UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

(Mark One) FORM 10-K

| þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| For the fiscal year ended December 31, 2012 |

or

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | |

| For the transition period from to |

Commission file number: 000-50140

|

ACL Semiconductors Inc. (Exact name of Registrant as specified in its charter) |

| Delaware | 16-1642709 | |

| State or other jurisdiction of incorporation or organization | (I.R.S. Employer Identification Number) |

| Room 1703, 17/F., Tower 1, Enterprise Square, 9 Sheung Yuet Road, Kowloon Bay, Kowloon, Hong Kong. | |

| (Address of principal executive offices) | (Zip Code) |

| Registrant’s telephone number including area code : 011-852-3666-9939 | |||||||||

| Securities registered pursuant to Section 12(b) of the Act: |

| Title of each class | Name of each exchange on which registered | |

| NONE | N/A |

Securities registered pursuant to Section 12(g) of the Act:

| Common Stock, $0.001 par value | ||||

| (Title of class) |

| Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. oYes þNo | |||||||||

| Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. oYes þNo | |||||||||

| Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. þYes oNo | |||||||||

| Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files.) þYes oNo | |||||||||

| Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K, or any amendment to this Form 10-K. o | |||||||||

| Indicate by check mark whether the registrant is large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. | |||||||||

| Large accelerated filer o | Accelerated filer o | ||||||||

| Non-accelerated filer o (Do not check if a smaller reporting company) | Smaller reporting company þ | ||||||||

| Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). oYes þNo | |||||||||

The aggregate market value of the voting common equity held by non-affiliates of the registrant as of June 30, 2012 was approximately $1,629,699.00 based upon the closing price of $0.20 of the registrant’s common stock on the OTC Bulletin Board. (For purposes of determining this amount, only directors, executive officers, and 10% or greater stockholders have been deemed affiliates).

The number of shares of Registrant’s Common Stock outstanding as of April 15, 2013 was 39,474,495.

DOCUMENTS INCORPORATED BY REFERENCE

NONE

Table of Contents

Form 10-K Index

| PAGE | |||

| FORWARD LOOKING STATEMENT | 1 | ||

| PART I | |||

| Item 1. | Business | 1 | |

| Item 1A. | Risk Factors | 10 | |

| Item 1B. | Unresolved Staff Comments | 19 | |

| Item 2. | Properties | 20 | |

| Item 3. | Legal Proceedings | 20 | |

| Item 4. | Mine Safety Disclosures | 20 | |

| PART II | |||

| Item 5. | Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 21 | |

| Item 6. | Selected Financial Data | 22 | |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 22 | |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 30 | |

| Item 8. | Financial Statements and Supplementary Data | 30 | |

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 30 | |

| Item 9A. | Controls and Procedures | 30 | |

| Item 9B. | Other Information | 33 | |

| PART III | |||

| Item 10. | Directors, Executive Officers and Corporate Governance | 34 | |

| Item 11. | Executive Compensation | 37 | |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 40 | |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | 41 | |

| Item 14. | Principal Accounting Fees and Services | 44 | |

| PART IV | |||

| Item 15. | Exhibits and Financial Statement Schedules | 45 | |

| Signatures | 47 | ||

| Index to Consolidated Financial Statements | F-1 | ||

FORWARD LOOKING STATEMENTS

This Annual Report on Form 10-K and the documents incorporated herein contain “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the Company, or industry results, to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. When used in this Annual Report, statements that are not statements of current or historical fact may be deemed to be forward-looking statements. Without limiting the foregoing, the words “plan”, “intend”, “may,” “will,” “expect,” “believe”, “could,” “anticipate,” “estimate,” or “continue” or similar expressions or other variations or comparable terminology are intended to identify such forward-looking statements. Readers are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date hereof. Except as required by applicable laws, the Company undertakes no obligation to update publicly any forward-looking statements for any reason, even if new information becomes available or other events occur in the future.

PART I

As used throughout this Annual Report, the terms “ACL”, “Company”, “we”, “us”, “our” or “Registrant” refer to ACL Semiconductors Inc. and its subsidiaries.

| Item 1. | Business |

Overview

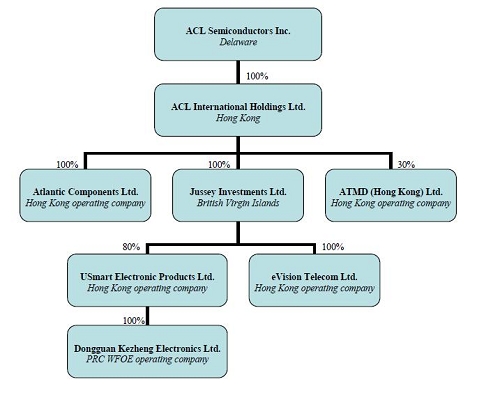

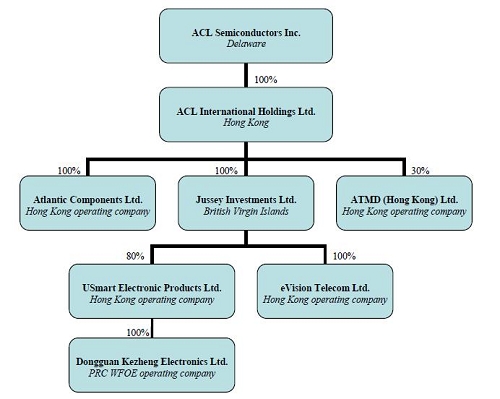

ACL Semiconductors Inc. was incorporated under the laws of the State of Delaware on September 17, 2002. The Company has been primarily engaged in the business of distribution of memory products mainly under “Samsung” brand name which principally comprised Dynamic Random Access Memory (“DRAM”), Graphic Random Access Memory (“Graphic RAM”) and Flash storage devices in the Hong Kong Special Administrative Region (“Hong Kong”) and People’s Republic of China (the “PRC” or “China”) markets formerly through its wholly owned subsidiary Atlantic Components Limited (“Atlantic”), a Hong Kong incorporated company, and through ATMD (Hong Kong) Limited (“ATMD”) after April 1, 2012. The Company, through its wholly owned subsidiary ACL International Holdings Limited (“ACL Holdings”), owns 30% equity interest in ATMD, the joint venture with Tomen Devices Corporation (“Tomen”). ATMD offers a broad range of industry-leading Samsung semiconductor products, and additional components from SAMCO (such as wifi and camera modules) and SMD (smartphone panels). Through the acquisition of Jussey Investments Limited (“Jussey”) on September 28, 2012, the Company has diversified its product portfolio and customer network, obtained design and manufacturing capabilities, and tapped into the blooming telecommunication industry with access to the 3G baseband licenses.

| 1 |

Corporate Structure

Background

ACL International Holdings Limited

ACL Holdings, a holding company incorporated in Hong Kong, is wholly owned by the Company. ACL Holdings owns 100% equity interest of Atlantic and 30% equity interest of ATMD, the joint venture with Tomen.

Atlantic Components Limited

Atlantic, a company incorporated in Hong Kong, is indirectly wholly owned by the Company. Atlantic was established in May 1991 by Mr. Chung-Lun Yang, the Company’s Chairman, as a regional distributor of memory products of various manufacturers. In 1993, Samsung Electronics Hong Kong Co., Ltd. (“Samsung”) appointed Atlantic as its authorized distributor and marketer of Samsung’s memory products in Hong Kong and overseas markets. In 2001, Atlantic established a representative office in Shenzhen, China, and began concentrating its distribution and marketing efforts in Southern China.

