SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

Report of Foreign Private Issuer

Pursuant to Rule 13a -16 or 15d -16 of

the Securities Exchange Act of 1934

Report on Form 6-K dated August 4, 2016

(Commission File No. 1-13202)

Nokia Corporation

Karaportti 3

FI-02610 Espoo

Finland

(Name and address of registrant’s principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover of Form 20-F or Form 40-F:

Form 20-F: x Form 40-F: o

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1):

Yes: o No: x

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7):

Yes: o No: x

Indicate by check mark whether the registrant by furnishing the information contained in this form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

Yes: o No: x

Enclosures:

Nokia stock exchange release dated August 4, 2016: Financial Report for Q2 and Half Year 2016

|

|

HALF YEAR FINANCIAL REPORT |

|

|

|

|

|

August 4, 2016 |

Nokia Corporation Financial Report for Q2 and Half Year 2016

Solid financial performance and raised cost savings target

Nokia Corporation

Half Year Financial Report

August 4, 2016 at 08:00 (CET +1)

This is a summary of the Nokia Corporation financial report for Q2 and half year 2016 published today. The complete financial report for Q2 and half year 2016 with tables is available at http://nokia.com/financials. Investors should not rely on summaries of our financial reports only, but should review the complete financial reports with tables.

FINANCIAL HIGHLIGHTS

· Non-IFRS net sales in Q2 2016 of EUR 5.7 billion (reported: EUR 5.6 billion). In the year-ago quarter, non-IFRS net sales would have been EUR 6.4 billion on a comparable combined company basis (reported: EUR 2.9 billion on a Nokia stand-alone basis).

· Non-IFRS diluted EPS in Q2 2016 of EUR 0.03 (reported: EUR negative 0.12).

· Raised annual cost savings target to approximately EUR 1.2 billion of total annual cost savings to be achieved in full year 2018, compared to the combined non-IFRS operating costs of Nokia and Alcatel-Lucent for full year 2015, excluding Nokia Technologies. Related to this, Nokia recorded approximately EUR 600 million of restructuring and associated charges in the second quarter 2016.

Nokia’s Networks business

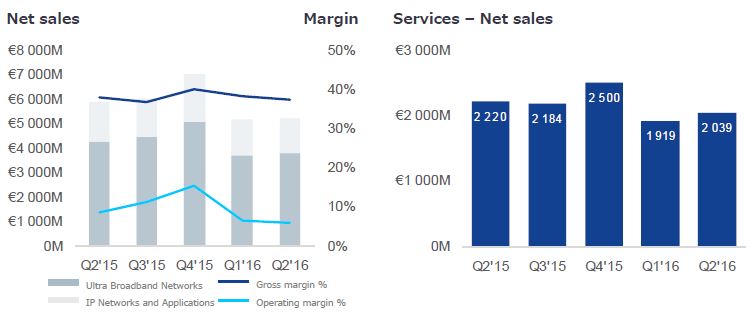

· 11% year-on-year net sales decrease in Q2 2016. Consistent with our outlook for the wireless infrastructure market, net sales were weak in Mobile Networks within Ultra Broadband Networks, and accounted for approximately 80% of the overall decrease in Nokia’s Networks business. IP Networks and Applications also contributed to the decrease. This was partially offset by strong growth in Fixed Networks within Ultra Broadband Networks.

· In Q2 2016, solid gross margin of 37.4% and operating margin of 6.0% were adversely affected by a customer in Latin America undergoing judicial recovery. Excluding this, gross margin would have been approximately 38% and operating margin would have been nearly 7%.

Nokia Technologies

· 11% year-on-year net sales decrease in Q2 2016. Excluding the impact of non-recurring items that benefitted the year-ago quarter, Nokia Technologies net sales would have grown by approximately 10% year-on-year, primarily due to higher intellectual property licensing income from existing licensees.

· Announced an expansion of the patent cross license agreement with Samsung on July 13, 2016 to cover certain additional patent portfolios, reinforcing Nokia’s leadership in technologies for the programmable world. The expansion of the agreement occurred subsequent to the end of the second quarter 2016, and therefore did not impact the second quarter of 2016 financials. Instead, the expanded agreement will have a positive impact to Nokia Technologies starting from the third quarter of 2016. Nokia expects total annualized net sales related to patent and brand licensing to grow to a run rate of approximately EUR 950 million by the end of 2016.

Q2 and January-June 2016 non-IFRS results. See note 1 to the interim financial statements for further details (1),(2)

|

|

|

|

|

Combined |

|

YoY |

|

|

|

QoQ |

|

Q1- |

|

Combined |

|

YoY |

|

|

EUR million |

|

Q2’16 |

|

Q2’15 |

|

change |

|

Q1’16 |

|

change |

|

Q2’16 |

|

Q1-Q2’15 |

|

change |

|

|

Net sales — constant currency (non-IFRS) |

|

|

|

|

|

(9 |

)% |

|

|

2 |

% |

|

|

|

|

(9 |

)% |

|

Net sales (non-IFRS) |

|

5 676 |

|

6 363 |

|

(11 |

)% |

5 603 |

|

1 |

% |

11 279 |

|

12 492 |

|

(10 |

)% |

|

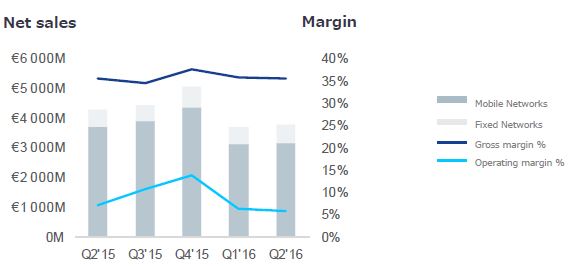

Nokia’s Networks business |

|

5 228 |

|

5 895 |

|

(11 |

)% |

5 181 |

|

1 |

% |

10 409 |

|

11 557 |

|

(10 |

)% |

|

Ultra Broadband Networks |

|

3 807 |

|

4 303 |

|

(12 |

)% |

3 729 |

|

2 |

% |

7 535 |

|

8 530 |

|

(12 |

)% |

|

IP Networks and Applications |

|

1 421 |

|

1 593 |

|

(11 |

)% |

1 452 |

|

(2 |

)% |

2 873 |

|

3 027 |

|

(5 |

)% |

|

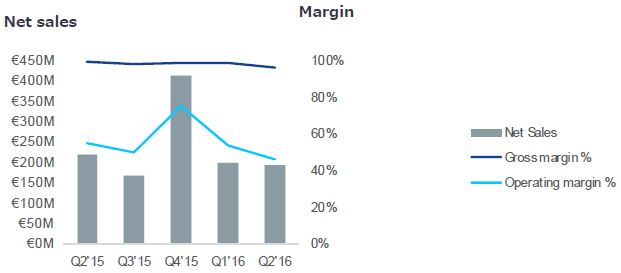

Nokia Technologies |

|

194 |

|

219 |

|

(11 |

)% |

198 |

|

(2 |

)% |

391 |

|

492 |

|

(21 |

)% |

|

Group Common and Other |

|

271 |

|

254 |

|

7 |

% |

236 |

|

15 |

% |

507 |

|

457 |

|

11 |

% |

|

Gross profit (non-IFRS) |

|

2 202 |

|

2 495 |

|

(12 |

)% |

2 205 |

|

0 |

% |

4 407 |

|

4 759 |

|

(7 |

)% |

|

Gross margin % (non-IFRS) |

|

38.8 |

% |

39.2 |

% |

(40 |

)bps |

39.4 |

% |

(60 |

)bps |

39.1 |

% |

38.1 |

% |

100 |

bps |

|

Operating profit (non-IFRS) |

|

332 |

|

649 |

|

(49 |

)% |

345 |

|

(4 |

)% |

677 |

|

925 |

|

(27 |

)% |

|

Nokia’s Networks business |

|

312 |

|

511 |

|

(39 |

)% |

337 |

|

(7 |

)% |

649 |

|

720 |

|

(10 |

)% |

|

Ultra Broadband Networks |

|

228 |

|

308 |

|

(26 |

)% |

234 |

|

(3 |

)% |

462 |

|

476 |

|

(3 |

)% |

|

IP Networks and Applications |

|

84 |

|

203 |

|

(59 |

)% |

103 |

|

(18 |

)% |

187 |

|

244 |

|

(23 |

)% |

|

Nokia Technologies |

|

89 |

|

120 |

|

(26 |

)% |

106 |

|

(16 |

)% |

195 |

|

297 |

|

(34 |

)% |

|

Group Common and Other |

|

(68 |

) |

18 |

|

|

|

(99 |

) |

|

|

(167 |

) |

(92 |

) |

|

|

|

Operating margin % (non-IFRS) |

|

5.8 |

% |

10.2 |

% |

(440 |

)bps |

6.2 |

% |

(40 |

)bps |

6.0 |

% |

7.4 |

% |

(140 |

)bps |

Q2 and January-June 2016 reported results, unless otherwise specified. See note 1 to the interim financial statements for further details(1),(3)

