Filed Pursuant to Rule 424(b)(3)

Registration Statement No. 333-262557

|

The Toronto-Dominion Bank

$1,500,000

Callable Contingent Coupon Trigger Notes

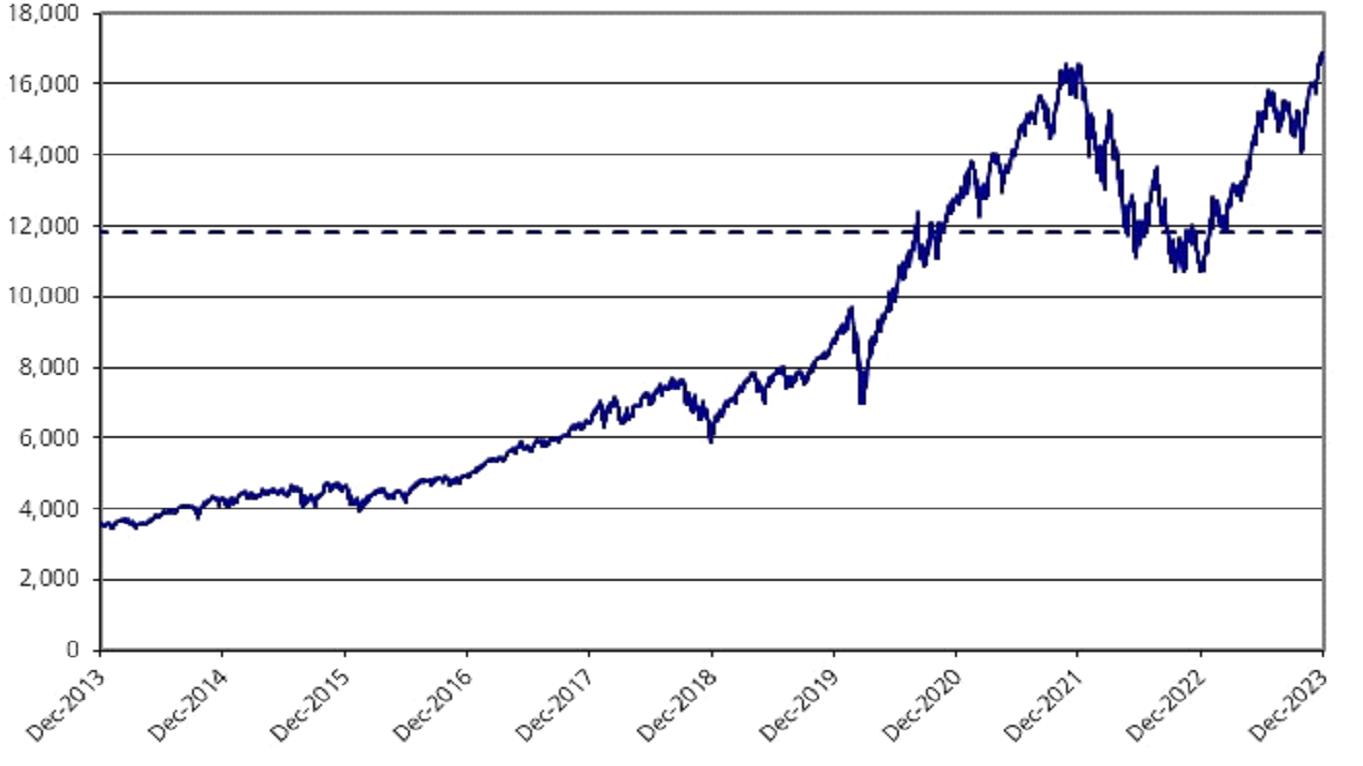

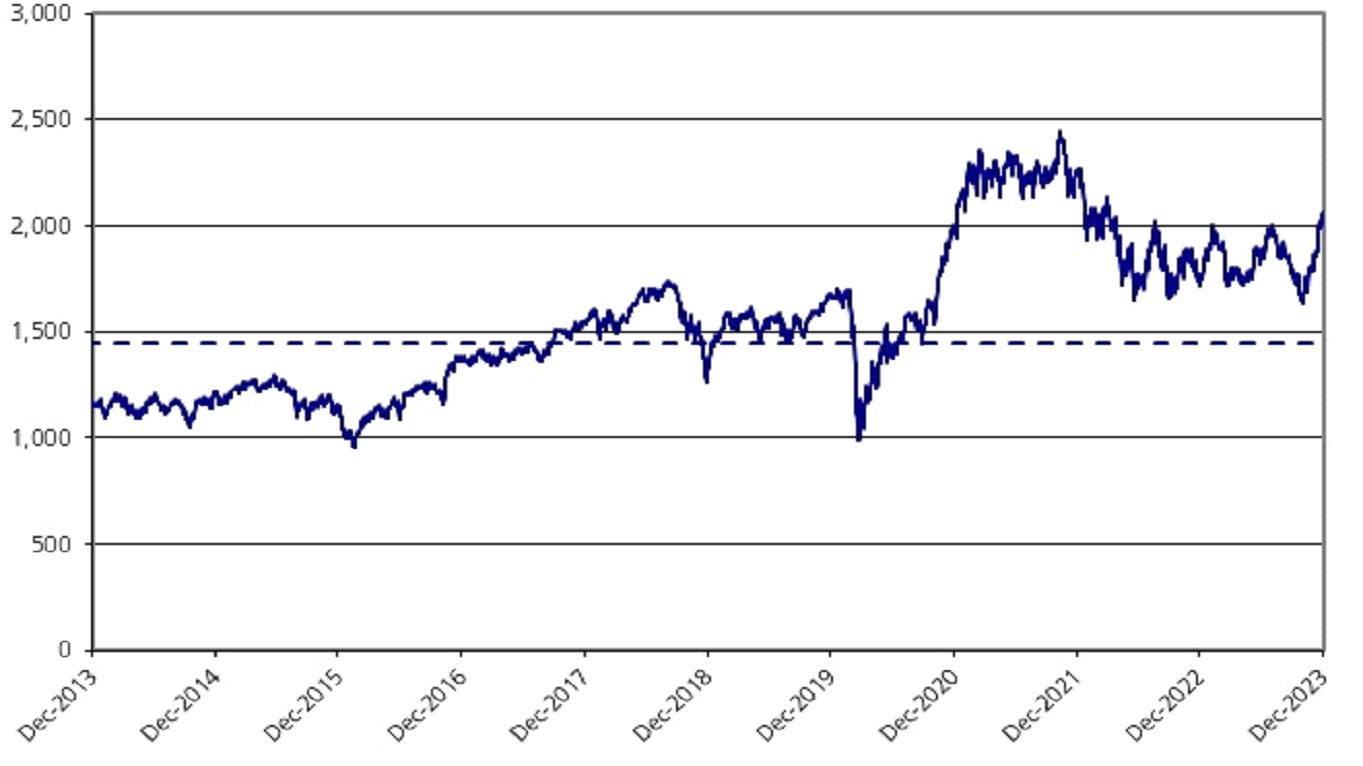

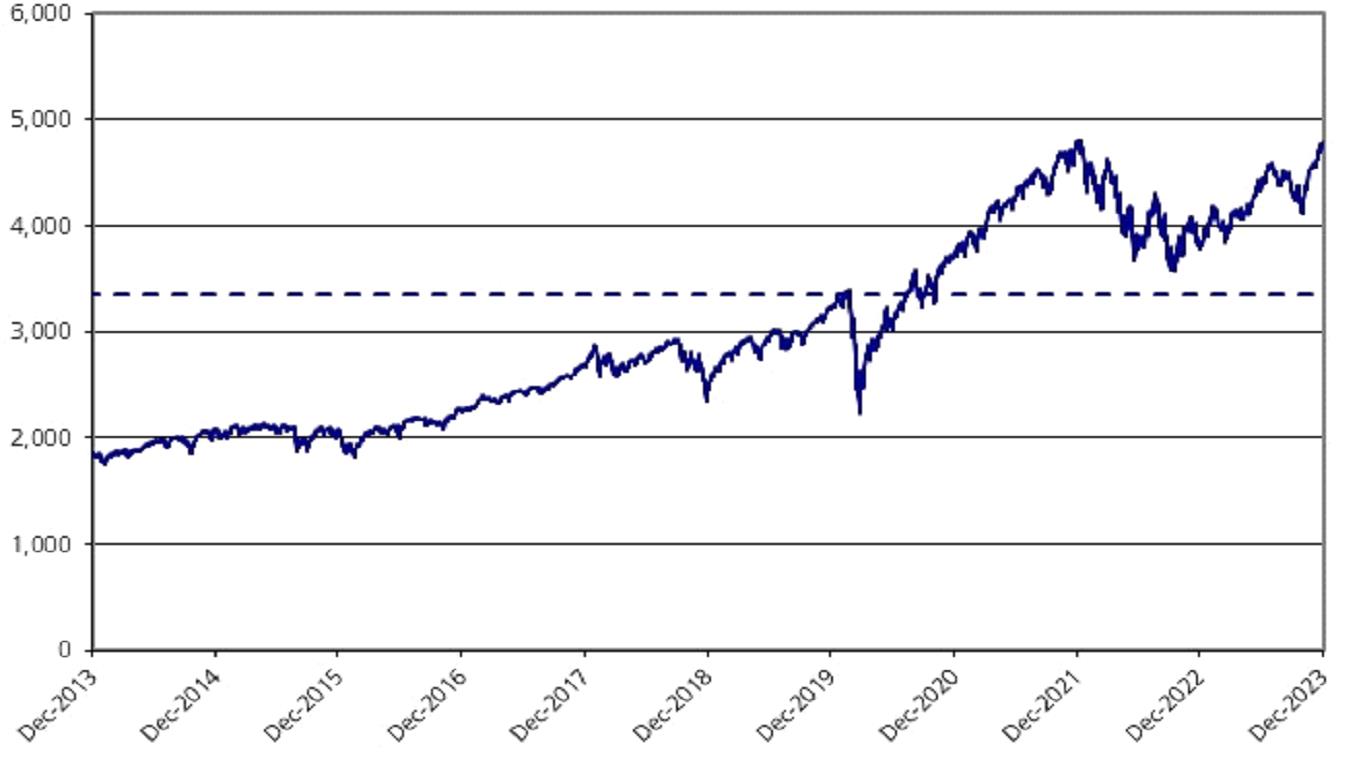

Linked to the Least Performing of the Nasdaq-100 Index®, the Russell 2000® Index and the S&P 500® Index due

July 2, 2026

|

The notes do not pay a fixed coupon and may pay no contingent coupon on a coupon payment date. The amount that you will be paid on your

notes is based on the performances of the Nasdaq-100 Index®, the Russell 2000® Index and the S&P 500® Index (each, a “reference asset”). The notes will mature on the maturity

date (July 2, 2026), unless we redeem them prior to maturity.

We may redeem your notes on any coupon payment date, upon at least three business days prior notice, beginning with the coupon payment date in March 2024 and

ending on the coupon payment date in May 2026, at 100% of their principal amount plus any contingent coupon otherwise due on the relevant coupon payment date.

If we do not redeem your notes, if the closing level of each reference asset on a coupon observation date (the 27th day of each month (provided that the coupon observation date for June 2026 is June 29, 2026),

commencing in January 2024 and ending in June 2026) is greater than or equal to 70.00% of its initial level (the initial level is 16,906.80 with respect to the Nasdaq-100 Index®, 2,066.214 with respect to the Russell 2000® Index and 4,781.58 with

respect to the S&P 500® Index), you will receive on the applicable coupon payment date (the 3rd business day after the relevant coupon observation date) a contingent coupon of $8.583 for each $1,000 principal amount of your notes. If the closing level of any reference asset on a coupon observation date is less than 70.00% of its initial level, you will not receive a contingent coupon on the applicable coupon payment date.

If we do not redeem your notes, the amount that you will be paid on your notes at maturity, in addition to the final contingent coupon, if any, will be based on the

performance of the least performing reference asset, which is the reference asset with the lowest percentage change. The percentage change of each reference asset is the percentage increase or decrease in its final level, which is the closing level

of such reference asset on the final valuation date (June 29, 2026), from its initial level. The least performing percentage change will be the percentage change of the least performing reference asset.

At maturity, for each $1,000 principal amount of your notes you will receive an amount in cash equal to:

| ● |

if the final level of each reference asset is greater than or equal to 70.00% of its initial level, $1,000 plus the final

contingent coupon; or

|

| ● |

if the final level of any reference asset is less than 70.00% of its initial level, the sum of (i) $1,000 plus (ii) the product of (a) $1,000 times (b) the least performing percentage change. You

will receive less than 70.00% of the principal amount of your notes and no contingent coupon.

|

If the final level of any reference asset is less than 70.00% of its initial level, the return on your notes will be negative and will equal the least performing percentage change. Specifically, you will lose 1% for every 1% that the final level of the least performing

reference asset is less than its initial level, and you could lose up to your entire investment in the notes. In such event, you will receive less than the principal amount of your notes and no contingent coupon. Any payments on the notes

are subject to our credit risk.

The notes are unsecured and are not savings accounts or insured deposits of a bank. The notes are not insured or guaranteed by the Canada Deposit Insurance Corporation, the U.S.

Federal Deposit Insurance Corporation or any other governmental agency or instrumentality of Canada or the United States. The notes will not be listed or displayed on any securities exchange or electronic communications network.

You should read the disclosure herein to better understand the terms and risks of your investment. See “Additional Risk Factors” beginning on page P-8 of this

pricing supplement.

Neither the Securities and Exchange Commission (the “SEC”) nor any state securities commission has approved or disapproved of these notes or determined that this

pricing supplement, the product supplement or the prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The initial estimated value of the notes at the time the terms of your notes were set on the pricing date was $979.80 per $1,000 principal amount,