The Company’s Samsung business was formerly conducted through Atlantic. After April 1, 2012, Atlantic integrated its business relating to procurement of semiconductors and electronic parts directly from Samsung to the new joint venture, ATMD. The transition of the business integration has been completed by December 31, 2012. During the transitional period, Atlantic extended its distributor agreement with Samsung to June 30, 2012. After the distributor agreement expired, Atlantic transformed its position from Samsung memory products distributor to a general memory products distributor, and continues its business by providing various brands of memory products to its customers.

| 2 |

Aristo Technologies Limited

On March 23, 2010, the Company concluded that Aristo Technologies Limited (“Aristo”), a related company solely owned by Mr. Yang, is a variable interest entity under FASB ASC 810-10-25 and is therefore subject to consolidation with the Company beginning fiscal year 2007 under the guidance applicable to variable interest entities. Atlantic sells Samsung memory chips to Aristo and allows long grace periods for Aristo to repay the open accounts receivable. Being the Company’s biggest creditor, the Company does not require Aristo to pledge assets or enter into any agreements to bind Aristo to specific repayment terms. The Company does not experience any bad debt from Aristo. Hence, the Company does not provide any bad debt provision derived from Aristo. Although, the Company is not involved in Aristo’s daily operation, it believes that there will not be significant additional risk derived from the trading relationship and transactions with Aristo. Aristo is engaged in the marketing, selling and servicing of computer products and accessories including semiconductors, LCD products, mass storage devices, consumer electronics, computer peripherals and electronic components for different generations of computer related products. In addition to Samsung-branded products, Aristo carries various brands of products, such as Hynix, Micron, Qimonda, Lexar, Dane-Elec, Elixir, SanDisk and Winbond. Aristo also provides value-added services to its products and resells it to its customers. Aristo’s 2012 and 2011 sales were around $2 million and $14 million; it was a distributor that accommodated special requirements for specific customers.

ATMD (Hong Kong) Limited

ATMD, our 30% owned joint venture company incorporated in Hong Kong, integrated both Atlantic and Tomen’s Samsung business in Hong Kong and PRC regions. On April 1, 2012, ATMD entered into a distribution agreement with Samsung Electronics Hong Kong Co., Ltd. and began to sell and distribute Samsung’s products to the Greater China market, as consented to and approved by Samsung. ATMD is authorized to distribute the same product types originally authorized to Atlantic – DRAMs, including Computing DRAMs, Consumer DRAMs and Graphics DRAMs, NAND Flashs, and LCD panels. Apart from the original authorized distribution of products distributed by Atlantic, ATMD is also authorized to distribute Applicable System LSI and Applicable System LCD products including, but not limited to wifi modules, camera modules, and smartphone panels which is used in the rapidly growing segments such as smartphones, netbooks, tablets, personal navigation devices, digital TV, Set Top Box, and wireless handheld PDAs.

The Company indirectly owns 30% equity interest of ATMD. Mr. Chung-Lun Yang, the Company’s Chairman was appointed the Chief Executive Officer of ATMD. Since ATMD is a newly established company, there will be a transitional period for account setup on both its suppliers and customers’ systems. Atlantic will continue conducting its business with its customers during this transitional period. The transitional period has been completed as of December 31, 2012. Atlantic integrated around 90% of its business relating to procurement of semiconductors and electronic parts from Samsung to ATMD. Since the Company has moved its Samsung sales team to ATMD commencing from April 1, 2012, the Company has compensated ATMD for the services provided to the Company relating to the sales of Samsung memory products during the transitional period. Subsequent to the start of the operations of ATMD, the relationships between sales, the Company’s cost of sales and operating expenses are expected to evolve in accordance with the transition of the Company’s business as described above.

Jussey Investments Limited

Jussey, a holding company incorporated in British Virgin Islands, which is wholly owned by the Company, owns 100% equity interest in eVision Telecom Limited (“eVision”), a Hong Kong incorporated company, and 80% equity interest in USmart Electronic Products Limited, a Hong Kong incorporated company, which owns 100% equity interest of Dongguan Kezheng Electronics Limited, a wholly foreign-owned enterprise (“WFOE”) organized under the laws of the PRC (USmart Electronic Products Limited and Dongguan Kezheng Electronics Limited are together referring as “USmart” hereafter.). Hence, Jussey indirectly owns 80% of Kezheng.

USmart Electronic Products Limited & Dongguan Kezheng Electronics Limited

USmart was founded in 2006 and it conducts its business through either itself or Kezheng, which has a factory located in Dongguan, PRC. USmart provides Research and Development (“R&D”) and both ODM (Original Design Manufacturing) and OEM (Original Equipment Manufacturing) services for the three “C” products – Computers, Communications and Consumer electronics devices, such as tablets, portable media players, digital photo frames, and smartphones. USmart has its own R&D and production teams. With the support from eVision, the business of which is described below, USmart is capable of providing its customers with total solutions from design to manufacturing. USmart holds its own brands – USmart and VSmart, which can be used on a broad spectrum of products including memory storage devices, visual and audio products such as digital flat screen television, DAB (Digital Audio Broadcasting) radios, digital photo frames, and other home electronic products. In 2010, USmart began its business development in the telecommunication industry, and successfully obtained the W-CDMA (Wideband Code Division Multiple Access is one of the third-generation (“3G”) wireless standards) license from Intel Mobile Communications GmbH., which offers cellular platforms for global phone makers. W-CDMA baseband is adapted by China Unicom, one of the three major telecommunication carriers in the PRC.

| 3 |

eVision Telecom Limited

Founded in 2011, eVision is a Hong Kong based solution house that specializes in CDMA2000 (also known as Evolution-Data Optimized or “EV-DO”) platform. CDMA2000 is one of the 3G wireless standards. This standard was adapted by China Telecom, one of the three major telecommunication carriers in China. The principal function of eVision is to provide CDMA2000 solutions to USmart. In May 2011, eVision entered into an exclusive R&D servicing agreement (the “Servicing Agreement”) with an independent third party in the PRC (the “R&D House”), a solution house that works closely with South China University of Technology and has a R&D team consisting of members with advanced academic qualifications. On behalf of eVision, the R&D House holds a CDMA2000 software license granted by VIA Telecom Co. Ltd. According to the Servicing Agreement, the R&D House provides R&D services relating to CDMA2000 technology exclusively to eVision, and eVision holds the sole and exclusive right, title and interest to and in the aforementioned license and any R&D results/products obtained or developed by the R&D House during the term of the Servicing Agreement. eVision will also hold all the intellectual property rights that are obtained or developed by the R&D House in the course of such research.

Key Events

ATMD, Joint Venture with Tomen

On March 9, 2012, ACL Holdings entered a Shareholders’ Agreement with Tomen regarding to the setup arrangement of the new joint venture, ATMD. The following is a summary of the material terms of the Shareholders’ Agreement.

Capital Contribution

Pursuant to the Shareholders’ Agreement, ACL Holdings and Tomen own 30% and 70%, respectively, of the equity interest of ATMD. The authorized share capital of ATMD is USD10 million, divided into 10 million ordinary shares of USD1.0 per share. 3 million and 7 million shares will be issued to ACL Holdings and Tomen, respectively, upon payments of capital contributions of USD3 million and USD7 million by ACL Holdings and Tomen, respectively.

