| Home | Previous Page | ||

|

||||||||||||||||

|

||||||||||||||||

|

|

Securities and Exchange Commission Investor Advisory CommitteeDraft Minutes of October 9, 2014 MeetingThe Investor Advisory Committee (IAC) met on October 9, 2014 in a public meeting that was transmitted live by webcast. The meeting convened at 10:00 a.m. in the multipurpose room of the Securities and Exchange Commission’s headquarters in Washington, D.C. The following persons attended the meeting: Commissioners of the Securities and Exchange Commission

Advisory Committee Members[1]

Staff of the Securities and Exchange Commission

MORNING SESSIONMr. Schacht opened the meeting and welcomed Ms. Peirce as the Committee’s newest member. Chair White offered an update on the Commission’s rulemaking agenda.[2] Since the Committee’s previous meeting in July, she noted, the Commission had adopted three sets of rulemakings: reforms involving money market funds, major changes to the registered asset-backed security disclosure regime, and completion of more than a dozen Dodd-Frank Act mandates related to conflict of interest and governance of credit rating agencies. Looking ahead, Chair White said that the Commission would focus in particular on rules to implement Dodd-Frank mandates concerning executive compensation and OTC derivatives. In addition, she said that the Commission would move forward in the near term on Regulation SCI to strengthen the resiliency of critical market systems. Turning to the disclosure effectiveness project, the Chair said that the Division of Corporation Finance was working to develop specific recommendations to update the disclosure requirements for companies. Chair White took note of three recent Commission staff appointments, including that of Tracey McNeil to the position of SEC Ombudsman within the Office of the Investor Advocate. The Chair then provided an update on the status on the Committee’s pending recommendations:

The other Commissioners gave brief opening remarks and welcomed Ms. Peirce. July 10, 2014, Meeting Minutes Approval Mr. Carcello asked that the minutes of the July meeting be amended to reflect that Mr. Glassman had attended the meeting. The Committee approved the amendment without objection. Consideration of Joint Recommendations of the Investor as Purchaser and the Investor Education Subcommittees Regarding the Accredited Investor Definition Ms. Roper and Mr. Ganser presented the joint recommendations: Recommendation As the Commission conducts its review of the accredited investor definition, as mandated by the Dodd-Frank Wall Street Reform and Consumer Protection Act, it should seek to determine whether the current definition achieves the goal of identifying a class of individuals who do not need the ’33 Act protections in order to be able to make an informed investment decision and protect their own interests. The Committee does not believe that the current definition as it pertains to natural persons effectively serves this function in all instances. We therefore encourage the Commission to consider alternative approaches that would better protect vulnerable investors without unnecessarily constraining the supply of capital in the private offering market, including approaches that would enable individuals to qualify as accredited investors based on their financial sophistication, consideration of whether financial thresholds need to be adjusted for inflation, as well as alternative approaches to setting financial thresholds. Finally, the Committee believes that protections for non-accredited investors who rely on recommendations from purchaser representatives to qualify as sophisticated should be strengthened. Recommendation 1 The Commission should carefully evaluate whether the accredited investor definition, as it pertains to natural persons, is effective in identifying a class of individuals who do not need the protections afforded by the ’33 Act. If, as the Committee expects, a closer analysis reveals that a significant percentage of individuals who currently qualify as accredited investors are not in fact capable of protecting their own interests, the Commission should promptly initiate rulemaking to revise the definition to better achieve its intended goal. Recommendation 2 The Commission should revise the definition to enable individuals to qualify as accredited investors based on their financial sophistication. Recommendation 3 If the Commission chooses to continue with an approach that relies exclusively or mainly on financial thresholds, the Commission should consider alternative approaches to setting such thresholds – in particular limiting investments in private offerings to a percentage of assets or income – which could better protect investors without unnecessarily shrinking the pool of accredited investors. Recommendation 4 The Commission should take concrete steps encourage development of an alternative means of verifying accredited investor status that shifts the burden away from issuers who may, in some cases, be poorly equipped to conduct that verification, particularly if the accredited investor definition is made more complex. While bar association membership does not provide the same type of regulatory oversight that exists for brokers and investment advisers, through the SEC and state securities regulators, or accountants, through the PCAOB, it does provide for a level of professional accountability. Recommendation 5 In addition to any changes to the accredited investor standard, the Commission should strengthen the protections that apply when non-accredited individuals, who do not otherwise meet the sophistication test for such investors, qualify to invest solely by virtue of relying on advice from a purchaser representative. Specifically, the Committee recommends that in such circumstances the Commission prohibit individuals who are acting as purchaser representatives in a professional capacity from having any personal financial stake in the investment being recommended, prohibit such purchaser representatives from accepting direct or indirect compensation or payment from the issuer, and require purchaser representatives who are compensated by the purchaser to accept a fiduciary duty to act in the best interests of the purchaser. Ms. Peirce began by expressing thanks for the opportunity to join the Committee. Turning to the recommendation, she argued that it fell short by assuming that people’s capabilities should trump their individual determinations about how they want to invest. She urged the Committee to think in broader terms and to consider, not only protecting investors from fraud, but also protecting their ability to invest. Other members argued that the recommendation struck a careful balance. Following discussion, the Committee voted to pass the recommendation by a vote of 15 to one. Consideration of the Recommendations of the Investor as Owner Subcommittee on Impartiality in the Disclosure of Preliminary Voting Results Mr. Silvers presented the recommendations: Recommendation 1 That the staff of the Commission take the steps necessary to ensure that the exemption in Rule 14a-2(a)(1) is conditioned upon the broker (and any intermediary designated by the broker) acting in an impartial and ministerial fashion throughout the proxy process, including the disclosure of preliminary voting information. Recommendation 2 That the staff of the Commission take the position that any broker relying on the exemption from the proxy rules in Rule 14a-2(a)(1) that uses an intermediary to fulfill the requirements of impartiality under Rule 14a-2(a)(1) take reasonable steps to verify, based upon all the relevant facts and circumstances, that the intermediary will act in an impartial fashion and is not subject to impermissible conflicts of interest that impair the ability of the intermediary to act in an impartial manner. Ms. Peirce argued that the recommendation would impose a new obligation on brokers, and she questioned what costs would be involved. Mr. Silvers and Mr. Kanzer maintained that brokers are already subject to the obligation to ensure impartiality. The Committee voted to adopt the recommendation by a vote of 15 to one. Discussion of Possible Recommendations of the Market Structure Subcommittee on the Settlement Cycle Mr. Wallman gave a summary of issues involved in moving from the current T+3 settlement cycle for U.S. equities to a T+2 settlement cycle. He asserted that the current three-day settlement cycle poses significant