UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2017 | |

OR

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from______to_______ | |

Commission file number: 1-1169

THE TIMKEN COMPANY

(Exact name of registrant as specified in its charter)

Ohio | 34-0577130 | |

(State or other jurisdiction of | (I.R.S. Employer | |

incorporation or organization) | Identification No.) | |

4500 Mt. Pleasant St. NW, North Canton, Ohio | 44720-5450 | |

(Address of principal executive offices) | (Zip Code) | |

234.262.3000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Name of each exchange on which registered | |

Common Shares, without par value | New York Stock Exchange | |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes x No o

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | x | Accelerated filer | o | Non-accelerated filer | o | Smaller reporting company | o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes o No x

As of June 30, 2017, the aggregate market value of the registrant’s common shares held by non-affiliates of the registrant was $3,097,156,335 based on the closing sale price as reported on the New York Stock Exchange.

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of the latest practicable date.

Class | Outstanding at January 31, 2018 | |

Common Shares, without par value | 77,882,884 shares | |

DOCUMENTS INCORPORATED BY REFERENCE

Document | Parts Into Which Incorporated | |

Proxy Statement for the Annual Meeting of Shareholders to be held on or about May 8, 2018 (Proxy Statement) | Part III | |

THE TIMKEN COMPANY

INDEX TO FORM 10-K REPORT

PAGE | |||

I. | |||

Item 1. | |||

Item 1A. | |||

Item 1B. | |||

Item 2. | |||

Item 3. | |||

Item 4. | |||

Item 4A. | |||

II. | |||

Item 5. | |||

Item 6. | |||

Item 7. | |||

Item 7A. | |||

Item 8. | |||

Item 9. | |||

Item 9A. | |||

Item 9B. | |||

III. | |||

Item 10. | |||

Item 11. | |||

Item 12. | |||

Item 13. | |||

Item 14. | |||

IV. | |||

Item 15. | |||

PART I.

Item 1. Business

General:

As used herein, the term “Timken” or the “Company” refers to The Timken Company and its subsidiaries unless the context otherwise requires. Timken engineers, manufactures and markets bearings, transmissions, gearboxes, belts, chain, lubrication systems, couplings, industrial clutches and brakes, and related products and offers a spectrum of power system rebuild and repair services around the world. The Company’s growing product and services portfolio features many strong industrial brands, including Timken®, Fafnir®, Philadelphia Gear®, Drives®, Lovejoy® and Groeneveld®.

The Company was founded in 1899 by Henry Timken, who received two patents on the design of a tapered roller bearing. Timken later became, and continues to be, the world's largest manufacturer of tapered roller bearings, leveraging its expertise to develop a full portfolio of industry-leading products and services. Timken built its reputation as a global leader by applying its knowledge of metallurgy, friction management and mechanical power transmission to increase the reliability and efficiency of its customers' equipment across a diverse range of industries. Today, the Company's global footprint consists of 97 manufacturing facilities/service centers, 23 technology and engineering centers, and 41 distribution centers and warehouses, supported by a team comprised of more than 15,000 employees. Timken operates in 33 countries around the globe.

Industry Segments and Geographical Financial Information:

Information required by this Item is incorporated herein by reference to Note 16 - Segment Information.

Major Customers:

The Company sells products and services to a diverse customer base globally, including customers in the following market sectors: industrial distribution, general industrial original equipment, mining, construction, agriculture, rail, aerospace and defense, automotive, heavy truck, metals and energy. No single customer accounts for 5% or more of total net sales.

Products:

Timken manufactures and manages global supply chains for multiple product lines including anti-friction bearings and mechanical power transmission products designed to operate in demanding environments. The Company leverages its technical knowledge, research expertise, and production and engineering capabilities across all of its products and end markets to deliver high-performance products and services to its customers. Differentiation among these product lines is generally based on either product type or the targeted applications utilizing the product.

Engineered Bearings:

The Timken® bearing portfolio features a broad range of anti-friction bearing products, including tapered, spherical and cylindrical roller bearings; thrust and ball bearings; and housed units. Timken is a leading authority on tapered roller bearings, and leverages its position by applying engineering know-how and technology across its entire bearing portfolio.

A bearing is a mechanical device that reduces friction between moving parts. The purpose of a bearing is to carry a load while allowing a machine shaft to rotate freely. The basic elements of the bearing include two rings, called races; a set of rollers that rotate around the bearing raceway; and a cage to separate and guide the rolling elements. Bearings come in a number of designs, featuring tapered, spherical, cylindrical or ball rolling elements. The various bearing designs accommodate radial and/or thrust loads differently, making certain bearing types better suited for specific applications.

Selection and development of bearings for customer applications and demand for high reliability require sophisticated engineering and analytical techniques. High precision tolerances, proprietary internal geometries and quality materials provide Timken bearings with high load-carrying capacity, excellent friction-reducing qualities and long service lives. The uses for bearings are diverse and can be found in transportation applications that include passenger cars and trucks, heavy trucks, helicopters, airplanes and trains. Ranging in size from precision bearings the size of a pencil eraser to those roughly three meters in diameter, Timken components also are used in a wide variety of industrial applications: paper and steel mills, mining, oil and gas extraction and production, machine tools, gear drives, health and positioning control, wind turbines and food processing.

1

Tapered Roller Bearings. Timken tapered roller bearings can increase power density and can include customized geometries, engineered surfaces and specialized sealing solutions. The Company’s tapered roller bearing line comes in thousands of combinations in single-, double- and four-row configurations. Tapered roller designs permit ready absorption of both radial and axial load combinations, which makes them particularly well-adapted to reducing friction where shafts, gears or wheels are used.

Spherical and Cylindrical Roller Bearings. Timken also produces spherical and cylindrical roller bearings that are used in gear drives, rolling mills and other industrial and infrastructure development applications. These products are sold worldwide to original equipment manufacturers ("OEMs") and industrial distributors serving major end-market sectors, including construction and mining, natural resources, defense, pulp and paper production, rolling mills and general industrial goods.

Ball Bearings. Timken radial, angular and precision ball bearings are used by customers in a variety of market sectors, including aerospace, agriculture, construction, health, machine tool, the automotive aftermarket and general industries. Radial ball bearings are designed to tolerate relatively high-speed operation under a range of load conditions. These bearing types consist of an inner and outer ring with a cage containing a complement of precision balls. Angular contact ball bearings are designed for a combination of radial and axial loading. Precision ball bearings are manufactured to tight tolerances and come in miniature and instrument, thin section and ball screw support designs.

Housed Units. Timken markets among the broadest range of bearing housed units in the industry. These products deliver durable, heavy-duty components designed to protect spherical, tapered and ball bearings in debris-filled, contaminated or high-moisture environments. Common housed unit applications include material handling and processing equipment.

Mechanical Power Transmission:

Belts. Timken makes and markets a full line of Carlisle® belts used in industrial, commercial and consumer applications. The portfolio features more than 20,000 parts designed for demanding applications, which are sold to original equipment and aftermarket customers. Carlisle® belts are engineered for maximum performance and durability, with products available in wrap molded, raw edge, v-ribbed and synchronous belt designs. Common applications include agriculture, construction, industrial machinery, outdoor power equipment and powersports.

Chain. Timken manufactures precision Drives® roller chain, pintle chain, agricultural conveyor chain, engineering class chain and oil field roller chain. These highly engineered products are used in a wide range of mobile and industrial machinery applications, including agriculture, oil and gas, aggregate and mining, primary metals, forest products and other heavy industries. These products also are utilized in the food and beverage and packaged goods sectors, which often require high-end, specialty products, including stainless-steel and corrosion-resistant roller chain.

Couplings. The Company offers a full range of industrial couplings within its mechanical power transmission products portfolio. The Lovejoy brand is widely known for its flexible coupling design and as the creator of the jaw-style coupling. Lovejoy® couplings are available in curved jaw, jaw in-shear, s-flex, gear-torsional and disc style configurations. These components are used in a wide range of industries such as steel, pulp and paper, power generation, food processing, mining and construction. The Company also offers an extensive line of torsional couplings offered under the Torsional Control Products brand.

