UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM

(Mark one)

☒ ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended

or

☐ TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from____________ to ____________

Commission file number:

.

(Exact name of registrant as specified in its charter)

|

|

|

|

|

(State or Other Jurisdiction of Incorporation or Organization) |

|

(I.R.S. Employer Identification No.) |

|

|

|

|

|

|

|

|

|

|

|

|

|

(Address of Principal Executive Offices) |

|

(Zip Code) |

(Registrant’s telephone number, including area code)

Not applicable.

(Former name, former address and former fiscal year, if changed since last report)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class Name of each exchange on which registered

|

|

|

|

Securities registered pursuant to Section 12(g) of the Act: None.

Indicate by check mark if the registrant is a well‑known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or Section 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S‑T during the preceding 12 months (or for such shorter period that the registrant was required to submit).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non‑accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and "emerging growth company" in Rule 12b‑2 of the Exchange Act. (Check one):

|

|

Large accelerated filer ☐ |

|

| Accelerated filer ☐ |

||

|

|

☐ |

|

| Smaller reporting company ☒ | ||

| Emerging growth company ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b‑2 of the Act). Yes ☐ ☒

As of June 30, 2019, the aggregate market value of the registrant’s common stock held by non‑affiliates of the registrant was $

DOCUMENTS INCORPORATED BY REFERENCE

|

Document |

|

Parts Into Which Incorporated |

|

Proxy Statement for the 2020 Annual Meeting of Shareholders (Proxy Statement) |

|

Part III |

| i |

General

Image Sensing Systems, Inc. (referred to in this Annual Report on Form 10-K as “we,” “us,” “our” and the “Company”) develops and markets video and radar processing products for use in traffic applications such as intersection control, highway, bridge and tunnel traffic management and traffic data collection.

We are a leading provider of above-ground detection products and solutions for the intelligent transportation systems (“ITS”) industry. Our family of products, which we market as Autoscope® video or video products (“Autoscope”), RTMS® radar or radar products (“RTMS”), and IntellitraffiQ® or iQ products provides end users with the tools needed to optimize traffic flow and enhance driver safety. Our technology analyzes signals from sophisticated sensors and transmits the information to management systems and controllers or directly to users. Our products provide end users with complete solutions for the intersection and transportation markets.

Our technology is a process in which software, rather than humans, examines outputs from various types of sophisticated sensors to determine what is happening in a field of view. In the ITS industry, this process is a critical component of managing congestion and traffic flow. In many cities, it is not possible to build roads, bridges and highways quickly enough to accommodate the increasing congestion levels. On average, United States commuters lose 97 hours a year in congestion, which costs motorists $87 billion a year in time, an average of $1,365 per driver (per INRIX 2018 Global Traffic scorecard). We believe this growing use of vehicles will make our ITS solutions increasingly necessary to complement existing and new roadway infrastructure to manage traffic flow and optimize throughput.

We believe our solutions are technically superior to those of our competitors because they have a higher level of accuracy, limit the occurrence of false detection, are generally easier to install with lower costs of ownership, work effectively in a multitude of light and weather conditions, and provide end users the ability to manage inputs from a variety of sensors for a number of tasks. It is our view that the technical advantages of our products make our solutions well suited for use in ITS markets.

We believe the strength of our distribution channels positions us to increase the penetration of our technology‑driven solutions in the marketplace. We market our Autoscope video products in the United States, Mexico, Canada and the Caribbean through exclusive agreements with Econolite Control Products, Inc. (“Econolite”), which we believe is the leading distributor of ITS intersection control products in these markets.

We market the RTMS radar systems to a network of distributors globally. On a limited basis, we may sell directly to the end user. We market our Autoscope video products outside the United States, Mexico, Canada and the Caribbean through a combination of distribution and direct sales channels through our office in Spain. Our end users primarily include governmental agencies and municipalities.

Industry Overview

The Intelligent Transportation Systems Market. ITS encompasses a broad range of information processing and control electronics technologies that, when integrated into roadway infrastructure, help monitor and manage traffic flow, reduce congestion and enhance driver safety. The ITS market has been built around the detection of conditions that impact the proper operation of roadway infrastructure. ITS applications include a wide array of traffic management systems, such as traffic signal control, tolling and variable messaging signs. ITS technologies include video vehicle detection, inductive loop detection, sensing technologies (such as radar), floating cellular data, computational technologies and wireless communications.

In traffic management applications, vehicle detection products are used for automated vehicle detection and are a primary data source upon which ITS solutions are built. Traditionally, automated vehicle detection is performed using inductive wire loops buried in the pavement. However, in‑pavement loop detectors are costly to install, difficult to maintain, expensive to repair and not capable of either wide‑area vehicle detection without installations of multiple loops.

| 1 |

Above‑ground detection solutions for ITS offer several advantages to in‑pavement loop detectors. Above‑ground detection solutions tend to have a lower total cost of ownership than in‑pavement loop detectors because above‑ground solutions are non‑destructive to road surfaces, do not require closing roadways to install or repair, and are capable of wide‑area vehicle detection with a single device, thus enabling one input device to do the work of many in‑pavement loops. Due to their location above-ground, these solutions have no exposure to the wear and tear associated with expanding and contracting pavement and generally less exposure to the vibration and compaction caused by traffic. Furthermore, in the event of malfunction or product failure, above‑ground detection solutions can be serviced and repaired without shutting down the roadway. Each of these factors results in greater up‑time and increased reliability of above‑ground detection solutions compared to in‑pavement loop detectors. These technology solutions also offer a broader set of detection capabilities and a wider field of view than in‑pavement loop detectors. In addition, a single unit video‑ or radar‑based system can detect and measure a variety of parameters, including vehicle presence, counts, speed, length, time occupancy, headway and flow rate as well as environmental factors and obstructions to the roadway. An equivalent installation using loops would require many installations per lane.

We believe that several trends are driving the growth in ITS and adjacent market segments:

Proliferation of Traffic. In many countries, there has been a surge in the number of vehicles on roadways. Due to the growth of emerging economies and elevated standards of living, more people desire and are able to afford automobiles. The number of vehicles utilizing the world’s roadway infrastructure is growing at a quicker pace than new roads, bridges and highways are being constructed. According to the Federal Highway Administration, American drivers put a record 3.26 trillion miles on public roads and highways in 2018, an increase of 1.0% from 3.22 trillion miles in 2017. Overall, the growth in roadway infrastructure is failing to match the surge in the number of vehicles using it. Above-ground detection-based traffic management and control systems address the problem by monitoring high traffic areas and analyzing data that can be used to mitigate traffic problems.

The Demographics of Urbanization. Accelerated worldwide urbanization drives the creation and expansion of middle classes and produces heightened demand for automobiles. By 2018, there were 548 cities around the world with over 1 million inhabitants, and by 2030, a projected 706 cities will have at least 1 million residents. Because automobiles can be introduced to a metropolitan area faster than roadway infrastructure can be constructed, the result is continuously worsening traffic. Expanding the roadway infrastructure is slow and costly to implement, and often environmentally undesirable, so government agencies are increasingly turning to technology‑based congestion solutions that optimize performance and throughput of existing and new roadway infrastructure. Detection is the requisite common denominator for any technology‑based solution.

