Form 485BPOS

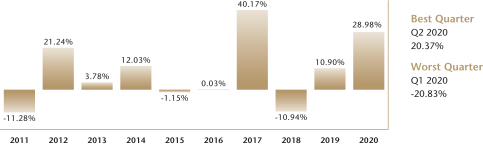

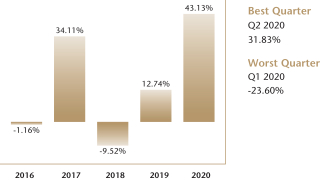

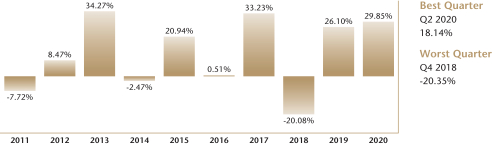

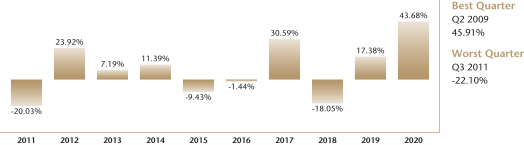

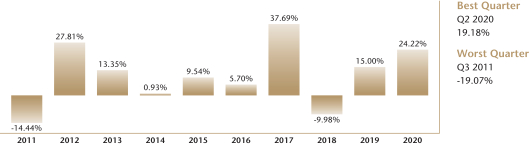

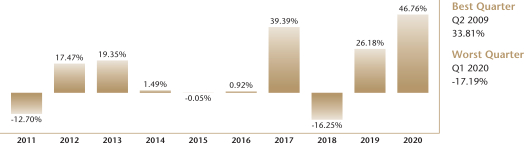

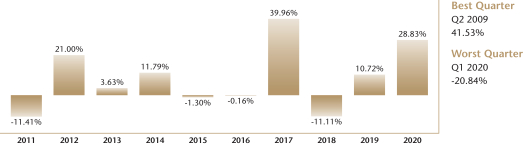

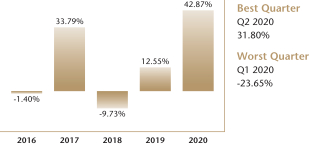

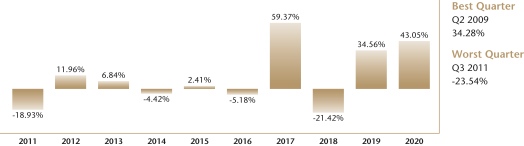

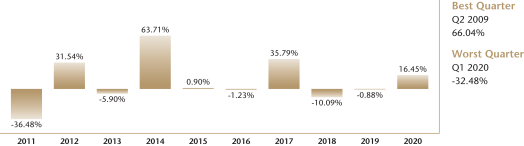

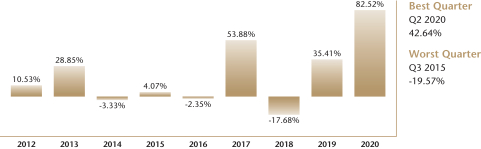

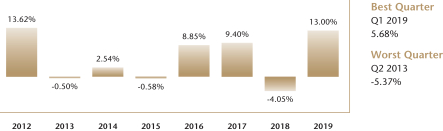

485BPOS2020-12-310000923184falseBest Quarter Q2 2020 19.26% Worst Quarter Q3 2011 -18.92%Best Quarter Q4 2020 15.53% Worst Quarter Q1 2020 -18.85%Best Quarter Q2 2020 30.96:% Worst Quarter Q1 2020 -17.15%Best Quarter Q2 2020 20.37% Worst Quarter Q1 2020 -20.83%Best Quarter Q2 2020 37.34% Worst Quarter Q1 2020 -19.77%Best Quarter Q2 2020 38.78% Worst Quarter Q3 2015 -16.68%Best Quarter Q1 2012 23.88% Worst Quarter Q1 2020 -32.44%Best Quarter Q2 2020 18.14% Worst Quarter Q4 2018 -20.35%Best Quarter Q2 2020 31.83% Worst Quarter Q1 2020 -23.60%Best Quarter Q4 2020 29.62% Worst Quarter Q1 2020 -22.40%Best Quarter Q1 2019 24.22% Worst Quarter Q3 2011 -23.49%Best Quarter Q2 2020 42.62% Worst Quarter Q3 2018 -14.44%Best Quarter Q2 2020 37.26% Worst Quarter Q3 2011 -22.10%Best Quarter Q2 2020 15.52% Worst Quarter Q1 2020 -18.88%Best Quarter Q2 2020 20.37% Worst Quarter Q1 2020 -19.10%Best Quarter Q2 2020 30.94% Worst Quarter Q1 2020 -17.19Best Quarter Q2 2020 19.18% Worst Quarter Q3 2011 -19.07%Best Quarter Q2 2020 9.15% Worst Quarter Q1 2020 -12.73%Best Quarter Q2 2020 20.35% Worst Quarter Q1 2020 -20.84%Best Quarter Q2 2020 10.30% Worst Quarter Q1 2020 -12.66%Best Quarter Q2 2020 31.80% Worst Quarter Q1 2020 -23.65%Best Quarter Q2 2020 42.64% Worst Quarter Q3 2015 -19.57%Best Quarter Q2 2020 38.74% Worst Quarter Q3 2011 -19.09%Best Quarter Q1 2019 24.08% Worst Quarter Q3 2011 -23.54%Best Quarter Q4 2020 29.53% Worst Quarter Q1 2020 -22.37%Best Quarter Q2 2020 18.18% Worst Quarter Q4 2018 -20.38%Best Quarter Q1 2012 23.84% Worst Quarter Q1 2020 -32.48%Best Quarter Q2 2020 20.40% Worst Quarter Q1 2020 -19.08%0.14220.10540.12580.11280.36350.07720.06050.18800.20030.10620.10020.12700.14440.11410.17260.18930.06450.07720.36480.09930.27900.27090.17630.21240.31740.08470.24160.12220.23920.26900.21630.17470.27810.21000.13620.10530.14110.11960.24050.08320.31540.21700.13720.05040.19630.03780.05670.34270.09870.06970.07190.04830.11270.19350.13350.03630.00500.28850.35610.06840.10110.34030.05900.11430.01110.00480.01630.12030.11650.09540.63800.02470.00390.04220.11390.00650.00320.01490.00930.11790.02540.03330.09240.04420.00730.02600.63710.00180.09710.04330.00240.01150.09230.04630.01120.20940.15270.02500.09430.04500.03860.00050.09540.01300.00580.04070.04480.02410.15160.20830.00900.03930.05900.01440.01060.00030.01240.08920.01000.00510.01160.06310.05060.01440.01340.04130.00920.05700.00160.08850.01400.02350.09100.05180.06320.00400.01230.04330.37880.22000.39640.40170.30580.53180.36050.33230.34110.44110.59710.30590.21850.34690.39390.37690.07860.39960.09400.33790.53880.52880.59370.43700.33140.35790.34770.09380.10840.16100.10940.17860.18400.09920.20080.09520.22150.21320.17480.18050.10960.12720.16250.09980.02880.11110.04050.09730.17680.18620.21420.22210.20180.10090.12640.15160.17460.26340.10900.17650.29710.00760.26100.12740.04010.34900.35680.17380.17260.11170.26180.15000.13340.10720.13000.12550.35410.29600.34560.03800.26080.00880.11350.24370.16180.47010.28980.43900.87010.16650.29850.43130.40760.42230.82890.43680.16000.31250.46760.24220.01800.28830.05360.42870.82520.86720.43050.40770.29820.16510.31291994-09-121994-08-311994-09-121994-08-311999-12-271999-12-311998-02-191998-02-191998-02-191995-01-031995-01-031998-12-311998-12-31Best QuarterBest QuarterBest QuarterBest QuarterBest QuarterBest QuarterBest QuarterBest QuarterBest QuarterBest QuarterBest QuarterBest QuarterBest QuarterBest QuarterBest QuarterBest QuarterBest QuarterBest QuarterBest QuarterBest QuarterBest QuarterBest QuarterBest QuarterBest QuarterBest QuarterBest QuarterBest QuarterBest Quarter2020-06-302020-12-312020-06-302020-06-302020-06-302020-06-302012-03-312020-06-302020-06-302020-12-312019-03-312020-06-302020-06-302020-06-302020-06-302020-06-302020-06-302020-06-302020-06-302020-06-302020-06-302020-06-302020-06-302019-03-312020-12-312020-06-302012-03-312020-06-300.19260.15530.30960.20370.37340.38780.23880.18140.31830.29620.24220.42620.37260.15520.20370.30940.19180.09150.20350.10320.31800.42640.38740.24080.29530.18180.23840.2040Worst QuarterWorst QuarterWorst QuarterWorst QuarterWorst QuarterWorst QuarterWorst QuarterWorse QuarterWorst QuarterWorst QuarterWorst QuarterWorst QuarterWorst QuarterWorst QuarterWorst QuarterWorst QuarterWorst QuarterWorst Quarter Worst QuarterWorst QuarterWorst QuarterWorst QuarterWorst QuarterWorst QuarterWorst QuarterWorst Quarter Worst QuarterWorst Quarter2011-09-302020-03-312020-03-312020-03-312020-03-312015-09-302020-03-312018-12-312020-03-312020-03-312011-09-302018-09-302011-09-302020-03-312020-03-312020-03-312011-09-302020-03-312020-03-312020-03-312020-03-312015-09-302011-09-302011-09-302020-03-312018-12-312020-03-312020-03-310.18920.18850.17150.20830.19770.16680.32440.20350.23600.22400.23490.14440.22100.18880.19100.17190.19070.12730.20840.12660.23650.19570.19090.23540.22370.20380.32480.1908<div style="display:none">~ http://matthews.com/role/ShareholderFeesInstitutionalClassProspectusMatthewsEmergingMarketsEquityFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesInstitutionalClassProspectusMatthewsEmergingMarketsEquityFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedInstitutionalClassProspectusMatthewsEmergingMarketsEquityFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesInstitutionalClassProspectusMatthewsChinaDividendFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesInstitutionalClassProspectusMatthewsChinaDividendFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedInstitutionalClassProspectusMatthewsChinaDividendFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualTotalReturnsBarChartInstitutionalClassProspectusMatthewsChinaDividendFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AverageAnnualTotalReturnsTransposedInstitutionalClassProspectusMatthewsChinaDividendFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesInstitutionalClassProspectusMatthewsAsianGrowthAndIncomeFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesInstitutionalClassProspectusMatthewsAsianGrowthAndIncomeFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedInstitutionalClassProspectusMatthewsAsianGrowthAndIncomeFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualTotalReturnsBarChartInstitutionalClassProspectusMatthewsAsianGrowthAndIncomeFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AverageAnnualTotalReturnsTransposedInstitutionalClassProspectusMatthewsAsianGrowthAndIncomeFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesInstitutionalClassProspectusMatthewsAsiaGrowthFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesInstitutionalClassProspectusMatthewsAsiaGrowthFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedInstitutionalClassProspectusMatthewsAsiaGrowthFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualTotalReturnsBarChartInstitutionalClassProspectusMatthewsAsiaGrowthFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AverageAnnualTotalReturnsTransposedInstitutionalClassProspectusMatthewsAsiaGrowthFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesInstitutionalClassProspectusMatthewsPacificTigerFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesInstitutionalClassProspectusMatthewsPacificTigerFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedInstitutionalClassProspectusMatthewsPacificTigerFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualTotalReturnsBarChartInstitutionalClassProspectusMatthewsPacificTigerFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AverageAnnualTotalReturnsTransposedInstitutionalClassProspectusMatthewsPacificTigerFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesInstitutionalClassProspectusMatthewsEmergingMarketsSmallCompaniesFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesInstitutionalClassProspectusMatthewsEmergingMarketsSmallCompaniesFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedInstitutionalClassProspectusMatthewsEmergingMarketsSmallCompaniesFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualTotalReturnsBarChartInstitutionalClassProspectusMatthewsEmergingMarketsSmallCompaniesFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AverageAnnualTotalReturnsTransposedInstitutionalClassProspectusMatthewsEmergingMarketsSmallCompaniesFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesInstitutionalClassProspectusMatthewsAsiaInnovatorsFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesInstitutionalClassProspectusMatthewsAsiaInnovatorsFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedInstitutionalClassProspectusMatthewsAsiaInnovatorsFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualTotalReturnsBarChartInstitutionalClassProspectusMatthewsAsiaInnovatorsFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AverageAnnualTotalReturnsTransposedInstitutionalClassProspectusMatthewsAsiaInnovatorsFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesInstitutionalClassProspectusMatthewsIndiaFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesInstitutionalClassProspectusMatthewsIndiaFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedInstitutionalClassProspectusMatthewsIndiaFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualTotalReturnsBarChartInstitutionalClassProspectusMatthewsIndiaFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AverageAnnualTotalReturnsTransposedInstitutionalClassProspectusMatthewsIndiaFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesInstitutionalClassProspectusMatthewsJapanFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesInstitutionalClassProspectusMatthewsJapanFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedInstitutionalClassProspectusMatthewsJapanFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualTotalReturnsBarChartInstitutionalClassProspectusMatthewsJapanFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AverageAnnualTotalReturnsTransposedInstitutionalClassProspectusMatthewsJapanFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesInstitutionalClassProspectusMatthewsAsiaEsgFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesInstitutionalClassProspectusMatthewsAsiaEsgFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedInstitutionalClassProspectusMatthewsAsiaEsgFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualTotalReturnsBarChartInstitutionalClassProspectusMatthewsAsiaEsgFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AverageAnnualTotalReturnsTransposedInstitutionalClassProspectusMatthewsAsiaEsgFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesInstitutionalClassProspectusMatthewsKoreaFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesInstitutionalClassProspectusMatthewsKoreaFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedInstitutionalClassProspectusMatthewsKoreaFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualTotalReturnsBarChartInstitutionalClassProspectusMatthewsKoreaFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AverageAnnualTotalReturnsTransposedInstitutionalClassProspectusMatthewsKoreaFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesInstitutionalClassProspectusMatthewsChinaFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesInstitutionalClassProspectusMatthewsChinaFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedInstitutionalClassProspectusMatthewsChinaFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualTotalReturnsBarChartInstitutionalClassProspectusMatthewsChinaFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AverageAnnualTotalReturnsTransposedInstitutionalClassProspectusMatthewsChinaFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesInstitutionalClassProspectusMatthewsChinaSmallCompaniesFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesInstitutionalClassProspectusMatthewsChinaSmallCompaniesFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedInstitutionalClassProspectusMatthewsChinaSmallCompaniesFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualTotalReturnsBarChartInstitutionalClassProspectusMatthewsChinaSmallCompaniesFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AverageAnnualTotalReturnsTransposedInstitutionalClassProspectusMatthewsChinaSmallCompaniesFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesInvestorClassProspectusMatthewsEmergingMarketsEquityFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesInvestorClassProspectusMatthewsEmergingMarketsEquityFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedInvestorClassProspectusMatthewsEmergingMarketsEquityFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesInvestorClassProspectusMatthewsEmergingMarketsSmallCompaniesFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesInvestorClassProspectusMatthewsEmergingMarketsSmallCompaniesFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedInvestorClassProspectusMatthewsEmergingMarketsSmallCompaniesFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualTotalReturnsBarChartInvestorClassProspectusMatthewsEmergingMarketsSmallCompaniesFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AverageAnnualTotalReturnsTransposedInvestorClassProspectusMatthewsEmergingMarketsSmallCompaniesFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesInvestorClassProspectusMatthewsAsianGrowthAndIncomeFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesInvestorClassProspectusMatthewsAsianGrowthAndIncomeFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedInvestorClassProspectusMatthewsAsianGrowthAndIncomeFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualTotalReturnsBarChartInvestorClassProspectusMatthewsAsianGrowthAndIncomeFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AverageAnnualTotalReturnsTransposedInvestorClassProspectusMatthewsAsianGrowthAndIncomeFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesInvestorClassProspectusMatthewsAsiaDividendFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesInvestorClassProspectusMatthewsAsiaDividendFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedInvestorClassProspectusMatthewsAsiaDividendFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualTotalReturnsBarChartInvestorClassProspectusMatthewsAsiaDividendFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AverageAnnualTotalReturnsTransposedInvestorClassProspectusMatthewsAsiaDividendFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesInvestorClassProspectusMatthewsAsiaGrowthFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesInvestorClassProspectusMatthewsAsiaGrowthFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedInvestorClassProspectusMatthewsAsiaGrowthFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualTotalReturnsBarChartInvestorClassProspectusMatthewsAsiaGrowthFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AverageAnnualTotalReturnsTransposedInvestorClassProspectusMatthewsAsiaGrowthFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesInvestorClassProspectusMatthewsChinaDividendFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesInvestorClassProspectusMatthewsChinaDividendFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedInvestorClassProspectusMatthewsChinaDividendFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualTotalReturnsBarChartInvestorClassProspectusMatthewsChinaDividendFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AverageAnnualTotalReturnsTransposedInvestorClassProspectusMatthewsChinaDividendFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesMatthewsAsiaCreditOpportunitiesFund column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesMatthewsAsiaCreditOpportunitiesFund column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedMatthewsAsiaCreditOpportunitiesFund column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualTotalReturnsBarChartMatthewsAsiaCreditOpportunitiesFund column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AverageAnnualTotalReturnsTransposedMatthewsAsiaCreditOpportunitiesFund