which is less than the public offering price listed below. See “Additional Information Regarding the Estimated Value of the Notes” on the following page and “Additional Risk Factors — Risks Relating to Estimated Value and Liquidity”

beginning on page P-11 of this pricing supplement. The actual value of your notes at any time will reflect many factors and cannot be predicted with accuracy.

|

Public Offering Price1

|

Underwriting Discount1

|

Proceeds to TD

|

|

|

Per Note

|

$1,000.00

|

$7.00

|

$993.00

|

|

Total

|

$1,500,000.00

|

$10,500.00

|

$1,489,500.00

|

1 See “Supplemental Plan of Distribution (Conflicts of Interest)” herein for additional information.

|

TD Securities (USA) LLC

|

Goldman Sachs & Co. LLC

|

|

Agent

|

Amendment No. 1 Dated January 12, 2024† to the

Pricing Supplement dated December 27, 2023

† This amended pricing supplement supersedes in its entirety the related pricing supplement dated December 27, 2023. We refer to this amended pricing supplement as the pricing supplement.

The public offering price, underwriting discount and proceeds to TD listed above relate to the notes we issue initially. We may decide to sell additional notes

after the date of this pricing supplement, at public offering prices and with underwriting discounts and proceeds to TD that differ from the amounts set forth above. The return (whether positive or negative) on your investment in the notes will

depend in part on the public offering price you pay for such notes.

We or Goldman Sachs & Co. LLC (“GS&Co.”), or any of our or their respective affiliates, may use this pricing supplement in the initial sale of the notes. In

addition, we or GS&Co. or any of our or their respective affiliates may use this pricing supplement in a market-making transaction in a note after its initial sale. Unless we or GS&Co., or any of our or their

respective affiliates, informs the purchaser otherwise in the confirmation of sale, this pricing supplement will be used in a market-making transaction.

Additional Information Regarding the Estimated Value of the Notes

The final terms for the Notes were determined on the Pricing Date, based on prevailing market conditions, and are specified elsewhere in this pricing supplement. The economic terms

of the Notes are based on TD’s internal funding rate (which is TD’s internal borrowing rate based on variables such as market benchmarks and TD’s appetite for borrowing), and several factors, including any sales commissions expected to be paid to

TDS, any selling concessions, discounts, commissions or fees expected to be allowed or paid to non-affiliated intermediaries, the estimated profit that TD or any of TD’s affiliates expect to earn in connection with structuring the Notes, estimated

costs which TD may incur in connection with the Notes and an estimate of the difference between the amounts TD pays to GS&Co. or an affiliate and the amounts that GS&Co. or an affiliate pays to us in connection with hedging your Notes as

described further under “Supplemental Plan of Distribution (Conflicts of Interest)” herein. Because TD’s internal funding rate generally represents a discount from the levels at which TD’s benchmark debt securities trade in the secondary market, the

use of an internal funding rate for the Notes rather than the levels at which TD’s benchmark debt securities trade in the secondary market is expected to have had an adverse effect on the economic terms of the Notes. On the cover page of this pricing

supplement, TD has provided the initial estimated value for the Notes. The initial estimated value was determined by reference to TD’s internal pricing models which take into account a number of variables and are based on a number of assumptions,

which may or may not materialize, typically including volatility, interest rates (forecasted, current and historical rates), price-sensitivity analysis, time to maturity of the Notes, and TD’s internal funding rate. For more information about the

initial estimated value, see “Additional Risk Factors” herein. Because TD’s internal funding rate generally represents a discount from the levels at which TD’s benchmark debt securities trade in the secondary market, the use of an internal funding

rate for the Notes rather than the levels at which TD’s benchmark debt securities trade in the secondary market is expected, assuming all other economic terms are held constant, to increase the estimated value of the Notes. For more information see

the discussion under “Additional Risk Factors — Risks Relating to Estimated Value and Liquidity — TD’s and GS&Co.’s Estimated Value of the Notes Are Determined By Reference to TD’s Internal Funding Rates and Are Not Determined By Reference to

Credit Spreads or the Borrowing Rate TD Would Pay for its Conventional Fixed-Rate Debt Securities”.