The Melding of Large City Service Domains. Large cities require a wide range of service domains, including traffic. These cities are increasingly turning to centralized management of these service domains, employing a command and control model that requires sharing and integrating data across service domains to operate effectively and lower total cost. For example, data collected for the traffic management service domain is relevant to all of the other service domains. This means that each sensor can supply information to multiple domain services. In turn, the sharing of detection information across service domains should increase the level of sophistication required to process and interpret that information. Additionally, above-ground detection products are more capable of performing certain complicated tasks than humans. This results in the realization of "smart city" initiatives through above-ground detection solutions cost effective, which we believe will result in the extensive proliferation of sophisticated sensors and detection devices.

Solutions for Adjacent Markets. We believe that the adjacent markets of ITS, connected vehicles and security/surveillance are converging, and that this convergence will accelerate as above-ground detection systems become more cost‑effective now that a single sensor can be used for multiple purposes. Because the technologies involved are closely related, our sensor technology can be adapted to or is already capable of addressing these adjacent markets.

Our Competitive Strengths

We are a leading provider of above-ground detection products and solutions for the ITS industry. We have the following competitive strengths that we expect will continue to enhance our leadership position:

Leading Proprietary Technologies and Strong Global Brand Recognition. Over the last two decades, we have developed or acquired a proprietary portfolio of complex software algorithms and applications that we have continuously enhanced and refined. These algorithms, which include our advanced signal processing technologies, allow our video and radar products to capture and analyze objects in diverse weather and lighting conditions and to balance the accuracy of positive detection and the avoidance of false detections. Due to the strength of our proprietary technologies, we believe we command premium pricing. Above-ground detection technologies similar to ours are also difficult to develop and refine in a commercially viable manner. We are therefore well positioned to quickly introduce innovative next‑generation products to market.

| 2 |

Proven Ability to Develop, Enhance and Market New Products. We are continually developing and enhancing our product offerings. Over the last three decades, we have demonstrated our ability to lead the market with new products and product enhancements. For example, the Autoscope Solo system was the first fully integrated color camera, zoom lens and machine vision processor in the above-ground detection market. Our RTMS Radar was the first radar‑based technology solutions for ITS applications, and we continue to lead the market with technology enhancements and new products. Furthermore, we recently introduced the RTMS Echo, an industry-leading, powerful IoT-ready device that has been built from the ground up to provide access to more actionable data than any radar on the market. We have successfully collaborated with our long‑term channel partners to market these products. We believe that developing, enhancing and marketing new products with our partners can translate into strong organic revenue growth and higher levels of profitability.

Leading Distribution Channel. Since 1991, we have maintained a relationship with Econolite, which has the exclusive right to manufacture, market and distribute our Autoscope video products in the United States, Mexico, Canada and the Caribbean. We believe that Econolite is one of the leading distributors of ITS control products in North America and the Caribbean. This relationship enhances our ability to commercialize and market new products and allows us to focus more resources on developing advanced signal processing software algorithms.

Broad Product Portfolio. Our product portfolio leverages our core software‑based algorithms to enable end users to detect and monitor objects in a designated field of view. We believe that our family of Autoscope video, RTMS radar, and IntellitraffiQ software products allows us to offer a broad product portfolio that meets the needs of our end users.

Experienced Management Team and Engineering Staff. Our management team and engineering staff are highly experienced in the ITS and software industries. Additionally, the continuity of our engineering staff should allow the uninterrupted development of new or improved products.

Our Growth Strategy

As part of our growth strategy, we seek to:

Enhance and Extend Our Technology Leadership in ITS. We believe we have established ourselves as a leading provider of technology in the ITS market segment. We believe that we continue to have an opportunity to accelerate our growth. We plan to do this by improving the accuracy and functionality of our products and opportunistically expanding our product offering into adjacent markets, as well as expanding our portfolio and channels through licensing. Having developed and introduced our next-generation RTMS radar product, we expect to take advantage of our technical leadership in ITS and further differentiate us from our competitors.

Expand into Adjacent Markets. One of our core competencies is the development and implementation of advanced above-ground detection platforms. While our focus has been on the application of this technology to the transportation market, we are now seeing more opportunities to deploy our highly accurate and ruggedized systems into adjacent markets. These adjacent opportunities are largely driven by the convergence of user needs and expectations within the transportation, safety, surveillance, and broader “smart-city” markets. We are continuously refining our technology road-map in response to emerging technology enablers and market needs. We believe our recent product introductions and near-term research and development initiatives will enable us to become a leading supplier of critical detection components that provide actionable data across incremental markets.

Increase the Scope of Our Distribution and Direct Sales. We have made substantial investments in product adjustments to tailor our solutions to the differing needs of our international end users and in new product acquisitions for both domestic and international markets. We have also invested in sales and marketing expansion, with a focus on our European subsidiaries. Markets in Eastern Europe, the Asia/Pacific region, the Middle East, Africa and South America, which have historically lagged North America and Western Europe in their use of above-ground detection, have begun to increase the adoption of detection technology in their traffic systems. We intend to take advantage of the accelerated pace of the adoption of above-ground detection throughout the developing world by increasing end user awareness of our products and applications as well as improve user aptitude.

Our Products and Solutions

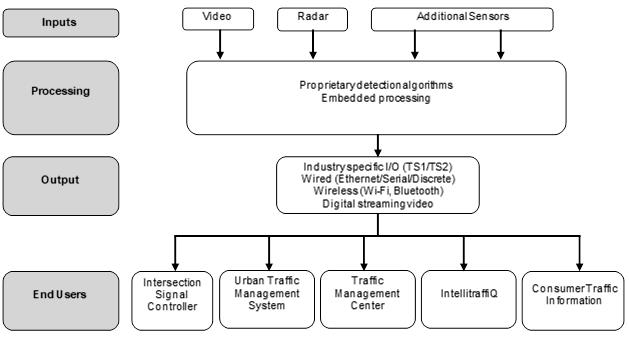

Our vehicle and traffic detection products are critical components of many ITS applications. Our Autoscope video systems and RTMS radar systems convert sensory input collected by video and radar modules into vehicle detection and traffic data used to operate, monitor and improve the efficiency and safety of roadway infrastructure. At the core of each product line are proprietary digital signal processing algorithms and sophisticated embedded software that analyze sensory input and deliver actionable data to integrated applications. We invested approximately $4.0 million and $3.6 million on research and development in 2019 and 2018, respectively, to develop and enhance our product technology. Our digital signal processing software algorithms represent a foundation on which to support additional product development into the automatic incident detection (AID) market. A diagram displaying our fundamental product architecture is shown below.

| 3 |

The Image Sensing Product Architecture

Autoscope Video. Our Autoscope video system processes video input from a traffic scene in real time and extracts the required traffic data, including vehicle presence, bicycle presence/differentiation, counts, speed, length, time occupancy (percent of time the detection zone is occupied), turning movements (quantifying the movement of vehicles) and flow rate (vehicles per hour per lane). Autoscope supports a variety of standard video cameras or can be purchased with an integrated high-definition video camera. For intersections, the system communicates with the intersection signal controller, which changes the traffic lights based on the data provided. The data may also be transmitted to a traffic management center via the internet or other standard communication means and processed in real time to assist in traffic management and stored for later analysis for traffic planning purposes.

