Exhibit 99.1

FOR IMMEDIATE RELEASE

January 25, 2012

Contact:

Daryl G. Byrd, President and CEO (337) 521-4003

John R. Davis, Senior Executive Vice President (337) 521-4005

IBERIABANK Corporation Reports Fourth Quarter Results

LAFAYETTE, LOUISIANA — IBERIABANK Corporation (NASDAQ: IBKC), holding company of the 124-year-old IBERIABANK (www.iberiabank.com), reported operating results for the fourth quarter ended December 31, 2011. For the quarter, the Company reported income available to common shareholders of $17 million and fully diluted earnings per share (“EPS”) of $0.59. The Company completed the acquisitions of OMNI BANCSHARES, Inc. (“OMNI”) and Cameron Bancshares, Inc. (“Cameron”) on May 31, 2011. Financial statements reflect the impact of those acquisitions beginning on that date. The conversions of branch and operating systems of OMNI and Cameron were successfully completed over the weekends of June 18-19 and July 9-10, respectively. The Company incurred pre-tax acquisition and conversion costs in the fourth quarter of 2011 equal to $4 million, or $0.10 per share on an after-tax basis. Excluding the acquisition and conversion costs, EPS in the fourth quarter of 2011 was $0.69 per share. The average analyst estimate for EPS for the fourth quarter of 2011 as reported in First Call was $0.65 per share.

Daryl G. Byrd, President and Chief Executive Officer commented, “Our Company continues to demonstrate tremendous growth and balance sheet strength during this challenging economic period. Our stellar asset quality ratios continued to show significant improvement throughout the year.” Byrd continued, “We are very proud of our investments and many accomplishments in 2011, and we are optimistic regarding our Company’s prospects for 2012. With great excitement, we will be celebrating our institution’s 125th anniversary on March 12, 2012.”

Highlights for the Fourth Quarter of 2011 and December 31, 2011:

| • | Loan growth of $262 million, or 5%, between quarter-ends (18% annualized rate), excluding loans, OREO, and other assets covered under FDIC loss share agreements (“Covered Assets”). |

| • | Core deposit growth (excluding time deposits) of $280 million, or 4% (17% annualized growth), compared to September 30, 2011. |

| • | Continued asset quality strength; Nonperforming assets (“NPAs”), excluding Covered Assets and impaired loans marked to fair value that were acquired in the OMNI and Cameron acquisitions, equated to 0.87% of total assets at December 31, 2011, compared to 0.89% at September 30, 2011. On that basis, loans past due 30 days or more declined 11%, and restructured loans declined 4% during the fourth quarter of 2011. |

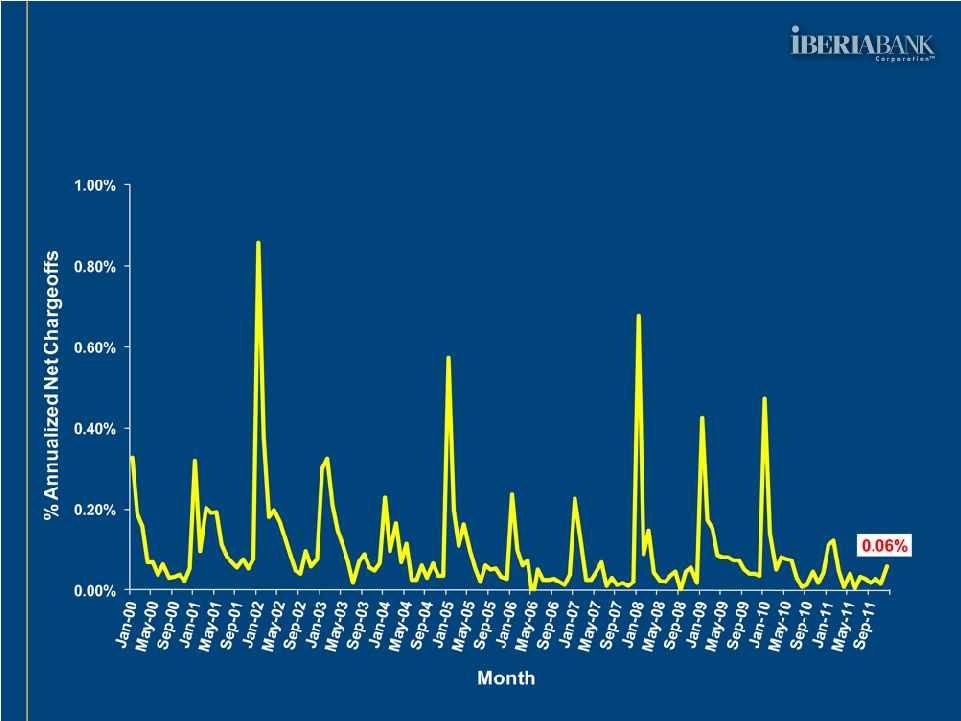

| • | For the year of 2011, net charge-offs excluding Covered Assets were $8 million, or 0.13% of average loans, compared to $27 million, or 0.60% of average loans in 2010. |

| • | Despite the significant improvement in asset quality measures in the legacy and FDIC Covered Assets, the Company incurred net impairment associated with Covered Assets totaling $2 million, or $0.04 per share on an after-tax basis. During the fourth quarter of 2011, the Company also wrote-down four properties formerly used for banking purposes totaling $1 million, or $0.02 per share on an after-tax basis. |

| • | Capital ratios remain strong; At December 31, 2011, the Company’s tangible common equity ratio was 9.52%, tier 1 leverage ratio was 10.45%, and total risk based capital ratio was 16.21%. |

1

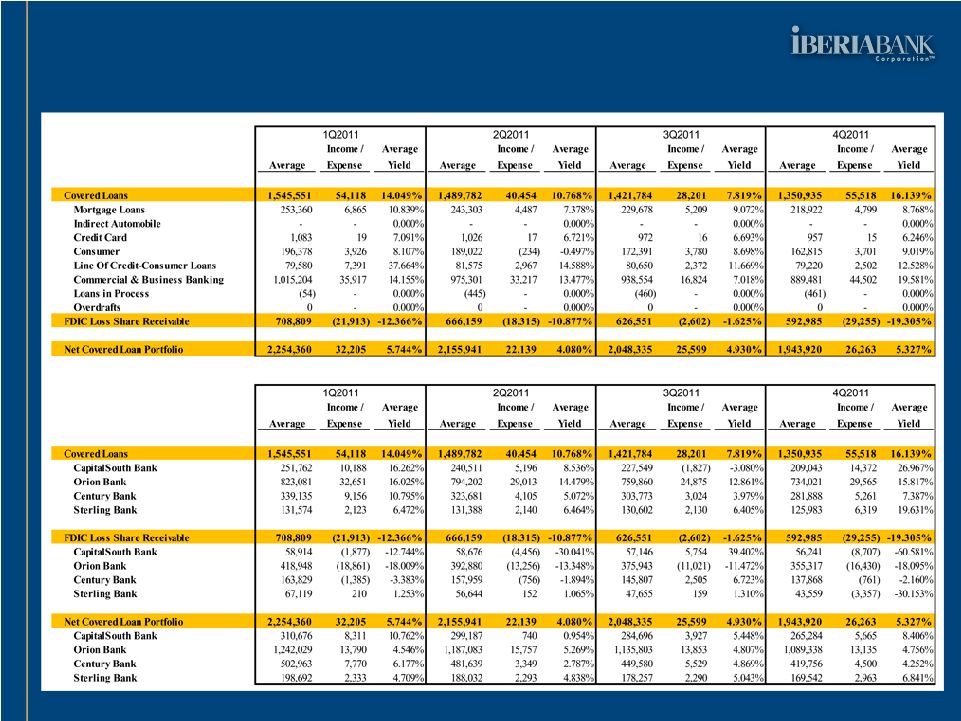

| • | At the time of acquisition of OMNI and Cameron, the Company used preliminary estimates to determine the fair values of assets acquired and liabilities assumed. In accordance with generally accepted accounting principles, acquirers have one year to complete analysis on facts and circumstances that existed at acquisition date and refine those estimates. During the fourth quarter of 2011, the Company performed further analysis that included a refinement of future estimated cash flows, review of loan types, refinement of discounts, losses given default, and underlying collateral values. As a result, the Company increased the original amount of goodwill recorded on Cameron at June 30, 2011 by $20 million and reduced loan interest income in the third quarter of 2011 by $1.5 million. The majority of the $20 million increase in goodwill on Cameron was associated with interest rate mark adjustments. |

| • | As a result of the OMNI and Cameron adjustments to loan interest income, the tax-equivalent net interest margin for the third quarter of 2011, was initially reported as 3.62%, was subsequently adjusted to 3.58%. The margin in the fourth quarter of 2011 was 3.62%. |

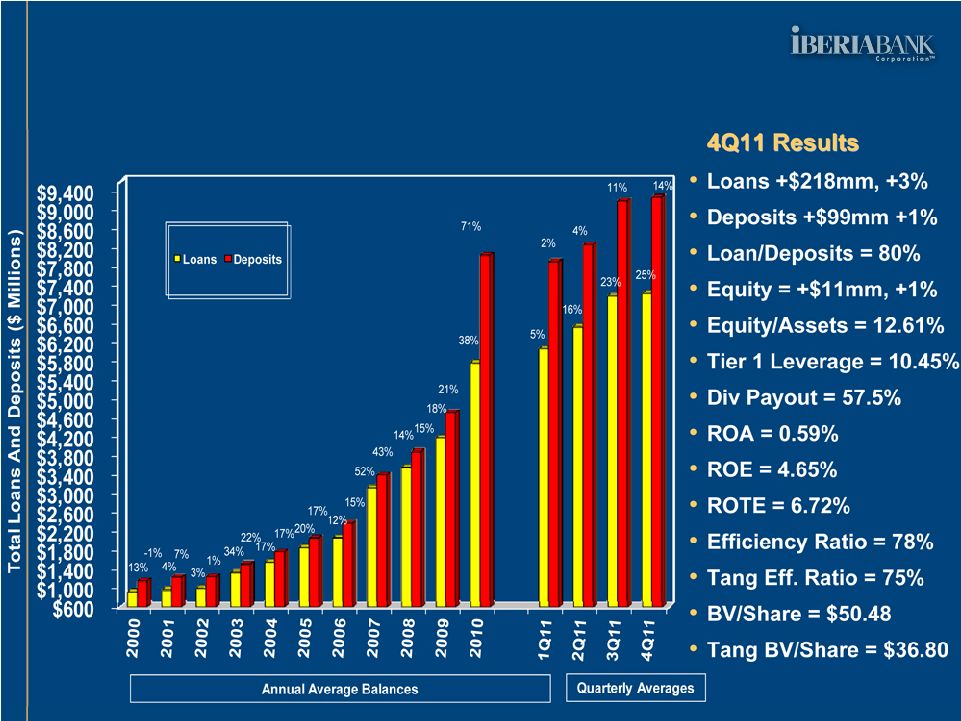

Balance Sheet Summary

Total assets increased $271 million, or 2%, since September 30, 2011, to $11.8 billion at December 31, 2011. Over this period, total loans increased $218 million, or 3%; investment securities decreased $59 million, or 3%; and total deposits increased $99 million, or 1%. Total shareholders’ equity increased $11 million, or 1%, since September 30, 2011, to $1.5 billion at December 31, 2011.

Investments

Total investment securities decreased $59 million during the fourth quarter of 2011, or 3%, to $2.0 billion at December 31, 2011. As a percentage of total assets, the investment portfolio declined from 18% at September 30, 2011, to 17% at December 31, 2011. The investment portfolio had a modified duration of 2.8 years at December 31, 2011, compared to 2.6 years at September 30, 2011. The unrealized gain in the investment portfolio increased from $42 million at September 30, 2011 to $46 million at December 31, 2011. Based on projected prepayment speeds and other assumptions, at December 31, 2011, the portfolio was expected to generate approximately $542 million in cash flows, or about 27% of the portfolio, over the next 12 months. The average yield on investment securities declined 15 basis points on a linked quarter basis, to 2.57% in the fourth quarter of 2011. The Company holds in its investment portfolio primarily government agency and municipal securities. Municipal securities comprised only 11% of the total investment portfolio at December 31, 2011. The Company holds no sovereign debt or foreign derivative exposure and has an immaterial exposure to accelerated bond premium amortization.

Loans

In the fourth quarter of 2011, total loans increased $218 million, or 3%. The loan portfolio associated with the FDIC-assisted acquisitions decreased $44 million, or 3%, compared to September 30, 2011. Excluding loans associated with the FDIC-assisted transactions, total loans increased $262 million, or 5%, over that period (18% annualized rate). On that basis, commercial and business banking loans grew $250 million, or 6% (23% annualized rate), and consumer loans increased $55 million, or 4% (18% annualized rate), while mortgage loans declined $43 million, or 14%, over that period. Between the times at which the acquisitions were completed and December 31, 2011, loans acquired in FDIC-assisted acquisitions decreased by approximately $559 million, or 30%.

Of the $7.4 billion total loan portfolio at December 31, 2011, $1.3 billion (net of discounts), or 18% of total loans, were Covered Assets, which provide considerable protection against credit risk. Approximately $74 million of the impaired loans from OMNI and Cameron at the time of acquisition were marked to estimated fair values.

2

Period-End Loan Volumes ($ in Millions)

| 12/31/10 | 3/31/11 | 6/30/11 | 9/30/11 | 12/31/11 | ||||||||||||||||

| Commercial |

$ | 3,123 | $ | 3,255 | $ | 4,230 | $ | 4,254 | $ | 4,504 | ||||||||||

| Consumer |

960 | 1,003 | 1,218 | 1,233 | 1,288 | |||||||||||||||

| Mortgage |

370 | 344 | 235 | 305 | 262 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Non-FDIC Loans |

$ | 4,453 | $ | 4,602 | $ | 5,683 | $ | 5,792 | $ | 6,054 | ||||||||||

| Covered Assets |

$ | 1,583 | $ | 1,520 | $ | 1,463 | $ | 1,378 | $ | 1,334 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Loans |

$ | 6,035 | $ | 6,122 | $ | 7,146 | $ | 7,170 | $ | 7,388 | ||||||||||

| Non-FDIC Growth |

4 | % | 3 | % | 25 | % | 2 | % | 5 | % | ||||||||||

On a linked quarter basis, the yield on average total loans (non-FDIC loans and FDIC covered loans, net of the FDIC indemnification asset) increased four basis points to 5.02%. The increase in this yield was primarily driven by the improvement in the yield on the FDIC covered loans, as the non-FDIC covered loan yield declined eight basis points. The loan yield on FDIC covered loans net of the FDIC indemnification asset was 5.33%, an improvement of 40 basis points on a linked quarter basis. The primary reason for the yield improvement in FDIC covered loans was positive adjustments that will occur from time to time.

