UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

_____________________________________________________________________________

FORM 10-K

_____________________________________________________________________________

x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2018

OR

¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

FOR THE TRANSITION PERIOD FROM TO

COMMISSION FILE NUMBER 000-26058

_____________________________________________________________________________

(Exact name of Registrant as specified in its charter)

_____________________________________________________________________________

FLORIDA | 59-3264661 | |

State or other jurisdiction of incorporation or organization | IRS Employer Identification No. | |

1001 EAST PALM AVENUE, TAMPA, FLORIDA | 33605 | |

Address of principal executive offices | Zip Code | |

REGISTRANT’S TELEPHONE NUMBER, INCLUDING AREA CODE: (813) 552-5000

_____________________________________________________________________________

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

TITLE OF EACH CLASS | NAME OF EACH EXCHANGE ON WHICH REGISTERED | |

Common Stock, $0.01 par value | The NASDAQ Stock Market LLC (NASDAQ Global Select Market) | |

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT:

None

_____________________________________________________________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “non-accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | x | Accelerated filer | ¨ | |||

Non-accelerated filer | ¨ (Do not check if a smaller reporting company) | Smaller reporting company | ¨ | |||

Emerging growth filer | ¨ | |||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act.): Yes ¨ No x

The aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold as of the last business day of the registrant’s most recently completed second fiscal quarter, June 30, 2018, was $786,439,764 . For purposes of this determination, common stock held by each officer and director and by each person who owns 10% or more of the registrant’s outstanding common stock have been excluded in that such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes.

The number of shares outstanding of the registrant’s common stock as of February 20, 2019 was 25,848,178 .

DOCUMENTS INCORPORATED BY REFERENCE:

Document | Parts Into Which Incorporated | |

Portions of Proxy Statement for the Annual Meeting of Shareholders scheduled to be held April 23, 2019 (“Proxy Statement”) | Part III | |

KFORCE INC.

ANNUAL REPORT ON FORM 10-K FOR THE FISCAL YEAR ENDED DECEMBER 31, 2018

TABLE OF CONTENTS

Item 1. | ||

Item 1A. | ||

Item 1B. | ||

Item 2. | ||

Item 3. | ||

Item 4. | ||

Item 5. | ||

Item 6. | ||

Item 7. | ||

Item 7A. | ||

Item 8. | ||

Item 9. | ||

Item 9A. | ||

Item 9B. | ||

Item 10. | ||

Item 11. | ||

Item 12. | ||

Item 13. | ||

Item 14. | ||

Item 15. | ||

Item 16. | ||

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

References in this document to “the Registrant,” “Kforce,” “the Company,” “we,” “the Firm,” “management,” “our” or “us” refer to Kforce Inc. and its subsidiaries, except where the context otherwise requires or indicates.

This report, particularly Item 1. Business, Item 1A. Risk Factors, and Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) and the documents we incorporate into this report contain certain statements that are, or may be deemed to be, forward-looking statements within the meaning of that term in Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), and are made in reliance upon the protections provided by such acts for forward-looking statements. Such statements may include, but may not be limited to, projections of financial or operational performance, our beliefs regarding potential government actions or changes in laws and regulations, anticipated costs and benefits of proposed acquisitions, divestitures and investments, effects of interest rate variations, financing needs or plans, estimates concerning the effects of litigation or other disputes, the occurrence of unanticipated expenses, estimates concerning our ability to collect on our trade accounts receivable, developments within the staffing sector including, but not limited to, the penetration rate (the percentage of temporary staffing to total employment) and growth in temporary staffing, a reduction in the supply of consultants and candidates or the Firm’s ability to attract such individuals, estimates concerning goodwill impairment, delays or termination or the failure to obtain awards, task orders or funding under contracts, changes in client demand for Firm services and our ability to adapt to such changes, the entry of new competitors in the market, the ability of the Firm to maintain and attract clients in the face of changing economic or competitive conditions, as well as assumptions as to any of the foregoing and all statements that are not based on historical fact but rather reflect our current expectations concerning future results and events. For a further list and description of various risks, relevant factors and uncertainties that could cause future results or events to differ materially from those expressed or implied in our forward-looking statements, refer to the Risk Factors and MD&A sections. In addition, when used in this discussion, the terms “anticipate,” “assume,” “estimate,” “expect,” “intend,” “plan,” “believe,” “will,” “may,” “likely,” “could,” “should,” “future” and variations thereof and similar expressions are intended to identify forward-looking statements.

Forward-looking statements are inherently subject to risks and uncertainties, some of which cannot be predicted. Future events and actual results could differ materially from those set forth in or underlying the forward-looking statements. Readers are cautioned not to place undue reliance on any forward-looking statements contained in this report, which speak only as of the date of this report. Kforce undertakes no obligation to update any forward-looking statements.

3

PART I

ITEM 1. BUSINESS.

Company Overview

Kforce Inc. and its subsidiaries (collectively, “Kforce”) provide professional staffing services and solutions to clients through the following segments: Technology (“Tech”); Finance and Accounting (“FA”); and Government Solutions (“GS”). Kforce provides staffing services and solutions on both a temporary (“Flex”) and permanent (“Direct Hire”) basis. We operate through our corporate headquarters in Tampa, Florida with approximately 60 field offices located throughout the U.S. Kforce was incorporated in 1994 but its predecessor companies have been providing staffing services since 1962. Kforce completed its Initial Public Offering in August 1995.

Kforce serves clients across many industries and geographies as well as companies of all sizes with a particular focus on Fortune 1000 and similarly-sized companies. We also provide services and solutions as a prime contractor and subcontractor to the U.S. Federal Government (the “Federal Government”) as well as state and local governments. We believe that our portfolio of service offerings is focused in areas of expected growth and are a key contributor to our long-term financial stability. Our 10 largest clients represented approximately 25% of revenue and no single client accounted for more than 5% of total revenue for the year ended December 31, 2018.

Substantially all of our revenues are derived from U.S. domestic operations. The asset sale of Kforce Global Solutions, Inc., (“Global”) a wholly-owned subsidiary located in the Philippines, was completed in September 2017. This sale did not meet the definition of discontinued operations. Global was included in our Tech segment and contributed approximately 1% of revenue in 2017 and 2016.

Our quarterly operating results can be affected by:

• | the number of billing days in a particular quarter; |

• | the seasonality of our clients’ businesses; |

• | increased holidays and vacation days taken, which is usually highest in the fourth quarter of each calendar year; and |

• | increased costs as a result of certain annual U.S. state and federal employment tax resets that occur at the beginning of each calendar year, which negatively impacts our gross profit and overall profitability in the first fiscal quarter of each calendar year. |

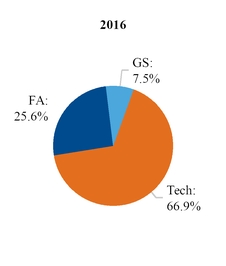

The following charts depict the percentage of our total revenue for each of our segments for the years ended December 31, 2018, 2017 and 2016:

For additional segment financial data see Note 2 – “Reportable Segments” in the Notes to Consolidated Financial Statements, included in Item 8. Financial Statements and Supplementary Data of this report.

