Exhibit 99.E

© South African Reserve Bank

All rights reserved. No part of this publication may be reproduced, stored in a retrieval system, or transmitted in any form or by any means, electronic, mechanical, photocopying, recording or otherwise, without fully acknowledging the Quarterly Bulletin of the South African Reserve Bank as the source. The contents of this publication are intended for general information only and are not intended to serve as financial or other advice. While every precaution is taken to ensure the accuracy of information, the South African Reserve Bank shall not be liable to any person for inaccurate information or opinions contained in this publication.

| Enquiries relating to this Bulletin should be addressed to: | ||||

| Head: Economic Research and Statistics Department |

||||

| South African Reserve Bank |

||||

| P O Box 427 |

||||

| Pretoria 0001 |

||||

| Tel. +27 12 313-3668/3676 |

||||

| http://www.reservebank.co.za |

ISSN 0038-2620 | |||

|

Quarterly Bulletin March 2016 |

Contents

Quarterly Economic Review

| Introduction |

1 | |||

| Domestic economic developments |

4 | |||

| Domestic output |

4 | |||

| Real gross domestic expenditure |

8 | |||

| Factor income |

14 | |||

| Gross saving |

15 | |||

| Employment |

15 | |||

| Labour cost and productivity |

20 | |||

| Prices |

22 | |||

| Foreign trade and payments |

29 | |||

| International economic developments |

29 | |||

| Current account |

32 | |||

| Financial account |

39 | |||

| Foreign debt |

42 | |||

| International investment position |

44 | |||

| International reserves and liquidity |

45 | |||

| Exchange rates |

47 | |||

| Turnover in the South African foreign-exchange market |

50 | |||

| Monetary developments, interest rates and financial markets |

51 | |||

| Structural and regulatory issues in 2015 and early 2016 |

51 | |||

| Money supply |

56 | |||

| Credit extension |

59 | |||

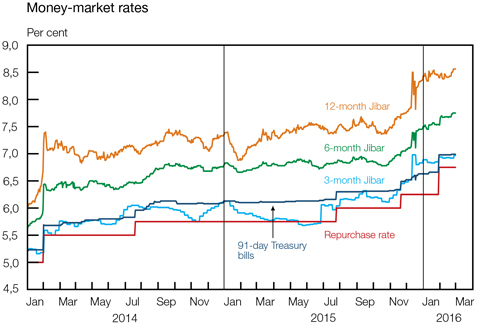

| Interest rates and yields |

62 | |||

| Money market |

67 | |||

| Bond market |

68 | |||

| Share market |

70 | |||

| Market for exchange-traded derivatives |

72 | |||

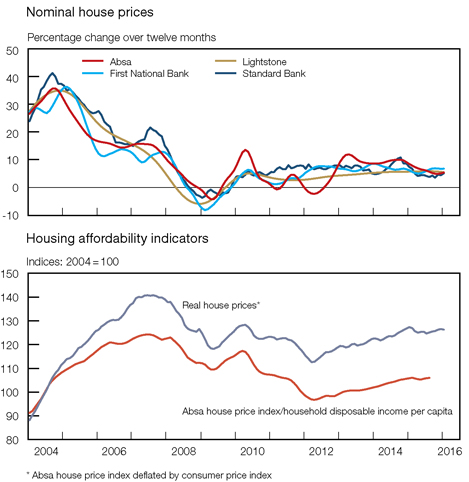

| Real-estate market |

73 | |||

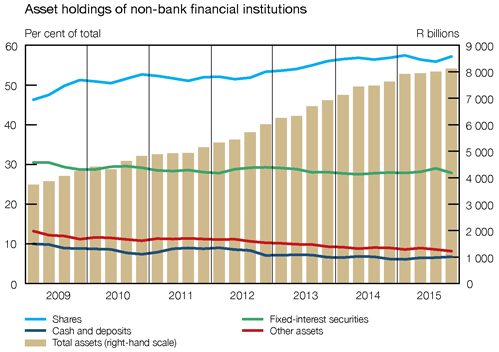

| Non-bank financial intermediaries |

74 | |||

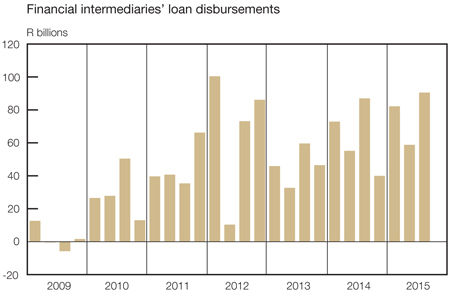

| Flow of funds |

75 | |||

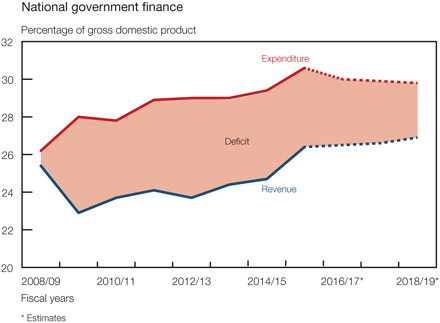

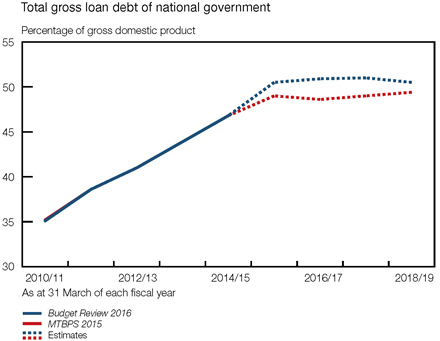

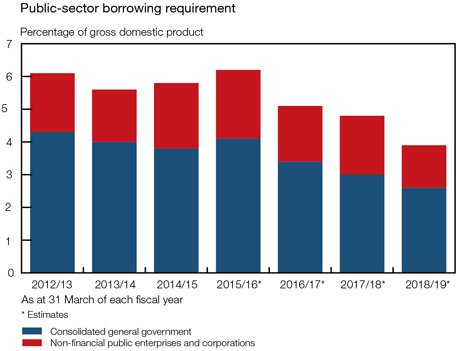

| Public finance |

78 | |||

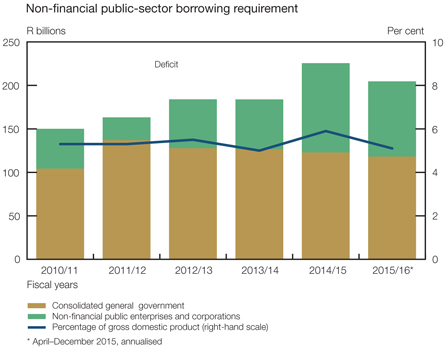

| Non-financial public-sector borrowing requirement |

78 | |||

| Budget comparable analysis of national government finance |

81 | |||

| The Budget for the fiscal years 2016/17 to 2018/19 |

88 | |||

| Statement issued by Lesetja Kganyago, Governor of the South African Reserve Bank |

||||

| 28 January 2016 |

94 | |||

| Note |

||||

| Business cycles in South Africa from 2009 to 2013 |

102 | |||

| Arrangements between the South African Reserve Bank and Statistics South Africa regarding the transfer of the compilation of the gross domestic product (expenditure approach) to Statistics South Africa |

113 | |||

| Statistical tables |

||||

| Contents |

S–0 | |||

| Statistical tables |

S–2 | |||

| Key information |

S–146 | |||

| Quarterly Bulletin March 2016 |

|

Quarterly Economic Review

Introduction

The global economic recovery remained modest and uneven in 2015. Following three successive quarters of economic expansion, global output faltered notably in the fourth quarter of 2015 as both the advanced and emerging-market economies recorded slower growth over the period. In 2015 as a whole, output growth accelerated marginally in advanced economies but slowed markedly in emerging-market and developing countries. In its World Economic Outlook Update published in January 2016, the International Monetary Fund (IMF) lowered its projections for global growth by 0,2 percentage points for both 2016 and 2017. The risks to the outlook, however, remained skewed to the downside and would be influenced by, inter alia, the general slowdown in emerging-market economies, the decline in commodity prices, and the gradual tightening of monetary conditions in the United States (US).

Global inflation remained muted in 2015 and has moved broadly sideways in recent months, reinforced by a notable further decline in international oil prices since September 2015. Monetary policy measures are expected to remain accommodative in most advanced economies, but could be tightened in some emerging-market countries faced by the need to adjust to lower commodity prices, declining export earnings, and depreciating exchange rates.

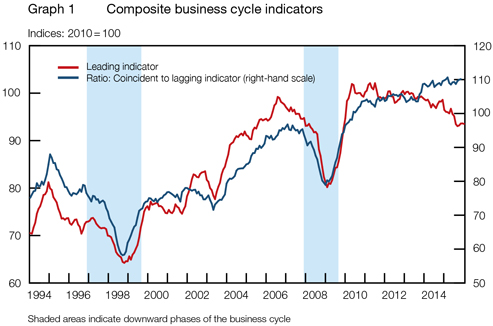

Domestically, the South African Reserve Bank (the Bank or SARB) has officially identified November 2013 as the upper turning point in the business cycle, implying that the South African economy is now officially in a downward phase of the business cycle.

Concurrent with indications of slower quarter-to-quarter global economic growth, real economic growth in South Africa slowed marginally to an annualised rate of only 0,6 per cent in the fourth quarter of 2015, bringing the real growth rate for 2015 as a whole to a disappointing 1,3 per cent. Agricultural output declined further in the final quarter of the year as dry weather conditions adversely affected field crop production in most areas of South Africa; livestock production held up well over the period, although in part reflecting the forced marketing of animals due to the drought. Mining output rose on account of increased production of coal, platinum-group metals and building materials, but more especially diamonds and nickel. Real value added in the manufacturing sector contracted anew in the final quarter of 2015 due to disappointing global and domestic demand conditions coupled with sustained supply-side constraints. Activity in the electricity, gas and water as well as construction sectors, however, strengthened somewhat during the quarter. In the services sector, the real value added expanded at a slower pace despite slightly stronger growth in the commerce sector.

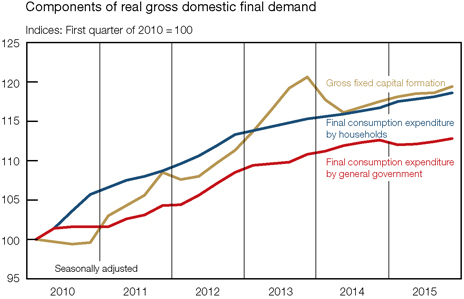

While growth in real production slowed marginally, real gross domestic expenditure growth picked up further to an annualised rate of 4,3 per cent in the fourth quarter of 2015. Growth in real final consumption expenditure by households inched higher, consistent with a slight acceleration in real disposable income and probably reinforced by expectations of higher prices in future arising from exchange rate depreciation. Firm increases were registered in the purchases of durable goods, in particular transport equipment, as well as semi-durable goods. Expenditure on non-durable goods and services, however, increased at more subdued rates over the period. The household-debt-to-disposable-income ratio decreased somewhat while the debt-service-cost ratio rose marginally in the final quarter of 2015. The pace of increase in general government’s real final consumption expenditure accelerated slightly over the period as government stepped up spending on non-wage goods and services.

