|

December 29, 2023 |

| |

|

|

2023 Summary Prospectus |

• iShares Emerging Markets Equity Factor ETF | EMGF | CBOE BZX

Before you invest, you

may want to review the Fund’s prospectus, which contains more information about the Fund and its risks. You can find the Fund’s prospectus (including

amendments and supplements) and other information about the Fund, including the

Fund’s statement of additional information and shareholder reports, online at https://www.blackrock.com/prospectus. You can also get this information at no cost by calling 1-800-iShares (1-800-474-2737) or

by sending an e-mail request to iSharesETFs@blackrock.com, or from your financial professional. The Fund’s prospectus and statement of additional information, both dated December 29, 2023, as amended and

supplemented from time to time, are incorporated by reference into (legally made a part of) this Summary Prospectus. Information on the Fund’s net asset

value, market price, premiums and discounts, and bid-ask spreads can be found at www.iShares.com.

The Securities and Exchange

Commission has not approved or disapproved these securities or passed upon the adequacy of this prospectus. Any representation to the contrary is a criminal offense.

iSHARES® EMERGING MARKETS EQUITY FACTOR ETF

Ticker: EMGFStock Exchange: Cboe BZX

Investment Objective

The

iShares Emerging Markets Equity Factor ETF (the “Fund”) seeks to track the investment results of

an index composed of stocks of large- and mid-capitalization companies in emerging markets that have favorable exposure to target style factors subject to constraints.

Fees

and Expenses

The following table describes the fees and expenses that you will incur if you buy, hold

and sell shares of the Fund. The investment advisory agreement between iShares, Inc. (the “Company”) and BlackRock Fund Advisors (“BFA”) (the “Investment Advisory Agreement”) provides that BFA will pay all operating expenses of the Fund, except: (i) the management fees, (ii) interest

expenses, (iii) taxes, (iv) expenses incurred with respect to the acquisition and disposition of portfolio securities and the execution of portfolio transactions, including brokerage commissions, (v) distribution fees or expenses, and (vi) litigation expenses

and any extraordinary expenses. The Fund may incur “Acquired Fund Fees and Expenses.” Acquired

Fund Fees and Expenses reflect the Fund's pro rata share of the fees and expenses incurred by investing in other investment companies. The impact of Acquired Fund Fees

and Expenses is included in the total returns of the Fund. Acquired Fund Fees and Expenses are not included in the calculation of the ratio of expenses to average net assets shown in the Financial Highlights section of the Fund's prospectus (the “Prospectus”). BFA, the investment adviser to the Fund, has contractually agreed to waive a portion of its management fees in an amount equal to the Acquired Fund Fees and Expenses, if any, attributable to investments by the Fund in other

series of iShares Trust and the Company through December 31, 2026. The contractual waiver may be terminated prior to December 31, 2026 only upon written agreement of the Company and BFA.

You may pay other fees, such as brokerage commissions and other fees to financial

intermediaries, which are not reflected in the tables and examples below.

| Annual Fund Operating

Expenses (ongoing expenses that you pay each year as a

percentage of the value of your investments)1,2 | ||||||

| Management

Fees |

Distribution and

Service (12b-1) Fees |

Other

Expenses3 |

Acquired Fund

Fees and Expenses3

|

Total Annual

Fund

Operating

Expenses |

Fee Waiver

and/or

Expense

Reimbursement3 |

Total

Annual Fund Operating Expenses

After Fee Waiver

and/or

Expense

Reimbursement |

| 0.25% |

None |

0.00% |

0.00% |

0.25% |

(0.00)% |

0.25% |

1

Operating expenses paid by BFA under the Investment Advisory Agreement exclude Acquired Fund Fees and Expenses, if any.

2

The expense information in the table has been restated to reflect current fees.

3

The amount rounded to 0.00%.

S-1

Example. This Example is intended to help you compare the cost of owning shares of the Fund with the cost of investing in other

funds. The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then sell all of your shares at the end of those periods. The Example also assumes that your investment has a 5% return each year and that the

Fund’s operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions, your costs would be:

| 1

Year |

3

Years |

5

Years |

10 Years |

| $26 |

$80 |

$141 |

$318 |

Portfolio Turnover. The Fund may pay transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in the Annual Fund Operating Expenses or in the Example, affect the Fund’s performance. During the most recent fiscal year, the Fund's portfolio turnover rate was 121% of the average value of its portfolio.

Principal Investment Strategies

The Fund seeks to

track the investment results of the STOXX Emerging Markets Equity Factor Index (the “Underlying Index”), which is a rules-based equity index

provided by STOXX Ltd. (the “Index Provider” or “STOXX”). The Underlying Index is composed of large- and mid-capitalization equity securities from the STOXX Emerging Markets Index (the

“Parent Index”) that are selected and weighted using an

optimization process designed to maximize exposure to five target factors: momentum, quality, value, low volatility and size. The Underlying Index seeks to control exposure to, among

other things, industries and countries, limit turnover and

maintain a level of risk similar to that of the Parent Index. The Parent Index is a free float market

capitalization-weighted index designed to measure the performance of large- and mid-capitalization companies from emerging markets. Large- and mid-capitalization companies, as calculated by the Index Provider, represent approximately the top 85% of the investable market capitalization of each emerging market country included in the Parent Index, as determined by STOXX.

