UNITED STATES SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

_________________________________________________

FORM 10-K

_________________________________________________

| (Mark One) | ||||||||||||||

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||||||||

For the fiscal year ended December 31 , 2021

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||||||||

For the transition period from to .

Commission file number 1-5353

_________________________________________________

(Exact name of registrant as specified in its charter)

_________________________________________________

(State or other jurisdiction of incorporation or organization) | (I.R.S. employer identification no.) | |||||||

| (Address of principal executive offices) | (Zip Code) | |||||||

Registrant’s telephone number, including area code: (610 ) 225-6800

| Securities registered pursuant to Section 12(b) of the Act: | ||||||||||||||

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act:

NONE

_________________________________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. | ||

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ | ||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | ||

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). | ||

| Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and "emerging growth company" in Rule 12b-2 of the Exchange Act. | ||

Accelerated filer ¨ | Non-accelerated filer ¨ | Smaller reporting company | Emerging growth company | |||||||||||||||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨ ¨ | ||||||||||||||||||||||||||

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act by the registered public accounting firm that prepared or issued its audit report. | ||||||||||||||||||||||||||

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes | ||||||||||||||||||||||||||

The aggregate market value of the Common Stock of the registrant held by non-affiliates of the registrant (29,100,050 shares) on June 27, 2021 (the last business day of the registrant’s most recently completed fiscal second quarter) was $ | ||||||||||||||||||||||||||

The registrant had | ||||||||||||||||||||||||||

DOCUMENT INCORPORATED BY REFERENCE:

TELEFLEX INCORPORATED

ANNUAL REPORT ON FORM 10-K

FOR THE YEAR ENDED DECEMBER 31, 2021

TABLE OF CONTENTS

| Page | ||||||||

| RESERVED | ||||||||

2

Information Concerning Forward-Looking Statements

All statements made in this Annual Report on Form 10-K, other than statements of historical fact, are forward-looking statements. The words “anticipate,” “believe,” “estimate,” “expect,” “intend,” “may,” “plan,” “will,” “would,” “should,” “guidance,” “potential,” “continue,” “project,” “forecast,” “confident,” “prospects” and similar expressions typically are used to identify forward-looking statements. Forward-looking statements are based on the then-current expectations, beliefs, assumptions, estimates and forecasts about our business and the industry and markets in which we operate. These statements are not guarantees of future performance and are subject to risks and uncertainties, which are difficult to predict. Therefore, actual outcomes and results may differ materially from what is expressed or implied by these forward-looking statements due to a number of factors, including:

•changes in business relationships with and purchases by or from major customers or suppliers;

•delays or cancellations in shipments;

•demand for and market acceptance of new and existing products;

•our inability to provide products to our customers, which may be due to, among other things, events that impact key distributors, suppliers and vendors that sterilize our products;

•our inability to integrate acquired businesses into our operations, realize planned synergies and operate such businesses profitably in accordance with our expectations;

•our inability to effectively execute our restructuring programs;

•our inability to realize anticipated savings resulting from restructuring plans and programs;

•the impact of enacted healthcare reform legislation and proposals to amend, replace or repeal the legislation;

•changes in Medicare, Medicaid and third-party coverage and reimbursements;

•the impact of tax legislation and related regulations;

•competitive market conditions and resulting effects on revenues and pricing;

•increases in raw material costs that cannot be recovered in product pricing;

•global economic factors, including currency exchange rates, interest rates, trade disputes, sovereign debt issues and international conflicts and hostilities, such as the ongoing conflict between Russia and Ukraine;

•public health epidemics including the novel coronavirus (referred to as COVID-19);

•difficulties entering new markets; and

•general economic conditions.

For a further discussion of the risks relating to our business, see Item 1A, “Risk Factors” in this Annual Report on Form 10-K. We expressly disclaim any obligation to update these forward-looking statements, except as otherwise explicitly stated by us or as required by law or regulation.

3

PART I

ITEM 1. BUSINESS

Teleflex Incorporated is referred to herein as “we,” “us,” “our,” “Teleflex” and the “Company.”

THE COMPANY

Teleflex is a global provider of medical technology products that enhance clinical benefits, improve patient and provider safety and reduce total procedural costs. We primarily design, develop, manufacture and supply single-use medical devices used by hospitals and healthcare providers for common diagnostic and therapeutic procedures in critical care and surgical applications. We market and sell our products to hospitals and healthcare providers worldwide through a combination of our direct sales force and distributors. Because our products are used in numerous markets and for a variety of procedures, we are not dependent upon any one end-market or procedure. Our major manufacturing operations are located in the Czech Republic, Malaysia, Mexico and the United States (the "U.S.").

We are focused on achieving consistent, sustainable and profitable growth and improving our financial performance by increasing our market share and improving our operating efficiencies through:

•development of new products and product line extensions;

•investment in new technologies and broadening the application of our existing technologies;

•expansion of the use of our products in existing markets and introduction of our products into new geographic markets;

•achievement of economies of scale as we continue to expand by utilizing our direct sales force and distribution network to sell new products, as well as by increasing efficiencies in our sales and marketing organizations, research and development activities and manufacturing and distribution facilities; and

•expansion of our product portfolio through select acquisitions, licensing arrangements and business partnerships that enhance, expand or expedite our development initiatives or our ability to increase our market share.

Our research and development capabilities, commitment to engineering excellence and focus on low-cost manufacturing enable us to bring to market cost effective, innovative products that improve the safety, efficacy and quality of healthcare. Our research and development initiatives focus on developing these products for both existing and new therapeutic applications, as well as developing enhancements to, and product line extensions of, existing products. During 2021 we introduced several product line extensions and five new products. Our portfolio of existing products and products under development consists primarily of Class I and Class II medical devices, most of which require 510(k) clearance by the U.S. Food and Drug Administration ("FDA") for sale in the U.S., and some of which are exempt from the requirement to obtain 510(k) clearance. We believe that seeking 510(k) clearance or qualifying for 510(k)-exempt status reduces our research and development costs and risks, and typically results in a shorter timetable for new product introductions as compared to the premarket approval, or PMA, process that would be required for Class III medical devices. See "Government Regulation" below for additional information.

HISTORY AND RECENT DEVELOPMENTS

Teleflex was founded in 1943 as a manufacturer of precision mechanical push/pull controls for military aircraft. From this original single market, single product orientation, we expanded and evolved through entries into new businesses, development of new products, introduction of products into new geographic or end-markets and acquisitions and dispositions of businesses. Throughout our history, we have continually focused on providing innovative, technology-driven, specialty-engineered products that help our customers meet their business requirements.

Beginning in 2007, we significantly changed the composition of our portfolio of businesses, expanding our presence in the medical device industry, while divesting all of our other businesses, which served the aerospace, automotive, industrial and marine markets. Following the divestitures of our marine business and cargo container and systems businesses in 2011, we became exclusively a medical device company.

In 2017, we completed two large scale acquisitions: NeoTract, Inc. ("NeoTract") and Vascular Solutions, Inc. (“Vascular Solutions”). NeoTract was a medical device company that developed and commercialized the UroLift System, a minimally invasive medical device for treating lower urinary tract symptoms due to benign prostatic hyperplasia, or BPH. Vascular Solutions was a medical device company that developed and marketed clinical products for use in minimally invasive coronary and peripheral vascular procedures.

