Table of Contents

| 2014 Prospectus |

|

| ► | iShares Emerging Markets Dividend ETF | DVYE | NYSE ARCA |

Table of Contents

Table of Contents

|

|

S-1 |

|

|

1 |

|

|

2 |

|

|

12 |

|

|

15 |

|

|

15 |

|

|

19 |

|

|

28 |

|

|

29 |

|

|

30 |

|

|

32 |

|

|

33 |

Table of Contents

Table of Contents

DIVIDEND ETF

| Ticker: DVYE | Stock Exchange: NYSE Arca |

| Annual

Fund Operating Expenses (ongoing expenses that you pay each year as a percentage of the value of your investments) | ||||||||||||

| Management

Fees |

Distribution

and Service (12b-1) Fees |

Other

Expenses |

Acquired

Fund Fees and Expenses |

Total

Annual Fund Operating Expenses |

Fee Waiver | Total

Annual Fund Operating Expenses After Fee Waiver | ||||||

| 0.68% | None | None | 0.00% | 0.68% | (0.19)% | 0.49% | ||||||

Table of Contents

| 1 Year | 3 Years | 5 Years | 10 Years | |||

| $50 | $198 | $360 | $829 |

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

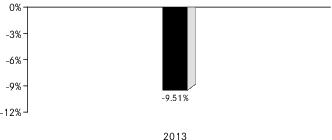

| 1 | The Fund’s total return for the six months ended June 30, 2014 was 2.92%. |

| One Year | Since

Fund Inception | ||

| (Inception Date: 2/23/2012) | |||

| Return Before Taxes | -9.51% | -2.10% | |

| Return After Taxes on Distributions2 | -10.60% | -2.98% | |

| Return After Taxes on Distributions and Sale of Fund Shares2 | -4.70% | -1.45% | |

| Dow Jones Emerging Markets Select Dividend Index (Index returns do not reflect deductions for fees, expenses, or taxes) | -10.01% | -2.52% |

| 2 | After-tax returns in the table above are calculated using the historical highest individual U.S. federal marginal income tax rates and do not reflect the impact of state or local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown, and after-tax returns shown are not relevant to tax-exempt investors or investors who hold shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts (“IRAs”). Fund returns after taxes on distributions and sales of Fund shares are calculated assuming that an investor has sufficient capital gains of the same character from other investments to offset any capital losses from the sale of Fund shares. As a result, Fund returns after taxes on distributions and sales of Fund shares may exceed Fund returns before taxes and/or returns after taxes on distributions. |

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

| ■ | Lower levels of liquidity and market efficiency; |

| ■ | Greater securities price volatility; |

| ■ | Exchange rate fluctuations and exchange controls; |

| ■ | Less availability of public information about issuers; |

| ■ | Limitations on foreign ownership of securities; |

| ■ | Imposition of withholding or other taxes; |

| ■ | Imposition of restrictions on the expatriation of the funds or other assets of the Fund; |

| ■ | Higher transaction and custody costs and delays in settlement procedures; |

| ■ | Difficulties in enforcing contractual obligations; |

| ■ | Lower levels of regulation of the securities markets; |

| ■ | Weaker accounting, disclosure and reporting requirements; and |

| ■ | Legal principles relating to corporate governance, directors’ fiduciary duties and liabilities and stockholders’ rights in markets in which the Fund invests may differ and/or may not be as extensive or protective as those that apply in the United States. |

Table of Contents

Table of Contents

| ■ | The risk of delays in settling portfolio transactions and the risk of loss arising out of the system of share registration and custody used in Russia; |

| ■ | Risks in connection with the maintenance of the Fund’s portfolio securities and cash with foreign sub-custodians and securities depositories, including the risk that appropriate sub-custody arrangements will not be available to the Fund; |

| ■ | The risk that the Fund’s ownership rights in portfolio securities could be lost through fraud or negligence as a result of the fact that ownership in shares of Russian companies is recorded by the companies themselves and by registrars, rather than by a central registration system; and |

Table of Contents

| ■ | The risk that the Fund may not be able to pursue claims on behalf of its shareholders because of the system of share registration and custody, and because Russian banking institutions and registrars are not guaranteed by the Russian government. |

Table of Contents

Table of Contents

Table of Contents

| ■ | The risk of delays in settling portfolio transactions and the risk of loss arising out of the system of share registration and custody used in certain Eastern European countries; |

| ■ | Risks in connection with the maintenance of the Fund's portfolio securities and cash with foreign sub-custodians and securities depositories, including the risk that appropriate sub-custody arrangements will not be available to the Fund; |

| ■ | The risk that the Fund's ownership rights in portfolio securities could be lost through fraud or negligence as a result of the fact that ownership in shares of certain Eastern European companies is recorded by the companies themselves and by registrars, rather than a central registration system; |

| ■ | The risk that the Fund may not be able to pursue claims on behalf of its shareholders because of the system of share registration and custody, and because certain Eastern European banking institutions and registrars are not guaranteed by their respective governments; and |

| ■ | Risks in connection with Eastern European countries' dependence on the economic health of Western European countries and the EU as a whole. |

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

| Approximate

Value of a Creation Unit |

Creation

Unit Size |

Standard

Creation/ Redemption Transaction Fee |

Maximum

Additional Charge for Creations* |

Maximum

Additional Charge for Redemptions* | ||||

| $2,443,500 | 50,000 | $3,000 | 3.0% | 2.0% |

| * | As a percentage of the net asset value per Creation Unit, inclusive, in the case of redemptions, of the standard redemption transaction fee. |

Table of Contents

Table of Contents

(For a share outstanding throughout each period)

| Year

ended Apr. 30,2014 |

Year

ended Apr. 30, 2013 |

Period

from Feb. 23, 2012a to Apr. 30, 2012 | |||

| Net asset value, beginning of period | $ 53.80 | $ 53.23 | $ 54.61 | ||

| Income

from investment operations: | |||||

| Net investment incomeb | 1.96 | 2.02 | 0.74 | ||

| Net realized and unrealized gain (loss)c | (5.18) | 0.56 | (1.98) | ||

| Total from investment operations | (3.22) | 2.58 | (1.24) | ||

| Less distributions from: | |||||

| Net investment income | (2.25) | (2.01) | (0.14) | ||

| Total distributions | (2.25) | (2.01) | (0.14) | ||

| Net asset value, end of period | $ 48.33 | $ 53.80 | $ 53.23 | ||

| Total return | (5.86)% | 5.09% | (2.27)% d | ||

| Ratios/Supplemental data: | |||||

| Net assets, end of period (000s) | $178,838 | $131,806 | $15,970 | ||

| Ratio of expenses to average net assetse | 0.49% | 0.49% | 0.49% | ||

| Ratio of expenses to average net assets prior to waived feese | 0.68% | 0.68% | 0.68% | ||

| Ratio of net investment income to average net assetse | 4.01% | 3.80% | 7.51% | ||

| Portfolio turnover ratef | 44% | 41% | 2% | ||

| a | Commencement of operations. |

| b | Based on average shares outstanding throughout each period. |

| c | The amounts reported for a share outstanding may not accord with the change in aggregate gains and losses in securities for the fiscal period due to the timing of capital share transactions in relation to the fluctuating market values of the Fund's underlying securities. |

| d | Not annualized. |

| e | Annualized for periods of less than one year. |

| f | Portfolio turnover rates exclude portfolio securities received or delivered in Creation Units but include portfolio transactions that are executed as a result of the Fund processing capital share transactions in Creation Units partially for cash in U.S. dollars. Excluding such cash transactions, the portfolio turnover rates for the years ended April 30, 2014 and April 30, 2013 were 39% and 41%, respectively. |

Table of Contents

Table of Contents

Table of Contents

Table of Contents

| Premium/Discount Range | Number of Days | Percentage of Total Days | ||

| Greater than 2.0% | 1 | 0.27% | ||

| Greater than 1.5% and Less than 2.0% | 1 | 0.27 | ||

| Greater than 1.0% and Less than 1.5% | 15 | 3.99 | ||

| Greater than 0.5% and Less than 1.0% | 99 | 26.33 | ||

| Between 0.5% and -0.5% | 208 | 55.31 | ||

| Less than -0.5% and Greater than -1.0% | 35 | 9.31 | ||

| Less than -1.0% and Greater than -1.5% | 14 | 3.72 | ||

| Less than -1.5% and Greater than -2.0% | 1 | 0.27 | ||

| Less than -2.0% and Greater than -2.5% | 2 | 0.53 | ||

| 376 | 100.00% |

Table of Contents

| Average Annual Total Returns | Cumulative Total Returns | |||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | |||

| 1 Year | (5.86)% | (5.96)% | (6.35)% | (5.86)% | (5.96)% | (6.35)% | ||

| Since Inception* | (1.53)% | (1.25)% | (1.80)% | (3.31)% | (2.72)% | (3.88)% | ||

| * | Total returns for the period since inception are calculated from the inception date of the Fund (2/23/12). The first day of secondary market trading in shares of the Fund was 2/24/12. |