|

EUR million |

|

|

|

Nokia |

|

YoY |

|

|

|

QoQ |

|

Q1- |

|

Nokia |

|

YoY |

|

|

(except for EPS in EUR) |

|

Q2’16 |

|

Q2’15 |

|

change |

|

Q1’16 |

|

change |

|

Q2’16 |

|

Q2’15 |

|

change |

|

|

Net Sales - constant currency |

|

|

|

|

|

93 |

% |

|

|

2 |

% |

|

|

|

|

89 |

% |

|

Net sales |

|

5 583 |

|

2 919 |

|

91 |

% |

5 499 |

|

2 |

% |

11 082 |

|

5 854 |

|

89 |

% |

|

Nokia’s Networks business |

|

5 228 |

|

2 729 |

|

92 |

% |

5 181 |

|

1 |

% |

10 409 |

|

5 400 |

|

93 |

% |

|

Ultra Broadband Networks |

|

3 807 |

|

2 440 |

|

56 |

% |

3 729 |

|

2 |

% |

7 535 |

|

4 795 |

|

57 |

% |

|

IP Networks and Applications |

|

1 421 |

|

289 |

|

392 |

% |

1 452 |

|

(2 |

)% |

2 873 |

|

605 |

|

375 |

% |

|

Nokia Technologies |

|

194 |

|

194 |

|

0 |

% |

198 |

|

(2 |

)% |

391 |

|

461 |

|

(15 |

)% |

|

Group Common and Other |

|

271 |

|

0 |

|

|

|

236 |

|

15 |

% |

507 |

|

0 |

|

|

|

|

Non-IFRS exclusions |

|

(93 |

) |

0 |

|

|

|

(104 |

) |

|

|

(197 |

) |

0 |

|

|

|

|

Gross profit |

|

2 028 |

|

1 343 |

|

51 |

% |

1 554 |

|

31 |

% |

3 582 |

|

2 527 |

|

42 |

% |

|

Gross margin % |

|

36.3 |

% |

46.0 |

% |

(970 |

)bps |

28.3 |

% |

800 |

bps |

32.3 |

% |

43.2 |

% |

(1 090 |

)bps |

|

Operating (loss)/profit |

|

(760 |

) |

493 |

|

|

|

(712 |

) |

|

|

(1 472 |

) |

721 |

|

|

|

|

Nokia’s Networks business |

|

312 |

|

331 |

|

(6 |

)% |

337 |

|

(7 |

)% |

649 |

|

442 |

|

47 |

% |

|

Ultra Broadband Networks |

|

228 |

|

312 |

|

(27 |

)% |

234 |

|

(3 |

)% |

462 |

|

445 |

|

4 |

% |

|

IP Networks and Applications |

|

84 |

|

19 |

|

342 |

% |

103 |

|

(18 |

)% |

187 |

|

(3 |

) |

|

|

|

Nokia Technologies |

|

89 |

|

108 |

|

(18 |

)% |

106 |

|

(16 |

)% |

195 |

|

294 |

|

(34 |

)% |

|

Group Common and Other |

|

(68 |

) |

57 |

|

|

|

(99 |

) |

|

|

(167 |

) |

8 |

|

|

|

|

Non-IFRS exclusions |

|

(1 092 |

) |

(3 |

) |

|

|

(1 057 |

) |

3 |

% |

(2 149 |

) |

(24 |

) |

|

|

|

Operating margin % |

|

(13.6 |

)% |

16.9 |

% |

(3 050 |

)bps |

(12.9 |

)% |

(70 |

)bps |

(13.3 |

)% |

12.3 |

% |

(2 560 |

)bps |

|

Profit (non-IFRS) |

|

171 |

|

336 |

|

(49 |

)% |

139 |

|

23 |

% |

310 |

|

519 |

|

(40 |

)% |

|

(Loss)/profit |

|

(726 |

) |

338 |

|

|

|

(613 |

) |

18 |

% |

(1 338 |

) |

507 |

|

|

|

|

EPS, diluted (non-IFRS) |

|

0.03 |

|

0.09 |

|

(67 |

)% |

0.03 |

|

0 |

% |

0.06 |

|

0.14 |

|

(57 |

)% |

|

EPS, diluted |

|

(0.12 |

) |

0.09 |

|

|

|

(0.09 |

) |

|

|

(0.21 |

) |

0.13 |

|

|

|

|

Net cash and other liquid assets |

|

7 077 |

|

3 830 |

|

85 |

% |

8 246 |

|

(14 |

)% |

7 077 |

|

3 830 |

|

85 |

% |

(1)Results are as reported unless otherwise specified. The results information in this report is unaudited. Non-IFRS results exclude costs related to the Alcatel-Lucent transaction and related integration, goodwill impairment charges, intangible asset amortization and purchase price related items, restructuring and associated charges, and certain other items that may not be indicative of Nokia’s underlying business performance. For details, please refer to the Non-IFRS Exclusions section included in discussions of both the quarterly and year to date performance and note 2, “Non-IFRS to reported reconciliation”, in the notes to the financial statements attached to this report. A reconciliation of the Q2 2015 non-IFRS combined company results to the reported results can be found in the “Nokia provides recast segment results for 2015 reflecting new financial reporting structure” stock exchange release published on April 22, 2016. Change in net sales at constant currency excludes the impact of changes in exchange rates in comparison to Euro, our reporting currency. For more information on currency exposures, please refer to note 1, “Basis of Preparation”, in the notes to the financial statements attached to this report.

(2) Combined company historicals reflect Nokia’s new operating and financial reporting structure, including Alcatel-Lucent, and are presented as additional information as described in the stock exchange release published on April 22, 2016. For more information on the combined company historicals, please refer to note 1, “Basis of Preparation”, in the notes to the financial statements attached to this report.

(3) Nokia standalone historicals are the recasting of Nokia’s historical standalone financial results, reflecting Nokia’s updated segment reporting structure, excluding Alcatel-Lucent. Beginning from the first quarter 2016, Nokia results include those of Alcatel-Lucent on a consolidated basis. Accordingly, Nokia results beginning from the first quarter 2016 are not directly comparable to prior period Nokia standalone results.

SUBSEQUENT EVENTS

Nokia and Samsung expand their intellectual property cross license

On July 13, 2016, Nokia announced that Nokia and Samsung have agreed terms to expand their patent cross license agreement to cover certain additional patent portfolios of both parties. This agreement is in addition to the outcome of the arbitration between the two companies that was announced on February 1, 2016.

The agreement expands access for each company to patented technologies of the other and reinforces Nokia’s leadership in technologies for the programmable world. With this expansion, Nokia expects a positive impact to the net sales of Nokia Technologies starting from the third quarter of 2016.

With this expanded agreement, Nokia Technologies’ total annualized net sales related to patent and brand licensing is expected to grow to a run rate of approximately EUR 950 million by the end of 2016.

NON-IFRS RESULTS

Non-IFRS results provide meaningful supplemental information regarding underlying business performance

In addition to information on our reported IFRS results, we provide certain information on a non-IFRS, or underlying business performance, basis. We believe that our non-IFRS results provide meaningful supplemental information to both management and investors regarding Nokia’s underlying business performance by excluding the below-described items that may not be indicative of Nokia’s business operating results. These non-IFRS financial measures should not be viewed in isolation or as substitutes to the equivalent IFRS measure(s), but should be used in conjunction with the most directly comparable IFRS measure(s) in the reported results.