Growth in total gross fixed capital formation accelerated somewhat in the fourth quarter of 2015, reflecting higher real capital outlays by all three institutional sectors. Real fixed capital formation by the private sector accelerated largely due to increased capital spending on renewable energy projects; real capital outlays in most other sectors contracted over the period given the availability of ample capacity. Over the same period, capital outlays by public corporations accelerated notably, underpinned by increased spending on construction works and transport equipment, whereas capital spending by general government continued at a steady pace to address the infrastructure bottlenecks constraining the economy from the supply side.

| Quarterly Bulletin March 2016 |

|

The sharp decline in real inventory holdings in the middle quarters of 2015 moderated in the final quarter of the year. The slower pace of destocking could largely be explained by a significant increase in the volume of crude oil imports following maintenance work performed at certain oil refineries in the preceding quarters alongside lower export sales. Viewed from the expenditure side, the disappointing performance of the economy was reinforced by weak net exports to the rest of the world.

Against the generally subdued growth in economic activity, enterprise-surveyed employment in the formal non-agricultural sector advanced only marginally in the year to the third quarter of 2015. Household-surveyed employment statistics that extend to the fourth quarter of 2015 suggest more vigorous increases in employment in the informal sector, although roughly a quarter of the workforce remains unemployed. With year-on-year remuneration growth slowing at a slightly faster pace than year-on-year output growth, the pace of increase in nominal unit labour cost in the formal non-agricultural sector moderated marginally to 5,0 per cent in the third quarter – consistent with the inflation target range.

Inflationary pressures have intensified in recent months. Headline consumer price inflation breached the upper limit of the inflation target range in January 2016 and is expected to remain outside the target throughout the year. The acceleration in headline consumer price inflation mainly reflected the delayed response of food price inflation to the severe drought conditions and the sharp depreciation in the exchange rate of the rand towards the end of 2015 when investor confidence retreated. Consumer goods price inflation quickened noticeably over the period, driven mainly by movements in petrol price inflation. Against the background of a steady uptick in most measures of producer and consumer price inflation, the inflation expectations of business and trade union representatives were adjusted upwards towards the end of 2015, exceeding the 6 per cent level by an even bigger margin.

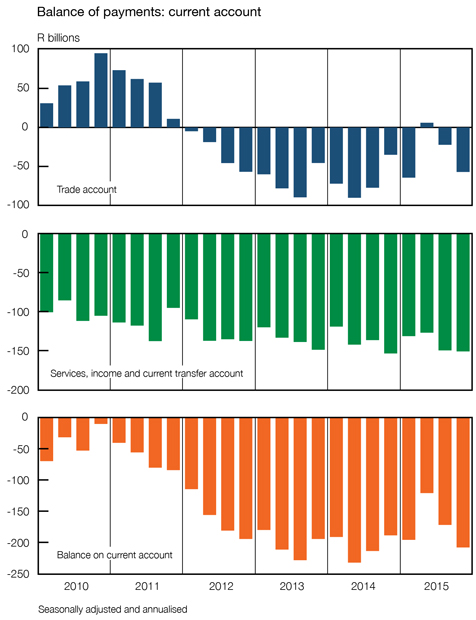

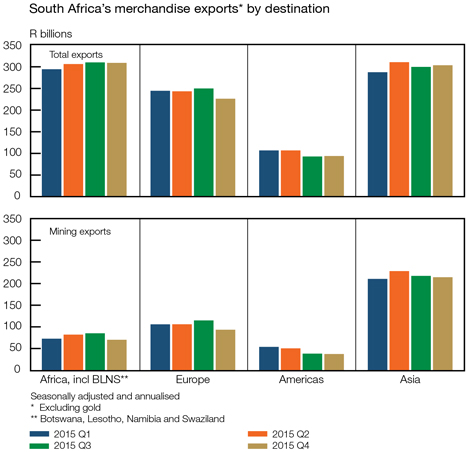

Reflecting the fragile world economy and the concomitant slower growth in world trade volumes, South African export volumes declined in the fourth quarter of 2015, the first contraction since the second quarter of 2014. Though the depreciation in the exchange value of the rand boosted the export earnings of domestic producers, these benefits were more than fully offset by a further fall in international commodity prices. By contrast, import volumes increased further, reflecting firm growth in real domestic expenditure that flowed through to rising imports of capital and consumption goods. South Africa’s trade deficit resultantly widened in the final quarter of 2015 notwithstanding a slight improvement in the country’s terms of trade. Together with a somewhat larger shortfall on the services, income and current transfer account, the deficit on the current account of the balance of payments widened to 5,1 per cent of gross domestic product in the fourth quarter of 2015.

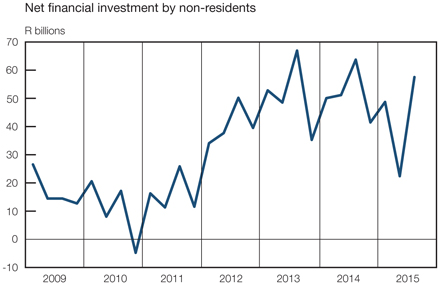

Despite bouts of increased risk awareness towards investment in emerging-market assets, the net inward movement of foreign capital was sufficient to finance the deficit on the current account. Financial inflows mainly took the form of other investment capital, as the domestic banking sector recorded an increase in foreign currency-denominated loans received as well as non-resident deposits while simultaneously repatriating loan finance previously extended to non-resident parties. The portfolio and direct investment categories registered capital outflows on a net basis during the quarter concerned.

In an environment of fairly subdued economic activity, growth in money supply and in total loans and advances to the domestic private sector nevertheless picked up moderately towards the end of 2015. Bank advances to the corporate sector rose firmly on account of increases in mortgage advances underpinning commercial property development and general loans related to projects in areas such as renewable energy. Credit extension to the household sector, however, remained subdued. Under these circumstances, house prices continued to increase, but at a pedestrian pace.

|

|

Quarterly Bulletin March 2016 |

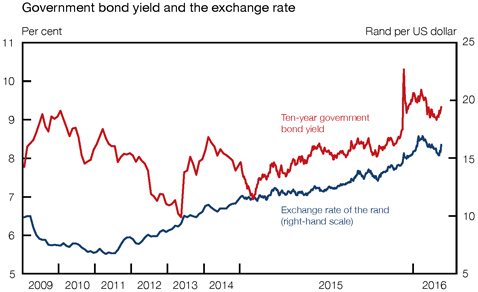

South African bond yields trended slowly higher during most of 2015 as inflation expectations deteriorated, but rose sharply in December as a sudden decline in investor confidence related to political events was reflected in the money and capital markets and the market for foreign exchange. Prompt action taken to restore confidence led to a partial recovery in financial rates and prices in the final weeks of 2015 and early 2016.

The budget for fiscal 2016/17, delivered in February 2016, strengthened measures to narrow the fiscal deficit more rapidly in the next three years and to stabilise government’s gross loan debt. The narrowing of the deficit is envisaged through various adjustments on both the revenue and expenditure side. Responding to the risk of higher inflation but also mindful of the need to protect the fragile economic growth momentum, the Monetary Policy Committee (MPC) of the SARB raised the repurchase rate by 25 basis points in July 2015 and by another 25 basis points in November. Given the subsequent notable deterioration in the inflation outlook, the MPC decided at its January 2016 meeting to raise the policy rate by a further 50 basis points to 6,75 per cent per annum, effective from 29 January 2016.

| Quarterly Bulletin March 2016 |

|

Domestic economic developments

Domestic output1, 2

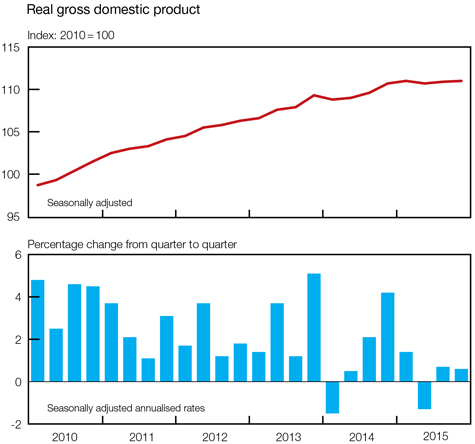

Economic activity in South Africa increased at a slightly slower pace in the fourth quarter of 2015. Following a contraction in the second quarter of 2015, annualised growth in real gross domestic product (GDP) accelerated to 0,7 per cent in the third quarter before slowing marginally to 0,6 per cent in the fourth quarter. The slower growth in the final quarter could be attributed to a decline in the real value added by the secondary sector alongside steady, but slower, growth in the tertiary sector. The real value added by the primary sector declined further over the period albeit at a somewhat slower pace than in the third quarter.

Excluding the contribution of the drought-affected agricultural sector, annualised growth in real GDP decelerated marginally from 1,1 per cent in the third quarter of 2015 to 0,9 per cent in the final quarter.

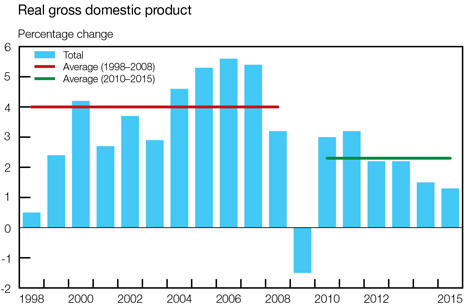

Consistent with the sluggish quarter-to-quarter growth registered throughout the year, growth in real gross domestic production moderated further from 1,5 per cent in 2014 to a disappointing 1,3 per cent in 2015 – with the exception of 2009, the slowest rate of expansion during the past 17 years. On average, annual growth amounted to 2,3 per cent between 2010 and 2015 compared with an annual average rate of 4,0 per cent in the ten years prior to 2009.

The lacklustre performance of the South African economy in 2015 could, to an important extent, be attributed to subdued business and consumer confidence levels, muted demand conditions, ongoing supply-side constraints, a further decline in the prices of key export commodities, and the knock-on effects of the widespread drought conditions in many parts of the country.

|

|

Quarterly Bulletin March 2016 |

Subsequent to a sharp contraction of 10,4 per cent in the third quarter of 2015, the real value added by the primary sector declined further, albeit at a slower pace in the final quarter of the year. Agricultural output shrank at a faster pace, alongside an increase in the real output of the mining sector.

Real gross domestic product

Percentage change at seasonally adjusted annualised rates

| 2014 | 2015 | |||||||||||||||||||||||

| Sector | Year | 1st qr | 2nd qr | 3rd qr | 4th qr | Year | ||||||||||||||||||

| Primary sector |

0,0 | 2,9 | -9,5 | -10,4 | -2,0 | 0,2 | ||||||||||||||||||

| Agriculture |

5,6 | -18,0 | -19,7 | -12,6 | -14,0 | -8,4 | ||||||||||||||||||

| Mining |

-1,6 | 10,2 | -6,4 | -9,8 | 1,5 | 3,0 | ||||||||||||||||||

| Secondary sector |

0,6 | -1,0 | -5,1 | 3,3 | -1,5 | 0,3 | ||||||||||||||||||

| Manufacturing |

0,0 | -2,4 | -6,3 | 6,2 | -2,6 | 0,1 | ||||||||||||||||||

| Tertiary sector |

2,1 | 1,7 | 1,0 | 1,9 | 1,5 | 1,7 | ||||||||||||||||||

| Non-primary sector |

1,8 | 1,1 | -0,4 | 2,2 | 0,8 | 1,4 | ||||||||||||||||||

| Total |

1,5 | 1,4 | -1,3 | 0,7 | 0,6 | 1,3 | ||||||||||||||||||

Activity in the agricultural sector contracted unabatedly throughout 2015. In addition to the devastating effect of dry weather conditions on field crops as well as animal and horticultural production, the country also experienced record-high temperatures in the final quarter of 2015, further scorching arable land. Livestock production held up well over the period, mitigating the rate of contraction. Negative growth in all four quarters of 2015 accordingly culminated in an annual decline of 8,4 per cent for the year as a whole.