4

Tech Segment

Our largest segment, Tech, provides both Flex and Direct Hire services to our clients, focusing primarily on areas of information technology such as systems/applications architecture and development, project management, enterprise data management, business intelligence, artificial intelligence, machine learning, network architecture and security. Within our Tech segment, we provide service to clients in a variety of industries with a strong footprint in the financial services, communications and insurance services and also to Federal government integrators. Revenue for our Tech segment increased 9.1% to $990.1 million in 2018 on a year-over-year basis. The average bill rate for our Tech segment in 2018 was approximately $73 per hour.

The September 2018 report published by Staffing Industry Analysts (“SIA”) stated that temporary technology staffing is expected to experience growth of 3% in 2019. Digital transformation, as a general trend, is driving organizations across all industries to increase their technology investments as competition and the speed of change intensifies. Nontraditional competitors are also entering new end markets; thus, putting increased pressure on companies to invest in innovation and the evolution of their business models. We believe these secular drivers will transcend traditional cyclical patterns as our clients' business models adjust. At the macro level, demand is also being driven by an ever-changing and complex regulatory and employment law environment, which increases the overall cost of employment for many companies. These factors, among others, are continuing to drive companies to look to temporary staffing providers, such as Kforce, to meet their human capital needs.

FA Segment

Our FA segment provides both Flex and Direct Hire services to our clients in areas such as general accounting, business analysis, accounts payable, accounts receivable, financial analysis and reporting, taxation, budget preparation and analysis, mortgage and loan processing, cost analysis, professional administration, outsourced functional support, credit and collections, audit services and systems and controls analysis and documentation. Within our FA segment, we provide services to clients in a variety of industries with a strong footprint in the financial services, healthcare and government sectors. Revenue for our FA segment decreased 9.3% to $313.8 million in 2018 on a year-over-year basis. The average bill rate for our FA segment in 2018 was approximately $35 per hour. The September 2018 report published by SIA stated that finance and accounting temporary staffing is expected to experience growth of 4% in 2019.

GS Segment

Our GS segment provides staffing services and solutions to the Federal Government as both a prime contractor and a subcontractor in the fields of information technology and finance and accounting. GS offers integrated business solutions to its clients in areas including but not limited to: information technology infrastructure transformation, healthcare informatics, data and knowledge management and analytics, research and development, audit readiness, financial management and accounting. GS contracts are concentrated among clients, such as the U.S. Department of Veteran Affairs, and the types of services and support that have historically been less likely to be impacted by sequestration threats and budget constraints, though a prolonged government shutdown could be expected to negatively impact GS revenue. Revenue for our GS segment increased 9.7% to $114.4 million in 2018. Our GS segment also includes a product business specialized in manufacturing and delivering trauma-training manikins, which accounted for approximately 14% of total GS revenue in 2018. The majority of GS services are supplied to the Federal Government (or through a prime contractor to the Federal Government) through field offices located in the Washington, D.C. metropolitan area and San Antonio and Austin, Texas.

Our backlog represents only those U.S. government contracts and subcontracts for which funding has been provided, excluding renewal option years. Our backlog was $47.4 million as of December 31, 2018 as compared to $59.3 million as of December 31, 2017.

Flex Revenue

Flex revenue represents approximately 96% of total revenue over the last three fiscal years. We provide our clients with qualified individuals (“consultants”) on a temporary basis when it is determined that they have the appropriate skills and experience and are the right match for our clients. We utilize a diversified set of recruitment platforms and databases to identify consultants who are actively seeking employment. These consultants can either be directly employed by Kforce, qualified independent contractors or foreign nationals sponsored by Kforce. Our success is dependent upon our internal employees’ (“associates”) ability to: (1) acknowledge, understand and participate in creating solutions for our clients’ needs; (2) determine and understand the experience and capabilities of the consultants being recruited; and (3) ensure excellence in delivering and managing the client-consultant relationship. We believe proper execution by our associates and consultants directly impacts the longevity of the assignments, increases the likelihood of generating repeat business with our clients and fosters a better experience for our consultants, which has a direct correlation to their redeployment.

5

The key drivers of Flex revenue are the number of consultant assignments and billable hours, the bill rate per hour and, to a limited extent, the amount of billable expenses incurred by Kforce. Our Flex gross profit is determined by deducting related costs of employment for consultants, including compensation, payroll taxes, certain fringe benefits and subcontractor costs from Flex revenue. Associate and field management compensation, payroll taxes and other fringe benefits are included in selling, general and administrative expenses (“SG&A”), along with other customary costs such as administrative and corporate costs. The Flex business model involves attempting to maximize the number of billable hours and bill rates, while managing consultant pay rates and benefit costs, as well as compensation and benefits for our associates.

Direct Hire Revenue

Our Direct Hire business involves locating qualified individuals (“candidates”) for permanent placement with our clients. Direct Hire revenue represents less than 4% of total revenue over the last three fiscal years; although it is a smaller portion of our business, it continues to be an important capability in ensuring that we can meet the talent needs of our clients through whatever means they prefer. We recruit candidates using methods that are consistent with Flex consultants. Candidate searches are generally performed on a contingency basis (as opposed to a retained search), therefore fees are only earned if the candidates are ultimately hired by our clients. The typical fee structure is based upon a percentage of the candidate’s annual compensation in their first year of employment, which is known or can be estimated at the time of placement.

The key drivers of Direct Hire revenue are the number of placements and the associated placement fee. Direct Hire revenue also includes conversion revenue, which may occur when a consultant initially assigned to a client on a temporary basis is later converted to a permanent placement for a fee. Direct Hire revenue is recognized net of an allowance for “fallouts,” which occur when candidates do not complete the applicable contingency period (typically 90 days or less). There are no consultant payroll costs associated with Direct Hire placements, thus, all Direct Hire revenue increases gross profit by the full amount of the fee. Direct Hire associate commissions, compensation and benefits are included in SG&A.

Industry Overview

The professional staffing industry is made up of thousands of companies, most of which are small local firms providing limited service offerings to a relatively small local client base. A report published by SIA in 2018 indicated that Kforce is one of the 10 largest publicly-traded specialty staffing firms in the U.S.