The momentum score is calculated from

the following signals: price momentum, earnings momentum and earnings announcement drift (i.e., the

difference between a stock’s performance on and immediately following an earnings announcement date).

The quality score is

calculated from the following signals: gross profitability, share dilution, accruals, changes in net

operating assets, carbon emissions intensity and greenhouse gas (“GHG”) reduction targets. Carbon emissions intensity

is based on the issuer’s Scope 1 and Scope 2 GHG emissions (i.e., direct emissions from sources that an issuer

owns or controls and indirect emissions from the issuer’s purchase of energy) relative to peers in

its Industry

S-2

Classification Benchmark (“ICB”) Supersector, as reported by Institutional

Shareholder Services

(“ISS”). The GHG targets signal is based on the

robustness of an issuer’s GHG reduction targets, including whether they are part of the Science Based Targets initiative

(“SBTi”) framework; this is assessed by ISS based

on its own ESG ratings data and SBTi data.

The value score is calculated from the following signals: current book value-to-price ratio, dividend yield (i.e.,

12-month trailing dividend divided by total market capitalization), earnings yield (i.e., 12-month net income

divided by total market capitalization), cash flow yield (i.e., 12-month cash flow divided by total market capitalization) and time series normalized cash flow yield over the previous 36 months.

The low volatility

score is based on prior 12-month volatility, as calculated by the Index Provider.

The size score seeks to measure an

issuer’s market capitalization relative to other companies in the Parent Index.

The maximum weight of a single security is

10%, and the sum of security weights that are individually greater than 4.5% must be less than 22.5% of

the Underlying Index. The Index Provider also applies other constraints, such as country and sector exposures relative to the Parent Index, among others. The Underlying Index is reviewed and rebalanced quarterly.

As of August 31, 2023, the Underlying Index

consisted of approximately 588 constituents from companies in the following countries or regions: Brazil,

Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Kuwait, Malaysia, Mexico, Philippines, Poland, Qatar, Saudi Arabia,

South Africa, South Korea, Taiwan, Thailand, Turkey and the United Arab Emirates.

As of August 31, 2023, a significant portion

of the Underlying Index is represented by securities of companies in the financials and technology industries or sectors. The components of the Underlying Index are likely to change over time.

BFA uses an indexing

approach to try to achieve the Fund’s investment objective. Unlike many investment companies, the Fund does not try to

“beat” the index it tracks and does not seek temporary defensive positions when markets decline or appear overvalued.

Indexing may eliminate the chance that the

Fund will substantially outperform the Underlying Index but also may reduce some of the risks of active

management, such as poor security selection. Indexing seeks to achieve lower costs and better after-tax performance by aiming to keep portfolio turnover low in comparison to actively managed investment companies.

BFA uses a representative sampling indexing

strategy to manage the Fund. “Representative sampling” is an indexing strategy that involves

investing in a representative sample of securities that collectively has an investment profile similar to that of an applicable underlying index. The securities selected are expected to have, in the aggregate, investment characteristics (based on factors such as market capitalization and industry weightings), fundamental characteristics (such as return variability and yield) and liquidity measures similar to those of an applicable underlying index. The Fund

S-3

may or may not hold all of the securities

in the Underlying Index.

The Fund

generally will invest at least 80% of its assets in the component securities of its Underlying Index and in

investments that have economic characteristics that are substantially identical to the component securities of its Underlying Index (i.e., depositary receipts

representing securities of the Underlying Index) and may invest up to 20% of its assets in certain futures,

options and swap contracts, cash and cash equivalents, including shares of money market funds advised by BFA or its affiliates, as well as in securities not included in the Underlying Index, but which BFA believes will help the Fund track the Underlying Index. Cash and cash equivalent investments associated with a derivative position will be treated as part of that position for the purposes of calculating the percentage of investments included in the Underlying Index. The Fund seeks to track the investment results of the Underlying Index before fees and expenses of the Fund.

The Fund may lend securities representing up

to one-third of the value of the Fund's total assets (including the value of any collateral

received).

The Underlying Index is sponsored by STOXX, which

is independent of the Fund and BFA. The Index Provider determines the composition and relative weightings of the securities in the Underlying Index and publishes information regarding the market value of the Underlying Index.

Industry Concentration

Policy. The Fund will concentrate its investments (i.e., hold 25% or more of its

total assets) in a particular industry or group of industries to approximately the same

extent that the Underlying Index is

concentrated. For purposes of this limitation, securities of the U.S. government (including its agencies and instrumentalities) and repurchase agreements collateralized by U.S. government securities are not considered to be issued by members of any industry.

