December 29, 2017

(as revised May 31, 2018)

| 2017 Prospectus |

|

| ► | iShares Edge MSCI Multifactor Emerging Markets ETF | EMGF | CBOE BZX |

The Securities and Exchange Commission

(“SEC”) has not approved or disapproved these securities or passed upon the adequacy of this prospectus. Any representation to the contrary is a criminal offense.

Table of Contents

|

|

S-1 |

|

|

1 |

|

|

2 |

|

|

22 |

|

|

28 |

|

|

28 |

|

|

31 |

|

|

46 |

|

|

46 |

|

|

48 |

|

|

48 |

|

|

50 |

“MSCI,” “MSCI Emerging Markets Diversified

Multiple-Factor Index” and “MSCI Emerging Markets Index” are servicemarks of MSCI Inc. and have been licensed for use for certain purposes by BlackRock Fund Advisors or its affiliates. iShares® and BlackRock® are registered trademarks of

BlackRock Fund Advisors and its affiliates. The Fund is neither sponsored, endorsed, sold nor promoted by MSCI Inc., and MSCI Inc. makes no representation regarding the advisability of investing in the Fund.

i

[THIS PAGE INTENTIONALLY LEFT BLANK]

iSHARES® EDGE MSCI MULTIFACTOR EMERGING MARKETS ETF

| Ticker: EMGF | Stock Exchange: Cboe BZX |

Investment Objective

The iShares Edge MSCI Multifactor Emerging Markets ETF (the

“Fund”) seeks to track the investment results of an index composed of stocks of large- and mid-capitalization companies in emerging markets that have favorable exposure to target style factors subject to constraints.

Fees and Expenses

The following table describes the fees and expenses that you

will incur if you own shares of the Fund. The investment advisory agreement between iShares, Inc. (the “Company”) and BlackRock Fund Advisors (“BFA”) (the “Investment Advisory Agreement”) provides that BFA will

pay all operating expenses of the Fund, except the management fees, interest expenses, taxes, expenses incurred with respect to the acquisition and disposition of portfolio securities and the execution of portfolio transactions, including brokerage

commissions, distribution fees or expenses, litigation expenses and any extraordinary expenses. The Fund may incur “Acquired Fund Fees and Expenses.” Acquired Fund Fees and Expenses reflect the Fund's pro

rata share of the fees and expenses incurred by investing in other investment companies. The impact of Acquired Fund Fees and Expenses is included in the total returns of the Fund. Acquired Fund Fees and Expenses are not included in the

calculation of the ratio of expenses to average net assets shown in the Financial Highlights section of the Fund's prospectus (the “Prospectus”). BFA, the investment adviser to the Fund, has

contractually agreed to waive a portion of its management fees in an amount equal to the Acquired Fund Fees and Expenses, if any, attributable to the Fund's investments in other series of iShares Trust and the Company through December 31, 2021. The

contractual waiver may be terminated prior to December 31, 2021 only upon written agreement of the Company and BFA.

You may also incur usual and customary brokerage commissions

and other charges when buying or selling shares of the Fund, which are not reflected in the Example that follows:

| Annual

Fund Operating Expenses (ongoing expenses that you pay each year as a percentage of the value of your investments)1 | ||||||||||||

| Management

Fees |

Distribution

and Service (12b-1) Fees |

Other

Expenses |

Acquired

Fund Fees and Expenses |

Total

Annual Fund Operating Expenses |

Fee Waiver | Total

Annual Fund Operating Expenses After Fee Waiver | ||||||

| 0.45% | None | None | 0.05% | 0.50% | (0.05)% | 0.45% | ||||||

| 1 | The expense information in the table has been restated to reflect current fees. |

S-1

Example. This Example is

intended to help you compare the cost of owning shares of the Fund with the cost of investing in other funds. The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then sell all of your shares at the end of those

periods. The Example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses remain the same. Although your actual costs may be higher or lower, based on these assumptions, your costs would

be:

| 1 Year | 3 Years | 5 Years | 10 Years | |||

| $46 | $144 | $258 | $607 |

S-2

S-3

S-4

S-5

S-6

S-7

S-8

S-9

S-10

S-11

Performance Information

The bar chart and table that follow show how the Fund has

performed on a calendar year basis and provide an indication of the risks of investing in the Fund. Both assume that all dividends and distributions have been reinvested in the Fund. Past performance (before and after taxes) does not necessarily

indicate how the Fund will perform in the future. Supplemental information about the Fund’s performance is shown under the heading Total Return Information in the

Supplemental Information section of the Prospectus. If BFA had not waived certain Fund fees during certain periods, the Fund's returns would have been lower.

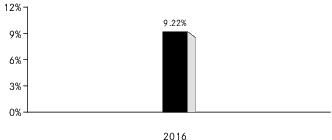

Year by Year Returns1 (Year Ended December 31)

| 1 | The Fund’s year-to-date return as of September 30, 2017 was 30.90%. |

The best calendar quarter return during the period shown above

was 7.60% in the 3rd quarter of 2016; the worst was -4.46% in the 4th quarter of 2016.

Updated performance information may be obtained by visiting our

website at www.iShares.com or by calling 1-800-iShares (1-800-474-2737) (toll free).

S-12

Average Annual Total Returns

(for the periods ended December 31, 2016)

| One Year | Since

Fund Inception | ||

| (Inception Date: 12/08/2015) | |||

| Return Before Taxes | 9.22% | 7.48% | |

| Return After Taxes on Distributions1 | 8.70% | 7.00% | |

| Return After Taxes on Distributions and Sale of Fund Shares1 | 5.65% | 5.70% | |

| MSCI Emerging Markets Diversified Multiple-Factor Index (Index returns do not reflect deductions for fees, expenses or taxes) | 9.60% | 7.76% |

| 1 | After-tax returns in the table above are calculated using the historical highest individual U.S. federal marginal income tax rates and do not reflect the impact of state or local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown, and after-tax returns shown are not relevant to tax-exempt investors or investors who hold shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts (“IRAs”). Fund returns after taxes on distributions and sales of Fund shares are calculated assuming that an investor has sufficient capital gains of the same character from other investments to offset any capital losses from the sale of Fund shares. As a result, Fund returns after taxes on distributions and sales of Fund shares may exceed Fund returns before taxes and/or returns after taxes on distributions. |

S-13

S-14

More Information About the Fund

This Prospectus contains important information about investing

in the Fund. Please read this Prospectus carefully before you make any investment decisions. Additional information regarding the Fund is available at www.iShares.com.

BFA is the investment adviser to the Fund. Shares of the Fund

are listed for trading on Cboe BZX Exchange, Inc. (“Cboe BZX”) (formerly known as BATS Exchange, Inc.). The market price for a share of the Fund may be different from the Fund’s most recent NAV.

ETFs are funds that trade like other publicly-traded

securities. The Fund is designed to track an index. Similar to shares of an index mutual fund, each share of the Fund represents an ownership interest in an underlying portfolio of securities and other instruments intended to track a market index.

Unlike shares of a mutual fund, which can be bought and redeemed from the issuing fund by all shareholders at a price based on NAV, shares of the Fund may be purchased or redeemed directly from the Fund at NAV solely by Authorized Participants and

only in Creation Unit increments. Also unlike shares of a mutual fund, shares of the Fund are listed on a national securities exchange and trade in the secondary market at market prices that change throughout the day.