Business of ATMD

ATMD is engaged in the business of sales and distribution in China, Hong Kong and Macau (collectively, the “Territory”) of certain semiconductors and electronics parts manufactured by Samsung under a certain distribution agreement with Samsung. To facilitate its business, ATMD has formed a wholly owned subsidiary incorporated in Shenzhen, China (the “PRC Subsidiary”).

Obligations of Both Parties In Connection With the ATMD’s Business

In addition to cash contributions, ACL Holding agreed to cause Atlantic to integrate its entire business relating to purchasing semiconductors and electronic parts from Samsung and selling them to customers in the Territory as a Samsung distributor and to transfer to ATMD its entire clientele (starting from April 1, 2012 (the “Effective Date”)), and Tomen agreed to transfer some or all of its non-Japanese clientele to ATMD starting from the Effective Date. Notwithstanding the foregoing, any outstanding customer agreement existing as of the Effective Date to which either Tomen or Atlantic is bound will continue to be performed by such party. Failure in fulfilling the foregoing respective agreements will give ACL Holdings or Tomen a right to terminate the Agreement in accordance with the terms thereof. Both parties agreed not to be engaged in any business competing with ATMD’s business as set forth in the Agreement.

Pursuant to the Shareholders’ Agreement, Tomen is responsible for securing financing for ATMD when necessary and ACL Holdings is responsible for promoting the sales of Samsung products and developing new customers in the Territory, on a best effort basis. No party is entitled to any fee or compensation with respect to its performance of the foregoing obligations under the Agreement.

Corporate Governance of ATMD

The business of ATMD is managed by the board of directors, which may consist of up to 7 directors, among which 5 directors will be appointed by Tomen and 2 directors will be appointed by ACL Holdings. All 7 directors have been appointed. Mr. Chung-Lun Yang, the Chairman of the Board of Directors, and Mr. Kenneth Lap Yin Chan, the Chief Operating Officer were appointed as ATMD’s directors.

ATMD will have two executive officers, namely, the Chief Executive Officer and Chief Financial Officer. ACL Holding is entitled to appoint one director to be the Chief Executive Officer and Tomen is entitled to appoint one director to be the Chief Financial Officer of ATMD.

| 4 |

Transfer of Shares of ATMD

Each party has the right of first refusal in the event the other party proposed to sell its ATMD shares pursuant to the terms of the Shareholders’ Agreement.

Termination of the Shareholders’ Agreement

The Shareholders’ Agreement contains ordinary termination causes regarding dissolution or bankruptcy of ACL Holdings, Tomen, ATMD or the PRC Subsidiary. Furthermore, the Shareholders’ Agreement provides that either party can terminate the Shareholders’ Agreement if (i) the Samsung products ceased to be available to ATMD or (ii) the profitability of ATMD and its PRC Subsidiary is not satisfactory in the opinion of either party, provided a party may not terminate the Shareholders’ Agreement based on profitability before the third anniversary of the Shareholders’ Agreement.

Acquisition of Jussey

On September 28, 2012, ACL Holdings entered into a Share Purchase Agreement (the “SPA”), pursuant to which ACL Holdings acquired 100% of outstanding equity of Jussey. Under the terms of the SPA, ACL Holdings purchased 100% outstanding equity of Jussey from an individual for an aggregate purchase consideration of approximately USD2,150,000.

Products

The primary products the Company’s subsidiaries and joint venture distribute and sell as of December 31, 2012 are described as follows:

Atlantic Components Limited

Since ATMD is a newly established company, there was a transitional period for account setup on both its suppliers and customers’ systems. Atlantic had been conducting Samsung distributor related business with its customers during the transitional period. The transitional period has been completed as of December 31, 2012.

After the distributor agreement expired, Atlantic transformed its position from Samsung memory products distributor to a general memory products distributor, and continues its business by providing various brands of memory products to its customers.

The primary products for Atlantic consist of the followings:

DRAM

Dynamic Random Access Memory (DRAM) is a type of random-access memory that stores each bit of data in a separate capacitor within an integrated circuit. The capacitor can be either charged or discharged; these two states are taken to represent the two values of a bit, conventionally called 0 and 1. Since capacitors leak charge, the information eventually fades unless the capacitor charge is refreshed periodically. Since the application range for DRAM is very broad, it is classified into three main categories, namely Computing DRAM, Consumer DRAM and Graphics DRAM.

Computing DRAM

Computing DRAM is widely used memory component in servers and personal computers (PC) such as desktops and notebooks.

Consumer DRAM

Consumer DRAM is the widely used memory components in consumer products such as Set-Top Boxes (STB), Digital TVs, High Definition TVs (HDTV), Digital Still Cameras (DSC), Video Cameras, Digital Single-Lens Reflex (DSLR) Cameras, Navigation devices (such as Global Positioning System (GPS), GLONASS and Galileo), and as well as the automotive industry.

Graphics DRAM

Graphics DRAM is a special purpose Double Data Rate (DDR) DRAM that is used in graphics-intensive products which require high-speed 3-dimensional calculation performance and a large memory size to be used as data storage buffer, such as for DVD and computer game displays.

| 5 |

Currently, the Computing and Consumer DRAM markets have been dominated by DDR3. The Synchronous Dynamic Random Access Memory (SDRAM), DDR and DDR2 are nearly fading out in the market. The Graphics DRAM market has been dominated by GDDR3 and GDDR5. The GDDR 2 is nearly fading out in the market.

NAND Flash

NAND Flash memory is a specialized type of memory component used to store user data and program code; it retains this information even when the power is off. Although NAND Flash is predominantly used in mobile phones and tablets, it is also commonly used in multimedia digital storage applications for products such as MP3 players, DSC, Digital Voice Recorders, USB Disks, Flash memory cards, solid-state drives (SSD), etc. Flash cards such as the micro SD cards, SD cards, and CF cards are widely used for digital cameras, mobile phones, portable game consoles, MP3 players, etc. In addition, the Company expects that mobile phones, particularly smartphones, and tablets to create impressive NAND Flash revenue growth in the coming year. Samsung is the major supplier in the world of Flash products. In the third quarter of 2012, Samsung’s NAND Flash revenue was approximately USD1,821 million, representing 39.3% of NAND Flash’s market share.

LCD Panel

LCD panel is a major component in visual consumer electronics products such as LCD TVs, tablets, smartphones, notebooks, digital phone frames, portable game consoles, etc.

USmart Electronic Products Limited, Dongguan Kezheng Electronics Limited & eVision Telecom Limited

The primary products for USmart and eVision consist of the followings:

Research & Development

USmart primary focus its R&D on providing smartphone solution under the Intel’s 3G baseband license, whereas eVision focus on providing smartphone solution under the VIA’s 3G baseband license.

Manufacturing Services

OEM (Original Equipment Manufacturing) services where USmart manufactures products or components to its customers to sell under its customers’ brand name. USmart has provided OEM services for various electronic products such as computer and peripherals, flash storage devices, smartphones and home electronic products.

ODM (Original Design Manufacturing) services where USmart designs and manufactures a product which is specified and eventually branded by another firm for sale. USmart has provided ODM services for various electronic products such as computer and peripherals, flash storage devices, smartphones and home electronic products.

