Table of Contents

Filed Pursuant

to Rule 424(b)(3)

Registration No. 333-204177

AVINTIV Specialty Materials Inc.

Offer to Exchange

$210,000,000 aggregate principal amount of 6.875% Senior Notes due 2019 (the “exchange notes”), which have been registered under the Securities Act of 1933, as amended (the “Securities Act”), for any and all outstanding $210,000,000 aggregate principal amount of 6.875% Senior Notes due 2019 that were issued on June 11, 2014 (the “outstanding notes” and together with the exchange notes, the “notes”).

The exchange notes will be fully and unconditionally guaranteed, jointly and severally, on a senior unsecured basis, by our domestic restricted subsidiaries that guarantee the outstanding notes or certain of our other indebtedness as described herein.

We are conducting the exchange offer in order to provide you with an opportunity to exchange your unregistered outstanding notes for freely tradeable exchange notes that have been registered under the Securities Act.

The Exchange Offer

| • | We will exchange all outstanding notes that are validly tendered and not validly withdrawn for an equal principal amount of exchange notes that are freely tradeable. |

| • | You may withdraw tenders of outstanding notes at any time prior to the expiration date of the exchange offer. |

| • | The exchange offer expires at 5:00 p.m., New York City time, on September 8, 2015 which is the 21st business day after the date of this prospectus. |

| • | The exchange of outstanding notes for exchange notes in the exchange offer will not be a taxable event for U.S. federal income tax purposes. |

| • | The terms of the exchange notes to be issued in the exchange offer are substantially identical to the outstanding notes, except that the exchange notes will be freely tradeable. |

Results of the Exchange Offer:

| • | The exchange notes may be sold in the over-the-counter market, in negotiated transactions or through a combination of such methods. We do not plan to list the exchange notes on a national market. |

All untendered outstanding notes will continue to be subject to the restrictions on transfer set forth in such outstanding notes and in the indenture governing the notes. In general, the outstanding notes may not be offered or sold, unless registered under the Securities Act, except pursuant to an exemption from, or in a transaction not subject to, the Securities Act and applicable state securities laws. Other than in connection with the exchange offer, we do not currently anticipate that we will register the outstanding notes under the Securities Act.

You should carefully consider the “Risk Factors” beginning on page 18 of this prospectus before participating in the exchange offer.

Each broker dealer that receives exchange notes for its own account pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of such exchange notes. This prospectus, as it may be amended or supplemented from time to time, may be used by a broker dealer in connection with resales of exchange notes received in exchange for outstanding notes where such outstanding notes were acquired as a result of market making activities or other trading activities.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the exchange notes to be distributed in the exchange offer or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is August 10, 2015.

Table of Contents

You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with different information. This prospectus may be used only for the purposes for which it has been published and no person has been authorized to give any information not contained herein. If you receive any other information, you should not rely on it. We are not making an offer of these securities in any state where the offer is not permitted.

| Page | ||||

| ii | ||||

| ii | ||||

| ii | ||||

| 1 | ||||

| 18 | ||||

| 35 | ||||

| 36 | ||||

| 37 | ||||

| Unaudited Pro Forma Condensed Combined Financial Information |

39 | |||

| 49 | ||||

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

51 | |||

| 94 | ||||

| 97 | ||||

| 106 | ||||

| 133 | ||||

| 135 | ||||

| 137 | ||||

| 198 | ||||

| 208 | ||||

| 209 | ||||

| 211 | ||||

| 212 | ||||

| 212 | ||||

| 212 | ||||

| F-1 | ||||

i

Table of Contents

MARKET, RANKING AND OTHER INDUSTRY DATA

The data included in this prospectus regarding the markets and the industry in which we operate, including the size of certain markets and our position and the position of our competitors within these markets, is based on reports of government agencies, independent industry sources (including a report prepared for us by Smithers Information Ltd., an independent third-party market research firm) and our own estimates relying on our management’s knowledge and experience in the markets in which we operate. Our management’s knowledge and experience, in turn, are based on information obtained from our customers, distributors, suppliers, trade and business organizations and other contacts in the markets in which we operate. We believe these reports, sources and estimates to be accurate as of their respective dates. However, this information may prove to be inaccurate because of the method by which we obtained some of the data for our estimates or because this information cannot always be verified with complete certainty due to the limits on the availability and reliability of raw data, the voluntary nature of the data gathering process and other limitations and uncertainties.

Although we believe market, ranking and other industry data included in this prospectus is generally reliable, we cannot guarantee the accuracy and completeness of the information and have not independently verified it. We have not independently verified any of the data from other third party sources, nor have we ascertained the underlying assumptions relied upon therein. As a result, you should be aware that market, ranking and other industry data included in this prospectus, and our estimates and beliefs based on that data, may not be reliable. Neither we nor the underwriters can guarantee the accuracy or completeness of any such information contained in this prospectus. While we are not aware of any misstatements regarding the industry data presented herein, our estimates involve risks and uncertainties and are subject to change based on various factors, including those discussed under the heading “Risk Factors,” “Forward-Looking Statements” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this prospectus.

TRADEMARKS, SERVICE MARKS AND TRADENAMES

This prospectus contains some of our trademarks, trade names and service marks, including the following: APEX, Chicopee, Chix, Chux, Durawipe, Fiberweb, KAMI, Masslinn, AVINTIV, AVINTIV Specialty Materials Inc., Providência, REEMAY, Spinlace, S-Tex, TYPAR and Worxwell. Each one of these trademarks, trade names or service marks is either (i) our registered trademark, (ii) a trademark for which we have a pending application, (iii) a trade name or service mark for which we claim common law rights or (iv) a registered trademark or application for registration which we have been licensed by a third party to use.

Solely for convenience, the trademarks, service marks, and trade names referred to in this prospectus are without the ® and ™ symbols, but such references are not intended to indicate, in any way, that we will not assert, to the fullest extent under applicable law, our rights or the rights of the applicable licensors to these trademarks, service marks, and trade names. This prospectus contains additional trademarks, service marks and trade names of others, which are the property of their respective owners. All trademarks, service marks and trade names appearing in this prospectus are, to our knowledge, the property of their respective owners.

As used in this prospectus, unless otherwise noted or the context otherwise requires:

| • | references to the “Issuer” are to AVINTIV Specialty Materials Inc. (f/k/a Polymer Group, Inc.), exclusive of its subsidiaries; |

| • | references to “we,” “us,” “our,” “AVINTIV,” and “the Company” are to AVINTIV Specialty Materials Inc. and its subsidiaries; |

| • | references to “Parent” are to AVINTIV Acquisition Corporation (f/k/a Scorpio Acquisition Corporation), the direct parent of the Issuer, exclusive of its subsidiaries; |

ii

Table of Contents

| • | references to “Holdings” are to AVINTIV Inc. (f/k/a PGI Specialty Materials, Inc.), the indirect parent of the Issuer, exclusive of its subsidiaries; |

| • | references to “Blackstone” and the “Sponsor” are to certain investment funds affiliated with Blackstone Capital Partners V L.P.; |

| • | references to the “Investor Group” are, collectively, to Blackstone and the management investors (as defined below); |

| • | references to the “management investors” are to certain members of our management team and employees who have made investments in the Issuer; |

| • | references to “Providência” are to Companhia Providência Indústria e Comércio, a Brazilian corporation ( sociedade anônima ); |

| • | references to “Acquisition Co.” are to our wholly-owned subsidiary, PGI Polímeros do Brasil S.A., a Brazilian corporation ( sociedade anônima ); |

| • | references to the “Providência Acquisition” are to the acquisition of approximately 71.25% of the outstanding capital stock of Providência by Acquisition Co.; |

| • | references to “Providência Refinancing” are to the borrowings under the Incremental Amendment (as defined below), the Senior Unsecured Notes (as defined below) and the use of proceeds therefrom; |