4

On May 15, 2021, we entered into a definitive agreement to sell certain product lines within our global respiratory product portfolio (the "Divested respiratory business") to Medline Industries, Inc. (“Medline”) for consideration of $286.0 million, reduced by $12 million in working capital not transferring to Medline (the "Respiratory business divestiture"). We completed the initial phase of the Respiratory business divestiture on June 28, 2021, pursuant to which we received cash proceeds of $259 million. The second and final phase of the Respiratory business divestiture will occur once we transfer certain additional manufacturing assets to Medline and is expected to occur prior to the end of 2023.

See "Our Products" below and Note 4 to the consolidated financial statements included in this Annual Report on Form 10-K for additional information.

We expect to continue to increase the size of our business through a combination of acquisitions and organic growth initiatives.

Restructuring programs

We continue to execute our footprint realignment and other restructuring programs designed to improve efficiencies in our manufacturing and distribution facilities and, to a lesser extent, our sales and marketing and research and development organizations. See Note 5 to the consolidated financial statements included in this Annual Report on Form 10-K for additional information.

OUR SEGMENTS

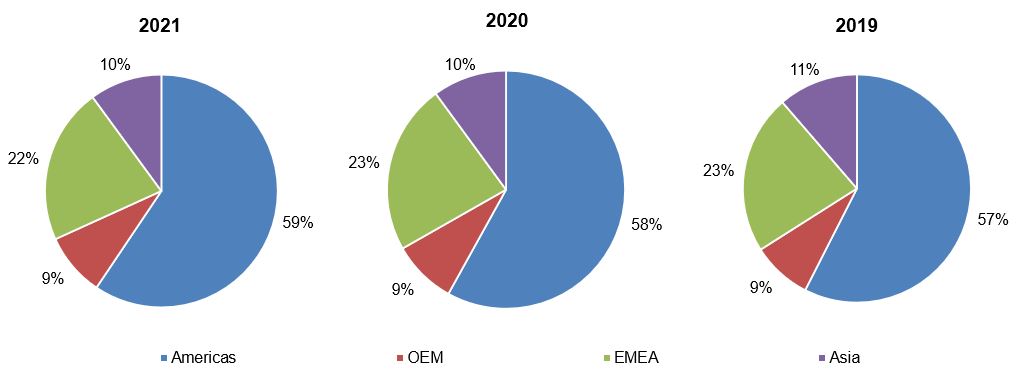

We have four segments: Americas, EMEA (Europe, the Middle East and Africa), Asia (Asia Pacific) and OEM (Original Equipment Manufacturer and Development Services).

Each of our three geographic segments provides a comprehensive portfolio of medical technology products used by hospitals and healthcare providers. However, certain of our products are more heavily concentrated within certain segments. For example, most of our urology products are sold by our EMEA segment and most of our interventional urology products are sold by our Americas segment. Our product portfolio is described in the products section below.

Our OEM segment designs, manufactures and supplies devices and instruments for other medical device manufacturers. Our OEM division, which includes the TFX Medical OEM, TFX OEM, Deknatel and HPC Medical brands, provides custom extrusions, micro-diameter film-cast tubing, diagnostic and interventional catheters, balloons and balloon catheters, film-insulated fine wire, coated mandrel wire, conductors, sheath/dilator introducers, specialized sutures and performance fibers, bioabsorbable sutures, yarns and resins.

The following charts depict our net revenues by reportable operating segment as a percentage of our total consolidated net revenues for the years ended December 31, 2021, 2020 and 2019:

OUR PRODUCTS

Our product categories within our geographic segments include vascular access, anesthesia, interventional, surgical, interventional urology, respiratory and urology. Each of these categories and the key products sold therein are described in more detail below.

5

Vascular Access: Our Vascular Access product category offers devices that facilitate a variety of critical care therapies and other applications with a focus on helping reduce vascular-related complications. These products primarily consist of our Arrow branded catheters, catheter navigation and tip positioning systems and our intraosseous, or in the bone, access systems.

Our catheters are used in a wide range of procedures, including the administration of intravenous therapies, the measurement of blood pressure and the withdrawal of blood samples through a single puncture site. Many of our catheters provide antimicrobial and antithrombogenic protection technology that have been shown to reduce the risk of catheter related bloodstream infections and microbial colonization and thrombus accumulation on catheter surfaces.

Our intraosseous access systems are designed for the delivery of medications and fluids when intravenous access is difficult to obtain in emergent, urgent or medically necessary cases. Our products offer a method for vascular access that can be administered quickly and effectively in the hospital and pre-hospital environments and include the EZ-IO Intraosseous Vascular Access System and Arrow FAST1 Sternal Intraosseous Infusion System.

Interventional: Our Interventional product category offers devices that facilitate a variety of applications to diagnose and deliver treatment via the vascular system of the body. These products primarily consist of a variety of coronary catheters, structural heart therapies, peripheral intervention products and cardiac assist products that are used by interventional cardiologists, interventional radiologists and vascular surgeons. Clinical benefits of our products include increased vein and artery access and increased support during complex medical procedures. Our product offerings consist of a portfolio of Arrow branded catheters, Guideline and Trapliner catheters, the Manta Vascular Closure and Arrow OnControl devices.

Anesthesia: Our Anesthesia product category is comprised of airway, pain management and hemostatic product lines that support hospital, emergency medicine and military channels.

Our airway management products and related devices are designed to enable use of standard and advanced anesthesia techniques in both pre-hospital emergency and hospital settings. Our key products include laryngoscopes, supraglottic airways, endotracheal tubes and atomization devices, which are branded under our LMA, Rusch and MAD trade names.

Our pain management product line includes catheters and disposable pain pumps for regional anesthesia, designed to improve patients’ post-operative pain experience, which are branded under our Arrow trade name.

Our hemostatic products accelerate the body's natural clotting cascade and are used in trauma situations where bleeding is difficult to control. The portfolio consists of external hemostats used by first responders, interventional products used in the catheter lab, and trauma products used by trauma surgeons, which are branded under our QuikClot trade name.

Surgical: Our Surgical product category consists of single-use and reusable products designed to provide surgeons with devices for use in a variety of surgical procedures. These products primarily consist of metal and polymer ligation clips, fascial closure surgical systems used in laparoscopic surgical procedures, percutaneous surgical systems and other surgical instruments. Our significant surgical brands include Weck, Minilap, Pleur-Evac, Deknatel, KMedic and Pilling.

Interventional Urology: Our interventional urology product category includes the UroLift System, a minimally invasive technology for treating lower urinary tract symptoms due to benign prostatic hyperplasia, or BPH. The UroLift System involves the placement of permanent implants, typically through a transurethral outpatient procedure, that hold the prostate lobes apart to relieve compression on the urethra without cutting, heating or removing prostate tissue. Our Interventional Urology product portfolio is most heavily weighted in our Americas segment.

Respiratory: Our respiratory products are used in a variety of care settings and primarily consist of oxygen therapy products. The Respiratory business divestiture included products marketed under the Hudson RCI brand name that comprised oxygen therapy products, aerosol therapy products, spirometry products and ventilation management products.

