UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

|

x |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES |

|

o |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES |

Commission File Number 001-33034

BMB MUNAI, INC.

(Exact name of registrant as specified in its charter)

|

Nevada |

|

30-0233726 |

|

(State or other jurisdiction of |

|

(I.R.S. Employer |

|

incorporation or organization) |

|

Identification No.) |

|

|

|

|

|

202 Dostyk Ave, 4th Floor |

|

|

|

Almaty, Kazakhstan |

|

050051 |

|

(Address of principal executive offices) |

|

(Zip Code) |

+7 (3272) 375-125

(Registrant’s telephone number, including area code)

Securities registered under Section 12(b) of the Exchange Act:

|

Title of Each Class |

|

Name of Exchange on Which Registered |

|

|

|

|

|

Common - $0.001 |

|

American Stock Exchange |

|

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the securities Act. | ||

|

|

x Yes o No |

|

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Exchange Act from their obligations under those Sections.

|

|

o Yes x No |

|

Indicate by check mark whether the registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

|

|

x Yes o No |

|

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

|

|

o |

|

|

Indicate by check mark whether the registrant is a large accelerated filed, an accelerated filer, or non-accelerated filer. |

|

|

Large accelerated Filer o |

Accelerated Filer x |

Non-accelerated Filer o |

|

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.) |

| |

|

|

o Yes x No | |

As of September 30, 2006 the aggregate market value of the common voting stock held by non-affiliates of the issuer based upon the closing stock price of $5.15 per share was approximately $193,199,345.

As of June 7, 2007, the registrant had 44,690,657 shares of common stock, par value $0.001, issued and outstanding.

DOCUMENTS INCORPORATED BY REFERENCE: None

Table of Contents

|

|

PART I |

|

|

|

|

Page |

|

Item 1. |

Business |

3 |

|

|

|

|

|

Item 1A. |

Risk Factors |

8 |

|

|

|

|

|

Item 1B. |

Unresolved Staff Comments |

14 |

|

|

|

|

|

Item 2. |

Properties |

15 |

|

|

|

|

|

Item 3. |

Legal Proceedings |

25 |

|

|

|

|

|

Item 4. |

Submission of Matters to a Vote of Security Holders |

26 |

|

|

|

|

|

|

PART II |

|

|

|

|

|

|

Item 5. |

Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

26 |

|

|

|

|

|

Item 6. |

Selected Financial Data |

30 |

|

|

|

|

|

Item 7. |

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

30 |

|

|

|

|

|

Item 7A. |

Quantitative and Qualitative Disclosures About Market Risk |

44 |

|

|

|

|

|

Item 8. |

Financial Statements and Supplementary Data |

45 |

|

|

|

|

|

Item 9.

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

45 |

|

|

|

|

|

Item 9A. |

Controls and Procedures |

46 |

|

|

|

|

|

Item 9B. |

Other Information |

50 |

|

|

|

|

|

|

PART III |

|

|

|

|

|

|

Item 10. |

Directors, Executive Officers and Corporate Governance |

50 |

|

|

|

|

|

Item 11. |

Executive Compensation |

55 |

|

|

|

|

|

Item 12. |

Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

63 |

|

|

|

|

|

Item 13. |

Certain Relationships and Related Transactions, and Director Independence |

65 |

|

|

|

|

|

Item 14. |

Principal Accounting Fees and Services |

66 |

|

|

|

|

|

Item 15. |

Exhibits, Financial Statement Schedules |

67 |

|

|

|

|

|

|

PART IV |

|

|

|

|

|

|

|

SIGNATURES |

68 |

3

BMB MUNAI, INC.

Unless otherwise indicated by the context, references herein to the “Company”, “BMB”, “we”, our” or “us” means BMB Munai, Inc, a Nevada corporation, and its corporate subsidiaries and predecessors.

Forward Looking Information

Certain of the statements contained in all parts of this document including, but not limited to, those relating to our drilling plans, future expenses, changes in wells operated and reserves, future growth and expansion, future exploration, future seismic data, expansion of operations, our ability to generate new prospects, our ability to obtain a production license, review of outside generated prospects and acquisitions, additional reserves and reserve increases, managing our asset base, expansion and improvement of capabilities, integration of new technology into operations, credit facilities, new prospects and drilling locations, future capital expenditures and working capital, sufficiency of future working capital, borrowings and capital resources and liquidity, projected cash flows from operations, future commodity price environment, expectations of timing, the outcome of legal proceedings, satisfaction of contingencies, the impact of any change in accounting policies on our financial statements, the number, timing or results of any wells, the plans for timing, interpretation and results of new or existing seismic surveys or seismic data, future production or reserves, future acquisitions of leases, lease options or other land rights, management’s assessment of internal control over financial reporting, financial results, opportunities, growth, business plans and strategy and other statements that are not historical facts contained in this report are forward-looking statements. When used in this document, words like “expect,” “project,” “estimate,” “believe,” “anticipate,” “intend,” “budget,” “plan,” “forecast,” “predict,” “may,” “should,” “could,” “will” and similar expressions are also intended to identify forward-looking statements. Such statements involve risks and uncertainties, including, but not limited to, market factors, market prices (including regional basis differentials) of natural gas and oil, results for future drilling and marketing activity, future production and costs and other factors detailed herein and in our other Securities and Exchange Commission filings. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual outcomes may vary materially from those indicated. These forward-looking statements speak only as of their dates and should not be unduly relied upon. We undertake no obligation to publicly update or revise any forward-looking statement, whether as a result of new information, future events or otherwise.

Throughout this annual report all references to dollar amounts ($) refers to U.S. dollars unless otherwise indicated.

