Medium Term

Budget Policy Statement

2017

National Treasury

Republic of South Africa

25 October 2017

| ISBN: |

978-0-621-45853-4

|

| RP: |

RP312/2017

|

The Medium Term Budget Policy Statement is compiled using the latest available information from departmental and other sources. Some of this information is unaudited or subject to revision.

To obtain additional copies of this document, please contact:

Communications Directorate

National Treasury

Private Bag X115

Pretoria

0001

South Africa

Tel: +27 12 315 5944

Fax: +27 12 407 9055

The document is also available on the internet at: www.treasury.gov.za.

ii

Foreword

The most urgent task before our nation is to ignite inclusive, job-creating economic growth.

The National Development Plan (NDP) targets sustained economic growth of 5.4 per cent per year to dramatically reduce unemployment, poverty and inequality. This year, we expect the economy to grow by only 0.7 per cent. This is clearly insufficient to achieve our development aspirations, and places pressure on our fiscal framework.

Government remains committed to a path of fiscal consolidation. We will take steps to narrow the primary budget deficit and stabilise gross public debt, while protecting social spending and investments supporting economic expansion. Yet there are limits to what these measures can achieve.

The only sustainable solution for our development and the health of our public finances is to grow the economy inclusively.

The strengthening world economy offers an opportunity to implement reforms that will enable inclusive growth. Business and consumer confidence are exceptionally weak, and have been undermined by political uncertainty, policy uncertainty and poor governance in several state-owned companies. Government recognises the need for decisive action in these areas, and in July announced 14 measures to boost confidence and investment. The Medium Term Budget Policy Statement reports on the progress of those measures.

To ensure growth benefits all, radical economic transformation is required to change the structures and patterns of ownership, management and control of the economy, so that they include all South Africans. Government policy should support higher levels of value addition in our exports, the use of public procurement to promote localisation and broad-based black economic empowerment, reindustrialisation and address market concentration, which undermines competition and raises barriers to entry for small businesses and the historically disadvantaged.

The budget remains progressive and redistributive, and makes large contributions to transformation and inclusive growth. Core social expenditure is protected.

Spending priorities for the medium-term expenditure framework period ahead are guided by the NDP and the Mandate Paper. Yet pressures on the public finances are mounting. Debt is expanding and debt-service costs are the fastest-growing category of government expenditure. In this context, a series of risks must be managed. This will require difficult trade-offs and compromises.

Government will maintain the expenditure ceiling over the medium term. A presidential task team is examining possible asset disposals to ensure that there is no breach of the ceiling in the current year. Given the shortfall in revenue, new spending initiatives can only be accommodated through reprioritisation or parallel tax increases.

I would like to thank President Jacob Zuma, the Cabinet, my colleagues across government and Deputy Minister Sfiso Buthelezi for their inputs. I appreciate the hard and diligent work of the National Treasury staff in putting together this Medium Term Budget Policy Statement.

Tough times require tough decisions. We are committed to making them. Working together, we can grow the economy for the benefit of all.

Malusi Gigaba

Minister of Finance

iii

Contents

|

Chapter 1

|

Overview

|

1

|

|

The budget, transformation and inclusive growth

|

1

|

|

|

Economic outlook

|

2

|

|

|

Fiscal outlook

|

4

|

|

|

Spending priorities

|

6

|

|

|

Conclusion

|

8

|

|

|

Chapter 2

|

Economic outlook

|

9

|

|

Transformation, inclusive growth and competitiveness

|

9

|

|

|

Global outlook

|

11

|

|

|

Review of domestic economic performance

|

13

|

|

|

Macroeconomic outlook

|

15

|

|

|

Chapter 3

|

Fiscal policy

|

19

|

|

Erosion of the fiscal position

|

19

|

|

|

Revenue performance and outlook

|

21

|

|

|

Expenditure performance and outlook

|

25

|

|

|

Fiscal framework

|

27

|

|

|

Financing and debt management strategy

|

29

|

|

|

Chapter 4

|

Expenditure priorities

|

31

|

|

Introduction

|

31

|

|

|

Expenditure priorities and pressures

|

32

|

|

|

In-year adjustments to spending

|

36

|

|

|

Medium-term spending priorities

|

36

|

|

|

Division of revenue

|

41

|

|

|

Annexure A

|

Fiscal risk statement

|

49

|

|

Annexure B

|

Compensation data

|

59

|

|

Annexure C

|

Technical annexure

|

67

|

|

Annexure D

|

Glossary

|

75

|

iv

|

Tables

|

Figures

|

||||||

|

1.1

|

Macroeconomic projections

|

2

|

1.1

|

South Africa’s per capita income

|

2

|

||

|

1.2

|

Consolidated government fiscal framework

|

5

|

1.2

|

Main budget revenue and noninterest spending

|

4

|

||

|

1.3

|

Consolidated government expenditure

|

7

|

1.3

|

Growth in gross tax revenue and nominal GDP

|

5

|

||

|

2.1

|

Economic growth in selected countries

|

12

|

2.1

|

Business confidence and private investment

|

10

|

||

|

2.2

|

Sector growth trends

|

15

|

2.2

|

Comparative pricing of 1GB of data across Africa

|

14

|

||

|

2.3

|

Macroeconomic performance and projections

|

15

|

2.3

|

Growth in fixed investment in key sectors

|

16

|

||

|

2.4

|

Assumptions used in the economic forecast

|

18

|

3.1

|

Gross debt-to-GDP outlook without additional fiscal measures

|

20

|

||

|

3.1

|

Gross tax revenue

|

21

|

3.2

|

Medical tax credit per income group

|

24

|

||

|

3.2

|

Medium-term revenue framework

|

23

|

3.3

|

Medical tax credit as percentage of taxable income of taxpayers

|

24

|

||

|

3.3

|

Main budget expenditure ceiling

|

25

|

3.4

|

Interest payments as a share of main budget revenue

|

27

|

||

|

3.4

|

Revisions to the 2017/18 expenditure ceiling

|

25

|

4.1

|

Average nominal growth in spending, 2017/18 – 2020/21

|

32

|

||

|

3.5

|

Main budget framework

|

28

|

4.2

|

Growth in main budget expenditure and consumer inflation

|

34

|

||

|

3.6

|

Consolidated fiscal framework

|

29

|

|||||

|

3.7

|

Total national government debt

|

29

|

|||||

|

3.8

|

Gross borrowing requirement

|

30

|

|||||

|

4.1

|

Summary of expenditure on cost containment related items: national and provinces

|

35

|

|||||

|

4.2

|

Consolidated expenditure by function

|

37

|

|||||

|

4.3

|

Consolidated expenditure by economic classification

|

39

|

|||||

|

4.4

|

Division of revenue framework

|

41

|

|||||

|

4.5

|

Changes to division of revenue

|

42

|

|||||

|

4.6

|

Provincial equitable share

|

43

|

|||||

v

vi

1

Overview

|

█ The budget, transformation and inclusive growth

|

||

|

South Africa’s budget makes a substantial contribution to transformation and inclusive growth. It finances the construction of houses and schools, the operation of hospitals and clinics, the education of youth, care of the elderly and social grants for the most vulnerable. A large number of programmes encourage the growth of new businesses, empower small farmers, develop human capabilities, and provide incentives for job creation and economic transformation.

|

Budget makes a large contribution to transformation and inclusive growth

|

|

|

The budget is strongly aligned with constitutional imperatives and is highly progressive. Two-thirds of spending goes to functions responsible for realising constitutionally mandated social rights. Among developing countries, South Africa’s fiscal system is notable for its capacity to redistribute resources from the wealthy to the poor and working families. The allocation of funds to provinces and municipalities is governed by transparent rules that ensure redistribution of resources from cities to the countryside.

|

||

|

The budget establishes a solid foundation for national development. But government’s ability to sustain improvements in the quality of life of citizens depends on investment and economic growth.

