The information in this preliminary pricing supplement is not complete and may be changed. We may not sell these Notes until the pricing supplement, the

accompanying product supplement, underlier supplement, prospectus supplement and prospectus (collectively, the “Offering Documents”) are delivered in final form. The Offering Documents are not an offer to sell these Notes and we are not soliciting

offers to buy these Notes in any state where the offer or sale is not permitted.

|

|

Subject to Completion

PRELIMINARY PRICING SUPPLEMENT

Dated May 7, 2024

Filed Pursuant to Rule 424(b)(2)

Registration Statement No. 333-261476

(To Prospectus dated December 29, 2021,

Prospectus Supplement dated December 29, 2021,

Underlier Supplement dated December 29, 2021

and Product Supplement dated December 29, 2021)

|

The Bank of Nova Scotia $• Trigger Autocallable Notes

Linked to the Nasdaq-100 Index® due on or about May 15, 2029

|

Investment Description

|

The Bank of Nova Scotia Trigger Autocallable Notes (the “Notes”) are senior unsecured debt securities issued by The Bank of Nova Scotia (“BNS” or the “issuer”) linked to the

Nasdaq-100 Index® (the “underlying asset”). BNS will automatically call the Notes early if the closing level of the underlying asset on any observation date (quarterly, callable after 12 months), including the final valuation date, is

equal to or greater than the call threshold level, which is equal to the closing level of the underlying asset on the trade date (the “initial level”). If the Notes are subject to an automatic call, BNS will pay on the applicable call settlement

date following such observation date a cash payment per Note equal to the “call price”, which is the principal amount plus a call return based on the call return rate, and no further payments will be owed to you under the Notes. The call return

increases the longer the Notes are outstanding. If the Notes are not subject to an automatic call and the closing level of the underlying asset on the final valuation date (the “final level”) is equal to or greater than the downside threshold, BNS

will pay you a cash payment per Note at maturity equal to the principal amount. If, however, the Notes are not subject to an automatic call and the final level is less than the downside threshold, BNS will pay you a cash payment per Note at

maturity that is less than the principal amount, if anything, resulting in a percentage loss on your principal amount equal to the percentage decline in the underlying asset from the trade date to the final valuation date (the “underlying return”)

and, in extreme situations, you could lose your entire investment in the Notes. Investing in the Notes involves significant risks. You will not receive a positive return if

the Notes are not automatically called and you may lose a significant portion or all of your investment. Higher call return rates are generally associated with a greater risk of loss and a greater risk that the Notes will not be subject to an

automatic call. Any payment on the Notes, including any repayment of principal, is subject to the creditworthiness of BNS. If BNS were to default on its payment obligations you may not receive any amounts

owed to you under the Notes and you could lose your entire investment in the Notes.

|

Features

|

|

❑

|

Automatic Call Feature — BNS will automatically call the Notes if the closing level of the underlying asset on any observation

date (quarterly, callable after 12 months), including the final valuation date, is equal to or greater than the call threshold level, which is equal to the initial level. If the Notes are subject to an automatic call, BNS will pay on

the applicable call settlement date a cash payment per Note equal to the call price for the relevant observation date. The call return increases the longer the Notes are outstanding. Following an automatic call, no further payments will

be owed to you under the Notes.

|

|

❑

|

Contingent Repayment of Principal at Maturity with Potential for Full Downside Market Exposure — If (i) the Notes have not been

subject to an automatic call at or prior to maturity and (ii) the final level is equal to or greater than the downside threshold, BNS will pay you a cash payment per Note at maturity equal to the principal amount. If, however, the Notes

are not subject to an automatic call and the final level is less than the downside threshold, BNS will pay you a cash payment per Note at maturity that is less than the principal amount, if anything, resulting in a percentage loss on

your principal amount equal to the underlying return and, in extreme situations, you could lose your entire investment in the Notes. The contingent repayment of principal applies only if you hold the Notes to maturity. Any payment on

the Notes, including any repayment of principal, is subject to the creditworthiness of BNS.

|

|

Key Dates*

|

|

Trade Date**

|

May 10, 2024

|

|

Settlement Date**

|

May 15, 2024

|

|

Observation Dates

|

Quarterly, callable after 12 months (see page 2)

|

|

Final Valuation Date

|

May 10, 2029

|

|

Maturity Date

|

May 15, 2029

|

|

*

|

Expected. See page P-2 for additional details.

|

|

**

|

We expect to deliver the Notes against payment on the third business day following the trade date. Under Rule 15c6-1 of the Securities Exchange Act of 1934, as amended,

trades in the secondary market generally are required to settle in two business days (T+2), unless the parties to a trade expressly agree otherwise. Accordingly, purchasers who wish to trade the Notes in the secondary market on any date

prior to two business days before delivery of the Notes will be required, by virtue of the fact that each Note initially will settle in three business days (T+3), to specify alternative settlement arrangements to prevent a failed

settlement of the secondary market trade.

|

Notice to investors: the Notes are significantly riskier than conventional debt instruments. The issuer is not necessarily obligated to repay the principal

amount of the Notes at maturity, and the Notes may have the same downside market risk as that of the underlying asset. This market risk is in addition to the credit risk inherent in purchasing a debt obligation of BNS. You should not purchase the

Notes if you do not understand or are not comfortable with the significant risks involved in investing in the Notes.

You should carefully consider the risks described under “Key Risks” beginning on page P-4 of this document and under “Additional Risk Factors

Specific to the Notes” beginning on page PS-6 of the accompanying product supplement and “Risk Factors” beginning on page S-2 of the accompanying prospectus supplement and on page 7 of the accompanying prospectus. Events relating to any of those

risks, or other risks and uncertainties, could adversely affect the market value of, and the return on, your Notes. You may lose a significant portion or all of your investment in the Notes. The Notes will not be listed or displayed on any

securities exchange or any electronic communications network.

| Note Offering |

The final terms of the Notes will be set on the trade date. The Notes are offered at a minimum investment of 100 Notes at $10 per Note (representing a $1,000 investment), and integral

multiples of $10 in excess thereof.

|

Underlying Asset

|

Bloomberg

Ticker

|

Call Return Rate*

|

Initial

Level

|

Call Threshold Level

|

Downside

Threshold

|

CUSIP

|

ISIN

|

|

Nasdaq-100 Index®

|

NDX

|

8.00% - 8.60% per annum

|

•

|

100.00% of the Initial Level

|

75.00% of the Initial Level

|

06418K215

|

US06418K2151

|

* The call return is based on the call return rate and will vary depending on whether, and if called, the call settlement date on which, the Notes are called.

The initial estimated value of your Notes at the time the terms of your Notes are set on the trade date is expected to be between $9.36 and $9.56 per principal amount, which will be

less than the issue price to public listed below. See “Additional Information Regarding Estimated Value of the Notes” herein and “Key Risks — Risks Relating to Estimated Value and Liquidity” beginning on page P-5 of this document for additional

information. The actual value of your Notes at any time will reflect many factors and cannot be predicted with accuracy.

See “Additional Information About BNS and the Notes” on page P-ii. The Notes will have the terms set forth in the accompanying product supplement, prospectus

supplement, underlier supplement and prospectus, each dated December 29, 2021, and this document.

Neither the Securities and Exchange Commission (the “SEC”) nor any other regulatory body has approved or disapproved of these Notes or passed upon the adequacy or

accuracy of this document, the accompanying product supplement, underlier supplement, prospectus supplement or prospectus. Any representation to the contrary is a criminal offense.

