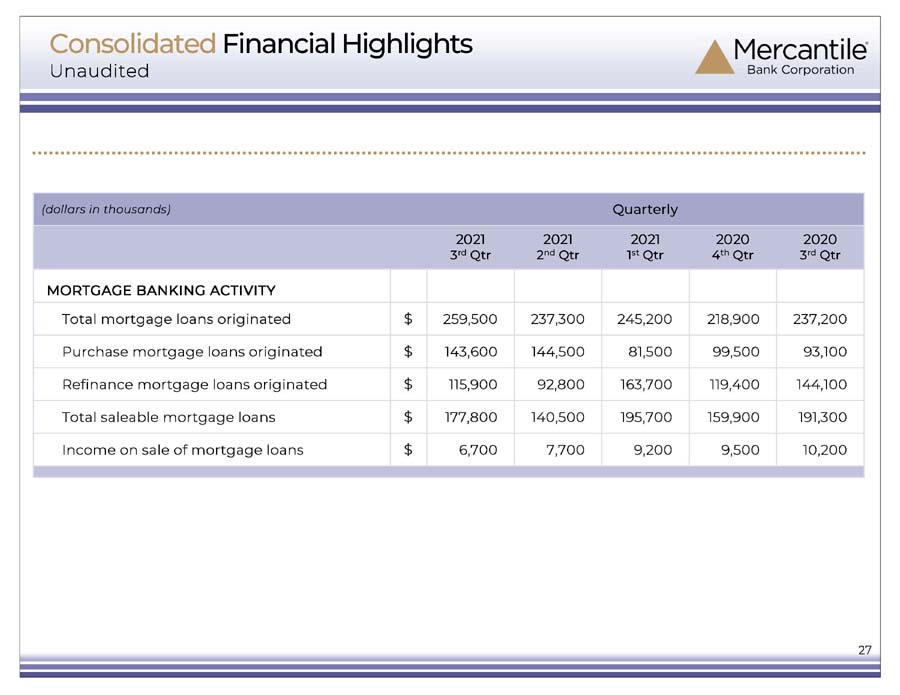

Noninterest income during the third quarter of 2021 was $15.6 million, an increase of 17.0 percent when compared to the prior-year third quarter. The higher level of noninterest income mainly reflected fee income generated from an interest rate swap program that was introduced during the fourth quarter of 2020, which provides certain commercial borrowers with a longer-term fixed-rate option and assists Mercantile in managing associated longer-term interest rate risk. Growth in debit and credit card income and service charges on accounts also contributed to the increased level of noninterest income. Mortgage banking income remained sound in the third quarter of 2021 as sustained strength in purchase mortgage originations largely mitigated the negative impacts of an expected decrease in refinance activity, a lower mortgage loan sold percentage, and a decreased gain on sale rate.

Noninterest expense totaled $26.2 million during the third quarter of 2021, down $0.2 million from the third quarter of 2020. The lower level of expense primarily resulted from decreased compensation costs, mainly reflecting a reduced bonus accrual and lower stock-based compensation expense, which more than offset increased regular salary expense primarily stemming from annual employee merit pay increases. The bonus accrual during the third quarter of last year was increased due to a change in estimate as no accruals were recorded during the first and second quarters of the year due to COVID-19 and associated weakened economic environment. Health insurance costs increased in the third quarter of 2021 compared to the prior-year third quarter mainly due to a higher level of claims, some of which resulted from the treatment of COVID-19 related medical conditions. Federal Deposit Insurance Corporation deposit insurance premiums were up in the current-year third quarter compared to the respective 2020 period primarily as a result of an increased assessment base and rate.

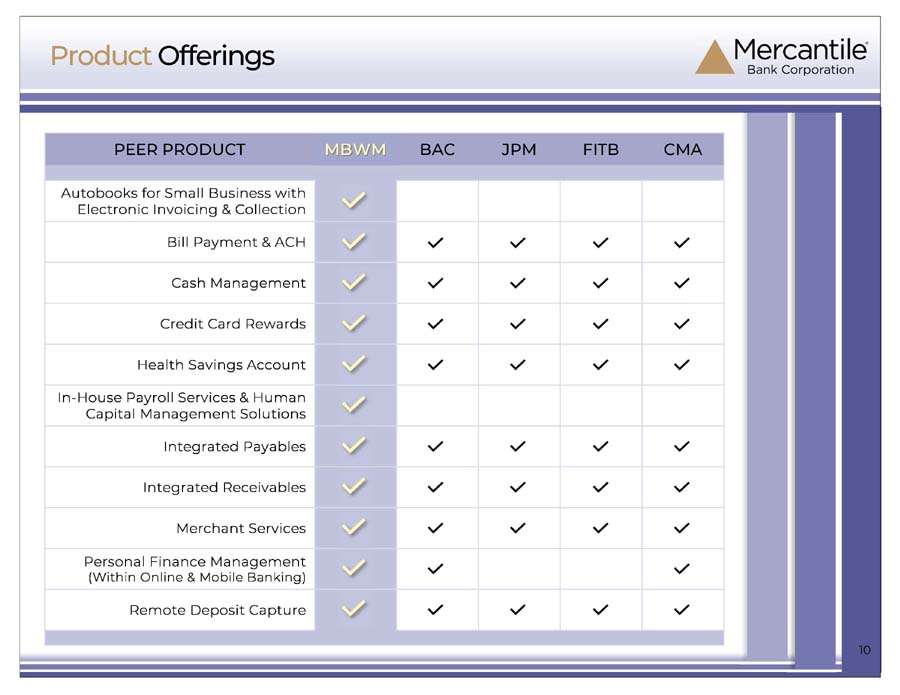

Mr. Kaminski commented, “The growth in key fee income categories reflects our continuing efforts to augment our noninterest income revenue streams, which represented 33 percent of operating revenue in the third quarter. Our interest rate risk swap program continues to be well received by commercial loan customers, and the ongoing success in developing new commercial and industrial loan relationships provides us with opportunities to cross sell treasury management products and services, which serve as another contributor to fee income. Growth in residential mortgage loan purchase originations has largely offset the negative impact of an expected decline in refinance activity on mortgage banking income. We remain committed to growing in a cost-conscious manner and are continually reviewing overhead categories in an effort to improve efficiency where feasible.”