Lubrication Systems. The Company's Groeneveld® lubrication solutions include a wide variety of automatic lubrication delivery devices, oil management systems and safety support systems designed to enhance vehicle and machine uptime in on- and off-highway applications. These systems complement the Company's Interlube® line of lubrication systems, which are used by the commercial vehicle, mining, and heavy and general industries. Timken also offers 27 formulations of grease, leveraging its knowledge of tribology and anti-friction bearings to enable smooth equipment operation.

Aerospace Drive Systems. The Company's portfolio of parts, systems and services for the aerospace market sector includes products used in helicopters for military and commercial use. Timken designs, manufactures and tests a wide variety of power transmission and drive train components, including transmissions, gears and rotor-head assemblies and housings. In addition to original equipment, Timken provides aftermarket overhaul and repair services for transmissions, gearboxes and other components.

2

Industrial Gearboxes. The Company’s Philadelphia Gear® line of low- and high-speed gear drive designs are used in large-scale industrial applications. These gear drive configurations are custom made to meet user specifications, offering a wide-array of size, footprint and gear arrangements. Low-speed drives commonly are used in crushing and pulverizing equipment, cooling towers, conveyors and pumps. High-speed drives typically are used by power generation, oil and gas, marine and pipeline industries.

Industrial Clutches and Brakes. Timken offers a selection of engineered clutches, brakes, hydraulic power take-off units and other torque management devices marketed under the PT Tech brand. These products are custom engineered for original equipment manufacturers and used in mining, aggregate, wood recycling and metals industries.

Other Products. The Company also offers a full line of seals, augers and other mechanical power transmission components. Timken industrial sealing solutions come in a variety of types and material options that are used in manufacturing, food processing, mining, power generation, chemical processing, primary metals, pulp and paper, and oil and gas industry applications. The Company also designs and manufactures Drives helicoid and sectional augers for agricultural applications, like conveying, digging and combines.

Services:

Power Systems. Timken services components in the industrial customer's drive train, including switch gears, electric motors and generators, gearboxes, bearings, couplings and central panels. The Company’s Philadelphia Gear services for gear drive applications include onsite technical services; inspection, repair and upgrade capabilities; and manufacturing of parts to OEM specifications. In addition, the Company’s Wazee, Smith Services, Schulz, Standard Machine and H&N service centers provide customers with services that include motor and generator rewind and repair and uptower wind turbine maintenance and repair. Timken Power Systems commonly serves customers in the power, wind energy, hydro and fossil fuel, water management, paper, mining and general manufacturing sectors.

Bearing Repair. Timken bearing repair services return worn bearings to like-new specifications, which increases bearing service life and often can restore bearings in less time than required to manufacture new. Bearing remanufacturing is available for any bearing type or brand - including competitor products - and is well-suited to heavy industrial applications such as paper, metals, mining, power generation and cement; railroad locomotives, passenger cars and freight cars; and aerospace engines and gearboxes.

Services accounted for approximately 6% of the Company’s net sales for the year ended December 31, 2017.

Sales and Distribution:

Timken products are sold principally by its own internal sales organizations. A portion of each segment's sales are made through authorized distributors.

Customer collaboration is central to the Company's sales strategy. Therefore, Timken goes where its customers need them, with sales engineers primarily working in close proximity to customers rather than at production sites. In some cases, Timken may co-locate with a customer at its facility to ensure optimized collaboration. The Company's sales force continuously updates the team's training and knowledge regarding all friction management products and market sector trends, and Timken employees assist customers during development and implementation phases and provide ongoing service and support.

The Company has a joint venture in North America focused on joint logistics and e-business services. This joint venture, CoLinx, LLC, includes five equity members: Timken, SKF Group, Schaeffler Group, ABB Group and Gates Industrial Corp. The e-business service focuses on information and business services for authorized distributors in the Process Industries segment.

Timken has entered into individually negotiated contracts with some of its customers. These contracts may extend for one or more years and, if a price is fixed for any period extending beyond current shipments, customarily include a commitment by the customer to purchase a designated percentage of its requirements from Timken. Timken does not believe that there is any significant loss of earnings risk associated with any given contract.

3

Competition:

The anti-friction bearing business is highly competitive in every country where Timken sells products. Timken primarily competes based on total value, including price, quality, timeliness of delivery, product design and the ability to provide engineering support and service on a global basis. The Company competes with domestic manufacturers and many foreign manufacturers of anti-friction bearings, including SKF Group, Schaeffler Group, NTN Corporation, JTEKT Corporation and NSK Ltd.

Joint Ventures:

Investments in affiliated companies accounted for under the equity method were approximately $2.5 million and $3.1 million, respectively, at December 31, 2017 and 2016. The investment balance at December 31, 2017 was reported in other non-current assets on the Consolidated Balance Sheets.

Backlog:

The following table provides the backlog of orders for the Company's domestic and overseas operations at December 31, 2017 and 2016:

December 31, | ||||||

(Dollars in millions) | 2017 | 2016 | ||||

Segment: | ||||||

Mobile Industries | $ | 882.3 | $ | 644.7 | ||

Process Industries | 588.3 | 398.4 | ||||

Total Company | $ | 1,470.6 | $ | 1,043.1 | ||

Approximately 90% of the Company’s backlog at December 31, 2017 is scheduled for delivery in the succeeding 12 months. Actual shipments depend upon customers' ever-changing production schedules. Accordingly, Timken does not believe that its backlog data and comparisons thereof, as of different dates, reliably indicate future sales or shipments.

Raw Materials:

The principal raw materials used by the Company to make anti-friction bearings are special bar quality ("SBQ") steel and steel components. SBQ steel and components are produced around the world by various suppliers. SBQ steel is purchased in bar, tube and wire forms, while components are commonly purchased as forgings, semi-finished or finished components. The primary inputs to SBQ steel include scrap metal, iron ore, alloys, energy and labor. The availability and price of SBQ steel are subject to changes in supply and demand, commodity prices for ferrous scrap, ore, alloy, electricity, natural gas, transportation fuel, and labor costs. The Company manages price variability of commodities by using surcharge mechanisms on some of its contracts with its customers that provides for partial recovery of these cost increases in the price of bearing products.

Any significant increase in the cost of steel could materially affect the Company’s earnings. Disruptions in the supply of SBQ steel could temporarily impair the Company’s ability to manufacture bearings for its customers, or require the Company to pay higher prices in order to obtain SBQ steel or components, which could affect the Company’s revenues or profitability. The availability of bearing-quality tubing is relatively limited, and the Company has taken steps to limit its exposure to this particular form of SBQ steel. Overall, the Company believes that the number of suppliers of SBQ steel is adequate to support the needs of global bearing production, and, in general, the Company is not dependent on any single source of supply.

Research:

Timken operates a network of technology and engineering centers to support its global customers with sites in North America, Europe and Asia. This network develops and delivers innovative friction management and mechanical power transmission solutions and technical services. Timken's largest technical center is located at the Company's world headquarters in North Canton, Ohio. Other sites in the United States include Manchester, Connecticut; Downer's Grove and Fulton, Illinois; Springfield, Massachusetts; Springfield, Missouri; Keene and Lebanon, New Hampshire; and King of Prussia, Pennsylvania. Within Europe, the Company has technology facilities in Plymouth, England; Colmar, France; Werdohl, Germany; and Ploiesti, Romania. In Asia, Timken operates technology and engineering facilities in Bangalore, India and Shanghai, China.

Expenditures for research and development amounted to approximately $35.3 million, $31.8 million and $32.6 million in 2017, 2016 and 2015, respectively. No amounts were funded by others in 2017, 2016 and 2015.

4

Environmental Matters:

The Company continues its efforts to protect the environment and comply with environmental protection laws. Additionally, it has invested in pollution control equipment and updated plant operational practices. The Company is committed to implementing a documented environmental management system worldwide and to becoming certified under the ISO 14001 standard where appropriate to meet or exceed customer requirements. As of the end of 2017, 17 of the Company’s plants had obtained ISO 14001 certification.

The Company believes it has established appropriate reserves to cover its environmental expenses and has a well-established environmental compliance audit program for its domestic and international units. This program measures performance against applicable laws, as well as against internal standards that have been established for all units worldwide. It is difficult to assess the possible effect of compliance with future requirements that differ from existing requirements.