Table of Contents

Table of Contents

|

|

| Call: | 1-800-iShares

or 1-800-474-2737 (toll free) Monday through Friday, 8:30 a.m. to 6:30 p.m. (Eastern time) |

| Email: | iSharesETFs@blackrock.com |

| Write: | c/o

BlackRock Investments, LLC 1 University Square Drive, Princeton, NJ 08540 |

Table of Contents

| 2014 Prospectus |

|

| ► | iShares MSCI Emerging Markets Horizon ETF | EMHZ | BATS |

Table of Contents

Table of Contents

Table of Contents

Table of Contents

| Ticker: EMHZ | Stock Exchange: BATS |

| Annual

Fund Operating Expenses (ongoing expenses that you pay each year as a percentage of the value of your investments) | ||||||

| Management

Fees |

Distribution

and Service (12b-1) Fees |

Other

Expenses |

Total

Annual Fund Operating Expenses | |||

| 0.50% | None | None | 0.50% | |||

| 1 Year | 3 Years | ||||

| $51 | $160 |

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

| ■ | Lower levels of liquidity and market efficiency; |

| ■ | Greater securities price volatility; |

| ■ | Exchange rate fluctuations and exchange controls; |

| ■ | Less availability of public information about issuers; |

| ■ | Limitations on foreign ownership of securities; |

| ■ | Imposition of withholding or other taxes; |

| ■ | Imposition of restrictions on the expatriation of the funds or other assets of the Fund; |

| ■ | Higher transaction and custody costs and delays in settlement procedures; |

| ■ | Difficulties in enforcing contractual obligations; |

| ■ | Lower levels of regulation of the securities markets; |

| ■ | Weaker accounting, disclosure and reporting requirements; and |

Table of Contents

| ■ | Legal principles relating to corporate governance, directors’ fiduciary duties and liabilities and stockholders’ rights in markets in which the Fund invests may differ and/or may not be as extensive or protective as those that apply in the United States. |

Table of Contents

Table of Contents

Table of Contents

Table of Contents

| ■ | The risk of delays in settling portfolio transactions and the risk of loss arising out of the system of share registration and custody used in certain Eastern European countries; |

Table of Contents

| ■ | Risks in connection with the maintenance of the Fund's portfolio securities and cash with foreign sub-custodians and securities depositories, including the risk that appropriate sub-custody arrangements will not be available to the Fund; |

| ■ | The risk that the Fund's ownership rights in portfolio securities could be lost through fraud or negligence as a result of the fact that ownership in shares of certain Eastern European companies is recorded by the companies themselves and by registrars, rather than a central registration system; |

| ■ | The risk that the Fund may not be able to pursue claims on behalf of its shareholders because of the system of share registration and custody, and because certain Eastern European banking institutions and registrars are not guaranteed by their respective governments; and |

| ■ | Risks in connection with Eastern European countries' dependence on the economic health of Western European countries and the EU as a whole. |

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

| Approximate

Value of a Creation Unit |

Creation

Unit Size |

Standard

Creation/ Redemption Transaction Fee |

Maximum

Additional Charge for Creations* |

Maximum

Additional Charge for Redemptions* | ||||

| $1,250,000 | 50,000 | $10,500 | 3.0% | 2.0% |

| * | As a percentage of the net asset value per Creation Unit, inclusive, in the case of redemptions, of the standard redemption transaction fee. |

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

|

|

| Call: | 1-800-iShares

or 1-800-474-2737 (toll free) Monday through Friday, 8:30 a.m. to 6:30 p.m. (Eastern time) |

| Email: | iSharesETFs@blackrock.com |

| Write: | c/o

BlackRock Investments, LLC 1 University Square Drive, Princeton, NJ 08540 |

Table of Contents

| 2014 Prospectus |

|

| ► | iShares Emerging Markets Corporate Bond ETF | CEMB | BATS |

Table of Contents

Table of Contents

|

|

S-1 |

|

|

1 |

|

|

2 |

|

|

13 |

|

|

14 |

|

|

15 |

|

|

17 |

|

|

26 |

|

|

27 |

|

|

28 |

|

|

28 |

|

|

30 |

Table of Contents

Table of Contents

| Ticker: CEMB | Stock Exchange: BATS |

| Annual

Fund Operating Expenses (ongoing expenses that you pay each year as a percentage of the value of your investments) | ||||||

| Management

Fees |

Distribution

and Service (12b-1) Fees |

Other

Expenses |

Total

Annual Fund Operating Expenses | |||

| 0.60% | None | None | 0.60% | |||

| 1 Year | 3 Years | 5 Years | 10 Years | |||

| $61 | $192 | $335 | $750 |

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

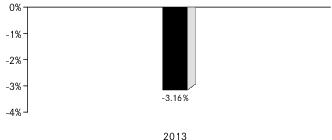

| One Year | Since

Fund Inception | ||

| (Inception Date: 4/17/2012) | |||

| Return Before Taxes | -3.16% | 3.21% | |

| Return After Taxes on Distributions1 | -4.75% | 1.68% | |

| Return After Taxes on Distributions and Sale of Fund Shares1 | -1.79% | 1.84% | |

| Morningstar ® Emerging Markets Corporate Bond IndexSM (Index returns do not reflect deductions for fees, expenses, or taxes) | -2.81% | 3.71% |

| 1 | After-tax returns in the table above are calculated using the historical highest individual U.S. federal marginal income tax rates and do not reflect the impact of state or local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown, and after-tax returns shown are not relevant to tax-exempt investors or investors who hold shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts (“IRAs”). Fund returns after taxes on distributions and sales of Fund shares are calculated assuming that an investor has sufficient capital gains of the same character from other investments to offset any capital losses from the sale of Fund shares. As a result, Fund returns after taxes on distributions and sales of Fund shares may exceed Fund returns before taxes and/or returns after taxes on distributions. |

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

| ■ | The risk of delays in settling portfolio transactions and the risk of loss arising out of the system of share registration and custody used in certain Eastern European countries; |

| ■ | Risks in connection with the maintenance of the Fund's portfolio securities and cash |

Table of Contents

| ■ | The risk that the Fund's ownership rights in portfolio securities could be lost through fraud or negligence as a result of the fact that ownership in shares of certain Eastern European companies is recorded by the companies themselves and by registrars, rather than a central registration system; |

| ■ | The risk that the Fund may not be able to pursue claims on behalf of its shareholders because of the system of share registration and custody, and because certain Eastern European banking institutions and registrars are not guaranteed by their respective governments; and |

| ■ | Risks in connection with Eastern European countries' dependence on the economic health of Western European countries and the European Union (the “EU”) as a whole. |

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

| Approximate

Value of a Creation Unit |

Creation

Unit Size |

Standard

Creation/ Redemption Transaction Fee |

Maximum

Additional Charge for Creations* |

Maximum

Additional Charge for Redemptions* | ||||

| $4,972,000 | 100,000 | $100 | 3.0% | 2.0% |

| * | As a percentage of the net asset value per Creation Unit, inclusive, in the case of redemptions, of the standard redemption transaction fee. |

Table of Contents

Table of Contents

(For a share outstanding throughout each period)

| Year

ended Oct. 31, 2013 |

Period

from Apr. 17, 2012a to Oct. 31, 2012 | ||

| Net asset value, beginning of period | $ 52.93 | $ 50.00 | |

| Income

from investment operations: | |||

| Net investment incomeb | 1.92 | 1.07 | |

| Net realized and unrealized gain (loss)c | (2.49) | 2.76 | |

| Total from investment operations | (0.57) | 3.83 | |

| Less distributions from: | |||

| Net investment income | (1.88) | (0.90) | |

| Total distributions | (1.88) | (0.90) | |

| Net asset value, end of period | $ 50.48 | $ 52.93 | |

| Total return | (1.07)% | 7.75% d | |

| Ratios/Supplemental data: | |||

| Net assets, end of period (000s) | $35,338 | $21,170 | |

| Ratio of expenses to average net assetse | 0.60% | 0.60% | |

| Ratio of net investment income to average net assetse | 3.74% | 3.87% | |

| Portfolio turnover ratef | 33% | 29% | |

| a | Commencement of operations. |

| b | Based on average shares outstanding throughout each period. |

| c | The amounts reported for a share outstanding may not accord with the change in aggregate gains and losses in securities for the fiscal period due to the timing of capital share transactions in relation to the fluctuating market values of the Fund's underlying securities. |

| d | Not annualized. |

| e | Annualized for periods of less than one year. |

| f | Portfolio turnover rates exclude portfolio securities received or delivered as a result of processing capital share transactions in Creation Units. |

Table of Contents

Table of Contents

Table of Contents

| Premium/Discount Range | Number of Days | Percentage of Total Days | ||

| Greater than 2.0% | 1 | 0.53% | ||

| Greater than 1.5% and Less than 2.0% | 3 | 1.60 | ||

| Greater than 1.0% and Less than 1.5% | 78 | 41.48 | ||

| Greater than 0.5% and Less than 1.0% | 28 | 14.89 | ||

| Between 0.5% and -0.5% | 16 | 8.51 | ||

| Less than -0.5% and Greater than -1.0% | 8 | 4.26 | ||

| Less than -1.0% and Greater than -1.5% | 14 | 7.45 | ||

| Less than -1.5% and Greater than -2.0% | 13 | 6.91 | ||

| Less than -2.0% and Greater than -2.5% | 19 | 10.11 | ||

| Less than -2.5% and Greater than -3.0% | 5 | 2.66 | ||

| Less than -3.0% and Greater than -3.5% | 3 | 1.60 | ||

| 188 | 100.00% |

Table of Contents

| Average Annual Total Returns | Cumulative Total Returns | |||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | |||

| 1 Year | (1.07)% | (4.06)% | (0.68)% | (1.07)% | (4.06)% | (0.68)% | ||

| Since Inception* | 4.22% | 2.81% | 4.73% | 6.59% | 4.37% | 7.35% | ||

| * | Total returns for the period since inception are calculated from the inception date of the Fund (4/17/12). The first day of secondary market trading in shares of the Fund was 4/19/12. |

