Table of Contents

Filed Pursuant to Rule 424(b)(3)

Registration File No.

333-186965

INFORMATION STATEMENT/PROSPECTUS

CENTURY PROPERTIES FUND XIX, LP

Century Properties Fund XIX, LP, or CPF XIX, has entered into an agreement and plan of merger with a wholly owned subsidiary of Aimco Properties, L.P., or Aimco OP. Under the merger agreement, AIMCO CPF XIX Merger Sub LLC, or the Aimco Subsidiary, will be merged with and into CPF XIX, with CPF XIX as the surviving entity. The Aimco Subsidiary was formed for the purpose of effecting this transaction and does not have any assets or operations. In the merger, each limited partnership unit of CPF XIX, or Limited Partnership Unit, will be converted into the right to receive, at the election of the holder of such unit, either:

| • | $364.65 in cash, or |

| • | $364.65 in partnership common units of Aimco OP, or OP Units. |

The merger consideration of $364.65 per Limited Partnership Unit was based on independent third party appraisal of CPF XIX’s properties by Cogent Realty Advisors, or CRA, and KTR Real Estate Advisors LLC, or KTR, independent valuation firms.

The number of OP Units offered for each Limited Partnership Unit will be calculated by dividing $364.65 by the average closing price of common stock of Apartment Investment and Management Company, or Aimco, as reported on the New York Stock Exchange, or the NYSE, over the ten consecutive trading days ending on the second trading day immediately prior to the consummation of the merger. For example, as of April 16, 2013, the average closing price of Aimco common stock over the preceding ten consecutive trading days was $31.49, which would have resulted in 11.58 OP Units offered for each Limited Partnership Unit. However, if Aimco OP determines that the law of the state or other jurisdiction in which a limited partner resides would prohibit the issuance of OP Units in that state or other jurisdiction (or that registration or qualification in that state or jurisdiction would be prohibitively costly), then such limited partner will not be entitled to elect OP Units, and will receive cash.

The OP Units are not listed on any securities exchange nor do they trade in an active secondary market. However, after a one-year holding period, OP Units are redeemable for shares of Aimco common stock (on a one-for-one basis) or cash equal to the value of such shares, as Aimco OP elects. As a result, the trading price of Aimco common stock is considered a reasonable estimate of the fair market value of an OP Unit. Aimco’s common stock is listed and traded on the NYSE under the symbol “AIV.”

In the merger, Aimco OP’s interest in the Aimco Subsidiary will be converted into Limited Partnership Units. As a result, after the merger, Aimco OP will be the sole limited partner of CPF XIX and will own all of the outstanding Limited Partnership Units.

Within ten days after the effective time of the merger, Aimco OP will prepare and mail to the former holders of Limited Partnership Units an election form pursuant to which they can elect to receive cash or OP Units. Former holders of Limited Partnership Units may elect their form of consideration by completing and returning the election form in accordance with its instructions. If the information agent does not receive a properly completed election form from a former holder before 5:00 p.m., New York time on the 30th day after the mailing of the election form, the former holder will be deemed to have elected to receive cash. Former holders of Limited Partnership Units may also use the election form to elect to receive, in lieu of the merger consideration, the appraised value of their Limited Partnership Units, determined through an arbitration proceeding.

Under Delaware law, the merger must be approved by CPF XIX’s general partner and a majority in interest of the Limited Partnership Units. Fox Partners II, the general partner of CPF XIX, has determined that the merger is advisable, fair to and in the best interests of CPF XIX and its limited partners and has approved the merger and the merger agreement. As of April 16, 2013, there were issued and outstanding 89,233 Limited Partnership Units, and Aimco OP and its affiliates owned 60,711.66 of those units, or approximately 68.04% of the number of units outstanding. 25,228.66 of the Limited Partnership Units owned by an affiliate of Aimco OP are subject to a voting restriction, which requires the Limited Partnership Units to be voted in proportion to the votes cast with respect to Limited Partnership Units not subject to this voting restriction. Aimco OP and its affiliates have indicated that they will vote all of their Limited Partnership Units that are not subject to this restriction, 35,483 Limited Partnership Units or approximately 39.76% of the outstanding Limited Partnership Units, in favor of the merger agreement and the merger. As a result, affiliates of Aimco OP will vote a total of approximately 49,469 Limited Partnership Units, or approximately 55.44% of the outstanding Limited Partnership Units in favor of the merger agreement and the merger.

Aimco OP and its affiliates have indicated that they intend to take action by written consent, as permitted under the partnership agreement, to approve the merger on or about June 18, 2013. As a result, approval of the merger is assured, and your consent to the merger is not required.

WE ARE NOT ASKING YOU FOR A PROXY AND

YOU ARE REQUESTED NOT TO SEND US A PROXY

This information statement/prospectus contains information about the merger and the securities offered hereby, and the reasons that Fox Partners II, the general partner of CPF XIX, has decided that the merger is in the best interests of CPF XIX and its limited partners. CPF XIX’s general partner has conflicts of interest with respect to the merger that are described in greater detail herein. Please read this information statement/prospectus carefully, including the section entitled “Risk Factors” beginning on page 16. It provides you with detailed information about the merger and the securities offered hereby. The merger agreement is attached to this information statement/prospectus as Annex A.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the securities to be issued in connection with the merger, determined if this information statement/prospectus is truthful or complete, approved or disapproved of the merger, passed upon the merits or fairness of the merger, or passed upon the adequacy or accuracy of the disclosure in this information statement/prospectus. Any representation to the contrary is a criminal offense.

This information statement/prospectus is dated April 17, 2013, and is first being mailed to limited partners on or about April 19, 2013.

Table of Contents

WE ARE CURRENTLY SEEKING QUALIFICATION TO ALLOW ALL HOLDERS OF LIMITED PARTNERSHIP UNITS OF CPF XIX THE ABILITY TO ELECT TO RECEIVE OP UNITS IN CONNECTION WITH THE MERGER. HOWEVER, AT THE PRESENT TIME, IF YOU ARE A RESIDENT OF ONE OF THE FOLLOWING STATES, YOU ARE NOT PERMITTED TO ELECT TO RECEIVE OP UNITS IN CONNECTION WITH THE MERGER:

CALIFORNIA

THE ATTORNEY GENERAL OF THE STATE OF NEW YORK HAS NOT PASSED ON OR ENDORSED THE MERITS OF THIS OFFERING. ANY REPRESENTATION TO THE CONTRARY IS UNLAWFUL.

ADDITIONAL INFORMATION

This information statement/prospectus incorporates important business and financial information about Aimco from documents that it has filed with the Securities and Exchange Commission, or the SEC, but that have not been included in or delivered with this information statement/prospectus. For a listing of documents incorporated by reference into this information statement/prospectus, please see “Where You Can Find Additional Information” beginning on page 91 of this information statement/prospectus.

Aimco will provide you with copies of such documents relating to Aimco (excluding all exhibits unless Aimco has specifically incorporated by reference an exhibit in this information statement/prospectus), without charge, upon written or oral request to:

ISTC Corporation

P.O. Box 2347

Greenville, South Carolina 29602

(864) 239-1029

If you have any questions or require any assistance, please contact our information agent, Eagle Rock Proxy Advisors, LLC, by mail at 12 Commerce Drive, Cranford, New Jersey 07016; by fax at (908) 497-2349; or by telephone at (800) 217-9608.

ABOUT THIS INFORMATION STATEMENT/PROSPECTUS

This information statement/prospectus, which forms a part of a registration statement on Form S-4 filed with the SEC by Aimco and Aimco OP, constitutes a prospectus of Aimco OP under Section 5 of the Securities Act of 1933, as amended, or the Securities Act, with respect to the OP Units that may be issued to holders of Limited Partnership Units in connection with the merger, and a prospectus of Aimco under Section 5 of the Securities Act with respect to shares of Aimco common stock that may be issued in exchange for such OP Units tendered for redemption. This document also constitutes an information statement under Section 14(c) of the Securities Exchange Act of 1934, as amended, or the Exchange Act, with respect to the action to be taken by written consent to approve the merger.