Summary of Principal Risks

As with any investment, you could lose all or

part of your investment in the Fund, and the Fund's performance could trail that of other investments. The

Fund is subject to certain risks, including the principal risks noted below, any of which may adversely affect the Fund's net asset value per share (“NAV”), trading price, yield, total return and ability

to meet its investment objective. Certain key risks are prioritized below (with others following in

alphabetical order), but the relative significance of any risk is difficult to predict and may change over time. You should review each risk factor carefully.

Risk of Investing in Emerging Markets. Investments in emerging market issuers may be subject to a greater risk of loss than investments in issuers located or operating in more developed markets. Emerging markets may be more likely to experience inflation, social instability, political turmoil or rapid changes in economic conditions than more developed markets. Companies in many emerging markets are not subject to the same degree of regulatory requirements, accounting standards or auditor oversight as companies in more developed countries, and as a result, information about the securities in which the Fund invests may be less reliable or complete. Emerging markets

S-4

often have less reliable securities valuations and greater risk associated with custody of securities than developed markets. There may be significant obstacles to obtaining information necessary for investigations into or litigation against companies and shareholders may have limited legal remedies. The Fund is not actively managed and does not select investments based on investor protection considerations.

Style Factors Risk. Each of the five equity style factors (i.e., momentum, quality, value,

low volatility and size) that determine the weight of each component security in the Underlying Index has characteristics that may cause the Fund to underperform the Parent Index or the market as a whole.

Momentum Factor Risk. Stocks that

previously exhibited relatively high momentum characteristics may not experience positive momentum or may experience more volatility than the market as a whole.

Quality

Factor Risk. Stocks included in the Underlying Index are deemed by the Index Provider to be quality stocks based on a number of attributes, but there is no guarantee that the past performance of these stocks will continue. Companies that issue these stocks may experience lower than expected returns or may experience negative growth, as well as increased leverage, resulting in lower than expected or negative returns to Fund shareholders. Many attributes of an issuer, as well as various market, regulatory and other external factors, can affect a stock’s quality and performance, and their impact on the stock or its price can be difficult to predict.

Value Factor Risk. Securities issued by companies that may be perceived as undervalued, particularly securities of a company that appear to trade at a significant discount to the company’s intrinsic value, may fail to appreciate for long periods of time and may never realize their full potential value. The Index Provider may be unsuccessful in applying a factor that emphasizes such securities. Value securities have generally performed better than non-value securities during periods of economic recovery, although there is no assurance that they will continue to do so. There may be periods where value securities go out of favor, thus causing the Fund’s performance to suffer.

Low Volatility Factor Risk. Securities in the Fund’s portfolio may be subject to price volatility, and the prices may not be any less volatile than the market as a whole,and could be more volatile.

Low Size Factor Risk.

Companies with relatively lower market capitalization within a broader index or market capitalization range (“low size companies”) may be less stable and more susceptible to adverse developments, and their securities may be more volatile and less liquid, than companies with relatively higher market capitalization.

Equity Securities Risk. Equity securities are subject to changes in

value, and their values may be more volatile than those of other asset classes. The Underlying Index is composed of common stocks, which generally subject their

holders to more risks than preferred stocks and debt securities because common stockholders’ claims are subordinated to those of holders of preferred stocks

S-5

and debt securities upon the bankruptcy

of the issuer.

Market Risk. The Fund could lose money over short periods due to short-term market movements and over longer periods during more prolonged market downturns. Local, regional or global events such as war, acts of terrorism, public health issues, recessions, the prospect or occurrence of a sovereign default or other financial crisis, or other events could have a significant impact on the Fund and its investments and could result in increased

premiums or discounts to the Fund’s NAV.

Index-Related Risk. There is no guarantee that the Fund’s investment results will have a high degree of correlation to those of the Underlying Index or that the Fund will achieve its investment objective. Market disruptions and regulatory restrictions could have an adverse effect on the Fund’s ability to adjust its exposure to the required levels in order to track the Underlying Index. Errors in index data, index computations or the construction of the Underlying Index in accordance with its methodology may occur from time to time and may not be identified and corrected by the Index Provider for a period of time or at all, which may have an adverse impact on the Fund and its shareholders. Unusual market conditions or other unforeseen circumstances (such as natural disasters, political unrest or war) may impact the Index Provider or a third-party data provider, and could cause the Index Provider to postpone a scheduled rebalance. This could cause the Underlying Index to vary from its normal or expected composition.

Asset Class Risk. Securities and other assets in the Underlying Index or in the Fund's portfolio may underperform in comparison to the general financial markets, a particular financial market or other asset classes.