PART I

Item 1. Business

Overview

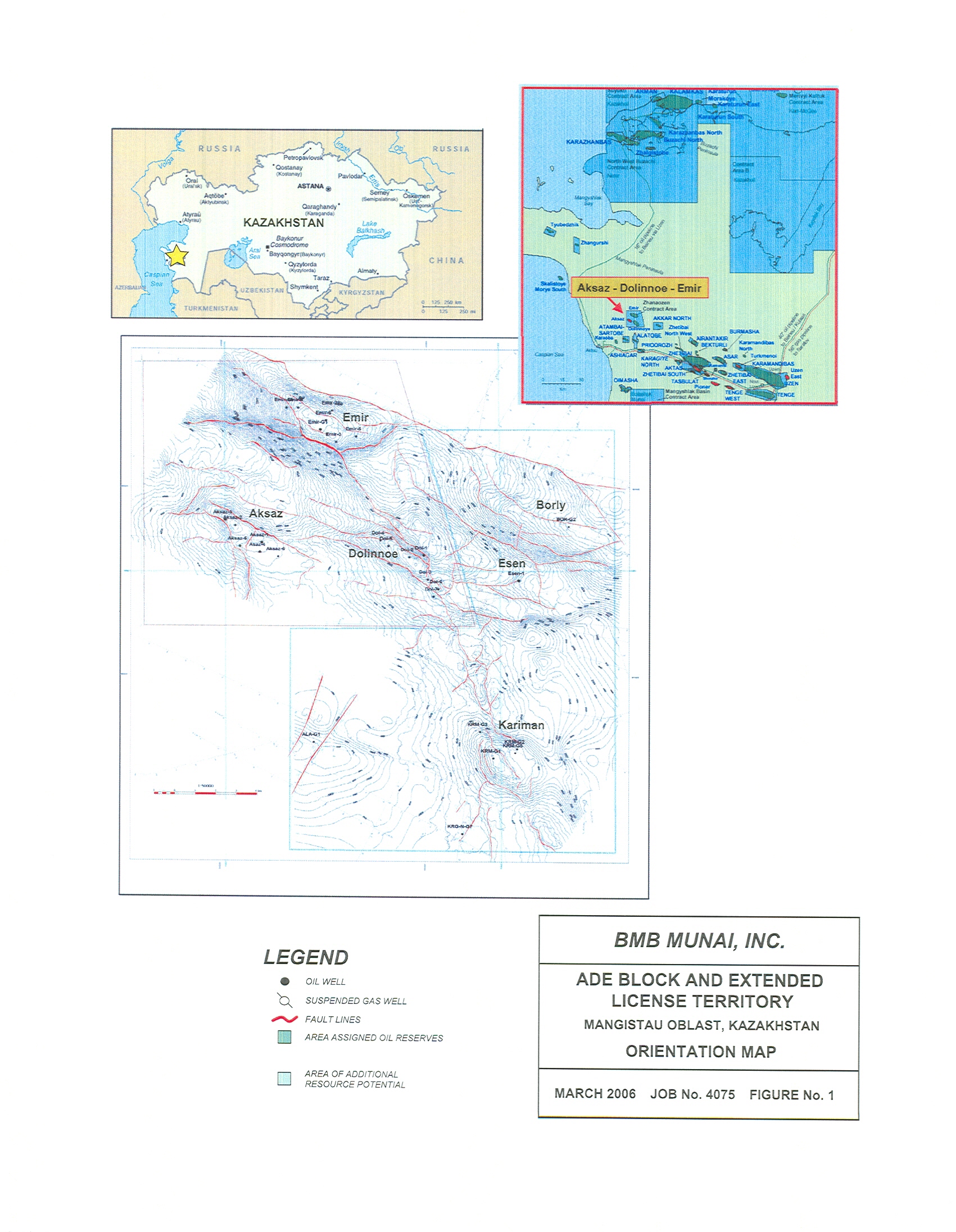

BMB Munai, Inc. is an independent oil and natural gas company engaged in the exploration, development, acquisition and production of crude oil and natural gas properties in the Republic of Kazakhstan (sometimes also referred to herein as the “ROK” or “Kazakhstan”). We hold a contract that allows us to explore and develop approximately 460 square kilometers in western Kazakhstan located onshore in the Mangistau Oblast, approximately 50 kilometers from the Kazakhstan city of Aktau, a seaport on the Caspian Sea.

4

We generate revenue, income and cash flow by producing and selling crude oil from production from our properties. We make significant capital expenditures in our exploration and development activities that we anticipate will allow us to increase and improve our ability to generate revenue. Our focus is toward enhancing cash flows and increasing proved developed reserves by drilling developmental wells within a proximity of existing wells, (which we believe decreases our likelihood of drilling a dry hole), while at the same time increasing our current production and cash flow. As cash flow justifies, we will drill exploratory wells to confirm potential reservoirs identified by the 3D seismic studies or extend known reservoirs. We believe this strategy will result in growth of proved developed reserves, production and financial strength.

To date, we have relied primarily on funds raised through the sale of our equity securities to fund operations. We currently use more cash in operations than we generate. Although presently the revenues derived from our properties are sufficient to meet our operating needs, exclusive of our drilling program, we will need additional financing to continue exploration activities on our properties.

Industry and Economic Factors

In managing our business, we must deal with many factors inherent in our industry. First and foremost is the fluctuation of oil and gas prices. Historically, oil and gas markets have been cyclical and volatile, with future price movements that are difficult to predict. While our revenues are a function of both production and prices, wide swings in commodity prices will likely have the greatest impact on our results of operations. We have no way of predicting those prices or of controlling them without losing an advantage from a potential upswing. The oil and gas industry has continued to experience high commodity prices in 2006 and 2007, which has positively impacted the entire industry as well as our Company.

Our operations entail significant complexities. Advanced technologies requiring highly trained personnel are utilized in both exploration and development. Even when the technology is properly used, we still may not know conclusively whether hydrocarbons will be present nor the rate at which they may be produced. Despite our best efforts to limit risk, exploration is a high-risk activity, often times resulting in no discovery of commercially productive reserves. Moreover, operating costs in our industry are substantial.

Our business, as with other extractive industries, is a depleting one in which each oil and gas equivalent produced must be replaced or our business, and a critical source of future liquidity, will shrink.

Strategy

Our goal is to increase stockholder value by investing in oil and natural gas projects with attractive rates of return on capital employed. We plan to achieve this goal by exploiting and developing our existing oil and gas properties and pursuing the acquisition of additional properties. We have and will continue to focus on the following:

Increasing our Production and Cash Flow. To sustain our operations we need capital. To date most of our operating capital has come from the sale of our securities. We believe that to increase shareholder value and economic stability, we must increase our revenues through increased production. For this reason, we have focused our efforts on drilling developmental

5

wells strategically located within proved areas with the intent to drill wells with a high probability of success. We believe this strategy will allow us to increase our current production and correspondingly our cash flows.

Developing and Exploiting Existing Properties. We believe that there is significant value to be created by drilling the identified undeveloped opportunities on our properties. We own interest in 720 gross (720 net) developed acres, plus 160 gross (160 net) acres of proved undeveloped reserves. We also own interest in approximately 49,150 gross (49,150 net) unproved, undeveloped acres. We plan to continue exploration, development, production and further infrastructure development during the 2008 fiscal year. We expect to fund our expenditures with future production revenues and a combination of commercial debt and the issuance of corporate debt and/or equity securities.

Pursuing Profitable Acquisitions. While our emphasis in fiscal 2008 is anticipated to focus on the further development of our existing properties, we will continue to look for properties with both existing cash flow from production and future development potential. We intend to pursue acquisitions of properties that we believe will provide attractive rates of return on capital invested. We have an experienced team of management professionals who we rely on to identify and evaluate acquisition opportunities.

Oil and Natural Gas Reserves

The following table sets forth our estimated net proved oil and natural gas reserves and the standardized measure of discounted future net cash flows related to such reserves as of March 31, 2007. We engaged Chapman Petroleum Engineering, Ltd. (“Chapman”), to estimate our net proved reserves, projected future production and the standardized measure of discounted future net cash flows as of March 31, 2007. Chapman’s estimates are based upon a review of production histories and other geologic, economic, ownership and engineering data provided by us. Chapman has independently evaluated our reserves for the past twelve months. In estimating the reserve quantities that are economically recoverable, Chapman used oil and natural gas prices in effect as of March 31, 2007 without giving effect to hedging activities. In accordance with requirements of the Securities and Exchange Commission (the “SEC”) regulations, no price or cost escalation or reduction was considered by Chapman. The standardized measure of discounted future net cash flows is not intended to represent the current market value of our estimated oil and natural gas reserves. The oil and natural gas reserve data included in or incorporated by reference in this document are only estimates and may prove to be inaccurate.

|

|

Proved Reserves | ||||

|

|

Developed(1) |

|

Undeveloped(2) |

|

Total |

|

Oil and condensate (MBbls)(3) |

11,854 |

|

3,426 |

|

15,280 |

|

Natural gas (MMcf) |

- |

|

- |

|

- |

|

Total BOE (MBbls) |

11,854 |

|

3,426 |

|

15,280 |

|

|

|

|

|

|

|

|

Standardize measure of discounted future net cash flows(4) (in thousands of US Dollars) |

|

|

|

|

$171,265 |

|

(1) |

Proved developed reserves are proved reserves that are expected to be recovered from existing wells with existing equipment and operating methods. |

|

(2) |

Proved undeveloped reserves are proved reserves which are expected to be recovered from new wells on undrilled acreage or from existing wells where a relatively major expenditure is required for recompletion. |

|

(3) |

Includes natural gas liquids. |

6

|

(4) |

The standardized measure of discounted future net cash flows represents the present value of future net cash flow net of all taxes. |

The reserve data set forth herein represents estimates only. Reserve engineering is a subjective process of estimating underground accumulations of oil and natural gas that cannot be measured in an exact manner. The accuracy of any reserve estimate is a function of the quality of available data and of engineering and geological interpretation and judgment. As a result, estimates made by different engineers often vary from one another. In addition, results of drilling, testing and production subsequent to the date of an estimate may justify revision of such estimates, and such revisions may be material. Accordingly, reserve estimates are generally different from the quantities of oil and natural gas that are ultimately recovered. Furthermore, the estimated future net revenue from proved reserves and the present value thereof are based upon certain assumptions, including current prices, production levels and costs that may not be what is actually incurred or realized.