Table of Contents

| Page | ||||

| 1 | ||||

| 4 | ||||

| 4 | ||||

| 5 | ||||

| Material United States Federal Income Tax Consequences of the Merger |

6 | |||

| 6 | ||||

| 8 | ||||

| 16 | ||||

| 16 | ||||

| 17 | ||||

| 17 | ||||

| Certain United States Tax Risks Associated with an Investment in the OP Units |

19 | |||

| SELECTED SUMMARY HISTORICAL FINANCIAL DATA OF APARTMENT INVESTMENT AND MANAGEMENT COMPANY |

21 | |||

| SELECTED SUMMARY HISTORICAL FINANCIAL DATA OF AIMCO PROPERTIES, L.P. |

23 | |||

| 25 | ||||

| 26 | ||||

| 27 | ||||

| 29 | ||||

| 30 | ||||

| 31 | ||||

| 32 | ||||

| Security Ownership of Certain Beneficial Owners and Management |

32 | |||

| 33 | ||||

| 34 | ||||

| 34 | ||||

| 37 | ||||

| 38 | ||||

| 38 | ||||

| Material United States Federal Income Tax Consequences of the Merger |

38 | |||

| 38 | ||||

| 38 | ||||

| 39 | ||||

| 39 | ||||

| 39 | ||||

| 40 | ||||

| 40 | ||||

| 40 | ||||

| 41 | ||||

| 41 | ||||

| 41 | ||||

| 41 | ||||

| 41 | ||||

| 41 | ||||

Table of Contents

| Page | ||||

| DESCRIPTION OF AIMCO OP UNITS; SUMMARY OF AIMCO OP PARTNERSHIP AGREEMENT |

43 | |||

| 43 | ||||

| 43 | ||||

| 43 | ||||

| 45 | ||||

| 45 | ||||

| 46 | ||||

| 47 | ||||

| 47 | ||||

| 47 | ||||

| 48 | ||||

| 48 | ||||

| 49 | ||||

| 49 | ||||

| 49 | ||||

| 50 | ||||

| 50 | ||||

| 50 | ||||

| 52 | ||||

| 52 | ||||

| 52 | ||||

| 58 | ||||

| COMPARISON OF CPF XIX LIMITED PARTNERSHIP UNITS AND AIMCO OP UNITS |

61 | |||

| 65 | ||||

| 66 | ||||

| United States Federal Income Tax Consequences Relating to the Merger |

67 | |||

| 67 | ||||

| 72 | ||||

| 86 | ||||

| 88 | ||||

| 89 | ||||

| 90 | ||||

| 91 | ||||

| Annexes |

||||

| A-1 | ||||

| B-1 | ||||

| C-1 | ||||

| D-1 | ||||

| Annex E CPF XIX’s Annual Report on Form 10-K for the year ended December 31, 2012 |

E-1 | |||

| F-1 | ||||

Table of Contents

This summary term sheet highlights the material information with respect to the merger, the merger agreement and the other matters described herein. It may not contain all of the information that is important to you. You are urged to carefully read the entire information statement/prospectus and the other documents referred to in this information statement/prospectus, including the merger agreement. Aimco, Aimco OP, Fox Partners II and Aimco’s subsidiaries that may be deemed to directly or indirectly beneficially own limited partnership units of CPF XIX are referred to herein, collectively, as the “Aimco Entities.”

| • | The Merger: CPF XIX has entered into an agreement and plan of merger with the Aimco Subsidiary and Aimco OP. Under the merger agreement, at the effective time of the merger, the Aimco Subsidiary will be merged with and into CPF XIX, with CPF XIX as the surviving entity. A copy of the merger agreement is attached as Annex A to this information statement/prospectus. You are encouraged to read the merger agreement carefully in its entirety because it is the legal agreement that governs the merger. |

| • | Merger Consideration: In the merger, each Limited Partnership Unit will be converted into the right to receive, at the election of the holder of such Limited Partnership Unit, either $364.65 in cash or equivalent value in OP Units, except in those jurisdictions where the law prohibits the offer of OP Units (or registration or qualification would be prohibitively costly). The number of OP Units issuable with respect to each Limited Partnership Unit will be calculated by dividing the $364.65 per unit cash merger consideration by the average closing price of Aimco common stock, as reported on the NYSE over the ten consecutive trading days ending on the second trading day immediately prior to the consummation of the merger. Each holder of Limited Partnership Units must make the same election (cash or OP Units) for all of his or her Limited Partnership Units. For a full description of the determination of the merger consideration, see “The Merger — Determination of Merger Consideration” beginning on page 37. |

| • | Fairness of the Merger: Although the Aimco Entities have interests that may conflict with those of CPF XIX’s unaffiliated limited partners, each of the Aimco Entities believes that the merger is fair to the unaffiliated limited partners of CPF XIX. The merger consideration of $364.65 was based on separate, independent third party appraisals of each of CPF XIX’s properties by both CRA and KTR, independent valuation firms. |

| • | Effects of the Merger: After the merger, Aimco OP will be the sole limited partner in CPF XIX, and will own all of the outstanding Limited Partnership Units. As a result, after the merger, you will cease to have any rights in CPF XIX as a limited partner. See “Special Factors — Effects of the Merger,” beginning on page 5. |

| • | Appraisal Rights: Pursuant to the terms of the merger agreement, Aimco OP will provide each limited partner with contractual dissenters’ appraisal rights that are similar to the dissenters’ appraisal rights available to a stockholder of a constituent corporation in a merger under Delaware law, and which will enable a limited partner to obtain an appraisal of the value of the limited partner’s Limited Partnership Units in connection with the merger. See “The Merger — Appraisal Rights,” beginning on page 39. A description of the appraisal rights being provided, and the procedures that a limited partner must follow to seek such rights, is attached to this information statement/prospectus as Annex B. |

| • | List of Investors: Under CPF XIX’s partnership agreement and Delaware law, a limited partner has the right to obtain by mail, free of charge, a list of the names and addresses and interests owned of the limited partners. This list may be obtained by making written request to Fox Partners II, c/o Eagle Rock Proxy Advisors, LLC, 12 Commerce Drive, Cranford, New Jersey 07016, or by fax at (908) 497-2349. |

| • | Parties Involved: |

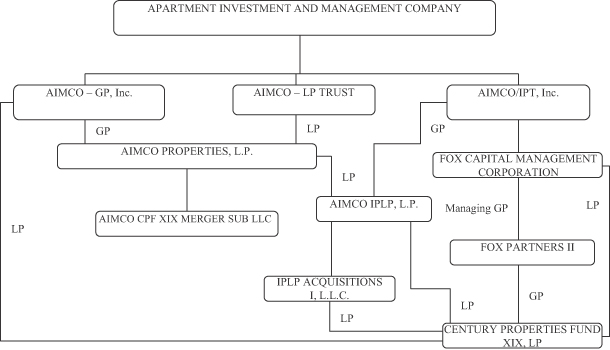

| • | Century Properties Fund XIX, LP, or CPF XIX, is a Delaware limited partnership formed on October 2, 2008, following a redomestication of a predecessor California limited partnership in Delaware. CPF XIX owns and operates two investment properties, which are collectively referred to as the properties: Lakeside at Vinings Mountain, a 220 unit apartment project located in Atlanta, Georgia, or the Lakeside Property; and The Peak at Vinings Mountain, a 280 unit apartment project located in |