Authorized Participant Concentration Risk. Only an Authorized Participant (as defined in the Creations and Redemptions section of the Prospectus) may engage in creation or redemption transactions directly with the Fund, and none of those Authorized Participants is obligated to engage in creation and/or redemption transactions. The Fund has a limited number of institutions that may act as Authorized Participants on an agency basis (i.e., on

behalf of other market participants). To the extent that Authorized Participants exit the business or are unable to proceed with creation or redemption orders with respect to the Fund and no other Authorized Participant is able to step forward to create or redeem, Fund shares may be more likely to trade at a premium or discount to NAV and possibly face trading halts or delisting. Authorized Participant concentration risk may be heightened for exchange-traded funds (“ETFs”), such as the Fund, that invest in

securities issued by non-U.S. issuers or other securities or instruments that have lower trading volumes.

Calculation Methodology Risk. The Index Provider relies on various sources of

information to assess the criteria of components of the Underlying Index, including information that may be

based on assumptions and estimates. Neither the Fund nor BFA can offer assurances that the Index Provider’s calculation methodology or sources of information will provide an accurate assessment of included components.

S-6

Commodity

Risk. The Fund invests in companies that are susceptible to fluctuations in certain commodity markets and to price changes due to trade relations. Any negative changes in commodity markets that may be due to changes in supply and demand for commodities, market events, war, regulatory developments, other catastrophic events, or other factors that the Fund cannot control could have an adverse impact on those companies.

Concentration Risk. The Fund may be susceptible to an increased risk of loss, including losses due to adverse events that affect the Fund’s investments more than the market as a whole, to the extent that the Fund's investments are concentrated in the securities and/or other assets of a particular issuer or issuers, country, group of countries, region, market, industry, group of industries, sector, market segment or asset class.

Currency Risk. Because the Fund's NAV is

determined in U.S. dollars, the Fund's NAV could decline if the currency of a non-U.S. market in which the

Fund invests depreciates against the U.S. dollar or if there are delays or limits on repatriation of such currency. Currency exchange rates can be very volatile and can change quickly and unpredictably. As a result, the Fund's NAV may change quickly and without warning.

Custody Risk. Less developed securities markets are more likely to experience problems with the clearing and settling of trades, as well as the holding of securities by local banks, agents and depositories.

Cybersecurity Risk. Failures or breaches of the

electronic systems of the Fund, the Fund's adviser, distributor, the Index Provider and other service

providers, market

makers, Authorized Participants or the issuers of securities in which the Fund invests have the ability to cause disruptions, negatively impact the Fund’s business operations and/or potentially result in financial losses to the Fund and its shareholders. While the Fund has established business continuity plans and risk management systems seeking to address system breaches or failures, there are inherent limitations in such plans and systems. Furthermore, the Fund cannot control the cybersecurity plans and systems of the Fund’s Index Provider and other service providers, market makers, Authorized Participants or issuers of securities in which the Fund invests.

Dividend-Paying Stock Risk. Investing in dividend-paying stocks involves the

risk that such stocks may fall out of favor with investors and underperform the broader market. Companies that issue dividend-paying stocks are not required to pay or continue paying dividends on such stocks. It is possible that issuers of the stocks held by the Fund will not declare dividends in the future or will reduce or eliminate the payment of dividends (including reducing or eliminating anticipated accelerations or increases in the payment of dividends) in the future.

ESG Risk. To the extent that the Underlying Index uses criteria related to the ESG characteristics of issuers, this may limit the types and number of investment opportunities available to the Fund and, as a result, the Fund may underperform other funds whose underlying index does not use ESG criteria. The Underlying Index’s use of ESG criteria may result in the Fund investing in, or allocating greater weight to, securities or market sectors that underperform the market as a whole or

S-7

underperform other funds that use ESG criteria. In addition, the use of representative sampling may result in divergence of the Fund’s overall ESG characteristics or ESG risk from those of the Underlying Index. The Index Provider may evaluate security-level ESG data and, if applicable, ESG objectives or constraints that are relevant to the Underlying Index only at index reviews or rebalances. Securities included in the Underlying Index may cease to meet the relevant ESG criteria but may nevertheless remain in the Underlying Index and the Fund until the next review or rebalance by the Index Provider. As a result, certain securities in the Underlying Index, or the Underlying Index as a whole, may not meet the relevant ESG objectives or constraints at all times.

Financials Sector Risk. The performance of companies

in the financials sector may be adversely impacted by many factors, including, among others, changes in government regulations, economic conditions, and interest rates, credit rating downgrades, adverse public perception, exposure concentration and decreased liquidity in credit markets. The impact of changes in regulation of any individual financial company, or of the financials sector as a whole, cannot be predicted. Cybersecurity incidents and technology malfunctions and failures have become increasingly frequent and have caused significant losses to companies in this sector, which may negatively impact the Fund.

Geographic Risk. A natural disaster could occur

in a geographic region in which the Fund invests, which could adversely affect the economy or the business operations of companies in the specific geographic region, causing an

adverse impact on the Fund's investments in, or which are exposed to, the affected region.