Non-IFRS results exclude costs related to the Alcatel-Lucent transaction and related integration, goodwill impairment charges, intangible asset amortization and purchase price related items, restructuring and associated charges, and certain other items that may not be indicative of Nokia’s underlying business performance. The non-IFRS exclusions are not allocated to the segments, and hence they are reported only at the Nokia consolidated level.

CEO STATEMENT

Nokia’s second quarter results were largely as expected and reflect solid execution in the midst of a challenging market and the ongoing integration of Alcatel-Lucent. When we announced our first quarter results, I said that we did not expect to see typical seasonal patterns in the first half of the year, and that prediction proved to be correct. Net sales were slightly up sequentially in Q2, while operating margin was slightly down, in part reflecting a meaningful negative impact from one of our major customers in Latin America.

During the quarter we continued to make excellent progress in many areas. We moved rapidly forward with our integration and cost savings efforts; saw robust growth in our Fixed Networks business; announced the acquisition of Gainspeed in order to accelerate our progress with cable operators; closed the acquisition of Withings; reached a licensing deal that will see the Nokia brand return to smartphones and tablets; and more.

I was particularly pleased that the work done in the second quarter to reach an agreement with Samsung on an expanded intellectual property licensing deal came to fruition. After the arbitration results were announced in February, we said that there was still more to come from Samsung and have now delivered on that, with the related financial impact starting in the third quarter.

The decline of our topline remains a concern, and reflects challenging market conditions. While we do not expect those conditions to improve in the near term, we believe we are well-positioned given the scope of our portfolio, focus on operational discipline, strengthening sales execution, and opportunities in the evolution from 4G towards 5G.

In fact, we are already starting to work with customers to help them move to 5G-ready architectures in the core, with a focus on software-defined networking and cloud technologies. As this process takes place, we expect there to be further evolution of 4G radio including more carrier aggregation in order to meet demands for capacity, speed and spectrum utilization. Our AirScale radio platform, which can support different LTE-Advanced Pro (4.5G) technologies and is ‘5G ready,’ is ideally suited to this environment.

We crossed the 95% ownership threshold of Alcatel-Lucent in June, allowing us to move to acquire the remaining shares and reach full ownership of Alcatel-Lucent, which we expect by the end of October. As our successful integration work continues and as we get increased granular visibility into the business, our confidence in our ability to deliver cost savings also increases. As a result, we are now targeting EUR 1.2 billion in total cost savings to be achieved in full year 2018. We have also continued the strategic review of our submarine cable business to determine the best long-term resolution for that business.

While plenty of hard work remains in front of us, we are making good progress and expect to see slight sequential improvement in both net sales and operating margin in our Networks business from the second quarter to the third, followed by significant improvement from the third to the fourth quarter.

Rajeev Suri

President and CEO

NOKIA IN Q2 2016 — NON-IFRS

FINANCIAL DISCUSSION

The following discussion is of Nokia’s results for the second quarter 2016, which comprise the results of Nokia’s businesses — Nokia’s Networks business and Nokia Technologies, as well as Group Common and Other. For more information on the recent changes to our reportable segments, please refer to note 3, “Segment information and eliminations”, in the notes to the financial statements attached to this report. Comparisons are given to the second quarter 2015 and first quarter 2016 results on a combined company basis, unless otherwise indicated.

This data has been prepared to reflect the financial results of the continuing operations of Nokia as if the new financial reporting structure had been in operation for the full year 2015. Certain accounting policy alignments, adjustments and reclassifications have been necessary, and these are explained in the “Basis of preparation” section of the stock exchange release published on April 22, 2016. These adjustments include also reallocation of items of costs and expenses based on their nature and changes to the definition of the line items in the combined company accounting policies, which affect also numbers presented in these interim financial statements for 2015. For more information on the combined company historicals, please refer to note 1, “Basis of Preparation”, in the notes to the financial statements attached to this report.

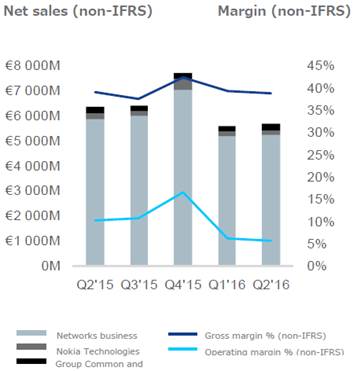

Non-IFRS Net sales

Nokia non-IFRS net sales decreased 11% year-on-year and increased 1% sequentially. On a constant currency basis, Nokia non-IFRS net sales would have decreased 9% year-on-year and increased 2% sequentially.

Year-on-year discussion

The year-on-year decrease in Nokia non-IFRS net sales in the second quarter 2016 was primarily due to Nokia’s Networks business.

Sequential discussion

The sequential increase in Nokia non-IFRS net sales in the second quarter 2016 was primarily due to Nokia’s Networks business and Group Common and Other.

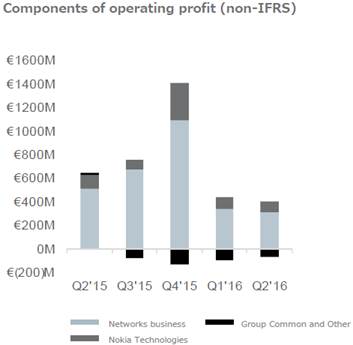

Non-IFRS Operating profit

Year-on-year discussion

Nokia non-IFRS operating profit decreased primarily due to lower non-IFRS gross profit and a net negative fluctuation in non-IFRS other income and expenses, partially offset by lower non-IFRS research and development (“R&D”) expenses and non-IFRS selling, general and administrative (“SG&A”) expenses.

The decrease in non-IFRS gross profit was primarily due to Nokia’s Networks business and, to a lesser extent, Nokia Technologies, partially offset by Group Common and Other. In Q2 2016, non-IFRS gross profit was adversely affected by a customer in Latin America undergoing judicial recovery, as revenue was deferred while the related costs of sale were expensed as incurred.

The decrease in non-IFRS R&D expenses was primarily due to Nokia’s Networks business and, to a lesser extent, Nokia Technologies and Group Common and Other.

The decrease in non-IFRS SG&A expenses was primarily due to Nokia’s Networks business and, to a lesser extent, Group Common and Other, partially offset by Nokia Technologies.

Nokia non-IFRS other income and expenses was an expense of EUR 41 million in the second quarter 2016, compared to an income of EUR 74 million in the year-ago quarter. On a year-on-year basis, the change was primarily due to the absence of realized gains and losses related to certain of Nokia’s investments made through its venture funds. In Q2 2016, non-IFRS other income and expenses were adversely affected by a customer in Latin America undergoing judicial recovery, as certain provisions were recorded due to the risk of asset impairment.

Sequential discussion

Nokia non-IFRS operating profit decreased primarily due to a net negative fluctuation in non-IFRS other income and expenses and higher non-IFRS SG&A expenses, partially offset by lower non-IFRS R&D expenses.

The slight decrease in non-IFRS gross profit was primarily due to Nokia’s Networks business, partially offset by Group Common and Other. In Q2 2016, non-IFRS gross profit was adversely affected by a customer in Latin

America undergoing judicial recovery, as revenue was deferred while the related costs of sale were expensed as incurred.

The decrease in non-IFRS R&D expenses was primarily due to Nokia’s Networks business.

The increase in non-IFRS SG&A expenses was primarily due to Nokia’s Networks business and Nokia Technologies.

Nokia non-IFRS other income and expenses was an expense of EUR 41 million in the second quarter 2016, compared to an expense of EUR 15 million in the first quarter 2016. On a sequential basis, the change was primarily due to Nokia’s Networks business, as well as the absence of realized gains and losses related to certain of Nokia’s investments made through its venture funds. In Q2 2016, non-IFRS other income and expenses were adversely affected by a customer in Latin America undergoing judicial recovery, as certain provisions were recorded due to the risk of asset impairment.

NOKIA IN Q2 2016 — REPORTED

FINANCIAL DISCUSSION

Net sales

Nokia net sales increased 91% year-on-year, compared to Nokia standalone net sales, and increased 2% sequentially. On a constant currency basis, Nokia net sales would have increased 93% year-on-year, compared to Nokia standalone net sales, and 2% sequentially.