The Autoscope system comes in two varieties. Autoscope Vision is our flagship integrated product that includes a color high-definition, zoom camera and a machine vision processing computer contained in a compact housing that is our leading offering in the North American market. Autoscope Pn-520 is our card-only machine vision processing computer that is located in an intersection signal controller, control hub, incident management center or traffic management center that receives video from a separate camera. The Pn-520 and its variants are our top selling Autoscope products in international markets. Autoscope rack-based products offer digital MPEG‑4 video streaming, high-speed Ethernet interface, web browser maintenance and data and video over power line communications. The Autoscope Vision product offers high definition streaming video, built-in WiFi for quick and easy setup, cost-effective three-wire cable, and full screen object detection and motion tracking algorithm technology for best in class detection accuracy.

RTMS Radar. Our RTMS radar systems use radar to measure vehicle presence, volume, occupancy, speed and classification information for roadway monitoring applications. Data is transmitted to a central computer at a traffic management center via standard communication means, including wireless. Data can be processed in real time to assist in traffic management and stored for later analysis for traffic planning purposes.

RTMS radar is an integrated radar transmitter/receiver and embedded processor contained in a compact, self‑contained unit. The unit is typically situated on roadway poles and side‑fired, making it especially well-suited for highway detection applications.

The RTMS radar system is available in different varieties which include the RTMS Sx-300 and the RTMS Echo. RTMS Sx-300 is a non-intrusive radar for the detection and measurement of traffic on roadways and is currently our leading offering in both North America and the Middle East. The RTMS Sx-300 HDCAM has a high-definition camera that provides the user with visual setup confirmation, data capture and real-time traffic surveillance. The Sx-300 HDCAM has been deployed in North America for various applications such as ramp metering and wrong way driver detection. We also offer a wrong way module that interfaces with the Sx-300 HDCAM digital video stream and leverages our video detection algorithms to detect occurrences of vehicles driving the incorrect direction. The event is captured and sent to the end users via short message service (SMS) and email in parallel with actuation or roadside or in-pavement warning systems. Our recently launched next generation RTMS Echo provides access to more actionable traffic data than any radar on the market. We believe this radar gives transportation engineers an easy to use, highly accurate radar that provides sophisticated traffic data.

| 4 |

IntellitraffiQ. Our IntellitraffiQ software provides traffic measurement and data collection across large and small areas. An enterprise-level system capable of monitoring traffic in hundreds of locations, IntellitraffiQ's simple yet powerful user interface helps traffic operation centers make decisions to keep traffic flowing smoothly.

IntellitraffiQ currently is available in an on-premise system that allows traffic managers the ability to monitor their network of sensors from one screen within the traffic management center. The IntellitraffiQ maps provide an interactive map of their sensor network, while displaying data coming directly from the sensors in the field.

Distribution, Sales and Marketing

We market and sell our products globally. Together with our partners, we offer a combination of high‑performance detection technology and experienced local support. Our end users primarily consist of federal, state, city and county departments of transportation, port, highway, tunnel and other transportation authorities. The decision‑makers within these entities typically are traffic planners and engineers, who in turn often rely on consulting firms that perform planning and feasibility studies. Our products sometimes are sold directly to system integrators or other suppliers of systems and services who are operating under subcontracts in connection with major road construction contracts.

Sales of Autoscope Video in the United States, Mexico, Canada and the Caribbean. We have granted Econolite an exclusive right to manufacture, market and distribute the Autoscope video system in the United States, Mexico, Canada and the Caribbean. The agreement with Econolite grants it a first refusal right that arises when we make a proposal to Econolite to extend the license to additional products in the United States, Mexico, Canada and the Caribbean and a first negotiation right that arises when we make a proposal to Econolite to include rights corresponding to Econolite’s rights under our current agreements in countries not in these territories. Econolite provides the marketing and technical support needed for its sales in these territories. Econolite pays us a royalty on the revenue derived from its sales of the Autoscope system. We provide second‑tier technical support for Autoscope and video products. We have the right to terminate our agreements with Econolite if it does not meet minimum annual sales levels or if Econolite fails to make payments as required by the agreements. In 2008, the term of the original agreement with Econolite, as amended, was extended to 2031. The agreement can be terminated by either party upon three years’ notice.

Sales of RTMS Radar in North America, the Caribbean and Latin America. We market the RTMS radar systems to a network of distributors covering countries in North America, the Caribbean and Latin America. On a limited basis, we sell directly to the end user. We provide technical support to these distributors from our various North American locations.

Sales in Europe, Asia, the Middle East and Africa. We market our Autoscope video and RTMS radar product lines of products to a network of distributors covering countries in Europe, the Middle East, Africa and Asia through our wholly‑owned subsidiaries that have offices in Europe. On a limited basis, we sell directly to the end user. Technical support to these distributors is provided by our wholly‑owned subsidiaries in Europe, with second‑tier support provided by our engineering groups. From time to time, we may grant exclusive rights to Econolite for markets outside of our significant markets for certain jurisdictions or product sales based on facts and circumstances related to the opportunities.

Competition

We compete with companies that develop, manufacture and sell traffic management devices using video and radar sensing technologies as well as other above‑ground detection technologies based on laser, infrared and acoustic sensors. For ITS applications, we also compete with providers of in‑pavement loop detectors and estimate that more than 60% of the traffic management systems currently in use in the U.S. use in‑pavement loop detectors. For competition with other above‑ground detection products, we typically compete on performance and functionality, and to a lesser extent on price. When competing against providers of loop detectors, we compete principally on ease of installation and the total cost of ownership over a multi‑year period, and to a lesser extent on functionality.

Among the companies that provide direct competition to Autoscope video worldwide are Iteris, Inc., Miovision, Wavetronix, LLC, FLIR Systems, Inc., GridSmart, Signal Group Inc. (Peek), Citilog S.A., Sensys Inc., and Smartmicro Inc. Among the companies that provide direct competition to RTMS radar worldwide are Wavetronix, LLC, Houston Radar, LLC, MS Sedco Inc., and Smartmicro Sensors GmbH. In addition, there are smaller local companies providing direct competition in specific markets throughout the world. We are aware that these and other companies will continue to develop technologies for use in traffic management applications. One or more of these technologies could in the future provide increased competition for our systems.

| 5 |

Manufacturing

Autoscope video products for sale under the Econolite license agreement are manufactured through agreements with Econolite. Econolite is responsible for setting warranty terms and must provide all service required under this warranty. In Europe and Asia, we engage contract manufacturers to manufacture the Autoscope family of products.

We engage E.I. Microcircuits, Inc. ("E.I. Micro") to manufacture our radar products and perform warranty and post-warranty repairs for all radar units sold.