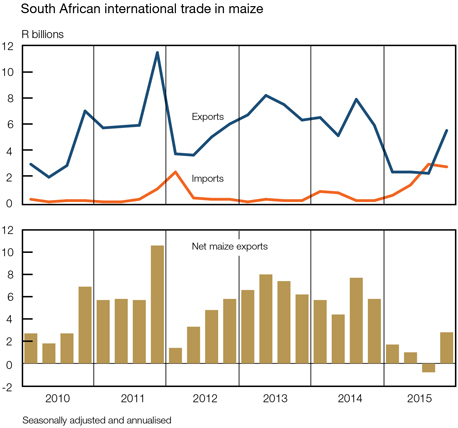

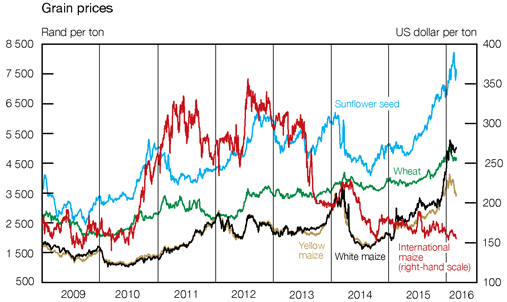

Early indications do not bode well for the 2015/16 planting and production season. According to the February 2016 estimates of the Crop Estimate Committee, South African producers are expected to plant roughly a 26 per cent smaller area than in the preceding year. Preliminary estimates of the commercial maize crop for the 2015/16 season amount to 7,3 million tons as opposed to 9,9 million tons in the 2014/15 season. Taking into account the available stock of white and yellow maize, the country might have to import white and yellow maize to meet annual domestic commercial consumption of roughly 9,6 million tons.

Mining production picked up in the final quarter of 2015; annualised growth in real output accelerated from -9,8 per cent in the third quarter of 2015 to 1,5 per cent in the final quarter, supported by the higher production of especially diamonds and nickel. The production volumes of coal, platinum-group metals and building materials increased at a more moderate pace despite further steps to enhance operational efficiencies, while the production of gold, manganese ore and other metallic minerals contracted over the period.

| Quarterly Bulletin March 2016 |

|

On an annual basis, growth in the real output of the mining sector turned around from -1,6 per cent in 2014 to 3,0 per cent in 2015, adding 0,2 percentage points to growth in aggregate GDP. Mining production in 2015 benefited mainly from the normalisation in platinum production following improved productivity and cost-containment measures introduced at a number of platinum mines after the protracted labour strike in the industry in 2014. In addition, in some of the other domestic mining subsectors work disruptions as a result of wage disputes were less prevalent in 2015. Despite this improved performance, the industry continued to be adversely affected by infrastructural constraints, policy uncertainty, ongoing labour tension, declining commodity prices, rising operational costs, and a global oversupply of certain mining products.

Owing mainly to the disappointing performance of the manufacturing sector, the real value added by the secondary sector switched from an annualised increase of 3,3 per cent in the third quarter of 2015 to a decline of 1,5 per cent in the fourth quarter. Activity in the electricity, gas and water as well as in the construction sectors strengthened over the period.

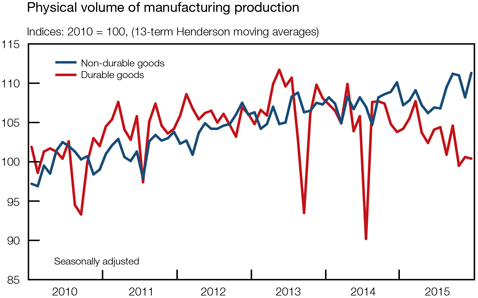

The quarter-to-quarter pickup in the real value added by the manufacturing sector in the third quarter of 2015 was short-lived as real manufacturing output contracted anew in the fourth quarter. Weighed down by lower production of primarily durable manufactured products, the real value added by the manufacturing sector contracted at an annualised rate of 2,6 per cent over the period – subtracting 0,3 percentage points from overall economic growth in the final quarter of 2015. Production volumes declined in the subsectors supplying basic iron and steel; non-ferrous metal products and machinery; electrical machinery; and motor vehicles, parts and accessories and other transport equipment. The weaker demand for processed metals affected by, among other factors, the slowdown in economic activity in China probably weighed on the production of these products.

By contrast, the production of non-durable goods rose over the period in line with increased consumer demand for these products. Increases were mainly evident in the production of petroleum and chemical products and of food and beverages. Consistent with the somewhat higher production levels in a number of subsectors, the utilisation of production capacity in the manufacturing sector increased from 80,1 per cent in the third quarter of 2015 to 80,5 per cent in the final quarter.

Annual growth in the real output of the manufacturing sector tapered off between 2010 and 2012, and thereafter remained virtually unchanged up to 2015; real output rose by only 0,1 per cent in 2015. Activity in the South African manufacturing sector continued to be negatively affected by weak domestic and global demand, the slowdown in activity in the agricultural sector, declining commodity prices affecting the mining sector, and electricity-supply constraints.

|

|

Quarterly Bulletin March 2016 |

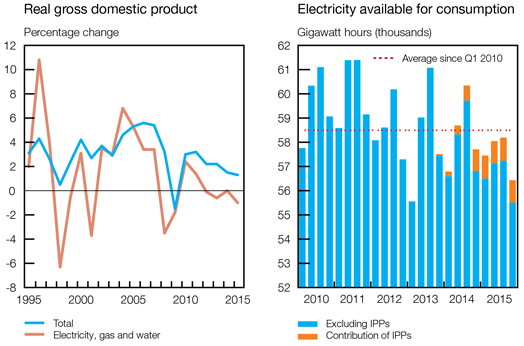

Following two successive quarters of negative growth, the real output of the electricity, gas and water sector advanced at a rate of 0,9 per cent in the fourth quarter of 2015. Scheduled maintenance done in preceding months at various plants together with additional electricity generated by independent power producers (IPPs) contributed to a more steady supply of electricity over the period. Reduced demand, mainly from energy-intensive sectors such as mining and metal processing, as well as the implementation of alternative energy sources by businesses and consumers probably also reduced electricity demand in the final quarter of 2015. Consistent with the overall slowdown in domestic economic activity, the real value added by the electricity, gas and water sector contracted by 1,0 per cent in 2015, the sharpest rate of decline since 2009.

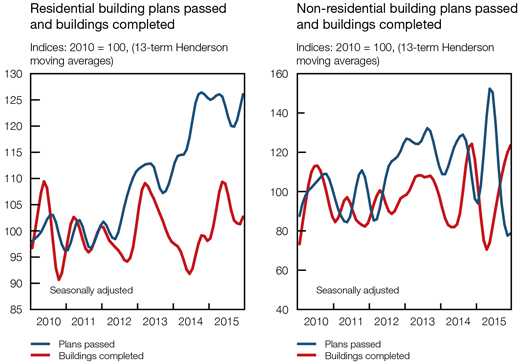

The real value added by the construction sector increased somewhat in the fourth quarter of 2015 as activity ticked up in essentially the non-residential building and civil construction segments. Residential building activity tapered off over the period.

| Quarterly Bulletin March 2016 |

|

In contrast to the usually more volatile goods-producing sectors, the services sector recorded relatively steady quarter-to-quarter growth throughout 2015. The pace of increase in the real value added by the tertiary sector, however, moderated somewhat in the final quarter of 2015, decelerating from 1,9 per cent in the third quarter of 2015 to 1,5 per cent in the fourth quarter. Activity in the finance, insurance, real-estate and business services; and the general government sectors advanced at a slower pace in the final quarter of 2015, while activity in the trade sector increased somewhat over the period. Real value added by the transport sector declined over the period.

Growth in the real value added by the commerce sector increased at a faster pace in the fourth quarter of 2015, accelerating from an annualised rate of 2,5 per cent in the third quarter of 2015 to 2,8 per cent in the fourth quarter. Retail trade activity remained firm notwithstanding the somewhat higher interest rate environment, the depreciation in the exchange value of the rand, and elevated debt levels of consumers. Retailers of non-durable and semi-durable products probably benefited from aggressive price promotions in an effort to boost trade volumes. General dealers; retailers of textile, clothing, footwear and leather goods; specialised food, beverage and tobacco stores; and retailers of pharmaceutical goods, cosmetics and toiletries, in particular, registered increased sales over the period. Consistent with the moderation in the domestic production of durable products, retail sales of household furniture, appliances and equipment decreased at a somewhat faster pace over the period. Activity in the wholesale trade subsector, however, declined in the fourth quarter of 2015.

In the fourth quarter of 2015, domestic sales of new vehicles increased marginally, probably on account of heightened expectations of price increases in the opening months of 2016 following the sustained depreciation in the exchange rate of the rand. By contrast, growth in the sales of used passenger vehicles decelerated in the fourth quarter of 2015. The real value added by the accommodation sector increased over the period.

Owing mainly to a decline in transport activity, the growth in real output of the transport, storage and communication sector receded from 0,1 per cent in the third quarter of 2015 to an annualised rate of -0,2 per cent in the fourth quarter. However, real value added by the sector benefited from uninterrupted growth in the communication subsector over the period.

Activity in the finance, insurance, real-estate and business services sector decelerated from an annualised rate of 2,8 per cent in the third quarter of 2015 to 1,9 per cent in the fourth quarter. This slower pace of increase was, in particular, evident in the real value added by the commercial banking sector coinciding with a marked deceleration in activity in the equity and derivative markets. Overall growth in the real value added by the sector, however, accelerated from 2,2 per cent in 2014 to 2,8 per cent in 2015.

Employment by general government increased at a slower pace in the fourth quarter of 2015, bringing about a deceleration in growth in real value added by general government from 1,2 per cent in the third quarter of 2015 to 1,0 per cent in the final quarter.

Real gross domestic expenditure

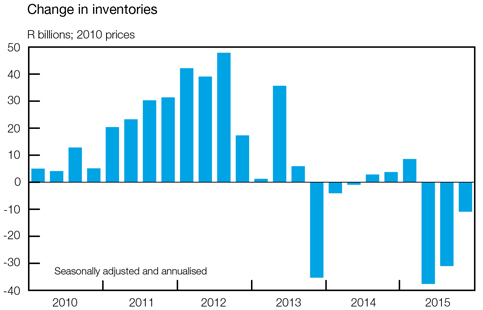

Notwithstanding the marginally slower growth in gross domestic production in the final quarter of 2015, growth in real gross domestic expenditure accelerated from an annualised rate of 1,4 per cent in the third quarter of 2015 to 4,3 per cent in the fourth quarter. Expenditure on all three components of final demand increased at a faster pace over the period alongside a moderation in the pace of destocking in real inventory holdings. For the year 2015 as a whole, real gross domestic expenditure nevertheless advanced by only 0,3 per cent – the slowest annual rate of increase since 2009.

|

|

Quarterly Bulletin March 2016 |

Real gross domestic expenditure

Percentage change at seasonally adjusted annualised rates

| 2014 | 2015 | |||||||||||||||||||||||

| Component | Year | 1st qr | 2nd qr | 3rd qr | 4th qr | Year | ||||||||||||||||||

| Final consumption expenditure |

||||||||||||||||||||||||

| Households |

1,4 | 2,6 | 1,2 | 0,9 | 1,6 | 1,6 | ||||||||||||||||||

| General government |

1,9 | -2,0 | 0,4 | 1,0 | 1,2 | 0,3 | ||||||||||||||||||

| Gross fixed capital formation |

-0,4 | 1,9 | 1,2 | 0,6 | 2,6 | 1,4 | ||||||||||||||||||

| Domestic final demand |

1,1 | 1,5 | 1,1 | 0,8 | 1,7 | 1,3 | ||||||||||||||||||

| Change in inventories (R billions)* |

0,4 | 8,6 | -37,6 | -31,0 | -10,9 | -17,7 | ||||||||||||||||||

| Gross domestic expenditure |

0,6 | 2,2 | -5,9 | 1,4 | 4,3 | 0,3 | ||||||||||||||||||

| * | At constant 2010 prices |

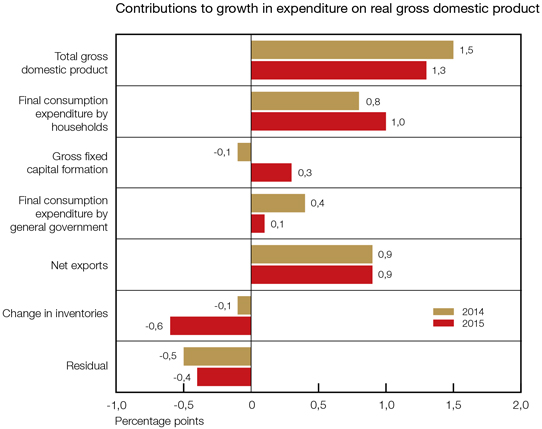

The change in real inventories made the largest contribution to the expansion in real GDP in the fourth quarter of 2015, adding 2,6 percentage points to overall economic growth. For the year 2015 as a whole, however, real net exports and private consumption expenditure by households were the main drivers of growth, contributing 0,9 and 1,0 percentage points respectively to

overall growth.