Table of Contents

Table of Contents

Table of Contents

|

|

| Call: | 1-800-iShares

or 1-800-474-2737 (toll free) Monday through Friday, 8:30 a.m. to 6:30 p.m. (Eastern time) |

| Email: | iSharesETFs@blackrock.com |

| Write: | c/o

BlackRock Investments, LLC 1 University Square Drive, Princeton, NJ 08540 |

Table of Contents

| 2014 Prospectus |

|

| ► | iShares Emerging Markets High Yield Bond ETF | EMHY | BATS |

Table of Contents

Table of Contents

|

|

S-1 |

|

|

1 |

|

|

2 |

|

|

12 |

|

|

14 |

|

|

14 |

|

|

17 |

|

|

26 |

|

|

27 |

|

|

28 |

|

|

28 |

|

|

30 |

Table of Contents

Table of Contents

| Ticker: EMHY | Stock Exchange: BATS |

| Annual

Fund Operating Expenses (ongoing expenses that you pay each year as a percentage of the value of your investments) | ||||||

| Management

Fees |

Distribution

and Service (12b-1) Fees |

Other

Expenses |

Total

Annual Fund Operating Expenses | |||

| 0.65% | None | None | 0.65% | |||

| 1 Year | 3 Years | 5 Years | 10 Years | |||

| $66 | $208 | $362 | $810 |

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

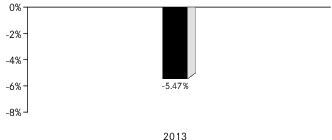

| One Year | Since

Fund Inception | ||

| (Inception Date: 4/3/2012) | |||

| Return Before Taxes | -5.47% | 4.59% | |

| Return After Taxes on Distributions1 | -7.81% | 2.32% | |

| Return After Taxes on Distributions and Sale of Fund Shares1 | -3.08% | 2.60% | |

| Morningstar ® Emerging Markets High Yield Bond IndexSM (Index returns do not reflect deductions for fees, expenses, or taxes) | -4.99% | 5.18% |

| 1 | After-tax returns in the table above are calculated using the historical highest individual U.S. federal marginal income tax rates and do not reflect the impact of state or local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown, and after-tax returns shown are not relevant to tax-exempt investors or investors who hold shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts (“IRAs”). Fund returns after taxes on distributions and sales of Fund shares are calculated assuming that an investor has sufficient capital gains of the same character from other investments to offset any capital losses from the sale of Fund shares. As a result, Fund returns after taxes on distributions and sales of Fund shares may exceed Fund returns before taxes and/or returns after taxes on distributions. |

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

| ■ | The risk of delays in settling portfolio transactions and the risk of loss arising out of the system of share registration and custody used in certain Eastern European countries; |

| ■ | Risks in connection with the maintenance of the Fund's portfolio securities and cash with foreign sub-custodians and securities depositories, including the risk that appropriate sub-custody arrangements will not be available to the Fund; |

| ■ | The risk that the Fund's ownership rights in portfolio securities could be lost through fraud or negligence as a result of the fact that ownership in shares of certain Eastern European companies is recorded by the companies themselves and by registrars, rather than a central registration system; |

| ■ | The risk that the Fund may not be able to pursue claims on behalf of its shareholders because of the system of share registration and custody, and because certain Eastern European banking institutions and registrars are not guaranteed by their respective governments; and |

| ■ | Risks in connection with Eastern European countries' dependence on the economic health of Western European countries and the EU as a whole. |

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

| Approximate

Value of a Creation Unit |

Creation

Unit Size |

Standard

Creation/ Redemption Transaction Fee |

Maximum

Additional Charge for Creations* |

Maximum

Additional Charge for Redemptions* | ||||

| $4,928,000 | 100,000 | $100 | 3.0% | 2.0% |

| * | As a percentage of the net asset value per Creation Unit, inclusive, in the case of redemptions, of the standard redemption transaction fee. |

Table of Contents

Table of Contents

(For a share outstanding throughout each period)

| Year

ended Oct. 31, 2013 |

Period

from Apr. 3, 2012a to Oct. 31, 2012 | ||

| Net asset value, beginning of period | $ 53.62 | $ 50.02 | |

| Income

from investment operations: | |||

| Net investment incomeb | 2.97 | 1.60 | |

| Net realized and unrealized gain (loss)c | (2.91) | 3.40 | |

| Total from investment operations | 0.06 | 5.00 | |

| Less distributions from: | |||

| Net investment income | (2.78) | (1.40) | |

| Total distributions | (2.78) | (1.40) | |

| Net asset value, end of period | $ 50.90 | $ 53.62 | |

| Total return | 0.14% | 10.21% d | |

| Ratios/Supplemental data: | |||

| Net assets, end of period (000s) | $203,604 | $166,231 | |

| Ratio of expenses to average net assetse | 0.65% | 0.65% | |

| Ratio of net investment income to average net assetse | 5.64% | 5.34% | |

| Portfolio turnover ratef | 57% | 40% | |

| a | Commencement of operations. |

| b | Based on average shares outstanding throughout each period. |

| c | The amounts reported for a share outstanding may not accord with the change in aggregate gains and losses in securities for the fiscal period due to the timing of capital share transactions in relation to the fluctuating market values of the Fund's underlying securities. |

| d | Not annualized. |

| e | Annualized for periods of less than one year. |

| f | Portfolio turnover rates exclude portfolio securities received or delivered as a result of processing capital share transactions in Creation Units. |

Table of Contents

Table of Contents

Table of Contents

| Premium/Discount Range | Number of Days | Percentage of Total Days | ||

| Greater than 1.0% and Less than 1.5% | 15 | 7.98% | ||

| Greater than 0.5% and Less than 1.0% | 86 | 45.74 | ||

| Between 0.5% and -0.5% | 75 | 39.89 | ||

| Less than -0.5% and Greater than -1.0% | 9 | 4.79 | ||

| Less than -1.0% and Greater than -1.5% | 3 | 1.60 | ||

| 188 | 100.00% |

Table of Contents

| Average Annual Total Returns | Cumulative Total Returns | |||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | |||

| 1 Year | 0.14% | (1.44)% | 0.53% | 0.14% | (1.44)% | 0.53% | ||

| Since Inception* | 6.43% | 6.31% | 7.02% | 10.36% | 10.15% | 11.27% | ||

| * | Total returns for the period since inception are calculated from the inception date of the Fund (4/3/12). The first day of secondary market trading in shares of the Fund was 4/3/12. |

Table of Contents

Table of Contents

Table of Contents

|

|

| Call: | 1-800-iShares

or 1-800-474-2737 (toll free) Monday through Friday, 8:30 a.m. to 6:30 p.m. (Eastern time) |

| Email: | iSharesETFs@blackrock.com |

| Write: | c/o

BlackRock Investments, LLC 1 University Square Drive, Princeton, NJ 08540 |

Table of Contents

| 2014 Prospectus |

|

| ► | iShares Emerging Markets Local Currency Bond ETF | LEMB | NYSE ARCA |

Table of Contents

Table of Contents

|

|

S-1 |

|

|

1 |

|

|

2 |

|

|

11 |

|

|

13 |

|

|

13 |

|

|

16 |

|

|

24 |

|

|

25 |

|

|

27 |

|

|

27 |

|

|

29 |

Table of Contents

Table of Contents

| Ticker: LEMB | Stock Exchange: NYSE Arca |

| Annual

Fund Operating Expenses (ongoing expenses that you pay each year as a percentage of the value of your investments) | ||||||

| Management

Fees |

Distribution

and Service (12b-1) Fees |

Other

Expenses |

Total

Annual Fund Operating Expenses | |||

| 0.60% | None | None | 0.60% | |||

| 1 Year | 3 Years | 5 Years | 10 Years | |||

| $61 | $192 | $335 | $750 |

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

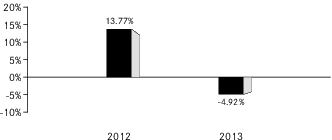

| One Year | Since

Fund Inception | ||

| (Inception Date: 10/18/2011) | |||

| Return Before Taxes | -4.92% | 2.46% | |

| Return After Taxes on Distributions1 | -5.94% | 1.67% | |

| Return After Taxes on Distributions and Sale of Fund Shares1 | -2.64% | 1.66% | |

| Barclays Emerging Markets Broad Local Currency Bond Index (Index returns do not reflect deductions for fees, expenses, or taxes) | -4.61% | 2.71% |

| 1 | After-tax returns in the table above are calculated using the historical highest individual U.S. federal marginal income tax rates and do not reflect the impact of state or local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown, and after-tax returns shown are not relevant to tax-exempt investors or investors who hold shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts (“IRAs”). Fund returns after taxes on distributions and sales of Fund shares are calculated assuming that an investor has sufficient capital gains of the same character from other investments to offset any capital losses from the sale of Fund shares. As a result, Fund returns after taxes on distributions and sales of Fund shares may exceed Fund returns before taxes and/or returns after taxes on distributions. |