The Company and certain of its United Stated ("U.S.") subsidiaries previously have been and could in the future be identified as potentially responsible parties for investigation and remediation at off-site disposal or recycling facilities under the Comprehensive Environmental Response, Compensation and Liability Act ("CERCLA"), known as the Superfund, or state laws similar to CERCLA. In general, such claims for investigation and remediation also have been asserted against numerous other entities.

Management believes any ultimate liability with respect to pending actions will not materially affect the Company’s operations, cash flows or consolidated financial position. The Company also is conducting environmental investigation and/or remediation activities at certain current or former operating sites. The costs of such investigation and remediation activities, in the aggregate, are not expected to be material to the operations or financial position of the Company.

New laws and regulations, stricter enforcement of existing laws and regulations, the discovery of previously unknown contamination or the imposition of new clean-up requirements may require Timken to incur costs or become the basis for new or increased liabilities that could have a materially adverse effect on the Company's business, financial condition or results of operations.

Patents, Trademarks and Licenses:

Timken owns numerous U.S. and foreign patents, trademarks and licenses relating to certain products. While Timken regards these as important, it does not deem its business as a whole, or any industry segment, to be materially dependent upon any one item or group of items.

Employment:

At December 31, 2017, Timken had more than 15,000 employees worldwide. Approximately 7% of Timken’s U.S. employees are covered under collective bargaining agreements.

Available Information:

The Company uses its Investor Relations website at http://investors.timken.com, as a channel for routine distribution of important information, including news releases, analyst presentations and financial information. The Company posts filings as soon as reasonably practicable after they are electronically filed with, or furnished to, the Securities and Exchange Commission (the "SEC"), including its annual, quarterly and current reports on Forms 10-K, 10-Q and 8-K; its proxy statements; and any amendments to those reports or statements. All such postings and filings are available on the Company’s website free of charge. In addition, this website allows investors and other interested persons to sign up to automatically receive e-mail alerts when the Company posts news releases and financial information on the Company’s website. The SEC also maintains a website, www.sec.gov, which contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC. The content on any website referred to in this Annual Report on Form 10-K is not incorporated by reference into this Annual Report unless expressly noted.

5

Item 1A. Risk Factors

The following are certain risk factors that could affect our business, financial condition and results of operations. The risks that are described below are not the only ones that we face. These risk factors should be considered in connection with evaluating forward-looking statements contained in this Annual Report on Form 10-K because these factors could cause our actual results and financial condition to differ materially from those projected in forward-looking statements. If any of the following risks actually occur, our business, financial condition or results of operations could be negatively affected.

Risk Relating to our Business

The bearing industry is highly competitive, and this competition results in significant pricing pressure for our products that could affect our revenues and profitability.

The global bearing industry is highly competitive. We compete with domestic manufacturers and many foreign manufacturers of anti-friction bearings, including SKF Group, Schaeffler Group, NTN Corporation, JTEKT Corporation and NSK Ltd., and an increasing number of emerging market competitors. Due to competitiveness within the bearing industry, we may not be able to increase prices for our products to cover increases in our costs or to achieve desired profitability. In many cases we face pressure from our customers to reduce prices, which could adversely affect our revenues and profitability. In addition, our customers may choose to purchase products from one of our competitors rather than pay the prices we seek for our products, which could adversely affect our revenues and profitability.

Our business is capital intensive, and if there are downturns in the industries that we serve, we may be forced to significantly curtail or suspend operations with respect to those industries, which could result in our recording asset impairment charges or taking other measures that may adversely affect our results of operations and profitability.

Our business operations are capital intensive, and we devote a significant amount of capital to certain industries. Our profitability is dependent on factors such as labor compensation and productivity and inventory management, which are subject to risks that we may not be able to control. If there are downturns in the industries that we serve, we may be forced to significantly curtail or suspend our operations with respect to those industries, including laying-off employees, reducing production, recording asset impairment charges and other measures, which may adversely affect our results of operations and profitability.

Weakness in global economic conditions or in any of the industries or geographic regions in which we or our customers operate, as well as the cyclical nature of our customers' businesses generally or sustained uncertainty in financial markets, could adversely impact our revenues and profitability by reducing demand and margins.

There has been significant volatility in the capital markets and in the end markets and geographic regions in which we and our customers operate, which has negatively affected our revenues. Our revenues also may be negatively affected by changes in customer demand, changes in the product mix and negative pricing pressure in the industries in which we operate. Margins in those industries are highly sensitive to demand cycles, and our customers in those industries historically have tended to delay large capital projects, including expensive maintenance and upgrades, during economic downturns. As a result, our revenues and earnings are impacted by overall levels of industrial production.

6

Our results of operations may be materially affected by conditions in global financial markets or in any of the geographic regions in which we, our customers and our suppliers, operate. If an end user cannot obtain financing to purchase our products, either directly or indirectly contained in machinery or equipment, demand for our products will be reduced, which could have a material adverse effect on our financial condition and earnings.

Global financial markets have experienced volatility in recent years, including volatility in securities prices and diminished liquidity and credit availability. Our access to the financial markets cannot be assured and is dependent on, among other things, market conditions and company performance. Accordingly, we may be forced to delay raising capital, issue shorter tenors than we prefer or pay unattractive interest rates, which could increase our interest expense, decrease our profitability and significantly reduce our financial flexibility.

If a customer becomes insolvent or files for bankruptcy, our ability to recover accounts receivable from that customer would be affected adversely and any payment we received during the preference period prior to a bankruptcy filing potentially may be recoverable by the bankruptcy estate. Furthermore, if certain of our customers liquidate in bankruptcy, we may incur impairment charges relating to obsolete inventory and machinery and equipment.

In addition, financial instability of certain companies in the supply chain could disrupt production in any particular industry. A disruption of production in any of the industries where we participate could have a material adverse effect on our financial condition and earnings. If any of our suppliers are unable or unwilling to provide the products or services that we require or materially increase their costs, our ability to offer and deliver our products on a timely and profitable basis could be impaired. We cannot assure you that any or all of our relationships will not be terminated or that such relationships will continue as presently in effect. Furthermore, if any of our suppliers were to become subject to bankruptcy, receivership or similar proceedings, we may be unable to arrange for alternate or replacement relationships on favorable terms, which could harm our sales and operating results.

Any change in raw material prices or the availability or cost of raw materials could adversely affect our results of operations and profit margins.

We require substantial amounts of raw materials, including steel, to operate our business. Our supply of raw materials could be interrupted for a variety of reasons, including availability and pricing. Prices for raw materials necessary for production have fluctuated significantly in the past and could do so in the future. We generally attempt to manage these fluctuations by passing along increased raw material prices to our customers in the form of price increases or surcharges; however, we may be unable to increase the price of our products due to pricing pressure, contract terms or other factors, which could adversely impact our revenue and profit margins.

Moreover, future disruptions in the supply of our raw materials could impair our ability to manufacture our products for our customers or require us to pay higher prices in order to obtain these raw materials from other sources. Any significant increase in the prices for such raw materials could adversely affect our results of operations and profit margins.

Warranty, recall, quality or product liability claims could materially adversely affect our earnings.

In our business, we are exposed to warranty and product liability claims. In addition, we may be required to participate in the recall of a product. If we fail to meet customer specifications for their products, we may be subject to product quality costs and claims. A successful warranty or product liability claim against us, or a requirement that we participate in a product recall, could have a material adverse effect on our earnings.

We may incur further impairment and restructuring charges that could materially affect our profitability.

We have taken approximately $163 million in impairment and restructuring charges in the aggregate during the last five years. Changes in business or economic conditions, or our business strategy, may result in additional restructuring programs and may require us to take additional charges in the future, which could have a material adverse effect on our earnings.

7

Environmental laws and regulations impose substantial costs and limitations on our operations and environmental compliance may be more costly than we expect.

We are subject to the risk of substantial environmental liability and limitations on our operations due to environmental laws and regulations. We are subject to extensive federal, state, local and foreign environmental, health and safety laws and regulations concerning matters such as air emissions, wastewater discharges, solid and hazardous waste handling and disposal and the investigation and remediation of contamination. The risks of substantial costs and liabilities related to compliance with these laws and regulations are an inherent part of our business, and future conditions may develop, arise or be discovered that create substantial environmental compliance or remediation liabilities and costs.