Industry Background

Memory products are integral to a wide variety of consumer and industrial applications, including: personal computer systems, workstations and servers, and handheld devices such as notebooks, netbooks, tablets, smartphones, e-Readers, etc. A market trend of increasingly high-throughput applications (including data processing applications, mobile applications, digital consumer electronics, graphics applications, etc) is creating demand for high performance memory products. At present, NAND Flash, DDR2 DRAM, DDR3 DRAM and GDDR5 DRAM are the dominant memory products used with high-throughput applications and Samsung is the world’s largest developer and manufacturer of these memory products.

| 6 |

Our Strategy

For the memory products business, the Company intends to, through operation of USmart and eVision, continue to provide its customers with a reliable source of memory products. For the R&D and manufacturing businesses, the Company intends to focus on research and development and manufacturing smartphone products.

The Company intends to implement the strategies by:

| · | Leverage network to become a leading smartphone solution provider; | |

| · | Capitalize on rapid migration of manufacturers to China and companies seeking to expand their international market coverage; | |

| · | Further consolidate leadership position by carrying best-in-class products from highly reputable brands and providing superior customer service; | |

| · | Maintain optimal product mix with diversified lifecycles to maximize sales as new and groundbreaking technology is introduced; and | |

| · | Provide “Total Memory Solutions” for computer, consumer electronic appliances and communications devices manufacturers. |

Competitive Strengths

The Company believes there are several key factors that will continue to differentiate us from its competitors in Hong Kong and PRC:

| · | There are currently five types of 3G wireless standards in the telecommunication industry. Three of them are adapted in China by the major mobile network carriers, China Unicom, China Telecom and China Mobile. The Company, through USmart and eVision, has access to two of the three 3G wireless standards, namely, WCDMA and CDMA2000 for its smartphones development. | |

| · | eVision has a strong R&D team specializing in the WCDA mobile network, while exclusively appointed an R&D House specializing in CDMA2000 mobile network that works closely with South China University of Technology. This R&D House has a R&D team consisting of members with advanced academic qualifications. |

In addition, compared with Atlantic, ATMD, the Company’s joined venture with Tomen, has an expanded product portfolio, the Company believes it has competitive advantages over its competitors in Greater China region. As the world’s largest memory products manufacturer, Samsung’s memory products are competitively priced and have an established reputation for product quality and brand name recognition in the retail and PC/Server OEM & Consumer Electronic segments. ATMD, as one of the largest distributors of Samsung’s memory products for Hong Kong and Southern China markets, is expected to be in a highly competitive position compared to other U.S., European, Japanese and Taiwanese memory products manufacturers and distributors.

Sales and Marketing

As of December 31, 2012, the Company employed a total of 5 full time sales and marketing personnel, each of whom has several years experience in the memory products and manufacturing industry. 2 of these salespeople are stationed in the Company’s headquarters in Hong Kong, and 3 of them work out of the Company’s China offices. These sales personnel co-operate with consumer electronics retailers and manufacturers, and International Purchase Offices to ensure that clients are supplied promptly with our products.

| 7 |

Research and Development

The Company is currently focusing its resources on research and development of middle to high-end smartphone solutions for WCDMA and CDMA2000 networks. Our in-house R&D team is focusing on research and development of solutions for WCDMA network, whereas the R&D House exclusively performs service to the Company is focusing on research and development of solutions for CDMA2000 network. The Company expects to continue to make substantial investments in research and development and to participate in the development of new and existing industry standards.

As of December 31, 2012, the research and development team consisted of 6 full time engineers and technical staff, and 20 engineers and technical staff working in its appointed R&D House.

The research and development expenses since September 27, 2012, the date of the Company acquired the manufacturing facility is $184,392.

Manufacturing

The manufacturing facility partially owned by the Company is located in the city of Dongguan in Guangdong Province. The manufacturing facility was awarded ISO 9001 certification for its production process and its production lines are RoHS (lead free) compliant to comply with today’s world environmental trends and standards.

The Company has its own quality control team to control quality and improve yields. This team consisted of 5 full time employees in China.

Competition

The memory products industry in Hong Kong and Southern China markets is very competitive. The Company competes with other memory products distributors, consumer electronics manufacturers, and smartphone research and development solution houses, many of which have substantially greater financial, technical, marketing, distribution channels and other resources.

Memory products, such as NAND flash, compete on the basis of product availability, price and customer service. We believe that we compete effectively with respect to each of these competitive factors. Price competition is significant and is expected to continue. Since we have been in the industry for over 20 years, we have maintained good connections with other distributors and memory products manufacturers on sourcing the requested products for our customers. In order to differ ourselves from the other competitors, we have maintained high quality customer service and employed a team of field application engineers to ensure the products we sourced are authentic and reduce the risk of malfunctioning on our customer’s products. The Company’s principal competitors also include the other non-exclusive distributors of Samsung memory products in the Hong Kong and Southern China markets.

The smartphones industry in the China market is also highly competitive and has been characterized by price competition, manufacturing capacity constraints and product availability constraints at various times. There are currently five types of 3G wireless standards in the telecommunication industry. Three of them are adopted in China by the major mobile network carriers, China Unicom, China Telecom and China Mobile. Currently, the Company has access to two of the three 3G wireless standards, namely, WCDMA and CDMA2000 from Intel and VIA respectively for its smartphones development. Intel and VIA may at its sole discretion increase the number of licensees in China, which would result in an increased competition for the Company. The Company’s principal competitors are other smartphone solution providers such as Cellon, Coolpal, and SIMCOM.

Seasonality

The memory products industry and smartphones industry are increasingly characterized by seasonality and wide fluctuations in supply and demand. Since a significant portion of our revenue is from consumer markets, our business may be subject to seasonally lower revenues in certain quarters of our fiscal year. The industry has also been impacted by significant shifts in consumer demand due to economic downturns or other factors, which may result in diminished product demand and production over-capacity. In recent periods, weakness in the general economic condition has had a more significant impact on our results than seasonality, and has made it difficult to assess the impact of seasonal factors on our business.

Market Research

The Company invests significant resources in market research to provide prompt and accurate market intelligence and feedback on a daily, weekly and monthly basis in order to assist the management in production planning and product allocation functions.

| 8 |

Suppliers

As of December 31, 2012, the majority of the Company’s distributed products was Samsung memory products. Since 1993, our procurement operations have been supported by Samsung. As of April 1, 2012, the Company established ATMD, a joint venture company incorporated in Hong Kong, integrated both Atlantic and Tomen’s Samsung memory business in Hong Kong and PRC regions. On April 1, 2012, ATMD entered into a distribution agreement with Samsung Electronics Hong Kong Co., Ltd. and began to sell and distribute Samsung’s products to the Greater China market, as consented to and approved by Samsung. Atlanitc’s distribution agreement with Samsung has been terminated on June 30, 2012. After the termination of Samsung distribution, Atlantic purchases the Samsung memory products from Tomen instead. In addition to Samsung-branded products, ATMD will sell products of other brands such as SAMCO and SMD.

Customers

As of April 15, 2013, the Company had approximately 50 customers in Hong Kong and Southern China, the majority of whom are memory product distributors and Consumer Electronics manufacturers. Other than the Company’s most significant two customers who accounted for 45% and 29% of the Company’s net sales for the year ended December 31, 2012, no other customer accounted for more than 25% of the Company’s net sales for 2012 and 2011. In order to control the Company’s credit risks, the Company does not offer any credit terms to its customers other than a small number of clients who have long-established business relationships with the Company. With the establishment of ATMD, the Company has shared and transferred the customer base related to Samsung distributorship business to ATMD. The Company and Tomen will contribute the majority of ATMD’s customers to ATMD’s customer base.