Year-on-year discussion

The year-on-year increase in Nokia net sales in the second quarter 2016, compared to Nokia standalone net sales, was primarily due to growth in Nokia’s Networks business and Group Common and Other, primarily related to the acquisition of Alcatel-Lucent, partially offset by non-IFRS exclusions.

Sequential discussion

The sequential increase in Nokia net sales in the second quarter 2016 was primarily due to growth in Nokia’s Networks business and Group Common and Other, as well as reduced negative impact related to purchase price allocation adjustment related to the reduced valuation of deferred revenue that existed on Alcatel-Lucent’s balance sheet at the time of the acquisition.

Operating profit

Year-on-year discussion

In the second quarter 2016, Nokia generated an operating loss, compared to a Nokia standalone operating profit in the year-ago period. The change was primarily due to restructuring and associated charges and other net negative fluctuations in other income and expenses, higher R&D expenses and higher SG&A expenses, partially offset by higher gross profit, all of which related primarily to the acquisition of Alcatel-Lucent.

The increase in gross profit was primarily due to Nokia’s Networks business and, to a lesser extent, Group Common and Other, partially offset by non-IFRS exclusions related to deferred revenue and to a lesser extent, the absence of a benefit recorded in the year-ago quarter, which related to a correction of items previously reported as cost of sales and reductions to accounts receivable. In Q2 2016, gross profit was adversely affected by a customer in Latin America undergoing judicial recovery, as revenue was deferred while the related costs of sale were expensed as incurred.

The increase in R&D expenses was primarily due to Nokia’s Networks business, non-IFRS exclusions related to amortization of intangible assets and, to a lesser extent, Group Common and Other.

The increase in SG&A expenses was primarily due to Nokia’s Networks business, non-IFRS exclusions related to amortization of intangible assets, as well as transaction and integration related costs and, to a lesser extent, Group Common and Other and Nokia Technologies.

Nokia’s other income and expenses was an expense of EUR 643 million in the second quarter 2016, compared to an income of EUR 114 million in the year-ago period. The change was primarily related to non-IFRS exclusions attributable to higher restructuring and associated charges and, to a lesser extent, the absence of realized gains and losses related to certain of Nokia’s investments made through its venture funds. In Q2 2016, other income and expenses were adversely affected by a customer in Latin America undergoing judicial recovery, as certain provisions were recorded due to the risk of asset impairment.

Sequential discussion

Nokia operating profit decreased primarily due to restructuring and associated charges, partially offset by higher gross profit and, to a lesser extent, lower SG&A and R&D expenses.

The increase in gross profit was primarily due to lower non-IFRS exclusions related to the absence of an inventory revaluation as part of the Alcatel-Lucent purchase accounting, which negatively affected the first quarter 2016. In Q2 2016, gross profit was adversely affected by a customer in Latin America undergoing judicial recovery, as revenue was deferred while the related costs of sale were expensed as incurred.

The decrease in R&D expenses was primarily due to Nokia’s Networks business.

The decrease in SG&A expenses was primarily due to lower non-IFRS exclusions related to transaction and integration related costs.

Nokia’s other income and expenses was an expense of EUR 643 million in the second quarter 2016, compared to an expense of EUR 40 million in the first quarter 2016. The increase was primarily related to non-IFRS exclusions attributable to recognition of restructuring and associated charges related to the overall cost savings program. In Q2 2016, other income and expenses were adversely affected by a customer in Latin America undergoing judicial recovery, as certain provisions were recorded due to the risk of asset impairment.

Descriptions of non-IFRS exclusions in Q2 2016

Non-IFRS exclusions consist of costs related to the Alcatel-Lucent transaction and related integration, goodwill impairment charges, intangible asset amortization and purchase price related items, restructuring and associated charges, and certain other items that may not be indicative of Nokia’s underlying business performance. For additional details, please refer to note 2, “Non-IFRS to reported reconciliation”, in the notes to the financial statements attached to this report.

|

|

|

|

|

Nokia |

|

YoY |

|

|

|

QoQ |

|

|

EUR million |

|

Q2’16 |

|

Q2’15 |

|

change |

|

Q1’16 |

|

change |

|

|

Net sales |

|

(93 |

) |

0 |

|

|

|

(104 |

) |

(11 |

)% |

|

Gross profit |

|

(174 |

) |

37 |

|

|

|

(651 |

) |

(73 |

)% |

|

R&D |

|

(162 |

) |

(13 |

) |

|

|

(156 |

) |

4 |

% |

|

SG&A |

|

(154 |

) |

(27 |

) |

|

|

(224 |

) |

(31 |

)% |

|

Other income and expenses |

|

(602 |

) |

0 |

|

|

|

(25 |

) |

|

|

|

Operating profit/(loss) |

|

(1 092 |

) |

(3 |

) |

|

|

(1 057 |

) |

3 |

% |

|

Financial income and expenses, net |

|

(3 |

) |

0 |

|

|

|

(36 |

) |

(92 |

)% |

|

Taxes |

|

200 |

|

5 |

|

|

|

341 |

|

(41 |

)% |

|

(Loss)/Profit |

|

(896 |

) |

2 |

|

|

|

(752 |

) |

19 |

% |

|

(Loss)/Profit attributable to the shareholders of the parent |

|

(862 |

) |

2 |

|

|

|

(680 |

) |

27 |

% |

|

Non-controlling interests |

|

(34 |

) |

0 |

|

|

|

(72 |

) |

(53 |

)% |

(1)Nokia standalone historicals are the recasting of Nokia’s historical standalone financial results, reflecting Nokia’s updated segment reporting structure, excluding Alcatel-Lucent. Beginning from the first quarter 2016, Nokia results include those of Alcatel-Lucent on a consolidated basis. Accordingly, Nokia results beginning from the first quarter 2016 are not directly comparable to prior period Nokia standalone results.

Net sales

In the second quarter 2016, non-IFRS exclusions in net sales amounted to EUR 93 million, and related to purchase price allocation adjustment related to the reduced valuation of deferred revenue that existed on Alcatel-Lucent’s balance sheet at the time of the acquisition.

Operating profit

In the second quarter 2016, non-IFRS exclusions in operating profit amounted to EUR 1 092 million, and were attributable to non-IFRS exclusions that negatively affected gross profit, R&D, SG&A and other income and expenses as follows:

In the second quarter 2016, non-IFRS exclusions in gross profit amounted to EUR 174 million, and primarily related to the deferred revenue and, to a lesser extent, product portfolio integration related costs resulting from the acquisition of Alcatel-Lucent.

In the second quarter 2016, non-IFRS exclusions in R&D expenses amounted to EUR 162 million, and primarily related to the amortization of intangible assets resulting from the acquisition of Alcatel-Lucent.

In the second quarter 2016, non-IFRS exclusions in SG&A expenses amounted to EUR 154 million, and primarily related to the amortization of intangible assets resulting from the acquisition of Alcatel-Lucent, as well as transaction and integration related costs.

In the second quarter 2016, non-IFRS exclusions in other income and expenses amounted to EUR 602 million, and primarily related to EUR 596 million of restructuring and associated charges for Nokia’s cost reduction and efficiency improvement initiatives.

Cost savings program

The following table summarizes the financial information related to our cost savings program, as of the end of the second quarter 2016. Balances related to previous Nokia and Alcatel-Lucent restructuring and cost savings programs have been included as part of this overall cost savings program.

|

In EUR million, approximately |

|

Q2’16 |

|

|

Opening balance of restructuring and associated liabilities |

|

450 |

|

|

+ Charges in the quarter |

|

600 |

|

|

- Cash outflows in the quarter |

|

80 |

|

|

= Ending balance of restructuring and associated liabilities |

|

970 |

|

|

of which restructuring provisions |

|

850 |

|

|

of which other associated liabilities |

|

120 |

|

|

|

|

|

|

|

Total expected restructuring and associated charges — updated program |

|

1 200 |

|

|

- Cumulative recorded — updated program |

|

600 |

|

|

= Charges remaining to be recorded — updated program |

|

600 |

|

|

|

|

|

|

|

Total expected restructuring and associated cash outflows |

|

1 650 |

|

|

- Cumulative recorded |

|

80 |

|

|

= Cash outflows remaining to be recorded |

|

1 570 |

|

The Q2 2016 opening balance of restructuring and associated liabilities of approximately EUR 450 million relates to previous Nokia and Alcatel-Lucent restructuring and cost-savings programs, and represents expected cash outflows which have been provisioned for but not yet paid out related to these programs. The approximately EUR 450 million of restructuring and associated liabilities consists of approximately EUR 380 million of restructuring provisions and approximately EUR 70 million of other related liabilities.