Balance Sheet

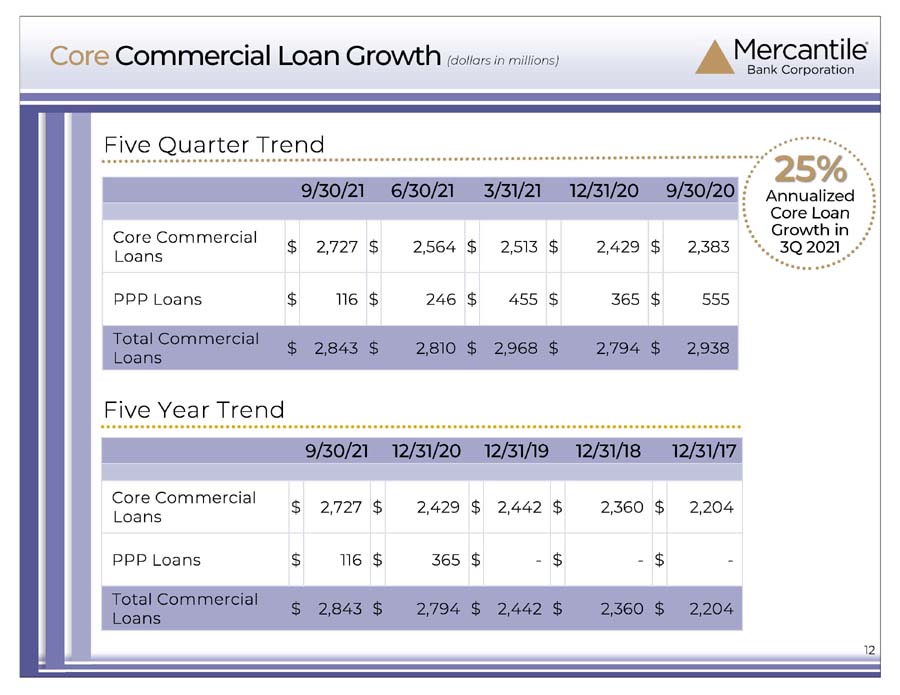

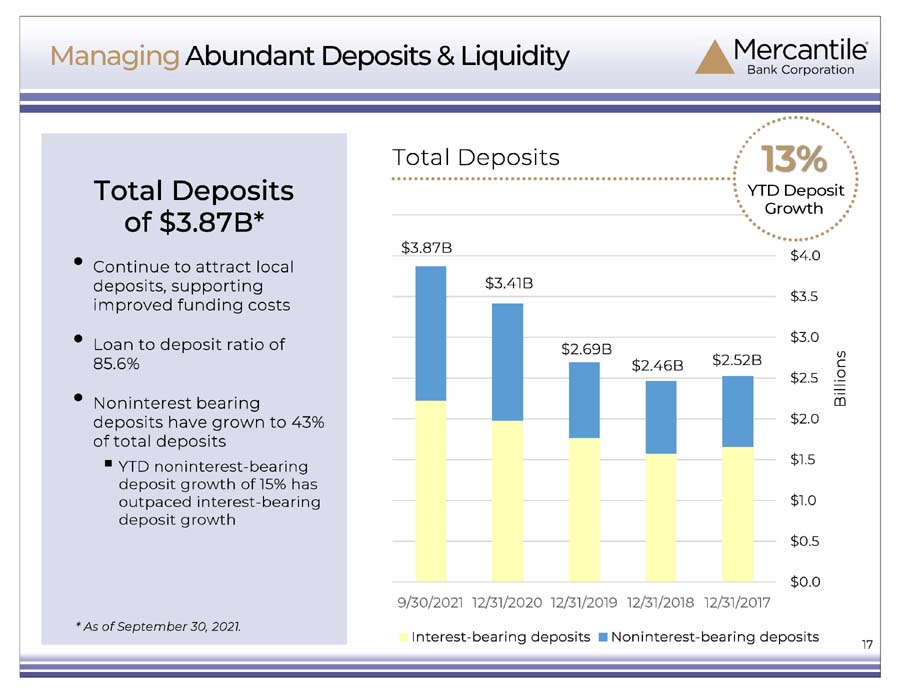

As of September 30, 2021, total assets were $4.96 billion, up $527 million, or 11.9 percent, from December 31, 2020. Total loans increased $120 million during the first nine months of 2021, primarily reflecting net increases in core commercial loans of $298 million, of which $162 million occurred in the third quarter, and residential mortgage loans of $73.7 million, which more than offset a net reduction in Paycheck Protection Program loans of $249 million. The growth in core commercial loans during the first nine months of 2021 equated to an annualized growth rate of approximately 16 percent. As of September 30, 2021, unfunded commitments on commercial construction and development loans totaled approximately $155 million, which are expected to be largely funded over the next 12 to 18 months.

Interest-earning deposits increased $178 million during the first nine months of 2021, mainly reflecting continuing local deposit growth, Paycheck Protection Program forgiveness activities and an increase in sweep accounts, which outpaced loan growth and an expanded securities portfolio.

Ray Reitsma, President of Mercantile Bank of Michigan, noted, “We are very pleased with the strong levels of core commercial loan and residential mortgage loan growth during the third quarter. The growth in the core commercial loan portfolio, which was achieved in a prudent manner with an unwavering emphasis on sound underwriting and risk-based pricing, reflects our commercial lending team’s continuing focus on meeting the needs of our existing customers and successful client acquisition efforts. A majority of the core commercial loan growth was in the commercial and industrial loan category, which typically generates additional local deposits and affords us the opportunity to cross sell treasury management products and services. We are also pleased with the sustained strength of our commercial loan and residential loan pipelines.”

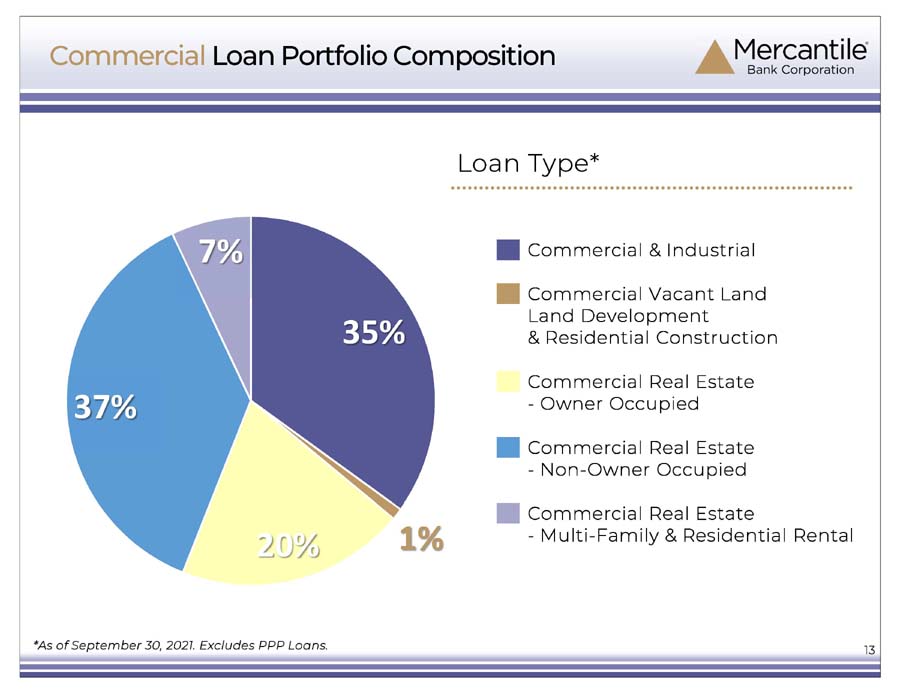

Excluding the impact of Paycheck Protection Program loan originations, commercial and industrial loans and owner-occupied commercial real estate loans together represented approximately 55 percent of total commercial loans as of September 30, 2021, a level that has remained relatively consistent and in line with internal expectations.

Total deposits at September 30, 2021, were $3.87 billion, up $457 million, or 13.4 percent, from December 31, 2020. Local deposits were up $480 million during the first nine months of 2021, while brokered deposits were down $23.0 million. The growth in local deposits, which occurred despite typical and expected seasonal business deposit withdrawals used for bonus and tax payments, primarily reflected federal government stimulus payments, reduced business and consumer investing and spending, deposits generated from newly established commercial loan relationships, and Paycheck Protection Program loan proceeds being deposited into customers’ accounts at the time the loans were originated and remaining on deposit as of September 30, 2021. Wholesale funds were $418 million, or approximately 9 percent of total funds, as of September 30, 2021, compared to $441 million, or approximately 11 percent of total funds, as of December 31, 2020.