Government Regulation

As of December 31, 2012, the Company’s business operations were not subject to the regulations of any jurisdiction other than Hong Kong SAR and the PRC. The Company executes its sales contracts and delivers its products in Hong Kong and PRC for its Chinese customers and there have been no restrictions imposed on the Company by the PRC authorities with respect to the Company’s pursuit of business growth and opportunities in China.

Employees

As of December 31, 2012, the Company had a total of 81 full time employees in Hong Kong and PRC, including 5 employees in sales and marketing, 4 employees in procurement, 32 employees in administration and accounts, 15 employees in engineering, 5 employees in quality control, 17 employees in production, 3 employees in customer service and liaison. None of the Company employees are represented by labor unions. Pursuant to the joint venture agreement, the Company had integrated Atlantic’s business with ATMD and transferred most of Atlantic’s employees in the sales, marketing and engineering departments to ATMD. After the ATMD was established, Atlantic had a total of 21 full time employees in Hong Kong and PRC, including 17 employees in administration and accounting, and 4 employees in engineering. As of September 28, 2012, the Company expanded the operations group by acquiring Jussey and increased the number of full time employees by 60. The Company has never experienced any work stoppage and believes that our employee relations are favorable.

The Company’s primary hiring sources for its employees include referrals from existing employees, print and internet advertising and direct recruiting. All of the Company’s employees are highly skilled and educated and subject to rigorous recruiting standards appropriate for a company involved in the distribution of brand name memory products. The Company attracts talent from numerous sources, including higher learning institutions, colleges and industry. Competition for these employees is intense. The Company believes its relationship with its employees to be good. However, the Company’s ability to achieve its financial and operational objectives depends in large part upon its continuing ability to attract, integrate, retain and motivate highly qualified personnel, and upon the continued service of its senior management and key personnel, especially Mr. Yang.

| 9 |

| Item 1A. | Risk Factors |

We are subject to a number of risks. Some of these risks are endemic to the high-technology and semiconductor industry and are the same or similar to those disclosed in our previous SEC filings. This section should be read in conjunction with the consolidated financial statements and the accompanying notes thereto, and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included in this Annual Report. The risks and uncertainties set out below are not the only risks and uncertainties we face. Our business could be harmed by any of these risks. The trading price of our common stock could decline due to any of these risks and investors may lose all or part of their investment. The information included in this Annual Report is provided as of the filing date with the SEC and future events or circumstances could differ significantly from the forward-looking statements included herein.

Risks Related to Our Business

Our independent auditor has issued a going concern opinion after auditing our financial statements; our ability to continue is dependent on our ability to raise additional capital and our operations could be curtailed if we are unable to obtain required additional funding when needed.

As of December 31, 2012, the Company has total current assets of $8,098,594 and current liabilities of $36,779,064. This raises substantial doubt about the Company’s ability to continue as a going concern. The Company is attempting to address its lack of liquidity by raising additional funds, either in the form of debt or equity or some combination thereof. Any additional equity financing may involve substantial dilution to our then existing shareholders. We currently have no agreements or arrangements with respect to any such financing and there can be no assurance that any needed funds will be available to us on acceptable terms or at all. Our failure to raise additional funds in the future will adversely affect our business operations, and may require us to suspend our operations. After auditing our financial statements, our independent auditor issued a going concern opinion and our ability to continue is dependent on our ability to raise additional capital. If we are unable to obtain necessary financing or working capital in the future, we will likely be required to curtail our development plans.

We hold a minority interest in the newly established ATMD, and entering into the Joint Venture Agreement has exposed the Company to various risks.

On March 9, 2012, ACL Holdings entered into an agreement with Tomen Devices Corporation (“Tomen”) to create a joint venture (the “Joint Venture Agreement”), ATMD, which became effective on April 1 2012. ACL Holdings and Tomen own 30% and 70%, respectively, of the equity interest of ATMD.

ATMD had entered into a distribution agreement with Samsung and started to sell and distribute Samsung’s products to the Greater China market, as consented to and approved by Samsung. Atlantic has discontinued its contractual relationship with Samsung under its distribution agreement. Since the Joint Venture Agreement contains non-compete provisions that prohibit ACL Holdings from working with ATMD’s suppliers, which provisions will limit our Company’s continuing business engagement as a distributor of semiconductor products. In addition, pursuant to the Joint Venture Agreement, Atlantic has transferred to ATMD its existing customer base and employees in the sales and engineering departments, which for an indefinite period of time will materially affect Atlantic’s ability to generate significant revenues. The Company may consider engaging suppliers that do not have a business relationship with ATMD, as well as exploring other business opportunities such as acquiring suitable target companies to broaden its business portfolio. However, there is no assurance that the Company may succeed in doing so or achieving and maintaining its profitability.

As Tomen owns a majority interest in ATMD and exercises voting control over most matters put to a vote of stockholders, the votes cast by Tomen may not be in the best interests for ACL holding as a minority stockholder. Tomen also has the right to appoint 5 directors out of a total number of 7 board members of ATMD and thereby control ATMD. Even though Mr. Yang, the Company’s Chairman of the Board of Directors will be the Chief Executive Officer of ATMD, there is no assurance that the board of the ATMD will be able to lead ATMD to business success. In the event we discontinue our involvement in the management of ATMD for any reason, we cannot provide assurance that new management will possess the skills, qualifications or abilities necessary to profitably operate such business.

The joint venture with Tomen is a new business model that we adopted and there is no assurance such model will be successful in the future. The joint venture may be terminated without other party’s prior consent, as either party can terminate the Joint Venture Agreement if (i) the Samsung products ceased to be available to ATMD or (ii) the profitability of ATMD and its PRC Subsidiary is not satisfactory in the opinion of either party, provided a party may not terminate the Agreement based on profitability before the third anniversary of the Agreement. In the event the joint venture is terminated for any reason, there is no assurance that we may obtain full recovery of our contribution and investment, nor is there any assurance that the Company may continue to work with Samsung and resume as its authorized distributor. In the event the joint venture is terminated and we cannot reconnect with Samsung, the Company’s financial conditions and operations will be materially affected.

| 10 |

The Joint Venture Agreement provides that each party to the agreement will bear the excess liabilities in proportion to their percentage interests in the event the joint venture does not have sufficient assets to repay its debts upon liquidation. Since Tomen controls the board and has broad powers to incur debts, if ATMD does not have sufficient assets to cover such debts upon liquidation, the Company will be responsible for part of the debts even though it did not vote for such debts at the board level. The assumption of such liabilities may also have negative impact on the Company’s financial conditions.

Lastly, pursuant to the Joint Venture Agreement, the Board of ATMD has the power to prohibit any transfer of the shares. As the Board is controlled by Tomen, Tomen may, in its sole discretion, deny any proposed sale of shares held by ACL Holdings.

We are expected to experience significant decrease in sales revenues because we hold a minority interest in ATMD and cannot consolidate with its financial results.

As of December 31, 2012, all of Atlantic’s Samsung distributor business has been transferred to ATMD. We expect to experience significant decrease in sales revenues after such transfer, because we only hold a minority interest in ATMD and cannot consolidate our financial results with ATMD’s, including its sales revenues.

If ATMD’s relationship with Samsung is terminated or deteriorated, our financial conditions will be materially adversely affected.

ATMD relies ultimately on Samsung to provide it with products for distribution to its clients.

Although Samsung has renewed distribution agreement with Atlantic in the past, no assurances can be given that Samsung will definitely renew the distribution Agreement with ATMD. In addition, even if such agreement is renewed, no assurance can be given that the terms will be satisfactory to us.