Non-Covered and Net Covered Loan Portfolio Volumes And Yields ($ in Millions)

| 4Q 2010 | 1Q 2011 | 2Q 2011 | 3Q 2011 | 4Q 2011 | ||||||||||||||||||||||||||||||||||||

| Avg Bal | Yield | Avg Bal | Yield | Avg Bal | Yield | Avg Bal | Yield | Avg Bal | Yield | |||||||||||||||||||||||||||||||

| Non Covered Loans |

$ | 4,333 | 4.94 | % | $ | 4,506 | 4.89 | % | $ | 5,004 | 4.92 | % | $ | 5,743 | 4.99 | % | $ | 5,874 | 4.91 | % | ||||||||||||||||||||

| FDIC Covered Loans |

$ | 1,466 | 10.67 | % | $ | 1,546 | 14.20 | % | $ | 1,490 | 10.89 | % | $ | 1,422 | 7.82 | % | $ | 1,351 | 16.14 | % | ||||||||||||||||||||

| FDIC Indemnification Asset |

900 | -3.75 | % | 709 | -12.37 | % | 666 | -10.88 | % | 627 | -1.63 | % | 593 | -19.31 | % | |||||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||||||||

| Net Covered Loans |

$ | 2,366 | 5.14 | % | $ | 2,254 | 5.74 | % | $ | 2,156 | 4.08 | % | $ | 2,048 | 4.93 | % | $ | 1,944 | 5.33 | % | ||||||||||||||||||||

The Company projects the prospective yield and average balance on the net covered loan portfolio in the first quarter of 2012 to approximate the level reported for the third quarter of 2011, based on current FDIC loss share accounting assumptions and estimates.

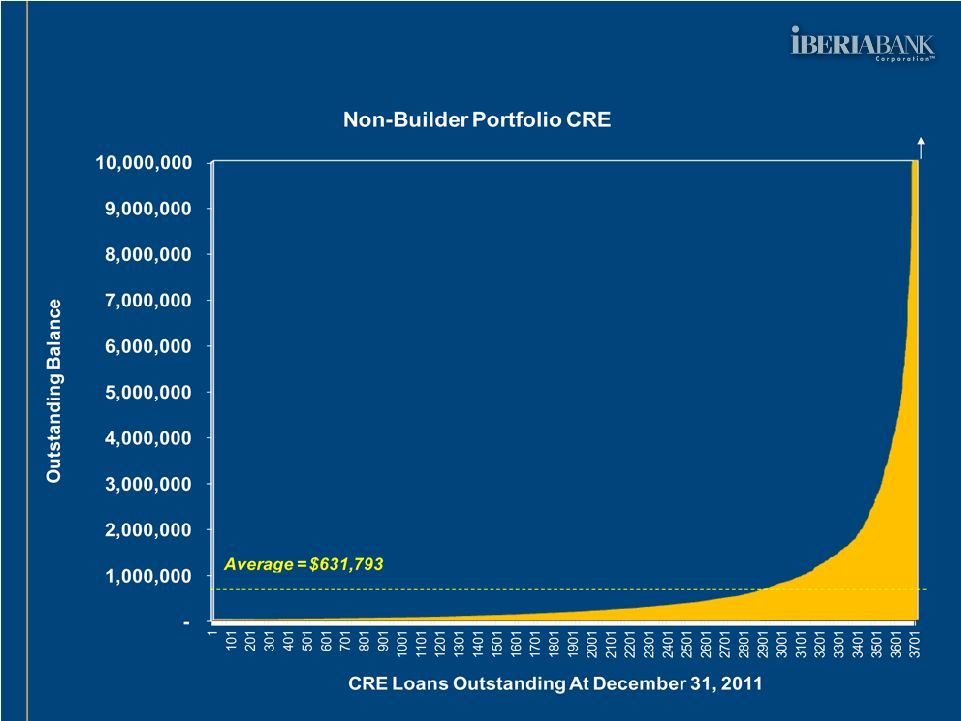

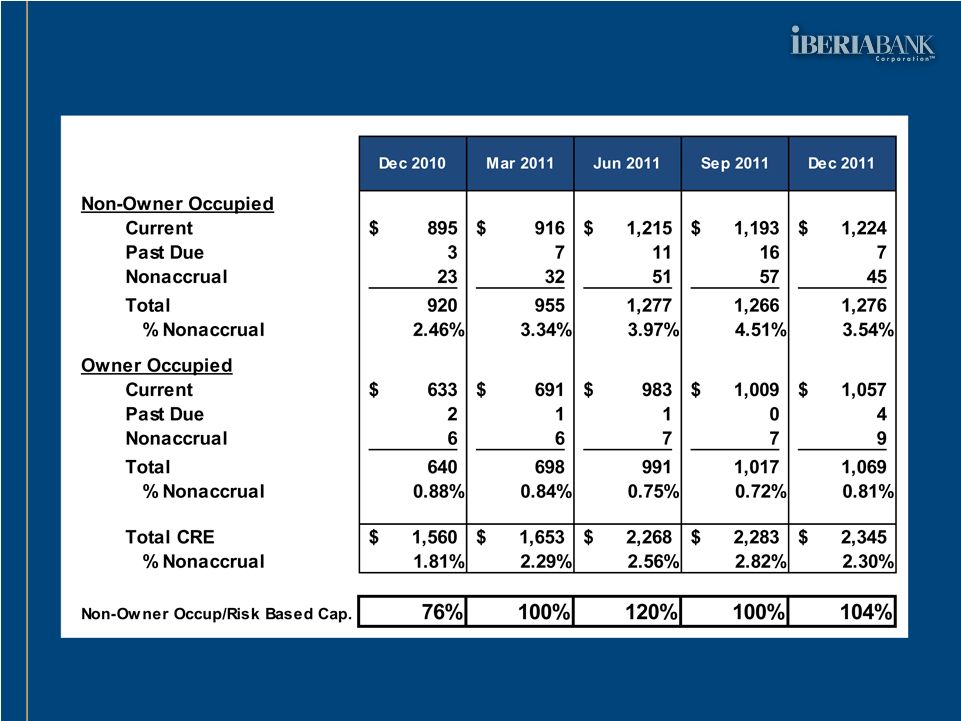

Commercial real estate loans totaled $3.3 billion at December 31, 2011, of which approximately $0.7 billion, or 22%, were Covered Assets. In addition, these Covered Assets were purchased at substantial discounts.

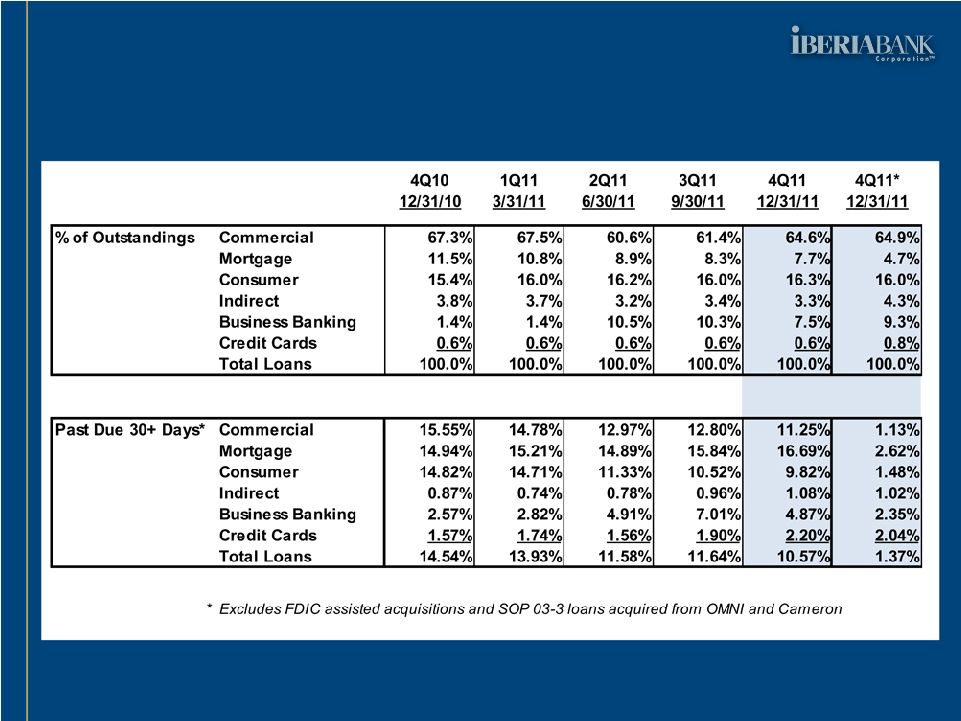

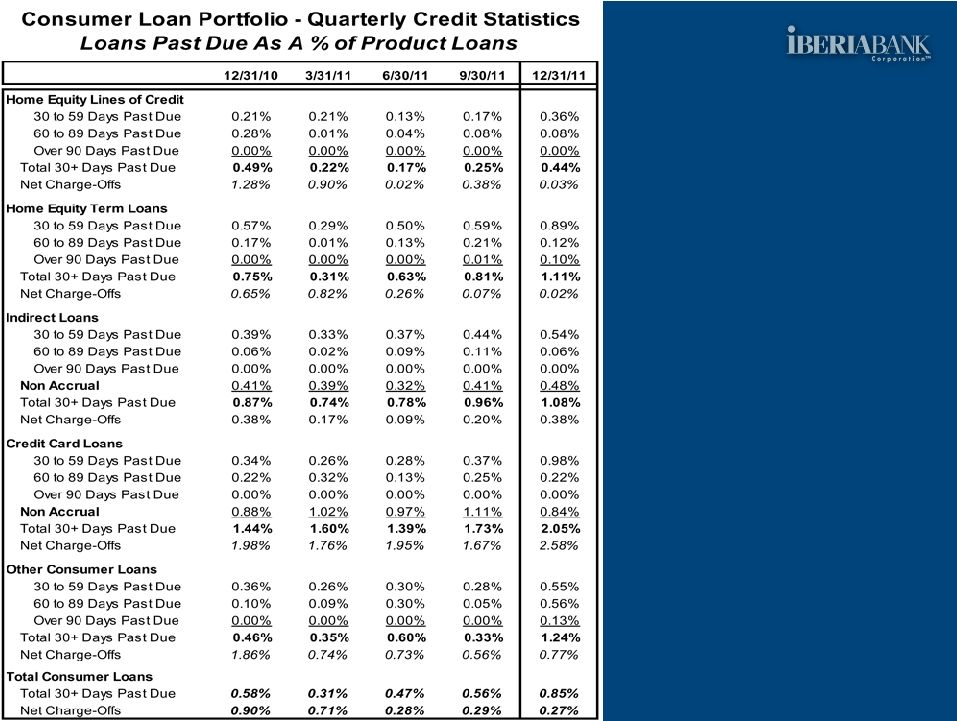

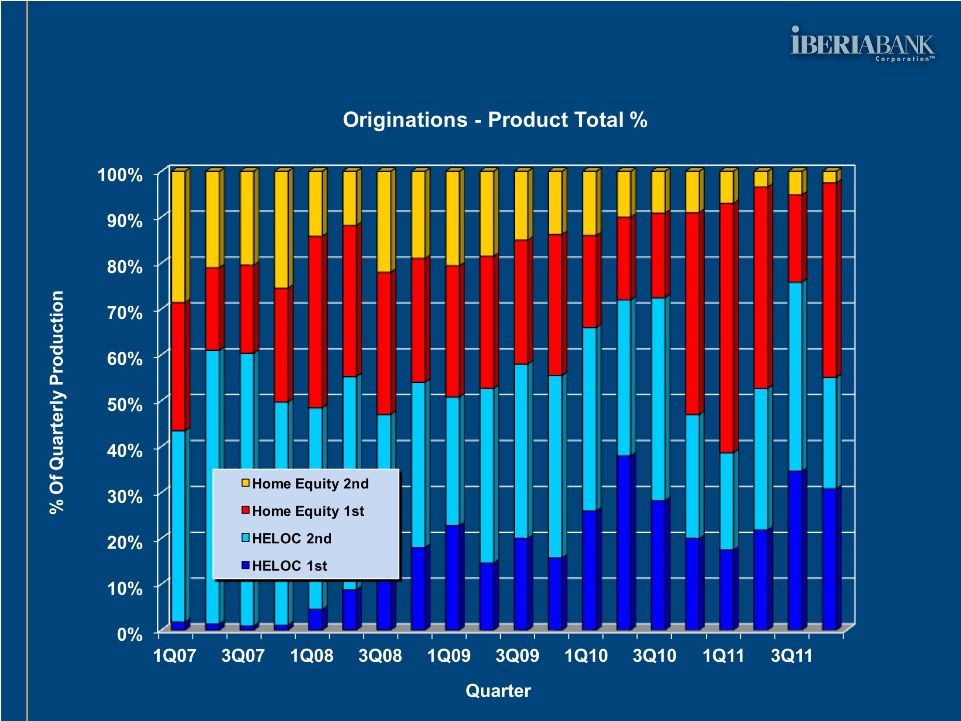

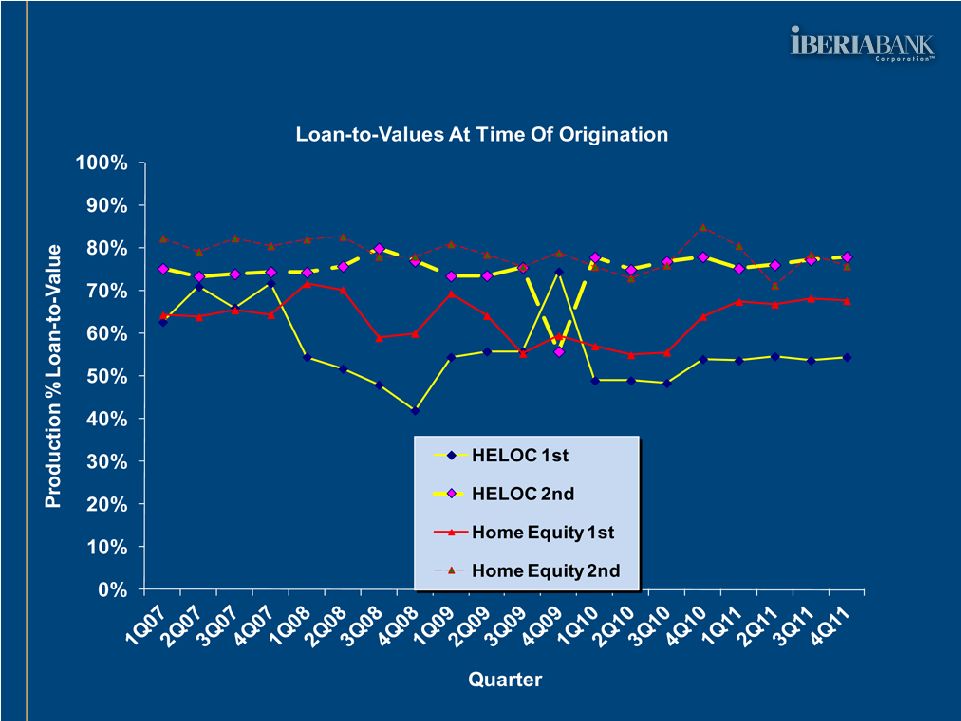

At December 31, 2011, approximately 12% of the Company’s direct consumer loan portfolio (net of discounts) was Covered Assets and impaired loans marked to fair value. The remaining legacy consumer portfolio maintained favorable asset quality. The average credit score of the legacy consumer loan portfolio borrower was 723, and consumer loans past due 30 days or more were 0.88% of total consumer loans at December 31, 2011 (compared to 0.55% at September 30, 2011). At December 31, 2011, legacy home equity loans totaled $509 million, with 1.11% past due 30 days or more (0.81% at September 30, 2011). Legacy home equity lines of credit totaled $340 million, with 0.44% past due 30 days or more (0.25% at September 30, 2011). Annualized net charge-offs in this portfolio were 0.03% of total consumer loans in the fourth quarter of 2011 (0.38% in the third quarter of 2011). The weighted average loan-to-value at origination for this portfolio over the last three years was 67%.