| • | references to the “Mandatory Tender Offer” are to the mandatory tender offer registration request filed by Acquisition Co., our wholly-owned subsidiary, with the Securities Commission of Brazil (Comissăo de Valores Mobiliários or “CVM”) in order to launch as required by Brazilian law, after the CVM’s approval, a tender offer to acquire the remaining approximately 28.75% of the outstanding capital stock of Providência that is currently held by minority shareholders; |

| • | references to “Fiberweb” are to Fiberweb Limited (formerly known as Fiberweb plc); |

| • | references to the “Fiberweb Acquisition” are to the completion of the acquisition of the entire issued ordinary share capital of Fiberweb, the borrowings under the Bridge Facilities and the use of proceeds therefrom; |

| • | references to “Terram Geosynthetics” are to Terram Geosynthetics Private Limited, a joint venture we acquired as part of the Fiberweb Acquisition in which we maintain a 65% interest; |

| • | references to the “ABL Facility” are to the Credit Agreement, dated as of January 28, 2011, among Parent, the Company, as lead borrower, the lenders from time to time party thereto, Citibank, N.A., as administrative agent and collateral agent, Morgan Stanley Senior Funding, Inc., as syndication agent, Barclays Bank PLC and RBC Capital Markets, as co-documentation agents, and Citigroup Global Markets Inc., Morgan Stanley Senior Funding, Inc., Barclays Capital Inc. and RBC Capital Markets LLC, as joint lead arrangers and joint book runners, as further amended or supplemented from time to time; |

| • | references to the “Secured Bridge Facility” are to the $268.0 million secured bridge credit facility, dated as of September 17, 2013, among the Company, Parent, the lenders from time to time party thereto, Citicorp North America, Inc., as administrative agent, Barclays Bank PLC, as syndication agent and Citigroup Global Markets Inc. and Barclays Bank PLC, as joint lead arrangers and joint bookrunners, as further amended or supplemented from time to time; |

| • | references to the “Unsecured Bridge Facility” are to the $50.0 million unsecured bridge credit facility, dated as of November 26, 2013, among the Company, Parent, the lenders from time to time party thereto, Citicorp North America, Inc., as administrative agent, Barclays Bank PLC, as syndication agent and Citigroup Global Markets Inc. and Barclays Bank PLC, as joint lead arrangers and joint bookrunners, as further amended or supplemented from time to time; |

| • | references to the “Bridge Facilities” are to the Secured Bridge Facility and the Unsecured Bridge Facility, collectively; |

iii

Table of Contents

| • | references to the “Term Loans” are to the $295.0 million of term loans outstanding pursuant to the Senior Secured Credit Agreement (the “Term Loan Facility”), dated as of December 19, 2013, among the Company, Parent, the lenders from time to time party thereto, Citicorp North America, Inc., as administrative agent, Barclays Bank PLC, as syndication agent, RBC Capital Markets and HSBC Bank USA, N.A., as co-documentation agents, Citigroup Global Markets Inc. and Barclays Bank PLC, as joint lead arrangers and Citigroup Global Markets Inc., Barclays Bank PLC, RBC Capital Markets and HSBC Securities (USA) Inc., as joint bookrunners, as further amended or supplemented from time to time; |

| • | references to “Additional Term Loans” are to the $415.0 million of incremental term loans outstanding pursuant to an incremental term loan amendment, dated as of June 10, 2014 (the “Incremental Amendment”), to our existing Term Loan Facility; |

| • | references to “2015 Additional Term Loans” are to the $283.0 million of incremental term loans outstanding pursuant to the second incremental term loan amendment, dated as of April 17, 2015 (the “Second Incremental Amendment”); |

| • | references to “Equity Contribution” are to an equity investment by the Sponsor of approximately $30.7 million in the Issuer, the proceeds of which were contributed as a capital contribution to Parent, which in turn contributed such proceeds to the Company as a capital contribution; |

| • | references to “pro forma” give pro forma effect to the Providência Acquisition and the Providência Refinancing for the period indicated; |

| • | references to the “Senior Unsecured Notes” or the “outstanding notes” are to the $210.0 million aggregate principal amount of 6.875% senior unsecured notes due 2019 issued by the Company on June 11, 2014; |

| • | references to the “Senior Secured Notes” are to the $560.0 million aggregate principal amount of 7.75% notes due 2019 issued by the Company on January 13, 2011; |

| • | reference to “spunmelt” are to spunmelt technology, which uses thermoplastic polymers that are melt-spun to manufacture continuous-filament products; |

| • | references to “Smithers Pira” are to Smithers Information Ltd., a market research firm. All information included herein that is attributed to Smithers Pira is based on Smithers Pira Consultancy Report: Global Nonwovens Market Study, dated June 15, 2015; |

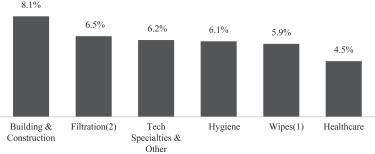

| • | references to “nonwovens industry” are to industry size, as measured by either volume (in metric tons) or value (in U.S. dollars), based on information by Smithers Pira. The nonwovens industry, as defined by Smithers Pira, encompasses nonwovens used for various products that serve the hygiene, healthcare filtration, dryer sheets, industrial and wipes applications. The industry also includes geocomposites products, which are an adjacent technology used in industrial applications that can utilize nonwovens; |

| • | references to “markets” or “regions” generally refers to the four geographic regions in which we operate: North America, South America, Europe (including our India operations), and Asia; and |

| • | references to “applications” generally are to the various customer end-use applications which our products serve. While our products serve a diverse range of applications, for convenience, we group these applications into three primary categories: Personal Care, Infection Prevention and High Performance Solutions. Personal Care includes hygiene applications (such as baby diapers, adult |

| incontinence products, and feminine hygiene products), personal care wipes, and fabric-softening dryer sheets. Infection Prevention includes healthcare applications (such as surgical gowns and drapes, face masks and wound care products), filtration products (including blood filters, pool and spa filters, and Hepa filtration), and disinfectant wipes (including patient care wipes and hard surface disinfectant wipes). High Performance Solutions includes building, construction and geosynthetics (including house wrap, road underlayment and industrial cable wrap), along with air filtration, home and bedding and industrial wiping applications, among others. |

iv

Table of Contents

On January 28, 2011, pursuant to an Agreement and Plan of Merger, dated as of October 4, 2010, we were acquired by affiliates of Blackstone, along with certain members of our management (the “Merger”). Periods prior to January 28, 2011 reflect the financial position, results of operations, and changes in financial position of the Company prior to the Merger (the “Predecessor”). The fiscal year ended December 31, 2011 reflects the financial position, results of operations, and changes in financial position of the Company after the Merger (the “Successor”).

Under the guidance provided by SEC Staff Accounting Bulletin Topic 5J, “New Basis of Accounting Required in Certain Circumstances,” push-down accounting is required when such transactions result in an entity becoming substantially wholly-owned. Under push-down accounting, certain transactions incurred by the acquirer, which would otherwise be accounted for in the accounts of the parent, are “pushed down” and recorded on the financial statements of the subsidiary. Therefore, the basis in shares of common stock of the Company has been pushed down from Holdings to the Company.

In addition, the Merger was recorded using the acquisition method of accounting in accordance with the accounting guidance for business combinations and non-controlling interest. The guidance prescribes that the purchase price be allocated to assets acquired and liabilities assumed based on the estimated fair market value of such assets and liabilities at the date of acquisition. As a result, periods prior to the Merger are not comparable to subsequent periods due to the difference in the basis of presentation of purchase accounting as compared to historical cost.

The audited financial statements of Providência as of and for the years ended December 31, 2013 and 2012 and the unaudited condensed interim financial statements as of and for the three months ended March 31, 2014 included in this prospectus have been prepared in Brazilian reals and in accordance with applicable IFRS as issued by the IASB. IFRS differs in certain significant respects from GAAP. See “Unaudited Pro Forma Condensed Combined Financial Information” for a discussion of significant differences between IFRS and GAAP as they relate to Providência.