Samsung has the right to increase the number of distributors of its memory products in Hong Kong and the Southern China markets without consulting us. If Samsung significantly increases the number of authorized distributors of its memory products, competition among Samsung distributors would increase and ATMD may not be able to operate profitably.

If Samsung is unable to respond to customer demand for diversified products or is unable to do so in a cost-effective manner, ATMD may lose market share and our financial conditions may be adversely affected.

In recent periods, the market has become relatively segmented, with diverse products need being driven by the different requirements of applications such as desktop and notebook PCs, netbooks, servers, workstations, handheld devices, and communications and industrial applications that demand specific solutions.

Samsung needs to dedicate significant resources to product design and development to respond to customer demand for the continued diversification of memory products. If Samsung is unable or unwilling to invest sufficient resources to meet the diverse memory needs of customers, we, as a major Samsung memory products distributor may lose market share. In addition, as ATMD diversifies its product lines, it may encounter difficulties penetrating certain markets, particularly markets where it does not have existing customers. If ATMD is unable to respond to customer demand for market diversification in a cost-effective manner, the results of its operations and accordingly our financial conditions may be adversely affected.

If Samsung’s global allocation process results in Samsung not having sufficient supplies of memory products to meet all of our customer orders, this would have a negative impact on our sales and could result in our loss of customers. However, such shortages are infrequent. On the other hand, no assurance can be given that such shortages will not occur in the future.

If Samsung’s manufacturing process is disrupted, the results of ATMD operations, cash flows and financial condition could be adversely affected.

Samsung manufactures products using highly complex processes that require technologically advanced equipment and continuous modification to improve yields and performance. Difficulties in the manufacturing process can reduce yields or disrupt production. ATMD may be unable to meet its customers’ requirements and they may purchase products from other suppliers. This could result in loss of revenues or affect its customer relationships. Additionally, any future health-related disruptions at Samsung’s manufacturers or other key suppliers could affect its ability to supply ATMD with products in a timely manner, which would harm its results of operations. It may lose orders from its customers and/or may incur compensation to those customers due to delay in delivery, and may have a negative impact on its financial results and positions.

| 11 |

ATMD is heavily dependent on major supplier, Samsung, and factors affecting Samsung could have a great impact on its business operations.

Samsung is the major supplier of ATMD’s products and therefore any factors that impact Samsung could have a great impact on ATMD’s business operations. For example, Samsung relies heavily on silicon wafer producers to produce the raw material, silicon wafers, for its products that we distribute, therefore, earthquakes, typhoons or other natural disasters in areas where silicon wafer are produced would affect Samsung’s supply of silicon wafers, which in turn, would negatively impact our business, financial condition, and operational results. For example, the 2011 earthquake and tsunami in Japan have adversely impacted Samsung’s suppliers located in Japan and its ability to source parts from companies located in Japan.

USmart and eVision are also dependent on Samsung to provide them with application processors.

The majority of solutions provided by USmart and eVision are Android based and the major components include application processors provided by Samsung. Should there be any disruption in the supply of such processors from Samsung during the fulfillment of orders, USmart and eVision may lose its orders from customers and/or may incur compensation to those customers due to delay in delivery, and may have a negative impact on its financial results and positions.

If the growth rate of either memory products or other components sold or the amount of memory or components used in each application decreases, sales of our products could decrease.

The Company and its joint venture, ATMD, are dependent on the computer and consumer electronics market as many of the products that we distribute are used in PCs, smartphones, or other consumer electronics. DRAMs are the most widely used semiconductor components in PCs. Flash products are mostly used in the consumer electronics products. Wifi and Camera modules are highly used in smartphones. LCD panels are used in many visual products, such as smartphones, tablets, and netbooks. If there is a continued reduction in the growth rate of the related consumer electronics markets, sales of our products built for those markets would decrease, and, as a result, our operations, cash flows and financial condition could be adversely affected.

The demand from the end-products that uses our solutions depends on many factors.

The demand from the end-products that use our solutions depend on many factors such as economic climate, change in technology, competiveness of competitors, etc. If such demand decreases as a result of negative impact from these factors, it will affect revenue, cash flows and financial conditions of the Company, and may adversely affect the Company’s share price.

The solutions provided by us rely on the licenses from Intel Mobile Communications GmbH. and VIA Telecom Co., Ltd, which we could lose.

The majority of solutions provided by USmart are under licenses from Intel Mobile Communications GmbH (“Intel”). Where as, the majority of solutions provided by eVision are under licenses from VIA Telecom Co. (“VIA”) Ltd. If such licenses are revoked or expire without renewal, USmart and eVision will not be able to provide those solutions to its customers and may result in loss of revenue and profits which will have a negative impact to its financial results and positions.

Competitive level is uncontrollable.

Business in telecommunication industry highly relies on the baseband license acquired from Intel. The current CDMA license providers are Intel, VIA and T3G Technology Co., Ltd. in China. USmart cannot control how many licensees the license providers authorized. If the number of licensees increases, it may increases the competition and result in loss of revenue and profits which may have a negative impact to its financial results and positions.

Our research and development may be costly and/or untimely, and there are no assurances that our research and development will either be successful or completed within the anticipated timeframe, if at all.

Our recent acquired business relies on research and development activities. The research and development of new products play an important role for our company. Development of new products requires significant research and development. If we are unable to perform research and development successfully, our business and results of operations could be negatively impacted.

The research and development of new products is costly and time consuming, and there are no assurances that our research and development of new products will either be successful or completed within the anticipated time frame, if at all. There are also no assurances that if the product is developed, that it will lead to actual commercialization and sales.

| 12 |

We are heavily dependent upon the electronics industry, and excess capacity or decreased demand for products produced by this industry could result in increased price competition as well as a decrease in our gross margins and unit volume sales.

Our business is heavily dependent on the electronics industry. The majority of our revenue is generated from the networking, high-end computing and computer peripherals segments of the electronics industry, which are characterized by intense competition, relatively short product life-cycles and significant fluctuations in product demand. Furthermore, these segments are subject to economic cycles, which have occurred in the past and are likely to occur in the future. A recession or any other event leading to excess capacity or a downturn in these segments of the electronics industry could result in intensified price competition, a decrease in our gross margins and unit volume sales and materially affect our business, prospects, financial condition and results of operations.

The memory product industry is highly competitive.

The Company and its joint venture, ATMD, face intense competition from a number of companies, some of which are large corporations or conglomerates, that may have greater resources to withstand downturns in the semiconductor memory market, invest in technology and capitalize on growth opportunities. To the extent Samsung memory products become less competitive, our ability to effectively compete against distributors of other memory products will diminish.

We face competition from other telecommunication and computer manufacturers.

We face competition from other telecom and computer manufacturers in China, particularly in the telecommunication sector. There are three major telecommunication companies in China and they can also provide R&D, manufacturing and marketing services to smartphone and other accessories that we feature. This competition may affect our ability to attract and retain customers and buyers and may reduce the prices we are able to charge. An inability to compete effectively could adversely affect our business, financial condition and results of operations.

We are operating in an industry with very short life cycle.

The mobile devices industry in which the newly acquired business is operating has a very short product life cycle. Inability to respond to an end of a product life cycle may result in the loss of revenue and profits which may have a negative impact to its financial results and positions.

We are operating in an industry with high demand in product features upgrade and fast generation change.

