UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

[X]

|

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

|

For the fiscal year ended December 31, 2014

|

|

|

[ ]

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

Commission file number 0-29630

SHIRE PLC

(Exact name of registrant as specified in its charter)

|

Jersey (Channel Islands)

(State or other jurisdiction of incorporation or organization)

|

98-0601486

(I.R.S. Employer Identification No.)

|

|

5 Riverwalk, Citywest Business Campus, Dublin 24, Republic of Ireland

(Address of principal executive offices and zip code)

|

+353 1 429 7700

(Registrant’s telephone number, including area code)

|

|

Securities registered pursuant to Section 12(b) of the Act:

|

|

|

Title of each class

|

Name of exchange on which registered

|

|

American Depositary Shares, each representing three Ordinary Shares 5 pence par value per share

|

NASDAQ Global Select Market

|

|

Securities registered pursuant to Section 12(g) of the Act:

|

|

|

None

|

|

|

(Title of class)

|

|

1

Indicate by check mark whether the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act

Yes [X] No [ ]

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act

Yes [ ] No [X]

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the Registrant’s knowledge, in definitive proxy or information statements incorporated by reference to Part III of this Form 10-K or any amendment to this Form 10-K.

[X]

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act.

Large accelerated filer [X] Accelerated filer Non-accelerated filer Smaller reporting company

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes [ ] No [X]

Indicate by check mark whether the Registrant has submitted electronically and posted on its corporate website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (232,405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes [X] No [ ]

As at June 30, 2014, the last business day of the Registrant’s most recently completed second quarter, the aggregate market value of the ordinary shares, £0.05 par value per share of the Registrant held by non-affiliates was approximately $ 45.9 billion. This was computed using the average bid and asked price at the above date.

As at February 13, 2015, the number of outstanding ordinary shares of the Registrant was 599,166,248.

2

THE “SAFE HARBOR” STATEMENT UNDER THE PRIVATE SECURITIES LITIGATION REFORM ACT OF 1995

Statements included herein that are not historical facts are forward-looking statements. Such forward-looking statements involve a number of risks and uncertainties and are subject to change at any time. In the event such risks or uncertainties materialize, Shire’s results could be materially adversely affected. The risks and uncertainties include, but are not limited to, that:

|

|

·

|

Shire’s products may not be a commercial success;

|

|

|

·

|

product sales from ADDERALL XR and INTUNIV are subject to generic competition;

|

|

|

·

|

the failure to obtain and maintain reimbursement, or an adequate level of reimbursement, by third-party payers in a timely manner for Shire's products may affect future revenues, financial condition and results of operations;

|

|

|

·

|

Shire conducts its own manufacturing operations for certain of its products and is reliant on third party contract manufacturers to manufacture other products and to provide goods and services. Some of the Shire’s products or ingredients are only available from a single approved source for manufacture. Any disruption to the supply chain for any of the Shire’s products may result in Shire being unable to continue marketing or developing a product or may result in Shire being unable to do so on a commercially viable basis for some period of time;

|

|

|

·

|

the manufacture of Shire’s products is subject to extensive oversight by various regulatory agencies. Regulatory approvals or interventions associated with changes to manufacturing sites, ingredients or manufacturing processes could lead to significant delays, an increase in operating costs, lost product sales, an interruption of research activities or the delay of new product launches;

|

|

|

·

|

Shire has a portfolio of products in various stages of research and development. The successful development of these products is highly uncertain and requires significant expenditures and time, and there is no guarantee that these products will receive regulatory approval;

|

|

|

·

|

the actions of certain customers could affect Shire's ability to sell or market products profitably. Fluctuations in buying or distribution patterns by such customers can adversely affect Shire’s revenues, financial conditions or results of operations;

|

|

|

·

|

investigations or enforcement action by regulatory authorities or law enforcement agencies relating to Shire’s activities in the highly regulated markets in which it operates may result in significant legal costs and the payment of substantial compensation or fines;

|

|

|

·

|

adverse outcomes in legal matters and other disputes, including Shire’s ability to enforce and defend patents and other intellectual property rights required for its business, could have a material adverse effect on Shire’s revenues, financial condition or results of operations;

|

|

|

·

|

Shire faces intense competition for highly qualified personnel from other companies and organizations. Shire is undergoing a corporate reorganization and was the subject of an unsuccessful acquisition proposal and the consequent uncertainty could adversely affect Shire’s ability to attract and/or retain the highly skilled personnel needed for Shire to meet its strategic objectives;

|

|

|

·

|

failure to achieve Shire’s strategic objectives with respect to the acquisition of NPS Pharmaceuticals Inc. (“NPS Pharma”) may adversely affect Shire’s financial condition and results of operations; and

|

other risks and uncertainties detailed from time to time in Shire’s filings with the Securities and Exchange Commission, including those risks outlined in “Item 1A: Risk Factors” in Shire’s Annual Report on Form 10-K for the year ended December 31, 2014.

3

The following are trademarks either owned or licensed by Shire plc or its subsidiaries, which are the subject of trademark registrations in certain territories, or which are owned by third parties as indicated and referred to in this Form 10-K:

ADDERALL XR® (mixed salts of a single entity amphetamine)

ADUVANZTM (lisdexamfetamine dimesylate)

AGRYLIN® (anagrelide hydrochloride)

AMITIZA® (trademark of Sucampo Pharmaceuticals)

APRISO® (trademark of Salix Pharmaceuticals, Ltd. (“Salix”))

ASACOL® (trademark of Medeva Pharma Suisse AG (used under license by Warner Chilcott Company, LLC (“Warner Chilcott”)))

BERINERT® (trademark of CSL Behring GmbH)

BERINERT P® (trademark of Aventis Behring GmbH)

BUCCOLAM® (midazolam hydrochloride oromucosal solution)

CALCICHEW® (trademark of Takeda Nycomed AS)

CARBATROL® (carbamazepine extended-release capsules)

CERDELGA® (trademark of Genzyme Corporation (“Genzyme”))

CEREZYME® (trademark of Genzyme)

CINRYZE® (C1 esterase inhibitor [human])

CLAVERSAL® (trademark of Merckle Recordati)

COLAZAL® (trademark of Salix Pharmaceuticals, Inc)

CONCERTA® (trademark of Alza Corporation (“Alza”))

CONSTELLATM (trademark of Ironwood Pharmaceuticals)

DAYTRANA® (trademark of Noven Pharmaceutical Inc. (“Noven”))

DELZICOL® (trademark of Warner Chilcott)

DERMAGRAFT® (trademark of Organogenesis Inc. (“Organogenesis”))

ELAPRASE® (idursulfase)

ELELYSO® (trademark of Pfizer Inc.)

ELVANSE® (lisdexamfetamine dimesylate)

ELVANSE ADULT® (lisdexamfetamine dimesylate)

ELVANSE VUXEN® (lisdexamfetamine dimesylate)

EPIVIR® (trademark of GlaxoSmithKline (“GSK”))

ESTRACE® (trademark of Trimel Pharmaceuticals Inc.)

EQUASYM® (methylphenidate hydrochloride)

EQUASYM XL® (methylphenidate hydrochloride)

EXPUTEX® (trademark of Phoenix Labs)

FABRAZYME® (trademark of Genzyme)

FIRAZYR® (icatibant)

FOCALIN® (trademark of Novartis AG)

FOCALIN XR® (trademark of Novartis AG)

FOSRENOL® (lanthanum carbonate)

GATTEX® (teduglutide [rDNA origin])

HUNTERASETM (trademark of Green Cross Corp.)

INTUNIV® (guanfacine extended release)

KALBITOR® (trademark of Dyax Corporation)

KAPVAY® (trademark of Shionogi Pharma, Inc. (“Shionogi”))

LIALDA® (trademark of Nogra International Limited)

MEDIKINET® (trademark of Medice Arzneimittel Pütter GmbH & Co. KG (“Medice”))

METADATE CD® (trademark of UCB Pharma, S.A.)

MEZAVANT® (trademark of Giuliani International Limited)

MICROTROL® (trademark of Supernus Pharmaceuticals, Inc. (“Supernus”))

MOVICOL® (trademark of Edra AG, S.A.)

NATPAR® (parathyroid hormone)

NATPARA® (parathyroid hormone (rDNA))

PENTASA® (trademark of Ferring B.V. Corp (“Ferring”))

PLENADREN (hydrocortisone, modified release tablet)

PREMIPLEX® (IGF-I/IGFBP-3)

QUILLIVANT® (trademark of Next Wave Pharmaceuticals, Inc.)