Based upon previous economic cycles experienced by Kforce, we believe that times of sustained economic recovery generally stimulate demand for additional temporary workers in the U.S. and, conversely, an economic slowdown results in a contraction in demand for additional temporary workers in the U.S. From an economic standpoint, temporary employment figures and trends are important indicators of staffing demand, which continued to be positive during 2018, based on data published by the Bureau of Labor Statistics and SIA. The percentage of temporary staffing to total employment (penetration rate) and unemployment rate was 2.1% and 3.9%, respectively, in December 2018. Total non-farm employment was up 1.8% year-over-year as of December 2018, and temporary help employment was up 3.3% year-over-year. In addition, the college-level unemployment rate, which we believe serves as a proxy for professional employment and therefore aligns well with the consultant and candidate population that Kforce most typically serves, was 2.1% in December 2018. Further, we believe that the unemployment rate in the specialties we serve, especially in certain technology skill sets, is lower than the published averages, which we believe speaks to the demand environment in which we are operating.

According to a SIA in September 2018, the technology temporary staffing industry and finance and accounting temporary staffing industry are expected to generate projected revenues of $32.0 billion and $8.5 billion, respectively, in 2019 and based on these projected revenues, our current market share is approximately 3% and 4%, respectively. Our business strategies are sharply focused around expanding our share of the U.S. temporary staffing industry and further penetrating our existing clients’ human capital needs.

Business Strategies

Our primary objectives are driving long-term shareholder value by achieving above-market revenue growth, making prudent investments to enhance efficiency and effectiveness within our operating model and significantly improving levels of operating profitability. We believe the following strategies will help us achieve our objectives.

Improving Productivity of our Talent. We believe that it is critical to provide our associates with high quality tools to effectively and efficiently perform their roles, to better evaluate business opportunities and to advance the value we bring to our clients and consultants. We continue to enhance our sales methodologies and processes in ways we believe will allow us to better evaluate and shape business opportunities with our clients as well as train our sales associates on our consistent and uniform methodology.

6

During 2018, we completed the deployment of a new time and expense application for our consultants and clients as well as a new expense application for our associates. In addition, we continue to make enhancements to our business and data intelligence capabilities as well as our customer relationship management system. We also began investing in a new talent relationship management system that we expect will better leverage our delivery strategies and processes and improve our capabilities. These investments are part of a multi-year effort to replace and upgrade our technology tools to equip our associates with improved capabilities to deliver exceptional service to our clients, consultants and candidates and improve the productivity of our associates and the scalability of our organization.

Enhancing our Client Relationships. We strive to differentiate ourselves by working collaboratively with our clients to better understand their business challenges and help them attain their organizational objectives. This collaboration focuses on building a consultative partnership rather than a transactional client relationship, which increases the intimacy with our clients and improves our ability to offer higher value and a broader array of services and support to our clients. To accomplish this, we align our revenue-generating talent with the appropriate clients based on their experience with markets, products and industries.

We measure our success in building long-lasting relationships with our clients using staffing industry benchmarks and surveys conducted by a specialized, independent third-party provider. Our client ratings compare very favorably against staffing industry averages and give us helpful insights directly from our clients on how to continue improving our relationships. We believe long-lasting relationships with our clients is a critical element in revenue growth.

Improving the Job Seeker Experience. Our consultants are a critical component to our business and essential in sustaining our client relationships. We are focused on effective and efficient processes and tools to find and attract prospective consultants, matching them to a client assignment and supporting them during their tenure with Kforce. Our success in this regard would be expected to positively influence the tenure and loyalty of our consultants and be their employer of choice, thus enabling us to deliver the highest quality talent to our clients.

We measure the quality of our service to and support of our consultants using staffing industry benchmarks and surveys conducted by a specialized, independent third-party provider. Our consultant ratings, similar to our client ratings, compare very favorably against staffing industry averages and give us helpful insights directly from our consultants on where and how we can continue improving our service during the various phases of our relationship.

Competition

We operate in a highly competitive and fragmented staffing industry comprised of large national and local staffing firms in each of our reporting segments. The local firms are typically operator-owned, and each market generally has one or more significant competitors. We also face competition from national and regional accounting, consulting and advisory firms that offer both solutions and staffing services. However, we believe that our U.S. geographic presence, concentration of service offerings in areas of greatest demand (especially technology), national delivery teams, delivery channels for foreign consultants, longevity of our brand and reputation in the market, along with our dedicated compliance and regulatory infrastructure, all provide a competitive advantage.

Many clients utilize Managed Service Providers (“MSP”) or Vendor Management Organizations (“VMO”) for the management and procurement of staffing services. Generally, MSPs and VMOs are organizations that standardize processes through the use of Vendor Management Systems (“VMS”), which are tools used to aggregate spend and measure supplier performance. VMSs can also be provided through independent providers. Typically, MSPs, VMOs and/or VMS providers charge staffing firms administrative fees ranging from 1% to 4% of total revenue. In addition, the aggregation of services by MSPs for their clients into a single program can result in significant buying power and, thus, pricing power. Therefore, the use of MSPs by our clients has, in certain instances, resulted in margin compression. Kforce does not currently provide MSP or VMO services directly to our clients; rather, our strategy has been to work with MSPs, VMOs and VMS providers that enable us to best extend our services to current and prospective clients.

We believe that the principal elements of competition in our industry are quality and availability of associates, candidates and consultants, level of service, effective monitoring of job performance, scope of geographic service and compliance orientation. To attract consultants and candidates, we emphasize on our ability to provide competitive compensation and benefits, quality and varied assignments, scheduling flexibility and permanent placement opportunities, all of which are important to Kforce being the employer of choice. Because individuals pursue other employment opportunities on a regular basis, it is important that we respond to market conditions affecting these individuals and focus on our consultant relationship objectives. Additionally, in certain markets, we have experienced significant pricing pressure as a result of our competitors’ pricing strategies. Although we believe we compete favorably with respect to these factors, we expect competition and pricing pressure to continue, which may result in us not being able to effectively compete or choosing to not participate in certain business that does not meet our profitability standard.

7

Regulatory Environment

Staffing firms are generally subject to one or more of the following types of government regulations: (1) regulation of the employer/employee relationship, such as wage and hour regulations, tax withholding and reporting, immigration regulations, social security and other retirement, anti-discrimination, employee benefits and workers’ compensation regulations; (2) registration, licensing, recordkeeping and reporting requirements; (3) worker classification regulations; and (4) substantive limitations on their operations.

In providing staffing and solution services to the Federal Government, we must comply with complex laws and regulations relating to the formation, administration and performance of Federal Government contracts. These laws and regulations create compliance risk and affect how we do business with our federal agency clients, and may impose additional costs on our business.

Because we operate in a complex regulatory environment, one of our top priorities is compliance. For more discussion of the potential impact that the regulatory environment could have on Kforce’s financial results, refer to Item 1A. Risk Factors.

Operating Employees and Personnel

As of December 31, 2018, Kforce employed approximately 2,400 associates and 11,400 consultants on assignment providing flexible staffing services and solutions to our clients. Approximately 92% of the consultants are employed directly by Kforce; the other 8% consists of qualified independent contractors. As the employer, Kforce is responsible for the employer’s share of applicable social security taxes (“FICA”), federal and state unemployment taxes, workers’ compensation insurance and other direct labor costs relating to our employees. We offer access to various health, life and disability insurance programs and other benefits for our employees. We have no collective bargaining agreements covering any of our employees, have never experienced any material labor disruption, and are unaware of any current efforts or plans to organize any of our employees.