Contribution of expenditure components to growth in real gross domestic product

Percentage points

| 2014 | 2015 | |||||||||||||||||||||||

| Component | Year | 1st qr | 2nd qr | 3rd qr | 4th qr | Year | ||||||||||||||||||

| Final consumption expenditure |

||||||||||||||||||||||||

| Households |

0,8 | 1,6 | 0,7 | 0,5 | 1,0 | 1,0 | ||||||||||||||||||

| General government |

0,4 | -0,4 | 0,1 | 0,2 | 0,2 | 0,1 | ||||||||||||||||||

| Gross fixed capital formation |

-0,1 | 0,4 | 0,2 | 0,1 | 0,5 | 0,3 | ||||||||||||||||||

| Change in inventories |

-0,1 | 0,6 | -6,0 | 0,9 | 2,6 | -0,6 | ||||||||||||||||||

| Net exports |

0,9 | -0,8 | 4,7 | -0,7 | -3,6 | 0,9 | ||||||||||||||||||

| Residual |

-0,5 | -0,1 | -1,0 | -0,4 | -0,2 | -0,4 | ||||||||||||||||||

| Gross domestic product |

1,5 | 1,4 | -1,3 | 0,7 | 0,6 | 1,3 | ||||||||||||||||||

| Quarterly Bulletin March 2016 |

|

Private consumption expenditure by households

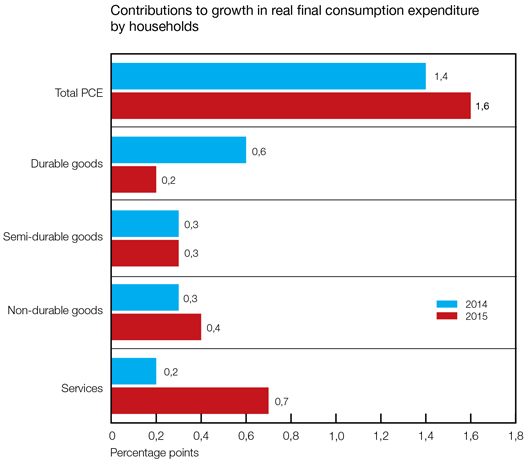

Real final consumption expenditure by households increased at an annualised rate of 1,6 per cent in the fourth quarter of 2015 – that is, at a somewhat faster pace than in the second and third quarters of the year. Spending on durable and non-durable goods switched from negative to positive growth, while real outlays on services increased at a slower pace over the period.

Real final consumption expenditure by households

Percentage change at seasonally adjusted annualised rates

| 2014 | 2015 | |||||||||||||||||||||||

| Category | Year | 1st qr | 2nd qr | 3rd qr | 4th qr | Year | ||||||||||||||||||

| Durable goods |

5,3 | 1,4 | 0,0 | -4,9 | 3,5 | 1,6 | ||||||||||||||||||

| Semi-durable goods |

3,2 | 3,7 | 3,2 | 4,3 | 5,1 | 3,5 | ||||||||||||||||||

| Non-durable goods |

0,8 | 3,6 | -0,7 | -0,2 | 1,3 | 1,1 | ||||||||||||||||||

| Services |

0,5 | 1,9 | 2,9 | 2,6 | 0,7 | 1,6 | ||||||||||||||||||

| Total |

1,4 | 2,6 | 1,2 | 0,9 | 1,6 | 1,6 | ||||||||||||||||||

Mainly underpinned by substantially higher real spending on services, growth in real consumption expenditure by households accelerated from 1,4 per cent in 2014 to 1,6 per cent in 2015. Relative to GDP, final consumption expenditure by households amounted to 60,9 per cent in 2015.

Subsequent to a decline of 4,9 per cent in the third quarter of 2015, real outlays on durable goods increased at an annualised rate of 3,5 per cent in the fourth quarter. Spending on especially passenger vehicles – accounting for roughly 50 per cent of real outlays on durable goods – increased in the final quarter of 2015, having declined in the third quarter of 2015.

|

|

Quarterly Bulletin March 2016 |

Expenditure on this category was probably boosted by pre-emptive buying in anticipation of possible price increases in the first quarter of 2016, a practice which consumers have become accustomed to in recent years. Spending on furniture and household appliances decreased somewhat while the pace of increase in real outlays on computers and related equipment slowed in the final quarter of 2015. On a calendar-year basis, the pace of increase in real spending on durable goods moderated notably from 5,3 per cent in 2014 to 1,6 per cent in 2015. The moderate rise in household indebtedness, amid a somewhat higher interest rate environment and an acceleration in durable goods price inflation following the sharp depreciation in the exchange value of the rand, is expected to hamper spending on this category in future.

Having advanced at a relatively firm pace throughout the first three quarters of 2015, growth in real spending on semi-durable goods accelerated even further to an annualised rate of 5,1 per cent in the fourth quarter. Apart from real outlays on recreational and entertainment goods, spending on all other categories of semi-durable goods increased over the period.

Subsequent to a contraction in the third quarter of 2015, real spending on non-durable goods bounced back in the fourth quarter of the year. Growth in spending on these largely non-discretionary products turned around from -0,2 per cent in the third quarter of 2015 to 1,3 per cent in the fourth quarter, contributing 0,5 percentage points to the increase in total private consumption expenditure over the period. Real outlays on household consumer goods, medical and pharmaceutical products and on petroleum products advanced further in the final quarter of 2015. Firm increases in expenditure on these products were partly countered by lower real spending on household fuel and power alongside a moderation in the pace of spending on food, beverages and tobacco, and recreational and entertainment goods. The slower pace of spending on food, beverages and tobacco probably reflected higher food price inflation following the severe drought conditions; higher prices for bread and cereals were partly countered by a deceleration in consumer meat price inflation over the period.

| Quarterly Bulletin March 2016 |

|

Growth in real expenditure by households on services slowed from an annualised rate of 2,6 per cent in the third quarter of 2015 to 0,7 per cent in the fourth quarter. Increased spending on transportation services was more than offset by lower outlays on miscellaneous services. For the year 2015 as a whole, real spending on services increased by 1,6 per cent, faster than the rate of increase of 0,5 per cent recorded in 2014.

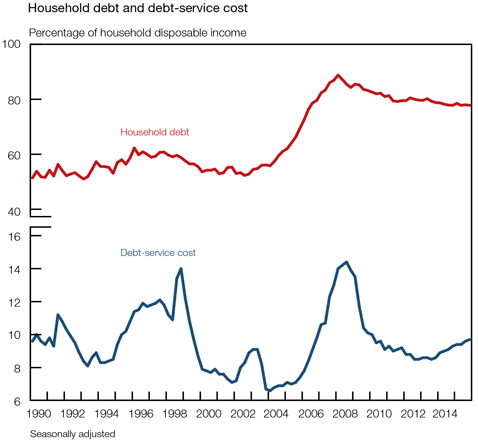

Growth in real disposable income of households accelerated marginally from an annualised rate of 0,8 per cent in the third quarter of 2015 to 1,1 per cent in the fourth quarter. The household sector continued to accumulate debt at a broadly similar pace in the third and fourth quarters of 2015, slower than the pace of increase in nominal disposable income. Consequently, the ratio of household debt to disposable income decreased from 78,0 per cent in the third quarter of 2015 to 77,8 per cent in the fourth quarter. By contrast, the debt-service cost of households rose from 9,6 per cent of disposable income to 9,7 per cent over the same period, largely reflecting the mild increase in lending rates in November 2015.

Final consumption expenditure by government

Quarter-to-quarter growth in real final consumption expenditure by general government remained subdued throughout 2015; government consumption expenditure increased at annualised rates of 1,0 per cent and 1,2 per cent in the third and fourth quarters of 2015 respectively. Consistent with government’s aim to continuously expand and enhance the quality of service delivery, real outlays in the fourth quarter of 2015 mainly reflected increased spending on health and education services. Growth in real government consumption expenditure, however, slowed from 1,9 per cent in 2014 to 0,3 per cent in 2015, largely reflecting a moderation in real expenditure on compensation of employees as government consolidated its spending as part of its effort to contain the budget deficit. Notwithstanding these developments, the ratio of final consumption expenditure by general government to GDP remained at roughly 20 per cent in both 2014 and 2015.

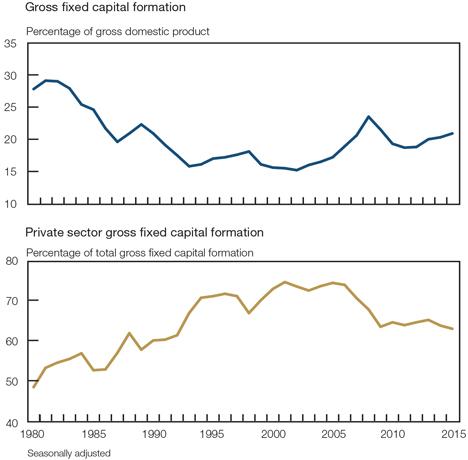

Fixed capital formation

Following relatively muted growth in the first three quarters of 2015, growth in real gross fixed capital formation accelerated to an annualised rate of 2,6 per cent in the fourth quarter of the

|

|

Quarterly Bulletin March 2016 |

year. Real capital spending by private business enterprises, which had declined in the third quarter of 2015, increased in the final quarter of 2015 along with an acceleration in growth in capital formation by general government and public corporations. Given the low business confidence levels, generally weak demand and ample capacity in most parts of the domestic economy, overall real gross fixed capital formation remained lustreless, registering annual growth rates of -0,4 per cent in 2014 and 1,4 per cent in 2015.

