UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

______________________________________________________

FORM 10-K

______________________________________________________

(check one)

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the fiscal year ended June 30 , 2021

OR

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |||||

For the transition period from __________ to __________

Commission File No. 1-367

______________________________________________________

THE L.S. STARRETT COMPANY

(Exact name of registrant as specified in its charter)

______________________________________________________

(State or other jurisdiction of

incorporation or organization)

(Address of principal executive offices)

(I.R.S. Employer

Identification No.)

(Zip Code)

Registrant’s telephone number, including area code 978 -249-3551

______________________________________________________

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

| Class B Common - $1.00 Per Share Par Value | Not applicable | Not applicable | ||||||||||||

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports) and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer”, “smaller reporting company”, and “emerging growth company” in Rule 12b-2 of the Exchange Act. (Check one)

Large Accelerated Filer ☐ Accelerated Filer ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Act). Yes ☐ No ☒

The Registrant had 6,448,814 and 655,854 shares, respectively, of its $1.00 par value Class A and B common stock outstanding on December 31, 2020. On December 31, 2020, the last business day of the Registrant’s second fiscal quarter, the aggregate market value of the common stock held by non-affiliates was approximately $26,731,773 .

There were 6,484,295 and 623,457 shares, respectively, of the Registrant’s $1.00 par value Class A and Class B common stock outstanding as of August 13, 2021.

The exhibit index is located on pages 65-67.

DOCUMENTS INCORPORATED BY REFERENCE

1

THE L.S. STARRETT COMPANY

FORM 10-K

FOR THE YEAR ENDED JUNE 30, 2021

TABLE OF CONTENTS

| Page Number | ||||||||

| 65-67 | ||||||||

All references in this Annual Report to “Starrett”, the “Company”, “we”, “our” and “us” mean The L.S. Starrett Company and its subsidiaries.

2

PART I

Item 1 - Business

General

Founded in 1880 by Laroy S. Starrett and incorporated in 1929, The L.S. Starrett Company (the “Company”) is engaged in the business of manufacturing over 5,000 different products for industrial, professional and consumer markets. The Company has a long history of global manufacturing experience and currently operates three major global manufacturing plants. The global manufacturing plants consist of the one domestic location in Athol, Massachusetts (1880) and the international operations located in Itu, Brazil (1956), and Suzhou, China (1997). The Company consolidated Jedburgh; Scotland and Mt. Airy, NC saw manufacturing operations into Brazil in fiscal year 2021. This strategic restructuring continues to improve manufacturing utilization and creates a global scale saw business. All subsidiaries principally serve the global manufacturing industrial base with concentration in the metalworking, construction, machinery, equipment, aerospace and automotive markets.

The Company offers its broad array of measuring and cutting products to the market through multiple channels of distribution throughout the world. The Company’s products include precision tools, electronic gages, gage blocks, optical, vision, laser measuring equipment, custom engineered granite solutions, tape measures, levels, chalk products, squares, band saw blades, hole saws, hacksaw blades, jig saw blades, reciprocating saw blades, M1® lubricant and precision ground flat stock. The Company primarily distributes its precision hand tools, saw and construction products through distributors or resellers both domestically and internationally. Starrett® is brand recognized around the world for precision, quality and innovation.

In accordance with the provisions of Financial Accounting Standards Board (FASB) Accounting Standards Codification (ASC) 280, Segment Reporting, for the fiscal year ended June 30, 2021 (fiscal 2021), we determined that we have two reportable operating segments (North America and International). Refer to Note 17, Financial Information by Segment & Geographical Area, contained in the Notes to Consolidated Financial Statements included in Part II, Item 8 of this Annual Report on Form 10-K, for more information on our reportable segments.

Products

The Company’s tools and instruments are sold throughout North America and in over 100 other countries. The largest consumer of these products is the manufacturing industry including metalworking, aerospace, medical, oil and gas, government and automotive. Other important consumers are marine and farm equipment shops, do-it-yourselfers and tradesmen such as builders, carpenters, plumbers and electricians.

For over 140 years, the Company has been a recognized leader in providing measurement and cutting solutions to industry. Measurement tools consist of precision instruments such as micrometers, vernier calipers, height gages, depth gages, electronic gages, dial indicators, steel rules, combination squares, custom, non-contact gaging such as vision, optical and laser measurement systems. The Company believes advanced, non-contact systems with easy-to use software will be attractive to industry to reduce measurement and inspection time and are ideal for quality assurance, inspection labs, manufacturing and research facilities. Skilled personnel, superior products, manufacturing expertise, innovation and unmatched service has earned the Company its reputation as the “Best in Class” provider of measuring application solutions for industry.

Notwithstanding the pandemic the Company introduced approximately 200 new Electronic Precision Measuring Tools and a new Wireless Data collection instruments this fiscal year. This investment was to support the Company’s strategic intent to provide measurement applications compatible with Industry 4.0. This major upgrade to ninety-five percent of the electronic micrometer offerings provided new features such as water & dust resistance, larger LCD displays, longer battery life, more tactile button feel, ergonomic frame design for comfort of use and wireless connectivity. This investments converted popular legacy mechanical measuring tools to electronic digital displays that broadened Starrett’s Industry 4.0 measuring tool portfolio.

In addition, The Company introduced DataSure 4.0 Wireless Data Collecting System. This system is used to collect and transmit measured data for production and quality control areas. This system operates on the latest wireless networking technology that uses short-wave radio frequencies providing unprecedented range and data security which includes multi-layer encryption protection. These new wireless tools allow data to be sent with the push of a button, are water and dust resistance, and include rechargeable batteries.

As one of the premier industrial brands, the Company continues to be focused on every touch point with its customers. To that end, the Company now offers modern, easy-to-use interfaces for distributors and end-users including interactive catalogs and several online applications.

3

The Company’s saw and hand tool product lines enjoy strong global brand recognition and market share. These products encompass a breadth of uses. The Company introduced several new products in the recent past including a new line of hand tools for measuring, marking and layout that include tapes, levels, chalk lines and other products for the building trades. The Company also introduced new products to its hand tool portfolio to extend its reach into the construction and retail trades. The continued focus on high performance, production band saw applications has resulted in the development of two new ADVANZ carbide tipped products MC5 and MC7 ideal for cutting ferrous materials (MC7) and non-ferrous metals and castings (MC5). These actions are aimed at positioning the Company for global growth in wide band products for production applications.

Over the last few years, the Company has launched new products, such as abrasive cut-off wheels and butcher knives, in order to become more product diverse and to invest in new distribution channels and industries such as the food industry. The Company was able to move into this channel with, in addition to meat and fish cutting blades, a variety of products such as butter knives, skinner and slicer blades, bandsaw machines and related products. The Company has also invested in new channels taking its traditional products such as Bi-metal bandsaws and its Power Tool Accessories product lines into welding and e-Commerce channels.

Personnel

At June 30, 2021, the Company had 1,436 employees, with approximately 50% in North America and 50% in International operations. This represents a net decrease from June 30, 2020 of 49 employees, consistent with the restructuring plan. The headcount change included an decrease of 11 in North American operations and a decrease of 38 internationally.

The Company's Brazilian operation has a form of collective bargaining among the workers trade union and the manufacturers association that is organized in Brazil by industrial sectors. Brazil has approximately 300 direct labor and another 100 in selling, general and administration. In general, the Company considers relations with its employees to be excellent. Domestic employees hold shares of Company stock resulting from various stock purchase plans and employee stock ownership plans. The Company believes that this dual role of owner-employee has strengthened employee morale over the years.

Competition

The Company competes on the basis of its reputation as the best in class for quality, precision and innovation combined with its commitment to customer service and strong customer relationships. To that end, Starrett is increasingly focusing on providing customer centric solutions. Although the Company is generally operating in highly competitive markets, the Company’s competitive position cannot be determined accurately in the aggregate or by specific market since none of its competitors offer all of the same product lines offered by the Company or serve all of the markets served by the Company.