Asset Quality

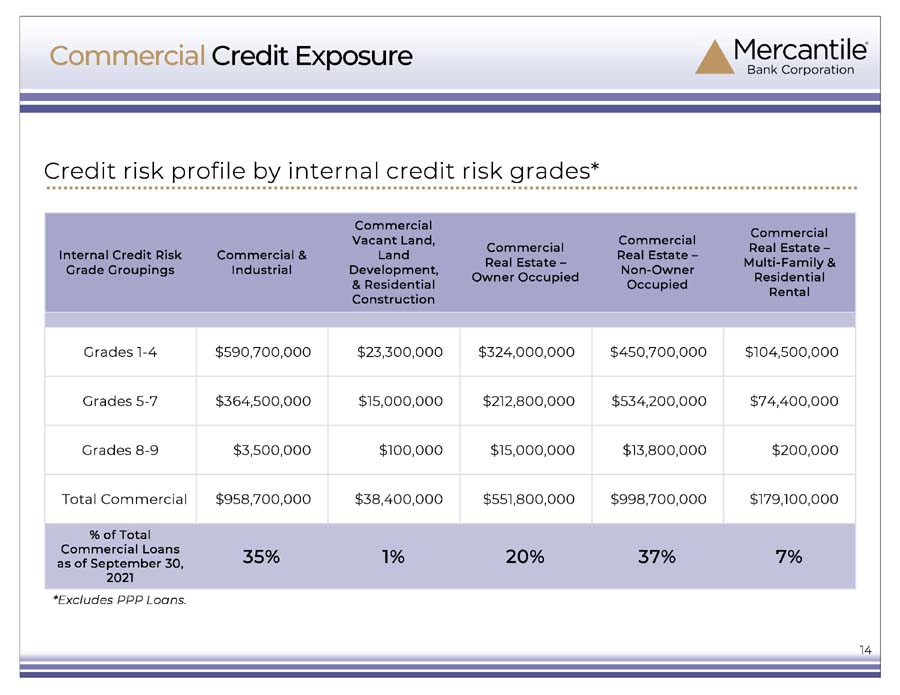

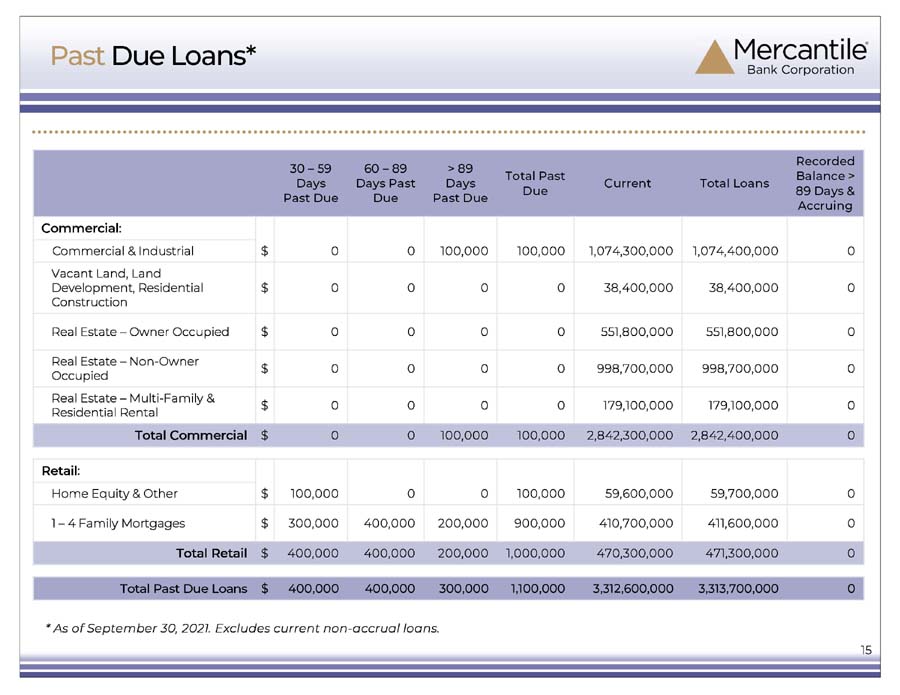

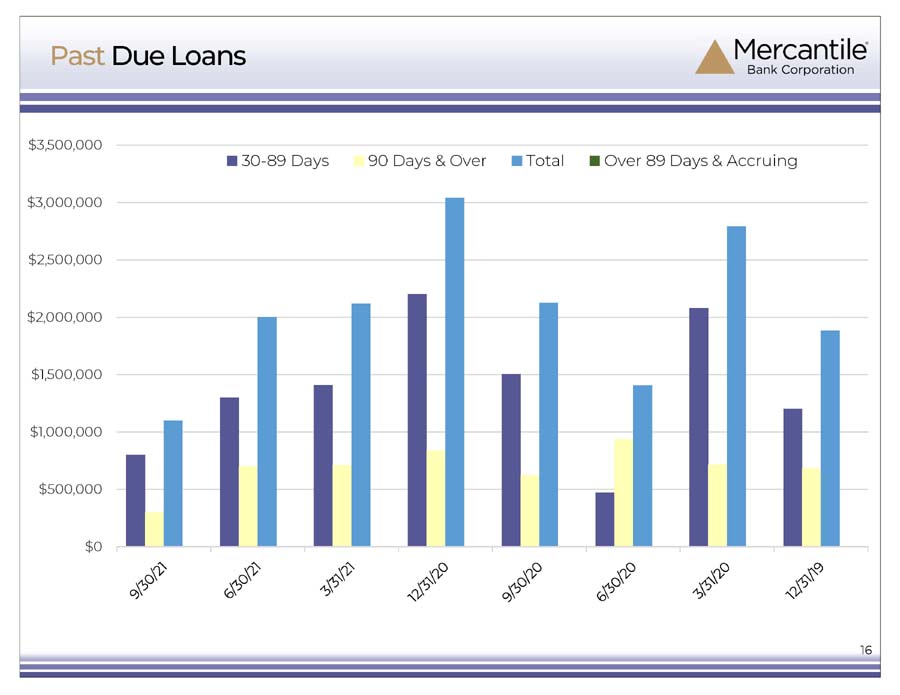

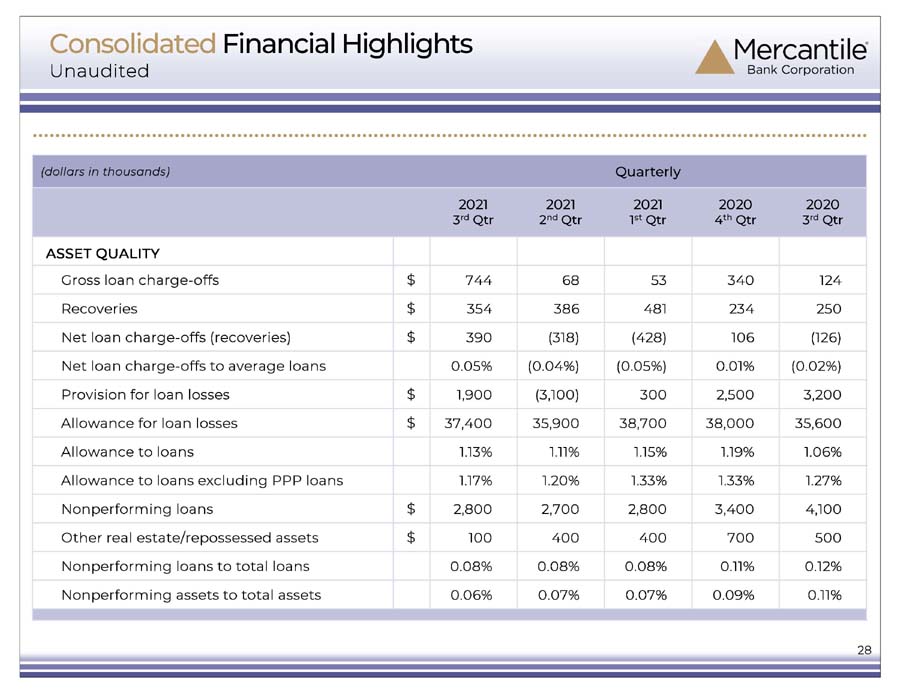

Nonperforming assets totaled $2.9 million, $4.1 million, and $4.7 million at September 30, 2021, December 31, 2020, and September 30, 2020, respectively, with each dollar amount representing 0.1 percent of total assets as of the respective dates. During the third quarter of 2021, loan charge-offs totaled $0.8 million, while recoveries of prior period loan charge-offs equaled $0.4 million, providing for net loan charge-offs of $0.4 million, or an annualized 0.05 percent of average total loans. During the first nine months of 2021, loan charge-offs totaled $0.9 million, while recoveries of prior period loan charge-offs equaled $1.2 million, providing for net loan recoveries of $0.3 million, or an annualized 0.01 percent of average total loans.

Mr. Reitsma commented, “As evidenced by the continuing low levels of past due loans, gross loan charge-offs, and nonperforming assets, our asset quality metrics have remained strong during the COVID-19 pandemic. The sustained strength in asset quality depicts our ongoing focus on proper underwriting and our commercial borrowers’ business acumen and success in addressing pandemic-related challenges, including the rising costs and disruption posed by supply chain shortages and a tight labor market.”

Capital Position

Shareholders’ equity totaled $452 million as of September 30, 2021, an increase of $10.7 million from year-end 2020. Mercantile Bank of Michigan’s capital position remains above “well-capitalized” with a total risk-based capital ratio of 12.4 percent as of September 30, 2021, compared to 13.5 percent at December 31, 2020. At September 30, 2021, Mercantile Bank of Michigan had approximately $94 million in excess of the 10.0 percent minimum regulatory threshold required to be considered a “well-capitalized” institution. Mercantile reported 15,717,663 total shares outstanding at September 30, 2021.

As part of $20.0 million common stock repurchase programs announced in May of 2019 and 2021, respectively, Mercantile repurchased approximately 289,000 shares for $8.9 million, at a weighted average all-in cost per share of $30.97, during the third quarter of 2021 and approximately 636,000 shares for $19.8 million, at a weighted average all-in cost per share of $31.14, during the first nine months of 2021. The 2021 program replaced the 2019 program, which was nearing exhaustion. The actual timing, number and value of shares repurchased under the program will be determined by management in its discretion and will depend on a number of factors, including Mercantile’s stock price, capital position, and financial performance, general market and economic conditions, alternative uses of capital, and applicable legal requirements. As of September 30, 2021, availability under the current program equaled $8.4 million. The program may be discontinued at any time.