The Company’s fiscal year is based on a 52 week period ending on the Saturday closest to each December 31. The one month ended January 28, 2011 for the Predecessor contains four weeks. The fiscal year ended December 31, 2011 for the Successor contains 48 weeks. The fiscal years ended December 29, 2012 and December 28, 2013 for the Successor contain operating results for 52 weeks. References herein to “2011,” “2012,” and “2013” generally refer to fiscal 2011, fiscal 2012 and fiscal 2013, respectively, unless the context indicates otherwise. In fiscal year 2014, the Company changed its year-end date to December 31. The Company’s 2014 fiscal year commenced on December 29, 2013 and concluded on December 31, 2014.

On June 4, 2015, we announced a new corporate brand and identity initiative. As a first step in this process, we selected “AVINTIV” as our new company name. Effective June 5, 2015, the Issuer changed its legal name from Polymer Group, Inc. to AVINTIV Specialty Materials Inc. In addition, Parent changed its legal name from Scorpio Acquisition Corporation to AVINTIV Acquisition Corporation and Holdings changed its legal name from PGI Specialty Materials, Inc. to AVINTIV Inc.

v

Table of Contents

This summary highlights selected information appearing elsewhere in this prospectus. Because it is a summary, it may not contain all of the information that may be important to you. You should read this entire prospectus carefully, including the information set forth under the heading “Risk Factors” and our financial statements. Before participating in the exchange offer, you should read the discussion under “Basis of Presentation” above for the definition of certain terms used in this prospectus and a description of certain transactions and other matters described in this prospectus.

Company Overview

We are a leading global innovator and manufacturer of specialty materials for use in a broad range of products that make the world safer, cleaner and healthier. We design and manufacture versatile high performance materials that can be engineered to possess specific value-added characteristics, including absorbency, tensile strength, softness and barrier properties. We serve customers focused on personal care, infection prevention, and high performance solutions, where our products are critical components used in a broad array of consumer and commercial products. For personal care applications, we supply specialty materials essential to the performance and feel of disposable baby diapers, feminine hygiene products, adult incontinence products, personal wipes and fabric softening dryer sheets. For infection prevention applications, our materials are utilized in products designed to ensure a clean environment, including disinfectant wipes, surgical gowns and drapes, face masks, wound care sponges, and water, air and blood filters. For high performance solutions, we supply protective house wrap, industrial cable wrap, construction and agricultural geosynthetics, as well as components for home and bedding products, industrial cleaning wipes, and various other applications.

Segment Overview

We manage our business through four reportable operating segments organized by geographic region: North America, South America, Europe and Asia. Each of our regional manufacturing facilities has a diverse range of capabilities and technologies to serve local demand trends and our customers’ specific requirements, which vary by region. Consequently, each of our regions serves a unique mix of customer applications; however, certain of our applications and customers are consistent across our regions. We believe that our ability to provide consistent, high-quality products across a variety of geographies is a strong competitive advantage in serving our global customers. In addition, our geographic breadth and broad range of applications reduce exposure to any one region, manufacturing facility, application, or customer.

North America

Our North America segment includes five manufacturing and converting facilities in the United States, one in Canada and one in Mexico. Our North America segment includes a broad array of product technologies, including our proprietary Reemay, Spinlace, Apex and TYPAR technologies, that collectively serve a wide spectrum of product applications. Markets served include personal care (baby diapers and feminine hygiene products and substrates for fabric-softening dryer sheets), infection prevention (specialty materials for use in various medical garments, such as surgical gowns and drapes as well as household cleaning wipes) and high performance solutions (filtration media for pool and spa filters, as well as protective house wrap). Net sales to external customers in fiscal 2014 totaled $828.6 million.

South America

Our South America segment includes two manufacturing facilities in Brazil, one in Argentina and one in Colombia. This footprint enables us to efficiently serve the Caribbean and Central America, the Andean

1

Table of Contents

Community (CAN) and the Southern Common Market (MERCOSUR) economic trade zones. All of our facilities in the region utilize leading-edge spunmelt technology and specialize in serving personal care applications, such as baby diapers and feminine hygiene products. However, we also serve certain specialty agriculture and industrial customers in this region. Net sales to external customers in fiscal 2014 totaled $306.2 million.

Europe

Our Europe segment includes two manufacturing facilities in the United Kingdom, two in France, and one in each of Germany, Italy, Spain and the Netherlands. Our Europe segment also includes our India joint venture with one manufacturing facility located in India. Our European segment includes our most diverse set of technologies, such as our proprietary S-tex spunmelt and hydroentanglement technologies, and serves a broad array of personal care, infection prevention and high performance solutions applications. We believe we are the leading global provider of industrial cable wrap and have significant positions in geosynthetics for civil engineering, landscape and military use. We also have meaningful positions in hygiene applications, such as baby diapers and adult incontinence products, and healthcare products, such as surgical drapes, blood filtration and face masks. Net sales to external customers in fiscal 2014 totaled $530.4 million.

Asia

Our Asia segment consists of two manufacturing facilities in China. In addition, we plan to utilize our leading-edge spunmelt technologies to participate in the rapid growth expected in the Asia region from rising disposable incomes and consumer adoption of personal care products. Net sales to external customers in fiscal 2014 totaled $194.7 million.

Our Strategy

Our mission is to provide superior products and services to enable our customers to create a safer, cleaner and healthier world. By leveraging our global team and broad portfolio of assets and technologies, we engineer customized solutions to meet our customers’ needs. We are focused on supplying consistent high quality products from our global manufacturing footprint, supported by knowledgeable local sales and technical service teams. We believe that our global presence and breadth of application expertise (further enhanced by the recent acquisitions of Fiberweb and Providência) provide a strong foundation for us to grow with our existing customers across the globe as well as for enhanced access to new customers across an array of highly specialized applications. As a result, we strive to grow our revenues consistent with the demand growth of the applications which we serve, while enhancing our operating efficiencies to improve our margins. To accomplish our mission and drive continued success, we are focused on the following strategies:

Support Continued Growth of Our Existing Customers Globally

We will invest to support the continued growth of our existing customers across the globe. As previously discussed, many of our customers’ products benefit from attractive growth trends and, consequently, our customers demand an increasing amount of our specialty materials. We will seek to enhance our competitive positions by providing cutting edge innovations, high quality and cost-effective products, and dedicated customer service. We will do so through initiatives to expand the production capacity of our current asset base as well as prudent capital investments to expand our capabilities. Many of our customers are increasingly growing their business globally, and we believe we are well positioned to gain share with these customers given our global presence and ability to reliably deliver consistent products across the globe.

Further Strengthen our Positions in Emerging Markets

We intend to establish stronger positions in emerging markets through partnerships with new customers, as well as by accelerating growth with existing accounts where we are viewed as a strategic supplier. We believe

2

Table of Contents

there will be significant growth in our existing markets in South America and Asia. Additionally, in the future, we believe there may be growth opportunities in currently under-developed regions, where current penetration rates for many of the applications we serve are lower compared to other regions. As these emerging markets develop, we will continue to make careful, disciplined investments to expand our global capabilities and operations.

Pursue Growth in Complementary Businesses

We intend to use our industry expertise and capabilities to pursue growth opportunities in complementary products that share one or more key characteristics with our core businesses, including customers, products, manufacturing technologies or supply chain. We will prioritize opportunities in higher value applications with greater product differentiation, higher margins and lower capital intensity. We may pursue these opportunities organically or through targeted acquisitions depending on the specific industry dynamics and required capabilities.

Drive Business Excellence to Pursue Economic Leadership and Enhance Margins

Our success is dependent upon our ability to offer an attractive value proposition to our customers and to maximize customer satisfaction through our innovation, product quality and reliability. Consequently, we will seek to use our global platform and capabilities to offer solutions which maximize customers’ value and streamline their operations. We will also seek to improve our supply chain management to improve our cost position. We will seek to accelerate our business excellence initiatives to generate recurring annual productivity savings to offset inflation, enable reinvestment in growth, and improve our margins. These initiatives are focused on procurement savings, manufacturing yield optimization, lean initiatives, preventative maintenance and logistics savings. Through the realization of acquisition-related cost savings and our business excellence initiatives, we plan to continue to pursue improved cost positions and operating margins in the future.