The Company is one of the largest producers of mechanics’ hand measuring tools and precision instruments. In the United States, there are three major foreign competitors and numerous small companies in the field. As a result, the industry is highly competitive. During fiscal 2021, there were no material changes in the Company’s competitive position. The Company’s products for the building trades, such as tape measures and levels, are under constant margin pressure due to a channel shift to large national home and hardware retailers. The Company has responded to such challenges by expanding its manufacturing operations in China. Certain large customers also offer their own private labels “own brand” that compete with Starrett branded products. These products are often sourced directly from low cost countries.

Saw products encounter competition from several domestic and international sources. The Company’s competitive position varies by market and country. Continued research and development, new patented products and processes, strategic acquisitions and investments and strong customer support have enabled the Company to compete successfully in both general and performance applications.

Foreign Operations

The operations of the Company’s foreign subsidiaries are consolidated in its financial statements. The subsidiaries located in Brazil and China are actively engaged in the manufacturing and distribution of precision measuring tools, saw blades, optical and vision measuring equipment and hand tools. Subsidiaries in Scotland, Canada, Australia, New Zealand, Mexico, and Singapore are engaged in distribution of the Company’s products. The Company expects its foreign subsidiaries to continue to play a significant role in its overall operations. A summary of the Company’s foreign operations is contained in Note 17 “Financial Information by Segment & Geographic Area” to the Company’s Consolidated Financial Statements.

Orders and Backlog

4

The Company generally fills orders from finished goods inventories on hand. Sales order backlog to fulfillment for the Company is shorter than many industries. As of June 30, 2021, backlog in our U.S. Precision Tools and Saws Manufacturing “Core U.S.” business were approximately $8.5 million or $4.8 million greater than June 30, 2020. Total Company inventories amounted to $60.6 million at June 30, 2021 and $53.0 million at June 30, 2020.

Intellectual Property

When appropriate, the Company applies for patent protection on new inventions and currently owns a number of patents. Its patents are considered important in the operation of the business, but no single patent is of material importance when viewed from the standpoint of its overall business. The Company relies on its continuing product research and development efforts, with less dependence on its current patent position. The Company has, for many years, maintained engineers and supporting personnel engaged in research, product development and related activities. The expenditures for these activities during fiscal years 2021, 2020, and 2019 were approximately $3.0 million, $3.8 million, and $3.7 million, respectively.

The Company uses trademarks with respect to its products and considers its trademark portfolio to be one of its most valuable assets. All of the Company’s important trademarks are registered and rigorously enforced.

Environmental

Compliance with federal, state, local, and foreign provisions that have been enacted or adopted regulating the discharge of materials into the environment or otherwise relating to protection of the environment is not expected to have a material effect on the capital expenditures, earnings and competitive position of the Company. The Company seeks to reduce, control and treat water discharges and air emissions.

Strategic Activities

Globalization has had a profound impact on product offerings and buying behaviors of industry and consumers in North America and around the world, resulting in the Company revising its strategy to fit this highly competitive business environment. The Company continuously evaluates most aspects of its business, aiming for new ideas to set itself apart from its competition.

The Company’s strategic concentration is to continue building a global brand and providing unique customer value propositions through technically supported application solutions for our customers. The Company’s job is to recommend and produce the best suited standard product or to design and build custom solutions. The combination of the right tool for the job with value added service maintains the Company’s competitive advantage. The Company continues its focus on lean manufacturing, plant consolidations, global sourcing, new software and hardware technologies, and improved logistics to optimize its value chain.

The execution of these strategic initiatives has expanded the Company’s manufacturing and distribution in developing economies, resulting in international sales revenues totaling 49% of consolidated sales for fiscal 2021.

SEC Filings and Certifications

The Company makes its public filings with the Securities and Exchange Commission “SEC”, including its Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and all exhibits and amendments to these reports, available free of charge at its website, www.starrett.com, as soon as reasonably practicable after the Company files such material with the SEC. Information contained on the Company’s website is not part of this Annual Report on Form 10-K.

Item 1A – Risk Factors

SAFE HARBOR STATEMENT UNDER THE PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995

This Annual Report on Form 10-K and the Company’s 2021 Annual Report to Stockholders, including the President’s letter, contain forward-looking statements about the Company’s business, competition, sales, gross margins, capital expenditures, foreign operations, plans for reorganization, interest rate sensitivity, debt service, liquidity and capital resources, and other operating and capital requirements. In addition, forward-looking statements may be included in future Company documents and in oral statements by Company representatives to security analysts and investors. The Company is subject to risks that could cause actual events to vary materially from such forward-looking statements, including the following risk factors:

Risks Related to Our Company and Financial Position

5

We operate in a highly competitive environment, which could adversely affect our sales and pricing if we fail to compete effectively in the future.

We operate in a highly competitive environment. We compete on the basis of a variety of factors, including product performance, customer service, quality and price. Additionally, the Company’s products for the building trades, such as tape measures and levels, are under constant margin pressure due to a channel shift to large national home and hardware retailers. Certain large customers also offer their own private labels “own brand” that compete with Starrett branded products. There can be no assurance that our products will be able to compete successfully with other companies’ products. Thus, our share of industry sales could be reduced due to aggressive pricing or product strategies pursued by competitors, unanticipated product or manufacturing difficulties, our failure to price our products competitively or our failure to produce our products at a competitive cost. Lack of customer acceptance of price increases we announce from time to time, changes in customer requirements for price discounts, changes in our customers’ behavior or a weak pricing environment could have an adverse impact on our business, results of operations and financial condition. In addition, our results and ability to compete may be impacted negatively by changes in our geographic and product mix of sales.

Economic weakness in the industrial manufacturing sector could adversely affect the Company’s financial results.

The market for most of the Company’s products is subject to economic conditions affecting the industrial manufacturing sector, including the level of capital spending by industrial companies and the general movement of manufacturing to low cost foreign countries where the Company does not have a substantial market presence. Accordingly, economic weakness in the industrial manufacturing sector may, and in some cases has, resulted in decreased demand for certain of the Company’s products, which adversely affects sales and performance. Economic weakness in the consumer market will also adversely impact the Company’s performance. In the event that demand for any of the Company’s products declines significantly, the Company could be required to recognize certain costs as well as asset impairment charges on long-lived assets related to those products.

The (COVID-19) pandemic continues and could have a material adverse effect on our business and results of operations.

The COVID-19 pandemic has negatively impacted the global economy, disrupted consumer spending and global supply chains, and created significant volatility and disruption of financial markets. The pandemic has had a material adverse impact on our business and financial performance. The extent of the impact of the on-going pandemic on our business and financial performance, including our ability to execute our near-term and long-term business strategies and initiatives in the expected time frame, will depend on future developments, including the duration and severity of the pandemic, which are uncertain and cannot be predicted.

We continue to monitor government mandates and recommendations, and attempt to protect the health and safety of our employees, consumers and communities that has negatively impacted our business, including following state guidelines for social distancing such as, but not limited to, modifying shift schedules, supporting office-base employees working remotely, educating employees and making accommodations related to personal and workplace hygiene, mandating the wearing of masks, daily monitoring of employee’s temperature and regularly communicating accordingly. To immediately address the immediate financial crisis management implemented plans globally in an effort to control variable cost and to preserve cash. These actions included, but are not limited to, wage and salary reductions, furloughs, reduced work weeks and layoffs.

Adverse global economic conditions and world events could affect our operating results, industry and business.

The Company’s results of operations have been and may continue to be materially affected by the conditions in the global economy. The demand for our products and services has in the past and continues to be significantly reduced in periods of economic weakness characterized by lower levels of government and business investment, lower levels of business confidence, lower corporate earnings, high real interest rates, lower credit activity or tighter credit conditions, perceived or actual industry overcapacity, higher unemployment and lower consumer spending. Economic conditions vary across regions and countries, and demand for our products and services generally increases in those regions and countries experiencing economic growth and investment. Slower economic growth or a change in the global mix of regions and countries experiencing economic growth and investment could have an adverse effect on our business, results of operations and financial condition.