REMINYL® (galantamine hydrobromide) (United Kingdom ("UK”) and Republic of Ireland) (trademark of Johnson & Johnson (“J&J”)), excluding UK and Republic of Ireland)

REPLAGAL® (agalsidase alfa)

RESOLOR® (prucalopride)

4

REVESTIVE® (teduglutide)

RITALIN LA® (trademark of Novartis AG)

RUCONEST® (trademark of Pharming Intellectual Property B.V.)

SALOFALK® (trademark of Dr Falk Pharma)

STRATTERA® (trademark of Eli Lilly and Company)

TYVENSE® (lisdexamfetamine dimesylate)

UCERIS® (trademark of Santarus, Inc.)

VASCUGEL® (allogeneic aortic endothelial cells cultured in a porcine gelatin matrix [Gelfoam®] with cytokines, implanted)

VANCOCIN® (trademark of ANI Pharmaceuticals Inc.)

VENVANSE® (lisdexamfetamine dimesylate)

VPRIV® (velaglucerase alfa)

VYVANSE® (lisdexamfetamine dimesylate)

XAGRID® (anagrelide hydrochloride)

ZAVESCA® (trademark of Actelion Pharmaceuticals, Ltd.)

ZEFFIX® (trademark of GSK)

3TC® (trademark of GSK)

5

SHIRE PLC

2014 Form 10-K Annual Report

Table of contents

|

PART I

|

|||||

|

ITEM 1. BUSINESS

|

|||||

|

General

|

7

|

||||

|

Strategy

|

7

|

||||

|

Business model

|

7

|

||||

|

2014 highlights

|

8

|

||||

|

Financial information about operating segments

|

9

|

||||

|

Sales and marketing

|

9

|

||||

|

Manufacturing and distribution

|

24

|

||||

|

Intellectual property

|

25

|

||||

|

Competition

|

27

|

||||

|

Government regulation

|

29

|

||||

|

Third party reimbursement and pricing

|

30

|

||||

|

Responsibility

|

32

|

||||

|

Employees

|

32

|

||||

|

Available information

|

32

|

||||

|

ITEM 1A. RISK FACTORS

|

33

|

||||

|

ITEM 1B. UNRESOLVED STAFF COMMENTS

|

40

|

||||

|

ITEM 2. PROPERTIES

|

41

|

||||

|

ITEM 3. LEGAL PROCEEDINGS

|

42

|

||||

|

ITEM 4. MINE SAFETY DISCLOSURES

|

42

|

||||

|

PART II

|

|||||

|

ITEM 5. MARKET FOR THE REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

|

43

|

||||

|

ITEM 6. SELECTED FINANCIAL DATA

|

46

|

||||

|

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

|

48

|

||||

|

ITEM 7A. QUANTITATIVE AND QUALITATIVE DISCLOSURES ABOUT MARKET RISK

|

76

|

||||

|

ITEM 8. FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA

|

79

|

||||

|

ITEM 9. CHANGES IN AND DISAGREEMENTS WITH ACCOUNTANTS ON ACCOUNTING AND FINANCIAL DISCLOSURE

|

79

|

||||

|

ITEM 9A. CONTROLS AND PROCEDURES

|

79

|

||||

|

ITEM 9B. OTHER INFORMATION

|

80

|

||||

|

PART III

|

|||||

|

ITEM 10. DIRECTORS, EXECUTIVE OFFICERS AND CORPORATE GOVERNANCE

|

81

|

||||

|

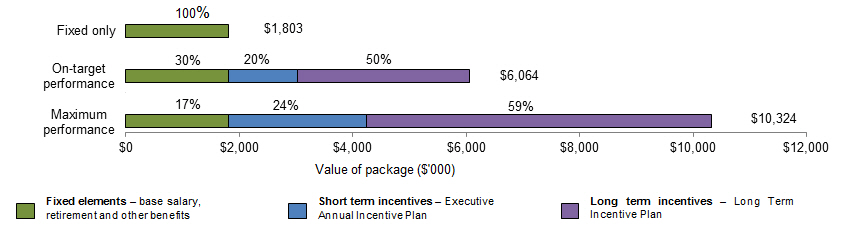

ITEM 11. EXECUTIVE COMPENSATION

|

86

|

||||

|

ITEM 12. SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT AND RELATED STOCKHOLDER MATTERS

|

117

|

||||

|

ITEM 13. CERTAIN RELATIONSHIPS AND RELATED TRANSACTIONS AND DIRECTOR INDEPENDENCE

|

118

|

||||

|

ITEM 14. PRINCIPAL ACCOUNTANT FEES AND SERVICES

|

118

|

||||

|

PART IV

|

|||||

|

ITEM 15. EXHIBITS AND FINANCIAL STATEMENT SCHEDULES

|

120

|

||||

6

PART I

ITEM 1: Business

General

Shire plc and its subsidiaries (collectively referred to as either “Shire”, or the “Company”) is a leading biopharmaceutical company that focuses on developing and marketing innovative medicines for patients with rare diseases and other specialty conditions.

The Company has grown both organically and through acquisition, completing a series of major transactions that have brought therapeutic, geographic and pipeline growth and diversification. The Company will continue to conduct its own research and development (“R&D”), focused on rare diseases, as well as evaluate companies, products and pipeline opportunities that offer a strategic fit and have the potential to deliver value to all of the Company’s stakeholders: patients, physicians, policy makers, payers, investors and employees.

Strategy

Shire’s purpose is to enable people with life altering conditions to lead better lives.

The Company aspires to become a leading global biotech delivering innovative medicines to patients with rare diseases and other specialty conditions. This is underpinned by four strategic drivers:

Growth:

|

|

·

|

Optimize In-Line assets via commercial excellence

|

|

|

·

|

Advance late-stage pipeline and launch new products

|

|

|

·

|

Accelerate growth through the acquisition of core / adjacent assets

|

Innovation:

|

|

·

|

Expand the Company’s rare disease expertise and offerings

|

|

|

·

|

Reinvest in R&D

|

|

|

·

|

Extend the Company’s portfolio to new indications and therapeutic areas

|

|

|

·

|

Collaborate globally to advance the Company’s scientific and commercial priorities

|

Efficiency:

|

|

·

|

Operate a lean and agile organization

|

|

|

·

|

Concentrate operations in Lexington, MA, US and Zug, Switzerland

|

|

|

·

|

Execute to a high standard by meeting milestones and delivering on the Company’s commitments

|

People:

|

|

·

|

Foster and reward a high performance culture

|

|

|

·

|

Attract, develop and retain the best talent

|

|

|

·

|

Live our values

|

Business model

In 2013 Shire integrated its operations into a simplified “One Shire” organization. The One Shire model has created a simple structure and a focused, efficient organization that is scalable for growth.

Shire has commercial units that focus exclusively on the commercial execution of its marketed products (the “In-Line” group) in the areas of Rare Diseases, Neuroscience, Gastrointestinal (“GI”) and Internal Medicine, and in Ophthalmics to support the development of Shire’s ophthalmic pipeline candidates. This ensures that the Company provides innovative treatments, and services the needs of its customers and patients, as efficiently as possible.

Shire has a single R&D organization (the “Pipeline” group), and early stage research is focused primarily on rare diseases. This single structure is designed to ensure Shire explores and develops opportunities built upon its core capabilities, priority commercial units and therapeutic areas, and also seeks to explore related and emerging areas.

7

Growth is also fuelled by the acquisition of new companies, in-licensing and new product development opportunities through R&D partnerships. Shire’s global corporate development team searches for new technologies, innovative products and strategic partnerships. The team engages in conversations with scientists and entrepreneurs on a global basis, while collaborating with commercial and R&D experts throughout the Company.

Shire’s support functions, including Technical Operations, are unified across the business to run as efficiently and effectively as possible to support the In-Line and Pipeline activities.

Shire leads its business through the Executive Committee, with support from its In-Line Committee and Pipeline Committee, which comprise senior management from across functions and commercial units to support the In-Line products and Pipeline activities. The Executive Committee is responsible for ensuring the appropriate allocation of resources and focused decision making across the enterprise in the best interests of Shire’s, patients, shareholders and other stakeholders.