Urology: Our urology product portfolio provides bladder management for patients in the hospital and individuals in the home care markets. The product portfolio consists principally of a wide range of catheters (including Foley and intermittent), urine collectors, catheterization accessories and products for operative endourology, which are

6

marketed under the Teleflex and Rusch brand names. Our urology product portfolio is most heavily weighted in our EMEA segment.

OUR MARKETS

We generally serve three end-markets: hospitals and healthcare providers, medical device manufacturers and home care. These markets are affected by a number of factors, including demographics, utilization and reimbursement patterns. The following charts depict the percentage of net revenues for the years ended December 31, 2021, 2020 and 2019 derived from each of our end markets:

GOVERNMENT REGULATION

We are subject to comprehensive government regulation both within and outside the U.S. relating to the development, manufacture, sale and distribution of our products.

Regulation of Medical Devices in the U.S

All of our medical devices manufactured or distributed in the U.S. are subject to requirements set forth by the Federal Food, Drug, and Cosmetic Act (“FDC Act”) and regulations promulgated by the FDA under the FDC Act, which are enforced by the FDA. The FDA and, in some cases, other government agencies administer requirements for the methods used in, and the facilities and controls used for, the design, manufacture, packaging, labeling, storage, installation, servicing, marketing, importing and exporting of all finished devices intended for human use. Additional FDA requirements include premarket clearance and approval, advertising and promotion, distribution and post-market surveillance of our medical devices and establishment of registration and device listing for our facilities.

Unless an exemption, pre-amendment grandfather status (that is, medical devices legally marketed in the U.S. before May 28, 1976) or FDA enforcement discretion applies, each medical device that we market in the U.S. must first receive either clearance as a Class I or, typically, a Class II device (after submitting a premarket notification (“510(k)”) or approval as a Class III device (after filing a premarket approval application (“PMA”)) from the FDA pursuant to the FDC Act. To obtain 510(k) clearance, a manufacturer must demonstrate to the FDA that the proposed device is substantially equivalent to a legally marketed device (a 510(k)-cleared device, a pre-amendment device for which FDA has not called for PMAs or a device with a de novo authorization), referred to as the "predicate device." Substantial equivalence is established by the applicant showing that the proposed device has the same intended use as the predicate device, and it either has the same technological characteristics or has been shown to be equally safe and effective and does not raise different questions of safety and effectiveness as compared to the predicate device. The FDA’s 510(k) clearance process requires regulatory competence to execute and usually takes four to nine months, but it can last longer. A device that is not eligible for the 510(k) process because there is no predicate device may be reviewed by the FDA through the de novo process (the process for granting marketing authorization when no substantially equivalent device exists) if the FDA agrees it is a low to moderate risk device. A device that is not exempt from premarket review and is not eligible for 510(k) clearance or de novo authorization is categorized as Class III and must follow the PMA approval pathway, which requires proof of the safety and effectiveness of the device to the FDA’s satisfaction. The process of obtaining PMA approval also requires specific regulatory competence and is more costly, lengthy and uncertain than the 510(k) or de novo

7

processes. The PMA process generally takes from one to three years or even longer. Our portfolio of existing products and pipeline of potential new products consist primarily of Class I (510(k) exempt) and Class II devices that require 510(k) clearance, although a few are 510(k)-exempt. In addition, certain modifications made to devices after they receive clearance or approval may require a new 510(k) clearance or approval of a PMA or PMA supplement. We cannot be sure that 510(k) clearance or PMA approval will be obtained in a timely matter if at all for any device that we propose to market.

A clinical trial is almost always required to support a PMA application and is sometimes required for a 510(k) clearance or a de novo authorization. The sponsor of a clinical trial must comply with and conduct the study in accordance with the applicable federal regulations, including FDA’s requirements for investigational device exemptions (“IDE”) requirements and good clinical practice (“GCP”). Clinical trials must also be approved by an institutional review board ("IRB"), which is an appropriately constituted group that has been formally designated to review biomedical research involving human subjects and which has the authority to approve, require modifications to, or disapprove research to protect the rights, safety, and welfare of human research subjects. The FDA may order the temporary or permanent hold or discontinuation of a clinical trial at any time, or impose other sanctions, if it believes that the clinical trial either is not being conducted in accordance with FDA requirements or presents an unacceptable risk to the clinical trial subjects. An IRB may also require the clinical trial to be halted at a given clinical trial site for failure to comply with the IRB’s requirements or to adequately ensure the protection of human subjects, or may impose other conditions. Conducting medical device clinical trials is a complex and costly activity and frequently requires the use of outsourced resources that specialize in planning, conducting and/or monitoring the clinical trial for the medical device manufacturer.

A device placed on the market must comply with numerous regulatory requirements. Those regulatory requirements include, but are not limited to, the following:

•device listing and establishment registration;

•adherence to the Quality System Regulation (“QSR”), which requires stringent design, testing, control, documentation, complaint handling and other quality assurance procedures;

•labeling, including advertising and promotion, requirements;

•prohibitions against the promotion of off-label uses or indications;

•adverse event and malfunction reporting (Medical Device Reports or "MDRs");

•post-approval restrictions or conditions, potentially including post-approval clinical trials or other required testing;

•post-market surveillance requirements;

•the FDA’s recall authority, whereby it can require or request the recall of products from the market; and

•reporting and documentation of voluntary corrections or removals.

The FDA has issued final regulations regarding the Unique Device Identification (“UDI”) System, which requires manufacturers to label or mark certain medical devices and/or their packaging with unique identifiers. Although the FDA expects that the UDI System will help track products during recalls and improve patient safety, it has required us to make changes to our manufacturing and labeling, which could increase our costs. The UDI System is being implemented in stages based on device risk, with the first requirements having taken effect in September 2014 and the last taking effect in September 2022.

Certain of our medical devices are sold in kits that include a drug component, such as lidocaine. These types of kits are generally regulated as combination products within the Center for Devices and Radiological Health ("CDRH") under the device regulations because the device provides the primary mode of action of the kit. Although the kit as a whole is regulated as a medical device, it may be subject to certain drug requirements such as current good manufacturing practices (“cGMPs”) and adverse drug experience reporting requirements, to the extent applicable to the drug-component repackaging activities and subject to inspection to verify compliance with cGMPs as well as other regulatory requirements.

Our manufacturing facilities, as well as those of certain of our suppliers, are subject to periodic and for-cause inspections by FDA personnel to verify compliance with the QSR (21 CFR Part 820) as well as other regulatory requirements. Similar inspections and audits are performed by Notified Bodies to verify compliance to applicable ISO standards (e.g. ISO 13485:2016), by auditing organizations under the Medical Device Single Audit Program

8

("MDSAP") applicable to regulatory requirements of Australia, Brazil, Canada, Japan and the U.S., and/or by regulatory authorities to verify compliance with medical device regulations and requirements from the countries in which we distribute product. If the FDA were to find that we or certain of our suppliers have failed to comply with applicable regulations, it could institute a wide variety of enforcement actions, ranging from issuance of a warning or untitled letter to more severe sanctions, such as product recalls or seizures, civil penalties, consent decrees, injunctions, criminal prosecution, operating restrictions, partial suspension or total shutdown of production, refusal to permit importation or exportation, refusal to grant, or delays in granting, clearances or approvals or withdrawal or suspension of existing clearances or approvals. The FDA also has the authority under certain circumstances to request repair, replacement or refund of the cost of any medical device manufactured or distributed by us. Any of these actions could have an adverse effect on our business.