3

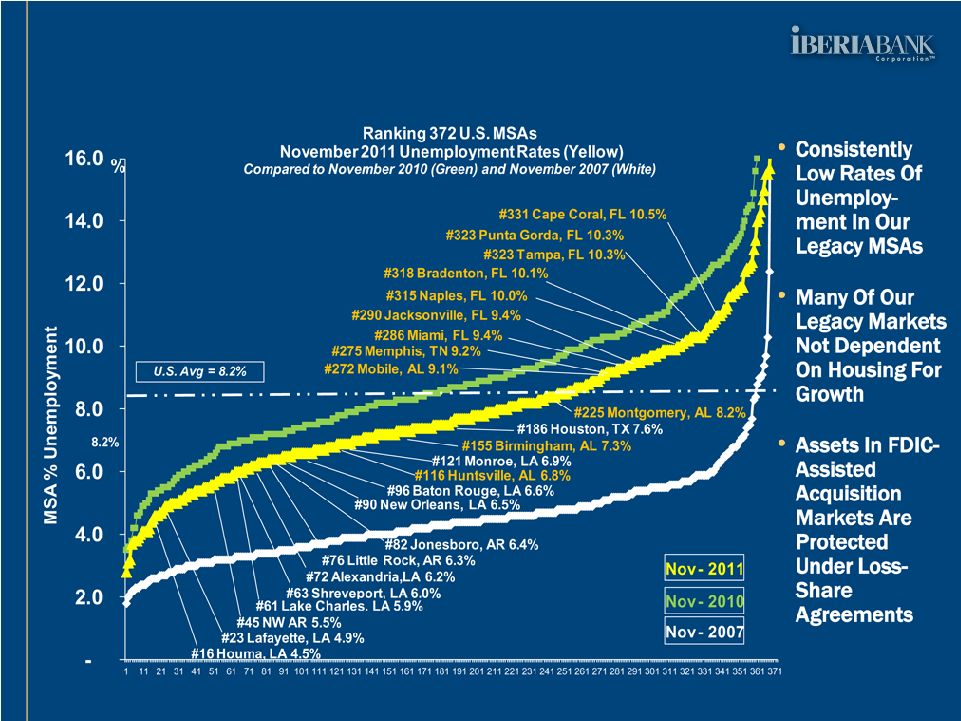

The indirect automobile loan portfolio totaled $262 million at December 31, 2011, up $2 million, or 1%, compared to this portfolio at September 30, 2011. At December 31, 2011, this portfolio equated to 4% of total loans and had 1.08% in loans past due 30 days or more (including nonaccruing loans), compared to 0.96% at September 30, 2011. Annualized net charge-offs in the indirect loan portfolio equated to approximately 0.38% of average loans in the fourth quarter of 2011, compared to 0.20% in the third quarter of 2011. Approximately 79% of the indirect automobile portfolio was loans to borrowers in the Acadiana region of Louisiana, which currently experiences a relatively favorable unemployment rate (4.9% in November 2011, the 23rd lowest unemployment rate of 372 MSAs in the United States).

Asset Quality

The Company’s credit quality statistics are significantly affected by the FDIC-assisted acquisitions. However, the loss share arrangements with the FDIC and acquisition discounts are expected to provide substantial protection against losses on those Covered Assets. Under loss share agreements in connection with the FDIC-assisted acquisitions, the FDIC will cover 80% of the losses on the disposition of loans and OREO up to $1.2 billion, or $965 million (the Company covered the remaining $241 million at acquisition). In addition, the FDIC will cover 95% of losses that exceed a $970 million threshold level. The Company received a discount of approximately $515 million on the purchase of assets in the transactions.

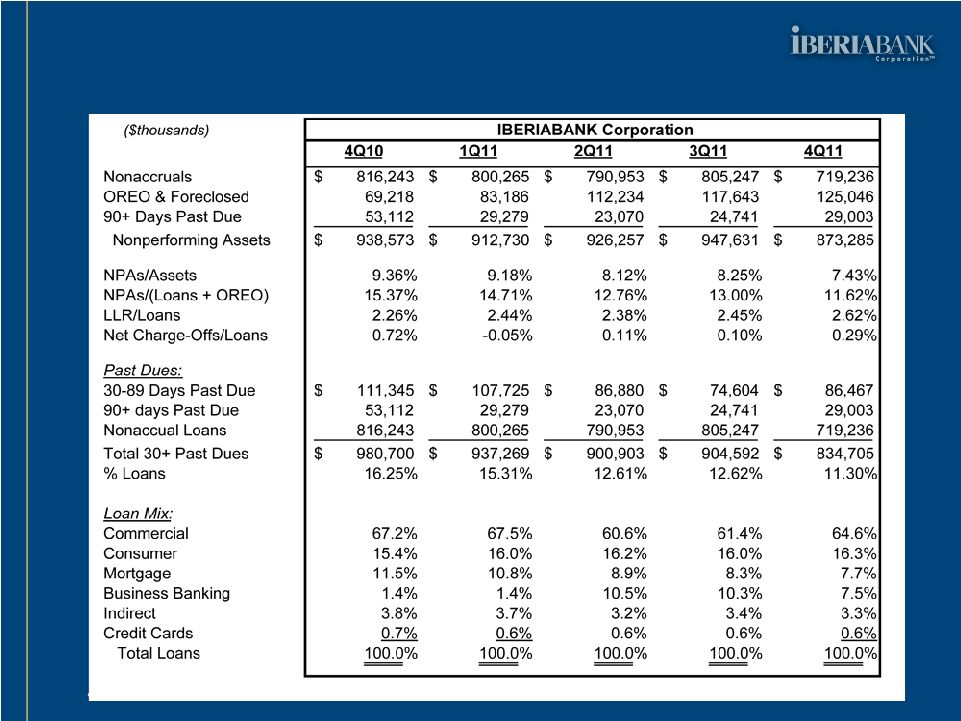

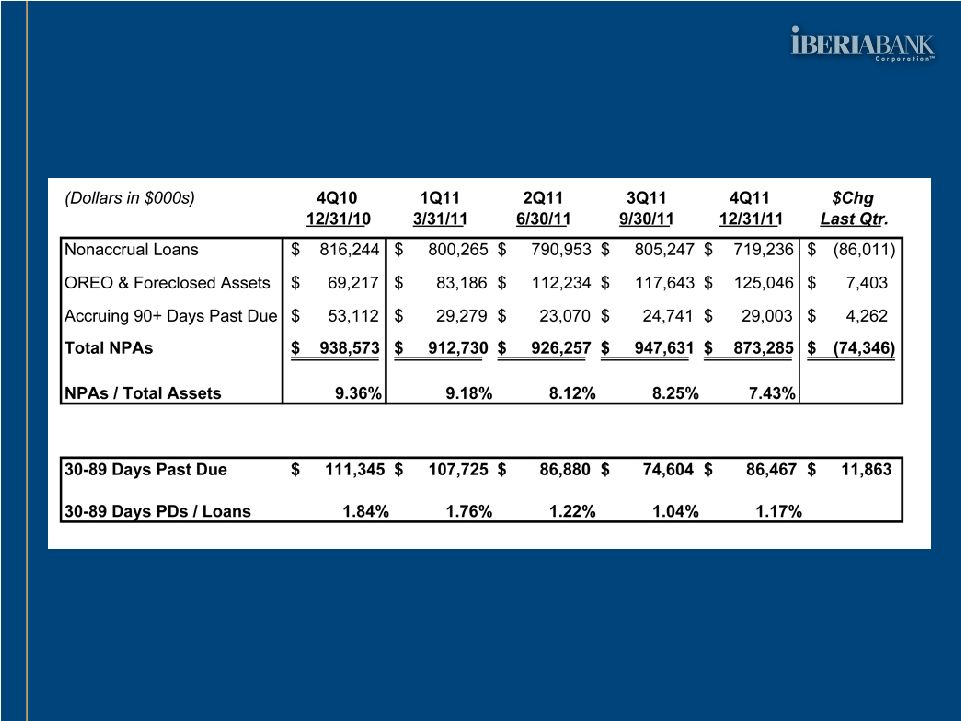

The majority of assets acquired in the four FDIC-assisted transactions completed in 2009 and 2010 are Covered Assets. Total NPAs at December 31, 2011, were $873 million, down $74 million, or 8%, compared to September 30, 2011. Excluding $788 million in NPAs which were Covered Assets or acquired impaired loans marked to fair value, NPAs at December 31, 2011 were $85 million, up $1 million, or 1%, compared to September 30, 2011. On that basis, NPAs were 0.87% of total assets at December 31, 2011, compared to 0.89% of assets at September 30, 2011 and 0.91% one year ago.

Summary Asset Quality Statistics

| ($ thousands) | IBERIABANK Corp. | |||||||||||||||||||

| 4Q10* | 1Q11* | 2Q11** | 3Q11** | 4Q11** | ||||||||||||||||

| Nonaccruals |

$ | 49,496 | $ | 60,034 | $ | 56,434 | $ | 70,833 | $ | 60,303 | ||||||||||

| OREO & Foreclosed |

18,496 | 17,056 | 18,461 | 12,301 | 21,382 | |||||||||||||||

| 90+ Days Past Due |

1,455 | 454 | 2,191 | 1,149 | 3,580 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Nonperforming Assets |

$ | 69,447 | $ | 77,544 | $ | 77,085 | $ | 84,283 | $ | 85,265 | ||||||||||

| NPAs/Assets |

0.91 | % | 1.01 | % | 0.84 | % | 0.89 | % | 0.87 | % | ||||||||||

| NPAs/(Loans + OREO) |

1.55 | % | 1.68 | % | 1.36 | % | 1.47 | % | 1.41 | % | ||||||||||

| LLR/Loans |

1.40 | % | 1.45 | % | 1.28 | % | 1.34 | % | 1.24 | % | ||||||||||

| Net Charge-Offs/Loans |

0.96 | % | -0.06 | % | 0.13 | % | 0.12 | % | 0.31 | % | ||||||||||

| * | Excludes the impact of all FDIC-assisted acquisitions |

| ** | Excludes the impact of all FDIC-assisted acquisitions and acquired impaired loans from OMNI and Cameron |

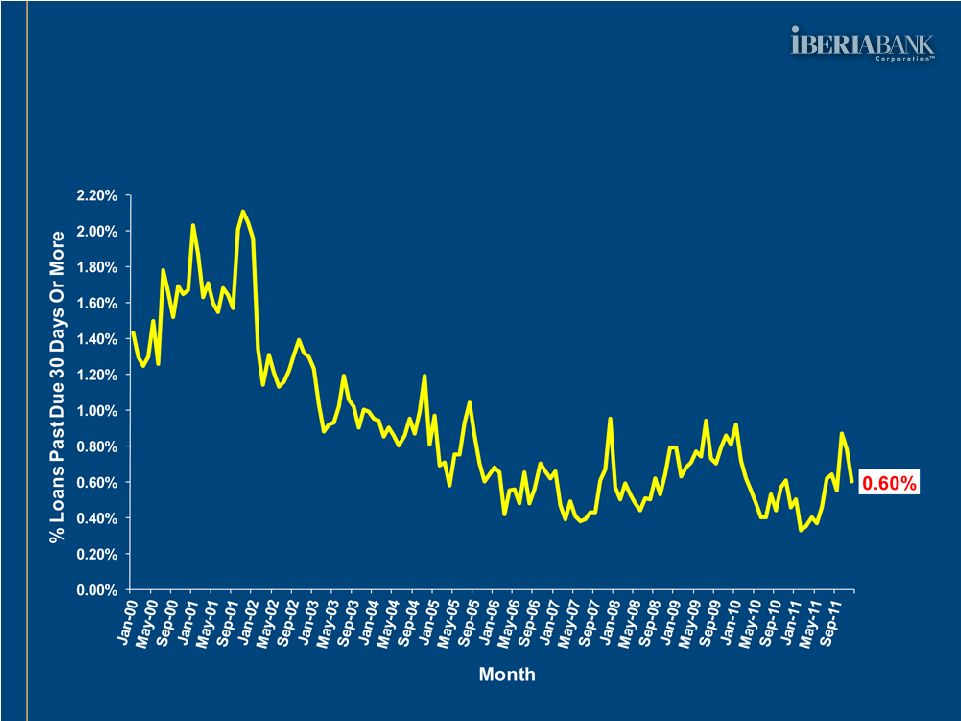

Excluding the FDIC-assisted transactions and impaired loans acquired at fair value, loans past due 30 days or more (including nonaccruing loans) decreased $14 million, or 15%, and represented 1.37% of total loans at December 31, 2011, compared to 1.68% of total loans at September 30, 2011. On that basis, loans past due 30-89 days at December 31, 2011 totaled $19 million, or 0.32% of total loans (compared to 0.44% of total loans at September 30, 2011), and troubled debt restructurings at December 31, 2011, totaled $28 million, or 0.46% of total loans (compared to 0.50% of loans at September 30, 2011). Substantially all of the troubled debt restructurings were included in the NPAs at December 31, 2011. The Company reported classified assets excluding Covered Assets totaling $206 million at December 31, 2011, or 1.75% of total assets (compared to $197 million, or 1.71% of total assets, at September 30, 2011). Since year-end 2011, approximately $14 million in classified assets have paid-off in full, including an $11 million loan which was past due and the Company’s second largest classified asset.