The Notes are not insured by the Canada Deposit Insurance Corporation (the “CDIC”) pursuant to the Canada Deposit Insurance Corporation Act (the “CDIC Act”) or the U.S. Federal

Deposit Insurance Corporation or any other government agency of Canada, the U.S. or any other jurisdiction. The Notes are not bail-inable debt securities under the CDIC Act.

|

Offering of Notes

|

Issue Price to Public

|

Underwriting Discount(1)(2)

|

Proceeds to The Bank of Nova Scotia(1)(2)

|

|||

|

Total

|

Per Note

|

Total

|

Per Note

|

Total

|

Per Note

|

|

|

Notes linked to the Nasdaq-100 Index®

|

$•

|

$10.00

|

$•

|

$0.25

|

$•

|

$9.75

|

|

(1)

|

Scotia Capital (USA) Inc. (“SCUSA”), our affiliate, will purchase the Notes at the principal amount and, as part of the distribution of the Notes, will sell the Notes to

UBS Financial Services Inc. (“UBS”) at the principal amount less the discount specified in the table above. See “Supplemental Plan of Distribution (Conflicts of Interest); Secondary Markets (if any)” herein for additional information.

|

|

(2)

|

This amount excludes any profits to BNS, SCUSA or any of our other affiliates from hedging. See “Key Risks — Risks Relating to Estimated Value and Liquidity” and “— Risks

Relating to Hedging Activities and Conflicts of Interest” and “Supplemental Plan of Distribution (Conflicts of Interest); Secondary Markets (if any)” herein for additional considerations relating to hedging activities.

|

|

Scotia Capital (USA) Inc.

|

UBS Financial Services Inc.

|

|

Additional Information About BNS and the Notes

|

You should read this pricing supplement together with the prospectus dated December 29, 2021, as supplemented by the prospectus supplement dated December 29,

2021, the underlier supplement dated December 29, 2021 and the product supplement (Market-Linked Notes, Series A) dated December 29, 2021, relating to our Senior Note Program, Series A, of which these Notes are a part. Capitalized terms used but

not defined in this pricing supplement will have the meanings given to them in the product supplement.

The Notes may vary from the terms described in the accompanying prospectus, prospectus supplement, underlier supplement and product supplement in several

important ways. You should read this pricing supplement carefully, including the documents incorporated by reference herein. In the event of any conflict between this pricing supplement and any of the foregoing, the following hierarchy will govern:

first, this pricing supplement; second, the accompanying product supplement; third, the accompanying underlier supplement; fourth, the accompanying prospectus supplement; and last, the accompanying prospectus. You may access these documents on the

SEC website at www.sec.gov as follows (or if that address has changed, by reviewing our filings for the relevant date on the SEC website).

This pricing supplement, together with the documents listed below, contains the terms of the Notes and supersedes all prior or contemporaneous oral statements

as well as any other written materials including preliminary or indicative pricing terms, correspondence, trade ideas, structures for implementation, sample structures, brochures or other educational materials of ours. You should carefully

consider, among other things, the matters set forth in “Key Risks” herein, in “Additional Risk Factors Specific to the Notes” of the accompanying product supplement and in “Risk Factors” of the accompanying prospectus supplement and of the

accompanying prospectus, as the Notes involve risks not associated with conventional debt securities.

We urge you to consult your investment, legal, tax, accounting and other advisors concerning an investment in the Notes in light of your particular circumstances.

You may access these documents on the SEC website at www.sec.gov as follows:

Product Supplement (Market-Linked Notes, Series A) dated December 29, 2021:

Underlier Supplement dated December 29, 2021:

Prospectus Supplement dated December 29, 2021:

Prospectus dated December 29, 2021:

References to “BNS”, “we”, “our” and “us” refer only to The Bank of Nova Scotia and not to its consolidated subsidiaries and references to the “Trigger

Autocallable Notes” or the “Notes” refer to the Notes that are offered hereby. Also, references to the “accompanying product supplement” mean the BNS product supplement, dated December 29, 2021, references to the “accompanying underlier supplement”

mean the BNS underlier supplement, dated December 29, 2021, references to the “accompanying prospectus supplement” mean the BNS prospectus supplement, dated December 29, 2021 and references to the “accompanying prospectus” mean the BNS prospectus,

dated December 29, 2021.

BNS reserves the right to change the terms of, or reject any offer to purchase, the Notes prior to their issuance. In the event of any changes to the terms of the Notes, BNS will

notify you and you will be asked to accept such changes in connection with your purchase. You may also choose to reject such changes in which case BNS may reject your offer to purchase.

P-ii

|

Investor Suitability

|

The Notes may be suitable for you if:

|

♦

|

You fully understand and are willing to accept the risks inherent in an investment in the Notes, including the risk of loss of a significant portion or all of your investment in the

Notes.

|

|

♦

|

You can tolerate a loss of a significant portion or all of your investment and are willing to make an investment that may have the same downside market risk as that of a hypothetical

investment in the underlying asset or the stocks comprising the underlying asset (the “underlying constituents”).

|

|

♦

|

You are willing to invest in the Notes based on the call threshold level and downside threshold indicated on the cover hereof.

|

|

♦

|

You believe that the closing level of the underlying asset will be equal to or greater than the call threshold level on one of the specified observation dates, including the final

valuation date, and you believe that the level of the underlying asset will increase over the term of the Notes by a percentage that is less than the applicable call return.

|

|

♦

|

You understand and accept that you will not earn any positive return unless the Notes are automatically called, you will not participate in any increase in the level

of the underlying asset beyond the applicable call return, and you are willing to invest in the Notes if the call return rate was set equal to the bottom of the range indicated on the cover hereof (the actual call return rate will be

set on the trade date).

|

|

♦

|

You can tolerate fluctuations in the price of the Notes prior to maturity that may be similar to or exceed the downside fluctuations in the level of the underlying asset.

|

|

♦

|

You do not seek guaranteed current income from your investment and are willing to forgo any dividends paid on the underlying constituents.

|

|

♦

|

You are willing to invest in Notes that may be subject to an automatic call and you are otherwise willing to hold such Notes to maturity and you accept that there may be little or no

secondary market for the Notes.

|

|

♦

|

You understand and are willing to accept the risks associated with the underlying asset.

|

|

♦

|

You are willing to assume the credit risk of BNS for all payments under the Notes, and understand that if BNS defaults on its obligations you may not receive any amounts due to you

including any repayment of principal.

|

The Notes may not be suitable for you if:

|

♦

|

You do not fully understand or are not willing to accept the risks inherent in an investment in the Notes, including the risk of loss of a significant portion or all of your investment

in the Notes.

|

|

♦

|

You require an investment designed to provide a full return of principal at maturity.

|

|

♦

|

You cannot tolerate a loss of a significant portion or all of your investment or are unwilling to make an investment that may have the same downside market risk as that of a hypothetical

investment in the underlying asset or the underlying constituents.

|

|

♦

|

You are unwilling to invest in the Notes based on the call threshold level or downside threshold specified on the cover hereof.

|

|

♦

|

You believe that the level of the underlying asset will decline during the term of the Notes and that the closing level will be less than the call threshold level on the specified

observation dates, including the final valuation date, or you believe that the level of the underlying asset will increase over the term of the Notes by a percentage that is greater than the applicable call return.

|

|

♦

|

You believe that the final level will be less than the downside threshold.

|

|

♦

|

You seek an investment that participates in the full increase in the level of the underlying asset or that has unlimited return potential, or you are unwilling to invest in the Notes if

the call return rate was set equal to the bottom of the range indicated on the cover hereof (the actual call return rate will be set on the trade date).