Real gross fixed capital formation

Percentage change at seasonally adjusted annualised rates

| 2014 | 2015 | |||||||||||||||||||||||

| Sector | Year | 1st qr | 2nd qr | 3rd qr | 4th qr | Year | ||||||||||||||||||

| Private business enterprises |

-3,4 | 1,7 | 0,4 | -0,6 | 1,7 | 0,4 | ||||||||||||||||||

| Public corporations |

1,6 | -0,1 | 0,2 | 0,5 | 3,3 | 0,8 | ||||||||||||||||||

| General government |

10,3 | 5,2 | 5,3 | 5,0 | 5,1 | 5,9 | ||||||||||||||||||

| Total |

-0,4 | 1,9 | 1,2 | 0,6 | 2,6 | 1,4 | ||||||||||||||||||

Having declined by 0,6 per cent in the third quarter of 2015, real gross fixed capital formation by private business enterprises increased at a rate of 1,7 per cent in the fourth quarter. Increased capital spending by the private electricity sector was underpinned by noticeable increases in capital outlays on projects being part of the Renewable Energy Independent Power Producer Procurement Programme. Under Bid Windows 1 and 2 of the programme, 41 independent power producers have to date successfully completed construction and are already in operation. Several projects under Bid Window 3 commenced construction during the fourth quarter of 2015. In most other sectors, real capital investment contracted in the fourth quarter of 2015, particularly in agriculture where capital spending on agricultural machinery contracted over the period following the severe drought experienced in many parts of the country.

| Quarterly Bulletin March 2016 |

|

Real fixed capital expenditure by public corporations increased from an annualised rate of 0,5 per cent in the third quarter of 2015 to 3,3 per cent in the fourth quarter, underpinned by increased spending on construction works and transport equipment by the water and transport subsectors in particular. Simultaneously, Transnet and the Passenger Rail Agency of South Africa (PRASA) raised their capital investment related to the acquisition of locomotives.

Real capital spending by general government increased at a fairly steady pace in excess of 5 per cent throughout 2015. Increased capital outlays by local government focused largely on improving the social and economic infrastructure as part of government’s priorities. Growth in real fixed capital expenditure by general government, however, moderated from 10,3 per cent in 2014 to 5,9 per cent in 2015.

Inventory investment

On an annualised basis, real inventories decreased by R31,0 billion in the third quarter of 2015 and by a further R10,9 billion in the fourth quarter. The slower pace of destocking added 2,6 percentage points to the growth in real GDP over the period. For the calendar year 2015 as a whole, real inventories declined by R17,7 billion compared with an increase of R0,4 billion in 2014.

Relatively weak demand coupled with a significant increase in the volume of crude oil imports following scheduled maintenance conducted at some oil refineries in the third quarter of 2015 contributed to a much slower pace of inventory de-accumulation in the manufacturing sector in the fourth quarter of 2015. However, industrial and commercial inventories as a percentage of non-agricultural GDP decreased from 13,5 per cent in the third quarter of 2015 to 13,1 per cent in the fourth quarter.

Factor income

Growth in total nominal factor income, measured over four quarters, accelerated from 4,1 per cent in the third quarter of 2015 to 4,4 per cent in the fourth quarter as the gross operating surpluses of business enterprises picked up at a marginally faster pace. Year-on-year growth in compensation of employees slowed over the same period. For 2015 as a whole, the rate of increase in total nominal factor income decelerated to 4,4 per cent from 7,2 per cent in 2014.

The year-on-year pace of increase in total compensation of employees decelerated from 7,9 per cent in the third quarter of 2015 to 7,8 per cent in the fourth quarter, reflecting a moderation in the remuneration of employees in almost all sectors of the economy with the exception of the general government sector. For 2015 as a whole, the compensation of employees increased by 7,8 per cent compared with a rate of increase of 7,6 per cent in 2014. In contrast, the

|

|

Quarterly Bulletin March 2016 |

Wage Settlement Survey conducted by Andrew Levy Employment Publications indicated that the average wage settlement rate for 2015 came to 7,7 per cent compared with an average settlement rate of 8,1 per cent in 2014.

Growth in the overall gross operating surplus, measured over a year, changed from 0,1 per cent in the third quarter to 0,3 per cent in the fourth quarter of 2015. Overall profitability in the economy continued to be affected by declining international commodity prices, rising production costs, sluggish demand, and subdued export proceeds over the period. The share of gross operating surplus in total factor income consequently declined from 46,0 per cent in the third quarter of 2015 to 45,8 per cent in the fourth quarter. For the year 2015 as a whole, the overall gross operating surplus rose by 0,7 per cent, significantly lower than the 6,8 per cent recorded in 2014 and far below the rate of inflation in the economy.

Gross saving

South Africa’s national saving ratio decreased for the third consecutive quarter in the fourth quarter of 2015. As a percentage of GDP gross saving weakened further from 14,6 per cent in the third quarter of 2015 to 14,2 per cent in the final quarter, reflecting marginally weaker saving by both households and corporate business enterprises alongside an increase in saving by general government. For the year as a whole, the national saving ratio expanded from 14,9 per cent in 2014 to 15,1 per cent in 2015, thereby lowering the portion of total gross capital formation to be financed through a net inflow of foreign capital from 26,7 per cent in 2014 to 22,4 per cent in 2015.

Gross saving by the corporate sector as a percentage of GDP edged lower from 14,1 per cent in the third quarter of 2015 to 13,6 per cent in the fourth quarter. Higher corporate tax payments more than offset the decline in dividend payments over the period. In line with the weaker saving reported by corporate business enterprises in 2015, the saving ratio declined from 14,9 per cent in 2014 to 14,0 per cent in 2015. This decline stemmed primarily from slower growth in gross operating surpluses of business enterprises in 2015 as overall profitability in the economy remained under pressure.

As a ratio of GDP, gross saving by general government rose marginally from 0,4 per cent in the third quarter of 2015 to 0,6 per cent in the fourth quarter. Government revenue was mainly boosted by a higher level of taxes paid by companies, while consumption expenditure by general government increased at a slower pace over the period. For the year as a whole, government’s saving ratio turned around from -0,2 per cent of GDP in 2014 to 1,0 per cent in 2015.

The gross saving ratio of the household sector weakened from 0,2 per cent in the first three quarters of 2015 to 0,1 per cent in the final quarter. A slight increase in household consumption expenditure together with a moderation in compensation earned by the household sector gave rise to the minor deterioration in the saving ratio in the fourth quarter of 2015.

Employment

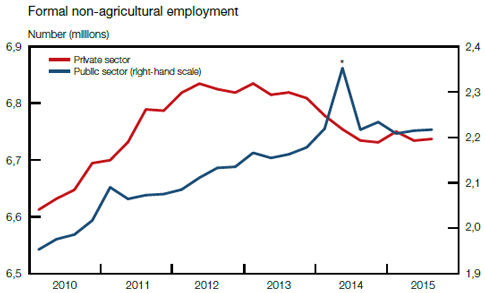

In an environment characterised by slowing domestic economic growth and heightened global uncertainty, total formal non-agricultural employment advanced only marginally in the third quarter of 2015. According to the Statistics South Africa (Stats SA) Quarterly Employment Statistics (QES) survey, employment increased by 0,2 per cent on a seasonally adjusted and annualised basis in the third quarter of 2015, with the total level of formal non-agricultural employment increasing by 5 100 job opportunities to an estimated 8,95 million.3 Employment levels in the public and private sectors rose by 0,4 per cent and 0,2 per cent respectively over the period.

| Quarterly Bulletin March 2016 |

|

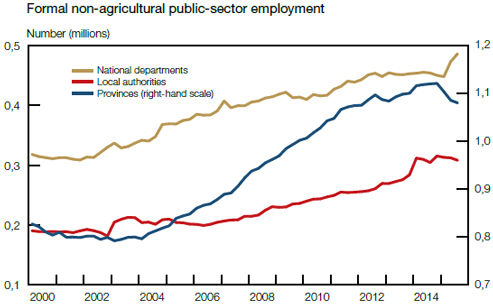

Employment growth in the public sector slowed somewhat from the second to the third quarter of 2015. National departments, and to a lesser extent other public-sector enterprises, continued to increase their staff complement in the third quarter of 2015. Similarly to the second quarter, the increase in employment by national departments resulted largely from the transfer of employees of technical vocational education and training colleges (former further education and training colleges) and community and education training colleges from provincial governments to the national Department of Higher Education and Training.4 These employment gains were partly countered by job-shedding at provincial level, at local government level, and in the public transport, storage and communication sector in the third quarter of 2015. Nevertheless, employment growth at provincial level has outpaced employment gains at national department and local authority level since 2005, as shown in the accompanying graph.

Private-sector employment growth remained sluggish. Following a decrease in the second quarter of 2015, a mere 2 900 private-sector job opportunities were created in the third quarter. Employment gains were registered in the private transport, storage and communication sector; the finance, insurance, real-estate and business services sector; the trade, catering and accommodation services sector; and the private community, social and personal services

|

|

Quarterly Bulletin March 2016 |

sector. Conversely, further job losses were recorded in the goods-producing sectors of the economy, with labour paring continuing in the mining, manufacturing and construction sectors in the third quarter of 2015.

Change in enterprise-surveyed formal non-agricultural employment by sector*

| Change over one quarter 3rd qr 2015 |

Change over four quarters to 3rd qr 2015 |

Cumulative job losses (-) gains (+) |

||||||||||||||||||||||

| Sector | Number | Per cent annualised |

Number | Per cent |

4th qr 2008 to 1st qr 2010 |

2nd qr 2010 to 3rd qr 2015 |

||||||||||||||||||

| Total mining |

-11 400 | -9,0 | -20 500 | -4,1 | -40 700 | -13 500 | ||||||||||||||||||

| Gold mining |

-300 | -1,1 | -4 000 | -3,3 | -9 600 | -45 000 | ||||||||||||||||||

| Other mining |

-11 100 | -11,4 | -16 500 | -4,4 | -31 100 | 31 400 | ||||||||||||||||||

| Manufacturing |

-5 400 | -1,9 | -3 300 | -0,3 | -113 800 | -71 100 | ||||||||||||||||||

| Construction |

-4 700 | -3,8 | -19 700 | -4,0 | -54 500 | -19 800 | ||||||||||||||||||

| Trade, catering and accommodation services |

9 800 | 2,1 | 22 900 | 1,2 | -77 500 | 88 900 | ||||||||||||||||||

| Private transport, storage and communication services |

2 000 | 2,7 | -2 600 | -0,8 | 400 | -5 200 | ||||||||||||||||||

| Finance, insurance, real-estate and business services |

11 700 | 2,4 | 29 400 | 1,5 | -190 900 | 119 900 | ||||||||||||||||||

| Community, social and personal services |

900 | 0,8 | -3 600 | -0,7 | 16 400 | 25 400 | ||||||||||||||||||

| Total private sector |

2 900 | 0,2 | 2 700 | 0,0 | -460 700 | 124 600 | ||||||||||||||||||

| National departments |

13 400 | 11,8 | 32 100 | 7,1 | -2 500 | 76 500 | ||||||||||||||||||

| Provinces |

-5 300 | -1,9 | -39 600 | -3,5 | 51 600 | 73 800 | ||||||||||||||||||

| Local governments |

-4 100 | -5,2 | 3 700 | 1,2 | 15 200 | 68 300 | ||||||||||||||||||

| Public transport, storage and communication services |

-3 500 | -10,4 | -100 | -0,1 | -4 900 | 22 700 | ||||||||||||||||||

| Other public-sector enterprises, including electricity and IEC** |

1 800 | 3,4 | 4 000 | 1,9 | -5 000 | 22 800 | ||||||||||||||||||

| Total public sector |

2 200 | 0,4 | 100 | 0,0 | 54 400 | 264 000 | ||||||||||||||||||

| Grand total |

5 100 | 0,2 | 2 800 | 0,0 | -406 400 | 388 600 | ||||||||||||||||||

| * | Seasonally adjusted. Components may not add to totals due to rounding |

| ** | IEC: Independent Electoral Commission |

Source: Statistics South Africa, Quarterly Employment Statistics (QES) survey

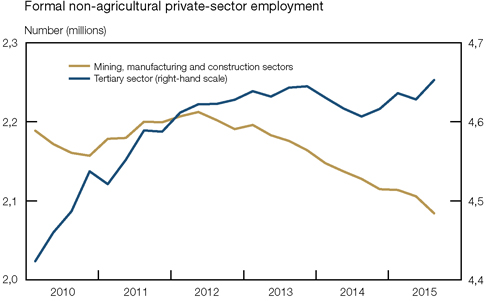

Formal private-sector employment growth has been fairly pedestrian following the 2008-09 economic recession, particularly in the goods-producing sectors of the economy. In fact, the accompanying graph shows that the mining, manufacturing and construction sectors have collectively shed 128 000 jobs between the second quarter of 2012 and the third quarter of 2015 as a hostile labour relations environment, electricity-supply constraints, policy uncertainty, low business confidence, and more recently weak global and domestic demand adversely affected investment and employment in these sectors of the economy. In addition, as output growth in the economy moderated gradually in recent years, employment growth in the tertiary sector slowed concomitantly, having initially grown fairly briskly following the 2008-09 recession. Furthermore, given the most severe drought in decades and the continued unwinding of the commodity supercycle, the private sector is not expected to create meaningful employment opportunities in the short run. The recent sharp depreciation in the exchange rate of the rand will probably intensify upward cost pressures in the economy, particularly in the goods-producing sectors.

| Quarterly Bulletin March 2016 |

|

.

