UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| [X] | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended September 30, 2016

| [ ] | Transition report under Section 13 or 15(d) of the Securities Exchange Act of 1934 |

Commission file number: 001-13992

RCI HOSPITALITY HOLDINGS, INC.

(Exact name of registrant as specified in its charter)

Texas

State or other jurisdiction of (I.R.S. Employer incorporation or organization Identification No.)

10737 Cutten Road, Houston, Texas 77066

(Address of principal executive offices)

(281) 397-6730

Registrant’s telephone number, including area code

Securities registered pursuant to Section 12(b) of the Act:

Common Stock, $0.01 Par Value

(Title of class)

NASDAQ Stock Market LLC

Name of each exchange on which registered

Securities registered pursuant to section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes [ ] No [X]

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes [ ] No [X]

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes [X] No [ ]

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes [X] No [ ]

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K [X]

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. Large accelerated filer [ ] Accelerated filer [X] Non-accelerated filer [ ] Smaller reporting company [ ]

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.): Yes [ ] No [X]

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold as of the last business day of the registrant’s most recently completed second fiscal quarter was $80,889,036.

As of December 1, 2016, there were approximately 9,740,127 shares of common stock outstanding.

NOTE ABOUT FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. These statements include, among other things, statements regarding plans, objectives, goals, strategies, future events or performance and underlying assumptions and other statements, which are other than statements of historical facts. Forward-looking statements may appear throughout this report, including without limitation, the following sections: Item 1 – “Business,” Item 1A – “Risk Factors,” and Item 7 – “Management’s Discussion and Analysis of Financial Condition and Results of Operations.” Forward-looking statements generally can be identified by words such as “anticipates,” “believes,” “estimates,” “expects,” “intends,” “plans,” “predicts,” “projects,” “will be,” “will continue,” “will likely result,” and similar expressions. These forward-looking statements are based on current expectations and assumptions that are subject to risks and uncertainties, which could cause our actual results to differ materially from those reflected in the forward-looking statements. Factors that could cause or contribute to such differences include, but are not limited to, those discussed in this Annual Report on Form 10-K, and, in particular, the risks discussed under the caption “Risk Factors” in Item 1A and those discussed in other documents we file with the Securities and Exchange Commission (“SEC”). Important factors that in our view could cause material adverse effects on our financial condition and results of operations include, but are not limited to, the risks and uncertainties associated with operating and managing an adult business, the business climates in cities where it operates, the success or lack thereof in launching and building the company’s businesses, risks and uncertainties related to cyber security, conditions relevant to real estate transactions, and numerous other factors such as laws governing the operation of adult entertainment businesses, competition and dependence on key personnel. We undertake no obligation to revise or publicly release the results of any revision to any forward-looking statements, except as required by law. Given these risks and uncertainties, readers are cautioned not to place undue reliance on such forward-looking statements.

| 2 |

TABLE OF CONTENTS

| 3 |

INTRODUCTION

RCI Hospitality Holdings, Inc. (sometimes referred to as RCIHH herein) is a holding company engaged in a number of activities in the hospitality and related businesses. All services and management operations are conducted by subsidiaries of RCIHH, including RCI Management Services, Inc.

Through our subsidiaries, as of November 30, 2016, we operated a total of 41 establishments that offer live adult entertainment, and/or restaurant and bar operations. We also operated a leading business communications company (the “Media Group”) serving the multi-billion-dollar adult nightclubs industry. We have two principal reportable segments: nightclubs and Bombshells restaurants and bars. In the context of club and restaurant/sports bar operations, the terms the “Company,” “we,” “our,” “us” and similar terms used in this Form 10-K refer to subsidiaries of RCIHH. Excepting executive officers of RCIHH, any employment referenced in this document is not with RCIHH but solely with one of its subsidiaries. RCIHH was incorporated in the State of Texas in 1994.

Our fiscal year ends on September 30. References to years 2016, 2015 and 2014 are for fiscal years ended September 30, 2016, 2015 and 2014, respectively. Our fiscal quarters chronologically end on December 31, March 31, June 30 and September 30.

Our website address is www.rcihospitality.com. Upon written request, we make available free of charge our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, and all amendments to those reports as soon as reasonably practicable after such material is electronically filed with the SEC under the Securities Exchange Act of 1934, as amended. Information contained in the website shall not be construed as part of this Form 10-K.

OUR BUSINESS

We operate several businesses. We aggregate our businesses into two principal reportable segments – nightclubs and Bombshells restaurants/sports bars, and combine other operating segments into “Other” which primarily includes the operations of our Media Group and Drink Robust.

Nightclubs

We operate our nightclubs through the following brands that target many different demographics of customers by providing a unique, quality entertainment environment:

| ● | “Rick’s Cabaret” – Elegant clubs with restaurants; | |

| ● | “Vivid Cabaret” – High-end high-energy club for young professionals; | |

| ● | “Tootsie’s Cabaret” – Nation’s largest mega club with 74,000 square feet; | |

| ● | “Club Onyx” – High-end clubs for African-American professionals; | |

| ● | “Jaguars Club” and “XTC Cabaret” – Lively BYOB clubs for blue collar patrons and the college crowd; | |

| ● | Other nightclub brands include “Hoops Cabaret,” “Downtown Cabaret,” “Temptations,” “Silver City Cabaret,” “Foxy’s Cabaret,” “Cabaret East,” and “The Seville.” |

| 4 |

Our Company has received a significant amount of media exposure over the years in national magazines such as Playboy, Penthouse, Glamour Magazine, The Ladies Home Journal, Time Magazine, Time Out New York, and Texas Monthly Magazine. Segments about RCIHH have aired on national and local television programs such as “20/20,” “Extra” and “Inside Edition,” and we have provided entertainers for pay-per-view features as well. Business stories about RCI Hospitality Holdings, Inc. have appeared in Forbes, Newsweek, The Wall Street Journal, The New York Times, The New York Post, Los Angeles Times, Houston Business Journal, and numerous other national and regional publications. RCI Hospitality Holdings, Inc. has been profiled in The Wall Street Journal, Fortune, MarketWatch, Corporate Board Member, Smart Money, USA Today, The New York Daily News and other publications.

Refer to Item 2 – “Properties” for a listing of all our nightclubs and their locations.

Restaurants/Sports Bars

As of September 30, 2016, we operated four restaurants/sports bar as “Bombshells” in Dallas, Austin and Houston, Texas. In 2015, our subsidiary, BMB Franchising Services, Inc. (“BMB”), announced that it was beginning a nationwide franchising program for Bombshells. As of March 2016, BMB has received approval to sell franchises in all 50 states. The restaurant sets itself apart with décor that pays homage to all branches of the U.S. military. Locations feature local DJs, large outdoor patios, and more than 75 state of the art flat screen TVs for watching your favorite sports. All food and drink menu items have military names. Bombshell Girls, with their military-inspired uniforms, are a key attraction. Their mission, in addition to waitressing, is to interact with guests and generate a fun atmosphere.

We opened the first Bombshells in March 2013 in Dallas, quickly becoming one of the most popular restaurant destinations in the area. Within a year, four more opened in the Austin and Houston, Texas areas. Of the five, three are freestanding pad sites and two are inline locations. In September 2016, we closed one Bombshells location in Webster, Texas. In addition, we currently operate a bar in Fort Worth, Texas as Vee Lounge (reconcepted in October 2016 as Studio 80).