1

Table of Contents

| Atlanta, Georgia, or the Peak Property. See “Information About Century Properties Fund XIX,” beginning on page 29. CPF XIX’s principal address is 80 International Drive, Suite 130, Greenville, South Carolina 29615, and its telephone number is (864) 239-1000. |

| • | Apartment Investment and Management Company, or Aimco, is a Maryland corporation that is a self-administered and self-managed real estate investment trust, or REIT. Aimco’s principal financial objective is to provide predictable and attractive returns to its stockholders. Aimco’s common stock is listed and traded on the NYSE under the symbol “AIV.” See “Information about the Aimco Entities,” beginning on page 27. Aimco’s principal address is 4582 South Ulster Street, Suite 1100, Denver, Colorado 80237, and its telephone number is (303) 757-8101. |

| • | AIMCO Properties, L.P., or Aimco OP, is a Delaware limited partnership which, through its operating divisions and subsidiaries, holds substantially all of Aimco’s assets and manages the daily operations of Aimco’s business and assets. See “Information about the Aimco Entities,” beginning on page 27. Aimco OP’s principal address is 4582 South Ulster Street, Suite 1100, Denver, Colorado 80237, and its telephone number is (303) 757-8101. |

| • | AIMCO CPF XIX Merger Sub LLC, or the Aimco Subsidiary, is a Delaware limited liability company formed for the purpose of consummating the merger with CPF XIX. The Aimco Subsidiary is a direct wholly-owned subsidiary of Aimco OP. See “Information about the Aimco Entities,” beginning on page 27. |

| • | Reasons for the Merger: Aimco and Aimco OP are in the business of acquiring, owning and managing apartment properties such as those owned by CPF XIX, and have decided to proceed with the merger as a means of acquiring the properties currently owned by CPF XIX in a manner that they believe (i) provides fair value to limited partners, (ii) offers limited partners an opportunity to receive immediate liquidity, or defer recognition of taxable gain (except where the law of the state or other jurisdiction in which a limited partner resides would prohibit the issuance of OP Units in that state or other jurisdiction, or where registration or qualification would be prohibitively costly, and except to the extent described in “Material United States Federal Income Tax Considerations – United States Federal Income Tax Consequences Relating to the Merger” beginning on page 67), and (iii) relieves CPF XIX of the expenses associated with a sale of the properties, including marketing and other transaction costs. The Aimco Entities decided to proceed with the merger at this time for the following reasons: |

| • | In the absence of a transaction, CPF XIX limited partners have only limited options to liquidate their investment in CPF XIX. The Limited Partnership Units are not traded on an exchange or other reporting system, and transactions in the securities are limited and sporadic. |

| • | The value of the properties owned by CPF XIX is not sufficient to justify its continued operation as a public company. As a public company with a significant number of unaffiliated limited partners, CPF XIX incurs costs associated with preparing audited annual financial statements, unaudited quarterly financial statements, tax returns and partner Schedule K-1s, and periodic SEC reports and other expenses. The Aimco Entities estimate these costs to be approximately $130,000 per year. The merger will eliminate a significant amount of these costs. |

| • | CPF XIX has been operating at a loss from continuing operations for the past several years, and has depended, in part, on loans from Aimco OP to fund its operations and capital improvements at its properties. At December 31, 2012, the total amount of loans owed by CPF XIX to Aimco OP was approximately $166,000. CPF XIX may receive additional advances of funds from Aimco OP, although Aimco OP is not obligated to provide such advances. If the Aimco Entities acquire 100% of the limited partnership interests of CPF XIX, they will have greater flexibility in financing and operating its properties. |

| • | Conflicts of Interest: CPF XIX’s general partner, Fox Partners II, is a general partnership, the managing general partner of which is wholly-owned and controlled by Aimco. Therefore, Fox Partners II has a conflict of interest with respect to the merger. Fox Partners II has fiduciary duties to its general partners and Aimco, as the beneficial owner of its managing general partner, on the one hand, and to the limited |

2

Table of Contents

| partners of CPF XIX, on the other hand. The duties of Fox Partners II to the limited partners of CPF XIX conflict with the duties of Fox Partners II to its general partners, which could result in Fox Partners II approving a transaction that is more favorable to Aimco than might be the case absent such conflict of interest. See “The Merger — Conflicts of Interest,” beginning on page 38. |

| • | Risk Factors: In evaluating the merger agreement and the merger, CPF XIX limited partners should carefully read this information statement/prospectus and especially consider the factors discussed in the section entitled “Risk Factors” beginning on page 16. Some of the risk factors associated with the merger are summarized below: |

| • | Aimco beneficially owns the managing general partner of Fox Partners II, the general partner of CPF XIX. As a result, Fox Partners II has a conflict of interest in the merger. A transaction with a third party in the absence of this conflict could result in better terms or greater consideration to CPF XIX limited partners. |

| • | CPF XIX limited partners who receive cash may recognize taxable gain in the merger and that gain could exceed the merger consideration. In addition, limited partners who receive OP Units in the merger could recognize taxable gain to the extent described in “Material United States Federal Income Tax Considerations – United States Federal Income Tax Consequences Relating to the Merger” beginning on page 67. |

| • | There are a number of significant differences between the Limited Partnership Units and Aimco OP Units relating to, among other things, the nature of the investment, voting rights, distributions and liquidity and transferability/redemption. For more information regarding those differences, see “Comparison of CPF XIX Limited Partnership Units and Aimco OP Units,” beginning on page 61. |

| • | CPF XIX limited partners may elect to receive OP Units as merger consideration, and there are risks related to an investment in OP Units, including the fact that there are restrictions on transferability of OP Units; there is no public market for OP Units; and there is no assurance as to the value that might be realized upon a future redemption of OP Units. |

| • | Material United States Federal Income Tax Consequences of the Merger: In general, any payment of cash for Limited Partnership Units will be treated as a sale of such Limited Partnership Units by the holder thereof, and any exchange of Limited Partnership Units for OP Units under the terms of the merger agreement will be treated as a tax free transaction, except to the extent described in “Material United States Federal Income Tax Considerations — United States Federal Income Tax Consequences Relating to the Merger” beginning on page 67. |

The foregoing is a general discussion of the material U.S. federal income tax consequences of the merger. This summary does not discuss all aspects of U.S. federal income taxation that may be relevant to you in light of your specific circumstances or if you are subject to special treatment under the U.S. federal income tax laws. The particular tax consequences of the merger to you will depend on a number of factors related to your tax situation. You should review “Material United States Federal Income Tax Considerations,” herein and consult your tax advisors for a full understanding of the tax consequences to you of the merger.

3

Table of Contents

Purposes, Alternatives and Reasons for the Merger

Aimco and Aimco OP are in the business of acquiring, owning and managing apartment properties such as those owned by CPF XIX, and have decided to proceed with the merger as a means of acquiring the properties currently owned by CPF XIX in a manner they and the other Aimco Entities believe (i) provides fair value to limited partners, (ii) offers limited partners an opportunity to receive immediate liquidity, or defer recognition of taxable gain (except where the law of the state or other jurisdiction in which a limited partner resides would prohibit the issuance of OP Units in that state or other jurisdiction, or where registration or qualification would be prohibitively costly, and except to the extent described in “Material United States Federal Income tax Considerations – United States Federal Income Tax Consequences Relating to the Merger” beginning on page 67), and (iii) relieves CPF XIX of the expenses associated with a sale of the properties, including marketing and other transaction costs.

The Aimco Entities determined to proceed with the merger at this time for the following reasons:

| • | In the absence of a transaction, CPF XIX limited partners have only limited options to liquidate their investment in CPF XIX. The Limited Partnership Units are not traded on an exchange or other reporting system, and transactions in the securities are limited and sporadic. |

| • | The value of the properties owned by CPF XIX is not sufficient to justify its continued operation as a public company. As a public company with a significant number of unaffiliated limited partners, CPF XIX incurs costs associated with preparing audited annual financial statements, unaudited quarterly financial statements, tax returns and partner Schedule K-1s, periodic SEC reports and other expenses. The Aimco Entities estimate these costs to be approximately $130,000 per year. The merger will eliminate a significant amount of these costs. |

| • | CPF XIX has been operating at a loss from continuing operations for the past several years, and has depended, in part, on loans from Aimco OP to fund its operations and capital improvements at its properties. At December 31, 2012, the total amount of loans owed by CPF XIX to Aimco OP was approximately $166,000. CPF XIX may receive additional advances of funds from Aimco OP, although Aimco OP is not obligated to provide such advances. If the Aimco Entities acquire 100% of the limited partnership interests of CPF XIX, they will have greater flexibility in financing and operating its properties. |

Before deciding to proceed with the merger, Fox Partners II and the other Aimco Entities considered the alternatives described below:

Continuation of CPF XIX as a Public Company Operating the Properties. Fox Partners II and the other Aimco Entities did not consider the continuation of CPF XIX as a public company operating the properties to be a viable alternative primarily because of the costs associated with preparing financial statements, tax returns, periodic SEC reports and other expenses. If CPF XIX is unable to generate sufficient funds to cover operating expenses, advances from Aimco OP may not be available in the future as Aimco OP is not obligated to provide such advances.