We typically provide a two- to three-year warranty on our products.

Most of the hardware components used to manufacture our products are standard electronics components that are available from multiple sources. Although some of the components used in our products are obtained from single‑source suppliers, we believe other component vendors are available should the necessity arise. The European Parliament has enacted a directive for the restriction of the use of certain hazardous substances in electrical and electronic equipment (“RoHS”). To our knowledge, our contract manufacturing and component vendors in Europe and Asia comply with the European directive on RoHS.

Intellectual Property

To protect our rights to our proprietary know‑how, technology and other intellectual property, it is our policy to require all employees and consultants to sign confidentiality agreements that prohibit the disclosure of confidential information to any third parties. These agreements also require disclosure and assignment to us of any discoveries and inventions made by employees and consultants while they are devoted to our business activities. We also rely on trade secret, copyright and trademark laws to protect our intellectual property. We have also entered into exclusive and non‑exclusive license and confidentiality agreements relating to our own and third‑party technologies. We aggressively protect our processes, products, and strategies as proprietary trade secrets. Our efforts to protect intellectual property and avoid disputes over proprietary rights include ongoing review of third‑party patents and patent applications.

Environmental Matters

We believe our operations are in compliance with all applicable environmental regulations within the jurisdictions in which we operate.

Employees

As of December 31, 2019, we had 55 employees, consisting of 52 employees in North America and three employees in Europe. None of our employees are represented by a union.

Information Regarding Forward‑Looking Statements

This Annual Report on Form 10‑K contains forward‑looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange of 1934, as amended. Forward‑looking statements represent our expectations or beliefs concerning future events and can be identified by the use of forward‑looking words such as “believes,” “may,” “will,” “should,” “intends,” “plans,” “estimates,” or “anticipates” or other comparable terminology. Forward‑looking statements are subject to risks and uncertainties that may cause our actual results to differ materially from the results discussed in the forward‑looking statements. Some factors that might cause these differences include the factors listed below. Although we have attempted to list these factors comprehensively, we wish to caution investors that other factors may prove to be important in the future and may affect our operating results. New factors may emerge from time to time, and it is not possible to predict all of these factors, nor can we assess the effect each factor or combination of factors may have on our business.

We further caution you not to unduly rely on any forward‑looking statements because they reflect our views only as of the date the statements were made. We undertake no obligation to publicly update or revise any forward‑looking statements whether as a result of new information, future events or otherwise.

| 6 |

If governmental entities elect not to use our products due to budgetary constraints, project delays or other reasons, our revenue may fluctuate severely or be substantially diminished.

Our products are sold primarily to governmental entities. We expect that we will continue to rely substantially on revenue and royalties from sales of our systems to governmental entities. In addition to normal business risks, it often takes considerable time before governmental initiated projects are developed to the point at which a purchase of our systems would be made, and a purchase of our products also may be subject to a time‑consuming approval process. Additionally, governmental budgets and plans may change without warning. Other risks of selling to governmental entities include dependence on appropriations and administrative allocation of funds, changes in governmental procurement legislation and regulations and other policies that may reflect political developments, significant changes in contract scheduling, competitive bidding and qualification requirements, performance bond requirements, government shutdowns, intense competition for government business, and termination of purchase decisions for the convenience of the governmental entity. Substantial delays in purchase decisions by governmental entities, or governmental budgetary constraints, could cause our revenue and income to drop substantially or to fluctuate significantly between fiscal periods.

A majority of our gross profit has been generated from sales of our Autoscope family of products, and if we do not maintain the market for these products, our business will be harmed.

Historically, a majority of our gross profit has been generated from sales of, or royalties from the sales of, our Autoscope products. Gross profit from Autoscope sales accounted for approximately 74% of our gross profit in 2019 and 78% in 2018. We anticipate that gross profit from the sale of Autoscope systems will continue to account for a substantial portion of our gross profit for the foreseeable future. As such, any significant decline in sales of our Autoscope system would have a material adverse impact on our business, financial condition and results of operations.

If Econolite’s sales volume decreases or if it fails to pay royalties to us in a timely manner or at all, our financial results will suffer.

We have agreements with Econolite under which Econolite is the exclusive distributor of the Autoscope video system in the United States, Mexico, Canada and the Caribbean. Our current agreements grant Econolite a first refusal right that arises when we make a proposal to Econolite to extend the license to additional products in the United States, Mexico, Canada and the Caribbean. In addition, the agreements grant Econolite a first negotiation right that arises when we make a proposal to Econolite to include rights corresponding to Econolite’s rights under our current agreements in countries not in these territories. In exchange for its rights under the agreements, Econolite pays us royalties for sales of the Autoscope video system. Since 2002, a substantial portion of our revenue has consisted of royalties resulting from sales made by Econolite, including 56% in 2019 and 61% in 2018. Econolite’s account receivable represented 59% of our accounts receivable at December 31, 2019 and 42% of our accounts receivable at December 31, 2018. We expect that Econolite will continue to account for a significant portion of our revenue for the foreseeable future. Any decrease in Econolite’s sales volume could significantly reduce our royalty revenue and adversely impact earnings. A failure by Econolite to make royalty payments to us in a timely manner or at all will harm our financial condition. In addition, we believe sales of our products are a material part of Econolite’s business, and any significant decrease in Econolite’s sales of the other products it sells could harm Econolite, which could have a material adverse effect on our business and prospects.

As a result of our continuing review of our business, we may have to undertake further restructuring plans that would require additional charges, including incurring facility exit and restructuring charges.

We continue to evaluate our business, which may result in restructuring activities. We may choose to divest certain business operations based on management's assessment of their strategic value to our business, consolidate or close certain facilities or outsource certain functions. Decisions to eliminate or limit certain business operations in the future could involve the expenditure of capital, consumption of management resources, realization of losses, transition and wind-up expenses, reduction in workforce, impairment of assets, facility consolidation and the elimination of revenues along with associated costs, any of which could cause our operating results to decline and may fail to yield the expected benefits. For more information regarding our restructuring and divestiture activities in 2019 and 2018, see the discussion in Note 13 of our Notes to Consolidated Financial Statements included elsewhere in this Annual Report on Form 10-K.

The features and functions in our products have not been as widely utilized as traditional products offered by our competitors, and the failure of our end users to accept the features and functions in our products could adversely affect our business and growth prospects.

Video and radar technologies have not been utilized in the traffic management industry as extensively as other more traditional technologies, mainly in‑pavement loop detectors. Our financial success and growth prospects depend on the continued development of the market for advanced technology solutions for traffic detection and management and the acceptance of our current Autoscope video and RTMS radar systems and also future systems we may develop as reliable, cost‑effective alternatives to traditional vehicle detection systems. We cannot assure you that we will be able to utilize our technology profitably in other products or markets. If our end users do not continue to increase their acceptance of the features and functions provided by our current systems or other systems we may develop in the future, our business and growth prospects could be adversely affected.

| 7 |

Our operating costs tend to be fixed, while our revenue tends to be seasonal, thereby resulting in operating results that fluctuate from quarter to quarter.