Media Group

The Media Group, made up of wholly owned subsidiaries, is the leading business communications company serving the multi-billion-dollar adult nightclubs industry. It owns a national industry convention and tradeshow; two national industry trade publications; two national industry award shows; and more than 25 industry websites. Included in the Media Group is ED Publications, publishers of the bimonthly ED Club Bulletin, the only national business magazine serving the 3,500-plus adult nightclubs in North America, which have annual revenues in excess of $5 billion, according to the Association of Club Executives. ED Publications, founded in 1991, also publishes the Annual VIP Guide of adult nightclubs, touring entertainers and industry vendors; produces the Annual Gentlemen’s Club Owners EXPO, a national convention and tradeshow; and offers the exclusive ED VIP Club Card, honored at more than 850 adult nightclubs. Also in the Media Group is Storerotica, founded in 2004, which publishes the bimonthly Storerotica Magazine, the industry trade publication for the multi-billion-dollar erotic apparel and adult novelty retail sales industries. The Media Group produces two nationally recognized industry award shows for the readers of both ED Club Bulletin and Storerotica magazines, and maintains a number of B-to-B and consumer websites for both industries.

Energy Drinks

In October 2014, we acquired 51% of a company with exclusive distribution rights to Robust brand energy drinks in North America. Robust targets the on-premises bar and mixer market in eight states. The company’s exclusive rights are for 10 years, with rights to renew, with Sun Mark Limited of the UK, which has been manufacturing and distributing the drink under the Bullet brand there since 2008. Robust comes in standard 8.4-ounce energy drink cans and in four flavors: regular, sugar free, cranberry and lemon mint, which mixes particularly well with whiskey and tequila.

In September 2016, we sold a 31% interest in Robust to its former owner for a $2.0 million note from him, retaining a 20% interest in the business. We recorded a $641,000 gain on the sale, including deferred tax credits released on the sale of the business, and recognized an impairment charge of $825,000 on the residual interest owned. Beginning as of the date of sale, we have begun to account for Robust as a cost method investment as we do not have significant influence.

| 5 |

OUR STRATEGY

Our overall objective is to create value for our shareholders by developing and operating profitable businesses in the hospitality and related space. We strive to achieve that by providing an attractive price-value entertainment and dining experience; by attracting and retaining quality personnel; and by focusing on unit-level operating performance. Aside from our operating strategy, we employ a capital allocation strategy.

Capital Allocation Strategy

Our capital allocation strategy provides us with disciplined guidelines on how we should use our free cash flows; provided, however, that we may deviate from this strategy if the circumstances warrant. We calculate free cash flow as net cash flows from operating activities minus maintenance capital expenditures. Using the after-tax yield of buying our own stock, or other strategic rationale in management’s opinion, as baseline, we believe we are able to make better investment decisions.

Based on our capital allocation strategy:

| ● | We believe that buying back our own stock provides risk-free returns on our free cash flows since we are buying our own assets that we know very well; | |

| ● | We consider acquiring or developing our own clubs or restaurants that we believe have the potential to provide two times the after-tax yield of buying our own stock, absent an otherwise strategic rationale; | |

| ● | We consider paying down our debt when our stock price increases to a level where the after-tax yield of buying back our own stock is equal or lower than the after-tax yield of paying down our debt. |

COMPETITION

The adult entertainment and the restaurant/sports bar businesses are highly competitive with respect to price, service and location. All of our nightclubs compete with a number of locally owned adult clubs, some of whose brands may have name recognition that equals that of ours. The names “Rick’s” and “Rick’s Cabaret,” “Tootsie’s Cabaret,” “XTC Cabaret,” “Silver City,” “Club Onyx,” “Downtown Cabaret,” “Temptations,” “The Seville,” “Jaguars,” “Hoops Cabaret,” and “Foxy’s Cabaret” are proprietary. In the restaurant/sports bar business, “Bombshells” is also proprietary. We believe that the combination of our existing brand name recognition and the distinctive entertainment environment that we have created will allow us to compete effectively in the industry and within the cities where we operate. Although we believe that we are well positioned to compete successfully, there can be no assurance that we will be able to maintain our high level of name recognition and prestige within the marketplace.

GOVERNMENTAL REGULATIONS

We are subject to various federal, state and local laws affecting our business activities. Particularly in Texas, the authority to issue a permit to sell alcoholic beverages is governed by the Texas Alcoholic Beverage Commission (“TABC”), which has the authority, in its discretion, to issue the appropriate permits. We presently hold a Mixed Beverage Permit and a Late Hour Permit at numerous Texas locations. Minnesota, North Carolina, Indiana, Louisiana, Arizona, Pennsylvania, Florida, and New York have similar laws that may limit the availability of a permit to sell alcoholic beverages or that may provide for suspension or revocation of a permit to sell alcoholic beverages in certain circumstances. It is our policy, prior to expanding into any new market, to take steps to ensure compliance with all licensing and regulatory requirements for the sale of alcoholic beverages as well as the sale of food.

| 6 |

In addition to various regulatory requirements affecting the sale of alcoholic beverages, in many cities where we operate, the location of an adult entertainment cabaret is subject to restriction by city, county or other governmental ordinance. The prohibitions deal generally with distance from schools, churches, and other sexually oriented businesses and contain restrictions based on the percentage of residences within the immediate vicinity of the sexually oriented business. The granting of a sexually oriented business permit is not subject to discretion; the permit must be granted if the proposed operation satisfies the requirements of the ordinance. In all states where we operate, management believes we are in compliance with applicable city, county, state or other local laws governing the sale of alcohol and sexually oriented businesses.

TRADEMARKS

Our rights to the trade names “RCI Hospitality Holdings, Inc.,” “Rick’s,” “Rick’s Cabaret,” “Tootsie’s Cabaret,” “Club Onyx,” “XTC Cabaret,” “Temptations,” “Jaguars,” “Downtown Cabaret,” “Cabaret East,” “Bombshells Restaurant & Bar,” “Vee Lounge,” “The Seville Club,” “Down In Texas Saloon,” “Silver City Cabaret,” and “Exotic Dancer” are established under common law based upon our substantial and continuous use of these trade names in interstate commerce, some of which have been in use at least as early as 1987. We have registered our service mark, “RICK’S AND STARS DESIGN,” and the “BOMBSHELLS RESTAURANT & BAR” logo design with the United States Patent and Trademark Office. We have also obtained service mark registrations from the Patent and Trademark Office for the “RCI HOSPITALITY HOLDINGS, INC.,” “RICK’S,” “RICK’S CABARET,” “CLUB ONYX,” “XTC CABARET,” “SILVER CITY CABARET,” “BOMBSHELLS RESTAURANT & BAR,” “THE SEVILLE CLUB,” “DOWN IN TEXAS SALOON,” and “EXOTIC DANCER” service marks. As of this date, we have pending registration applications for the names “CLUB DULCE,” “FOXY’S CABARET,” and “HOOPS CABARET.” We also own the rights to numerous trade names associated with our media division. There can be no assurance that the steps we have taken to protect our service marks will be adequate to deter misappropriation.

EMPLOYEES AND INDEPENDENT CONTRACTORS

As of September 30, 2016, we had approximately 2,000 employees, of which approximately 160 are in management positions, including corporate and administrative operations, and approximately 1,840 are engaged in entertainment, food and beverage service, including bartenders, waitresses, and certain entertainers. None of our employees are represented by a union. We consider our employee relations to be good. Additionally, as of September 30, 2016, we had independent contractor entertainers, who are self-employed and conduct business at our locations on a non-exclusive basis. Our entertainers at Rick’s Cabaret in Minneapolis, Minnesota act as commissioned employees. Also, as of October 2016, our entertainers at Jaguars Club in Phoenix, Arizona are now classified as commissioned employees. All employees and independent contractors sign arbitration non-class action participation agreements.

We believe that the adult entertainment industry standard of treating entertainers as independent contractors provides us with safe harbor protection to preclude payroll tax assessment for prior years. We have prepared plans that we believe will protect our profitability in the event that the sexually oriented business industry is required in all states to convert entertainers, who are now independent contractors, into employees. See related discussion in “Risk Factors.”

| 7 |

An investment in our common stock involves a high degree of risk. You should carefully consider the risks described below before deciding to purchase shares of our common stock. If any of the events, contingencies, circumstances or conditions described in the risks below actually occurs, our business, financial condition or results of operations could be seriously harmed. The trading price of our common stock could, in turn, decline and you could lose all or part of your investment.

