|

|

| |

(as revised June 1, 2023) |

|

2022 Prospectus |

• iShares Frontier and Select EM ETF | FM | NYSE ARCA

The Securities and Exchange Commission (“SEC”) has not approved or disapproved these securities or passed upon the adequacy of this prospectus. Any representation to the contrary is a criminal offense.

Table of Contents

iShares® and BlackRock® are registered trademarks of BlackRock Fund Advisors and its affiliates.

i

iSHARES® FRONTIER AND SELECT EM ETF

Ticker: FMStock Exchange: NYSE Arca

Investment Objective

The iShares Frontier and Select EM ETF (the “Fund”) seeks to provide exposure to frontier market equities along with select emerging market equities.

Fees and Expenses

The following table describes the fees and expenses that you will incur if you buy, hold and sell shares of the Fund. The investment advisory agreement between iShares, Inc. (the “Company”) and BlackRock Fund Advisors (“BFA”) (the “Investment Advisory Agreement”) provides that BFA will pay all operating expenses of the Fund, except: (i) the management fees, (ii) interest expenses, (iii) taxes, (iv) expenses incurred with respect to the acquisition and disposition of portfolio securities and the execution of portfolio transactions, including brokerage commissions, (v) distribution fees or expenses, and (vi) litigation expenses and any extraordinary expenses.

You may pay other fees, such as brokerage commissions and other fees to financial intermediaries, which are not reflected in the tables and examples below.

| Annual Fund Operating Expenses | |||

| Management Fees |

Distribution and Service (12b-1) Fees |

Other Expenses |

Total Annual Fund Operating Expenses |

| |

|

|

|

| 1 Year |

3 Years |

5 Years |

10 Years |

| $ |

$ |

$ |

$ |

S-1

Principal Investment Strategies

The Fund seeks to achieve its investment objective by investing, under normal circumstances, at least 80% of the value of its net assets, plus the amount of any borrowings for investment purposes, in equity securities of issuers economically tied to frontier markets and issuers economically tied to emerging markets, or in depositary receipts representing such securities.

Frontier markets are those markets that are considered to be among the smallest, least mature and least liquid investable equity markets. Additionally, the emerging markets in which the Fund seeks to invest are those markets selected from the lower size spectrum of emerging markets (i.e., emerging market countries with lower gross national income per capita and total stock market capitalizations relative to those of the full spectrum of emerging market countries). For this purpose, frontier markets and select emerging markets include, but are not limited to, the markets included in the MSCI Frontier and Emerging Markets Select

Index (the “Benchmark”). As of May 15, 2023, the Benchmark consisted of securities in the following countries or regions: Bahrain, Bangladesh, Colombia, Egypt, Estonia, Jordan, Kazakhstan, Kenya, Lithuania, Morocco, Nigeria, Oman, Pakistan, Peru, the Philippines, Romania, Slovenia, Sri Lanka and Vietnam. To the extent that markets restrict or delay repatriation of the applicable local currency, the Fund may choose not to invest in, or limit their investments in, such markets.

The Fund is an actively managed exchange-traded fund (“ETF”) and does not seek to replicate the performance of a specified index. In selecting investments for the Fund, BFA uses optimization techniques relative to the Benchmark in order to provide exposure to frontier markets and select emerging markets while taking into account, among other things, regulatory requirements, market limitations, and repatriation restrictions as determined by BFA. As a result of the optimization techniques, the performance of the Fund may materially differ from that of the Benchmark.

The Fund may also invest in other securities and instruments, including but not limited to, certain futures, options and swap contracts, cash and cash equivalents, including shares of money market funds advised by BFA or its affiliates. In certain situations or market conditions, the Fund may temporarily depart from its normal investment process, provided that the alternative, in the opinion of BFA, is consistent with the Fund’s investment objective and is in the best interest of the Fund.

The Fund may lend securities representing up to one-third of the value of the Fund’s total assets (including the value of any collateral received).

S-2

Summary of Principal Risks

Asset Class Risk. Securities and other assets in the Fund's portfolio may underperform in comparison to the general financial markets, a particular financial market or other asset classes.

Authorized Participant Concentration Risk. Only an Authorized Participant (as defined in the Creations and Redemptions section of this prospectus (the “Prospectus”)) may engage in creation or redemption transactions directly with the Fund, and none of those Authorized Participants is obligated to engage in creation and/or redemption transactions. The Fund has a limited number of institutions that may act as Authorized Participants on an agency basis (i.e., on behalf of other market participants). To the extent that Authorized Participants exit the business or are unable to proceed with creation or redemption orders with respect to the Fund and no other Authorized Participant is able to step forward to create or redeem, Fund shares may be more likely to trade at a premium or discount to NAV and possibly face trading halts or delisting. Authorized Participant concentration risk may be heightened for exchange-traded funds (“ETFs”), such as the Fund,

that invest in securities issued by non-U.S. issuers or other securities or instruments that have lower trading volumes.

Commodity Risk. The Fund invests in companies that are susceptible to fluctuations in certain commodity markets and to price changes due to trade relations. Any negative changes in commodity markets that may be due to changes in supply and demand for commodities, market events, war, regulatory developments, other catastrophic events, or other factors that the Fund cannot control could have an adverse impact on those companies.

Concentration Risk. The Fund may be susceptible to an increased risk of loss, including losses due to adverse events that affect the Fund’s investments more than the market as a whole, to the extent that the Fund's investments are concentrated in the securities and/or other assets of a particular issuer or issuers, country, group of countries, region, market, industry, group of industries, sector, market segment or asset class.

Currency Risk. Because the Fund's NAV is determined in U.S. dollars, the Fund's NAV could decline if the currency of a non-U.S. market in which the Fund invests depreciates against the U.S. dollar or if there are delays or limits on repatriation of such currency. Currency exchange rates can be very volatile and can change quickly and unpredictably. As a result, the Fund's NAV may change quickly and without warning.

Custody Risk. Less developed securities markets are more likely to experience problems with the clearing and settling of trades, as well as the holding of securities by local banks, agents and depositories.

S-3

Cybersecurity Risk. Failures or breaches of the electronic systems of the Fund, the Fund's adviser, distributor, the benchmark provider and other service providers, market makers, Authorized Participants or the issuers of securities in which the Fund invests have the ability to cause disruptions, negatively impact the Fund’s business operations and/or potentially result in financial losses to the Fund and its shareholders. While the Fund has established business continuity plans and risk management systems seeking to address system breaches or failures, there are inherent limitations in such plans and systems. Furthermore, the Fund cannot control the cybersecurity plans and systems of the Fund’s benchmark provider and other service providers, market makers, Authorized Participants or issuers of securities in which the Fund invests.

Dividend-Paying Stock Risk. Investing in dividend-paying stocks involves the risk that such stocks may fall out of favor with investors and underperform the broader market. Companies that issue dividend-paying stocks are not required to pay or continue paying dividends on such stocks. It is possible that issuers of the stocks held by the Fund will not declare dividends in the future or will reduce or eliminate the payment of dividends (including reducing or eliminating anticipated accelerations or increases in the payment of dividends) in the future.

Equity Securities Risk. Equity securities are subject to changes in value, and their values may be more volatile than those of other asset classes. Common stocks generally subject their holders to more risks than preferred stocks and debt securities because common stockholders’ claims

are subordinated to those of holders of preferred stocks and debt securities upon the bankruptcy of the issuer.