Compliance with environmental, health and safety legislation and regulatory requirements may prove to be more limiting and costly than we anticipate. To date, we have committed significant expenditures in our efforts to achieve and maintain compliance with these requirements at our facilities, and we expect that we will continue to make significant expenditures related to such compliance in the future. From time to time, we may be subject to legal proceedings brought by private parties or governmental authorities with respect to environmental matters, including matters involving alleged noncompliance with or liability arising from environmental, health and safety laws, property damage or personal injury. New laws and regulations, including those that may relate to emissions of greenhouse gases, stricter enforcement of existing laws and regulations, the discovery of previously unknown contamination or the imposition of new clean-up requirements could require us to incur costs or become the basis for new or increased liabilities that could have a material adverse effect on our business, financial condition or results of operations.

The Company may be subject to risks relating to its information technology systems.

The Company relies on information technology systems to process, transmit and store electronic information and manage and operate its business. A breach in security could expose the Company, its employees and its customers and suppliers to risks of misuse of confidential information, manipulation and destruction of data, production downtimes and operational disruptions, which in turn could adversely affect the Company's reputation, competitive position, business or results of operations.

The global nature of our business exposes us to foreign currency fluctuations that may affect our asset values, results of operations and competitiveness.

We are exposed to the risks of currency exchange rate fluctuations because a significant portion of our net sales, costs, assets and liabilities, are denominated in currencies other than the U.S. dollar. These risks include a reduction in our asset values, net sales, operating income and competitiveness.

For those countries outside the United States where we have significant sales, a strengthening in the U.S. dollar or devaluation in the local currency would reduce the value of our local inventory as presented in our Consolidated Financial Statements. In addition, a stronger U.S. dollar or a weaker local currency would result in reduced revenue, operating profit and shareholders' equity due to the impact of foreign exchange translation on our Consolidated Financial Statements. Fluctuations in foreign currency exchange rates may make our products more expensive for others to purchase or increase our operating costs, affecting our competitiveness and our profitability.

Changes in exchange rates between the U.S. dollar and other currencies and volatile economic, political and market conditions in emerging market countries have in the past adversely affected our financial performance and may in the future adversely affect the value of our assets located outside the United States, our gross profit and our results of operations.

8

Global political instability and other risks of international operations may adversely affect our operating costs, revenues and the price of our products.

Our international operations expose us to risks not present in a purely domestic business, including primarily:

• | changes in tariff regulations, which may make our products more costly to export or import; |

• | difficulties establishing and maintaining relationships with local OEMs, distributors and dealers; |

• | import and export licensing requirements; |

• | compliance with a variety of foreign laws and regulations, including unexpected changes in taxation and environmental or other regulatory requirements, which could increase our operating and other expenses and limit our operations; |

• | disadvantages of competing against companies from countries that are not subject to U.S. laws and regulations, including the Foreign Corrupt Practices Act ("FCPA"); |

• | difficulty in staffing and managing geographically diverse operations; and |

• | tax exposures related to cross-border intercompany transfer pricing and other tax risks unique to international operations. |

These and other risks also may increase the relative price of our products compared to those manufactured in other countries, reducing the demand for our products in the markets in which we operate, which could have a material adverse effect on our revenues and earnings.

Expenses and contributions related to our defined benefit plans are affected by factors outside our control, including the performance of plan assets, interest rates, actuarial data and experience, and changes in laws and regulations, all of which could impact our funded status.

Our future expense and funding obligations for the defined benefit pension plans depend upon a number of factors, including the level of benefits provided for by the plans, the future performance of assets set aside in trusts for these plans, the level of interest rates used to determine the discount rate to calculate the amount of liabilities, actuarial data and experience and any changes in government laws and regulations. In addition, if the various investments held by our pension trusts do not perform as expected or the liabilities increase as a result of discount rates and other actuarial changes, our pension expense and required contributions would increase and, as a result, could materially adversely affect our business or require us to record charges that could be significant and would cause a reduction in our shareholders' equity. We may be required legally to make contributions to the pension plans in the future in excess of our current expectations, and those contributions could be material.

Future actions involving our defined benefit and other postretirement plans, such as annuity purchases, lump sum payouts, and/or plan terminations could cause us to incur significant pension and postretirement settlement and curtailment charges, and require cash contributions.

We have purchased annuities and offered lump sum payouts to defined benefit plan and other postretirement plan participants and retirees in the past. If we were to take similar actions in the future, we could incur significant pension settlement and curtailment charges related to the reduction in pension and postretirement obligations from annuity purchases, lump-sum payouts of benefits to plan participants, and/or plan terminations. Pursuing these types of actions could require us to make additional contributions to the defined plans to maintain a legally required funded status.

Work stoppages or similar difficulties could significantly disrupt our operations, reduce our revenues and materially affect our earnings.

A work stoppage at one or more of our facilities, or at facilities of one or more of our suppliers, could have a material adverse effect on our business, financial condition and results of operations. Also, if one or more of our customers were to experience a work stoppage, that customer likely would halt or limit purchases of our products, which could have a material adverse effect on our business, financial condition and results of operations.

9

We are subject to a wide variety of domestic and foreign laws and regulations that could adversely affect our results of operations, cash flow or financial condition.

We are subject to a wide variety of domestic and foreign laws and regulations, and legal compliance risks, including securities laws, tax laws, employment and pension-related laws, competition laws, U.S. and foreign export and trade laws, and laws governing improper business practices. We are affected by new laws and regulations, and changes to existing laws and regulations, including interpretations by courts and regulators.

In addition, we could be adversely affected by violations of the FCPA and similar worldwide anti-bribery laws as well as export controls and economic sanction laws. The FCPA and similar anti-bribery laws in other jurisdictions generally prohibit companies and their intermediaries from making improper payments to non-U.S government officials for the purpose of obtaining or retaining business. Recently, there has been a substantial increase in the global enforcement of anti-corruption laws. We operate in many parts of the world that have experienced governmental corruption to some degree and, in certain circumstances, strict compliance with anti-bribery laws may conflict with local customs and practices. Our policies mandate compliance with these laws, but we cannot assure you that our internal controls and procedures always will protect us from the improper acts committed by our employees or agents. If we are found to be liable for FCPA, export control or sanction violations, we could suffer from criminal or civil penalties or other sanctions, including loss of export privileges or authorization needed to conduct aspects of our international business, which could have a material adverse effect on our business.

Compliance with the laws and regulations described above or with other applicable foreign, federal, state, and local laws and regulations currently in effect or that may be adopted in the future could materially adversely affect our competitive position, operating results, financial condition and liquidity.

If we are unable to attract and retain key personnel, our business could be materially adversely affected.

Our business substantially depends on the continued service of key members of our management and other key employees. The loss of the services of a significant number of members of our management or other key employees could have a material adverse effect on our business. Our future success also will depend on our ability to attract and retain highly skilled personnel, such as engineering, finance, marketing and senior management professionals. Competition for these types of employees is intense, and we could experience difficulty from time to time in hiring and retaining the personnel necessary to support our business. If we do not succeed in retaining our current employees and attracting new high quality employees, our business could be materially adversely affected.

We may not realize the improved operating results that we anticipate from past and future acquisitions and we may experience difficulties in integrating acquired businesses.

We seek to grow, in part, through strategic acquisitions, joint ventures and other alliances, which are intended to complement or expand our businesses, and expect to continue to do so in the future. These acquisitions involve challenges and risks. In the event that we do not successfully integrate these acquisitions into our existing operations so as to realize the expected return on our investment, our results of operations, cash flow or financial condition could be adversely affected.

Our operating results depend in part on continued successful research, development and marketing of new and/or improved products and services, and there can be no assurance that we will continue to successfully introduce new products and services.

The success of new and improved products and services depends on their initial and continued acceptance by our customers. Our businesses are affected, to varying degrees, by technological change and corresponding shifts in customer demand, which could result in unpredictable product transitions or shortened life cycles, especially as it relates to market and technological changes driven by electrification, climate change requirements or increased digitization. We may experience difficulties or delays in the research, development, production, or marketing of new products and services that may prevent us from recouping or realizing a return on the investments required to bring new products and services to market. The end result could be a negative impact on our operating results.

10

If our internal controls are found to be ineffective, our financial results or our stock price may be adversely affected.