Insurance

Kforce maintains a number of insurance policies including general liability, automobile liability, workers’ compensation and employers’ liability, liability for certain foreign exposure, umbrella and excess liability, property, crime, fiduciary, directors and officers, employment practices liability, cybersecurity, professional liability and excess health insurance coverage. These policies provide coverage subject to their terms, conditions, limits of liability and deductibles, for certain liabilities that may arise from Kforce’s operations. There can be no assurance that any of the above policies will be adequate for our needs or that we will maintain all such policies in the future.

Availability of Reports and Other Information

We make available, free of charge, through the Investor Relations page on our website, and by mailed requests addressed to Michael Blackman, Chief Corporate Development Officer, our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K, Proxy Statements on Schedule 14A and amendments to those materials filed or furnished pursuant to Section 13(a) or 15(d) of the Exchange Act as soon as reasonably practicable after we electronically submit such materials to the SEC. Our corporate website address is http://www.kforce.com. The information contained on our website, or on other websites linked to our website, is not part of this document. The SEC also provides reports, proxy and information statements on its website, free of charge, and other information regarding issuers, such as us, that file electronically with the SEC. The SEC’s website is http://www.sec.gov. Information provided on the SEC’s website is not part of this report.

8

ITEM 1A. RISK FACTORS.

The U.S. professional staffing industry in which we operate is significantly affected by fluctuations in general economic and employment conditions.

Demand for staffing services is significantly affected by the general level of economic activity and employment in the U.S. Based upon previous economic cycles that Kforce has experienced, we believe that times of sustained economic recovery generally stimulate demand for additional U.S. temporary workers and, conversely, an economic slowdown results in a contraction in demand for additional U.S. temporary workers. Even without uncertainty and volatility, it is difficult for us to forecast future demand for our services due to the inherent difficulties in forecasting the strength of economic cycles, and the short-term nature of many of our agreements. As economic activity slows, companies may defer projects for which they utilize our services or reduce their use of temporary employees before laying off permanent employees. In addition, an economic downturn could result in a reduction in the temporary staffing penetration rate, an increase in the unemployment rate and a deceleration of growth in the segments in which we and our clients operate. We may also experience more competitive pricing pressures during periods of economic downturn. Any substantial economic downturn in the U.S. or global impact on the U.S. could have a material adverse effect on our business, financial condition, and results of operations.

Kforce faces significant employment-related legal risk.

Kforce employs people internally and in the workplaces of our clients. An inherent risk of such activity includes possible claims of or relating to discrimination and harassment; wrongful termination; violations of employment rights related to employment screening or privacy issues; misclassification of workers as employees or independent contractors; violations of wage and hour requirements and other labor laws; employment of illegal aliens; criminal activity; torts; breach of contract; failure to protect confidential personal information; intentional criminal misconduct; misuse or misappropriation of client intellectual property; employee benefits; or other claims. In some cases, we are contractually obligated to indemnify our clients against such risks. Such claims may result in negative publicity, injunctive relief, criminal investigations and/or charges, civil litigation, payment by Kforce of defense costs, monetary damages or fines that may be significant, discontinuation of client relationships or other material adverse effects on our business. To reduce our exposure, we maintain policies, procedures and guidelines to promote compliance with laws, rules, regulations and best practices applicable to our business. Even claims without merit could cause us to incur significant expense or reputational harm. We also maintain insurance coverage for professional malpractice liability, fidelity, employment practices liability, and general liability in amounts and with deductibles that we believe are appropriate for our operations. However, our insurance coverage may not cover all potential claims against us, may require us to meet a deductible or may not continue to be available to us at a reasonable cost. In this regard, we face various employment-related risks not covered by insurance, such as wage and hour laws and employment tax responsibility. U.S. courts in recent years have been receiving large numbers of wage and hour class action claims alleging misclassification of overtime-eligible workers and/or failure to pay overtime-eligible workers for all hours worked.

Kforce may be exposed to unforeseeable negative acts by our personnel that could have a material adverse effect on our business.

An inherent risk of employing people internally and in the workplace of other businesses is that many of these individuals have access to client information systems and confidential information. The risks of such activity include possible acts of errors and omissions; intentional misconduct; release, misuse or misappropriation of client intellectual property, confidential information, personally identifiable information, funds, or other property; cybersecurity breaches affecting our clients and/or us; or other acts. These risks are particularly significant in our government business. Such acts may result in negative publicity or other material adverse effects on our business. In addition, these occurrences may give rise to litigation, which could be time-consuming and expensive. To reduce our exposure, we maintain policies, procedures and insurance coverage for types and amounts we believe are appropriate in light of the aforementioned exposures. There can be no assurance that the corporate policies and practices we have in place to help reduce our exposure to these risks will be effective or that we will not experience losses as a result of these risks. In addition, our insurance coverage may not cover all potential claims against us, may require us to meet a deductible or may not continue to be available to us at a reasonable cost.

Kforce may not be able to recruit and retain qualified consultants and candidates.

Kforce depends upon the abilities of its staff to attract and retain consultants and candidates, particularly technical, professional, and cleared government services individuals, who possess the skills and experience necessary to meet the staffing requirements of our clients. We must continually evaluate and upgrade our methods of attracting qualified consultants and candidates to keep pace with changing client needs and emerging technologies. We expect significant competition for individuals with proven technical or professional skills for the foreseeable future. The supply of available consultants and candidates has been constrained during this economic recovery, especially in our Tech segment. If qualified individuals are not available to us in sufficient numbers and upon economic terms acceptable to us, it could have a material adverse effect on our business.

9

Our failure to keep pace with technological change in our industry will potentially place us at a competitive disadvantage.

Our future success may depend on our ability to successfully keep pace with technological changes and advances occurring across our industry. Our business is reliant on a variety of systems and technologies, including those that support candidate searching and matching, hiring and tracking, order management, billing, and client data analytics. Our success may depend on our ability to keep pace with rapid technological changes in the development and implementation of these services. If our systems become outdated, or if our investments in technology fail to provide the expected results, then we may be unable to maintain our technological capabilities relative to our competitors and our business could be negatively affected.

Cybersecurity risks and cyber incidents could adversely affect our business and disrupt operations.