Financials Sector Risk. Performance of companies in the financials sector may be adversely impacted by many factors, including, among others, changes in government regulations, economic conditions, and interest rates, credit rating downgrades, and decreased liquidity in credit markets. The extent to which the Fund may invest in a company that engages in securities-related activities or banking is limited by applicable law. The impact of changes in capital requirements and recent or future regulation of any individual financial company, or of the financials sector as a whole, cannot be predicted. Cybersecurity incidents and technology malfunctions and failures have become increasingly frequent and have caused significant losses to companies in this sector, which may negatively impact the Fund.

Geographic Risk. A natural disaster could occur in a geographic region in which the Fund invests, which could adversely affect the economy or the business operations of companies in the specific geographic region, causing an adverse impact on the Fund's investments in, or which are exposed to, the affected region.

Illiquid Investments Risk. The Fund may not acquire any illiquid investment if, immediately after the acquisition, the Fund would have invested more than 15% of its net assets in illiquid investments. An illiquid investment is any investment that the Fund reasonably expects cannot be sold or disposed of in current market conditions in seven calendar days or less without significantly changing the

S-4

market value of the investment. To the extent the Fund holds illiquid investments, the illiquid investments may reduce the returns of the Fund because the Fund may be unable to transact at advantageous times or prices. In addition, if the Fund is limited in its ability to sell illiquid investments during periods when shareholders are redeeming their shares, the Fund will need to sell liquid securities to meet redemption requests and illiquid securities will become a larger portion of the Fund’s holdings. During periods of market volatility, liquidity in the market for the Fund’s shares may be impacted by the liquidity in the market for the underlying securities or instruments held by the Fund, which could lead to the Fund’s shares trading at a premium or discount to the Fund’s NAV.

Infectious Illness Risk. A widespread outbreak of an infectious illness, such as the COVID-19 pandemic, may result in travel restrictions, disruption of healthcare services, prolonged quarantines, cancellations, supply chain disruptions, business closures, lower consumer demand, layoffs, ratings downgrades, defaults and other significant economic, social and political impacts. Markets may experience temporary closures, extreme volatility, severe losses, reduced liquidity and increased trading costs. Such events may adversely affect the Fund and its investments and may impact the Fund’s ability to purchase or sell securities or cause elevated tracking error and increased premiums or discounts to the Fund's NAV. Despite the development of vaccines, the duration of the COVID-19 pandemic and its effects cannot be predicted with certainty.

Issuer Risk. The performance of the Fund depends on the performance of

individual securities to which the Fund has exposure. Changes in the financial condition or credit rating of an issuer of those securities may cause the value of the securities to decline.

Large-Capitalization Companies Risk. Large-capitalization companies may be less able than smaller capitalization companies to adapt to changing market conditions. Large-capitalization companies may be more mature and subject to more limited growth potential compared with smaller capitalization companies. During different market cycles, the performance of large-capitalization companies has trailed the overall performance of the broader securities markets.

Large Shareholder and Large-Scale Redemption Risk. Certain shareholders, including an Authorized Participant, a third-party investor, the Fund’s adviser or an affiliate of the Fund’s adviser, a market maker, or another entity, may from time to time own or manage a substantial amount of Fund shares, or may invest in the Fund and hold their investment for a limited period of time. There can be no assurance that any large shareholder or large group of shareholders would not redeem their investment. Redemptions of a large number of Fund shares could require the Fund to dispose of assets to meet the redemption requests, which can accelerate the realization of taxable income and/or capital gains and cause the Fund to make taxable distributions to its shareholders earlier than the Fund otherwise would have. In addition, under certain circumstances, non-redeeming shareholders may be treated as receiving a disproportionately large taxable distribution during or with respect to such year. In some circumstances, the Fund may hold a

S-5

relatively large proportion of its assets in cash in anticipation of large redemptions, diluting its investment returns. These large redemptions may also force the Fund to sell portfolio securities when it might not otherwise do so, which may negatively impact the Fund’s NAV, increase the Fund’s brokerage costs and/or have a material effect on the market price of the Fund shares.

Management Risk. The Fund is subject to management risk, which is the risk that the investment process, techniques and risk analyses applied by BFA will not produce the desired results, and that securities selected by BFA may underperform the market or any relevant benchmark. In addition, legislative, regulatory, or tax developments may affect the investment techniques available to BFA in connection with managing the Fund and may also adversely affect the ability of the Fund to achieve its investment objective.

Market Risk. The Fund could lose money over short periods due to short-term market movements and over longer periods during more prolonged market downturns. The countries in which the Fund invests may be subject to considerable degrees of economic, political and social instability. Local, regional or global events such as war, acts of terrorism, the spread of infectious illness or other public health issues, recessions, or other events could have a significant impact on the Fund and its investments and could result in increased premiums or discounts to the Fund’s NAV.

Market Trading Risk. The Fund faces numerous market trading risks, including the potential lack of an active

market for Fund shares, losses from trading in secondary markets, periods of high volatility and disruptions in the creation/redemption process. ANY OF THESE FACTORS, AMONG OTHERS, MAY LEAD TO THE FUND'S SHARES TRADING AT A PREMIUM OR DISCOUNT TO NAV.

Mid-Capitalization Companies Risk. Compared to large-capitalization companies, mid-capitalization companies may be less stable and more susceptible to adverse developments. In addition, the securities of mid-capitalization companies may be more volatile and less liquid than those of large-capitalization companies.

National Closed Market Trading Risk. To the extent that the underlying securities and/or other assets held by the Fund trade on foreign exchanges or in foreign markets that may be closed when the securities exchange on which the Fund’s shares trade is open, there are likely to be deviations between the current price of such an underlying security and the last quoted price for the underlying security (i.e., the Fund’s quote from the closed foreign market). The impact of a closed foreign market on the Fund is likely to be greater where a large portion of the Fund’s underlying securities and/or other assets trade on that closed foreign market or when the foreign market is closed for unscheduled reasons. These deviations could result in premiums or discounts to the Fund’s NAV that may be greater than those experienced by other ETFs.

Non-U.S. Securities Risk. Investments in the securities of non-U.S. issuers are subject to the risks associated with investing in those non-U.S. markets, such as heightened risks of inflation or

S-6

nationalization. The Fund may lose money due to political, economic and geographic events affecting issuers of non-U.S. securities or non-U.S. markets. In addition, non-U.S. securities markets may trade a small number of securities and may be unable to respond effectively to changes in trading volume, potentially making prompt liquidation of holdings difficult or impossible at times. The Fund is specifically exposed to African Economic Risk and Asian Economic Risk.

Operational Risk. The Fund is exposed to operational risks arising from a number of factors, including, but not limited to, human error, processing and communication errors, errors of the Fund’s service providers, counterparties or other third parties, failed or inadequate processes and technology or systems failures. The Fund and BFA seek to reduce these operational risks through controls and procedures. However, these measures do not address every possible risk and may be inadequate to address significant operational risks.

Privatization Risk. Some countries in which the Fund invests have privatized, or have begun the process of privatizing, certain entities and industries. Privatized entities may lose money or be re-nationalized.

Reliance on Trading Partners Risk. The Fund invests in countries or regions whose economies are heavily dependent upon trading with key partners. Any reduction in this trading may have an adverse impact on the Fund's investments. Through its holdings of securities of certain issuers, the Fund is specifically exposed to African Economic Risk, Asian

Economic Risk, European Economic Risk and Middle Eastern Economic Risk.