No estimates of proved reserves comparable to those included herein have been included in reports to any federal agency other than the SEC.

In accordance with SEC regulations, the Chapman Report used oil and natural gas prices in effect at March 31, 2007. The prices used in calculating the standardized measure of discounted future net cash flows attributable to proved reserves do not necessarily reflect market prices for oil and natural gas production subsequent to March 31, 2007. There can be no assurance that all of the proved reserves will be produced and sold within the periods indicated, that the assumed prices will actually be realized for such production or that existing contracts will be honored or judicially enforced.

Sales to Major Customers

We are now exporting all of our test production for sale in the world market. Currently, all of our production is being sold to one client, Euro-Asian Oil AG. We anticipate that once we move to commercial production we will market our production to third parties consistent with industry practices.

Our crude oil is transported via the Aktau sea port to world markets. Sales prices at the port locations are based on the average quoted Brent crude oil price from Platt’s Crude Oil Marketwire for the three days following the bill of lading date less discount of $14.15 for transportation expenses, freight charges and other expenses borne by Euro-Asian Oil AG.

In the exploration, development and production business, production is normally sold to relatively few customers. Our customers are concentrated in the oil and gas industry, and revenue can be materially affected by current economic conditions and the price of certain commodities such as natural gas and crude oil the cost of which is passed through to the customer. However, based on the current demand for natural gas and crude oil and the fact that alternate purchasers are readily available, we believe that the loss of Euro-Asian Oil AG would not have a long–term material adverse effect on our operations.

Marketing

There are a variety of factors which affect the market for oil and natural gas, including the extent of domestic production and imports of oil and natural gas, the availability, proximity and capacity of natural gas pipelines and other transportation facilities, demand for oil and

7

natural gas, the marketing of competitive fuels and the effects of state and federal regulations on oil and natural gas productions and sales.

Competition

Hydrocarbons exploration is highly competitive. Competition in Kazakhstan and Central Asia includes other junior hydrocarbons exploration companies, mid-size producers and major exploration and production companies. We compete for additional exploration and production properties with these companies who in many cases may have greater financial resources and larger technical staff than we do.

We believe we have an advantage over our competitor: our executive management and our board of directors have domestic and international experience and have been working in Kazakhstan and Russia for up to 30 years. They have developed relationships with the Kazakhstan government, its departments and ministries at many levels. We also employ experienced national and foreign specialists at senior levels in our operating subsidiary, Emir Oil, LLP.

We face significant competition for capital from other exploration and production companies and industry sectors. At times, other industry sectors may be more in favor with investors, limiting our ability to obtain necessary capital.

Government Regulation

Our operations are subject to various levels of government controls and regulations at various levels in both the United States and in Kazakhstan. We attempt to comply with all legal requirements in the conduct of our operations and employ business practices that we consider to be prudent under the circumstances in which we operate. It is not possible for us to separately calculate the costs of compliance with environmental and other governmental regulations as such costs are an integral part of our operations.

In Kazakhstan, legislation affecting the oil and gas industry is under constant review for amendment or expansion. Pursuant to such legislation, various governmental departments and agencies have issued extensive rules and regulations which affect the oil and gas industry, some of which carry substantial penalties for failure to comply. These laws and regulations can have a significant impact on the industry by increasing the cost of doing business and, consequentially, can adversely affect our profitability. Inasmuch as new legislation affecting the industry is commonplace and existing laws and regulations are frequently amended or reinterpreted, we are unable to predict the future cost or impact of complying with such laws and regulations.

Employees

As of May 15, 2007 we had 261 full-time employees. We believe that our relationships with our employees are good. None of our employees are covered by a collective bargaining agreement. From time to time we utilize the services of independent consultants and contractors to perform various professional services. Field and on-site production operation services, such as pumping, maintenance, dispatching, inspection and testing are generally provided by independent contractors.

8

Executive Offices

Our principal executive and corporate offices are located in an office building located at 202 Dostyk Avenue, in Almaty, Kakzakhstan. We lease this space and believe it is sufficient to meet our needs for the foreseeable future.

We also maintain an administrative office in Salt Lake City, Utah. The address is 324 South 400 West, Suite 250, Salt Lake City, Utah 84101, USA.

Reports to Security holders

We file Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and other items with the Securities and Exchange Commission (SEC). We provide free access to all of these SEC filings, as soon as reasonably practicable after filing, on our Internet web site located at www.bmbmunai.com. In addition, the public may read and copy any documents we file with the SEC at the SEC’s Public Reference Room at 100 F Street N.E., Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains its Internet site www.sec.gov, which contains reports, proxy and information statements and other information regarding issuers like BMB Munai.

Item 1A. Risk Factors

A substantial or extended decline in oil prices may adversely affect our business, financial condition, cash flow, liquidity or results of operations, ourability to meet our capital expenditure obligations and financial commitments or to implement our business strategy.

Our business is heavily dependent upon the price of and demand for oil production and the level of such production will be subject to wide fluctuations and depend on numerous factors beyond our control, including the following:

|

|

• |

the domestic and foreign supply of oil; |

|

|

|

• |

the price and quantity of imports of crude oil; | |

• political conditions and events in other oil-producing countries, including embargoes, continued hostilities in the Middle East, Iran, Nigeria and other sustained military campaigns, and acts of terrorism or sabotage;

|

|

• |

the actions of the Organization of Petroleum Exporting Countries, or OPEC; | ||||||

|

|

• |

domestic government regulation, legislation and policies; |

| |||||

|

|

• |

the level of global oil inventories; |

| |||||

|

|

• |

weather conditions; |

| |||||

|

|

• |

technological advances affecting energy consumption; |

| |||||

|

|

• |

the price availability of alternative fuels; and |

| |||||

|

|

• |

overall economic conditions. |

| |||||

10

Any continued or extended decline in the price of crude oil or natural gas will adversely affect:

|

|

• |

our revenues, profitability and cash flow from operations; | |||

|

|

• |

the value of our proved oil reserves; |

| ||

|

|

• |

the economic viability of certain of our drilling prospects; | |||

|

|

• |

our borrowing capacity; and |

| ||

|

|

• |

our ability to obtain additional capital. |

| ||

In December 2005 we were granted our first export quota from the Ministry of Energy and Mineral Resources of the Republic of Kazakhstan (“MEMR”), which allowed us to begin exporting oil for sale in the world market in January 2006. We have applied for and been granted an export quota each month since, with the exception of February 2006, when we did not apply for a quota. Prior to January 2006, we were limited to selling our test production to the domestic market in Kazakhstan. The price of oil in the domestic market in Kazakhstan is materially lower than the price in the world market. There is no guarantee that the Republic of Kazakhstan will continue to grant us export quotas in the future. In the event we are not granted an export quota in the future, we will be limited to selling our production to the domestic Kazakhstan market, which likely will result in us realizing lower revenue per barrel of oil sold than we would realize in the world market.