|

|

♦

|

You cannot tolerate fluctuations in the price of the Notes prior to maturity that may be similar to or exceed the downside fluctuations in the level of the underlying

asset.

|

|

♦

|

You seek guaranteed current income from this investment or prefer to receive any dividends paid on the underlying constituents.

|

|

♦

|

You are unable or are unwilling to invest in Notes that may be subject to an automatic call, you are otherwise unable or unwilling to hold the Notes to maturity or you seek an investment

for which there will be an active secondary market for the Notes.

|

|

♦

|

You do not understand or are unwilling to accept the risks associated with the underlying asset.

|

|

♦

|

You are unwilling to assume the credit risk of BNS for all payments under the Notes, including any repayment of principal.

|

The suitability considerations identified above are not exhaustive. Whether or not the Notes are a suitable investment for you will depend on your individual circumstances and you

should reach an investment decision only after you and your investment, legal, tax, accounting and other advisors have carefully considered the suitability of an investment in the Notes in light of your particular circumstances. You should review

“Information About the Underlying Asset” herein for more information on the underlying asset. You should also review carefully the “Key Risks” section herein and the more detailed “Additional Risk Factors Specific to the Notes” in the accompanying

product supplement for risks related to an investment in the Notes.

P-1

| Preliminary Terms |

|

Issuer

|

The Bank of Nova Scotia

|

|

Issue

|

Senior Note Program, Series A

|

|

Agents

|

Scotia Capital (USA) Inc. (“SCUSA”) and UBS Financial Services Inc. (“UBS”). See “Supplemental Plan of Distribution (Conflicts of Interest);

Secondary Markets (if any)” herein for additional information.

|

|

Principal

Amount

|

$10 per Note

|

|

Term

|

Approximately 5 years, unless subject to an automatic call. In the event that we make any change to the expected trade date and settlement date, the calculation agent may

adjust the observation dates (including the final valuation date), as well as the potential call settlement dates (including the maturity date) to ensure that the stated term of the Notes remains the same.

|

|

Underlying

Asset |

The Nasdaq-100 Index®

|

|

Automatic

Call Feature

|

BNS will automatically call the Notes if the closing level of the underlying asset on any observation date (quarterly, callable after 12 months), including the final

valuation date, is equal to or greater than the call threshold level.

If the Notes are subject to an automatic call, BNS will pay on the call settlement date a cash payment per Note equal to the call price for the relevant observation date.

Following an automatic call, no further payments will be made on the Notes.

|

|

Call Return

Rate |

The call return rate will be between 8.00% – 8.60% per annum (the actual call return rate will be set on the trade date).

|

|

Call Return

|

As set forth in the table below. The call return increases the longer the Notes are outstanding and is based upon the call return rate (the actual call return rate will be

set on the trade date).

|

|

Call Price

|

The call price equals the principal amount per Note plus the applicable call return.

|

The table below assumes a call return rate of 8.00% per annum (the bottom of the range indicated on the cover hereof). The actual call return rate and call

return will be set on the trade date.

|

Observation Date(1)

|

Call Settlement

Date(1)(2)

|

Call

Return

|

Call Price

(per Note) |

|

May 16, 2025

|

May 20, 2025

|

8.00%

|

$10.80

|

|

August 11, 2025

|

August 13, 2025

|

10.00%

|

$11.00

|

|

November 10, 2025

|

November 13, 2025

|

12.00%

|

$11.20

|

|

February 10, 2026

|

February 12, 2026

|

14.00%

|

$11.40

|

|

May 11, 2026

|

May 13, 2026

|

16.00%

|

$11.60

|

|

August 10, 2026

|

August 12, 2026

|

18.00%

|

$11.80

|

|

November 10, 2026

|

November 13, 2026

|

20.00%

|

$12.00

|

|

February 10, 2027

|

February 12, 2027

|

22.00%

|

$12.20

|

|

May 10, 2027

|

May 12, 2027

|

24.00%

|

$12.40

|

|

August 10, 2027

|

August 12, 2027

|

26.00%

|

$12.60

|

|

November 10, 2027

|

November 15, 2027

|

28.00%

|

$12.80

|

|

February 10, 2028

|

February 14, 2028

|

30.00%

|

$13.00

|

|

May 10, 2028

|

May 12, 2028

|

32.00%

|

$13.20

|

|

August 10, 2028

|

August 14, 2028

|

34.00%

|

$13.40

|

|

November 10, 2028

|

November 14, 2028

|

36.00%

|

$13.60

|

|

February 12, 2029

|

February 14, 2029

|

38.00%

|

$13.80

|

|

Final Valuation Date

|

Maturity Date

|

40.00%

|

$14.00

|

| (1) |

Subject to the market disruption event provisions set forth under “General Terms of the Notes—Unavailability of the Closing Value of a Reference Asset; Adjustments to a Reference Asset — Unavailability of the

Closing Value of a Reference Index; Alternative Calculation Methodology” and “General Terms of the Notes— Market Disruption Events” in the accompanying product supplement.

|

| (2) |

If any observation date is postponed, the related call settlement date will be postponed such that the number of business days between the observation date and the call settlement date remain the same. If a call

settlement date is not a business day, such date will be the next following business day.

|

|

Payment at

Maturity

(per Note)

|

If the Notes are not subject to an automatic call and the final level is equal to or greater than the downside threshold, BNS

will pay you a cash payment equal to:

Principal Amount of $10

If the Notes are not subject to an automatic call and the final level is less than the downside threshold, BNS will pay you a cash

payment that is less than the principal amount, if anything, equal to:

$10 × (1 + Underlying Return)

In this case, you will suffer a percentage loss on your principal amount equal to the underlying return and, in extreme situations,

you could lose your entire investment in the Notes.

|

|

Underlying

Return

|

The quotient, expressed as a percentage, of the following formula:

|

|

Call

Threshold

Level(1)

|

A specified level of the underlying asset that is equal to the initial level, as specified on the cover hereof.

|

|

Downside

Threshold(1)

|

A specified level of the underlying asset that is less than the initial level, equal to a percentage of the initial level, as specified on the cover hereof.

|

|

Initial Level(1)

|

The closing level of the underlying asset on the trade date.

|

|

Final Level(1)

|

The closing level of the underlying asset on the final valuation date.

|

|

Trading Day

|

As specified in the product supplement under “General Terms of the Notes — Special Calculation Provisions — Trading Day”.

|

|

Business Day

|

A day other than a Saturday or Sunday or a day on which banking institutions in New York City are authorized or required by law to close

|

|

Tax

Redemption

|

Notwithstanding anything to the contrary in the accompanying product supplement, the provision set forth under “General Terms of the Notes — Payment of Additional Amounts”

and “General Terms of the Notes — Tax Redemption” shall not apply to the Notes.

|

|

Canadian

Bail-in

|

The Notes are not bail-inable debt securities under the CDIC Act.

|

|

Terms

Incorporated

|

All of the terms appearing above the item under the caption “General Terms of the Notes” in the accompanying product supplement, as modified by this pricing supplement, and

for purposes of the foregoing, references herein to “underlying asset”, “underlying constituents”, “closing level”, “underlying return”, “downside threshold” and “observation dates” mean “reference asset”, “reference asset constituents”,

“closing value”, “reference asset return”, “barrier value” and “valuation dates”, respectively, each as defined in the accompanying product supplement. In addition to those terms, the following two sentences are also so incorporated into

the master note: BNS confirms that it fully understands and is able to calculate the effective annual rate of interest applicable to the Notes based on the methodology for calculating per annum rates provided for in the Notes. BNS

irrevocably agrees not to plead or assert Section 4 of the Interest Act (Canada), whether by way of defense or otherwise, in any proceeding relating to the Notes.

|

(1) As determined by the calculation agent and as may be adjusted as described under “General Terms of the Notes — Unavailability of the Closing Value of a Reference

Asset; Adjustments to a Reference Asset — Unavailability of the Closing Value of a Reference Index; Alternative Calculation Methodology”, as described in the accompanying product supplement.