Our expense levels are based in part on our product development efforts and our expectations regarding future revenues and, in the short‑term, are generally fixed. Our quarterly revenues, however, have varied significantly in the past, with our first quarter historically being the weakest due to weather conditions in parts of North America, Europe and Asia that make roadway construction more difficult. Additionally, our international revenues have a significant large project component, resulting in a varying revenue stream. We expect the seasonality of our revenue and the fixed nature of our operating costs to continue in the foreseeable future. Therefore, we may be unable to adjust our spending in a timely manner to compensate for any unexpected revenue shortfall. As a result, if anticipated revenues in any quarter do not occur or are delayed, our operating results for the quarter would be disproportionately affected. Operating results also may fluctuate due to factors such as the demand for our products; product life cycle; the development, introduction and acceptance of new products and product enhancements by us or our competitors; changes in the mix of distribution channels through which our products are offered; changes in the level of operating expenses; end user order deferrals in anticipation of new products; competitive conditions in the industry; and economic conditions generally. No assurance can be given that we will be able to achieve or maintain profitability on a quarterly or annual basis in the future.

Increased competition may make it difficult for us to acquire and retain end users. If we are unsuccessful in developing new applications and product enhancements, our products may become noncompetitive or obsolete.

Competition in ITS is continuing to grow. Some of the companies that may compete with us in the business of developing and implementing traffic control, related security systems and connected vehicles have substantially more financial, technological, marketing, personnel and research and development resources than we have. Therefore, they may be able to respond more quickly than we can to new or changing opportunities, technologies, standards or end user requirements. If we are unable to compete successfully with these companies, the market share for our products will decrease, and competitive pressures may seriously harm our business.

Additionally, the market for vehicle detection is continuously seeking more advanced technological solutions to problems. Technologies such as embedded loop detectors, pressure plates, pneumatic tubes, radars, lasers, magnetometers, acoustics and microwaves that have been used as traffic sensing devices in the past are being enhanced for use in the traffic management industry, and new technologies may be developed. We are aware of several companies that are developing traffic management devices using machine vision technology or other advanced technology. Floating vehicle and/or radio frequency identification (RFID) tagged license plate initiatives are under consideration and may be implemented. We expect to face increasingly competitive product developments, applications and enhancements. New technologies or applications in traffic control systems from other companies or the development of new and emerging technologies and applications, including vehicle-to-vehicle (V2V) communications, mobile applications, and new algorithms or sensor technologies, may provide our end users with alternatives to our products and could render our solutions noncompetitive or obsolete. If we are unable to increase the number of our applications and develop and commercialize product enhancements and applications in a timely and cost-effective manner that respond to changing technology and satisfy the needs of our end users, our business and financial results will suffer.

We may not achieve our growth plans for the expansion of our business.

In addition to market penetration, our long‑term success depends on our ability to expand our business through new product development, mergers and acquisitions, and/or geographic expansion.

New product development would require that we maintain our ability to improve existing products, continue to bring innovative products to market in a timely fashion, and adapt products to the needs and standards of current and potential customers. Our products and services may become less competitive or eclipsed by technologies to which we do not have access or which render our solutions obsolete.

Geographic expansion would be primarily outside of the U.S. and hence will be disproportionately subject to the risks of international operations discussed in this Annual Report on Form 10-K.

Mergers and acquisitions would be accompanied by risks which may include:

● difficulties identifying suitable acquisition candidates at acceptable costs;

● unavailability of capital to conduct acquisitions;

● failure to achieve the financial and strategic goals for the acquired and combined businesses;

● difficulty assimilating the operations and personnel of the acquired businesses;

● disruption of ongoing business and distraction of management from the ongoing business;

● dilution of existing shareholders and earnings per share;

● unanticipated, undisclosed or inaccurately assessed liabilities, legal risks and costs; and

● difficulties retaining our key vendors, customers or employees or those of the acquired business.

| 8 |

In addition, acquisitions of businesses having a significant presence outside the U.S. will increase our exposure to the risks of international operations discussed in this Annual Report on Form 10-K.

Our dependence on third parties for manufacturing and marketing our products may prevent us from meeting customers’ needs in a timely manner.

We do not have, and do not intend to develop in the near future, internal capabilities to manufacture our products. We have entered into agreements with Econolite to manufacture the Autoscope system, and E.I. Micro to manufacture the RTMS radar products and related products for sales in the United States, Mexico, Canada and the Caribbean. We work with suppliers, most of whom are overseas, to manufacture the rest of our products. Due to the outbreak of the coronavirus, some of our suppliers have recently expressed concern about lead times and availability of components, especially those components coming out of Asia. We are currently assessing our current inventory positions and taking actions to minimize any disruptions to our supply chain, although such actions may not be successful. There are a number of risks associated with our dependence on contract manufacturers, including reduced control over delivery schedules; reliance on the quality assurance procedures of third parties; potential uncertainty regarding manufacturing yields and costs; potential lack of adequate capacity during periods of high demand; limited warranties on components; potential misappropriation of our intellectual property; and potential manufacturing disruptions (including disruptions caused by geopolitical events, military actions, work stoppages, natural disasters or international health emergencies such as coronavirus). If Econolite, E.I. Micro, or our other suppliers are unable to manufacture our products in the future, we may be unable to identify other manufacturers able to meet product and quality demands in a timely manner or at all. Our inability to find suitable manufacturers for our products could result in delays or reductions in product shipments, which in turn may harm our business reputation and results of operations. In addition, we have granted Econolite the exclusive right to market the Autoscope video system and related products in the United States, Mexico, Canada and the Caribbean. Consequently, our revenue depends to a significant extent on Econolite’s marketing efforts. Econolite’s inability to effectively market the Autoscope video system, or the disruption or termination of that relationship, could result in reduced revenue and market share for our products.

We and our third-party manufacturers may experience difficulty obtaining materials or components for our products, or the cost of materials or components may increase, either of which may prevent us from meeting customers’ needs in a timely manner and could therefore reduce our sales.

Although substantially all of the hardware components incorporated into our products are standard electronics components that are available from multiple sources, we and our third-party manufacturers obtain some of the components from a single source. Some materials or components may become scarce or difficult to obtain in the market or they may increase in price. This could force us or our manufacturers to identify new suppliers, which could increase our costs, affect the quality of materials, reduce our sales and profitability, or harm our customer relations by delaying product deliveries due to increased lead times, any of which could harm our business. For example, the recent coronavirus may cause a disruption of the global supply chain for certain components necessary for our products, and it is unknown the magnitude of or how long any such impact may continue.

Regulations related to the use of conflict‑free minerals may increase our costs and cause us to incur additional expenses.