High Portfolio Turnover Risk. High portfolio turnover (considered by the Fund

to mean higher than 100% annually) may result in increased transaction costs to the Fund, including brokerage commissions, dealer mark-ups and other transaction costs on the sale of the securities and on reinvestment in other securities.

Indexing Investment Risk. The Fund is not actively

managed, and BFA generally does not attempt to take defensive positions under any market conditions,

including declining markets.

Infectious Illness Risk. A widespread outbreak of an infectious illness, such as the COVID-19 pandemic, may result in travel restrictions, disruption of healthcare services, prolonged quarantines, cancellations, supply chain disruptions, business closures, lower consumer demand, layoffs, ratings downgrades, defaults and other significant economic, social and political impacts. Markets may experience temporary closures, extreme volatility, severe losses, reduced liquidity and increased trading costs. Such events may adversely affect the Fund and its investments and may impact the Fund’s ability to purchase or sell securities or cause elevated tracking error and increased premiums or discounts to the Fund's NAV. Despite the development of vaccines, the duration of the COVID-19 pandemic and its effects cannot be predicted with certainty.

Information Technology Sector Risk. Information technology companies face intense competition and potentially rapid product obsolescence. They are also heavily dependent on intellectual

S-8

property rights and may be adversely affected by the loss or impairment of those rights. Companies in the information technology sector are facing increased government and regulatory scrutiny and may be subject to adverse government or regulatory action. Companies in the software industry may be adversely affected by, among other things, the decline or fluctuation of subscription renewal rates for their products and services and actual or perceived vulnerabilities in their products or services.

Issuer Risk. The performance of the Fund depends on the performance of individual securities to which the Fund has exposure. Changes in the financial condition or credit rating of an issuer of those securities may cause the value of the securities to decline.

Large-Capitalization Companies Risk. Large-capitalization companies may be less able than smaller capitalization companies to adapt to changing market conditions. Large-capitalization companies may be more mature and subject to more limited growth potential compared with smaller capitalization companies. During different market cycles, the performance of large-capitalization companies has trailed the overall performance of the broader securities markets.

Large Shareholder and Large-Scale Redemption Risk. Certain shareholders, including an Authorized Participant, a third-party investor, the Fund’s adviser or an affiliate of the Fund’s adviser, a market maker, or another entity, may from time to time own or manage a substantial amount of Fund shares, or may invest in the Fund and hold their investment for a limited period of time. There can be no

assurance that any large shareholder or large group of

shareholders would not redeem their investment. Redemptions of a large number of Fund shares could require the Fund to dispose of assets to meet the redemption requests, which can accelerate the realization of taxable income and/or capital gains and cause the Fund to make taxable distributions to its shareholders earlier than the Fund otherwise would have. In addition, under certain circumstances, non-redeeming shareholders may be treated as receiving a disproportionately large taxable distribution during or with respect to such year. In some circumstances, the Fund may hold a relatively large proportion of its assets in cash in anticipation of large redemptions, diluting its investment returns. These large redemptions may also force the Fund to sell portfolio securities when it might not otherwise do so, which may negatively impact the Fund’s NAV, increase the Fund’s brokerage costs and/or have a material effect on the market price of the Fund shares.

Management Risk. As the Fund will not fully

replicate the Underlying Index, it is subject to the risk that BFA's investment strategy may not produce

the intended results.

Market Trading Risk. The Fund faces numerous market trading risks,

including the potential lack of an active market for Fund shares, losses from trading in secondary markets, periods of high volatility and disruptions in the creation/redemption process. ANY OF THESE FACTORS, AMONG OTHERS, MAY LEAD TO THE FUND'S SHARES TRADING AT A PREMIUM OR DISCOUNT TO NAV.

S-9

Mid-Capitalization Companies Risk. Compared

to large-capitalization companies, mid-capitalization companies may be less stable and more susceptible to adverse developments. In addition, the securities of mid-capitalization companies may be more volatile and less liquid than those of large-capitalization companies.

Model Risk. Neither the Fund nor BFA can offer assurances that the Index Provider’s model will result in the Fund meeting its investment objective. The Fund may underperform other funds that do not similarly invest.

National Closed Market Trading Risk. To the extent that the underlying securities or other instruments held by the Fund trade on foreign exchanges or in foreign markets that may be closed when the securities exchange on which the Fund’s shares trade is open, there are likely to be deviations between the current price of such an underlying security and the last quoted price for the underlying security (i.e.,

the Fund’s quote from the closed foreign market). The impact of a closed foreign market on the Fund is likely to be greater where a large portion of the Fund’s underlying securities or other instruments trade on that closed foreign market or when the foreign market is closed for unscheduled reasons. These deviations could result in premiums or discounts to the Fund’s NAV that may be greater than those experienced by other ETFs.