The value of your Notes at any time will reflect many factors and cannot be predicted; however, the price (not including GS&Co.’s customary bid and ask spreads) at which

GS&Co. would initially buy or sell Notes in the secondary market (if GS&Co. makes a market, which it is not obligated to do) and the value that GS&Co. will initially use for account statements and otherwise is equal to approximately

GS&Co.’s estimate of the market value of your Notes on the Pricing Date, based on its pricing models and taking into account TD’s internal funding rate.

The price (not including GS&Co.’s customary bid and ask spreads) at which GS&Co. would buy or sell your Notes (if it makes a market) will equal

approximately the then-current estimated value of your Notes determined by reference to such pricing models. For additional information regarding the value of your Notes shown in your GS&Co. account statements and the price at which GS&Co.

would buy or sell your Notes (if GS&Co. makes a market, which it is not obligated to do), each based on GS&Co.’s pricing models, see “Additional Risk Factors — Risks Relating to Estimated Value and Liquidity — The Price At Which GS&Co.

Would Buy or Sell Your Notes (If GS&Co. Makes a Market, Which It Is Not Obligated to Do) Will Be Based On GS&Co.’s Estimated Value of Your Notes”.

If a party other than the Agents or their affiliates is buying or selling your Notes in the secondary market based on its own estimated value of your Notes which

was calculated by reference to TD’s credit spreads or the borrowing rate TD would pay for its conventional fixed-rate debt securities (as opposed to TD’s internal funding rate), the price at which such party would buy or sell your Notes could be

significantly less.

We urge you to read the “Additional Risk Factors” in this pricing supplement.

Summary

The information in this “Summary” section is qualified by the more detailed information set forth in this pricing supplement, the product supplement and the prospectus.

|

Issuer:

|

Toronto Dominion Bank (“TD”)

|

|

Issue:

|

Senior Debt Securities, Series E

|

|

Type of Note:

|

Callable Contingent Coupon Trigger Notes

|

|

Term:

|

Approximately 30 months, subject to our election to redeem the Notes at our option

|

|

Reference Assets:

|

The Nasdaq-100 Index® (Bloomberg ticker: NDX), the Russell 2000® Index (Bloomberg ticker: RTY) and the S&P 500® Index (Bloomberg ticker: SPX). We may refer to the Nasdaq-100

Index® as the “NDX”, the Russell 2000® Index as the “RTY” and the S&P 500® Index as the “SPX” herein.

|

|

CUSIP / ISIN:

|

89115FME8 / US89115FME87

|

|

Agents:

|

TD Securities (USA) LLC (“TDS”) and Goldman Sachs & Co. LLC (“GS&Co.”)

|

|

Currency:

|

U.S. Dollars

|

|

Minimum Investment:

|

$1,000 and minimum denominations of $1,000 in excess thereof

|

|

Principal Amount:

|

$1,000 per Note; $1,500,000 in the aggregate for all the Notes; the aggregate Principal Amount of the Notes may be increased if TD, at its sole option, decides to sell an additional amount

of the Notes on a date subsequent to the date of this pricing supplement.

|

|

Pricing Date:

|

December 27, 2023

|

|

Issue Date:

|

December 29, 2023

|

|

Final Valuation Date:

|

The last Coupon Observation Date, June 29, 2026, subject to postponement for market disruption events and other disruptions, as specified below under “Coupon Observation Dates”.

|

|

Maturity Date:

|

July 2, 2026, subject to adjustment due to a market disruption event, a non-trading day or a non-business day as described in more detail under “—Coupon Payment Dates” below and “General

Terms of the Notes — Maturity Date” in the product supplement.

|

|

Contingent Coupon:

|

Subject to the Early Redemption feature, on each Coupon Payment Date, for each $1,000 Principal Amount of your Notes, we will pay you an amount in cash equal to:

o if the Closing Level of each Reference Asset is greater than or equal to its Coupon Barrier on the related Coupon Observation Date, $8.583; or

o If the Closing Level of any Reference Asset is less than

its Coupon Barrier on the related Coupon Observation Date, $0.

Contingent Coupons on the Notes are not guaranteed. You will not receive a Contingent Coupon on a Coupon Payment Date if the Closing Level of any Reference Asset is less

than its Coupon Barrier on the related Coupon Observation Date.

|

|

Coupon Barrier:

|

With respect to NDX: 11,834.76

With respect to RTY: 1,446.3498

With respect to SPX: 3,347.106

In each case, equal to 70.00% of the Initial Level of such Reference Asset

|

|

Coupon Observation Dates:

|

The 27th day of each month (provided that the coupon observation date for June 2026 is June 29, 2026), commencing in January 2024 and ending in June 2026.

If a market disruption event occurs or is continuing with respect to a Reference Asset on any Coupon Observation Date for any Reference Asset, the Coupon Observation Date for the affected

Reference Asset will be postponed until the next Trading Day on which no market disruption event occurs or is continuing for that Reference Asset. In no event, however, will any Coupon Observation Date for any Reference Asset be postponed by

more than eight Trading Days. If the determination of the Closing Level of a Reference Asset for any Coupon Observation Date is postponed to the last possible day, but a market disruption event occurs or is continuing on that day, that day

will nevertheless be the date on which the Closing Level of such Reference Asset will be determined. In such an event, the Calculation Agent will estimate the Closing Level that would have prevailed in the absence of the market disruption

event.

For the avoidance of doubt, if on any Coupon Observation Date, no market disruption event is occurring with respect to a particular Reference Asset, the Coupon Observation Date for such

Reference Asset will be the originally scheduled Coupon Observation Date irrespective of the occurrence of a market disruption event with respect to another Reference Asset.

For a description of events that constitute a market disruption event see “General Terms of the Notes—Market Disruption Events” in the product supplement. Each Coupon Observation Date will

be a “valuation date” in the product supplement.

|

|

Coupon Payment Dates:

|

The third Business Day following the relevant Coupon Observation Date, with the exception of the final Coupon Payment Date, which will be the Maturity Date, subject to postponement as

described above under “— Coupon Observation Dates” or, in each case, if such day is not a Business Day, the next following Business Day.

If we elect to redeem the Notes early on a Coupon Payment Date, such Coupon Payment Date will be the “Early Redemption Date”.

If a Coupon Observation Date (or Final Valuation Date) is postponed for any Reference Asset as described under “—Coupon Observation Dates” above, the related Coupon Payment Date (or Maturity

Date) will also be postponed to maintain the same number of Business Days following the latest postponed Coupon Observation Date as existed prior to such postponement(s).

|

|

Early Redemption Feature:

|

We may redeem the Notes early, at our option, in whole but not in part, on any Coupon Payment Date, upon at least three business days prior notice, commencing in March 2024 and ending in May

2026. If the Notes are subject to an Early Redemption on a Coupon Payment Date, we will pay on such Coupon Payment Date an amount in cash for each $1,000 Principal Amount of the Notes equal to $1,000 plus

any Contingent Coupon otherwise due with respect to the related Coupon Observation Date. Following an Early Redemption, no further payments will be made on the Notes.

|

|

Payment at Maturity:

|

If the Notes are not redeemed early, for each $1,000 Principal Amount of your Notes, in addition to the final Contingent Coupon, if any, we will pay you on the Maturity Date an

amount in cash equal to:

o If the Final Level of each Reference Asset is greater than or

equal to its Trigger Level,

$1,000; or

o If the Final Level of any Reference Asset is less than its Trigger Level, the sum of (i) $1,000 plus (ii) the product of (a) $1,000 times (b) the Least Performing Percentage Change.

In this case you will suffer a percentage loss on your initial investment equal to the negative Percentage Change of the Least Performing Reference Asset. Specifically,

you will lose 1% of the Principal Amount of your Notes for each 1% that the Final Level of the Least Performing Reference Asset is less than its Initial Level, and you could lose up to your entire initial investment. In such event, you will

receive less than the Principal Amount of your Notes and no Contingent Coupon.

|

P-4

|

Trigger Level:

|

With respect to NDX: 11,834.76

With respect to RTY: 1,446.3498

With respect to SPX: 3,347.106

In each case, equal to 70.00% of the initial level of such Reference Asset

|

|

Percentage Change:

|

For each Reference Asset, the quotient of (1) its Final Level minus its Initial Level divided by (2) its

Initial Level, expressed as a percentage.

|

|

Initial Level:

|

With respect to NDX: 16,906.80

With respect to RTY: 2,066.214

With respect to SPX: 4,781.58

The Initial Level of each Reference Asset equals its Closing Level on the Pricing Date, as determined by the Calculation Agent.

|

|

Closing Level:

|

For each Reference Asset (or any “successor index” thereto, as defined in the product supplement) on any Trading Day, the Closing Level will be its Closing Level published by its sponsor

(its “Index Sponsor”) as displayed on the relevant Bloomberg Professional® service (“Bloomberg”) page or any successor page or service.

|

|

Final Level:

|

For each Reference Asset, the Closing Level of such Reference Asset on its Final Valuation Date, except in the limited circumstances described under “General Terms of the Notes — Market

Disruption Events” and subject to adjustment as provided under “General Terms of the Notes — Unavailability of the Level of, or Change in Law Event Affecting, the Reference Asset; Modification to Method of Calculation” in the product

supplement.