Table of Contents

Table of Contents

Table of Contents

Table of Contents

| ■ | The risk of delays in settling portfolio transactions and the risk of loss arising out of the system of share registration and custody used in certain Eastern European countries; |

| ■ | Risks in connection with the maintenance of the Fund's portfolio securities and cash |

Table of Contents

| ■ | The risk that the Fund's ownership rights in portfolio securities could be lost through fraud or negligence as a result of the fact that ownership in shares of certain Eastern European companies is recorded by the companies themselves and by registrars, rather than a central registration system; |

| ■ | The risk that the Fund may not be able to pursue claims on behalf of its shareholders because of the system of share registration and custody, and because certain Eastern European banking institutions and registrars are not guaranteed by their respective governments; and |

| ■ | Risks in connection with Eastern European countries' dependence on the economic health of Western European countries and the European Union (the “EU”) as a whole. |

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

| Approximate

Value of a Creation Unit |

Creation

Unit Size |

Standard

Creation/ Redemption Transaction Fee |

Maximum

Additional Charge for Creations* |

Maximum

Additional Charge for Redemptions* | ||||

| $9,824,000 | 200,000 | $2,000 | 7.0% | 2.0% |

| * | As a percentage of the net asset value per Creation Unit, inclusive, in the case of redemptions, of the standard redemption transaction fee. |

Table of Contents

(For a share outstanding throughout each period)

| Year

ended Oct. 31, 2013 |

Year

ended Oct. 31, 2012 |

Period

from Oct. 18, 2011a to Oct. 31, 2011 | |||

| Net asset value, beginning of period | $ 51.94 | $ 51.13 | $ 49.85 | ||

| Income

from investment operations: | |||||

| Net investment incomeb | 2.07 | 2.31 | 0.02 | ||

| Net realized and unrealized gain (loss)c | (1.92) | 0.41 | 1.26 | ||

| Total from investment operations | 0.15 | 2.72 | 1.28 | ||

| Less distributions from: | |||||

| Net investment income | (1.39) | (0.81) | − | ||

| Return of capital | (0.04) | (1.10) | − | ||

| Total distributions | (1.43) | (1.91) | − | ||

| Net asset value, end of period | $ 50.66 | $ 51.94 | $ 51.13 | ||

| Total return | 0.28% | 5.48% | 2.57% d | ||

| Ratios/Supplemental data: | |||||

| Net assets, end of period (000s) | $638,342 | $207,753 | $30,681 | ||

| Ratio of expenses to average net assetse | 0.60% | 0.60% | 0.60% | ||

| Ratio of net investment income to average net assetse | 4.04% | 4.57% | 1.21% | ||

| Portfolio turnover ratef | 41% | 61% | 0% | ||

| a | Commencement of operations. |

| b | Based on average shares outstanding throughout each period. |

| c | The amounts reported for a share outstanding may not accord with the change in aggregate gains and losses in securities for the fiscal period due to the timing of capital share transactions in relation to the fluctuating market values of the Fund's underlying securities. |

| d | Not annualized. |

| e | Annualized for periods of less than one year. |

| f | Portfolio turnover rates exclude portfolio securities received or delivered in Creation Units but includes portfolio transactions that are executed as a result of the Fund processing capital share transactions in Creation Units partially for cash in U.S. dollars. Excluding |

Table of Contents

Table of Contents

Table of Contents

Table of Contents

| Premium/Discount Range | Number of Days | Percentage of Total Days | ||

| Greater than 2.0% and Less than 2.5% | 1 | 0.40% | ||

| Greater than 1.5% and Less than 2.0% | 7 | 2.78 | ||

| Greater than 1.0% and Less than 1.5% | 79 | 31.34 | ||

| Greater than 0.5% and Less than 1.0% | 36 | 14.29 | ||

| Between 0.5% and -0.5% | 111 | 44.05 | ||

| Less than -0.5% and Greater than -1.0% | 16 | 6.35 | ||

| Less than -1.0% | 2 | 0.79 | ||

| 252 | 100.00% |

Table of Contents

| Average Annual Total Returns | Cumulative Total Returns | |||||||

| NAV | MARKET | INDEX | NAV | MARKET | INDEX | |||

| 1 Year | 0.28% | (1.60)% | 0.57% | 0.28% | (1.60)% | 0.57% | ||

| Since Inception* | 4.10% | 3.82% | 4.31% | 8.54% | 7.93% | 8.96% | ||

| * | Total returns for the period since inception are calculated from the inception date of the Fund (10/18/11). The first day of secondary market trading in shares of the Fund was 10/20/11. |

Table of Contents

Table of Contents

|

|

| Call: | 1-800-iShares

or 1-800-474-2737 (toll free) Monday through Friday, 8:30 a.m. to 6:30 p.m. (Eastern time) |

| Email: | iSharesETFs@blackrock.com |

| Write: | c/o

BlackRock Investments, LLC 1 University Square Drive, Princeton, NJ 08540 |

Table of Contents

(as revised January 7, 2015)

| Fund | Ticker | Stock Exchange | ||

| iShares Emerging Markets Dividend ETF (the “Fund”) | DVYE | NYSE Arca |

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

| • | The Fund generally supports the board’s nominees in the election of directors and generally supports proposals that strengthen the independence of boards of directors; |

| • | When a director has committed himself or herself to service on more than four public company boards (but no |

Table of Contents

| more than six public company boards in most circumstances), the Fund will consider such director’s individual circumstances in determining whether the director will be able to commit sufficient focus and time to a particular company; | |

| • | The Fund generally defers to an issuer’s choice of auditors so long as the corporate auditors represent the interests of shareholders and provide an independent view of the propriety of financial reporting decisions of management; |

| • | The Fund generally favors disclosure of a company’s compensation and benefits policies and opposes excessive compensation, but believes that compensation matters are normally best determined by a company’s board of directors; |

| • | The Fund generally expects to support capital structure requests that it believes enhance the rights of common shareholders and oppose requests that appear to be unreasonably dilutive; |

| • | The Fund generally does not support proposals on social issues that lack a demonstrable economic benefit to the issuer and the Fund investing in such issuer; and |

| • | The Fund generally votes against anti-takeover proposals and proposals that would create additional barriers or costs to corporate transactions that are likely to deliver a premium to shareholders. |

Table of Contents

Table of Contents

| 1. | Concentrate its investments (i.e., invest 25% or more of its total assets in the securities of a particular industry or group of industries), except that the Fund will concentrate to approximately the same extent that the Underlying Index concentrates in the securities of a particular industry or group of industries. For purposes of this limitation, securities of the U.S. government (including its agencies and instrumentalities), repurchase agreements collateralized by U.S. government securities, and securities of state or municipal governments and their political subdivisions are not considered to be issued by members of any industry. |

| 2. | Borrow money, except that (i) the Fund may borrow from banks for temporary or emergency (not leveraging) purposes, including the meeting of redemption requests which might otherwise require the untimely disposition of securities; and (ii) the Fund may, to the extent consistent with its investment policies, enter into repurchase agreements, reverse repurchase agreements, forward roll transactions and similar investment strategies and techniques. To the extent that it engages in transactions described in (i) and (ii), the Fund will be limited so that no more than 33 1/3% of the value of its total assets (including the amount borrowed) is derived from such transactions. Any borrowings which come to exceed this amount will be reduced in accordance with applicable law. |

| 3. | Issue any senior security, except as permitted under the 1940 Act, as interpreted, modified or otherwise permitted by any regulatory authority having jurisdiction, from time to time. |

| 4. | Make loans, except as permitted under the 1940 Act, as interpreted, modified or otherwise permitted by regulatory authority having jurisdiction, from time to time. |

| 5. | Purchase or sell real estate unless acquired as a result of ownership of securities or other instruments (but this restriction shall not prevent the Fund from investing in securities of companies engaged in the real estate business or securities or other instruments backed by real estate or mortgages), or commodities or commodity contracts (but this restriction shall not prevent the Fund from trading in futures contracts and options on futures contracts, including options on currencies to the extent consistent with the Fund’s investment objective and policies). |

| 6. | Engage in the business of underwriting securities issued by other persons, except to the extent that the Fund may technically be deemed to be an underwriter under the 1933 Act, in disposing of portfolio securities. |

Table of Contents

| • | The frequency of trades and quotes for the security; |

| • | The number of dealers wishing to purchase or sell the security and the number of other potential purchasers; |

| • | Dealer undertakings to make a market in the security; and |

| • | The nature of the security and the nature of the marketplace in which it trades (e.g., the time needed to dispose of the security, the method of soliciting offers and the mechanics of transfer). |