2014 and Recent Highlights

See “Currently marketed products” and “Products under development” below for a full discussion of 2014 product, pipeline and business highlights, including:

Pipeline development:

|

|

·

|

the announcement that the US Food and Drug Administration (“FDA”) approved VYVANSE (lisdexamfetamine dimesylate) Capsules (CII), the first and only medication for the treatment of moderate to severe binge eating disorder (“BED”) in adults;

|

|

|

·

|

the announcement that the FDA has granted Fast Track designation for SHP609 (idursulfase-IT; also known as HGT-2310) for the treatment of neurocognitive decline associated with Hunter syndrome (mucopolysaccharidosis II or MPSII);

|

|

|

·

|

the announcement of the Company’s intention to submit a New Drug Application (“NDA”) for lifitegrast in the first quarter of 2015 as a treatment for the signs and symptoms of Dry Eye disease in adults;

|

|

|

·

|

the submission of an Investigational New Drug (“IND”) application for SHP607 for the prevention of retinopathy of prematurity (“ROP”) with the FDA. Shire further announced that it has received Fast Track designation from the FDA for SHP607;

|

|

|

·

|

the completion of two Phase 2 studies of SHP620 (maribavir) for the treatment of cytomegalovirus infection (“CMV”) in transplant patients. The results of the first study showed that maribavir, at all doses, was at least as effective as valganciclovir in the reduction of circulating CMV to below the limits of assay detection (undetectable plasma CMV) in the treatment of asymptomatic CMV viremia in transplant recipients. The second study showed that maribavir, at all doses, was effective at lowering CMV to below the limits of assay detection in patients with disease which is resistant or refractory to the standard of care CMV therapy (e.g., valganciclovir, foscarnet). Approximately two-thirds of patients across the maribavir treatment groups achieved an undetectable plasma CMV DNA (viral load) within six weeks. SHP620 has been granted orphan drug designation in both the US and EU;

|

|

|

·

|

the announcement of top-line results from two Phase 4 efficacy and safety studies of VYVANSE compared with CONCERTA (methylphenidate HCl). In SPD489-406, the forced-dose titration study, VYVANSE was found to be statistically superior to CONCERTA on the primary efficacy analysis. In SPD489-405, the dose optimization study, neither VYVANSE nor CONCERTA was found to be statistically superior to the other on the primary efficacy analysis, with a larger mean improvement found for VYVANSE than CONCERTA;

|

Geographical expansion:

|

·

|

the approval of a marketing authorization by the Ministry of Health, Labour and Welfare (“MHLW”) and subsequent launch for AGRYLIN (marketed as XAGRID in the EU) in Japan in adult essential thrombocythaemia patients;

|

|

|

·

|

the approval of a marketing authorization by the MHLW and subsequent launch of VPRIV in Japan, for the improvement of symptoms of Gaucher disease;

|

|

|

·

|

the acceptance of the submission of a Marketing Authorisation Application (“MAA”) by the European Medicines Agency (“EMA”) for INTUNIV the once-daily, non-stimulant guanfacine extended release for the treatment of Attention Deficit Hyperactivity Disorder (“ADHD”) in children/adolescents aged 6-17 years;

|

|

|

·

|

the announcement that ELVANSE received a positive response from the European Decentralised Procedure (“DCP”) in the three European countries participating in the procedure (UK, Denmark and Sweden);

|

Business development:

|

|

·

|

the acquisition of NPS Pharma on February 21, 2015 for a total cash consideration of approximately $5.2 billion. This acquisition added global rights to an innovative product portfolio with multiple growth catalysts, including, GATTEX/REVESTIVE with growing sales for the treatment of adults with Short Bowl Syndrome (“SBS”), a rare GI condition; and NATPARA/NATPAR, following its US approval on January 23, 2015, the only bioengineered hormone replacement therapy for use in the treatment of Hyperparathyroidism (“HPT”), a rare endocrine disease;

|

8

|

|

·

|

the acquisition of Lumena Pharmaceuticals, Inc. (“Lumena”) which added global rights to two late stage pipeline assets, SHP625 (formerly LUM001), in Phase 2 clinical development with four potential orphan indications; and SHP626 (formerly LUM002), ready to enter a Phase 1b multiple dose trial in the first half of 2015;

|

|

|

·

|

the acquisition of Fibrotech Therapeutics Pty Ltd. (“Fibrotech”) which added global rights of SHP627 (formerly FT011) in Phase 1b clinical development, a new class of oral drug with a novel mechanism of action which has the potential to address both the inflammatory and fibrotic components of disease processes. In addition Shire has acquired Fibrotech’s library of novel molecules including SHP628 (formerly FT061), which is in pre-clinical development;

|

|

·

|

the acquisition of BIKAM Pharmaceuticals Inc. (“BIKAM”) which added global rights to SHP630 (formerly BIK-406) in pre-clinical development, for the potential treatment of autosomal dominant retinitis pigmentosa (“adRP”);

|

|

|

·

|

the announcement of a worldwide licensing and collaboration agreement with ArmaGen Technologies, Inc. (“ArmaGen”) to develop and commercialize AGT-182, an investigational enzyme replacement therapy for the potential treatment of both the central nervous system and somatic manifestations in patients with Hunter syndrome;

|

|

|

·

|

the successful acquisition and integration of ViroPharma Inc. (“ViroPharma”) which added a marketed product for the prophylactic treatment of Hereditary Angioedema (“HAE”), CINRYZE, as well as a number of other marketed products and a pipeline of product candidates in the rare disease area.

|

Other developments:

|

|

·

|

the termination of AbbVie’s offer for Shire, pursuant to which AbbVie paid the break fee due under the cooperation agreement of approximately $1.635 billion;

|

|

|

·

|

the receipt of the assessments and subsequent settlement with the Canadian revenue authorities by which Shire’s Canadian subsidiary, Shire Canada Inc. received total cash repayments equivalent to $417 million;

|

|

|

·

|

the announcement that the US Supreme Court has granted Shire’s petition in the Shire v. Watson patent case regarding LIALDA. The granting of this petition by the Supreme Court vacates the decision of the US Court of Appeals for the Federal Circuit with respect to the claim construction in the case against Watson (now Actavis). For further information see ITEM 3: Legal Proceedings and Note 18, “Commitments and Contingencies, Legal and other proceedings” to the consolidated financial statements set forth in this Annual Report on Form 10-K;

|

|

|

·

|

the announcement related to patent infringement lawsuit regarding VYVANSE, that certain claims of the patents protecting VYVANSE were both infringed and valid. The Court’s summary judgment ruling concerning Shire’s motion included 18 patent claims from four of the FDA Orange Book-listed patents for VYVANSE, which cover VYVANSE’s active ingredient, the lisdexamfetamine dimesylate compound, and a method of using lisdexamfetamine dimesylate for the treatment of ADHD; and

|

|

|

·

|

the announcement that Shire reached final agreement on all matters with the US Government relating to a previously disclosed civil investigation of its US sales and marketing practices relating to ADDERALL XR, VYVANSE, DAYTRANA, LIALDA and PENTASA.

|

The Company comprises a single operating and reportable segment. This segment is engaged in the research, development, licensing, manufacturing, marketing, distribution and sale of innovative specialist medicines to meet significant unmet patient needs. Additional segment information is presented in Note 24 to the Company’s consolidated financial statements contained in ITEM 15: Exhibits and Financial Statement Schedules of this Annual Report on Form 10-K.

At December 31, 2014 the Company employed 2,151 (2013: 2,185) sales and marketing staff to service its operations throughout the world, including its major markets in North America, Europe, Latin America, and Asia Pacific.

9

Currently marketed products

The table below lists the Company’s main marketed products at December 31, 2014 indicating the owner/licensor, disease area and the key territories in which Shire markets the product.

|

Products

|

Disease area

|

Owner/licensor

|

Key territories

|

|

Treatments for Neuroscience

|

|||

|

VYVANSE/VENVANSE/

ELVANSE/TYVENSE/ELVANSE VUXEN/ADUVANZ (lisdexamfetamine dimesylate)

|

ADHD

|

Shire

|

US, Europe, Canada and Brazil (1)

|

|

ADDERALL XR (mixed salts of a single-entity amphetamine)

|

ADHD

|

Shire

|

US and Canada

|

|

INTUNIV (extended release guanfacine)

|

ADHD

|

Shire

|

US and Canada

|

|

EQUASYM (methylphenidate hydrochloride) modified release (XL)

|

ADHD

|

Shire

|

Europe

|

|

BUCCOLAM

|

Epilepsy

|

Shire

|

Europe

|

|

Treatments for gastrointestinal (“GI”) diseases

|

|||

|

LIALDA (mesalamine)/ MEZAVANT(mesalazine)

|

Ulcerative Colitis

|

Nogra SpA

|

US, Canada and Europe (2,3)

|

|

PENTASA (mesalamine)

|

Ulcerative Colitis

|

Shire

|

US

|

|

RESOLOR (prucalopride)

|

Chronic constipation in women

|

Shire

|

Europe

|

10

|

Treatments for Rare Diseases

|

|||

|

REPLAGAL (agalsidase alfa)

|

Fabry disease

|

Shire

|

Europe, Latin America and Asia Pacific(4)

|

|

ELAPRASE (idursulfase)

|

Hunter syndrome (Mucopolysaccharidosis Type II, MPS II)

|

Shire

|

Global(5)

|

|

VPRIV (velaglucerase alfa)

|

Gaucher disease, Type 1

|

Shire

|

Global

|

|

FIRAZYR (icatibant)

|

HAE

|

Shire

|

US, Europe and Latin America

|

|

CINRYZE C1 esterase inhibitor [human]

|

HAE

|

Shire

|

US, Europe and Latin America

|

|

Treatments for diseases in Other therapeutic areas

|

|||

|

FOSRENOL (lanthanum carbonate)

|

Hyperphosphatemia in end stage renal disease

|

Shire

|

US, Europe and Japan(2, 6)

|

|

XAGRID/ AGRYLIN (anagrelide hydrochloride)

|

Elevated platelet counts in at risk essential thrombocythemia patients

|

Shire

|

Europe and Japan (2)

|

|

PLENADREN (modified release hydrocortisone)

|

Indicated for treatment of adrenal insufficiency in adults

|

Shire

|

Europe

|

(1) Marketed in Brazil as VENVANSE and in the EU as ELVANSE or TYVENSE.