|

|

Least Performing Reference

Asset:

|

The Reference Asset with the lowest Percentage Change as compared to the Percentage Change of any other Reference Asset.

|

|

Least Performing Percentage

Change:

|

The Percentage Change of the Least Performing Reference Asset.

|

|

Business Day:

|

Any day that is a Monday, Tuesday, Wednesday, Thursday or Friday that is neither a legal holiday nor a day on which banking institutions are authorized or required by law to close in New

York City.

|

|

U.S. Tax Treatment:

|

By purchasing the Notes, you agree, in the absence of a statutory or regulatory change or an administrative determination or judicial ruling to the contrary, to treat the Notes, for U.S.

federal income tax purposes, as prepaid derivative contracts with respect to the Reference Assets. Pursuant to this approach, it is likely that any Contingent Coupon that you receive should be included in ordinary income at the time you

receive the payment or when it accrues, depending on your regular method of accounting for U.S. federal income tax purposes. Based on certain factual representations received from us, our special U.S. tax counsel, Fried, Frank, Harris,

Shriver & Jacobson LLP, is of the opinion that it would be reasonable to treat the Notes in the manner described above. However, because there is no authority that specifically addresses the tax treatment of the Notes, it is possible that

your Notes could alternatively be treated for tax purposes as a single contingent payment debt instrument, or pursuant to some other characterization, such that the timing and character of your income from the Notes could differ materially

and adversely from the treatment described above, as described further under “Material U.S. Federal Income Tax Consequences” herein and in the product supplement. An investment in the Notes is not appropriate

for non-U.S. holders and we will not attempt to ascertain the tax consequences to non-U.S. holders of the purchase, ownership or disposition of the Notes.

|

P-5

|

Canadian Tax Treatment:

|

Please see the discussion in the product supplement under “Supplemental Discussion of Canadian Tax Consequences”, which applies to the Notes. In addition to the assumptions, limitations and

conditions described therein, such discussion assumes that no amount paid or payable to a Non-resident Holder in respect of the Notes will be the deduction component of a “hybrid mismatch arrangement” under which the payment arises within the

meaning of proposed paragraph 18.4(3)(b) of the Canadian Tax Act (as defined in the prospectus) contained in proposals to amend the Canadian Tax Act released by the Minister of Finance (Canada) on April 29, 2022 (the “Hybrid Mismatch

Proposals”). Investors should note that the Hybrid Mismatch Proposals are in consultation form, are highly complex, and there remains significant uncertainty as to their interpretation and application. There can be no assurance that the

Hybrid Mismatch Proposals will be enacted in their current form, or at all. We will not pay any additional amounts as a result of any withholding required by reason of the Hybrid Mismatch Proposals.

|

|

Record Date:

|

The Business Day preceding the relevant Coupon Payment Date.

|

|

Calculation Agent:

|

TD

|

|

Listing:

|

The Notes will not be listed or displayed on any securities exchange or electronic communications network.

|

|

Clearance and Settlement:

|

DTC global (including through its indirect participants Euroclear and Clearstream, Luxembourg) as described under “Description of the Debt Securities — Forms of the Debt Securities” and

“Ownership, Book-Entry Procedures and Settlement” in the prospectus.

|

|

Canadian Bail-in:

|

The Notes are not bail-inable debt securities (as defined in the prospectus) under the Canada Deposit Insurance Corporation Act.

|

|

Change in Law Event:

|

Not applicable, notwithstanding anything to the contrary in the product supplement.

|

P-6

Additional Terms of Your Notes

You should read this pricing supplement together with the prospectus, as supplemented by the product supplement, relating to our Senior Debt Securities, Series

E, of which these Notes are a part. Capitalized terms used but not defined in this pricing supplement will have the meanings given to them in the product supplement. In the event of any conflict the following hierarchy will govern: first, this

pricing supplement; second, the product supplement; and last, the prospectus. The Notes vary from the terms described in the product supplement in several important ways. You should read this

pricing supplement carefully.

This pricing supplement, together with the documents listed below, contains the terms of the Notes and supersedes all prior or contemporaneous oral statements as well as any other written materials

including preliminary or indicative pricing terms, correspondence, trade ideas, structures for implementation, sample structures, brochures or other educational materials of ours. You should carefully consider, among other things, the matters set

forth in “Additional Risk Factors” herein, “Additional Risk Factors Specific to the Notes” in the product supplement and “Risk Factors” in the prospectus, as the Notes involve risks not associated with conventional debt securities. We urge you to

consult your investment, legal, tax, accounting and other advisors concerning an investment in the Notes. You may access these documents on the SEC website at www.sec.gov as follows (or if that address has changed, by reviewing our filings for the

relevant date on the SEC website):

| ◾ |

Prospectus dated March 4, 2022:

|

| ◾ |

Product Supplement MLN-EI-1 dated March 4, 2022:

|

Our Central Index Key, or CIK, on the SEC website is 0000947263. As used in this pricing supplement, the “Bank,” “we,” “us,” or “our” refers to The Toronto-Dominion Bank and its subsidiaries.

We reserve the right to change the terms of, or reject any offer to purchase, the Notes prior to their issuance. In the event of any changes to the terms of the Notes, we will notify you and you will be asked to accept

such changes in connection with your purchase. You may also choose to reject such changes, in which case we may reject your offer to purchase.

This amended and restated pricing supplement amends, restates and supersedes the pricing supplement related hereto dated December 27, 2023 in its entirety.

P-7

Additional Risk Factors

The Notes involve risks not associated with an investment in conventional debt securities. This section describes the most significant risks relating to the terms of the Notes. For additional

information as to these and other risks, please see “Additional Risk Factors Specific to the Notes” in the product supplement and “Risk Factors” in the prospectus.

You should carefully consider whether the Notes are suited to your particular circumstances. Accordingly, investors should consult their investment, legal, tax, accounting and other advisors as to

the risks entailed by an investment in the Notes and the suitability of the Notes in light of their particular circumstances.

Risks Relating to Return Characteristics

Risk of Loss at Maturity.

You may lose all or a substantial portion of your investment in the Notes. If the Notes are not redeemed early, the Payment at Maturity depends on the Percentage Change of the Least Performing

Reference Asset. The Bank will only repay you the full Principal Amount of your Notes on the Maturity Date if the Final Level of each Reference Asset is greater than or equal to its Trigger Level and therefore the Least Performing Percentage Change

is greater than or equal to -30.00%. If the Final Level of any Reference Asset is less than its Trigger Level, and therefore the Least Performing Percentage Change is less than -30.00%, you will have a loss for each $1,000 Principal Amount of your

Notes equal to the product of (i) the Least Performing Percentage Change times (ii) $1,000. Specifically, if the Final Level of any Reference Asset is less than its

Trigger Level, you will lose 1% of the Principal Amount of your Notes for each 1% that the Final Level of the Least Performing Reference Asset is less than its Initial Level. Accordingly, you may lose up to your

entire investment in the Notes if the Notes are not redeemed early and the percentage decline of the Least Performing Reference Asset from its Initial Level to its Final Level is greater than 30.00%.

The Return on Your Notes May Change Significantly Despite Only a Small Change in the Level of the Least Performing Reference Asset.

If your Notes are not redeemed early and the Final Level of the Least Performing Reference Asset is less than its Trigger Level, you will receive less than the Principal Amount

of your Notes and you could lose all or a substantial portion of your investment in the Notes. This means that while a decrease in the Final Level of the Least Performing Reference Asset to its Trigger Level will not result in a loss of principal on

the Notes, a decrease in the Final Level of the Least Performing Reference Asset to less than its Trigger Level will result in a loss of a significant portion of the Principal Amount of the Notes despite only a small change in the level of the Least

Performing Reference Asset.

You May Not Receive Any Contingent Coupons With Respect to Your Notes.

You may not receive any Contingent Coupons with respect to your Notes. You will receive a Contingent Coupon on a Coupon Payment Date only if the Closing Level of each Reference Asset is greater than

or equal to its Coupon Barrier on the corresponding Coupon Observation Date. If the Closing Level of any Reference Asset is less than its Coupon Barrier on a Coupon Observation Date, you will not receive a Contingent Coupon on the applicable Coupon

Payment Date. If the Closing Level of any Reference Asset is less than its Coupon Barrier on each Coupon Observation Date over the term of the Notes, you will not receive any Contingent Coupons during the term of, and you will not receive a positive

return on, your Notes. Generally, this non-payment of any Contingent Coupon will coincide with a greater risk of principal loss on your Notes.

You will only receive a Contingent Coupon on a Coupon Payment Date if the Closing Level of each Reference Asset on the related Coupon Observation Date is greater than or equal to its Coupon Barrier.

You should be aware that, with respect to any prior Coupon Observation Dates that did not result in the payment of a Contingent Coupon, you will not be compensated for any opportunity cost implied by inflation and other factors relating to the time

value of money. Further, there is no guarantee that you will receive any Contingent Coupon payment with respect to the Notes at any time and you may lose your entire investment in the Notes.

The Potential Positive Return on the Notes Is Limited to the Contingent Coupons Paid on the Notes, If Any, Regardless of Any Appreciation of Any Reference Asset.