Liquidation of CPF XIX. As discussed above, Fox Partners II and the other Aimco Entities considered a liquidation of CPF XIX in which CPF XIX’s properties would be marketed and sold to third parties for cash, with any net proceeds remaining after the payment of all liabilities distributed to CPF XIX’s limited partners. The primary advantage of such transactions would be that the sale prices would reflect arm’s-length negotiations and might therefore be higher than the appraised values which have been used to determine the merger consideration. Fox Partners II and the other Aimco Entities elected not to pursue this alternative because of: (i) the risk that a third party purchaser might not be found that would offer a satisfactory price; (ii) the costs imposed on CPF XIX in connection with marketing and selling the properties; (iii) the fact that limited partners would recognize taxable gain on the sales without the option of deferring that gain; and (iv) the fact that in Fox Partners II’s judgment, the costs imposed on CPF XIX in connection with marketing and selling its properties, as well as the fact that in such a sale limited partners would recognize taxable gain on the sale without the option of deferring that gain, would likely make the sale of the properties and dissolution of CPF XIX less advantageous to the limited partners than a merger.

4

Table of Contents

Contribution of the Properties to Aimco OP. Fox Partners II and the other Aimco Entities considered a transaction in which CPF XIX’s properties would be contributed to Aimco OP in exchange for OP Units. The primary advantage of such a transaction would be that CPF XIX limited partners generally would not recognize taxable gain. Fox Partners II and the other Aimco Entities elected not to pursue this alternative because it would not offer limited partners an opportunity for immediate liquidity.

The Aimco Entities believe that the merger will have the following benefits and detriments to unaffiliated limited partners, CPF XIX and the Aimco Entities:

Benefits to Unaffiliated Limited Partners. The merger is expected to have the following principal benefits to unaffiliated limited partners:

Liquidity. Limited partners are given a choice of merger consideration, and may elect to receive either cash or OP Units in the merger, except in those jurisdictions where the law prohibits the offer of OP Units (or registration or qualification would be prohibitively costly). Limited partners who receive cash consideration will receive immediate liquidity with respect to their investment.

Option to Defer Taxable Gain. Limited partners who receive OP Units in the merger may defer recognition of taxable gain (except where the law of the state or other jurisdiction in which a limited partner resides would prohibit the issuance of OP Units in that state or other jurisdiction, or where registration or qualification would be prohibitively costly, and except to the extent described in “Material United States Federal Income Tax Considerations — United States Federal Income Tax Consequences Relating to the Merger” beginning on page 67).

Diversification. Limited partners who receive OP Units in the merger will have the opportunity to participate in Aimco OP, which has a more diversified property portfolio than CPF XIX.

Benefits to CPF XIX. The merger is expected to have the following principal benefits to CPF XIX:

Elimination of Costs Associated with SEC Reporting Requirements and Multiple Limited Partners. After the merger, the Aimco Entities will own all of the limited partner interests in CPF XIX, and CPF XIX will terminate registration and cease filing periodic reports with the SEC. As a result, CPF XIX will no longer incur costs associated with preparing audited annual financial statements, unaudited quarterly financial statements, tax returns and partner Schedule K-1s, periodic SEC reports and other expenses. The Aimco Entities estimate these expenses to be approximately $130,000 per year. The merger will eliminate a significant amount of these costs.

Benefits to the Aimco Entities. The merger is expected to have the following principal benefits to the Aimco Entities:

Increased Interest in CPF XIX. Upon completion of the merger, Aimco OP will be the sole limited partner of CPF XIX. As a result, the Aimco Entities will receive all of the benefit from any future appreciation in value of the properties after the merger, and any future income from the properties.

Detriments to Unaffiliated Limited Partners. The merger is expected to have the following principal detriments to unaffiliated limited partners:

Taxable Gain. Limited partners who receive cash consideration may recognize taxable gain in the merger and that gain could exceed the merger consideration. In addition, limited partners who receive OP Units in the merger could recognize taxable gain to the extent described in “Material United States Federal Income Tax Considerations – United States Federal Income Tax Consequences Relating to the Merger” beginning on page 67.

Risks Related to OP Units. Limited partners who receive OP Units in the merger will be subject to the risks related to an investment in OP Units, as described in greater detail under the heading “Risk Factors — Risks Related to an Investment in OP Units.”

Conflicts of Interest; No Separate Representation of Unaffiliated Limited Partners. CPF XIX’s general partner, Fox Partners II, is a general partnership, the managing general partner of which is wholly-owned and

5

Table of Contents

controlled by Aimco. Therefore, Fox Partners II has a conflict of interest with respect to the merger. Fox Partners II has fiduciary duties to its general partners and Aimco, as the beneficial owner of its managing general partner, on the one hand, and to the limited partners of CPF XIX, on the other hand. The duties of Fox Partners II to the limited partners of CPF XIX conflict with the duties of Fox Partners II to its general partners, which could result in Fox Partners II approving a transaction that is more favorable to Aimco than might be the case absent such conflict of interest. As the general partner of CPF XIX, Fox Partners II seeks the best possible terms for CPF XIX’s limited partners. This conflicts with Aimco’s interest in obtaining the best possible terms for Aimco OP. In negotiating the merger agreement, no one separately represented the interests of the unaffiliated limited partners. If an independent advisor had been engaged, it is possible that such advisor could have negotiated better terms for CPF XIX’s unaffiliated limited partners.

Decreased Interest in CPF XIX. Upon completion of the merger, unaffiliated limited partners will no longer hold an interest in CPF XIX and Aimco OP will be the sole limited partner of CPF XIX. As a result, unaffiliated limited partners will no longer benefit from any future appreciation in the value of the property after the merger, and any future income from such property.

Detriments to CPF XIX. The merger is not expected to have any detriments to CPF XIX.

Detriments to the Aimco Entities. The merger is expected to have the following principal detriments to the Aimco Entities:

Increased Interest in CPF XIX. Upon completion of the merger, the Aimco Entities’ limited partner interest in the net book value of CPF XIX will increase from 68.04% to 100%, or from a deficit of $5.32 million to a deficit of $7.82 million as of December 31, 2012, and their limited partner interest in the losses from continuing operations of CPF XIX will increase from 68.04% to 100%, or from $1.94 million to $2.85 million for the period ended December 31, 2012.

Upon completion of the merger, Aimco OP will be the sole limited partner of CPF XIX. As a result, Aimco OP will bear the burden of all future operating or other losses, as well as any decline in the value of CPF XIX’s properties.

Burden of Capital Expenditures. Upon completion of the merger, the Aimco Entities will have sole responsibility for providing any funds necessary to pay for capital expenditures at the properties.

Material United States Federal Income Tax Consequences of the Merger

For a discussion of the material United States federal income tax consequences of the merger, see “Material United States Federal Income Tax Considerations — United States Federal Income Tax Consequences Relating to the Merger,” beginning on page 67.