The Fund invests in a particular segment of the securities

markets and seeks to track the performance of a securities index that may not be representative of the market as a whole. The Fund is designed to be used as part of broader asset allocation strategies. Accordingly, an investment in the Fund should

not constitute a complete investment program.

An index is

a financial calculation, based on a grouping of financial instruments, and is not an investment product, while the Fund is an actual investment portfolio. The performance of the Fund and the Underlying Index may vary for a number of reasons,

including transaction costs, non-U.S. currency valuations, asset valuations, corporate actions (such as mergers and spin-offs), timing variances and differences between the Fund’s portfolio and the Underlying Index resulting from the Fund's

use of representative sampling or from legal restrictions (such as diversification requirements) that apply to the Fund but not to the Underlying Index. From time to time, the Index Provider may make changes to the methodology or other adjustments

to the Underlying Index. Unless otherwise determined by BFA, any such change or adjustment will be reflected in the calculation of the Underlying Index performance on a going-forward basis after the effective date of such change or adjustment.

Therefore, the Underlying Index performance shown for periods prior to the effective date of any such change or adjustment will generally not be recalculated or restated to reflect such change or adjustment.

“Tracking error” is the divergence of the

performance (return) of the Fund's portfolio from that of the Underlying Index. BFA expects that, over time, the Fund’s tracking error will not exceed 5%. Because the Fund uses a representative sampling indexing strategy, it can be expected to

have a larger tracking error than if it used a replication

1

indexing strategy. “Replication” is an indexing strategy in which

a fund invests in substantially all of the securities in its underlying index in approximately the same proportions as in the underlying index.

Under continuous listing standards adopted by the Fund's

listing exchange, which went into effect on January 1, 2018, the Fund is required to confirm on an ongoing basis that the components of the Underlying Index satisfy the applicable listing requirements. In the event that the Underlying Index does not

comply with the applicable listing requirements, the Fund is required to rectify such non-compliance by requesting that the Index Provider modify the Underlying Index, adopting a new underlying index, or obtaining relief from the SEC. Failure to

rectify such non-compliance may result in the Fund being delisted by the listing exchange.

The Fund may borrow as a temporary measure for extraordinary or

emergency purposes, including to meet redemptions or to facilitate the settlement of securities or other transactions. The Fund does not intend to borrow money in order to leverage its portfolio. The Fund has adopted a non-fundamental investment

restriction such that, under normal market conditions, any borrowings by the Fund will not exceed 10% of the Fund’s net assets.

An investment in the Fund is not a bank deposit and it is not

insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency, BFA or any of its affiliates.

The Fund's investment objective and the Underlying Index may be

changed without shareholder approval.

A Further

Discussion of Principal Risks

The Fund is subject to

various risks, including the principal risks noted below, any of which may adversely affect the Fund’s NAV, trading price, yield, total return and ability to meet its investment objective. You could lose all or part of your investment in the

Fund, and the Fund could underperform other investments.

Asian Economic Risk. Many Asian

economies have experienced rapid growth and industrialization in recent years, but there is no assurance that this growth rate will be maintained. Other Asian economies, however, have experienced high inflation, high unemployment, currency

devaluations and restrictions, and over-extension of credit. Economic events in any one Asian country may have a significant economic effect on the entire Asian region, as well as on major trading partners outside Asia. Any adverse event in the

Asian markets may have a significant adverse effect on some or all of the economies of the countries in which the Fund invests. Many Asian countries are subject to political risk, including political instability, corruption and regional conflict

with neighboring countries. North Korea and South Korea each have substantial military capabilities, and historical tensions between the two countries present the risk of war; in the recent past, these tensions have escalated. Any outbreak of

hostilities between the two countries could have a severe adverse effect on the entire Asian region. In addition, many Asian countries are subject to social and labor risks associated with demands for improved political, economic and social

conditions. These

2

risks, among others, may adversely affect the value of the Fund’s or an

Underlying Fund's investments.

Asset Class Risk. The securities and other assets in the Underlying Index or in the Fund’s or an Underlying Fund's portfolio may underperform in comparison to other securities or indexes that track other countries, groups of

countries, regions, industries, groups of industries, markets, asset classes or sectors. Various types of securities, currencies and indexes may experience cycles of outperformance and underperformance in comparison to the general financial

markets depending upon a number of factors including, among other things, inflation, interest rates, productivity, global demand for local products or resources, and regulation and governmental controls. This may cause the Fund to underperform

other investment vehicles that invest in different asset classes.

Assets Under Management (AUM) Risk. From time to time, an Authorized Participant, a third-party investor, the Fund’s adviser or an affiliate of the Fund’s adviser, or a fund may invest in the Fund and hold its investment for a specific period

of time in order to facilitate commencement of the Fund’s operations or to allow the Fund to achieve size or scale. There can be no assurance that any such entity would not redeem its investment or that

the size of the Fund would be maintained at such levels, which could negatively impact the Fund.

Authorized Participant Concentration Risk. Only an Authorized Participant may engage in creation or redemption transactions directly with the Fund. The Fund has a limited number of institutions that may act as Authorized Participants on an agency basis (i.e., on behalf of other market participants). To the extent that Authorized Participants exit the business or are unable to proceed with creation or redemption

orders with respect to the Fund and no other Authorized Participant is able to step forward to create or redeem Creation Units, Fund shares may be more likely to trade at a premium or discount to NAV and possibly face trading halts or delisting.

Authorized Participant concentration risk may be heightened because ETFs, such as the Fund, that invest in non-U.S. securities or other securities or instruments that are less widely traded often involve greater settlement and operational issues and

capital costs for Authorized Participants, which may limit the availability of Authorized Participants.

Calculation Methodology Risk.

The Underlying Index relies on various sources of information to assess the criteria of issuers included in the Underlying Index (or its Parent Index), including information that may be based on assumptions and estimates. Neither the Fund nor BFA

can offer assurances that the Underlying Index’s calculation methodology or sources of information will provide an accurate assessment of included issuers.

Central and South American Economic Risk. The economies of certain Central and South American countries have experienced high interest rates, economic volatility, inflation, currency devaluations, government defaults and high unemployment rates. In addition,

commodities (such as oil, gas and minerals) represent a significant percentage of exports for these regions and many economies in these regions are particularly sensitive to fluctuations in commodity prices. Adverse economic events in one country

may have a significant adverse effect on other countries in these regions.

3

Commodity Risk. The energy,

materials, and agriculture sectors account for a large portion of the exports of certain countries in which the Fund invests. Any changes in these sectors or fluctuations in the commodity markets could have an adverse impact on a country's economy.

Commodity prices may be influenced or characterized by unpredictable factors, including, where applicable, high volatility, changes in supply and demand relationships, weather, agriculture, trade, pestilence, political instability, changes in

interest rates and monetary and other governmental policies, action and inaction. Securities of companies held by the Fund that are dependent on a single commodity, or are concentrated in a single commodity sector, may typically exhibit even higher

volatility attributable to commodity prices.

Concentration Risk. The Fund

may be susceptible to an increased risk of loss, including losses due to adverse events that affect the Fund’s investments more than the market as a whole, to the extent that the Fund's or an Underlying Fund's investments are concentrated in

the securities of a particular issuer or issuers, country, group of countries, region, market, industry, group of industries, sector or asset class. The Fund may be more adversely affected by the underperformance of those securities, may experience

increased price volatility and may be more susceptible to adverse economic, market, political or regulatory occurrences affecting those securities than a fund that does not concentrate its investments.