column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesInvestorClassProspectusMatthewsPacificTigerFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesInvestorClassProspectusMatthewsPacificTigerFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedInvestorClassProspectusMatthewsPacificTigerFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualTotalReturnsBarChartInvestorClassProspectusMatthewsPacificTigerFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AverageAnnualTotalReturnsTransposedInvestorClassProspectusMatthewsPacificTigerFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesMatthewsAsiaTotalReturnBondFund column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesMatthewsAsiaTotalReturnBondFund column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedMatthewsAsiaTotalReturnBondFund column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualTotalReturnsBarChartMatthewsAsiaTotalReturnBondFund column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AverageAnnualTotalReturnsTransposedMatthewsAsiaTotalReturnBondFund column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesInvestorClassProspectusMatthewsAsiaEsgFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesInvestorClassProspectusMatthewsAsiaEsgFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedInvestorClassProspectusMatthewsAsiaEsgFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualTotalReturnsBarChartInvestorClassProspectusMatthewsAsiaEsgFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AverageAnnualTotalReturnsTransposedInvestorClassProspectusMatthewsAsiaEsgFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesInvestorClassProspectusMatthewsChinaSmallCompaniesFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesInvestorClassProspectusMatthewsChinaSmallCompaniesFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedInvestorClassProspectusMatthewsChinaSmallCompaniesFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualTotalReturnsBarChartInvestorClassProspectusMatthewsChinaSmallCompaniesFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AverageAnnualTotalReturnsTransposedInvestorClassProspectusMatthewsChinaSmallCompaniesFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesInvestorClassProspectusMatthewsAsiaInnovatorsFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesInvestorClassProspectusMatthewsAsiaInnovatorsFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedInvestorClassProspectusMatthewsAsiaInnovatorsFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualTotalReturnsBarChartInvestorClassProspectusMatthewsAsiaInnovatorsFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AverageAnnualTotalReturnsTransposedInvestorClassProspectusMatthewsAsiaInnovatorsFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesInvestorClassProspectusMatthewsChinaFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesInvestorClassProspectusMatthewsChinaFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedInvestorClassProspectusMatthewsChinaFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualTotalReturnsBarChartInvestorClassProspectusMatthewsChinaFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AverageAnnualTotalReturnsTransposedInvestorClassProspectusMatthewsChinaFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesInvestorClassProspectusMatthewsKoreaFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesInvestorClassProspectusMatthewsKoreaFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedInvestorClassProspectusMatthewsKoreaFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualTotalReturnsBarChartInvestorClassProspectusMatthewsKoreaFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AverageAnnualTotalReturnsTransposedInvestorClassProspectusMatthewsKoreaFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesInvestorClassProspectusMatthewsJapanFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesInvestorClassProspectusMatthewsJapanFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedInvestorClassProspectusMatthewsJapanFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualTotalReturnsBarChartInvestorClassProspectusMatthewsJapanFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AverageAnnualTotalReturnsTransposedInvestorClassProspectusMatthewsJapanFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesInvestorClassProspectusMatthewsIndiaFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesInvestorClassProspectusMatthewsIndiaFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedInvestorClassProspectusMatthewsIndiaFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualTotalReturnsBarChartInvestorClassProspectusMatthewsIndiaFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AverageAnnualTotalReturnsTransposedInvestorClassProspectusMatthewsIndiaFundInvestorClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ShareholderFeesInstitutionalClassProspectusMatthewsAsiaDividendFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualFundOperatingExpensesInstitutionalClassProspectusMatthewsAsiaDividendFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/ExpenseExampleTransposedInstitutionalClassProspectusMatthewsAsiaDividendFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AnnualTotalReturnsBarChartInstitutionalClassProspectusMatthewsAsiaDividendFundInstitutionalClassShares column period compact * ~</div><div style="display:none">~ http://matthews.com/role/AverageAnnualTotalReturnsTransposedInstitutionalClassProspectusMatthewsAsiaDividendFundInstitutionalClassShares column period compact * ~</div>“Other Expenses” are based on estimated amounts for the current fiscal year and calculated as a percentage of the Fund’s assets. Matthews has contractually agreed (i) to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class to 0.90%. If the operating expenses fall below the expense limitation within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the lesser of (i) the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or (ii) the expense limitation in effect at the time of recoupment. This agreement will remain in place until April 30, 2022 and may be terminated at any time by the Board of Trustees on behalf of the Fund on 60 days’ written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date.Matthews has contractually agreed to waive a portion of its advisory fee and administrative and shareholder services fee if the Fund’s average daily net assets are over $3 billion, as follows: for every $2.5 billion average daily net assets of the Fund that are over $3 billion, the advisory fee rate and the administrative and shareholder services fee rate for the Fund with respect to such excess average daily net assets will be each reduced by 0.01%, in each case without reducing such fee rate below 0.00%. Any amount waived by Matthews pursuant to this agreement may not be recouped by Matthews. This agreement will remain in place until April 30, 2022 and may be terminated (i) at any time by the Board of Trustees upon 60 days’ prior written notice to Matthews; or (ii) by Matthews at the annual expiration date of the agreement upon 60 days’ prior written notice to the Trust, in each case without payment of any penalty.Matthews has contractually agreed to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class to 1.15%. If the operating expenses fall below the expense limitation within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the lesser of (i) the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or (ii) the expense limitation in effect at the time of recoupment. This agreement will remain in place until April 30, 2022 and may be terminated at any time by the Board of Trustees on behalf of the Fund on 60 days’ written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date.