Sustained increases in funding obligations under the pension plans may impair our liquidity or financial condition.

The Company maintains certain defined benefit pension plans in both the United States and the United Kingdom for the benefit of its employees. Defined benefit pension plans impose certain funding obligations on the Company. The Company froze the domestic defined benefit pension plan as of December 31, 2016, and therefore no future benefits will accrue to employees under that plan. Additionally, the Company limited eligibility under the postretirement benefit plan as of December 31, 2013,

6

reducing the liability for the plan. Nevertheless, the Company expects to be required to provide more funding to the domestic pension (and postretirement) plan in the future.

The Company’s U.S. defined benefit pension plan is underfunded primarily due to lower discount rates which increase the Company’s liability. The Company made contributions of $6.9 million in fiscal 2021, and $6.8 million in fiscal 2020 and will be required to make additional contributions in fiscal 2022 of $6.0 million for the U.S. defined benefit pension plan. The Company’s United Kingdom pension plan, which is also underfunded, required Company contributions of $1.0 million and $0.9 million during fiscal 2021 and 2020, respectively. The Company expects to make a $1.0 million contribution to its United Kingdom pension plan in fiscal 2022.

In determining our future payment obligations under the plans, we assume certain rates of return on the plan assets and a certain level of future benefit payments. Significant adverse changes in credit or capital markets could result in actual rates of return being materially lower than projected and result in increased contribution requirements. Our assumptions for future benefit payments may also change over time, and could be materially higher than originally projected.

We expect to make contributions to our pension plans in the future, and may be required to make contributions that could be material. We may fund contributions through the use of cash on hand, the proceeds of borrowings, shares of our common stock, or a combination of the foregoing, as permitted by applicable law. We may also explore other strategic alternatives in order to address expected pension liability, including de-risking options or acquisitions or sales of assets or divestitures, in order to meet the Company’s liquidity needs. Divestitures could result in decreased future revenues and profits, and an obligation to make contributions to our pension plans could reduce the cash available for working capital and other corporate uses, and may have an adverse impact on our operations, financial condition and liquidity.

Our ability to raise additional capital to fund our operations and growth may be limited.

Possible failure in the future to obtain necessary capital or enter into new or replacement financing arrangements could have a material adverse effect on our business, financial condition, results of operations and cash flows.

As of June 30, 2021, the Company's total indebtedness was $22.0 million as compared to indebtedness of $30.9 million as of June 30, 2020. As previously disclosed by Company in the June 30, 2020 Form 10-K, as a result of a decrease in sales related to the COVID-19 epidemic, the Company anticipated potential non-compliance with its fixed charge coverage ratio for the year ended June 30, 2020 under its Loan and Security Agreement by and among the Company and its U.S. operating companies and TD Bank, N.A. (“TD Bank”). On June 25, 2020, the Company and TD Bank entered into an amendment and restatement (the “Amendment and Restatement”) of the Loan Agreement. The Amendment and Restatement waived the fixed charge coverage ratio for the quarter ended June 30, 2020. In addition, the Amendment and Restatement clarifies that certain non-cash adjustments to the definition of EBITDA are permitted under the Loan Agreement, as amended. Additionally, the Amendment and Restatement increases the permitted borrowings from a foreign bank from $5.0 million to $15.0 million and permits the Company to draw the remainder of the outstanding balance under the Loan Agreement, which was approximately $7.2 million as of June 30, 2020 and $15.1 million as of June 30, 2021. The “First Amendment” to this loan agreement was executed on September 17, 2020, which included, among other things, (i) pause testing of the Fixed Charge Coverage Ratio until September 30, 2021 and (ii) establishment of a new minimum cumulative EBITDA and minimum liquidity covenants in lieu thereof. (See note 13 Debt for more details).

Financing, including the costs of such financing, may be dependent on numerous factors, including (but not limited to) :

•general economic and capital market conditions, including the then-prevailing interest rate environment;

•credit availability from banks and other financial institutions willing to lend;

•investor confidence in us and our ability to grow the business;

•our financial performance, especially our cash flow and profitability from operations or lack thereof;

•our level of any of our indebtedness and our compliance with covenants in debt agreements for such financing;

•attaining and maintenance of acceptable credit ratings or credit quality; and

•provisions of tax and securities laws that may impact raising capital.

We may not be successful in obtaining financing for a variety of business and market reasons. Our failure to obtain necessary capital or enter into new or replacement financing arrangements may have a material adverse effect on our business, financial condition, results of operations and cash flows.

7

Increased information technology security threats and more sophisticated computer crime pose a risk to our systems, networks, products and services. Any inadequacy, interruption, integration failure or security failure with respect to our information technology could harm our ability to effectively operate our business.

The efficient operation of the Company's business is dependent on its information systems, including its ability to operate them effectively and to successfully implement new technologies, systems, controls and adequate disaster recovery systems. In addition, the Company must protect the confidentiality of data of its business, employees, customers and other third parties. Information technology security threats -- from user error to cybersecurity attacks designed to gain unauthorized access to our systems, networks and data – are increasing in frequency and sophistication. Cybersecurity attacks may range from random attempts to coordinated and targeted attacks, including sophisticated computer crime and advanced persistent threats. On October 7, 2020 our information technology ("IT") systems were exposed to a ransomware attack, which partially impaired certain IT systems for a short period of time. We do not believe we experienced any material losses related to the ransomware attack and although we continually attempt to improve upon our security we consider that one attack resolved.

These threats pose a risk to the security of our systems and networks and the confidentiality, availability and integrity of our data. Cybersecurity attacks could also include attacks targeting customer data or the security, integrity and/or reliability of the hardware and software installed in our products. It is possible that our information technology systems and networks, or those managed by third parties, could have vulnerabilities, which could go unnoticed for a period of time. The possible failure of the Company's information systems to perform as designed or its failure to implement and operate them effectively could disrupt the Company's business or subject it to liability and thereby harm its profitability. While the Company continues to enhance the applications contained in the Enterprise Resource Planning (ERP) system as well as improvements to other operating systems, there can be no guarantee that the actions and controls we have implemented and are implementing, or which we cause or have caused third party service providers to implement, will be sufficient to protect our systems, information or other property.

Our operational results are dependent on how well we can scale our manufacturing capacity and resources to the level of our customers’ demand.

We sell our products in industries that require manufacturers to make highly efficient use of manufacturing capacity. Insufficient or excess capacity threatens our ability to generate competitive profit margins and may expose us to liabilities such as contractual commitments. Although from time to time we close or consolidate facilities, adapting or modifying our capacity is difficult, as modifications take substantial time to execute, are inherently disruptive and costly and, in some cases, may require regulatory approval. Additionally, delivering products during process or facility modifications requires special coordination. The cost and resources required to adapt our capacity, such as through facility acquisitions, facility closings or process moves between facilities, may negate any planned cost reductions or may result in costly delays, product quality issues or material shortages, all of which could adversely affect our operational results and our reputation with our customers.

Changes in government monetary or fiscal policies may negatively impact our results.

Most countries where our products are sold have established central banks to regulate monetary systems and influence economic activities, generally by adjusting interest rates. Interest rate changes affect overall economic growth, which could affect sales of our products. Interest rate changes may also impact our customers’ ability to finance machine purchases and the ability of our suppliers to finance the production of parts and components necessary to manufacture and support our products. Increases in interest rates could negatively impact sales and create supply chain inefficiencies.

Central banks and other policy arms of many countries may take actions to vary the amount of liquidity and credit available in an economy. The impact from a change in liquidity and credit policies could negatively impact the customers and markets we serve or our suppliers, create supply chain inefficiencies and could adversely impact our business.

If we do not meet customers’ product quality, reliability standards and expectations, we may experience increased or unexpected product warranty claims and other adverse consequences to our business.

Product quality and reliability are significant factors influencing customers' decisions to purchase our products. Inability to maintain the high quality of our products relative to the perceived or actual quality of similar products offered by competitors could result in the loss of market share, loss of revenue, reduced profitability, an increase in warranty costs, government investigations and/or damage to our reputation.