systemic risks to the financial system. Mr. Wallman then introduced three guest speakers representing the Depository Trust & Clearing Corporation (DTCC): Bari Jane Wolfe, Managing Director, Head of Regulatory Relations; John Abel, Vice President, Settlement and Asset Services; and Brian Werstler, Director, Government Relations. Mr. Abel walked the Committee through the current three-day post-trade clearing and settlement process, which ends with the exchange of cash and securities. He explained the differences in the processing of retail and institutional investor trades. Mr. Abel also described current industry efforts to consider changing the settlement cycle from T+3 to T+2. Mr. Abel observed that most U.S. equities settle on a T+3 settlement cycle, while most U.S. mutual funds and fixed income securities settle on a T+1 cycle. Mr. Wallman maintained that these differences can cause confusion among retail investors. He argued that a shorter settlement cycle and greater harmonization would reduce confusion and benefit retail investors. Mr. Holmes voiced his support for a shortened settlement cycle. Ms. Bradbury observed that the subcommittee was still considering what form a recommendation should take – whether it should call on the Commission to adopt a new rule, provide new guidance, or use other means to encourage the industry to hasten adoption of a shortened time cycle. Commissioner Piwowar said that it would be helpful to quantify the risks in the current settlement cycle and to compare the costs and benefits of moving to T+2 versus T+1. Mr. Abel said that the Boston Consulting Group (BCG) had already released such a study. Mr. Schacht offered to obtain and re-circulate it to the Committee. RECESSThe Committee went into recess at 12:20 p.m. for a group photograph, followed by a lunch break and non-public subcommittee meetings. AFTERNOON SESSIONThe public meeting resumed at approximately 2:10 p.m. Commission Staff Briefing on Municipal Finance Bond Market Transparency Mr. Fleming introduced John J. Cross III, Director of the SEC Office of Municipal Securities, to provide a briefing on Commission activity on this topic. Mr. Cross began with a brief overview of the muni market, noting its predominately retail character. He elaborated on three short-term priorities of his office: a best execution obligation for dealers; a requirement for a mark-up disclosure on certain transactions executed around the same time; and pre-trade price transparency initiatives involving alternative trading systems. Commissioner Piwowar praised staff work on the municipal market as a highly effective use of Commission resources to help investors. He added that the area was ripe for comment from the Committee. Asked whether greater price transparency would lead to smaller spreads, Mr. Cross confirmed that price information disclosure affects market behavior. Mr. Silvers and Ms. Roper, while expressing their support for greater price transparency, recalled an argument about unintended consequences in the debate on tick sizes for small-cap stocks: namely, that smaller spreads reduce liquidity by making dealers more reluctant to make markets. Commissioner Piwowar suggested that similar concerns did not arise at this point in the municipal market because it would have far less transparency than that in equity markets, even if disclosure reforms are undertaken. Mr. Fleming asked whether standardization would be possible in municipal securities. Mr. Cross replied that doing so would improve the market by expanding the institutional base. He cautioned, however, that standardization efforts with municipal securities would encounter exponentially greater challenges than such efforts with corporate debt. Discussion with Outside Legal Experts of Issuer Adoption of Fee-Shifting Bylaws for Intra-Corporate Litigation Mr. Schacht introduced Professors John C. Coffee Jr. of Columbia University Law School and Larry Hamermesh of Widener University School of Law to discuss a new development in which corporations adopt fee-shifting bylaw and charter provisions. The professors’ submitted testimonies are attached as an appendix to these minutes. Mr. Hamermesh described how the new provisions shift the corporation’s costs and expenses in shareholder litigation to the plaintiff shareholder if the latter is less than completely successful. The provisions can apply not only to current or prior stockholders, but also to anyone who offers substantial assistance in pursuit of the claim. Mr. Coffee described these new provisions as an unnoticed and silent revolution with ominous implications. He urged the Commission to respond, and he proposed several specific ways in which it could do so. Several Committee members expressed concerns over the implications of the fee-shifting provisions. Ms. Peirce, meanwhile, expressed concerns over certain of Professor Coffee’s proposals for Commission action. The discussion ended with Mr. Schacht suggesting that the issues would continue to be discussed at the IAC subcommittee level. Subcommittee Reports/Discussion The chairs of the subcommittees reported on the non-public discussions each group had held preceding the afternoon session. Barbara Roper, chair of the Investor as Purchaser Subcommittee, reported that the group had started to discuss two issues that it will take up next: municipal securities, and ways to make retail investor disclosures more effective. Mr. Wallman, chairman of the Market Structure Subcommittee, said that the group would present the full Committee with a recommendation on shortening settlement cycles. In addition, he said that the subcommittee was considering issues involving fixed income and municipal securities, as well as interaction with the SEC Market Structure Advisory Committee that was being formed. Ann Yerger, acting chair of the Investor as Owner Subcommittee, reported that the group received two briefings. First, Commission staff from several divisions gave a presentation on structured data. Second, a representative of the U.S. Chamber of Commerce’s Center for Capital Markets Competitiveness described its report, “Corporate Disclosure Effectiveness.” Mr. Ganser, chairman of the Investor Education Subcommittee, said that the group had continued its discussion on uniform multi-agency messaging regarding elder fraud. He said that the group also had explored ideas for funding investor education. CLOSINGThe meeting was adjourned at 3:41 p.m. Appendix One: Testimony Submitted by Professor Larry Hamermesh of Widener University School of Law