Opportunistically Pursue Value-Enhancing Acquisitions

The nonwovens industry has experienced significant consolidation in recent years, including our acquisitions of Fiberweb and Providência. However, the industry remains relatively fragmented with many smaller regional players. In the future, we will continue to opportunistically evaluate potential acquisitions that enhance our business. We will prioritize transactions that complement our existing businesses, offer a potential for meaningful cost savings, enhance our capabilities in complementary products or regions or improve our growth profile by leveraging our existing customer relationships, technologies, global manufacturing and distribution network, and expertise in engineered materials.

Develop and Attract Top Talent

We strive to attract and develop the best talent in the industry. We work as a team to make a positive impact to our organization, our customers and suppliers, and the community. We believe that our history of growth and innovation coupled with our strong global position will highlight the Company as an attractive career opportunity for talented business leaders. Over the past several years, we have redesigned our global organization structure and significantly enhanced the senior leadership team adding resources and capabilities in several key areas to address our strategic growth priorities.

Recent Acquisitions

We have recently completed two significant acquisitions. On June 11, 2014, Acquisition Co., our wholly-owned subsidiary, completed the acquisition of approximately 71.25% of the outstanding capital stock of Providência and on November 15, 2013, PGI Acquisition Limited, our indirect wholly-owned subsidiary,

3

Table of Contents

completed the acquisition of the entire issued ordinary share capital of Fiberweb. As required by Brazilian law, we intend to launch, subject to CVM approval, the Mandatory Tender Offer to acquire the remaining outstanding capital stock of Providência from the minority shareholders. See “Business—Expansion and Optimization—Providência Acquisition.”

Providência is a leading manufacturer of spunmelt nonwoven products based in Brazil, with a presence throughout the Americas, offering nonwoven fabrics under the KAMI brand. Its products are primarily used in hygienic and personal care applications, such as disposable diapers, sanitary pads, cleansing tissues and adult incontinence products. Providência operates state-of-the-art spunmelt technology, utilizing 13 Reicofil lines situated in three sites in North and South America. Providência was founded in 1963 and is based in São José dos Pinhais, Brazil. Following the completion of the Providência acquisition, Herminio Vicente Smania de Freitas joined AVINTIV as President—South America & Global Hygiene. He continues to serve as Chief Executive Officer of Providência.

The Providência Acquisition strengthened our competitive position in North and South America. With three well-invested manufacturing facilities (two in Brazil and one in the United States) focused on hygiene applications, Providência’s operations were highly complementary with our existing operations. In particular, as a result of the acquisition, we became the largest producer of nonwovens in South America, with facilities in Brazil, Argentina and Colombia that enable us to cost-effectively serve customers across the continent. We have begun the integration of Providência into our existing regional operations and expect to generate meaningful cost savings from the elimination of duplicative costs, implementation of best practices, and by leveraging our enhanced scale.

Fiberweb is one of the largest global manufacturers of specialized technical fabrics with eight production sites in six countries. Fiberweb creates specialty materials that are found in many critical applications, including hygiene and healthcare, as well as house wrap, filtration, dryer sheets, and several other specialized niche applications. In each area, Fiberweb helps its customers meet a range of technical challenges from precise filtration to reducing the energy demands of housing.

With operations in North America and Europe, Fiberweb improved our capabilities in several existing applications (such as hygiene and healthcare) but also meaningfully expanded our positions in several complementary applications, such as filtration, dryer sheets, and house wrap. Fiberweb also provided access to several new technologies such as S-Tex (hygiene) and Nano fiber (filtration), which offer differentiated products to address our customers’ needs for innovation and customized solutions. Fiberweb has been fully integrated into our European and North American regions and we believe will generate significant cost savings, in excess of our initial estimates. As of December 31, 2014, we have fully implemented initiatives at Fiberweb accounting for approximately $39.2 million of annualized savings (above our initial estimates of $28 million).

Recent Developments

Dounor Acquisition

On March 25, 2015, we announced that PGI France Holdings SAS, our wholly-owned subsidiary, entered into an agreement to acquire Dounor SAS (“Dounor”), a French manufacturer of materials used in hygiene, healthcare and industrial applications. The acquisition of Dounor was completed on April 17, 2015 using the proceeds from borrowings under an incremental amendment (the “Second Incremental Amendment”) to the Company’s existing Term Loan Facility.

Term Loan Facility Amendment

On April 17, 2015, we entered into the Second Incremental Amendment. Pursuant to the Second Incremental Amendment, we obtained $283.0 million of commitments for incremental term loans (the “2015 Additional Term Loans”). A portion of the proceeds of the 2015 Additional Term Loans were used to fund the

4

Table of Contents

consideration due in respect of the previously announced acquisition of Dounor. The remaining proceeds were used to redeem $200.0 million outstanding principal amount of our outstanding Senior Secured Notes, to pay related fees and expenses (including the redemption premium) and for general corporate purposes.

Redemption of Senior Secured Notes

On May 8, 2015, we redeemed $200.0 million of the outstanding principal amount of our Senior Secured Notes at a redemption price of 103.875% of the principal amount thereof, plus accrued and unpaid interest on the Senior Secured Notes to, but excluding, the redemption date.

Pending Acquisition by Berry Plastics

On July 31, 2015, Holdings announced that it had entered into a definitive agreement for Berry Plastics Group, Inc. (“Berry Plastics”) to acquire Holdings and its subsidiaries (including the Company) for approximately $2.45 billion in cash on a debt-free, cash-free basis (the “Merger”).

Simultaneously with the closing of the Merger, Berry Plastics expects to repay, or cause to be repaid, on behalf of Holdings and its subsidiaries, all outstanding indebtedness under (1) the Term Loan Facility, including Term Loans, Additional Term Loans and 2015 Additional Term Loans; (2) the ABL Facility; (3) the Senior Secured Notes; and (4) the Senior Unsecured Notes. The Merger, which is subject to customary closing conditions, is expected to close by the end of 2015. There is no assurance that the Merger or the repayment of indebtedness described above will be consummated within any particular time period or at all.

5

Table of Contents

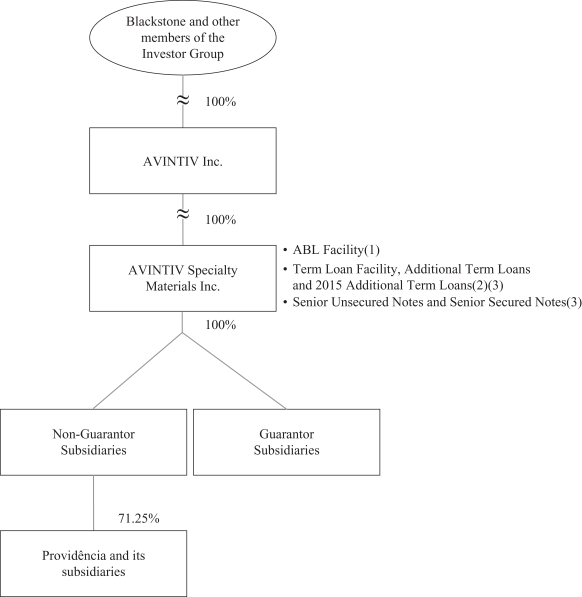

The following chart summarizes our organizational structure, equity ownership and our principal indebtedness as of the date of this prospectus. This chart is provided for illustrative purposes only and does not represent all legal entities of the Company and its consolidated subsidiaries or all obligations of such entities.

| (1) | Our ABL Facility is secured, subject to certain limitations and exclusions, by (i) a first-priority security interest in personal property of the Issuer and the subsidiary guarantors consisting of accounts receivable (including related contracts and contract rights, inventory, cash, deposit accounts, other bank accounts and securities accounts), inventory, intercompany notes and intangible assets (other than intellectual property), instruments, chattel paper, documents and commercial tort claims to the extent arising out of the foregoing, books and records of the Issuer, and the proceeds thereof including any business interruption insurance |