Product quality and reliability are determined in part by factors that are not entirely within our control. We depend on our suppliers for parts and components that meet our standards. If our suppliers fail to meet those standards, we may not be able to deliver the quality of products that our customers expect, which may impair our reputation, resulting in lower revenue and higher warranty costs.

8

We provide our customers a warranty covering workmanship, and in some cases materials, on products we manufacture. Our warranty generally provides that products will be free from defects for 1 year. If a product fails to comply with the warranty, we may be obligated, at our expense, to correct any defect by repairing or replacing the defective product. Although we maintain warranty reserves in an amount based primarily on the number of units shipped and on historical and anticipated warranty claims, there can be no assurance that future warranty claims will follow historical patterns or that we can accurately anticipate the level of future warranty claims. While the Company has historically not incurred significant warranty expense, an increase in the rate of warranty claims or the occurrence of unexpected warranty claims, for which we are not insured or where we cannot recover from our vendors to the extent their materials or workmanship were defective, could materially and adversely affect our financial condition, results of operations and cash flows.

If our manufacturing processes and products do not comply with applicable statutory and regulatory requirements, or if we manufacture products containing design or manufacturing defects, demand for our products may decline and we may be subject to product liability claims.

Our designs, manufacturing processes and facilities need to comply with applicable statutory and regulatory requirements. We may also have the responsibility to ensure that products we design satisfy safety and regulatory standards including those applicable to our customers and to obtain any necessary certifications. As a result, products that we manufacture may at times contain manufacturing or design defects, and our manufacturing processes may be subject to errors or not be in compliance with applicable statutory and regulatory requirements or demands of our customers. Potential defects in the products we manufacture or design, whether caused by a design, manufacturing or component failure or error, or deficiencies in our manufacturing processes, may result in delayed shipments to customers, replacement costs or reduced or canceled customer orders. If these defects or deficiencies are significant, our business reputation may also be damaged. The failure of the products that we manufacture or our manufacturing processes and facilities to comply with applicable statutory and regulatory requirements may subject us to legal fines or penalties and, in some cases, require us to shut down or incur considerable expense to correct a manufacturing process or facility.

Any manufacturing or design defects may also result in product liability claims. Furthermore, customers use some of our products in potentially hazardous applications that can cause injury or loss of life and damage to property, equipment or the environment. We may be named as a defendant in product liability or other lawsuits asserting potentially large claims if an accident occurs at a location where our equipment and services have been or are being used. We also maintain certain insurance policies which may limit our financial exposures. Any significant liabilities which are not covered by insurance could have an adverse effect on our financial condition, results of operation and cash flows. Likewise, a substantial increase in the number of claims that are made against us or the amounts of any judgments or settlements could materially and adversely affect our reputation and our financial condition, results of operations and cash flows.

Volatility in the price of energy and raw materials, large or rapid increases in the cost of raw materials or components parts, substantial decreases in their availability, or our dependence on particular suppliers of raw materials and component parts could materially and adversely affect our operating results.

Steel is the principal raw material used in the manufacture of the Company’s products. Historically, market prices of some of our key raw materials have fluctuated on a cyclical basis and have often depended on a variety of factors over which the Company has no control, including as a result of tariffs or other trade barriers. If in the future we are not able to reduce product costs in other areas or pass raw material price increases on to our customers, our margins could be adversely affected. In addition, because we maintain limited raw material and component inventories, even brief unanticipated delays in delivery by suppliers—including those due to capacity constraints, labor disputes, impaired financial condition of suppliers, weather emergencies, global pandemics, such as COVID-19, or other natural disasters— may impair our ability to satisfy our customers and could adversely affect our financial performance. The cost of producing the Company’s products is also sensitive to the price of energy. If we are unable to manage pricing from these suppliers effectively or pass future cost increases through to our customers, our financial performance could be adversely affected. Likewise, if our suppliers terminate these agreements and we are unable to procure alternate products at substantially similar competitive pricing, our financial performance could be adversely affected.

We may not be able to maintain our engineering, technological and manufacturing expertise.

The markets for our products are characterized by changing technology and evolving process development. The continued success of our business will depend upon our ability to:

•hire, retain and expand our pool of qualified engineering and technical personnel;

•maintain technological leadership in our industry;

•successfully anticipate or respond to changes in manufacturing processes in a cost-effective and timely manner; and

9

•successfully anticipate or respond to changes in cost to serve in a cost-effective and timely manner

We cannot be certain that we will develop the capabilities required by our customers in the future. The emergence of new technologies, industry standards or customer requirements may render our equipment, inventory or processes obsolete or non-competitive. We may have to acquire new technologies and equipment to remain competitive. The acquisition and implementation of new technologies and equipment may require us to incur significant expense and capital investment, which could reduce our margins and affect our operating results. When we establish new facilities, we may not be able to maintain or develop our engineering, technological and manufacturing expertise due to a lack of trained personnel, effective training of new staff or technical difficulties with machinery. Failure to anticipate and adapt to customers’ changing technological needs and requirements or to hire and retain a sufficient number of engineers and maintain engineering, technological and manufacturing expertise may have a material adverse effect on our business.

If we fail to protect our intellectual property rights or maintain our rights to use licensed intellectual property, our business could be adversely affected.

Our intellectual property, including our patents, trade secrets, trademarks and licenses are important in the operation of our business. Although we intend to protect our intellectual property rights vigorously, we cannot be certain that we will be successful in doing so. Third parties may assert or prosecute infringement claims against us in connection with the services and products that we offer, and we may or may not be able to successfully defend these claims. Litigation, either to enforce our intellectual property rights or to defend against claimed infringement of the rights of others, could result in substantial costs and in a diversion of our resources.

In addition, if a third party would prevail in an infringement claim against us, then we would likely need to obtain a license from the third party on commercial terms, which would likely increase our costs. Our failure to maintain or obtain necessary licenses or an adverse outcome in any litigation relating to patent infringement or other intellectual property matters could have a material adverse effect on our financial condition, results of operations and cash flows.

Risks Related to Legal and Regulatory

International operations and our financial results in those markets may be affected by legal, regulatory, political, currency exchange and other economic risks.

During the fiscal year 2021, revenue from sales outside of the United States was $107.9 million, representing approximately 49% of consolidated sales. In addition, a significant amount of our manufacturing and production operations are located, or our products are sourced from, outside the United States. As a result, our business is subject to risks associated with international operations. These risks include the burdens of complying with foreign laws and regulations, unexpected changes in tariffs, taxes or regulatory requirements, changes in governmental monetary and fiscal policies, and political unrest and corruption. Regulatory changes could occur in the countries in which we sell, produce or source our products or significantly increase the cost of operating in or obtaining materials originating from certain countries. Restrictions imposed by such changes can have a significant impact on our business.

In addition, the functional currency for most of our foreign operations is the applicable local currency. As a result, fluctuations in foreign currency exchange rates affect the results of our operations and the value of our foreign assets and liabilities, which in turn may adversely affect results of operations and cash flows and the comparability of period-to-period results of operations. Changes in foreign currency exchange rates may also affect the relative prices at which we and foreign competitors sell products in the same market. Foreign governmental policies and actions regarding currency valuation could result in actions by the United States and other countries to offset the effects of such fluctuations. Given the unpredictability and volatility of foreign currency exchange rates, ongoing or unusual volatility may adversely impact our business and financial conditions.

Countries in which our products are manufactured or sold may from time to time impose additional new regulations, or modify existing regulations, including:

•changes in duties, taxes, tariffs and other charges on imports;

•limitations on the quantity of goods which may be imported into the United States from a particular country;

•requirements as to where products and/or inputs are manufactured or sourced;

•creation of export licensing requirements, imposition of restrictions on export quantities or specification of minimum export pricing and/or export prices or duties;

•currency fluctuations;

•limitations on foreign owned businesses; or

10

•government actions to cancel contracts, re-denominate the official currency, renounce or default on obligations, renegotiate terms unilaterally or expropriate assets.