Our business operations are subject to regulatory uncertainties which may affect our ability to continue operations of existing nightclubs, acquire additional nightclubs, or be profitable.

Adult entertainment nightclubs are subject to local, state and federal regulations. Our business is regulated by local zoning, local and state liquor licensing, local ordinances, and state and federal time place and manner restrictions. The adult entertainment provided by our nightclubs has elements of speech and expression and, therefore, enjoys some protection under the First Amendment to the United States Constitution. However, the protection is limited to the expression, and not the conduct of an entertainer. While our nightclubs are generally well established in their respective markets, there can be no assurance that local, state and/or federal licensing and other regulations will permit our nightclubs to remain in operation or profitable in the future.

Our business has been, and may continue to be, adversely affected by conditions in the U.S. financial markets and economic conditions generally.

Our nightclubs are often acquired with a purchase price based on historical EBITDA (Earnings Before Interest, Taxes, Depreciation and Amortization). This results in certain nightclubs carrying a substantial amount of intangible value, mostly allocated to licenses and goodwill. Generally accepted accounting principles require an annual impairment review of these indefinite-lived intangible assets. As a result of our annual impairment review, we recorded impairment charges of $4.3 million (including $1.4 million in one of our properties held for sale and $825,000 relating to the remaining interest in Robust), $1.7 million and $2.3 million for fiscal 2016, 2015 and 2014, respectively. If difficult market and economic conditions continue over the next year and/or we experience a decrease in revenue at one or more nightclubs, we could incur a decline in fair value of one or more of our nightclubs. This could result in future impairment charges of up to the total value of the indefinite-lived intangible assets.

We may deviate from our present capital allocation strategy.

We believe that our present capital allocation strategy will provide us with optimized returns. However, implementation of our capital allocation strategy depends on the interplay of different factors such as our stock price, our outstanding common shares, the interest rates on our debt, and the rate of return on available investments. If these factors are not conducive to implementing our present capital allocation strategy, or we determine that adopting a different capital allocation strategy is in the best interest of shareholders, we reserve the right to deviate from this approach. There can be no assurance that we will not deviate from or adopt an alternative capital allocation strategy moving forward.

We may need additional financing or our business expansion plans may be significantly limited.

If cash generated from our operations is insufficient to satisfy our working capital and capital expenditure requirements, we will need to raise additional funds through the public or private sale of our equity or debt securities. The timing and amount of our capital requirements will depend on a number of factors, including cash flow and cash requirements for nightclub acquisitions and new restaurant development. If additional funds are raised through the issuance of equity or convertible debt securities, the percentage ownership of our then-existing shareholders will be reduced. We cannot assure you that additional financing will be available on terms favorable to us, if at all. Any future equity financing, if available, may result in dilution to existing shareholders; and debt financing, if available, may include restrictive covenants. Any failure by us to procure timely additional financing, if needed, will have material adverse consequences on our business operations.

| 8 |

There is substantial competition in the nightclub entertainment industry, which may affect our ability to operate profitably or acquire additional clubs.

Our nightclubs face substantial competition. Some of these competitors may have greater financial and management resources than we do. Additionally, the industry is subject to unpredictable competitive trends and competition for general entertainment dollars. There can be no assurance that we will be able to remain profitable in this competitive industry.

The adult entertainment industry standard is to classify adult entertainers as independent contractors, not employees. If federal or state law mandates that they be classified as employees, our business could be adversely impacted.

The adult entertainment industry standard is to classify adult entertainers as independent contractors, not employees. The Internal Revenue Service regulations and applicable state law guidelines regarding independent contractor classification are subject to judicial and agency interpretation, and it could be determined that the independent contractor classification is inapplicable. Further, if legal standards for classification of independent contractors change, it may be necessary to modify our compensation structure for these adult entertainers, including by paying additional compensation or reimbursing expenses. While we take steps to ensure that our adult entertainers are deemed independent contractors, if our adult entertainers are determined to have been misclassified as independent contractors, we would incur additional exposure under federal and state law, workers’ compensation, unemployment benefits, labor, employment and tort laws, including for prior periods, as well as potential liability for employee benefits and tax withholdings. Any of these outcomes could result in substantial costs to us, could significantly impair our financial condition and our ability to conduct our business as we choose, and could damage our ability to attract and retain other personnel.

The adult entertainment industry is extremely volatile.

Historically, the adult entertainment, restaurant and bar industry has been an extremely volatile industry. The industry tends to be extremely sensitive to the general local economy, in that when economic conditions are prosperous, entertainment industry revenues increase, and when economic conditions are unfavorable, entertainment industry revenues decline. Coupled with this economic sensitivity are the trendy personal preferences of the customers who frequent adult cabarets. We continuously monitor trends in our customers’ tastes and entertainment preferences so that, if necessary, we can make appropriate changes which will allow us to remain one of the premiere adult cabarets. However, any significant decline in general corporate conditions or uncertainties regarding future economic prospects that affect consumer spending could have a material adverse effect on our business. In addition, we have historically catered to a clientele base from the upper end of the market. Accordingly, further reductions in the amounts of entertainment expenses allowed as deductions from income under the Internal Revenue Code of 1954, as amended, could adversely affect sales to customers dependent upon corporate expense accounts.

Private advocacy group actions targeted at the kind of adult entertainment we offer could result in limitations and our inability to operate in certain locations and negatively impact our business.

Our ability to operate successfully depends on the protection provided to us under the First Amendment to the U.S. Constitution. From time to time, private advocacy groups have sought to target our nightclubs by petitioning for non-renewal of certain of our permits and licenses. Furthermore, private advocacy groups which have influences on certain financial institutions have managed to sway these financial institutions into not doing business with us. In addition to possibly limiting our operations and financing options, negative publicity campaigns, lawsuits and boycotts could negatively affect our businesses and cause additional financial harm by discouraging investors from investing in our securities or requiring that we incur significant expenditures to defend our business.

| 9 |

Our revenues could be significantly affected by limitations relating to permits to sell alcoholic beverages.

We derive a significant portion of our revenues from the sale of alcoholic beverages. States in which we operate may have laws which may limit the availability of a permit to sell alcoholic beverages or which may provide for suspension or revocation of a permit to sell alcoholic beverages in certain circumstances. The temporary or permanent suspension or revocations of any such permits would have a material adverse effect on our revenues, financial condition and results of operations. In all states where we operate, management believes we are in compliance with applicable city, county, state or other local laws governing the sale of alcohol.

Activities or conduct at our nightclubs may cause us to lose necessary business licenses, expose us to liability, or result in adverse publicity, which may increase our costs and divert management’s attention from our business.

We are subject to risks associated with activities or conduct at our nightclubs that are illegal or violate the terms of necessary business licenses. Some of our nightclubs operate under licenses for sexually oriented businesses and are afforded some protection under the First Amendment to the U.S. Constitution. While we believe that the activities at our nightclubs comply with the terms of such licenses, and that the element of our business that constitutes an expression of free speech under the First Amendment to the U.S. Constitution is protected, activities and conduct at our nightclubs may be found to violate the terms of such licenses or be unprotected under the U.S. Constitution. This protection is limited to the expression and not the conduct of an entertainer. An issuing authority may suspend or terminate a license for a nightclub found to have violated the license terms. Illegal activities or conduct at any of our nightclubs may result in negative publicity or litigation. Such consequences may increase our cost of doing business, divert management’s attention from our business and make an investment in our securities unattractive to current and potential investors, thereby lowering our profitability and our stock price.

We have developed comprehensive policies aimed at ensuring that the operation of each of our nightclubs is conducted in conformance with local, state and federal laws. We have a “no tolerance” policy on illegal drug use in or around the facilities. We continually monitor the actions of entertainers, waitresses and customers to ensure that proper behavior standards are met. However, such policies, no matter how well designed and enforced, can provide only reasonable, not absolute, assurance that the policies’ objectives are being achieved. Because of the inherent limitations in all control systems and policies, there can be no assurance that our policies will prevent deliberate acts by persons attempting to violate or circumvent them. Notwithstanding the foregoing limitations, management believes that our policies are reasonably effective in achieving their purposes.