Risk of Investing in Emerging Markets. Investments in emerging market issuers may be subject to a greater risk of loss than investments in issuers located or operating in more developed markets. Emerging markets may be more likely to experience inflation, political turmoil and rapid changes in economic conditions than more developed markets. Companies in many emerging markets are not subject to the same degree of regulatory requirements, accounting standards or auditor oversight as companies in more developed countries, and as a result, information about the securities in which the Fund invests may be less reliable or complete. Emerging markets often have less reliable securities valuations and greater risk associated with custody of securities than developed markets. There may be significant obstacles to obtaining information necessary for investigations into or litigation against companies and shareholders may have limited legal remedies.

Risk of Investing in Frontier Markets. Frontier markets are those emerging markets that are considered to be among the smallest, least mature and least liquid, and as a result, may be more likely to experience inflation, political turmoil and rapid changes in economic conditions than more developed and traditional emerging markets. Investments in frontier markets may be subject to a greater risk of loss than investments in more developed and traditional emerging markets. Frontier markets often have less uniformity in accounting and reporting requirements, unreliable

S-7

securities valuations and greater risk associated with custody of securities. Economic, political, illiquidity and currency risks may be more pronounced with respect to investments in frontier markets than in emerging markets.

Risk of Investing in Vietnam. Investments in Vietnamese issuers involve risks that are specific to Vietnam, including legal, regulatory, political and economic risks.

Securities Lending Risk. The Fund may engage in securities lending. Securities lending involves the risk that the Fund may lose money because the borrower of the loaned securities fails to return the securities in a timely manner or at all. The Fund could also lose money in the event of a decline in the value of collateral provided for loaned securities or a decline in the value of any investments made with cash collateral. These events could also trigger adverse tax consequences for the Fund.

Security Risk. Some countries and regions in which the Fund invests have experienced security concerns, such as war, terrorism and strained international relations. Incidents involving a country's or region's security may cause uncertainty in its markets and may adversely affect its economy and the Fund's investments.

Small-Capitalization Companies Risk. Compared to mid- and large-

capitalization companies, small-capitalization companies may be less stable and more susceptible to adverse developments. In addition, the securities of small-capitalization companies may be more volatile and less liquid than those of mid- and large-capitalization companies.

Valuation Risk. The price the Fund could receive upon the sale of a security or other asset may differ from the Fund's valuation of the security or other asset, particularly for securities or other assets that trade in low volume or volatile markets or that are valued using a fair value methodology as a result of trade suspensions or for other reasons. In addition, the value of the securities or other assets in the Fund's portfolio may change on days or during time periods when shareholders will not be able to purchase or sell the Fund's shares. Authorized Participants who purchase or redeem Fund shares on days when the Fund is holding fair-valued securities may receive fewer or more shares, or lower or higher redemption proceeds, than they would have received had the securities not been fair valued or been valued using a different methodology. The ability to value investments may be impacted by technological issues or errors by pricing services or other third-party service providers.

S-8

Performance Information

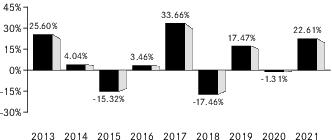

Year by Year Returns1 (Years Ended December 31)

1

The best calendar quarter return during the periods shown above was 12.25 % in the 2nd quarter of 2021 ; the worst was -26.85 % in the 1st quarter of 2020 .

Updated performance information, including the Fund’s current NAV, may be obtained by visiting our website at www.iShares.com or by calling 1-800-iShares (1-800-474-2737) (toll free) .

S-9

Average Annual Total Returns

(for the periods ended December 31, 2021)

(for the periods ended December 31, 2021)

| |

One Year |

Five Years |

Since Fund Inception |

| (Inception Date: |

|

|

|

| Return Before Taxes |

|

|

|

| Return After Taxes on Distributions1 |

|

|

|

| Return After Taxes on Distributions and Sale of Fund Shares1 |

|

|

|

| MSCI Frontier and Emerging Markets Select Index2 (Index returns do not reflect deductions for fees, expenses or taxes) |

|

|

|

1

2

S-10

Management

Investment Adviser. BlackRock Fund Advisors.

Portfolio Managers. Jennifer Hsui, Greg Savage and Paul Whitehead (the “Portfolio Managers”) are primarily responsible for the day-to-day management of the Fund. Each Portfolio Manager supervises a portfolio management team. Ms. Hsui and Mr. Savage have been Portfolio Managers of the Fund since 2012. Mr. Whitehead has been a Portfolio Manager of the Fund since 2022.

Purchase and Sale of Fund Shares

The Fund is an ETF. Individual shares of the Fund may only be bought and sold in the secondary market through a broker-dealer. Because ETF shares trade at market prices rather than at NAV, shares may trade at a price greater than NAV (a premium) or less than NAV (a discount). An investor may incur costs attributable to the difference between the highest price a buyer is willing to pay to purchase shares of the Fund (bid) and the lowest price a seller is willing to accept for shares of the Fund (ask) when buying or selling shares in the secondary market (the “bid-ask spread”).

Tax Information

The Fund intends to make distributions that may be taxable to you as ordinary income or capital gains, unless you are investing through a tax-deferred arrangement such as a 401(k) plan or an IRA, in which case, your distributions generally will be taxed when withdrawn.

Payments to Broker-Dealers and Other Financial Intermediaries

If you purchase shares of the Fund through a broker-dealer or other financial intermediary (such as a bank), BFA or other related companies may pay the intermediary for marketing activities and presentations, educational training programs, conferences, the development of technology platforms and reporting systems or other services related to the sale or promotion of the Fund. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

S-11

More Information About the Fund

This Prospectus contains important information about investing in the Fund. Please read this Prospectus carefully before you make any investment decisions. Additional information regarding the Fund is available at www.iShares.com.

On June 1, 2023, the name of the Fund changed from the iShares MSCI Frontier and Select EM ETF to the iShares Frontier and Select EM ETF. The Fund is an actively managed ETF and, thus, does not seek to replicate the performance of a specified index. Accordingly, the management team has discretion on a daily basis to manage the Fund’s portfolio in accordance with the Fund’s investment objective.

BFA is the investment adviser to the Fund. Shares of the Fund are listed for trading on NYSE Arca, Inc. (“NYSE Arca”). The market price for a share of the Fund may be different from the Fund’s most recent NAV.

ETFs are funds that trade like other publicly traded securities. Similar to shares of a mutual fund, each share of the Fund represents an ownership interest in an underlying portfolio of securities and other instruments. Unlike shares of a mutual fund, which can be bought and redeemed from the issuing fund by all shareholders at a price based on NAV, shares of the Fund may be purchased or redeemed directly from the Fund at NAV solely by Authorized Participants and only in aggregations of a specified number of shares (“Creation Units”). Also unlike shares of a mutual fund, shares of the Fund are listed on a national securities exchange and trade in the secondary market at market prices that change throughout the day.

The Fund invests in a particular segment of the securities markets that is not representative of the market as a whole. The Fund is designed to be used as part of broader asset allocation strategies. Accordingly, an investment in the Fund should not constitute a complete investment program.

Additional Information on Principal Investment Strategies.

The Fund seeks to achieve its investment objective by investing, under normal circumstances, at least 80% of the value of its net assets, plus the amount of any borrowings for investment purposes, in equity securities of issuers economically tied to frontier markets and issuers economically tied to emerging markets, or in depositary receipts representing such securities.