Appendix TwoTestimony of Professor John C. Coffee Jr., Adolf A. Berle Professor of Law, Columbia University Law School And Director of its Center on Corporate Governance Before SEC Investor Advisory Committee, Securities and Exchange Commission, Washington, D.C. October 9, 2014

“Fee-Shifting Bylaws: Can They Apply in Federal Court?— The Case For Preemption”

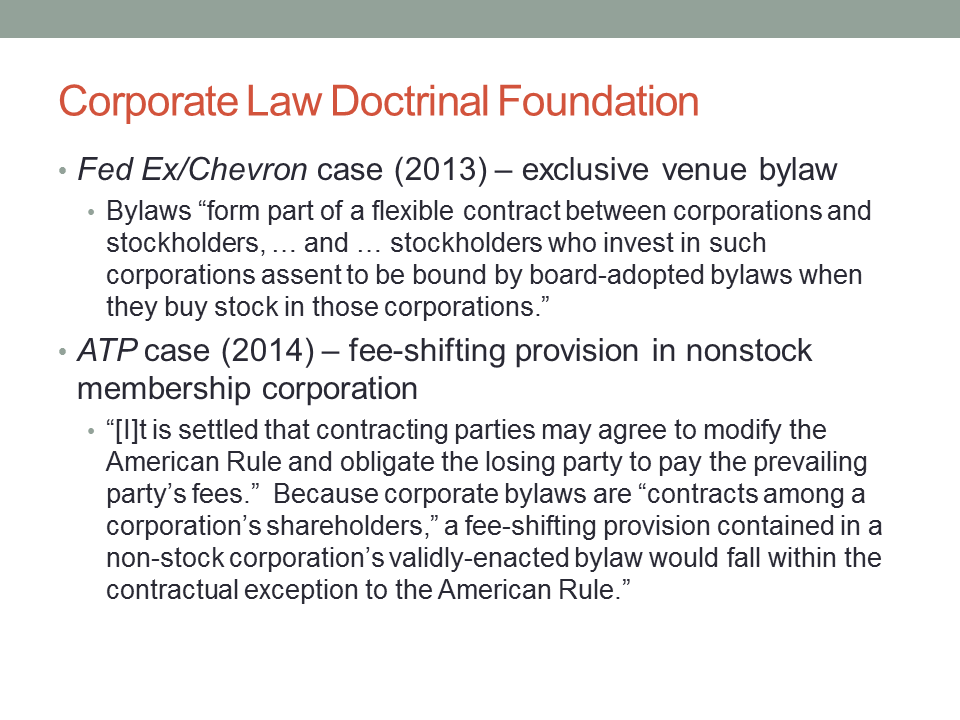

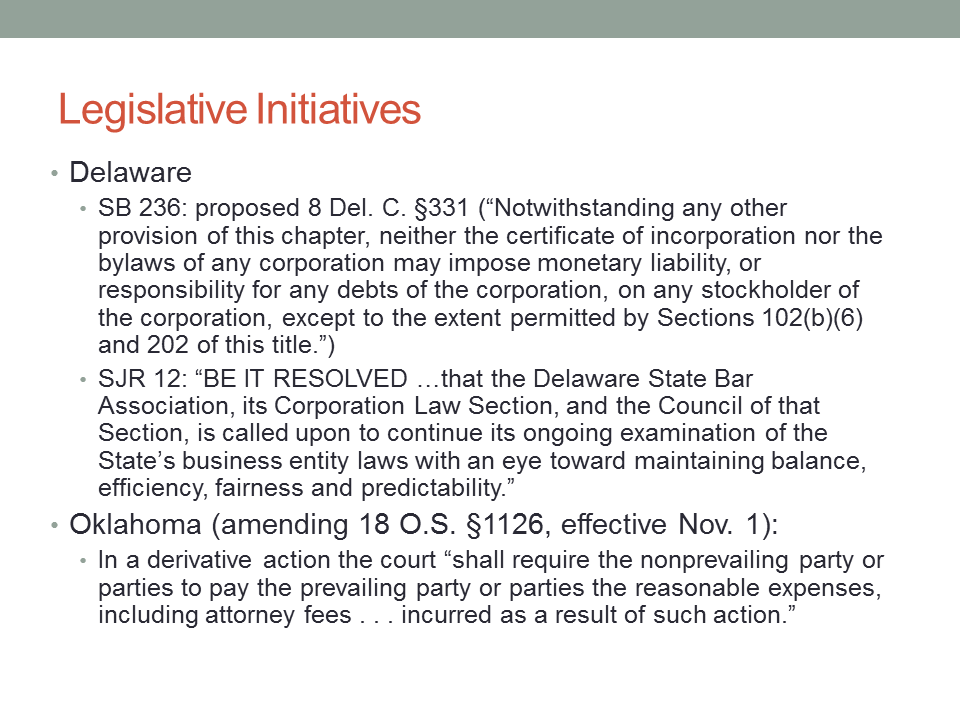

Beginning this year, a number of public corporations (including the recent Alibaba IPO) have adopted bylaws or charter provisions that shift the corporation’s costs and expenses in shareholder litigation to the plaintiff shareholder if the latter is unsuccessful (or, in some cases, is less than completely successful[i]). In effect, this is a one-way “loser pays” rule imposed by a board-adopted bylaw. These new bylaws derive from a 2014 decision of the Delaware Supreme Court, ATP Tour, Inc. v. Deutscher Tennis Bund,[ii] which found a particularly sweeping bylaw adopted by a Delaware non-stock corporation to be “facially valid.” That decision makes clear that a fee-shifting bylaw can be enforceable under Delaware law and applicable to shareholders who acquired their shares both before and after the bylaw was adopted, but it further noted that a legally permissible bylaw that is adopted for an “improper purpose” will be unenforceable in equity. This limitation is an application of the familiar Delaware rule, first stated in Schnell v. Chris-Craft Industries,[iii] that powers legitimately possessed may not be used for an inequitable purpose. Although the number of companies adopting such a bylaw is still small (I have a list of 24 examples, all adopted since May, 2014), the trend is accelerating, and many more companies would be likely to follow their lead if doubts about the enforceability of such a bylaw can be resolved in its favor. So where does that leave us? The Delaware legislature may yet act to bar or limit fee-shifting bylaws.[iv] Delaware may be motivated to act by the very plausible fear that such bylaws will reduce the volume of litigation in Delaware courts and thereby adversely affect Delaware’s leading local industry (i.e., corporate litigation). But even if Delaware were to act, the issue would still not disappear, both because Delaware might only modestly limit the use of such bylaws and because corporations incorporated in other jurisdictions may adopt similar bylaws (and the prestige of the Delaware Supreme Court may lead other courts to accept its ruling, even if the Delaware legislature were to reverse or amend it). This brief memorandum will not attempt any brief-like statement of the complicated case law on preemption,[v] but will focus instead on the policy issues and the need for SEC action. As our starting point, the initial question is: when will the Delaware Chancery Court (in the absence of new legislation) find that a fee-shifting bylaw was adopted for an improper purpose? Here, a particularly relevant statement in ATP Tour, Inc. is that: “The intent to deter litigation, however is not invariably an improper purpose. Fee-shifting provisions, by their nature, deter litigation. Because the fee-shifting provisions are not per se invalid, an intent to deter litigation would not necessarily render the bylaw unenforceable in equity.” 91 A. 2d at 560. Although it is certainly conceivable that a bylaw adopted after a specific corporate transaction was initiated by the board (or even after a lawsuit challenging the transaction had been filed) could be seen as a self-interested and “improper” attempt by the board to immunize itself, it is far less likely that a fee-shifting bylaw adopted well in advance of the transaction would be similarly invalidated—at least by Delaware courts. To be sure, the Delaware Supreme Court did not need to address these questions because the ATP Tour case came to it as a certified question from another court, and it properly limited itself to questions of law. Nonetheless, within Delaware and absent legislation, the message of ATP Tour seems clear: fee-shifting will be upheld unless evidence of bad faith or improper purpose can be shown.