“Total Annual Fund Operating Expenses After Fee Waiver and Expense Reimbursement” do not correlate to the corresponding ratio included in the Fund’s Financial Highlights because the contractual fee waiver/expense reimbursement was changed subsequent to the fiscal year ended December 31, 2020 and was not in effect for that fiscal year.After-tax returns are calculated using the highest historical individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts.Effective April 30, 2021, in connection with changes to the Fund’s name and principal investment strategies, the primary benchmark changed from the MSCI All Country Asia ex Japan Small Cap Index to the MSCI Emerging Markets Small Cap Index.Matthews has contractually agreed to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class to 1.20%. If the operating expenses fall below the expense limitation within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the lesser of (i) the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or (ii) the expense limitation in effect at the time of recoupment. This agreement will remain in place until April 30, 2022 and may be terminated at any time by the Board of Trustees on behalf of the Fund on 60 days’ written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date.Korea Composite Stock Price Index performance data may be readjusted periodically by the Korea Exchange due to certain factors, including the declaration of dividends.Matthews has contractually agreed (i) to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class (which is offered through a separate prospectus to eligible investors) to 0.90%, first by waiving class specific expenses (e.g., shareholder service fees specific to a particular class) of the Institutional Class and then, to the extent necessary, by waiving non-class specific expenses (e.g., custody fees) of the Institutional Class, and (ii) if any Fund-wide expenses (i.e., expenses that apply to both the Institutional Class and the Investor Class) are waived for the Institutional Class to maintain the 0.90% expense limitation, to waive an equal amount (in annual percentage terms) of those same expenses for the Investor Class. The Total Annual Fund Operating Expenses After Fee Waiver and Expense Reimbursement for the Investor Class may vary from year to year and will in some years exceed 0.90%. If the operating expenses fall below the expense limitation within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the lesser of (i) the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or (ii) the expense limitation in effect at the time of recoupment. This agreement will remain in place until April 30, 2022 and may be terminated at any time by the Board of Trustees on behalf of the Fund on 60 days’ written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date.Matthews has contractually agreed (i) to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class (which is offered through a separate prospectus to eligible investors) to 1.15%, first by waiving class specific expenses (e.g., shareholder service fees specific to a particular class) of the Institutional Class and then, to the extent necessary, by waiving non-class specific expenses (e.g., custody fees) of the Institutional Class, and (ii) if any Fund-wide expenses (i.e., expenses that apply to both the Institutional Class and the Investor Class) are waived for the Institutional Class to maintain the 1.15% expense limitation, to waive an equal amount (in annual percentage terms) of those same expenses for the Investor Class. The Total Annual Fund Operating Expenses After Fee Waiver and Expense Reimbursement for the Investor Class may vary from year to year and will in some years exceed 1.15%. If the operating expenses fall below the expense limitation within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the lesser of (i) the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or (ii) the expense limitation in effect at the time of recoupment. This agreement will remain in place until April 30, 2022 and may be terminated at any time by the Board of Trustees on behalf of the Fund on 60 days’ written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date.Effective [April 30], 2021, in connection with changes to the Fund’s name and principal investment strategies, the primary benchmark changed from the MSCI All Country Asia ex Japan Small Cap Index to the MSCI Emerging Markets Small Cap Index.Matthews has contractually agreed (i) to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class to 0.90% first by waiving class specific expenses (e.g., shareholder service fees specific to a particular class) of the Institutional Class and then, to the extent necessary, by waiving non-class specific expenses (e.g., custody fees) of the Institutional Class, and (ii) if any Fund-wide expenses (i.e., expenses that apply to both the Institutional Class and the Investor Class) are waived for the Institutional Class to maintain the 0.90% expense limitation, to waive an equal amount (in annual percentage terms) of those same expenses for the Investor Class. The Total Annual Fund Operating Expenses After Fee Waiver and Expense Reimbursement for the Investor Class may vary from year to year and will in some years exceed 0.90%. Pursuant to this agreement, any amount waived for prior fiscal years with respect to the Fund is not subject to recoupment. This agreement will remain in place until April 30, 2022 and may be terminated at any time by the Board of Trustees on behalf of the Fund on 60 days’ written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date.After-tax returns are calculated using the highest historical individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor's tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts. After-tax returns are shown for only one class of shares and after-tax returns for the other class of shares will vary.As of May 1, 2016, the HSBC Asian Local Bond Index became the Markit iBoxx Asian Local Bond Index. The Index performance reflects the returns of the discontinued predecessor HSBC Asian Local Bond Index up to December 31, 2012 and the returns of the successor Markit iBoxx Asian Local Bond Index thereafter. Matthews has contractually agreed (i) to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class (which is offered through a separate prospectus to eligible investors) to 1.20%, first by waiving class specific expenses (e.g., shareholder service fees specific to a particular class) of the Institutional Class and then, to the extent necessary, by waiving non-class specific expenses (e.g., custody fees) of the Institutional Class, and (ii) if any Fund-wide expenses (i.e., expenses that apply to both the Institutional Class and the Investor Class) are waived for the Institutional Class to maintain the 1.20% expense limitation, to waive an equal amount (in annual percentage terms) of those same expenses for the Investor Class. The Total Annual Fund Operating Expenses After Fee Waiver and Expense Reimbursement for the Investor Class may vary from year to year and will in some years exceed 1.20%. If the operating expenses fall below the expense limitation within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the lesser of (i) the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or (ii) the expense limitation in effect at the time of recoupment. This agreement will remain in place until April 30, 2022 and may be terminated at any time by the Board of Trustees on behalf of the Fund on 60 days’ written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date.Calculated from 2/28/98.Index performance data prior to 11/25/08 is not available. 