Frontier markets are those markets that are considered to be among the smallest, least mature and least liquid investable equity markets. Additionally, the emerging markets in which the Fund seeks to invest are those markets selected from the lower size spectrum of emerging markets (i.e.,emerging market countries with lower gross national income per capita and total stock market capitalizations relative to those of the full spectrum of emerging market countries). For this purpose, frontier markets and select emerging markets include, but are not limited to, the markets included in the Benchmark. As of May 15, 2023, the Benchmark consisted of securities in the following countries or regions: Bahrain, Bangladesh, Colombia, Egypt, Estonia, Jordan, Kazakhstan, Kenya, Lithuania, Morocco, Nigeria, Oman, Pakistan, Peru, the Philippines,

1

Romania, Slovenia, Sri Lanka and Vietnam. To the extent that markets restrict or delay repatriation of the applicable local currency, the Fund may choose not to invest in, or limit their investments in, such markets.

The Fund is an actively managed ETF and does not seek to replicate the performance of a specified index. In selecting investments for the Fund, BFA uses optimization techniques relative to the Benchmark in order to provide exposure to frontier markets and select emerging markets while taking into account, among other things, regulatory requirements, market limitations, and repatriation restrictions as determined by BFA. As a result of the optimization techniques, the performance of the Fund may materially differ from that of the Benchmark.

The Fund may also invest in other securities, including but not limited to, cash and cash equivalents, including shares of money market funds advised by BFA or its affiliates. In certain situations or market conditions, the Fund may temporarily depart from its normal investment process, provided that the alternative, in the opinion of BFA, is consistent with the Fund’s investment objective and is in the best interest of the Fund.

The Fund may lend securities representing up to one-third of the value of the Fund’s total assets (including the value of any collateral received).

The Fund has no stated minimum holding period for investments and may buy or sell securities whenever Fund management sees an appropriate opportunity in accordance with the Fund's investment objective. An investment in the Fund is not a bank deposit and it is not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency, BFA or any of its affiliates.

The Fund's investment objective is a non-fundamental policy and may be changed without shareholder approval.

The Fund has not been categorized under the European Union (“EU”) sustainable finance disclosure regulation (“SFDR”) as an “Article 8” or “Article 9” product. In addition, the Fund’s investment strategy does not take into account the criteria for environmentally sustainable economic activities under the EU sustainable investment taxonomy regulation or principal adverse impacts (“PAIs”) on sustainability factors under the SFDR. PAIs are identified under the SFDR as the material impacts of investment decisions on sustainability factors relating to environmental, social and employee matters, respect for human rights, and anti-corruption and anti-bribery matters.

A Further Discussion of Principal Risks

The Fund is subject to various risks, including the principal risks noted below, any of which may adversely affect the Fund’s NAV, trading price, yield, total return and ability to meet its investment objective. You could lose all or part of your investment in the Fund, and the Fund could underperform other investments. The order of the below risk factors does not indicate the significance of any particular risk factor. The Fund discloses its portfolio holdings daily at www.iShares.com.

African Economic Risk. Investing in the economies of African countries involves risks not typically associated with investments in securities of issuers in more developed

2

economies, countries or geographic regions that may negatively affect the value of investments in the Fund. Such heightened risks include, among others, expropriation and/or nationalization of assets, restrictions on and government intervention in international trade, confiscatory taxation, imposition of capital controls and delays or limits on repatriation of local currency, political instability, including authoritarian and/or military involvement in governmental decision making, armed conflict, civil war, and social instability as a result of religious, ethnic and/or socioeconomic unrest or widespread outbreaks of disease.

The securities markets in Africa are underdeveloped and are often considered to be less correlated to global economic cycles than markets located in more developed economies, countries or geographic regions. Securities markets in African countries are subject to greater risks associated with market volatility, lower market capitalization, lower trading volume, illiquidity, inflation, greater price fluctuations, uncertainty regarding the existence of trading markets, governmental control and heavy regulation of labor and industry. Moreover, trading on African securities markets may be suspended altogether.

Certain governments in African countries may restrict or control to varying degrees the ability of foreign investors to invest in securities of issuers located or operating in those countries. Moreover, certain countries in Africa may require governmental approval or special licenses prior to investment by foreign investors; may limit the amount of investment by foreign investors in a particular industry and/or issuer; may limit such foreign investment to a certain class of securities of an issuer that may have less advantageous rights than the classes available for purchase by domestic investors of those countries; and/or may impose additional taxes on foreign investors. These factors, among others, make investing in issuers located or operating in countries in Africa significantly riskier than investing in issuers located or operating in more developed countries.

Asian Economic Risk. Many Asian economies have experienced rapid growth and industrialization in recent years, but there is no assurance that this growth rate will be maintained. Other Asian economies, however, have experienced high inflation, high unemployment, currency devaluations and restrictions, and over-extension of credit. Geopolitical hostility, political instability, and economic or environmental events in any one Asian country may have a significant economic effect on the entire Asian region, as well as on major trading partners outside Asia. Any adverse event in the Asian markets may have a significant adverse effect on some or all of the economies of the countries in which the Fund invests. In particular, China is a key trading partner of many Asian countries and any changes in trading relationships between China and other Asian countries may affect the region as a whole. Many Asian countries are subject to political risk, including political instability, corruption and regional conflict with neighboring countries. North Korea and South Korea each have substantial military capabilities, and historical tensions between the two countries present the risk of war. Escalated tensions involving the two countries and any outbreak of hostilities between the two countries, or even the threat of an outbreak of hostilities, could have a severe adverse effect on the entire Asian region. Certain Asian countries have developed increasingly strained relationships with the U.S. or with China, and if these

3

relations were to worsen, they could adversely affect Asian issuers that rely on the U.S. or China for trade. In addition, many Asian countries are subject to social and labor risks associated with demands for improved political, economic and social conditions. These risks, among others, may adversely affect the value of the Fund's investments.

Asset Class Risk. The securities and other assets in the Fund’s portfolio may underperform in comparison to other securities or indexes that track other issuers, countries, groups of countries, regions, industries, groups of industries, markets, market segments, asset classes or sectors. Various types of securities may experience cycles of outperformance and underperformance in comparison to the general financial markets depending upon a number of factors including, among other things, inflation, interest rates, productivity, global demand for local products or resources, and regulation and governmental controls. This may cause the Fund to underperform other investment vehicles that invest in different asset classes.

Authorized Participant Concentration Risk. Only an Authorized Participant may engage in creation or redemption transactions directly with the Fund, and none of those Authorized Participants is obligated to engage in creation and/or redemption transactions. The Fund has a limited number of institutions that may act as Authorized Participants on an agency basis (i.e., on behalf of other market participants). To the extent that Authorized Participants exit the business or are unable to proceed with creation or redemption orders with respect to the Fund and no other Authorized Participant is able to step forward to create or redeem Creation Units, Fund shares may be more likely to trade at a premium or discount to NAV and possibly face trading halts or delisting. Authorized Participant concentration risk may be heightened because ETFs, such as the Fund, that invest in securities issued by non-U.S. issuers or other securities or instruments that are less widely traded often involve greater settlement and operational issues and capital costs for Authorized Participants, which may limit the availability of Authorized Participants.