Factors in Favor of Fairness Determination. The Aimco Entities (including Fox Partners II as general partner of CPF XIX) believe that the merger is advisable, fair to and in the best interests of CPF XIX and its unaffiliated limited partners. In support of such determination, the Aimco Entities considered the following factors:

| • | The merger consideration of $364.65 per Limited Partnership Unit was based on separate, independent third party appraisals of each of CPF XIX’s two properties by both CRA and KTR, independent valuation firms. The merger consideration was calculated on the basis of the higher of the two appraisals for each of the properties. |

| • | In the case of both the Peak Property and the Lakeside Property, the appraisals upon which the merger consideration was based exceeded the appraised values obtained in connection with the refinancings of mortgages on those properties carried out in 2009 and 2011. |

| • | The merger consideration is greater than the Aimco Entities’ estimate of liquidation value because there was no deduction for certain amounts that would be payable upon an immediate sale of the underlying properties, such as sales commissions or prepayment penalties that would apply (based on current interest |

6

Table of Contents

| rates) if the Peak Property or the Lakeside Property were sold after the expiration of the current lockout period (during which a prepayment of the mortgage debt is prohibited) in June 2013. |

| • | The merger consideration is equal to the Aimco Entities’ estimate of going concern value, calculated as the aggregate appraised value of CPF XIX’s properties, plus the amount of its other assets, less the amount of CPF XIX’s liabilities, including the market value of mortgage debt (but without deducting any prepayment penalties thereon). |

| • | The mark-to-market adjustment to the mortgage debt encumbering the properties is less than the prepayment penalties that would be payable (based on current interest rates) upon a sale of the Peak Property and the Lakeside Property after the expiration of the current lockout period. |

| • | The merger consideration exceeds the net book value per unit (a deficit of $87.65 per Limited Partnership Unit at December 31, 2012). |

| • | Limited partners may defer recognition of taxable gain by electing to receive OP Units in the merger, except in those jurisdictions where the law prohibits the offer of OP Units (or registration or qualification would be prohibitively costly, and except to the extent described in “Material United States Federal Income Tax Considerations – United States Federal Income Tax Consequences Relating to the Merger” beginning on page 67). |

| • | The number of OP Units issuable to limited partners in the merger will be determined based on the average closing price of Aimco common stock, as reported on the NYSE, over the ten consecutive trading days ending on the second trading day immediately prior to the consummation of the merger. |

| • | Limited partners who receive cash consideration will achieve immediate liquidity with respect to their investment. |

| • | Limited partners who receive OP Units in the merger will have the opportunity to participate in Aimco OP, which has a more diversified property portfolio than CPF XIX. |

| • | Although limited partners are not entitled to dissenters’ appraisal rights under Delaware law, the merger agreement provides them with contractual dissenters’ appraisal rights that are similar to the dissenters’ appraisal rights that are available to stockholders in a corporate merger under Delaware law. |

| • | Although the merger agreement may be terminated by either side at any time, Aimco OP and the Aimco Subsidiary are very likely to complete the merger on a timely basis. |

| • | Unlike a typical property sale agreement, the merger agreement contains no indemnification provisions, so there is no risk of subsequent reduction of the proceeds. |

| • | In contrast to a sale of the properties to a third party, which would involve marketing and other transaction costs, Aimco OP has agreed to pay all expenses associated with the merger. |

| • | The merger consideration is greater than the prices at which Limited Partnership Units have recently sold in the secondary market ($20.00 to $226.78 per Limited Partnership Unit from January 1, 2012 through March 31, 2013). |

| • | The merger consideration is greater than the prices at which Limited Partnership Units have historically sold in the secondary market ($25.00 to $241.10 per Limited Partnership Unit from January 1, 2010 through December 31, 2011). |

Factors Not in Favor of Fairness Determination. In addition to the foregoing factors, the Aimco Entities also considered the following countervailing factors:

| • | Fox Partners II, the general partner of CPF XIX, has substantial conflicts of interest with respect to the merger as a result of (i) the fiduciary duties it owes to unaffiliated limited partners, who have an interest in receiving the highest possible consideration, and (ii) the fiduciary duties it owes to its general partners, one of which is an indirect subsidiary of Aimco, which has an interest in obtaining the CPF XIX properties for the lowest possible consideration. |

7

Table of Contents

| • | The terms of the merger were not approved by any independent directors. |

| • | An unaffiliated representative was not retained to act solely on behalf of the unaffiliated limited partners for purposes of negotiating the merger agreement on an independent, arm’s-length basis, which might have resulted in better terms for the unaffiliated limited partners. |

| • | The merger agreement does not require the approval of any unaffiliated limited partners. |

| • | In calculating the merger consideration, the market value of the mortgage debt encumbering CPF XIX’s properties was deducted, which resulted in less merger consideration than would have been the case if the aggregate amount outstanding was deducted. |

| • | Limited partners who receive cash consideration in the merger may recognize taxable gain and that gain could exceed the merger consideration. |

| • | Limited partners who receive OP Units in the merger could recognize taxable gain to the extent described in “Material United States Federal Income Tax Considerations — United States Federal Income Tax Consequences Relating to the Merger” beginning on page 67. |

| • | Limited partners who receive OP Units in the merger will be subject to the risks related to an investment in OP Units, as described in greater detail under the heading “Risk Factors — Risks Related to an Investment in OP Units.” |

| • | CRA and KTR, the valuation firm that appraised the properties, have performed work for Aimco OP and its affiliates in the past and this pre-existing relationship could negatively impact the independence of CRA and KTR. |

| • | The Aimco Entities have not engaged an independent financial advisor to prepare a fairness opinion with respect to the merger consideration. This decision was taken in light of the costs associated with such an engagement and the decision to calculate the merger consideration using the higher of the two appraisal values received from CRA and KTR for each of the CPF XIX properties. |

The Aimco Entities did not assign relative weights to the above factors in reaching their decision that the merger is fair to CPF XIX and its unaffiliated limited partners. However, in determining that the benefits of the merger outweigh the costs and risks, they relied primarily on the following factors: (i) the merger consideration of $364.65 per Limited Partnership Unit is based on the higher of the two independent third party appraisals of each of CPF XIX’s properties, (ii) limited partners may defer recognition of taxable gain by electing to receive OP Units in the merger, except in certain jurisdictions where the law prohibits the offer of OP Units (or registration or qualification would be prohibitively costly, and except to the extent described in “Material United States Federal Income Tax Considerations – United States Federal Income Tax Consequences Relating to the Merger” beginning on page 67) and (iii) limited partners are entitled to contractual dissenters’ appraisal rights. The Aimco Entities were aware of, but did not place much emphasis on, information regarding prices at which CPF XIX units may have sold in the secondary market because they do not view that information as a reliable measure of value. The Limited Partnership Units are not traded on an exchange or other reporting system, and transactions in the secondary market are very limited and sporadic. In addition, some of the historical prices are not comparable to current value because of intervening events, including advances from affiliates of Fox Partners II and the sale of two properties owned by CPF XIX during 2012.

Procedural Fairness. The Aimco Entities determined that the merger is fair from a procedural standpoint despite the absence of any customary procedural safeguards, such as the engagement of an unaffiliated representative, the approval of independent directors or approval by a majority of unaffiliated limited partners. In making this determination, the Aimco Entities relied primarily on the dissenters’ appraisal rights provided to unaffiliated limited partners under the merger agreement that are similar to the dissenters’ appraisal rights available to stockholders in a corporate merger under Delaware law.

Selection and Qualifications of Independent Appraiser. The general partner of CPF XIX retained the services of both CRA and KTR to appraise the market value of each of CPF XIX’s properties. CRA and KTR are

8

Table of Contents

each experienced independent valuation consulting firms that have performed appraisal services for Aimco OP and its affiliates in the past. Aimco OP believes that its relationship with CRA and KTR had no negative impact on its independence in conducting the appraisals related to the merger.

Factors Considered. Each of CRA and KTR performed complete appraisals of the Lakeside Property and the Peak Property. CRA and KTR have each represented that its reports were prepared in conformity with the Uniform Standards of Professional Appraisal Practice, as promulgated by the Appraisal Standards Board of the Appraisal Foundation and the Code of Professional Ethics and Standards of Professional Appraisal Practice of the Appraisal Institute. CPF XIX furnished CRA and KTR with all of the necessary information requested by them in connection with the appraisals. The appraisals were not prepared in conjunction with a request for a specific value or a value within a given range or predicated upon loan approval. In preparing its valuation of each property, CRA and KTR, among other things:

| • | Inspected the property and its environs; |

| • | Reviewed demographic and other socioeconomic trends pertaining to the city and region where the property is located; |

| • | Examined regional apartment market conditions, with special emphasis on the property’s apartment submarket; |

| • | Investigated lease and sale transactions involving comparable properties in the influencing market; |

| • | Reviewed the existing rent roll and discussed the leasing status with the building manager and leasing agent. In addition, CRA and KTR reviewed the property’s recent operating history and those of competing properties; |

| • | Utilized appropriate appraisal methodology to derive estimates of value; and |

| • | Reconciled the estimates of value into a single value conclusion. |

Summary of Approaches and Methodologies Employed. The following summary describes the approaches and analyses employed by CRA and KTR in preparing the appraisals. CRA and KTR each principally relied on two approaches to valuation: (i) the income capitalization approach and (ii) the sales comparison approach.