4

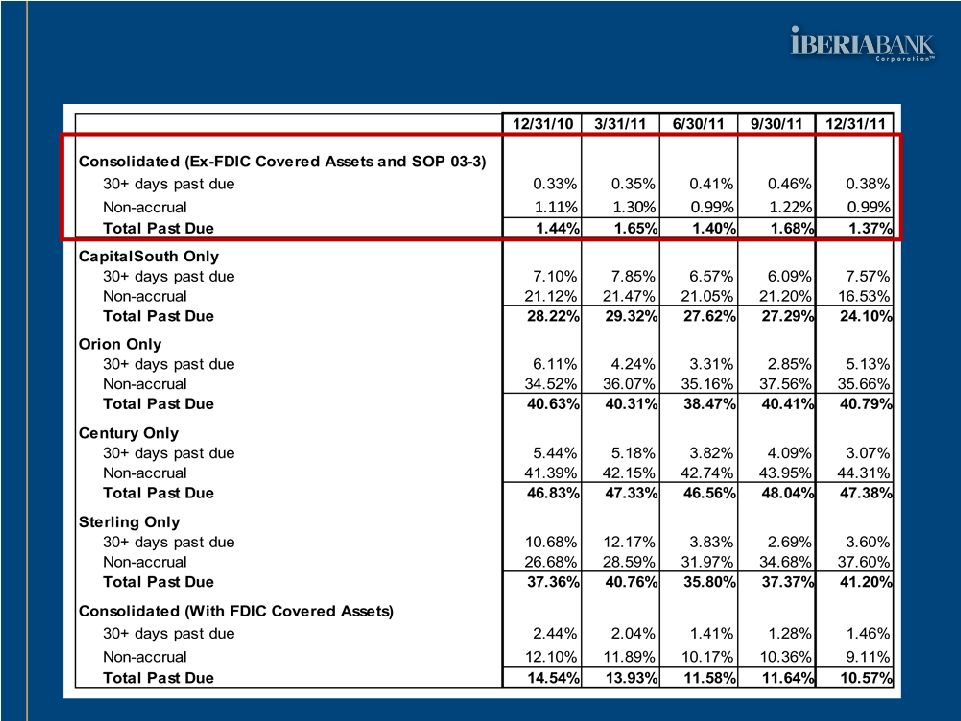

Loans Past Due

Loans Past Due 30 Days Or More And Nonaccruing Loans As % Of Loans Outstanding

| 12/31/10 | 3/31/11 | 6/30/11 | 9/30/11 | 12/31/11 | ||||||||||||||||

| Consolidated (Ex-FDIC Covered Assets and SOP 03-3) |

||||||||||||||||||||

| 30+ days past due |

0.33 | % | 0.35 | % | 0.41 | % | 0.46 | % | 0.38 | % | ||||||||||

| Non-accrual |

1.11 | % | 1.30 | % | 0.99 | % | 1.22 | % | 0.99 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Past Due |

1.44 | % | 1.65 | % | 1.40 | % | 1.68 | % | 1.37 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Consolidated (With FDIC Covered Assets) |

||||||||||||||||||||

| 30+ days past due |

2.44 | % | 2.04 | % | 1.41 | % | 1.28 | % | 1.46 | % | ||||||||||

| Non-accrual |

12.10 | % | 11.89 | % | 10.17 | % | 10.36 | % | 9.11 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Past Due |

14.54 | % | 13.93 | % | 11.58 | % | 11.64 | % | 10.57 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

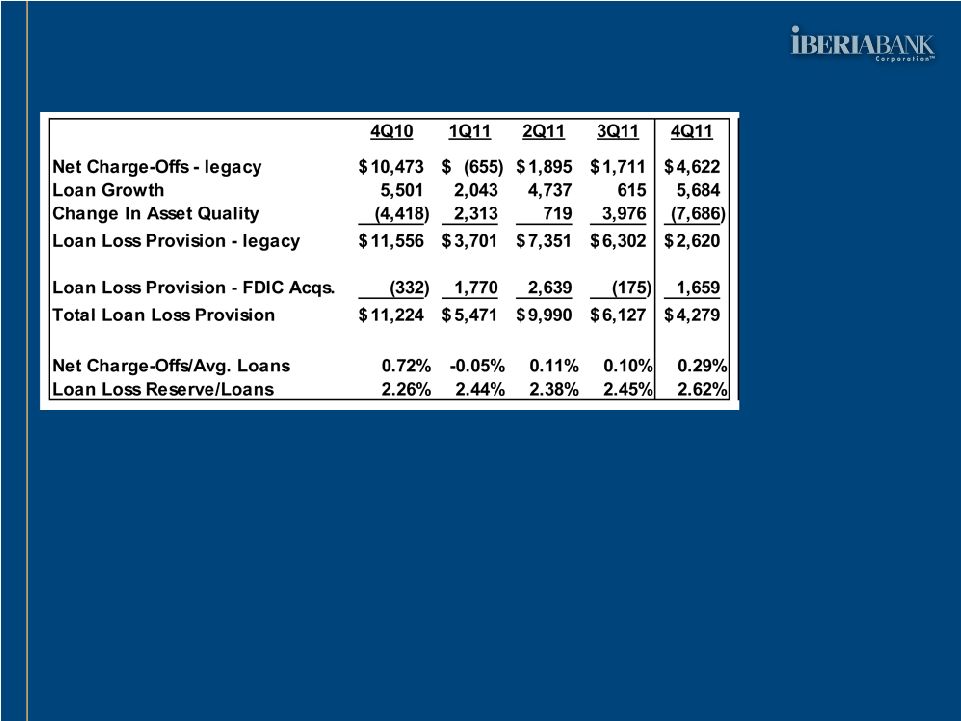

The Company reported net charge-offs of $5 million in the fourth quarter of 2011, compared to $2 million on a linked quarter basis. The ratio of net charge-offs to average loans was 0.29% in the fourth quarter of 2011 (0.31% excluding Covered Assets and impaired loans acquired at fair value), compared to 0.10% in the third quarter of 2011. The Company recorded a $4 million loan loss provision in the fourth quarter of 2011, down $2 million, or 30%, on a linked quarter basis. The loan loss provision in the fourth quarter was related to organic loan growth, partially offset by reduced provision associated with the improvement in asset quality.

At December 31, 2011, the allowance for loan losses was 2.62% of total loans, compared to 2.45% at September 30, 2011. In accordance with generally accepted accounting principles, the Covered Assets and OMNI and Cameron acquired loans were preliminarily marked to market at acquisition, including estimated loan impairments. Excluding FDIC covered assets and impaired loans that were marked to fair value, the Company’s ratio of loan loss reserves to loans decreased from 1.34% at September 30, 2011, to 1.24% at December 31, 2011. Excluding the Covered Assets and all other acquired loans, the Company’s ratio of loan loss reserve to loans decreased from 1.51% at September 30, 2011 to 1.39% at December 31, 2011. Management considered the loan loss reserve adequate to absorb credit losses inherent in the loan portfolio at December 31, 2011.

Deposits

During the fourth quarter of 2011, total deposits increased $99 million, or 1%. Noninterest bearing deposits climbed $70 million, or 5% (20% annualized rate); NOW accounts increased $189 million, or 11% (45% annualized rate); savings and money market deposits increased $21 million, or 1% (3% annualized rate); and time deposits decreased $181 million, or 7%.

Period-End Deposit Volumes ($ in Millions)

| Mix | ||||||||||||||||||||||||||||

| 12/31/10 | 3/31/11 | 6/30/11 | 9/30/11 | 12/31/11 | 12/31/10 | 12/31/11 | ||||||||||||||||||||||

| Noninterest |

$ | 879 | $ | 941 | $ | 1,323 | $ | 1,415 | $ | 1,485 | 11 | % | 16 | % | ||||||||||||||

| NOW Accounts |

1,282 | 1,395 | 1,639 | 1,688 | 1,877 | 16 | % | 20 | % | |||||||||||||||||||

| Savings/MMkt |

2,910 | 2,919 | 3,284 | 3,360 | 3,381 | 37 | % | 36 | % | |||||||||||||||||||

| Time Deposits |

2,844 | 2,604 | 2,828 | 2,727 | 2,546 | 36 | % | 27 | % | |||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||||

| Total Deposits |

$ | 7,915 | $ | 7,859 | $ | 9,074 | $ | 9,190 | $ | 9,289 | 100 | % | 100 | % | ||||||||||||||

| Growth |

-4 | % | -1 | % | 15 | % | 1 | % | 1 | % | ||||||||||||||||||

5

Average noninterest bearing deposits increased $87 million, or 6%, and interest-bearing deposits were relatively stable on a linked quarter basis. The rate on average interest bearing deposits in the fourth quarter of 2011 was 0.80%, a decrease of 10 basis points on a linked quarter basis.

Other Interest Bearing Liabilities

On a linked quarter basis, average long-term debt decreased $9 million, or 2%, and the cost of the debt increased 21 basis points to 2.84%. The Company had $192 million of short-term borrowings at December 31, 2011. The cost of average interest bearing liabilities was 0.90% in the fourth quarter of 2011, a decrease of eight basis points on a linked quarter basis. For the month of December 2011, the average cost of interest bearing liabilities was 0.87%.

Capital Position

The Company maintains strong capital ratios. The equity-to-assets ratio was 12.61% at December 31, 2011, compared to 12.81% at September 30, 2011, and 13.00% one year ago. At December 31, 2011, the Company reported a tangible common equity ratio of 9.52%, compared to 9.64% at September 30, 2011 and 10.65% one year ago. The Company’s Tier 1 leverage ratio was 10.45%, compared to 10.42% at September 30, 2011 and 11.24% one year ago. The Company’s total risk-based capital ratio at December 31, 2011 was 16.21%, compared to 16.62% at September 30, 2011 and 19.74% one year ago.

Regulatory Capital Ratios

At December 31, 2011

| Capital Ratio |

Well Capitalized |

IBERIABANK | IBERIABANK Corporation |

|||||||||

| Tier 1 Leverage |

5.00 | % | 9.00 | % | 10.45 | % | ||||||

| Tier 1 Risk Based |

6.00 | % | 12.88 | % | 14.94 | % | ||||||

| Total Risk Based |

10.00 | % | 14.14 | % | 16.21 | % | ||||||

On May 31, 2011, the Company acquired both OMNI and Cameron. At the time of these acquisitions, the Company used preliminary estimates (“provisional amounts”) to determine the fair values of many of the assets acquired and liabilities assumed. The Company disclosed in previous press releases and Form 10-Q filings that the estimates used to determine the fair value of the acquired loans were provisional amounts and might change as additional analysis of future cash flows was performed.

The period of time subsequent to the acquisition date for the Company to obtain the information necessary to measure all aspects of the business combinations in accordance with ASC 805 (i.e., to measure and recognize all aspects of the business combinations at acquisition-date fair values) is limited to one year. During this period, the Company may adjust any provisional amounts made for the business combinations based on any additional information subsequently obtained regarding their fair values as of the acquisition date.

During the fourth quarter, the Company performed further analysis of the facts and circumstances that existed at the acquisition date. This analysis included a refinement of the future estimated cash flows, review of loan types, and a refinement of discounts, losses given default and underlying collateral values.

As a result of this analysis, it was determined that the provisional amounts assigned to certain asset values of OMNI and Cameron initially estimated as of the acquisition date should be adjusted. The adjustments were performed retrospectively, as if they had existed at acquisition date. The Company increased the original amount of goodwill recorded in the fiscal quarter ended June 30, 2011 by $20.7 million. Due to the change in provisional amounts of

6

loans relating to this change in goodwill, the associated loan interest income was reduced by $1.5 million in the fiscal quarter ended September 30, 2011. These changes have been reported in the quarterly comparative balance sheet, income statement and tables included in this press release.

These refinements to the OMNI and Cameron acquisition estimates reduced book value per share at September 30, 2011 from $50.19 as originally reported to $50.16 as adjusted, and tangible book value per share at September 30, 2011 from $37.12 as originally reported to $36.41 as adjusted. At December 31, 2011, book value per share was $50.48 and tangible book value per share was $36.80. Based on the closing stock price of the Company’s common stock of $54.35 per share on January 24, 2012, this price equated to 1.08 times December 31, 2011 book value and 1.48 times December 31, 2011 tangible book value per share.

On December 12, 2011, the Company declared a quarterly cash dividend of $0.34 per share. This dividend level equated to an annualized dividend rate of $1.36 per share and an indicated dividend yield of 2.50%.

On October 26, 2011, the Company announced a share repurchase program totaling 900,000 shares of common stock to be completed over a one-year period. No shares were purchased during the fourth quarter of 2011.