We rely heavily on information technology in our operations and any material failure, weakness, interruption or breach of security could prevent us from effectively operating our business.

Our operations and corporate functions rely heavily on information systems, including point-of-sale processing, management of our supply chain, payment of obligations, collection of cash, electronic communications, data warehousing to support analytics, finance and accounting systems, mobile technologies to enhance the customer experience, and other various processes and procedures, some of which are handled by third parties. Our ability to efficiently and effectively manage our business depends significantly on the reliability and capacity of these systems. The failure of these systems to operate effectively, maintenance problems, upgrading or transitioning to new platforms, or a breach in security relating to these systems could result in delays in consumer service and reduce efficiency in our operations. These problems could adversely affect our results of operations, and remediation could result in significant, unplanned capital investments.

Security breaches of confidential customer information or personal employee information may adversely affect our business.

A significant portion of our revenues are paid through debit and credit cards. Other restaurants and retailers have experienced significant security breaches in which debit and credit card information or other personal information of their customers have been stolen. We also maintain certain personal information regarding our employees. Although we aim to safeguard our technology systems, they could potentially be vulnerable to damage, disability or failures due to physical theft, fire, power outage, telecommunication failure or other catastrophic events, as well as from internal and external security breaches, employee error or malfeasance, denial of service attacks, viruses, worms and other disruptive problems caused by hackers and cyber criminals. A breach in our systems that compromises the information of our customers or employees could result in widespread negative publicity, damage to our reputation, a loss of customers, and legal liabilities. We may in the future become subject to lawsuits or other proceedings for purportedly fraudulent transactions arising from the actual or alleged theft of our customers’ debit and credit card information or if customer or employee information is obtained by unauthorized persons or used inappropriately. Any such claim or proceeding, or any adverse publicity resulting from such an event, may have a material adverse effect on our business.

| 10 |

Our acquisitions may result in disruptions in our business and diversion of management’s attention.

We have made and may continue to make acquisitions of complementary nightclubs, restaurants or related operations. Any acquisitions will require the integration of the operations, products and personnel of the acquired businesses and the training and motivation of these individuals. Such acquisitions may disrupt our operations and divert management’s attention from day-to-day operations, which could impair our relationships with current employees, customers and partners. We may also incur debt or issue equity securities to pay for any future acquisitions. These issuances could be substantially dilutive to our stockholders. In addition, our profitability may suffer because of acquisition-related costs or amortization, or impairment costs for acquired goodwill and other intangible assets. If management is unable to fully integrate acquired business, products or persons with existing operations, we may not receive the benefits of the acquisitions, and our revenues and stock trading price may decrease.

The impact of new club or restaurant openings could result in fluctuations in our financial performance.

Performance of any new club or restaurant location will usually differ from its originally targeted performance due to a variety of factors, and these differences may be material. New clubs and restaurants typically encounter higher customer traffic and sales in their initial months, which may decrease over time. Accordingly, sales achieved by new or reconcepted locations may not be indicative of future operating results. Additionally, we incur substantial pre-opening expenses each time we open a new establishment, which expenses may be higher than anticipated. Due to the foregoing factors, results for any one fiscal quarter are not necessarily indicative of results to be expected for any other fiscal quarter or for a full fiscal year.

We must continue to meet NASDAQ Global Market Continued Listing Requirements or we risk delisting.

Our securities are currently listed for trading on the NASDAQ Global Market. We must continue to satisfy NASDAQ’s continued listing requirements or risk delisting which would have an adverse effect on our business. If our securities are ever delisted from NASDAQ, they may trade on the over-the-counter market, which may be a less liquid market. In such case, our shareholders’ ability to trade or obtain quotations of the market value of shares of our common stock would be severely limited because of lower trading volumes and transaction delays. These factors could contribute to lower prices and larger spreads in the bid and ask prices for our securities. There is no assurance that we will be able to maintain compliance with the NASDAQ continued listing requirements.

We incur significant costs as a result of operating as a public company, and our management devotes substantial time to new compliance initiatives.

We will incur significant legal, accounting and other expenses that our non-public competition does not incur. The Sarbanes-Oxley Act of 2002 (the “Sarbanes-Oxley Act”), as well as new rules subsequently implemented by the SEC, have imposed various requirements on public companies, including requiring certain corporate governance practices. Our management and other personnel devote a substantial amount of time to these compliance initiatives. Moreover, these rules and regulations increase our legal and financial compliance costs, and will make some activities more time-consuming and costly.

In addition, the Sarbanes-Oxley Act requires, among other things, that we maintain effective internal controls for financial reporting and disclosure controls and procedures. In particular, we have been required to perform system and process evaluation and testing on the effectiveness of our internal controls over financial reporting, as required by Section 404 of the Sarbanes-Oxley Act. Then, beginning in fiscal 2010, our independent registered public accounting firm has reported on the effectiveness of our internal controls over financial reporting, as required by Section 404 of the Sarbanes-Oxley Act. In the future, our testing, or the subsequent testing by our independent registered public accounting firm, may reveal deficiencies in our internal controls over financial reporting that are deemed to be material weaknesses. Our compliance with Section 404 requires that we incur substantial accounting expense and expend significant management efforts. Moreover, if we are not able to comply with the requirements of Section 404 in a timely manner, or if we or our independent registered public accounting firm identifies deficiencies in our internal controls over financial reporting that are deemed to be material weaknesses, the market price of our stock could decline, and we could be subject to sanctions or investigations by the SEC or other regulatory authorities, which would require additional financial and management resources.

| 11 |

Our quarterly operating results may fluctuate and could fall below the expectations of securities analysts and investors due to seasonality and other factors, some of which are beyond our control, resulting in a decline in our stock price.

Our nightclub operations are affected by seasonal factors. Historically, we have experienced reduced revenues from April through September with the strongest operating results occurring during October through March. As a result, our quarterly and annual operating results and comparable restaurant sales may fluctuate significantly as a result of seasonality and the factors discussed above. Accordingly, results for any one fiscal quarter are not necessarily indicative of results to be expected for any other fiscal quarter or for any fiscal year and same-store sales for any particular future period may decrease. In the future, operating results may fall below the expectations of securities analysts and investors. In that event, the price of our common stock would likely decrease.

We may have uninsured risks in excess of our insurance coverage.

We maintain insurance in amounts we consider adequate for personal injury and property damage to which the business of the Company may be subject. However, there can be no assurance that uninsured liabilities in excess of the coverage provided by insurance, which liabilities may be imposed pursuant to the Texas “Dram Shop” statute or similar “Dram Shop” statutes or common law theories of liability in other states where we operate or expand. For example, the Texas “Dram Shop” statute provides a person injured by an intoxicated person the right to recover damages from an establishment that wrongfully served alcoholic beverages to such person if it was apparent to the server that the individual being sold, served or provided with an alcoholic beverage was obviously intoxicated to the extent that he presented a clear danger to himself and others. An employer is not liable for the actions of its employee who over-serves if (i) the employer requires its employees to attend a seller training program approved by the TABC; (ii) the employee has actually attended such a training program; and (iii) the employer has not directly or indirectly encouraged the employee to violate the law. It is our policy to require that all servers of alcohol working at our clubs in Texas be certified as servers under a training program approved by the TABC, which certification gives statutory immunity to the sellers of alcohol from damage caused to third parties by those who have consumed alcoholic beverages at such establishment pursuant to the Texas Alcoholic Beverage Code. There can be no assurance, however, that uninsured liabilities may not arise in the markets in which we operate which could have a material adverse effect on the Company.

Our previous liability insurer may be unable to provide coverage to us and our subsidiaries.

As previously reported, the Company and its subsidiaries were insured under a liability policy issued by Indemnity Insurance Corporation, RRG (“IIC”) through October 25, 2013. The Company and its subsidiaries changed insurance companies on that date.