The income capitalization approach is based on the premise that value is derived by converting anticipated benefits into property value. Anticipated benefits include the present value of the net income and the present value of the net proceeds resulting from the re-sale of the property. CRA and KTR reported that the Lakeside Property and the Peak Property each have an adequate operations history to determine its income-producing capabilities over the near future. In addition, performance levels of competitive properties served as an adequate check as to the reasonableness of each property’s actual performance. As such, the income capitalization approach was utilized in the appraisal of each property.

As part of the income capitalization approach, CRA and KTR used the direct capitalization method to estimate a value for the Lakeside Property and the Peak Property. According to CRA’s and KTR’s reports, the basic steps in the direct capitalization analysis are as follows: (i) calculate potential gross income from all sources that a competent owner could legally generate; (ii) estimate and deduct an appropriate vacancy and collection loss factor to arrive at effective gross income; (iii) estimate and deduct operating expenses that would be expected during a stabilized year to arrive at a probable net operating income; (iv) develop an appropriate overall capitalization rate to apply to the net operating income; and (v) estimate value by dividing the net operating income by the overall capitalization rate. In addition, any adjustments to account for differences between the current conditions and stabilized conditions are also considered. The assumptions utilized by CRA and KTR with respect to each property are set forth below. The property-specific assumptions were determined by CRA and KTR to be reasonable based on its review of historical operating and financial data for each property and comparison of said data to the operating statistics of similar properties in the influencing market areas. The capitalization rate for each property was determined to be reasonable by CRA and KTR based on their review of applicable data ascertained within the market in which each property is located.

The sales comparison approach is an estimate of value based upon a process of comparing recent sales of similar properties in the surrounding or competing areas to the subject property. This comparative process

9

Table of Contents

involves judgment as to the similarity of the subject property and the comparable sales with respect to many value factors such as location, contract rent levels, quality of construction, reputation and prestige, age and condition, and the interest transferred, among others. The value estimated through this approach represents the probable price at which the subject property would be sold by a willing seller to a willing and knowledgeable buyer as of the date of value. The reliability of this technique is dependent upon the availability of comparable sales data, the verification of the sales data, the degree of comparability and extent of adjustment necessary for differences, and the absence of atypical conditions affecting the individual sales prices. CRA and KTR each reported that its research revealed adequate sales activity to form a reasonable estimation of each of the subject property’s market value pursuant to the sales comparison approach.

For each of its appraisals, CRA and KTR conducted research in each market in an attempt to locate sales of properties similar to each of the appraised properties. In each of the appraisals, numerous sales were uncovered and the specific sales included in the appraisal reports were deemed representative of the most comparable data available at the time the appraisals were prepared. Important criteria utilized in selecting the most comparable data included: conditions under which the sale occurred (i.e. seller and buyer were typically motivated); date of sale — every attempt was made to utilize recent sales transactions; sales were selected based on their physical similarity to the appraised property; transactions were selected based on the similarity of location between the comparable and appraised property; and, similarity of economic characteristics between the comparable and appraised property. Sales data that may have been uncovered during the course of research that was not included in the appraisal did not meet the described criteria and/or could not be adequately confirmed.

According to CRA’s and KTR’s reports, the basic steps in processing the sales comparison approach are outlined as follows: (i) research the market for recent sales transactions, listings, and offers to purchase or sell of properties similar to the subject property; (ii) select a relevant unit of comparison and develop a comparative analysis; (iii) compare comparable sale properties with the subject property using the elements of comparison and adjust the price of each comparable to the subject property; and (iv) reconcile the various value indications produced by the analysis of the comparables.

The final step in the appraisal process is the reconciliation of the value indicators into a single value estimate. CRA and KTR reviewed each approach in order to determine its appropriateness relative to each property. The accuracy of the data available and the quantity of evidence were weighted in each approach. For each of the appraisals, CRA and KTR placed primary emphasis on the income capitalization approach to valuation and the direct capitalization method was utilized in the conclusion of value under this approach. For each property, CRA and KTR relied secondarily on the sales comparison approach, and reported that the value conclusion derived pursuant to the sales comparison approach is utilized as a means to support the value conclusion rendered for the properties pursuant to the income capitalization approach.

Summary of Independent Appraisals of the Properties. CRA and KTR performed complete appraisals of the Lakeside Property and the Peak Property. The appraisal report by CRA of the Lakeside Property was dated October 31, 2012 and indicates that the estimated market value of the Lakeside Property was $31.4 million as of October 24, 2012. The appraisal report was updated by CRA as reflected in CRA’s supplemental letter dated January 23, 2013. The appraisal report, as updated by the supplemental letter, provides an estimated market value of the Lakeside Property of $32.0 million as of January 18, 2013. The increase in the estimated market value of the Lakeside Property is mainly due to changes in the assumptions employed by CRA to determine the value of the Lakeside Property under the income capitalization approach (including lower loss to lease and higher other income from apartment unit rentals) as a result of receiving updated financial information, and the fact that CRA placed the greatest reliance upon the income capitalization approach to valuation. The appraisal report by KTR of the Lakeside Property was dated January 28, 2013 and indicates that the estimated market value of the Lakeside Property was $31.0 million as of January 18, 2013. The appraisal report by CRA of the Peak Property was dated October 31, 2012 and indicates that the estimated market value of the Peak Property was $34.6 million as of October 24, 2012. The appraisal report was updated by CRA as reflected in CRA’s supplemental letter dated January 23, 2013. The appraisal report, as updated by the supplemental letter, provides an estimated market value of the Peak Property of $35.0 million as of January 18, 2013. The increase in the estimated market value of the Peak Property is mainly due to changes in the assumptions employed by CRA to determine the value of the Peak Property under the income capitalization approach (including lower loss to lease and lower total expenses from

10

Table of Contents

apartment unit rentals) as a result of receiving updated financial information, and the fact that CRA placed the greatest reliance upon the income capitalization approach to valuation. The appraisal report by KTR of the Peak Property was dated January 28, 2013 and indicates that the estimated market value of the Peak Property was $34.6 million as of January 18, 2013. The summaries set forth below describe the material conclusions reached by CRA and KTR based on the values determined under the valuation was approaches and subject to the assumptions and limitations described below.

The Lakeside Property — The CRA Appraisal. The following is a summary of the appraisal report by CRA of the Lakeside Property dated October 31, 2012, as updated by the supplemental letter dated January 23, 2013:

Valuation Under Income Capitalization Approach. Using the income capitalization approach, CRA performed a direct capitalization analysis to derive a value for the Lakeside Property. The direct capitalization analysis resulted in a valuation conclusion for the Lakeside Property of approximately $31.4 million as of October 24, 2012 and $32.0 million as of January 18, 2013.

The assumptions employed by CRA to determine the value of the Lakeside Property as of January 18, 2013 under the income capitalization approach using a direct capitalization analysis included:

| • | potential gross income from apartment unit rentals of $237,010 per month or $2,844,120 for the appraised year; |

| • | a loss to lease allowance of 3.0% of the gross rent potential; |

| • | rent concessions of 0.5% of the gross rent potential; |

| • | a combined vacancy and credit loss allowance of 4.0%; |

| • | estimated utility recovery of $86,900, or $395 per unit; |

| • | other income of $875 per unit; |

| • | estimated total expenses (including reserves) of $1,068,431; and |

| • | capitalization rate of 5.75%. |

Using a direct capitalization analysis, CRA calculated the value of the Lakeside Property by dividing the stabilized net operating income (including an allowance for reserves) by the concluded capitalization rate of 5.75%. CRA calculated the value conclusion of the Lakeside Property under the income capitalization approach of approximately $31.4 million as of October 24, 2012 and $32.0 million as of January 18, 2013.