Regulation of Medical Devices Outside of the U.S.

Medical device laws also are in effect in many of the markets outside of the U.S. in which we do business. These laws range from comprehensive device approval requirements for some or all of our products to requests for product data or certifications. Inspection of and controls over manufacturing, as well as monitoring of device-related adverse events, are components of most of these regulatory systems. Manufacturing certification requirements and audits through the MDSAP program or other regulatory authority inspections also apply. In addition, the European Union (“EU”) has adopted the EU Medical Device Regulation (the “EU MDR”), which imposes stricter requirements for the marketing and sale of medical devices (as compared to the predecessor Medical Device Directive (the "EU MDD")), including in the area of clinical evaluation requirements, quality systems, economic operators and post-market surveillance. The EU MDR went into effect in May 2021. As of the effective date, new and modified devices must be certified under, and be compliant with, the EU MDR. Devices that previously satisfied EU MDD requirements can continue to be marketed in the EU, subject to certain limitations, until the expiration of their current EU MDD certifications, which may be no later than May 2024. Failure to obtain EU MDR certifications prior to the expiration of existing EU MDD certifications may limit our ability to sell certain products in the EU until EU MDR certification is obtained. Additionally, certain EU MDR requirements will go into effect for all devices in May 2024. Failure to meet the applicable EU MDR requirements could adversely impact our business in the EU and other regions that tie their product registrations to the EU requirements.

Healthcare Laws

We are subject to various federal, state and local laws in the U.S. targeting fraud and abuse in the healthcare industry. These laws prohibit us from, among other things, soliciting, offering, receiving or paying any remuneration to induce the referral or use of any item or service reimbursable under Medicare, Medicaid or other federally or state financed healthcare programs. Violations of these laws are punishable by imprisonment, criminal fines, civil monetary penalties and exclusion from participation in federal healthcare programs. In addition, we are subject to federal and state false claims laws in the U.S. that prohibit the submission of false payment claims under Medicare, Medicaid or other federally or state funded programs. Certain marketing practices, such as off-label promotion, and violations of federal anti-kickback laws may also constitute violations of these laws.

In addition, we are subject to various federal and state reporting and disclosure requirements related to the healthcare industry. Rules issued by the Centers for Medicare & Medicaid Services ("CMS") require us to collect and report information on payments or transfers of value to physicians and teaching hospitals, as well as investment interests held by physicians and their immediate family members. Effective January 2022, we are also required to collect and report information on payments or transfers of value to physician assistants, nurse practitioners, clinical nurse specialists, certified registered nurse anesthetists and certified nurse-midwives. The reported data is available to the public on the CMS website. Failure to submit required information may result in civil monetary penalties. In addition, several states now require medical device companies to report expenses relating to the marketing and promotion of device products and to report gifts and payments to individual physicians in these states. Other states prohibit various other marketing-related activities. The federal government and certain other states require the posting of information relating to clinical studies and their outcomes. The shifting commercial compliance environment and the need to build and maintain robust and expandable systems to comply with the different compliance and/or reporting requirements among a number of jurisdictions increases the possibility that a healthcare company may violate one or more of the requirements, resulting in increased compliance costs that could adversely impact our results of operations.

Further, the Patient Protection and Affordable Care Act, as amended by the Health Care and Education Reconciliation Act (collectively, the “Affordable Care Act”), imposed regulatory mandates and other measures designed to contain the cost of healthcare, in addition to annual reporting and disclosure requirements on device

9

manufacturers for any “transfer of value” made or distributed to physicians or teaching hospitals. Violations of these laws are punishable by a range of fines, penalties and other sanctions.

Other Regulatory Requirements

We are also subject to the U.S. Foreign Corrupt Practices Act and similar anti-bribery laws applicable in jurisdictions outside the U.S. that generally prohibit companies and their intermediaries from improperly offering or paying anything of value to non-U.S. government officials for the purpose of obtaining or retaining business. Because of the predominance of government-sponsored healthcare systems around the world, most of our customer relationships outside of the U.S. are with government entities and are therefore subject to such anti-bribery laws. Our policies mandate compliance with these anti-bribery laws. We operate in many parts of the world that have experienced government corruption to some degree, and in certain circumstances, strict compliance with anti-bribery laws may conflict with local customs and practices. In the sale, delivery and servicing of our medical devices and software outside of the U.S., we must also comply with various export control and trade embargo laws and regulations, including those administered by the Department of Treasury’s Office of Foreign Assets Control (“OFAC”) and the Department of Commerce’s Bureau of Industry and Security (“BIS”) which may require licenses or other authorizations for transactions relating to certain countries and/or with certain individuals identified by the U.S. government. Despite our global trade and compliance program, our internal control policies and procedures may not always protect us from reckless or criminal acts committed by our employees, distributors or other agents. Violations of these requirements are punishable by criminal or civil sanctions, including substantial fines and imprisonment.

COMPETITION

The medical device industry is highly competitive. We compete with many companies, ranging from small start-up enterprises to companies that are larger and more established than us and have access to significantly greater financial resources. Furthermore, extensive product research and development and rapid technological advances characterize the market in which we compete. We must continue to develop and acquire new products and technologies for our businesses to remain competitive. We believe that we compete primarily on the basis of clinical superiority and innovative features that enhance patient benefit, product reliability, performance, customer and sales support, and cost-effectiveness.

SALES AND MARKETING

Our product sales are made directly to hospitals, healthcare providers, distributors and to original equipment manufacturers of medical devices through our own sales forces, independent representatives and independent distributor networks.

BACKLOG

Most of our products are sold to hospitals or healthcare providers on orders calling for delivery within a few days or weeks, with longer order times for products sold to medical device manufacturers. Therefore, our backlog of orders is not indicative of revenues to be anticipated in any future 12-month period.

PATENTS AND TRADEMARKS

We own a portfolio of patents, patents pending and trademarks. We also license various patents and trademarks. Patents for individual products extend for varying periods based upon the date of patent filing or grant and the legal term of patents in the various countries where patent protection is obtained. Trademark rights may potentially extend for longer periods of time and are dependent upon national laws and use of the marks. All product names throughout this document are trademarks owned by, or licensed to, us or our subsidiaries. Although these have been of value and are expected to continue to be of value in the future, we do not consider any single patent or trademark, except for the Teleflex name and the Arrow and UroLift brands, to be essential to the operation of our business.

SUPPLIERS AND MATERIALS

Materials used in the manufacture and sterilization of our products are purchased from a large number of suppliers in diverse geographic locations. We are not dependent on any single supplier for a substantial amount of the materials used, the components supplied and the sterilization services provided for our overall operations. Most of the materials, components and sterilization services we utilize are available from multiple sources, and where practical, we attempt to identify alternative suppliers. However, our ability to establish alternate sources of supply of materials and sterilization services may be delayed due to FDA and other regulatory authority requirements

10

regarding the manufacture and sterilization of our products. Volatility in commodity prices, and freight costs, can have a significant impact on the cost of producing and supplying certain of our products.

RESEARCH AND DEVELOPMENT

We are engaged in both internal and external research and development. Our research and development efforts support our strategic objectives to provide innovative new, safe and effective products that enhance clinical value by reducing infections, improving patient and clinician safety, enhancing patient outcomes and enabling less invasive procedures.