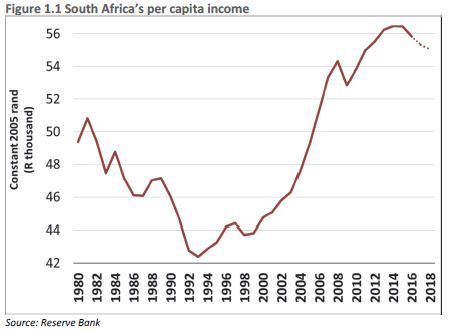

Over the last several years, South Africa’s per capita income has begun to stagnate. Unemployment is rising and, at 27.7 per cent, has reached the highest level recorded since 2003. Poverty, which had been in decline, has risen since 2011, and more than 30 million South Africans live on less than R1 000 per month.

To expand job creation, build an inclusive and transformed economy, and reduce inequality, South Africa needs a strong, sustained economic expansion. Growth is also the essential prerequisite for restoring the health of the nation’s public finances.

|

Government’s ability to improve citizens’ quality of life depends on investment and economic growth

|

|

1

|

2017 MEDIUM TERM BUDGET POLICY STATEMENT

|

|

||

|

█ Economic outlook

|

||

|

Economic growth revised down to 0.7 per cent in 2017, reaching 1.9 per cent by 2020

|

The 2017 Budget projected GDP growth of 1.3 per cent in 2017. That projection has been revised down to 0.7 per cent, following a recession in the fourth quarter of 2016 and the first quarter of this year. Economic growth is expected to recover slowly, reaching 1.9 per cent in 2020.

The weaker growth outlook reflects a continued deterioration in business and consumer confidence that has gathered pace since 2014. It also flows from perceptions of heightened risk as indicated in lower credit ratings, higher bond yields and sluggish investment. In 2016, gross fixed capital investment declined by 3.9 per cent, with large decreases in mining and manufacturing. Capital investment is expected to decline by 0.6 per cent in the current year.

Conditions in the global economy continue to improve, but the risks of financial turbulence remain high, and the longer-term outlook for growth and commodity prices is muted.

|

Table 1.1 Macroeconomic projections

|

Calendar year

|

2016

Actual |

2017

Estimate |

2018

|

2019

Forecast |

2020

|

|

Percentage change unless otherwise indicated

|

|||||

|

Household consumption

|

0.8

|

1.0

|

1.2

|

1.6

|

1.9

|

|

Gross fixed capital formation

|

-3.9

|

-0.6

|

0.5

|

3.0

|

3.5

|

|

Real GDP growth

|

0.3

|

0.7

|

1.1

|

1.5

|

1.9

|

|

GDP at current prices (R billion)

|

4 338.9

|

4 601.8

|

4 888.8

|

5 222.3

|

5 611.9

|

|

CPI inflation

|

6.3

|

5.4

|

5.2

|

5.5

|

5.5

|

|

Current account balance (% of GDP)

|

-3.3

|

-2.3

|

-2.6

|

-2.9

|

-3.1

|

Source: Reserve Bank and National Treasury

|

These factors are important in the context of South Africa’s external vulnerabilities. The country consumes more than it produces, and relies on foreign savings to finance the gap between low levels of domestic savings and the capital required for its investments. This relationship is expressed in the form of a persistent current account deficit, which is expected to widen over the medium term. Government debt held by non-residents has risen from 4.4 per cent of GDP in 2007 to 17.6 per cent of GDP in 2017. A sharply negative shift in global investor sentiment towards South Africa could result in large capital outflows, with highly destabilising consequences for the economy.

|

2

|

CHAPTER 1: OVERVIEW

|

|

Decisive action needed for a new growth trajectory

|

||

|

Last year’s Medium Term Budget Policy Statement warned that further deterioration of the economy could see South Africa entering a low-growth trap. In such a scenario, weak gross domestic product (GDP) growth produces less tax revenue. Aggressive fiscal consolidation to stabilise the growth of national debt and narrow the budget deficit might reduce perceived financial risks, but could also weaken demand, curbing investment and job creation. Yet taking no action could well result in credit-rating downgrades, rapid exchange-rate depreciation and capital flight.

|

South Africa confronts a low-growth trap

|

|

|

This cycle feeds on itself. Falling incomes and shrinking resources for public services raise social tensions, deepening political polarisation and creating doubts about future development. Declining confidence and economic uncertainty curb investment, entrenching low growth.

|

||

|

The National Treasury’s macroeconomic projections imply that per capita income will continue to stagnate in the years ahead. Unless decisive action is taken to chart a new course, the country could remain caught in a cycle of weak growth, mounting government debt, shrinking budgets and rising unemployment. Much depends on the policy choices made and the effectiveness of their implementation. Hard choices are required to return the public finances to a sustainable position. A failure to make such decisions, or to effectively implement them, will reinforce economic and fiscal deterioration.

|

Much depends on policy choices and their effective implementation

|

|

|

Government recognises these risks and opportunities, and is acting to break out of the low-growth trap. A new cycle of inclusive development requires clear intervention to stimulate economic activity, ensure effective regulation, improve the competitiveness of manufactured exports, promote localisation and reindustrialise the economy. This in turn requires renewed attention to strengthen the capacity of the state to develop the country’s economic potential.

|

||

|

In July, the Minister of Finance announced a set of 14 actions agreed to by Cabinet to revive investment. Progress has been made on several fronts:

|

Progress registered on 14 actions agreed by Cabinet to revive investment

|

|

●

|

A new board and CEO have been appointed to lead a turnaround at South African Airways (SAA).

|

||

|

●

|

The Budget Facility for Infrastructure, which is intended to overcome shortcomings in the planning and execution of large infrastructure projects, has begun considering proposals.

|

||

|

●

|

New procurement regulations have been implemented.

|

||

|

●

|

The Financial Sector Regulation Act has been signed into law.

|

|

Work is under way to license broadband spectrum, optimise government’s asset portfolio, reform the governance of state-owned companies and encourage private-sector participation in public investment programmes. A stronger package of measures to stimulate economic growth is being developed.

|

Work is under way to license broadband spectrum and optimise the state asset portfolio

|

|

|

Government continues to prioritise the expansion of network infrastructure to support the economy, alongside social infrastructure that serves community needs. The public sector will spend more than R300 billion each year on infrastructure, with about half of this funded directly from the budget.

|

3

|

2017 MEDIUM TERM BUDGET POLICY STATEMENT

|

|

Reforms needed to transform markets, improve national competitiveness and reconfigure urban landscape

|

To sustain economic growth, these measures need to be accompanied by microeconomic reforms that raise productivity and labour absorption. These include taking strong steps to transform markets, improve national competitiveness through innovation, break down structural barriers to new economic participants, promote manufacturing development and deconcentrate industries dominated by a few producers. Such reforms need to be complemented by plans to reconfigure the urban landscape, which remains dominated by inefficient and inequitable patterns of settlement.

|

|

|

█ Fiscal outlook

|

||

|

Strong tax revenues, which sustained fiscal consolidation efforts, are now under threat

|

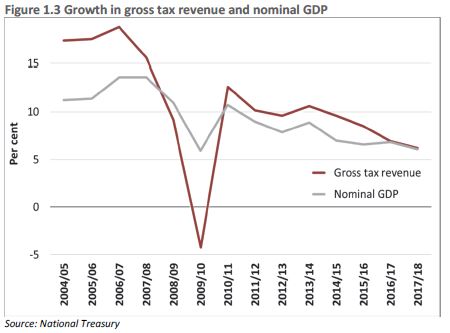

Over the past five years, government’s efforts to achieve a measured and balanced fiscal consolidation met with some success. While the stabilisation of debt proved elusive, expenditure remained well contained, and the primary balance – the gap between revenue and non-interest spending – narrowed. This progress was sustained by tax revenues that outperformed economic growth.

|

|

|

||

|

Strong revenue collection was partly the result of policy changes that raised the rate of taxation. Growth in key sectors of the economy bolstered revenues. Personal income taxes benefited from robust public- and private-sector wage settlements. The expanding middle class contributed to resilient household demand. The sustained depreciation of the exchange rate in an environment of contained inflation lifted profits in tradable sectors, adding to company tax receipts. Growth in capital investment continued to draw in imports, attracting value-added tax and customs duties.