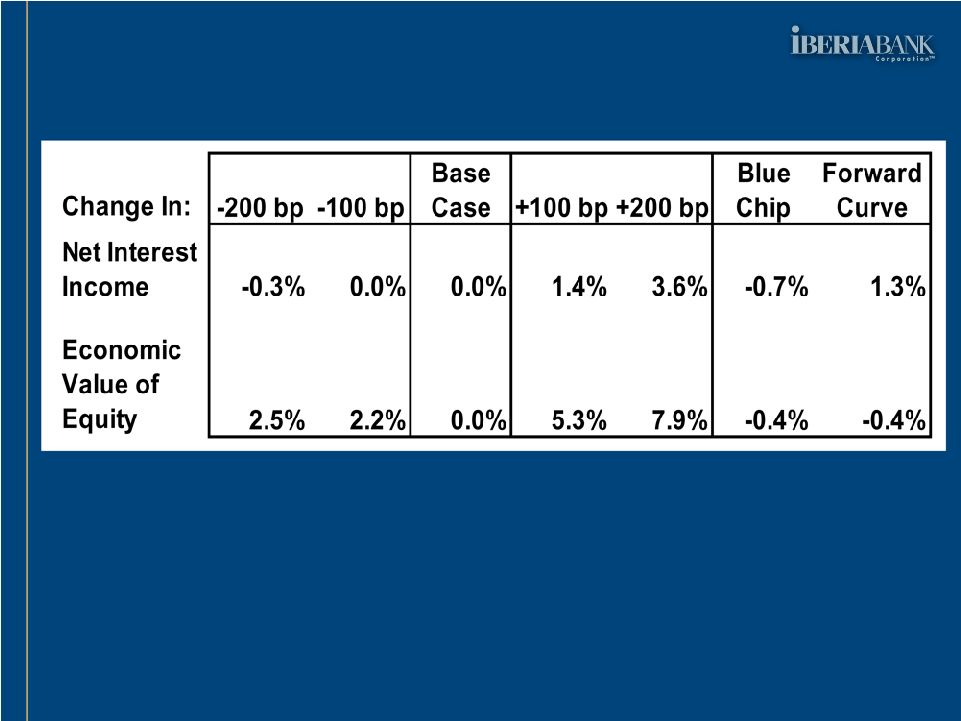

Interest Rate Risk Position

The Company’s interest rate risk modeling at December 31, 2011, indicated the Company is fairly balanced over a 12-month time frame. A 100 basis point instantaneous and parallel upward shift in interest rates at December 31, 2011, was estimated to increase net interest income over 12 months by approximately 1.4%. Similarly, a 100 basis point decrease in interest rates was expected to decrease net interest income by less than 1%. At December 31, 2011, approximately 50% of the Company’s total loan portfolio had fixed interest rates. Eliminating fixed rate loans that mature within a one-year time frame reduces this percentage to 48%. Approximately 75% of the Company’s time deposit base will re-price within 12 months from December 31, 2011.

Operating Results

On a linked quarter basis, the average earning asset yield decreased three basis points, while the cost of interest bearing deposits and liabilities decreased 10 and eight basis points, respectively. As a result, the tax-equivalent net interest spread and margin improved five and four basis points, respectively. On a linked quarter basis, tax-equivalent net interest income increased $2 million, or 2%, as average earning assets edged up $53 million, or less than 1%, and the margin improved four basis points.

Quarterly Average Yields/Cost (Taxable Equivalent Basis)

| 4Q10 | 1Q11 | 2Q11 | 3Q11 | 4Q11 | ||||||||||||||||

| Earning Asset Yield |

4.16 | % | 4.47 | % | 4.17 | % | 4.39 | % | 4.36 | % | ||||||||||

| Cost Of Int-Bearing Liabs |

1.27 | % | 1.10 | % | 1.09 | % | 0.98 | % | 0.90 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net Interest Spread |

2.89 | % | 3.37 | % | 3.09 | % | 3.41 | % | 3.46 | % | ||||||||||

| Net Interest Margin |

3.10 | % | 3.55 | % | 3.28 | % | 3.58 | % | 3.62 | % | ||||||||||

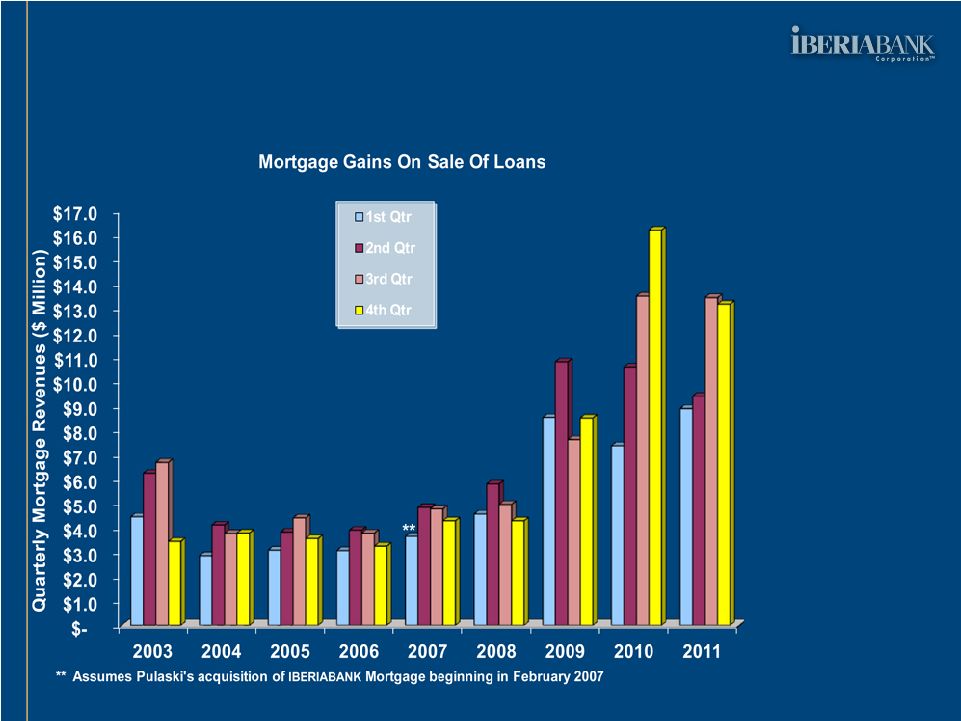

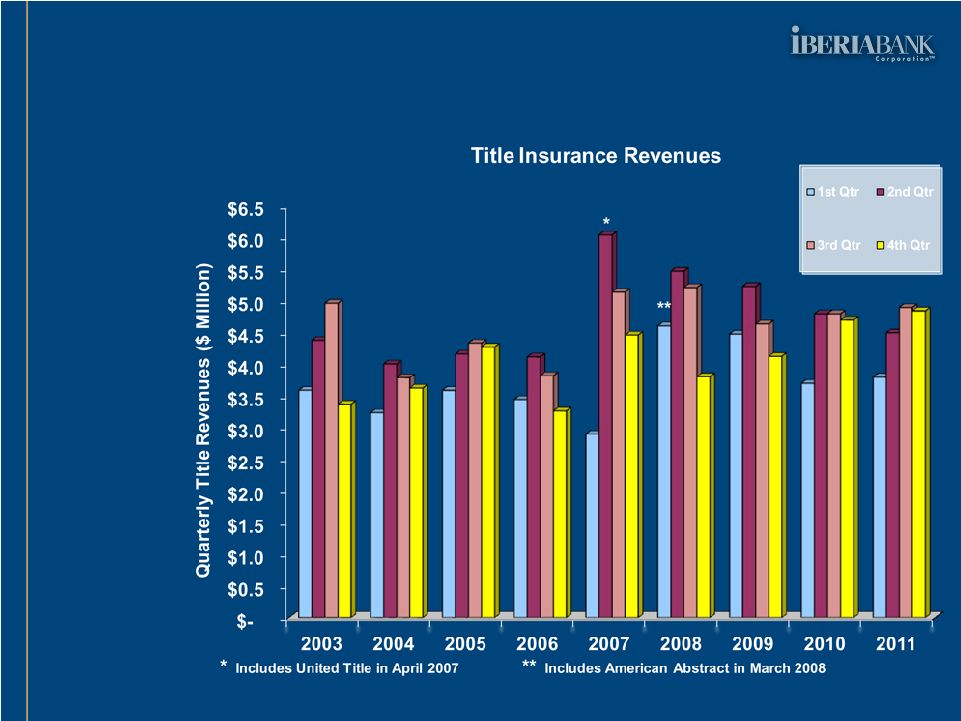

Aggregate noninterest income decreased $2 million, or 4%, on a linked quarter basis. The primary reasons for the decline were debit fee income declined $1.1 million, or 36%, service charges on deposit accounts decreased $0.8 million, or 11%, gains on the sale of investments totaling $0.8 million declined $0.4 million, or 34%, and mortgage revenues decreased $0.3 million, or 2%. Revenues from brokerage, trust, capital markets, and title insurance remained relatively unchanged on a linked quarter basis. Trust assets under management were approximately $725 million at December 31, 2011, up $24 million, or 3% compared to September 30, 2011.

7

Results for the fourth quarter were negatively impacted by reordering the posting sequence for electronic debit transactions associated with the settlement of the previously disclosed class action law suit and reduced debit card interchange fee income associated with implementation of Durbin Amendment provisions of the Dodd-Frank Act. The impact of the reordering was approximately $1.1 million, or $0.02 per share on an after-tax basis, and the Durbin Amendment debit card transaction impact was approximately $0.9 million, or $0.02 per share on an after-tax basis. The Company has undertaken revenue enhancements, the effects of which beginning in 2012 are expected to partially mitigate the revenue decline experienced in the fourth quarter of 2011 due to the above mentioned factors.

The Company originated $1.7 billion in mortgage loans in 2011, down 6% compared to 2010. In the fourth quarter of 2011, the Company originated $516 million in mortgage loans, up $12 million, or 2%, on a linked quarter basis. Client loan refinancing opportunities accounted for approximately 48% of mortgage loan applications in the fourth quarter of 2011, compared to 37% in the third quarter of 2011, and approximately 47% between December 31, 2011, and January 20, 2012. The Company sold $495 million in mortgage loans during the fourth quarter of 2011, up $48 million, or 11%, compared to the third quarter of 2011. Sales margins and gains on the sale of mortgage loans remained fairly stable on a linked quarter basis. The mortgage origination pipeline was approximately $131 million at December 31, 2011, compared to $229 million at September 30, 2011, and approximately $158 million at January 20, 2012. Mortgage loan repurchases and make-whole payments were $0.7 million in the fourth quarter of 2011 compared to less than $0.3 million in each of the three prior quarters of 2011.

Noninterest expense increased $0.2 million, or less than 1%, on a linked quarter basis. Excluding acquisition and conversion-related costs, noninterest expense increased $2 million, or 2%, over that period. On that basis, mortgage commissions increased $1.0 million on a linked quarter basis, or 31%, legal and professional expense climbed $0.9 million, or 32%, marketing and business development expense increased $0.8 million, or 38%, and computer service expense increased $0.6 million, or 25%.

In the third quarter of 2011, the Company incurred costs totaling approximately $3 million in association with a then potential settlement of a class action lawsuit and a trust preferred securities prepayment premium; no similar costs were incurred in the fourth quarter of 2011. In the fourth quarter of 2011, the Company incurred costs totaling $0.9 million associated with the write-down of four facilities (three of which were acquired in prior acquisitions), and $0.5 million associated with the impairment of a revenue bond.

The tangible efficiency ratio of IBERIABANK, excluding acquisition and conversion costs, was approximately 68% in the fourth quarter of 2011, compared to 67% in the third quarter of 2011.

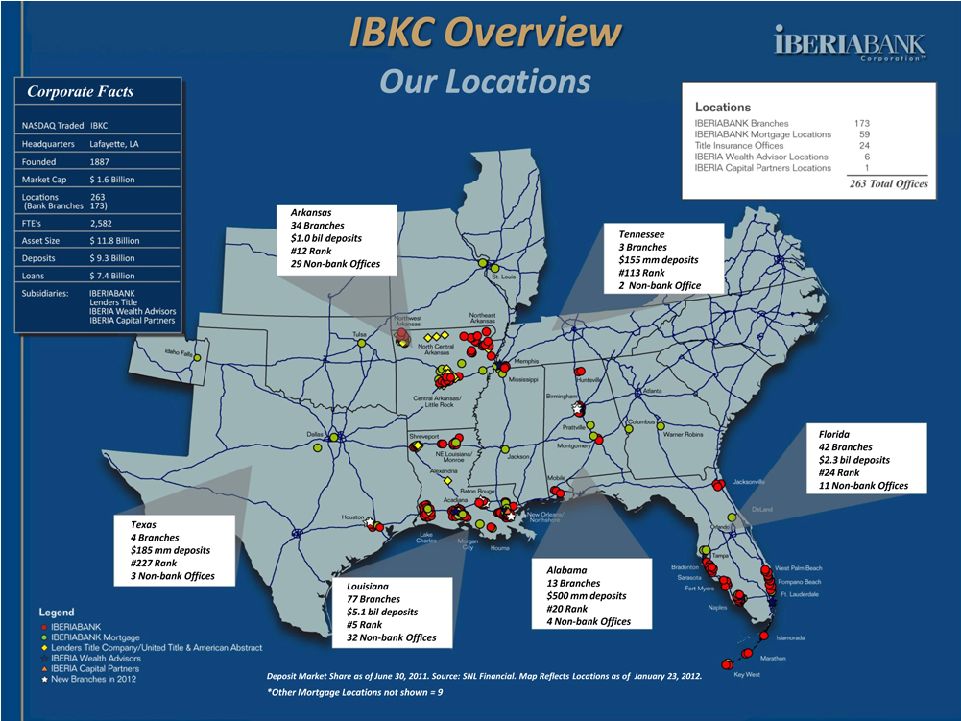

IBERIABANK Corporation

IBERIABANK Corporation is a financial holding company with 263 combined offices, including 173 bank branch offices in Louisiana, Arkansas, Tennessee, Alabama, Texas, and Florida, 24 title insurance offices in Arkansas and Louisiana, mortgage representatives in 59 locations in 12 states, six locations with representatives of IBERIA Wealth Advisors in four states, and one IBERIA Capital Partners, LLC office in New Orleans. The Company opened three branch offices since September 30, 2011, in Memphis, Tennessee, Hoover and Mountain Brook, Alabama, and a new mortgage office in Fort Lauderdale.

The Company’s common stock trades on the NASDAQ Global Select Market under the symbol “IBKC.” The Company’s market capitalization was approximately $1.6 billion, based on the NASDAQ closing stock price on January 24, 2012.

The following 13 investment firms currently provide equity research coverage on IBERIABANK Corporation:

| • | FIG Partners, LLC |

| • | Guggenheim Partners |

| • | Jefferies & Co., Inc. |

| • | Keefe, Bruyette & Woods |

8

| • | Morgan Keegan & Company, Inc. |

| • | Oppenheimer & Co., Inc. |

| • | Raymond James & Associates, Inc. |

| • | Robert W. Baird & Company |

| • | Stephens, Inc. |

| • | Sterne, Agee & Leach |

| • | Stifel Nicolaus & Company |

| • | SunTrust Robinson-Humphrey |

| • | Wunderlich Securities |

Conference Call

In association with this earnings release, the Company will host a live conference call to discuss the financial results for the quarter just completed. The telephone conference call will be held on Wednesday, January 25, 2012, beginning at 9:00 a.m. Central Time by dialing 1-800-230-1096. The confirmation code for the call is 231990. A replay of the call will be available until midnight Central Time on February 1, 2012 by dialing 1-800-475-6701. The confirmation code for the replay is 231990. The Company has prepared a PowerPoint presentation that supplements information contained in this press release. The PowerPoint presentation may be accessed on the Company’s web site, www.iberiabank.com, under “Investor Relations” and then “Presentations.”