Currency Risk. Because the

Fund's NAV is determined on the basis of the U.S. dollar, investors may lose money if the currency of a non-U.S. market in which the Fund invests depreciates against the U.S. dollar or if there are delays or limits on repatriation of such currency,

even if such currency value of the Fund's holdings in that market increases. Currency exchange rates can be very volatile and can change quickly and unpredictably. As a result, the Fund’s NAV may change quickly and without

warning.

Custody Risk. Custody risk refers to the risks inherent in the process of clearing and settling trades, as well as the holding of securities by local banks, agents and depositories. Low trading volumes and volatile prices in less

developed markets may make trades harder to complete and settle, and governments or trade groups may compel local agents to hold securities in designated depositories that may not be subject to independent evaluation. Local agents are held only to

the standards of care of their local markets. In general, the less developed a country’s securities markets are, the greater the likelihood of custody problems.

Cyber Security Risk. With the

increased use of technologies such as the internet to conduct business, the Fund, Authorized Participants, service providers and the relevant listing exchange are susceptible to operational, information security and related “cyber”

risks both directly and through their service providers. Similar types of cyber security risks are also present for issuers of securities in which the Fund invests, which could result in material adverse consequences for such issuers and may cause

the Fund’s investment in such portfolio companies to lose value. Unlike many other types of risks faced by the Fund, these risks typically are not covered by insurance. In general, cyber incidents can result from deliberate attacks or

unintentional events. Cyber incidents include, but are not limited to, gaining unauthorized access to digital systems (e.g., through

“hacking” or malicious software coding) for purposes of

4

misappropriating assets or sensitive information, corrupting data, or causing

operational disruption. Cyber attacks may also be carried out in a manner that does not require gaining unauthorized access, such as causing denial-of-service attacks on websites (i.e., efforts to make network

services unavailable to intended users). Cyber security failures by or breaches of the systems of the Fund’s adviser, distributor and other service providers (including, but not limited to, index providers, fund accountants, custodians,

transfer agents and administrators), market makers, Authorized Participants or the issuers of securities in which the Fund invests, have the ability to cause disruptions and impact business operations, potentially resulting in: financial losses,

interference with the Fund’s ability to calculate its NAV, disclosure of confidential trading information, impediments to trading, submission of erroneous trades or erroneous creation or redemption orders, the inability of the Fund or its

service providers to transact business, violations of applicable privacy and other laws, regulatory fines, penalties, reputational damage, reimbursement or other compensation costs, or additional compliance costs. In addition, cyber attacks may

render records of Fund assets and transactions, shareholder ownership of Fund shares, and other data integral to the functioning of the Fund inaccessible or inaccurate or incomplete. Substantial costs may be incurred by the Fund in order to resolve

or prevent cyber incidents in the future. While the Fund has established business continuity plans in the event of, and risk management systems to prevent, such cyber attacks, there are inherent limitations in such plans and systems, including the

possibility that certain risks have not been identified and that prevention and remediation efforts will not be successful. Furthermore, the Fund cannot control the cyber security plans and systems put in place by service providers to the Fund,

issuers in which the Fund invests, the Index Provider, market makers or Authorized Participants. The Fund and its shareholders could be negatively impacted as a result.

Equity Securities Risk. The

Fund invests in equity securities, which are subject to changes in value that may be attributable to market perception of a particular issuer or to general stock market fluctuations that affect all issuers. Investments in equity securities may be

more volatile than investments in other asset classes. The Underlying Index is comprised of common stocks, which generally subject their holders to more risks than holders of preferred stocks and debt securities because common

stockholders’ claims are subordinated to those of holders of preferred stock and debt securities upon the bankruptcy of the issuer.

European Economic Risk. The EU

requires compliance by member countries with restrictions on inflation rates, deficits, interest rates and debt levels, as well as fiscal and monetary controls, each of which may significantly affect every country in Europe, including those

countries that are not members of the EU. Changes in imports or exports, changes in governmental or EU regulations on trade, changes in the exchange rate of the euro (the common currency of certain EU countries), the default or threat of default by

an EU member country on its sovereign debt and/or an economic recession in an EU member country may have a significant adverse effect on the economies of EU member countries and their trading partners. The European financial markets have

historically experienced volatility and adverse trends due to concerns about economic downturns or rising government debt levels in several European countries, including, but not limited to, Austria, Belgium, Cyprus, France, Greece, Ireland, Italy,

Portugal,

5

Spain and Ukraine. These events have adversely affected the exchange rate of

the euro and may continue to significantly affect European countries.

Responses to financial problems by European governments,

central banks and others, including austerity measures and reforms, may not produce the desired results, may result in social unrest, may limit future growth and economic recovery or may have other unintended consequences. Further defaults or

restructurings by governments and other entities of their debt could have additional adverse effects on economies, financial markets and asset valuations around the world. In addition, one or more countries may abandon the euro and/or withdraw from

the EU. In a referendum held on June 23, 2016, the United Kingdom (the “U.K.”) resolved to leave the EU. The referendum may introduce significant uncertainties and instability in the financial markets as the U.K. negotiates its exit from

the EU. Secessionist movements, such as the Catalan movement in Spain, as well as governmental or other responses to such movements, may also create instability and uncertainty in the region.

The occurrence of terrorist incidents throughout Europe also

could impact financial markets. The impact of these events is not clear but could be significant and far-reaching and adversely affect the value of the Fund.

Financials Sector Risk.

Companies in the financials sector of an economy are subject to extensive governmental regulation and intervention, which may adversely affect the scope of their activities, the prices they can charge, the amount of capital they must maintain and,

potentially, their size. Governmental regulation may change frequently and may have significant adverse consequences for companies in the financials sector, including effects not intended by such regulation. The impact of more stringent capital

requirements, or recent or future regulation in various countries, on any individual financial company or on the financials sector as a whole cannot be predicted. Certain risks may impact the value of investments in the financials sector more

severely than those of investments outside this sector, including the risks associated with companies that operate with substantial financial leverage. Companies in the financials sector may also be adversely affected by increases in interest rates

and loan losses, decreases in the availability of money or asset valuations, credit rating downgrades and adverse conditions in other related markets. Insurance companies, in particular, may be subject to severe price competition and/or rate

regulation, which may have an adverse impact on their profitability. The financials sector is particularly sensitive to fluctuations in interest rates. The financials sector is also a target for cyber attacks, and may experience technology

malfunctions and disruptions. In recent years, cyber attacks and technology malfunctions and failures have become increasingly frequent in this sector and have reportedly caused losses to companies in this sector, which may negatively impact the

Fund.

Geographic Risk. Some of the companies in which the Fund invests are located in parts of the world that have historically been prone to natural disasters such as earthquakes, tornadoes, volcanic eruptions, droughts, floods, hurricanes

or tsunamis and are economically sensitive to environmental events. Any such event may adversely impact the economies of these geographic areas or business operations of companies in these geographic areas, causing an adverse impact on the value of

the Fund.