Non-U.S. Securities Risk. Investments in the securities

of non-U.S. issuers are subject to the risks associated with investing in those non-U.S. markets, such as heightened risks of inflation or nationalization. The Fund may lose money due to political, economic and

geographic events affecting issuers of non-U.S.

securities or non-U.S. markets. In addition, non-U.S. securities markets may trade a small number of securities and may be unable to respond effectively to changes in trading volume, potentially making prompt liquidation of holdings difficult or impossible at times. The Fund is specifically exposed to Asian Economic Risk.

Operational Risk. The Fund is exposed to

operational risks arising from a number of factors, including, but not limited to, human error, processing

and communication errors, errors of the Fund’s service providers, counterparties or other third parties, failed or inadequate processes and technology or systems failures. The Fund and BFA seek to reduce these operational risks through controls and procedures. However, these measures do not address every possible risk and may be inadequate to address significant operational risks.

Privatization Risk. Some countries in which the Fund invests have privatized, or have begun the process of privatizing, certain entities and industries. Privatized entities may lose money or be re-nationalized.

Reliance on Trading Partners Risk. The Fund

invests in countries or regions whose economies are heavily dependent upon trading with key partners. Any reduction in this trading may have an adverse impact on the Fund's investments. Through its holdings of securities of certain issuers, the Fund is specifically exposed to Asian Economic Risk.

Risk of

Investing in China. Investments in Chinese securities, including certain Hong Kong-listed and U.S.-listed securities, subject the Fund

S-10

to risks specific to China. China may be

subject to considerable degrees of economic, political and social instability. China is an emerging market and demonstrates significantly higher volatility from time to time in comparison to developed markets. Over the last few decades, the Chinese government has undertaken reform of economic and market practices and has expanded the sphere of private ownership of property in China. However, Chinese markets generally continue to experience inefficiency, volatility and pricing anomalies resulting from governmental influence, a lack of publicly available information and/or political and social instability.

Chinese

companies are also subject to the risk that Chinese authorities can intervene in their operations and

structure. Internal social unrest or confrontations with neighboring countries, including military conflicts in response to such events, may also disrupt economic development in China and result in a greater risk of currency fluctuations, currency non-convertibility, interest rate fluctuations and higher rates of inflation.

China has experienced

security concerns, such as terrorism and strained international relations. Additionally, China is alleged to have participated in state-sponsored cyberattacks against foreign companies and foreign governments. Actual and threatened responses to such activity and strained international relations, including purchasing restrictions, sanctions, tariffs or cyberattacks on the Chinese government or Chinese companies, may impact China’s economy and Chinese issuers of securities in which the Fund invests. Incidents involving China's or the

region's security may cause uncertainty in Chinese markets and

may adversely affect the Chinese economy and the Fund's investments. Export growth continues to be a major driver of China's rapid economic growth. Reduction in spending on Chinese products and services, supply chain diversification, institution of additional tariffs or other trade barriers (including as a result of heightened trade tensions or a trade war between China and the U.S. or in response to actual or alleged Chinese cyber activity) or a downturn in any of the economies of China's key trading partners may have an adverse impact on the Chinese economy. The Underlying Index may include companies that are subject to economic or trade restrictions (but not investment restrictions) imposed by the U.S. or other governments due to national security, human rights or other concerns of such government. So long as these restrictions do not include restrictions on investments, the Fund is generally expected to invest in such companies, consistent with its objective to track the performance of the Underlying Index.

Chinese companies, including Chinese companies

that are listed on U.S. exchanges, are not subject to the same degree of regulatory requirements, accounting standards or auditor oversight as companies in more developed countries. As a result, information about the Chinese securities in which the Fund invests may be less reliable or complete. Chinese companies with securities listed on U.S. exchanges may be delisted if they do not meet U.S. accounting standards and auditor oversight requirements, which would significantly decrease the liquidity and value of the securities.

S-11

There may be significant obstacles to obtaining information necessary for investigations into or litigation against Chinese companies, and shareholders may have limited legal remedies. The Fund is not actively managed and does not select investments based on investor protection considerations.

Risk of Investing in Russia. Investing in Russian securities involves significant risks, including legal, regulatory, currency and economic risks that are specific to Russia. In addition, investing in Russian securities involves risks associated with the settlement of portfolio transactions and loss of the Fund’s ownership rights in its portfolio securities as a result of the system of share registration and custody in Russia. Governments in the U.S. and many other countries have imposed economic sanctions on certain Russian individuals and Russian corporate and banking entities. A number of jurisdictions may also institute broader sanctions on Russia. Russia has issued a number of countersanctions, some of which restrict the distribution of profits by limited liability companies (e.g., dividends), and prohibit