0000923184 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000068521Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000027009Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001030Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001035Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001029Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000023269Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001034Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001036Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001033Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000049136Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001031Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001032Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000032816Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000068521Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000023269Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001030Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000013856Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001035Member 2021-04-30 2021-04-30 0000923184 ck0000923184:S000027009Member ck0000923184:InvestorClassProspectusMember 2021-04-30 2021-04-30 0000923184 ck0000923184:S000053714Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001029Member 2021-04-30 2021-04-30 0000923184 ck0000923184:S000034706Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000049136Member 2021-04-30 2021-04-30 0000923184 ck0000923184:S000032816Member ck0000923184:InvestorClassProspectusMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001034Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001032Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001031Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001033Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001036Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000013856Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000068521Member ck0000923184:C000219130Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000027009Member ck0000923184:C000093231Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001030Member ck0000923184:C000093222Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001035Member ck0000923184:C000093227Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001029Member ck0000923184:C000093221Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000023269Member ck0000923184:C000093230Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001034Member ck0000923184:C000093226Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001036Member ck0000923184:C000093228Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001033Member ck0000923184:C000093225Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000049136Member ck0000923184:C000154926Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:C000093223Member ck0000923184:S000001031Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001032Member ck0000923184:C000093224Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000032816Member ck0000923184:C000195803Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000068521Member ck0000923184:C000219129Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000023269Member ck0000923184:C000068052Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001030Member ck0000923184:C000002786Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000013856Member ck0000923184:C000038018Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001035Member ck0000923184:C000002793Member 2021-04-30 2021-04-30 0000923184 ck0000923184:S000027009Member ck0000923184:C000081250Member ck0000923184:InvestorClassProspectusMember 2021-04-30 2021-04-30 0000923184 ck0000923184:S000053714Member ck0000923184:C000168876Member 2021-04-30 2021-04-30 0000923184 ck0000923184:S000053714Member ck0000923184:C000168877Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001029Member ck0000923184:C000002785Member 2021-04-30 2021-04-30 0000923184 ck0000923184:S000034706Member ck0000923184:C000106893Member 2021-04-30 2021-04-30 0000923184 ck0000923184:S000034706Member ck0000923184:C000106892Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000049136Member ck0000923184:C000154925Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000032816Member ck0000923184:C000101279Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001034Member ck0000923184:C000002792Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001032Member ck0000923184:C000002790Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001031Member ck0000923184:C000002788Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001033Member ck0000923184:C000002791Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001036Member ck0000923184:C000002794Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000013856Member ck0000923184:C000093229Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000027009Member ck0000923184:C000093231Member rr:AfterTaxesOnDistributionsMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000027009Member ck0000923184:C000093231Member rr:AfterTaxesOnDistributionsAndSalesMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000027009Member ck0000923184:MsciChinaIndexMember 2021-04-30 2021-04-30 0000923184 ck0000923184:S000001030Member ck0000923184:InstitutionalClassProspectusMember ck0000923184:C000093222Member rr:AfterTaxesOnDistributionsMember 2021-04-30 2021-04-30 0000923184 ck0000923184:S000001030Member ck0000923184:InstitutionalClassProspectusMember ck0000923184:C000093222Member rr:AfterTaxesOnDistributionsAndSalesMember 2021-04-30 2021-04-30 0000923184 ck0000923184:S000001030Member ck0000923184:InstitutionalClassProspectusMember ck0000923184:MsciAllCountryAsiaExJapanIndexMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001035Member ck0000923184:C000093227Member rr:AfterTaxesOnDistributionsMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001035Member ck0000923184:C000093227Member rr:AfterTaxesOnDistributionsAndSalesMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001035Member ck0000923184:MsciAllCountryAsiaPacificIndexMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001029Member ck0000923184:C000093221Member rr:AfterTaxesOnDistributionsMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001029Member ck0000923184:C000093221Member rr:AfterTaxesOnDistributionsAndSalesMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001029Member ck0000923184:MsciAllCountryAsiaExJapanIndexMember 2021-04-30 2021-04-30 0000923184 ck0000923184:S000023269Member ck0000923184:InstitutionalClassProspectusMember ck0000923184:C000093230Member rr:AfterTaxesOnDistributionsMember 2021-04-30 2021-04-30 0000923184 ck0000923184:S000023269Member ck0000923184:InstitutionalClassProspectusMember ck0000923184:C000093230Member rr:AfterTaxesOnDistributionsAndSalesMember 2021-04-30 2021-04-30 0000923184 ck0000923184:S000023269Member ck0000923184:InstitutionalClassProspectusMember ck0000923184:MsciEmergingMarketsSmallCapIndexMember 2021-04-30 2021-04-30 0000923184 ck0000923184:S000023269Member ck0000923184:InstitutionalClassProspectusMember ck0000923184:MsciAllCountryAsiaExJapanSmallCapIndexMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001034Member ck0000923184:C000093226Member rr:AfterTaxesOnDistributionsMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001034Member ck0000923184:C000093226Member rr:AfterTaxesOnDistributionsAndSalesMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001034Member ck0000923184:MsciAllCountryAsiaExJapanIndexMember 2021-04-30 2021-04-30 0000923184 rr:AfterTaxesOnDistributionsAndSalesMember ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001036Member ck0000923184:C000093228Member 2021-04-30 2021-04-30 0000923184 rr:AfterTaxesOnDistributionsMember ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001036Member ck0000923184:C000093228Member 2021-04-30 2021-04-30 0000923184 ck0000923184:SpBombayStockExchange100IndexMember ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001036Member 2021-04-30 2021-04-30 0000923184 rr:AfterTaxesOnDistributionsMember ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001033Member ck0000923184:C000093225Member 2021-04-30 2021-04-30 0000923184 rr:AfterTaxesOnDistributionsAndSalesMember ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001033Member ck0000923184:C000093225Member 2021-04-30 2021-04-30 0000923184 ck0000923184:MsciJapanIndexMember ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001033Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000049136Member ck0000923184:C000154926Member rr:AfterTaxesOnDistributionsAndSalesMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000049136Member ck0000923184:C000154926Member rr:AfterTaxesOnDistributionsMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000049136Member ck0000923184:MsciAllCountryAsiaExJapanIndexMember 2021-04-30 2021-04-30 0000923184 ck0000923184:C000093223Member rr:AfterTaxesOnDistributionsAndSalesMember ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001031Member 2021-04-30 2021-04-30 0000923184 ck0000923184:C000093223Member rr:AfterTaxesOnDistributionsMember ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001031Member 2021-04-30 2021-04-30 0000923184 ck0000923184:KoreaCompositeStockPriceIndexMember ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001031Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001032Member ck0000923184:C000093224Member rr:AfterTaxesOnDistributionsMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001032Member ck0000923184:C000093224Member rr:AfterTaxesOnDistributionsAndSalesMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001032Member ck0000923184:MsciChinaIndexMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000001032Member ck0000923184:MsciChinaAllSharesIndexMember 2021-04-30 2021-04-30 0000923184 rr:AfterTaxesOnDistributionsMember ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000032816Member ck0000923184:C000195803Member 2021-04-30 2021-04-30 0000923184 rr:AfterTaxesOnDistributionsAndSalesMember ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000032816Member ck0000923184:C000195803Member 2021-04-30 2021-04-30 0000923184 ck0000923184:MsciChinaSmallCapIndexMember ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000032816Member 2021-04-30 2021-04-30 0000923184 rr:AfterTaxesOnDistributionsMember ck0000923184:C000068052Member ck0000923184:InvestorClassProspectusMember ck0000923184:S000023269Member 2021-04-30 2021-04-30 0000923184 rr:AfterTaxesOnDistributionsAndSalesMember ck0000923184:C000068052Member ck0000923184:InvestorClassProspectusMember ck0000923184:S000023269Member 2021-04-30 2021-04-30 0000923184 ck0000923184:MsciAllCountryAsiaExJapanSmallCapIndexMember ck0000923184:InvestorClassProspectusMember ck0000923184:S000023269Member 2021-04-30 2021-04-30 0000923184 ck0000923184:MsciEmergingMarketsSmallCapIndexMember ck0000923184:InvestorClassProspectusMember ck0000923184:S000023269Member 2021-04-30 2021-04-30 0000923184 rr:AfterTaxesOnDistributionsAndSalesMember ck0000923184:C000002786Member ck0000923184:InvestorClassProspectusMember ck0000923184:S000001030Member 2021-04-30 2021-04-30 0000923184 rr:AfterTaxesOnDistributionsMember ck0000923184:C000002786Member ck0000923184:InvestorClassProspectusMember ck0000923184:S000001030Member 2021-04-30 2021-04-30 0000923184 ck0000923184:MsciAllCountryAsiaExJapanIndexMember ck0000923184:InvestorClassProspectusMember ck0000923184:S000001030Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000013856Member ck0000923184:C000038018Member rr:AfterTaxesOnDistributionsMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000013856Member ck0000923184:C000038018Member rr:AfterTaxesOnDistributionsAndSalesMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000013856Member ck0000923184:MsciAllCountryAsiaPacificIndexMember 2021-04-30 2021-04-30 0000923184 rr:AfterTaxesOnDistributionsMember ck0000923184:C000002793Member ck0000923184:InvestorClassProspectusMember ck0000923184:S000001035Member 2021-04-30 2021-04-30 0000923184 rr:AfterTaxesOnDistributionsAndSalesMember ck0000923184:C000002793Member ck0000923184:InvestorClassProspectusMember ck0000923184:S000001035Member 2021-04-30 2021-04-30 0000923184 ck0000923184:MsciAllCountryAsiaPacificIndexMember ck0000923184:InvestorClassProspectusMember ck0000923184:S000001035Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000027009Member ck0000923184:C000081250Member rr:AfterTaxesOnDistributionsMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000027009Member ck0000923184:C000081250Member rr:AfterTaxesOnDistributionsAndSalesMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000027009Member ck0000923184:MsciChinaIndexMember 2021-04-30 2021-04-30 0000923184 ck0000923184:S000053714Member ck0000923184:C000168876Member rr:AfterTaxesOnDistributionsMember 2021-04-30 2021-04-30 0000923184 ck0000923184:S000053714Member ck0000923184:C000168876Member rr:AfterTaxesOnDistributionsAndSalesMember 2021-04-30 2021-04-30 0000923184 ck0000923184:S000053714Member ck0000923184:JpMorganAsiaCreditIndexMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001029Member ck0000923184:C000002785Member rr:AfterTaxesOnDistributionsMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001029Member ck0000923184:C000002785Member rr:AfterTaxesOnDistributionsAndSalesMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001029Member ck0000923184:MsciAllCountryAsiaExJapanIndexMember 2021-04-30 2021-04-30 0000923184 ck0000923184:S000034706Member ck0000923184:FiftyMarkitIboxxAsianLocalBondIndex50JpMorganAsiaCreditIndexMember 2021-04-30 2021-04-30 0000923184 ck0000923184:S000034706Member ck0000923184:C000106893Member rr:AfterTaxesOnDistributionsMember 2021-04-30 2021-04-30 0000923184 ck0000923184:S000034706Member ck0000923184:C000106893Member rr:AfterTaxesOnDistributionsAndSalesMember 2021-04-30 2021-04-30 0000923184 rr:AfterTaxesOnDistributionsAndSalesMember ck0000923184:C000154925Member ck0000923184:S000049136Member ck0000923184:InvestorClassProspectusMember 2021-04-30 2021-04-30 0000923184 rr:AfterTaxesOnDistributionsMember ck0000923184:C000154925Member ck0000923184:S000049136Member ck0000923184:InvestorClassProspectusMember 2021-04-30 2021-04-30 0000923184 ck0000923184:MsciAllCountryAsiaExJapanIndexMember ck0000923184:S000049136Member ck0000923184:InvestorClassProspectusMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000032816Member rr:AfterTaxesOnDistributionsMember ck0000923184:C000101279Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000032816Member rr:AfterTaxesOnDistributionsAndSalesMember ck0000923184:C000101279Member 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000032816Member ck0000923184:MsciChinaSmallCapIndexMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001034Member ck0000923184:C000002792Member rr:AfterTaxesOnDistributionsAndSalesMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001034Member ck0000923184:C000002792Member rr:AfterTaxesOnDistributionsMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001034Member ck0000923184:MsciAllCountryAsiaExJapanIndexMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001032Member ck0000923184:C000002790Member rr:AfterTaxesOnDistributionsMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001032Member ck0000923184:C000002790Member rr:AfterTaxesOnDistributionsAndSalesMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001032Member ck0000923184:MsciChinaIndexMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001032Member ck0000923184:MsciChinaAllSharesIndexMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001031Member ck0000923184:C000002788Member rr:AfterTaxesOnDistributionsMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001031Member ck0000923184:C000002788Member rr:AfterTaxesOnDistributionsAndSalesMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001031Member ck0000923184:KoreaCompositeStockPriceIndexMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001033Member ck0000923184:MsciJapanIndexMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001033Member ck0000923184:C000002791Member rr:AfterTaxesOnDistributionsMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001033Member ck0000923184:C000002791Member rr:AfterTaxesOnDistributionsAndSalesMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001036Member ck0000923184:SpBombayStockExchange100IndexMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001036Member ck0000923184:C000002794Member rr:AfterTaxesOnDistributionsMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InvestorClassProspectusMember ck0000923184:S000001036Member ck0000923184:C000002794Member rr:AfterTaxesOnDistributionsAndSalesMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000013856Member ck0000923184:C000093229Member rr:AfterTaxesOnDistributionsMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000013856Member ck0000923184:C000093229Member rr:AfterTaxesOnDistributionsAndSalesMember 2021-04-30 2021-04-30 0000923184 ck0000923184:InstitutionalClassProspectusMember ck0000923184:S000013856Member ck0000923184:MsciAllCountryAsiaPacificIndexMember 2021-04-30 2021-04-30 iso4217:USD xbrli:pure