Our most recent evaluation resulted in our conclusion that, as of December 31, 2017, our internal control over financial reporting was effective. We believe that we currently have adequate internal control procedures in place for future periods, including processes related to newly acquired businesses; however, increased risk of internal control breakdowns generally exists in a business environment that is decentralized. In addition, if our internal control over financial reporting is found to be ineffective, investors may lose confidence in the reliability of our financial statements, which may adversely affect our stock price.

Changes in accounting guidance could have an adverse effect on our results of operations, as reported in our financial statements.

Our consolidated financial statements are prepared in accordance with U.S. Generally Accepted Accounting Principles ("U.S. GAAP"), which is periodically revised and/or expanded. Accordingly, from time to time we are required to adopt new or revised accounting guidance and related interpretations issued by recognized authoritative bodies, including the Financial Accounting Standards Board and the SEC. The impact of accounting pronouncements that have been issued but not yet implemented is disclosed in this Annual Report on Form 10-K and our Quarterly Reports on Form 10-Q. It is possible that future accounting guidance we are required to adopt, or future changes in accounting principles, could change the current accounting treatment that we apply to our consolidated financial statements and that such changes could have an adverse effect on our results of operations, as reported in our consolidated financial statements.

Certain members of our Board of Directors and management may have actual or potential conflicts of interest because of their ownership of shares of TimkenSteel Corporation ("TimkenSteel") or their relationships with TimkenSteel following the spinoff of TimkenSteel into an independent publicly traded company on June 30, 2015 (the "Spinoff").

Certain members of our Board of Directors and management own shares of TimkenSteel and/or options to purchase shares of TimkenSteel, which could create, or appear to create, potential conflicts of interest when our directors and executive officers are faced with decisions that could have different implications for us and TimkenSteel. One of our directors, Ward J. Timken, Jr., is also Chairman, President and Chief Executive Officer of TimkenSteel. This may create, or appear to create, potential conflicts of interest if Mr. Timken is faced with decisions that could have different implications for TimkenSteel than the decisions have for us.

Item 1B. Unresolved Staff Comments

None.

Item 2. Properties

Timken has manufacturing facilities at multiple locations in the United States and in a number of countries outside the United States. The aggregate floor area of these facilities worldwide is approximately 10.8 million square feet, all of which, except for approximately 1.8 million square feet, is owned in fee. The facilities not owned in fee are leased. The buildings occupied by Timken are principally made of brick, steel, reinforced concrete and concrete block construction. The Company believes all buildings are in satisfactory operating condition to conduct business.

Timken’s Mobile Industries segment's manufacturing facilities and service centers in the United States are located in Los Alamitos, California; Manchester, Connecticut; Carlyle, Illinois; Lenexa, Kansas; Rochester Hills, Michigan; Keene and Lebanon, New Hampshire; Iron Station, North Carolina; Bucyrus, Canton, New Philadelphia and Sharon Center, Ohio; Gaffney and Honea Path, South Carolina; Pulaski and Knoxville, Tennessee; and Ogden, Utah. These facilities, including warehouses at plant locations and a technology center in North Canton, Ohio, have an aggregate floor area of approximately 3.5 million square feet.

11

Timken’s Mobile Industries segment’s manufacturing plants and service centers outside the United States are located in Belo Horizonte Curitiba, and Rio Clara, Brazil; Yantai, China; Cheltenham, Northampton and Plymouth, England; Colmar, France; Jamshedpur, India; Karmiel, Israel; Cassago, Valmadrea and Villa Carcina, Italy; Sosnowiec, Poland; Gauteng, South Africa. These facilities, including warehouses at plant locations, have an aggregate floor area of approximately 2.3 million square feet.

Timken's Process Industries segment's manufacturing plants and service centers in the United States are located in Hueytown, Alabama; Sante Fe Springs, California; Broomfield and Denver, Colorado; New Haven, Connecticut; New Castle, Delaware; Downers Grove, Fulton and Mokena, Illinois; Mishawaka, Indiana; Fort Scott, Kansas; Augusta and Portland, Maine; Springfield, Massachusetts; South Haven, Michigan; Springfield, Missouri; Randleman and Rutherfordton, North Carolina; Union, South Carolina; Ferndale, Pasco and Vancouver, Washington; Princeton, West Virginia; and Casper, Wyoming. These facilities, including warehouses at plant locations and a wind center in North Canton, Ohio, have an aggregate floor area of approximately 2.8 million square feet.

Timken's Process Industries segment's manufacturing plants and service centers outside the United States are located in Mississauga, Prince George and Sasakatoon, Canada; Chengdu, Jiangsu and Wuxi, China; Dudley, England; Werdohl, Germany; Chennai and Durg, India; Karmiel, Israel; and Ploiesti and Prahova, Romania. These facilities, including warehouses at plant locations, have an aggregate floor area of approximately 2.2 million square feet.

In addition to the manufacturing and distribution facilities discussed above, Timken owns or leases warehouses and distribution facilities in Argentina, Australia, Brazil, Canada, China, France, England, Mexico, New Zealand, Poland, South Africa, Singapore, Spain and the United States.

The extent to which the Company uses its properties varies by property and from time to time. The Company believes that its capacity levels are adequate for its present and anticipated future needs. Most of the Company’s manufacturing facilities remain capable of handling additional volume increases.

Item 3. Legal Proceedings

The Company is involved in various claims and legal actions arising in the ordinary course of business. In the opinion of management, the ultimate disposition of these matters will not have a material adverse effect on the Company’s consolidated financial position or results of operations.

In October 2014, the Brazilian government antitrust agency announced that it had opened an investigation of alleged antitrust violations in the bearing industry. The Company’s Brazilian subsidiary, Timken do Brasil Comercial Importadora Ltda, was included in the investigation. While the Company is unable to predict the ultimate length, scope or results of the investigation, management believes that the outcome will not have a material effect on the Company’s consolidated financial position; however, any such outcome may be material to the results of operations of any particular period in which costs, if any, are recognized. Based on current facts and circumstances, the low end of the range for potential penalties, if any, would be immaterial to the Company.

Item 4. Mine Safety Disclosures

Not applicable.

12

Item 4A. Executive Officers of the Registrant

The executive officers are elected by the Board of Directors normally for a term of one year and until the election of their successors. All executive officers have been employed by Timken or by a subsidiary of the Company during the past five-year period other than Ms. Cheverine, who was hired by the Company in May 2017. The executive officers of the Company as of February 15, 2018 are as follows:

Name | Age | Current Position and Previous Positions During Last Five Years | ||

Carolyn E. Cheverine | 55 | 2017 Executive Vice President, General Counsel and Secretary | ||

2016 Vice President & Chief Counsel, Tax & International Transactions - Eaton Corporation | ||||

2014 Senior Vice President and Chief Counsel, Industrial Sector - Eaton Corporation | ||||

2011 Vice President, General Counsel and Secretary - Cliffs Natural Resources Inc. (subsequently renamed Cleveland-Cliffs Inc.) | ||||

Christopher A. Coughlin | 57 | 2014 Executive Vice President, Group President | ||

2012 Group President | ||||

Philip D. Fracassa | 49 | 2014 Executive Vice President and Chief Financial Officer | ||

2012 Senior Vice President - Planning and Development | ||||

Richard G. Kyle | 52 | 2014 President and Chief Executive Officer; Director | ||

2013 Chief Operating Officer - B&PT; Director | ||||

2012 Group President | ||||

Ronald J. Myers | 59 | 2017 Executive Vice President - Human Resources | ||

2015 Vice President of Human Resources | ||||

2014 Vice President of Organizational Advancement Operations | ||||

2012 Vice President - Operational Organizational Advancement | ||||

13

PART II.

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

The Company’s common shares are traded on the New York Stock Exchange under the symbol “TKR.” The estimated number of record holders of the Company’s common shares at December 31, 2017 was 4,005. The estimated number of beneficial shareholders at December 31, 2017 was 56,244.

The following table provides information about the high and low sales prices for the Company’s common shares and dividends paid for each quarter for the last two fiscal years.