On November 7, 2013, the Court of Chancery of the State of Delaware entered a Rehabilitation and Injunction Order (“Rehabilitation Order”), which declared IIC impaired, insolvent and in an unsafe condition and placed IIC under the supervision of the Insurance Commissioner of the State of Delaware (“Commissioner”) in her capacity as receiver (“Receiver”). The Rehabilitation Order empowered the Commissioner to rehabilitate IIC through a variety of means, including gathering assets and marshaling those assets, as necessary. Further, the order stayed or abated pending lawsuits involving IIC as the insurer until May 6, 2014.

| 12 |

On April 10, 2014, the Court of Chancery of the State of Delaware entered a Liquidation and Injunction Order With Bar Date (“Liquidation Order”), which ordered the liquidation of IIC and terminated all insurance policies or contracts of insurance issued by IIC. The Liquidation Order further ordered that all claims against IIC must have been filed with the Receiver before the close of business on January 16, 2015 and that all pending lawsuits involving IIC as the insurer were further stayed or abated until October 7, 2014. As a result, the Company and its subsidiaries no longer had insurance coverage under the liability policy with IIC. Currently, there are several civil lawsuits pending against the Company and its subsidiaries. The Company has retained counsel to defend against and evaluate these claims and lawsuits. We are funding 100% of the costs of litigation and will seek reimbursement from the bankruptcy receiver. The Company filed the appropriate claims against IIC with the Receiver before the January 16, 2015 deadline; however, there are no assurances of any recovery from these claims. It is unknown at this time what effect this uncertainty will have on the Company. As previously stated, since October 25, 2014, the Company obtained general liability coverage from other insurers, which have covered and/or will cover any claims arising from actions after that date.

The protection provided by our service marks is limited.

Our rights to the trade names “RCI Hospitality Holdings, Inc.,” “Rick’s,” “Rick’s Cabaret,” “Tootsie’s Cabaret,” “Club Onyx,” “XTC Cabaret,” “Temptations,” “Jaguars,” “Downtown Cabaret,” “Cabaret East,” Cabaret North,” Bombshells,” and “Vee Lounge” are established under common law, based upon our substantial and continuous use of these trade names in interstate commerce, some of which have been in use at least as early as 1987. “RICK’S AND STARS DESIGN” logo, “RCI HOSPITALITY HOLDINGS, INC.,” “RICKS,” “RICK’S CABARET,” “CLUB ONYX,” “XTC CABARET,” “SILVER CITY CABARET,” “BOMBSHELLS” and “EXOTIC DANCER” are registered through service mark registrations issued by the United States Patent and Trademark Office. As of this date, we have pending registration applications for the names “THE SEVILLE” and “DOWN IN TEXAS SALOON.” We also own the rights to numerous trade names associated with our media division. There can be no assurance that these steps we have taken to protect our service marks will be adequate to deter misappropriation of our protected intellectual property rights. Litigation may be necessary in the future to protect our rights from infringement, which may be costly and time consuming. The loss of the intellectual property rights owned or claimed by us could have a material adverse effect on our business.

Anti-takeover effects of the issuance of our preferred stock could adversely affect our common stock.

Our Board of Directors has the authority to issue up to 1,000,000 shares of preferred stock in one or more series, to fix the number of shares constituting any such series, and to fix the rights and preferences of the shares constituting any series, without any further vote or action by the stockholders. The issuance of preferred stock by the Board of Directors could adversely affect the rights of the holders of our common stock. For example, such issuance could result in a class of securities outstanding that would have preferences with respect to voting rights and dividends and in liquidation over the common stock, and could (upon conversion or otherwise) enjoy all of the rights appurtenant to common stock. The Board’s authority to issue preferred stock could discourage potential takeover attempts and could delay or prevent a change in control of the Company through merger, tender offer, proxy contest or otherwise by making such attempts more difficult to achieve or costlier. There are no issued and outstanding shares of preferred stock; there are no agreements or understandings for the issuance of preferred stock; and the Board of Directors has no present intention to issue preferred stock.

Future sales or the perception of future sales of a substantial amount of our common stock may depress our stock price.

The market price of our common stock could decline as a result of sales of substantial amounts of our common stock in the public market, or as a result of the perception that these sales could occur. In addition, these factors could make it more difficult for us to raise funds through future offerings of common stock.

| 13 |

Our stock price has been volatile and may fluctuate in the future.

The trading price of our securities may fluctuate significantly. This price may be influenced by many factors, including:

| ● | our performance and prospects; | |

| ● | the depth and liquidity of the market for our securities; | |

| ● | sales by selling shareholders of shares issued or issuable in connection with certain convertible notes; | |

| ● | investor perception of us and the industry in which we operate; | |

| ● | changes in earnings estimates or buy/sell recommendations by analysts; | |

| ● | general financial and other market conditions; and | |

| ● | domestic economic conditions. |

Public stock markets have experienced, and may experience, extreme price and trading volume volatility. These broad market fluctuations may adversely affect the market price of our securities.

We are dependent on key personnel.

Our future success is dependent, in a large part, on retaining the services of Mr. Eric Langan, our President and Chief Executive Officer. Mr. Langan possesses a unique and comprehensive knowledge of our industry. While Mr. Langan has no present plans to leave or retire in the near future, his loss could have a negative effect on our operating, marketing and financial performance if we are unable to find an adequate replacement with similar knowledge and experience within our industry. We maintain key-man life insurance with respect to Mr. Langan. Although Mr. Langan is under an employment agreement (as described herein), there can be no assurance that Mr. Langan will continue to be employed by us.

Cumulative voting is not available to our stockholders.

Cumulative voting in the election of Directors is expressly denied in our Articles of Incorporation. Accordingly, the holder or holders of a majority of the outstanding shares of our common stock may elect all of our Directors.

Our directors and officers have limited liability and have rights to indemnification.

Our Articles of Incorporation and Bylaws provide, as permitted by governing Texas law, that our directors and officers shall not be personally liable to us or any of our stockholders for monetary damages for breach of fiduciary duty as a director or officer, with certain exceptions. The Articles further provide that we will indemnify our directors and officers against expenses and liabilities they incur to defend, settle, or satisfy any civil litigation or criminal action brought against them on account of their being or having been its directors or officers unless, in such action, they are adjudged to have acted with gross negligence or willful misconduct.

The inclusion of these provisions in the Articles may have the effect of reducing the likelihood of derivative litigation against directors and officers, and may discourage or deter stockholders or management from bringing a lawsuit against directors and officers for breach of their duty of care, even though such an action, if successful, might otherwise have benefited us and our stockholders.

The Articles provide for the indemnification of our officers and directors, and the advancement to them of expenses in connection with any proceedings and claims, to the fullest extent permitted by Texas law. The Articles include related provisions meant to facilitate the indemnitee’s receipt of such benefits. These provisions cover, among other things: (i) specification of the method of determining entitlement to indemnification and the selection of independent counsel that will in some cases make such determination, (ii) specification of certain time periods by which certain payments or determinations must be made and actions must be taken, and (iii) the establishment of certain presumptions in favor of an indemnitee.

| 14 |

Insofar as indemnification for liabilities arising under the Securities Act may be permitted to our directors, officers and controlling persons pursuant to the foregoing provisions, we have been advised that in the opinion of the Securities and Exchange Commission, such indemnification is against public policy as expressed in the Securities Act and is therefore unenforceable.

A failure to maintain food safety throughout the supply chain and food-borne illness concerns may have an adverse effect on our business.

Food safety is a top priority, and we dedicate substantial resources to ensuring that our guests enjoy safe, quality food products. However, food safety issues could be caused at the point of source or by food suppliers or distributors and, as a result, be out of our control. In addition, regardless of the source or cause, any report of food-borne illnesses such as E. coli, hepatitis A, trichinosis or salmonella, and other food safety issues including food tampering or contamination, at one of our restaurants or clubs could adversely affect the reputation of our brands and have a negative impact on our sales. Even instances of food-borne illness, food tampering or food contamination occurring solely at restaurants of our competitors could result in negative publicity about the food service industry generally and adversely impact our sales. The occurrence of food-borne illnesses or food safety issues could also adversely affect the price and availability of affected ingredients, resulting in higher costs and lower margins.