Cyberattacks or other breaches of network or information technology used by our associates and consultants, as well as risks associated with compliance on data privacy could adversely affect on our systems, services, operations and financial results. These attacks include, but are not limited to, gaining unauthorized access to digital systems for purposes of misappropriating assets or sensitive information, corrupting data, or causing operational disruption. While we have policies, procedures and systems in place to detect, prevent and deter cyberattacks or other breaches of our networks, techniques used to obtain unauthorized access or cause system interruption change frequently and may not immediately produce signs of intrusion. As a result, we may be unable to anticipate these incidents or techniques, timely discover them, or implement adequate preventative measures. We maintain cyber risk insurance, but this insurance may not be sufficient to cover all of our losses from any future breaches of our systems or information. Our information technology may not provide sufficient protection, and as a result we may lose significant information about us, our employees or clients. Other results of these incidents could include, but are not limited to, increased cybersecurity protection costs, litigation, regulatory penalties, monetary damages, and reputational damage adversely affecting client or investor confidence.

Declines in business or a loss of our major client accounts could have a material adverse effect on our revenues and financial results.

Part of our business strategy includes enhancing our service offerings and relationships with large consumers of temporary staffing, which is intended to enable us to profitably grow our revenues with these clients. However, it also creates the potential for concentrating a significant portion of our revenues among our largest clients and exposes us to increased risks arising from decreases in the volume of business from, the pricing of business with, or the possible loss of business with these clients. Organizational changes occurring within those clients, or a deterioration of their financial condition or business prospects, could reduce their need for our services and result in a significant decrease in the revenues we derive from those clients and could have a material adverse effect on our financial results.

Our collection, use and retention of personally identifiable information of our associates and consultants create risks that may harm our business.

In the ordinary course of our business, we collect and retain personal information of our associates and consultants and their dependents including, without limitation, full names, social security numbers, addresses, birth dates, and payroll-related information. We use commercially available information security technologies to protect such information in digital format. We also use security and business controls to limit access to such information and continually monitor our systems for potential breaches. However, as our reliance on technology has increased so have the risks posed to our systems, both internal and those managed by third party service providers. It is possible that the controls in place will not be able to prevent the improper disclosure of personally identifiable information of our associates and consultants in the event of a computer virus, system breach or cyberattack, particularly in light of the increasing sophistication of perpetrators. Employees or third parties (including third parties with substantially greater resources than our own, e.g. foreign governments) may be able to circumvent our security measures and acquire or misuse such information, resulting in privacy breaches, errors in the storage, use or transmission of such information, and an interruption to our operations. Privacy breaches may require notification and other remedies, which can be costly, and which may have other serious adverse consequences for our business, including regulatory penalties and fines, claims for breach of contract, claims for damages, adverse publicity, reduced demand for our services by clients and/or consultants, harm to our reputation, and regulatory oversight by state or federal agencies.

The possession and use of personal information and data in conducting our business subjects us to legislative and regulatory burdens. We may be required to incur significant expenses to comply with mandatory privacy and security standards and protocols imposed by law, regulation, industry standards or contractual obligations.

Kforce may be adversely affected by government regulation of the staffing business and of the workplace.

Our business is subject to regulation and licensing in many states. There can be no assurance that we will be able to continue to obtain all necessary licenses or approvals or that the cost of compliance will not prove to be material. If we fail to comply, such failure could materially adversely affect Kforce’s financial results.

10

A large part of our business entails employing individuals on a temporary basis and placing such individuals in clients’ workplaces. Increased government regulation of the workplace or of the employer/employee relationship could have a material adverse effect on Kforce. For example, changes to government regulations, including changes to statutory hourly wage and overtime regulations, could adversely affect the Firm’s results of operations by increasing its costs. Due to the substantial number of state and local jurisdictions in which we operate and the widening disparity among state and local laws, there also is a risk that we may be unaware of, or unable to adequately monitor, actual or proposed changes in, or the interpretation of, the laws or governmental regulations of such states and localities. Any delay in our compliance with changes in such laws or governmental regulations could result in potential fines, penalties, or other sanctions for non-compliance.

Reclassification of our independent contractors by tax or regulatory authorities could materially and adversely affect our business model and could require us to pay significant retroactive wages, taxes and penalties.

We utilize individuals to provide services in connection with our business as qualified third-party independent contractors rather than our direct employees. Heightened state and federal scrutiny of independent contractor relationships could adversely affect us given that we utilize independent contractors to perform our services. An adverse determination related to the independent contractor status of these subcontracted personnel could result in a substantial tax or other liabilities to us.

Significant increases in wages or payroll-related costs could adversely affect Kforce’s business.

Significant increases in wages or the effective rates of any payroll-related costs could have a material adverse effect on Kforce. Kforce is required to pay a number of federal, state, and local payroll and related costs or provide certain benefits such as paid time off, sick leave, unemployment taxes, workers’ compensation and insurance premiums and claims, FICA, and Medicare, among others, related to our employees. Costs could also increase as a result of health care reforms or the possible imposition of additional requirements and restrictions related to the placement of personnel. We may not be able to increase the fees charged to our clients in a timely manner or in a sufficient amount to cover these potential cost increases.

Kforce may be adversely affected by immigration restrictions and reform.

Our Tech segment utilizes a significant number of foreign nationals employed by us on work visas, primarily under the H-1B visa classification. The H-1B visa classification that enables U.S. employers to hire qualified foreign nationals is subject to legislative and administrative changes, as well as changes in the application of standards and enforcement. Immigration laws and regulations can be significantly affected by political developments and levels of economic activity. Current and future restrictions on the availability of such visas could restrain our ability to employ the skilled professionals we need to meet our clients’ needs, which could have a material adverse effect on our business. The U.S. Citizenship and Immigration Service (“USCIS”) continues to closely scrutinize companies seeking to sponsor, renew or transfer H-1B status, including Kforce and Kforce’s subcontractors and has issued internal guidance to its field offices that appears to narrow the eligibility criteria for H-1B status in the context of staffing services. In addition to USCIS restrictions, certain aspects of the H-1B program are also subject to regulation and review by the U.S. Department of Labor and U.S. Department of State, which have recently increased enforcement activities in the program. Vigorous enforcement and/or legislative or executive action relating to immigration could adversely affect our ability to recruit or retain foreign national consultants, and consequently, reduce our supply of skilled consultants and candidates and subject us to fines, penalties and sanctions, or result in increased labor and compliance costs.

Kforce’s success depends upon retaining the services of its management team and key operating employees.

Kforce is highly dependent on its management team and expects that continued success will depend largely upon their efforts, expertise and abilities. The loss of the services of any key executive for any reason could have a material adverse effect on Kforce. To attract and retain executives and other key employees (particularly management, client servicing, and consultant and candidate recruiting employees) in a competitive marketplace, we must provide a competitive compensation package, including cash-based and equity-based compensation. Kforce expends significant resources in the recruiting and training of its employees, as the pool of available applicants for these positions is limited. The loss or any sustained attrition of our key operating employees could have a material adverse effect on our business, including our ability to establish and maintain client, consultant and candidate, professional and technical relationships.

11

Kforce’s temporary staffing business could be adversely impacted by health care reform.