2017 | 2016 | ||||||||||||||||||

Stock prices | Dividends | Stock prices | Dividends | ||||||||||||||||

High | Low | per share | High | Low | per share | ||||||||||||||

First quarter | $ | 46.45 | $ | 40.05 | $ | 0.26 | $ | 33.64 | $ | 22.22 | $ | 0.26 | |||||||

Second quarter | $ | 51.75 | $ | 42.50 | $ | 0.27 | $ | 37.07 | $ | 28.72 | $ | 0.26 | |||||||

Third quarter | $ | 49.95 | $ | 42.55 | $ | 0.27 | $ | 35.28 | $ | 29.31 | $ | 0.26 | |||||||

Fourth quarter | $ | 53.10 | $ | 44.73 | $ | 0.27 | $ | 41.15 | $ | 31.60 | $ | 0.26 | |||||||

Issuer Purchases of Common Shares:

The following table provides information about purchases of its common shares by the Company during the quarter ended December 31, 2017.

Period | Total number of shares purchased (1) | Average price paid per share (2) | Total number of shares purchased as part of publicly announced plans or programs | Maximum number of shares that may yet be purchased under the plans or programs (3) | |||||

10/1/2017 - 10/31/2017 | 50,791 | $ | 49.71 | 44,000 | 9,076,000 | ||||

11/1/2017 - 11/30/2017 | 4,341 | 47.26 | 4,000 | 9,072,000 | |||||

12/1/2017 - 12/31/2017 | 5,080 | 50.12 | — | 9,072,000 | |||||

Total | 60,212 | $ | 49.57 | 48,000 | — | ||||

(1) | Of the shares purchased in October, November and December, 6,791, 341 and 5,080, respectively, represent common shares of the Company that were owned and tendered by employees to exercise stock options, and to satisfy withholding obligations in connection with the exercise of stock options and vesting of restricted shares. |

(2) | For shares tendered in connection with the vesting of restricted shares, the average price paid per share is an average calculated using the daily high and low of the Company’s common shares as quoted on the New York Stock Exchange at the time of vesting. For shares tendered in connection with the exercise of stock options, the price paid is the real-time trading share price at the time the options are exercised. |

(3) | On February 6, 2017, the Company's Board of Directors approved a share repurchase plan pursuant to which the Company may purchase up to ten million of its common shares, in the aggregate. This new share purchase plan expires on February 28, 2021. Under this plan the Company purchased shares from time to time in open market purchases or privately negotiated transactions and was able to make all or part of the purchases pursuant to accelerated share repurchases or Rule 10b5-1 plans. |

14

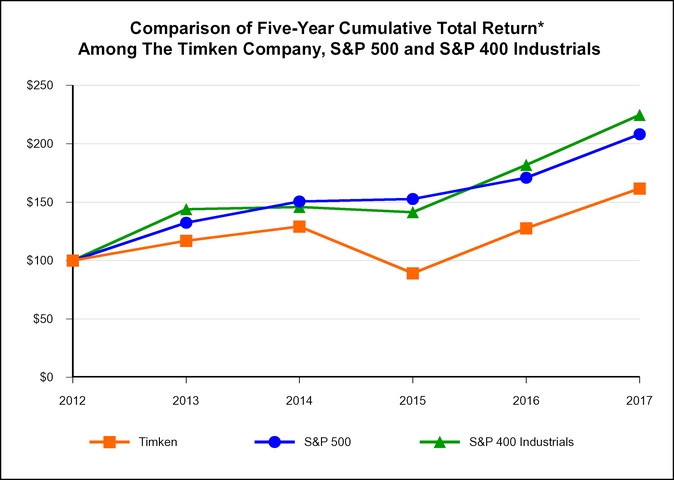

*Total return assumes reinvestment of dividends. Fiscal years ending December 31.

2013 | 2014 | 2015 | 2016 | 2017 | |||||||||||

Timken | $ | 117 | $ | 129 | $ | 89 | $ | 128 | $ | 162 | |||||

S&P 500 | 132 | 151 | 153 | 171 | 208 | ||||||||||

S&P 400 Industrials | 144 | 146 | 141 | 182 | 225 | ||||||||||

The line graph compares the cumulative total shareholder returns over five years for The Timken Company, the S&P 500 Stock Index and the S&P 400 Industrials Index. The graph assumes, in each case, an initial investment of $100 on January 1, 2012, in Timken common shares, S&P 500 Index and S&P 400 Industrials Index, based on market prices at the end of each fiscal year through and including December 31, 2017, and reinvestment of dividends (and taking into account the value of the TimkenSteel common shares distributed in the Spinoff).

15

Item 6. Selected Financial Data

Summary of Operations and Other Comparative Data:

(Dollars in millions, except per share and per employee data) | 2017 | 2016 | 2015 | 2014 | 2013 | ||||||||||

Statements of Income | |||||||||||||||

Net sales | $ | 3,003.8 | $ | 2,669.8 | $ | 2,872.3 | $ | 3,076.2 | $ | 3,035.4 | |||||

Gross profit | 810.4 | 668.5 | 819.5 | 851.2 | 1,041.7 | ||||||||||

Selling, general and administrative expenses | 521.4 | 470.7 | 457.7 | 611.8 | 324.8 | ||||||||||

Impairment and restructuring charges | 4.3 | 21.7 | 14.7 | 113.4 | 8.7 | ||||||||||

Operating income (1) | 284.7 | 174.5 | 255.9 | 125.8 | 708.0 | ||||||||||

Continued Dumping and Subsidy Offset Act income, net | — | 59.6 | — | — | — | ||||||||||

Other income (expense), net | 9.4 | (0.9 | ) | (7.5 | ) | 19.9 | 6.7 | ||||||||

Interest expense, net | 34.2 | 31.6 | 30.7 | 24.3 | 22.5 | ||||||||||

Income from continuing operations | 202.3 | 141.1 | 191.4 | 85.2 | 434.0 | ||||||||||

Income from discontinued operations, net of income taxes | — | — | — | 30.5 | 224.7 | ||||||||||

Net income attributable to The Timken Company | $ | 203.4 | $ | 140.8 | $ | 188.6 | $ | 113.2 | $ | 658.4 | |||||

Balance Sheets | |||||||||||||||

Inventories, net | $ | 738.9 | $ | 553.7 | $ | 551.1 | $ | 593.7 | $ | 590.6 | |||||

Property, plant and equipment, net | 864.2 | 804.4 | 777.8 | 780.5 | 855.8 | ||||||||||

Total assets | 3,402.4 | 2,763.2 | 2,789.0 | 3,002.9 | 4,480.3 | ||||||||||

Total debt: | |||||||||||||||

Short-term debt | 105.4 | 19.2 | 62.0 | 7.4 | 18.6 | ||||||||||

Current portion of long-term debt | 2.7 | 5.0 | 15.1 | 0.6 | 250.7 | ||||||||||

Long-term debt | 854.2 | 635.0 | 579.4 | 518.4 | 175.6 | ||||||||||

Total debt | $ | 962.3 | $ | 659.2 | $ | 656.5 | $ | 526.4 | $ | 444.9 | |||||

Net debt | |||||||||||||||

Total debt | 962.3 | 659.2 | 656.5 | 526.4 | 444.9 | ||||||||||

Less: cash and cash equivalents and restricted cash | (125.4 | ) | (151.5 | ) | (129.8 | ) | (294.1 | ) | (399.7 | ) | |||||

Net debt (2) | $ | 836.9 | $ | 507.7 | $ | 526.7 | $ | 232.3 | $ | 45.2 | |||||

Total liabilities | 1,927.5 | 1,452.3 | 1,439.5 | 1,408.7 | 1,828.4 | ||||||||||

Total equity | $ | 1,474.9 | $ | 1,310.9 | $ | 1,349.5 | $ | 1,594.2 | $ | 2,651.9 | |||||

Capital: | |||||||||||||||

Net debt | 836.9 | 507.7 | 526.7 | 232.3 | 45.2 | ||||||||||

Total equity | 1,474.9 | 1,310.9 | 1,349.5 | 1,594.2 | 2,651.9 | ||||||||||

Net debt + total equity (capital) | $ | 2,311.8 | $ | 1,818.6 | $ | 1,876.2 | $ | 1,826.5 | $ | 2,697.1 | |||||

Other Comparative Data | |||||||||||||||

Income from continuing operations / net sales | 6.7 | % | 5.3 | % | 6.7 | % | 2.8 | % | 14.3 | % | |||||