As filed with the Securities and Exchange Commission on April 30, 2021

Securities Act of 1933 File

No. 033-78960

Investment Company Act of 1940 File

No. 811-08510

SECURITIES AND EXCHANGE COMMISSION

|

|

|

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 |

|

☒ |

Pre-Effective Amendment No. |

|

☐ |

Post-Effective Amendment No. 92 |

|

☒ |

THE INVESTMENT COMPANY ACT OF 1940

MATTHEWS INTERNATIONAL FUNDS

(Exact Name of Registrant as Specified in

Charter

)

Four Embarcadero

Center

, Suite

550

(Address of Principal Executive Offices) (Zip Code)

Registrant’s Telephone Number, including Area Code: (415)

788-7553

William J. Hackett, President

Four Embarcadero Center, Suite 550

(Name and Address of Agent for Service)

David Monroe, Vice President

Four Embarcadero Center, Suite 550

101 California Street, 48th Floor

It is proposed that this filing will become effective (check appropriate box)

| |

☐ |

immediately upon filing pursuant to paragraph (b) |

| |

☒ |

on April 30, 2021 pursuant to paragraph (b) |

| |

☐ |

60 days after filing pursuant to paragraph (a)(1) |

| |

☐ |

on pursuant to paragraph (a)(1) |

| |

☐ |

75 days after filing pursuant to paragraph (a)(2) |

| |

☐ |

on pursuant to paragraph (a)(2) of rule 485. |

If appropriate, check the following box:

| |

☐ |

this post-effective amendment designates a new effective date for a previously filed post-effective amendment. |

Matthews Asia Funds |

Prospectus

April 30, 2021

|

matthewsasia.com

INSTITUTIONAL CLASS SHARES

Matthews Emerging Markets Equity Fund (MIEFX)

Matthews Emerging Markets Small Companies Fund (MISMX)

(formerly known as the Matthews Asia Small Companies Fund)

Matthews Asian Growth and Income Fund (MICSX)

Matthews Asia Dividend Fund (MIPIX)

Matthews China Dividend Fund (MICDX)

Matthews Asia Growth Fund (MIAPX)

Matthews Pacific Tiger Fund (MIPTX)

Matthews Asia ESG Fund (MISFX)

Matthews Asia Innovators Fund (MITEX)

Matthews China Fund (MICFX)

Matthews India Fund (MIDNX)

Matthews Japan Fund (MIJFX)

Matthews Korea Fund (MIKOX)

Matthews China Small Companies Fund (MICHX)

The U.S. Securities and Exchange Commission (the “SEC”) has not approved or disapproved the Funds. Also, the SEC has not passed upon the adequacy or accuracy of this prospectus. Anyone who informs you otherwise is committing a crime.