We also acquire or license products and technologies that are consistent with our strategic objectives and enhance our ability to provide a full range of product and service options to our customers.

SEASONALITY

Portions of our revenues are subject to seasonal fluctuations. Incidence of flu and other disease patterns and, to a lesser extent, the frequency of elective medical procedures affect revenues related to single-use products. Historically, we have experienced higher sales in the fourth quarter as a result of these factors.

HUMAN CAPITAL RESOURCES

As of December 31, 2021, we employed approximately 14,000 employees, including 4,000 employees in the U.S. and 10,000 employees in 31 other countries around the world. Our manufacturing employees make up 58% of the total employee population and are located primarily in Mexico, Malaysia and the Czech Republic. Our commercial organization comprises 25% of the employee base, located throughout the globe. The remaining 17% of employees work in various corporate functions, based in each of our locations.

We believe our employees are a significant differentiating factor and play a critical role in our ability to deliver on our commitments to patients and execute our strategy to our customers and shareholders. Our management team places significant focus and attention to matters affecting our people, particularly our commitment to our Core Values, capability development, total rewards and diversity, as well as how each employee experiences our culture.

Culture

The culture of our organization is critical to the human capital we attract, develop and retain and who, in turn, contribute to the results and success of our organization. Our culture is framed by our Core Values – building trust, entrepreneurial spirit and making our workplace fun, with people at the center of all we do. We strive to develop and sustain our culture by embedding these values in all aspects of our organization, including our human capital strategies.

Talent Management, Development and Learning

We are committed to providing our employees with opportunities for growth, development and career advancement and to building a high-performance culture that supports our Core Values throughout the employee lifecycle. We have implemented a talent management process that provides regular coaching check-ins between employees and their managers to review the employee’s developmental objectives and career progression. We also regularly review our talent portfolio and succession plans to ensure we can deliver on our company strategy.

In addition, we offer a number of internal educational and training resources to employees throughout our organization. Among these resources is the Teleflex Academy, a curriculum that provides learning opportunities for our employees to further develop their skills and receive training across broad subject areas such as leadership; communications; diversity, equity and inclusion; sales; customer service; and business acumen. We have recently implemented a diversity, equity and inclusion development program for all of our people managers within Teleflex to support our employees and continue to drive a culture of inclusion. Additionally, we provide support opportunities for diverse candidates through our Global Coaching and Mentoring Programs.

Diversity, Equity and Inclusion

We believe that diversity, equity, and inclusion (DEI) drives value for employees, patients, customers and shareholders by engaging a broad range of perspectives and experiences to enrich our offering to these communities. We are continuing to cultivate this diversity through the efforts of our Corporate DEI Council and four regional DEI councils (North America, Latin America, EMEA and APAC), whose goals include supporting the attraction, development and retention of diverse employees in alignment with our Core Values.

11

One pillar of our DEI platform includes sponsoring our globally expanding Employee Resource Groups (ERGs), which we initiated with Women Inspiring Learning and Leadership in 2016, and have expanded to include several other ERGs across our geographic regions. Examples of new initiatives in 2021 include the establishment of a women, parents and caregiver support group in our EMEA region and a young professional support group in our APAC region. Our ERGs are managed by employees and participation is open to all.

In our efforts to provide a diverse slate of candidates to our hiring managers, we deploy several recruitment channels to source talent from a variety of organizations including multiple social media outlets, co-op placement, local universities and technology institutes. We also work with numerous external recruiting firms that focus on diverse candidates and work to ensure diverse interviewing panels whenever possible.

Total Rewards

We actively manage our global compensation and benefit programs to ensure we can attract and retain the critical human capital we need to continue to deliver on our commitments to employees, customers, patients and shareholders. We believe our compensation offering is aligned to competitive market pay levels and, along with our culture and Core Values, acts to incentivize the right behaviors and actions to achieve the best results for the organization. We structure our compensation to include a mix of pay components of base salary, short-term cash incentives and long-term incentives. We offer our employees health, welfare and retirement benefits and have implemented policies addressing paid time off, flexible work schedules, employee assistance, parental leave and family benefits, among others.

In 2021, we engaged external consultants to perform an in-depth pay equity analysis on the pay practices within our organization. No systemic gender or ethnicity bias was identified within our compensation programs.

Environmental, Health and Safety

Our Environmental Health and Safety (EHS) vision is to protect the safety and health of Teleflex personnel and the environments in which we operate. We have a vested interest in protecting our most valuable assets – our employees. Everyone is a steward of EHS, fostering a culture of being actively responsible in all our operations. We remain fully committed to complying with all relevant EHS legislation and to achieving our vision. We have and will continue to expend resources to construct, maintain, operate and improve our facilities across the globe for environmental, health, safety and sustainability of our operations. For example, in response to the risks associated with the COVID-19 pandemic, we have expended resources to implement various safety measures, including implementing social distancing protocols and expanding personal protective equipment availability and usage, across our facilities globally in an effort to protect the health and safety of our employees and others. Further, we understand that our environment is both complex and delicate, and we prioritize managing and limiting the impact our business has on the environment as part of our Zero Harm Culture. In response to protecting the environment, we have initiated programs to track and lower our consumption of energy, water and gas as well as reduce waste and the use of hazardous materials. In addition, we have developed an EHS program focused in the areas of training our personnel with respect to, deploying and auditing global EHS standards as well as other programs to engage our employees on EHS initiatives.

ENVIRONMENTAL

We are subject to various environmental laws and regulations both within and outside the U.S. Our operations, like those of other medical device companies, involve the use of substances regulated under environmental laws, primarily in manufacturing and sterilization processes. While we continue to devote resources to compliance with existing environmental laws and regulations, we cannot ensure that our costs of complying with current or future environmental protection, health and safety laws and regulations will not exceed our estimates or will not have a material adverse effect on our business, financial condition, results of operations and cash flows. Further, we cannot ensure that we will not be subject to environmental claims for personal injury or cleanup in the future based on our past, present or future business activities.

INVESTOR INFORMATION

We are subject to the reporting requirements of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Therefore, we file reports, proxy statements and other information with the Securities and Exchange Commission (SEC). The SEC maintains a website (http://www.sec.gov) that contains reports, proxy and information statements and other information regarding issuers that file electronically with the SEC.

You can access financial and other information about us in the Investors section of our website, which can be accessed at www.teleflex.com. We make available through our website, free of charge, copies of our annual report

12

on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports filed with or furnished to the SEC under Section 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable after electronically filing or furnishing such material to the SEC. The information on our website is not part of this Annual Report on Form 10-K. The reference to our website address is intended to be an inactive textual reference only.

We are a Delaware corporation incorporated in 1943. Our executive offices are located at 550 East Swedesford Road, Suite 400, Wayne, PA 19087.