Non-GAAP Financial Measures

This press release contains financial information determined by methods other than in accordance with GAAP. The Company’s management uses these non-GAAP financial measures in their analysis of the Company’s performance. These measures typically adjust GAAP performance measures to exclude the effects of the amortization of intangibles and include the tax benefit associated with revenue items that are tax-exempt, as well as adjust income available to common shareholders for certain significant activities or nonrecurring transactions. Since the presentation of these GAAP performance measures and their impact differ between companies, management believes presentations of these non-GAAP financial measures provide useful supplemental information that is essential to a proper understanding of the operating results of the Company’s core businesses. These non-GAAP disclosures should not be viewed as a substitute for operating results determined in accordance with GAAP, nor are they necessarily comparable to non-GAAP performance measures that may be presented by other companies. Reconciliations of GAAP to non-GAAP disclosures are included as tables at the end of this release.

Forward Looking Statements

To the extent that statements in this press release relate to future plans, objectives, financial results or performance of IBERIABANK Corporation, these statements are deemed to be forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements, which are based on management’s current information, estimates and assumptions and the current economic environment, are generally identified by the use of the words “plan”, “believe”, “expect”, “intend”, “anticipate”, “estimate”, “project” or similar expressions. IBERIABANK Corporation’s actual strategies and results in future periods may differ materially from those currently expected due to various risks and uncertainties.

Actual results could differ materially because of factors such as the current level of market volatility and our ability to execute our growth strategy, including the availability of future FDIC-assisted failed bank opportunities, unanticipated losses related to the integration of, and accounting for, acquired businesses and assets and assumed liabilities in FDIC-assisted transactions, adjustments of fair values of acquired assets and assumed liabilities and of deferred taxes in FDIC-assisted acquisitions, credit risk of our customers, effects of the on-going correction in residential real estate prices and reduced levels of home sales, sufficiency of our allowance for loan losses, changes in interest rates, access to funding sources, reliance on the services of executive management, competition for loans,

9

deposits and investment dollars, reputational risk and social factors, changes in government regulations and legislation, increases in FDIC insurance assessments, geographic concentration of our markets and economic conditions in these markets, rapid changes in the financial services industry, dependence on our operational, technological, and organizational infrastructure, hurricanes and other adverse weather events, the volatility and low trading volume of our common stock, and valuation of intangible assets. These and other factors that may cause actual results to differ materially from these forward-looking statements are discussed in the Company’s Annual Report on Form 10-K and other filings with the Securities and Exchange Commission (the “SEC”), available at the SEC’s website, http://www.sec.gov, and the Company’s website, http://www.iberiabank.com, under the heading “Investor Information.” All information in this release is as of the date of this release. The Company undertakes no duty to update any forward-looking statement to conform the statement to actual results or changes in the Company’s expectations.

10

IBERIABANK CORPORATION

FINANCIAL HIGHLIGHTS

| For The Quarter Ended | For The Quarter Ended | |||||||||||||||||||

| December 31, | September 30, | |||||||||||||||||||

| 2011 | 2010 | % Change | 2011 | % Change | ||||||||||||||||

| Income Data (in thousands): |

||||||||||||||||||||

| Net Interest Income |

$ | 92,573 | $ | 72,349 | 28 | % | $ | 90,971 | 2 | % | ||||||||||

| Net Interest Income (TE) (1) |

94,918 | 73,934 | 28 | % | 93,314 | 2 | % | |||||||||||||

| Net Income |

17,357 | 13,042 | 33 | % | 16,347 | 6 | % | |||||||||||||

| Earnings Available to Common Shareholders- Basic |

17,357 | 13,042 | 33 | % | 16,347 | 6 | % | |||||||||||||

| Earnings Available to Common Shareholders- Diluted |

17,050 | 12,781 | 33 | % | 16,057 | 6 | % | |||||||||||||

| Per Share Data: |

||||||||||||||||||||

| Earnings Available to Common Shareholders - Basic |

$ | 0.59 | $ | 0.49 | 22 | % | $ | 0.55 | 8 | % | ||||||||||

| Earnings Available to Common Shareholders - Diluted |

0.59 | 0.48 | 23 | % | 0.54 | 8 | % | |||||||||||||

| Book Value Per Share |

50.48 | 48.50 | 4 | % | 50.16 | 1 | % | |||||||||||||

| Tangible Book Value Per Common Share (2) |

36.80 | 38.68 | (5 | %) | 36.41 | 1 | % | |||||||||||||

| Cash Dividends |

0.34 | 0.34 | — | 0.34 | — | |||||||||||||||

| Closing Stock Price |

49.30 | 59.13 | (17 | %) | 47.06 | 5 | % | |||||||||||||

| Key Ratios: (3) |

||||||||||||||||||||

| Operating Ratios: |

||||||||||||||||||||

| Return on Average Assets |

0.59 | % | 0.50 | % | 0.56 | % | ||||||||||||||

| Return on Average Common Equity |

4.65 | % | 3.94 | % | 4.31 | % | ||||||||||||||

| Return on Average Tangible Common Equity (2) |

6.72 | % | 5.26 | % | 6.22 | % | ||||||||||||||

| Net Interest Margin (TE) (1) |

3.62 | % | 3.10 | % | 3.58 | % | ||||||||||||||

| Efficiency Ratio |

77.9 | % | 73.5 | % | 77.7 | % | ||||||||||||||

| Tangible Efficiency Ratio (TE) (1) (2) |

75.2 | % | 70.9 | % | 75.0 | % | ||||||||||||||

| Full-time Equivalent Employees |

2,582 | 2,122 | 2,541 | |||||||||||||||||

| Capital Ratios: |

||||||||||||||||||||

| Tangible Common Equity Ratio |

9.52 | % | 10.65 | % | 9.64 | % | ||||||||||||||

| Tangible Common Equity to Risk-Weighted Assets |

13.86 | % | 17.00 | % | 14.21 | % | ||||||||||||||

| Tier 1 Leverage Ratio |

10.45 | % | 11.24 | % | 10.42 | % | ||||||||||||||

| Tier 1 Capital Ratio |

14.94 | % | 18.48 | % | 15.35 | % | ||||||||||||||

| Total Risk Based Capital Ratio |

16.21 | % | 19.74 | % | 16.62 | % | ||||||||||||||

| Common Stock Dividend Payout Ratio |

57.5 | % | 70.1 | % | 61.0 | % | ||||||||||||||

| Asset Quality Ratios: |

||||||||||||||||||||

| Excluding FDIC Covered Assets and acquired impaired loans |

||||||||||||||||||||

| Nonperforming Assets to Total Assets (4) |

0.87 | % | 0.91 | % | 0.89 | % | ||||||||||||||

| Allowance for Loan Losses to Loans |

1.24 | % | 1.40 | % | 1.34 | % | ||||||||||||||

| Net Charge-offs to Average Loans |

0.31 | % | 0.96 | % | 0.12 | % | ||||||||||||||

| Nonperforming Assets to Total Loans and OREO (4) |

1.41 | % | 1.55 | % | 1.47 | % | ||||||||||||||

| For The Quarter Ended | For The Quarter Ended | |||||||||||||||||||

| December 31, | September 30, | June 30, | March 31, | |||||||||||||||||

| 2011 | 2011 | 2011 | 2011 | 2011 | ||||||||||||||||

| Balance Sheet Summary (in thousands): | End of Period | Average | Average | Average | Average | |||||||||||||||

| Excess Liquidity (5) |

$ | 379,125 | $ | 328,869 | $ | 217,447 | $ | 104,819 | $ | 217,017 | ||||||||||

| Total Investment Securities |

1,997,969 | 2,051,564 | 2,152,993 | 2,061,814 | 2,030,287 | |||||||||||||||

| Loans, Net of Unearned Income |

7,388,037 | 7,224,613 | 7,164,164 | 6,493,790 | 6,051,841 | |||||||||||||||

| Loans, Net of Unearned Income, Excluding Covered Loans and SOP 03-3 |

6,017,210 | 5,850,558 | 5,679,590 | 4,979,056 | 4,506,308 | |||||||||||||||

| Total Assets |

11,757,927 | 11,585,185 | 11,506,895 | 10,438,931 | 10,005,614 | |||||||||||||||

| Total Deposits |

9,289,013 | 9,252,647 | 9,169,770 | 8,246,544 | 7,893,757 | |||||||||||||||

| Total Shareholders’ Equity |

1,482,661 | 1,480,538 | 1,505,355 | 1,387,239 | 1,313,138 | |||||||||||||||

| (1) | Fully taxable equivalent (TE) calculations include the tax benefit associated with related income sources that are tax-exempt using a marginal tax rate of 35%. |

| (2) | Tangible calculations eliminate the effect of goodwill and acquisition related intangible assets and the corresponding amortization expense on a tax-effected basis where applicable. |

| (3) | All ratios are calculated on an annualized basis for the period indicated. |

| (4) | Nonperforming assets consist of nonaccruing loans, accruing loans 90 days or more past due and other real estate owned, including repossessed assets. |

| (5) | Excess Liquidity includes interest-bearing deposits in banks and fed funds sold. |

IBERIABANK CORPORATION

CONDENSED CONSOLIDATED FINANCIAL INFORMATION

(dollars in thousands except per share data)

| December 31, | (1) September 30, |

|||||||||||||||||||

| 2011 | 2010 | % Change | 2011 | % Change | ||||||||||||||||

| BALANCE SHEET (End of Period) |

||||||||||||||||||||

| ASSETS |

||||||||||||||||||||

| Cash and Due From Banks |

$ | 194,171 | $ | 94,941 | 104.5 | % | $ | 206,464 | (6.0 | %) | ||||||||||

| Interest-bearing Deposits in Banks |

379,125 | 242,837 | 56.1 | % | 263,924 | 43.6 | % | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Cash and Equivalents |

573,296 | 337,778 | 69.7 | % | 470,388 | 21.9 | % | |||||||||||||

| Investment Securities Available for Sale |

1,805,205 | 1,729,794 | 4.4 | % | 1,776,827 | 1.6 | % | |||||||||||||

| Investment Securities Held to Maturity |

192,764 | 290,020 | (33.5 | %) | 280,533 | (31.3 | %) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Investment Securities |

1,997,969 | 2,019,814 | (1.1 | %) | 2,057,360 | (2.9 | %) | |||||||||||||

| Mortgage Loans Held for Sale |

153,013 | 83,905 | 82.4 | % | 131,726 | 16.2 | % | |||||||||||||

| Loans, Net of Unearned Income |

7,388,037 | 6,035,332 | 22.4 | % | 7,169,642 | 3.0 | % | |||||||||||||

| Allowance for Loan Losses |

(193,761 | ) | (136,100 | ) | 42.4 | % | (175,320 | ) | 10.5 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Loans, net |

7,194,276 | 5,899,232 | 22.0 | % | 6,994,322 | 2.9 | % | |||||||||||||

| Loss Share Receivable |

591,844 | 726,871 | (18.6 | %) | 601,862 | (1.7 | %) | |||||||||||||

| Premises and Equipment |

285,607 | 208,403 | 37.0 | % | 280,709 | 1.7 | % | |||||||||||||

| Goodwill and Other Intangibles |

401,888 | 264,110 | 52.2 | % | 403,275 | (0.3 | %) | |||||||||||||

| Other Assets |

560,034 | 486,653 | 15.1 | % | 547,052 | 2.4 | % | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Assets |

$ | 11,757,927 | $ | 10,026,766 | 17.3 | % | $ | 11,486,694 | 2.4 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| LIABILITIES AND SHAREHOLDERS’ EQUITY |

||||||||||||||||||||

| Noninterest-bearing Deposits |

$ | 1,485,058 | $ | 878,768 | 69.0 | % | $ | 1,414,520 | 5.0 | % | ||||||||||

| NOW Accounts |

1,876,797 | 1,281,825 | 46.4 | % | 1,688,310 | 11.2 | % | |||||||||||||

| Savings and Money Market Accounts |

3,381,502 | 2,910,114 | 16.2 | % | 3,359,711 | 0.6 | % | |||||||||||||

| Certificates of Deposit |

2,545,656 | 2,844,399 | (10.5 | %) | 2,727,488 | (6.7 | %) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Deposits |

9,289,013 | 7,915,106 | 17.4 | % | 9,190,029 | 1.1 | % | |||||||||||||

| Short-term Borrowings |

192,000 | — | 100.00 | % | — | 100.00 | % | |||||||||||||

| Securities Sold Under Agreements to Repurchase |

203,543 | 220,328 | (7.6 | %) | 214,824 | (5.3 | %) | |||||||||||||

| Trust Preferred Securities |

111,862 | 111,250 | 0.6 | % | 111,862 | 0.0 | % | |||||||||||||

| Other Long-term Debt |

340,871 | 321,001 | 6.2 | % | 350,120 | (2.6 | %) | |||||||||||||

| Other Liabilities |

137,977 | 155,623 | (11.3 | %) | 148,569 | (7.1 | %) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Liabilities |

10,275,266 | 8,723,308 | 17.8 | % | 10,015,404 | 2.6 | % | |||||||||||||

| Total Shareholders’ Equity |

1,482,661 | 1,303,458 | 13.7 | % | 1,471,290 | 0.8 | % | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Liabilities and Shareholders’ Equity |

$ | 11,757,927 | $ | 10,026,766 | 17.3 | % | $ | 11,486,694 | 2.4 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| December 31, 2011 |