We have not entered into crude oil hedging arrangements on any of our anticipated sales. However, we may in the future enter into such arrangements in order to reduce our exposure to price risks. Such arrangements may limit our ability to benefit from increases in oil prices.

Reserve estimates depend on many assumptions that may turn out to be inaccurate. Any material inaccuracies in these reserve estimates or underlying assumptions will materially affect the quantities and present value of our reserves.

The process of estimating oil and natural gas reserves is complex. It requires interpretations of available technical data and many assumptions, including assumptions relating to economic factors. Any significant inaccuracies in these interpretations or assumptions could materially affect the estimated quantities and present value of reserves shown in this report.

In order to prepare estimates, we must project production rates and timing of development expenditures. We must also analyze available geological, geophysical, production and engineering data. The extent, quality and reliability of this data can vary. The process also requires economic assumptions about matters such as oil and natural gas prices, drilling and operating expenses, capital expenditures, taxes and availability of funds. Therefore, estimates of oil and natural gas reserves are inherently imprecise.

Actual future production, oil and natural gas prices, revenues, taxes, development expenditures, operating expenses and quantities of recoverable oil and natural gas reserves most likely will vary from our estimates. Any significant variance could materially affect the estimated quantities and present value of reserves shown in this report. In addition, we may adjust estimates of proved reserves to reflect production history, results of exploration and development, prevailing oil and natural gas prices and other factors, many of which are beyond our control.

11

You should not assume that the present value of future net revenues from our proved reserves referred to in this report is the current market value of our estimated oil and natural gas reserves. In accordance with SEC requirements, we generally base the estimated discounted future net cash flows from our proved reserves on prices and costs on the date of the estimate. Actual future prices and costs may differ materially from those used in the present value estimate. If future values decline or costs increase, it could have a negative impact on our ability to finance operations; individual properties could cease being commercially viable; affecting our decision to continue operations on producing properties or to attempt to develop properties. All of these factors would have a negative impact on earnings and net income, and most likely the trading price of our securities.

Twenty two percent of our proven properties are undeveloped; therefore the risk associated with our success is greater than would be the case if all of our properties were categorized as “proved developed producing.”

Because a portion of our proved reserves (approximately 22%) are “Proved Undeveloped” additional capital for the drilling and completion of an additional well will be required before these reserves become productive. Further, because of the inherent uncertainties associated with drilling for oil and gas, this well may never be developed to the extent that it develops into positive cash flow. Even if we are successful in our development efforts, it could take several years to achieve positive cash flow from our proved undeveloped reserves.

We will be unable to produce up to 84% of our proved reserves if we are not able to extend our current contract or obtain a new contract from the Republic of Kazakhstan, which would likely require us to terminate our operations.

Under our current contract for exploration of hydrocarbons on our properties we have the right to produce oil and gas only until July 2009, yet 84% of our proved reserves are scheduled to be produced after July 2009. We have the exclusive right to negotiate a commercial production contract as per the terms of our exploration contract. The MEMR does not make public its determinations on the granting of commercial production rights. Based on discussions with the MEMR, we have learned that the primary factors used by the MEMR in determining whether to grant commercial production rights were whether the contract holder’s fulfillment of minimum work program commitments, proof of commercial discovery and submission of an approved development plan by a third-party petroleum institute in Kazakhstan to exploit the established commercial reserves. Typically, if commercial production rights are not granted it is because the contract holder has failed to make a commercial discovery within their contract territory and had decided to abandon the contract territory or the contract holder has insufficient funds to complete its minimum work program requirement and was unable to complete the necessary work to substantiate the presence of commercially producible reserves to the MEMR. Our efforts are focused toward meeting our minimum work program requirements and making and substantiating commercial discoveries in each of identified structures to support our application for commercial production rights. If we are not granted commercial production rights prior to the expiration of our exploration contract, we may lose our right to produce the reserves on our current properties. If we are unable to produce those reserves, we will be unable to realize revenues and earnings and to fund operations and we would most likely be unable to continue as a going concern.

Prospects that we decide to drill may not yield oil or natural gas in commercially viable quantities or quantities sufficient to meet our targeted rate of return.

12

A “prospect” is a property which, based on available seismic and geological data, we believe shows potential oil or natural gas. Our prospects are in various stages of evaluation and interpretation. There is no way to accurately predict in advance of incurring drilling and completion costs whether a prospect will be economically viable. Even with seismic data and other technologies and the study of producing fields in the same area, we cannot know conclusively prior to drilling whether oil or natural gas will be present or, if present, will be present in commercial quantities. The analysis that we perform using data from other wells, more fully explored prospects and /or producing fields may not be useful in predicting the characteristics and potential reserves associated with our drilling prospects. If we drill additional unsuccessful wells, our drilling success rate may decline and we may not achieve our targeted rate of return.

We may incur substantial losses and be subject to substantial liability claims as a result of our operations.

We are not insured against all risks. Losses and liabilities arising from uninsured and underinsured events could materially and adversely affect our business, financial condition or results of operations. Our oil and natural gas exploration and production activities are subject to all of the operating risks associated with drilling for and producing oil and natural gas, including the possibility of:

|

|

• |

environmental hazards, such as uncontrollable flows of oil, natural gas, brine, well fluids, toxic gas or other pollution into the environment, including groundwater and shoreline contamination; |

|

|

• |

abnormally pressured formations; |

|

|

• |

mechanical difficulties, such as stuck oil field drilling and service tools and casing collapse; |

|

|

• |

fires and explosions; |

|

|

• |

personal injuries and death; and |

|

|

• |

natural disasters. |

Any of these risks could adversely affect our ability to conduct operations or result in substantial losses. We may elect not to obtain insurance if we believe that the cost of available insurance is excessive relative to the risks presented. In addition, pollution and environmental risks generally are not fully insurable. If a significant accident or other event occurs that is not fully covered by insurance, it could adversely affect us.

We are subject to complex laws that can affect the cost, manner or feasibility of doing business.

Exploration, development, production and sale of oil and natural gas are subject to extensive federal, state, local and international regulation. We may be required to make large expenditures to comply with governmental regulations. Matters subject to regulation include:

|

|

• |

discharge permits for drilling operations; |

|

|

• |

drilling bonds; |

|

|

• |

reports concerning operations; |

|

|

• |

The spacing of wells; |

|

|

• |

unitization and pooling of properties; and |

|

|

• |

taxation. |

14

Under these laws, we could be liable for personal injuries, property damage and other damages. Failure to comply with these laws may also result in the suspension or termination of our operations and subject us to administrative, civil and criminal penalties. Moreover, these laws could change in ways that substantially increase our costs. Any such liabilities, penalties, suspensions, terminations or regulatory changes could materially adversely affect our financial condition and results of operations.

We may incur substantial liabilities to comply with environmental laws and regulations.

Our oil and natural gas operations are subject to stringent federal, state and local laws and regulations relating to the release or disposal of materials into the environment or otherwise relating to environmental protection. These laws and regulations may require the acquisition of permits before drilling commences, restrict the types, quantities and concentration of substances that can be released into the environment in connection with drilling and production activities, limit or prohibit drilling activities on certain lands lying within wilderness, wetlands and other protected areas, and impose substantial liabilities for pollution resulting from our operations. Failure to comply with these laws and regulations may result in the assessment of administrative, civil and criminal penalties, imposition of investigatory or remedial obligations or even injunctive relief. Changes in environmental laws and regulations occur frequently. Any changes that result in more stringent or costly waste handling, storage, transport, disposal or cleanup requirements could require us to make significant expenditures to maintain compliance, and may otherwise have a material adverse effect on our results of operations, competitive position or financial condition as well as on the industry in general. Under these environmental laws and regulations, we could be held strictly liable for the removal or remediation of previously released materials or property contamination regardless of whether we were responsible for the release or whether our operations were standard in the industry at the time they were performed.