|

||

|

Revenue shortfall of R50.8 billion projected in 2017/18

|

This period of revenue buoyancy appears to have run its course. The National Treasury projects a revenue shortfall of R50.8 billion in 2017/18. Lower revenue this year carries forward, and gross tax revenue is projected to fall short of the 2017 Budget estimates by R69.3 billion in 2018/19 and R89.4 billion in 2019/20. This reflects slowing economic growth, but may also suggest a profound shift in the relationship between economic growth and tax collection in the years ahead.

|

4

|

CHAPTER 1: OVERVIEW

|

|

||

|

Fiscal framework

|

||

|

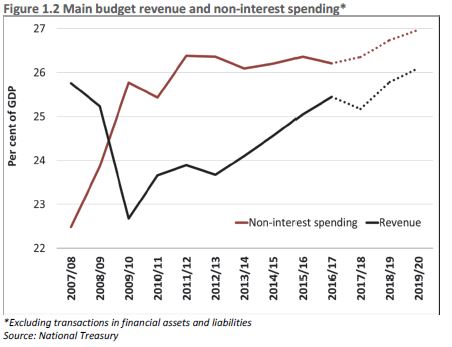

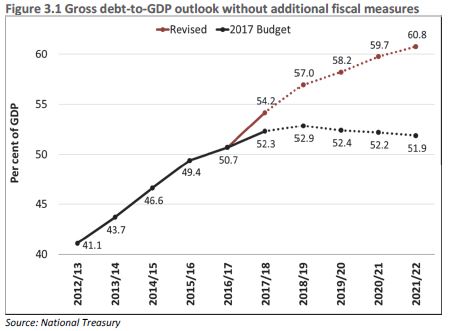

As a result of revenue shortfalls, the consolidated budget deficit for 2017/18 is expected to be 4.3 per cent of GDP, compared with a 2017 Budget estimate of 3.1 per cent. The main budget deficit, which determines government’s net borrowing requirement, will be 4.7 per cent of GDP this year.

In contrast to projections set out in the last budget, the revised projection is for the deficit to remain at this elevated level over the medium term. On this estimate, gross national debt is projected to continue rising, reaching over 60 per cent of GDP by 2022.

|

Consolidated budget deficit is 4.3 per cent of GDP in current year against projection of 3.1 per cent

|

Table 1.2 Consolidated government fiscal framework

|

2016/17

|

2017/18

|

2018/19

|

2019/20

|

2020/21

|

|

|

R billion/Percentage of GDP

|

Outcome

|

Revised

|

Medium-term estimates

|

||

|

Revenue

|

1 298.2

|

1 363.6

|

1 477.5

|

1 594.2

|

1 709.3

|

|

29.5%

|

29.2%

|

29.7%

|

30.0%

|

29.9%

|

|

|

Expenditure

|

1 445.7

|

1 566.6

|

1 670.6

|

1 802.3

|

1 935.1

|

|

32.8%

|

33.5%

|

33.6%

|

33.9%

|

33.9%

|

|

|

Budget balance

|

-147.5

|

-203.0

|

-193.1

|

-208.1

|

-225.8

|

|

-3.3%

|

-4.3%

|

-3.9%

|

-3.9%

|

-3.9%

|

|

|

Total gross loan debt

|

2 232.9

|

2 530.5

|

2 829.6

|

3 094.2

|

3 415.6

|

|

50.7%

|

54.2%

|

57.0%

|

58.2%

|

59.7%

|

|

Source: National Treasury

|

In this context, government faces difficult choices. To offset revenue shortfalls and reduce borrowing, the contingency reserve has been pared down to R16 billion over the next three years. This leaves government little room to manoeuvre if risks to the expenditure ceiling materialise. Beyond this, it is likely that some programmes will need to be eliminated, or their funding reduced.

South Africa’s stated policy aspirations and its social needs far exceed available public resources. Moreover, there is little space for tax increases in the current environment. Any new policy proposals, or expansion of existing programmes, should address only the most effective and necessary interventions.

|

5

|

2017 MEDIUM TERM BUDGET POLICY STATEMENT

|

|

Government remains committed to operating within the expenditure ceiling over the medium term. In the current year, however, the recapitalisation of SAA and the South African Post Office put the ceiling at risk of a R3.9 billion breach.

|

|

Risks to fiscus include rising debt-service costs and public-sector wage bill

|

In addition, there are several risks to the fiscus over the period ahead:

|

||

|

●

|

The economy and revenue could underperform projections. The GDP growth outlook may be improving, but the relationship between growth and revenue collection could deteriorate further.

|

||

|

●

|

Strains and imbalances within the public finances may become more pronounced. The public-sector wage bill has increasingly crowded out other spending and limited government’s ability to increase public employment.

|

||

|

●

|

Debt-service costs are set to absorb a rising share of revenue.

|

||

|

●

|

Several years of fiscal restraint have left funding gaps in both infrastructure and social services, reflected in the build-up of unpaid accounts and financial imbalances.

|

||

|

●

|

Continued financial deterioration of major state-owned companies is a clear and substantial danger to the public finances.

|

||

|

Changing course to mitigate risks

|

||

|

Over the next three years, government will adhere strictly to the spending limits it has set for itself. But more is clearly required. A combination of fiscal measures and economic interventions is needed to grow the economy, address immediate challenges facing the public finances and reduce long-term risks.

|

||

|

Presidential task team to develop proposals to stabilise debt over medium term

|

A team of Cabinet ministers reporting directly to the President has been established to develop proposals to stabilise the national debt over the medium term. These will include proposals to narrow the deficit, stimulate economic growth and build investor confidence. The team will work to ensure that the spending ceiling remains intact in the current year. A broader set of asset disposals is also under consideration, along with a restructuring of the portfolio of public assets to reduce risks posed by contingent liabilities. A new framework for the management of guarantees is being developed.

|

|

|

Additional measures to reduce expenditure, raise revenue and improve the impact of public resources on economic growth will be announced in the 2018 Budget.

|

||

|

█ Spending priorities

|

||

|

Mandate Paper intended to strengthen alignment of budget, medium-term strategic framework and NDP

|

In August 2017, Cabinet approved a Mandate Paper to guide the spending choices of national government. Its purpose is to strengthen alignment of the national budget, the medium-term strategic framework and the National Development Plan (NDP) during the remaining term of the current administration.

|

|

|

The paper observes that on current trends, South Africa is unlikely to achieve its NDP goals. It also notes that there will be no additional funds available to increase baseline expenditure over the 2018 Budget, and some programmes may have to be cut to meet unanticipated spending pressures. It proposes seven expenditure priorities for the MTEF period:

|

6

|

CHAPTER 1: OVERVIEW

|

|

●

|

Job creation and small business development

|

||

|

●

|

Youth development

|

||

|

●

|

Infrastructure expansion and maintenance

|

||

|

●

|

Land reform, smallholder farmer and agriculture development

|

||

|

●

|

Comprehensive social security, education and skills

|

||

|

●

|

An integrated plan to fight crime

|

||

|

●

|

Advancing the national interest in the Southern African Development Community, throughout Africa, and through participation in the BRICS (Brazil, Russia, India, China and South Africa) bloc and the Indian Ocean Rim Association.

|

|

Government spending priorities continue to align with the NDP, as elaborated in the medium-term strategic framework and the Mandate Paper for 2018.