Commodity Risk. The energy, materials, and agriculture sectors account for a large portion of the exports of certain countries in which the Fund invests. Any changes in these sectors or fluctuations in the commodity markets could have an adverse impact on a country’s economy. Commodity prices may be influenced or characterized by unpredictable factors, including, where applicable, high volatility, changes in supply and demand relationships, weather (including physical changes as a result of climate change), agriculture, the transition to low carbon alternatives or clean energy, trade, pestilence, political instability, war, catastrophic events, changes in interest rates and monetary and other governmental policies, action and inaction, including price changes due to trade relations, as well as social or governance factors. Securities of companies held by the Fund that are dependent on a single commodity, or are concentrated in a single commodity sector, may typically exhibit even higher volatility attributable to commodity prices.

Concentration Risk. The Fund may be susceptible to an increased risk of loss, including losses due to adverse events that affect the Fund’s investments more than the market as a whole, to the extent that the Fund's investments are concentrated in the securities and/or other assets of a particular issuer or issuers, country, group of countries, region, market, industry, group of industries, sector, market segment or

4

asset class. The Fund may be more adversely affected by the underperformance of those securities and/or other assets, may experience increased price volatility and may be more susceptible to adverse economic, market, political, sustainability-related or regulatory occurrences affecting those securities and/or other assets than a fund that does not concentrate its investments.

Currency Risk. Because the Fund's NAV is determined on the basis of the U.S. dollar, investors may lose money if the currency of a non-U.S. market in which the Fund invests depreciates against the U.S. dollar or if there are delays or limits on repatriation of such currency, even if such currency value of the Fund's holdings in that market increases. Currency exchange rates can be very volatile and can change quickly and unpredictably. As a result, the Fund’s NAV may change quickly and without warning.

Custody Risk. Custody risk refers to the risks inherent in the process of clearing and settling trades, as well as the holding of securities by local banks, agents and depositories. Low trading volumes and volatile prices in less developed markets may make trades harder to complete and settle, and governments or trade groups may compel local agents to hold securities in designated depositories that may not be subject to independent evaluation. Local agents are held only to the standards of care of their local markets. In general, the less developed a country’s securities markets are, the higher the degree of custody risk.

Cybersecurity Risk. The Fund, Authorized Participants, service providers and the relevant listing exchange are susceptible to operational, information security and related “cyber” risks both directly and through their service providers. Similar types of cybersecurity risks are also present for issuers of securities in which the Fund invests, which could result in material adverse consequences for such issuers and may cause the Fund’s investment in such issuers to lose value. In general, cyber incidents can result from deliberate attacks or unintentional events. Cyber incidents include, but are not limited to, gaining unauthorized access to digital systems (e.g., through “hacking” or malicious software coding) for purposes of misappropriating assets or sensitive information, corrupting data, or causing operational disruption. Cyberattacks may also be carried out in a manner that does not require gaining unauthorized access, such as causing denial-of-service attacks on websites (i.e., efforts to make network services unavailable to intended users). Recently, geopolitical tensions may have increased the scale and sophistication of deliberate attacks, particularly those from nation-states or from entities with nation-state backing.

Cybersecurity failures by, or breaches of, the systems of the Fund's adviser, distributor and other service providers (including, but not limited to, index and benchmark providers, fund accountants, custodians, transfer agents and administrators), market makers, Authorized Participants or the issuers of securities in which the Fund invests have the ability to cause disruptions and impact business operations, potentially resulting in: financial losses, interference with the Fund’s ability to calculate its NAV, disclosure of confidential trading information, impediments to trading, submission of erroneous trades or erroneous creation or redemption orders, the inability of the Fund or its service providers to transact business, violations of applicable privacy and other laws, regulatory fines, penalties, reputational damage, reimbursement or other

5

compensation costs, or additional compliance costs. In addition, cyberattacks may render records of Fund assets and transactions, shareholder ownership of Fund shares, and other data integral to the functioning of the Fund inaccessible, inaccurate or incomplete. Substantial costs may be incurred by the Fund in order to resolve or prevent cyber incidents in the future. While the Fund has established business continuity plans in the event of, and risk management systems to prevent, such cyber incidents, there are inherent limitations in such plans and systems, including the possibility that certain risks have not been identified, that prevention and remediation efforts will not be successful or that cyberattacks will go undetected. Furthermore, the Fund cannot control the cybersecurity plans and systems put in place by service providers to the Fund, issuers in which the Fund invests, market makers or Authorized Participants. The Fund and its shareholders could be negatively impacted as a result.

Dividend-Paying Stock Risk. Investing in dividend-paying stocks involves the risk that such stocks may fall out of favor with investors and underperform the broader market. Companies that issue dividend-paying stocks are not required to pay or continue paying dividends on such stocks. It is possible that issuers of the stocks held by the Fund will not declare dividends in the future or will reduce or eliminate the payment of dividends (including reducing or eliminating anticipated accelerations or increases in the payment of dividends) in the future.

Equity Securities Risk. The Fund invests in equity securities, which are subject to changes in value that may be attributable to market perception of a particular issuer or to general stock market fluctuations that affect all issuers. Investments in equity securities may be more volatile than investments in other asset classes. Holders of common stocks, which generally subject their holders to more risks than preferred stocks and debt securities because common stockholders' claims are subordinated to those of holders of preferred stocks and debt securities upon the bankruptcy of the issuer.

European Economic Risk. The Economic and Monetary Union (the “eurozone”) of the EU requires compliance by member states that are members of the eurozone with restrictions on inflation rates, deficits, interest rates and debt levels, as well as fiscal and monetary controls, each of which may significantly affect every country in Europe, including those countries that are not members of the eurozone. Additionally, European countries outside of the eurozone may present economic risks that are independent of the indirect effects that eurozone policies have on them. In particular, the United Kingdom's (the “U.K.”) economy may be affected by global economic, industrial and financial shifts. Changes in imports or exports, changes in governmental or EU regulations on trade, changes in the exchange rate of the euro (the common currency of eurozone countries), the default or threat of default by an EU member state on its sovereign debt and/or an economic recession in an EU member state may have a significant adverse effect on the economies of other EU member states and their trading partners. The European financial markets have historically experienced volatility and adverse trends due to concerns about economic downturns or government debt levels in several European countries, including, but not limited to, Austria, Belgium, Cyprus, France, Greece, Ireland, Italy, Portugal, Spain and Ukraine.

6

These events have affected and may in the future adversely affect the exchange rate of the euro and may significantly affect European countries.

Responses to financial problems by European governments, central banks and others, including austerity measures and reforms, may not produce the desired results, may result in social unrest, may limit future growth and economic recovery or may have other unintended consequences. Further defaults or restructurings by governments and other entities of their debt could have additional adverse effects on economies, financial markets and asset valuations around the world. In addition, one or more countries may abandon the euro and/or withdraw from the EU. The U.K. left the EU (“Brexit”) on January 31, 2020. The U.K. and EU reached an agreement on the terms of their future trading relationship effective January 1, 2021, which principally relates to the trading of goods rather than services, including financial services. Further discussions are to be held between the U.K. and the EU in relation to matters not covered by the trade agreement, such as financial services. The Fund faces risks associated with the potential uncertainty and consequences that may follow Brexit, including with respect to volatility in exchange rates and interest rates. Brexit could adversely affect European or worldwide political, regulatory, economic or market conditions and could contribute to instability in global political institutions, regulatory agencies and financial markets. Brexit has also led to legal uncertainty and could lead to politically divergent national laws and regulations as a new relationship between the U.K. and EU is defined and the U.K. determines which EU laws to replace or replicate. Any of these effects could adversely affect any of the companies to which the Fund has exposure and any other assets in which the Fund invests. The political, economic and legal consequences of Brexit are not yet fully known. In the short term, financial markets may experience heightened volatility, particularly those in the U.K. and Europe, but possibly worldwide. The U.K. and Europe may be less stable than they have been in recent years, and investments in the U.K. and the EU may be difficult to value or subject to greater or more frequent volatility. In the longer term, there is likely to be a period of significant political, regulatory and commercial uncertainty as the U.K. continues to negotiate the terms of its future trading relationships.