The Patient Protection and Affordable Care Act and the Health Care and Education Reconciliation Act of 2010, and the rules and regulations thereunder (the “PPACA”), imposes requirements and restrictions, including, but not limited to, guaranteed coverage requirements, prohibitions on some annual and all lifetime limits on amounts paid on behalf of or to our employees, increased restrictions on rescinding coverage, establishment of minimum requirements, the establishment of state insurance exchanges and essential benefit packages, and greater limitations on product pricing. Because the regulations governing the PPACA’s employer mandate are subject to interpretation, it is possible that Kforce may incur liability in the form of penalties, fines, or damages if the health plans we offer are subsequently found not to meet minimum essential coverage, affordability or minimum value standards, or if our method for determining eligibility for coverage is found inadequate or our clients seek indemnification for health care claims resulting from consultants working on client assignments. The cost of any such penalties, fines or damages could have a material adverse effect on Kforce’s financial and operating results.

New business initiatives and strategic changes may divert management’s attention from normal business operations, which could adversely affect our performance.

New business initiatives and strategic changes in the composition of our business mix can be a diversion to our management’s attention from other business concerns and disruptive to our operations, which could cause our business and results of operations to suffer materially. Acquisitions and new business initiatives could involve significant unanticipated challenges and risks, including the possibility that: they may not advance our business strategy; we may not realize our anticipated return on our investment; we may lose key personnel; we may retain unforeseen liabilities; we may experience difficulty in implementing initiatives or integrating acquired operations; or management's attention may be diverted from our other businesses. These events could cause material harm to our business, operating results, or financial condition.

Kforce maintains debt that exposes us to interest rate risk and contains restrictive covenants that could trigger prepayment of obligations or additional costs.

We have a credit facility consisting of a revolving line of credit of up to $300.0 million, subject to certain limitations. Borrowings under the credit facility are secured by substantially all of the tangible and intangible assets of the Firm, excluding the Firm’s corporate headquarters and certain other designated executed collateral.

Adverse changes in credit markets, including increases in interest rates, could increase our cost of borrowing and/or make it more difficult to refinance our existing indebtedness, if necessary. We have reduced our exposure to rising interest rates by entering into an interest rate hedging arrangement, although this and other arrangements may result in us incurring higher interest expenses than we would have otherwise incurred. If interest rates increase in the absence of such arrangements though, we would need to dedicate more of our cash flow from operations to service our debt.

Kforce is subject to certain affirmative and negative covenants under our credit facility. Our failure to comply with such restrictive covenants could result in an event of default, which, if not cured or waived, could result in Kforce being required to repay the outstanding balance before the due date. If this occurs, we may not be able to repay our debt or we may be forced to refinance on terms not acceptable to us, which could have a material adverse effect on our results of operations and financial condition.

Kforce depends on the proper functioning of its information systems.

Kforce is dependent on the proper functioning of information systems in operating our business. Critical information systems are used in every aspect of Kforce’s daily operations, most significantly, in the identification and matching of staffing resources to client assignments and in the client billing and consultant or vendor payment functions. Kforce’s information systems may not perform as anticipated and are vulnerable to damage or interruption including natural disasters, fire or casualty theft, technical failures, terrorist acts, cybersecurity breaches, power outages, telecommunications failures, physical or software intrusions, computer viruses, employee errors and similar events. Our corporate headquarters and data center are located in a hurricane-prone area although we have disaster recovery systems for some key information systems, such as billing and payroll, but not for all such key systems. Failure or interruption of our critical information systems may require significant additional capital and management resources to resolve, which could materially adversely affect our business. Additionally, many of our information technology systems and networks are cloud-based or managed by third parties, whose future performance and reliability we cannot control. The risk of a cyberattack or security breach on a third party carries the same risks to Kforce as those associated with our internal systems. We seek to reduce these risks by performing vendor due diligence procedures prior to engaging with any third party vendor who will have access to sensitive data. Additionally, we require audits of the relevant third parties’ information technology processes on an annual basis. However, there can be no assurance that such parties will not experience cybersecurity breaches that could adversely affect our employees, customers and businesses or that our audit or diligence processes will successfully deter or prevent such breach.

12

Delays in collecting our trade accounts receivable could adversely affect our business.

We generate a significant amount of trade accounts receivable from our clients. Delays in payments owed to us could have a material adverse effect on our financial condition and cash flows generated by our business. Factors that could cause a delay include business failures, turmoil in the financial and credit markets, sluggish or recessionary U.S. economic conditions, our exposure to clients in high-risk sectors such as the financial services industry, declines in the credit worthiness of our clients, extension in payment terms with our clients and declines in the business of our clients.

Adverse results in tax audits or interpretations of tax laws could adversely impact our business.

Kforce is subject to periodic federal, state and local tax audits for various tax years. We also need to comply with new, evolving or revised tax laws and regulations. The Tax Cuts and Jobs Act enacted in December 2017 continues to require significant interpretation; as additional regulatory guidance is issued and we continue to analyze the application of the new law, we may be required to refine our estimates, which could materially affect our tax obligations and effective tax rate. Although Kforce attempts to comply with all taxing authority regulations, adverse findings or assessments made by taxing authorities as the result of an audit could have a material adverse effect on Kforce.

Due to inherent limitations, there can be no assurance that our system of disclosure and internal controls and procedures will be successful in preventing all errors and fraud, or in making all material information known in a timely manner to management.

Our management, including our CEO and CFO, does not expect that our disclosure controls and internal controls will prevent all errors and fraud. A control system, regardless of how well designed and operated, can provide only reasonable, not absolute, assurance that the objectives of the control system are met. Because of the inherent limitations in all control systems, no evaluation of controls can provide absolute assurance that all control issues and instances of fraud, if any, within Kforce have been detected. These inherent limitations include the realities that judgments in decision-making can be faulty, and that breakdowns can occur because of a simple error or mistake. Additionally, controls can be circumvented by the individual acts of some persons, by collusion of two or more people, or by management override of the control.

The design of any system of controls is also based in part upon certain assumptions about the likelihood of future events, and there can be no assurance that any design will succeed in achieving its stated goals under all potential future conditions; over time, a control may become inadequate because of changes in conditions, or the degree of compliance with the policies or procedures may deteriorate. Because of the inherent limitations, misstatements due to error or fraud may occur and not be detected.

We are exposed to intangible asset risk which could result in future impairment.

We regularly review our intangible assets for impairment when events or changes in circumstances indicate that the carrying value may not be recoverable. We test goodwill and indefinite-lived intangible assets for impairment at least annually. Factors that may be considered a change in circumstances, indicating that the carrying value of the intangible assets may not be recoverable, include: macroeconomic conditions; industry and market considerations; increases in labor or other costs that have a negative effect on earnings and cash flows; negative or declining cash flows or a decline in actual or planned revenue or earnings compared with actual and projected results of relevant prior periods; and other relevant entity-specific events, such as changes in key personnel, strategy, or clients, and sustained decreases in share price. We may be required to record a charge in our financial statements, which could be material, during the period in which we determine an impairment of our acquired intangible assets has occurred, negatively impacting our financial results.