The potential positive return on the Notes is limited to any Contingent Coupons paid, meaning any positive return on the Notes will be composed solely by the sum of any Contingent Coupons paid over

the term of the Notes, regardless of any appreciation of any Reference Asset. Further, if the Notes are redeemed early, you will not receive any Contingent Coupons or any other payment in respect of any Coupon Observation Dates after the Early

Redemption date. Because the Notes may be subject to an Early Redemption, the total return on the Notes could be less than if the Notes had been outstanding until maturity. Therefore, if the appreciation of any Reference Asset exceeds the sum of any

Contingent Coupons actually paid on the Notes, the return on the Notes will be less than the return on a hypothetical direct investment in such Reference Asset, in a security directly linked to the positive performance of such Reference Asset or in

an investment in its Reference Asset Constituent Stocks.

The Contingent Repayment of Principal Applies Only Upon Early Redemption or on the Maturity Date.

You should be willing to hold your Notes to an Early Redemption or the Maturity Date. If you are able to sell your Notes prior to an Early Redemption or the Maturity Date in the secondary market, the price you receive

will likely not reflect the full economic value of the payment upon an Early Redemption or at maturity and any return on the Notes may be less than such payment, even if the amount you receive is greater than the Principal Amount. You can receive the

full benefit of the Early Redemption feature and the Payment at Maturity only if

P-8

you hold your Notes to an Early Redemption or the Maturity Date, as applicable, and we elect to redeem the Notes early or the Closing Level of each Reference Asset on the Final Valuation Date is

greater than or equal to its Trigger Level, as the case may be.

Additionally, if you are able to sell your Notes prior to an Early Redemption or the Maturity Date in the secondary market, you may have to sell them at a loss relative to your initial investment

even if the level of each Reference Asset at such time is greater than or equal to its Initial Level or Trigger Level, respectively.

We Are Able to Redeem Your Notes at Our Option.

We may redeem the Notes early, at our option, in whole but not in part, on any Coupon Payment Date, commencing in March 2024 and ending in May 2026. Even if we do not exercise our option to redeem

your Notes, our ability to do so may adversely affect the value of your Notes. It is our sole option whether to redeem your Notes prior to maturity and we may or may not exercise this option for any reason. Therefore, the term for your Notes may be

reduced to as short as approximately 3 months. You may not be able to reinvest the proceeds from an investment in the Notes at a comparable return for a similar level of risk in the event that we redeem the Notes prior to maturity. For the avoidance

of doubt, if your Notes are redeemed early, no discounts, commissions or fees described herein will be rebated or reduced.

It is more likely that we will elect to redeem the Notes early when the expected Contingent Coupons payable on the Notes are greater than the interest that would be payable on other instruments

issued by us of comparable maturity, terms and credit rating trading in the market. The greater likelihood of us redeeming the Notes in that environment increases the risk that you will not be able to reinvest the proceeds from the redeemed Notes in

an equivalent investment with a similar Contingent Coupon rate. To the extent you are able to reinvest such proceeds in an investment comparable to the Notes, you may incur transaction costs such as dealer discounts and hedging costs built into the

price of the new notes. We are less likely to redeem the Notes early when the expected Contingent Coupons payable on the Notes are less than the interest that would be payable on other comparable instruments issued by us, which includes when the

level of any of the Reference Assets is less than its Coupon Barrier. Therefore, the Notes are more likely to remain outstanding when the expected amount payable on the Notes is less than what would be payable on other comparable instruments and when

your risk of not receiving a Contingent Coupon is relatively higher.

The Contingent Coupon Does Not Reflect the Actual Performance of the Reference Assets

from the Pricing Date to Any Coupon Observation Date or from Coupon Observation Date to Coupon Observation Date.

The Contingent Coupon for each Coupon Payment Date is different from, and may be less than, a coupon determined based on the percentage difference of the Closing Levels of the Reference Assets

between the Pricing Date and any Coupon Observation Date or between two Coupon Observation Dates. Accordingly, the Contingent Coupons, if any, on the Notes may be less than the return you could earn on another instrument linked to the Reference

Assets that pays coupons based on the performance of the Reference Assets from the Pricing Date to any Coupon Observation Date or from Coupon Observation Date to Coupon Observation Date.

Any Amounts Payable on the Notes Are Not Linked to the Closing Level of Any Reference Asset at Any Time Other Than on the Applicable Coupon Observation Dates

(Including the Final Valuation Date) (Except in the Case of Tax Redemptions).

Any payments on the Notes will be based on the Closing Level of each Reference Asset only on the applicable Coupon Observation Dates (including the Final Valuation Date). Therefore, the Closing

Levels of the Reference Assets on dates other than the applicable Coupon Observation Date will have no effect on any amount paid in respect of your Notes. In addition, if the Notes are not redeemed early, the Payment at Maturity will be based on the

Final Level of the Least Performing Reference Asset, which will be the Reference Asset with the lowest Percentage Change based on its Closing Level on the Final Valuation Date as compared to that of any other Reference Asset. Therefore, for example,

if the level of the Least Performing Reference Asset dropped precipitously on the Final Valuation Date, the Payment at Maturity for the Notes may be significantly less than it would otherwise have been had the Payment at Maturity been linked to the

level of the Least Performing Reference Asset prior to such drop. Although the actual Closing Levels of the Reference Assets on the Coupon Payment Dates, Maturity Date or at other times during the term of the Notes may be higher than the Closing

Levels of the Reference Assets on the Coupon Observation Dates or the Final Valuation Date, you will not benefit from the Closing Level of any Reference Asset at any time other than on the applicable Coupon Observation Dates or the Final Valuation

Date, as the case may be (except in the case of tax redemptions as described further under “Tax Redemption” in the accompanying prospectus).

If You Purchase Your Notes at a Premium to the Principal Amount, the Return on Your Investment Will Be Lower Than the Return on Notes Purchased at the Principal Amount and the

Impact of Certain Key Terms of the Notes Will Be Negatively Affected.

Neither the payment of any Contingent Coupon or upon an Early Redemption nor the Payment at Maturity will be adjusted based on the original issue price you pay for the Notes. If you purchase Notes

at a price that differs from the Principal Amount of the Notes, then the return on your investment in such Notes held to the Early Redemption date upon an Early Redemption or the Maturity Date will differ from, and may be substantially less than, the

return on Notes purchased at the Principal Amount. If you purchase your Notes at a premium to the Principal Amount and hold them to the Early Redemption date upon an Early Redemption or the Maturity Date, the return on your investment in the Notes

will be lower than it would have been had you purchased the Notes at the Principal Amount or at a discount to the Principal Amount.

In addition, the impact of the payment of any Contingent Coupon or upon an Early Redemption and the trigger levels on the return on your investment will depend upon the price you pay for your Notes relative to the

Principal Amount. For example, if you purchase your Notes at a premium to the Principal Amount, the Notes are not redeemed early and the Final Level of the least performing reference asset is less than its trigger level, you will incur a greater

percentage decrease in your investment in the Notes than would have been the case if you had purchased the Notes at the Principal Amount. Similarly, any return from any Contingent Coupon received on the Notes

P-9

will be lower than it would have been had you purchased the Notes at the Principal Amount, relative to your initial investment.

Risks Relating to Characteristics of the Reference Assets

There Are Market Risks Associated With Each Reference Asset.

The value of each Reference Asset can rise or fall sharply due to factors specific to such Reference Asset, its Reference Asset Constituents and their issuers (the “Reference Asset Constituent

Issuers”), such as stock price volatility, earnings, financial conditions, corporate, industry and regulatory developments, management changes and decisions and other events, as well as general market factors, such as general stock market volatility

and levels, interest rates and economic and political conditions. In addition, recently, the coronavirus infection has caused volatility in the global financial markets and a slowdown in the global economy. Coronavirus or any other communicable

disease or infection may adversely affect the Reference Asset Constituent Issuers and, therefore, the Reference Assets. You, as an investor in the Notes, should make your own investigation into the Reference Assets, the Reference Asset Constituents

and the Reference Asset Constituent Issuers for your Notes. For additional information, see “Information Regarding the Reference Assets” in this pricing supplement.

Investors Are Exposed to the Market Risk of Each Reference Asset on Each Coupon Observation Date (Including the Final Valuation Date).

Your return on the Notes is not linked to a basket consisting of the Reference Assets. Rather, it will be contingent upon the performance of each Reference Asset. Unlike an instrument with a return

linked to a basket of indices, common stocks or other underlying securities, in which risk is mitigated and diversified among all of the components of the basket, you will be exposed equally to the risks related to each Reference Asset on each Coupon

Observation Date (including the Final Valuation Date). Poor performance by any Reference Asset over the term of the Notes will negatively affect your return and will not be offset or mitigated by a positive performance by any other Reference Asset.

For instance, if the Final Level of any Reference Asset is less than its Trigger Level on its Final Valuation Date, you will receive a negative return equal to the Least Performing Percentage Change, even if the Percentage Change of another Reference

Asset is positive or has not declined as much. Accordingly, your investment is subject to the market risk of each Reference Asset.