|

Table 1.3 Consolidated government expenditure

|

2017/18

|

2018/19

|

2019/20

|

2020/21

|

Average

|

|

|

Revised

|

Medium-term estimates

|

annual

|

|||

|

growth

|

|||||

|

2017/18–

|

|||||

|

R billion

|

2020/21

|

||||

|

Learning and culture

|

317.8

|

340.7

|

367.3

|

395.7

|

7.6%

|

|

Health

|

189.6

|

204.5

|

220.0

|

235.5

|

7.5%

|

|

Social development

|

234.2

|

251.2

|

269.0

|

286.9

|

7.0%

|

|

Community development

|

193.5

|

210.1

|

226.5

|

243.1

|

7.9%

|

|

Economic development

|

190.9

|

202.2

|

217.7

|

229.9

|

6.4%

|

|

Peace and security

|

195.5

|

206.2

|

220.7

|

235.5

|

6.4%

|

|

General public services

|

62.3

|

64.7

|

67.5

|

71.6

|

4.8%

|

|

Payments for financial assets

|

19.5

|

5.0

|

5.2

|

5.5

|

–

|

|

Total expenditure by function

|

1 403.3

|

1 484.5

|

1 594.0

|

1 703.8

|

6.7%

|

|

Debt-service costs

|

163.3

|

183.1

|

203.3

|

223.4

|

11.0%

|

|

Contingency reserve

|

–

|

3.0

|

5.0

|

8.0

|

–

|

|

Total expenditure

|

1 566.6

|

1 670.6

|

1 802.3

|

1 935.1

|

7.3%

|

Source: National Treasury

|

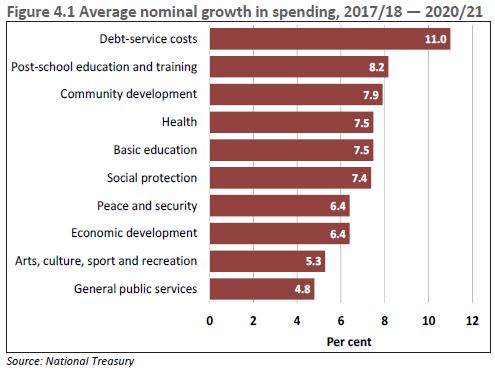

Over the medium term, expenditure will grow by an annual average of 7.3 per cent, from R1.6 trillion in 2017/18 to R1.9 trillion in 2020/21. The fastest-growing category of expenditure is debt-service costs, which reach nearly 15 per cent of revenue in the outer year and increasingly crowd out spending on services. The fastest-growing elements of spending are Learning and Culture (which includes post-school education and training), Health and Community Development, with growth rates of 7.6 per cent, 7.5 per cent and 7.9 per cent respectively.

|

||

|

Despite a highly constrained fiscal environment, government is protecting expenditure that delivers services to low-income households. However, additional resources to support spending priorities are severely limited.

|

Spending that aims to deliver services to low-income households is protected

|

|

|

As in recent years, additional allocations will be funded mainly through reprioritisation of existing budget baselines. Structural increases in expenditure to accommodate new policy initiatives, and resulting adjustments to the spending ceiling, will need to be matched by parallel tax increases.

|

7

|

2017 MEDIUM TERM BUDGET POLICY STATEMENT

|

|

█ Conclusion

|

||

|

Improved confidence and microeconomic reforms will return the economy to a higher growth rate over time

|

Stronger economic growth is required to return the public finances to a sustainable position, and put South Africa back on a path of rising employment and increasing prosperity. Government is committed to transformation and confidence-boosting measures to promote investment. Combined with microeconomic reforms, higher levels of business and consumer confidence will return the economy to a higher growth path over time.

|

8

2

Economic outlook

|

In brief

|

|

|

●

|

South Africa’s projected GDP growth for 2017, forecast at 1.3 per cent at the time of the 2017 Budget, has been revised down to 0.7 per cent. Over the medium term, GDP growth is expected to increase slowly, reaching 1.9 per cent in 2020.

|

|

●

|

Despite substantial risks, the global economic outlook is improving, with growth of 3.7 per cent forecast in 2018. Higher global growth can benefit South Africa’s medium- to long-term growth prospects if the country can boost investment and export competitiveness.

|

|

●

|

Concerns about policy and political uncertainty, along with weak domestic demand, weigh heavily on business and consumer confidence, deterring investment and job creation.

|

|

●

|

Government’s economic policy, guided by the objectives of the National Development Plan, centres on inclusive growth, transformation and competitiveness. Progress has been registered on the 14 confidence-boosting measures announced earlier this year. A series of microeconomic reforms would provide impetus to confidence and investment.

|

|

█ Transformation, inclusive growth and competitiveness

|

||

|

The South African economy grew by an annual average of 1.9 per cent between 2010 and 2016, well below the target of 5.4 per cent envisaged in the National Development Plan (NDP). Per capita GDP has declined for two consecutive years, severely constraining efforts to transform the economy, and threatening the sustainability of the public finances.

|

Slow economic growth severely constrains efforts to transform the economy

|

|

|

Persistently weak economic growth reinforces the country’s legacy of socioeconomic exclusion. Today, 30.4 million South Africans are living in poverty. Unemployment is 27.7 per cent – the highest level since September 2003. The share of total income going to the top 10 per cent of income earners is between 60 and 65 per cent. Wealth inequality is even more pronounced. Low levels of economic opportunity for a large proportion of the population undermine growth potential and the realisation of the constitutional vision of a more equal society.

|

||

9

|

2017 MEDIUM TERM BUDGET POLICY STATEMENT

|

|

Inclusive growth, transformation and competitiveness form a virtuous circle

|

Government is focused on inclusive growth, transformation and competitiveness. These three policy objectives form a virtuous circle. Inclusive growth reduces poverty and inequality, and provides the resources to support critical social spending. Broad-based economic transformation opens up the economy to those previously marginalised, generating new businesses and wealth. A competitive economy sells goods and services to the rest of the world and attracts investment to support its own development.

|

|

|

Guided by the NDP and the nine-point plan announced in February 2015, government aims to break down structural impediments to new economic activity, deconcentrate industries dominated by few participants, accelerate the inclusion of millions of black South Africans into jobs and businesses, and return to a path of rising incomes for all.

|

||

|

The central challenge for economic policy remains effective implementation.

|

||

|

Rebuilding confidence

|

||

|

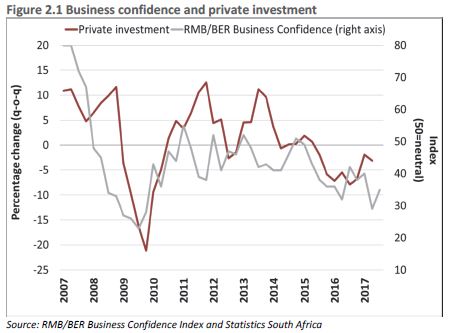

Weak business and consumer confidence reduce investment, job creation and household spending

|

Business and consumer confidence have been exceptionally weak in recent years, with direct consequences for investment, job creation and household spending. At present, concerns about policy and political uncertainty, along with weak domestic demand, weigh heavily on business and consumer confidence.

|

|

|

||

|

Delays in finalising key regulatory processes, as well as a pattern of poor governance in several large state-owned companies, contribute to concerns about policy uncertainty. Addressing these concerns would bolster confidence, supporting higher levels of investment and growth.

|

||

|

Restoring South Africa’s potential growth rate, which has fallen below 2 per cent since 2014, requires additional policy measures. Rapid implementation of a range of microeconomic reforms, as outlined in the NDP, would boost confidence and provide support to the economy.

|

10

|

CHAPTER 2: ECONOMIC OUTLOOK

|

|

South Africa’s macroeconomic framework is underpinned by fiscal sustainability and credibility, inflation-targeting and a flexible exchange rate. This approach protects the public finances for generations to come, and shields businesses and households from a range of economic shocks.

|

|

Update on government’s short-term confidence-boosting measures

|

|

|

Restore the sustainability of fiscal policy:

|

|

|

−

|

The Budget Facility on Infrastructure run by the National Treasury and the Presidential Infrastructure Coordinating Commission received 59 project submissions with an aggregate funding requirement of R135 billion. Several projects have been recommended for detailed appraisal.

|

|

−

|

Negotiations on the next public-service wage agreement are under way.

|

|

Promote transformation and competitive outcomes by implementing sector reforms:

|

|

|

−

|

The Preferential Procurement Policy Framework Act Regulations took effect on 1 April 2017.

|

|

−

|

The Financial Sector Regulation Act was signed into law on 21 August 2017.

|

|

−

|

The Government Technical Advisory Centre has been commissioned to set up a fund to benefit small and medium enterprises, with a particular focus on start-ups.

|

|

Manage fiscal and economic risks associated with state-owned entities:

|

|

|

−

|

Government granted South African Airways R5.2 billion to address debt obligations. This allowed SAA to avoid default, roll over some debt and continue negotiations with lenders. A permanent chief executive officer has been appointed and the appointment of a chief restructuring officer is under way.