(2) Marketed by distributors in certain other markets.

(3) Marketed in the US as LIALDA and in Europe as MEZAVANT XL or MEZAVANT.

(4) Marketed in Japan under license by Dainippon Sumitomo Pharma Co., Ltd. (“DSP”).

(5) Marketed in Asia Pacific under license by Genzyme.

(6) Marketed in Japan under license by Bayer Yakuhin Limited (“Bayer”).

Treatments for Neuroscience

ADHD is a chronic neurobehavioral disorder that manifests as a persistent pattern of inattention and/or hyperactivity-impulsivity that is more frequent and severe than is typically observed in individuals at a comparable level of development. Although there is no cure for ADHD, there are accepted treatments that have been demonstrated to improve symptoms. Standard treatments include educational approaches, psychological therapies that may include behavior modification, and/or medication.

The worldwide prevalence of ADHD is estimated at 5.3% (Am J Psych. 2007). In the US, approximately 9.5% of all school-aged children (4-17 years old) have been diagnosed with ADHD at some point in their lives and two-thirds (66.3%) of those with a current ADHD diagnosis were taking medication (CDC, 2010). Over 50% of children may have symptoms that persist into adulthood. According to the results from the National Comorbidity Survey Replication (Am J Psychiatry, 2006), the disorder is estimated to affect 4.4% of US adults aged 18 to 44. The international ADHD market was approximately $903 million in 2013 (moving annual total (“MAT”) October 2013) and grew 10.0% to reach approximately $993 million in the same period in 2014.

According to IMS Health National Prescription Audit (“IMS NPA”), a leading global provider of business intelligence for the pharmaceutical and healthcare industries, the US ADHD market was valued at approximately $8.9 billion for the twelve months ended December 2014; this represents an increase of approximately 6.2% from the twelve months ended December 2013.

11

VYVANSE/ VENVANSE/ ELVANSE/ TYVENSE

VYVANSE is the first pro-drug stimulant for the treatment of ADHD, where the amino acid l-lysine is linked to d-amphetamine. VYVANSE is therapeutically inactive until metabolized in the body.

The FDA approved VYVANSE as a once-daily treatment for children aged 6 to 12 with ADHD in February 2007, for adults in April 2008 and for adolescents aged 13 to 17 in November 2010. In addition VYVANSE became the first drug in its class to be approved by the FDA for maintenance treatment, having been approved both as a maintenance treatment in adults with ADHD in January 2012, and as a maintenance treatment in pediatrics and adolescents aged 6 to 17 in April 2013. VYVANSE is available in the US in seven dosage strengths: 10mg, 20mg, 30mg, 40mg, 50mg, 60mg and 70mg.

VYVANSE was approved by Health Canada for the treatment of ADHD in pediatric patients aged 6 to 12 in February 2009, for adolescents and adults in November 2010, and was launched in Canada in January 2010 for pediatric patients and January 2011 for adolescents and adults.

VENVANSE was granted marketing authorization by ANVISA, the Brazilian health authority, for the treatment of ADHD in children aged 6-12, and launched in May 2011 and launched for adolescents and adults in November 2013.

ELVANSE/TYVENSE received a positive outcome from the European Decentralised Procedure in December 2012. ELVANSE is indicated as part of a comprehensive treatment program for ADHD in children 6 years of age and over when response to previous methylphenidate treatment is considered clinically inadequate. The product has received Marketing Authorization approvals and launched in eight countries (UK, Germany, Sweden, Spain, Norway, Finland, Denmark, and Ireland).

ELVANSE ADULT/ELVANSE VUXEN/ADUVANZ received a positive outcome from the European Decentralised Procedure in January 2015. ELVANSE ADULT is indicated as part of a comprehensive treatment programme for ADHD in adults taking into consideration the profile of the patient, including a thorough assessment of the severity and chronicity of the patient’s symptoms, the potential for abuse, misuse or diversion and clinical response to any previous pharmacotherapies for the treatment of ADHD. The product has received Marketing Authorization approval in the UK and Marketing Authorization for Sweden and Denmark is expected in the first quarter of 2015.

VYVANSE was also approved in January 2015 as the first and only treatment of moderate to severe BED. BED is defined as recurring episodes (more than once weekly), for at least 3 months, of consuming a large amount of food in a short time, compared with others. Patients feel a lack of control during a binge eating episode and marked distress over their eating. They typically experience shame and guilt, among other symptoms, about their binge eating and may conceal the symptoms. Unlike people with other eating disorders, adults with BED don’t routinely try to “undo” their excessive eating with extreme actions like purging or over-exercising. BED is the most common eating disorder in the US, affecting an estimated 2.8 million adults1 according to a national survey. BED occurs in both men and women and is more common than anorexia and bulimia combined. BED can occur in normal, overweight, and obese adults, and is seen across racial and ethnic groups.

Litigation proceedings relating to the Company’s VYVANSE patents are in progress. For further information see ITEM 3: Legal Proceedings and Note 18, “Commitments and Contingencies, Legal and other proceedings” to the consolidated financial statements set forth in this Annual Report on Form 10-K.

1 Crossrow N, Russo LJ, Ming EE,, Witt EA, Victor TW, Wadden TA. Poster, APA 167th Annual Meeting, New York, NY, May 3 – 7, 2014

ADDERALL XR

ADDERALL XR is an extended release treatment for ADHD, which uses MICROTROL drug delivery technology and is designed to provide once-daily dosing. It is available in 5mg, 10mg, 15mg, 20mg, 25mg and 30mg capsules.

The FDA approved ADDERALL XR as a once-daily treatment for children aged 6 to 12 with ADHD in October 2001, for adults in August 2004 and for adolescents aged 13 to 17 in July 2005.

Teva Pharmaceutical Industries, Ltd. (“Teva”) and Impax Laboratories, Inc. (“Impax”) commenced commercial shipment of their authorized generic versions of ADDERALL XR in April and October 2009, respectively. Shire currently receives royalties from Impax’s sales of authorized generic ADDERALL XR. Shire’s supply obligations to Impax ended September 30, 2014. Shire has extended its supply agreement with Teva until September 30, 2016. From the third quarter of 2012 Shire also started receiving royalties from Actavis’ sales of its generic version of ADDERALL XR. In December 2013, Shire entered into an agreement with Sandoz Inc. (“Sandoz”) whereby Shire will supply Sandoz with an authorized generic version of ADDERALL XR beginning July 1, 2016. From the December 1, 2013 effective date of the agreement through the end of the agreement’s five-year term, Sandoz has agreed to exclusively sell the authorized generic version of ADDERALL XR supplied by Shire. Shire will receive a royalty on Sandoz's sales of the product.

In June 2012 the FDA stated that it will require that all abbreviated new drug applications (“ANDAs”) for ADDERALL XR will have to establish bioequivalence using partial area under the curve measurements at multiple time points post-dosing and for both d- and l-amphetamine. The FDA response is consistent with recent decisions on other long-acting ADHD products.

Further information about litigation proceedings regarding ADDERALL XR can be found in ITEM 3: Legal Proceedings and Note 18, “Commitments and contingencies, Legal and other proceedings” to the consolidated financial statements set forth in this Annual Report on Form 10-K.

12

INTUNIV

INTUNIV is a selective alpha-2A receptor agonist indicated for the treatment of ADHD. Alpha-2A-adrenoceptors strengthen working memory networks by inhibiting cAMP-HCN channel signalling in the prefrontal cortex (Cell. 2007;129:397-410). INTUNIV is non-scheduled and has no known potential for abuse or dependence.