Mr. Kaminski concluded, “We are pleased that our ongoing financial strength has allowed us to continue our regular quarterly cash dividend program and provide shareholders with meaningful cash returns on their investments. Our business model, which focuses on mutually beneficial relationship building, exceptional customer service, local decision making, and market-leading products and services, has proven effective in retaining existing clients and attracting new customers, and we believe we are well positioned to produce strong operating results in future periods and remain a consistent high performer that delivers steady and profitable growth.”

Investor Presentation

Mercantile has prepared presentation materials that management intends to use during its previously announced third quarter 2021 conference call on Tuesday, October 19, 2021, at 10:00 a.m. Eastern Time, and from time to time thereafter in presentations about the Company’s operations and performance. The Investor Presentation also contains information relating to Mercantile’s COVID-19 pandemic response plan, which may be modified to address new developments, as the company carefully monitors the recent surge in cases. These materials have been furnished to the U.S. Securities and Exchange Commission concurrently with this press release, and are also available on Mercantile’s website at www.mercbank.com.

About Mercantile Bank Corporation

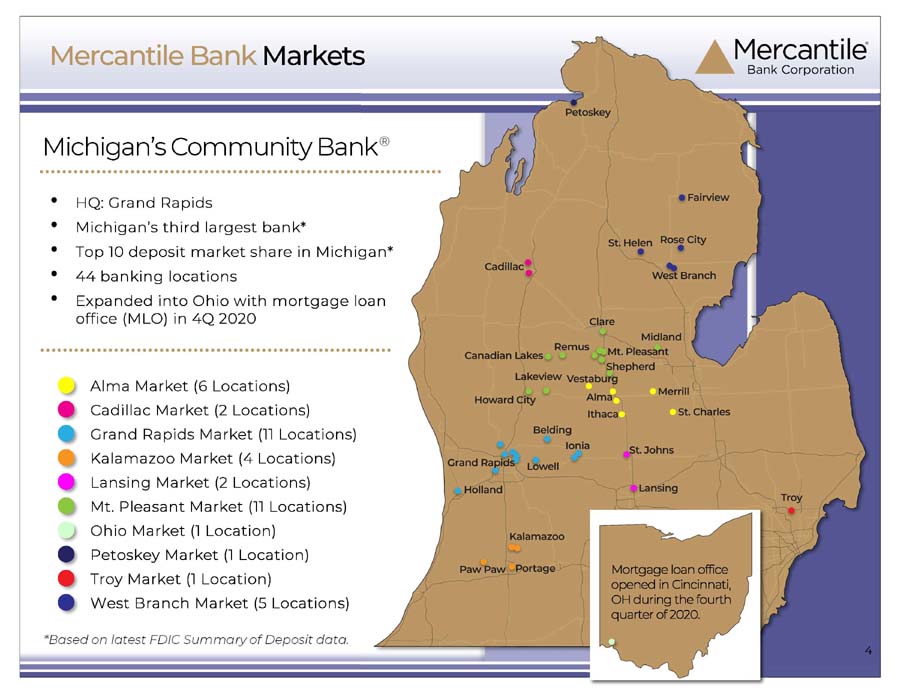

Based in Grand Rapids, Michigan, Mercantile Bank Corporation is the bank holding company for Mercantile Bank of Michigan. Mercantile provides banking services to businesses, individuals and governmental units, and differentiates itself on the basis of service quality and the expertise of its banking staff. Mercantile has assets of approximately $4.9 billion and operates 43 banking offices. Mercantile Bank Corporation’s common stock is listed on the NASDAQ Global Select Market under the symbol “MBWM.”

Forward-Looking Statements

This news release contains statements or information that may constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Forward-looking statements can be identified by words such as: “anticipate,” “intend,” “plan,” “goal,” “seek,” “believe,” “project,” “estimate,” “expect,” “strategy,” “future,” “likely,” “may,” “should,” “will,” and similar references to future periods. Any such statements are based on current expectations that involve a number of risks and uncertainties. Actual results may differ materially from the results expressed in forward-looking statements. Factors that might cause such a difference include changes in interest rates and interest rate relationships; increasing rates of inflation and slower growth rates; significant declines in the value of commercial real estate; market volatility; demand for products and services; the degree of competition by traditional and nontraditional financial services companies; changes in banking regulation or actions by bank regulators; changes in tax laws; changes in prices, levies, and assessments; the impact of technological advances; potential cyber-attacks, information security breaches and other criminal activities; our participation in the Paycheck Protection Program administered by the Small Business Administration; litigation liabilities; governmental and regulatory policy changes; the outcomes of existing or future contingencies; trends in customer behavior as well as their ability to repay loans; changes in local real estate values; damage to our reputation resulting from adverse publicity, regulatory actions, litigation, operational failures, and the failure to meet client expectations and other facts; changes in the method of determining Libor and the phase-out of Libor; changes in the national and local economies, including the ongoing disruption to financial market and other economic activity caused by the COVID-19 pandemic; and other factors, including those expressed as risk factors, disclosed from time to time in filings made by Mercantile with the Securities and Exchange Commission. Mercantile undertakes no obligation to update or clarify forward-looking statements, whether as a result of new information, future events or otherwise. Investors are cautioned not to place undue reliance on any forward-looking statements contained herein.

FOR FURTHER INFORMATION:

|

Robert B. Kaminski, Jr. President & CEO 616-726-1502 rkaminski@mercbank.com |

Charles Christmas Executive Vice President & CFO 616-726-1202 cchristmas@mercbank.com |