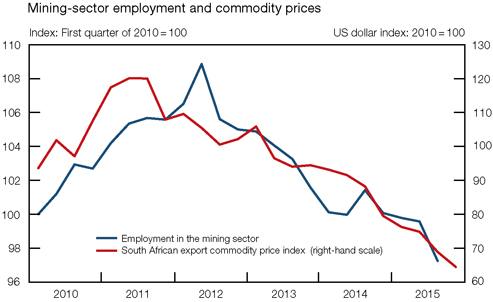

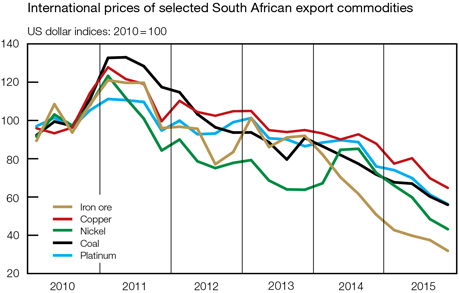

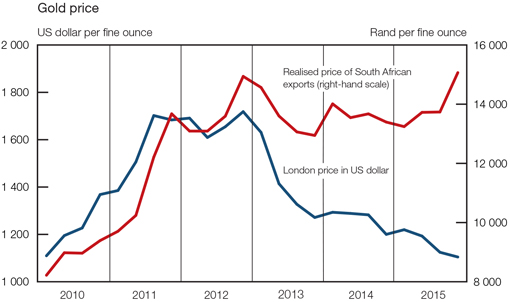

Employment in the domestic mining sector has decreased almost unabatedly from a recent peak in the second quarter of 2012 up to the third quarter of 2015. Throughout this period the domestic mining industry had to operate within an environment characterised by disruptive labour relations, often resulting in protracted labour strikes, as well as an escalation in operating costs. In addition, international commodity prices have declined notably since 2011, as depicted in the accompanying graph. The drop in commodity prices continued in 2015, owing to reduced demand from China and a global oversupply of many commodities. The pace of job-shedding in the mining sector accelerated in the third quarter of 2015, particularly in the non-gold mining sector which was affected by retrenchments in the platinum-mining sector as well as the closure and downscaling of some coal and chrome mines. Employment levels in the gold-mining sector decreased only marginally in the third quarter of 2015, having remained unchanged in the previous quarter. The recent sharp depreciation in the exchange rate of the rand has to some extent compensated for the decline in international commodity prices, at least in the short term, providing a much-needed boost to the profitability of South African mining companies.

Employment levels in the manufacturing sector decreased at a roughly similar pace in both the second and third quarters of 2015, representing a cumulative loss of almost 12 000 job opportunities. Furthermore, the Manufacturing Survey of Stellenbosch University’s Bureau for

|

|

Quarterly Bulletin March 2016 |

Economic Research (BER) indicated that business confidence among manufacturers remained unchanged at 34 index points in the fourth quarter of 2015; the index has remained below the neutral level of 50 since the third quarter of 2011. The pessimistic sentiment was pervasive throughout the manufacturing sector, exacerbated by a renewed deceleration in production volume growth for durable goods in particular. Although the recent sharp depreciation in the exchange rate of the rand could improve the profitability of manufacturing exporters, domestic demand for manufactured goods remained fairly weak, aggravated by the severe drought conditions and the commodity price-driven restructuring in the mining sector. Employment prospects in the manufacturing sector thus remain bleak, as suggested by the sharp drop in the employment sub-index of the Barclays Manufacturing Purchasing Managers’ Index (PMI), from an average of 47,2 index points in the third quarter of 2015 to an average of 43,7 index points in the fourth quarter.

Construction-sector employment contracted at an accelerated pace in the third quarter of 2015, weighed down by disappointing government infrastructure spending on large projects and sluggish private-sector capital investment by the mining sector in particular. In fact, the construction sector has shed a cumulative 27 400 job opportunities in the five quarters up to the third quarter of 2015. Despite improving somewhat in the fourth quarter of 2015, confidence levels in the building and construction sector remained low; the First National Bank (FNB)/BER Building Confidence Index rose by 4 index points to 48 in the fourth quarter of 2015, while the FNB/BER Civil Confidence Index increased by 3 index points to 42 over the same period. In addition, the real value of building plans passed decreased notably from the third to the fourth quarter of 2015.

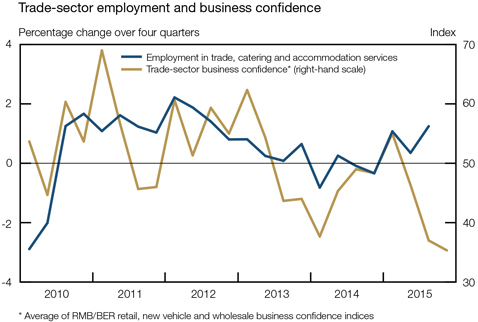

Contrary to developments in the primary and secondary sectors of the economy, employment levels increased in the tertiary sector of the economy in the third quarter of 2015. The finance, insurance, real-estate and business services sector created 11 700 employment opportunities in the third quarter, more than offsetting the losses recorded in the previous quarter. In addition, the trade, catering and accommodation services sector continued to record fairly meaningful employment gains for a third successive quarter, supported by continued growth in household consumption expenditure. However, results from the BER’s Retail Survey for the fourth quarter of 2015 suggest that underlying consumer demand could be deteriorating. Business confidence among retailers, wholesalers and new vehicle dealers remained depressed in the fourth quarter of 2015, owing to low sales volume growth, rising input costs, and generally tough trading conditions. In addition, the FNB/BER Consumer Confidence Index plummeted to -14 in the fourth quarter of 2015 from -5 in the third quarter, suggesting that consumer spending on especially durable goods could come under increased pressure in the first half of 2016.

| Quarterly Bulletin March 2016 |

|

According to the Quarterly Labour Force Survey (QLFS) conducted by Stats SA, the number of persons employed in South Africa increased by 190 000 from the third quarter of 2015 to the fourth quarter, raising the total level of employment to roughly 16,02 million.5 Employment numbers are usually boosted in the fourth quarter of each year by seasonal workers employed in the trade, catering and accommodation services sector in particular. Although QLFS outcomes for 2015 are not strictly comparable to those of 2014, total employment nevertheless increased by 698 000 in the year to the fourth quarter of 2015. Notable employment gains were recorded in all the main QLFS sub-categories, largely due to enhanced coverage following the introduction of the new master sample. Bearing this in mind, the formal non-agricultural sector and the informal sector added 269 000 and 236 000 employment opportunities respectively in the year to the fourth quarter of 2015.

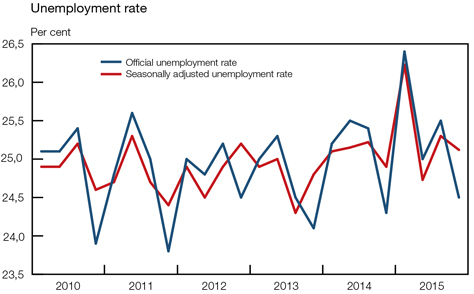

The number of unemployed persons decreased by 225 000 from the third to the fourth quarter of 2015, aided by temporary seasonal job creation, but increased by a notable 284 000 in the year to the fourth quarter of 2015, bringing the total number of unemployed South Africans to around 5,19 million. However, Stats SA cautioned that following the introduction of the new master sample, quarterly unemployment trends have become rather unstable and should be interpreted with circumspection. Encouragingly, the number of discouraged job seekers decreased by 124 000 in the year to the fourth quarter of 2015. As unemployment grew at a slightly faster pace than employment in the year to the fourth quarter of 2015, the official unemployment rate increased marginally to 24,5 per cent from 24,3 per cent a year earlier. The seasonally adjusted unemployment rate decreased from 25,3 per cent in the third quarter of 2015 to 25,1 per cent in the fourth quarter.6 The youth unemployment rate rose to 50,4 per cent in the fourth quarter of 2015, up from 48,8 per cent a year earlier.

Labour cost and productivity

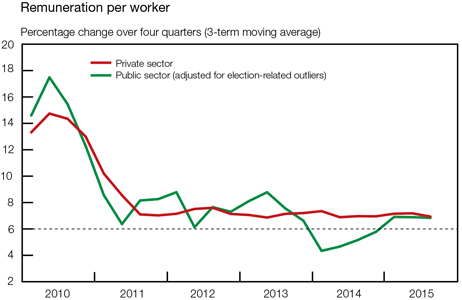

The year-on-year pace of increase in nominal remuneration per worker in the formal non-agricultural sector of the economy decelerated from 8,7 per cent in the second quarter of 2015 to 6,5 per cent in the third quarter, as both public- and private-sector remuneration growth moderated. Likewise, growth in the average real salaries and wages per worker in the formal non-agricultural sector decelerated from 5,1 per cent in the second quarter of 2015 to 3,1 per cent in the third quarter.

Public-sector remuneration growth moderated from 12,1 per cent7 in the second quarter of 2015 – exacerbated by the low base created in the second quarter of 2014 when a large number of low-earning temporary employees were appointed by the Independent Electoral Commission (IEC) to assist with the general elections – to 6,1 per cent in the third quarter. Remuneration growth slowed at national department and local government levels while quickening at provincial level in the third quarter of 2015.

|

|

Quarterly Bulletin March 2016 |

Similarly, the tempo of increase in average private-sector salaries and wages per worker decelerated from a year-on-year rate of 7,7 per cent in the second quarter of 2015 to 6,7 per cent in the third quarter. The highest wage increases per worker were recorded in the mining sector (9,8 per cent), followed by the finance, insurance, real-estate and business services sector (7,8 per cent); the private community, social and personal services sector (7,4 per cent); the manufacturing sector (7,3 per cent); the construction sector (5,1 per cent); the private transport, storage and communication services sector (4,9 per cent); and the trade, catering and accommodation services sector (3,6 per cent).