(1) September 30, 2011 |

(1) June 30, 2011 |

March 31, 2011 |

December 31, 2010 |

||||||||||||||||

| BALANCE SHEET (Average) |

||||||||||||||||||||

| ASSETS |

||||||||||||||||||||

| Cash and Due From Banks |

$ | 188,517 | $ | 199,610 | $ | 157,412 | $ | 145,062 | $ | 100,550 | ||||||||||

| Interest-bearing Deposits in Banks |

328,869 | 217,423 | 104,800 | 211,773 | 608,927 | |||||||||||||||

| Investment Securities |

2,051,564 | 2,152,993 | 2,061,814 | 2,030,287 | 2,014,934 | |||||||||||||||

| Mortgage Loans Held for Sale |

131,787 | 87,769 | 56,783 | 47,883 | 127,723 | |||||||||||||||

| Loans, Net of Unearned Income |

7,224,613 | 7,164,164 | 6,493,790 | 6,051,841 | 5,799,144 | |||||||||||||||

| Allowance for Loan Losses |

(167,433 | ) | (172,030 | ) | (147,889 | ) | (135,525 | ) | (129,082 | ) | ||||||||||

| Loss Share Receivable |

592,985 | 626,551 | 666,159 | 708,809 | 899,558 | |||||||||||||||

| Other Assets |

1,234,283 | 1,230,415 | 1,046,062 | 945,484 | 947,860 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Assets |

$ | 11,585,185 | $ | 11,506,895 | $ | 10,438,931 | $ | 10,005,614 | $ | 10,369,614 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| LIABILITIES AND SHAREHOLDERS’ EQUITY |

||||||||||||||||||||

| Noninterest-bearing Deposits |

$ | 1,455,097 | $ | 1,368,014 | $ | 1,090,281 | $ | 901,529 | $ | 881,634 | ||||||||||

| NOW Accounts |

1,718,337 | 1,682,568 | 1,472,547 | 1,338,437 | 1,269,316 | |||||||||||||||

| Savings and Money Market Accounts |

3,413,278 | 3,350,035 | 3,053,046 | 2,922,483 | 2,995,002 | |||||||||||||||

| Certificates of Deposit |

2,665,935 | 2,769,153 | 2,630,670 | 2,731,308 | 2,988,638 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Deposits |

9,252,647 | 9,169,770 | 8,246,544 | 7,893,757 | 8,134,590 | |||||||||||||||

| Short-term Borrowings |

4,337 | — | 21,919 | — | 3,234 | |||||||||||||||

| Securities Sold Under Agreements to Repurchase |

218,926 | 218,290 | 200,565 | 216,494 | 233,116 | |||||||||||||||

| Trust Preferred Securities |

111,862 | 111,862 | 106,944 | 109,119 | 111,292 | |||||||||||||||

| Long-term Debt |

343,687 | 352,610 | 315,570 | 307,964 | 324,528 | |||||||||||||||

| Other Liabilities |

173,188 | 149,008 | 160,150 | 165,142 | 248,671 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Liabilities |

10,104,647 | 10,001,540 | 9,051,692 | 8,692,476 | 9,055,431 | |||||||||||||||

| Total Shareholders’ Equity |

1,480,538 | 1,505,355 | 1,387,239 | 1,313,138 | 1,314,183 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Liabilities and Shareholders’ Equity |

$ | 11,585,185 | $ | 11,506,895 | $ | 10,438,931 | $ | 10,005,614 | $ | 10,369,614 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (1) | As a result of additional information relating to facts and circumstances that existed at the time of the intital valuation, the Company has recorded adjustments to certain September 30, 2011 and June 30, 2011 balances to account for its updated goodwill valuation based on additional information available during the current quarter. The Company updated its acquired loan and OREO valuations in the current quarter for OMNI and Cameron, resulting in an increase in goodwill of $19.7 million. Average balances for the respective accounts have also been revised. |

IBERIABANK CORPORATION

CONDENSED CONSOLIDATED FINANCIAL INFORMATION

(dollars in thousands except per share data)

| For The Three Months Ended | ||||||||||||||||||||

| December 31, | September 30, | |||||||||||||||||||

| 2011 | 2010 | % Change | 2011 (2) | % Change | ||||||||||||||||

| INCOME STATEMENT |

||||||||||||||||||||

| Interest Income |

$ | 111,799 | $ | 97,716 | 14.4 | % | $ | 111,966 | (0.1 | %) | ||||||||||

| Interest Expense |

19,226 | 25,367 | (24.2 | %) | 20,995 | (8.4 | %) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net Interest Income |

92,573 | 72,349 | 28.0 | % | 90,971 | 1.8 | % | |||||||||||||

| Provision for Loan Losses |

4,278 | 11,224 | (61.9 | %) | 6,127 | (30.2 | %) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net Interest Income After Provision for Loan Losses |

88,295 | 61,125 | 44.4 | % | 84,844 | 4.1 | % | |||||||||||||

| Service Charges |

6,613 | 6,013 | 10.0 | % | 7,448 | (11.2 | %) | |||||||||||||

| ATM / Debit Card Fee Income |

1,997 | 2,673 | (25.3 | %) | 3,132 | (36.2 | %) | |||||||||||||

| BOLI Proceeds and Cash Surrender Value Income |

899 | 947 | (5.1 | %) | 924 | (2.7 | %) | |||||||||||||

| Gain on Acquisition |

— | — | 0.0 | % | — | 0.0 | % | |||||||||||||

| Gain on Sale of Loans, net |

13,173 | 16,172 | (18.5 | %) | 13,438 | (2.0 | %) | |||||||||||||

| Gain (Loss) on Sale of Investments, net |

793 | 93 | 753.4 | % | 1,206 | (34.3 | %) | |||||||||||||

| Title Revenue |

4,846 | 4,715 | 2.8 | % | 4,900 | (1.1 | %) | |||||||||||||

| Broker Commissions |

2,457 | 2,326 | 5.6 | % | 2,501 | (1.7 | %) | |||||||||||||

| Other Noninterest Income |

4,677 | 5,113 | (8.5 | %) | 3,571 | 31.0 | % | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Noninterest Income |

35,455 | 38,052 | (6.8 | %) | 37,120 | (4.5 | %) | |||||||||||||

| Salaries and Employee Benefits |

51,416 | 45,160 | 13.9 | % | 52,679 | (2.4 | %) | |||||||||||||

| Occupancy and Equipment |

14,404 | 9,343 | 54.2 | % | 14,017 | 2.8 | % | |||||||||||||

| Amortization of Acquisition Intangibles |

1,384 | 1,340 | 3.2 | % | 1,385 | (0.1 | %) | |||||||||||||

| Other Noninterest Expense |

32,522 | 25,259 | 28.8 | % | 31,485 | 3.3 | % | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Noninterest Expense |

99,726 | 81,102 | 23.0 | % | 99,566 | 0.2 | % | |||||||||||||

| Income Before Income Taxes |

24,024 | 18,075 | 32.9 | % | 22,398 | 7.3 | % | |||||||||||||

| Income Taxes |

6,667 | 5,033 | 32.5 | % | 6,051 | (10.2 | %) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net Income |

$ | 17,357 | $ | 13,042 | 33.1 | % | $ | 16,347 | 6.2 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Preferred Stock Dividends |

— | — | — | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Earnings Available to Common Shareholders - Basic |

17,357 | 13,042 | 33.1 | % | 16,347 | 6.2 | % | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Earnings Allocated to Unvested Restricted Stock |

(307 | ) | (261 | ) | 17.5 | % | (290 | ) | 5.6 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Earnings Available to Common Shareholders - Diluted |

17,050 | 12,781 | 33.4 | % | 16,057 | 6.2 | % | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Earnings Per Share, diluted |

$ | 0.59 | $ | 0.48 | 22.5 | % | $ | 0.54 | 8.5 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Impact of Merger-related Expenses |

$ | 0.10 | $ | 0.04 | 126.0 | % | $ | 0.12 | (23.8 | %) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Earnings Per Share, diluted, Excluding Merger-related Expenses |

$ | 0.69 | $ | 0.52 | 30.8 | % | $ | 0.66 | 4.0 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| NUMBER OF SHARES OUTSTANDING |

||||||||||||||||||||

| Basic Shares (Average) |

29,307,297 | 26,844,077 | 9.2 | % | 29,908,906 | (2.0 | %) | |||||||||||||

| Diluted Shares (Average) |

28,857,342 | 26,498,060 | 8.9 | % | 29,472,519 | (2.1 | %) | |||||||||||||

| Book Value Shares (Period End) (1) |

29,373,905 | 26,874,613 | 9.3 | % | 29,332,856 | 0.1 | % | |||||||||||||

| 2011 | 2010 | |||||||||||||||||||

| Fourth Quarter |

Third Quarter |

Second Quarter |

First Quarter |

Fourth Quarter |

||||||||||||||||

| INCOME STATEMENT |

||||||||||||||||||||

| Interest Income |

$ | 111,799 | $ | 111,966 | $ | 97,127 | $ | 99,434 | $ | 97,716 | ||||||||||

| Interest Expense |

19,226 | 20,995 | 21,162 | 20,686 | 25,367 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net Interest Income |

92,573 | 90,971 | 75,965 | 78,748 | 72,349 | |||||||||||||||

| Provision for Loan Losses |

4,278 | 6,127 | 9,990 | 5,471 | 11,224 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net Interest Income After Provision for Loan Losses |

88,295 | 84,844 | 65,975 | 73,277 | 61,125 | |||||||||||||||

| Total Noninterest Income |

35,455 | 37,120 | 30,988 | 28,295 | 38,052 | |||||||||||||||

| Total Noninterest Expense |

99,727 | 99,566 | 92,706 | 81,732 | 81,102 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Income Before Income Taxes |

24,023 | 22,398 | 4,257 | 19,840 | 18,075 | |||||||||||||||

| Income Taxes |

6,667 | 6,051 | (929 | ) | 5,193 | 5,033 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Net Income |

$ | 17,357 | $ | 16,347 | $ | 5,186 | $ | 14,647 | $ | 13,042 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Preferred Stock Dividends |

— | — | — | — | — | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Earnings Available to Common Shareholders - Basic |

17,357 | 16,347 | 5,186 | 14,647 | 13,042 | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Earnings Allocated to Unvested Restricted Stock |

(307 | ) | (290 | ) | (291 | ) | (291 | ) | (261 | ) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Earnings Available to Common Shareholders - Diluted |

$ | 17,050 | $ | 16,057 | $ | 4,895 | $ | 14,356 | $ | 12,781 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Earnings Per Share, basic |

$ | 0.59 | $ | 0.55 | $ | 0.19 | $ | 0.54 | $ | 0.49 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Earnings Per Share, diluted |

$ | 0.59 | $ | 0.54 | $ | 0.18 | $ | 0.54 | $ | 0.48 | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Book Value Per Common Share |

$ | 50.48 | $ | 50.16 | $ | 49.88 | $ | 48.68 | $ | 48.50 | ||||||||||

| Tangible Book Value Per Common Share |

$ | 36.80 | $ | 36.41 | $ | 38.53 | $ | 38.95 | $ | 38.68 | ||||||||||

| Return on Average Assets |

0.59 | % | 0.56 | % | 0.20 | % | 0.59 | % | 0.50 | % | ||||||||||

| Return on Average Common Equity |

4.65 | % | 4.31 | % | 1.50 | % | 4.52 | % | 3.94 | % | ||||||||||

| Return on Average Tangible Common Equity |

6.72 | % | 6.22 | % | 2.24 | % | 5.95 | % | 5.26 | % | ||||||||||

| (1) | Shares used for book value purposes exclude shares held in treasury at the end of the period. |

| (2) | As a result of additional information, the Company has recorded adjustments to certain September 30, 2011 amounts to account for its updated goodwill valuation based on additional information available during the current quarter. The Company updated its acquired loan and OREO valuations in the current quarter, resulting in a decrease in interest income and income tax expense of $1.5 million and $0.5 million, respectively, for the three months ended September 30, 2011. Affected ratios and per share amounts have also been revised. |

IBERIABANK CORPORATION

CONDENSED CONSOLIDATED FINANCIAL INFORMATION

(dollars in thousands except per share data)

| For The Year Ended | ||||||||||||

| December 31, | ||||||||||||

| 2011 | 2010 | % Change | ||||||||||

| INCOME STATEMENT |

||||||||||||

| Interest Income |

$ | 420,327 | $ | 396,371 | 6.0 | % | ||||||

| Interest Expense |

82,069 | 114,744 | (28.5 | %) | ||||||||

|

|

|

|

|

|

|

|||||||

| Net Interest Income |

338,258 | 281,627 | 20.1 | % | ||||||||

| Provision for Loan Losses |

25,867 | 42,451 | (39.1 | %) | ||||||||

|

|

|

|

|

|

|

|||||||

| Net Interest Income After Provision for Loan Losses |

312,391 | 239,176 | 30.6 | % | ||||||||

| Service Charges |

25,915 | 24,375 | 6.3 | % | ||||||||

| ATM / Debit Card Fee Income |

11,008 | 10,117 | 8.8 | % | ||||||||

| BOLI Proceeds and Cash Surrender Value Income |

3,296 | 3,100 | 6.3 | % | ||||||||

| Gain on Acquisition |

— | 3,781 | (100.0 | %) | ||||||||

| Gain on Sale of Loans, net |

44,892 | 47,689 | (5.9 | %) | ||||||||

| Gain (Loss) on Sale of Investments, net |

3,475 | 5,251 | (33.8 | %) | ||||||||

| Title Revenue |

18,048 | 18,083 | (0.2 | %) | ||||||||

| Broker Commissions |

10,224 | 7,530 | 35.8 | % | ||||||||

| Other Noninterest Income |

15,001 | 13,964 | 7.4 | % | ||||||||

|

|

|

|

|

|

|

|||||||

| Total Noninterest Income |

131,859 | 133,890 | (1.5 | %) | ||||||||

| Salaries and Employee Benefits |

193,773 | 161,482 | 20.0 | % | ||||||||

| Occupancy and Equipment |

49,600 | 33,837 | 46.6 | % | ||||||||

| Amortization of Acquisition Intangibles |

5,121 | 4,935 | 3.8 | % | ||||||||

| Other Noninterest Expense |

125,237 | 103,995 | 20.4 | % | ||||||||

|

|

|

|

|

|

|

|||||||

| Total Noninterest Expense |

373,731 | 304,249 | 22.8 | % | ||||||||

| Income Before Income Taxes |

70,519 | 68,817 | 2.5 | % | ||||||||

| Income Taxes |

16,981 | 19,991 | (15.1 | %) | ||||||||

|

|

|

|

|

|

|

|||||||

| Net Income |

$ | 53,538 | $ | 48,826 | 9.7 | % | ||||||

|

|

|

|

|

|

|

|||||||

| Preferred Stock Dividends |

— | — | — | |||||||||

|

|

|

|

|

|

|

|||||||

| Earnings Available to Common Shareholders - Basic |

53,538 | 48,826 | 9.7 | % | ||||||||

|

|

|

|

|

|

|

|||||||

| Earnings Allocated to Unvested Restricted Stock |

(966 | ) | (978 | ) | (1.2 | %) | ||||||

|

|

|

|

|

|

|

|||||||

| Earnings Available to Common Shareholders - Diluted |

52,572 | 47,848 | 9.9 | % | ||||||||

|

|

|

|

|

|

|

|||||||

| Earnings Per Share, diluted |

$ | 1.87 | $ | 1.88 | (0.9 | %) | ||||||

|

|

|

|

|

|

|

|||||||

| Impact of Merger-related Expenses |

$ | 0.41 | $ | 0.23 | 76.5 | % | ||||||

|

|

|

|

|

|

|

|||||||

| Earnings Per Share, diluted, Excluding Merger-related Expenses |

$ | 2.28 | $ | 2.11 | 75.7 | % | ||||||

|

|

|

|

|

|

|

|||||||

IBERIABANK CORPORATION

CONDENSED CONSOLIDATED FINANCIAL INFORMATION

(dollars in thousands)

| December 31, | September 30, | |||||||||||||||||||

| 2011 | 2010 | % Change | 2011 | % Change | ||||||||||||||||

| LOANS RECEIVABLE |

||||||||||||||||||||

| Residential Mortgage Loans: |

||||||||||||||||||||

| Residential 1-4 Family |

$ | 462,454 | $ | 616,550 | (25.0 | %) | $ | 490,737 | (5.8 | %) | ||||||||||

| Construction/ Owner Occupied |

16,143 | 14,822 | 8.9 | % | 17,256 | (6.4 | %) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Residential Mortgage Loans |