The telecommunication industry in which our recently acquired business is operating has high demand in product features upgrade and fast generation change. Inability to respond to the features upgrade and generation change may result in the loss of revenue and profits which may have a negative impact to its financial results and positions.

If our current product strategy and operating system strategy are not successful, our telecommunication business could be negatively impacted.

Our current strategy is to concentrate our mobile solution on smartphones and to use third-party and/or open-source operating systems and associated application ecosystems, predominantly the Google Android operating system (a royalty-free open-source platform). As a result, we are dependent on third-parties’ continued development of operating systems, software application ecosystem infrastructures and such third-parties’ approval of our implementations of their operating system and associated applications. If we had to change our strategy, our financial results could be negatively impacted because a resulting shift away from using Android and the associated applications ecosystem could be costly and difficult. A strategy shift could increase the burden of development to the Company and potentially create a gap in our portfolio for a period of time, which could competitively disadvantage the Company.

We are at risk if Android-based smartphones do not remain competitive in the marketplace. Even if Android-based smartphones remain competitive, the Android operating system is an open-source platform and many other companies sell competing Android-based smartphones solutions. If the Android-based smartphones solutions of our competitors are more successful than ours, our financial results could be negatively impacted. It is also critical to the success of the Android operating system that third-party developers continue to develop and offer applications for this operating system that are competitive with applications developed for other operating systems. From an overall risk perspective, the industry is currently engaged in an extremely competitive phase with respect to operating system platforms, applications and software generally. If Android does not continue to gain operator and/or developer adoption, or any updated versions or new releases of Google’s Android operating system or applications are not made available to us in a timely fashion, the Company could be competitively disadvantaged and our financial results could be negatively impacted.

| 13 |

We may not be able to adequately protect our brand name and intellectual property rights that we developed.

Our brand names and intellectual property rights are important to our business and we rely on them to conduct our business operations. Unauthorized use of our brand names and intellectual property rights by third parties may materially adversely affect our business and reputation. We rely on trademark and copyright laws to protect our intellectual property rights. Despite our precautions, it may be possible for third parties to obtain and use our brand names or intellectual property rights without authorization.

We cannot be assured that third parties will not infringe or misappropriate our brand names or intellectual property rights. We may, at times, have to incur significant legal costs and spend time in defending our trademarks and copyrights. Any defense efforts, whether successful or not, would divert both time and resources from the operation and growth of our business.

Current economic and political conditions may harm our business.

Global economic conditions and the effects of military or terrorist actions may cause significant disruptions to worldwide commerce. If these disruptions result in delays or cancellations of customer orders, a decrease in corporate spending on information technology or our inability to effectively market, manufacture or ship our products, our results of operations, cash flows and financial condition could be adversely affected. There is a risk that the events in Japan could negatively affected semiconductor markets, and may continue to have severe and unpredictable effects on the price of certain raw materials in the future. In addition, our ability to raise capital for working capital purposes and ongoing operations is dependent upon ready access to capital markets. During times of adverse global economic and political conditions, accessibility to capital markets could decrease. If we are unable to access the capital markets over an extended period of time, we may be unable to fund operations, which could materially adversely affect our results of operations, cash flows and financial condition.

We believe that we will require additional equity financing to reduce our long-term debts and implement our business plan.

We anticipate that we will require additional equity financing in order to reduce our long-term debts and implement our business plan of increasing sales in the Southern China markets. There can be no assurance that we will be able to obtain the necessary additional capital on a timely basis or on terms acceptable to us. If we obtain such financing, the holders of our Common Stock may experience substantial dilution.

To finance our new business, debt or equity financing may be required and may adversely impact our share price.

In order to expand the business of USmart and eVision as well as the Company, the Company may need to raise fund in form of equity and/or debt to incur substantial additional indebtedness to finance such expansion. If we or our subsidiaries incur additional debt, the risks that we face as a result of an increased indebtedness could have important consequences to you. For example, it could:

| • | limit our ability to satisfy our obligations under our borrowings; | |

| • | increase our vulnerability to adverse general economic and industry conditions; | |

| • | require us to dedicate a substantial portion of our cash flow from operations to servicing and repaying our indebtedness, thereby reducing the availability of our cash flow to fund working capital, capital expenditures and other general corporate purposes; | |

| • | limit our flexibility in planning for or reacting to changes in our businesses and the industry in which we operate; | |

| • | place us at a competitive disadvantage compared to our competitors that have less debt; | |

| • | limit, along with the restrictive covenants of our indebtedness, among other things, our ability to borrow additional funds or make guarantees; and | |

| • | increase the cost of additional financing. |

Our ability to generate sufficient cash to satisfy our outstanding and future debt obligations will depend upon our future operating performance, which will be affected by prevailing economic conditions and financial, business and other factors, many of which are beyond our control. We anticipate that our operating cash flow will be sufficient to meet our anticipated operating expenses and to service our debt obligations as they become due. However, we may not always be able to generate sufficient cash flow for these purposes. If we are unable to service our indebtedness, we will be forced to adopt an alternative strategy that may include actions such as reducing or delaying capital expenditures, selling assets, restructuring or refinancing our indebtedness or seeking equity capital. These strategies may not be instituted on satisfactory terms, if at all. As a result, the share price may be adversely affected due to increase in gearing or shareholder base.

| 14 |

Risks Relating to the Recent Acquisition

The acquisition may not result in the increase of revenue and profits of the Company.

While the management expects that the acquisition of Jussey will enable the Company to tap into and expand its operations in mobile devices and telecommunication business segments through USmart and eVision, USmart and eVision may not be able to contribute an increase in revenue and profit to the results of the Company as other factors such as changes in future economic climate, intensity of competition from competitors, ability to adapt due to change in technology, number of orders to be received may not be correctly anticipated, which will have a significant impact on the results of USmart and eVision that could generate.

Successful operation of the acquired business is not assured.

Despite that USmart and eVision have orders / projects on hand and pipeline of orders are anticipated, the Company may not be able to expand the business of USmart or eVision beyond these orders / projects and may suffer losses after these orders have been fulfilled as USmart and eVision have operated at a loss making in the past, which may have a significant negative impact to the Company financial position.

Successful integration of the USmart and eVision businesses with our other businesses is not assured.

While management expects that they will be able to integrate the business of USmart and eVision into the Company’s existing trading business within the expected timeframe which would enables the Company to operate more effectively and efficiently and to create synergy hence lower costs of operations, such integration may fail or fail to achieve the desired level of synergy and may increase the overall administrative expenses at a ratio higher than the proportionate revenue and profit contribution from USmart and eVision, and may have significant negative impact to the Company.

USmart and eVision may not be able to distribute dividends to the Company.

USmart and eVision are Hong Kong incorporated company and may distribute retained profits to its shareholders. Since USmart and eVision have been operating at a loss in the past and does not have retained profits available for distribution to the Company, it may not be able to generate enough profits to recover losses from prior years and therefore may not be able to distribute dividends to the Company for further distributions to its shareholders.

A lack of expertise over USmart and eVision financial reporting in U.S. GAAP could result in an inability to accurately report our financial results, which may lead to loss of investor confidence in our financial statements and may adversely affect the Company’s share price.

While the management will pursue to ensure that the financial results of USmart and eVision will be reported accurately under U.S. GAAP, the financial results of USmart and eVision may be inaccurately reported under U.S. GAAP due to lack of U.S. GAAP expertise from USmart and eVision and may adversely affect the Company’s share price, loss of investor confidence and regulatory penalty.

Our ability to execute on our business strategy and growth will depend in part on the success of the telecommunication industry.