OUTLOOK

|

|

|

Metric |

|

Guidance |

|

Commentary |

|

Nokia |

|

Annual cost savings for Nokia, excluding Nokia Technologies |

|

Approximately EUR 1.2 billion of total annual cost savings to be achieved in full year 2018 (update) |

|

Compared to the combined non-IFRS operating costs of Nokia and Alcatel-Lucent for full year 2015, excluding Nokia Technologies.

Under this expanded cost savings program, restructuring and associated charges are expected to total approximately EUR 1.2 billion, of which approximately EUR 600 million was recorded in Q2 2016.

Related restructuring and associated cash outflows are expected to total approximately EUR 1.65 billion, which includes the |

|

|

|

|

|

|

|

approximately EUR 450 million balance of restructuring and associated cash outflows that were provisioned for but not yet paid as of the beginning of Q2 2016, related to previous Nokia and Alcatel-Lucent restructuring and cost savings programs.

In addition to the above amounts, note that Nokia’s overall charges and cash outflows will also include amounts related to network equipment swaps. The charges related to network equipment swaps will be recorded as non-IFRS exclusions, and therefore will not affect Nokia’s non-IFRS operating profit.

This is an update to the earlier outlook for above EUR 900 million of net operating cost synergies to be achieved in full year 2018. |

|

|

|

|

|

|

|

|

|

|

|

FY16 Non-IFRS financial income and expense |

|

Expense of approximately EUR 300 million |

|

Primarily includes net interest expenses related to interest-bearing liabilities, interest costs related to the defined benefit pension and other post-employment benefit plans, as well as the impact from changes in foreign exchange rates on certain balance sheet items. This outlook may vary subject to changes in the above listed items. |

|

|

|

|

|

|

|

|

|

|

|

FY16 Non-IFRS tax rate |

|

Above 40% for full year 2016 |

|

The increase in the non-IFRS tax rate for the combined company, compared to Nokia on a standalone basis, is primarily attributable to unfavorable changes in the regional profit mix as a result of the acquisition of Alcatel-Lucent. This outlook is for full year 2016; the quarterly non-IFRS tax rate is expected to be subject to volatility, primarily influenced by fluctuations in profits made by Nokia in different tax jurisdictions. Nokia expects its effective long-term non-IFRS tax rate to be clearly below the full year 2016 level, and intends to provide further commentary later in 2016. |

|

|

|

|

|

|

|

|

|

|

|

FY16 Cash outflows related to taxes |

|

Approximately EUR 400 million |

|

May vary due to profit levels in different jurisdictions and the amount of licensing income subject to withholding tax. |

|

|

|

|

|

|

|

|

|

|

|

FY16 Capital expenditures |

|

Approximately EUR 650 million |

|

Primarily attributable Nokia’s Networks business. |

|

|

|

|

|

|

|

|

|

Nokia’s Networks business |

|

FY16 net sales |

|

Decline YoY |

|

Combined company net sales and operating margin are expected to be influenced by factors including: |

|

|

FY16 operating margin |

|

7-9% |

|

· A flattish capital expenditure environment in 2016 for our overall addressable market; · A declining wireless infrastructure market in 2016; · Significant focus on the integration of Alcatel-Lucent, particularly in the first half of 2016; · Slight QoQ net sales growth and operating margin expansion in Q3 2016; · Significant QoQ net sales growth and operating margin expansion in Q4 2016; · Competitive industry dynamics; · Product and regional mix; · The timing of major network deployments; and · Execution of synergy plans.

This is an update to the earlier FY16 operating margin guidance of above 7%. |

|

Nokia Technologies |

|

FY16 Net sales |

|

Not provided |

|

Due to risks and uncertainties in determining the timing and value of significant licensing agreements, Nokia believes it is not appropriate to provide an annual outlook for fiscal year 2016. Nokia expects annualized net sales related to patent and brand licensing to grow to a run rate of approximately EUR 950 million by the end of 2016. License agreements which currently contribute approximately EUR 150 million to the annualized net sales run rate are set to expire before the end of 2016. If we do not renew these license agreements, nor sign any new licensing agreements, the annualized net sales run rate would be approximately EUR 800 million in early 2017. Furthermore, the contribution of the Withings acquisition to Nokia Technologies net sales is expected to be approximately EUR 50 million in the second half of 2016, with strong Q4 seasonality. The contribution of the acquisition to Nokia Technologies operating profit is expected to be slightly negative for the second half of 2016. |

RISKS AND FORWARD-LOOKING STATEMENTS

It should be noted that Nokia and its businesses are exposed to various risks and uncertainties and certain statements herein that are not historical facts are forward-looking statements, including, without limitation, those regarding: A) our ability to integrate Alcatel Lucent into our operations and achieve the targeted business plans and benefits, including targeted synergies in relation to the acquisition of Alcatel Lucent announced on April 15, 2015 and closed in early 2016; B) our ability to squeeze out the remaining Alcatel Lucent shareholders in a timely manner or at all to achieve full ownership of Alcatel Lucent; C) expectations, plans or benefits related to our strategies and growth management; D) expectations, plans or benefits related to future performance of our businesses; E) expectations, plans or benefits related to changes in our management and other leadership, operational structure and operating model, including the expected characteristics, business, organizational structure, management and operations following the acquisition of Alcatel Lucent; F) expectations regarding market developments, general economic conditions and structural changes; G) expectations and targets regarding financial performance, results, operating expenses, taxes, currency exchange rates, hedging, cost savings and competitiveness, as well as results of operations including targeted synergies and those related to market share, prices, net sales, income and margins; H) timing of the deliveries of our products and services; I) expectations and targets regarding collaboration and partnering arrangements, as well as our expected customer reach; J) outcome of pending and threatened litigation, arbitration, disputes, regulatory proceedings or investigations by authorities; K) expectations regarding restructurings, investments, uses of proceeds from transactions, acquisitions and divestments and our ability to achieve the financial and operational targets set in connection with any such restructurings, investments, divestments and acquisitions; and L) statements preceded by or including “believe,” “expect,” “anticipate,” “foresee,” “sees,” “target,” “estimate,” “designed,” “aim,” “plans,” “intends,” “focus,” “continue,” “project,” “should,” “will” or similar expressions. These statements are based on the management’s best assumptions and beliefs in light of the information currently available to it. Because they involve risks and uncertainties, actual results may differ materially from the results that we currently expect. Factors, including risks and uncertainties, that could cause such differences include, but are not limited to: 1) our ability to execute our strategy, sustain or improve the operational and financial performance of our business or correctly identify or successfully pursue business opportunities or growth; 2) our ability to achieve the anticipated business and operational benefits and synergies from the Alcatel Lucent transaction, including our ability to integrate Alcatel Lucent into our operations and within the timeframe targeted, and our ability to implement our organization and operational