In addition, political and economic changes or volatility, geopolitical regional conflicts, terrorist activity, political unrest, civil strife, acts of war, public corruption and other economic or political uncertainties could interrupt and negatively affect our business operations. All of these factors could result in increased costs or decreased revenues and could materially and adversely affect our product sales, financial condition and results of operations.

Failure to comply with laws, rules and regulations could negatively affect our business operations and financial performance.

Due to the international scope of our operations, we are subject to a complex system of federal, state, local and international laws, rules and regulations, such as state and local wage and hour laws, the U.S. Foreign Corrupt Practices Act (the “FCPA”), the False Claims Act, the Employee Retirement Income Security Act (“ERISA”), securities laws, import and export laws (including customs regulations) and many others. We may also be subject to investigations or audits by governmental authorities and regulatory agencies, which can occur in the ordinary course of business or which can result from increased scrutiny from a particular agency towards an industry, country or practice. Such investigations or audits may subject us to increased government scrutiny, investigation and civil and criminal penalties, and may limit our ability to import or export our products or to provide services outside the United States.

Furthermore, embargoes and sanctions imposed by the United States and other governments restricting or prohibiting sales to specific persons or countries or based on product classification may expose us to potential criminal and civil sanctions. We cannot predict the nature, scope or effect of future regulatory requirements to which our operations might be subject or in certain locations the manner in which existing laws might be administered or interpreted.

In addition, as a result of operating in multiple countries, we must comply with multiple foreign laws and regulations that may differ substantially from country to country and may conflict with corresponding U.S. laws and regulations. The FCPA and similar foreign anti-corruption laws generally prohibit companies and their intermediaries from making improper payments or providing anything of value to improperly influence foreign government officials for the purpose of obtaining or retaining business, or obtaining an unfair advantage. Recent years have seen a substantial increase in the global enforcement of anti-corruption laws. Our operations outside the United States, including in developing countries, expose us to the risk of such violations. If we fail to comply with laws, rules and regulations or the manner in which they are interpreted or applied, we may be subject to government enforcement action, class action litigation or other litigation, damage to our reputation, civil and criminal liability, damages, fines and penalties, and increased cost of regulatory compliance, any of which could adversely affect our results of operations and financial performance.

Failure to comply with exchange listing requirements, rules and regulations could negatively affect our Company's listing on the New York Stock Exchange.

On October 1, 2020, the Company was notified by the New York Stock Exchange (the “NYSE”) that it was not in compliance with the continued listing standard set forth in Section 802.01B of the NYSE Listed Company Manual because the Company’s average market capitalization was less than $50 million over a consecutive 30 trading-day period and the stockholders’ equity of the Company was less than $50 million. On March 4, 2021 the NYSE notified the Company that L.S. Starrett is back in compliance in relation to the NYSE's quantitative continued listing standards. This decision comes as a result of the Company’s achievement of compliance with the NYSE’s minimum market capitalization and shareholders’ equity requirements during fiscal 2021.

However, in accordance with the NYSE’s Listed Company Manual, the Company will be subject to a 12-month follow-up period within which the Company will be reviewed to ensure that the Company does not once again fall below any of the NYSE’s continued listing standards. If within 12 months of this letter the Company is again determined to be below any of the continued listing standards, the NYSE will gain an understanding of the reason(s) for falling below such standards, which may include a re-evaluation of the Company’s originally reviewed method of financial recovery. The NYSE will then take the appropriate action, which, depending on circumstances, may include truncating the compliance procedures described in the NYSE Listed Company Manual or beginning the initiation of NYSE trading suspension procedures. The Company will, of course, be subject to the NYSE’s normal continued listing monitoring.

Costs associated with lawsuits or investigations or adverse rulings in enforcement or other legal proceedings may have an adverse effect on our results of operations.

11

From time to time, we are involved in various claims and lawsuits that arise in and outside of the ordinary course of our business. The industries in which we operate are also periodically reviewed or investigated by regulators, which could lead to enforcement actions, fines and penalties or the assertion of private litigation claims. It is not possible to predict with certainty the outcome of claims, investigations and lawsuits, and we could in the future incur judgments, fines or penalties or enter into settlements of lawsuits and claims that could have an adverse effect on our reputation, business, results of operations or financial condition in any particular period. The global and diverse nature of our operations means that legal and compliance risks will continue to exist and additional legal proceedings and other contingencies, the outcome of which cannot be predicted with certainty, may arise from time to time. In addition, subsequent developments in legal proceedings may affect our assessment and estimates of loss contingencies recorded as a reserve and require us to make payments in excess of our reserves, which could have an adverse effect on our reputation, business and results of operations or financial condition.

Our tax rate is dependent upon a number of factors, a change in any of which could impact our future tax rates and net income.

Our future tax rates may be adversely affected by a number of factors, including the enactment of certain tax legislation being considered in the United States and other countries; other changes in tax laws or the interpretation of such tax laws; changes in the estimated realization of our net deferred tax assets; the jurisdictions in which profits are determined to be earned and taxed; the repatriation of non-U.S. earnings for which we have not previously provided for U.S. income and non-U.S. withholding taxes; adjustments to estimated taxes upon finalization of various tax returns; increases in expenses that are not deductible for tax purposes, including impairment of goodwill in connection with acquisitions; changes in available tax credits; and the resolution of issues arising from tax audits with various tax authorities. Losses for which no tax benefits can be recorded could materially impact our tax rate and its volatility from one quarter to another. Any significant change in our jurisdictional earnings mix or in the tax laws in those jurisdictions could impact our future tax rates and net income in those periods.

Item 1B – Unresolved Staff Comments

None.

Item 2 - Properties

The Company’s principal plant and its corporate headquarters are located in Athol, MA on approximately 15 acres of Company-owned land. The plant consists of 25 buildings, mostly of brick construction of varying dates, with approximately 535,000 square feet.

The Company’s Webber Gage Division in Cleveland, OH, owns and occupies two buildings totaling approximately 50,000 square feet.

The Company completed a sale and partial leaseback of the Mount Airy, North Carolina facility in December 2020. The Company sold three buildings amounting to 313,000 square feet and entered into an operating lease for 66,000 square feet for on-going operations.

The Company’s subsidiary in Itu, Brazil owns and occupies several buildings totaling 209,000 square feet.

The Company’s subsidiary in Jedburgh, Scotland owns and occupies a 175,000 square foot building.

A wholly owned manufacturing subsidiary in The People’s Republic of China leases a 133,000 square foot building in Suzhou and leases a sales office in Shanghai.

The Tru-Stone Division owns and occupies a 106,000 square foot facility in Waite Park, MN.

The Kinemetric Engineering Division occupies an 18,000 square foot leased facility in Laguna Hills, CA.

The Bytewise Division occupies a 22,000 square foot leased facility in Columbus, GA.

In addition, the Company operates warehouses and/or sales-support offices in the U.S., Australia, New Zealand, Mexico, Singapore and Japan.

In the Company’s opinion, all of its property, plant and equipment are in good operating condition, well maintained and adequate for its current and foreseeable needs.

12

Item 3 - Legal Proceedings In the ordinary course of business, the Company is involved from time to time in litigation that is not considered material to its financial condition or operations.

Item 4 – Mine Safety Disclosures

Not applicable.