Secessionist movements, such as the Catalan movement in Spain and the independence movement in Scotland, as well as governmental or other responses to such movements, may also create instability and uncertainty in the region. In addition, the national politics of countries in the EU have been unpredictable and subject to influence by disruptive political groups and ideologies. The governments of EU countries may be subject to change and such countries may experience social and political unrest. Unanticipated or sudden political or social developments may result in sudden and significant investment losses. The occurrence of terrorist incidents throughout Europe or war in the region could also impact financial markets. The impact of these events is not clear but could be significant and far-reaching and could adversely affect the value and liquidity of the Fund's investments.

Russian Invasion of Ukraine. Russia launched a large-scale invasion of Ukraine on February 24, 2022. The extent and duration of the military action, resulting sanctions and resulting future market disruptions, including declines in its stock markets and the value of the ruble against the U.S. dollar, are impossible to predict, but could be

7

significant. Disruptions caused by Russian military action or other actions (including cyberattacks and espionage) or resulting actual and threatened responses to such activity, including purchasing and financing restrictions, boycotts or changes in consumer or purchaser preferences, sanctions, import and export restrictions, tariffs or cyberattacks on the Russian government, Russian companies or Russian individuals, including politicians, may impact Russia's economy and Russian issuers of securities in which the Fund invests. Actual and threatened responses to Russian military action may also impact the markets for certain Russian commodities, such as oil and natural gas, as well as other sectors of the Russian economy, and are likely to have collateral impacts on such sectors globally.

Financials Sector Risk. Companies in the financials sector of an economy are subject to extensive governmental regulation and intervention, which may adversely affect the scope of their activities, the prices they can charge, the amount of capital they must maintain and, potentially, their size. The extent to which the Fund may invest in a company that engages in securities-related activities or banking is limited by applicable law. Governmental regulation may change frequently and may have significant adverse consequences for companies in the financials sector, including effects not intended by such regulation. Increased risk taking by banks may also result in greater overall risk in the U.S. and global financials sector. The impact of changes in capital requirements, or recent or future regulation in various countries, on any individual financial company or on the financials sector as a whole cannot be predicted.

Certain risks may impact the value of investments in the financials sector more severely than those of investments outside this sector, including the risks associated with companies that operate with substantial financial leverage. Companies in the financials sector are exposed directly to the credit risk of their borrowers and counterparties, who may be leveraged to an unknown degree, including through swaps and other derivatives products. Financial services companies may have significant exposure to the same borrowers and counterparties, with the result that a borrower’s or counterparty’s inability to meet its obligations to one company may affect other companies with exposure to the same borrower or counterparty. This interconnectedness of risk may result in significant negative impacts to companies with direct exposure to the defaulting counterparty as well as adverse cascading effects in the markets and the financials sector generally. Companies in the financials sector may also be adversely affected by increases in interest rates and loan losses, decreases in the availability of money or asset valuations, credit rating downgrades and adverse conditions in other related markets. Insurance companies, in particular, may be subject to severe price competition and/or rate regulation, which may have an adverse impact on their profitability. The financials sector is particularly sensitive to fluctuations in interest rates. The financials sector is also a target for cyberattacks, and may experience technology malfunctions and disruptions. Cybersecurity incidents and technology malfunctions and failures have become increasingly frequent in this sector and have reportedly caused losses to companies in this sector, which may negatively impact the Fund.

Geographic Risk. Some of the companies in which the Fund invests are located in parts of the world that have historically been prone to natural disasters, such as

8

earthquakes, tornadoes, volcanic eruptions, droughts, floods, hurricanes or tsunamis, and are economically sensitive to environmental events. Any such event may adversely impact the economies of these geographic areas or business operations of companies in these geographic areas, causing an adverse impact on the value of the Fund.

Illiquid Investments Risk. The Fund may not acquire any illiquid investment if, immediately after the acquisition, the Fund would have invested more than 15% of its net assets in illiquid investments. An illiquid investment is any investment that the Fund reasonably expects cannot be sold or disposed of in current market conditions in seven calendar days or less without significantly changing the market value of the investment. Liquid investments may become illiquid after purchase by the Fund, particularly during periods of market turmoil. There can be no assurance that a security or instrument that is deemed to be liquid when purchased will continue to be liquid for as long as it is held by the Fund, and any security or instrument held by the Fund may be deemed an illiquid investment pursuant to the Fund’s liquidity risk management program. To the extent the Fund holds illiquid investments, the illiquid investments may reduce the returns of the Fund because the Fund may be unable to transact at advantageous times or prices. An investment may be illiquid due to, among other things, the reduced number and capacity of traditional market participants to make a market in securities or instruments, the lack of an active market for such securities or instruments, capital controls, delays or limits on repatriation of local currency, or insolvency of local governments. In particular, some frontier markets in which the Fund invests are experiencing a shortage of USD reserves (including Kenya, Nigeria and Sri Lanka) and have recently restricted or delayed repatriation of local currency, and these issues are likely to persist. To the extent that the Fund invests in securities or instruments with substantial market and/or credit risk, the Fund will tend to have increased exposure to the risks associated with illiquid investments. Illiquid investments may be harder to value, especially in changing markets. If the Fund is forced to sell underlying investments at reduced prices or under unfavorable conditions to meet redemption requests or for other cash needs, the Fund may suffer a loss. This may be magnified in a rising interest rate environment or other circumstances where redemptions from the Fund may be greater than normal. Other market participants may be attempting to liquidate holdings at the same time as the Fund, causing increased supply of the Fund’s underlying investments in the market and contributing to illiquid investments risk and downward pricing pressure. In addition, if the Fund is limited in its ability to sell illiquid investments during periods when shareholders are redeeming their shares, the Fund will need to sell liquid securities to meet redemption requests and illiquid securities will become a larger portion of the Fund’s holdings. During periods of market volatility, liquidity in the market for the Fund’s shares may be impacted by the liquidity in the market for the underlying securities or instruments held by the Fund, which could lead to the Fund’s shares trading at a premium or discount to the Fund's NAV.

Infectious Illness Risk. A widespread outbreak of an infectious illness, such as the COVID-19 pandemic, may adversely affect the economies of many nations and the global economy and may impact individual issuers and capital markets in ways that cannot be foreseen.

9

An infectious illness outbreak may result in travel restrictions, closed international borders, disruption of healthcare services, prolonged quarantines, cancellations, supply chain disruptions, lower consumer demand, temporary and permanent closures of businesses, layoffs, defaults and other significant economic, social and political impacts, as well as general concern and uncertainty.

An infectious illness outbreak may result in extreme volatility, severe losses, credit deterioration of issuers, and disruptions in markets, which could adversely impact the Fund and its investments, including impairing any hedging activity.

Certain local markets may be subject to closures. Any suspension of trading in markets in which the Fund invests will have an impact on the Fund and its investments and will impact the Fund’s ability to purchase or sell securities in such markets. Market or economic disruptions could result in elevated tracking error and increased premiums or discounts to the Fund's NAV. Additionally, an outbreak could impair the operations of the Fund’s service providers, including BFA, which could adversely impact the Fund.