6

Table of Contents

| proceeds, subject to permitted liens and other customary exceptions (the “ABL Priority Collateral”); and (ii) a second-priority security interest in the collateral securing the Senior Secured Notes and the Term Loan Facility (described below). See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Indebtedness—ABL Facility.” |

| (2) | The Senior Secured Notes and the Term Loan Facility, the Additional Term Loans and the 2015 Additional Term Loans are secured (i) together with up to $7.5 million under the ABL Facility, on a first-priority lien basis by substantially all of the assets of the Issuer, and any existing and future subsidiary guarantors (other than ABL Priority Collateral), including all of the capital stock of the Issuer and each restricted subsidiary (which, in the case of foreign subsidiaries, will be limited to 65% of the capital stock of each first-tier foreign subsidiary) and (ii) on a second-priority basis by the ABL Priority Collateral, in each case, subject to certain exceptions and permitted liens. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Indebtedness.” |

| (3) | The Senior Secured Notes, the notes, the ABL Facility and the Term Loan Facility (including the Additional Term Loans and the 2015 Additional Term Loans) are unconditionally guaranteed, jointly and severally, on a senior basis, by each of our existing and future material wholly-owned domestic restricted subsidiaries and by certain other restricted subsidiaries that guarantee our or a subsidiary guarantor’s indebtedness as described herein. Our existing and future foreign subsidiaries are not expected to guarantee the notes. In addition, the ABL Facility, the Term Loan Facility, the Additional Term Loans and the 2015 Additional Term Loans are guaranteed by Parent. |

Corporate Information

AVINTIV Specialty Materials Inc. was incorporated under the laws of the State of Delaware in 1994. Our principal executive office is located at 9335 Harris Corners Parkway, Suite 300, Charlotte, North Carolina. Our telephone number is (704) 697-5100.

Our Sponsor

Blackstone (NYSE: BX) is one of the world’s leading investment firms. Blackstone’s asset management businesses, with approximately $310.5 billion in assets under management as of March 31, 2015, include investment vehicles focused on private equity, real estate, public debt and equity, non-investment grade debt and secondary funds, all on a global basis. Blackstone also provides various financial advisory services, including financial and strategic advisory, restructuring and reorganization advisory and fund placement services.

7

Table of Contents

The Exchange Offer

The following summary is provided solely for your convenience and is not intended to be complete. You should read the full text and more specific details contained elsewhere in this prospectus for a more detailed description of the notes.

| General |

On June 11, 2014, the Issuer issued in a private offering $210,000,000 aggregate principal amount of 6.875% Senior Notes due 2019. In connection with the private offering, the Issuer and the guarantors of the outstanding notes entered into a registration rights agreement with the initial purchasers pursuant to which they agreed, among other things, to complete the exchange offer on or prior to September 4, 2015. |

You are entitled to exchange in the exchange offer your outstanding notes for exchange notes which are identical in all material respects to the outstanding notes except:

| • | the exchange notes have been registered under the Securities Act; |

| • | the exchange notes are not entitled to any registration rights which are applicable to the outstanding notes under the registration rights agreement; and |

| • | the additional interest provisions of the registration rights agreement are not applicable. |

| The Exchange Offer |

The Issuer is offering to exchange $210,000,000 aggregate principal amount of 6.875% Senior Notes due 2019 which have been registered under the Securities Act for any and all of its existing unregistered 6.875% Senior Notes due 2019 that were issued on June 11, 2014. |

| You may only exchange outstanding notes in a principal amount of $2,000 or in integral multiples of $1,000 in excess thereof. |

| Resale |

Based on an interpretation by the staff of the Securities and Exchange Commission (the “SEC”) set forth in no-action letters issued to third parties, we believe that the exchange notes issued pursuant to the exchange offer in exchange for outstanding notes may be offered for resale, resold and otherwise transferred by you (unless you are our “affiliate” within the meaning of Rule 405 under the Securities Act) without compliance with the registration and prospectus delivery provisions of the Securities Act, provided that: |

| • | you are acquiring the exchange notes in the ordinary course of your business; and |

| • | you have not engaged in, do not intend to engage in, and have no arrangement or understanding with any person to participate in, a distribution of the exchange notes. |

| If you are a broker-dealer and receive exchange notes for your own account in exchange for outstanding notes that you acquired as a |

8

Table of Contents

| result of market-making activities or other trading activities, you must acknowledge that you will deliver this prospectus in connection with any resale of the exchange notes. See “Plan of Distribution.” |

| Any holder of outstanding notes who: |

• is our affiliate;

• does not acquire exchange notes in the ordinary course of its business; or

• tenders its outstanding notes in the exchange offer with the intention to participate, or for the purpose of participating, in a distribution of exchange notes;

| cannot rely on the position of the staff of the SEC enunciated in Morgan Stanley & Co. Incorporated (available June 5, 1991) and Exxon Capital Holdings Corporation (available May 13, 1988), as interpreted in the SEC’s letter to Shearman & Sterling (available July 2, 1993), or similar no-action letters and, in the absence of an exemption therefrom, must comply with the registration and prospectus delivery requirements of the Securities Act in connection with any resale of the exchange notes. |

| Expiration Date |

The exchange offer will expire at 5:00 p.m., New York City time, on September 8, 2015, which is the 21st business day after the date of this prospectus, unless extended by the Issuer. The Issuer does not currently intend to extend the expiration date. |

| Withdrawal |

You may withdraw the tender of your outstanding notes at any time prior to the expiration of the exchange offer. The Issuer will return to you any of your outstanding notes that are not accepted for any reason for exchange, without expense to you, promptly after the expiration or termination of the exchange offer. |

| Interest on the exchange notes and the outstanding notes |

The exchange notes will bear interest at the rate per annum set forth on the cover page of this prospectus from the most recent date to which interest has been paid on the outstanding notes. The interest will be payable semi-annually on June 1 and December 1. No interest will be paid on outstanding notes following their acceptance for exchange. |

| Conditions to the Exchange Offer |

The exchange offer is subject to customary conditions, which the Issuer may waive. |

| See “The Exchange Offer—Conditions to the Exchange Offer.” |

| Procedures for Tendering Outstanding Notes |

If you wish to participate in the exchange offer, you must complete, sign and date the accompanying letter of transmittal, or a facsimile of such letter of transmittal, according to the instructions contained in |

9

Table of Contents

| this prospectus and the letter of transmittal. You must then mail or otherwise deliver the letter of transmittal, or a facsimile of such letter of transmittal, together with the outstanding notes and any other required documents, to the exchange agent at the address set forth on the cover page of the letter of transmittal. |

| If you hold outstanding notes through The Depository Trust Company (“DTC”) and wish to participate in the exchange offer, you must comply with the Automated Tender Offer Program procedures of DTC, by which you will agree to be bound by the letter of transmittal. By signing or agreeing to be bound by the letter of transmittal, you will represent to us that, among other things: |

| • | you are not our “affiliate” within the meaning of Rule 405 under the Securities Act or, if you are our affiliate, that you will comply with any applicable registration and prospectus delivery requirements of the Securities Act; |

| • | you do not have an arrangement or understanding with any person or entity to participate in the distribution of the exchange notes; |

| • | you are acquiring the exchange notes in the ordinary course of your business; and |

| • | if you are a broker-dealer that will receive exchange notes for your own account in exchange for outstanding notes that were acquired as a result of market-making activities, that you will deliver a prospectus, as required by law, in connection with any resale of such exchange notes. |

| Special Procedures for Beneficial Owners |

If you are a beneficial owner of outstanding notes that are registered in the name of a broker, dealer, commercial bank, trust company or other nominee, and you wish to tender those outstanding notes in the exchange offer, you should contact the registered holder promptly and instruct the registered holder to tender those outstanding notes on your behalf. If you wish to tender on your own behalf, you must, prior to completing and executing the letter of transmittal and delivering your outstanding notes, either make appropriate arrangements to register ownership of the outstanding notes in your name or obtain a properly completed bond power from the registered holder. The transfer of registered ownership may take considerable time and may not be able to be completed prior to the expiration date. |

| Guaranteed Delivery Procedures |

If you wish to tender your outstanding notes and your outstanding notes are not immediately available or you cannot deliver your outstanding notes, the letter of transmittal or any other required documents, or you cannot comply with the applicable procedures under DTC’s Automated Tender Offer Program for transfer of book-entry interests, prior to the expiration date, you must tender your outstanding notes according to the guaranteed delivery procedures set forth in this prospectus under “The Exchange Offer—Guaranteed Delivery Procedures.” |