Russian persons from entering into transactions with designated persons from “unfriendly states” as well as the export of raw materials or

other products from Russia to certain sanctioned persons. Russia launched a large-scale invasion of Ukraine on February 24, 2022. The extent and duration of the military action, resulting sanctions and resulting future market disruptions, including declines in its stock markets and the value of the ruble against the U.S. dollar, are impossible to predict, but could be significant. Disruptions caused by Russian military action or other actions (including cyberattacks and

espionage) or resulting actual and threatened responses to such activity, including purchasing and financing restrictions, boycotts or changes in consumer or purchaser preferences, sanctions, import and export restrictions, tariffs or cyberattacks on the Russian government, Russian companies, or Russian individuals, including politicians, may impact Russia’s economy and Russian companies in which the Fund invests. Actual and threatened responses to Russian military action may also impact the markets for certain Russian commodities, such as oil and natural gas, as well as other sectors of the Russian economy, and are likely to have collateral impacts on such sectors globally. Russian companies may be unable to pay dividends and, if they pay dividends, the Fund may be unable to receive them. As a result of sanctions, the Fund is currently restricted from trading in Russian securities, including those in its portfolio, while the Underlying Index has removed Russian securities. It is unknown when, or if, sanctions may be lifted or the Fund’s ability to trade in Russian securities will resume.

Risk of Investing in Saudi Arabia. The ability of foreign

investors (such as the Fund) to invest in the securities of Saudi Arabian issuers is relatively new. Such

ability could be restricted by the Saudi Arabian government at any time, and unforeseen risks could materialize with respect to foreign ownership in such securities. The economy of Saudi Arabia is dominated by petroleum exports. A sustained decrease in petroleum prices could have a negative impact on all aspects of the economy. Investments in the securities of Saudi Arabian issuers involve risks not typically associated

S-12

with investments in securities of issuers

in more developed countries that may negatively affect the value of the Fund’s investments. Such heightened risks may include, among others, expropriation and/or nationalization of assets, restrictions on and government intervention in international trade, confiscatory taxation, political instability, including authoritarian and/or military involvement in governmental decision making, armed conflict, crime and instability as a result of religious, ethnic and/or socioeconomic unrest. There remains the possibility that instability in the larger Middle East region could adversely impact the economy of Saudi Arabia, and there is no assurance of political stability in Saudi Arabia.

Saudi Arabia Broker Risk. There are a number of different ways of conducting

transactions in equity securities in the Saudi Arabian market. The Fund generally expects to conduct its transactions in a manner in which the Fund would not be limited by Saudi Arabian regulations to a single broker. However, there may be a limited number of brokers who can provide services to the Fund, which may have an adverse impact on the prices, quantity or timing of Fund transactions.

Securities Lending Risk. The Fund may engage in securities lending. Securities lending involves the risk that the Fund may lose money because the borrower of the loaned securities fails to return the securities in a timely manner or at all. The Fund could also lose money in the event of a decline in the value of collateral provided for loaned securities or a decline in the value of any investments made with cash collateral. These events could also trigger adverse tax consequences for the Fund.

Security

Risk. Some countries and regions in which the Fund invests have experienced security concerns, such as war, terrorism and strained international relations. Incidents involving a country's or region's security may cause uncertainty in its markets and may adversely affect its economy and the Fund's investments.

Technology Sector Risk. Technology companies,

including information technology companies, may have limited product lines, markets, financial

resources or personnel. Technology companies typically face intense competition and potentially rapid product obsolescence. They are also heavily dependent on intellectual property rights and may be adversely affected by the loss or impairment of those rights. Companies in the technology sector may face increased government and regulatory scrutiny and may be subject to adverse government or regulatory action.

Tracking Error Risk. The Fund may be subject to

“tracking error,” which is the divergence of the Fund’s performance from that of the Underlying Index. Tracking error may occur because of differences between the securities and other instruments held in the Fund’s portfolio and those included in the Underlying Index, pricing differences (including,

as applicable, differences between a security’s price at the local market close and the Fund's

valuation of a security at the time of calculation of the Fund's NAV), transaction costs incurred by the Fund, the Fund’s holding of uninvested cash, differences in timing of the accrual or the valuation of dividends or interest received by the Fund or distributions paid to the Fund’s shareholders, the requirements to maintain pass-through

S-13

tax treatment, portfolio transactions carried out to minimize the distribution of capital gains to shareholders, acceptance of custom baskets, changes to the Underlying Index or the costs to the Fund of complying with various new or existing regulatory requirements, among other reasons. This risk may be heightened during times of increased market volatility or other unusual market conditions. Tracking error also may result because the Fund incurs fees and expenses, while the Underlying Index does not. Tracking error may occur due to differences between the methodologies used in calculating the value of the Underlying Index and determining the Fund’s NAV. BFA EXPECTS THAT THE FUND WILL EXPERIENCE HIGHER TRACKING ERROR THAN IS TYPICAL FOR SIMILAR INDEX ETFs.