According to Andrew Levy Employment Publications, the average wage settlement rate in collective bargaining agreements moderated from 8,1 per cent in 2014 to 7,7 per cent in 2015. Encouragingly, the number of working days lost due to strike action fell notably from 11,8 million in 2014 (exacerbated by the prolonged platinum-mining strike in the first half of that year) to 640 000 in 2015, assisted by the avoidance of a public-sector strike in the year. The 2015 number was the lowest since 2000, when only 500 000 working days lost were recorded.

| Quarterly Bulletin March 2016 |

|

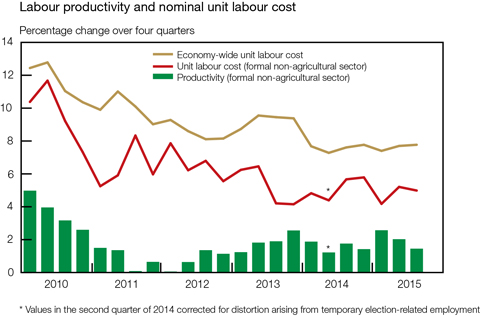

Owing to the moderation in year-on-year output growth and the slight acceleration in year-on-year employment growth in the third quarter of 2015, growth in labour productivity in the formal non-agricultural sector of the economy slowed from 3,5 per cent in the second quarter of 2015 to 1,5 per cent in the third quarter. Conversely, productivity growth in the manufacturing sector accelerated from -1,1 per cent in the second quarter of 2015 to 2,3 per cent in the third quarter, as output growth accelerated more than employment growth. With year-on-year remuneration growth decelerating at a slightly faster pace than year-on-year output growth, the pace of increase in nominal unit labour cost in the formal non-agricultural sector moderated marginally from 5,1 per cent in the second quarter of 2015 to 5,0 per cent in the third quarter – consistent with the inflation target range.

Prices

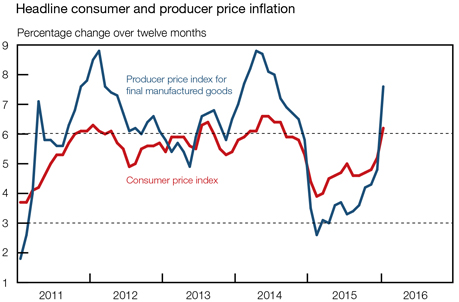

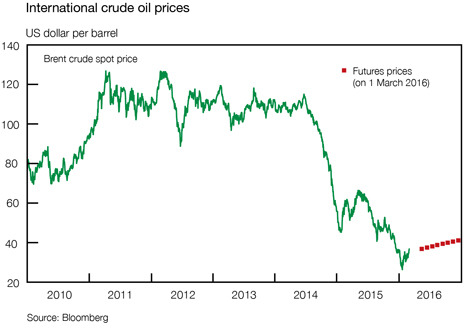

The sharp decline in international commodity prices in 2015 led to a subdued global inflationary environment and contributed meaningfully to a more benign domestic inflation outcome than initially anticipated. In addition, domestic demand and output growth slowed throughout the year, reducing inflationary pressures further. Consequently, headline consumer price inflation moderated from an annual average of 6,1 per cent in 2014 to 4,6 per cent in 2015 – the first moderation in annual average headline consumer price inflation in four years.

Despite the decline in crude oil and other international commodity prices, consumer price inflation accelerated gradually from a recent low of 3,9 per cent in February 2015 to 4,8 per cent in November, affected by the gradual depreciation in the exchange rate of the rand throughout the first eleven months of the year. However, inflationary pressures intensified towards the end of 2015 and in the opening months of 2016 as food price inflation quickened in response to the severe drought conditions and as the exchange rate of the rand depreciated sharply.8 As such, consumer price inflation quickened to 6,2 per cent in January 2016.

Consumer and producer price inflation

Annual average percentage change

| 2013 | 2014 | 2015 | Jan 2016* | |||||||||||||

| Headline consumer prices |

5,7 | 6,1 | 4,6 | 6,2 | ||||||||||||

| Consumer goods |

5,1 | 6,2 | 3,4 | 6,5 | ||||||||||||

| Consumer services |

6,3 | 6,0 | 5,8 | 6,0 | ||||||||||||

| Producer prices |

||||||||||||||||

| Final manufactured goods |

6,0 | 7,5 | 3,6 | 7,6 | ||||||||||||

| Intermediate manufactured goods |

7,9 | 8,2 | 0,8 | 3,8 | ||||||||||||

| Electricity and water |

10,6 | 9,9 | 11,1 | 11,6 | ||||||||||||

| Mining |

5,3 | 4,2 | -4,1 | 2,5 | ||||||||||||

| Agriculture, forestry and fishing |

2,6 | 5,3 | 4,7 | 23,6 | ||||||||||||

| * | Movement in prices from January 2015 to January 2016 |

Driven largely by falling international commodity prices, most measures of domestic producer price inflation moderated markedly in 2015. Producer price inflation for mining products decelerated substantially from an annual average of 4,2 per cent in 2014 to an annual average of -4,1 per cent in 2015. Likewise, producer price inflation for final manufactured goods more than halved from an annual average of 7,5 per cent in 2014 to 3,6 per cent in 2015, while producer price inflation for intermediate manufactured goods moderated from an annual average of 8,2 per cent in 2014 to a mere 0,8 per cent in 2015, as price inflation slowed across a broad range of product categories. When measured as an annual average, producer price inflation for agriculture, forestry and fishing products moderated from 5,3 per cent in 2014 to 4,7 per cent in 2015. However, producer price inflation for electricity and water – both administered prices – remained elevated throughout 2015, accelerating somewhat from an annual average of 9,9 per cent in 2014 to 11,1 per cent in 2015.

|

|

Quarterly Bulletin March 2016 |

Notwithstanding the slowing annual average rates of inflation, most measures of producer price inflation accelerated in recent months; producer price inflation for final manufactured goods and intermediate manufactured goods amounted to 7,6 per cent and 3,8 per cent respectively in January 2016. Driven largely by steep drought-induced agricultural price increases, producer price inflation for agriculture, forestry and fishing products accelerated markedly in the closing months of 2015, amounting to 23,6 per cent in January 2016.

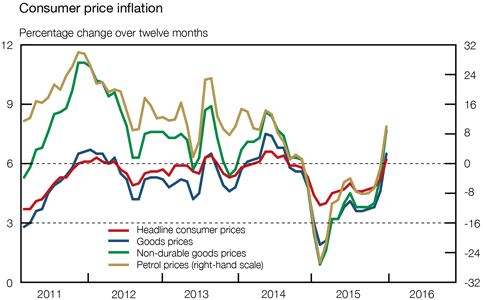

Throughout 2015, headline consumer price inflation outcomes were primarily shaped by movements in consumer goods price inflation, in particular that of non-durable goods. Consumer goods price inflation accelerated from a recent low of 3,6 per cent in September 2015 to 6,5 per cent in January 2016, as non-durable goods price inflation – representing 71 per cent of the total consumer goods price basket – quickened from 3,8 per cent to 7,7 per cent over the same period, in turn driven largely by movements in petrol price inflation and to a lesser extent by food price inflation. The acceleration in petrol price inflation occurred despite falling international crude oil prices and was driven by the depreciation in the exchange rate of the rand as well as the dissipation of favourable base effects in recent months.

| Quarterly Bulletin March 2016 |

|

Suppressed by relatively weak domestic demand conditions, durable and semi-durable goods price inflation has remained fairly subdued in recent months; semi-durable goods price inflation slowed from 4,3 per cent in June 2015 to 3,4 per cent in December, largely due to a slow pace of increase in the prices of clothing and footwear, while durable goods price inflation accelerated marginally from 2,2 per cent to 3,0 per cent over the same period, despite the depreciation in the exchange rate of the rand.

Consumer services price inflation remained steady around the upper limit of the inflation target range of 6,0 per cent for a prolonged period up to the middle of 2015. Thereafter, it slowed somewhat to 5,7 per cent in December 2015, as moderations in transport, restaurant and hotel services price inflation outweighed a quickening in housing and utility services price inflation.

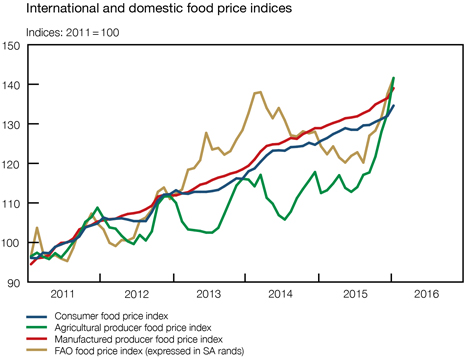

International food prices declined for a fourth consecutive year in 2015, with the international food price index of the United Nations Food and Agriculture Organization (FAO) averaging 19,1 per cent below its level in 2014 on account of abundant global food supplies and an appreciating US dollar. However, when expressed in rand terms, the year-on-year change in the FAO international food price index accelerated notably from July 2015 onwards, amounting to 19,1 per cent in January 2016 following the marked depreciation in the exchange rate of the rand in recent months. Abundant supplies and high inventory levels following, among others, the removal of export taxes in Argentina and continued good crop prospects, resulted in international cereals prices falling further in 2015 with the FAO international cereals price index being 15,4 per cent lower than in 2014. However, despite lower international cereal prices, the dramatically reduced 2015 domestic maize crop following the most severe drought in decades resulted in domestic maize and wheat prices soaring to all-time high levels and occasionally trading above import parity levels.

Domestic agricultural producer food price inflation accelerated notably from -3,0 per cent in January 2015 to 25,9 per cent a year later. The quickening in agricultural producer food price inflation resulted almost entirely from a marked acceleration in price inflation for cereals and other crops, from -17,5 per cent in January 2015 to 79,2 per cent in January 2016, as the severe drought conditions ravaged crops in South Africa’s primary maize- and wheat-producing areas. The rise in domestic maize prices was exacerbated by expectations that South Africa might have to import roughly 4 million tons of maize in the wake of the drought. Conversely, producer price inflation for live animals moderated notably from 11,5 per cent in May 2015 to 1,0 per cent in January 2016 due to the increased selling and slaughtering of herds in drought-stricken areas.

|

|

Quarterly Bulletin March 2016 |

Agricultural producer food prices

Percentage change over twelve months

| Weight | Nov 2015 |

Dec 2015 |

Jan 2016 |

|||||||||||||

| Products of crop and horticulture |

50,74 | 18,6 | 22,6 | 48,5 | ||||||||||||

| Cereals and other crops |

25,80 | 42,4 | 53,7 | 79,2 | ||||||||||||

| Fruit and vegetables |

24,93 | 1,4 | 0,6 | 23,7 | ||||||||||||

| Live animals and animal products |

49,26 | 2,3 | 1,5 | 2,3 | ||||||||||||

| Live animals |

35,34 | 2,5 | 1,0 | 1,0 | ||||||||||||

| Milk and eggs |

12,37 | -0,7 | -0,8 | -0,6 | ||||||||||||

| All items |

100,00 | 10,7 | 12,7 | 25,9 | ||||||||||||

Producer food price inflation at the manufactured level has not fully responded to the pickup in agricultural food price inflation, decelerating to 5,0 per cent in July and August 2015 before quickening to 7,8 per cent in January 2016. However, in recent months some pass-through from the notable acceleration in inflation for agricultural crops and cereals became visible in price inflation for grain mill, starch and animal feed products, as well as for bakery products. Nevertheless, similarly to the price movements for live animals, price inflation for manufactured producer meat products slowed markedly to a mere 0,8 per cent in January 2016.