INFORMATION ABOUT OUR EXECUTIVE OFFICERS

The names and ages of our executive officers and the positions and offices held by each such officer are as follows:

| Name | Age | Positions and Offices with Company | ||||||||||||

| Liam J. Kelly | 55 | Chairman, President and Chief Executive Officer | ||||||||||||

| Thomas E. Powell | 60 | Executive Vice President and Chief Financial Officer | ||||||||||||

| Cameron P. Hicks | 57 | Corporate Vice President, Human Resources and Communications | ||||||||||||

| Daniel V. Logue | 48 | Corporate Vice President, General Counsel and Secretary | ||||||||||||

| Jay White | 48 | Corporate Vice President and President, Global Commercial | ||||||||||||

| James Winters | 49 | Corporate Vice President, Manufacturing and Supply Chain | ||||||||||||

Mr. Kelly has been our President and Chief Executive Officer since January 2018 and has been Chairman of our Board of Directors since May 2020. From May 2016 to December 31, 2017, Mr. Kelly served as our President and Chief Operating Officer. From April 2015 to April 2016, he served as Executive Vice President and Chief Operating Officer. From April 2014 to April 2015, Mr. Kelly served as Executive Vice President and President, Americas. From June 2012 to April 2014 Mr. Kelly served as Executive Vice President and President, International. He also has held several positions with regard to our EMEA segment, including President from June 2011 to June 2012, Executive Vice President from November 2009 to June 2011, and Vice President of Marketing from April 2009 to November 2009. Prior to joining Teleflex, Mr. Kelly held various senior level positions with Hill-Rom Holdings, Inc., a medical device company, from October 2002 to April 2009, serving as its Vice President of International Marketing and R&D from August 2006 to February 2009.

Mr. Powell has been our Executive Vice President and Chief Financial Officer since February 2013. From March 2012 to February 2013, Mr. Powell was Senior Vice President and Chief Financial Officer. He joined Teleflex in August 2011 as Senior Vice President, Global Finance. Prior to joining Teleflex, Mr. Powell served as Chief Financial Officer and Treasurer of Tomotherapy Incorporated, a medical device company, from June 2009 until June 2011. In 2008, he served as Chief Financial Officer of Textura Corporation, a software provider. From April 2001 until January 2008, Mr. Powell was employed by Midway Games, Inc., a software provider, serving as its Executive Vice President, Chief Financial Officer and Treasurer from September 2001 until January 2008. Mr. Powell has also held leadership positions with Dade Behring, Inc., PepsiCo, Bain & Company, Tenneco Inc. and Arthur Andersen & Company.

Mr. Hicks has been our Corporate Vice President, Human Resources and Communications since April 2013. Prior to joining Teleflex, Mr. Hicks served as Executive Vice President of Human Resources & Organizational Effectiveness for Harlan Laboratories, Inc., a private global provider of pre-clinical and non-clinical research services, from July 2010 to March 2013. From April 1990 to January 2010, Mr. Hicks held various leadership roles with MDS Inc., a provider of products and services for the development of drugs and the diagnosis and treatment of disease, including Senior Vice President of Human Resources for MDS’ global Pharma Services division from November 2000 to January 2010.

Mr. Logue has been our Corporate Vice President, General Counsel and Secretary since January 2021. Mr. Logue joined Teleflex in 2004 and previously held the positions of Deputy General Counsel from February 2017 to December 2020, Associate General Counsel from March 2013 to January 2017 and Assistant General Counsel from June 2004 to February 2013. Prior to joining Teleflex, Mr. Logue was an associate at the law firm of Pepper Hamilton LLP (now Troutman Pepper Hamilton Sanders LLP) from September 1999 to June 2004.

Mr. White has been our Corporate Vice President and President, Global Commercial since February 2021. From February 2017 to January 2021, Mr. White served as our President, The Americas, and from December 2013 to January 2017 he served as President and General Manager, Vascular. From January 2013 to November 2013,

13

Mr. White served as our President and General Manager, Surgical. Prior to that, he served as our Vice President and General Manager, Surgical from January 2010 to December 2012. Mr. White joined Teleflex in March 2005 as our Director of Marketing, North America. Prior to joining Teleflex, Mr. White worked at Covidien plc (now part of Medtronic plc) where he held senior leadership positions in sales and marketing over a five-year period.

Mr. Winters has been our Corporate Vice President, Manufacturing and Supply Chain since February 2020. He previously held the position of Vice President, Global Manufacturing from March 2018 to January 2020. Prior to joining Teleflex, Mr. Winters held various senior management and operational roles with the DePuy Synthes division of Johnson & Johnson, a healthcare company, from August 2005 to February 2018. Most recently, Mr. Winters served as Vice President of Global Manufacturing for Global Joint Reconstruction for DePuy Synthes from February 2015 to February 2018. Prior to that, Mr. Winters served as Plant Manager for the DePuy Synthes Ireland Manufacturing Operation.

Our officers are elected annually by our board of directors. Each officer serves at the discretion of the board.

ITEM 1A. RISK FACTORS

In addition to the other information set forth in this Annual Report on Form 10-K, you should carefully consider the following factors which could have a material adverse effect on our business, financial condition, results of operations, cash flows or stock price. The risks below are not the only risks we face. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial may also adversely affect our business, financial condition, results of operations or stock price.

Risks Relating to our Business and Operations

We face strong competition. Our failure to successfully develop and market new products could adversely affect our business.

The medical device industry is highly competitive. We compete with many domestic and foreign medical device companies ranging from small start-up enterprises that might sell only a single or limited number of competitive products or compete only in a specific market segment, to companies that are larger and more established than us, have a broad range of competitive products, participate in numerous markets and have access to significantly greater financial and marketing resources than we do.

In addition, the medical device industry is characterized by extensive product research and development and rapid technological advances. The future success of our business will depend, in part, on our ability to design and manufacture new competitive products and enhance existing products. Our product development efforts may require us to make substantial investments. There can be no assurance that we will be able to successfully develop new products, enhance existing products or achieve market acceptance of our products, due to, among other things, our inability to:

•identify viable new products;

•maintain sufficient liquidity to fund our investments in research and development and product acquisitions;

•obtain adequate intellectual property protection;

•gain market acceptance of new products; or

•successfully obtain regulatory approvals.

In addition, our competitors currently may be developing, or may develop in the future, products that provide better features, clinical outcomes or economic value than those that we currently offer or subsequently develop. Our failure to successfully develop and market new products or enhance existing products could have a material adverse effect on our business, financial condition and results of operations.

Our results of operations and financial condition may be adversely affected by public health epidemics, including the ongoing COVID-19 global health pandemic.

We are subject to risks associated with public health threats, including the ongoing COVID-19 pandemic. The COVID-19 pandemic has significantly impacted economic activity and markets around the world and has negatively impacted our operations, financial performance and cash flows. Because the severity, magnitude, and duration of the COVID-19 pandemic and its economic consequences are uncertain, rapidly changing and difficult to predict, the pandemic’s impact on our operations and financial performance, as well as its impact on our ability to execute our business strategies and initiatives successfully, remains uncertain and difficult to predict. Further, the ultimate

14

impact of the COVID-19 pandemic on our operations and financial performance depends on many factors that are not within our control, including, but not limited, to: governmental, business and individuals’ actions that have been and continue to be taken in response to the pandemic (including restrictions on travel, transport and workforce pressures, and deferrals or postponements of elective procedures); the impact of the pandemic and actions taken in response on global and regional economies, travel and economic activity; the availability of federal, state, local or non-U.S. funding programs; general economic uncertainty in key global markets and financial market volatility; global economic conditions and levels of economic growth; and the timing and pace of recovery when the COVID-19 pandemic subsides, which could be impacted by a number of factors, including limited provider capacity to perform procedures using our products that were deferred as a result of the pandemic.