P-2

|

Investment Timeline

|

|

Trade Date

|

The initial level of the underlying asset is observed and the final terms of the Notes are set.

|

|

|

||

|

Observation Dates

(Quarterly, callable

after 12 months) |

The Notes will be subject to an automatic call if the closing level of the underlying asset on any observation date (quarterly, callable after 12

months), including the final valuation date, is equal to or greater than the call threshold level.

If the Notes are subject to an automatic call, BNS will pay on the call settlement date a cash payment per Note equal to the call price for the relevant

observation date. Following an automatic call, no further payments will be made on the Notes.

|

|

| |

||

|

Maturity Date

|

The final level is observed on the final valuation date and the underlying return is calculated.

If the Notes are not subject to an automatic call and the final level is equal to or greater than the downside

threshold, BNS will pay you a cash payment per Note at maturity equal to:

Principal Amount of $10

If the Notes are not subject to an automatic call and the final level is less than the downside threshold, BNS will pay you a cash payment per Note at maturity that is less than the principal amount, if anything, equal to:

$10 × (1 + Underlying Return)

In this case, you will suffer a percentage loss on your principal amount equal to the underlying return and, in

extreme situations, you could lose your entire investment in the Notes.

|

Investing in the Notes involves significant risks. You may lose a significant portion or all of your investment in the Notes. Any payment on the Notes, including any repayment of principal, is

subject to the creditworthiness of BNS. If BNS were to default on its payment obligations, you may not receive any amounts owed to you under the Notes and you could lose your entire investment in the Notes.

If the Notes are not subject to an automatic call, you may lose a significant portion or all of your investment. Specifically, if the Notes are not subject to an automatic call and

the final level is less than the downside threshold, you will lose a percentage of your principal amount equal to the underlying return and, in extreme situations, you could lose your entire investment in the Notes.

P-3

|

Key Risks

|

An investment in the offering of the Notes involves significant risks. Investing in the Notes is not equivalent to a hypothetical investment in the underlying asset or underlying

constituents. Some of the key risks that apply to the Notes are summarized below, but we urge you to read the more detailed explanation of risks relating to the Notes under “Additional Risk Factors Specific to the Notes” of the accompanying product

supplement and “Risk Factors” of the accompanying prospectus supplement and of the accompanying prospectus. We also urge you to consult your investment, legal, tax, accounting and other advisors concerning an investment in the Notes in light of your

particular circumstances.

Risks Relating to Return Characteristics

| ♦ |

Risk of loss at maturity — The Notes differ from ordinary debt securities in that BNS will not make periodic coupon payments and will not necessarily repay the principal

amount of the Notes at maturity. If the Notes are not subject to an automatic call and the final level is less than the downside threshold, you will lose a percentage of your principal amount equal to the underlying return and, in extreme

situations, you could lose your entire investment in the Notes.

|

| ♦ |

The contingent repayment of principal applies only at maturity — You should be willing to hold your Notes to an automatic call or maturity. If you are able to sell your

Notes prior to an automatic call or maturity in the secondary market, you may have to sell them at a loss relative to your investment even if the then-current level of the underlying asset is equal to or greater than the downside threshold

and call threshold level. All payments on the Notes are subject to the creditworthiness of BNS.

|

| ♦ |

No interest payments — BNS will not pay any interest with respect to the Notes.

|

| ♦ |

Your potential return on the Notes is limited to any call return and you will not participate in any increase in the level of the underlying asset or any underlying constituent —

The return potential of the Notes is limited to the pre-specified call return resulting from an automatic call regardless of any increase in the level of the underlying asset. Investors will not participate in any increase in the closing

level of the underlying asset from the initial level beyond the call return, if applicable, which may be significant. The Notes will be subject to an automatic call only if the closing level of the underlying asset on any observation date

(including the final valuation date) is equal to or greater than the call threshold level. In addition, because the call return increases the longer the Notes have been outstanding, the call price payable with respect to earlier observation

dates is less than the call price payable with respect to later observation dates. The earlier the Notes are subject to an automatic call, if at all, the lower your return will be. Because the Notes may be subject to an automatic call as

early as the first potential call settlement date, the total return on the Notes could be less than if the Notes remained outstanding until maturity. Furthermore, if the Notes are not subject to an automatic call, you will not receive any

positive return and you will be fully exposed to the decline in the level of the underlying asset if the final level is less than the downside threshold. In addition, as an owner of the Notes, you will not have voting rights or any other

rights of a holder of any underlying constituent.

|

| ♦ |

A higher call return rate or lower downside threshold or call threshold level may reflect greater expected volatility of the underlying asset, and greater expected volatility

generally indicates an increased risk of loss at maturity — The economic terms for the Notes, including the call return rate, call threshold level and downside threshold, are based, in part, on the expected volatility of the

underlying asset at the time the terms of the Notes are set. “Volatility” refers to the frequency and magnitude of changes in the level of the underlying asset. The greater the expected volatility of the underlying asset as of the trade date,

the greater the expectation is as of that date that the closing level or the final level, as applicable, of the underlying asset could be less than the call threshold level on any observation date (including the final valuation date) and that

the final level could be less than the downside threshold and, as a consequence, indicates an increased risk of the Notes not being subject to an automatic call and an increased risk of loss, respectively. All things being equal, this greater

expected volatility will generally be reflected in a higher call return rate than the yield payable on our conventional debt securities with a similar maturity or on otherwise comparable securities, and/or a lower downside threshold and/or

call threshold level than those terms on otherwise comparable securities. Therefore, a relatively higher call return rate may indicate an increased risk of loss. Further, a relatively lower downside threshold and/or call threshold level may

not necessarily indicate that the Notes have a greater likelihood of a return of principal at maturity and/or being automatically called. You should be willing to accept the downside market risk as that of the underlying asset and the

potential to lose a significant portion or all of your investment in the Notes.

|

| ♦ |

Reinvestment risk — The Notes will be subject to an automatic call if the closing level of the underlying asset is equal to or greater than the call threshold level on any

observation date (including the final valuation date). Because the Notes could be subject to an automatic call as early as the first potential call settlement date, the term of your investment may be limited. In the event that the Notes are

subject to an automatic call, there is no guarantee that you would be able to reinvest the proceeds at a comparable return and/or with a comparable call return rate for a similar level of risk. In addition, to the extent you are able to

reinvest such proceeds in an investment comparable to the Notes, you may incur transaction costs such as dealer discounts and hedging costs built into the price of the new securities. Generally, however, the longer the Notes remain

outstanding, the less likely the Notes will be subject to an automatic call due to the decline in the level of the underlying asset and the shorter time remaining for the level of the underlying asset to recover. Such periods generally

coincide with a period of greater risk of principal loss on your Notes.

|

P-4

Risks Relating to Characteristics of the Underlying Asset

| ♦ |

Market risk — The return on the Notes, which may be negative, is directly linked to the performance of the underlying asset and indirectly linked to the value of the

underlying constituents. The level of the underlying asset can rise or fall sharply due to factors specific to the underlying asset and its underlying constituents and their issuers (each, an “underlying constituent issuer”), such as stock

price volatility, earnings and financial conditions, corporate, industry and regulatory developments, management changes and decisions and other events, as well as general market factors, such as general stock market or commodity market

volatility and levels, interest rates and economic, political and other conditions. You, as an investor in the Notes, should conduct your own investigation into the underlying asset and underlying constituents.