Governmental and quasi-governmental authorities and regulators throughout the world may respond to an outbreak and any resulting economic disruptions with a variety of fiscal and monetary policy changes, including direct capital infusions into companies and other issuers, new monetary policy tools, and changes in interest rates. A reversal of these policies, or the ineffectiveness of such policies, is likely to increase market volatility, which could adversely affect the Fund’s investments.

An outbreak may exacerbate other pre-existing political, social and economic risks in certain countries or globally, which could adversely affect the Fund and its investments and could result in increased premiums or discounts to the Fund's NAV.

Despite the development of vaccines, the duration of the COVID-19 pandemic and its effects cannot be predicted with certainty.

Issuer Risk. The performance of the Fund depends on the performance of individual securities to which the Fund has exposure. Any issuer of these securities may perform poorly, causing the value of its securities to decline. Poor performance may be caused by poor management decisions, competitive pressures, changes in technology, expiration of patent protection, disruptions in supply, labor problems or shortages, corporate restructurings, fraudulent disclosures, credit deterioration of the issuer or other factors. Issuers may, in times of distress or at their own discretion, decide to reduce or eliminate dividends, which may also cause their stock prices to decline. An issuer may also be subject to risks associated with the countries, states and regions in which the issuer resides, invests, sells products, or otherwise conducts operations.

Large-Capitalization Companies Risk. Large-capitalization companies may be less able than smaller capitalization companies to adapt to changing market conditions. Large-capitalization companies may be more mature and subject to more limited growth potential compared with smaller capitalization companies. During different market cycles, the performance of large-capitalization companies has trailed the overall performance of the broader securities markets.

Large Shareholder and Large-Scale Redemption Risk. Certain shareholders, including an Authorized Participant, a third-party investor, the Fund’s adviser or an affiliate of the Fund’s adviser, a market maker, or another entity, may from time to time

10

own or manage a substantial amount of Fund shares or may invest in the Fund and hold their investment for a limited period of time. These shareholders may also pledge or loan Fund shares (to secure financing or otherwise), which may result in the shares becoming concentrated in another party. There can be no assurance that any large shareholder or large group of shareholders would not redeem their investment or that the size of the Fund would be maintained. Redemptions of a large number of Fund shares by these shareholders may adversely affect the Fund’s liquidity and net assets. To the extent the Fund permits redemptions in cash, these redemptions may force the Fund to sell portfolio securities when it might not otherwise do so, which may negatively impact the Fund’s NAV, have a material effect on the market price of the Shares and increase the Fund’s brokerage costs and/or accelerate the realization of taxable income and/or gains and cause the Fund to make taxable distributions to its shareholders earlier than the Fund otherwise would have. In addition, under certain circumstances, non-redeeming shareholders may be treated as receiving a disproportionately large taxable distribution during or with respect to such tax year. The Fund also may be required to sell its more liquid Fund investments to meet a large redemption, in which case the Fund’s remaining assets may be less liquid, more volatile, and more difficult to price. To the extent these large shareholders transact in shares on the secondary market, such transactions may account for a large percentage of the trading volume for the shares of the Fund and may, therefore, have a material upward or downward effect on the market price of the Fund shares. In addition, large purchases of Fund shares may adversely affect the Fund’s performance to the extent that the Fund is delayed in investing new cash and is required to maintain a larger cash position than it ordinarily would, diluting its investment returns.

Management Risk. The Fund is subject to management risk because it does not seek to replicate the performance of a specified index. BFA and the portfolio managers will utilize a proprietary investment process, techniques and risk analyses in making investment decisions for the Fund, but there can be no guarantee that these decisions will produce the desired results. In addition, legislative, regulatory, or tax developments may affect the investment techniques available to BFA in connection with managing the Fund and may also adversely affect the ability of the Fund to achieve its investment objective.

Market Risk. The Fund could lose money over short periods due to short-term market movements and over longer periods during more prolonged market downturns. The value of a security, asset, or other instrument may decline due to changes in general market conditions, economic trends or events that are not specifically related to the issuer of the security or other asset, or factors that affect a particular issuer or issuers, exchange or exchanges, country, group of countries, region, market, industry, group of industries, sector or asset class. Local, regional or global events such as war, acts of terrorism, the spread of infectious illness or other public health issues, recessions, or other events could have a significant impact on the Fund and its investments and could result in increased premiums or discounts to the Fund’s NAV. During a general market downturn, multiple asset classes may be negatively affected. Changes in market conditions and interest rates generally do not have the same impact on all types of securities and instruments.

11

The countries in which the Fund invests may be subject to considerable degrees of economic, political and social instability.

Political and Social Risk. Disparities of wealth, the pace and success of democratization and ethnic, religious and racial disaffection, among other factors, may exacerbate social unrest, violence and labor unrest in some of the countries in which the Fund may invest. Unanticipated or sudden political or social developments may result in sudden and significant investment losses.

Economic Risk. Some countries in which the Fund may invest may experience economic instability, including instability resulting from substantial rates of inflation or significant devaluations of their currency, or economic recessions, which would have a negative effect on the economies and securities markets of their economies. Some of these countries may also impose restrictions on the exchange or export of currency or adverse currency exchange rates and may be characterized by a lack of available currency hedging instruments.

Expropriation Risk. Investments in certain countries in which the Fund may invest may be subject to loss due to expropriation or nationalization of assets and property or the imposition of restrictions on foreign investments and repatriation of capital.

Large Government Debt Risk. Chronic structural public sector deficits in some countries in which the Fund may invest may adversely impact securities held by the Fund.

Market Trading Risk.

Absence of Active Market. Although shares of the Fund are listed for trading on one or more stock exchanges, there can be no assurance that an active trading market for such shares will develop or be maintained by market makers or Authorized Participants.

Risk of Secondary Listings. The Fund's shares may be listed or traded on U.S. and non-U.S. stock exchanges other than the U.S. stock exchange where the Fund's primary listing is maintained, and may otherwise be made available to non-U.S. investors through funds or structured investment vehicles similar to depositary receipts. There can be no assurance that the Fund’s shares will continue to trade on any such stock exchange or in any market or that the Fund’s shares will continue to meet the requirements for listing or trading on any exchange or in any market. The Fund's shares may be less actively traded in certain markets than in others, and investors are subject to the execution and settlement risks and market standards of the market where they or their broker direct their trades for execution. Certain information available to investors who trade Fund shares on a U.S. stock exchange during regular U.S. market hours may not be available to investors who trade in other markets, which may result in secondary market prices in such markets being less efficient.

Secondary Market Trading Risk. Shares of the Fund may trade in the secondary market at times when the Fund does not accept orders to purchase or redeem shares. At such times, shares may trade in the secondary market with more significant premiums or discounts than might be experienced at times when the Fund accepts purchase and redemption orders.

12

Secondary market trading in Fund shares may be halted by a stock exchange because of market conditions or for other reasons. In addition, trading in Fund shares on a stock exchange or in any market may be subject to trading halts caused by extraordinary market volatility pursuant to “circuit breaker” rules on the stock exchange or market.

Shares of the Fund, similar to shares of other issuers listed on a stock exchange, may be sold short and are therefore subject to the risk of increased volatility and price decreases associated with being sold short. In addition, trading activity in derivative products based on the Fund may lead to increased trading volume and volatility in the secondary market for the shares of the Fund.