Table of Contents

| Name (Age) | Position | Principal

Occupation(s) During the Past 5 Years |

Other

Directorships Held by Director | |||

| Robert

S. Kapito1 (57) |

Director

(since 2009). |

President and Director, BlackRock, Inc. (since 2006); Vice Chairman of BlackRock, Inc. and Head of BlackRock, Inc.’s Portfolio Management Group (since its formation in 1998) and BlackRock, Inc.’s predecessor entities (since 1988); Trustee, University of Pennsylvania (since 2009); President of Board of Directors, Hope & Heroes Children’s Cancer Fund (since 2002); President of the Board of Directors, Periwinkle Theatre for Youth (since 1983). | Trustee of iShares Trust (since 2009); Director of iShares MSCI Russia Capped ETF, Inc. (since 2010); Trustee of iShares U.S. ETF Trust (since 2011); Director of BlackRock, Inc. (since 2006). | |||

| Mark

Wiedman2 (43) |

Director (since 2013). | Managing Director, BlackRock, Inc. (since 2007); Global Head of iShares (since 2011); Head of Corporate Strategy, BlackRock, Inc. (2009-2011). | Trustee of iShares Trust (since 2013); Director of iShares MSCI Russia Capped ETF, Inc. (since 2013); Trustee of iShares U.S. ETF Trust (since 2013); Director of PennyMac Financial Services, Inc. (since 2008). |

| 1 | Robert S. Kapito is deemed to be an “interested person” (as defined in the 1940 Act) of the Company due to his affiliations with BlackRock, Inc. |

| 2 | Mark Wiedman is deemed to be an “interested person” (as defined in the 1940 Act) of the Company due to his affiliations with BlackRock, Inc. and its affiliates. |

Table of Contents

| Name (Age) | Position | Principal

Occupation(s) During the Past 5 Years |

Other

Directorships Held by Director | |||

| Robert

H. Silver (59) |

Director

(since 2007); Independent Chairman (since 2012). |

President and Co-Founder of The Bravitas Group, Inc. (since 2006); Director and Vice Chairman of the YMCA of Greater NYC (2001-2011); Broadway Producer (2006-2011); Co-Founder and Vice President of Parentgiving Inc. (since 2008); Director and Member of the Audit and Compensation Committee of EPAM Systems, Inc. (2006-2009); President and Chief Operating Officer of UBS Financial Services Inc. (formerly Paine Webber Inc.) (2003-2005) and various executive positions with UBS and its affiliates (1988-2005); CPA and Audit Manager of KPMG, LLP (formerly Peat Marwick Mitchell) (1977-1983). | Trustee of iShares Trust (since 2007); Director of iShares MSCI Russia Capped ETF, Inc. (since 2010); Trustee of iShares U.S. ETF Trust (since 2011); Independent Chairman of iShares Trust, iShares MSCI Russia Capped ETF, Inc. and iShares U.S. ETF Trust (since 2012). | |||

| George

G.C. Parker (75) |

Director

(since 2002). |

Dean Witter Distinguished Professor of Finance, Emeritus, Stanford University Graduate School of Business (Professor since 1973; Emeritus since 2006). | Trustee of iShares Trust (since 2000); Director of iShares MSCI Russia Capped ETF, Inc. (since 2010); Trustee of iShares U.S. ETF Trust (since 2011); Director of Tejon Ranch Company (since 1999); Director of Threshold Pharmaceuticals (since 2004); Director of Colony Financial, Inc. (since 2009); Director of First Republic Bank (since 2010). | |||

| John

E. Martinez (53) |

Director

(since 2003); Securities Lending Committee Chair (since 2012). |

Director of FirstREX Agreement Corp. (formerly EquityRock, Inc.) (since 2005). | Trustee of iShares Trust (since 2003); Director of iShares MSCI Russia Capped ETF, Inc. (since 2010); Trustee of iShares U.S. ETF Trust (since 2011). | |||

| Cecilia

H. Herbert (65) |

Director

(since 2005); Nominating and Governance Committee Chair and Equity Plus Committee Chair (since 2012). |

Director (1998-2013) and President (2007-2011) of the Board of Directors, Catholic Charities CYO; Trustee (2002-2011) and Chair of the Finance and Investment Committee (2006-2010) of the Thacher School; Member (since 1992) and Chair (1994-2005) of the Investment Committee, Archdiocese of San Francisco; Trustee and Member of the Investment Committee, WNET, the New York public broadcasting/media company (since 2011). | Trustee of iShares Trust (since 2005); Director of iShares MSCI Russia Capped ETF, Inc. (since 2010); Trustee of iShares U.S. ETF Trust (since 2011); Director of Forward Funds (34 portfolios) (since 2009). |

Table of Contents

| Name (Age) | Position | Principal

Occupation(s) During the Past 5 Years |

Other

Directorships Held by Director | |||

| Charles

A. Hurty (70) |

Director

(since 2005); Audit Committee Chair (since 2006). |

Retired; Partner, KPMG LLP (1968-2001). | Trustee of iShares Trust (since 2005); Director of iShares MSCI Russia Capped ETF, Inc. (since 2010); Trustee of iShares U.S. ETF Trust (since 2011); Director of GMAM Absolute Return Strategy Fund (1 portfolio) (since 2002); Director of SkyBridge Alternative Investments Multi-Adviser Hedge Fund Portfolios LLC (2 portfolios) (since 2002). | |||

| John

E. Kerrigan (59) |

Director

(since 2005); Fixed Income Plus Committee Chair (since 2012). |

Chief Investment Officer, Santa Clara University (since 2002). | Trustee of iShares Trust (since 2005); Director of iShares MSCI Russia Capped ETF, Inc. (since 2010); Trustee of iShares U.S. ETF Trust (since 2011). | |||

| Madhav

V. Rajan (50) |

Director

(since 2011); 15(c) Committee Chair (since 2012). |

Robert K. Jaedicke Professor of Accounting and Senior Associate Dean for Academic Affairs and Head of MBA Program, Stanford University Graduate School of Business (since 2001); Professor of Law (by courtesy), Stanford Law School (since 2005); Visiting Professor, University of Chicago (2007-2008). | Trustee

of iShares Trust (since 2011); Director of iShares MSCI Russia Capped ETF, Inc. (since 2011); Trustee of iShares U.S. ETF Trust (since 2011); Director, Cavium, Inc. (since 2013). |

| Name (Age) | Position | Principal

Occupation(s) During the Past 5 Years | ||

| Manish

Mehta (43) |

President (since 2013). | Managing Director, BlackRock, Inc. (since 2009); Chief Operating Officer for iShares (since 2009); Head of Strategy and Corporate Development, BGI (2005-2009); Chief of Staff to the CEO, BGI (2005-2009). | ||

| Jack

Gee (54) |

Treasurer

and Chief Financial Officer (since 2008). |

Managing Director, BlackRock, Inc. (since 2009); Senior Director of Fund Administration of Intermediary Investor Business, BGI (2009); Director of Fund Administration of Intermediary Investor Business, BGI (2004-2009). |

Table of Contents

| Name (Age) | Position | Principal

Occupation(s) During the Past 5 Years | ||

| Eilleen

M. Clavere (62) |

Secretary

(since 2007). |

Director of Global Fund Administration, BlackRock, Inc. (since 2009); Director of Legal Administration of Intermediary Investor Business, BGI (2006-2009); Legal Counsel and Vice President of Atlas Funds, Atlas Advisers, Inc. and Atlas Securities, Inc. (2005-2006); Counsel at Kirkpatrick & Lockhart LLP (2001-2005). | ||

| Edward

B. Baer (45) |

Vice

President and Chief Legal Officer (since 2012). |

Managing Director of Legal & Compliance, BlackRock, Inc. (since 2006); Director of Legal & Compliance, BlackRock, Inc. (2004-2006). | ||

| Scott

Radell (45) |

Executive

Vice President (since 2012). |

Managing Director, BlackRock, Inc. (since 2009); Head of Portfolio Solutions, BlackRock, Inc. (since 2009); Head of Portfolio Solutions, BGI (2007-2009); Credit Portfolio Manager, BGI (2005-2007); Credit Research Analyst, BGI (2003-2005). | ||

| Amy

Schioldager (51) |

Executive

Vice President (since 2007). |

Senior Managing Director, BlackRock, Inc. (since 2009); Global Head of Index Equity, BGI (2008-2009); Global Head of U.S. Indexing, BGI (2006-2008); Head of Domestic Equity Portfolio Management, BGI (2001-2006). | ||

| Ira

P. Shapiro (51) |

Vice

President (since 2007). |

Managing Director, BlackRock, Inc. (since 2009); Head of Strategic Product Initiatives for iShares (since 2012); Chief Legal Officer, Exchange-Traded Fund Complex (2007-2012); Associate General Counsel, BGI (2004-2009). |