Unless we replace our oil and natural gas reserves, our reserves and future production will decline, which would adversely affect our cash flows and income.

Unless we conduct successful development, exploration and exploitation activities or acquire properties containing proved reserves, our proved reserves will decline as those reserves are produced. Producing oil and natural gas reservoirs generally are characterized by declining production rates that vary depending upon reservoir characteristics and other factors. Our future oil and natural gas reserves and production, and, therefore our cash flow and income, are highly dependent on our success in efficiently developing and exploiting our current reserves and economically finding or acquiring additional recoverable reserves. If we are unable to develop, exploit, find or acquire additional reserves to replace our current and future production, our cash flow and income will decline as production declines, until our existing properties would be incapable of sustaining commercial production.

Our activities, and correspondingly, our ability to generate revenue to support operations, could be adversely affected because of inadequate infrastructure in the region where our properties are located.

Our exploration and development activities could suffer due to inadequate infrastructure in the region. We are working to improve the infrastructure on our properties. Any problem or adverse change affecting our operational infrastructure, or infrastructure provided by third parties, could have a material adverse effect on our financial condition and results of operations. Similarly, if we are unsuccessful in developing the infrastructure on our properties it could have

15

a material adverse effect on our financial conditions and results of operations.

The unavailability or high cost of drilling rigs, equipment, supplies, personnel and oil field services could adversely affect our ability to execute on a timely basis our exploration and development plans within our budget.

Shortages or the high cost of drilling rigs, equipment, supplies or personnel could delay or adversely affect our development and exploration operations. As the price of oil and natural gas has remained high, demand for production equipment and personnel has also remained high, resulting, in some cases in shortages of equipment and skilled personnel. In addition, larger producers may be able to secure access to such equipment by offering drilling companies more lucrative terms. As demand for services and personnel increases, the cost also increases, which can delay our ability to convert our reserves into cash flow as well as significantly increasing the cost of producing those reserves, thereby having a negative impact on anticipated net income.

The unavailability or high price of transportation systems could adversely affect our ability to deliver our oil on terms that would allow us to operate profitably, or at all.

Because of the location of our properties, the crude oil we produce must be transported by truck or by rail. In the future it will likely also be transported by pipelines. These railways and pipelines are operated by state-owned entities or other third parties, and there can be no assurance that these transportation systems will always be functioning and available, or that the transportation costs will remain at acceptable levels. In addition, any increase in the cost of transportation or reduction in its availability to us could have a material adverse effect on our results of operations. There is no assurance that we will be able to procure sufficient transportation capacity on economical terms, if at all.

Competition in the oil and natural gas industry is intense, which may adversely affect our ability to compete.

We operate in a highly competitive environment for acquiring properties, marketing oil and natural gas and securing trained personnel. Many of our competitors possess and employ financial, technical and personnel resources that are substantially greater than ours. Those companies may be able both to pay more for productive oil and natural gas properties and exploratory prospects and to evaluate, bid for and purchase a greater number of properties and prospects than our financial or personnel resources permit. Our ability to acquire additional prospects and to find and develop reserves in the future will depend on our ability to evaluate and select suitable properties and to consummate transactions in a highly competitive environment. There is substantial competition for capital available for investment in the oil and natural gas industry. We may not be able to compete successfully in the future in acquiring prospective reserves, developing reserves, marketing hydrocarbons, attracting and retaining quality personnel or raising additional capital.

Risks Relating to Our Business

If you purchase shares of our stock, your investment will be subject to the same risks inherent in international operations, including, but not limited to, adverse governmental actions, political risks, and expropriation of assets, loss of revenues and the risk of civil unrest or war.

We believe that the present policies of the government of the Republic of Kazakhstan are favorable to foreign investment and to exploration and production and we are not aware of any

16

impending changes. While there is a certain amount of bureaucratic “red tape” we have significant experience working in Kazakhstan, and good relationships with government agencies at many levels.

We, however, remain subject to all the risks inherent in international operations, including adverse governmental actions, uncertain legal and political systems, and expropriation of assets, loss of revenues and the risk of civil unrest or war. Our primary oil and gas properties are located in Kazakhstan, which until 1990 was part of the Soviet Union. Kazakhstan retains many of the laws and customs of the former Soviet Union, but has and is continuing to develop its own legal, regulatory and financial systems. As the political and regulatory environment changes, we may face uncertainty about the interpretation of our agreements; in the event of dispute, we may have limited recourse within the legal and political system.

If we are successful in establishing commercially producible reserves on our properties, an application will be made for a commercial production contract. We have the exclusive right to negotiate this contract for the ADE Block and Extended Territory, and the government is required to conduct these negotiations under the “Law of Petroleum.” The terms of the commercial production contract will establish the royalty and other payments due to the government in connection with commercial production. At the time the commercial production contract is issued, we will be required to begin repaying the government its historical investment costs of exploration and development of the ADE Block and the Extended Territory. Our obligation associated with the ADE Block is approximately $6 million. Our obligation associated with the Extended Territory is approximately $5.3 million. If satisfactory terms for commercial production rights cannot be negotiated, it could have a material adverse effect on our financial position.

Item 1B. Unresolved Staff Comments

|

|

None. |

Item 2. Properties

17

We currently own a 100% interest in a license to use subsurface mineral resources and a hydrocarbon exploration contract issued by the ROK in 1999 and 2000, respectively (collectively referred to herein as the “license” or the “contract”). The original contract granted us the right to engage in exploration and development activities in an area of approximately 200 square kilometers referred to herein as the ADE Block. The ADE Block is comprised of three fields, the Aksaz, Dolinnoe and Emir fields. During our 2006 fiscal year our exploration contract was expanded to include an additional 260 kilometers of land adjacent to the ADE Block, which we refer to as the “Extended Territory. The Extended Territory is governed by the terms of the original contract. The ADE Block and the Extended Territory are sometimes collectively referred to herein as “our properties.”

When initially granted, the exploration and development stage of the contract had a five year term. The time for exploration and development was then extended to July 9, 2007, with the right to seek an additional two-year extension. In February 2007, the MEMR granted our request for extension of our exploration contract. Under the terms of the contract extension, the exploration period will extend to July 2009 over the entire exploration contract territory.

Under the terms of our contract we have the right to gather and sell all oil and natural gas we produce in test production until the expiration of our exploration contract, as extended, with the revenue from such sales belonging to BMB.

Under the statutory scheme in the Republic of Kazakhstan prospective oil fields are developed in two stages. The first stage is an exploration and appraisal stage during which a private contractor, such as BMB, is given a license to explore for oil and gas on a territory for a set term of years. During this stage the primary focus is on the search for a commercial discovery, i.e., a discovery of a sufficient quantity of oil and gas to make it commercially feasible to pursue execution of, or transition to, a production contract with the government.

In order to be assured that adequate exploration activities are undertaken by the contractor, the MEMR establishes an annual mandatory minimum work program to be accomplished in each year of the exploration contract. Under the minimum work program the contractor is required to invest a minimum dollar amount in exploration activities on the contract territory that may include geophysical studies, construction of field infrastructure or drilling activities. During the exploration stage, the contractor is also required to drill sufficient wells to establish the existence of commercially producible reserves in any structure for which it seeks a commercial production license. Failure to complete the minimum work program during the term of an exploration contract could preclude a contractor from receiving a longer-term production contract, regardless the success of the contractor in proving commercial reserves during the partial fulfillment of the minimum work program. Therefore, completion of the exploration contract’s minimum work program is essential to the success of any oil company working in Kazakhstan.