6

Index-Related Risk. The Fund

seeks to achieve a return that corresponds generally to the price and yield performance, before fees and expenses, of the Underlying Index as published by the Index Provider. There is no assurance that the Index Provider or any agents that may act

on its behalf will compile the Underlying Index accurately, or that the Underlying Index will be determined, composed or calculated accurately. While the Index Provider provides descriptions of what the Underlying Index is designed to achieve,

neither the Index Provider nor its agents provide any warranty or accept any liability in relation to the quality, accuracy or completeness of the Underlying Index or its related data, and they do not guarantee that the Underlying Index will be in

line with the Index Provider’s methodology. BFA’s mandate as described in this Prospectus is to manage the Fund consistently with the Underlying Index provided by the Index Provider to BFA. BFA does not provide any warranty or guarantee

against the Index Provider’s or any agent’s errors. Errors in respect of the quality, accuracy and completeness of the data used to compile the Underlying Index may occur from time to time and may not be identified and corrected by the

Index Provider for a period of time or at all, particularly where the indices are less commonly used as benchmarks by funds or managers. Therefore, gains, losses or costs associated with errors of the Index Provider or its agents will generally be

borne by the Fund and its shareholders. For example, during a period where the Underlying Index contains incorrect constituents, the Fund would have market exposure to such constituents and would be underexposed to the Underlying Index’s other

constituents. Such errors may negatively or positively impact the Fund and its shareholders.

Apart from scheduled rebalances, the Index Provider or its

agents may carry out additional ad hoc rebalances to the Underlying Index in order, for example, to correct an error in the selection of index constituents. When the Underlying Index is rebalanced and the Fund in turn rebalances its portfolio to

attempt to increase the correlation between the Fund’s portfolio and the Underlying Index, any transaction costs and market exposure arising from such portfolio rebalancing will be borne directly by the Fund and its shareholders. Unscheduled

rebalances to the Underlying Index may expose the Fund to additional tracking error risk, which is the risk that the Fund's returns may not track those of the Underlying Index. Therefore, errors and additional ad hoc rebalances carried out by the

Index Provider or its agents to the Underlying Index may increase the costs to and the tracking error risk of the Fund.

Information Technology Sector Risk. Information technology companies face intense competition, both domestically and internationally, which may have an adverse effect on their profit margins. Like other technology companies, information technology

companies may have limited product lines, markets, financial resources or personnel. The products of information technology companies may face obsolescence due to rapid technological developments, frequent new product introduction, unpredictable

changes in growth rates and competition for the services of qualified personnel. Companies in the information technology sector are heavily dependent on patent and intellectual property rights. The loss or impairment of these rights may adversely

affect the profitability of these companies.

Issuer

Risk. The performance of the Fund depends on the performance of individual securities to which the Fund has exposure. Any issuer of these securities may perform

7

poorly, causing the value of its securities to decline. Poor performance may

be caused by poor management decisions, competitive pressures, changes in technology, expiration of patent protection, disruptions in supply, labor problems or shortages, corporate restructurings, fraudulent disclosures, credit deterioration of the

issuer or other factors. Issuers may, in times of distress or at their own discretion, decide to reduce or eliminate dividends, which may also cause their stock prices to decline.

Large-Capitalization Companies Risk. Large-capitalization companies may be less able than smaller capitalization companies to adapt to changing market conditions. Large-capitalization companies may be more mature and subject to more limited growth

potential compared with smaller capitalization companies. During different market cycles, the performance of large-capitalization companies has trailed the overall performance of the broader securities markets.

Management Risk. The Fund may

not fully replicate the Underlying Index and may hold securities not included in the Underlying Index. As a result, the Fund is subject to the risk that BFA’s investment strategy, the implementation of which is subject to a number of

constraints, may not produce the intended results.

Market Risk. The Fund could

lose money over short periods due to short-term market movements and over longer periods during more prolonged market downturns. The value of a security or other asset may decline due to changes in general market conditions, economic trends or

events that are not specifically related to the issuer of the security or other asset, or factors that affect a particular issuer or issuers, country, group of countries, region, market, industry, group of industries, sector or asset class.

During a general market downturn, multiple asset classes may be negatively affected. Changes in market conditions and interest rates generally do not have the same impact on all types of securities and instruments.

Market Trading Risk

Absence of Active Market.

Although shares of the Fund are listed for trading on one or more stock exchanges, there can be no assurance that an active trading market for such shares will develop or be maintained by market makers or Authorized Participants.

Risk of Secondary Listings.

The Fund's shares may be listed or traded on U.S. and non-U.S. stock exchanges other than the U.S. stock exchange where the Fund's primary listing is maintained, and may otherwise be made available to non-U.S.

investors through funds or structured investment vehicles similar to depositary receipts. There can be no assurance that the Fund’s shares will continue to trade on any such stock exchange or in any market or that the Fund’s shares will

continue to meet the requirements for listing or trading on any exchange or in any market. The Fund's shares may be less actively traded in certain markets than in others, and investors are subject to the execution and settlement risks and market

standards of the market where they or their broker direct their trades for execution. Certain information available to investors who trade Fund shares on a U.S. stock exchange during regular U.S. market hours may not be available to investors who

trade in other markets, which may result in secondary market prices in such markets being less efficient.

8

Secondary Market Trading Risk.

Shares of the Fund may trade in the secondary market at times when the Fund does not accept orders to purchase or redeem shares. At such times, shares may trade in the secondary market with more significant premiums or discounts than might be

experienced at times when the Fund accepts purchase and redemption orders.

Secondary market trading in Fund shares may be halted by a

stock exchange because of market conditions or for other reasons. In addition, trading in Fund shares on a stock exchange or in any market may be subject to trading halts caused by extraordinary market volatility pursuant to “circuit

breaker” rules on the stock exchange or market.

Shares of the Fund, similar to shares of other issuers listed

on a stock exchange, may be sold short and are therefore subject to the risk of increased volatility and price decreases associated with being sold short.

Shares of the Fund May Trade at Prices Other Than NAV. Shares of the Fund trade on stock exchanges at prices at, above or below the Fund’s most recent NAV. The NAV of the Fund is calculated at the end of each business day and fluctuates with changes in the market value

of the Fund’s holdings. The trading price of the Fund's shares fluctuates continuously throughout trading hours based on both market supply of and demand for Fund shares and the underlying value of the Fund's portfolio holdings or NAV. As

a result, the trading prices of the Fund’s shares may deviate significantly from NAV during periods of market volatility. ANY OF THESE FACTORS, AMONG OTHERS, MAY LEAD TO THE FUND'S

SHARES TRADING AT A PREMIUM OR DISCOUNT TO NAV. However, because shares can be created and redeemed in Creation Units at NAV, BFA believes that large discounts or premiums to the NAV of the Fund are not likely

to be sustained over the long term (unlike shares of many closed-end funds, which frequently trade at appreciable discounts from, and sometimes at premiums to, their NAVs). While the creation/redemption feature is designed to make it more likely

that the Fund’s shares normally will trade on stock exchanges at prices close to the Fund’s next calculated NAV, exchange prices are not expected to correlate exactly with the Fund's NAV due to timing reasons, supply and demand

imbalances and other factors. In addition, disruptions to creations and redemptions, including disruptions at market makers, Authorized Participants, or other market participants, and during periods of significant market volatility, may result in

trading prices for shares of the Fund that differ significantly from its NAV. Authorized Participants may be less willing to create or redeem Fund shares if there is a lack of an active market for such shares or its underlying investments, which may

contribute to the Fund’s shares trading at a premium or discount to NAV.