13

PART II

Item 5 - Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities

The Company’s Class A common stock is traded on the New York Stock Exchange. Quarterly high/low closing market price information is presented in the table below. The Company’s Class B common stock is generally nontransferable, except to lineal descendants of stockholders, and thus has no established trading market, but it can be converted into Class A common stock at any time. The Class B common stock was issued on October 5, 1988, and the Company has paid the same dividends thereon as have been paid on the Class A common stock since that date. On June 30, 2021, there were approximately 1,048 registered holders of Class A common stock and approximately 854 registered holders of Class B common stock. In the fourth quarter of fiscal 2021, there were zero Class A shares and 2,983 Class B shares repurchased.

| Quarter Ended | High | Low | ||||||||||||

| September 2019 | 6.90 | 5.25 | ||||||||||||

| December 2019 | 6.03 | 5.23 | ||||||||||||

| March 2020 | 6.03 | 3.03 | ||||||||||||

| June 2020 | 4.09 | 3.02 | ||||||||||||

| September 2020 | 3.56 | 2.95 | ||||||||||||

| December 2020 | 4.34 | 2.55 | ||||||||||||

| March 2021 | 7.25 | 4.21 | ||||||||||||

| June 2021 | 9.90 | 5.96 | ||||||||||||

The Company’s dividend policy is subject to periodic review by the Board of Directors. Based upon economic conditions, the Board of Directors suspended its quarterly dividend of $0.10 as of the quarter ended March 31, 2018.

PERFORMANCE GRAPH

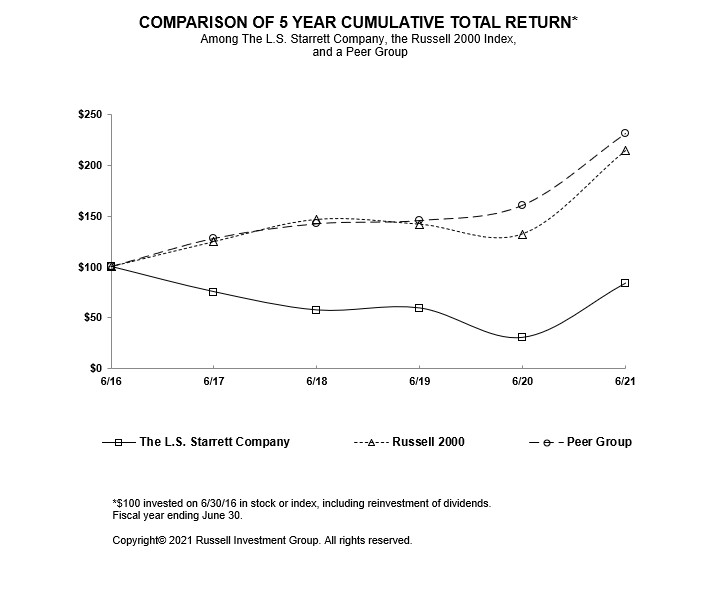

The following graph sets forth information comparing the cumulative total return to holders of the Company’s Class A common stock based on the market price of the Company’s Class A common stock over the last five fiscal years with (1) the cumulative total return of the Russell 2000 Index (“Russell 2000”) and (2) a peer group index (the “Peer Group”) reflecting the cumulative total returns of certain small cap manufacturing companies as described below. The peer group is comprised of the following companies: Acme United, Q.E.P. Co. Inc., Badger Meter, National Presto Industries, Regal-Beloit Corp., Tennant Company, The Eastern Company and WD-40.

14

| Base | FY17 | FY18 | FY19 | FY20 | FY21 | ||||||||||||||||||

| The L.S. Starrett Company | $ | 100.00 | $ | 75.20 | $ | 57.30 | $ | 59.30 | $ | 30.40 | $ | 83.60 | |||||||||||

| Russell 2000 | $ | 100.00 | $ | 124.60 | $ | 146.49 | $ | 141.64 | $ | 132.26 | $ | 214.29 | |||||||||||

| Peer Group | $ | 100.00 | $ | 127.79 | $ | 142.22 | $ | 145.41 | $ | 160.48 | $ | 231.30 | |||||||||||

Item 6 - Selected Financial Data

The following selected financial data have been derived from and should be read in conjunction with “Management Discussion and Analysis of Financial Condition and Results of Operations” and our Consolidated Financial Statements and notes thereto, included elsewhere in this Annual Report on Form 10-K.

15

| Years ended June 30 (in $000s except per share data) | |||||||||||||||||||||||||||||

| 2021 | 2020 | 2019 | 2018 | 2017 | |||||||||||||||||||||||||

| Net sales | $ | 219,644 | $ | 201,451 | $ | 228,022 | $ | 216,328 | $ | 207,023 | |||||||||||||||||||

| Net earnings (loss) | 15,533 | (21,839) | 6,079 | (3,633) | 991 | ||||||||||||||||||||||||

| Basic earnings (loss) per share | 2.20 | (3.14) | 0.87 | (0.52) | 0.14 | ||||||||||||||||||||||||

| Diluted earnings (loss) per share | 2.11 | (3.14) | 0.87 | (0.52) | 0.14 | ||||||||||||||||||||||||

| Long-term debt | 6,010 | 26,341 | 17,541 | 17,307 | 6,095 | ||||||||||||||||||||||||

| Total assets | 184,486 | 172,683 | 190,087 | 182,286 | 192,665 | ||||||||||||||||||||||||

| Dividends per share | 0.00 | 0.00 | 0.00 | 0.20 | 0.40 | ||||||||||||||||||||||||

Items 7 and 7A- Management’s Discussion and Analysis of Financial Condition and Results of Operations and Quantitative and Qualitative Disclosures about Market Risk

RESULTS OF OPERATIONS

Use of Non- U.S. GAAP Financial Measures

In "Management's discussion and analysis on financial condition and results of operations" in this annual report on Form 10-K, we discuss non-U.S. GAAP financial measures related to currency-neutral sales revenues, as well as adjusted operating income to adjust for restructuring costs, gain on the sale of assets, or the impairment of intangibles that are reflected in one period but not the other, in order to show comparative operational performance.

We present these non-U.S. GAAP financial measures because we believe they assist investors in comparing our performance across reporting periods on a consistent basis by eliminating items that we do not believe are indicative of our core operating performance. Such non-U.S. GAAP financial measures assist investors in understanding the ongoing operating performance of the Company by presenting financial results between periods on a more comparable basis. Such measures should be considered in addition to, and not in lieu of, the financial measures calculated and presented in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”). $ We include a reconciliation of adjusted operating income to its comparable U.S. GAAP financial measures.

References to currency-neutral revenues and adjusted operating income should not be considered in isolation or as a substitute for other financial measures calculated and presented in accordance with U.S. GAAP and may not be comparable to similarly titled non-U.S GAAP financial measures used by other companies. In evaluating these non-U.S. GAAP financial measures, investors should be aware that in the future we may incur expenses or be involved in transactions that are the same as or similar to some of the adjustments in this presentation. Our presentation of non-U.S. GAAP financial measures should not be construed to imply that its future results will be unaffected by any such adjustments. Non-U.S. GAAP financial measures have limitations as analytical tools, and investors should not consider them in isolation or as a substitute for analysis of our results as reported under U.S. GAAP.

Please see Note 17 regarding segment results of operations. The Company’s business is aggregated into two reportable segments based on geography of operations: North American Operations and International Operations. Segment income is measured for internal reporting purposes by excluding corporate expenses, which are included in the unallocated column in the following tables as well as Note 17. These tables below are included to better explain our consolidated operational performance by showing more detail by business segment and reconciling U.S. GAAP operating income and adjusted operating income.