Other risk factors may adversely affect our financial performance.

Other risk factors that could cause our actual results to differ materially from those indicated in the forward-looking statements by affecting, among many things, pricing, consumer spending and consumer confidence, include, without limitation, changes in economic conditions and financial and credit markets, credit availability, increased fuel costs and availability for our employees, customers and suppliers, health epidemics or pandemics or the prospects of these events (such as reports on avian flu), consumer perceptions of food safety, changes in consumer tastes and behaviors, governmental monetary policies, changes in demographic trends, terrorist acts, energy shortages and rolling blackouts, and weather (including, major hurricanes and regional snow storms) and other acts of God.

Item 1B. Unresolved Staff Comments.

None.

We currently own 45 real estate properties. On 30 of these properties, we operate clubs or restaurants, including a multi-unit shopping center in Miami Gardens, Florida where Tootsie’s Cabaret is located. We lease other units in our Miami Gardens property to 14 different third-party tenants. Our remaining clubs and restaurants are in leased locations.

Three of our owned properties are locations where we previously operated clubs but now lease the buildings to third parties. Four are non-income producing properties for corporate use, including our corporate office. Six other properties are currently offered for sale, while the remaining two properties are large parcels, which we plan to further subdivide for a future Bombshells site and for sale.

Our principal corporate office as of September 30, 2016 was located at 10959 Cutten Road, Houston, Texas 77066, which consisted of a 9,000 square feet office/warehouse building. That corporate office was no longer adequate to meet our needs so we have constructed a new corporate facility on a nearby tract of land, which we own. The new corporate facility, which is located at 10737 Cutten Road, Houston, Texas 77066, consists of a 21,000-square foot corporate office and an 18,000-square foot warehouse facility. We completed our move to the new corporate facility in October 2016.

| 15 |

Below is a list of locations we operate:

| Name of Establishment | Year Acquired/Opened | |||

| Club Onyx, Houston, TX | 1995 | |||

| Rick’s Cabaret, Minneapolis, MN | 1998 | |||

| XTC Cabaret, Austin, TX | 1998 | |||

| XTC Cabaret, San Antonio, TX | 1998 | |||

| XTC Cabaret, Houston, TX | 2004 | (2) | ||

| Rick’s Cabaret, New York City, NY | 2005 | |||

| Club Onyx, Charlotte, NC | 2005 | (2) | ||

| Rick’s Cabaret, San Antonio, TX | 2006 | |||

| XTC Cabaret, South Houston, TX | 2006 | (2) | ||

| Rick’s Cabaret, Fort Worth, TX | 2007 | |||

| Tootsie’s Cabaret, Miami Gardens, FL | 2008 | |||

| XTC Cabaret, Dallas, TX | 2008 | |||

| Foxy’s Cabaret, Dallas, TX | 2008 | (1) | ||

| Club Onyx, Philadelphia, PA | 2008 | |||

| Rick’s Cabaret, Round Rock, TX | 2009 | |||

| Cabaret East, Fort Worth, TX | 2010 | |||

| Rick’s Cabaret DFW, Fort Worth, TX | 2011 | |||

| Downtown Cabaret, Minneapolis, MN | 2011 | |||

| Temptations, Aledo, TX | 2011 | (2) | ||

| Silver City Cabaret, Dallas, TX | 2012 | |||

| Jaguars Club, Odessa, TX | 2012 | |||

| Jaguars Club, Phoenix, AZ | 2012 | |||

| Jaguars Club, Lubbock, TX | 2012 | |||

| Jaguars Club, Longview, TX | 2012 | |||

| Jaguars Club, Tye, TX | 2012 | |||

| Jaguars Club, Edinburg, TX | 2012 | |||

| Jaguars Club, El Paso, TX | 2012 | |||

| Jaguars Club, Harlingen, TX | 2012 | |||

| Studio 80, Fort Worth, TX | 2013 | (1)(2) | ||

| Bombshells, Dallas, TX | 2013 | |||

| Temptations, Sulphur, LA | 2013 | |||

| Temptations, Beaumont, TX | 2013 | |||

| Club Onyx, Dallas, TX | 2013 | (1) | ||

| Vivid Cabaret, New York, NY | 2014 | (2) | ||

| Bombshells, Austin, TX | 2014 | (2) | ||

| Rick’s Cabaret, Odessa, TX | 2014 | |||

| Bombshells, Spring TX | 2014 | (2) | ||

| Bombshells, Houston, TX | 2014 | (2) | ||

| Foxy’s Cabaret, Austin TX | 2015 | (1) | ||

| The Seville, Minneapolis, MN | 2015 | |||

| Hoops Cabaret and Sports Bar, New York, NY | 2016 | (2)(3) | ||

(1) Reconcepted in 2016.

(2) Leased location.

(3) Officially opened on October 6, 2016.

Our property leases are typically for a fixed rental rate without revenue percentage rentals. The lease terms generally have initial terms of 10 to 20 years with renewal terms of 5 to 20 years. At September 30, 2016, certain of our owned properties were collateral for mortgage debt amounting to approximately $76.2 million. Also, see more information in the following Notes to Consolidated Financial Statements: F - Property and Equipment, H - Long-Term Debt and K - Commitments and Contingencies.

See the “Legal Matters” section within Note K - Commitments and Contingencies of Notes to Consolidated Financial Statements within this Annual Report on Form 10-K for the requirements of this Item, which section is incorporated herein by reference.

Item 4. Mine Safety Disclosures.

Not applicable.

| 16 |

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities.

Our common stock is quoted on the NASDAQ Global Market under the symbol “RICK.” The following table sets forth the quarterly high and low of sales prices per share for the common stock for the last two fiscal years.

| COMMON STOCK PRICE RANGE | High | Low | ||||||

| Fiscal Year Ended September 30, 2016 | ||||||||

| First Quarter | $ | 10.75 | $ | 9.38 | ||||

| Second Quarter | $ | 9.94 | $ | 7.50 | ||||

| Third Quarter | $ | 11.10 | $ | 8.77 | ||||

| Fourth Quarter | $ | 11.60 | $ | 9.90 | ||||

| Fiscal Year Ended September 30, 2015 | ||||||||

| First Quarter | $ | 12.25 | $ | 9.13 | ||||

| Second Quarter | $ | 11.04 | $ | 9.57 | ||||

| Third Quarter | $ | 12.50 | $ | 10.30 | ||||

| Fourth Quarter | $ | 12.14 | $ | 10.25 | ||||

On December 8, 2016, the closing stock price for our common stock as reported by NASDAQ was $14.38. On December 1, 2016, there were approximately 177 stockholders of record of our common stock (excluding broker held shares in street name). We estimate that there are approximately 5,100 stockholders to have beneficial ownership in street name.

TRANSFER AGENT AND REGISTRAR

The transfer agent and registrar for our common stock is American Stock Transfer & Trust Company, 6201 15th Avenue, Brooklyn, NY 11219.

DIVIDEND POLICY

Prior to 2016, we have not paid cash dividends on our common stock. Starting in March 2016, in conjunction with our share buyback program (see discussion below), our Board of Directors has declared quarterly cash dividends of $0.03 per share ($0.12 per share on an annual basis). During fiscal 2016, we paid an aggregate amount of $862,000 for cash dividends.