|

| ♦ |

There can be no assurance that the investment view implicit in the Notes will be successful — It is impossible to predict whether and the extent to which the level of the

underlying asset will rise or fall and there can be no assurance that the closing level or the final level, as applicable, of the underlying asset will be equal to or greater than the call threshold level on any observation date, including

the final valuation date. The level of the underlying asset will be influenced by complex and interrelated political, economic, financial and other factors that affect the underlying constituent issuers. You should be willing to accept the

downside risks associated with the relevant market(s) tracked by the underlying asset in general and the underlying constituents in particular, and the risk of losing a significant portion or all of your investment.

|

| ♦ |

The underlying asset reflects price return, not total return — The return on your Notes is based on the performance of the underlying asset, which reflects the changes in

the market prices of the underlying constituents. Your Notes are not, however, linked to a “total return” index or strategy, which, in addition to reflecting those price returns, would also reflect any dividends paid on the underlying

constituents. The return on your Notes will not include such a total return feature or any dividend component.

|

| ♦ |

The Notes are subject to risks associated with non-U.S. securities — The Notes are subject to risks associated with non-U.S. securities because the underlying asset is

comprised, in part, of non-U.S. companies. Market developments may affect non-U.S. markets differently from U.S. securities markets and direct or indirect government intervention to stabilize these non-U.S. markets, as well as cross

shareholdings in non-U.S. companies, may affect trading prices and volumes in those markets. Securities issued by non-U.S. companies are subject to political, economic, financial and social factors that may be unique to the particular

country. These factors, which could negatively affect the applicable underlying constituents include the possibility of recent or future changes in the non-U.S. government’s economic and fiscal policies, the possible imposition of, or changes

in, currency exchange laws or other non-U.S. laws or restrictions applicable to non-U.S. companies or investments in non-U.S. equity securities and the possibility of fluctuations in the rate of exchange between currencies. Moreover, certain

aspects of a particular non-U.S. economy may differ favorably or unfavorably from the U.S. economy in important respects, such as growth of gross national product, rate of inflation, capital reinvestment, resources and self-sufficiency.

|

| ♦ |

BNS and the Agents cannot control actions by the index sponsor and the index sponsor has no obligation to consider your interests — None of BNS, UBS or our or their

respective affiliates are affiliated with the index sponsor or have any ability to control or predict its actions, including any errors in or discontinuation of public disclosure regarding methods or policies relating to the calculation of

the underlying asset. The index sponsor is not involved in the Notes offering in any way and has no obligation to consider your interest as an owner of the Notes in taking any actions that might affect the market value of, and any amount

payable on, the Notes.

|

| ♦ |

Changes affecting the underlying asset could have an adverse effect on the market value of, and any amount payable on, the Notes — The policies of the index sponsor as

specified under “Information About the Underlying Asset” (the “index sponsor”), concerning additions, deletions and substitutions of the underlying constituents and the manner in which the index sponsor takes account of certain changes

affecting those underlying constituents may adversely affect the level of the underlying asset. The policies of the index sponsor with respect to the calculation of the underlying asset could also adversely affect the level of the underlying

asset. The index sponsor may discontinue or suspend calculation or dissemination of the underlying asset. Any such actions could have an adverse effect on the market value of, and any amount payable on, the Notes.

|

Risks Relating to Estimated Value and Liquidity

| ♦ |

BNS’ initial estimated value of the Notes at the time of pricing (when the terms of your Notes are set on the trade date) will be lower than the issue price of the Notes —

BNS’ initial estimated value of the Notes is only an estimate. The issue price of the Notes will exceed BNS’ initial estimated value. The difference between the issue price of the Notes and BNS’ initial estimated value reflects costs

associated with selling and structuring the Notes, as well as hedging its obligations under the Notes. Therefore, the economic terms of the Notes are less favorable to you than they would have been if these expenses had not been paid or had

been lower.

|

| ♦ |

Neither BNS’ nor SCUSA’s estimated value of the Notes at any time is determined by reference to credit spreads or the borrowing rate BNS would pay for its conventional fixed-rate

debt securities — BNS’ initial estimated value of the Notes and SCUSA’s estimated value of the Notes at any time are determined by reference to BNS’ internal funding rate. The internal funding rate used in the determination of the

estimated value of the Notes generally represents a discount from the credit spreads for BNS’ conventional fixed-rate debt securities and the borrowing rate BNS would pay for its conventional fixed-rate debt securities. This discount is based

on, among other things, BNS’ view of the funding value of the Notes as well as the higher issuance, operational and ongoing liability management costs of the Notes in comparison to those costs for BNS’ conventional fixed-rate debt. If the

interest rate implied by the credit spreads for BNS’ conventional fixed-rate debt securities, or the borrowing rate BNS would pay for its conventional fixed-rate debt securities were to be used, BNS would expect the economic terms of the

Notes to be more favorable

|

P-5

to you. Consequently, the use of an internal funding rate for the Notes increases the estimated value of the Notes at any time and has an adverse

effect on the economic terms of the Notes.

| ♦ |

BNS’ initial estimated value of the Notes does not represent future values of the Notes and may differ from others’ (including SCUSA’s) estimates — BNS’ initial estimated

value of the Notes is determined by reference to its internal pricing models when the terms of the Notes are set. These pricing models consider certain factors, such as BNS’ internal funding rate on the trade date, the expected term of the

Notes, market conditions and other relevant factors existing at that time, and BNS’ assumptions about market parameters, which can include volatility of the underlying asset, dividend rates, interest rates and other factors. Different pricing

models and assumptions (including the pricing models and assumptions used by SCUSA) could provide valuations for the Notes that are different, and perhaps materially lower, from BNS’ initial estimated value. Therefore, the price at which

SCUSA would buy or sell your Notes (if SCUSA makes a market, which it is not obligated to do) may be materially lower than BNS’ initial estimated value. In addition, market conditions and other relevant factors in the future may change, and

any assumptions may prove to be incorrect.

|

| ♦ |

The Notes have limited liquidity — The Notes will not be listed on any securities exchange or automated quotation system. Therefore, there may be little or no secondary

market for the Notes. SCUSA and any other affiliates of BNS intend, but are not required, to make a market in the Notes. Even if there is a secondary market, it may not provide enough liquidity to allow you to trade or sell the Notes easily.