|

|

−

|

A private-sector participation framework and a template to determine and cost developmental mandates have been approved by Cabinet.

|

|

−

|

An energy task team resolved not to provide balance sheet support to Eskom. The Minister of Energy announced that Eskom will sign power-purchase agreements with independent power producers at a tariff not exceeding 77c/kWh.

|

|

Create policy certainty by finalising key legislative and policy processes:

|

|

|

−

|

The Council for Scientific and Industrial Research completed a study on spectrum availability and open access.

|

|

−

|

The Competition Commission launched a market inquiry to investigate data prices.

|

|

−

|

Draft legislation is being finalised to facilitate the licensing of Postbank.

|

|

−

|

Implementation of the revised Mining Charter has been postponed to December 2017.

|

|

−

|

Government is consulting stakeholders on the Regulation of Agricultural Land Holdings Bill.

|

|

█ Global outlook

|

||

|

The world economy continues to strengthen. According to the International Monetary Fund (IMF), global growth is projected to reach 3.6 per cent in 2017 and 3.7 per cent in 2018, up from 3.2 per cent in 2016.

|

World economy is strengthening, with projected growth of 3.7 per cent in 2018

|

|

|

The outlook largely reflects a recovery in demand and trade in Europe and Asia. World trade volumes are expected to increase by 4.2 per cent in 2017. Low interest rates in the United States, Europe and Japan remain supportive of growth. The euro area should benefit from strong domestic demand, and better-than-expected growth in Japan’s net exports will improve its performance in 2017. Brazil and Russia have returned to growth after lengthy recessions, supported by a strong export performance (Brazil), and stabilising oil prices and improved confidence (Russia).

|

||

11

|

2017 MEDIUM TERM BUDGET POLICY STATEMENT

|

|

These upward revisions in growth projections offset lower estimates for the US and the United Kingdom. The UK economy slowed more than anticipated in the first half of the year. The US growth forecast for 2017 has been trimmed from 2.3 per cent to 2.2 per cent, because an expected fiscal stimulus driven by tax cuts did not come about. US growth is projected to reach the pre-crisis average of 2.3 per cent in 2018.

|

||

|

Growth in sub-Saharan Africa projected to tick upwards in 2017, reaching 2.6 per cent.

|

Growth in sub-Saharan Africa has been depressed as a result of underperformance in the region’s two largest economies – Nigeria and South Africa. Economic growth in the region is projected to tick upwards, reaching 2.6 per cent in 2017 and 3.4 per cent in 2018, in response to improved oil production and agricultural output. The Angolan economy is expected to grow by 1.5 per cent in 2017. Growth outcomes for fuel-importers in the region are generally better. Kenya and Ethiopia are expected to grow at 5.0 and 8.5 per cent respectively in 2017 due to strong domestic demand and infrastructure investment.

|

Table 2.1 Economic growth in selected countries

|

Region / country

|

2000-2008

|

2010-2015

|

2016

|

2017

|

2018

|

|

Percentage

|

Pre-crisis

|

Post-crisis

|

Average GDP1

|

||

|

World

|

4.3

|

3.9

|

3.2

|

3.6

|

3.7

|

|

Advanced economies

|

2.4

|

1.9

|

1.7

|

2.2

|

2.0

|

|

US

|

2.3

|

2.2

|

1.5

|

2.2

|

2.3

|

|

Euro area

|

2.0

|

1.0

|

1.8

|

2.1

|

1.9

|

|

UK

|

2.5

|

2.0

|

1.8

|

1.7

|

1.5

|

|

Japan

|

1.2

|

1.5

|

1.0

|

1.5

|

0.7

|

|

Developing countries

|

6.5

|

5.5

|

4.3

|

4.6

|

4.9

|

|

Brazil

|

3.8

|

2.2

|

-3.6

|

0.7

|

1.5

|

|

Russia

|

7.0

|

2.2

|

-0.2

|

1.8

|

1.6

|

|

India

|

6.8

|

7.4

|

7.1

|

6.7

|

7.4

|

|

Chile

|

4.8

|

4.2

|

1.6

|

1.4

|

2.5

|

|

Mexico

|

2.6

|

3.2

|

2.3

|

2.1

|

1.9

|

|

Indonesia

|

5.3

|

5.7

|

5.0

|

5.2

|

5.3

|

|

China

|

10.4

|

8.3

|

6.7

|

6.8

|

6.5

|

|

Sub-Saharan Africa

|

5.9

|

5.0

|

1.4

|

2.6

|

3.4

|

|

South Africa2

|

4.2

|

2.3

|

0.3

|

0.7

|

1.1

|

| 1. |

IMF World Economic Outlook Update, October 2017

|

| 2. |

National Treasury Forecasts

|

|

Yet despite the cyclical upturn, there are considerable risks to the global outlook. These include high levels of debt, continued political and policy uncertainty in advanced economies, imbalances in the Chinese financial system and a more rapid tightening of global financial conditions.

|

||

|

Risks to global outlook include changes to US trade policy, Brexit and tightening global financial conditions

|

Possible changes to US trade policy and uncertainty about the terms of the UK’s exit from the European Union pose risks to global trade. Tighter global financial conditions could result from higher interest rates in advanced economies or developments that prompt global risk aversion, raising external financing risks and reducing capital flows to developing economies. Lower capital inflows could lead to currency depreciation, higher inflation and rising interest rates. A debt crisis in China’s banking sector would lower global growth significantly, particularly for countries that are reliant on trade with China.

|

12

|

CHAPTER 2: ECONOMIC OUTLOOK

|

|

The improved global outlook can strengthen South Africa’s medium- to long-term growth prospects, provided the country can boost export competiveness. South Africa’s post-crisis growth outcomes were marginally better than those of Brazil and Russia, but worse than Chile and Indonesia, which undertook a range of microeconomic reforms.

|

Improved world outlook can benefit South Africa, provided economy can boost investment and export performance

|

|

|

█ Review of domestic economic performance

|

||

|

The South African economy grew by an annualised 2.5 per cent in the second quarter of 2017, following a recession that began in the fourth quarter of 2016. The stronger-than-expected rebound was underpinned by a return to growth in the services sector and robust agricultural output.

|

||

|

Overview of major economic sectors

|

||

|

Agriculture

|

||

|

Real value added in the agriculture, forestry and fishing sector grew by 21.2 per cent in the first half of 2017 compared with the same period in 2016. Good rains in the summer rainfall region led to a recovery following a severe drought, which caused agriculture to contract in 2015 and 2016. Maize production is expected to reach 16.7 million tons in 2017 – a 115 per cent increase from the 2016 crop of 7.8 million tons. Soybean production is expected to increase by 77 per cent. Wheat production, however, is expected to decline by 10 per cent in 2017 due to continued drought in the Western Cape. An ongoing outbreak of avian flu in June 2017 may lead to higher poultry prices. Growth in the sector is expected to be sustained throughout 2017.

|

Strong rebound in agriculture following good season in summer rainfall regions

|

|

|

Mining

|

||

|

Mining value added expanded by 4.3 per cent in the first half of 2017 compared with the same period in 2016. The sector is recovering from the contraction of 2016, supported by higher commodity prices and growth in iron ore, manganese and copper. Mineral sales increased by 6.8 per cent in the first half of 2017 compared with the same period last year, driven largely by coal and iron ore. Gold sales fell by 16.2 per cent over the same period.

|

Mining recovering from low of 2016, but policy uncertainty limits growth

|

|

|

Declining fixed investment in mining undermines sustainable growth. Elevated operating costs and uncertainty related to the Mining Charter and the Mineral and Petroleum Resources Development Amendment Bill continue to constrain growth. South Africa is currently ranked 13th in Africa on the mining Investment Attractiveness Index. The mining outlook remains subdued due to continued domestic policy uncertainty and rising production costs.