Because the Notes Are Linked to the Least Performing Reference Asset, You Are Exposed to a Greater Risk of Receiving No Contingent Coupons and Losing All or a

Substantial Portion of Your Initial Investment at Maturity Than If the Notes Were Linked to a Single Reference Asset Or Fewer Reference Assets.

The risk that you will receive no Contingent Coupons and lose all or a substantial portion of your initial investment in the Notes is greater if you invest in the Notes than the

risk of investing in substantially similar securities that are linked to the performance of only one Reference Asset. With more Reference Assets, it is more likely that the Closing Level or Final Level of any Reference Asset will be less than its

Coupon Barrier on any Coupon Observation Date (including the Final Valuation Date) than if the Notes were linked to a single Reference Asset or fewer Reference Assets.

In addition, a lower correlation between the performance of a pair of Reference Assets results in a greater likelihood that a Reference Asset will decline in value to a Closing

Level that is less than its Coupon Barrier on any Coupon Observation Date or a Final Level that is less than its Trigger Level on the Final Valuation Date. Although the correlation of the Reference Assets’ performance may change over the term of the

Notes, the economic terms of the Notes, including the Contingent Coupon, Coupon Barriers and Trigger Levels, are determined, in part, based on the correlation of the Reference Assets’ performance calculated using our internal models at the time when

the terms of the Notes are finalized. All things being equal, a higher Contingent Coupon and lower Coupon Barriers and Trigger Levels are generally associated with lower correlation of the Reference Assets. Therefore, if the performance of a pair of

Reference Assets is not correlated to each other or is negatively correlated, the risk that you will not receive any Contingent Coupons or that the Final Level of any Reference Asset is less than its Trigger Level will occur is even greater despite

lower Coupon Barriers and Trigger Levels. Therefore, it is more likely that you will not receive any Contingent Coupons and that you will lose all or a substantial portion of your initial investment at maturity.

We Have No Affiliation With Any Index Sponsor and Will Not Be Responsible for Any Actions Taken by Any Index Sponsor.

No index sponsor as specified under “Information Regarding the Reference Assets” (an “Index Sponsor”) is an affiliate of ours and no such entity will be involved in any offering of the Notes in any

way. Consequently, we have no control of any actions of any Index Sponsor, including any actions of the type that could adversely affect the value of the applicable Reference Asset or any amounts payable on the Notes. No Index Sponsor has any

obligation of any sort with respect to the Notes. Thus, no Index Sponsor has any obligation to take your interests into consideration for any reason, including in taking any actions that might affect the value of the Notes. None of our proceeds from

any issuance of the Notes will be delivered to any Index Sponsor, except to the extent that we are required to pay an Index Sponsor licensing fees with respect to the applicable Reference Asset.

The Reference Assets Reflect Price Return, Not Total Return.

The return on your Notes is based on the performance of the Reference Assets, which reflect the changes in the market prices of their respective Reference Asset Constituents. It is not, however, linked to “total

return” indices or strategies, which, in addition to reflecting those price returns, would also reflect dividends paid on the Reference Asset Constituents. The return on your Notes will not include such a total return feature or dividend component.

P-10

As Compared to Other Index Sponsors, Nasdaq, Inc. Retains Significant Control and Discretionary Decision-Making Over the Nasdaq-100 Index®, Which May Have an Adverse Effect on the Level of

the Nasdaq-100 Index® and on Your Notes.

Pursuant to the Nasdaq-100 Index® methodology, the Index Sponsor retains the right, from time to time, to exercise reasonable discretion as it deems appropriate in order to ensure index

integrity, including, but not limited to, changes to quantitative inclusion criteria. The Index Sponsor may also, due to special circumstances, apply discretionary adjustments to ensure and maintain quality of the Nasdaq-100 Index®.

Although it is unclear how and to what extent this discretion could or would be exercised, it is possible that it could be exercised by the Index Sponsor in a manner that materially and adversely affects the level of the Nasdaq-100 Index®

and, therefore, the market value of, and return on, your Notes. The Index Sponsor is not obligated to, and will not, take account of your interests in exercising the discretion described above.

The Notes are Subject to Risks Associated with Non-U.S. Companies.

The Notes are subject to risks associated with non-U.S. companies because certain of the Reference Asset Constituents may be the stocks of companies incorporated in one or more non-U.S. countries.

Investments linked to the value of non-U.S. companies involve particular risks. For example, non-U.S. companies are likely subject to accounting, auditing and financial reporting standards and requirements that differ from those applicable to U.S.

companies. Additionally, the prices of securities of non-U.S. companies are subject to political, economic, financial and social factors that are unique to such non-U.S. country’s geographical region. These factors include: recent changes, or the

possibility of future changes, in the applicable non U.S. government’s economic and fiscal policies; the possible implementation of, or changes in, currency exchange laws or other laws or restrictions applicable to non-U.S. companies or investments

in non-U.S. equity securities; fluctuations, or the possibility of fluctuations, in currency exchange rates; and the possibility of outbreaks of hostility, political instability, natural disaster or adverse public health developments. Non-U.S.

economies may also differ from the U.S. economy in important respects, including growth of gross national product, rate of inflation, capital reinvestment, resources and self-sufficiency, which may have a positive or negative effect on non-U.S.

securities prices.

The Notes are Subject to Small-Capitalization Stock Risks.

The Notes are subject to risks associated with small-capitalization companies because the Russell 2000® Index is

comprised of stocks of companies that are considered small-capitalization companies. These companies often have greater stock price volatility, lower trading volume and less liquidity than large-capitalization companies and therefore the Russell 2000® Index may be more volatile than an index in which a greater percentage of the Reference Asset Constituents are issued by large-capitalization

companies. Stock prices of small-capitalization companies are also more vulnerable than those of large-capitalization companies to adverse business and economic developments, and the stocks of small-capitalization companies may be thinly traded. In

addition, small-capitalization companies are typically less stable financially than large-capitalization companies and may depend on a small number of key personnel, making them more vulnerable to loss of personnel. Small-capitalization companies are

often given less analyst coverage and may be in early, and less predictable, periods of their corporate existences. Such companies tend to have smaller revenues, less diverse product lines, smaller shares of their product or service markets, fewer

financial resources and less competitive strengths than large-capitalization companies and are more susceptible to adverse developments related to their products.

Changes that Affect the Reference Assets May Adversely Affect the Market Value of, and Return on, the Notes.

The policies of each Index Sponsor concerning the calculation of the applicable Reference Asset, additions, deletions or substitutions of the Reference Asset Constituents and the manner in which

changes affecting those Reference Asset Constituents, such as stock dividends, reorganizations or mergers, may be reflected in the applicable Reference Asset and could adversely affect the market value of, and return on, the Notes. The market value

of, and return on, the Notes could also be affected if an Index Sponsor changes these policies, for example, by changing the manner in which it calculates the applicable Reference Asset, or if an Index Sponsor discontinues or suspends calculation or

publication of the applicable Reference Asset. If events such as these occur, the Calculation Agent may select a successor index or take other actions as discussed in the product supplement and, notwithstanding these adjustments, the market value of,

and return on, the Notes may be adversely affected.

Market Disruption Events and Postponements.

The Coupon Observation Dates (including the Final Valuation Date) and therefore the Coupon Payment Dates (including the Maturity Date), are subject to postponement as described herein and in the

product supplement due to the occurrence of one or more market disruption events. For a description of what constitutes a market disruption event as well as the consequences of that market disruption event, see “General Terms of the Notes—Market

Disruption Events” in the product supplement.

Risks Relating to Estimated Value and Liquidity

TD’s Initial Estimated Value of the Notes at the Time of Pricing (When the Terms of Your Notes Were Set on the Pricing Date) is Less Than the Public Offering Price of the Notes.

TD’s initial estimated value of the Notes is only an estimate. TD’s initial estimated value of the Notes is less than the public offering price of the Notes. The difference between the public offering price of the

Notes and TD’s initial estimated value reflects costs and expected profits associated with selling and structuring the Notes, as well as hedging its obligations under the Notes with a third party. Because hedging our obligations entails risks and may

be influenced by market forces beyond our control, this hedging may result in a profit that is more or less than expected, or a loss.

P-11

TD’s and GS&Co.’s Estimated Value of the Notes Are Determined By Reference to TD’s Internal Funding Rates and Are Not Determined By Reference to Credit Spreads or the

Borrowing Rate TD Would Pay for its Conventional Fixed-Rate Debt Securities.

TD’s initial estimated value of the Notes and GS&Co.’s estimated value of the Notes at any time are determined by reference to TD’s internal funding rate. The internal funding rate used in the

determination of the estimated value of the Notes generally represents a discount from the credit spreads for TD’s conventional fixed-rate debt securities and the borrowing rate TD would pay for its conventional fixed-rate debt securities. This

discount is based on, among other things, TD’s view of the funding value of the Notes as well as the higher issuance, operational and ongoing liability management costs of the Notes in comparison to those costs for TD’s conventional fixed-rate debt,

as well as estimated financing costs of any hedge positions, taking into account regulatory and internal requirements. If the interest rate implied by the credit spreads for TD’s conventional fixed-rate debt securities, or the borrowing rate TD would

pay for its conventional fixed-rate debt securities were to be used, TD would expect the economic terms of the Notes to be more favorable to you. Additionally, assuming all other economic terms are held constant, the use of an internal funding rate

for the Notes is expected to increase the estimated value of the Notes at any time.