Because we do not expect that other broker-dealers will participate in the secondary market for the Notes, the price at which you may be able to trade your Notes is likely to depend on the price, if any, at which SCUSA is willing to purchase

the Notes from you. If at any time SCUSA does not make a market in the Notes, it is likely that there would be no secondary market for the Notes. Accordingly, you should be willing to hold your Notes to maturity.

|

| ♦ |

The price at which SCUSA would buy or sell the Notes (if SCUSA makes a market, which it is not obligated to do) will be based on SCUSA’s estimated value of the Notes and may be

greater than BNS’ valuation of the Notes at that time, greater than any other secondary market prices provided by unaffiliated dealers (if any) and, depending on your broker, greater than the valuation provided on your customer account

statements — SCUSA’s estimated value of the Notes is determined by reference to its pricing models and takes into account BNS’ internal funding rate. The price at which SCUSA would initially buy or sell the Notes in the secondary

market (if SCUSA makes a market, which it is not obligated to do) may exceed (i) SCUSA’s estimated value of the Notes at the time of pricing, (ii) any secondary market prices provided by unaffiliated dealers, potentially including UBS, and

(ii) depending on your broker, the valuation provided on your customer account statement. The price that SCUSA may initially offer to buy such Notes following issuance will exceed the valuations indicated by its internal pricing models due to

the inclusion for a limited period of time of the aggregate value of the costs associated with structuring and selling the Notes, including the underwriting discount, hedging costs, issuance costs and theoretical projected trading profit. The

portion of such amounts included in any secondary market price will decline to zero on a straight line basis over a period ending no later than the date specified under “Supplemental Plan of Distribution (Conflicts of Interest); Secondary

Markets (if any).” Thereafter, if SCUSA buys or sells the Notes it will do so at prices that reflect the estimated value determined by reference to SCUSA’s pricing models at that time. The price at which SCUSA will buy or sell the Notes at

any time also will reflect its then current bid and ask spread for similar sized trades of structured notes. The temporary positive differential relative to SCUSA’s internal pricing models arises from requests from and arrangements made by

BNS and the Agents. As described above, SCUSA and its affiliates are not required to make a market for the Notes and may stop making a market at any time. SCUSA reflects this temporary positive differential on its customer account statements.

Investors should inquire as to the valuation provided on customer account statements provided by unaffiliated dealers, including UBS.

|

SCUSA’s pricing models consider certain variables, including principally BNS’ internal funding rate, interest rates (forecasted, current and historical rates),

volatility of the underlying asset, price-sensitivity analysis and the time to maturity of the Notes. These pricing models are proprietary and rely in part on certain assumptions about future events, which may prove to be incorrect. As a result, the

actual value you would receive if you sold your Notes in the secondary market, if any, to others may differ, perhaps materially, from the estimated value of the Notes determined by reference to SCUSA’s models, taking into account BNS’ internal

funding rate, due to, among other things, any differences in pricing models or assumptions used by others. If SCUSA calculated its estimated value of the Notes by reference to BNS’ credit spreads or the borrowing rate BNS would pay for its

conventional fixed-rate debt securities (as opposed to BNS’ internal funding rate), the price at which SCUSA would buy or sell the Notes (if SCUSA makes a market, which it is not obligated to do) could be significantly lower.

In addition to the factors discussed above, the value and quoted price of the Notes at any time will reflect many factors and cannot be predicted. If SCUSA makes a

market in the Notes, the price quoted by SCUSA would reflect any changes in market conditions and other relevant factors, including any deterioration in BNS’ creditworthiness or perceived creditworthiness. These changes may adversely affect the value

of the Notes, including the price you may receive for the Notes in any market making transaction. To the extent that SCUSA makes a market in the Notes, the quoted price will reflect the estimated value determined by reference to SCUSA’s pricing

models at that time, plus or minus SCUSA’s then current bid and ask spread for similar sized trades of structured notes (and subject to the declining excess amount described above). Furthermore, if you sell your Notes, you will likely be charged a

commission for secondary market transactions, or the price will likely reflect a dealer discount. This commission or discount will further reduce the proceeds you would receive for your Notes in a secondary market sale.

P-6

| ♦ |

The price of the Notes prior to maturity will depend on a number of factors and may be substantially less than the principal amount — Because structured notes, including the

Notes, can be thought of as having a debt component and a derivative component, factors that influence the values of debt instruments and options and other derivatives will also affect the terms and features of the Notes at issuance and the

market price of the Notes prior to maturity. Some of these factors include, but are not limited to: (i) actual or anticipated changes in the level of the underlying asset over the full term of the Notes, (ii) volatility of the level of the

underlying asset and their underlying constituents and the market's perception of future volatility of the foregoing, (iii) changes in interest rates generally, (iv) any actual or anticipated changes in our credit ratings or credit spreads,

(v) dividend yields on the underlying asset constituents and (vi) time remaining to maturity. In particular, because the provisions of the Notes relating to the call return and the payment at maturity behave like options, the value of the

Notes will vary in ways which are non-linear and may not be intuitive.

|

Depending on the actual or anticipated level of the underlying asset and other relevant factors, the market value of the Notes may decrease and you may receive

substantially less than the principal amount if you sell your Notes prior to maturity regardless of the level of the underlying asset at such time.

Risks Relating to Hedging Activities and Conflicts of Interest

| ♦ |

Hedging activities by BNS and SCUSA may negatively impact investors in the Notes and cause our respective interests and those of our clients and counterparties to be contrary to

those of investors in the Notes — We, SCUSA or one or more of our other affiliates has hedged or expects to hedge our obligations under the Notes. Such hedging transactions may include entering into swap or similar agreements,

purchasing shares of the underlying constituents and/or purchasing futures, options and/or other instruments linked to the underlying asset and/or one or more of the underlying constituents. We, SCUSA or one or more of our or their respective

affiliates also expects to adjust the hedge by, among other things, purchasing or selling any of the foregoing, and perhaps other instruments linked to the underlying asset and/or one or more of the underlying constituents, at any time and

from time to time, and to unwind the hedge by selling any of the foregoing on or before the final valuation date. We, SCUSA or one or more of our or their respective affiliates may also enter into, adjust and unwind hedging transactions

relating to other basket- or index-linked Notes whose returns are linked to changes in the level of the underlying asset and/or one or more of the underlying constituents. Any of these hedging activities may adversely affect the level of the

underlying asset—directly or indirectly by affecting the price of the underlying constituents — and therefore the market value of the Notes and the amount you will receive, if any, on the Notes.

|

You should expect that these transactions will cause BNS, SCUSA or our other affiliates, or our or their respective clients or counterparties, to have economic

interests and incentives that do not align with, and that may be directly contrary to, those of an investor in the Notes. None of BNS, SCUSA or any of our other affiliates will have any obligation to take, refrain from taking or cease taking any

action with respect to these transactions based on the potential effect on an investor in the Notes, and any of the foregoing may receive substantial returns with respect to these hedging activities while the market value of, and return on, the Notes

declines.

| ♦ |

We, the Agents and our or their respective affiliates regularly provide services to, or otherwise have business relationships with, a broad client base, which has included and may

include us and the underlying constituent issuers and the market activities by us, the Agents or our or their respective affiliates for our or their own respective accounts or for our or their respective clients could negatively impact

investors in the Notes — We, the Agents and our or their respective affiliates regularly provide a wide range of financial services, including financial advisory, investment advisory and transactional services to a substantial and

diversified client base. As such, we each may act as an investor, investment banker, research provider, investment manager, investment advisor, market maker, trader, prime broker or lender. In those and other capacities, we, the Agents and/or

our or their respective affiliates purchase, sell or hold a broad array of investments, actively trade securities (including the Notes or other securities that we have issued), the underlying constituents, derivatives, loans, credit default

swaps, indices, baskets and other financial instruments and products for our or their own respective accounts or for the accounts of our or their respective customers, and we will have other direct or indirect interests, in those securities

and in other markets that may not be consistent with your interests and may adversely affect the level of the underlying asset and/or the value of the Notes. You should assume that we or they will, at present or in the future, provide such

services or otherwise engage in transactions with, among others, us and the underlying constituent issuers, or transact in securities or instruments or with parties that are directly or indirectly related to these entities. These services

could include making loans to or equity investments in those companies, providing financial advisory or other investment banking services, or issuing research reports. Any of these financial market activities may, individually or in the

aggregate, have an adverse effect on the level of the underlying asset and the market for your Notes, and you should expect that our interests and those of the Agents and/or our or their respective affiliates, clients or counterparties, will

at times be adverse to those of investors in the Notes.

|

You should expect that we, the Agents, and our or their respective affiliates, in providing these services, engaging in such transactions, or acting for our or their

own respective accounts, may take actions that have direct or indirect effects on the Notes or other securities that we may issue, the underlying constituents or other securities or instruments similar to or linked to the foregoing, and that such

actions could be adverse to the interests of investors in the Notes. In addition, in connection with these activities, certain personnel within us, the Agents or our or their respective affiliates may have access to confidential material non-public

information about these parties that would not be disclosed to investors in the Notes.