Valuation Under Sales Comparison Approach. CRA estimated the property value of Lakeside Property under the sales comparison approach by analyzing sales from the influencing market that were most similar to the Lakeside Property in terms of age, size, tenant profile and location. CRA reported that adequate sales existed to formulate a defensible value for Lakeside Property under the sales comparison approach.

The sales comparison approach resulted in a valuation conclusion for the Lakeside Property of approximately $29.7 million as of October 24, 2012 and $29.7 million as of January 18, 2013.

In reaching a valuation conclusion for the Lakeside Property, CRA examined and analyzed comparable sales of five properties in the influencing market. The sales reflected per unit unadjusted sales prices ranging from $106,140 to $136,290. After adjustment, the comparable sales illustrated a range from $117,921 to $136,290 per unit with mean and median adjusted sale prices of $130,045 and $133,221 per unit, respectively. CRA estimated a value of $135,000 per unit. Applied to the Lakeside Property’s 220 units, this resulted in CRA’s total value estimate for the Lakeside Property of approximately $29.7 million as of January 18, 2013.

Reconciliation of Values and Conclusion of Appraisal. For the appraisal of the Lakeside Property, CRA relied principally on the income capitalization approach to valuation. CRA relied secondarily on the sales comparison approach, and reported that the value conclusion derived pursuant to the sales comparison approach was supportive of the conclusion derived pursuant to the income capitalization approach. The income capitalization approach using a direct capitalization method resulted in a value of $32.0 million, and the sales comparison approach resulted in a value of $29.7 million. CRA concluded that the market value of the Lakeside Property as of January 18, 2013 was $32.0 million.

11

Table of Contents

Extraordinary Assumption. In connection with the preparation of its October 31, 2012 appraisal report of the Lakeside Property, CRA inspected the property on October 24, 2012. CRA noted that the scope of work of the January 23, 2013 appraisal report of the Lakeside Property did not include a physical inspection of the Lakeside Property, and that the value in the report is based on the extraordinary assumption that the physical condition of the Lakeside Property has not materially changed since October 24, 2012.

The Lakeside Property — The KTR Appraisal. The following is a summary of the appraisal report by KTR of the Lakeside Property dated January 28, 2013:

Valuation Under Income Capitalization Approach. Using the income capitalization approach, KTR performed a direct capitalization analysis to derive a value for the Lakeside Property. The direct capitalization analysis resulted in a valuation conclusion for the Lakeside Property of approximately $31.5 million as of January 18, 2013.

The assumptions employed by KTR to determine the value of the Lakeside Property as of January 18, 2013 under the income capitalization approach using a direct capitalization analysis included:

| • | potential gross income from apartment unit rentals of $233,690 per month or $2,804,280 for the appraised year; |

| • | a loss to lease allowance of 2.0% of the gross rent potential; |

| • | no concessions allowance of the gross rent potential; |

| • | a combined vacancy and credit loss allowance of 5.0%; |

| • | other income of $1,349 per unit; |

| • | estimated total expenses (including reserves) of $1,096,022; and |

| • | capitalization rate of 5.75%. |

Using a direct capitalization analysis, KTR calculated the value of the Lakeside Property by dividing the stabilized net operating income (including an allowance for reserves) by the concluded capitalization rate of 5.75%. KTR calculated the value conclusion of the Lakeside Property under the income capitalization approach of approximately $31.5 million as of January 18, 2013.

Valuation Under Sales Comparison Approach. KTR estimated the property value of Lakeside Property under the sales comparison approach by analyzing sales from the influencing market that were most similar to the Lakeside Property in terms of age, size, tenant profile and location. KTR reported that adequate sales existed to formulate a defensible value for Lakeside Property under the sales comparison approach.

The sales comparison approach resulted in a valuation conclusion for the Lakeside Property of approximately $28.6 million as of January 18, 2013.

In reaching a valuation conclusion for the Lakeside Property, KTR examined and analyzed comparable sales of four properties in the influencing market. The sales reflected per unit unadjusted sales prices ranging from $87,237 to $136,290. After adjustment, the comparable sales illustrated a range from $100,323 to $136,290 per unit. KTR estimated a value of $130,000 per unit. Applied to the Lakeside Property’s 220 units, this resulted in KTR’s total value estimate for the Lakeside Property of approximately $28.6 million as of January 18, 2013.

Reconciliation of Values and Conclusion of Appraisal. For the appraisal of the Lakeside Property, KTR relied principally on the income capitalization approach to valuation. KTR relied secondarily on the sales comparison approach, and reported that the value conclusion derived pursuant to the sales comparison approach was supportive of the conclusion derived pursuant to the income capitalization approach. The income capitalization approach using a direct capitalization method resulted in a value of $31.5 million, and the sales comparison approach resulted in a value of $28.6 million. KTR concluded that the market value of the Lakeside Property as of January 18, 2013 was $31.0 million.

12

Table of Contents

The Peak Property — The CRA Appraisal. The following is a summary of the appraisal report by CRA of the Peak Property dated October 31, 2012 as updated by the supplemental letter dated January 23, 2013:

Valuation Under Income Capitalization Approach. Using the income capitalization approach, CRA performed the direct capitalization method to estimate a value for the Peak Property. The direct capitalization method resulted in a valuation conclusion for the Peak Property of approximately $34.6 million as of October 24, 2012 and $35.0 million as of January 18, 2013.

The assumptions employed by CRA to determine the value of the Peak Property as of January 18, 2013 under the income capitalization approach using the direct capitalization method included:

| • | potential gross income from apartment unit rentals of $272,920 per month or $3,275,040 for the appraised year; |

| • | a loss to lease allowance of 1.5% of gross rent potential; |

| • | concession allowance of 0.5% of the gross rent potential; |

| • | a combined vacancy and collection loss allowance of 4.0%; |

| • | estimated utility income of $112,000, or $400 per unit; |

| • | estimated other income of $800 per unit; |

| • | estimated total expenses (including reserves) of $1,402,876; and |

| • | capitalization rate of 5.75%. |

Using the direct capitalization method, CRA calculated the value of the Peak Property by dividing the stabilized net operating income by the concluded overall capitalization rate of 5.75%. CRA calculated the value conclusion of the Peak Property under the income capitalization approach of approximately $34.6 million as of October 24, 2012 and $35.0 million as of January 18, 2013.

Valuation Under Sales Comparison Approach. CRA estimated the property value of the Peak Property under the sales comparison approach by analyzing sales from the influencing market that were most similar to the Peak Property in terms of age, size, tenant profile and location. CRA reported that the local market has been active in terms of investment sales of similar properties, and that adequate sales existed to formulate a defensible value for the Peak Property under the sales comparison approach.

The sales comparison approach resulted in a valuation conclusion for the Peak Property of approximately $35.0 million as of October 24, 2012 and 35.0 million as of January 18, 2013.

In reaching a valuation conclusion for the Peak Property, CRA examined and analyzed comparable sales of five properties in the influencing market. The sales reflected unadjusted sales prices ranging from $106,140 to $136,290 per unit. After adjustment, the comparable sales illustrated a value range of $112,561 to $129,476 per unit, with mean and median adjusted sale prices of $121,704 and $123,010 per unit, respectively. CRA estimated a value of $125,000 per unit. Applied to the Peak Property’s 280 units, this resulted in CRA’s total value estimate for the Peak Property of approximately $35.0 million.

Reconciliation of Values and Conclusion of Appraisal. For the appraisal of the Peak Property, CRA gave the greatest consideration to the income capitalization approach in the final conclusion of market value. CRA relied secondarily on the sales comparison approach, and reported that the value conclusion derived pursuant to the sales comparison approach is supportive of the conclusion derived pursuant to the income capitalization approach. The income capitalization approach using a direct capitalization analysis resulted in a value of $35.0 million, and the sales comparison approach resulted in a value of $35.0 million. CRA concluded that the market value of the Peak Property as of January 18, 2013 was $35.0 million.

Extraordinary Assumption. In connection with the preparation of its October 31, 2012 appraisal report of the Peak Property, CRA inspected the property on October 24, 2012. CRA noted that the scope of work of the January 23, 2013 appraisal report of the Peak Property did not include a physical inspection of the Peak Property, and that the value in the report is based on the extraordinary assumption that the physical condition of the Peak Property has not materially changed since October 24, 2012.