TD’s Initial Estimated Value of the Notes Does Not Represent Future Values of the Notes and May Differ From Others’ (Including GS&Co.’s) Estimates.

TD’s initial estimated value of the Notes was determined by reference to its internal pricing models when the terms of the Notes are set. These pricing models take into account a number of

variables, such as TD’s internal funding rate on the Pricing Date, and are based on a number of assumptions as discussed further under “Additional Information Regarding the Estimated Value of the Notes” herein. Different pricing models and

assumptions (including the pricing models and assumptions used by GS&Co.) could provide valuations for the Notes that are different from, and perhaps materially less than, TD’s initial estimated value. Therefore, the price at which GS&Co.

would buy or sell your Notes (if GS&Co. makes a market, which it is not obligated to do) may be materially less than TD’s initial estimated value. In addition, market conditions and other relevant factors in the future may change, and any

assumptions may prove to be incorrect.

The Price At Which GS&Co. Would Buy or Sell Your Notes (If GS&Co. Makes a Market, Which It Is Not Obligated to Do) Will Be Based On GS&Co.’s Estimated Value of Your

Notes.

GS&Co.’s estimated value of the Notes is determined by reference to its pricing models and takes into account TD’s internal funding rate. If GS&Co. buys or sells your Notes (if it makes a

market, which it is not obligated to do so) it will do so at prices that reflect the estimated value determined by reference to GS&Co.’s pricing models at that time. The price at which GS&Co. will buy or sell your Notes at any time also will

reflect its then current bid and ask spread for similar sized trades of structured notes. If a party other than the Agents or their affiliates is buying or selling your Notes in the secondary market based on its own estimated value of your Notes

which is calculated by reference to TD’s credit spreads or the borrowing rate TD would pay for its conventional fixed-rate debt securities (as opposed to TD’s internal funding rate), the price at which such party would buy or sell your Notes could be

significantly less.

GS&Co.’s pricing models consider certain variables, including principally TD’s internal funding rate, interest rates (forecasted, current and historical rates), volatility, price-sensitivity

analysis and the time to maturity of the Notes. These pricing models are proprietary and rely in part on certain assumptions about future events, which may prove to be incorrect. As a result, the actual value you would receive if you sold your Notes

in the secondary market, if any, to others may differ, perhaps materially, from the estimated value of your Notes determined by reference to GS&Co.’s models, taking into account TD’s internal funding rate, due to, among other things, any

differences in pricing models or assumptions used by others. See “— The Market Value of Your Notes May Be Influenced by Many Unpredictable Factors” herein.

In addition to the factors discussed above, the value and quoted price of your Notes at any time will reflect many factors and cannot be predicted. If GS&Co. makes a market in the Notes, the

price quoted by GS&Co. would reflect any changes in market conditions and other relevant factors, including any deterioration in TD’s creditworthiness or perceived creditworthiness. These changes may adversely affect the value of your Notes,

including the price you may receive for your Notes in any market making transaction. To the extent that GS&Co. makes a market in the Notes, the quoted price will reflect the estimated value determined by reference to GS&Co.’s pricing models

at that time, plus or minus GS&Co.’s then current bid and ask spread for similar sized trades of structured notes.

Furthermore, if you sell your Notes, you will likely be charged a commission for secondary market transactions, or the price will likely reflect a dealer discount. This commission or discount will

further reduce the proceeds you would receive for your Notes in a secondary market sale.

There is no assurance that GS&Co. or any other party will be willing to purchase your Notes at any price and, in this regard, GS&Co. is not obligated to make a market in the Notes. See

“—There May Not Be an Active Trading Market for the Notes — Sales in the Secondary Market May Result in Significant Losses” herein.

The Market Value of Your Notes May Be Influenced by Many Unpredictable Factors.

When we refer to the market value of your Notes, we mean the value that you could receive for your Notes if you chose to sell them in the open market before the Maturity Date. A number of factors, many of which are

beyond our control, will influence the market value of your Notes, including:

| • |

the levels of the Reference Assets;

|

| • |

the volatility – i.e., the frequency and magnitude of changes – in the levels of the Reference Assets;

|

| • |

the correlation of the Reference Assets;

|

P-12

| • |

the dividend rates, if applicable, of the Reference Asset Constituents;

|

| • |

economic, financial, regulatory and political, military, public health or other events that may affect the prices of any of the Reference Asset Constituents and thus the level of the Reference Assets;

|

| • |

interest rates and yield rates in the market;

|

| • |

the time remaining until your Notes mature;

|

| • |

any fluctuations in the exchange rate between currencies in which the Reference Asset Constituents are quoted and traded and the U.S. dollar, as applicable; and

|

| • |

our creditworthiness, whether actual or perceived, and including actual or anticipated upgrades or downgrades in our credit ratings or changes in other credit measures.

|

These factors will influence the price you will receive if you sell your Notes before maturity, including the price you may receive for your Notes in any market-making

transaction. If you sell your Notes prior to maturity, you may receive less than the Principal Amount of your Notes.

The future levels of the Reference Assets cannot be predicted. The actual change in the level of the Reference Assets over the term of the Notes, as well as the Payment at Maturity, may bear little

or no relation to the hypothetical historical Closing Levels of the Reference Assets or to the hypothetical examples shown elsewhere in this pricing supplement.

There May Not Be an Active Trading Market for the Notes — Sales in the Secondary Market May Result in Significant Losses.

There may be little or no secondary market for the Notes. The Notes will not be listed or displayed on any securities exchange or electronic communications network. TDS, GS&Co. and our or their

respective affiliates may make a market for the Notes; however, they are not required to do so. TDS, GS&Co. and our or their respective affiliates may stop any market-making activities at any time. Even if a secondary market for the Notes

develops, it may not provide significant liquidity or trade at prices advantageous to you. We expect that transaction costs in any secondary market would be high. As a result, the difference between bid and ask prices for your Notes in any secondary

market could be substantial.

If you sell your Notes before the Maturity Date, you may have to do so at a substantial discount from the public offering price irrespective of the level of the Reference Asset and, as a result, you

may suffer substantial losses.

If the Level of Any Reference Asset Changes, the Market Value of Your Notes May Not Change in the Same Manner.

Your Notes may trade quite differently from the performance of any of the Reference Assets. Changes in the level of any Reference Asset may not result in a comparable change in the market value of

your Notes. Even if the level of each Reference Asset remain greater than or equal to its Trigger Level and Coupon Barrier or increases to greater than the Initial Level during the term of the Notes, the market value of your Notes may not increase by

the same amount and could decline.

Risks Relating to Hedging Activities and Conflicts of Interest

The Underwriting Discount, Offering Expenses and Certain Hedging Costs Are Likely to Adversely Affect Secondary Market Prices.

Assuming no changes in market conditions or any other relevant factors, the price, if any, at which you may be able to sell the Notes will likely be less than the public offering price. The public

offering price includes, and any price quoted to you is likely to exclude, the underwriting discount paid in connection with the initial distribution, offering expenses as well as the cost of hedging our obligations under the Notes. In addition, any

such price is also likely to reflect dealer discounts, mark-ups and other transaction costs, such as a discount to account for costs associated with establishing or unwinding any related hedge transaction. In addition, if the dealer from which you

purchase Notes, or one of its affiliates, is to conduct hedging activities for us in connection with the Notes, that dealer, or one of its affiliates, may profit in connection with such hedging activities and such profit, if any, will be in addition

to the compensation that the dealer receives for the sale of the Notes to you. You should be aware that the potential for the dealer or one of its affiliates to earn fees in connection with hedging activities may create a further incentive for the

dealer to sell the Notes to you in addition to the compensation they would receive for the sale of the Notes.

Trading and Business Activities of TD, the Agents and Their Respective Affiliates May Adversely Affect the Market Value of, and Any Amount Payable on, the Notes.

TD, GS&Co. and our or their respective affiliates may hedge our obligations under the Notes by purchasing securities, futures, options or other derivative instruments with returns linked or related to changes in

the level of the Reference Asset or the prices of one or more Reference Asset Constituents, and we or they may adjust these hedges by, among other things, purchasing or selling any of the foregoing at any time. It is possible that we, GS&Co. or

one or more of our or their respective affiliates could receive substantial returns from these hedging activities while the market value of, and any amount payable on, the Notes declines. We, GS&Co. or one or more of our or their respective

affiliates may also issue or underwrite other securities or financial or derivative instruments with returns linked or related to the performance of the Reference Assets or one or more Reference Asset Constituents.

These trading activities may present a conflict between the holders’ interest in the Notes and the interests we, GS&Co. and our or their respective affiliates will have in our or their

proprietary accounts, in facilitating transactions, including options and other derivatives transactions, for our or their customers’ accounts and in accounts under our or their management. These trading activities could be adverse to the interests

of the holders of the Notes.