But what is the status of such a board-adopted bylaw in federal court? Here, it is important to note that the ATP Tour case was in fact brought in federal court in Delaware. The plaintiff lost at trial,[vi] and the defendant moved for its costs pursuant to the bylaw. The District Court denied this motion, effectively ruling that federal law preempts the enforcement of fee-shifting agreements when antitrust claims are involved.[vii] But the Third Circuit reversed the District Court’s order, ruling that before addressing federal preemption issues, the District Court should have first determined whether the bylaw was enforceable under state law.[viii] In fact, the Third Circuit expressed skepticism that the bylaw was enforceable under Delaware law.[ix] On remand, the District Court certified this question of the bylaw’s enforceability under Delaware law to the Delaware Supreme Court. With that initial question now resolved, the focus now shifts back to the preemption issue. In general, federal courts have refused to enforce state law penalties intended to deter frivolous litigation. In a leading case, Burlington Northern Railroad Company v. Woods,[x] a tort action was removed by the defendant from Alabama state court to federal court, where the defendant lost at trial and then appealed, posting a mandatory bond to stay the judgment. On affirmance of the decision below, the Eleventh Circuit granted plaintiff’s motion for a mandatory penalty of 10% of the judgment amount, based on an Alabama statute that sought to deter frivolous appeals by imposing an automatic 10% penalty. The Supreme Court reversed, finding that the Alabama statute had no application to a case in federal court (even when removed to federal court based on diversity jurisdiction). Following its leading precedent of Hanna v. Plumer,[xi] the Supreme Court held that federal procedural rules applied in federal court. Further, it noted a conflict between the Federal Rules of Civil Procedure (which permit a court in its discretion to impose a penalty for a frivolous appeal) and the Alabama statute (which made the penalty mandatory, whether the appeal was frivolous or not). If we assume Burlington Northern to govern, the same conflict arguably exists between mandatory fee-shifting under a bylaw and the discretionary sanctions authorized for frivolous litigation by Federal Rule of Civil Procedure 11. Yet, other decisions have applied state law requirements that amount in substance to fee-shifting in federal court.[xii] In any event, before one concludes that federal law should preempt state law on this issue, one must focus on a critical difference between Burlington Northern and the case of a fee-shifting bylaw. Fee-shifting under ATP Tours is not based on a state statute, but on a contract. Indeed, the Delaware statute authorizing broad bylaws is no different from that of any other state jurisdiction. Rather, under standard “black letter” corporate law, bylaws set forth a contract among the shareholders. From this perspective, the fee-shifting bylaw is the same as an indemnification provision in which one party by contract agreed to pay the other’s legal expenses (at least under certain circumstances.) In fact, the ATP Tour decision emphasizes that contractual agreements are an exception to the usual American rule on fee-shifting (under which each side bears its own legal expenses) that Delaware normally follows. Hence, the Supreme Court’s standard position that federal procedural rules apply in federal court (and state procedural rules do not) might be sidestepped here if we view the bylaw as simply a contract among the parties. But again one cannot stop at this point either—for at least two reasons. First, federal courts have held that some contracts for indemnification are unenforceable because they conflict with the policies underlying specific federal statutes. The leading such decision is Globus v. Law Research Service, Inc.,[xiii] in which the Second Circuit denied indemnification to an underwriter who had knowledge of the misstatement because, it said, such indemnification would be contrary to the policies underlying the federal securities laws. Second, in Atlantic Marine Construction Co., Inc. v. United States District Court for the Western District of Texas,[xiv] the Supreme Court held in 2013 that contractual provisions among the parties do not supercede the Federal Rules of Civil Procedure but must be interpreted in a manner consistent with them. In Atlantic Marine, the parties had agreed to a forum-selection clause providing that all disputes would be litigated in Virginia. Yet, when a dispute arose, the plaintiff sued in Texas, and the defendant sought to have the case either dismissed or, in the alternative, transferred to federal court in Virginia. Both the district court and the Fifth Circuit refused to do either, ruling that 28 U.S.C. §1404(a) was the exclusive mechanism for enforcing a forum-selection clause. Both further concluded that the district court had to undertake a balancing-of-interests analysis. On appeal, the Supreme Court partially disagreed. Although it found that Section 1404 (and not the contract, itself) governed, it held that the District Court’s analysis improperly placed the burden on the defendant to prove that the requested transfer was appropriate. Instead, it said the burden was on the plaintiff, as the party “flouting” its contractual obligations, to show that public-interest factors overwhelmingly disfavored the requested transfer to Virginia: “Only under extraordinary circumstances unrelated to the convenience of the parties should a §1404(a) motion be denied.”[xv] Because there was no preemption issue in Atlantic Marine, its relevance is limited, but it does have two implications: (1) contracts governing litigation are not necessarily enforced as written but must be interpreted through the prism of the Federal Rules of Civil Procedure; and (2) public policy questions may retain some modest relevance, even when there is no federal statute involved. On this basis, a forum selection bylaw requiring federal securities class actions to be brought in a preferred federal forum (for example, federal district court in Delaware) is likely enforceable, but will have to be implemented by means of Section 1404. Atlantic Marine implies that fee shifting bylaws must at least be consistent with the Federal Rules of Civil Procedure, and these rules address the award of attorneys fees in Rules 54(d)(2) and 23(h). Under Rule 54(d)(2)(C), the court must give a party “an opportunity for adversary submissions on the motion in accordance with Rule 43(a) or 78” and the court “must find the facts and state its conclusions of law as provided in Rule 52(a).” Under Rule 23(h), the court must hold a hearing and any class member may object to the motion. These restrictions are minimal, but they do provide a hearing at which the SEC could appear.

To ask this question is not to answer it. The specific bylaw needs to be considered to determine the extent of the burden. Most bylaws will presumably require a losing shareholder who sued the company unsuccessfully to pay indemnification, but some go even further and require the plaintiff to be completely successful (or face fee-shifting).[xvi] Most (if not all) such bylaws will not pay the successful plaintiff’s fees or expenses.[xvii] Such bylaws thus have two key faults: (1) they are one-sided in that they reimburse successful defendants, but not successful plaintiffs (thus, they are unlike the English Rule which shifts fees both ways evenly); and (2) they require fee-shifting even in cases that were reasonable or even meritorious (but lost on a technical legal defense or possibly were largely, but not entirely, successful). These deficiencies may not seem as egregious as indemnifying a knowingly culpable defendant (which was the fact pattern in Globus), but they may do more to deter and chill private enforcement of law. Inherently, defendants’ fees and expenses will often exceed plaintiffs’ expected fee award (in part because there tend to be multiple counsel representing the various defendants), and thus plaintiffs’ attorneys must accept a potential liability greater than their potential gain. Since at least J. I. Case Co. v. Borak,[xviii] federal decisions and the SEC have asserted that private enforcement of law is a “necessary supplement” to public enforcement by the SEC and the Department of Justice.[xix] Although the Supreme Court’s attitude may be less certain on this point today and clearly it will no longer imply a federal private cause of action, absent clear legislative direction, the Court has still shown itself unwilling to dismantle Rule 10b-5 class actions.[xx] The SEC has not formally retreated from its support for private enforcement, but this issue will put its resolve to the test. The case for preemption of fee-shifting bylaws is further strengthened in the context of the federal securities laws because Congress has struck a special balance in this area. This balance recognizes that fee-shifting against the losing side may be appropriate, but requires judicial oversight. Under Section 21D(c)(3) of the Securities Exchange Act of 1934 (which provision was added by the Private Securities Litigation Reform Act of 1995), a presumption in favor of fee-shifting is created if any motion or pleading fails to comply with Rule 11(b) of the Federal Rules of Civil Procedure. This approach is two-sided and equally punitive to both sides in making full fee-shifting (rather than a lesser financial sanction) the presumptive penalty. Because this approach is tougher and more punitive than the normal approach under Rule 11 of the Federal Rules (which would typically involve lesser financial sanctions), it represents a carefully focused federal policy that is in sharp conflict with automatic and one-sided fee-shifting without any role for judicial discretion. Effectively, bylaws can turn a Congressionally-mandated system of two-sided fee shifting that is dependent on judicial discretion into an automatic system of one-way fee-shifting. Bottom Line: Although there may be a case for preemption of fee-shifting bylaws in many contexts, this case is stronger in the case of securities litigation.