The Dodd‑Frank Wall Street Reform and Consumer Protection Act contains provisions to improve the transparency and accountability of the use by public companies in their products of minerals mined in certain countries and to prevent the sourcing of such “conflict” minerals. As a result, the Securities and Exchange Commission enacted annual disclosure and reporting requirements for public companies who use these minerals in their products, which apply to us. Under the final rules, we are required to conduct due diligence to determine the source of any conflict minerals used in our products. Although we expect to file the required report on a timely basis, our supply chain is broad‑based and complex, and we may not be able to easily verify the origins for all minerals used in our products. To the extent that any information furnished to us by our suppliers is inaccurate or inadequate, we could face reputational and enforcement risks. In addition, the conflict mineral rules could reduce the number of suppliers who provide components and products containing conflict‑free minerals and thus could disrupt our supply chain or that of our manufacturers and increase the cost of the components used in manufacturing our products and the costs of our products to us. Any increased costs and expenses could have a material adverse impact on our financial condition and results of operations.

Some of our products are covered by our warranties and, if the cost of fulfilling these warranties exceeds our warranty allowance, it could adversely affect our financial condition and results of operations.

Unanticipated warranty and other costs for defective products could adversely affect our financial condition and results of operations and our reputation. We generally provide a two- to three-year warranty on our product sales. These warranties require us to repair or replace faulty products, among other customary warranty provisions. Although we monitor our warranty claims and provide an allowance for estimated warranty costs, unanticipated claims in excess of the allowance could have a material adverse impact on our financial condition and results of operations. Additionally, we rely on our third-party manufacturers to fulfill our warranty repair obligations to our customers. Adverse changes in these parties’ abilities to perform these repairs could cause a delay in repairs or require us to source other parties to perform the repairs and could adversely affect impact our financial condition and results of operations. In addition, the need to repair or replace products with design or manufacturing defects could adversely affect our reputation.

| 9 |

We may face increased competition if we fail to adequately protect our intellectual property rights, and any efforts to protect our intellectual property rights may result in costly litigation.

Our success depends in large measure on the protection of our proprietary technology rights. We rely on trade secret, copyright and trademark laws, confidentiality agreements with employees and third parties, and patents, all of which offer only limited protection. We cannot assure you that the scope of these protective measures will exclude competitors or provide competitive advantages to us. We also cannot assure you that we will become aware of all instances in which others develop similar products, duplicate any of our products, or reverse engineer or misappropriate our proprietary technology. If our proprietary technology is misappropriated, our business and financial results could be adversely affected. Litigation may be necessary in the future to enforce our intellectual property rights, to protect our trade secrets or to determine the validity and scope of the proprietary rights of others. In addition, we may be the subject of lawsuits by others who claim we violate their intellectual property rights.

Intellectual property litigation is very costly and could result in substantial expense and diversions of our resources, either of which could adversely affect our business and financial condition and results of operations. In addition, there may be no effective legal recourse against infringement of our intellectual property by third parties, whether due to limitations on enforcement of rights in foreign jurisdictions or as a result of other factors.

We have not applied for patent protection in all countries in which we market and sell our products. Consequently, our proprietary rights in the technology underlying our systems in countries other than the U.S. will be protected only to the extent that trade secret, copyright or other non‑patent protection is available and to the extent we are able to enforce our rights. The laws of other countries in which we market our products may afford little or no effective protection of our proprietary technology, which could harm our business.

We plan to continue introducing new products and technologies and may not realize the degree or timing of benefits we initially anticipated, which could adversely affect our business and results of operations.

We regularly invest substantial amounts in research and development efforts that pursue advancements in a range of technologies, products and services. Our ability to realize the anticipated benefits of these advancements depends on a variety of factors, including meeting development, production, certification and regulatory approval schedules; the execution of internal and external performance plans; the availability of supplier‑produced parts and materials; the performance of suppliers and vendors; achieving cost efficiencies; the validation of innovative technologies; and the level of end user interest in new technologies and products. These factors involve significant risks and uncertainties. We may encounter difficulties in developing and producing these new products and may not realize the degree or timing of benefits initially anticipated. In particular, we cannot predict with certainty whether, when or in what quantities our current or potential end users will have a demand for products currently in development or pending release. Moreover, as new products are announced, sales of current products may decrease as end users delay making purchases until such new products are available. Any of the foregoing could adversely affect our business and results of operations.

Our business could be adversely affected by product liability and commercial litigation.

Our products or services may be claimed to cause or contribute to personal injury or property damage to our customers’ employees or facilities. Additionally, we are, at times, involved in commercial disputes with third parties, such as customers, distributors, vendors and others. See Item 3 and Note 15 of our Notes to Consolidated Financial Statements included elsewhere in this Annual Report on Form 10-K. The ensuing claims may arise singularly, in groups of related claims, or in class actions involving multiple claimants. Such claims and litigation are frequently expensive and time‑consuming to resolve and may result in substantial liability to us, which liability and related costs and expenses may not be recoverable through insurance or any other forms of reimbursement.

Our business could be affected by various legal and regulatory compliance risks, including those involving antitrust, environmental, anti-bribery or anti-corruption laws and regulations.

We are subject to various legal and regulatory requirements and risks in the U.S. and other countries in which we have facilities or sell our products involving compliance with antitrust, environmental, anti-bribery and anti-corruption laws and regulations, including the U.S. Foreign Corrupt Practices Act and the U.K. Anti-Bribery Act. Although we have internal policies and procedures with the intention of assuring compliance with these laws and regulations, our employees, contractors, agents and licensees involved in our international sales may take actions in violation of such policies. Any future adverse development, ruling or settlement could result in charges that could have an adverse effect on our results of operations or cash flows.

We price a segment of our product portfolio at a premium compared to other technologies. As such, we may not be able to quickly respond to emerging low‑cost competitors, and our inability to do so could adversely affect revenue and profitability.

We price a segment of our product portfolio at a premium as compared to products using less sophisticated technologies. As the technological sophistication of our competitors and the size of the market increase, competing low‑cost developers of machine vision products for traffic are likely to emerge and grow stronger. If end users prefer low‑cost alternatives over our products, our revenue and profitability could be adversely affected.

| 10 |

Our revenue could be adversely affected by the emergence of local competitors and local biases in international markets.

Our experience indicates that local officials that purchase traffic management products in the international markets we serve favor products that are developed and manufactured locally. As local competitors to our products emerge, local biases could erode our revenue in Europe and Asia and adversely affect our sales and revenue in those markets.

We sell our products internationally and are subject to various risks relating to such international activities, which could harm our international sales and profitability.