Costs of Buying or Selling Fund Shares. Buying or selling Fund shares on an exchange involves two types of costs that apply to all securities transactions. When buying or selling shares of the Fund through a broker, you will likely incur a brokerage commission

and other charges. In addition, you may incur the cost of the “spread”; that is, the difference between what investors are willing to pay for Fund shares (the “bid” price) and the price at which they are willing to sell Fund

shares (the “ask” price). The spread, which varies over time for shares of the Fund based on trading volume and market liquidity, is generally narrower if the Fund has more trading volume

9

and market liquidity and wider if the Fund has less trading volume and market

liquidity. In addition, increased market volatility may cause wider spreads. There may also be regulatory and other charges that are incurred as a result of trading activity. Because of the costs inherent in buying or selling Fund shares, frequent

trading may detract significantly from investment results and an investment in Fund shares may not be advisable for investors who anticipate regularly making small investments through a brokerage account.

Mid-Capitalization Companies Risk. Stock prices of mid-capitalization companies may be more volatile than those of large-capitalization companies and, therefore, the Fund’s share price may be more volatile than those of funds that invest a larger

percentage of their assets in stocks issued by large-capitalization companies. Stock prices of mid-capitalization companies are also more vulnerable than those of large-capitalization companies to adverse business or economic developments, and the

stocks of mid-capitalization companies may be less liquid, making it difficult for the Fund to buy and sell shares of mid-capitalization companies. In addition, mid-capitalization companies generally have less diverse product lines than

large-capitalization companies and are more susceptible to adverse developments related to their products.

Model Risk. Neither the Fund

nor BFA can offer assurances that the Index Provider’s model will result in the Fund meeting its investment objective. The Fund may underperform other funds that do not similarly invest.

Momentum Securities Risk.

Stocks that have previously exhibited high momentum characteristics may not experience positive momentum in the future or may experience more volatility than the market as a whole. The Index Provider may be unsuccessful in creating an index that

emphasizes momentum securities. In addition, there may be periods when the momentum style of investing is out of favor and the investment performance of the Fund may suffer.

National Closed Market Trading Risk. To the extent that the underlying securities held by the Fund trade on foreign exchanges that may be closed when the securities exchange on which the Fund’s or the Underlying Fund's shares trade is open,

there are likely to be deviations between the current price of an underlying security and the last quoted price for the underlying security (i.e.,

the Fund’s or the Underlying Fund's quote from the closed foreign market). These deviations could result in premiums or discounts to the Fund’s or the Underlying Fund's NAV that may be greater than those experienced by other

ETFs.

Non-Diversification Risk. The Fund and the Underlying Funds are classified as “non-diversified.” This means that the Fund and the Underlying Funds may invest a large percentage of their assets in securities issued by or representing

a small number of issuers. As a result, the Fund and the Underlying Funds may be more susceptible to the risks associated with these particular issuers or to a single economic, political or regulatory occurrence affecting these issuers.

Non-U.S. Securities Risk.

Investments in the securities of non-U.S. issuers are subject to the risks of investing in the markets where such issuers are located, including heightened risks of inflation, nationalization and market fluctuations caused

10

by economic and political developments. As a result of investing in non-U.S.

securities, the Fund may be subject to increased risk of loss caused by any of the factors listed below:

| ■ | Lower levels of liquidity and market efficiency; |

| ■ | Greater securities price volatility; |

| ■ | Exchange rate fluctuations and exchange controls; |

| ■ | Less availability of public information about issuers; |

| ■ | Limitations on foreign ownership of securities; |

| ■ | Imposition of withholding or other taxes; |

| ■ | Imposition of restrictions on the expatriation of the funds or other assets of the Fund; |

| ■ | Higher transaction and custody costs and delays in settlement procedures; |

| ■ | Difficulties in enforcing contractual obligations; |

| ■ | Lower levels of regulation of the securities markets; |

| ■ | Weaker accounting, disclosure and reporting requirements; and |

| ■ | Legal principles relating to corporate governance, directors’ fiduciary duties and liabilities and stockholders’ rights in markets in which the Fund invests may differ and/or may not be as extensive or protective as those that apply in the U.S. |

Operational Risk. The Fund is exposed to operational risks arising from a number of factors, including, but not limited to, human error, processing and communication errors, errors of the Fund’s service providers, counterparties or

other third-parties, failed or inadequate processes and technology or systems failures. The Fund and BFA seek to reduce these operational risks through controls and procedures. However, these measures do not address every possible risk and may be

inadequate to address significant operational risks.

Passive Investment Risk. The

Fund is not actively managed and may be affected by a general decline in market segments related to the Underlying Index. The Fund invests in securities included in, or representative of, the Underlying Index, regardless of their investment merits.

BFA generally does not attempt to invest the Fund's assets in defensive positions under any market conditions, including declining markets.

Privatization Risk. Some

countries in which the Fund invests have privatized, or have begun the process of privatizing, certain entities and industries. Newly privatized companies may face strong competition from government-sponsored competitors that have not been

privatized. In some instances, investors in newly privatized entities have suffered losses due to the inability of the newly privatized entities to adjust quickly to a competitive environment or changing regulatory and legal standards or, in some

cases, due to re-nationalization of such privatized entities. There is no assurance that similar losses will not recur.

Quality Stocks Risk. The Fund

invests in stocks that are deemed by the Index Provider to be of high quality based on a number of factors, including, among others, historical and expected high returns on equity, stable earnings growth and low debt-to-equity, but there is no

guarantee that the past performance of these stocks will

11

continue. The Index Provider may be unsuccessful in creating an index that

reflects the quality of individual stocks. Companies that issue these stocks may not be able to sustain consistently high returns on equity, earnings and growth year after year and may need to borrow money or issue debt despite their prior history.

Earnings, growth and other measures of a stock’s quality can be adversely affected by market, regulatory, political, environmental and other factors. The price of a stock also may be affected by factors other than those factors considered by

the Index Provider. The degree to which these factors affect a stock’s performance can be difficult to predict.

Reliance on Trading Partners Risk. Economies in emerging market countries generally are heavily dependent upon commodity prices and international trade. Accordingly, these countries have been, and may continue to be, affected adversely by the economies

of their trading partners, trade barriers, exchange controls or managed adjustments in relative currency values and may suffer from extreme and volatile debt burdens or inflation rates. These countries may be subject to other protectionist measures

imposed or negotiated by the countries with which they trade.

Risk of Investing in China.

Investments in Chinese securities, including certain Hong Kong-listed securities, subject the Fund to risks specific to China. The Chinese economy is subject to a considerable degree of economic, political and social instability:

Political and Social Risk. The

Chinese government is authoritarian and has periodically used force to suppress civil dissent. Disparities of wealth and the pace of economic liberalization may lead to social turmoil, violence and labor unrest. In addition, China continues to

experience disagreements related to integration with Hong Kong and religious and nationalist disputes in Tibet and Xinjiang. There is also a greater risk in China than in many other countries of currency fluctuations, currency non-convertibility,

interest rate fluctuations and higher rates of inflation as a result of internal social unrest or conflicts with other countries. Unanticipated political or social developments may result in sudden and significant investment losses. China's growing

income inequality, rapidly aging population and significant environmental issues also are factors that may affect the Chinese economy.

Government Control and Regulations. The Chinese government has implemented significant economic reforms in order to liberalize trade policy, promote foreign investment in the economy, reduce government control of the economy and develop market mechanisms.