|

||

|

Manufacturing

|

||

|

Real value added in manufacturing declined by 1.5 per cent and production contracted by 1.8 per cent in the first half of 2017 compared to the same period last year. Production in petrochemicals and wood and paper fell by 6.1 per cent and 2.9 per cent respectively. Capacity utilisation in manufacturing moderated slightly from 81.5 per cent in the first quarter of 2017 to 81.3 per cent in the second. Fixed-capital stock in manufacturing has declined every year since 2009, indicating a gradual erosion of capacity.

|

Manufacturing remains subdued and fixed-capital stock continues to decline

|

13

|

2017 MEDIUM TERM BUDGET POLICY STATEMENT

|

|

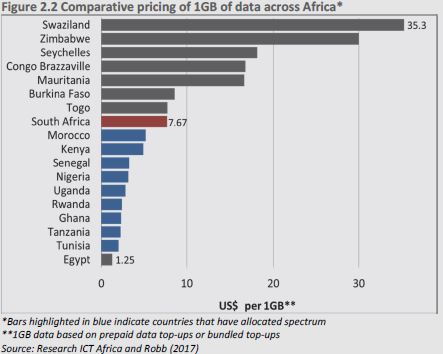

Realising the benefits of a well-designed telecommunications spectrum auction

|

|

The delay in allocating telecommunications spectrum constrains growth across the economy. Lack of radio frequency limits the ability of businesses to deploy new technologies and contributes to the high cost of broadband. A well-designed spectrum auction can promote transformation and improve competition as new participants enter the market. Universal service conditions can improve access for low-income households. And a competitive auction can sharply reduce data costs. The bulk of additional spectrum is ready to be allocated immediately, without requiring the migration of existing spectrum users to digital television.

|

|

|

Finance

|

||

|

Bank profitability remains resilient despite declining growth in interest income

|

Financial and business services grew by 1 per cent in the first half of 2017 compared with the same period in 2016. Lacklustre growth reflects high levels of household debt and slowing income growth, which affects banks and insurance companies. Bank profitability remains relatively resilient despite declining growth in interest income, which averaged 3.8 per cent in the first half of 2017 compared with 14.8 per cent a year earlier. Tier 1 capital adequacy, denoting high-quality reserves, rose from 12.5 per cent to 13.5 per cent in the year to July 2017. Asset quality is strong, with impaired advances as a share of outstanding loans at 2.9 per cent.

|

|

|

Employment

|

||

|

Formal employment declined by 0.2 per cent in first half of 2017, and about 6.2 million people are searching for work

|

Formal non-agricultural employment declined by 0.2 per cent in the first half of 2017 compared to the same period last year. Employment in community services fell by 41 041 during the first half of the year. Financial and business services lost 7 681 jobs over the same period, mostly in banking and insurance. Employment prospects in manufacturing remain constrained. Similarly, employment growth in the trade sector is likely to remain under pressure given low consumer confidence and weak credit growth. Mining recovered some jobs in the first half of 2017, expanding employment by 1.6 per cent. The ability of the economy to absorb new workers peaked in 2008 and has not recovered. An estimated 6.2 million South Africans are actively looking for work.

|

14

|

CHAPTER 2: ECONOMIC OUTLOOK

|

Table 2.2 Sector growth trends

|

Percentage

|

2012

|

2013

|

2014

|

2015

|

2016

|

20171

|

|

Agriculture, forestry and fishing

|

1.8

|

4.5

|

6.9

|

-6.1

|

-7.8

|

21.2

|

|

Mining and quarrying

|

-2.9

|

4.0

|

-1.4

|

3.9

|

-4.7

|

4.3

|

|

Manufacturing

|

2.1

|

1.0

|

0.2

|

-0.2

|

0.7

|

-1.5

|

|

Electricity and water

|

-0.4

|

-0.6

|

-1.1

|

-1.5

|

-3.5

|

-0.5

|

|

Construction

|

2.6

|

4.6

|

3.6

|

1.7

|

0.7

|

0.3

|

|

Wholesale and retail trade

|

4.0

|

2.0

|

1.6

|

1.4

|

1.2

|

-1.1

|

|

Transport and communication

|

2.4

|

2.9

|

3.2

|

1.1

|

0.4

|

1.3

|

|

Finance, real estate and business services

|

3.0

|

2.6

|

2.2

|

2.8

|

1.9

|

1.0

|

|

Personal services

|

2.1

|

2.6

|

2.0

|

1.1

|

1.2

|

0.8

|

|

General government

|

3.0

|

3.2

|

2.9

|

0.8

|

1.4

|

0.4

|

|

GDP

|

2.2

|

2.5

|

1.7

|

1.3

|

0.3

|

1.1

|

1. The first 6 months of 2017

Source: Statistics South Africa

|

█ Macroeconomic outlook

|

||

|

South Africa’s projected GDP growth for 2017, forecast at 1.3 per cent at the time of the 2017 Budget, has been revised down to 0.7 per cent. GDP growth is expected to increase slowly, reaching 1.9 per cent in 2020.

|

GDP growth projected to grow moderately, reaching 1.9 per cent in 2020

|

|

|

Revisions to the forecast reflect a significant deterioration in business and consumer confidence over the past year. Other contributing factors include weaker-than-anticipated growth in the fourth quarter of 2016, a large contraction in the finance sector in the first quarter of 2017 and a higher risk premium, reflected in higher bond yields. The impact of domestic factors on economic growth has been partially offset by improved global growth and commodity prices.

|

Table 2.3 Macroeconomic performance and projections

|

Calendar year

|

2014

|

2015

|

2016

|

2017

|

2018

|

2019

|

2020

|

|

Percentage change

|

Actual | Estimate | Forecast | ||||

|

Household consumption

|

0.7

|

1.7

|

0.8

|

1.0

|

1.2

|

1.6

|

1.9

|

|

Government consumption

|

1.1

|

0.5

|

2.0

|

0.9

|

1.7

|

1.0

|

1.0

|

|

Gross fixed capital formation

|

1.7

|

2.3

|

-3.9

|

-0.6

|

0.5

|

3.0

|

3.5

|

|

Gross domestic expenditure

|

0.6

|

1.8

|

-0.8

|

1.2

|

1.1

|

1.5

|

2.0

|

|

Exports

|

3.2

|

3.9

|

-0.1

|

2.5

|

3.2

|

3.4

|

3.5

|

|

Imports

|

-0.5

|

5.4

|

-3.7

|

4.0

|

3.1

|

3.5

|

3.8

|

|

Real GDP growth

|

1.7

|

1.3

|

0.3

|

0.7

|

1.1

|

1.5

|

1.9

|

|

GDP inflation

|

5.8

|

5.0

|

6.8

|

5.1

|

5.0

|

5.3

|

5.5

|

|

GDP at current prices (R billion)

|

3 807.7

|

4 049.8

|

4 338.9

|

4 601.8

|

4 888.8

|

5 222.3

|

5 611.9

|

|

CPI inflation

|

6.1

|

4.6

|

6.3

|

5.4

|

5.2

|

5.5

|

5.5

|

|

Current account balance (% of GDP)

|

-5.3

|

-4.4

|

-3.3

|

-2.3

|

-2.6

|

-2.9

|

-3.1

|

Source: National Treasury

|

Household consumption

|

||

|

Growth in household spending increased marginally to 1.1 per cent in the first half of the year from 0.6 per cent over the same period of 2016.

|

||

15

|

2017 MEDIUM TERM BUDGET POLICY STATEMENT

|

|

Notably, expenditure on durable goods, such as vehicles and washing machines, contracted during the first half of 2017.

|

||

|

Household consumption expenditure is projected to grow by 1 per cent in 2017

|

A 2.1 per cent contraction in real household disposable income in the first quarter was followed by growth of 4.5 per cent in the second, supported by rising real wages. Nominal year-on-year growth in employee compensation was 7 per cent in the second quarter, with strong increases in general government services. High debt levels continue to constrain household spending. The ratio of household debt to disposable income was 73 per cent in the first half of 2017, compared with 75 per cent in the same period in 2016. Growth in household consumption expenditure is projected to increase to 1 per cent in 2017, reaching 1.9 per cent in 2020 as employment growth strengthens and confidence improves.