|

Mercantile Bank Corporation |

|

Third Quarter 2021 Results |

|

MERCANTILE BANK CORPORATION |

|

CONSOLIDATED BALANCE SHEETS |

|

(Unaudited) |

|

SEPTEMBER 30, |

DECEMBER 31, |

SEPTEMBER 30, |

||||||||||

|

2021 |

2020 |

2020 |

||||||||||

|

ASSETS |

||||||||||||

|

Cash and due from banks |

$ | 83,804,000 | $ | 62,832,000 | $ | 59,283,000 | ||||||

|

Interest-earning deposits |

741,557,000 | 563,174,000 | 495,308,000 | |||||||||

|

Total cash and cash equivalents |

825,361,000 | 626,006,000 | 554,591,000 | |||||||||

|

Securities available for sale |

559,564,000 | 387,347,000 | 312,424,000 | |||||||||

|

Federal Home Loan Bank stock |

18,002,000 | 18,002,000 | 18,002,000 | |||||||||

|

Loans |

3,313,709,000 | 3,193,470,000 | 3,324,202,000 | |||||||||

|

Allowance for loan losses |

(37,423,000 | ) | (37,967,000 | ) | (35,572,000 | ) | ||||||

|

Loans, net |

3,276,286,000 | 3,155,503,000 | 3,288,630,000 | |||||||||

|

Premises and equipment, net |

57,465,000 | 58,959,000 | 60,446,000 | |||||||||

|

Bank owned life insurance |

72,963,000 | 72,131,000 | 71,170,000 | |||||||||

|

Goodwill |

49,473,000 | 49,473,000 | 49,473,000 | |||||||||

|

Core deposit intangible, net |

1,589,000 | 2,436,000 | 2,754,000 | |||||||||

|

Mortgage loans held for sale |

47,247,000 | 22,888,000 | 26,342,000 | |||||||||

|

Other assets |

56,462,000 | 44,599,000 | 36,778,000 | |||||||||

|

Total assets |

$ | 4,964,412,000 | $ | 4,437,344,000 | $ | 4,420,610,000 | ||||||

|

LIABILITIES AND SHAREHOLDERS' EQUITY |

||||||||||||

|

Deposits: |

||||||||||||

|

Noninterest-bearing |

$ | 1,647,380,000 | $ | 1,433,403,000 | $ | 1,449,879,000 | ||||||

|

Interest-bearing |

2,221,611,000 | 1,978,150,000 | 1,922,155,000 | |||||||||

|

Total deposits |

3,868,991,000 | 3,411,553,000 | 3,372,034,000 | |||||||||

|

Securities sold under agreements to repurchase |

175,850,000 | 118,365,000 | 157,017,000 | |||||||||

|

Federal Home Loan Bank advances |

394,000,000 | 394,000,000 | 394,000,000 | |||||||||

|

Subordinated debentures |

48,074,000 | 47,563,000 | 47,392,000 | |||||||||

|

Accrued interest and other liabilities |

25,219,000 | 24,309,000 | 18,267,000 | |||||||||

|

Total liabilities |

4,512,134,000 | 3,995,790,000 | 3,988,710,000 | |||||||||

|

SHAREHOLDERS' EQUITY |

||||||||||||

|

Common stock |

285,033,000 | 302,029,000 | 301,896,000 | |||||||||

|

Retained earnings |

167,541,000 | 134,039,000 | 124,451,000 | |||||||||

|

Accumulated other comprehensive income/(loss) |

(296,000 | ) | 5,486,000 | 5,553,000 | ||||||||

|

Total shareholders' equity |

452,278,000 | 441,554,000 | 431,900,000 | |||||||||

|

Total liabilities and shareholders' equity |

$ | 4,964,412,000 | $ | 4,437,344,000 | $ | 4,420,610,000 | ||||||

|

Mercantile Bank Corporation |

|

Third Quarter 2021 Results |

|

MERCANTILE BANK CORPORATION |

|

CONSOLIDATED REPORTS OF INCOME |

|

(Unaudited) |

|

THREE MONTHS ENDED |

THREE MONTHS ENDED |

NINE MONTHS ENDED |

NINE MONTHS ENDED |

|||||||||||||

|

September 30, 2021 |

September 30, 2020 |

September 30, 2021 |

September 30, 2020 |

|||||||||||||

|

INTEREST INCOME |

||||||||||||||||

|

Loans, including fees |

$ | 33,656,000 | $ | 33,664,000 | $ | 100,430,000 | $ | 101,428,000 | ||||||||

|

Investment securities |

1,941,000 | 1,788,000 | 5,375,000 | 8,554,000 | ||||||||||||

|

Other interest-earning assets |

291,000 | 142,000 | 642,000 | 711,000 | ||||||||||||

|

Total interest income |

35,888,000 | 35,594,000 | 106,447,000 | 110,693,000 | ||||||||||||

|

INTEREST EXPENSE |

||||||||||||||||

|

Deposits |

2,184,000 | 3,466,000 | 7,247,000 | 11,808,000 | ||||||||||||

|

Short-term borrowings |

46,000 | 38,000 | 122,000 | 132,000 | ||||||||||||

|

Federal Home Loan Bank advances |

2,072,000 | 2,072,000 | 6,149,000 | 6,499,000 | ||||||||||||

|

Other borrowed money |

462,000 | 509,000 | 1,401,000 | 1,857,000 | ||||||||||||

|

Total interest expense |

4,764,000 | 6,085,000 | 14,919,000 | 20,296,000 | ||||||||||||

|

Net interest income |

31,124,000 | 29,509,000 | 91,528,000 | 90,397,000 | ||||||||||||

|

Provision for loan losses |

1,900,000 | 3,200,000 | (900,000 | ) | 11,550,000 | |||||||||||

|

Net interest income after provision for loan losses |

29,224,000 | 26,309,000 | 92,428,000 | 78,847,000 | ||||||||||||

|

NONINTEREST INCOME |

||||||||||||||||

|

Service charges on accounts |

1,324,000 | 1,135,000 | 3,687,000 | 3,401,000 | ||||||||||||

|

Mortgage banking income |

6,554,000 | 9,479,000 | 23,049,000 | 19,746,000 | ||||||||||||

|

Credit and debit card income |

1,947,000 | 1,636,000 | 5,545,000 | 4,371,000 | ||||||||||||

|

Interest rate swap income |

3,938,000 | 0 | 6,086,000 | 0 | ||||||||||||

|

Payroll services |

412,000 | 399,000 | 1,374,000 | 1,346,000 | ||||||||||||

|

Earnings on bank owned life insurance |

298,000 | 290,000 | 872,000 | 933,000 | ||||||||||||

|

Gain on sale of branch |

0 | 0 | 1,058,000 | 0 | ||||||||||||

|

Other income |

1,095,000 | 368,000 | 1,916,000 | 1,042,000 | ||||||||||||

|

Total noninterest income |

15,568,000 | 13,307,000 | 43,587,000 | 30,839,000 | ||||||||||||

|

NONINTEREST EXPENSE |

||||||||||||||||

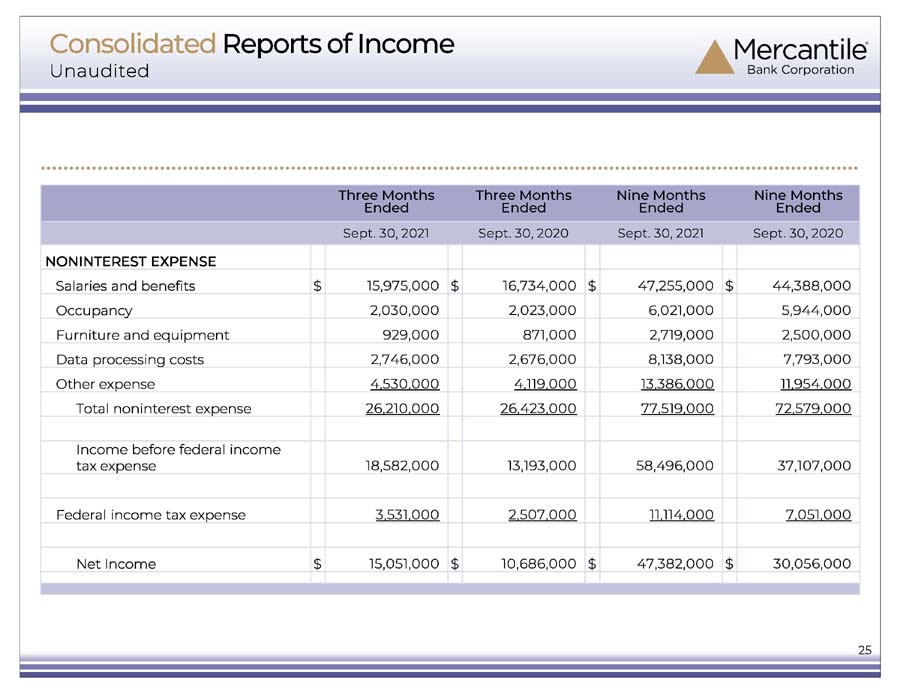

|

Salaries and benefits |

15,975,000 | 16,734,000 | 47,255,000 | 44,388,000 | ||||||||||||

|

Occupancy |

2,030,000 | 2,023,000 | 6,021,000 | 5,944,000 | ||||||||||||

|

Furniture and equipment |

929,000 | 871,000 | 2,719,000 | 2,500,000 | ||||||||||||

|

Data processing costs |

2,746,000 | 2,676,000 | 8,138,000 | 7,793,000 | ||||||||||||

|

Other expense |

4,530,000 | 4,119,000 | 13,386,000 | 11,954,000 | ||||||||||||

|

Total noninterest expense |

26,210,000 | 26,423,000 | 77,519,000 | 72,579,000 | ||||||||||||

|

Income before federal income tax expense |

18,582,000 | 13,193,000 | 58,496,000 | 37,107,000 | ||||||||||||

|

Federal income tax expense |

3,531,000 | 2,507,000 | 11,114,000 | 7,051,000 | ||||||||||||

|

Net Income |

$ | 15,051,000 | $ | 10,686,000 | $ | 47,382,000 | $ | 30,056,000 | ||||||||

|

Basic earnings per share |

$ | 0.95 | $ | 0.66 | $ | 2.95 | $ | 1.85 | ||||||||

|

Diluted earnings per share |

$ | 0.95 | $ | 0.66 | $ | 2.95 | $ | 1.85 | ||||||||

|

Average basic shares outstanding |

15,859,955 | 16,233,196 | 16,084,806 | 16,265,208 | ||||||||||||

|

Average diluted shares outstanding |

15,860,314 | 16,233,666 | 16,085,274 | 16,265,986 | ||||||||||||

|

Mercantile Bank Corporation |

|

Third Quarter 2021 Results |

|

MERCANTILE BANK CORPORATION |

|

CONSOLIDATED FINANCIAL HIGHLIGHTS |

|

(Unaudited) |

|

Quarterly |

Year-To-Date |

|||||||||||||||||||||||||||

|

(dollars in thousands except per share data) |

2021 |

2021 |

2021 |

2020 |

2020 |

|||||||||||||||||||||||

|

3rd Qtr |

2nd Qtr |

1st Qtr |

4th Qtr |

3rd Qtr |

2021 |

2020 |

||||||||||||||||||||||

|

EARNINGS |

||||||||||||||||||||||||||||

|

Net interest income |

$ | 31,124 | 30,871 | 29,533 | 31,849 | 29,509 | 91,528 | 90,397 | ||||||||||||||||||||

|

Provision for loan losses |

$ | 1,900 | (3,100 | ) | 300 | 2,500 | 3,200 | (900 | ) | 11,550 | ||||||||||||||||||

|

Noninterest income |

$ | 15,568 | 14,556 | 13,463 | 14,333 | 13,307 | 43,587 | 30,839 | ||||||||||||||||||||