The FDA approved INTUNIV as a once-daily monotherapy treatment of ADHD in children and adolescents aged 6 to 17 and as adjunctive therapy to stimulants in February 2011. It is available in 1mg, 2mg, 3mg and 4mg tablets.

INTUNIV XR was approved by Health Canada as monotherapy for the treatment of ADHD in children aged 6 to 12 years and as adjunctive therapy to psychostimulants for the treatment of ADHD in children, aged 6 to 12 years, with a sub-optimal response to psychostimulants in July 2013 and was launched in Canada in November 2013.

In March 2014, the Company announced the acceptance of submission of a MAA by the EMA for once-daily, non-stimulant guanfacine extended release for the treatment of ADHD in children/adolescents aged 6-17 years.

In April 2013, Shire settled outstanding litigation with Actavis Inc. and certain of its respective affiliates (“Actavis”) and six other ANDA filers regarding their respective ANDAs for INTUNIV. The settlement provides Actavis with a license to make and market Actavis’ generic versions of INTUNIV in the United States for 180 days starting on December 1, 2014. Such sales require the payment of a royalty of 25% of gross profits to Shire during the 180 day period of Actavis’ exclusivity. The settlement also provides the other six ANDA filers with a license to make and market their respective generic versions of INTUNIV in the United States 181 days after Actavis’ launch of generic INTUNIV. Actavis launched a generic version of INTUNIV on December 1, 2014.

Further information about litigation proceedings regarding INTUNIV can be found in ITEM 3: Legal Proceedings and Note 18, “Commitments and contingencies, Legal and other proceedings” to the consolidated financial statements set forth in this Annual Report on Form 10-K.

EQUASYM

In March 2009, Shire acquired from UCB the worldwide rights (excluding US, Canada and Barbados) to EQUASYM immediate release and modified release (XL) preparations for the treatment of ADHD in children and adolescents aged 6 to 17. Shire is focusing exclusively on the XL form. At December 31, 2014 EQUASYM XL was commercially available in 10 countries in 10mg, 20mg and 30mg strengths. EQUASYM XL is marketed in Mexico and South Korea by Shire under the trade name METADATE CD.

Epilepsy disease state

Epilepsy is a chronic condition in which a person has a tendency to have recurrent seizures, normally diagnosed after 2 seizures3. Young children are most at risk because the developing brain is more prone to seizures than the mature brain. In Europe, approximately 6 million1 people are affected. An estimated 700,000 suffer2 from this condition between 3 months and less than 18 years of age. At least 30% of patients have inadequate seizure3 control, despite appropriate therapy. The aim of anti-epileptic drugs treatment is ‘seizure freedom’ – to prevent seizures. Prolonged, acute seizures are one of the most common neurological emergencies in children, which, if left untreated, can progress to status epilepticus, a condition that is associated with significant morbidity and mortality. Current estimates of case-fatality in childhood range between 2.7% and 5.2%4, but in those admitted to paediatric intensive care units it ranges between 5% and 8%. Early treatment of prolonged, acute seizures is important, as delayed medical intervention can affect outcomes and drug response. A prospective, population-based study in children demonstrated that for every minute of delay from the start of convulsive status epilepticus to arrival at hospital, there is a 5% cumulative increase in the risk of the seizure5 lasting longer than 60 minutes. Clinical guidelines outlining the treatment of prolonged seizures in children have been issued in several EU countries (UK, Belgium, Finland, France, Germany, Italy, Netherlands, and Sweden).

1 (ILAE/IBE/WHO Global Campaign Against Epilepsy 2010)

2 (Calculation from incidence rate, validated with Young Epilepsy)

3 (Kwan and Brodie 2000; Pellock 2007)

4 (Novorol CL, Chin RF, Scott RC. Outcome of convulsive status epilepticus: a review. Arch Dis Child 2007;92 (11):948–951)

5 (Chin RF, Neville BG, Peckham C, et al. Treatment of community-onset, childhood convulsive status epilepticus: a prospective, population based study. Lancet Neurol 2008;7 (8):696–703

BUCCOLAM

BUCCOLAM is the first and only licensed oromucosal midazolam solution for the treatment of prolonged, acute, convulsive seizures in infants, toddlers, children and adolescents (from 3 months to 18 years of age) designed to be used by care givers in out of hospital settings. BUCCOLAM must only be used by parents/care givers where the patient has been diagnosed to have epilepsy. For infants 3–6 months of age treatment should be in a hospital setting where monitoring is possible and resuscitation equipment is available. BUCCOLAM received a positive outcome from the European Union Centralised Procedure in June 2011 resulting in Marketing Authorization approvals in all EU member states. BUCCOLAM was the first Paediatric Use Marketing Authorisation (PUMA) to be approved in Europe (in September 2011). PUMA for BUCCOLAM provides doctors and pharmacists the opportunity to prescribe and dispense a product for children where the quality, safety, and efficacy have been independently assessed, transparently and publicly, and the product determined to be of appropriate quality and the benefit-risk favourable. Additionally, PUMA gives 8 years of data exclusivity plus an additional 2 years of marketing exclusivity to encourage the development of medicines for children. BUCCOLAM is launched and marketed in UK, Ireland, France, Nordics, Spain, Germany, Italy, Israel and Greece. BUCCOLAM is supplied in pre-filled, ready-to-use, unit-dose preparation, oral syringes.

13

Treatments for Ulcerative Colitis (“UC”)

UC was estimated to affect approximately 1.2 million patients in major markets (US and EU5) in 2010 according to Ulcerative Colitis: Decision Resources’ Market Forecast and Opportunity Analysis (May, 2012). UC is a serious chronic inflammatory disease of the colon in which part or all of the large intestine becomes inflamed and often ulcerated. Typically, patients go through periods of relapse and remission and can suffer from diarrhea, bleeding and abdominal pain. Once diagnosis is confirmed, patients are usually treated for life. The first line treatment for inflammatory bowel disease is mesalamine (5-aminosalicylic acid (“5-ASA”)) based products.

LIALDA/MEZAVANT

LIALDA is indicated in the US and Canada for the induction of remission in patients with mild to moderately active UC and for the maintenance of remission of UC. The addition of the indication for maintenance of remission of UC was approved by Health Canada in February 2011 and by the FDA in July 2011. LIALDA is the first and only FDA-approved once-daily oral formulation of mesalamine indicated for the induction and maintenance of remission. LIALDA contains the highest commercially available mesalamine dose per tablet (1.2g), so patients can take as few as two tablets once daily. In 2012, the FDA issued draft bioequivalence guidelines for orally-delivered delayed or extended-release mesalamine-based drugs (including LIALDA and PENTASA; see PENTASA section below).

LIALDA was approved by the FDA in January 2007 and was launched in the US in March 2007. Following approvals in other countries, at December 31, 2014, LIALDA/MEZAVANT was commercially available in 19 countries either directly or through distributor arrangements. LIALDA is marketed in certain territories outside the US by Shire under the trade name MEZAVANT and MEZAVANT XL.

Litigation proceedings relating to the Company’s LIALDA patents are in progress. For further information see ITEM 3: Legal Proceedings and Note 18, “Commitments and Contingencies, Legal and other proceedings” to the consolidated financial statements set forth in this Annual Report on Form 10-K.

PENTASA

PENTASA controlled release capsules are marketed by Shire in the US and are indicated for the induction of remission and for the treatment of patients with mild to moderately active UC.

PENTASA is an ethylcellulose-coated, controlled release capsule formulation designed to release therapeutic quantities of mesalamine throughout the gastrointestinal tract. PENTASA is available in the US in 250mg and 500mg capsules.

In September 2012, the FDA issued draft bioequivalence guidelines for generic approvals of orally-delivered delayed or extended-release mesalamine-based drugs (including LIALDA and PENTASA).

Treatments for chronic constipation

Chronic idiopathic constipation is a widespread and often debilitating disorder. The constipated patient population can be split into three distinct groups: (1) patients with primary constipation (without other underlying diseases or not caused by use of medication); (2) patients constipated as a result of regular use of medication such as opioids and (3) patients with severe constipation resulting from neurodegenerative disorders such as multiple sclerosis and Parkinson’s disease. Chronic constipation is characterized by infrequent and difficult passage of stool over a prolonged period. Other symptoms include infrequent bowel movements, bloating, straining, abdominal discomfort and pain, incomplete evacuation and unsuccessful attempts at evacuation. The disease has been clearly defined by the widely accepted Rome III criteria based on the type and duration of the symptoms. Chronic constipation is seen as a persistent disease with approximately 70% of patients having more than three symptom episodes per week.