Paper copies of the Funds’ annual and semi-annual shareholder reports are no longer being sent by mail, unless you specifically request paper copies of the reports. Instead, the reports will be made available on the Funds’ website matthewsasia.com, and you will be notified by mail each time a report is posted and provided with a website link to access the report. You may elect to receive paper copies of shareholder reports and other communications from the Funds anytime by contacting your financial intermediary (such as a broker-dealer or bank) or, if you are a direct investor, by calling 800.789.ASIA (2742).

Your election to receive reports in paper will apply to all Funds held in your account if you invest through your financial intermediary or all Funds held directly with Matthews Asia Funds.

Matthews Asia Funds

|

|

|

|

|

| |

|

|

|

|

|

|

GLOBAL EMERGING MARKETS STRATEGIES |

|

|

|

|

|

|

| |

|

|

1 |

|

|

|

| |

|

|

6 |

|

|

|

ASIA GROWTH AND INCOME STRATEGIES |

|

|

|

|

|

|

| |

|

|

1 1 |

|

|

|

| |

|

|

1 5 |

|

|

|

| |

|

|

1 9 |

|

|

|

| |

|

|

|

|

|

|

| |

|

|

2 3 |

|

|

|

| |

|

|

2 7 |

|

|

|

| |

|

|

3 1 |

|

|

|

| |

|

|

3 5 |

|

|

|

| |

|

|

3 9 |

|

|

|

| |

|

|

4 3 |

|

|

|

| |

|

|

4 7 |

|

|

|

| |

|

|

50 |

|

|

|

| |

|

|

5 4 |

|

|

|

| |

|

|

5 9 |

|

|

|

Additional Fund Information |

|

|

|

|

|

|

| |

|

|

7 3 |

|

|

|

| |

|

|

7 3 |

|

|

|

| |

|

|

7 3 |

|

|

|

| |

|

|

7 6 |

|

|

|

| |

|

|

9 2 |

|

|

|

| |

|

|

9 8 |

|

|

|

| |

|

|

9 8 |

|

|

|

| |

|

|

9 8 |

|

|

|

| |

|

|

10 1 |

|

|

|

| |

|

|

10 1 |

|

|

|

| |

|

|

10 2 |

|

|

|

| |

|

|

10 3 |

|

|

|

| |

|

|

10 6 |

|

|

|

| |

|

|

10 7 |

|

|

|

| |

|

|

10 7 |

|

Please read this document carefully before you make any investment decision. If you have any questions, do not hesitate to contact a Matthews Asia Funds representative at 800.789.ASIA (2742) or visit matthewsasia.com.

Please keep this prospectus with your other account documents for future reference.

Matthews Emerging Markets Equity Fund

Long-term capital appreciation.

Fees and Expenses of the Fund

This table describes the fees and expenses that you may pay if you buy and hold shares of this Fund.

(fees paid directly from your investment)

|

|

|

|

|

|

|

|

|

| Maximum Account Fee on Redemptions (for wire redemptions only) |

|

|

|

|

|

|

$9 |

|

ANNUAL OPERATING EXPENSES

(expenses that you pay each year as a percentage of the value of your investment)

|

|

|

|

|

|

|

|

|

| Management Fees |

|

|

|

|

|

|

0.67% |

|

| Distribution (12b-1) Fees |

|

|

|

|

|

|

0.00% |

|

| Other Expenses 1 |

|

|

|

|

|

|

1.99% |

|

|

|

|

| Administration and Shareholder Servicing Fees |

|

|

0.15% |

|

|

|

|

|

Total Annual Fund Operating Expenses |

|

|

|

|

|

|

|

|

| Fee Waiver and Expense Reimbursement 2 |

|

|

|

|

|

|

(1.76%) |

|

Total Annual Fund Operating Expenses After Fee Waiver and Expense Reimbursement |

|

|

|

|

|

|

|

|

| |

1 |

“Other Expenses” are based on estimated amounts for the current fiscal year and calculated as a percentage of the Fund’s assets. |

| |

2 |

Matthews has contractually agreed (i) to waive fees and reimburse expenses to the extent needed to limit Total Annual Fund Operating Expenses (excluding Rule 12b-1 fees, taxes, interest, brokerage commissions, short sale dividend expenses, expenses incurred in connection with any merger or reorganization or extraordinary expenses such as litigation) of the Institutional Class to 0.90%. If the operating expenses fall below the expense limitation within three years after Matthews has made a waiver or reimbursement, the Fund may reimburse Matthews up to an amount that does not cause the expenses for that year to exceed the lesser of (i) the expense limitation applicable at the time of that fee waiver and/or expense reimbursement or (ii) the expense limitation in effect at the time of recoupment. This agreement will remain in place until April 30, 2022 and may be terminated at any time by the Board of Trustees on behalf of the Fund on 60 days’ written notice to Matthews. Matthews may decline to renew this agreement by written notice to the Trust at least 30 days before its annual expiration date. |

This example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of those periods. The example also assumes that your investment has a 5% return each year and that the Fund’s operating expenses remain the same. The example reflects the fee waiver for the one year period only. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover may indicate higher transaction costs and may result in higher taxes when Fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example of fund expenses, affect the Fund’s performance. During the most recent fiscal year, the Fund’s portfolio turnover rate was 62% of the average value of its portfolio.

|

|

|

|

|

|

|

|

|

|

|

|

|

MATTHEWS EMERGING MARKETS EQUITY FUND |

|

|

|

|

Principal Investment Strategy

Under normal circumstances, the Matthews Emerging Markets Equity Fund seeks to achieve its investment objective by investing at least 80% of its net assets, which include borrowings for investment purposes, in the common and preferred stocks of companies located in emerging market countries. Emerging market countries generally include every country in the world except the United States, Australia, Canada, Hong Kong, Israel, Japan, New Zealand, Singapore and most of the countries in Western Europe. Certain emerging market countries may also be classified as “frontier” market countries, which are a subset of emerging market countries with newer or even less developed economies and markets, such as Sri Lanka and Vietnam. The list of emerging market countries and frontier market countries may change from time to time. The Fund may also invest in companies located in developed countries; however, the Fund may not invest in any company located in a developed country if, at the time of purchase, more than 20% of the Fund’s assets are invested in developed market companies. The Fund has concentrated its investments (meaning more than 25% of its assets) from time to time in a single country, including China.