|

Noninterest expense |

$ | 26,210 | 26,192 | 25,117 | 25,941 | 26,423 | 77,519 | 72,579 | ||||||||||||||||||||

|

Net income before federal income tax expense |

$ | 18,582 | 22,335 | 17,579 | 17,741 | 13,193 | 58,496 | 37,107 | ||||||||||||||||||||

|

Net income |

$ | 15,051 | 18,091 | 14,239 | 14,082 | 10,686 | 47,382 | 30,056 | ||||||||||||||||||||

|

Basic earnings per share |

$ | 0.95 | 1.12 | 0.87 | 0.87 | 0.66 | 2.95 | 1.85 | ||||||||||||||||||||

|

Diluted earnings per share |

$ | 0.95 | 1.12 | 0.87 | 0.87 | 0.66 | 2.95 | 1.85 | ||||||||||||||||||||

|

Average basic shares outstanding |

15,859,955 | 16,116,070 | 16,283,044 | 16,279,052 | 16,233,196 | 16,084,806 | 16,265,208 | |||||||||||||||||||||

|

Average diluted shares outstanding |

15,860,314 | 16,116,666 | 16,283,490 | 16,279,243 | 16,233,666 | 16,085,274 | 16,265,986 | |||||||||||||||||||||

|

PERFORMANCE RATIOS |

||||||||||||||||||||||||||||

|

Return on average assets |

1.23 | % | 1.53 | % | 1.26 | % | 1.25 | % | 0.98 | % | 1.34 | % | 0.99 | % | ||||||||||||||

|

Return on average equity |

13.10 | % | 16.27 | % | 13.02 | % | 12.75 | % | 9.86 | % | 14.12 | % | 9.44 | % | ||||||||||||||

|

Net interest margin (fully tax-equivalent) |

2.71 | % | 2.76 | % | 2.77 | % | 3.00 | % | 2.86 | % | 2.76 | % | 3.19 | % | ||||||||||||||

|

Efficiency ratio |

56.13 | % | 57.66 | % | 58.42 | % | 56.17 | % | 61.71 | % | 57.37 | % | 59.87 | % | ||||||||||||||

|

Full-time equivalent employees |

629 | 634 | 621 | 621 | 618 | 629 | 618 | |||||||||||||||||||||

|

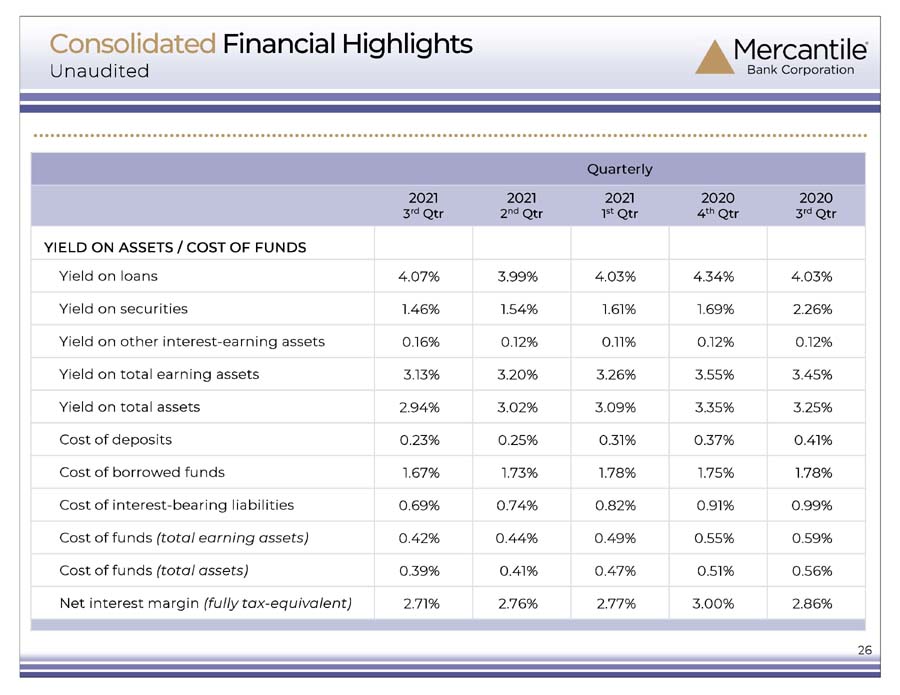

YIELD ON ASSETS / COST OF FUNDS |

||||||||||||||||||||||||||||

|

Yield on loans |

4.07 | % | 3.99 | % | 4.03 | % | 4.34 | % | 4.03 | % | 4.06 | % | 4.28 | % | ||||||||||||||

|

Yield on securities |

1.46 | % | 1.54 | % | 1.61 | % | 1.69 | % | 2.26 | % | 1.53 | % | 3.47 | % | ||||||||||||||

|

Yield on other interest-earning assets |

0.16 | % | 0.12 | % | 0.11 | % | 0.12 | % | 0.12 | % | 0.13 | % | 0.32 | % | ||||||||||||||

|

Yield on total earning assets |

3.13 | % | 3.20 | % | 3.26 | % | 3.55 | % | 3.45 | % | 3.21 | % | 3.91 | % | ||||||||||||||

|

Yield on total assets |

2.94 | % | 3.02 | % | 3.09 | % | 3.35 | % | 3.25 | % | 3.01 | % | 3.67 | % | ||||||||||||||

|

Cost of deposits |

0.23 | % | 0.25 | % | 0.31 | % | 0.37 | % | 0.41 | % | 0.26 | % | 0.52 | % | ||||||||||||||

|

Cost of borrowed funds |

1.67 | % | 1.73 | % | 1.78 | % | 1.75 | % | 1.78 | % | 1.72 | % | 1.98 | % | ||||||||||||||

|

Cost of interest-bearing liabilities |

0.69 | % | 0.74 | % | 0.82 | % | 0.91 | % | 0.99 | % | 0.75 | % | 1.15 | % | ||||||||||||||

|

Cost of funds (total earning assets) |

0.42 | % | 0.44 | % | 0.49 | % | 0.55 | % | 0.59 | % | 0.45 | % | 0.72 | % | ||||||||||||||

|

Cost of funds (total assets) |

0.39 | % | 0.41 | % | 0.47 | % | 0.51 | % | 0.56 | % | 0.42 | % | 0.67 | % | ||||||||||||||

|

PURCHASE ACCOUNTING ADJUSTMENTS |

||||||||||||||||||||||||||||

|

Loan portfolio - increase interest income |

$ | 48 | 54 | 51 | 158 | 332 | 153 | 786 | ||||||||||||||||||||

|

Trust preferred - increase interest expense |

$ | 171 | 171 | 171 | 171 | 171 | 513 | 513 | ||||||||||||||||||||

|

Core deposit intangible - increase overhead |

$ | 238 | 291 | 318 | 318 | 318 | 847 | 1,086 | ||||||||||||||||||||

|

MORTGAGE BANKING ACTIVITY |

||||||||||||||||||||||||||||

|

Total mortgage loans originated |

$ | 259,512 | 237,299 | 245,200 | 218,904 | 237,195 | 742,011 | 645,540 | ||||||||||||||||||||

|

Purchase mortgage loans originated |

$ | 143,635 | 144,476 | 81,529 | 99,490 | 93,068 | 369,640 | 197,621 | ||||||||||||||||||||

|

Refinance mortgage loans originated |

$ | 115,877 | 92,823 | 163,671 | 119,414 | 144,127 | 372,371 | 447,919 | ||||||||||||||||||||

|

Total saleable mortgage loans |

$ | 177,837 | 140,497 | 195,655 | 159,942 | 191,318 | 513,989 | 512,310 | ||||||||||||||||||||

|

Income on sale of mortgage loans |

$ | 6,659 | 7,690 | 9,182 | 9,476 | 10,199 | 23,531 | 20,045 | ||||||||||||||||||||