Shares of the Fund May Trade at Prices Other Than NAV. Shares of the Fund trade on stock exchanges at prices at, above or below the Fund’s most recent NAV. The NAV of the Fund is calculated at the end of each business day and fluctuates with changes in the market value of the Fund’s holdings. The trading price of the Fund's shares fluctuates continuously throughout trading hours based on both market supply of and demand for Fund shares and the underlying value of the Fund's portfolio holdings or NAV. As a result, the trading prices of the Fund’s shares may deviate significantly from NAV during periods of market volatility. ANY OF THESE FACTORS, AMONG OTHERS, MAY LEAD TO THE FUND'S SHARES TRADING AT A PREMIUM OR DISCOUNT TO NAV. However, because shares can be created and redeemed in Creation Units at NAV, BFA believes that large discounts or premiums to the NAV of the Fund are not likely to be sustained over the long term (unlike shares of many closed-end funds, which frequently trade at appreciable discounts from, and sometimes at premiums to, their NAVs). While the creation/redemption feature is designed to make it more likely that the Fund’s shares normally will trade on stock exchanges at prices close to the Fund’s next calculated NAV, exchange prices are not expected to correlate exactly with the Fund's NAV due to timing reasons, supply and demand imbalances and other factors. In addition, disruptions to creations and redemptions, including disruptions at market makers, Authorized Participants, or other market participants, and during periods of significant market volatility, may result in trading prices for shares of the Fund that differ significantly from its NAV. Authorized Participants may be less willing to create or redeem Fund shares if there is a lack of an active market for such shares or its underlying investments, which may contribute to the Fund’s shares trading at a premium or discount to NAV.

Costs of Buying or Selling Fund Shares. Buying or selling Fund shares on an exchange involves two types of costs that apply to all securities transactions. When buying or selling shares of the Fund through a broker, you will likely incur a brokerage commission and other charges. In addition, you may incur the cost of the “spread”; that is, the difference between what investors are willing to pay for Fund shares (the “bid” price) and the price at which they are willing to sell Fund shares (the “ask” price). The spread, which varies over time for shares of the Fund based on trading volume and market liquidity, is generally narrower if the Fund has more trading volume and market liquidity and wider if the Fund has less trading volume and market liquidity. In addition, increased market volatility may cause wider spreads. There may also be regulatory and other charges that are incurred as a result of trading activity. Because

13

of the costs inherent in buying or selling Fund shares, frequent trading may detract significantly from investment results and an investment in Fund shares may not be advisable for investors who anticipate regularly making small investments through a brokerage account.

Mid-Capitalization Companies Risk. Stock prices of mid-capitalization companies may be more volatile than those of large-capitalization companies and, therefore, the Fund’s share price may be more volatile than those of funds that invest a larger percentage of their assets in stocks issued by large-capitalization companies. Stock prices of mid-capitalization companies are also more vulnerable than those of large-capitalization companies to adverse business or economic developments, and the stocks of mid-capitalization companies may be less liquid than those of large-capitalization companies, making it difficult for the Fund to buy and sell shares of mid-capitalization companies. In addition, mid-capitalization companies generally have less diverse product lines than large-capitalization companies and are more susceptible to adverse developments related to their products.

Middle Eastern Economic Risk. Many Middle Eastern countries have little or no democratic tradition, and the political and legal systems in such countries may adversely impact the companies in which the Fund invests and, as a result, the value of the Fund. Middle Eastern governments have exercised and continue to exercise substantial influence over many aspects of the private sector. Many economies in the Middle East are highly reliant on income from the sale of oil and natural gas or trade with countries involved in the sale of oil and natural gas, and their economies are therefore vulnerable to changes in the market for oil and natural gas and foreign currency values. As global demand for oil and natural gas fluctuates, many Middle Eastern economies may be significantly impacted. A sustained decrease in commodity prices could have a significant negative impact on all aspects of the economy in the region. Middle Eastern economies may be subject to acts of terrorism, political strife, religious, ethnic or socioeconomic unrest and sudden outbreaks of hostilities with neighboring countries.

Certain Middle Eastern countries have strained relations with other Middle Eastern countries due to territorial disputes, historical animosities, international alliances, religious tensions or defense concerns, which may adversely affect the economies of these countries. Certain Middle Eastern countries experience significant unemployment, as well as widespread underemployment.

Many Middle Eastern countries periodically have experienced political, economic and social unrest as protestors have called for widespread reform. Some of these protests have resulted in a governmental regime change, internal conflict or civil war. If further regime changes were to occur, internal conflict were to intensify, or a civil war were to continue in any of these countries, such instability could adversely affect the economies of Middle Eastern countries in which the Fund invests and could decrease the value of the Fund’s investments.

National Closed Market Trading Risk. To the extent that the underlying securities and/or other assets held by the Fund trade on foreign exchanges or in foreign markets that may be closed when the securities exchange on which the Fund’s shares trade is open, there are likely to be deviations between the current price of an underlying

14

security and the last quoted price for the underlying security (i.e., the Fund’s quote from the closed foreign market). The impact of a closed foreign market on the Fund is likely to be greater where a large portion of the Fund’s underlying securities and/or other assets trade on that closed foreign market or when the foreign market is closed for unscheduled reasons. These deviations could result in premiums or discounts to the Fund’s NAV that may be greater than those experienced by other ETFs.

Non-U.S. Securities Risk. Investments in the securities of non-U.S. issuers are subject to the risks of investing in the markets where such issuers are located, including heightened risks of inflation, nationalization and market fluctuations caused by economic and political developments. As a result of investing in non-U.S. securities, the Fund may be subject to increased risk of loss caused by any of the factors listed below:

◾

Government intervention in issuers' operations or structure;

◾

A lack of market liquidity and market efficiency;

◾

Greater securities price volatility;

◾

Exchange rate fluctuations and exchange controls;

◾

Less availability of public information about issuers;

◾

Limitations on foreign ownership of securities;

◾

Imposition of withholding or other taxes;

◾

Imposition of restrictions on the expatriation of the funds or other assets of the Fund;

◾

Higher transaction and custody costs and delays in settlement procedures;

◾

Difficulties in enforcing contractual obligations;

◾

Lower levels of regulation of the securities markets;

◾

Weaker accounting, disclosure and reporting requirements and the risk of being delisted from U.S. exchanges; and

◾

Legal principles relating to corporate governance, directors’ fiduciary duties and liabilities and stockholders’ rights in markets in which the Fund invests may differ from or may not be as extensive or protective as those that apply in the U.S.

Withholding Tax Reclaims Risk. The Fund may file claims to recover withholding tax on dividend and interest income (if any) received from issuers in certain countries where such withholding tax reclaim is possible. Whether or when the Fund will receive a withholding tax refund in the future is within the control of the tax authorities in such countries. Where the Fund expects to recover withholding tax based on a continuous assessment of probability of recovery, the NAV of the Fund generally includes accruals for such tax refunds. The Fund continues to evaluate tax developments for potential impact to the probability of recovery. If the likelihood of receiving refunds materially decreases, for example due to a change in tax regulation or approach, accruals in the Fund’s NAV for such refunds may need to be written down partially or in full, which will adversely affect that Fund’s NAV. Investors in the Fund at the time an accrual is written down will bear the impact of any resulting reduction in NAV regardless of whether they were investors during the accrual period. Conversely, if a Fund receives a tax refund

15