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

| Name of Director | Fund | Dollar

Range of Equity Securities in the Fund |

Aggregate

Dollar Range of Equity Securities in all Registered Investment Companies Overseen by Director in Family of Investment Companies | |||

| Robert S. Kapito | None | None | None | |||

| Mark Wiedman1 | iShares Core MSCI EAFE ETF | Over $100,000 | Over $100,000 | |||

| iShares Core MSCI Emerging Markets ETF | $50,001-$100,000 | |||||

| iShares Core S&P Total U.S. Stock Market ETF | $50,001-$100,000 | |||||

| Robert H. Silver | iShares iBonds Sep 2015 AMT-Free Muni Bond ETF | Over $100,000 | Over $100,000 | |||

| iShares iBonds Sep 2016 AMT-Free Muni Bond ETF | Over $100,000 | |||||

| iShares iBonds Sep 2017 AMT-Free Muni Bond ETF | Over $100,000 | |||||

| iShares iBonds Sep 2018 AMT-Free Muni Bond ETF | Over $100,000 | |||||

| iShares Core High Dividend ETF | Over $100,000 | |||||

| iShares Core MSCI EAFE ETF | Over $100,000 | |||||

| iShares Core MSCI Emerging Markets ETF | Over $100,000 | |||||

| iShares Core MSCI Total International Stock ETF | Over $100,000 | |||||

| iShares Core S&P 500 ETF | Over $100,000 | |||||

| iShares Core S&P Mid-Cap ETF | Over $100,000 | |||||

| iShares Core S&P Small-Cap ETF | Over $100,000 | |||||

| iShares Core S&P Total U.S. Stock Market ETF | Over $100,000 | |||||

| iShares iBoxx $ Investment Grade Corporate Bond ETF | Over $100,000 |

Table of Contents

| Name of Director | Fund | Dollar

Range of Equity Securities in the Fund |

Aggregate

Dollar Range of Equity Securities in all Registered Investment Companies Overseen by Director in Family of Investment Companies | |||

| iShares J.P. Morgan USD Emerging Markets Bond ETF | $1-$10,000 | |||||

| iShares MSCI ACWI ex U.S. ETF | $1-$10,000 | |||||

| iShares MSCI BRIC ETF | $10,001-$50,000 | |||||

| iShares MSCI Emerging Markets ETF | $1-$10,000 | |||||

| iShares MSCI Frontier 100 ETF | $50,001-$100,000 | |||||

| iShares National AMT-Free Muni Bond ETF | Over $100,000 | |||||

| iShares Russell 1000 Growth ETF | Over $100,000 | |||||

| iShares Russell 1000 Value ETF | Over $100,000 | |||||

| iShares Russell 2000 ETF | $10,001-$50,000 | |||||

| iShares Russell 2000 Growth ETF | Over $100,000 | |||||

| iShares Russell 2000 Value ETF | Over $100,000 | |||||

| iShares Russell 3000 ETF | Over $100,000 | |||||

| iShares Russell Mid-Cap Growth ETF | $1-$10,000 | |||||

| iShares Russell Mid-Cap Value ETF | $1-$10,000 | |||||

| iShares Select Dividend ETF | $10,001-$50,000 | |||||

| iShares U.S. Broker-Dealers ETF | Over $100,000 | |||||

| iShares U.S. Financial Services ETF | $50,001-$100,000 | |||||

| iShares U.S. Preferred Stock ETF | Over $100,000 | |||||

| iShares U.S. Regional Banks ETF | Over $100,000 | |||||

| iShares U.S. Technology ETF | $50,001-$100,000 | |||||

| George G.C. Parker | iShares California AMT-Free Muni Bond ETF | Over $100,000 | Over $100,000 | |||

| iShares Core S&P 500 ETF | Over $100,000 | |||||

| iShares Core U.S. Aggregate Bond ETF | $10,001-$50,000 | |||||

| iShares iBoxx $ Investment Grade Corporate Bond ETF | Over $100,000 | |||||

| iShares MSCI EAFE ETF | Over $100,000 | |||||

| iShares S&P 100 ETF | Over $100,000 | |||||

| iShares Select Dividend ETF | Over $100,000 | |||||

| John E. Martinez | iShares Core MSCI Emerging Markets ETF | $50,001-$100,000 | Over $100,000 | |||

| iShares Core S&P 500 ETF | Over $100,000 | |||||

| iShares Emerging Markets Infrastructure ETF | Over $100,000 | |||||

| iShares Global Consumer Staples ETF | Over $100,000 | |||||

| iShares MSCI All Country Asia ex Japan ETF | Over $100,000 | |||||

| iShares MSCI EAFE ETF | Over $100,000 | |||||

| iShares Russell 1000 ETF | Over $100,000 |

Table of Contents

| Name of Director | Fund | Dollar

Range of Equity Securities in the Fund |

Aggregate

Dollar Range of Equity Securities in all Registered Investment Companies Overseen by Director in Family of Investment Companies | |||

| iShares Russell 1000 Value ETF | Over $100,000 | |||||

| iShares Russell 2000 ETF | Over $100,000 | |||||

| iShares TIPS Bond ETF | Over $100,000 | |||||

| Cecilia H. Herbert | iShares China Large-Cap ETF | Over $100,000 | Over $100,000 | |||

| iShares Core MSCI Emerging Markets ETF | $10,001-$50,000 | |||||

| iShares Core MSCI Total International Stock ETF | $10,001-$50,000 | |||||

| iShares Core S&P Total U.S. Stock Market ETF | $10,001-$50,000 | |||||

| iShares iBoxx $ High Yield Corporate Bond ETF | $10,001-$50,000 | |||||

| iShares International Select Dividend ETF | $1-$10,000 | |||||

| iShares MSCI EAFE ETF | $10,001-$50,000 | |||||

| iShares MSCI Emerging Markets ETF | $1-$10,000 | |||||

| iShares MSCI Japan ETF | $10,001-$50,000 | |||||

| iShares National AMT-Free Muni Bond ETF | $10,001-$50,000 | |||||

| iShares U.S. Preferred Stock ETF | $10,001-$50,000 | |||||

| Charles A. Hurty | iShares China Large-Cap ETF | $10,001-$50,000 | Over $100,000 | |||

| iShares Core High Dividend ETF | $10,001-$50,000 | |||||

| iShares Core MSCI Emerging Markets ETF | $50,001-$100,000 | |||||

| iShares Core S&P 500 ETF | $10,001-$50,000 | |||||

| iShares Global Energy ETF | $10,001-$50,000 | |||||

| iShares Global Tech ETF | $10,001-$50,000 | |||||

| iShares MSCI EAFE ETF | $10,001-$50,000 | |||||

| iShares MSCI Japan ETF | $10,001-$50,000 | |||||

| iShares North American Tech-Multimedia Networking ETF | $1-$10,000 | |||||

| iShares U.S. Energy ETF | $10,001-$50,000 | |||||

| iShares U.S. Financials ETF | $1-$10,000 | |||||

| iShares U.S. Technology ETF | $50,001-$100,000 | |||||

| John E. Kerrigan | iShares MSCI ACWI ex U.S. ETF | Over $100,000 | Over $100,000 | |||

| iShares Short-Term National AMT-Free Muni Bond ETF | Over $100,000 | |||||

| Madhav V. Rajan | iShares Core High Dividend ETF | Over $100,000 | Over $100,000 | |||

| iShares Core MSCI Emerging Markets ETF | Over $100,000 | |||||

| iShares Core S&P 500 ETF | Over $100,000 | |||||

| iShares iBoxx $ High Yield Corporate Bond ETF | $50,001-$100,000 |

Table of Contents

| Name of Director | Fund | Dollar

Range of Equity Securities in the Fund |

Aggregate

Dollar Range of Equity Securities in all Registered Investment Companies Overseen by Director in Family of Investment Companies | |||

| iShares iBoxx $ Investment Grade Corporate Bond ETF | Over $100,000 | |||||

| iShares Select Dividend ETF | Over $100,000 |

| Name of Director | iShares

Emerging Markets Dividend ETF |

Pension

or Retirement Benefits Accrued As Part of Company Expenses3 |

Estimated

Annual Benefits Upon Retirement3 |

Total

Compensation From the Fund and Fund Complex4 | ||||

| Independent Directors: | ||||||||

| Robert H. Silver | $ 337 | Not Applicable | Not Applicable | $ 325,000 | ||||

| George G.C. Parker | 285 | Not Applicable | Not Applicable | 275,000 | ||||

| John E. Kerrigan | 301 | Not Applicable | Not Applicable | 315,882 | ||||

| Charles A. Hurty | 327 | Not Applicable | Not Applicable | 315,000 | ||||

| Cecilia H. Herbert | 317 | Not Applicable | Not Applicable | 305,000 | ||||

| John E. Martinez | 301 | Not Applicable | Not Applicable | 290,000 | ||||

| Madhav V. Rajan | 301 | Not Applicable | Not Applicable | 301,765 | ||||

| Interested Directors: | ||||||||

| Robert S. Kapito | $ 0 | Not Applicable | Not Applicable | $ 0 | ||||

| Mark Wiedman1 | 0 | Not Applicable | Not Applicable | 0 | ||||

| Michael Latham2 | 0 | Not Applicable | Not Applicable | 0 |

Table of Contents

| Name of Director | iShares

Emerging Markets Dividend ETF |

Pension

or Retirement Benefits Accrued As Part of Company Expenses3 |

Estimated

Annual Benefits Upon Retirement3 |

Total

Compensation From the Fund and Fund Complex4 | ||||

| 1 | Appointed to serve as an Interested Director effective December 31, 2013. |

| 2 | Served as an Interested Director through December 31, 2013. |

| 3 | No Director or officer is entitled to any pension or retirement benefits from the Company. |

| 4 | Includes compensation for service on the Boards of Trustees for iShares Trust and iShares U.S. ETF Trust and the Board of Directors of iShares MSCI Russia Capped ETF, Inc. |

| Name and Address | Percentage

of Ownership | |

| National

Financial Services LLC 200 Liberty Street 5th Floor New York, NY 10281 |

34.76% | |

| Merrill

Lynch, Pierce Fenner & Smith Safekeeping 101 Hudson Street 8th Floor Jersey City, NJ 07302 |