The SEC could take a number of steps, all consistent with past practice. First, the SEC could assert the case for preemption selectively as an amicus curiae in cases where no violation of Rule 11 seemed present. This will require some careful case analysis by the SEC and should not be an automatic response. Alternatively, the SEC could assert that automatic fee-shifting is always in violation of the Securities Exchange Act, unless it is predicated on a judicial finding that Rule 11 was violated. This would be more controversial and it might involve the SEC seeking to defend a less-than-attractive plaintiff’s attorney. Second, the SEC has in a closely related area refused to accelerate registration statements where the company’s certificate of incorporation or bylaws contained a mandatory arbitration clause. This threat seems to have been effective.[xxi] Yet, the SEC has not held up registration statements with fee-shifting provisions. This is inconsistent. Functionally, the two cases are equivalent, because both provisions effectively bar private enforcement. Third, the SEC could require registrants to state in their registration statements that they understand that the SEC believes that the federal securities laws are inconsistent with fee-shifting bylaws. Such a statement is already specified in Forms S-1 and S-3 with respect to indemnification provisions.[xxii] This at least imposes an embarrassment cost on the issuer and alerts courts to the SEC’s views without the need for an SEC amicus position. Finally, the SEC is uniquely positioned to gather relevant data. In assessing the impact of fee-shifting bylaws, it would be useful to know what the average costs are that defendant firms incur on such litigation and that they would seek to shift. The impact on the typical plaintiff’s firm could also be evaluated empirically. Similarly, the SEC could assess whether insurance could alleviate this problem (if it were available) and at what cost. Lastly, if Delaware were to impose partial curbs (permitting only some limited fee shifting), the SEC could assess the likely empirical impact of such a modified fee-shifting bylaw. Conclusion The impact of fee-shifting bylaws could be decisive. The defendant’s expenses in a securities class action can easily exceed $10 million, and this amount would bankrupt many smaller plaintiff’s law firms. It is questionable (and certainly unresolved) whether plaintiff’s law firms could obtain liability insurance to cover these amounts. Even if a bold plaintiff’s law firm did sue, it would likely have to agree to indemnify the class representative from fee-shifting, and some class representatives might decline the position, fearing that the plaintiff’s firm could not fully protect them. As the case proceeded, the defendant’s expenses will progressively mount, increasing the potential penalty. This will predictably force cheaper settlements, thereby injuring the class. If fee-shifting bylaws are upheld, defendant issuers should logically regard them as a riskless move that has little downside. Probably, proxy advisors would object to such board-adopted bylaws,[xxiii] but this is not the kind of board action that could easily fuel a proxy contest or be easily overturned by a shareholder vote.[xxiv] As a result, such bylaws, if upheld, will predictably become widely prevalent. Bottom Line: For the short-term, the ball is still in Delaware’s court while its legislature considers possible curbs. Although the SEC need not oppose all fee-shifting provisions adopted through board or shareholder action, it must be prepared to take on open-ended and more sweeping bylaws—or concede the decline of private enforcement. Final Thought: If Delaware does act to restrain fee-shifting through bylaws, the potential for a “race to the bottom” arises. Other states of a more conservative bent (consider, for example, Texas) might accept or even endorse fee-shifting bylaws. At this point, some corporate lawyers will predictably advise their clients to reincorporate in Texas, and many IPO issuers might prefer to incorporate in Texas initially. Even if small changes in corporate law will not produce a migration into or away from Delaware, this difference is a major one because it protects corporate managers and directors from potential personal liability. In this light, an SEC announcement that it will challenge fee-shifting bylaws would chill interstate charter competition over protective bylaws (and might even be welcomed in Delaware). [1] James Glassman, Joseph Grundfest, Eugene Duffy, Roy Katzovicz, and Anne Sheehan did not attend the meeting.

[2] A copy of Chair White’s remarks are available at http://www.sec.gov/News/PublicStmt/Detail/PublicStmt/1370543132802.

[3] Subsequently, on Nov. 7, 2014, the Commission opened the public comment period, with comments due on December 22.