Manufactured producer food prices

Percentage change over twelve months

| Weight | Nov 2015 |

Dec 2015 |

Jan 2016 |

|||||||||||||

| Meat, fish, fruit, vegetables, oils and fats |

37,34 | 3,9 | 3,7 | 5,4 | ||||||||||||

| Meat and meat products |

19,96 | 1,3 | 0,3 | 0,8 | ||||||||||||

| Fish and fish products |

7,42 | 6,7 | 7,4 | 8,4 | ||||||||||||

| Fruit and vegetables |

6,07 | 3,5 | 3,6 | 5,4 | ||||||||||||

| Oils and fats |

3,89 | 14,1 | 16,0 | 26,1 | ||||||||||||

| Dairy products |

8,97 | 0,1 | -0,7 | 0,2 | ||||||||||||

| Grain mill, starch and animal feed products |

12,46 | 10,3 | 10,8 | 15,6 | ||||||||||||

| Grain mill products |

5,24 | 12,8 | 12,0 | 20,1 | ||||||||||||

| Starch and animal feed products |

7,22 | 8,1 | 9,9 | 12,4 | ||||||||||||

| Other food products |

41,23 | 8,1 | 8,2 | 9,7 | ||||||||||||

| Bakery products |

30,24 | 8,2 | 7,8 | 9,6 | ||||||||||||

| Sugar |

5,71 | 9,4 | 12,5 | 11,3 | ||||||||||||

| Other food products |

5,28 | 6,1 | 5,9 | 7,3 | ||||||||||||

| All items |

100,00 | 5,9 | 5,9 | 7,8 | ||||||||||||

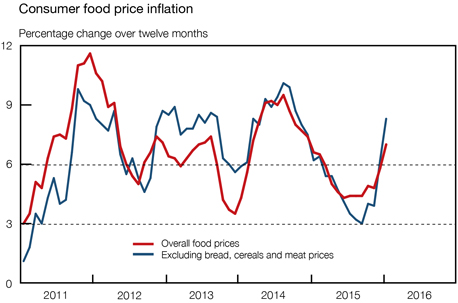

Consumer food price inflation responded to the acceleration in agricultural and manufactured producer food price inflation with a time lag, initially moderating to 4,3 per cent in June 2015 before accelerating to 7,0 per cent in January 2016. Nonetheless, the impact of the prolonged drought was evident in the quickening of price inflation for bread and cereals from 2,4 per cent in April 2015 to 8,4 per cent in January 2016 and a concomitant slowdown in meat price inflation from 6,4 per cent to 4,3 per cent over the same period, offsetting each other to some extent. The acceleration in consumer food price inflation has become more broad-based in recent months, as price inflation for especially vegetables quickened notably in January 2016 due the increased need for irrigation following the extreme temperatures experienced during the month.

| Quarterly Bulletin March 2016 |

|

Consumer food prices

Percentage change over twelve months

| Weight | Nov 2015 |

Dec 2015 |

Jan 2016 |

|||||||||||||

| Bread and cereals |

25,00 | 7,3 | 7,5 | 8,4 | ||||||||||||

| Meat |

32,11 | 4,2 | 4,1 | 4,3 | ||||||||||||

| Fish |

2,6 | 7,0 | 7,6 | 7,4 | ||||||||||||

| Milk, eggs and cheese |

12,25 | 2,0 | 1,9 | 2,5 | ||||||||||||

| Oils and fats |

3,87 | 11,3 | 14,1 | 17,4 | ||||||||||||

| Fruit |

1,62 | -5,9 | -2,4 | 3,8 | ||||||||||||

| Vegetables |

11,34 | 2,3 | 9,4 | 14,1 | ||||||||||||

| Sugar, sweets and desserts |

4,58 | 8,7 | 9,4 | 9,4 | ||||||||||||

| Other food products |

6,62 | 3,7 | 4,7 | 4,8 | ||||||||||||

| All items |

100,00 | 4,8 | 5,8 | 7,0 | ||||||||||||

The accompanying graph shows that when the prices of bread, cereals and meat – together accounting for 57 per cent of the consumer food price basket – are excluded, consumer food price inflation accelerated more briskly, from a low of 3,0 per cent in September 2015 to 8,3 per cent in January 2016.

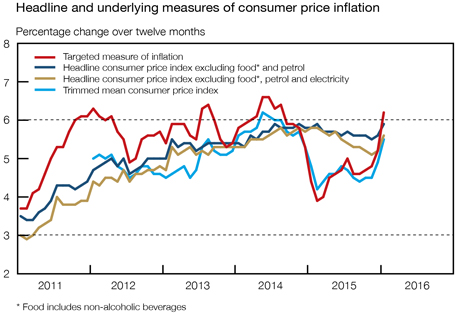

Within an environment of fairly limited pricing power in the domestic economy on account of weak consumer demand, most measures of underlying inflation have moderated throughout 2015 before accelerating in December 2015 and January 2016. Subtracting the impact of the more volatile food, non-alcoholic beverages and petrol prices from the calculation of targeted headline consumer price inflation, underlying inflation slowed from 5,9 per cent in February 2015 to 5,5 per cent in November before accelerating to 5,9 per cent in January 2016. Similarly, when further excluding the impact of electricity prices from the calculation, the resultant underlying measure of inflation moderated from 5,8 per cent to 5,1 per cent before quickening to 5,6 per cent over the same period. However, the sharp depreciation in the exchange rate of the rand in December 2015 and January 2016 is expected to add to underlying inflationary pressures in coming months, irrespective of weak domestic demand.

|

|

Quarterly Bulletin March 2016 |

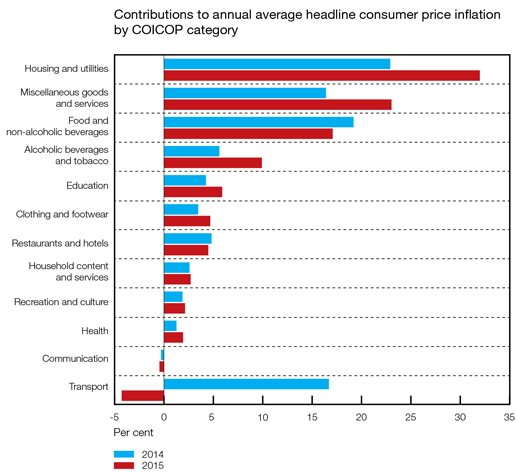

An analysis of price changes based on the classification of individual consumption by purpose (COICOP) categories suggests a slight slackening in inflationary pressures from 2014 to 2015. As such, annual consumer price inflation in 2015 exceeded the upper limit of the inflation target range in four of the twelve COICOP categories (as opposed to six categories in 2014), while four categories recorded price increases within the inflation target range (the same as in 2014) and four categories registered rates of change below the lower limit of the inflation target range (compared to two categories in 2014). The accompanying graph shows that the housing and utilities category remained the main contributor to annual consumer price inflation in 2015 (increasing its contribution notably), followed by the miscellaneous goods and services category, which moved up from fourth position in 2014.

| Quarterly Bulletin March 2016 |

|

Consistent with extremely benign petrol price inflation following the decline in international crude oil prices, coupled with relatively subdued motor vehicle price inflation throughout 2015, the transport category subtracted from annual consumer price inflation in 2015 after contributing meaningfully to consumer price inflation in 2014.

Driven largely by movements in petrol price inflation, administered price inflation accelerated from a recent low of -4,5 per cent in February 2015 to 8,8 per cent in January 2016. Even though domestic petrol prices fell somewhat in the three months to January 2016 – the inland price of unleaded 95-octane petrol decreased by a cumulative 24 cents per litre over the three-month period – the year-on-year rate of change in consumer petrol price inflation accelerated markedly from -8,0 per cent in October 2015 to 10,0 per cent in January 2016, largely due to unfavourable base effects. Furthermore, when excluding the effect of petrol prices from the calculation of administered prices, the rate of increase accelerated from 6,3 per cent in February 2015 to 8,5 per cent in December 2015 and January 2016, driven largely by accelerations in price inflation for electricity, water and assessment rates. When excluding electricity prices from the calculation of administered prices as well, the rate of increase quickened from 6,2 per cent in June 2015 to 7,4 per cent in December, before moderating to 7,1 per cent in January 2016. In early March 2016, the National Energy Regulator of South Africa (NERSA) awarded Eskom a 9,4 per cent increase for 2016/17.

Average inflation expectations, as measured in the Inflation Expectations Survey conducted by the BER in the fourth quarter 2015, shifted higher over the whole forecast period. The average headline inflation expectations of financial analysts, business representatives and trade unions increased marginally by 0,1 percentage points to 5,6 per cent and 6,2 per cent for 2015 and 2016 respectively, but increased by a more substantial 0,3 percentage points to 6,2 per cent for 2017. Analysts and business representatives revised their 2017 forecasts slightly upwards to 5,6 per cent (up by 0,2 percentage points) and 6,6 per cent (up by 0,1 percentage points) respectively. In contrast, trade union officials raised their forecast by a noticeable 0,4 percentage points to 6,3 per cent. Analysts expect inflation to quicken notably to 5,9 per cent in 2016 before moderating to 5,6 per cent in 2017. Business representatives and trade unions, in turn, expect inflation to accelerate in 2016 and 2017, from 6,4 per cent in 2016 to 6,6 per cent in 2017 in the case of business representatives, and from 6,2 per cent to 6,3 per cent over the same period in the case of trade union officials.

Headline consumer price inflation expectations

Per cent, as surveyed in the fourth quarter of 2015

| Average inflation expected for: | Financial analysts |

Business representatives |

Trade union representatives |

All surveyed participants |

||||||||||||

| 2015 |

4,8 | 6,2 | 5,9 | 5,6 | ||||||||||||

| 2016 |

5,9 | 6,4 | 6,2 | 6,2 | ||||||||||||

| 2017 |

5,6 | 6,6 | 6,3 | 6,2 | ||||||||||||

| The next five years |

5,5 | 6,5 | 6,2 | 6,1 | ||||||||||||

Source: Bureau for Economic Research, Stellenbosch University

After edging lower to 5,9 per cent in the third quarter of 2015, average five-year inflation expectations rebounded to 6,1 per cent in the fourth quarter. While business representatives kept their five-year inflation expectations unchanged at 6,5 per cent, those of analysts and trade union officials rose by 0,1 percentage points to 5,5 per cent and by 0,3 percentage points to 6,2 per cent, respectively. Average household inflation expectations for the next twelve months increased somewhat from 6,7 per cent in the third-quarter 2015 survey to 6,9 per cent in the fourth-quarter survey.

|

|

Quarterly Bulletin March 2016 |

Foreign trade and payments

International economic developments

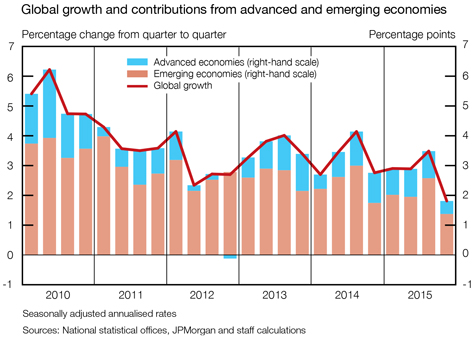

Global economic growth moderated notably from an annualised rate of 3,5 per cent in the third quarter of 2015 to 1,9 per cent in the fourth quarter. The pace of growth almost halved in emerging-market economies, driven primarily by weaker economic conditions in China, India and Russia. In advanced economies, economic activity slowed largely due to a sharp moderation in US economic growth and a contraction of economic activity in Japan.

The International Monetary Fund (IMF) lowered its 2016 global growth forecast by 0,2 percentage points to 3,4 per cent in its January 2016 World Economic Outlook Update. In particular, growth projections for emerging-market and developing economies were scaled down by 0,2 percentage points to 4,3 per cent. The recession in Brazil was estimated to be more protracted than previously expected, while growth prospects for major oil- and other commodity-exporting countries such as Nigeria, Russia, Saudi Arabia and South Africa also weakened.