Our business is dependent upon maintaining our reputation, our relationships and our performance.

The reputation and relationships that we have established and currently maintain with our clients are important to maintaining existing business and identifying new business. If our reputation or relationships were damaged, it could materially adversely affect on our operations. In addition, if our performance does not meet our clients’ expectations, our revenues and operating results could be materially harmed.

Agreements may be terminated by clients and consultants at will and the termination of a significant number of such agreements could adversely affect our revenues.

Our agreements do not provide for exclusive use of our services, and clients are free to place orders with our competitors. Each consultant’s relationship with us is terminable at will. If clients terminate a significant number of our agreements and we are unable to generate new contracts, or a significant number of our consultants cease performing services for us and we are unable to find suitable replacements, the growth of our business could be adversely affected, and our revenues and results of operations could be harmed.

13

Kforce’s current market share may decrease as a result of limited barriers to entry for new competitors and discontinuation of clients outsourcing their staffing needs.

We face significant competition in the markets we serve, and there are limited barriers to entry for new competitors. The competition among staffing services firms is intense. Kforce competes for potential clients with providers of outsourcing services, systems integrators, computer systems consultants, temporary personnel agencies, search firms, and other providers of staffing services. Some of our competitors possess substantially greater resources than we do. From time to time, we experience significant pressure from our clients to reduce price levels. During these periods, we may face increased competitive pricing pressures and may not be able to recruit the personnel necessary to fulfill our clients’ needs. We also face the risk that certain of our current and prospective clients will decide to provide similar services internally, particularly if regulatory burdens are reduced.

Vendor management services are considered a competitor and increasing use by our clients could affect our relationships.

Increasingly, many clients and potential clients are retaining third parties to provide vendor management services. The third party, or vendor management company, is responsible for retaining companies that will provide temporary information technology personnel to the client. This results in Kforce contracting with such third parties and not directly with the end customer. This change can weaken Kforce’s relationship with its clients, which may make it more difficult to maintain and expand our business with existing customers. In addition, the agreements with vendor management companies are frequently structured as subcontracting agreements, with the vendor management company entering into a services agreement directly with the end customer. As a result, in the event of a bankruptcy of a vendor management company, Kforce’s ability to collect its outstanding receivables and continue to provide services could be adversely affected.

Kforce’s stock price may be volatile.

The market price of our stock has fluctuated substantially in the past and could fluctuate substantially in the future, based on a variety of factors, including our operating results, changes in general conditions in the economy, the financial markets, the staffing industry, or other developments affecting us, our clients, or our competitors; some of which may be unrelated to our performance.

In addition, the stock market in general, especially The NASDAQ Global Select Market (“NASDAQ”) tier, along with market prices for staffing companies, has experienced volatility that has often been unrelated to the operating performance of these companies. These broad market and industry fluctuations may adversely affect the market price of our common stock, regardless of our operating results.

Among other things, volatility in our stock price could mean that investors will not be able to sell their shares at or above the prices they pay. The volatility also could impair our ability in the future to offer common stock as a source of additional capital or as consideration in the acquisition of other businesses.

Provisions in Kforce’s articles and bylaws and under Florida law may have certain anti-takeover effects.

Kforce’s articles of incorporation and bylaws and Florida law contain provisions that may have the effect of inhibiting a non-negotiated merger or other business combination. In particular, our articles of incorporation provide for a staggered Board of Directors (“Board”) and permit the removal of directors only for cause. Additionally, the Board may issue up to 15 million shares of preferred stock, and fix the rights and preferences thereof, without a further vote of the shareholders. In addition, certain of our officers and managers have employment agreements containing certain provisions that call for substantial payments to be made to such employees in certain circumstances after a change in control. Certain of these provisions may discourage a future acquisition of Kforce, including an acquisition in which shareholders might otherwise receive a premium for their shares. As a result, shareholders who might desire to participate in such a transaction may not have the opportunity to do so. Moreover, the existence of these provisions could negatively impact the market price of our common stock.

RISKS RELATED TO OUR GOVERNMENT BUSINESS

Our GS segment is substantially dedicated to contracting with and serving U.S. Federal Government agencies (the “Government Business”). In addition, Kforce supplies services to the Federal Government which poses additional risks to those mentioned previously. Federal contractors, including Kforce, face a number of risks, including but not limited to the following:

14

Our failure to comply with complex federal procurement laws and regulations could cause us to lose business, incur additional costs and subject us to a variety of penalties, including suspension and debarment from contracting with the Federal Government.

We must comply with complex laws and regulations relating to the formation, administration, and performance of Federal Government contracts. These laws and regulations create compliance risk, affect how we do business with our federal agency clients, and may impose added costs on our business. If a government review, audit or investigation uncovers improper or illegal activities, we may be subject to civil and criminal penalties and administrative sanctions, including termination of contracts, forfeiture of profits, harm to our reputation, suspension of payments, fines, and suspension or debarment from contracting with Federal Government agencies.

The Federal Government also may reform its procurement practices or adopt new contracting rules and regulations, including cost accounting standards, which could be costly to satisfy or impact our ability to obtain new contracts. A failure to comply with all applicable laws and regulations could result in contract termination, price or fee reductions, or suspension or debarment from contracting with Federal Government agencies; each of which could lead to a material reduction in our revenues, cash flows and operating results.

Changes in the spending policies or budget priorities of the Federal Government including the failure by Congress to approve budgets, raise the U.S. debt ceiling or avoid sequestration on a timely basis for the federal agencies we support could delay, reduce or stop federal spending and cause us to lose revenue or impair our intangible assets.

Changes in Federal Government fiscal or spending policies could materially adversely affect our Government Business; in particular, our business could be materially adversely affected by decreases in Federal Government spending. In addition, on an annual basis, Congress must approve, and the President must sign the appropriation bills that govern spending by each of the federal agencies we support. If Congress is unable to agree on budget priorities and is unable to appropriate funds or pass the annual budget on a timely basis, or a prolonged government shutdown were to occur (as happened recently), there may be delays, reductions or cessations of funding for our services and solutions. In addition, from time to time it has been necessary for Congress to raise the U.S. debt ceiling in order to allow for borrowing necessary to fund government operations. If that becomes necessary again and Congress fails to raise the debt ceiling on a timely basis, there may be delays, reductions or cessations of funding for our services and solutions. Furthermore, legislatively mandated cuts in federal programs, known as sequestration, could result in delays, reductions or cessation of funding for our services and solutions.

Unfavorable government audit results could force us to refund previously recognized revenue and could subject us to a variety of penalties and sanctions.

Federal agencies can audit and review our performance on contracts, pricing practices, cost structure, incurred cost submissions and compliance with applicable laws, regulations, and standards. An audit of our work, including an audit of work performed by companies Kforce has acquired or may acquire, or subcontractors we have hired or may hire, could force us to refund previously recognized revenues.