structure efficiently; 3) our ability to complete the purchases of the remaining outstanding Alcatel Lucent securities and realize the benefits of the public exchange offer for all outstanding Alcatel Lucent securities; 4) our dependence on general economic and market conditions and other developments in the economies where we operate; 5) our dependence on the development of the industries in which we operate, including the cyclicality and variability of the telecommunications industry; 6) our exposure to regulatory, political or other developments in various countries or regions, including emerging markets and the associated risks in relation to tax matters and exchange controls, among others; 7) our ability to effectively and profitably compete and invest in new competitive high-quality products, services, upgrades and technologies and bring them to market in a timely manner; 8) our dependence on a limited number of customers and large multi-year agreements; 9) Nokia Technologies’ ability to maintain and establish new sources of patent licensing income and IPR-related revenues, particularly in the smartphone market; 10) our dependence on IPR technologies, including those that we have developed and those that are licensed to us, and the risk of associated IPR-related legal claims, licensing costs and restrictions on use; 11) our exposure to direct and indirect regulation, including economic or trade policies, and the reliability of our governance, internal controls and compliance processes to prevent regulatory penalties; 12) our reliance on third-party solutions for data storage and the distribution of products and services, which expose us to risks relating to security, regulation and cybersecurity breaches; 13) Nokia Technologies’ ability to generate net sales and profitability through licensing of the Nokia brand, the development and sales of products and services, as well as other business ventures which may not materialize as planned; 14) our exposure to legislative frameworks and jurisdictions that regulate fraud, economic trade sanctions and policies, and Alcatel Lucent’s previous and current involvement in anti-corruption allegations; 15) the potential complex tax issues, tax disputes and tax obligations we may face in various jurisdictions, including the risk of obligations to pay additional taxes; 16) our actual or anticipated performance, among other factors, which could reduce our ability to utilize deferred tax assets; 17) our ability to retain, motivate, develop and recruit appropriately skilled employees; 18) our ability to manage our manufacturing, service creation, delivery, logistics and supply chain processes, and the risk related to our geographically concentrated production sites; 19) the impact of unfavorable outcome of litigation, arbitration, agreement-related disputes or allegations of product liability associated with our businesses; 20) exchange rate fluctuations, as well as hedging activities; 21) inefficiencies, breaches, malfunctions or disruptions of information technology systems; 22) our ability to optimize our capital structure as planned and re-establish our investment grade credit rating or otherwise improve our credit ratings; 23) uncertainty related to the amount of dividends and equity return we are able to distribute to shareholders for each financial period; 24) our ability to achieve targeted benefits from or successfully implement planned transactions, as well as the liabilities related thereto; 25) our involvement in joint ventures and jointly-managed companies; 26) performance failures by our partners or failure to agree to partnering arrangements with third parties; 27) our ability to manage and improve our financial and operating performance, cost savings, competitiveness and synergy benefits after the acquisition of Alcatel Lucent; 28) adverse developments with respect to customer financing or extended payment terms we provide to customers; 29) the carrying amount of our goodwill may not be recoverable; 30) risks related to undersea infrastructure; 31) unexpected liabilities with respect to pension plans, insurance matters and employees; and 32) unexpected liabilities or issues with respect to the acquisition of Alcatel Lucent, including pension, postretirement, health and life insurance and other employee liabilities or higher than expected transaction costs as well as the risk factors specified on pages 69 to 87 of our annual report on Form 20-F filed on April 1, 2016 under “Operating and financial review and prospects—Risk factors”, as well as in Nokia’s other filings with the U.S. Securities and Exchange Commission. Other unknown or unpredictable factors or underlying assumptions subsequently proven to be incorrect could cause actual results to differ materially from those in the forward-looking statements. We do not undertake any obligation to publicly update or revise forward-looking

statements, whether as a result of new information, future events or otherwise, except to the extent legally required.

The financial statements were authorized for issue by management on August 3, 2016.

Media and Investor Contacts:

Corporate Communications, tel. +358 10 448 4900 email: press.services@nokia.com

Investor Relations, tel. +358 4080 3 4080 email: investor.relations@nokia.com

· Nokia plans to publish its third quarter 2016 results on October 27, 2016.

· Nokia plans to hold its Capital Markets Day in Barcelona on November 15, 2016.

![]()

Financial Report for Q2 and Half Year 2016

Solid financial performance and raised cost savings target

Financial highlights

· Non-IFRS net sales in Q2 2016 of EUR 5.7 billion (reported: EUR 5.6 billion). In the year-ago quarter, non-IFRS net sales would have been EUR 6.4 billion on a comparable combined company basis (reported: EUR 2.9 billion on a Nokia stand-alone basis).

· Non-IFRS diluted EPS in Q2 2016 of EUR 0.03 (reported: EUR negative 0.12).

· Raised annual cost savings target to approximately EUR 1.2 billion of total annual cost savings to be achieved in full year 2018, compared to the combined non-IFRS operating costs of Nokia and Alcatel-Lucent for full year 2015, excluding Nokia Technologies. Related to this, Nokia recorded approximately EUR 600 million of restructuring and associated charges in the second quarter 2016.

Nokia’s Networks business

· 11% year-on-year net sales decrease in Q2 2016. Consistent with our outlook for the wireless infrastructure market, net sales were weak in Mobile Networks within Ultra Broadband Networks, and accounted for approximately 80% of the overall decrease in Nokia’s Networks business. IP Networks and Applications also contributed to the decrease. This was partially offset by strong growth in Fixed Networks within Ultra Broadband Networks.

· In Q2 2016, solid gross margin of 37.4% and operating margin of 6.0% were adversely affected by a customer in Latin America undergoing judicial recovery. Excluding this, gross margin would have been approximately 38% and operating margin would have been nearly 7%.

Nokia Technologies

· 11% year-on-year net sales decrease in Q2 2016. Excluding the impact of non-recurring items that benefitted the year-ago quarter, Nokia Technologies net sales would have grown by approximately 10% year-on-year, primarily due to higher intellectual property licensing income from existing licensees.

· Announced an expansion of the patent cross license agreement with Samsung on July 13, 2016 to cover certain additional patent portfolios, reinforcing Nokia’s leadership in technologies for the programmable world. The expansion of the agreement occurred subsequent to the end of the second quarter 2016, and therefore did not impact the second quarter of 2016 financials. Instead, the expanded agreement will have a positive impact to Nokia Technologies starting from the third quarter of 2016. Nokia expects total annualized net sales related to patent and brand licensing to grow to a run rate of approximately EUR 950 million by the end of 2016.

![]()

August 4, 2016

Q2 and January-June 2016 non-IFRS results. See note 1 to the interim financial statements for further details (1),(2)

|

|

|

|

|

Combined |

|

YoY |

|

|

|

QoQ |

|

Q1- |

|

Combined |

|

YoY |

|

|

EUR million |

|

Q2’16 |

|

Q2’15 |

|

change |

|

Q1’16 |

|

change |

|

Q2’16 |

|

Q1-Q2’15 |

|

change |

|

|

Net sales — constant currency (non-IFRS) |

|

|

|

|

|

(9 |

)% |

|

|

2 |

% |

|

|

|

|

(9 |

)% |

|

Net sales (non-IFRS) |

|

5 676 |

|

6 363 |

|

(11 |

)% |

5 603 |

|

1 |

% |

11 279 |

|

12 492 |

|

(10 |

)% |

|

Nokia’s Networks business |

|

5 228 |

|

5 895 |

|

(11 |

)% |

5 181 |

|

1 |

% |

10 409 |

|

11 557 |

|

(10 |

)% |

|

Ultra Broadband Networks |

|

3 807 |

|

4 303 |

|

(12 |

)% |

3 729 |

|

2 |

% |

7 535 |

|

8 530 |

|

(12 |

)% |

|

IP Networks and Applications |

|

1 421 |

|

1 593 |

|

(11 |

)% |

1 452 |

|

(2 |

)% |

2 873 |

|

3 027 |

|

(5 |

)% |

|

Nokia Technologies |

|

194 |

|

219 |

|

(11 |

)% |

198 |

|

(2 |

)% |

391 |

|

492 |

|

(21 |

)% |

|

Group Common and Other |

|

271 |

|

254 |

|

7 |

% |

236 |

|

15 |

% |

507 |

|

457 |

|

11 |

% |

|

Gross profit (non-IFRS) |

|

2 202 |

|

2 495 |

|

(12 |

)% |

2 205 |

|

0 |

% |

4 407 |

|

4 759 |

|

(7 |

)% |

|

Gross margin % (non-IFRS) |

|

38.8 |

% |

39.2 |

% |

(40 |

)bps |

39.4 |

% |

(60 |

)bps |

39.1 |

% |

38.1 |

% |

100 |

bps |

|

Operating profit (non-IFRS) |

|

332 |

|

649 |

|

(49 |

)% |

345 |

|

(4 |

)% |

677 |

|

925 |

|

(27 |

)% |

|

Nokia’s Networks business |

|

312 |

|

511 |

|

(39 |

)% |

337 |

|

(7 |

)% |

649 |

|

720 |

|

(10 |

)% |

|

Ultra Broadband Networks |

|

228 |

|

308 |

|

(26 |

)% |

234 |

|

(3 |

)% |

462 |

|

476 |

|

(3 |

)% |

|

IP Networks and Applications |

|

84 |

|

203 |

|

(59 |

)% |

103 |

|

(18 |

)% |

187 |

|

244 |

|

(23 |

)% |

|

Nokia Technologies |

|

89 |

|

120 |

|

(26 |

)% |

106 |

|

(16 |

)% |

195 |

|

297 |

|

(34 |

)% |

|

Group Common and Other |

|

(68 |

) |

18 |

|

|

|

(99 |

) |

|

|

(167 |

) |

(92 |

) |

|

|

|

Operating margin % (non-IFRS) |

|

5.8 |

% |

10.2 |

% |

(440 |

)bps |

6.2 |

% |

(40 |

)bps |

6.0 |

% |

7.4 |

% |

(140 |

)bps |

Q2 and January-June 2016 reported results, unless otherwise specified. See note 1 to the interim financial statements for further details(1),(3)