Net income attributable to The Timken Company / net sales | 6.8 | % | 5.3 | % | 6.6 | % | 3.7 | % | 21.7 | % | |||||

Return on equity (3) | 13.7 | % | 10.8 | % | 14.2 | % | 5.3 | % | 16.4 | % | |||||

Net sales per employee (4) | $ | 206.3 | $ | 185.3 | $ | 197.5 | $ | 210.9 | $ | 203.1 | |||||

Capital expenditures | 104.7 | 137.5 | 105.6 | 126.8 | 133.6 | ||||||||||

Depreciation and amortization | 137.7 | 131.7 | 130.8 | 137.0 | 142.4 | ||||||||||

Capital expenditures / net sales | 3.5 | % | 5.2 | % | 3.7 | % | 4.1 | % | 4.4 | % | |||||

Dividends per share | $ | 1.07 | $ | 1.04 | $ | 1.03 | $ | 1.00 | $ | 0.92 | |||||

Basic earnings per share - continuing operations (5) | 2.62 | 1.79 | 2.23 | 0.92 | 4.56 | ||||||||||

Diluted earnings per share - continuing operations (5) | 2.58 | 1.78 | 2.21 | 0.91 | 4.52 | ||||||||||

Basic earnings per share (6) | 2.62 | 1.79 | 2.23 | 1.25 | 6.92 | ||||||||||

Diluted earnings per share (6) | 2.58 | 1.78 | 2.21 | 1.24 | 6.86 | ||||||||||

Net debt to capital (2) | 36.2 | % | 27.9 | % | 28.1 | % | 12.7 | % | 1.7 | % | |||||

Number of employees at year-end (7) | 15,006 | 14,111 | 14,709 | 14,378 | 14,794 | ||||||||||

Number of shareholders (8) | 56,244 | 43,458 | 40,257 | 44,271 | 52,218 | ||||||||||

(1) | Operating income included pension settlement charges of $119.9 million during 2015. |

(2) | The Company presents net debt because it believes net debt is more representative of the Company’s financial position than total debt due to the amount of cash and cash equivalents. |

(3) | Return on equity is defined as income from continuing operations divided by ending total equity. |

(4) | Dollars in thousands, based on average number of employees employed during the year. |

(5) | Based on average number of shares outstanding during the year. |

(6) | Based on average number of shares outstanding during the year and includes discontinued operations for 2013 and 2014. |

(7) | Adjusted to exclude temporary employees for all periods. |

(8) | Includes an estimated count of shareholders having common shares held for their accounts by banks, brokers and trustees for benefit plans. |

16

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations

(Dollars in millions, except per share data)

OVERVIEW

Introduction:

The Timken Company engineers, manufactures and markets bearings, transmissions, gearboxes, belts, chain, lubrication systems, couplings, industrial clutches and brakes and related products and offers a variety of power system rebuild and repair services. The Company’s growing product and services portfolio features many strong industrial brands, such as Timken®, Fafnir®, Philadelphia Gear®, Drives®, Lovejoy® and Groeneveld®. Timken applies its deep knowledge of metallurgy, friction management and mechanical power transmission across the broad spectrum of bearings and related systems to improve the reliability and efficiency of machinery and equipment all around the world. Known for its quality products and collaborative technical sales model, Timken focuses on providing value to diverse markets worldwide through both original equipment manufacturers ("OEMs") and aftermarket channels. With more than 15,000 people operating in 33 countries, Timken makes the world more productive and keeps industry in motion. The Company operates under two reportable segments: (1) Mobile Industries and (2) Process Industries. The following further describes these business segments:

• | Mobile Industries serves OEM customers that manufacture off-highway equipment for the agricultural, mining and construction markets; on-highway vehicles including passenger cars, light trucks, and medium- and heavy-duty trucks; rail cars and locomotives; outdoor power equipment; rotorcraft and fixed-wing aircraft; and other mobile equipment. Beyond service parts sold to OEMs, aftermarket sales and services to individual end users, equipment owners, operators and maintenance shops are handled directly or through the Company's extensive network of authorized automotive and heavy-truck distributors. |

• | Process Industries serves OEM and end-user customers in industries that place heavy demands on the fixed operating equipment they make or use in heavy and other general industrial sectors. This includes metals, cement and aggregate production; coal and wind power generation; oil and gas extraction and refining; pulp and paper and food processing; and health and critical motion control equipment. Other applications include marine equipment, gear drives, cranes, hoists and conveyors. This segment also supports aftermarket sales and service needs through its global network of authorized industrial distributors and through the provision of services directly to end users. |

Timken creates value by understanding customer needs and applying its know-how in attractive market sectors, serving a broad range of customers and industries across the globe. The Company’s business strengths include its product technology, end-market diversity, geographic reach and aftermarket mix. Timken collaborates with OEMs to improve equipment efficiency with its engineered products and captures subsequent equipment replacement cycles by selling largely through independent channels in the aftermarket. Timken focuses its international efforts and footprint in regions of the world where strong macroeconomic factors such as urbanization, infrastructure development and sustainability create demand for its products and services.

17

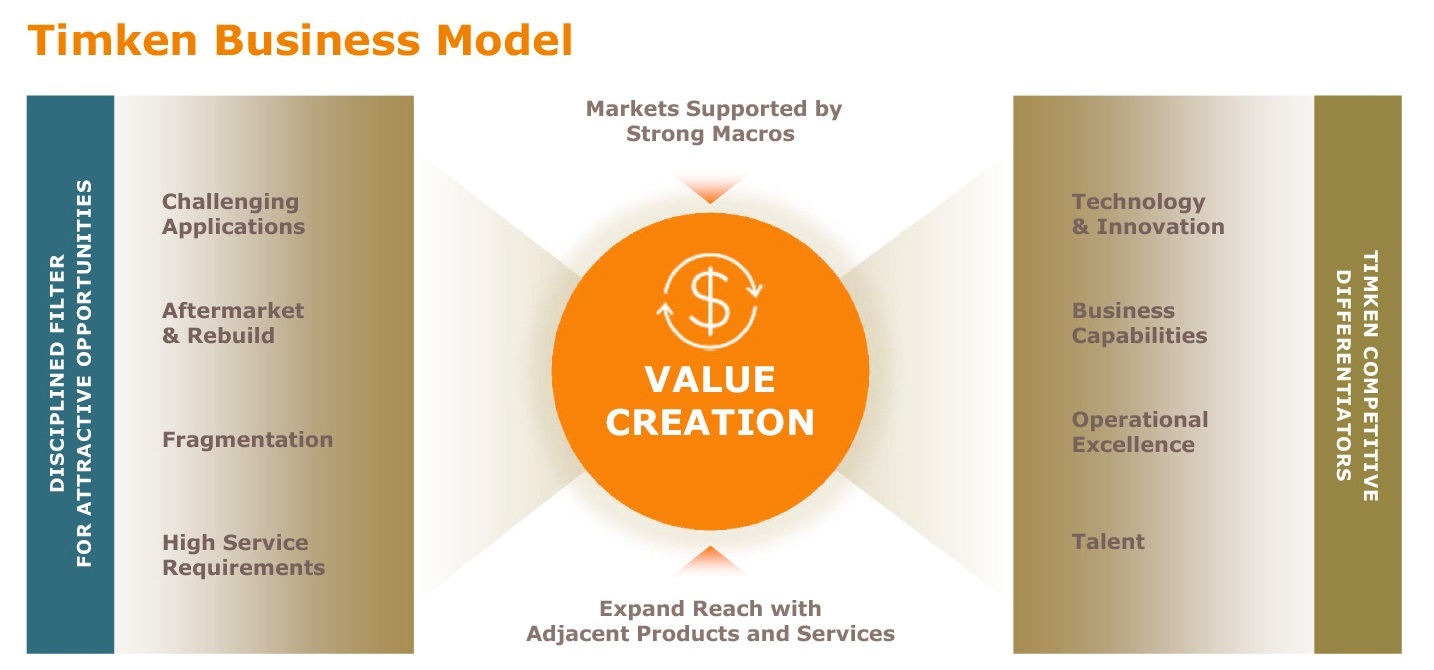

The Timken Business Model is the specific framework for how the Company evaluates opportunities and differentiates itself in the market.