10

Table of Contents

| Effect on Holders of Outstanding Notes |

As a result of the making of, and upon acceptance for exchange of all validly tendered outstanding notes pursuant to the terms of the exchange offer, the Issuer and the guarantors will have fulfilled a covenant under the registration rights agreement. Accordingly, there will be no increase in the interest rate on the outstanding notes under the circumstances described in the registration rights agreement. If you do not tender your outstanding notes in the exchange offer, you will continue to be entitled to all the rights and limitations applicable to the outstanding notes as set forth in the indenture governing the outstanding notes, except the Issuer and the guarantors will not have any further obligation to you to provide for the exchange and registration of the outstanding notes under the registration rights agreement. To the extent that outstanding notes are tendered and accepted in the exchange offer, the trading market for remaining outstanding notes that are not so tendered and exchanged could be adversely affected. |

| Consequences of Failure to Exchange |

All untendered outstanding notes will continue to be subject to the restrictions on transfer set forth in the outstanding notes and in the indenture governing the outstanding notes. In general, the outstanding notes may not be offered or sold unless registered under the Securities Act, except pursuant to an exemption from, or in a transaction not subject to, the Securities Act and applicable state securities laws. Other than in connection with the exchange offer, the Issuer and the guarantors do not currently anticipate that they will register the outstanding notes under the Securities Act. |

| Certain U.S. Federal Income Tax Considerations |

The exchange of outstanding notes for exchange notes in the exchange offer will not be a taxable event for U.S. federal income tax purposes. See “Certain U.S. Federal Income Tax Considerations.” |

| Use of Proceeds |

We will not receive any cash proceeds from the issuance of exchange notes in the exchange offer. See “Use of Proceeds.” |

| Exchange Agent |

Wilmington Trust, National Association is the exchange agent for the exchange offer. The addresses and telephone numbers of the exchange agent are set forth in the section captioned “The Exchange Offer—Exchange Agent” of this prospectus. |

11

Table of Contents

The Exchange Notes

The terms of the exchange notes are identical in all material respects to the terms of the outstanding notes, except that the exchange notes will not contain terms with respect to transfer restrictions or additional interest upon a failure to fulfill certain of our obligations under the registration rights agreement. The exchange notes will evidence the same debt as the outstanding notes. The exchange notes will be governed by the same indenture under which the outstanding notes were issued. The following summary is not intended to be a complete description of the terms of the exchange notes. For a more detailed description of the notes, see “Description of the Notes.”

| Issuer |

AVINTIV Specialty Materials Inc. (formerly known as Polymer Group, Inc.) |

| Notes Offered |

$210.0 million aggregate principal amount of 6.875% Senior Notes due 2019. |

| Maturity Date |

June 1, 2019. |

| Interest |

The exchange notes will accrue interest at a rate of 6.875% per annum, payable on June 1 and December 1 of each year. |

| Guarantees |

The exchange notes will be fully and unconditionally guaranteed, jointly and severally, on a senior unsecured basis, by our wholly-owned domestic restricted subsidiaries that guarantee our or a subsidiary guarantor’s indebtedness (including the outstanding notes) and any non-wholly owned domestic restricted subsidiaries that guarantee our or a subsidiary guarantor’s capital markets debt securities, in each case, as described herein. Our existing and future foreign subsidiaries are not expected to guarantee the notes. These guarantees are subject to release under specified circumstances. See “Description of the Notes—Guarantees.” |

| Ranking |

The exchange notes and guarantees thereof will be our and our guarantors’ senior unsecured obligations and will rank: |

| • | equally in right of payment with all of our and the guarantors’ existing and future senior unsecured obligations; and |

| • | senior in right of payment to any of our and our guarantors’ subordinated indebtedness. |

| The exchange notes and the guarantees thereof will be effectively subordinated in right of payment to our and the guarantors’ secured indebtedness, including the ABL Facility, the Senior Secured Notes, the Term Loans, the Additional Term Loans and the 2015 Additional Term Loans, to the extent of the value of the collateral securing such indebtedness. |

| The exchange notes will also be structurally subordinated to all existing and future indebtedness, claims of holders of preferred stock and other liabilities (including trade payables) of our subsidiaries that do not guarantee the notes. |

| As of March 31, 2015: |

| • | we had $1,475.5 million of total indebtedness outstanding, all of which was senior; |

12

Table of Contents

| • | we had $1,205.3 million of senior secured indebtedness outstanding; and |

| • | we had $51.7 million of availability to incur secured indebtedness under our revolving ABL Facility (after giving effect to $19.3 million of outstanding letters of credit). |

| On a pro forma basis, the Company’s non-guarantor subsidiaries accounted for $1,449.8 million, or 72%, of net sales for the year ended December 31, 2014. The Company’s non-guarantor subsidiaries accounted for $327.8 million, or 71%, of net sales for the three months ended March 31, 2015, respectively. As of March 31, 2015, the Company’s non-guarantor subsidiaries accounted for $1,512.0 million, or 24%, of total assets and $1,383.5 million, or 26% of total liabilities (in each case, as adjusted for intercompany assets and liabilities). |

| Optional Redemption |

We may, at our option, redeem at any time and from time to time prior to December 1, 2015 some or all of the exchange notes at 100% of their principal amount thereof plus accrued and unpaid interest to the redemption date plus the applicable “make-whole premium” described under “Description of the Notes—Optional Redemption.” From and after December 1, 2015, we may, at our option, redeem at any time and from time to time some or all of the exchange notes at the applicable redemption prices set forth in this prospectus. In addition, on or prior to December 1, 2015, we may, at our option, redeem up to 35% of the notes, including the exchange notes, with the proceeds from certain equity offerings at the applicable redemption prices listed under “Description of the Notes—Optional Redemption.” |

| Change of Control Offer |

Upon the occurrence of specific kinds of a change of control, if we do not redeem the exchange notes, you will have the right, as holders of the exchange notes, to require us to repurchase some or all of your exchange notes at 101% of their principal amount, plus accrued and unpaid interest to the repurchase date. See “Description of the Notes—Repurchase at the Option of Holders—Change of Control.” |

| Asset Sale Proceeds |

If the Issuer or its restricted subsidiaries engage in asset sales, the Issuer generally must either invest the net proceeds from such asset sales in its business within a specific period of time, prepay certain of its or its restricted subsidiaries’ debt or make an offer to purchase a principal amount of the exchange notes with the specified excess net proceeds, subject to certain exceptions. The purchase price of the exchange notes will be 100% of their principal amount plus accrued and unpaid interest, if any. For more information, see “Description of the Notes—Repurchase at the Option of Holders—Asset Sales.” |

| Certain Covenants |

The indenture governing the exchange notes contains covenants that, among other things, limit our ability and the ability of certain of our subsidiaries to: |

| • | incur or guarantee additional debt or issue disqualified stock or preferred stock; |

13

Table of Contents

| • | pay dividends and make other distributions on, or redeem or repurchase, capital stock; |

| • | make certain investments; |

| • | incur certain liens; |

| • | enter into transactions with affiliates; |

| • | merge or consolidate; |

| • | enter into agreements that restrict the ability of restricted subsidiaries to make dividends or other payments to the Issuer; |

| • | designate restricted subsidiaries as unrestricted subsidiaries; and |

| • | transfer or sell assets. |

| These covenants are subject to a number of important limitations and exceptions. In addition, during any period of time that the exchange notes have investment grade ratings from both Moody’s Investors Service, Inc. and Standard & Poor’s, many of the covenants will be suspended. See “Description of the Notes—Certain Covenants.” |

| Use of Proceeds |

We will not receive any proceeds from the exchange offer. See “Use of Proceeds.” |

| No Prior Market |

The exchange notes will generally be freely transferable (subject to certain restrictions discussed in “The Exchange Offer”) but will be a new issue of securities for which there will not initially be a market. Accordingly, there can be no assurance as to the development or liquidity of any market for the exchange notes. The initial purchasers in the private offering of the outstanding notes have advised us that they currently intend to make a market for the exchange notes, as permitted by applicable laws and regulations. However, they are not obligated to do so and may discontinue any such market-making activities at any time without notice. We do not intend to apply for a listing of the exchange notes on any securities exchange or automated dealer quotation system. |

| Governing Law |

The exchange notes will be governed by the laws of the State of New York. |

Risk Factors

You should carefully consider the information set forth under the caption “Risk Factors” beginning on page 18 of this prospectus before participating in the exchange offer.