|

|

|

||

|

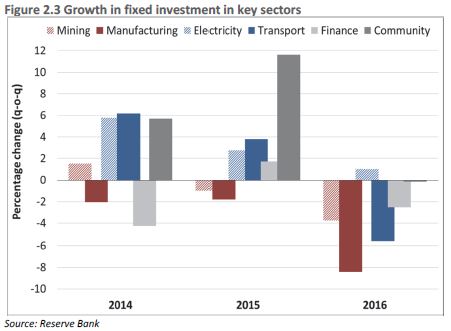

Fixed investment

|

||

|

Capital investment by public corporations has declined for four quarters

|

Total capital investment fell by 1.1 per cent in the first half of 2017 compared with a 2.7 per cent decline in the corresponding period of 2016. Investment by general government grew by 6.3 per cent. Investment by public and private corporations fell by 3.7 per cent and 2.5 per cent respectively. Capital investment by public corporations has declined for four consecutive quarters. In 2016, total capital investment declined for the first time since 2010, with large decreases in mining and manufacturing.

|

|

|

Private-sector investment accounts for 60 per cent of South Africa’s total investment. Weak domestic demand and continued policy uncertainty continue to curb investment plans. Over the long term, this reduces the economy’s potential growth rate. Gross fixed capital formation is expected to average 2.3 per cent growth over the next three years.

|

||

|

Net exports and the current account

|

||

|

Current account deficit narrowed to 2.2 per cent of GDP in first half of 2017

|

The current account deficit narrowed to 2.2 per cent of GDP in the first half of 2017 from 3.8 per cent over the same period in 2016. Imports declined, and the trade surplus improved to 1.3 per cent of GDP in the first half of 2017, compared with 0.1 per cent of GDP in the same period in 2016.

|

16

|

CHAPTER 2: ECONOMIC OUTLOOK

|

|

Merchandise exports saw an uptick from R541.5 billion in the first half of 2016 to R563.3 billion in the first half of this year. Increased mining and manufactured exports were supported by higher commodity prices. The shortfall in the net services, income and transfers balance narrowed from 3.9 per cent of GDP in the first half of 2016 to 3.6 per cent during the same period in 2017.

|

||

|

The current account deficit is projected to increase to 2.3 per cent of GDP in 2017, reaching 3.1 per cent in 2020.

|

||

|

Inflation

|

||

|

Consumer price index (CPI) inflation returned to within the 3 to 6 per cent target band in the second quarter of 2017. CPI inflation declined from 6.6 per cent in January to 4.8 per cent in August. Core inflation, which excludes price-volatile items such as food, fuel and electricity, fell from 5.9 per cent in December 2016 to 4.6 per cent in August 2017, reflecting weak domestic demand. Food price inflation declined from 12 per cent in December 2016 to 5.7 per cent in August 2017 as drought conditions subsided. Noting the improved inflation outlook, the Reserve Bank cut the repurchase (repo) rate from 7 per cent to 6.75 per cent in July 2017.

|

CPI inflation fell back within the target band, reflecting lower core inflation and food prices

|

|

|

Inflation expectations remain near the upper end of the target band. However, the inflation outlook has improved since the 2017 Budget. Headline inflation is now expected to average 5.4 per cent in 2017, down from 6.4 per cent. The revisions to the inflation outlook reflect lower oil and food prices, and a slightly stronger exchange rate assumption. The risks to the inflation outlook remain currency depreciation, higher oil prices, rising electricity tariffs and further sovereign rating downgrades.

|

||

|

Risks to the outlook

|

||

|

Policy and political uncertainty remain central risks to the domestic economic outlook. Elevated policy and political uncertainty, coupled with weak confidence, discourage investment and consumption. Further risks include a downgrade of the local currency rating and higher administrative prices, which would lead to higher inflation. In contrast, improving commodity prices can benefit mining, especially if policy certainty is restored. Better rainfall, especially in the Western and Northern Cape, can result in stronger-than-expected growth in agriculture.

|

Policy and political uncertainty, coupled with weak confidence, discourage investment and consumption

|

|

|

Economic assumptions

|

||

|

The macroeconomic forecast is underpinned by a set of assumptions. Those related to growth and inflation for key trading partners are sourced from the IMF. Commodity prices and global exchange rates are informed by futures curves, and calculated as a moving monthly average. Public investment assumptions are based on approved infrastructure expenditure plans. Food inflation assumptions are informed by high-frequency indicators and analysis.

|

Assumptions underpinning forecast cover global growth, inflation, trade and commodity prices

|

17

|

2017 MEDIUM TERM BUDGET POLICY STATEMENT

|

Table 2.4 Assumptions used in the economic forecast

|

2015

|

2016

|

2017

|

2018

|

2019

|

2020

|

|

|

Percentage

|

Actual

|

Estimate

|

Forecast

|

|||

|

Global demand1

|

4.2

|

4.0

|

4.3

|

4.4

|

4.2

|

4.2

|

|

International commodity prices2

|

||||||

|

Oil (US$ per barrel)

|

52.7

|

44.2

|

52.0

|

51.6

|

52.1

|

52.7

|

|

Gold (US$ per ounce)

|

1 160.4

|

1 247.9

|

1 267.6

|

1 320.0

|

1 342.0

|

1 363.6

|

|

Platinum (US$ per ounce)

|

1 055.4

|

988.3

|

967.7

|

992.2

|

1 014.5

|

1 037.4

|

|

Coal (US$ per ton)

|

57.1

|

64.4

|

83.8

|

79.8

|

74.6

|

71.8

|

|

Iron ore (US$ per ton)

|

56.1

|

58.6

|

73.8

|

67.8

|

61.6

|

57.9

|

|

Food inflation

|

5.1

|

10.5

|

7.3

|

5.1

|

5.9

|

6.0

|

|

Electricity inflation

|

9.2

|

9.2

|

4.7

|

5.1

|

8.0

|

8.0

|

|

Sovereign risk premium

|

2.9

|

3.4

|

2.9

|

2.8

|

2.4

|

2.3

|

|

Real public corporation investment

|

6.0

|

0.7

|

-1.3

|

0.0

|

3.0

|

4.3

|

|

Real private residential investment

|

8.4

|

-1.8

|

0.4

|

-2.1

|

1.2

|

4.4

|

| 1. |

Combined growth index of South Africa’s top 15 trading partners (IMF World Economic Outlook, October 2017)

|

| 2. |

Source: Bloomberg futures prices as at 8 September 2017

|

Source: National Treasury

|

The main revisions to the assumptions since the February 2017 forecast include greater global demand and improved commodity prices, mainly due to higher-than-expected iron ore prices. The risk premium – a measure of the extra return required by global buyers of South African bonds – is higher to reflect domestic policy uncertainty. Investment by public corporations is lower as capital projects are delayed due to weak economic conditions.

|

||

|

Alternative scenarios

|

||

|

The National Treasury has generated three alternate scenarios quantifying some of the risks to the baseline economic forecast.

|

||

|

Scenarios model effects of risk premium increases, as well as higher-than-expected global growth

|

Two scenarios involve downgrades to the local currency debt by global ratings agencies. In both scenarios, the risk premium increases to varying degrees. Global developments leading to broad aversion towards developing-country debt, or a sharp deterioration in the balance sheet of a state-owned company, could have similar effects. A moderate increase in the risk premium could see growth slow to 0.6 per cent in 2018 and 0.9 per cent in 2019. A large increase in the risk premium could see growth contracting by 1.2 per cent in 2018 and 0.8 per cent in 2019.

|

|

|

In the third scenario, global growth improves by an annual average of 0.5 percentage points over the medium term. Export commodity prices are 5 per cent higher than the baseline. The risk premium and bond yields are lower. Growth reaches 1.4 per cent in 2018 and 2.4 per cent in 2020.

|

||

|

The scenarios are presented in Annexure A.

|

18

3

Fiscal policy

|

In brief

|

|

|

●

|

The economic outlook has deteriorated significantly since the beginning of the year. Gross tax revenue for the 2017/18 – 2019/20 period is projected to fall short of the 2017 Budget estimates by R209 billion.