19

The contract we hold follows the above format. The contract sets the minimum dollar amount we must expend through July 2009:

|

Amount of Expenditure |

Through July 2005 |

Through July 2006 |

Through July 2007 |

Through July 2008 |

Through July 2009 |

Total |

|

Mandated by Contract |

$21,500,000 |

$6,000,000 |

$12,700,000 |

$ 8,480,000 |

$70,000 |

$48,750,000 |

|

Actually Made |

$38,400,000 |

$12,700,000 |

$37,410,000* |

$ - |

$ - |

$88,510,000 |

* Investment as of March 31, 2007.

Under the rules of the MEMR there is an option for our expenditures above the minimum requirements in one period to be carried over to meet minimum obligations in future periods. As the above chart shows we have exceeded the minimum expenditure requirement in each period of the contract. In connection with the recent extension grant, the MEMR required an additional capital expenditures of $16,750,000 through the end of the extension period. We expect our planned drilling activities through 2009 to exceed the new amounts added to our minimum work program.

As noted above, from June 2006 through March 31, 2007 we invested approximately $37.4 million in the exploration and development of our properties. During the year ended March 31, 2007, we incurred and capitalized expenses of approximately $18.4 million attributable to drilling activities at the Kariman-1, Kariman-2, Dolinnoe-6 and Emir-6 wells during the year, as discussed in more detail below. We also incurred and capitalized approximately $6.2 million in well workover expenses, almost $1.3 million in geological and geophysical works and $9.5 million in materials used in exploration and development activities. Such capitalized costs are recorded as oil and gas properties on our balance sheet as at March 31, 2007. See Note 6 to Consolidated Financial Statements.

The second aspect of the mandatory minimum work program is the requirement that we drill a sufficient number of wells on any structure for which we seek commercial production rights to support our claim of a commercial discovery within the structure. Typically, one exploratory well and two appraisal wells are sufficient to support such a claim, although in some cases, commercial reserves have been demonstrated with fewer wells. The number of wells to be drilled is generally determined by the number of structures identified by the seismic studies done on a territory. The 3D seismic studies of our contract territory, as extended, have identified six potential structures. Therefore, we anticipate the need to drill up to 18 wells during the exploration phase of our contract as reflected on the top half of the following chart:

19

|

Structures |

Aksaz |

Dolinnoe |

Emir |

Kariman |

Borly |

Yessen |

|

Exploratory Wells |

1 |

1 |

1 |

1 |

1 |

1 |

|

Appraisal Wells |

2 |

2 |

2 |

2 |

2 |

2 |

|

|

|

|

|

|

|

|

|

Existing Wells |

2 |

4 |

1 |

2 |

0 |

0 |

|

Wells in Progress |

0 |

0 |

1 |

2 |

0 |

0 |

|

Remaining Wells to Drill by 2009 |

1 |

0 |

1 |

0 |

3 |

3 |

The bottom half of the above chart shows our current progress on drilling of exploratory and appraisal wells, the second aspect of our mandatory minimum work program. As the chart shows, for purposes of meeting the minimum work program requirements, we have nine wells completed and three wells currently in progress.

To date we have been conservative in our approach to exploration. It has been our practice to drill our first few wells serially. Our first well was the Dolinnoe-2 well drilled in 2004. This was followed by the Dolinnoe-3 well, and then the Aksaz-4 and Kariman-1 wells. We have verified the presence of oil and gas in all our wells thus far. We have expended substantial time and money to study our wells very closely.

It is important to remember that the purpose of the exploration stage is to study the geology and geophysical characteristics of each field and individual wells, with a view to qualifying for a longer-term production contract. Once drilling of a well is completed, our emphasis focuses on an extended period of testing a well’s production characteristics and capacities to determine the best method for producing oil from a well and to gain insight into the further development of the entire field. During this stage of exploration, oil production is subject to wide fluctuations caused by varying pressures commonly experienced by new wells and by significant periods of well closure to accommodate various mandatory testing. Maximizing oil production only becomes the central focus during the post-exploration phase when exploiting the commercial discovery commences under a production contract.

In addition to the wells currently in progress, we anticipate the need to complete up to eight additional wells by the end of the term of our exploration contract in order to qualify for a commercial production license on each of our structures. This will require that we continue to accelerate our drilling activities during the next two years if we wish to obtain commercial production rights for each of the structures within our properties.

Under our contract, we have the exclusive right to apply for and negotiate a commercial production contract. The government is required to negotiate the terms of these rights in good faith in accordance with the Law of Petroleum of Kazakhstan. Based on discussions with the MEMR, the primary factors used by the MEMR in determining whether to grant commercial production rights are whether the contract holder has fulfilled the minimum work program commitments, proved the existence of a commercial discovery and submitted and received approval of a development plan prepared by a third-party petroleum institute in Kazakhstan for the exploitation of the established commercial reserves. All our efforts during exploration stage have and will continue to focus on meeting these criteria. We have not yet applied for commercial production rights because we enjoy certain economic advantages during exploration and development.

20

The terms of our commercial production rights and royalty rates will be negotiated at the time we apply to move to commercial production. During exploration and development stage, we have the right to produce and sell oil and natural gas at a royalty rate of 2%. When we move to commercial production, the negotiated royalty rates may change depending on reserves and production rates. Royalty rates are established by the taxing authorities of the ROK and are based on production rates; the rate increases on a sliding scale. Current royalty rates range for 2% to 6%. We also anticipate that we will be required to pay rent export tax when we move to commercial production. The current rent export tax rate is tied to the Brent oil price; the rate increases on a sliding scale, at the present time it is 33%. Under our contract during exploration stage we are not required to pay rent export tax on the oil we sell to the world markets. We anticipate that at the time we move to commercial production, the government will impose the rent export tax on all oil and natural gas we sell outside the domestic market in Kazakhstan.

Drilling Operations

The following table sets forth our drilling activity for the years ended March 31, 2005, March 31, 2006 and March 31, 2007. In the table, “Gross” refers to the total wells in which we have a working interest or back-in working interest after payout and “Net” refers to gross wells multiplied by our working interest therein.

|

|

March 31, 2007 |

|

March 31, 2006 |

|

March 31, 2005 | |||||||

|

|

|

Gross |

|

Net |

|

Gross |

|

Net |

|

Gross |

|

Net |

|

Exploratory: |

|

|

|

|

|

|

|

|

|

|

|

|

|

Productive |

|

- |

|

- |

|

- |

|

- |

|

- |

|

- |

|

Non-productive |

|

- |

|

- |

|

- |

|

- |

|

- |

|

- |

|

Total |

|

- |

|

- |

|

- |

|

- |

|

- |

|

- |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Development: |

|

|

|

|

|

|

|

|

|

|

|

|

|

Productive |

|

9 |

|

9 |

|

6 |

|

6 |

|

5 |

|

5 |

|

Non-productive |

|

- |

|

- |

|

- |

|

- |

|

- |

|

- |

|

Total |

|

- |

|

- |

|

- |

|

- |

|

- |

|

- |

|

Grand Total |

|

9 |

|

9 |

|

6 |

|

6 |

|

5 |

|

5 |

During the fourth quarter of fiscal 2006 we took steps to secure drilling rigs to allow us to accelerate our drilling activities over previous years. In January 2006 we signed one-year contracts with Great Wall, a Chinese drilling company, and Oil and Gas Exploration Krakow, a Polish drilling company, to furnish heavy rigs of sufficient size to drill wells to the depth of 4,000 meters, which is generally our target depth in Triassic carbonate structures. We also signed a turnkey contract with KandyagashBurService, LLP, a Kazakhstani drilling company, for drilling of new wells on the Emir oil field. In addition, we hired Great Wall to provide a lighter rig we use for completion, workover and testing activities on completed wells. Fiscal 2007 was the first year when we engaged in drilling several wells simultaneously compared to our drilling strategy in the past when we drilled wells serially.