14.67% | |

| Morgan

Stanley & Co. Harborside Financial Center Plaza 3, 1st Floor Jersey City, NJ 07311 |

7.25% | |

| Charles

Schwab & Co., Inc. 111 Pavonia Avenue Jersey City, NJ 07310 |

6.08% |

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

| Management

Fee |

Fund

Inception Date |

Management

Fees Paid for Fiscal Year Ended April 30, 2014 |

Management

Fees Paid for Fiscal Year Ended April 30, 2013 |

Management

Fees Paid for Fiscal Year Ended April 30, 2012 | ||||

| 0.68% | 02/23/12 | $1,133,588 | $382,587 | $14,853 |

| Christopher Bliss | ||||

| Types of Accounts | Number | Total Assets | ||

| Registered Investment Companies | 51 | $ 75,000,000,000 | ||

| Other Pooled Investment Vehicles | 290 | 767,000,000,000 | ||

| Other Accounts | 296 | 463,000,000,000 | ||

| Accounts with Incentive-Based Fee Arrangements | 0 | N/A |

Table of Contents

| Matthew Goff | ||||

| Types of Accounts | Number | Total Assets | ||

| Registered Investment Companies | 248 | $544,000,000,000 | ||

| Other Pooled Investment Vehicles | 3 | 13,000,000,000 | ||

| Other Accounts | 2 | 185,500,000 | ||

| Accounts with Incentive-Based Fee Arrangements | 0 | N/A |

| Diane Hsiung | ||||

| Types of Accounts | Number | Total Assets | ||

| Registered Investment Companies | 252 | $546,000,000,000 | ||

| Other Pooled Investment Vehicles | 6 | 89,300,000 | ||

| Other Accounts | 1 | 19,000,000 | ||

| Accounts with Incentive-Based Fee Arrangements | 0 | N/A |

| Jennifer Hsui | ||||

| Types of Accounts | Number | Total Assets | ||

| Registered Investment Companies | 252 | $546,000,000,000 | ||

| Other Pooled Investment Vehicles | 0 | N/A | ||

| Other Accounts | 0 | N/A | ||

| Accounts with Incentive-Based Fee Arrangements | 0 | N/A |

| Greg Savage | ||||

| Types of Accounts | Number | Total Assets | ||

| Registered Investment Companies | 319 | $609,000,000,000 | ||

| Other Pooled Investment Vehicles | 91 | 89,300,000,000 | ||

| Other Accounts | 2 | 185,500,000,000 | ||

| Accounts with Incentive-Based Fee Arrangements | 0 | N/A |

Table of Contents

| Christopher Bliss | ||||

| Types of Accounts | Number

of Other Accounts with Performance Fees Managed by Portfolio Manager |

Aggregate

of Total Assets | ||

| Registered Investment Companies | N/A | N/A | ||

| Other Pooled Investment Vehicles | N/A | N/A | ||

| Other Accounts | N/A | N/A |

| Matthew Goff | ||||

| Types of Accounts | Number

of Other Accounts with Performance Fees Managed by Portfolio Manager |

Aggregate

of Total Assets | ||

| Registered Investment Companies | N/A | N/A | ||

| Other Pooled Investment Vehicles | N/A | N/A | ||

| Other Accounts | N/A | N/A |

| Diane Hsiung | ||||

| Types of Accounts | Number

of Other Accounts with Performance Fees Managed by Portfolio Manager |

Aggregate

of Total Assets | ||

| Registered Investment Companies | N/A | N/A | ||

| Other Pooled Investment Vehicles | N/A | N/A | ||

| Other Accounts | N/A | N/A |

| Jennifer Hsui | ||||

| Types of Accounts | Number

of Other Accounts with Performance Fees Managed by Portfolio Manager |

Aggregate

of Total Assets | ||

| Registered Investment Companies | N/A | N/A | ||

| Other Pooled Investment Vehicles | N/A | N/A | ||

| Other Accounts | N/A | N/A |

| Greg Savage | ||||

| Types of Accounts | Number

of Other Accounts with Performance Fees Managed by Portfolio Manager |

Aggregate

of Total Assets | ||

| Registered Investment Companies | N/A | N/A | ||

| Other Pooled Investment Vehicles | N/A | N/A | ||

| Other Accounts | N/A | N/A |

Table of Contents

Table of Contents

| Fund

Inception Date |

Administration,

Custodian, Transfer Agency Expenses Paid During Fiscal Year Ended April 30, 2014 |

Administration,

Custodian, Transfer Agency Expenses Paid During Fiscal Year Ended April 30, 2013 |

Administration,

Custodian, Transfer Agency Expenses Paid During Fiscal Year Ended April 30, 2012 | |||

| 02/23/12 | $57,635 | $30,238 | $5,628 |

| Fund

Inception Date |

Distributor

Compensation Paid During Fiscal Year Ended April 30, 2014 |

Distributor

Compensation Paid During Fiscal Year Ended April 30, 2013 |

Distributor

Compensation Paid From April 1, 2012 to April 30, 20121 |

Distributor

Compensation Paid From February 23, 2012 to March 31, 20122 | ||||

| 02/23/12 | $7,660 | $7,457 | $827 | $1,712 |

| 1 | BRIL serves as the distributor to the Fund effective April 1, 2012. These fees reflect payments made to SEI, acting as an agent of the Distributor. |

| 2 | SEI served as the distributor to the Fund through March 31, 2012. |

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

| Fund

Inception Date |

Brokerage

Commissions Paid During Fiscal Year Ended April 30, 2014 |

Brokerage

Commissions Paid During Fiscal Year Ended April 30, 2013 |

Brokerage

Commissions Paid During Fiscal Year Ended April 30, 2012 | |||

| 02/23/12 | $106,226 | $72,996 | $4,318 |

Table of Contents

| Fiscal Year ended April 30, 2014 | Fiscal Year ended April 30, 2013 | |||

| 44% | 41% |

Table of Contents

Table of Contents

Table of Contents

| Shares

Per Creation Unit |

Value

Per Creation Unit (U.S.$) | |

| 50,000 | $2,443,500 |

Table of Contents

Table of Contents

Table of Contents

Table of Contents

| Standard

Creation Transaction Fee |

Maximum

Additional Charge* | |

| $3,000 | 3.0% |

| * | As a percentage of the net asset value per Creation Unit. |

Table of Contents

| Standard

Redemption Transaction Fee |

Maximum

Additional Charge* | |

| $3,000 | 2.0% |

| * | As a percentage of the net asset value per Creation Unit, inclusive of the standard redemption transaction fee. |