478,597 | 631,372 | (24.2 | %) | 507,993 | (5.8 | %) | |||||||||||||

| Commercial Loans: |

||||||||||||||||||||

| Real Estate |

3,334,582 | 2,647,107 | 26.0 | % | 3,312,138 | 0.7 | % | |||||||||||||

| Business |

2,045,399 | 1,515,856 | 34.9 | % | 1,872,710 | 9.2 | % | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Commercial Loans |

5,379,982 | 4,162,963 | 29.2 | % | 5,184,848 | 3.8 | % | |||||||||||||

| Consumer Loans: |

||||||||||||||||||||

| Indirect Automobile |

261,707 | 255,322 | 2.5 | % | 260,002 | 0.7 | % | |||||||||||||

| Home Equity |

1,066,349 | 834,840 | 27.7 | % | 1,022,292 | 4.3 | % | |||||||||||||

| Automobile |

38,600 | 31,266 | 23.5 | % | 36,753 | 5.0 | % | |||||||||||||

| Credit Card Loans |

48,732 | 44,071 | 10.6 | % | 45,700 | 6.6 | % | |||||||||||||

| Other |

114,070 | 75,500 | 51.1 | % | 112,055 | 1.8 | % | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Consumer Loans |

1,529,458 | 1,240,998 | 23.2 | % | 1,476,802 | 3.6 | % | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Loans Receivable |

7,388,037 | 6,035,332 | 22.4 | % | 7,169,642 | 3.0 | % | |||||||||||||

|

|

|

|

|

|||||||||||||||||

| Allowance for Loan Losses |

(193,761 | ) | (136,100 | ) | (175,320 | ) | ||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||

| Loans Receivable, Net |

$ | 7,194,276 | $ | 5,899,232 | $ | 6,994,322 | ||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||

| December 31, | September 30, | |||||||||||||||||||

| 2011 | 2010 | % Change | 2011 | % Change | ||||||||||||||||

| ASSET QUALITY DATA (1) |

||||||||||||||||||||

| Nonaccrual Loans |

$ | 719,236 | $ | 816,244 | (11.9 | %) | $ | 805,247 | (10.7 | %) | ||||||||||

| Foreclosed Assets |

4 | 163 | (97.8 | %) | 32 | (88.6 | %) | |||||||||||||

| Other Real Estate Owned |

125,042 | 69,054 | 81.1 | % | 117,611 | 6.3 | % | |||||||||||||

| Accruing Loans More Than 90 Days Past Due |

29,003 | 53,112 | (45.4 | %) | 24,741 | 17.2 | % | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Nonperforming Assets |

$ | 873,285 | $ | 938,573 | (7.0 | %) | $ | 947,631 | (7.8 | %) | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Loans 30-89 Days Past Due |

86,467 | 111,345 | (22.3 | %) | 74,604 | 15.9 | % | |||||||||||||

| Nonperforming Assets to Total Assets |

7.43 | % | 9.36 | % | (20.6 | %) | 8.25 | % | (9.9 | %) | ||||||||||

| Nonperforming Assets to Total Loans and OREO |

11.62 | % | 15.37 | % | (24.4 | %) | 13.00 | % | (10.6 | %) | ||||||||||

| Allowance for Loan Losses to Nonperforming Loans (4) |

25.9 | % | 15.7 | % | 65.4 | % | 21.1 | % | 22.6 | % | ||||||||||

| Allowance for Loan Losses to Nonperforming Assets |

22.2 | % | 14.5 | % | 53.0 | % | 18.5 | % | 19.9 | % | ||||||||||

| Allowance for Loan Losses to Total Loans |

2.62 | % | 2.26 | % | 16.3 | % | 2.45 | % | 7.3 | % | ||||||||||

| Year to Date Charge-offs |

$ | 16,535 | $ | 33,858 | (51.2 | %) | $ | 10,186 | N/M | |||||||||||

| Year to Date Recoveries |

(8,351 | ) | (6,818 | ) | 22.5 | % | (7,352 | ) | N/M | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Year to Date Net Charge-offs (Recoveries) |

$ | 8,184 | $ | 27,040 | (69.7 | %) | $ | 2,834 | N/M | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Quarter to Date Net Charge-offs (Recoveries) |

$ | 5,350 | $ | 10,506 | (49.1 | %) | $ | 1,880 | 184.7 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (1) | For purposes of this table, nonperforming assets include all loans meeting nonperforming asset criteria, including assets acquired in FDIC-assisted transactions. |

| (2) | Troubled debt restructurings meeting past due and nonaccruing criteria are included in loans past due and nonaccrual loans above. |

| (3) | Current troubled debt restructurings are defined as troubled debt restructurings not past due or on nonaccrual status for the respective periods. |

| (4) | Nonperforming loans consist of nonaccruing loans and accruing loans 90 days or more past due. |

N/M - Comparison of the information presented is not meaningful given the periods presented

IBERIABANK CORPORATION

CONDENSED CONSOLIDATED FINANCIAL INFORMATION

(dollars in thousands)

| December 31, | September 30, | |||||||||||||||||||

| 2011 | 2010 | % Change | 2011 | % Change | ||||||||||||||||

| LOANS RECEIVABLE (Ex-Covered Assets and Acquired Impaired Loans) (1) |

||||||||||||||||||||

| Residential Mortgage Loans: |

||||||||||||||||||||

| Residential 1-4 Family |

$ | 257,635 | $ | 355,164 | (27.5 | %) | $ | 278,991 | (7.7 | %) | ||||||||||

| Construction/ Owner Occupied |

16,143 | 14,822 | 8.9 | % | 17,256 | (6.4 | %) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Residential Mortgage Loans |

273,778 | 369,986 | (26.0 | %) | 296,247 | (7.6 | %) | |||||||||||||

| Commercial Loans: |

||||||||||||||||||||

| Real Estate |

2,592,008 | 1,781,758 | 45.5 | % | 2,487,885 | 4.2 | % | |||||||||||||

| Business |

1,869,990 | 1,341,338 | 39.4 | % | 1,723,423 | 8.5 | % | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Commercial Loans |

4,461,998 | 3,123,096 | 42.9 | % | 4,211,308 | 6.0 | % | |||||||||||||

| Consumer Loans: |

||||||||||||||||||||

| Indirect Automobile |

261,547 | 255,322 | 2.4 | % | 259,789 | 0.7 | % | |||||||||||||

| Home Equity |

824,873 | 555,749 | 48.4 | % | 773,388 | 6.7 | % | |||||||||||||

| Automobile |

38,560 | 31,266 | 23.3 | % | 36,716 | 5.0 | % | |||||||||||||

| Credit Card Loans |

47,763 | 42,916 | 11.3 | % | 44,710 | 6.8 | % | |||||||||||||

| Other |

108,692 | 74,250 | 46.4 | % | 110,340 | (1.5 | %) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Consumer Loans |

1,281,434 | 959,503 | 33.6 | % | 1,224,943 | 4.6 | % | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Loans Receivable |

6,017,210 | 4,452,585 | 35.2 | % | 5,732,498 | 5.0 | % | |||||||||||||

|

|

|

|

|

|||||||||||||||||

| Allowance for Loan Losses |

(74,862 | ) | (62,460 | ) | (76,864 | ) | ||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||

| Loans Receivable, Net |

$ | 5,942,349 | $ | 4,390,125 | $ | 5,655,634 | ||||||||||||||

|

|

|

|

|

|

|

|||||||||||||||

| December 31, | September 30, | |||||||||||||||||||

| 2011 | 2010 | % Change | 2011 | % Change | ||||||||||||||||

| ASSET QUALITY DATA (Ex-Covered Assets and Acquired Impaired Loans) (1) |

||||||||||||||||||||

| Nonaccrual Loans |

$ | 60,303 | $ | 49,496 | 21.8 | % | $ | 70,833 | (14.9 | %) | ||||||||||

| Foreclosed Assets |

4 | 9 | (59.8 | %) | 32 | (88.6 | %) | |||||||||||||

| Other Real Estate Owned |

21,378 | 18,487 | 15.6 | % | 12,269 | 74.3 | % | |||||||||||||

| Accruing Loans More Than 90 Days Past Due |

3,580 | 1,455 | 146.1 | % | 1,149 | 211.4 | % | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Total Nonperforming Assets |

$ | 85,265 | $ | 69,447 | 22.8 | % | $ | 84,283 | 1.2 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Loans 30-89 Days Past Due |

19,455 | 13,311 | 46.2 | % | 25,678 | (24.2 | %) | |||||||||||||

| Troubled Debt Restructurings (2) |

27,855 | 17,471 | 59.4 | % | 29,105 | (4.3 | %) | |||||||||||||

| Current Troubled Debt Restructurings (3) |

161 | 10,215 | (98.4 | %) | 1,415 | (88.6 | %) | |||||||||||||

| Nonperforming Assets to Total Assets |

0.87 | % | 0.91 | % | (4.1 | %) | 0.89 | % | (2.3 | %) | ||||||||||

| Nonperforming Assets to Total Loans and OREO |

1.41 | % | 1.55 | % | (9.2 | %) | 1.47 | % | (3.6 | %) | ||||||||||

| Allowance for Loan Losses to Nonperforming Loans (4) |

117.2 | % | 122.6 | % | (4.4 | %) | 106.8 | % | 9.7 | % | ||||||||||

| Allowance for Loan Losses to Nonperforming Assets |

87.8 | % | 89.9 | % | (2.4 | %) | 91.2 | % | (3.7 | %) | ||||||||||

| Allowance for Loan Losses to Total Loans |

1.24 | % | 1.40 | % | (11.3 | %) | 1.34 | % | (6.9 | %) | ||||||||||

| Year to Date Charge-offs |

$ | 15,398 | $ | 33,533 | (54.1 | %) | $ | 9,786 | N/M | |||||||||||

| Year to Date Recoveries |

(7,825 | ) | (6,816 | ) | 14.8 | % | (6,836 | ) | N/M | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Year to Date Net Charge-offs (Recoveries) |

$ | 7,573 | $ | 26,717 | (71.7 | %) | $ | 2,950 | N/M | |||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| Quarter to Date Net Charge-offs (Recoveries) |

$ | 4,622 | $ | 10,472 | (55.9 | %) | $ | 1,711 | 170.2 | % | ||||||||||

|

|

|

|

|

|

|

|

|

|

|

|||||||||||

| (1) | For purposes of this table, nonperforming assets include all loans meeting nonperforming asset criteria, including assets acquired in FDIC-assisted transactions. |

| (2) | Troubled debt restructurings meeting past due and nonaccruing criteria are included in loans past due and nonaccrual loans above. |

| (3) | Current troubled debt restructurings are defined as troubled debt restructurings not past due or on nonaccrual status for the respective periods. |

| (4) | Nonperforming loans consist of nonaccruing loans and accruing loans 90 days or more past due. |

N/M - Comparison of the information presented is not meaningful given the periods presented

IBERIABANK CORPORATION

CONDENSED CONSOLIDATED FINANCIAL INFORMATION

Taxable Equivalent Basis

(dollars in thousands)

| For The Quarter Ended | ||||||||||||||||||||||||

| December 31, 2011 | September 30, 2011 | December 31, 2010 | ||||||||||||||||||||||

| Average Balance |

Average Yield/Rate (%) |

Average Balance (3) |

Average Yield/Rate (%) |

Average Balance |

Average Yield/Rate (%) |

|||||||||||||||||||

| ASSETS |

||||||||||||||||||||||||

| Earning Assets: |

||||||||||||||||||||||||

| Loans Receivable: |

||||||||||||||||||||||||

| Mortgage Loans |

$ | 492,262 | 7.00 | % | $ | 526,668 | 7.14 | % | $ | 637,748 | 7.12 | % | ||||||||||||

| Commercial Loans (TE) (1) |

5,235,122 | 7.22 | % | 5,168,460 | 5.14 | % | 3,928,998 | 6.02 | % | |||||||||||||||

| Consumer and Other Loans |

1,497,229 | 6.29 | % | 1,469,036 | 6.43 | % | 1,232,398 | 7.08 | % | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total Loans |

7,224,613 | 7.01 | % | 7,164,164 | 5.55 | % | 5,799,144 | 6.37 | % | |||||||||||||||

| Loss Share Receivable |

592,985 | -19.31 | % | 626,551 | -1.63 | % | 899,558 | -3.75 | % | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total Loans and Loss Share Receivable |

7,817,598 | 5.02 | % | 7,790,715 | 4.98 | % | 6,698,702 | 5.01 | % | |||||||||||||||

| Mortgage Loans Held for Sale |

131,787 | 3.21 | % | 87,769 | 4.19 | % | 127,723 | 3.08 | % | |||||||||||||||

| Investment Securities (TE) (1)(2) |

1,985,826 | 2.57 | % | 2,110,070 | 2.72 | % | 1,946,658 | 2.60 | % | |||||||||||||||

| Other Earning Assets |

385,158 | 0.68 | % | 278,771 | 0.78 | % | 678,245 | 0.42 | % | |||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Total Earning Assets |