|

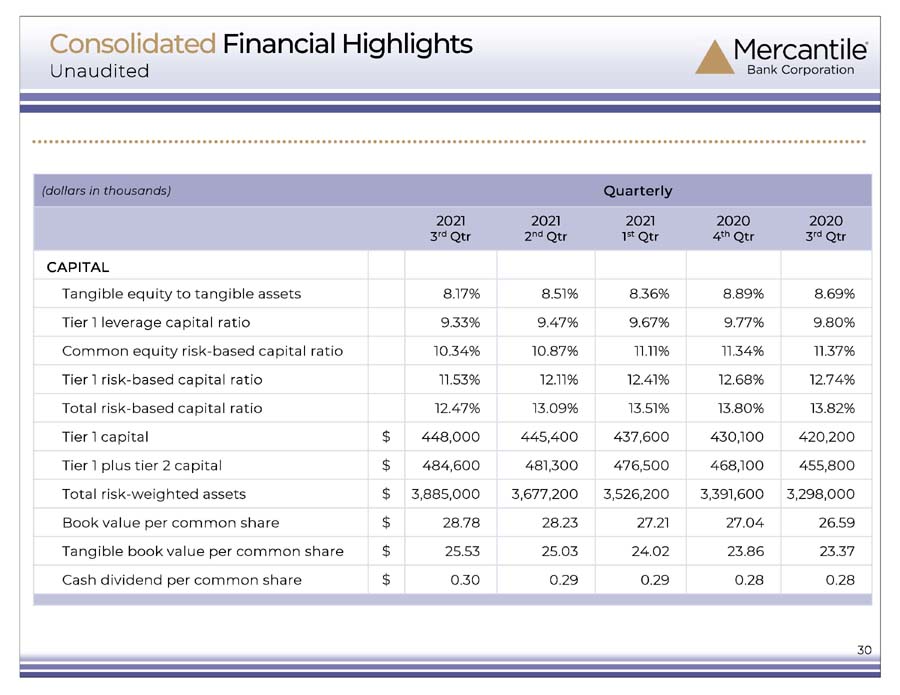

CAPITAL |

||||||||||||||||||||||||||||

|

Tangible equity to tangible assets |

8.17 | % | 8.51 | % | 8.36 | % | 8.89 | % | 8.69 | % | 8.17 | % | 8.69 | % | ||||||||||||||

|

Tier 1 leverage capital ratio |

9.33 | % | 9.47 | % | 9.67 | % | 9.77 | % | 9.80 | % | 9.33 | % | 9.80 | % | ||||||||||||||

|

Common equity risk-based capital ratio |

10.34 | % | 10.87 | % | 11.11 | % | 11.34 | % | 11.37 | % | 10.34 | % | 11.37 | % | ||||||||||||||

|

Tier 1 risk-based capital ratio |

11.53 | % | 12.11 | % | 12.41 | % | 12.68 | % | 12.74 | % | 11.53 | % | 12.74 | % | ||||||||||||||

|

Total risk-based capital ratio |

12.47 | % | 13.09 | % | 13.51 | % | 13.80 | % | 13.82 | % | 12.47 | % | 13.82 | % | ||||||||||||||

|

Tier 1 capital |

$ | 448,010 | 445,410 | 437,567 | 430,146 | 420,225 | 448,010 | 420,225 | ||||||||||||||||||||

|

Tier 1 plus tier 2 capital |

$ | 484,594 | 481,324 | 476,462 | 468,113 | 455,797 | 484,594 | 455,797 | ||||||||||||||||||||

|

Total risk-weighted assets |

$ | 3,884,999 | 3,677,180 | 3,526,161 | 3,391,563 | 3,298,047 | 3,884,999 | 3,298,047 | ||||||||||||||||||||

|

Book value per common share |

$ | 28.78 | 28.23 | 27.21 | 27.04 | 26.59 | 28.78 | 26.59 | ||||||||||||||||||||

|

Tangible book value per common share |

$ | 25.53 | 25.03 | 24.02 | 23.86 | 23.37 | 25.53 | 23.37 | ||||||||||||||||||||

|

Cash dividend per common share |

$ | 0.30 | 0.29 | 0.29 | 0.28 | 0.28 | 0.88 | 0.84 | ||||||||||||||||||||

|

ASSET QUALITY |

||||||||||||||||||||||||||||

|

Gross loan charge-offs |

$ | 744 | 68 | 53 | 340 | 124 | 865 | 499 | ||||||||||||||||||||

|

Recoveries |

$ | 354 | 386 | 481 | 234 | 250 | 1,221 | 632 | ||||||||||||||||||||

|

Net loan charge-offs (recoveries) |

$ | 390 | (318 | ) | (428 | ) | 106 | (126 | ) | (356 | ) | (133 | ) | |||||||||||||||

|

Net loan charge-offs to average loans |

0.05 | % | (0.04% | ) | (0.05% | ) | 0.01 | % | (0.02% | ) | (0.01% | ) | (0.01% | ) | ||||||||||||||

|

Allowance for loan losses |

$ | 37,423 | 35,913 | 38,695 | 37,967 | 35,572 | 37,423 | 35,572 | ||||||||||||||||||||

|

Allowance to loans |

1.13 | % | 1.11 | % | 1.15 | % | 1.19 | % | 1.06 | % | 1.13 | % | 1.06 | % | ||||||||||||||

|

Allowance to loans excluding PPP loans |

1.17 | % | 1.20 | % | 1.33 | % | 1.33 | % | 1.27 | % | 1.17 | % | 1.27 | % | ||||||||||||||

|

Nonperforming loans |

$ | 2,766 | 2,746 | 2,793 | 3,384 | 4,141 | 2,766 | 4,141 | ||||||||||||||||||||

|

Other real estate/repossessed assets |

$ | 111 | 404 | 374 | 701 | 512 | 111 | 512 | ||||||||||||||||||||

|

Nonperforming loans to total loans |

0.08 | % | 0.08 | % | 0.08 | % | 0.11 | % | 0.12 | % | 0.08 | % | 0.12 | % | ||||||||||||||

|

Nonperforming assets to total assets |

0.06 | % | 0.07 | % | 0.07 | % | 0.09 | % | 0.11 | % | 0.06 | % | 0.11 | % | ||||||||||||||