There can be no assurance these reforms will continue or that they will be effective. Despite recent reform and privatizations, government control over certain sectors or enterprises and significant regulation of investment and industry is still

pervasive, including restrictions on investment in companies or industries deemed to be sensitive to particular national interests, and the Chinese government may restrict foreign ownership of Chinese corporations and/or the repatriation of assets

by foreign investors. Limitations or restrictions on foreign ownership of securities may have adverse effects on the liquidity and performance of the Fund, and could lead to higher tracking error. Government market interventions may have a negative

impact on market sentiment, which may in turn affect the performance of the Chinese economy and the Fund’s investments. Chinese markets generally continue to experience inefficiency, volatility and pricing anomalies that may

12

be connected to governmental influence, lack of publicly-available

information and/or political and social instability.

Economic Risk. The Chinese

economy has grown rapidly in the recent past and there is no assurance that this growth rate will be maintained. In fact, the Chinese economy may experience a significant slowdown as a result of, among other things, a deterioration in global demand

for Chinese exports, as well as contraction in spending on domestic goods by Chinese consumers. In addition, China may experience substantial rates of inflation or economic recessions, which would have a negative effect on its economy and securities

market. Delays in enterprise restructuring, slow development of well-functioning financial markets and widespread corruption have also hindered performance of the Chinese economy. China continues to receive substantial pressure from trading partners

to liberalize official currency exchange rates. Reduction in spending on Chinese products and services, institution of tariffs or other trade barriers, including as a result of heightened trade tensions between China and the U.S., or a downturn in

any of the economies of China’s key trading partners may have an adverse impact on the Chinese economy.

Expropriation Risk. The

Chinese government maintains a major role in economic policymaking and investing in China involves risk of loss due to expropriation, nationalization, or confiscation of assets and property or the imposition of restrictions on foreign investments

and on repatriation of capital invested.

Security

Risk. China has strained international relations with Taiwan, India, Russia and other neighbors due to territorial disputes, historical animosities, defense concerns and other security concerns. Relations between

China's Han ethnic majority and other ethnic groups in China, including Tibetans and Uighurs, are also strained and have been marked by protests and violence. These situations may cause uncertainty in the Chinese market and may adversely affect the

Chinese economy. In addition, conflict on the Korean Peninsula could adversely affect the Chinese economy.

Chinese Equity Markets. The

Fund may invest in H-shares (securities of companies incorporated in the People’s Republic of China (“PRC”) that are denominated in Hong Kong dollars and listed on the Stock Exchange of Hong Kong), A-shares (securities of companies

incorporated in the PRC that are denominated in renminbi and listed on the Shanghai Stock Exchange (“SSE”) and the Shenzhen Stock Exchange (“SZSE”)) and B-shares (securities of companies incorporated in the PRC that are

denominated in U.S. dollars (in the case of the SSE) or Hong Kong dollars (in the case of the SZSE) and listed on the SSE and the SZSE). The Fund may also invest in certain Hong Kong listed securities known as Red-Chips (securities issued by

companies incorporated in certain foreign jurisdictions, which are controlled, directly or indirectly, by entities owned by the national government or local governments in the PRC and derive substantial revenues or allocate substantial assets in the

PRC) and P-Chips (securities issued by companies incorporated in certain foreign jurisdictions, which are controlled, directly or indirectly, by individuals in the PRC and derive substantial revenues or allocate substantial assets in the PRC). The

issuance of B-shares and H-shares by Chinese companies and the ability to obtain a “back-door listing” through Red-Chips or P-Chips is still regarded by the Chinese authorities as an experiment in economic reform. “Back-door

listing” is a means by which a mainland Chinese company issues Red-Chips

13

or P-Chips to obtain quick access to international listing and international

capital. All of these share mechanisms are relatively untested and subject to political and economic policy in China.

Hong Kong Political Risk. Hong

Kong reverted to Chinese sovereignty on July 1, 1997 as a Special Administrative Region (SAR) of the PRC under the principle of “one country, two systems.” Although China is obligated to maintain the current capitalist economic and

social system of Hong Kong through June 30, 2047, the continuation of economic and social freedoms enjoyed in Hong Kong is dependent on the government of China. Any attempt by China to tighten its control over Hong Kong's political, economic, legal

or social policies may result in an adverse effect on Hong Kong's markets. In addition, the Hong Kong dollar trades at a fixed exchange rate in relation to (or, is “pegged” to) the U.S. dollar, which has contributed to the growth and

stability of the Hong Kong economy. However, it is uncertain how long the currency peg will continue or what effect the establishment of an alternative exchange rate system would have on the Hong Kong economy. Because the Fund's NAV is denominated

in U.S. dollars, the establishment of an alternative exchange rate system could result in a decline in the Fund's NAV.

Risk of Investing in Emerging Markets. Investments in emerging market issuers are subject to a greater risk of loss than investments in issuers located or operating in more developed markets. This is due to, among other things, the potential for greater

market volatility, lower trading volume, higher levels of inflation, political and economic instability, greater risk of a market shutdown and more governmental limitations on foreign investments in emerging market countries than are typically found

in more developed markets. Moreover, emerging markets often have less uniformity in accounting and reporting requirements, less reliable securities valuations and greater risks associated with custody of securities than developed markets. In

addition, emerging markets often have greater risk of capital controls through such measures as taxes or interest rate control than developed markets. Certain emerging market countries may also lack the infrastructure necessary to attract large

amounts of foreign trade and investment. Local securities markets in emerging market countries may trade a small number of securities and may be unable to respond effectively to increases in trading volume, potentially making prompt liquidation of

holdings difficult or impossible at times. Settlement procedures in emerging market countries are frequently less developed and reliable than those in the United States (and other developed countries). In addition, significant delays may occur in

certain markets in registering the transfer of securities. Settlement or registration problems may make it more difficult for the Fund to value its portfolio securities and could cause the Fund to miss attractive investment

opportunities.

Investing in emerging market

countries involves a higher risk of expropriation, nationalization, confiscation of assets and property or the imposition of restrictions on foreign investments and on repatriation of capital invested by certain emerging market countries.

Risk of Investing in India.

India is an emerging market country and exhibits significantly greater market volatility from time to time in comparison to more developed markets. Political and legal uncertainty, greater government control over

14

the economy, currency fluctuations or blockage, and the risk of

nationalization or expropriation of assets may result in higher potential for losses.

Moreover, governmental actions can have a significant effect on

the economic conditions in India, which could adversely affect the value and liquidity of the Fund's investments. In November of 2016, the Indian government eliminated certain large denomination cash notes as legal tender, causing uncertainty in

certain financial markets. The securities markets in India are comparatively underdeveloped, and stockbrokers and other intermediaries may not perform as well as their counterparts in the United States and other more developed securities markets.

The limited liquidity of the Indian securities markets may also affect the Fund’s ability to acquire or dispose of securities at the price and time that it desires.

Global factors and foreign actions may inhibit the flow of

foreign capital on which India is dependent to sustain its growth. In addition, the Reserve Bank of India (“RBI”) has imposed limits on foreign ownership of Indian securities, which may decrease the liquidity of the Fund’s

portfolio and result in extreme volatility in the prices of Indian securities. These factors, coupled with the lack of extensive accounting, auditing and financial reporting standards and practices, as compared to the U.S., may increase the Fund's

risk of loss.

Further, certain Indian regulatory

approvals, including approvals from the Securities and Exchange Board of India (“SEBI”), the RBI, the central government and the tax authorities (to the extent that tax benefits need to be utilized), may be required before the Fund can

make investments in the securities of Indian companies. Capital gains from Indian securities may be subject to local taxation.

Risk of Investing in Russia.