Sales outside of the United States, including export sales from our U.S. business locations, accounted for approximately 25% of our total revenue in 2019 and 20% of our total revenue in 2018. By doing business in international markets, we are exposed to risks separate and distinct from those we face in our U.S. operations. Our international business may be adversely affected by changing political and economic conditions in foreign countries. Additionally, fluctuations in currency exchange rates could affect demand for our products or otherwise negatively affect profitability. Engaging in international business inherently involves a number of other difficulties and risks, including:

• export restrictions and controls relating to technology;

• pricing pressure that we may experience internationally;

• exposure to the risk of currency value fluctuations where payment for products is denominated in a currency other than U.S. dollars;

• variability in the U.S. dollar value of foreign currency‑denominated assets, earnings and cash flows;

• required compliance with existing and new foreign regulatory requirements and laws;

• laws and business practices favoring local companies;

• longer payment cycles;

• difficulty of enforcing agreements, including patent and trademarks, and collecting receivables through foreign legal systems;

• disputes with parties outside of the U.S., which may be more difficult, expensive and time-consuming to resolve than disputes with parties located in the U.S.;

• political and economic instability, including volatility in the economic environment of the European Union caused by the ongoing sovereign debt crisis in Europe;

• tax rates in certain foreign countries that exceed those in the U.S. and the imposition of withholding requirements on foreign earnings;

• higher danger of terrorist activity, war or civil unrest compared to domestic operations;

• disruptions to our global supply chain, including disruptions caused by geopolitical events, military actions, work stoppages, natural disasters, or international health emergencies, such as the coronavirus;

• difficulties and costs of staffing and managing foreign operations; and

• difficulties in enforcing intellectual property rights.

| 11 |

Our exposure to each of these risks may increase our costs, lengthen our sales cycle and require significant management attention. One or more of these factors may harm our business.

The United Kingdom’s withdrawal from the European Union could harm our business and financial results.

On January 31, 2020, the United Kingdom officially withdrew from the European Union (commonly referred to as "Brexit"), subject to a transition period until December 21, 2020, which could be extended up to two years under certain conditions. There is uncertainty as to the scope, nature, and terms of the relationship between the United Kingdom and the European Union after this Brexit transition period. This uncertainty could adversely impact customer or investor confidence, result in additional market volatility, legal uncertainty, and divergent national laws and regulations. In addition, the consequences for the economies of the European Union members and of the United Kingdom exiting the European Union are unknown and unpredictable. Depending on the final terms of Brexit, we could face new regulatory costs and challenges and greater volatility in the Pound Sterling and the euro. Any adjustments we make to our business and operations because of Brexit could result in significant time and expense to complete. Any of the foregoing factors could have a material adverse effect on our business, results of operations or financial condition.

Changes in U.S. trade policies may adversely impact our business and financial results.

The Company’s operations and performance depend significantly on global, regional and U.S. economic and geopolitical conditions. In recent years, there have been significant changes to U.S. trade policies, legislation, treaties and tariffs, as well as trade policies and tariffs affecting China. These and any other changes to current policies by the U.S. government could affect our business, including potentially through increased import tariffs and other influences on U.S. trade relations with China and other countries. The imposition of tariffs or other trade barriers could increase our costs in certain markets and may cause our customers to find alternative sourcing. In addition, other countries may change their own policies on business and foreign investment in companies in their respective countries. Additionally, it is possible that U.S. policy changes and uncertainty about such changes could increase market volatility and currency exchange rate fluctuations. Market volatility and currency exchange rate fluctuations could have a material adverse effect on our business, financial condition, results of operations or cash flows.

Our inability to comply with European and Asian regulatory restrictions over hazardous substances and electronic waste could restrict product sales in those markets and reduce profitability in the future.

The European Union’s Waste Electrical and Electronic Equipment (“WEEE”) directive makes producers of electrical goods financially responsible for specified collection, recycling, treatment and disposal of past and future covered products. This directive must be enacted and implemented by individual European Union governments, and certain producers will be financially responsible under the WEEE legislation. This may impose requirements on us, which, if we are unable to meet them, could adversely affect our ability to market our products in European Union countries, and our sales revenues and profitability would suffer as a consequence. In addition, the European Parliament has enacted a directive for the restriction of the use of certain hazardous substances in electrical and electronic equipment. This RoHS legislation restricts the use of substances such as mercury, lead, cadmium and hexavalent cadmium. If we are unable to have our products manufactured in compliance with the RoHS directive, we would be unable to market our products in European Union countries, and our revenues and profitability would suffer. In addition, various Asian governments could adopt their own versions of environment‑friendly electronic regulations similar to the European directives, RoHS and WEEE. This could require new and unanticipated manufacturing changes, product testing and certification requirements, thereby increasing cost, delaying sales and lowering revenue and profitability.

Our inability to manage growth effectively could seriously harm our business.

Growth and expansion of our business could significantly strain our capital resources as well as the time and abilities of our management personnel. Our ability to manage growth effectively will require continued improvement of our operational, financial and management systems and the successful training, motivation and management of our employees. If we are unable to manage growth successfully, our business and operating results will suffer.

| 12 |

Our business operations will be severely disrupted if we lose key personnel or if we fail to attract and retain qualified personnel.

Our technology depends upon the knowledge, experience and skills of our key management and scientific and technical personnel. Additionally, our ability to continue technological developments and to market our products, and thereby develop a competitive edge in the marketplace, depends in large part on our ability to attract and retain qualified scientific and technical personnel. Competition for qualified personnel is intense, and we cannot assure you that we will be able to attract and retain the individuals we need, especially if our business expands and requires us to employ additional personnel. In addition, the loss of personnel or our failure to hire additional personnel could materially and adversely affect our business, operating results and ability to expand. The loss of key personnel, or our inability to hire and retain qualified personnel, would harm our business.

We may not be successful in integrating any acquired companies into our business, which could materially and adversely affect our financial condition and operating results.

Part of our business strategy has been to acquire or invest in companies, products or technologies that complement our current products, enhance our market coverage or technical capabilities or offer growth opportunities. For any acquisition, a significant amount of management’s time and financial resources may be required to complete the acquisition and integrate the acquired business into our existing operations. Even with this investment of management time and financial resources, an acquisition may not produce the revenue, earnings or business synergies anticipated. Acquisitions involve numerous other risks, including the assumption of unanticipated operating problems or legal liabilities; problems integrating the purchased operations, technologies or products; the diversion of management’s attention from our core businesses; restrictions on the manner in which we may use purchased companies or assets imposed by acquisition agreements; adverse effects on existing business relationships with suppliers and customers; incorrect estimates made in the accounting for acquisitions and amortization of acquired intangible assets that would reduce future reported earnings (such as goodwill impairments); ensuring acquired companies’ compliance with the requirements of the U.S. federal securities laws and accounting rules; and the potential loss of customers or key employees of acquired businesses. We cannot assure you that any acquisitions, investments, strategic alliances or joint ventures will be completed or integrated in a timely manner or achieve anticipated synergies, will be structured or financed in a way that will enhance our business or creditworthiness, or will meet our strategic objectives or otherwise be successful.

We may be required to recognize impairment charges for long‑lived assets.

As of December 31, 2019, the net carrying value of our long‑lived assets (property and equipment, deferred tax assets and other intangible assets) totaled approximately $9.7 million. In accordance with U.S. generally accepted accounting principles (GAAP), we periodically assess these assets to determine if they are impaired. Significant negative industry or economic trends, a significant and sustained decline in our stock price, disruptions to our businesses, significant unexpected or planned changes in our use of assets, divestitures and market capitalization declines may result in impairments to our goodwill and other long‑lived assets. Future impairment charges could significantly affect our results of operations in the periods recognized.

Our stock is thinly traded and our stock price is volatile.