P-7

We, the Agents and our or their respective affiliates regularly offer a wide array of securities, financial instruments and other products into the marketplace, including

existing or new products that are similar to the Notes or other securities that we may issue, the underlying constituents or other securities or instruments similar to or linked to the foregoing. Investors in the Notes should expect that we, the

Agents and our or their respective affiliates offer securities, financial instruments, and other products that may compete with the Notes for liquidity or otherwise.

| ♦ |

Potential impact on price by BNS or the Agents — Trading or transactions by BNS, the Agents or our or their respective affiliates in the underlying asset or any underlying

constituents, listed and/or over-the-counter options, futures, exchange-traded funds or other instruments with returns linked to the performance of the underlying asset or any underlying constituents may adversely affect the level of the

underlying asset or underlying constituents and, therefore, the market value of the Notes, the likelihood of the Notes being automatically called and receiving the call return on any call settlement date. See “— Hedging activities by BNS and

SCUSA may negatively impact investors in the Notes and cause our respective interests and those of our clients and counterparties to be contrary to those of investors in the Notes” for additional information regarding hedging-related

transactions and trading.

|

| ♦ |

The calculation agent will have significant discretion with respect to the Notes, which may be exercised in a manner that is adverse to your interests — The calculation

agent will be an affiliate of BNS. The calculation agent will determine whether the Notes are automatically called and the call return is payable to you on any call settlement date and the payment at maturity of the Notes, if any, based on

observed closing levels of the underlying asset. The calculation agent can postpone the determination of the closing level or final level (and therefore the related call settlement date or maturity date, as applicable) if a market disruption

event occurs and is continuing with respect to the underlying asset on any observation date (including the final valuation date).

|

| ♦ |

Potentially inconsistent research, opinions or recommendations by BNS or the Agents — BNS, the Agents and our or their respective affiliates may publish research from time

to time on financial markets and other matters that may influence the value of the Notes, or express opinions or provide recommendations that are inconsistent with purchasing or holding the Notes. Any research, opinions or recommendations

expressed by BNS, the Agents or our or their respective affiliates may not be consistent with each other and may be modified from time to time without notice. Investors should make their own independent investigation of the merits of

investing in the Notes and the underlying asset to which the Notes are linked.

|

Risks Relating to General Credit Characteristics

| ♦ |

Credit risk of BNS — The Notes are senior unsecured debt obligations of BNS and are not, either directly or indirectly, an obligation of any third party. Any payment to be

made on the Notes, including any repayment of principal, depends on the ability of BNS to satisfy its obligations as they come due. As a result, BNS’ actual and perceived creditworthiness may affect the market value of the Notes. If BNS were

to default on its obligations, you may not receive any amounts owed to you under the terms of the Notes and you could lose your entire investment in the Notes.

|

| ♦ |

BNS is subject to the resolution authority under the CDIC Act — Although the Notes are not bail-inable debt securities under the CDIC Act, as described elsewhere in this

pricing supplement, BNS remains subject generally to Canadian bank resolution powers under the CDIC Act. Under such powers, the Canada Deposit Insurance Corporation may in certain circumstances take actions that could negatively impact

holders of the Notes and result in a loss on your investment. See “Risk Factors — Risks Related to the Bank’s Debt Securities” in the accompanying prospectus for more information.

|

Risks Relating to Canadian and U.S. Federal Income Taxation

| ♦ |

Uncertain tax treatment — Significant aspects of the tax treatment of the Notes are uncertain. You should consult your tax advisor about your tax situation. See “Material

Canadian Income Tax Consequences” and “What Are the Tax Consequences of the Notes?” herein.

|

P-8

|

Hypothetical Examples of How the Notes Might Perform

|

The below examples are based on hypothetical terms. The actual terms will be set on the trade date and will be indicated on the cover of the final pricing supplement.

The examples below illustrate the payment upon an automatic call or at maturity for a $10.00 Note on a hypothetical offering of the Notes, with the following assumptions (amounts may have been rounded

for ease of analysis):

|

Principal Amount:

|

$10.00

|

|

Term:

|

Approximately 5 years

|

|

Call Return Rate:

|

8.00% per annum

|

|

Observation Dates:

|

Quarterly (callable after 12 months)

|

|

Initial Level:

|

18,000

|

|

Call Threshold Level:

|

18,000 (which is 100.00% of the Initial Level)

|

|

Downside Threshold:

|

13,500 (which is 75.00% of the Initial Level)

|

Example 1 — The Closing Level of the Underlying Asset is equal to or greater than the Call Threshold Level on the Observation Date corresponding to the first potential Call

Settlement Date.

|

Date

|

Closing Level

|

Payment (per Note)

|

||

|

First Observation Date

|

18,500 (equal to or greater than Call Threshold Level)

|

$10.80 (Call Price)

|

||

|

Total Payment:

|

$10.80 (8.00% total return)

|

Because the Notes are subject to an automatic call on the first potential call settlement date (which is approximately 12 months after the trade date), BNS will pay on the corresponding call

settlement date a total of $10.80 per Note (reflecting your principal amount plus the applicable call return), a total return of 8.00% on the Notes. You will not receive any further payments on the Notes.

Example 2 — The Closing Level of the Underlying Asset is equal to or greater than the Call Threshold Level on the Observation Date corresponding to the third potential Call

Settlement Date.

|

Date

|

Closing Level

|

Payment (per Note)

|

||

|

First Observation Date

|

15,250 (less than Call Threshold Level)

|

$0.00

|

||

|

Second Observation Date

|

16,400 (less than Call Threshold Level)

|

$0.00

|

||

|

Third Observation Date

|

18,100 (equal to or greater than Call Threshold Level)

|

$11.20 (Call Price)

|

||

|

Total Payment:

|

$11.20 (12.00% total return)

|

Because the Notes are subject to an automatic call on the third potential call settlement date (which is approximately 18 months after the trade date), BNS will pay on the corresponding call

settlement date a total of $11.20 per Note (reflecting your principal amount plus the applicable call return), a total return of 12.00% on the Notes. You will not receive any further payments on the Notes.

Example 3 — The Final Level is equal to or greater than the Call Threshold Level on the Final Valuation Date.

|

Date

|

Closing Level

|

Payment (per Note)

|

||

|

First Observation Date

|

15,150 (less than Call Threshold Level)

|

$0.00

|

||

|

Second through Sixteenth Observation Date

|

Various (all less than Call Threshold Level)

|

$0.00

|

||

|

Final Valuation Date

|

19,250 (equal to or greater than Call Threshold Level and Downside Threshold)

|

$14.00 (Call Price)

|

||

|

Total Payment:

|

$14.00 (40.00% total return)

|

Because the Notes are subject to an automatic call on the final valuation date (which is approximately 5 years after the trade date), BNS will pay on the corresponding call settlement date (which is

also the maturity date) a total of $14.00 per Note (reflecting your principal amount plus the applicable call return), a total return of 40.00% on the Notes.