Valuation Risk. The price the Fund could

receive upon the sale of a security or other asset may differ from the Fund's valuation of the security or

other

asset and from

the value used by the Underlying Index, particularly for securities or other assets that trade in low volume or volatile markets or that are valued using a fair value methodology as a result of trade suspensions or for other reasons. In addition, the value of the securities or other assets in the Fund's portfolio may change on days or during time periods when shareholders will not be able to purchase or sell the Fund's shares. Authorized Participants who purchase or redeem Fund shares on days when the Fund is holding fair-valued securities may receive fewer or more shares, or lower or higher redemption proceeds, than they would have received had the securities not been fair valued or been valued using a different methodology. The ability to value investments may be impacted by technological issues or errors by pricing services or other third-party service providers.

S-14

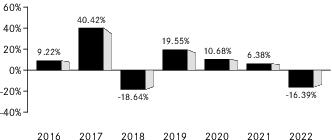

Performance

Information

The bar chart and table that follow show how the Fund has performed on a calendar year basis and provide some indication of the risks of investing in the Fund by showing how the Fund’s average

annual returns for 1 and 5 years and since inception compare with the Underlying Index. Both assume that all dividends and distributions have been reinvested in the Fund. Past performance (before and after taxes) does not necessarily indicate how the Fund will

perform in the future. If BFA had not waived certain Fund fees during certain periods, the Fund's returns would have been lower.

Calendar Year by Year Returns1

1

The Fund’s year-to-date return as of September 30, 2023 was 1.49%.

The best calendar quarter return during the periods

shown above was 16.16% in the 2nd quarter of 2020; the worst was -24.27% in the 1st quarter of 2020.

Updated performance information, including the Fund’s current NAV, may be obtained by visiting our website at www.iShares.com or by calling 1-800-iShares (1-800-474-2737) (toll free).

S-15

Average

Annual Total Returns

(for the periods ended December 31, 2022)

(for the periods ended December 31, 2022)

| |

One Year |

Five Years |

Since

Inception |

| (Inception Date: 12/08/2015) |

|

|

|

| Return Before Taxes |

-16.39% |

-0.86% |

5.42% |

| Return After Taxes on Distributions1

|

-16.96% |

-1.44% |

4.85% |

| Return After Taxes on Distributions and Sale of Fund Shares1

|

-8.94% |

-0.57% |

4.33% |

| MSCI Emerging Markets Diversified Multiple-Factor Index2(Index returns do not reflect deductions for fees, expenses or taxes) |

-15.90% |

-0.34% |

5.96% |

| STOXX Emerging Markets Equity Factor Index2(Index

returns do not reflect deductions for fees, expenses or

taxes) |

N/A |

N/A |

N/A |

1

After-tax returns in the table above are calculated using the historical highest individual

U.S. federal marginal income tax rates and do not reflect the impact of state or local taxes. Actual

after-tax returns depend on an investor’s tax situation and may differ from those shown, and after-tax returns shown are not relevant to tax-exempt investors or investors

who hold shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts

(“IRAs”). Fund returns after taxes on distributions and sales of Fund shares are calculated assuming that an investor has

sufficient capital gains of the same character from other investments to offset any capital losses from the sale of Fund shares. As a result, Fund returns after taxes on distributions and sales of Fund shares may exceed Fund returns before taxes

and/or returns after taxes on distributions.

2

Effective March 1, 2023, the Fund's Underlying Index changed from the MSCI Emerging Markets Diversified Multiple-Factor Index to the STOXX Emerging Markets Equity Factor Index.

S-16

Management

Investment Adviser. BlackRock

Fund Advisors.

Portfolio Managers. Jennifer

Hsui, Greg Savage and Paul Whitehead (the “Portfolio Managers”) are primarily responsible for the day-to-day management of the Fund. Each Portfolio Manager supervises a portfolio management team. Ms. Hsui and Mr. Savage have been Portfolio Managers of the Fund since 2015. Mr. Whitehead has been a Portfolio Manager of the Fund since 2022.

Purchase and Sale of Fund Shares

The Fund is an ETF.

Individual shares of the Fund may only be bought and sold in the secondary market through a

broker-dealer. Because ETF shares trade at market prices rather than at NAV, shares may trade at a price greater than NAV (a premium) or less than NAV (a discount). An investor may incur costs attributable to the difference between the highest price a buyer is willing to pay to purchase shares of the Fund (bid) and the lowest price a seller is willing to accept for shares of the Fund (ask) when buying or selling shares in the secondary market (the “bid-ask spread”).

Tax

Information

The Fund intends to make distributions that may be taxable to you as ordinary income or capital gains, unless you are investing through a tax-deferred arrangement such as a 401(k) plan or an IRA, in which case, your distributions generally will be taxed when withdrawn.

Payments to Broker-Dealers and Other Financial Intermediaries

If you purchase shares of the Fund through a

broker-dealer or other financial intermediary (such as a bank), BFA or other related companies may pay the intermediary for marketing activities and presentations, educational training programs, conferences, the development of technology platforms and reporting systems or other services related to the sale or promotion of the Fund. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

S-17