PURCHASES OF EQUITY SECURITIES BY THE ISSUER

During the fiscal year ended September 30, 2016, we purchased a total of 747,081 shares of common stock in the open market at prices ranging from $7.69 to $11.55. In May 2016, the Board of Directors increased the repurchase authorization by an additional $5.0 million.

| 17 |

The table below sets forth information regarding our common stock repurchases during the three months ended September 30, 2016:

| Month Ended | Total Number of Shares (or Units) Purchased | Average Price Paid per Share | Total Number of Shares (or Units) Purchased as Part of Publicly Announced Plans or Programs | Maximum Number (or Approximate Dollar Value) of Shares (or Units) That May Yet be Purchased Under the Plans or Programs | ||||||||||||

| July 31, 2016 | 41,486 | $ | 10.38 | 41,486 | $ | 5,341,543 | ||||||||||

| August 31, 2016 | 46,200 | $ | 10.82 | 46,200 | $ | 4,841,459 | ||||||||||

| September 30, 2016 | 52,400 | $ | 11.44 | 52,400 | $ | 4,242,209 | ||||||||||

EQUITY COMPENSATION PLAN INFORMATION

We have no stock options nor any other equity award outstanding under equity compensation plans as of September 30, 2016.

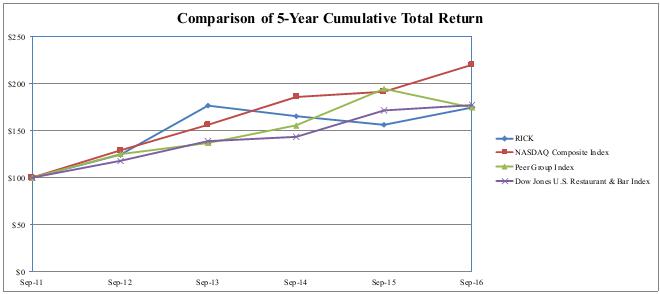

STOCK PERFORMANCE GRAPH

The following chart compares the 5-year cumulative total stock performance of our common stock; the NASDAQ Composite Index; our former peer group consisting of BJ’s Restaurant Group, Cheesecake Factory, Ark Restaurants and Buffalo Wild Wings; and the Dow Jones U.S. Restaurant & Bar Index, our current peer index. The graph assumes that $100 was invested at inception in each of our common stock and in each of the indices and that all dividends were reinvested. The measurement points utilized in the graph consist of the last trading day as of September 30 each year, representing the last day of our fiscal year. The calculations exclude trading commissions and taxes. We have selected the Dow Jones U.S. Restaurant & Bar Index as our new peer index since it represents a broader group of restaurant and bar operators than our former four-company peer group, both of which are shown below for comparison. The historical stock performance presented below is not intended to and may not be indicative of future stock performance.

| 18 |

Item 6. Selected Financial Data.

The following table sets forth certain of the Company’s historical financial data. The selected historical consolidated financial position data as of September 30, 2016 and 2015 and results of operations data for the years ended September 30, 2016, 2015 and 2014 have been derived from the Company’s audited consolidated financial statements and the related notes included elsewhere in this Annual Report on Form 10-K. The selected historical consolidated financial data as of September 30, 2014, 2013 and 2012 and for the years ended September 30, 2013 and 2012 have been derived from the Company’s audited financial statements for such years, as revised (see footnotes 1 and 2 below), which are not included in this Annual Report on Form 10-K. The selected historical consolidated financial data set forth are not necessarily indicative of the results of future operations and should be read in conjunction with the discussion under the heading “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and the historical consolidated financial statements and accompanying notes included herein. The historical results are not necessarily indicative of the results to be expected in any future period.

Please read the following selected consolidated financial data in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our consolidated financial statements and the related notes appearing elsewhere in this Annual Report on Form 10-K for a discussion of information that will enhance understanding of these data (in thousands, except per share data and percentages).

| Years Ended September 30, | ||||||||||||||||||||

| 2016 | 2015 | 2014 | 2013 | 2012 | ||||||||||||||||

| Revenue(1) | $ | 134,860 | $ | 135,449 | $ | 121,432 | $ | 105,921 | $ | 90,201 | ||||||||||

| Income from operations | $ | 20,848 | $ | 20,878 | $ | 18,875 | $ | 21,883 | $ | 16,259 | ||||||||||

| Net income attributable to RCIHH | $ | 11,089 | $ | 9,312 | $ | 11,240 | $ | 9,191 | $ | 7,578 | ||||||||||

| Diluted earnings per share | $ | 1.10 | $ | 0.90 | $ | 1.13 | $ | 0.96 | $ | 0.78 | ||||||||||

| Adjusted EBITDA(3) | $ | 34,531 | $ | 34,125 | $ | 31,703 | $ | 28,559 | $ | 24,222 | ||||||||||

| Non-GAAP operating income(3) | $ | 27,721 | $ | 28,125 | $ | 25,762 | $ | 24,690 | $ | 20,364 | ||||||||||

| Non-GAAP operating margin(3) | 20.6 | % | 20.8 | % | 21.2 | % | 23.3 | % | 22.6 | % | ||||||||||

| Non-GAAP net income(3) | $ | 13,402 | $ | 13,971 | $ | 11,961 | $ | 11,317 | $ | 10,308 | ||||||||||

| Non-GAAP diluted net income per share(3) | $ | 1.32 | $ | 1.35 | $ | 1.20 | $ | 1.18 | $ | 1.06 | ||||||||||

| Free cash flow(3) | $ | 20,513 | $ | 14,889 | $ | 18,734 | $ | 17,153 | $ | 16,074 | ||||||||||

| Capital expenditures | $ | 28,148 | $ | 19,259 | $ | 16,034 | $ | 9,675 | $ | 6,898 | ||||||||||

| Dividends declared per share | $ | 0.09 | $ | - | $ | - | $ | - | $ | - | ||||||||||

| September 30, | ||||||||||||||||||||

| 2016 | 2015 | 2014 | 2013 | 2012 | ||||||||||||||||

| Cash and cash equivalents | $ | 11,327 | $ | 8,020 | $ | 9,964 | $ | 10,638 | $ | 5,520 | ||||||||||

| Total current assets(2) | $ | 29,387 | $ | 16,935 | $ | 17,973 | $ | 16,042 | $ | 11,073 | ||||||||||

| Total assets(2) | $ | 276,488 | $ | 266,799 | $ | 233,504 | $ | 218,242 | $ | 188,602 | ||||||||||

| Total current liabilities (excluding current portion of long-term debt) | $ | 14,507 | $ | 13,154 | $ | 26,879 | $ | 20,083 | $ | 16,175 | ||||||||||

| Long-term debt (including current portion)(2) | $ | 105,886 | $ | 94,349 | $ | 70,092 | $ | 78,352 | $ | 63,447 | ||||||||||

| Total liabilities(2) | $ | 146,346 | $ | 138,313 | $ | 120,205 | $ | 121,127 | $ | 100,990 | ||||||||||

| Total RCIHH stockholders’ equity | $ | 127,558 | $ | 122,623 | $ | 110,289 | $ | 93,781 | $ | 84,306 | ||||||||||

| (1) | Due to a change in accounting policy, we have reported revenues net of sales taxes and other revenue related taxes since the beginning of fiscal 2016. Prior year revenues and expenses have been revised to reflect this change. Refer to Note B to the consolidated financial statements for further discussion. | |

| (2) | Certain items in the prior year financial statements have been reclassified to conform to current year financial statement presentation, in particular, debt issuance costs as prescribed by ASU 2015-03 and deferred tax assets and liabilities as prescribed by ASU 2015-17. Refer to Note B to the consolidated financial statements for further discussion. | |

| (3) | Reconciliation and discussion of non-GAAP financial measures are included under the “Non-GAAP Financial Measures” section of Item 7 – “Management’s Discussion and Analysis of Financial Condition and Results of Operations” that follows. See also notes on comparability of adjustment items at the end of the section. |

| 19 |

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

OVERVIEW

The following Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) is intended to help the reader understand RCI Hospitality Holdings, Inc., our operations and our present business environment. MD&A is provided as a supplement to — and should be read in conjunction with — our consolidated financial statements and the accompanying notes thereto contained in Item 8 – “Financial Statements and Supplementary Data” of this report. This overview summarizes the MD&A, which includes the following sections:

| ● | Our Business — a general description of our business and the adult nightclub industry, our objective, our strategic priorities, our core capabilities, and challenges and risks of our business. | |

| ● | Critical Accounting Policies and Estimates — a discussion of accounting policies that require critical judgments and estimates. | |

| ● | Operations Review — an analysis of our Company’s consolidated results of operations for the three years presented in our consolidated financial statements. | |

| ● | Liquidity and Capital Resources — an analysis of cash flows, aggregate contractual obligations, and an overview of financial position. |