The COVID-19 pandemic has subjected, and is expected to continue to subject, our operations, financial performance and financial condition to a number of risks, including, but not limited to those discussed below:

•It has resulted, and we expect it will continue to result, in lower revenues in certain of our product categories, including our interventional urology (which revenues are primarily concentrated in our Americas segment), surgical, interventional, anesthesia and OEM product categories, in which we sell products largely utilized in elective procedures, which have been significantly reduced or suspended due to the pandemic.

•It has resulted in higher revenues in our respiratory and vascular access product categories. However, we are unable to predict how long this increased demand will last or how significant it will be.

•It has caused and may continue to cause disruptions in the manufacture of our products. We rely on our major manufacturing operations located in the Czech Republic, Malaysia, Mexico and the U.S., to manufacture our products. The COVID-19 pandemic, and/or the governmental or regulatory actions taken in response to COVID-19 pandemic, may interfere with our ability, or that of our employees or suppliers to perform our and their respective responsibilities and obligations relative to the conduct of our business and create a risk to our ability to manufacture our products in a timely manner, or at all. We have experienced and expect to continue to experience inefficiencies in our manufacturing operations due to government-mandated and self-imposed restrictions placed on facilities in certain locations primarily in North America and Asia. Additionally, we have experienced and continue to experience a higher than normal level of absenteeism across our global manufacturing sites. In an effort to increase the wider availability of needed medical device products, we may elect to, or the government may require us to, allocate manufacturing capacity (for example, pursuant to the U.S. Defense Production Act) in a way that adversely affects our regular operations and financial results, results in differential treatment of customers and/or adversely affects our customer relationships and reputation.

•While we have not experienced significant payment defaults by, or identified other significant collectability concerns with, our customers to date, we may be adversely impacted by delays in payments of outstanding receivables if our customers experience financial difficulties or are unable to borrow money to fund their operations, which may adversely impact their ability to pay for our products on a timely basis, if at all.

•The COVID-19 pandemic, including related illness, border closures, travel restrictions, quarantines, lockdowns or other workforce disruptions, has generally had an adverse effect on macroeconomic conditions across the globe. Accordingly, this has impacted various aspects of our global supply chain, including causing logistical transport challenges for our freight transport providers, and has resulted in cost inflation. While we have not yet experienced significant disruptions in the global supply chain for our products that are in high demand, we have in some cases experienced lengthened delivery times, resulting in backorders for some of our products. These disruptions, or our failure to respond to them, could increase manufacturing or distribution costs or cause further delays in delivering, or an inability to deliver, products to our customers.

•The COVID-19 pandemic has increased volatility and pricing in the capital markets, and volatility is likely to continue. We might not be able to continue to access preferred sources of liquidity when we would like, and our borrowing costs could increase.

•As a U.S. federal government contractor, we are subject to a federal executive order requiring our U.S. employees to be vaccinated unless they qualify for medical or religious exemptions. The order has been challenged in court, and its ultimate status and impact on our business is uncertain. However, this requirement or other future vaccine mandates could adversely affect our workforce retention and hiring, which may adversely affect our business and results of operations, including through the disruption of our manufacturing and distribution operations.

These and other impacts of the COVID-19 pandemic, or other pandemics or epidemics, could have the effect of heightening many of the other risks described herein. We might not be able to predict or respond to all impacts on a timely basis to prevent near- or long-term adverse impacts to our results. However, these effects could have an

15

adverse impact on our liquidity, capital resources, operations and business and those of the third parties on which we rely, and such impact could be material.

Our customers depend on third party coverage and reimbursements, and the failure of healthcare programs to provide sufficient coverage and reimbursement for our medical products could adversely affect us.

The ability of our customers to obtain coverage and reimbursement for our products is important to our business. Demand for many of our existing and new medical products is, and will continue to be, affected by the extent to which government healthcare programs and private health insurers reimburse our customers for patients’ medical expenses in the countries where we do business. Even when we develop or acquire a promising new product, demand for the product may be limited unless reimbursement approval is obtained from private and government third party payors. Internationally, healthcare reimbursement systems vary significantly. In some countries, medical centers are constrained by fixed budgets, regardless of the volume and nature of patient treatment. Other countries require application for, and approval of, government or third party reimbursement. Without both favorable coverage determinations by, and the financial support of, government and third party insurers, the market for many of our medical products would be adversely affected. In this regard, we cannot be sure that third party payors will maintain the current level of coverage and reimbursement to our customers for use of our existing products. Adverse coverage determinations, including reductions in the amount of reimbursement, could harm our business by discouraging customers’ selection of, and reducing the prices they are willing to pay for, our products.

In addition, as a result of their purchasing power, third party payors have implemented and are continuing to implement cost cutting measures such as seeking discounts, price reductions or other incentives from medical products suppliers and imposing limitations on coverage and reimbursement for medical technologies and procedures. These trends could compel us to reduce prices for our products and could cause a decrease in the size of the market or a potential increase in competition that could negatively affect our business, financial condition and results of operations.

We are subject to extensive government regulation, which may require us to incur significant expenses to ensure compliance. Our failure to comply with those regulations could have a material adverse effect on our business, results of operations, financial condition and cash flows.

Our products are medical devices and are subject to extensive regulation in the U.S. by the FDA and by comparable government agencies in other countries. The regulations govern, among other things, the development, design, clinical testing, premarket clearance and approval, manufacturing, labeling, importing and exporting and sale and marketing of many of our products. Moreover, these regulations are subject to future change.

In the U.S., before we can market a new medical device, or a new use of, or claim for, or significant modification to, an existing product, we generally must first receive either 510(k) clearance or de novo authorization or approval of a premarket approval application, or PMA, from the FDA. Similarly, most major markets for medical devices outside the U.S. also require clearance, approval, authorization or compliance with certain standards before a product can be commercially marketed. In the EU, the EU MDR went into effect in May 2021 and includes significant additional pre- and post-market requirements. The process of obtaining regulatory clearances and approvals to market a medical device, particularly from the FDA and certain foreign government authorities, can be costly and time consuming, and clearances and approvals might not be granted for new products on a timely basis, if at all. In addition, once a device has been cleared or approved, a new clearance or approval may be required before the device may be modified or its labeling changed. Furthermore, the FDA or a foreign government authority may make its review and clearance or approval process more rigorous, which could require us to generate additional clinical or other data, and expend more time and effort, in obtaining future product clearances or approvals. The regulatory clearance and approval process may result in, among other things, delayed realization of product revenues, substantial additional costs or limitations on indicated uses of products, any one of which could have a material adverse effect on our financial condition and results of operations. Even after a product has received marketing approval or clearance, such product approval or clearance can be withdrawn or limited due to unforeseen problems with the device or issues relating to its application, or the FDA or a foreign government authority may change the classification of a product, which could require additional clinical studies and new marketing submissions.

Failure to comply with applicable regulations could lead to adverse effects on our business, which could include:

•partial suspension or total shutdown of manufacturing;

16

•product shortages;

•delays in product manufacturing;

•warning or untitled letters;

•fines or civil penalties;

•delays in or restrictions on obtaining new regulatory clearances or approvals;

•withdrawal or suspension of required clearances, approvals or licenses;

•product seizures or recalls;

•injunctions;

•criminal prosecution;

•advisories or other field actions;

•operating restrictions; and

•prohibitions against exporting of products to, or importing products from, countries outside the U.S.