|

EUR million (except for |

|

|

|

Nokia |

|

YoY |

|

|

|

QoQ |

|

Q1- |

|

Nokia |

|

YoY |

|

|

EPS in EUR) |

|

Q2’16 |

|

Q2’15 |

|

change |

|

Q1’16 |

|

change |

|

Q2’16 |

|

Q1-Q2’15 |

|

change |

|

|

Net Sales - constant currency |

|

|

|

|

|

93 |

% |

|

|

2 |

% |

|

|

|

|

89 |

% |

|

Net sales |

|

5 583 |

|

2 919 |

|

91 |

% |

5 499 |

|

2 |

% |

11 082 |

|

5 854 |

|

89 |

% |

|

Nokia’s Networks business |

|

5 228 |

|

2 729 |

|

92 |

% |

5 181 |

|

1 |

% |

10 409 |

|

5 400 |

|

93 |

% |

|

Ultra Broadband Networks |

|

3 807 |

|

2 440 |

|

56 |

% |

3 729 |

|

2 |

% |

7 535 |

|

4 795 |

|

57 |

% |

|

IP Networks and Applications |

|

1 421 |

|

289 |

|

392 |

% |

1 452 |

|

(2 |

)% |

2 873 |

|

605 |

|

375 |

% |

|

Nokia Technologies |

|

194 |

|

194 |

|

0 |

% |

198 |

|

(2 |

)% |

391 |

|

461 |

|

(15 |

)% |

|

Group Common and Other |

|

271 |

|

0 |

|

|

|

236 |

|

15 |

% |

507 |

|

0 |

|

|

|

|

Non-IFRS exclusions |

|

(93 |

) |

0 |

|

|

|

(104 |

) |

|

|

(197 |

) |

0 |

|

|

|

|

Gross profit |

|

2 028 |

|

1 343 |

|

51 |

% |

1 554 |

|

31 |

% |

3 582 |

|

2 527 |

|

42 |

% |

|

Gross margin % |

|

36.3 |

% |

46.0 |

% |

(970 |

)bps |

28.3 |

% |

800 |

bps |

32.3 |

% |

43.2 |

% |

(1 090 |

)bps |

|

Operating (loss)/profit |

|

(760 |

) |

493 |

|

|

|

(712 |

) |

|

|

(1 472 |

) |

721 |

|

|

|

|

Nokia’s Networks business |

|

312 |

|

331 |

|

(6 |

)% |

337 |

|

(7 |

)% |

649 |

|

442 |

|

47 |

% |

|

Ultra Broadband Networks |

|

228 |

|

312 |

|

(27 |

)% |

234 |

|

(3 |

)% |

462 |

|

445 |

|

4 |

% |

|

IP Networks and Applications |

|

84 |

|

19 |

|

342 |

% |

103 |

|

(18 |

)% |

187 |

|

(3 |

) |

|

|

|

Nokia Technologies |

|

89 |

|

108 |

|

(18 |

)% |

106 |

|

(16 |

)% |

195 |

|

294 |

|

(34 |

)% |

|

Group Common and Other |

|

(68 |

) |

57 |

|

|

|

(99 |

) |

|

|

(167 |

) |

8 |

|

|

|

|

Non-IFRS exclusions |

|

(1 092 |

) |

(3 |

) |

|

|

(1 057 |

) |

3 |

% |

(2 149 |

) |

(24 |

) |

|

|

|

Operating margin % |

|

(13.6 |

)% |

16.9 |

% |

(3 050 |

)bps |

(12.9 |

)% |

(70 |

)bps |

(13.3 |

)% |

12.3 |

% |

(2 560 |

)bps |

|

Profit (non-IFRS) |

|

171 |

|

336 |

|

(49 |

)% |

139 |

|

23 |

% |

310 |

|

519 |

|

(40 |

)% |

|

(Loss)/profit |

|

(726 |

) |

338 |

|

|

|

(613 |

) |

18 |

% |

(1 338 |

) |

507 |

|

|

|

|

EPS, diluted (non-IFRS) |

|

0.03 |

|

0.09 |

|

(67 |

)% |

0.03 |

|

0 |

% |

0.06 |

|

0.14 |

|

(57 |

)% |

|

EPS, diluted |

|

(0.12 |

) |

0.09 |

|

|

|

(0.09 |

) |

|

|

(0.21 |

) |

0.13 |

|

|

|

|

Net cash and other liquid assets |

|

7 077 |

|

3 830 |

|

85 |

% |

8 246 |

|

(14 |

)% |

7 077 |

|

3 830 |

|

85 |

% |

(1)Results are as reported unless otherwise specified. The results information in this report is unaudited. Non-IFRS results exclude costs related to the Alcatel-Lucent transaction and related integration, goodwill impairment charges, intangible asset amortization and purchase price related items, restructuring and associated charges, and certain other items that may not be indicative of Nokia’s underlying business performance. For details, please refer to the Non-IFRS Exclusions section included in discussions of both the quarterly and year to date performance and note 2, “Non-IFRS to reported reconciliation”, in the notes to the financial statements attached to this report. A reconciliation of the Q2 2015 non-IFRS combined company results to the reported results can be found in the “Nokia provides recast segment results for 2015 reflecting new financial reporting structure” stock exchange release published on April 22, 2016. Change in net sales at constant currency excludes the impact of changes in exchange rates in comparison to Euro, our reporting currency. For more information on currency exposures, please refer to note 1, “Basis of Preparation”, in the notes to the financial statements attached to this report.

(2)Combined company historicals reflect Nokia’s new operating and financial reporting structure, including Alcatel-Lucent, and are presented as additional information as described in the stock exchange release published on April 22, 2016. For more information on the combined company historicals, please refer to note 1, “Basis of Preparation”, in the notes to the financial statements attached to this report.

(3)Nokia standalone historicals are the recasting of Nokia’s historical standalone financial results, reflecting Nokia’s updated segment reporting structure, excluding Alcatel-Lucent. Beginning from the first quarter 2016, Nokia results include those of Alcatel-Lucent on a consolidated basis. Accordingly, Nokia results beginning from the first quarter 2016 are not directly comparable to prior period Nokia standalone results.

Subsequent events

Nokia and Samsung expand their intellectual property cross license

On July 13, 2016, Nokia announced that Nokia and Samsung have agreed terms to expand their patent cross license agreement to cover certain additional patent portfolios of both parties. This agreement is in addition to the outcome of the arbitration between the two companies that was announced on February 1, 2016.

The agreement expands access for each company to patented technologies of the other and reinforces Nokia’s leadership in technologies for the programmable world. With this expansion, Nokia expects a positive impact to the net sales of Nokia Technologies starting from the third quarter of 2016.

With this expanded agreement, Nokia Technologies’ total annualized net sales related to patent and brand licensing is expected to grow to a run rate of approximately EUR 950 million by the end of 2016.

Non-IFRS results

Non-IFRS results provide meaningful supplemental information regarding underlying business performance

In addition to information on our reported IFRS results, we provide certain information on a non-IFRS, or underlying business performance, basis. We believe that our non-IFRS results provide meaningful supplemental information to both management and investors regarding Nokia’s underlying business performance by excluding the below-described items that may not be indicative of Nokia’s business operating results. These non-IFRS financial measures should not be viewed in isolation or as substitutes to the equivalent IFRS measure(s), but should be used in conjunction with the most directly comparable IFRS measure(s) in the reported results.