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

| 2014 | ||||||

| Country | Trade

Date |

Settlement

Date |

Number

of Days to Settle | |||

| China | 01/27/14 | 02/10/14 | 14 | |||

| 01/28/14 | 02/11/14 | 14 | ||||

| 01/29/14 | 02/12/14 | 14 | ||||

| 04/28/14 | 05/08/14 | 10 | ||||

| 04/29/14 | 05/09/14 | 10 | ||||

| 04/30/14 | 05/12/14 | 12 | ||||

| 09/26/14 | 10/08/14 | 12 | ||||

| 09/29/14 | 10/09/14 | 10 | ||||

Table of Contents

| 2014 | ||||||

| Country | Trade

Date |

Settlement

Date |

Number

of Days to Settle | |||

| 09/30/14 | 10/10/14 | 10 | ||||

| The Czech Republic | 12/19/14 | 12/29/14 | 10 | |||

| 12/22/14 | 12/30/14 | 8 | ||||

| 12/23/14 | 01/02/15 | 10 | ||||

| Egypt | 01/06/14 | 01/14/14 | 8 | |||

| 04/14/14 | 04/22/14 | 8 | ||||

| 04/15/14 | 04/23/14 | 8 | ||||

| 04/16/14 | 04/24/14 | 8 | ||||

| 04/17/14 | 04/27/14 | 10 | ||||

| 07/21/14 | 07/31/14 | 10 | ||||

| 07/22/14 | 08/03/14 | 12 | ||||

| 07/24/14 | 08/04/14 | 11 | ||||

| 09/29/14 | 10/07/14 | 8 | ||||

| 09/30/14 | 10/08/14 | 8 | ||||

| 10/01/14 | 10/09/14 | 8 | ||||

| 10/02/14 | 10/12/14 | 10 | ||||

| Hungary | 12/19/14 | 12/29/14 | 10 | |||

| 12/22/14 | 12/30/14 | 8 | ||||

| 12/23/14 | 12/31/14 | 8 | ||||

| Indonesia | 07/23/14 | 08/04/14 | 12 | |||

| 07/24/14 | 08/05/14 | 12 | ||||

| 07/25/14 | 08/06/14 | 12 | ||||

| 12/19/14 | 12/29/14 | 10 | ||||

| 12/22/14 | 12/30/14 | 8 | ||||

| 12/23/14 | 01/02/15 | 11 | ||||

| Malaysia | 01/27/14 | 02/04/14 | 8 | |||

| 01/28/14 | 02/05/14 | 8 | ||||

| 01/29/14 | 02/06/14 | 8 | ||||

| 07/23/14 | 07/31/14 | 8 | ||||

| 07/24/14 | 08/01/14 | 8 | ||||

| 07/25/14 | 08/04/14 | 10 | ||||

| The Philippines | 12/19/14 | 12/29/14 | 10 | |||

| 12/22/14 | 01/02/15 | 11 | ||||

| 12/23/14 | 01/05/15 | 13 | ||||

| 12/28/14 | 01/05/15 | 8 | ||||

| 12/29/14 | 01/06/15 | 8 | ||||

| Russia | 12/27/14 | 01/09/15 | 13 | |||

| 12/30/14 | 01/10/15 | 11 | ||||

| 12/31/14 | 01/13/15 | 13 | ||||

| 12/24/14 | 01/09/15 | 16 | ||||

| 12/26/14 | 01/12/15 | 17 | ||||

| 12/29/14 | 01/13/15 | 15 | ||||

Table of Contents

| 2014 | ||||||

| Country | Trade

Date |

Settlement

Date |

Number

of Days to Settle | |||

| South Africa | 03/14/14 | 03/24/14 | 10 | |||

| 03/17/14 | 03/25/14 | 8 | ||||

| 03/18/14 | 03/26/14 | 8 | ||||

| 03/19/14 | 03/27/14 | 8 | ||||

| 03/20/14 | 03/28/14 | 8 | ||||

| 04/11/14 | 04/22/14 | 9 | ||||

| 04/14/14 | 04/23/14 | 9 | ||||

| 04/15/14 | 04/24/14 | 9 | ||||

| 04/16/14 | 04/25/14 | 9 | ||||

| 04/17/14 | 04/29/14 | 12 | ||||

| 04/22/14 | 04/30/14 | 8 | ||||

| 04/23/14 | 05/02/14 | 9 | ||||

| 04/24/14 | 05/05/14 | 11 | ||||

| 04/25/14 | 05/06/14 | 11 | ||||

| 04/29/14 | 05/07/14 | 8 | ||||

| 04/30/14 | 05/08/14 | 8 | ||||

| 06/09/14 | 06/17/14 | 8 | ||||

| 06/10/14 | 06/18/14 | 8 | ||||

| 06/11/14 | 06/19/14 | 8 | ||||

| 06/12/14 | 06/20/14 | 8 | ||||

| 06/13/14 | 06/23/14 | 10 | ||||

| 09/17/14 | 09/25/14 | 8 | ||||

| 09/18/14 | 09/26/14 | 8 | ||||

| 09/19/14 | 09/29/14 | 10 | ||||

| 09/22/14 | 09/30/14 | 8 | ||||

| 09/23/14 | 10/01/14 | 8 | ||||

| 12/09/14 | 12/17/14 | 8 | ||||

| 12/10/14 | 12/18/14 | 8 | ||||

| 12/11/14 | 12/19/14 | 8 | ||||

| 12/12/14 | 12/22/14 | 10 | ||||

| 12/15/14 | 12/23/14 | 8 | ||||

| 12/18/14 | 12/29/14 | 11 | ||||

| 12/19/14 | 12/30/14 | 11 | ||||

| 12/22/14 | 12/31/14 | 9 | ||||

| 12/23/14 | 01/02/15 | 10 | ||||

| 12/24/14 | 01/05/15 | 12 | ||||

| 12/29/14 | 01/06/15 | 8 | ||||

| 12/30/14 | 01/07/15 | 8 | ||||

| 12/31/14 | 01/08/15 | 8 | ||||

| Taiwan | 01/24/14 | 02/05/14 | 12 | |||

| 01/27/14 | 02/06/14 | 10 | ||||

| 2015 | ||||||

| Country | Trade

Date |

Settlement

Date |

Number

of Days to Settle | |||

| China | 02/13/15 | 02/25/15 | 12 | |||

| 02/16/15 | 02/26/15 | 10 | ||||

Table of Contents

| 2015 | ||||||

| Country | Trade

Date |

Settlement

Date |

Number

of Days to Settle | |||

| 02/17/15 | 02/27/15 | 10 | ||||

| 09/28/15 | 10/08/15 | 10 | ||||

| 09/29/15 | 10/09/15 | 10 | ||||

| 09/30/15 | 10/12/15 | 12 | ||||

| Russia | 12/24/15 | 01/11/16 | 18 | |||

| 12/28/15 | 01/15/16 | 15 | ||||

| 12/29/15 | 01/18/16 | 18 | ||||

| South Africa | 03/27/15 | 04/07/15 | 11 | |||

| 03/30/15 | 04/08/15 | 9 | ||||

| 03/31/15 | 04/09/15 | 9 | ||||

| 04/01/15 | 04/10/15 | 9 | ||||

| 04/02/15 | 04/13/15 | 11 | ||||

| 04/20/15 | 04/28/15 | 8 | ||||

| 04/21/15 | 04/29/15 | 8 | ||||

| 04/22/15 | 04/30/15 | 8 | ||||

| 04/23/15 | 05/01/15 | 8 | ||||

| 04/23/15 | 05/04/15 | 11 | ||||

| 04/24/15 | 05/05/15 | 11 | ||||

| 04/28/15 | 05/06/15 | 8 | ||||

| 04/29/15 | 05/07/15 | 8 | ||||

| 04/30/15 | 05/08/15 | 8 | ||||

| 06/09/15 | 06/17/15 | 8 | ||||

| 06/10/15 | 06/18/15 | 8 | ||||

| 06/11/15 | 06/19/15 | 8 | ||||

| 06/12/15 | 06/22/15 | 10 | ||||

| 06/15/15 | 06/23/15 | 8 | ||||

| 08/03/15 | 08/11/15 | 8 | ||||

| 08/04/15 | 08/12/15 | 8 | ||||

| 08/05/15 | 08/13/15 | 8 | ||||

| 08/06/15 | 08/14/15 | 8 | ||||

| 08/07/15 | 08/17/15 | 10 | ||||

| 09/17/15 | 09/25/15 | 8 | ||||

| 09/18/15 | 09/28/15 | 10 | ||||

| 09/21/15 | 09/29/15 | 8 | ||||

| 09/22/15 | 09/30/15 | 8 | ||||

| 09/23/15 | 10/01/15 | 8 | ||||

| 12/09/15 | 12/17/15 | 8 | ||||

| 12/10/15 | 12/18/15 | 8 | ||||

| 12/11/15 | 12/21/15 | 10 | ||||

| 12/14/15 | 12/22/15 | 8 | ||||

| 12/15/15 | 12/23/15 | 8 | ||||

| 12/18/15 | 12/28/15 | 10 | ||||

| 12/21/15 | 12/29/15 | 8 | ||||

| 12/22/15 | 12/30/15 | 8 | ||||

| 12/23/15 | 12/31/15 | 8 | ||||

| 12/24/15 | 01/04/16 | 11 | ||||

| 12/28/15 | 01/05/16 | 8 | ||||

| 12/29/15 | 01/06/16 | 8 | ||||

Table of Contents

| 2015 | ||||||

| Country | Trade

Date |

Settlement

Date |

Number

of Days to Settle | |||

| 12/30/15 | 01/07/16 | 8 | ||||

| 12/31/15 | 01/08/16 | 8 | ||||

| Taiwan | 02/16/15 | 02/24/15 | 8 | |||

| 02/17/15 | 02/25/15 | 8 | ||||

| Thailand | 04/08/15 | 04/16/15 | 8 | |||

| 04/09/15 | 04/17/15 | 8 | ||||

| 04/10/15 | 04/20/15 | 10 | ||||

| * | These worst-case redemption cycles are based on information regarding regular holidays, which may be out of date. Based on changes in holidays, longer (worse) redemption cycles are possible. |

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

(as revised January 7, 2015)

| Fund | Ticker | Stock Exchange | ||

| iShares MSCI Emerging Markets Horizon ETF (the “Fund”) | EMHZ | BATS |

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

Table of Contents

| • | The Fund generally supports the board’s nominees in the election of directors and generally supports proposals that strengthen the independence of boards of directors; |

| • | When a director has committed himself or herself to service on more than four public company boards (but no more than six public company boards in most circumstances), the Fund will consider such director’s individual circumstances in determining whether the director will be able to commit sufficient focus and time to a particular company; |

| • | The Fund generally defers to an issuer’s choice of auditors so long as the corporate auditors represent the interests of shareholders and provide an independent view of the propriety of financial reporting decisions of management; |

| • | The Fund generally favors disclosure of a company’s compensation and benefits policies and opposes excessive compensation, but believes that compensation matters are normally best determined by a company’s board of directors; |

| • | The Fund generally expects to support capital structure requests that it believes enhance the rights of common shareholders and oppose requests that appear to be unreasonably dilutive; |

Table of Contents