The acquisition is part of the Company’s business strategy to grow and expand through access to the telecommunication industry. As a result, the success of USmart and eVision businesses will have a material impact on the overall success of the Company.

| 15 |

Risks Associated With Doing Business in China

There are substantial risks associated with doing business in China, some of which are addressed in the following risk factors.

Economic, political and social conditions, as well as government policies in China could have a material adverse effect on our business, results of operations and financial condition.

Part of our business is conducted in, and part of our revenues is derived from, the PRC.

The economy of the PRC differs from the economies of most developed countries in many respects, including, but not limited to structure, governmental involvement, level of development, growth rate, capital re-investment, allocation of resources, control of foreign currency and rate of inflation. The economy of the PRC has been transitioning from a planned economy to a market-oriented economy. Although in recent years the PRC government has implemented measures emphasizing the utilization of market forces for economic reform, a substantial portion of productive assets in the PRC is still owned by the PRC government. In addition, the PRC government continues to play a significant role in regulating industries by imposing industrial policies. It also exercises significant control over the PRC’s economic growth through allocating resources, controlling payment of foreign currency-denominated obligations, setting monetary policy and providing preferential treatment to particular industries or companies.

Policies and other measures taken by the PRC government to regulate the economy could have a significant negative impact on economic conditions in the PRC, with a resulting negative impact on our business. For example, our business, results of operations and financial condition may be materially and adversely affected by:

| • | new laws and regulations and the interpretations of those laws and regulations; | |

| • | the introduction of measures to control inflation or stimulate growth; | |

| • | changes in the rate or method of taxation; or | |

| • | the imposition of additional restrictions on currency conversions and remittances abroad. |

Macroeconomic measures taken by the PRC government to manage economic growth could have adverse economic consequences.

In response to concerns about the PRC’s high growth rate in industrial production, bank credit, fixed investment and money supply, the PRC government has periodically taken measures to slow economic growth to a more manageable level. Among the measures that the PRC government has taken are restrictions on bank loans in certain sectors. These measures have contributed to a modest slowdown in economic growth in the PRC and a reduction in demand for consumer goods and real property. These measures and any additional measures, including an increase in interest rates, could contribute to a further slowdown in the PRC economy, which could result in a decline in demand for industrial materials and lower revenues for us.

In particular, the State Council has recently announced further macroeconomic measures to control perceived overinvestment in the real property market. The detailed regulations issued by central government agencies to implement these measures include, without limitation, restrictions on foreign investment and strict enforcement of tax collection. We can give you no assurance that these measures and regulations will not adversely affect our business.

The PRC legal system has inherent uncertainties that could negatively impact our business.

Our business is operated through, and our revenues are generated by, our operating subsidiaries in the PRC. Substantially all of our assets are located in the PRC. The PRC legal system is based on written statutes. Prior court decisions may be cited for reference but have limited precedential value. Since 1979, the PRC government has promulgated laws and regulations dealing with economic matters such as foreign investment, corporate organization and governance, commerce, taxation and trade. However, because these laws and regulations are relatively new, and because of the limited volume of published cases and their nonbinding nature, interpretation and enforcement of these laws and regulations involve uncertainties. In addition, as the legal system in China develops, changes in such laws and regulations, their interpretation or their enforcement may have a negative effect on our business, financial condition and results of operations.

| 16 |

It may be difficult to affect service of process upon us or our directors or to enforce any judgments obtained from non-PRC courts.

Our operations are conducted and a substantial part of our assets are located within China. Our key management reside in Hong Kong and China, where substantially all of their assets are located. Investors may experience difficulties in effecting service of process upon us, our directors or our senior management as it may not be possible to affect such service of process outside China. In addition, our PRC counsel has advised us that China does not have treaties with the United States and many other countries providing for reciprocal recognition and enforcement of court judgments. Therefore, recognition and enforcement in China of judgments of a court in the United States or certain other jurisdictions may be difficult or impossible.

Restrictions on foreign currency exchange may limit our ability to obtain and remit foreign currency or to utilize our revenues effectively.

We receive substantially part of our revenues in Renminbi through our ownership and operation of USmart. As a result, any restriction on currency exchange may limit our ability to use revenues generated in Renminbi to service and repay our indebtedness. Our ability to satisfy our debt obligations depends upon the ability of our subsidiaries incorporated in the PRC to obtain and remit sufficient foreign currency. Our subsidiaries incorporated in the PRC must present certain documents to the designated foreign exchange bank before they can obtain and remit foreign currency out of the PRC (including, in the case of dividends, evidence that the relevant PRC taxes have been paid and, in the case of shareholder loans, evidence of the registration of the loan with the State Administration for Foreign Exchange). There can be no assurance that our subsidiaries incorporated in the PRC will not encounter difficulty in the future when undertaking these activities. If our subsidiaries in the PRC are unable to remit dividends to us, we could be unable to make payment of interest on and principal of our indebtedness.

Currency fluctuations and restrictions on currency exchange may adversely affect our business, including limiting our ability to convert Chinese Renminbi into foreign currencies and, if Chinese Renminbi were to decline in value, reducing our revenue in US Dollar terms.

Our reporting currency is the US Dollar and our operations in China use their local currency as their functional currencies. Part of our revenue and expenses in China are in the Chinese currency, the Renminbi. We are subject to the effects of exchange rate fluctuations with respect to any of these currencies. For example, the value of the Renminbi depends to a large extent on Chinese government policies and China’s domestic and international economic and political developments, as well as supply and demand in the local market. Since 1994, the official exchange rate for the conversion of the Renminbi to the US Dollar had generally been stable and the Renminbi had appreciated slightly against the US Dollar. In July 2005, the Chinese government changed its policy of pegging the value of the Renminbi to the US Dollar. Under this policy, which was halted in 2008 due to the worldwide financial crisis, the Renminbi was permitted to fluctuate within a narrow and managed band against a basket of certain foreign currencies. In June 2010, the Chinese government announced its intention to again allow the Renminbi to fluctuate within the 2005 parameters. It is possible that the Chinese government could adopt an even more flexible currency policy, which could result in more significant fluctuation of Renminbi against the US Dollar, or it could adopt a more restrictive policy. We can offer no assurance that the Renminbi will be stable against the US Dollar or any other foreign currency.

Our financial statements are translated into US Dollars at the average exchange rates in each applicable period. To the extent the US Dollar strengthens against foreign currencies, the translation of these foreign currencies denominated transactions results in reduced revenue, operating expenses and net income for our international operations. Similarly, to the extent the US Dollar weakens against foreign currencies, the translation of these foreign currency denominated transactions results in increased revenue, operating expenses and net income for our international operations. We are also exposed to foreign exchange rate fluctuations as we convert the financial statements of our foreign consolidated subsidiaries into US Dollars in consolidation. If there is a change in foreign currency exchange rates, the conversion of the foreign consolidated subsidiaries’ financial statements into US Dollars will lead to a translation gain or loss which is recorded as a component of other comprehensive income. In addition, we have certain assets and liabilities that are denominated in currencies other than the relevant entity’s functional currency. Changes in the functional currency value of these assets and liabilities create fluctuations that will lead to a transaction gain or loss. We have not entered into agreements or purchased instruments to hedge our exchange rate risks, although we may do so in the future. The availability and effectiveness of any hedging transaction may be limited and we may not be able to hedge our exchange rate risks.

The cyclical nature of the telecommunication and computer industry could adversely affect our results of operation.