During the fiscal year ended March 31, 2007, we drilled to deepen the Kariman–1 well, completed drilling of Dolinnoe-6 and Kariman-2 well and continued drilling of Emir-6 well. We also continued testing and development works on the Dolinnoe-1, Dolinnoe- 2, Dolinnoe- 3, Emir -1 and Aksaz -1 and Aksaz-4 wells.

In February 2006 we commenced drilling in the Extended Territory. Our initial project was increasing the depth of an existing non-producing well, which is designated as the Kariman-1 well. Drilling operations were conducted by Oil and Gas Exploration Kracow, Poland. The

22

Kariman-1 well was cased to a depth of 1,661 meters and drilled to a total depth of 3,069 meters in 1967 by the Soviet government. Drilling was suspended at that depth because it was believed that the oil-bearing formations would not be found deeper than the lower Jurassic formations.

Our study of more recent advanced geological and geophysical information indicated that oil-bearing formations in the Kariman field are expected at a depth of 3,600 to 3,800 meters, through the Triassic formation. During reaming of the existing wellbore we discovered that the technical condition of the well had deteriorated significantly from the condition described in the original drilling logs. Because of the poor conditions within the wellbore, we began a sidetrack at 1,660 meters and essentially drilled a new bore from that depth.

Upon penetration the Middle Triassic formation between 3,356 and 3,361 meters we encountered very high formation pressure, additional intensive oil shows and a substantial increase in the gas content in drilling fluid. Therefore, as a safety precaution, we compensated by increasing drilling fluid weight. The increased weight of the required drilling fluid allowed us to determine that the Middle Triassic formation is characterized by abnormally high pressure of approximately 600 atmospheres.

Due to the high weight of the drilling fluid, beginning at 3,361 meters there was a loss circulation within the wellbore. Analysis of electric logging data determined that the loss circulation area was located at a depth of 1,660-1,860 meters. Therefore, we separated the loss circulation from the inflow by installing a cement plug and running casing to the depth of 3,100 meters.

Due to high pressure and strong degassing of drilling fluid in the penetrated portion of the Middle Triassic formations, our operations managers stopped drilling at a depth of 3,361 meters and retained Kezbie, a Kazakhstani company to commence well completion operations. Completion operations were followed by limited testing of a portion of the Kariman-1 well. The tests have been conducted in the open wellbore without perforation of the Upper Triassic formation, despite the fact that the flows from this horizon were partially locked by drilling fluid preliminary testing conducted during the first three days of testing yielded results ranging from 380 to 570 barrels per day.

Despite encouraging preliminary results of testing in the open wellbore, we decided to shut the well until arrival of a liner, smaller-diameter casing. The equipment has been procured and the casing was run-in during February-March of 2007. We intend to commence completion operations followed by extensive testing of the Upper Triassic sandstone formations during the first quarter of the 2008 fiscal year.

During the summer of 2007 we commenced drilling operations on three wells simultaneously, Kariman-2, Dolinnoe-6 and Borly -2.

Kariman-2, the first well drilled by us from surface, was spudded on August 15, 2006, by company contractor, Oil and Gas Exploration Krakow. The well is located 500 meters to the south of the Kariman-1 well. Drilling of the Kariman-2 was finished on December 25, 2006, with the final depth of 3,535 meters upon reaching the end of the targeted Middle Triassic horizons. Completion operations were completed by Burgylau LLP, a local contractor, during January 2007. We commenced testing of the well in February 2007. Since then the well has been steadily test producing with the range between 1,400 and 1,700 bpd on a 6mm choke.

23

Dolinnoe-6 well was spudded by our drilling contractor, Great Wall (China), on August 8, 2006. The well is located 800 meters to the southeast of the Dolinnoe-3 well drilled by the Company in 2005. Drilling operations were completed on January 23, 2007, with the final depth of 3,883 meters. Completion operations were subcontracted to Burgylau LLP and were carried out during March and April 2007. Completion operations were commenced at the end of March-beginning of April. We expect to continue intensive testing activities during the first quarter and to announce results of such testing upon receiving detailed information.

On July 5, 2006, our drilling contractor, Great Wall, has placed a 150-ton rig on Borly-2, well drilled to a depth of 2,382 meters during 1995 by MangyshlakMunaiGas, a subsidiary of the Kazakhstani National Oil and Gas Company. The well was previously cased to a depth of 1,900 meters. During the process we made a decision to cease and postpone re-entry operations on the well until a heavier rig becomes available.

On October 2, 2006, our third drilling contractor, KanyagashBurService LLP (KBS), completed mobilization of a 175-ton drilling rig and spudded a new well, designated Emir-6, on the Emir oil field. We signed a turnkey contract with the KBS for drilling of this well with a target depth of 3,100 meters. We expect drilling, completion and testing operations to be completed in the first quarter of fiscal year 2008.

Production

The following table sets forth the number of productive oil and natural gas wells in which we owned an interest as of March 31, 2007.

|

|

Company-operated |

|

Non-operated |

|

Total | ||||||

|

|

Gross |

|

Net |

|

Gross |

|

Net |

|

Gross |

|

Net |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Oil |

9 |

|

9 |

|

- |

|

- |

|

9 |

|

9 |

|

Natural Gas |

- |

|

- |

|

- |

|

- |

|

- |

|

- |

|

Total |

9 |

|

9 |

|

- |

|

- |

|

9 |

|

9 |

As of the end of the 2007 fiscal year we had nine wells in workover, testing or test production. According to the laws of the Republic of Kazakhstan, we are required to test every prospective object on our properties separately, this includes the completion of well surveys on different modes with various choke sizes on each horizon.

In the course of well testing, when the transfer from object to object occurs, the well must be shut in; oil production ceases for the period of mobilization/ demobilization of the workover rig, pull out of the hole, run in the hole, perforation, packer installation time, etc. This has the effect of artificially diminishing production rates averaged over a set period of time.

Our production figures for the month of March 2007 covering production from the ADE block and Kariman field in the extended license territory were as following: daily total high production was 2,693 bpd; daily total low production was 1,946 bpd with an average daily total production for the 31 days of March of 2,337 bpd. Because this only accounts for one zone per well, this may not be representative of the cumulative total production rate from all of the tested intervals in each of the wells.

Following is a brief description of the current production status of each of our nine wells and the Emir-6 well, which is nearing completion of drilling.

24

Aksaz -1

This well is currently not producing. Prior to workover, four producing intervals were tested. The single interval test production rates in Aksaz-1 using a 10 mm diameter choke was 140 bpd. We expect to undertake workover operations on this well, consisting primary of fishing works, once the workover rig will become available following testing of the Dolinnoe-6, Kariman-1 and Emir-6 wells.

Aksaz – 4

Drilling of this well was completed in August 2005. Two producing intervals have been tested. Current production rates from single interval testing using a 6 mm diameter choke ranges from 76 to 107 bpd.

Dolinnoe – 1

During the third quarter of fiscal 2007 we conducted workover operations on this well and it is currently producing. Production rates from single interval testing using a 6 mm diameter choke ranges from 221 to 438 bpd.

Dolinnoe – 2

This well is also producing. Current production rates from single interval testing using a 8 mm diameter choke ranges from 32 to 290 bpd.