14

Table of Contents

Summary Historical and Pro Forma Condensed Combined Financial Information

The following summary historical and pro forma condensed combined financial information and other data set forth below should be read in conjunction with “Summary—Recent Acquisitions,” “Basis of Presentation,” “Unaudited Pro Forma Condensed Combined Financial Information” and the historical financial statements of the Company and Providência, including the related notes, included elsewhere in this prospectus.

The summary historical financial information presented below as of and for the fiscal years ended December 31, 2014, December 28, 2013 and December 29, 2012 has been derived from our audited consolidated financial statements included elsewhere in this prospectus. The summary historical financial information presented below is not necessarily indicative of the results to be expected for any future period. The summary historical financial information and other data presented below as of March 31, 2015 and for the three month periods ended March 31, 2015 and March 29, 2014 have been derived from our unaudited consolidated financial statements included elsewhere in this prospectus. Operating results for the three months ended March 31, 2015 are not necessarily indicative of the results that may be expected for the fiscal year ended December 31, 2015.

The summary unaudited pro forma condensed combined financial information presented below is based upon the historical consolidated financial statements of the Company and Providência and has been prepared to illustrate the effects of the Providência Acquisition and the Providência Refinancing (collectively, the “Transactions”). The summary unaudited pro forma condensed combined statement of operations data for the fiscal year ended December 31, 2014 has been prepared to give pro forma effect to the Transactions as if they had occurred on December 29, 2013.

The summary unaudited pro forma condensed combined financial information includes only adjustments that are directly attributable to the Transactions, factually supportable and with respect to the statement of operations, expected to have a continuing impact on the combined results. The Providência Acquisition has been accounted for using the acquisition method of accounting in accordance with Financial Accounting Standards Board (“FASB”) Accounting Standard Codification (“ASC”) Topic 805, Business Combinations (“ASC 805”). ASC 805 requires, among other things, that the assets acquired and liabilities assumed be recognized at their acquisition date fair values, with any excess of the consideration transferred over the estimated fair values of the identifiable net assets acquired recorded as goodwill.

The summary unaudited pro forma condensed combined financial information has been presented for informational purposes only and is not necessarily indicative of what the combined company’s results of operations actually would have been had the Transactions been completed as of the dates indicated, nor is it necessarily indicative of future operating results of the combined company. As a result, the summary pro forma condensed combined statement of operations has not been adjusted to reflect future events that may have occurred since the date of acquisition and/or are expected to occur after the Transactions, including, but not limited to, the anticipated realization of ongoing savings from operating synergies and certain one-time charges we expect to incur in connection with the Providência Acquisition, including but not limited to, costs in connection with the integration of the operations of the Company and Providência.

15

Table of Contents

| (in thousands) | Three Months Ended March 31, 2015 |

Three Months Ended March 29, 2014 |

Pro Forma Fiscal Year Ended December 31, 2014 |

Fiscal Year Ended December 31, 2014 |

Fiscal Year Ended December 28, 2013 |

Fiscal Year Ended December 29, 2012 |

||||||||||||||||||

| (unaudited) | (unaudited) | (unaudited) | ||||||||||||||||||||||

| Statement of Operations Data: |

||||||||||||||||||||||||

| Net sales |

$ | 461,238 | $ | 422,584 | $ | 2,005,678 | $ | 1,859,914 | $ | 1,214,862 | $ | 1,155,163 | ||||||||||||

| Cost of goods sold |

(355,820 | ) | (348,119 | ) | (1,649,134 | ) | (1,526,406 | ) | (1,018,806 | ) | (957,917 | ) | ||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Gross profit |

105,418 | 74,465 | 356,544 | 333,508 | 196,056 | 197,246 | ||||||||||||||||||

| Selling, general and administrative expenses |

(64,989 | ) | (55,534 | ) | (280,490 | ) | (254,280 | ) | (153,188 | ) | (140,776 | ) | ||||||||||||

| Special charges, net |

|

(6,022 |

) |

(8,711 | ) | (40,633 | ) | (59,185 | ) | (33,188 | ) | (19,592 | ) | |||||||||||

| Other operating, net |

1,423 | (1,069 | ) | (3,346 | ) | (1,845 | ) | (2,512 | ) | 287 | ||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Operating income (loss) |

35,830 | 9,151 | 32,075 | 18,198 | 7,168 | 37,165 | ||||||||||||||||||

| Other income (expense): |

||||||||||||||||||||||||

| Interest expense |

(27,633 | ) | (17,906 | ) | (111,177 | ) | (96,153 | ) | (55,974 | ) | (50,414 | ) | ||||||||||||

| Debt modification and extinguishment costs |

|

— |

|

— | (2,587 | ) | (15,725 | ) | (3,334 | ) | — | |||||||||||||

| Foreign currency and other, net |

(43,923 | ) | 4,959 | (43,004 | ) | (27,083 | ) | (8,851 | ) | (5,134 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Income (loss) before income taxes |

(35,726 | ) | (3,796 | ) | (124,693 | ) | (120,763 | ) | (60,991 | ) | (18,383 | ) | ||||||||||||

| Income tax (provision) benefit |

(4,548 | ) | |

(5,700 |

) |

(5,400 | ) | 1,523 | 36,024 | (7,655 | ) | |||||||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| Net income (loss) |

(40,274 | ) | (9,496 | ) | (130,093 | ) | (119,240 | ) | (24,967 | ) | (26,038 | ) | ||||||||||||

| Less: Earnings attributable to noncontrolling interest and redeemable noncontrolling interest |

|

(316 |

) |

|

(16 |

) |

(9,573 | ) | (3,943 | ) | (34 | ) | — | |||||||||||

| Net income (loss) attributable to AVINTIV Specialty Materials Inc. |

$ | (39,958 | ) | $ | (9,480 | ) | $ | (120,520 | ) | $ | (115,297 | ) | $ | (24,933 | ) | $ | (26,038 | ) | ||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|||||||||||||

| (in thousands) | Three Months Ended March 31, 2015 |

Three Months Ended March 29, 2014 |

Fiscal Year Ended December 31, 2014 |

Fiscal

Year Ended December 28, 2013 |

Fiscal

Year Ended December 29, 2012 |

|||||||||||||||

| (unaudited) | (unaudited) | |||||||||||||||||||

| Statement of Cash Flows Data: |

||||||||||||||||||||

| Net cash provided by (used in) operating activities |

$ | (529 | ) | $ | (14,589 | ) | $ | 49,148 | $ | 16,850 | $ | 75,471 | ||||||||

| Net cash provided by (used in) investing activities |

$ | (10,591 | ) | $ | (14,172 | ) | $ | (436,682 | ) | $ | (337,759 | ) | $ | (50,233 | ) | |||||