The following tables represent key results of operations on a consolidated basis for the periods indicated:

16

| Comparison to Fiscal Year 2020 | Comparison to Fiscal Year 2019 | |||||||||||||||||||||||||

| Fiscal Year | Fiscal Year | Favorable (unfavorable) | Fiscal Year | Favorable (unfavorable) | ||||||||||||||||||||||

| (Amounts in Thousands) | 6/30/2021 | 6/30/2020 | $ Change | % Change | 6/30/2019 | $ Change | % Change | |||||||||||||||||||

| Net sales | $ | 219,644 | $ | 201,451 | $ | 18,193 | 9.0 | % | 228,022 | (8,378) | (3.7) | % | ||||||||||||||

| Gross margin | 73,342 | 62,210 | 11,132 | 17.9 | % | 74,941 | (1,599) | (2.1) | % | |||||||||||||||||

| % of net sales | 33.4 | % | 30.9 | % | 32.9 | % | ||||||||||||||||||||

| Selling, general, and administrative expenses | 56,316 | 59,437 | 3,121 | 5.3 | % | 63,720 | 7,404 | 11.6 | % | |||||||||||||||||

| % of net sales | 25.6 | % | 29.5 | % | 27.9 | % | ||||||||||||||||||||

| Restructuring charges | 3,664 | 1,580 | (2,084) | (131.9) | % | — | (3,664) | (100.0) | % | |||||||||||||||||

| Goodwill and intangible impairment | — | 6,496 | 6,496 | 100.0 | % | — | +0 | — | % | |||||||||||||||||

| Gain on sale of building | (3,204) | — | 3,204 | 100.0 | % | — | 3,204 | 100.0 | % | |||||||||||||||||

| Operating income | 16,566 | (5,303) | 21,869 | 412.4 | % | 11,221 | 5,345 | 47.6 | % | |||||||||||||||||

| % of net sales | 7.5 | % | (2.6) | % | 4.9 | % | ||||||||||||||||||||

| Other Income (expense) | 860 | (14,694) | 15,554 | 105.9 | % | (1,611) | 2,471 | (153.4) | % | |||||||||||||||||

| Net earnings (loss) | 17,426 | (19,997) | 37,423 | 187.1 | % | 9,610 | 7,816 | 81.3 | % | |||||||||||||||||

| Income tax expense | 1,893 | 1,842 | (51) | (2.8) | % | 3,531 | 1,638 | 46.4 | % | |||||||||||||||||

| Net earnings (loss) | $ | 15,533 | $ | (21,839) | $ | 37,372 | 171.1 | % | $ | 6,079 | $ | 9,454 | 155.5 | % | ||||||||||||

| US GAAP to NON-U.S. GAAP Reconciliation | Comparison to Fiscal 2020 | Comparison to Fiscal 2019 | ||||||||||||||||||||||||

| Fiscal Year | Fiscal Year | Favorable (unfavorable) | Fiscal Year | Favorable (unfavorable) | ||||||||||||||||||||||

| (Amounts in Thousands) | 6/30/2021 | 6/30/2020 | $ Change | % Change | 6/30/2019 | $ Change | % Change | |||||||||||||||||||

| Operating income, as reported | $ | 16,566 | $ | (5,303) | $ | 21,869 | 412.4 | % | $ | 11,221 | $ | 5,345 | 47.6 | % | ||||||||||||

| Restructuring charges | 3,664 | 1,580 | 2,084 | 131.9 | % | — | 3,664 | 100.0 | % | |||||||||||||||||

| Goodwill and intangibles impairment | — | 6,496 | (6,496) | (100.0) | % | — | — | — | % | |||||||||||||||||

| Gain on sale of building | (3,204) | — | (3,204) | 100.0 | % | — | (3,204) | (100.0) | % | |||||||||||||||||

| Adjusted operating income | $ | 17,026 | $ | 2,773 | $ | 14,253 | 514.0 | % | $ | 11,221 | $ | 5,805 | 51.7 | % | ||||||||||||

| % of net sales | 7.8 | % | 1.4 | % | +640 bps | 4.9 | % | +290 bps | ||||||||||||||||||

| US GAAP to NON-U.S. GAAP Reconciliation by Reporting Segment | ||||||||||||||||||||||||||||||||||||||

| Fiscal Year 2021 | Fiscal Year 2020 | Fiscal Year 2019 | ||||||||||||||||||||||||||||||||||||

| (Amounts in Thousands) | North America | Inter-national | Corp | Total | North America | Inter-national | Corp | Total | North America | Inter-national | Corp | Total | ||||||||||||||||||||||||||

| Net Sales | $ | 119,619 | $ | 100,025 | $ | — | $ | 219,644 | $ | 121,834 | $ | 79,617 | $ | 201,451 | $ | 136,387 | $ | 91,635 | $ | 228,022 | ||||||||||||||||||

| Operating income, as reported | 13,144 | 10,821 | (7,399) | 16,566 | (2,055) | 3,842 | (7,090) | (5,303) | 9,468 | 8,043 | (6,290) | 11,221 | ||||||||||||||||||||||||||

| Restructuring charges | 1,059 | 2,605 | — | 3,664 | 341 | 1,239 | — | 1,580 | — | — | — | — | ||||||||||||||||||||||||||

| Goodwill and intangibles impairment | — | — | — | — | 6,496 | — | — | 6,496 | — | — | — | — | ||||||||||||||||||||||||||

| Gain on sale of building | (3,204) | — | — | (3,204) | — | — | — | — | — | — | — | — | ||||||||||||||||||||||||||

| Adjusted operating income | $ | 10,999 | $ | 13,426 | $ | (7,399) | $ | 17,026 | $ | 4,782 | $ | 5,081 | $ | (7,090) | $ | 2,773 | $ | 9,468 | $ | 8,043 | $ | (6,290) | $ | 11,221 | ||||||||||||||

| % of net sales | 9.2 | % | 13.4 | % | 7.8 | % | 3.9 | % | 6.4 | % | 1.4 | % | 6.9 | % | 8.8 | % | 4.9 | % | ||||||||||||||||||||

17

NON-U.S. GAAP Measure Reconciliation: FY21 "Currency Neutral" Net Sales

| Fiscal Year ending | Comparison to Fiscal Year 2020 | Fiscal Year ending | Comparison to Fiscal Year 2019 | |||||||||||||||||||||||

| (Amounts in Thousands) | 6/30/2021 | 6/30/2020 | $ Change | % Change | 6/30/2021 | 6/30/2019 | $ Change | % Change | ||||||||||||||||||

| Total Net Sales, as reported | $ | 219,644 | $ | 201,451 | $ | 18,193 | 9.0 | % | $ | 219,644 | $ | 228,022 | $ | (8,378) | (3.7) | % | ||||||||||

| Currency Neutralizing Adjustment* | 11,361 | — | 11,361 | 5.6 | % | 24,695 | — | 24,695 | 10.8 | % | ||||||||||||||||

| TOTAL FY21 Currency Neutral Net Sales | $ | 231,005 | $ | 201,451 | $ | 29,554 | 14.7 | % | $ | 244,339 | $ | 228,022 | $ | 16,317 | 7.2 | % | ||||||||||

| North America Net Sales, as reported | 119,619 | 121,834 | -2,215 | (1.8) | % | 119,619 | 136,387 | (16,768) | (12.3) | % | ||||||||||||||||

| Currency Neutralizing Adjustment* | (174) | — | -174 | (0.1) | % | 67 | — | +67 | — | |||||||||||||||||

| FY21 Currency Neutral North America Net Sales | 119,445 | 121,834 | (2,389) | (2.0) | % | 119,686 | 136,387 | (16,701) | (12.2) | % | ||||||||||||||||

| International Net Sales, as reported | 100,025 | 79,617 | 20,408 | 25.6 | % | 100,025 | 91,635 | 8,390 | 9.2 | % | ||||||||||||||||

| Currency Neutralizing Adjustment* | 11,535 | — | 11,535 | 14.5 | % | 24,628 | — | 24,628 | 26.9 | % | ||||||||||||||||

| FY21 Currency Neutral International Net Sales | $ | 111,560 | $ | 79,617 | $31,943 | 40.1 | % | $ | 124,653 | $ | 91,635 | $ | 33,018 | 36.0 | % | |||||||||||

| *"Currency Neutralizing Adjustment" = Change when converting FY21 sales in non USD functional currencies at the same exchange rates used in the comparison period | ||||||||||||||||||||||||||

COVID-19 pandemic

The Covid-19 Pandemic has had a substantial impact on the Company's global sales over the past two fiscal years. This impact was felt beginning in January 2020 in our operation in Suzhou, China and then intensified in March 2020 by affecting our global markets. We initiated several restructuring activities designed to consolidate manufacturing capacity and reduce selling, general and administrative expenses globally, which included the sale of our facility in Mt. Airy, North Carolina. These restructuring activities commenced in the second quarter of fiscal 2020, continued throughout and completed in fiscal 2021.