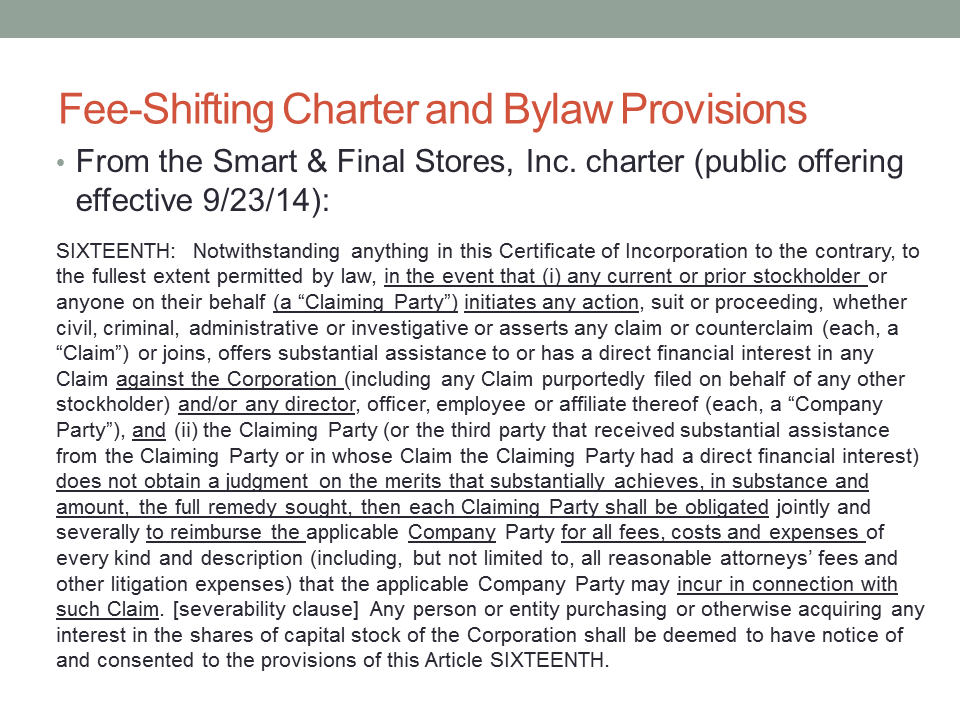

Endnotes [i] For an example of how sweeping some of the bylaws can be, see Article Sixteenth of the Second Amended and Restated Certificate of Incorporation of Smart & Final Stores, Inc. (available at http://www.sec.gov/Archives/edgar/data/1563407/000104746914007436/a2221270zex-3_1.htm). The company is a West Coast food and supply chain, which is incorporated in Delaware. Article Sixteenth reads as follows: Notwithstanding anything in this Certificate of Incorporation to the contrary, to the fullest extent permitted by law, in the event that (i) any current or prior stockholder or anyone on their behalf (a “Claiming Party”) initiates any action, suit or proceeding, whether civil, criminal, administrative, or investigative, or asserts any claim or counterclaim (each, a “Claim”) or joins, offers substantial assistance to or has a direct financial interest in any Claim against the Corporation (including any Claim purportedly filed on behalf of any other stockholder) and/or any director, officer, employee or affiliate thereof (each, a “Company Party”), and (ii) the Claiming Party (or the third party that received substantial assistance from the Claiming Party or in whose Claim the Claiming Party had a direct financial interest) does not obtain a judgment on the merits that substantially achieves, in substance and amount, the full remedy sought, then each Claiming Party shall be obligated jointly and severally to reimburse the applicable Company Party for all fees, costs, and expenses of every kind and description (including, but not limited to, all reasonable attorneys’ fees and other litigation expenses) that the applicable Company Party may incur in connection with such Claim. If any provision (or any part thereof) of this Article SIXTEENTH shall be held to be invalid, illegal or unenforceable facially or as applied to any circumstance for any reason whatsoever: (1) the validity, legality and enforceability of such provision (or part thereof) in any other circumstance and of the remaining provisions of this Article SIXTEENTH (including, without limitation, each portion of any subsection of this Article SIXTEENTH containing any such provision (or part thereof) held to be invalid, illegal or unenforceable that is not itself held to be invalid, illegal or unenforceable) shall not in any way be affected or impaired thereby, and (2) to the fullest extent permitted by law, the provisions of this Article SIXTEENTH (including, without limitation, each such portion containing any such provisions (or part thereof) held to be invalid, illegal or unenforceable) shall be construed for the benefit of the Corporation to the fullest extent permitted by law so as to (a) give effect to the intent manifested by the provision (or part thereof) held invalid, illegal, or unenforceable, and (b) permit the Corporation to protect its directors, officers, employees and agents from personal liability in respect of their good faith service. Any person or entity purchasing or otherwise acquiring any interest in the shares of capital stock of the Corporation shall be deemed to have notice of and consented to the provisions of this Article SIXTEENTH. Obviously, this provision goes beyond a “loser pays” rule and is in effect “a-less-than-100%-successful-plaintiff-pays” rule. For the Alibaba example, see Section 173 (“Claims Against the Corporation”) of the Amended and Restated Memorandum and Articles of Association of Alibaba Group Holding limited, which is incorporated in the Cayman Islands (available at http://www.sec.gov/Archives/edgar/data/1577552/000119312514333674/d709111dex32.htm). [ii] 91 A. 3d 554 (2014). This decision is fully consistent with other recent Delaware decisions upholding board-adopted bylaws containing forum selection clauses requiring intracorporate litigation to be brought in Delaware. See Boilermakers Local 154 Retirement Fund v. Chevron Corp., 73 A. 3d 934 (2013) and City of Providence v. First Citizens Bankshares, Inc., 2014 Del. Ch. LEXIS 168 (Del. Ch. Sept. 8, 2014). State court decisions in Louisiana, New York, Illinois and elsewhere have recently upheld and enforced Delaware forum selection clauses [iii] 285 A. 2d 437 (Del. 1971). [iv] I will defer to Professor Lawrence A. Hamermesh with regard to this topic of pending developments in Delaware. However, it should be noted that, shortly after the ATP Tour decision, the Corporation Law Section of the Delaware State Bar Association proposed in mid-2014 an amendment to the Delaware General Corporation Law that would deny Delaware corporations the authority to adopt fee-shifting bylaws. For a time, this provision seemed headed for adoption, but then the process slowed as corporate lobbyists appeared on the scene. This lobbying battle poses a unique and still unresolved conflict between the interests of Delaware corporations and those of the Delaware Bar. [v] Nonetheless, it is relevant to observe that a number of cases have addressed the issue of federal preemption in connection with deciding whether state anti-takeover statutes were in conflict with the goals of the Williams Act (i.e., Sections 13 and 14(d),(e), and (f) of the Securities Exchange Act of 1934). The most popular standard adopted in these cases has been the “meaningful opportunity for success” test. See, e.g., City Capital Associates v. Interco, Inc., 696 F. Supp. 1551 (D. Del. 1988); West Point-Pepperell, Inc. v. Farley, Inc., 711 F. Supp. 1096, 1102 (N.D. Ga. 1989); RP Acquisition Corp. v. Staley Cont’l, Inc., 686 F. Supp. 476, 482 (D. Del. 1988); BNS