13

Table of Contents

The Peak Property — The KTR Appraisal. The following is a summary of the appraisal report by KTR of the Peak Property dated January 28, 2013:

Valuation Under Income Capitalization Approach. Using the income capitalization approach, KTR performed the direct capitalization method to estimate a value for the Peak Property. The direct capitalization method resulted in a valuation conclusion for the Peak Property of approximately $34.6 million as of January 18, 2013.

The assumptions employed by KTR to determine the value of the Peak Property as of January 18, 2013 under the income capitalization approach using the direct capitalization method included:

| • | potential gross income from apartment unit rentals of $280,460 per month or $3,365,520 for the appraised year; |

| • | a loss to lease allowance of 2.0% of gross rent potential; |

| • | no concession allowance of the gross rent potential; |

| • | a combined vacancy and collection loss allowance of 5.0%; |

| • | estimated other income of $1,180 per unit; |

| • | estimated total expenses (including reserves) of $1,468,195; and |

| • | capitalization rate of 5.75%. |

Using the direct capitalization method, KTR calculated the value of the Peak Property by dividing the stabilized net operating income by the concluded overall capitalization rate of 5.75%. KTR calculated the value conclusion of the Peak Property under the income capitalization approach of approximately $34.6 million as of January 18, 2013.

Valuation Under Sales Comparison Approach. KTR estimated the property value of the Peak Property under the sales comparison approach by analyzing sales from the influencing market that were most similar to the Peak Property in terms of age, size, tenant profile and location. KTR reported that the local market has been active in terms of investment sales of similar properties, and that adequate sales existed to formulate a defensible value for the Peak Property under the sales comparison approach.

The sales comparison approach resulted in a valuation conclusion for the Peak Property of approximately $35.0 million as of January 18, 2013.

In reaching a valuation conclusion for the Peak Property, KTR examined and analyzed comparable sales of four properties in the influencing market. The sales reflected unadjusted sales prices ranging from $87,237 to $136,290 per unit. After adjustment, the comparable sales illustrated a value range of $91,599 to $129,476 per unit. KTR estimated a value of $125,000 per unit. Applied to the Peak Property’s 280 units, this resulted in KTR’s total value estimate for the Peak Property of approximately $35.0 million.

Reconciliation of Values and Conclusion of Appraisal. For the appraisal of the Peak Property, KTR gave the greatest consideration to the income capitalization approach in the final conclusion of market value. KTR relied secondarily on the sales comparison approach, and reported that the value conclusion derived pursuant to the sales comparison approach is supportive of the conclusion derived pursuant to the income capitalization approach. The income capitalization approach using a direct capitalization analysis resulted in a value of $34.6 million, and the sales comparison approach resulted in a value of $35.0 million. KTR concluded that the market value of the Peak Property as of January 18, 2013 was $34.6 million.

Assumptions, Limitations and Qualifications of CRA’s and KTR’s Valuations. In preparing each of the appraisals, CRA and KTR relied, without independent verification, on the information furnished by others. Each of CRA’s appraisal reports and KTR’s appraisal reports were subject to certain assumptions and limiting conditions including the following: no responsibility was assumed for the legal description or for matters including legal or title considerations, and title to each property was assumed to be good and marketable unless otherwise stated; each property was appraised free and clear of any or all liens or encumbrances unless otherwise

14

Table of Contents

stated; responsible ownership and competent property management were assumed; all engineering was assumed to be correct; there were no hidden or unapparent conditions of the property, subsoil, or structures that render it more or less valuable, and no responsibility was assumed for such conditions or for arranging for engineering studies that may be required to discover them; there was full compliance with all applicable federal, state, and local environmental regulations and laws unless noncompliance was stated, defined, and considered in the appraisal report; all applicable zoning and use regulations and restrictions have been complied with, unless nonconformity had been stated, defined, and considered in the appraisal report; all required licenses, certificates of occupancy, consents, or other legislative or administrative authority from any local, state, or national government or private entity or organization have been or can be obtained or renewed for any use on which the value estimate contained in each report was based; the utilization of the land and improvements is within the boundaries or property lines of the property described and that there is no encroachment or trespass unless noted in either report; the distribution, if any, of the total valuation in each report between land and improvements applies only under the respective stated program of utilization; unless otherwise stated in each report, the existence of hazardous substances, including without limitation, asbestos, polychlorinated biphenyls, petroleum leakage, or agricultural chemicals, which may or may not be present on each property, or other environmental conditions, were not called to the attention of nor did the appraiser become aware of such during the appraiser’s inspection, and the appraiser had no knowledge of the existence of such materials on or in the property unless otherwise stated; the appraiser has not made a specific compliance survey and analysis of this property to determine whether or not it is in conformity with the various detailed requirements of the Americans with Disabilities Act; and former personal property items such as kitchen and bathroom appliances were, at the time of each appraisal report, either permanently affixed to the real estate or were implicitly part of the real estate in that tenants expect the use of such items in exchange for rent and never gain any of the rights of ownership, and the intention of the owners is not to remove the articles which are required under the implied or express warranty of habitability.

Compensation of Appraiser. CRA’s fee for the appraisal of the Lakeside Property and the Peak Property was approximately $15,900. KTR’s fee for the appraisal of the Lakeside Property and the Peak Property was approximately $9,500. Aimco OP paid for the costs of the appraisals. Neither CRA’s fee nor KTR’s fee for the appraisals was contingent on the approval or completion of the merger. Aimco OP also has agreed to indemnify CRA and KTR for certain liabilities that may arise out of the rendering of the appraisals. In addition to the appraisals performed in connection with the merger, during the prior two years, CRA and KTR have been paid approximately $144,700 and $159,700, respectively, for appraisal services by Aimco OP and its affiliates, including, in the case of CRA, fees of approximately $13,000 for the appraisals of the Lakeside Property and Peak Property in 2011. Except as set forth above, during the prior two years, no material relationship has existed between CRA or KTR, on the one hand, and CPF XIX or Aimco OP or any of their affiliates, on the other hand. Aimco OP believes that its relationship with CRA and KTR had no negative impact on its independence in conducting the appraisals.

Availability of Appraisal Reports. You may obtain a full copy of CRA’s appraisals and KTR’s appraisals upon request, without charge, by contacting Eagle Rock Proxy Advisors, LLC, by mail at 12 Commerce Drive, Cranford, New Jersey 07016; by fax at (908) 497-2349; or by telephone at (800) 217-9608. In addition, the appraisal reports have been filed with the SEC. For more information about how to obtain a copy of the appraisal reports see “Where You Can Find Additional Information.”

15

Table of Contents

Conflicts of Interest. CPF XIX’s general partner, Fox Partners II, is a general partnership, the managing general partner of which is wholly-owned and controlled by Aimco. Therefore, Fox Partners II has a conflict of interest with respect to the merger. Fox Partners II has fiduciary duties to its general partners and Aimco, as the beneficial owner of its managing general partner, on the one hand, and to the limited partners of CPF XIX, on the other hand. The duties of Fox Partners II to the limited partners of CPF XIX conflict with the duties of Fox Partners II to its general partners, which could result in Fox Partners II approving a transaction that is more favorable to Aimco than might be the case absent such conflict of interest. As the general partner of CPF XIX, Fox Partners II seeks the best possible terms for CPF XIX’s limited partners. This conflicts with Aimco’s interest in obtaining the best possible terms for Aimco OP.

No independent representative was engaged to represent the unaffiliated limited partners in negotiating the terms of the merger. If an independent advisor had been engaged, it is possible that such advisor could have negotiated better terms for CPF XIX’s unaffiliated limited partners.

The terms of the merger have not been determined in arm’s-length negotiations. The terms of the merger, including the merger consideration, were determined through discussions between officers and directors of CPF XIX, on one hand, and officers of Aimco, on the other. All of the officers and directors of CPF XIX are also officers of Aimco. There are no independent directors of CPF XIX. If the terms of the merger had been determined through arm’s-length negotiations, the terms might be more favorable to CPF XIX and its limited partners.