RESOLOR

RESOLOR is the first of a new generation of selective, high-affinity 5-HT4 receptor agonists that stimulates gastrointestinal motility and acts primarily on different parts of the lower gastrointestinal tract (prokinetic).

In October 2009 RESOLOR was approved by the EMA throughout the EU as a once daily oral treatment for symptomatic treatment of chronic constipation in women in whom laxatives fail to provide adequate relief. In July 2010, Swissmedic granted RESOLOR marketing authorization in Switzerland for the treatment of idiopathic chronic constipation in adults for whom the currently available treatment options involving dietary measures and laxatives do not provide sufficient effect. RESOLOR is available in 1mg and 2mg dose strengths, both for once-daily dosing. As of December 31, 2014 RESOLOR was available in 18 EU countries.

On January 10, 2012 Shire announced that it had acquired the rights to develop and market RESOLOR in the US pursuant to an agreement with Janssen Pharmaceutica N.V., part of the J&J Group.

14

Treatments for Rare Diseases

A rare disease is a life-threatening or chronically debilitating condition affecting a limited number of patients. It is defined as rare in Europe when fewer than 5 in 10,000 people are affected, and in the US when fewer than 200,000 people are affected (Aronson J. Br J Clin Pharmacol 2006). Although rare diseases affect only a small number of people, collectively they impact millions of patients and their families. Globally, an estimated 350 million people – almost five percent of the world’s population – are living with a rare disease (Global Genes. Rare diseases: facts and statistics). There are approximately 7,000 rare diseases identified, of which 80% are genetic (Engel PA. Journal of Rare Disorders 2013 / Global Genes. Rare diseases: facts and statistics).

Compared to widespread conditions that strike hundreds of millions of people, rare diseases can lack similar levels of interest amongst the general public and medical/research communities (Shire Impact Report). Many people with a rare disease continue to experience low quality of life, high levels of disability, and may be at risk of early death due to delay in diagnosis or misdiagnosis (EURODIS. The voice of 12,000 patients). Effective treatments are available for only about 1% of rare diseases (Rollet P. Orphanet J Rare Dis 2013). These untreated diseases impose very high societal, emotional and economic costs.

REPLAGAL

REPLAGAL is marketed for the treatment of Fabry disease outside of the US. Fabry disease is a rare, inherited genetic disorder resulting from a deficiency in the activity of the lysosomal enzyme alpha-galactosidase A, which is involved in the breakdown of fats. Although the signs and symptoms of Fabry disease vary widely from patient to patient, the most common include severe pain of the extremities, impaired kidney function which often progresses to kidney failure, early heart disease, stroke and disabling gastrointestinal symptoms. The disease is estimated to affect 1 in 27,000 people (Spada et al, 2006).

REPLAGAL is a fully human alpha-galactosidase A protein made in human cells that replaces the deficient alpha-galactosidase A with an active enzyme to ameliorate certain clinical manifestations of Fabry disease.

In August 2001, REPLAGAL was granted marketing authorization in the EU. At December 31, 2014 REPLAGAL was approved in 46 countries excluding the US.

ELAPRASE

ELAPRASE is a treatment for Hunter syndrome (also known as Mucopolysaccharidosis Type II or MPS II). Hunter syndrome is a rare, inherited genetic disorder mainly affecting males that interferes with the body's ability to break down and recycle waste substances called mucopolysaccharides, also known as glycosaminoglycans or GAGs. In patients with Hunter syndrome, cumulative build-up of GAGs in cells throughout the body interferes with the way certain tissues and organs function, leading to severe clinical complications and early mortality. The disease is estimated to affect approximately 1 in 162,000 males (Meikle et al, 1999).

ELAPRASE was approved by the FDA in July 2006 and granted marketing authorization by the EMA in January 2007 for the long term treatment of patients with Hunter syndrome. ELAPRASE has been granted orphan drug exclusivity by both the FDA and the EMA. ELAPRASE also benefits from the 12 years of data exclusivity from the date of grant of registration given to innovator biologics in the US under the Patient Protection and Affordable Care Act (“PPACA” or “ACA”).

ELAPRASE received approval from the MHLW in Japan in October 2007. As part of an agreement with Genzyme, Genzyme manages the sales and distribution of ELAPRASE in Japan as well as certain other countries in the Asia Pacific region.

At December 31, 2014 ELAPRASE was approved in 51 countries.

VPRIV

VPRIV is a treatment for Type 1 Gaucher disease. Gaucher disease is a rare, inherited genetic disorder which results in a deficiency of the lysosomal enzyme beta-glucocerebrosidase. This enzymatic deficiency causes an accumulation of glucocerebroside, primarily in macrophages called Gaucher cells in the liver, spleen, bone marrow, and other organs. The accumulation of glucocerebrosidase in Gaucher cells in the liver and spleen leads to organomegaly. Presence of Gaucher cells in the bone marrow and spleen leads to clinically significant anemia and thrombocytopenia. The disease is estimated to affect 1 in 40,000 individuals, with a higher incidence in the Ashkenazi Jewish population (Sidransky et al, 2010, and National Gaucher Foundation).

VPRIV was approved by the FDA in February 2010 for the long term treatment of patients with Type 1 Gaucher disease. The EMA approved the marketing authorization for the use of VPRIV in August 2010. VPRIV has been granted orphan drug status in the EU with up to ten year’s market exclusivity from August 2010. VPRIV also benefits from the 12 years of data exclusivity in the US from the date of grant of registration given to innovator biologics under the ACA.

15

At December 31, 2014 VPRIV was approved in 40 countries.

FIRAZYR

FIRAZYR is a first-in-class peptide-based therapeutic developed for the symptomatic treatment of acute attacks of HAE. HAE is a debilitating and potentially life-threatening genetic disease characterized by unpredictable recurring swelling attacks in the hands, feet, face, larynx, or abdomen. The disease is estimated to affect approximately 1 in 50,000 individuals (Bowen et al, 2008).

In July 2008 the EMA granted marketing authorization throughout the EU for the use of FIRAZYR for the symptomatic treatment of acute attacks of HAE, and in May 2011 approved FIRAZYR for self-administration after training in subcutaneous injection technique by a healthcare professional. In August 2011 the FDA granted marketing approval for FIRAZYR in the US for treatment of acute attacks of HAE in adults aged 18 and older and, after injection training, patients may self-administer FIRAZYR. FIRAZYR has been granted orphan drug exclusivity by both the FDA and the EMA, providing it with up to 7 and 10 years market exclusivity in the US and EU, respectively, from the date of the grant of the relevant marketing authorization.

At December 31, 2014 FIRAZYR was approved in 38 countries.

CINRYZE

CINRYZE is a C1 esterase inhibitor therapy for routine prophylaxis against HAE, also known as C1 inhibitor (C1-INH) deficiency. CINRYZE is marketed and sold in the US for routine prophylaxis against HAE attacks in adolescent and adult patients with HAE. CINRYZE has been granted orphan drug exclusivity by the FDA, providing it with up to 7 years market exclusivity in the US from October 2008. CINRYZE also benefits from the 12 years of data exclusivity from the date of grant of registration given to innovator biologics in the US under the ACA from October 2008. In June 2011, marketing authorization in the EU was granted for CINRYZE in adults and adolescents with HAE for routine prevention, pre-procedure prevention and acute treatment of angioedema attacks. The approval also includes a self-administration option for appropriately trained patients.

At December 31, 2014 CINRYZE was approved in 36 countries.

Treatments for Other therapeutic areas

FOSRENOL

FOSRENOL is a phosphate binder that is indicated for use in patients with end-stage renal disease (stage 5) receiving dialysis and, from October 2009, is also indicated in the EU for the treatment of adult patients with Chronic kidney disease (“CKD”) who are not on dialysis with serum phosphate > 1.78 mmol/L (5.5 mg/dL) in which a low phosphate diet alone is insufficient to control serum phosphate levels. It is estimated that there are approximately 2 million patients worldwide with end-stage renal disease on dialysis (Nephrol Dial Transplant, 2005). In this condition the kidneys are unable to regulate the balance of phosphate in the body. If untreated, the blood phosphate levels can become elevated (hyperphosphatemia). The Kidney Disease Improving Global Outcomes (KDIGO) guidelines recommend that serum phosphate levels in CKD patients should be managed towards normal (Kidney International, 2009). FOSRENOL binds dietary phosphate in the gastrointestinal tract to prevent it from passing through the gut lining and, based upon this mechanism of action, phosphate absorption from the diet is decreased.