|

NONPERFORMING ASSETS - COMPOSITION |

||||||||||||||||||||||||||||

|

Residential real estate: |

||||||||||||||||||||||||||||

|

Land development |

$ | 33 | 34 | 34 | 35 | 36 | 33 | 36 | ||||||||||||||||||||

|

Construction |

$ | 0 | 0 | 0 | 0 | 198 | 0 | 198 | ||||||||||||||||||||

|

Owner occupied / rental |

$ | 2,063 | 2,137 | 2,305 | 2,607 | 2,597 | 2,063 | 2,597 | ||||||||||||||||||||

|

Commercial real estate: |

||||||||||||||||||||||||||||

|

Land development |

$ | 0 | 0 | 0 | 0 | 0 | 0 | 0 | ||||||||||||||||||||

|

Construction |

$ | 0 | 0 | 0 | 0 | 0 | 0 | 0 | ||||||||||||||||||||

|

Owner occupied |

$ | 100 | 363 | 646 | 1,232 | 1,576 | 100 | 1,576 | ||||||||||||||||||||

|

Non-owner occupied |

$ | 0 | 0 | 0 | 22 | 23 | 0 | 23 | ||||||||||||||||||||

|

Non-real estate: |

||||||||||||||||||||||||||||

|

Commercial assets |

$ | 673 | 606 | 169 | 172 | 198 | 673 | 198 | ||||||||||||||||||||

|

Consumer assets |

$ | 8 | 10 | 13 | 17 | 25 | 8 | 25 | ||||||||||||||||||||

|

Total nonperforming assets |

2,877 | 3,150 | 3,167 | 4,085 | 4,653 | 2,877 | 4,653 | |||||||||||||||||||||

|

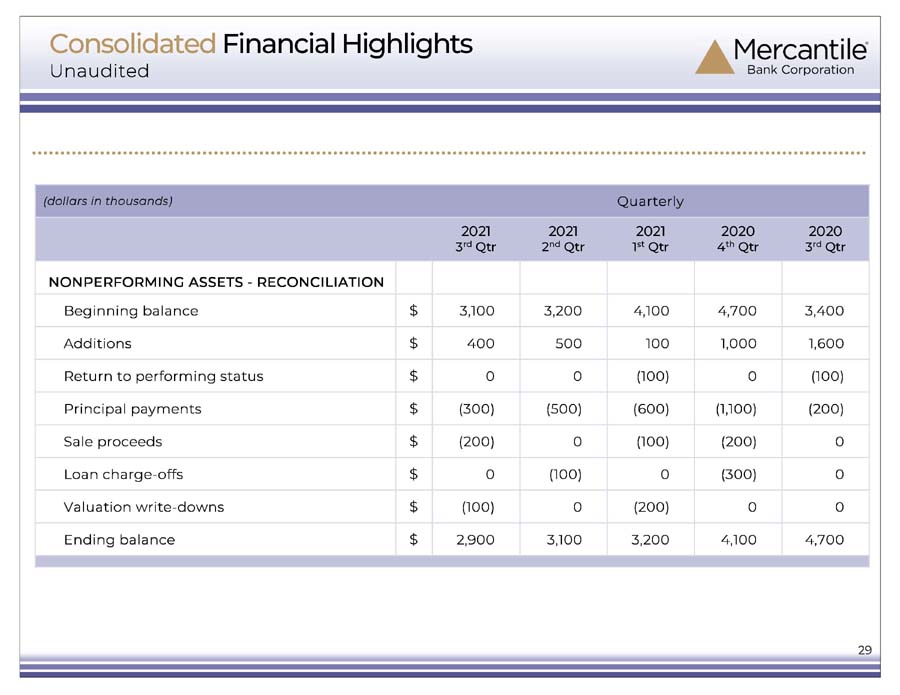

NONPERFORMING ASSETS - RECON |

||||||||||||||||||||||||||||

|

Beginning balance |

$ | 3,150 | 3,167 | 4,085 | 4,653 | 3,410 | 4,085 | 2,736 | ||||||||||||||||||||

|

Additions |

$ | 361 | 522 | 116 | 972 | 1,615 | 999 | 3,148 | ||||||||||||||||||||

|

Return to performing status |

$ | (50 | ) | 0 | (115 | ) | 0 | (72 | ) | (165 | ) | (105 | ) | |||||||||||||||

|

Principal payments |

$ | (291 | ) | (484 | ) | (559 | ) | (1,064 | ) | (249 | ) | (1,334 | ) | (637 | ) | |||||||||||||

|

Sale proceeds |

$ | (209 | ) | 0 | (77 | ) | (245 | ) | 0 | (286 | ) | (241 | ) | |||||||||||||||

|

Loan charge-offs |

$ | 0 | (55 | ) | (33 | ) | (231 | ) | (51 | ) | (88 | ) | (224 | ) | ||||||||||||||

|

Valuation write-downs |

$ | (84 | ) | 0 | (250 | ) | 0 | 0 | (334 | ) | (24 | ) | ||||||||||||||||

|

Ending balance |

$ | 2,877 | 3,150 | 3,167 | 4,085 | 4,653 | 2,877 | 4,653 | ||||||||||||||||||||

|

LOAN PORTFOLIO COMPOSITION |

||||||||||||||||||||||||||||

|

Commercial: |

||||||||||||||||||||||||||||

|

Commercial & industrial |

$ | 1,074,394 | 1,103,807 | 1,284,507 | 1,145,423 | 1,321,419 | 1,074,394 | 1,321,419 | ||||||||||||||||||||

|

Land development & construction |

$ | 38,380 | 43,111 | 58,738 | 55,055 | 50,941 | 38,380 | 50,941 | ||||||||||||||||||||

|

Owner occupied comm'l R/E |

$ | 551,762 | 550,504 | 544,342 | 529,953 | 549,364 | 551,762 | 549,364 | ||||||||||||||||||||

|

Non-owner occupied comm'l R/E |

$ | 998,697 | 950,993 | 932,334 | 917,436 | 878,897 | 998,697 | 878,897 | ||||||||||||||||||||

|

Multi-family & residential rental |

$ | 179,126 | 161,894 | 147,294 | 146,095 | 137,740 | 179,126 | 137,740 | ||||||||||||||||||||

|

Total commercial |

$ | 2,842,359 | 2,810,309 | 2,967,215 | 2,793,962 | 2,938,361 | 2,842,359 | 2,938,361 | ||||||||||||||||||||

|

Retail: |

||||||||||||||||||||||||||||

|

1-4 family mortgages |

$ | 411,618 | 380,292 | 337,844 | 337,888 | 322,118 | 411,618 | 322,118 | ||||||||||||||||||||

|

Home equity & other consumer |

$ | 59,732 | 58,240 | 59,311 | 61,620 | 63,723 | 59,732 | 63,723 | ||||||||||||||||||||

|

Total retail |

$ | 471,350 | 438,532 | 397,155 | 399,508 | 385,841 | 471,350 | 385,841 | ||||||||||||||||||||

|

Total loans |

$ | 3,313,709 | 3,248,841 | 3,364,370 | 3,193,470 | 3,324,202 | 3,313,709 | 3,324,202 | ||||||||||||||||||||

|

END OF PERIOD BALANCES |

||||||||||||||||||||||||||||

|

Loans |

$ | 3,313,709 | 3,248,841 | 3,364,370 | 3,193,470 | 3,324,202 | 3,313,709 | 3,324,202 | ||||||||||||||||||||

|

Securities |

$ | 577,566 | 524,127 | 452,259 | 405,349 | 330,426 | 577,566 | 330,426 | ||||||||||||||||||||

|

Other interest-earning assets |

$ | 741,557 | 683,638 | 596,855 | 563,174 | 495,308 | 741,557 | 495,308 | ||||||||||||||||||||

|

Total earning assets (before allowance) |

$ | 4,632,832 | 4,456,606 | 4,413,484 | 4,161,993 | 4,149,936 | 4,632,832 | 4,149,936 | ||||||||||||||||||||

|

Total assets |

$ | 4,964,412 | 4,757,414 | 4,713,023 | 4,437,344 | 4,420,610 | 4,964,412 | 4,420,610 | ||||||||||||||||||||

|

Noninterest-bearing deposits |

$ | 1,647,380 | 1,620,829 | 1,605,471 | 1,433,403 | 1,449,879 | 1,647,380 | 1,449,879 | ||||||||||||||||||||

|

Interest-bearing deposits |

$ | 2,221,611 | 2,050,442 | 2,039,491 | 1,978,150 | 1,922,155 | 2,221,611 | 1,922,155 | ||||||||||||||||||||

|

Total deposits |

$ | 3,868,991 | 3,671,271 | 3,644,962 | 3,411,553 | 3,372,034 | 3,868,991 | 3,372,034 | ||||||||||||||||||||

|

Total borrowed funds |

$ | 619,441 | 613,205 | 584,672 | 562,360 | 600,892 | 619,441 | 600,892 | ||||||||||||||||||||

|

Total interest-bearing liabilities |

$ | 2,841,052 | 2,663,647 | 2,624,163 | 2,540,510 | 2,523,047 | 2,841,052 | 2,523,047 | ||||||||||||||||||||

|

Shareholders' equity |

$ | 452,278 | 451,888 | 441,243 | 441,554 | 431,900 | 452,278 | 431,900 | ||||||||||||||||||||

|

AVERAGE BALANCES |

||||||||||||||||||||||||||||

|

Loans |

$ | 3,276,863 | 3,365,686 | 3,318,281 | 3,268,866 | 3,292,025 | 3,308,119 | 3,132,885 | ||||||||||||||||||||

|

Securities |

$ | 547,336 | 483,805 | 419,514 | 365,631 | 327,668 | 484,020 | 335,443 | ||||||||||||||||||||

|

Other interest-earning assets |

$ | 733,801 | 619,358 | 591,617 | 559,593 | 457,598 | 648,780 | 288,310 | ||||||||||||||||||||

|

Total earning assets (before allowance) |

$ | 4,558,000 | 4,468,849 | 4,329,412 | 4,194,090 | 4,077,291 | 4,440,919 | 3,756,638 | ||||||||||||||||||||

|

Total assets |

$ | 4,856,611 | 4,752,858 | 4,578,887 | 4,459,370 | 4,346,624 | 4,730,482 | 4,024,175 | ||||||||||||||||||||

|

Noninterest-bearing deposits |

$ | 1,641,158 | 1,619,976 | 1,510,334 | 1,478,616 | 1,454,887 | 1,590,969 | 1,228,729 | ||||||||||||||||||||

|

Interest-bearing deposits |

$ | 2,125,920 | 2,074,759 | 2,026,896 | 1,936,069 | 1,863,302 | 2,076,221 | 1,785,391 | ||||||||||||||||||||

|

Total deposits |

$ | 3,767,078 | 3,694,735 | 3,537,230 | 3,414,685 | 3,318,189 | 3,667,190 | 3,014,120 | ||||||||||||||||||||

|

Total borrowed funds |

$ | 614,061 | 594,199 | 576,645 | 588,100 | 583,994 | 595,105 | 569,729 | ||||||||||||||||||||

|

Total interest-bearing liabilities |

$ | 2,739,981 | 2,668,958 | 2,603,541 | 2,524,169 | 2,447,296 | 2,671,326 | 2,355,120 | ||||||||||||||||||||

|

Shareholders' equity |

$ | 455,902 | 445,930 | 443,548 | 438,171 | 429,865 | 448,516 | 423,924 | ||||||||||||||||||||