If a government audit uncovers improper or illegal activities, we may be subject to civil and criminal penalties and administrative sanctions, including termination of contracts, forfeiture of profits, suspension of payments, fines, and suspension or debarment from doing business with Federal Government agencies. In addition, we could suffer serious harm to our reputation if allegations of impropriety were made against us, regardless of the veracity.

We are dependent upon the ability of government agencies to administratively manage our contracts.

After we are awarded a contract and the contract is funded by the Federal Government, we are still dependent upon the ability of the relevant agency to administratively manage our contract. We can be adversely impacted by delays in the start-up of already awarded and funded projects, including delays due to shortages of acquisition and contracting personnel within the Federal Government agencies.

Competition is intense in the Government Business.

There is often intense competition to win federal agency contracts. The competitive bidding process entails substantial costs and management time to prepare bids and proposals for contracts that may not be awarded to us or may be split among competitors. Even when a contract is awarded to us, we may encounter significant expenses, delays, contract modifications or bid protests from competitors. If we are unable to successfully compete for new business or win competitions to maintain existing business, our operations could be materially adversely affected. Many of our competitors are larger and have greater resources, larger client bases and greater brand recognition than we do. Our larger competitors also may be able to provide clients with different or greater capabilities or benefits than we can provide.

15

Loss of our General Services Administration (“GSA”) Schedules or other contracting vehicles could impair our ability to win new business.

GSA Schedules constitute a significant percentage of revenues from our federal agency clients. If we were to lose one or more of these Schedules or other contracting vehicles, we could lose revenues and our operating results could be materially adversely affected. These Schedules or contracts typically have an initial term with multiple options that may be exercised by our government agency clients to extend the contract for successive periods of one or more years. We can provide no assurance that our clients will exercise these options.

Security breaches in sensitive government information systems could result in the loss of our clients and cause negative publicity.

Many of the systems we develop, install, and maintain involve managing and protecting information used in intelligence, national security, and other sensitive or classified government functions. A security breach in one of these systems could cause serious harm to our business, damage our reputation, and prevent us from being eligible for further work on sensitive or classified systems for Federal Government clients. We could incur losses from such a security breach that could exceed the policy limits under our insurance. Damage to our reputation or limitations on our eligibility for additional work resulting from a security breach in one of our systems could materially reduce our revenues.

Our employees may engage in misconduct or other improper activities, which could harm our business.

Like all government contractors, we are exposed to the risk that employee fraud or other misconduct could occur. Misconduct by our employees could include intentional or unintentional failures to comply with Federal Government procurement regulations, engaging in unauthorized activities, seeking reimbursement for improper expenses, or falsifying time records. Employee misconduct could also involve the improper use of our clients’ sensitive or classified information, which could result in regulatory sanctions against us and serious harm to our reputation. It is not always possible to deter employee misconduct, and precautions to prevent and detect this activity may not be effective in controlling such risks or losses, which could materially adversely affect our business.

Our failure to obtain and maintain necessary security clearances may limit our ability to perform classified work for government clients, which could cause us to lose business.

Some government contracts require us to maintain facility security clearances and require some of our employees to maintain individual security clearances. If our employees lose or are unable to timely obtain security clearances, or we lose a facility clearance, a government agency client may terminate the contract or decide not to renew it upon its expiration.

We are the prime contractor on many of our contracts and if our subcontractors fail to appropriately perform their obligations, our performance and our ability to win future contracts could be harmed.

For many of our contracts where we are the prime contractor, we involve subcontractors, which we rely on to perform a portion of the services that we must provide to our clients. There is a risk that we may have disputes with our subcontractors, including disputes regarding the quality and timeliness of work performed or client concerns about the subcontractor’s performance. In addition, the contracting parties on which we rely may be affected by changes in the economic environment and constraints on available financing to meet their performance requirements or provide needed supplies on a timely basis. A failure by one or more of those contracting parties to provide the agreed-upon supplies or perform the agreed-upon services on a timely basis may affect our ability to perform our obligations.

We are the subcontractor on many of our contracts and if we, or the applicable prime contractors, fail to appropriately perform our and their obligations, our financial condition may be harmed.

For many of our contracts, we are a subcontractor; therefore, we rely on the applicable prime contractor to secure contracts when they are put up for bid for a renewal or a new contract. There is a risk that the applicable prime contractor is unable to secure such bids for a number of reasons, including the prime contractor’s quality and timeliness of services, financial condition, and relationships with the Federal Government. In addition, there are risks that we are unable to provide such subcontractor services with the quality and timeliness demanded by the prime contractor or the ultimate end-client. Any failure by the applicable prime contractor to secure contracts or by us to perform adequately could materially adversely affect our business.

ITEM 1B. UNRESOLVED STAFF COMMENTS.

None.

16

ITEM 2. PROPERTIES.

We own our corporate headquarters in Tampa, Florida, which is approximately 128,000 square feet of space. In addition, as of December 31, 2018, we leased approximately 325,000 square feet of total office space in approximately 60 field offices located throughout the U.S., with lease terms ranging from three to seven years, although a limited number of leases contain short-term renewal provisions that range from month-to-month to one year.

Although additional field offices may be established based on the requirements of our operations, we believe that our facilities are adequate for our current needs, and we do not expect to materially expand or contract our facilities in the foreseeable future.

ITEM 3. LEGAL PROCEEDINGS.

We are involved in legal proceedings, claims and administrative matters that arise in the ordinary course of our business. We have made accruals with respect to certain of these matters, where appropriate, that are reflected in our consolidated financial statements but are not, individually or in the aggregate, considered material. For other matters for which an accrual has not been made, we have not yet determined that a loss is probable, or the amount of loss cannot be reasonably estimated. While the ultimate outcome of the matters cannot be determined, we currently do not expect that these proceedings and claims, individually or in the aggregate, will have a material effect on our financial position, results of operations, or cash flows. The outcome of any litigation is inherently uncertain, however, and if decided adversely to us, or if we determine that settlement of particular litigation is appropriate, we may be subject to liability that could have a material adverse effect on our financial position, results of operations, or cash flows. Kforce maintains liability insurance in amounts and with such coverage and deductibles as management believes is reasonable. The principal liability risks that Kforce insures against are workers’ compensation, personal injury, bodily injury, property damage, directors’ and officers’ liability, errors and omissions, cyber liability, employment practices liability and fidelity losses. There can be no assurance that Kforce’s liability insurance will cover all events or that the limits of coverage will be sufficient to fully cover all liabilities.

ITEM 4. MINE SAFETY DISCLOSURES.

Not applicable.

PART II

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES.

Holders of Common Stock

Our common stock trades on the NASDAQ using the ticker symbol “KFRC”. As of February 21, 2019, there were approximately 150 holders of record.

Purchases of Equity Securities by the Issuer