P-9

Example 4 — The Notes are NOT subject to an Automatic Call and the Final Level is equal to or greater than the Downside Threshold.

|

Date

|

Closing Level

|

Payment (per Note)

|

||

|

First Observation Date

|

16,150 (less than Call Threshold Level)

|

$0.00

|

||

|

Second through Sixteenth Observation Date

|

Various (all less than Call Threshold Level)

|

$0.00

|

||

|

Final Valuation Date

|

16,800 (less than Call Threshold Level and equal to or greater than Downside Threshold)

|

$10.00 (Payment at Maturity)

|

||

|

Total Payment:

|

$10.00 (0.00% total return)

|

Because the Notes are not subject to an automatic call and the final level is equal to or greater than the downside threshold, on the maturity date, BNS will pay you the principal amount of $10.00 per

Note (reflecting your principal amount), a total return of 0.00% on the Notes.

Example 5 — The Notes are NOT subject to an Automatic Call and the Final Level is less than the Downside Threshold.

|

Date

|

Closing Level

|

Payment (per Note)

|

||

|

First Observation Date

|

16,550 (less than Call Threshold Level)

|

$0.00

|

||

|

Second through Sixteenth Observation Date

|

Various (all less than Call Threshold Level)

|

$0.00

|

||

|

Final Valuation Date

|

7,200 (less than Call Threshold Level and Downside Threshold)

|

$10.00 × (1 + Underlying Return)

= $10.00 × [1 + (-60.00%)]

= $10.00 × 0.40

= $4.00 (Payment at Maturity)

|

||

|

Total Payment:

|

$4.00 (60.00% loss)

|

Because the Notes are not subject to an automatic call and the final level is less than the downside threshold, you will be exposed to the underlying return and, on the maturity date, BNS will pay you

$4.00 per Note, a loss of 60.00% on the Notes.

Investing in the Notes involves significant risks. The Notes differ from ordinary debt securities in that BNS is not necessarily obligated to repay the principal amount. If the Notes

are not subject to an automatic call, you may lose a significant portion or all of your investment in the Notes. Specifically, if the Notes are not subject to an automatic call and the final level is less than the downside threshold, you will lose a

percentage of your principal amount equal to the underlying return and, in extreme situations, you could lose your entire investment in the Notes.

Any payment on the Notes, including any payments in respect of an automatic call or any repayment of principal, is subject to the creditworthiness of BNS. If BNS were to default on

its payment obligations, you may not receive any amounts owed to you under the Notes and you could lose your entire investment in the Notes.

P-10

|

Information About the Underlying Asset

|

All disclosures contained in this document regarding the underlying asset are derived from publicly available information. BNS has not conducted any independent review or due diligence of any publicly

available information with respect to the underlying asset. You should make your own investigation into the underlying asset.

|

Nasdaq-100 Index®

|

We have derived all information contained herein regarding the underlying asset, including without limitation, its make-up, method of calculation and changes in its components from publicly available

information. Such information reflects the policies of, and is subject to change by, Nasdaq, Inc. (“Nasdaq” or its “index sponsor”), and/or its affiliates.

The underlying asset includes 100 of the largest domestic and international non-financial stocks listed on The Nasdaq Stock Market based on market capitalization. Please see “Indices — The Nasdaq-100®

Index” in the accompanying underlier supplement for additional information regarding the underlying asset, the index sponsor and our license agreement with respect to the underlying asset. Additional information regarding the underlying asset,

including its sectors, sector weightings and top constituents, may be available on the index sponsor’s website.

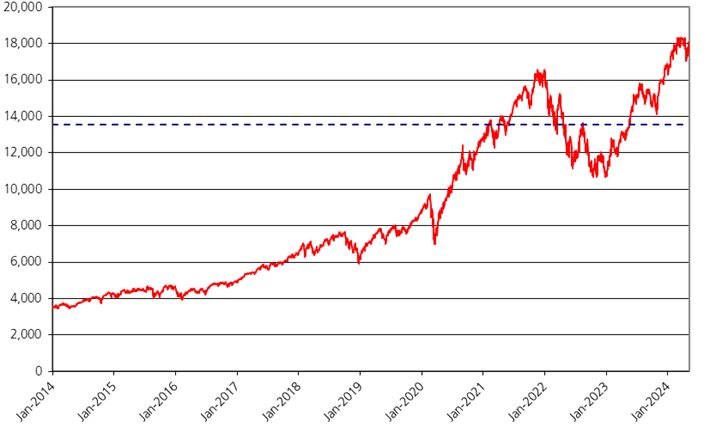

Historical Information

The graph below illustrates the performance of the underlying asset from January 1, 2014 through May 6, 2024, based on the daily closing levels as reported by Bloomberg Professional® service

(“Bloomberg”), without independent verification. BNS has not conducted any independent review or due diligence of publicly available information obtained from Bloomberg. The closing level of the underlying asset on May 6, 2024 was 18,093.57 (the

“hypothetical initial level”). The green and blue dotted lines respectively represent the hypothetical call threshold level of 18,093.57 and the hypothetical downside threshold of 13,570.18, which are equal to 100.00% and 75.00%, respectively, of the

hypothetical initial level. The actual initial level, call threshold level and downside threshold will be determined on the trade date. Past performance of the underlying asset is not indicative

of the future performance of the underlying asset during the term of the Notes.

P-11

|

What Are the Tax Consequences of the Notes?

|

The U.S. federal income tax consequences of your investment in the Notes are uncertain. There are no statutory provisions, regulations, published rulings or judicial decisions

addressing the characterization for U.S. federal income tax purposes of securities with terms that are substantially the same as the Notes. Some of these tax consequences are summarized below, but we urge you to read the more detailed discussion in

“Material U.S. Federal Income Tax Consequences” in the accompanying product supplement and to discuss the tax consequences of your particular situation with your tax advisor. This discussion is based upon the U.S. Internal Revenue Code of 1986, as

amended (the “Code”), final, temporary and proposed U.S. Department of the Treasury (the “Treasury”) regulations, rulings and decisions, in each case, as available and in effect as of the date hereof, all of which are subject to change, possibly with

retroactive effect. Tax consequences under state, local and non-U.S. laws are not addressed herein. No ruling from the U.S. Internal Revenue Service (the “IRS”) has been sought as to the U.S. federal income tax consequences of your investment in the

Notes, and the following discussion is not binding on the IRS.

U.S. Tax Treatment. Pursuant to the terms of the Notes, BNS and you agree, in the absence of a statutory or regulatory change or an administrative determination

or judicial ruling to the contrary, to characterize the Notes as prepaid derivative contracts with respect to the underlying asset. If your Notes are so treated, you should generally recognize long-term capital gain or loss if you hold your Notes for

more than one year (and, otherwise, short-term capital gain or loss) upon the taxable disposition (including cash settlement) of your Notes in an amount equal to the difference between the amount you receive at such time and the amount you paid for

your Notes. The deductibility of capital losses is subject to limitations.

Although uncertain, it is possible that the call return, or proceeds received from the taxable disposition of your Notes prior to the call settlement date that could be attributed to the expected call

return, could be treated as ordinary income. You should consult your tax advisor regarding this risk.

Based on certain factual representations received from us, our special U.S. tax counsel, Fried, Frank, Harris, Shriver & Jacobson LLP, is of the opinion that it would be

reasonable to treat your Notes in the manner described above. However, because there is no authority that specifically addresses the tax treatment of the Notes, it is possible that your Notes could alternatively be treated for tax purposes as a

single contingent payment debt instrument or pursuant to some other characterization, such that the timing and character of your income from the Notes could differ materially and adversely from the treatment described above, as described further

under “Material U.S. Federal Income Tax Consequences” in the accompanying product supplement.