Outgrowing Our Markets. The Company intends to expand into new and existing markets by leveraging its collective knowledge of metallurgy, friction management and mechanical power transmission to create value for Timken customers. Using a highly collaborative technical selling approach, the Company places particular emphasis on creating unique solutions for challenging and/or demanding applications. The Company intends to grow in attractive market sectors around the world, emphasizing those spaces that are highly fragmented, demand high service and value the reliability and efficiency offered by Timken products. The Company also targets those applications that offer significant aftermarket demand, thereby providing product and services revenue throughout the equipment’s lifetime.

Operating With Excellence. Timken operates with a relentless drive for exceptional results and a passion for superior execution. The Company embraces a continuous improvement culture that is charged with increasing efficiency, lowering costs, eliminating waste, encouraging organizational agility and building greater brand equity to fuel future growth. This requires the Company’s ongoing commitment to attract, retain and develop the best talent across the world.

Deploying Capital to Drive Shareholder Value. The Company is intently focused on providing the highest returns for shareholders through its capital allocation framework, which includes: (1) investing in the core business through capital expenditures, research and development and organic growth initiatives; (2) pursuing strategic acquisitions to broaden our portfolio and capabilities, with a focus on bearings, adjacent power transmission products and related services; and (3) returning capital to shareholders through dividends and share repurchases. As part of this framework, the Company also may restructure, reposition or divest underperforming product lines or assets.

18

The following items highlight certain of the Company's more significant strategic accomplishments in 2017:

Acquisitions

• | On April 3, 2017, the Company completed the acquisition of the shares of Torsion Control Products, Inc. ("Torsion Control Products"), a manufacturer of engineered torsional couplings used in the construction, agriculture and mining industries. Torsion Control Products, located in Rochester Hills, Michigan, had sales of approximately $20 million for the 12 months ended December 31, 2016. Based on markets and customers served, substantially all of the results for Torsion Control Products are reported in the Mobile Industries segment. |

• | On May 5, 2017, the Company completed the acquisition of the assets of PT Tech, Inc. ("PT Tech"), a manufacturer of engineered clutches, brakes, hydraulic power take-off units and other torque management devices used in mining, aggregate, wood recycling and metals industries. PT Tech, located in Sharon Center, Ohio, had sales of approximately $22 million for the 12 months ended April 30, 2017. Based on markets and customers served, substantially all of the results for PT Tech are reported in the Mobile Industries segment. |

• | On July 3, 2017, the Company completed the acquisition of the shares of Wenjo B.V. ("Groeneveld"), a leading provider of automated lubrication solutions used in on- and off-highway applications. Groeneveld, located in Gorinchem, Netherlands with manufacturing facilities in Italy, had sales of approximately $105 million for the 12 months ended May 31, 2017. Based on markets and customers served, substantially all of the results for Groeneveld are reported in the Mobile Industries segment. |

• | On July 5, 2017, the Company announced that the Company's majority-owned subsidiary, Timken India Ltd. ("Timken India"), entered into a definitive agreement to acquire ABC Bearings Limited ("ABC Bearings"), a manufacturer of tapered, cylindrical and spherical roller bearings and slewing rings in India. The transaction is structured as a merger of ABC Bearings into Timken India, whereby shareholders of ABC Bearings will receive shares of Timken India as consideration. The transaction is subject to receipt of various approvals in India, which are expected to be completed in the first half of 2018. ABC Bearings, located in Mumbai, India, operates primarily out of manufacturing facilities in Bharuch, Gujarat and Dehradun, Uttarakhand and had sales of approximately $29 million for the 12 months ended May 31, 2017. |

Operational Highlights

• | On June 13, 2017, the Company held the grand opening for its new state-of-the-art bearing plant in Prahova, Romania, where Timken® metric tapered roller bearings are manufactured. The new plant strengthens the Company's global footprint and product offering. |

19

RESULTS OF OPERATIONS

2017 vs. 2016

Overview:

2017 | 2016 | $ Change | % Change | ||||||||

Net sales | $ | 3,003.8 | $ | 2,669.8 | $ | 334.0 | 12.5 | % | |||

Net income | 202.3 | 141.1 | 61.2 | 43.4 | % | ||||||

Net (loss) income attributable to noncontrolling interest | (1.1 | ) | 0.3 | (1.4 | ) | (466.7 | %) | ||||

Net income attributable to The Timken Company | $ | 203.4 | $ | 140.8 | $ | 62.6 | 44.5 | % | |||

Diluted earnings per share | $ | 2.58 | $ | 1.78 | $ | 0.80 | 44.9 | % | |||

Average number of shares—diluted | 78,911,149 | 79,234,324 | — | (0.4 | %) | ||||||

The increase in net sales was primarily due to higher end-market demand and the benefit of acquisitions. The increase in net income in 2017 compared with 2016 was primarily due to improved performance across the business, as well as lower net actuarial losses due to the remeasurement of pension and other postretirement assets and obligations ("Mark-to-Market Charges"), restructuring charges, and income tax expense, partially offset by lower pre-tax U.S. Continued Dumping and Subsidy Offset Act ("CDSOA") income of $59.6 million. The improvement in business performance reflects higher volume, favorable manufacturing performance, the benefit of acquisitions and the favorable impact of foreign currency exchange rate changes, partially offset by unfavorable price/mix and higher material, logistics and selling, general and administrative ("SG&A") expenses.

Outlook:

The Company expects 2018 full-year sales to increase 9% to 10% compared with 2017 primarily due to increased demand across most end-market sectors, higher pricing, the benefit of acquisitions and the favorable impact of foreign currency exchange rate changes. The Company's earnings are expected to be higher in 2018 than 2017, primarily due to the impact of higher volume, favorable price/mix, the benefit of acquisitions and the favorable impact of foreign currency exchange rate changes, partially offset by higher operating costs, a higher income tax rate and higher interest expense.

The Company expects to generate operating cash of approximately $350 million in 2018, an increase from 2017 of approximately $113 million or 48%, as the Company anticipates higher net income and lower working capital requirements. The Company expects capital expenditures to be 3.5% to 4.0% of sales in 2018, compared with 3.5% of sales in 2017.

20

THE STATEMENTS OF INCOME

Sales:

2017 | 2016 | $ Change | % Change | ||||||||

Net sales | $ | 3,003.8 | $ | 2,669.8 | $ | 334.0 | 12.5 | % | |||

Net sales increased in 2017 compared with 2016 primarily due to higher organic revenue of $186 million, the benefit of acquisitions of $131 million and the favorable impact of foreign currency exchange rate changes of $17 million. The increase in organic revenue was driven by higher demand across most of the Company's market sectors led by the off-highway, industrial distribution and heavy truck sectors, partially offset by lower demand in the rail sector.

Gross Profit:

2017 | 2016 | $ Change | Change | ||||||||

Gross profit | $ | 810.4 | $ | 668.5 | $ | 141.9 | 21.2 | % | |||

Gross profit % to net sales | 27.0 | % | 25.0 | % | — | 200 | bps | ||||

Gross profit increased in 2017 compared with 2016 primarily due to the impact of higher volume of $74 million, the benefit of acquisitions of $52 million, favorable manufacturing performance of $49 million and lower Mark-to-Market Charges of $31 million. These factors were partially offset by higher material and logistics costs of $34 million and unfavorable price/mix of $34 million.

Selling, General and Administrative Expenses:

2017 | 2016 | $ Change | Change | |||||||

Selling, general and administrative expenses | $ | 521.4 | $ | 470.7 | $ | 50.7 | 10.8% | |||

Selling, general and administrative expenses % to net sales | 17.4 | % | 17.6 | % | — | (20) bps | ||||

The increase in SG&A expenses in 2017 compared with 2016 was primarily due to the impact of acquisitions and higher incentive compensation expense, partially offset by lower Mark-to-Market Charges.

Impairment and Restructuring Charges:

2017 | 2016 | $ Change | |||||||

Impairment charges | $ | 0.1 | $ | 3.9 | $ | (3.8 | ) | ||

Severance and related benefit costs | 3.5 | 15.3 | (11.8 | ) | |||||

Exit costs | 0.7 | 2.5 | (1.8 | ) | |||||

Total | $ | 4.3 | $ | 21.7 | $ | (17.4 | ) | ||