We could be required to expend significant financial and human resources to remediate failures to comply with applicable regulations and quality assurance guidelines. In addition, civil and criminal penalties, including exclusion under Medicaid or Medicare, could result from certain regulatory violations. Any one or more of these events could have a material adverse effect on our business, financial condition and results of operations.

Medical devices are cleared or approved for one or more specific intended uses and performance claims must be adequately substantiated. Promoting a device for a use outside of the cleared or approved intended use or population, that is, an off-label use, or making false, misleading or unsubstantiated claims could result in government enforcement action.

Furthermore, our facilities are subject to periodic inspection by the FDA and other federal, state and foreign government authorities, which require manufacturers of medical devices to adhere to certain regulations, including the FDA’s Quality System Regulation ("QSR"), which requires, among other things, periodic audits, design controls, quality control testing and documentation procedures, as well as complaint evaluations and investigation. In addition, any facilities assembling kits that include drug components and are registered as drug repackaging establishments are also subject to current good manufacturing practices requirements for drugs. The FDA also requires the reporting of certain adverse events and product malfunctions and requires the reporting of certain recalls or other field safety corrective actions for medical devices. Issues identified through such inspections and reports may result in FDA enforcement action through any of the actions discussed above. Moreover, issues identified through such inspections and reports may require significant resources to resolve.

We are subject to healthcare fraud and abuse laws, regulation and enforcement; our failure to comply with those laws could have a material adverse effect on our results of operations and financial condition.

We are subject to healthcare fraud and abuse regulation and enforcement by the federal government and the governments of those states and foreign countries in which we conduct our business. The laws that may affect our ability to operate include:

•the federal healthcare anti-kickback statute, which, among other things, prohibits persons from knowingly and willfully offering or paying remuneration, one purpose of which is to induce either the referral of an individual for, or the purchase, order or recommendation of, any good or service for which payment may be made under federal healthcare programs such as Medicare and Medicaid, or soliciting payment for such referrals, purchases, orders and recommendations;

•federal false claims laws which, among other things, prohibit individuals or entities from knowingly presenting, or causing to be presented, false or fraudulent claims for payment from the federal government, including Medicare, Medicaid or other third-party payors;

•the federal Health Insurance Portability and Accountability Act of 1996 (“HIPAA”), which prohibits schemes to defraud any healthcare benefit program and false statements relating to healthcare matters; and

•state law equivalents of each of the above federal laws, such as anti-kickback and false claims laws which may apply to items or services reimbursed by any third-party payor, including commercial insurers.

If our operations are found to be in violation of any of these laws or any other government regulations, we may be subject to penalties, including civil and criminal penalties, damages, fines, the curtailment or restructuring of our

17

operations, the exclusion from participation in federal and state healthcare programs and imprisonment of personnel, any of which could adversely affect our ability to operate our business and our financial results. The risk of our being found to have violated these laws is increased by the fact that many of them have not been fully interpreted by the regulatory authorities or the courts, and their provisions are open to a variety of interpretations.

Further, the Affordable Care Act imposed annual reporting and disclosure requirements on device manufacturers for any “transfer of value” made or distributed to physicians or teaching hospitals. Effective January 2021, we are required to collect and report information on payments or transfers of value to physician assistants, nurse practitioners, clinical nurse specialists, certified registered nurse anesthetists (including anesthesiology assistants) and certified nurse-midwives. The reported information is made publicly available in a searchable format. In addition, device manufacturers are required to report and disclose any ownership or investment interests held by physicians and their immediate family members during the preceding calendar year. Failure to submit required information may result in civil monetary penalties for each payment, transfer of value or ownership or investment interests not reported in an annual submission, up to an aggregate of $150,000 per year (and up to an aggregate of $1 million per year for “knowing failures”).

There are also certain states, including Connecticut, Massachusetts, and Vermont, that require device manufacturers to track and report payments or transfers of value provided to certain health care providers and health care entities. In addition, some states, such as California, Connecticut, Nevada and Massachusetts, mandate implementation of compliance programs that include the tracking and reporting of gifts, compensation for consulting and other services, and other remuneration to healthcare providers. The shifting commercial compliance environment and the need to build and maintain robust and expandable systems to comply with the different compliance and/or reporting requirements among a number of jurisdictions increases the possibility that we may inadvertently violate one or more of the requirements, resulting in increased compliance costs that could adversely impact our results of operations.

We may not be successful in achieving expected operating efficiencies and sustaining or improving operating expense reductions, and may experience business disruptions associated with restructuring, facility consolidations, realignment, cost reduction and other strategic initiatives.

Over the past several years we have implemented a number of restructuring, realignment and cost reduction initiatives, including facility consolidations, organizational realignments and reductions in our workforce, and we may engage in similar efforts in the future. While we have realized some efficiencies from these initiatives, we may not realize the benefits of these or future initiatives to the extent we anticipated. Further, such benefits may be realized later than expected, and the ongoing difficulties in implementing these measures may be greater than anticipated, which could cause us to incur additional costs or result in business disruptions. In addition, if these measures are not successful or sustainable, we may be compelled to undertake additional restructuring, realignment and cost reduction efforts, which could result in significant additional charges. Moreover, if our restructuring, realignment and cost reduction efforts prove ineffective, our ability to achieve our strategic and business plan goals may be adversely affected.

In addition, as part of our efforts to increase operating efficiencies, we have implemented a number of initiatives over the past several years to consolidate our enterprise resource planning, or ERP, systems. To date, we have not experienced any significant disruptions to our business or operations in connection with these initiatives. However, as we continue our efforts to further consolidate our ERP systems, we could experience business disruptions, which could adversely affect customer relationships and divert the attention of management away from daily operations. In addition, any delays in the implementation of these initiatives could cause us to incur additional unexpected costs. Should we experience such difficulties, our business, cash flows and results of operations could be adversely affected.

Disruptions in sterilization of our products or regulatory initiatives further restricting the use of ethylene oxide in sterilization facilities could adversely affect our results of operations and financial condition.

Many of our products require sterilization prior to sale. A common method for sterilizing medical products involves the use of ethylene oxide, which is listed as a hazardous air pollutant under the Clean Air Act, as amended, and emissions of which are regulated by the U.S. Environmental Protection Agency ("EPA") and other regulatory authorities. One of our contract sterilizers, Sterigenics U.S., LLC, uses ethylene oxide in its sterilization process, including at its facilities in Smyrna, Cobb County, Georgia and Santa Teresa, New Mexico, which have sterilized some of our vascular, surgical, intermittent catheter and OEM products. During the fourth quarter of the year ended December 31, 2019, operations at the Smyrna facility were suspended by state and local officials due to issues

18

associated with the facility's use of ethylene oxide in its sterilization operations, but have since reopened. In December 2020, the New Mexico Attorney General initiated legal proceedings involving the Santa Teresa facility, alleging that its operations have resulted in impermissible ethylene oxide emissions. While both plants are currently operating normally, should their operations be suspended or adversely affected, our ability to provide affected products to our customers could be impaired if we are unable to utilize alternate facilities and sources for sterilization services.