Investing in Russian securities involves significant risks, in addition to those described under “Risk of Investing in Emerging Markets” and “Non-U.S. Securities Risk” that are not typically associated with investing in U.S.

securities, including:

| ■ | The risk of delays in settling portfolio transactions and the risk of loss arising out of the system of share registration and custody used in Russia; |

| ■ | Risks in connection with the maintenance of the Fund’s portfolio securities and cash with foreign sub-custodians and securities depositories, including the risk that appropriate sub-custody arrangements will not be available to the Fund; |

| ■ | The risk that the Fund’s ownership rights in portfolio securities could be lost through fraud or negligence because ownership in shares of Russian companies is recorded by the companies themselves and by registrars, rather than by a central registration system; and |

| ■ | The risk that the Fund may not be able to pursue claims on behalf of its shareholders because of the system of share registration and custody, and because Russian banking institutions and registrars are not guaranteed by the Russian government. |

The U.S. and the Economic and

Monetary Union of the EU, along with the regulatory bodies of a number of countries including Japan, Australia, Norway, Switzerland and Canada (collectively, “Sanctioning Bodies”), have imposed economic sanctions, which consist of asset

freezes and sectoral sanctions, on certain Russian individuals and

15

Russian corporate entities. The Sanctioning Bodies could also institute

broader sanctions on Russia. These sanctions, or even the threat of further sanctions, may result in the decline of the value and liquidity of Russian securities, a weakening of the ruble or other adverse consequences to the Russian economy. These

sanctions could also result in the immediate freeze of Russian securities and/or funds invested in prohibited assets, impairing the ability of the Fund to buy, sell, receive or deliver those securities and/or assets. Additional sanctions against

Russia have been, and may in the future be, imposed by the U.S. or other countries.

The sanctions against certain Russian issuers include

prohibitions on transacting in or dealing in certain issuances of new debt or new equity of such issuers. Securities held by the Fund issued prior to the date of the sanctions being imposed are not currently subject to any restrictions under the

sanctions. However, compliance with each of these sanctions may impair the ability of the Fund to buy, sell, hold, receive or deliver the affected securities or other securities of such issuers. If it becomes impracticable or unlawful for the Fund

to hold securities subject to, or otherwise affected by, sanctions (collectively, “affected securities”), or if deemed appropriate by BFA, the Fund may prohibit in-kind deposits of the affected securities in connection with creation

transactions and instead require a cash deposit, which may also increase the Fund's transaction costs. The Fund may also be legally required to freeze assets in a blocked account.

Also, if an affected security is included in the Fund's

Underlying Index, the Fund may, where practicable, seek to eliminate its holdings of the affected security by employing or augmenting its representative sampling strategy to seek to track the investment results of its Underlying Index. The use of

(or increased use of) a representative sampling strategy may increase the Fund’s tracking error risk. If the affected securities constitute a significant percentage of the Underlying Index, the Fund may not be able to effectively implement a

representative sampling strategy, which may result in significant tracking error between the Fund’s performance and the performance of its Underlying Index.

Current or future sanctions may result in Russia taking counter

measures or retaliatory actions, which may further impair the value and liquidity of Russian securities. These retaliatory measures may include the immediate freeze of Russian assets held by the Fund. In the event of such a freeze of any Fund

assets, including depositary receipts, the Fund may need to liquidate non-restricted assets in order to satisfy any Fund redemption orders. The liquidation of Fund assets during this time may also result in the Fund receiving substantially lower

prices for its securities.

These sanctions may also lead

to changes in the Fund’s Underlying Index. The Fund’s Index Provider may remove securities from the Underlying Index or implement caps on the securities of certain issuers that have been subject to recent economic sanctions. In such an

event, it is expected that the Fund will rebalance its portfolio to bring it in line with the Underlying Index as a result of any such changes, which may result in transaction costs and increased tracking error. These sanctions, the volatility that

may result in the trading markets for Russian securities and the possibility that Russia may impose investment or currency controls on investors may cause the Fund to invest in, or increase the Fund’s investments in, depositary receipts that

represent the securities

16

of the Underlying Index. These investments may result in increased transaction

costs and increased tracking error.

Risk of Investing in

South Korea. Investments in South Korean issuers involve risks that are specific to South Korea, including legal, regulatory, political, currency, security and economic risks. Substantial political tensions exist

between North Korea and South Korea and recently these political tensions have escalated. The outbreak of hostilities between the two nations, or even the threat of an outbreak of hostilities, will likely adversely impact the South Korean economy.

In addition, South Korea's economic growth potential has recently been on a decline because of a rapidly aging population and structural problems, among other factors.

Securities Lending Risk. The

Fund or an Underlying Fund may engage in securities lending. Securities lending involves the risk that the Fund may lose money because the borrower of the loaned securities fails to return the securities in a timely manner or at all. The Fund could

also lose money in the event of a decline in the value of collateral provided for loaned securities or a decline in the value of any investments made with cash collateral. These events could also trigger adverse tax consequences for the Fund.

BlackRock Institutional Trust Company, N.A., the Fund's securities lending agent, will take into account the tax impact to shareholders of substitute payments for dividends when managing the Fund's securities lending program.

Security Risk. Some geographic

areas in which the Fund invests have experienced acts of terrorism and strained international relations due to territorial disputes, historical animosities, defense concerns and other security concerns. These situations may cause uncertainty in the

markets of these geographic areas and may adversely affect their economies.

Structural Risk. Certain

political, economic, legal and currency risks could contribute to a high degree of price volatility in the equity markets of some of the countries in which the Fund may invest and could adversely affect investments in the Fund:

Political and Social Risk.

Disparities of wealth, the pace and success of democratization and ethnic, religious and racial disaffection, among other factors, may exacerbate social unrest, violence and labor unrest in some of the countries in which the Fund may invest.

Unanticipated or sudden political or social developments may result in sudden and significant investment losses.

Economic Risk. Some countries

in which the Fund may invest may experience economic instability, including instability resulting from substantial rates of inflation or significant devaluations of their currency, or economic recessions, which would have a negative effect on the

economies and securities markets of their economies. Some of these countries may also impose restrictions on the exchange or export of currency or adverse currency exchange rates and may be characterized by a lack of available currency hedging

instruments.

Expropriation Risk. Investments in certain countries in which the Fund may invest may be subject to loss due to expropriation or nationalization of assets and property or the imposition of restrictions on foreign investments and

repatriation of capital.

17

Large Government Debt Risk.

Chronic structural public sector deficits in some countries in which the Fund may invest may adversely impact securities held by the Fund.

Tax Risk. Because the Fund

invests in Underlying Funds, the Fund’s realized losses on sales of shares of the Underlying Funds may be indefinitely or permanently deferred as “wash sales.” Distributions of short-term capital gains by the Underlying Funds will

be recognized as ordinary income by the Fund and would not be offset by the Fund’s capital loss carryforwards, if any. Capital loss carryforwards of the Underlying Funds, if any, would not offset net capital gains of the Fund. Each of these

effects is caused by the Fund’s investment in the Underlying Funds and may result in distributions to Fund shareholders being of higher magnitudes and less likely to qualify for lower capital gain tax rates than if the Fund were to invest

otherwise directly in the securities and other instruments comprising the Underlying Index.