Formulated as a chewable tablet, FOSRENOL is available in 500mg, 750mg and 1,000mg dosage strengths. The FDA approved the 500mg dosage strength in 2004 and the 750mg and 1,000 mg dosage strengths were approved in 2005. In March 2009 FOSRENOL was launched in Japan. An oral powder formulation was approved and made available in certain European countries in 2012 and was approved in the US in 2014.

At December 31, 2014 FOSRENOL was approved in 48 countries.

XAGRID/ AGRYLIN

XAGRID is an orphan medicinal product which is marketed in Europe for the reduction of elevated platelet counts in at-risk ET patients. It was granted a marketing authorization in the EU in November 2004. In November 2014, the orphan exclusivity was extended for an additional two years to November 2016 under the EU Pediatric Regulation.

In the US, anagrelide hydrochloride is sold by the Company under the trade name AGRYLIN for the treatment of thrombocythemia secondary to a MPD. Generic versions of AGRYLIN have been available in the US market since 2005.

At December 31, 2014 XAGRID/AGRYLIN was approved in 47 countries.

16

PLENADREN

Adrenal insufficiency (AI) is a rare, chronic and potentially fatal endocrine disorder characterised by failure in the production of the hormone cortisol. AI affects less than 4.5 in 10,000 people in Europe1,2, but can lead to serious, life-threatening conditions such as cardiovascular, malignant or infectious diseases, as well as disorders which impact on health and quality of life. The many symptoms of AI include fatigue, anorexia, weight-loss, fever, muscle weakness, abdominal pains, dizziness and headaches. To survive, AI patients need replacement therapy with glucocorticoids (usually hydrocortisone) and because it is a chronic condition, they require this life-saving therapy throughout their lives3.

PLENADREN is indicated for the treatment of adrenal insufficiency in adults in the since 2011. It is a novel, once daily hydrocortisone, dual-release tablet, designed to better mimic the body's natural cortisol production compared to standard treatment. PLENADREN is proven to be effective and well tolerated compared to standard therapy, demonstrating a delivery of cortisol that is more in line with the body's own cortisol profile, thus avoiding the unphysiological cortisol peaks seen with standard glucocorticoid therapy. These peaks are thought to be associated with an increased risk of morbidity and premature mortality.

1 Laureti S, Vecchi L, Santeusanio F, Falorni A. Is the Prevalence of Addison's Disease Underestimated? J Clin Endocrinol Metab. 1999 May;84(5):1762.

2 Regal M, Páramo C, Sierra JM, García-Mayor RV. Prevalence and Incidence of Hypopituitarism in an Adult Caucasian Population in Northwestern Spain. Clin Endocrinol (Oxf). 2001;55:735–740

3 Arlt W, Allolio B. Adrenal insufficiency. Lancet. 2003 May 31;361(9372):1881-93.

17

Royalties received from other products

Antiviral products

The Company receives royalties on antiviral products based on certain of the Company’s patents licensed to GSK. These antiviral products are for Human Immunodeficiency Virus (“HIV”) and Hepatitis B virus. Royalty terms expired in most territories outside of the US during 2012. In the US, royalty terms expire between 2015 and 2018.

ADHD

ADDERALL XR

Shire receives royalties from Impax’s sales of its authorized generic version of ADDERALL XR. From the third quarter of 2012, Shire also started receiving royalties from Actavis’ sales of their generic version of ADDERALL XR.

INTUNIV

Commencing December 1, 2014 Shire is entitled to royalties from Actavis’ sales of its generic version of INTUNIV, for 180 days from launch. Such sales will require the payment of a royalty of 25% of gross profits to Shire during the 180 day period of Actavis’ exclusivity, which will be between December 1, 2014 and May 21, 2015.

Hyperphosphatemia

FOSRENOL

The Company licensed the rights to FOSRENOL in Japan to Bayer in December 2003. Bayer launched FOSRENOL in Japan in March 2009. Shire receives royalties from Bayer’s sales of FOSRENOL in Japan. The Company has also received milestone payments from Bayer based on the achievement of certain sales thresholds and may receive further milestone payments in the future if certain sales thresholds are achieved.

Other royalties

The Company has licensed the rights to certain other products to third parties and receives royalties on third party sales.

18

Products under development

The Company focuses its development resources on projects in a number of therapeutic areas, including rare diseases, neuroscience, ophthalmics, hematology and GI, and focuses its early development projects primarily on rare diseases. Total R&D expenditures (including impairment charges and depreciation) of $1,067.5 million, $933.4 million and $953.0 million were incurred in the years ended December 31, 2014, 2013 and 2012, respectively.

The table below lists the Company’s products in clinical development and registration as of December 31, 2014 by stage of development indicating the most advanced development status reached in major markets and the Company’s territorial rights in respect of each product candidate. If these product candidates are ultimately approved and marketed, they may benefit from patent and/or other forms of exclusivity, as described in more detail in the sections headed “Intellectual property” and “Government Regulation” in this ITEM 1. Some of the patents (or their analogous foreign patent applications or foreign granted patents) listed in the table on pages 25-26 of this ITEM 1 are potentially relevant to the corresponding development projects listed below. However as these product candidates remain in development and are subject to change as development progresses, the patents listed may not necessarily be representative of the scope of patent protection that may ultimately be available if each product candidate is approved and marketed.

|

Product

|

Disease area

|

Development status at December 31, 2014

|

The Company’s territorial rights

|

||

|

INTUNIV

|

ADHD in children and adolescents

|

Registration in EU (regulatory submission in Q1 2014)

|

Global

|

||

|

VYVANSE (lisdexamfetamine dimesylate)

|

BED in adults

|

Registration in US (regulatory submission in Q3 2014)

|

Global(1)

|

||

|

SHP606

|

Treatment of Dry Eye Disease (“DED”)

|

Phase 3 in US (entered Phase 3 in Q4 2012)

|

Global

|

||

|

SHP465

|

Treatment of ADHD in adults

|

Phase 3 in US (originally entered Phase 3 in 2005)

|

US

|

||

|

FIRAZYR

|

ACE inhibitor-induced Angioedema (“ACE-1 AE”)

|

Phase 3 in US (entered Phase 3 in Q4 2013)

|

Global

|

||

|

FIRAZYR

|

HAE

|

Phase 3-ready in Japan (entered Phase 3 in Q1 2015)

|

Global

|

||

|

SHP555 (prucalopride)

|

Chronic constipation in Males

|

Phase 3 in EU (entered Phase 3 in Q4 2010)

Phase 3-ready in US

|

US and EU

|

||

|

INTUNIV

|

ADHD in children and adolescents

|

Phase 3 in Japan (entered Phase 3 in Q2 2013)

|

Global(2)

|

||

|

SHP616 (CINRYZE)

|

Prophylaxis and acute treatment of angioedema

|

Phase 3-ready in Japan

|

US, EU and Japan

|

||

|

LDX (lisdexamfetamine dimesylate)

|

ADHD in children and adolescents

|

Phase 2 in Japan

|

Global(2)

|

||

|

SHP602

|

Chronic Iron-overload

(on clinical hold)

|

Phase 2

|

Global

|

||

|

SHP607

|

Retinopathy of Prematurity (“ROP”)

|

Phase 2

|

Global

|

||

|

SHP609

|

Hunter syndrome with

CNS symptoms

|

Phase 2/3

|

Global (3)

|

19

|

SHP610

|

Sanfilippo A Syndrome (MPS IIIA)

|

Phase 2b

|

Global(3)

|

||

|

SHP620

|

Treatment of cytomegalovirus infection (“CMV”) in transplant patients

|

Phase 2

|

Global

|

||

|

SHP625 (formerly LUM001)

|

Treatment of cholestatic liver diseases

|

Phase 2

|

US and EU

|

||

|

SHP611

|

Metachromatic Leukodystrophy (“MLD”)

|

Phase 1/2

|

Global

|

||

|

SHP616 (CINRYZE SC)

|

Routine prophylaxis against HAE attacks in adolescent and adult patients by sub-cutaneous injection

|

Phase 1

|

Global

|

||

|

SHP616 (CINRYZE-life cycle management and new uses)

|

Acute Neuromyelitis Optica (“NMO”), and Paroxysmal Nocturnal Hemoglobinuria (“PNH”),

|

Phase 1

|

Global

|

||

|

SHP616 (CINRYZE-life cycle management and new uses)

|

Acute Antibody Mediated Rejection (“AMR”)

|

Phase 2

|

Global

|

||

|

SHP622 (formerly VP 20629)

|

Treatment of Friedreich’s Ataxia (“FA”)

|

Phase 1

|

Global

|

||

|

SHP626 (formerly LUM002)

|

Treatment of nonalcoholic steatohepatitis (“NASH”)

|

Phase 1

|

Global

|

||

|

SHP627(formerly FT001)

|

Focal Segmental Glomerulosclerosis

|

Phase 1b

|

Global

|

|

|

(1)

|

FDA approval obtained on January 30, 2015.

|

|

|

(2)

|

Under co-development with Shionogi in Japan as a result of a license and collaboration agreement.

|

|

|

(3)

|

Genzyme has rights to manage marketing and distribution in Japan and certain other Asia Pacific countries under a license with Shire.

|

Products in registration as at December 31, 2014

INTUNIV for the treatment of ADHD in the EU

In March 2014, the Company announced the acceptance of submission of an MAA by the EMA for once-daily, non-stimulant guanfacine extended release for the treatment of ADHD in children/adolescents aged 6-17 years.