P-13

We, GS&Co. and our or their respective affiliates may, at present or in the future, engage in business with one or more Reference Asset Constituent Issuers, including making loans to or

providing advisory services to those companies. These services could include investment banking and merger and acquisition advisory services. These business activities may present a conflict between us, GS&Co. or one or more of our or their

respective affiliates’ obligations, and your interests as a holder of the Notes. Moreover, we, GS&Co. and our or their respective affiliates may have published, and in the future expect to publish, research reports with respect to any of the

Reference Assets or one or more Reference Asset Constituents. This research is modified from time to time without notice and may express opinions or provide recommendations that are inconsistent with purchasing or holding the Notes. Even if we or our

affiliates, or GS&Co. or its affiliates, provides research that expresses a negative opinion about one or more of the Reference Asset Constituents, or if market conditions in the finance sector or otherwise change, the composition of the

Reference Assets will not change during the term of the Notes (except under the limited circumstances described below). Any of these business activities by us, GS&Co. and our or their respective affiliates may affect the level of the Reference

Assets or one or more Reference Asset Constituents and, therefore, the market value of, and any amount payable on, the Notes.

There Are Potential Conflicts of Interest Between You and the Calculation Agent.

The Calculation Agent will, among other things, determine the amount of your payment on the Notes. We will serve as the Calculation Agent and may appoint a different Calculation Agent after the

Issue Date without notice to you. The Calculation Agent will exercise its judgment when performing its functions and may take into consideration our ability to unwind any related hedges. Because this discretion by the Calculation Agent may affect

payments on the Notes, the Calculation Agent may have a conflict of interest if it needs to make any such decision. For example, the Calculation Agent may have to determine whether a market disruption event affecting any Reference Asset has occurred.

This determination may, in turn, depend on the Calculation Agent’s judgment whether the event has materially interfered with our ability or the ability of one of our affiliates to unwind our hedge positions. Because this determination by the

Calculation Agent will affect the payment on the Notes, the Calculation Agent may have a conflict of interest if it needs to make a determination of this kind. For additional information as to the Calculation Agent’s role, see “General Terms of the

Notes — Role of Calculation Agent” in the product supplement.

Risks Relating to General Credit Characteristics

Investors Are Subject to TD’s Credit Risk, and TD’s Credit Ratings and Credit Spreads May Adversely Affect the Market Value of the Notes.

Although the return on the Notes will be based on the performance of the Least Performing Reference Asset, the payment of any amount due on the Notes is subject to TD’s credit risk. The Notes are

TD’s senior unsecured debt obligations. Investors are dependent on TD’s ability to pay all amounts due on the Notes and, therefore, investors are subject to the credit risk of TD and to changes in the market’s view of TD’s creditworthiness. Any

decrease in TD’s credit ratings or increase in the credit spreads charged by the market for taking TD’s credit risk is likely to adversely affect the market value of the Notes. If TD becomes unable to meet its financial obligations as they become

due, investors may not receive any amounts due under the terms of the Notes.

Risks Relating to Canadian and U.S. Federal Income Taxation

Significant Aspects of the Tax Treatment of the Notes Are Uncertain.

The U.S. tax treatment of the Notes is uncertain. Please read carefully the section entitled “Material U.S. Federal Income Tax Consequences” herein and in the product supplement. You should consult

your tax advisor as to the tax consequences of your investment in the Notes.

For a discussion of the Canadian federal income tax consequences of investing in the Notes, please see the discussion in the product supplement under “Supplemental Discussion of Canadian Tax

Consequences” and the further discussion herein under “Summary”. If you are not a Non-resident Holder (as that term is defined in the prospectus) for Canadian federal income tax purposes or if you acquire the Notes in the secondary market, you should

consult your tax advisors as to the consequences of acquiring, holding and disposing of the Notes and receiving the payments that might be due under the Notes.

General Risk Factors

We May Sell an Additional Aggregate Principal Amount of the Notes at a Different Public Offering Price.

At our sole option, we may decide to sell an additional aggregate Principal Amount of the Notes subsequent to the date of this pricing supplement. The public offering price of the Notes in the subsequent sale may

differ substantially (higher or lower) from the original public offering price you paid as provided on the cover of this pricing supplement.

P-14

Hypothetical Returns

The examples set out below are included for illustration purposes only. They should not be taken as an indication or prediction of future investment results and are intended merely to illustrate the

impact that the various hypothetical Closing Levels and Final Levels of the Reference Assets on a Coupon Observation Date and on the Final Valuation Date, respectively, could have on the amount payable on a Coupon Payment Date or the Payment at

Maturity, as the case may be, assuming all other variables remain constant.

The examples below are based on a range of Closing Levels that are entirely hypothetical; the levels of the Reference Assets on any day throughout the term of the Notes, including the Closing Levels

of the Reference Assets on any Coupon Observation Date or the Final Levels on the Final Valuation Date, cannot be predicted. The Reference Assets have been highly volatile in the past, meaning that the levels of the Reference Assets have changed

considerably in relatively short periods, and their performance cannot be predicted for any future period.

The information in the following examples reflects hypothetical rates of return on the Notes assuming that they are purchased on the Issue Date at the Principal Amount and held to an Early

Redemption Date or the Maturity Date, as the case may be. If you sell your Notes in a secondary market prior to an Early Redemption or the Maturity Date, as the case may be, your return will depend upon the market value of your Notes at the time of

sale, which may be affected by a number of factors that are not reflected in the examples below, such as interest rates, the volatility of the Reference Assets, the correlation of the Reference Assets and our creditworthiness. In addition, the

estimated value of your Notes at the time the terms of your Notes were set on the Pricing Date (as determined by reference to pricing models used by us) is less than the Public Offering Price of your Notes. For more information on the estimated value

of your Notes, see “Additional Risk Factors — Risks Relating to Estimated Value and Liquidity — TD’s Initial Estimated Value of the Notes at the Time of Pricing (When the Terms of Your Notes Were Set on the Pricing Date) is Less Than the Public

Offering Price of the Notes” in this pricing supplement. The information in the examples also reflect the key terms and assumptions in the box below.

|

Key Terms and Assumptions

|

|

|

Principal Amount

|

$1,000

|

|

Contingent Coupon

|

$8.583

|

|

Coupon Barrier

|

With respect to each Reference Asset, 70.00% of its Initial Level

|

|

Trigger Level

|

With respect to each Reference Asset, 70.00% of its Initial Level

|

|

Neither a market disruption event nor a non-Trading Day occurs on an originally scheduled Coupon Observation Date (including the originally scheduled Final Valuation Date)

|

|

|

No change in or affecting any of the Reference Asset Constituent Stocks or the method by which the applicable sponsor calculates any Reference Asset

|

|

|

Notes purchased on the Issue Date at the Principal Amount and held to the Maturity Date or Early Redemption Date

|

|

The actual performance of the Reference Assets over the term of your Notes, the actual Closing Levels of the Reference Assets on any Coupon Observation Date, the Contingent Coupon

payable, if any, on any Coupon Payment Date, as well as the amount payable upon an Early Redemption or at maturity, may bear little relation to the hypothetical examples shown below or to the historical levels of the Reference Assets shown elsewhere

in this pricing supplement. For information about the historical levels of the Reference Assets, see “Information Regarding the Reference Assets” below.

Also, the hypothetical examples shown below do not take into account the effects of applicable taxes. Because of the U.S. tax treatment applicable to your Notes, tax liabilities could affect the

after-tax rate of return on your Notes to a comparatively greater extent than the after-tax return on the Reference Asset Constituent Stocks.

P-15

Hypothetical Contingent Coupon Payments

The examples below show hypothetical performances of each Reference Asset as well as the hypothetical Contingent Coupons, if any, that we would pay on each Coupon Payment Date with respect to each

$1,000 Principal Amount of the Notes if the hypothetical Closing Level of each Reference Asset on the applicable Coupon Observation Date was the percentage of its Initial Level shown.

Scenario 1

|

Hypothetical Coupon

Observation Date

|

Hypothetical Closing

Level of the NDX (as

Percentage of its Initial

Level)

|

Hypothetical Closing

Level of the RTY (as

Percentage of its Initial

Level)

|

Hypothetical Closing

Level of the SPX (as

Percentage of its Initial

Level)

|

Hypothetical

Contingent Coupon

|

|

First

|

40.00%

|

65.00%

|

68.00%

|

$0.000

|

|

Second

|

25.00%

|

60.00%

|

120.00%

|

$0.000

|

|

Third

|

70.00%

|

80.00%

|

75.00%

|

$8.583

|

|

Fourth

|

80.00%

|

55.00%

|

35.00%

|

$0.000

|

|

Fifth

|

25.00%

|

50.00%

|

45.00%

|

$0.000

|

|

Sixth

|

110.00%

|

75.00%

|

105.00%

|

$8.583

|

|

Seventh

|

20.00%

|

40.00%

|

30.00%

|

$0.000

|

|

Eighth

|

85.00%

|

65.00%

|

60.00%

|

$0.000

|

|

Ninth