|

|

●

|

The consolidated budget deficit will widen to 4.3 per cent of GDP in 2017/18, against a 2017 Budget target of 3.1 per cent of GDP. Gross national debt is projected to reach over 60 per cent of GDP by 2022, with debt-service costs reaching 15 per cent of main budget revenue by 2020/21.

|

|

●

|

The expenditure ceiling could be breached by R3.9 billion in the current year, mainly as a result of government’s recapitalisation of South African Airways and the South African Post Office. Government is considering the disposal of assets to offset these appropriations during the current year.

|

|

●

|

Additional risks to the framework include more financial demands from state-owned companies, public-service compensation pressures and new spending commitments, particularly in higher education.

|

|

●

|

A presidential task team is considering a range of steps to bring the public finances back onto a sustainable path. Announcements will be made at the time of the 2018 Budget.

|

|

█ Erosion of the fiscal position

|

||

|

Over the past four years, government has followed a path of measured fiscal consolidation, aiming to stabilise the debt-to-GDP ratio by reducing spending and introducing tax increases. This strategy met with some success, reflected in a narrowing primary deficit. But debt has continued to rise as a share of GDP as economic growth rates have declined.

|

Debt levels have risen as economic growth and revenue collection have deteriorated

|

|

|

This year, a sharp deterioration in revenue collection and further downward revisions to economic growth projections have significantly eroded government’s fiscal position. Tax revenue is projected to fall short of the 2017 Budget estimate by R50.8 billion in the current year, the largest under-collection since the 2009 recession. At the same time, additional appropriations of R13.7 billion have been agreed to forestall calls against guaranteed debt by the creditors of South African Airways (SAA) and the South African Post Office (SAPO). These are partially offset by use of the contingency reserve, as well as projected underspending.

|

||

19

|

2017 MEDIUM TERM BUDGET POLICY STATEMENT

|

|

Consolidated budget deficit set to widen to 4.3 per cent of GDP in 2017/18

|

As a result of these developments, the consolidated budget deficit will widen to 4.3 per cent of GDP in 2017/18, against a 2017 Budget target of 3.1 per cent of GDP. Government’s short-term options to reverse this situation are limited. Given that per capita income is falling, the economic impact of further expenditure cuts or tax hikes could be counter-productive.

|

|

|

Following several years of expenditure restraint, further budget cuts will involve hard choices and difficult compromises. Sudden or deep additional cuts that are not well-targeted could put severe pressure on already stressed departmental budgets. Some national departments are battling to operate within the compensation limits set by Parliament in the current year. And several provincial departments are running up unpaid bills to maintain service delivery levels.

|

||

|

Stabilising gross debt below 60 per cent of GDP will require large spending cuts or tax hikes

|

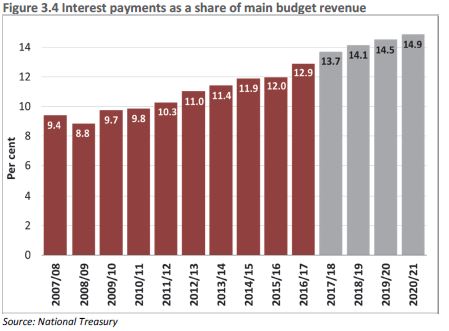

At the same time, government is acutely aware of the dangers of unchecked debt accumulation. Debt-service costs are the fastest-growing category of expenditure, crowding out social and economic spending. By 2020/21, nearly 15 per cent of main budget revenue will be spent servicing debt. The National Treasury estimates that stabilising gross debt below 60 per cent of GDP over the coming decade will require spending cuts or tax hikes amounting to 0.8 per cent of GDP. In 2018/19, 0.8 per cent of GDP would amount to R40 billion.

|

|

|

||

|

Sustainable public finances require significantly higher economic growth

|

Over the medium term, government is committed to maintaining the ceiling on non-interest expenditure. New spending priorities will have to be met by funds reallocated from within existing limits. Any adjustments to the ceiling itself would need to be matched by revenue increases.

|

|

|

A team of Cabinet ministers reporting directly to the President is considering a range of proposals to bring the public finances back onto a sustainable path. Announcements are expected to be made at the time of the 2018 Budget. More fundamentally, sustainable public finances require a significant acceleration of economic growth.

|

20

|

CHAPTER 3: FISCAL POLICY

|

|

█ Revenue performance and outlook

|

||

|

Over the past five years, despite a declining rate of economic growth, tax revenue continued to grow more rapidly than GDP. This trend came to an abrupt halt towards the end of 2016/17 as South Africa entered a recession. Despite substantial tax increases over the past two years, tax revenue growth has barely exceeded the low rate of economic growth.

|

The trend of buoyant revenue collection has run its course

|

|

|

In 2016/17, the largest shortfall against the 2017 Budget estimate was in customs duties, which slowed in tandem with falling import growth. Personal income tax, value-added tax (VAT) and corporate income tax also performed below projections. These shortfalls were offset by higher-than-projected dividend withholding taxes amounting to R5.4 billion. This windfall may have resulted from artificial declarations of dividend payments before the effective date to avoid the higher tax rate introduced in the 2017 Budget.

|

||

Table 3.1 Gross tax revenue

|

2016/17

|

2017/18

|

|||||

|

R billion

|

Budget1

|

Outcome

|

Deviations

|

Budget1

|

Revised

|

Deviations

|

|

Persons and individuals

|

425.8

|

424.5

|

-1.3

|

482.1

|

461.3

|

-20.8

|

|

Companies

|

205.1

|

204.4

|

-0.7

|

218.7

|

213.9

|

-4.8

|

|

Value-added tax

|

290.0

|

289.2

|

-0.8

|

312.8

|

301.3

|

-11.4

|

|

Dividend withholding tax2

|

25.7

|

31.1

|

5.4

|

34.2

|

31.6

|

-2.6

|

|

Specific excise duties

|

35.7

|

35.8

|

0.1

|

39.9

|

37.4

|

-2.5

|

|

Fuel levy

|

63.0

|

62.8

|

-0.2

|

70.9

|

70.1

|

-0.8

|

|

Customs duties

|

47.5

|

45.6

|

-1.9

|

52.6

|

47.2

|

-5.4

|

|

Ad-valorem excise duties

|

3.4

|

3.4

|

0.0

|

3.6

|

3.6

|

-0.0

|

|

Other

|

48.2

|

47.3

|

-0.9

|

50.7

|

48.4

|

-2.3

|

|

Gross tax revenue

|

1 144.4

|

1 144.1

|

-0.3

|

1 265.5

|

1 214.7

|

-50.8

|

| 1. |

2017 Budget figures

|

| 2. |

Includes secondary tax on companies

|

Source: National Treasury

|

Factors contributing to poor revenue performance

|

||

|

The lower outcomes in 2016/17 explain part of the shortfall in the current year. However, revenue growth has remained weak, even as the economy emerged from recession in the second quarter of 2017. For the first six months of 2017/18, gross tax revenue grew by 5.9 per cent year-on-year against a target of 10.7 per cent. All tax instruments are performing poorly, with large shortfalls for personal and corporate income tax, and dividend withholding tax. The National Treasury projects a tax revenue shortfall of R50.8 billion in 2017/18 compared with the 2017 Budget estimate.

Revenue weakness reflects a number of economic factors:

|

Projected revenue shortfall of R50.8 billion in current year

|

|

●

|

Growth in key sectors that have supported buoyant revenue collection – such as finance, retail and telecommunications – has slowed.

|

||

|

●

|

Personal income tax collection has been affected by low bonus payments, moderate wage settlements, job losses and a slower expansion of public-sector employment.

|

||

|

●

|

Corporate income tax under-collections in the first half of 2017/18 resulted from persistently weak growth and commodity price volatility.

|

||

|

●

|

Weak investment and household consumption led to a sharp contraction in imports in 2016, affecting VAT and customs duties.

|

|

21

|

2017 MEDIUM TERM BUDGET POLICY STATEMENT

|

|

●

|

The stabilisation of the rand has muted the buoyancy of import taxes and revenue on profits in traded sectors, such as mining.

|

|

Compliance concerns mounting in face of tax administration challenges and weaker tax morality

|