| Net cash provided by (used in) financing activities |

$ | (1,744 | ) | $ | 2,849 | $ | 487,376 | $ | 308,190 | $ | (42 | ) | ||||||||

16

Table of Contents

| As of | ||||||||||||||||

| (in thousands) | Three Months Ended March 31, 2015 |

December 31, 2014 |

December 28, 2013 |

December 29, 2012 |

||||||||||||

| (unaudited) | ||||||||||||||||

| Balance Sheet Data: |

||||||||||||||||

| Cash and cash equivalents |

$ | 160,601 | $ | 178,491 | $ | 86,064 | $ | 97,879 | ||||||||

| Operating working capital(1) |

$ | 126,989 | $ | 100,115 | $ | 43,170 | $ | 29,628 | ||||||||

| Total assets |

$ | 1,901,761 | $ | 2,035,173 | $ | 1,464,520 | $ | 1,022,069 | ||||||||

| Short-term borrowings and long-term debt, including current portion |

$ | 1,475,507 | $ | 1,482,840 | $ | 896,668 | $ | 599,689 | ||||||||

| Redeemable noncontrolling interest |

$ | 76,584 | $ | 89,181 | $ | — | $ | — | ||||||||

| Total AVINTIV Specialty Materials Inc. shareholders’ equity (deficit) |

$ | (89,745 | ) | $ | (24,355 | ) | $ | 158,896 | $ | 139,202 | ||||||

| Ratio of earnings to fixed charges(2) |

— | — | — | — | ||||||||||||

| (1) | Operating working capital is defined as accounts receivable plus inventories less trade accounts payable and accrued liabilities. |

| (2) | For purposes of determining the ratio of earnings to fixed charges, earnings are defined as pre-tax earnings from continuing operations plus fixed charges. Fixed charges include interest expense on all indebtedness, amortization of debt issuance fees and one-third of rental expense on operating leases representing that portion of rental expense deemed to be attributable to interest. Earnings were insufficient to cover fixed charges for the three months ended March 31, 2015, the fiscal year ended December 31, 2014, the fiscal year ended December 28, 2013 and the fiscal year ended December 29, 2012 by $36.2 million, $121.9 million, $62.1 million and $20.0 million, respectively. |

17

Table of Contents

You should carefully consider the following risk factors and all other information contained in this prospectus before participating in the exchange offer. The risks and uncertainties described below are not the only risks facing us and your investment in the exchange notes. Additional risks and uncertainties that we are unaware of, or those we currently deem immaterial, also may become important factors that affect us. The following risks could materially and adversely affect our business, financial condition, cash flows or results of operations.

Risks Related to the Exchange Offer

If you choose not to exchange your outstanding notes in the exchange offer, the transfer restrictions currently applicable to your outstanding notes will remain in force and the market price of your outstanding notes could decline.

If you do not exchange your outstanding notes for exchange notes in the exchange offer, then you will continue to be subject to the transfer restrictions on the outstanding notes as set forth in the offering memorandum distributed in connection with the private offering of the outstanding notes. In general, the outstanding notes may not be offered or sold unless they are registered or exempt from registration under the Securities Act and applicable state securities laws. Except as required by the registration rights agreement, we do not intend to register resales of the outstanding notes under the Securities Act.

The tender of outstanding notes under the exchange offer will reduce the remaining principal amount of the outstanding notes, which may have an adverse effect upon and increase the volatility of, the market price of the outstanding notes due to reduction in liquidity.

Your ability to transfer the exchange notes may be limited by the absence of an active trading market, and an active trading market may not develop for the notes.

The exchange notes are a new issue of securities for which there is no established trading market. We do not intend to have the exchange notes listed on a national securities exchange or to arrange for quotation on any automated quotation system. The initial purchasers in the private offering of the outstanding notes have advised us that they intend to make a market in the exchange notes, as permitted by applicable laws and regulations; however, the initial purchasers are not obligated to make a market in the exchange notes, and they may discontinue their market-making activities at any time without notice. Therefore, we cannot assure you as to the development or liquidity of any trading market for the exchange notes. The liquidity of any market for the exchange notes will depend on a number of factors, including:

| • | the number of holders of exchange notes; |

| • | our operating performance and financial condition; |

| • | the market for similar securities; |

| • | the interest of securities dealers in making a market in the exchange notes; and |

| • | prevailing interest rates. |

Historically, the market for non-investment grade debt has been subject to disruptions that have caused substantial volatility in the prices of securities similar to the exchange notes. The market, if any, for the exchange notes may face similar disruptions that may adversely affect the prices at which you may sell your exchange notes. Therefore, you may not be able to sell your exchange notes at a particular time and the price that you receive when you sell may not be favorable.

18

Table of Contents

Risks Related To Our Business

The specialized markets in which we sell our products are highly competitive, as a result we may have difficulty growing our business and maintaining profit margins.

The markets for our products are highly competitive. The primary competitive factors include product innovation and performance, quality, service, cost, distribution and technical support. In addition, we compete against a number of competitors in each of our markets. Some of these competitors are larger companies that have greater financial, technological, manufacturing and marketing resources than we do. A reduction in overall demand, a significant increase in manufacturing capacity in excess of demand or increased costs to design and produce our products would likely further increase competition and that increased competition could lead to reduced sales or cause us to reduce our prices, which could lower our profit margins and impair our ability to grow.

The global nonwovens market has historically experienced stable growth. However, beginning in late 2010, several of our competitors, primarily in the hygiene markets, installed or announced an intent to install capacity in excess of what we believe to be then current market demand. Consequently, as this manufacturing capacity entered into commercial production, the short-term to mid-term excess supply created unfavorable market dynamics, resulting in a downward pressure on selling prices. In recent years, we believe growing demand has filled a portion of this excess capacity and we have observed fewer new capacity expansions, leading to improving capacity utilization in our view.

Increases in prices for raw materials and energy could reduce our profit margins.

The primary raw materials used to manufacture most of our products are polypropylene resins (accounting for approximately 75% of raw materials costs historically), polyester fiber, polyethylene resin and, to a lesser extent, rayon and tissue paper. In addition, energy-related costs are a significant expense for us (both directly and as inputs to our primary raw materials). The prices of raw materials and energy can be volatile and are susceptible to rapid and substantial changes due to factors beyond our control such as changing economic conditions, currency fluctuations, political unrest and instability in energy-producing nations, and supply and demand considerations. To the extent that we are able to pass along raw material price increases to some of our customers, there is often a delay between the time we are required to pay the increased raw material price and the time we are able to pass the increase on to our customers. To the extent we are not able to pass along all or a portion of such increased prices of raw materials, our cost of goods sold would increase and our operating income and margins would correspondingly decrease. There can be no assurance that the prices of raw materials and energy will not increase in the future or that we will be able to pass on any increases to our customers. In addition, volatility in the prices for raw materials could make it more difficult for us to pass along all or a portion of any increase to our customers. Material increases in raw material and energy prices that cannot be passed on to customers could have a material adverse effect on our profit margins, results of operations and financial condition.

The industries that we serve are subject to the overall economic environment and demand for end-use products.

Our net sales are affected by general economic conditions, and the development of demand for and prices of end-use products in the industries that we serve. Geographically, general economic conditions constitute important factors affecting the demand for our products. Our results may also be affected by the cyclicality of the end-uses applications and industries we serve, although these cycles vary across industries and geographic regions. Demand for and prices of our products have fluctuated during the past years as demand by end-users and intermediate converters has changed. A substantial decline in general economic conditions combined with a consequent decline in the prices and/or demand for our products could have an adverse effect on our business, results of operations or financial condition.

19

Table of Contents

The loss of any of our large volume customers could significantly reduce our revenues and profits.

A significant amount of our products are sold to large volume customers. We have one major customer, Procter & Gamble, that accounts for over approximately 12% of our business and our 20 largest customers represented approximately 51% of our sales in 2014. We also do not have any long-term volume commitments with our customers and, as a result, the amount, and prices at which, our customers purchase from us may vary across periods. As a result, a decrease in business from, or the loss of any large volume customers, could materially reduce our product sales, lower our profits and impair our financial condition.

Our international operations pose risks to our business that may not be present with our domestic operations.