VYVANSE for the treatment of BED

In November 2013, the Company reported positive top-line results from two identically designed randomized placebo-controlled Phase 3 studies evaluating the efficacy and safety of VYVANSE versus placebo in adults with BED. In both studies VYVANSE was found to be statistically superior to placebo on the primary efficacy analysis (p-value <0.001) of the change from baseline at weeks 11 to 12 in terms of number of binge days per week. The safety for VYVANSE in these two studies appears to be generally consistent with the known profile established in studies in adults with ADHD. On September 15, 2014, Shire announced that the FDA had accepted for filing with priority review a sNDA for VYVANSE as a treatment for adults with BED. On January 30, 2015 the FDA approved VYVANSE for the treatment of moderate to severe BED in adults.

20

Products in clinical development as at December 31, 2014

Phase 3 and Phase 3-ready

SHP606 (lifitegrast) for the treatment of DED

Following a meeting with the FDA, on May 16, 2014 Shire announced that it intends to submit an NDA for SHP606 in the first quarter of 2015 as a treatment for the signs and symptoms of DED in adults. In parallel to preparing for the NDA submission, Shire is conducting a Phase 3 safety and efficacy study (OPUS-3) in support of a potential US label and labels in international markets. OPUS-3 is a multicenter, randomized, double-masked, placebo-controlled, parallel arm study with a 14 day open-label placebo screening run-in period followed by a 12 week randomized, masked treatment period with a primary efficacy endpoint in subjective patient reported symptoms of dry eye disease, eye dryness score.

On April 30, 2014 Shire announced top-line results from the prospective, randomized, double-masked, placebo-controlled SONATA trial which indicated no ocular or drug-related serious adverse events. The safety data indicated in the SONATA trial was entirely consistent with that observed in the Phase 2, OPUS-1 and OPUS-2 studies for lifitegrast. Additional data and analyses will be submitted for presentation at upcoming medical meetings.

SHP465 for the treatment of ADHD in adults

Shire’s NDA for SHP465 was previously submitted in 2006 to support the use of SHP465 as a longer-acting, once-daily treatment for ADHD in adults. With the growing adult ADHD population there is now a larger patient population and Shire expects a greater commercial need for this type of product than in 2006. SHP465 (mixed salts of a single entity amphetamine) capsules provide an extended-release of amphetamines to provide coverage of ADHD symptoms for adults throughout the day. On October 9, 2014 Shire announced that it had received further guidance from the FDA on the regulatory path for SHP465. After a series of follow-up discussions, the FDA has now clarified that additional pediatric data would be required for resubmission of SHP465.

FIRAZYR for the treatment of ACE-I AE

A Phase 3 clinical trial to assess the efficacy of FIRAZYR for the treatment of ACE-I AE was initiated in the fourth quarter of 2013 and is ongoing.

FIRAZYR for the treatment of HAE in Japan

Shire plans to initiate a Phase 3 trial to evaluate the efficacy and safety of FIRAZYR for the treatment of HAE in Japanese patients in 2015.

SHP555 (prucalopride; marketed as RESOLOR in the EU) for the treatment of chronic constipation in the US

On January 10, 2012, Shire announced that it had acquired the rights to develop and market prucalopride in the US in an agreement with Janssen Pharmaceutica N.V. Discussions have been conducted with the FDA and an NDA submission pathway has been agreed. Planning is underway to confirm Phase 3 program activities and timelines.

INTUNIV for the treatment of ADHD in Japan

Under a collaboration agreement, Shionogi and Shire will co-develop and sell treatments for ADHD in Japan, including INTUNIV. A Phase 3 clinical program to evaluate the efficacy and safety of INTUNIV in Japanese patients aged 6 to 17 was initiated in the second quarter of 2013.

SHP616 (CINRYZE) for routine prophylaxis against HAE attacks in adolescent and adult patients in Japan

CINRYZE is indicated in the US for prophylaxis and in the EU for both prophylaxis and acute treatment of angioedema attacks in adolescent and adult patients with HAE. Based on feedback from the Pharmaceutical and Medical Devices Agency (“PMDA”), a Clinical Trial Notification (“CTN”) was resubmitted and approved on October 2, 2014. The Company plans to initiate a Phase 3 trial in the first quarter of 2015.

Phase 2

LDX1 for the treatment of ADHD in Japan

Under a collaboration agreement, Shionogi and Shire will co-develop and sell ADHD products in Japan, including LDX. A Phase 2 clinical program to evaluate the efficacy and safety of LDX in Japanese patients aged 6 to 17 was initiated in the second quarter of 2013 and is ongoing.

|

1.

|

Currently marketed as VYVANSE in the US and ELVANSE in certain countries in the EU for the treatment of ADHD.

|

21

SHP602 iron chelating agent for the treatment of iron overload secondary to chronic transfusion

A Phase 2 trial in pediatric and adult patients with transfusion iron overload is currently on clinical hold as Shire evaluates nonclinical toxicology findings. The potential relevance of these findings to humans, if any, is unknown. This product has received orphan drug designation in both the US and EU for the treatment of chronic iron overload requiring chelation therapy.

SHP607 for the prevention of ROP

SHP607 is in development as a protein replacement therapy for the preventative treatment of ROP, a rare eye disorder associated with premature birth. In December 2014 Shire received notification that SHP607 was granted Fast Track designation by the FDA. In addition, this product has been granted orphan drug designation in both the US and EU. A Phase 2 clinical trial is currently ongoing.

SHP609 for the treatment of Hunter syndrome with CNS symptoms

SHP609 is in development as an enzyme replacement therapy (“ERT”) delivered intrathecally for Hunter syndrome patients with cognitive impairment. In January 2015 the FDA granted SHP609 Fast Track designation. In addition, this product has been granted orphan designation in the US. The Company initiated a pivotal Phase 2/3 clinical trial in the fourth quarter of 2013 which is ongoing.

SHP610 for Sanfilippo A syndrome (Mucopolysaccharidosis IIIA)

SHP610 is in development as an ERT delivered intrathecally for the treatment of Sanfilippo A syndrome, a Lysosomal Storage Disorder. The Company initiated a Phase 1/2 clinical trial in August 2010 which has now completed. Shire initiated a Phase 2b clinical trial for SHP610, which is designed to establish clinical proof of concept. The product has been granted orphan drug designation in the US and in the EU.

SHP620 (maribavir) for the treatment of CMV in transplant patients

SHP620 was acquired as part of the acquisition of ViroPharma on January 24, 2014. Shire has completed two Phase 2 studies in transplant recipients. The first trial was in first-line treatment of asymptomatic CMV viremia in transplant recipients and the results of this study showed that maribavir, at all doses, was at least as effective as valganciclovir in the reduction of circulating CMV to below the limits of assay detection (undetectable plasma CMV). The second study recently completed was for the treatment of resistant/refractory CMV infection/disease in transplant recipients. The purpose of this study was to determine whether maribavir is efficacious and safe in patients with disease which is resistant or refractory to the standard of care CMV therapy (e.g., valganciclovir, foscarnet). This study also showed that maribavir, at all doses, was effective at lowering CMV to below the limits of assay detection. Approximately two-thirds of patients across the maribavir treatment groups achieved an undetectable plasma CMV DNA (viral load) within 6 weeks. This product has been granted orphan drug designation in both the US and EU.

SHP625 (formerly LUM001) for the treatment of cholestatic liver disease

SHP625 was acquired as part of the recent acquisition of Lumena. Shire is currently conducting Phase 2 studies in the following indications: Alagille Syndrome, Progressive Familial Intrahepatic Cholestasis, Primary Biliary Cirrhosis, and Primary Sclerosing Cholangitis. This product has been granted orphan drug designation both in the US and EU.

SHP616 (CINRYZE) for the treatment of AMR

A Phase 2 study for the treatment of AMR with SHP616 was completed in 18 patients. Shire has received FDA feedback and Shire plans to initiate a Phase 2/3 study in 2015.

Phase 1

SHP611 for the treatment of MLD