Inc. v. Koppers Co., 683 F. Supp. 458, 469 (D. Del 1988). If this standard were to govern, it would not preempt all fee-shifting bylaws, but only those likely to impose an “undue burden” by precluding shareholder litigation. Bylaws that imposed a more modest sanction could be upheld. [vi] For the treatment of the substantive claims, see Deutscher Tennis Bund v. ATP Tour, Inc., 610 F. 3d 820 (3d Cir. 2010). [vii] See Deutscher Tennis Bund v. ATP Tour, Inc., 2009 U.S. Dist. LEXIS 97851, 2009 WL 3367041 at *4 (D. Del. Oct. 19, 2009). [viii] See Deutscher Tennis Bund v. ATP Tour, Inc., 480 Fed. Appx. 124, 126 (3d Cir. 2012). [ix] Id. at 127 (“Indeed, we have doubts that Delaware courts would conclude that Article 23.3 imposes a legally enforceable burden on Deutscher and Qatar.”). Apparently, it guessed wrong. [x] 480 U.S. 1 (1987). [xi] 380 U.S. 460 (1965). [xii] The case most favorable to enforcing a fee-shifting bylaw is probably Cohen v. Beneficial Industrial Loan Corp., 337 U.S. 541 (1949), which upheld the application of a state mandatory security-for-expense bond requirement in federal court. The Supreme Court concluded that this statute was not truly procedural because its real intent was to deter frivolous litigation, not regulate procedure. Such an argument could also be made for fee-shifting bylaws, which similarly levy costs against the losing plaintiff. But Cohen was enforcing a substantive state policy intended to regulate corporate governance (which is traditionally left to state law). In this sense, Cohen is easily distinguishable. First, Delaware has no substantive policy favoring fee-shifting (but rather generally follows the American Rule and leaves departures from that rule to private ordering at present). Second, while the security-for-expense bond in Cohen applied only to derivative actions (which are principally brought in state court), the fee-shifting bylaw here at issue will apply to federal securities class actions (which cannot be brought in state court, at least in the case of Rule 10b-5, because federal courts have exclusive subject matter jurisdiction). Hence, it is arguable that Delaware lacks any legitimate interest in regulating actions that can exclusively be filed in federal court. [xiii] 418 F. 2d 1276 (2d Cir. 1969). Globus does not stand alone and has been widely followed. See, e.g., Heizer Corp. v. Ross, 601 F. 2d 330, 334 (7th Cir. 1979); DeHaas v. Empire Petroleum Co., 286 F. Supp. 809, 815 (D. Colo. 1968), aff’d in relevant part, 435 F. 2d 1223 (10th Cir. 1970). [xiv] 134 S. Ct. 568 (2013). [xv] 134 S. Ct. at 581. [xvi] For example, the actual bylaw in the ATP Tour case was even more sweeping (and was still upheld by the Delaware Supreme Court) in that it required the plaintiff to reimburse the other side’s expenses if it did “not obtain a judgment on the merits that substantially achieves, in substance in amount, the full remedy sought.” 91 A. 3d at 555. Wow! Plaintiffs rarely win on everything and so could achieve a 95% victory and still face fee-shifting. See also the bylaw set forth supra in Note 1. [xvii] The successful plaintiff’s attorney can seek a court-awarded fee from the class’s recovery, but under the American rule defendants are not usually liable for the plaintiff’s attorney fees, even if the facts were overwhelmingly in the plaintiff’s favor. Thus, the plaintiff’s fees comes from its successful clients’ recovery, not from the defendants. [xviii] 377 U.S. 426 (1964). [xix] Id at 432. [xx] See Halliburton Co. v. Erica P. John Fund, Inc., 134 S. Ct. 2398 (2014) (upholding “fraud on the market” doctrine). [xxi] In 2012, the Carlyle Group inserted a mandatory arbitration provision into its governance documents as it was preparing its IPO, but quickly dropped it under regulatory and investor pressure. See Note, In a Bind: Mandatory Arbitration Clauses in the Corporate Derivative Context, 28 Ohio St. J. on Disp. Resol. 737, 745 (2013). [xxii] See Form S-3 at Item 13 (“Disclosure for Securities Act Liabilities”). This Item requires the registrant to provide the information required by Item 510 of at Regulation S-K (17 C.F.R. 229.510), which requires the registrant (if indemnification is authorized) to state that it has “been informed that in the opinion of the Securities and Exchange Commission such indemnification is against public policy as expressed by the Act and is therefore unenforceable.” [xxiii] Indeed, Institutional Shareholder Services has also objected to board-adopted forum selection bylaws and supported an effort to repeal Chevron’s bylaw to this effect. [xxiv] Activists could seek passage of an advisory shareholder vote recommending the repeal of the bylaw, but such a vote (presumably pursuant to SEC Rule 14a-8) will likely have to be precatory only. See CA, Inc. v. AFSCME Employees Pension Plan, 953 A. 2d 227 (Del 2008) (holding that a bylaw mandating reimbursement of expenses in proxy contests must be subject to a “fiduciary out,” meaning that the board can refuse to accept the shareholders’ position). In administering Rule 14a-8, the SEC will generally permit issuers to exclude shareholder resolutions that are not simply precatory. With respect to the possibility of a proxy contest, the passage of a fee-shifting bylaw will hardly reduce the corporation’s value and thus will not make it a candidate for hedge fund activism (which usually is aimed at increasing share value over the short-term). No one else is likely to undertake the high costs of a proxy contest.

http://www.sec.gov/spotlight/investor-advisory-committee-2012/iac100914-minutes.htm

|