Dolinnoe – 3

This well was initially completed to a depth of 3,800 meters in September 2005. During initial testing, we were able to perforate only 17 of 24 meters of the producing interval because of intensive oil and gas shows. Subsequent perforation of the remaining 7 meters of the interval was disrupted when tubing was impacted by the heavy drilling mud components, and the blowout preventer was damaged, which required the forced killing of the well. Although we were able to restore limited oil production from the well, the production was substantially lower than the well’s initial test production performance. We have conducted numerous tests during the past six months in an effort to increase daily production rates to levels consistent with management expectations. In August 2006 we completed the acid treatment of the Dolinnoe-3 well. During the ten days following completion of the acid treatment the well produced between 460 and 630 bpd while being tested using chokes between 6mm and 10mm in size. We believe these initial test results indicate that we have developed a suitable hydrochloric acid formula to conduct effective acid treatment of the carbonate formations with temperature and pressure conditions characterized by the Dolinnoe field. Current production rates from single interval testing using an 8 mm diameter choke range from 170 to 347 bpd. We plan to continue application of acid treatment to Dolinnoe field wells to stimulate production from such wells.

Dolinnoe - 6

Drilling of the Dolinnoe-6 well was completed on January 23, 2007. This well was drilled through the full Middle Triassic layer to a depth of 3,883 meters. Completion activities have been performed and testing of the well commenced in the third week of March. Stable production estimates will not be available until conclusion of the testing period.

25

Emir – 1

This well currently is not producing. Single interval production from this well prior to workover was 1.3 to 9.5 bpd.

Emir - 6

Drilling of the Emir-6 well has been completed on June 2, 2007. This well was drilled to a depth of 3,197 meters. Completion activities have been performed and we anticipate perforating the well within the next two weeks. Following perforation of the well, we will begin the testing.

Kariman - 1

Re-entry of the Kariman-1 well was completed on June 30, 2006 and well completion to the upper Triassic formation was completed by July 17, 2006. Despite the fact that the flows from this horizon are partially blocked by drilling fluid, preliminary testing conducted during the first month of testing using chokes ranging from 20 mm to 30 mm yielded results ranging from 380 to 570 barrels per day. The well was then put into a pressure-build up test to better understand the source of the high pressures encountered during earlier re-entry operations at the upper four meters of Middle Triassic formation. We have obtained and run down a specialized low diameter casing in the well. Perforation and subsequent testing of Upper Triassic sandstone formations are scheduled for the first quarter of fiscal 2008.

Kariman – 2

This well was spudded on August 15, 2006, and is the first well we have drilled from the surface in the Kariman oil field. Drilling of the Kariman-2 well was finished on December 25, 2006. Drilling operations were concluded at the depth of 3,535 meters, upon reaching the end of the targeted Middle Triassic horizons.

Well completion activities were conducted utilizing a drilling rig specifically employed for workover and completion operations. Subsequent testing of the well during the months of February and March yielded test production ranging from 996 to 1,859 bpd with steady production in the range of 1,4000 to 1,7000 bpd. We plan to continue test production from this well.

Cost Information

|

|

Capitalized Costs |

Capitalized costs and accumulated depletion, depreciation and amortization relating to our oil and natural gas producing activities, all of which are conducted in the Republic of Kazakhstan, are summarized below:

|

|

March 31, 2007 |

|

March 31, 2006 |

|

|

|

|

|

|

Developed oil and natural gas properties |

$ 82,311,230 |

|

$ 68,079,938 |

|

Unevaluated oil and natural gas properties |

25,279,813 |

|

- |

|

Accumulated depletion, depreciation and |

(3,403,475) |

|

(1,396,641) |

|

Net capitalized cost |

$ 104,187,568 |

|

$ 66,683,297 |

27

Exploration, Development and Acquisition Capital Expenditures

The following table sets forth certain information regarding the total costs incurred associated with exploration, development and acquisition activities.

|

|

|

March 31, 2007 |

|

March 31, 2006 |

|

|

|

|

|

|

|

Acquisition costs: |

|

|

|

|

|

Unproved properties |

|

$ - |

|

$ - |

|

Proved properties |

|

20,788,119 |

|

20,788,119 |

|

Exploration costs |

|

8,197,492 |

|

6,826,695 |

|

Development costs |

|

76,611,170 |

|

39,547,849 |

|

Subtotal |

|

105,596,781 |

|

67,162,663 |

|

Asset retirement costs |

|

1,994,262 |

|

917,275 |

|

Total costs incurred |

|

$ 107,591,043 |

|

$ 68,079,938 |

Oil and Natural Gas Volumes, Prices and Operating Expense

The following table sets forth certain information regarding production volumes, average sales prices and average operating expense associated with our sale of oil and natural gas for the periods indicated.

|

|

For the Year Ended March 31, 2007 |

|

For the Year Ended March 31, 2006 |

|

For the Year Ended March 31, 2005 |

|

Production: |

|

|

|

|

|

|

Oil and condensate (Bbls) |

321,993 |

|

242,522 |

|

68,755 |

|

Natural gas liquids (Bbls) |

- |

|

- |

|

- |

|

Natural gas (Mcf) |

- |

|

- |

|

- |

|

Barrels of oil equivalent (BOE) |

321,993 |

|

242,522 |

|

68,755 |

|

|

|

|

|

|

|

|

Sales(1)(3): |

|

|

|

|

|

|

Oil and condensate (Bbls) |

315,540 |

|

227,976 |

|

64,084 |

|

Natural gas liquids (Bbls) |

- |

|

- |

|

- |

|

Natural gas (Mcf) |

- |

|

- |

|

- |

|

Barrels of oil equivalent (BOE) |

315,540 |

|

227,976 |

|

64,084 |

|

|

|

|

|

|

|

|

Average Sales Price(1): |

|

|

|

|

|

|

Oil and condensate ($ per Bbl) |

$ 50.03 |

|

$ 26.13 |

|

$ 15.19 |

|

Natural gas liquids ($ per Bbl) |

$ - |

|

$ - |

|

$ - |

|

Natural gas ($ per Mcf) |

$ - |

|

$ - |

|

$ - |

|

Barrels of Oil equivalent ($ per BOE) |

$ 50.03 |

|

$ 26.13 |

|

$ 15.19 |

|

|

|

|

|

|

|

|

Average oil and natural gas operating expenses |

$ 7.20 |

|

$ 3.84 |

|

$ 6.34 |

(1) During the years ended March 31, 2007, 2006 and 2005, the Company has not engaged in any hedging activities, including derivatives.

(2) Includes transportation cost, production cost and ad valorem taxes.

(3) We use sales volume rather than production volume for calculation of per unit cost because not all volume produced is sold during the period. The related production costs were expensed only for the units sold, not produced based on a matching principle of accounting. Therefore, oil and gas operating expense per BOE was calculated by dividing oil and gas operating expenses for the year by the volume of oil sold during the year.

28

|

Item 3. |

Legal Proceedings |

In December 2003, a complaint was filed in the 15th Judicial Court in and for Palm Beach County, Florida, naming, among others, the Company and former directors, Georges Benarroch and Alexandre Agaian, as defendants. The plaintiffs, Brian Savage, Thomas Sinclair and Sokol Holdings, Inc., allege claims of breach of contract, unjust enrichment, breach of fiduciary duty, conversion and violation of a Florida trade secret statute in connection with a business plan for the development Aksaz, Dolinnoe and Emir oil and gas fields owned by Emir Oil, LLP. The parties mutually agreed to dismiss this lawsuit without prejudice.

In April 2005, Sokol Holdings, Inc., also filed a complaint in United States District Court, Southern District of New York alleging that BMB Munai, Inc., Boris Cherdabayev, and former BMB directors Alexandre Agaian, Bakhytbek Baiseitov, Mirgali Kunayev and Georges Benarroch wrongfully induced Toleush Tolmakov to breach a contract under which Mr. Tolmakov had agreed to sell to Sokol 70% of his 90% interest in Emir Oil LLP.