Tracking Error Risk. Tracking

error is the divergence of a fund’s performance from that of an applicable underlying index. Tracking error may occur because of differences between the securities (including shares of an underlying fund) and other instruments held in a

fund’s portfolio and those included in the applicable underlying index, pricing differences (including, as applicable, differences between a security’s price at the local market close and the fund’s valuation of a security at the

time of calculation of the fund’s NAV), differences in transaction costs, the fund’s holding of uninvested cash, differences in timing of the accrual of or the valuation of dividends or other distributions, interest, tax gains or losses,

changes to the applicable underlying index and the cost to the fund of complying with various new or existing regulatory requirements. These risks may be heightened during times of increased market volatility or other unusual market conditions. In

addition, tracking error may result because a fund incurs fees and expenses, while the applicable underlying index does not. To the extent that the Fund seeks its investment objective through investments in an underlying fund, the Fund may

experience increased tracking error. The potential for increased tracking error may result from investments in the Underlying Fund due to, among other things, differences in the composition of the investment portfolio of the Underlying Fund as

compared to the index tracked by the Underlying Fund and differences in the timing of the Fund’s valuation of: (i) the Underlying Fund and the foreign currency forward contracts (each valued as of the close of the NYSE, typically 4:00 p.m.,

Eastern Time), (ii) the valuation of the securities in the Underlying Index (generally valued as of each security’s local market close) and (iii) the foreign currency forward contracts included in the Underlying Index (generally valued at 4:00

p.m., London time). INDEX ETFs THAT TRACK INDICES WITH SIGNIFICANT WEIGHT IN EMERGING MARKETS ISSUERS MAY EXPERIENCE HIGHER TRACKING ERROR THAN OTHER INDEX ETFs THAT DO NOT TRACK SUCH INDICES.

Treaty/Tax Risk. The Fund

operates, in part, through a Subsidiary, which in turn invests in securities of Indian issuers.

An investor is required to submit the tax residency certificate

as issued in the country of residence and provide other documents and information as prescribed by the Government of India to claim benefits under the DTAA.

18

India and Mauritius signed a protocol (“Protocol”)

amending the double tax avoidance arrangement between the two countries (India-Mauritius DTAA) on May 10, 2016. The Protocol gives India the right to tax capital gains that arise from alienation of shares of an Indian company acquired by a Mauritian

tax resident. However, the Protocol provides for grandfathering of investments in shares made before April 1, 2017. Returns from investments in shares made on or after April 1, 2017 will be subject to capital gains tax in India, although the

Protocol introduces a limitation of benefits provision which shall be a prerequisite for a reduced rate of tax (50% of domestic tax rate) on capital gains arising during a two year transition period from April 1, 2017 to March 31, 2019. The Protocol

is now in effect, which could result in the imposition of withholding and capital gains taxes and/or other taxes on the Subsidiary by tax authorities in India. This could significantly reduce the return to the Fund on its investments in shares and

the return received by the Fund’s shareholders.

Criteria for Residence of Companies in India.

A foreign company will be considered a resident in India if its

place of effective management (“POEM”) (defined as a place where key management and commercial decisions that are necessary for the conduct of the business of an entity as a whole are in substance made) is in India in the relevant

financial year. This test is to be applied taking the relevant financial year as a whole into consideration. Under prior law, an offshore company was treated as a non-resident in India unless it was wholly controlled and managed from India. The POEM

test has been introduced as the criteria for determining tax residence of companies established outside India. The POEM test is presently in effect starting April 1, 2016 (FY 2016-17). The Central Board of Direct Taxes (“CBDT”) has also

issued final guidelines for determination of POEM of a company established outside India through Circular No. 6 of 2017 (“Guidelines”). The Guidelines provide that the test will be fact-based, and also provide separate tests for

companies engaged in active business outside India, and other companies. CBDT vide circular issued on February 23, 2017 clarified that the provisions in relation to POEM shall not apply to a company having turnover of INR 500 million or less in a

year.

Indirect Transfers.

The current legislation, (Indian) Income Tax Act, 1961

(“IT Act”) imposes Indian tax and withholding obligations with respect to the transfer of shares and interest in an overseas company that derives its value substantially from assets situated in India (“indirect transfers”).

It has been clarified that Indian tax authorities will not reopen any assessment proceedings that were completed before April 1, 2012 and where no notice for reassessment has been issued prior to that date. The CBDT also clarified that any

assessment or any other order which stands validated due to the amendments in the Finance Act would be enforced. Given this clarification issued by the CBDT, the Fund does not expect that shareholders or the Fund will become subject to tax

or to withholding obligations with respect to completed assessments.

It has been clarified that the share or interest of the foreign

entity shall be deemed to derive its value substantially from the assets located in India, if the value of such Indian assets exceeds INR 100 million, and represents at least 50% of the value of all the assets owned by the foreign entity. The value

of an asset shall be the fair market value as of the specified date, of such an asset without reduction of liabilities. The fair

19

market value will be determined in accordance with the final rules ratified on

June 28, 2016. It also provides that where all the assets of the foreign entity are not located in India, only such part of the income as is reasonably attributable to the Indian assets shall be subject to capital gains tax in India.

Further, it provides an exemption from indirect transfer

provisions to the small shareholders of such foreign entity in the following cases:

| ■ | With respect to a foreign entity that holds the Indian assets directly, if the transferor of share or interest in such a foreign entity (along with its associated enterprises), at any time in the twelve months preceding the year of transfer neither holds the right of control or management in the foreign entity, nor holds voting power or share capital or interest exceeding 5% of the total voting power or total share capital or total interest in such foreign entity. |

| ■ | With respect to a foreign entity that holds the Indian assets indirectly, if the transferor of share or interest in such foreign entity (along with its associated enterprises), at any time in the twelve months preceding the year of transfer does not hold the right of control or management in relation to the foreign entity, which would entitle them to the right of control or management in the foreign entity which directly holds the Indian assets; or does not hold voting power or share capital or interest exceeding 5% of the total voting power or total share capital or total interest in the foreign entity, which results in holding the same share capital or voting power in the entity which directly holds the Indian assets. |

If the gains arising from transfer of shares or

interests in a foreign entity are taxable in India in accordance with the aforementioned provisions of indirect transfer, the purchaser of the securities will be required to withhold applicable Indian taxes.

Gains realized when a non-resident acquires shares of a foreign

company from another non-resident and the foreign company derives “substantial value” from Indian assets, (meaning that the value of Indian assets (i) exceeds INR 100 million, and (ii) represents at least 50% of the value the

company’s assets), such gains are taxable in India and subject to withholding, to the extent that they are reasonably attributable to the Indian assets.

Because the Fund invests in Indian securities through the

Subsidiary, the Subsidiary or the Fund may be considered to derive “substantial value” from Indian assets, and accordingly, shareholder redemptions of Fund/Subsidiary shares and sales of Fund shares may have been subject to Indian tax

and withholding obligations. However, through Finance Act 2017 (“FA 2017”), the government had introduced an exemption to shareholders in Category I and Category II foreign portfolio investors (“FPI”) from the applicability

of indirect transfer taxation. The Subsidiary is a Category II FPI. Therefore, any redemptions or transfers by the Fund or the shareholders in the Fund should not be subject to Indian indirect transfer tax.

FA 2017 provides that aforesaid indirect transfer provisions

will not apply to foreign investors making an investment directly or indirectly in a SEBI registered Category I and Category II foreign portfolio investor. This provision is applicable from April 1, 2014 (FY 2014-15).

General Anti-Avoidance Rules.

20

The current legislation provides for the general anti-avoidance

rules (“GAAR”) to curb aggressive tax planning with the use of sophisticated structures. GAAR became applicable with effect from April 1, 2017. Further, investments in shares made up until March 31, 2017 are exempted from the