OUR BUSINESS

The following are our operating segments:

| Nightclubs | Our wholly owned subsidiaries own and/or operate upscale adult nightclubs serving primarily businessmen and professionals. These nightclubs are in Houston, Austin, San Antonio, Dallas, Fort Worth, Beaumont, Longview, Harlingen, Edinburg, Tye, Lubbock, El Paso and Odessa, Texas; Charlotte, North Carolina; Minneapolis, Minnesota; New York, New York; Miami Gardens, Florida; Philadelphia, Pennsylvania; and Phoenix, Arizona. No sexual contact is permitted at any of our locations. | |

| Bombshells Restaurants and Sports Bars | Our wholly owned subsidiaries own and operate non-adult nightclubs, restaurants, and sports bars in Houston, Dallas, Austin, Spring, and Fort Worth, Texas under the brand names Bombshells and Vee Lounge (reconcepted in October 2016 as Studio 80). | |

| Media Group | Our wholly owned subsidiaries own a media division, including the leading trade magazine serving the multi-billion-dollar adult nightclubs industry. We also own an industry trade show, one other industry trade publications and more than 15 industry websites. |

| 20 |

Our revenues are derived from the sale of liquor, beer, wine, food, merchandise, cover charges, membership fees, facility use fees, commissions from vending and ATM machines, valet parking and other products and services for both nightclub and restaurant/sports bar operations. Media Group revenues include the sale of advertising content and revenues from our annual Expo convention. Our fiscal year end is September 30.

We calculate same-store sales by comparing year-over-year revenues from nightclubs and restaurants/sports bars operating at least 12 full months. We exclude from a particular month’s calculation units previously included in the same-store sales base that have closed temporarily for more than 15 days until its next full month of operations. We also exclude from the same-store sales base units that are being reconcepted or are closed due to renovations or remodels. Acquired units are included in the same-store sales calculation as long as they qualify based on the definition stated above. Revenues from non-nightclub and non-restaurant/sports bar operations are excluded from same-store sales calculation.

Our goal is to use our Company’s assets — our brands, financial strength, and the talent and strong commitment of our management and associates — to become more competitive and to accelerate growth in a manner that creates value for our shareholders.

CRITICAL ACCOUNTING POLICIES AND ESTIMATES

Management’s discussion and analysis of financial condition and results of operations are based upon our financial statements, which have been prepared in accordance with accounting principles generally accepted in the United States (“GAAP”). The preparation of these consolidated financial statements requires our management to make assumptions and estimates about future events, and apply judgments that affect the reported amounts of assets, liabilities, revenues and expenses, and related disclosure of contingent assets and liabilities. These estimates are based on management’s historical industry experience and on various other assumptions that are believed to be reasonable under the circumstances. On a regular basis, we evaluate these accounting policies, assumptions, estimates and judgments to ensure that our financial statements are presented fairly and in accordance with GAAP. However, because future events and their effects cannot be determined with certainty, actual results may differ from our estimates, and such differences could be material.

A full discussion of our significant accounting policies is contained in Note B – Summary of Significant Accounting Policies, which is included in Item 8 – “Financial Statements and Supplementary Data” of this report. We believe that the following accounting estimates are the most critical to aid in fully understanding and evaluating our financial results. These estimates require our most difficult, subjective or complex judgments because they relate to matters that are inherently uncertain. We have reviewed these critical accounting policies and estimates and related disclosures with our Audit Committee.

Impairment of Long-Lived Assets

We review long-lived assets, such as property and equipment, and purchased intangible assets subject to amortization, for impairment whenever events or changes in circumstances indicate that the carrying amount of an asset may not be recoverable. Recoverability of assets to be held and used is measured by a comparison of the carrying amount of an asset to estimated undiscounted future cash flows expected to be generated by the asset. If the carrying amount of an asset exceeds its estimated future cash flows, an impairment charge is recognized by the amount by which the carrying amount of the asset exceeds the fair value of the asset. Assets to be disposed of would be separately presented in the balance sheet and reported at the lower of the carrying amount or fair value less costs to sell, and are no longer depreciated. We impaired one property held for sale by $1.4 million based on estimated realizable value less costs to sell.

Goodwill and intangible assets that have indefinite useful lives are tested annually for impairment, and are tested for impairment more frequently if events and circumstances indicate that the asset might be impaired. An impairment loss is recognized to the extent that the carrying amount of the reporting unit exceeds its fair value.

| 21 |

Our impairment calculations require management to make assumptions and to apply judgment in order to estimate fair values. If our actual results are not consistent with our estimates and assumptions, we may be exposed to impairments that could be material. We do not believe that there is a reasonable likelihood that there will be a material change in the estimates or assumptions we used to calculate impairment charges.

To begin the review, we determine the cash flows from each unit and compare these to prior periods along with comparisons of gross margin and same store sales comparisons. For any of these units that we believe require further analysis as a result of the comparisons made, we prepare an estimated discounted future cash flows expected to be generated by the asset to determine the estimated fair value of the unit. This is compared to the carrying value of the unit and reviewed for reasonableness. If necessary, an impairment charge is recognized by the amount by which the carrying amount of any unit exceeds the fair value of the assets. For the year ended September 30, 2016, we impaired one unit in this manner in the amount of $2.1 million. There were no other units in which the estimated fair value was not substantially in excess of the carrying value.

Income Taxes

We estimate certain components of our provision for income taxes. These estimates include depreciation and amortization expense allowable for tax purposes, allowable tax credits for items such as taxes paid on employee tip income, effective rates for state and local income taxes, and the deductibility of certain other items, among others. We adjust our annual effective income tax rate as additional information on outcomes or events becomes available.

Legal and Other Contingencies

As mentioned in Item 3 – “Legal Proceedings” and in a more detailed discussion in Note K to our consolidated financial statements, we are involved in various suits and claims in the normal course of business. We record a liability when it is probable that a loss has been incurred and the amount is reasonably estimable. There is significant judgment required in both the probability determination and as to whether an exposure can be reasonably estimated. In the opinion of management, there was not at least a reasonable possibility that we may have incurred a material loss, or a material loss in excess of a recorded accrual, with respect to loss contingencies for asserted legal and other claims. However, the outcome of legal proceedings and claims brought against the Company is subject to significant uncertainty. Therefore, although management considers the likelihood of such an outcome to be remote, if one or more of these legal matters were resolved against the Company in a reporting period for amounts in excess of management’s expectations, the Company’s consolidated financial statements for that reporting period could be materially adversely affected.

OPERATIONS REVIEW

The following tables presents a comparison of our results of operations as a percentage of total revenues for the past three fiscal years:

| 2016 | 2015 | 2014 | ||||||||||

| Sales of alcoholic beverages | 42.4 | % | 41.2 | % | 39.4 | % | ||||||

| Sales of food and merchandise | 13.3 | % | 13.8 | % | 12.1 | % | ||||||

| Service revenues | 38.0 | % | 39.1 | % | 42.8 | % | ||||||

| Other | 6.3 | % | 5.8 | % | 5.7 | % | ||||||

Total revenues | 100.0 | % | 100.0 | % | 100.0 | % | ||||||

| Cost of goods sold | 15.2 | % | 15.0 | % | 13.5 | % | ||||||

| Salaries and wages | 27.8 | % | 27.9 | % | 26.8 | % | ||||||

| Selling, general and administrative | 31.9 | % | 32.2 | % | 33.8 | % | ||||||