Non-IFRS results exclude costs related to the Alcatel-Lucent transaction and related integration, goodwill impairment charges, intangible asset amortization and purchase price related items, restructuring and associated charges, and certain other items that may not be indicative of Nokia’s underlying business performance. The non-IFRS exclusions are not allocated to the segments, and hence they are reported only at the Nokia consolidated level.

CEO statement

Nokia’s second quarter results were largely as expected and reflect solid execution in the midst of a challenging market and the ongoing integration of Alcatel-Lucent. When we announced our first quarter results, I said that we did not expect to see typical seasonal patterns in the first half of the year, and that prediction proved to be correct. Net sales were slightly up sequentially in Q2, while operating margin was slightly down, in part reflecting a meaningful negative impact from one of our major customers in Latin America.

During the quarter we continued to make excellent progress in many areas. We moved rapidly forward with our integration and cost savings efforts; saw robust growth in our Fixed Networks business; announced the acquisition of Gainspeed in order to accelerate our progress with cable operators; closed the acquisition of Withings; reached a licensing deal that will see the Nokia brand return to smartphones and tablets; and more.

I was particularly pleased that the work done in the second quarter to reach an agreement with Samsung on an expanded intellectual property licensing deal came to fruition. After the arbitration results were announced in February, we said that there was still more to come from Samsung and have now delivered on that, with the related financial impact starting in the third quarter.

The decline of our topline remains a concern, and reflects challenging market conditions. While we do not expect those conditions to improve in the near term, we believe we are well-positioned given the scope of our portfolio, focus on operational discipline, strengthening sales execution, and opportunities in the evolution from 4G towards 5G.

In fact, we are already starting to work with customers to help them move to 5G-ready architectures in the core, with a focus on software-defined networking and cloud technologies. As this process takes place, we expect there to be further evolution of 4G radio including more carrier aggregation in order to meet demands for capacity, speed and spectrum utilization. Our AirScale radio platform, which can support different LTE-Advanced Pro (4.5G) technologies and is ‘5G ready,’ is ideally suited to this environment.

We crossed the 95% ownership threshold of Alcatel-Lucent in June, allowing us to move to acquire the remaining shares and reach full ownership of Alcatel-Lucent, which we expect by the end of October. As our successful integration work continues and as we get increased granular visibility into the business, our confidence in our ability to deliver cost savings also increases. As a result, we are now targeting EUR 1.2 billion in total cost savings to be achieved in full year 2018. We have also

continued the strategic review of our submarine cable business to determine the best long-term resolution for that business.

While plenty of hard work remains in front of us, we are making good progress and expect to see slight sequential improvement in both net sales and operating margin in our Networks business from the second quarter to the third, followed by significant improvement from the third to the fourth quarter.

Rajeev Suri

President and CEO

Nokia in Q2 2016 — Non-IFRS

|

|

|

|

Financial discussion

The following discussion is of Nokia’s results for the second quarter 2016, which comprise the results of Nokia’s businesses — Nokia’s Networks business and Nokia Technologies, as well as Group Common and Other. For more information on the recent changes to our reportable segments, please refer to note 3, “Segment information and eliminations”, in the notes to the financial statements attached to this report. Comparisons are given to the second quarter 2015 and first quarter 2016 results on a combined company basis, unless otherwise indicated.

This data has been prepared to reflect the financial results of the continuing operations of Nokia as if the new financial reporting structure had been in operation for the full year 2015. Certain accounting policy alignments, adjustments and reclassifications have been necessary, and these are explained in the “Basis of preparation” section of the stock exchange release published on April 22, 2016. These adjustments include also reallocation of items of costs and expenses based on their nature and changes to the definition of the line items in the combined company accounting policies, which affect also numbers presented in these interim financial statements for 2015. For more information on the combined company historicals, please refer to note 1, “Basis of Preparation”, in the notes to the financial statements attached to this report.

Non-IFRS Net sales

Nokia non-IFRS net sales decreased 11% year-on-year and increased 1% sequentially. On a constant currency basis, Nokia non-IFRS net sales would have decreased 9% year-on-year and increased 2% sequentially.

Year-on-year discussion

The year-on-year decrease in Nokia non-IFRS net sales in the second quarter 2016 was primarily due to Nokia’s Networks business.

Sequential discussion

The sequential increase in Nokia non-IFRS net sales in the second quarter 2016 was primarily due to Nokia’s Networks business and Group Common and Other.

Non-IFRS Operating profit

Year-on-year discussion

Nokia non-IFRS operating profit decreased primarily due to lower non-IFRS gross profit and a net negative fluctuation in non-IFRS other income and expenses, partially offset by lower non-IFRS research and development (“R&D”) expenses and non-IFRS selling, general and administrative (“SG&A”) expenses.

The decrease in non-IFRS gross profit was primarily due to Nokia’s Networks business and, to a lesser extent, Nokia Technologies, partially offset by Group Common and Other. In Q2 2016, non-IFRS gross profit was adversely affected by a customer in Latin America undergoing judicial recovery, as revenue was deferred while the related costs of sale were expensed as incurred.

The decrease in non-IFRS R&D expenses was primarily due to Nokia’s Networks business and, to a lesser extent, Nokia Technologies and Group Common and Other.

The decrease in non-IFRS SG&A expenses was primarily due to Nokia’s Networks business and, to a lesser extent, Group Common and Other, partially offset by Nokia Technologies.

Nokia non-IFRS other income and expenses was an expense of EUR 41 million in the second quarter 2016, compared to an income of EUR 74 million in the year-ago quarter. On a year-on-year basis, the change was primarily due to the absence of realized gains and losses related to certain of Nokia’s investments made through its venture funds. In Q2 2016, non-IFRS other income and expenses were adversely affected by a customer in Latin America undergoing judicial recovery, as certain provisions were recorded due to the risk of asset impairment.

Sequential discussion

Nokia non-IFRS operating profit decreased primarily due to a net negative fluctuation in non-IFRS other income and expenses and higher non-IFRS SG&A expenses, partially offset by lower non-IFRS R&D expenses.

The slight decrease in non-IFRS gross profit was primarily due to Nokia’s Networks business, partially offset by Group Common and Other. In Q2 2016, non-IFRS gross profit was adversely affected by a customer in Latin America undergoing judicial recovery, as revenue was deferred while the related costs of sale were expensed as incurred.

The decrease in non-IFRS R&D expenses was primarily due to Nokia’s Networks business.

The increase in non-IFRS SG&A expenses was primarily due to Nokia’s Networks business and Nokia Technologies.

Nokia non-IFRS other income and expenses was an expense of EUR 41 million in the second quarter 2016, compared to an expense of EUR 15 million in the first quarter 2016. On a sequential basis, the change was primarily due to Nokia’s Networks business, as well as the absence of realized gains and losses related to certain of Nokia’s investments made through its venture funds. In Q2 2016, non-IFRS other income and expenses were adversely affected by a customer in Latin America undergoing judicial recovery, as certain provisions were recorded due to the risk of asset impairment.

Nokia in Q2 2016 — Reported

|

|

|

|

Financial discussion

Net sales

Nokia net sales increased 91% year-on-year, compared to Nokia standalone net sales, and increased 2% sequentially. On a constant currency basis, Nokia net sales would have increased 93% year-on-year, compared to Nokia standalone net sales, and 2% sequentially.

Year-on-year discussion

The year-on-year increase in Nokia net sales in the second quarter 2016, compared to Nokia standalone net sales, was primarily due to growth in Nokia’s Networks business and Group Common and Other, primarily related to the acquisition of Alcatel-Lucent, partially offset by non-IFRS exclusions.

Sequential discussion

The sequential increase in Nokia net sales in the second quarter 2016 was primarily due to growth in Nokia’s Networks business and Group Common and Other, as well as reduced negative impact related to purchase price allocation adjustment related to the reduced valuation of deferred revenue that existed on Alcatel-Lucent’s balance sheet at the time of the acquisition.

Operating profit

Year-on-year discussion

In the second quarter 2016, Nokia generated an operating loss, compared to a Nokia standalone operating profit in the year-ago period. The change was primarily due to restructuring and associated charges and other net negative fluctuations in other income and expenses, higher R&D expenses and higher SG&A expenses, partially offset by higher gross profit, all of which related primarily to the acquisition of Alcatel-Lucent.