As we closed fiscal 2021, order intake and sales volume across our offerings were equal to or exceeding pre-pandemic levels. Sales began to increase in the first half of fiscal 2021 particularly in Brazil and in our Tru-Stone subsidiary, reflective of the strength of the sectors in which they participate. Brazil experienced strong growth in the Consumer DIY and Food sectors, and Tru-Stone benefited from increasingly high demand in equipment for the high end chip making industry . Order intake and sales volume in other areas of the North American Industrial and Metrology businesses remained very low in the first half of fiscal 2021, and only began to show signs of recovery late in the third quarter.

With the increased sales volume, reduced cost, and planned production utilization improvement throughout fiscal 2021, our financial performance continued to improve, and was especially strong during the fourth quarter. In fiscal 2021, we had a 7.8% operating income as a percentage of sales as compared to an operating loss in fiscal 2020 and operating income of 4.9% in fiscal 2019. As shown in the above table, management also looks at the non-GAAP reconciliation, adjusting out restructuring, impairment and the gain on facility sales. The non-GAAP adjusted operating income was 7.8%, the same as U.S. GAAP because the facility gain and restructuring expense essentially offset. This was a 640 basis point increase over fiscal 2020 and a 290 basis point increase over 2019, even though fiscal 2019 had $8.4 million more in annual sales.

Fiscal 2021 Compared to Fiscal 2020 and Fiscal 2019

The Company recognizes the more standard presentation is to first compare fiscal 2021 with fiscal 2020 and separately compare fiscal 2020 with fiscal 2019, as we have in previous fiscal years. As a smaller reporting company this discussion covers the two-year period required and uses a presentation we believe will allow the reader to view performance from management's perspective, given that fiscal 2019 was the last year prior to fiscal 2020, the first fiscal year which was materially impacted by the COVID-19 pandemic.

Overview

Sales for the first half of fiscal 2021 were 4.9% below the first half of fiscal 2020 at $103.5 million, largely due to the pandemic. This trend began to change in the second quarter of fiscal 2021, as international sales, particularly in Brazil, began to strengthen. The March quarter sales of $54.9 million and the June quarter sales of $61.2 of fiscal 2021 (cumulatively $116.1 million) compares favorably to the $50.0 in the March quarter and $42.5 million in the June quarter of fiscal year 2020 (cumulatively $92.5 million), emphasizing the continuous steady sales recovery throughout fiscal 2021.

18

Overall, fiscal 2021 sales were $219.6 million and fiscal 2020 sales were $201.5 million, an increase of $18.2 million, or 9.0%. On a foreign currency neutral basis, sales in the fiscal year ending June 30, 2021 increased by $29.5 million, or 14.7% from fiscal 2020, reflecting the weakening of the Brazilian currency versus the U.S. Dollar during the comparative periods. In comparison to fiscal 2019, the full year prior to the pandemic, reported sales in fiscal 2021 were 3.7%, or $8.4 million lower than the $228.0 million of reported sales in fiscal 2019. However, on a foreign currency neutral basis, fiscal 2021 sales exceeded fiscal 2019 by 7.2%. This is due to the higher mix of Brazil sales in fiscal 2021, as sales in Brazil recovered before North American sales, and a 39.3% weakening of the Brazilian currency from fiscal 2019 through fiscal 2021.

Gross margins increased $11.1 million in fiscal 2021, or 17.9% from $62.2 million in fiscal 2020 to $73.3 million. As a percent of sales, gross margins increased from 30.9% in fiscal 2020 to 33.4% in fiscal 2021. The increase in gross margin is the result of both the increase in sales of $18.2 million and the favorable impact of restructuring activities completed throughout the last six quarters as shown through improved plant utilization and higher gross margin as a percentage of sales. When comparing fiscal 2021 to fiscal 2019, gross margin decreased by $1.7 million, but as a percentage of sales, increased from 32.9% in fiscal 2019 to 33.4% in fiscal 2021.

Selling, general and administrative expenses decreased by $3.1 million from $59.4 million in fiscal 2020 to $56.3 million in fiscal 2021, or 5.3%. Several austerity measures began in Q3 of fiscal 2020, restructuring began in Q4 of fiscal 2020, and plant consolidations were carried on throughout the last three quarters of fiscal 2021. The reductions were partially offset by increases in some variable selling costs in International locations which experienced substantial sales growth in fiscal 2021. Compared to fiscal 2019, selling, general and administrative expenses were $7.4 million, or 11.7% lower in fiscal 2021.

In the quarter ending June 30, 2020 we recorded a restructuring charge related to headcount reductions and saw manufacturing consolidation in response to conditions presented by the COVID-19 pandemic. The Company recorded a $1.6 million restructuring charge, of which $1.1 million remained accrued at June 30, 2020. During fiscal year 2021, as we completed the restructuring plans, an additional $3.7 million of restructuring charges were recorded as costs were incurred. There were no restructuring charges recorded in fiscal 2019.

As shown, above, in the U.S. GAAP to non-GAAP reconciliation, non-GAAP operating income in fiscal 2021 was $17.0 million, an increase of $14.4 million over the prior year excluding adjustments related to restructuring of $3.7 million, and the gain on the sale of the building of $3.2 million. This compares to a non-GAAP operating income of $2.8 million in fiscal 2020 exclusive of adjustments related to goodwill and intangibles impairment of a combined $6.5 million and restructuring of $1.6 million. Compared to fiscal 2019, which had no adjustments, fiscal 2021 non-GAAP operating income as adjusted above increased by $5.8 million, or 51.7% from an operating income of $11.2 million in fiscal 2019.

Net Sales

Net sales in North America decreased by $2.2 million or 1.8% from $121.8 million in fiscal 2020 to $119.6 million in fiscal 2021. North American sales only began to rebound in the fourth quarter of fiscal 2021. International sales increased $20.4 million or 25.6% from $79.6 million in fiscal 2020 to $100.0 million in fiscal 2021 driven primarily by Brazil. When adjusting for foreign exchange, the increase in International sales is even more pronounced, at 40.6%, primarily due to Brazil, which benefited from strong demand in the Consumer DIY and Food sectors.

When comparing to fiscal 2019, net sales in North America decreased from $136.4 million in fiscal 2019 to $119.6 million in fiscal 2021, a decrease of 12.3%. International sales increased to $100.0 million in fiscal 2021, from $91.6 million in fiscal 2019, or by 9.2%. On a currency-neutral basis, fiscal 2021 International sales increased 36.0% from fiscal 2019, reflecting a significant increase in sales in Brazil beginning in the second quarter of fiscal 2021, and a 39.3% devaluation of the Brazilian Real relative to the U.S. Dollar during the two comparative periods.

Gross Margin

Gross margin in fiscal 2021 increased $11.1 million or 17.9% to $73.3 million or 33.4% of sales compared to $62.2 million or 30.8% of sales in fiscal 2020. The increase in absolute and relative gross margin can be attributed to the increase in revenues and the restructuring activities completed over the last six quarters, in addition to a favorable LIFO adjustment of $2.2 million in North America in the fourth quarter of fiscal 2021.

North America gross margin increased $3.4 million or 10.5% to $36.0 million from $32.6 million, in fiscal 2020, or 30.1% and 26.8% of sales respectively This improvement is due to sales mix and restructuring activities, in addition to the LIFO adjustment mentioned above as a result of lower inventory levels in the U.S. Compared to fiscal 2019, North American gross margin in fiscal 2021 decreased by $4.7 million, or 11.6% to $36.0 from $40.7 million in fiscal 2019, or 29.9% and 30.1% of sales respectively. This is commensurate with the reduction in sales between the two comparative periods

19

International gross margins increased $7.7 million or 26% to $37.3 million from $29.6 million, in fiscal 2020 or 37.3% and 37.1% of sales respectively, commensurate with the increase in sales. Compared to fiscal 2019, International gross margins in fiscal 2021 increased $3.1 million or 9.1% to $37.3 from $34.2 million in fiscal 2019 or 37.3% and 37.3% of sales in fiscal 2021.

Selling, General and Administrative Expenses