Our common stock is thinly traded, with 3,888,654 shares of our 5,322,849 outstanding shares held by non‑affiliates as of February 29, 2020. Based on the trading history of our common stock and the nature of the market for publicly traded securities of companies in evolving high‑tech industries, we believe there are several factors that have caused and are likely to continue to cause the market price of our common stock to fluctuate substantially. The fluctuations may occur on a day‑to‑day basis or over a longer period of time. Factors that may cause fluctuations in our stock price include announcements of large orders obtained by us or our competitors, substantial cutbacks in government funding of highway projects or of the potential availability of alternative technologies for use in traffic control and safety, quarterly fluctuations in our financial results or the financial results of our competitors, consolidation among our competitors, fluctuations in stock market prices and volumes, and the volatility of the stock market.

Rising interest rates may affect our ability to obtain financing and may cause us to suffer competitive disadvantages.

The Company’s exposure to changes in interest rates relates primarily to the Company’s ability to obtain financing in the future. If obtaining financing is adversely affected by rising interest rates or other factors, it could make it more difficult or expensive for us to obtain financing, which in turn would adversely affect our ability to take advantage of significant business opportunities and to react to changes in market or industry conditions.

| 13 |

The transition away from LIBOR may adversely affect our cost to obtain financing.

Central banks around the world, including the Board of Governors of the Federal Reserve, have commissioned working groups of market participants and official sector representatives with the goal of finding suitable replacements for the London Interbank Offered Rate (“LIBOR”) based on observable market transactions. It is expected that a transition away from the widespread use of LIBOR to alternative rates will occur over the course of the next few years. The U.K. Financial Conduct Authority (FCA), which regulates LIBOR, has announced that it has commitments from panel banks to continue to contribute to LIBOR through the end of 2021, but that it will not use its powers to compel contributions beyond such date. Accordingly, there is considerable uncertainty regarding the publication of such rates beyond 2021. The Federal Reserve Bank of New York and various other authorities have commenced the publication of reforms and actions relating to alternatives to U.S. dollar LIBOR. Although the full impact of such reforms and actions, together with any transition away from LIBOR, including the potential or actual discontinuance of LIBOR publication, remains unclear, these changes may have a material adverse impact on the availability of financing, including LIBOR-based loans, and on our financing costs.

Difficult and volatile conditions in the capital, credit and commodities markets and in the overall economy could continue to adversely affect our financial position, results of operations and cash flows, and we do not know if these conditions will improve in the near future.

Our financial position, results of operations and cash flows could continue to be adversely affected by difficult conditions and significant volatility in the capital, credit and commodities markets and in the overall worldwide economy. Although certain economic conditions in the United States have improved, economic growth has been slow and uneven and may not be sustained. During economic downturns, governmental entities in particular, which constitute most of our end users, reduce or delay their purchase of our products, which has had and may continue to have an adverse effect on our business. Any uncertainty about the federal budget in the U.S. could have a negative effect on the U.S. and global economy. The continuing impact that these factors might have on us and our business is uncertain and cannot be estimated at this time. Current economic conditions, including the recent volatility in the stock market caused by the outbreak of the coronavirus, have accentuated each of these risks and magnified their potential effect on us and our business. The difficult conditions in these markets and the overall economy affect our business in a number of ways. For example:

| • | Although we believe we have sufficient liquidity to run our business, under extreme market conditions, there can be no assurance that financing, if needed, would be available or sufficient, and, in such a case, we may not be able to successfully obtain financing on favorable terms, or at all. | |

| • |

Continuing market volatility has exerted downward pressure on our stock price, which could make it more difficult or unfavorable for us to raise additional capital in the future. | |

| • |

Economic conditions could result in customers in our markets continuing to experience financial difficulties, including limited liquidity and their inability to obtain financing or electing to limit spending because of the economy which may result, for example, in customers’ inability to pay us at all or on a timely basis and in declining tax revenue for our customers that are governmental entities, which in turn could result in decreased sales and earnings for us. |

We do not know if market conditions or the state of the overall economy will improve in the near future, when improvement will occur or if any improvement will benefit our market segment.

Our articles of incorporation and bylaws, Minnesota law and our shareholder rights plan may inhibit a takeover that shareholders consider favorable.Provisions of our articles of incorporation and bylaws and applicable provisions of Minnesota law may delay or discourage transactions involving an actual or potential change in our control or change in our management, including transactions in which shareholders might otherwise receive a premium for their shares or transactions that our shareholders might otherwise deem to be in their best interests. These provisions:

| • | permit our board of directors to issue up to 5,000,000 shares of preferred stock with any rights, preferences and privileges as it may designate, including the right to approve an acquisition or other change in our control; | |

| • |

provide that the authorized number of directors may be increased by resolution of the board of directors; | |

| • |

provide that all vacancies, including newly‑created directorships, may, except as otherwise required by law, be filled by the affirmative vote of a majority of directors then in office, even if less than a quorum; and | |

| • | eliminate cumulative voting rights, therefore allowing the holders of a majority of the shares of common stock entitled to vote in any election of directors to elect all of the directors standing for election, if they should so choose. |

| 14 |

Section 302A.671 of the Minnesota Business Corporation Act (“MBCA”) generally limits the voting rights of a shareholder acquiring a substantial percentage of our voting shares in an attempted takeover or otherwise becoming a substantial shareholder of our company unless holders of a majority of the voting power of all outstanding shares and the disinterested shares approve full voting rights for the substantial shareholder. Section 302A.673 of the MBCA generally limits our ability to engage in any business combination with certain persons who own 10% or more of our outstanding voting stock or any of our associates or affiliates who at any time in the past four years have owned 10% or more of our outstanding voting stock. These provisions of the MBCA may have the effect of entrenching our management team and may deprive shareholders of the opportunity to sell their shares to potential acquirers at a premium over prevailing market prices. This potential inability to obtain a control premium could reduce the price of our common stock.

In addition, in June 2013, we adopted a shareholder rights plan and declared a dividend to our shareholders of one preferred share purchase right for each outstanding share of common stock. In August 2016, our Board of Directors amended the shareholder rights plan to preserve the value of certain deferred tax benefits to the Company, including those generated by net operating losses. Generally, the shareholder rights plan, as amended, provides that if a person or group acquires 4.99% or more of our outstanding shares of common stock, subject to certain exceptions and under certain circumstances, the rights may be exchanged by us for common stock or the holders of the rights, other than the acquiring person or group, could acquire additional shares of our capital stock at a discount of the then current market price. Such exchanges or exercise of rights could cause substantial dilution to a particular acquirer and discourage the acquirer from pursuing the Company. The mere existence of a shareholder rights plan often delays or makes a merger, tender offer or other acquisition more difficult to complete. In March 2018, our Board of Directors recommended amending the shareholder rights plan to extending the term of the shareholder rights plan from June 6, 2018 to June 5, 2020, subject to shareholder approval, to continue to preserve the value of certain deferred tax assets. Our shareholders approved the amendment at the Company's annual meeting of shareholders held in May 2018.

We can issue shares of preferred stock without shareholder approval, which could adversely affect the rights of common shareholders.