Table of Contents

As filed with the Securities and Exchange Commission on April 30, 2015

Securities Act of 1933 File No. 033-78960

Investment Company Act of 1940 File No. 811-08510

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-1A

REGISTRATION STATEMENT

UNDER

| THE SECURITIES ACT OF 1933 | x | |||

| Pre-Effective Amendment No. | ¨ | |||

| Post-Effective Amendment No. 60 | x |

and/or

REGISTRATION STATEMENT

UNDER

| THE INVESTMENT COMPANY ACT OF 1940 | x |

Amendment No. 63

MATTHEWS INTERNATIONAL FUNDS

(Exact Name of Registrant as Specified in Charter)

Four Embarcadero Center, Suite 550

San Francisco, CA 94111

(Address of Principal Executive Offices) (Zip Code)

Registrant’s Telephone Number, including Area Code: (415) 788-6036

William J. Hackett, President

Four Embarcadero Center, Suite 550

San Francisco, CA 94111

(Name and Address of Agent for Service)

Copies To:

David Monroe, Vice President

Four Embarcadero Center, Suite 550

San Francisco, CA 94111

David A. Hearth, Esq.

Paul Hastings LLP

55 Second Street

San Francisco, CA 94105

It is proposed that this filing will become effective (check appropriate box)

| x | immediately upon filing pursuant to paragraph (b) |

| ¨ | on pursuant to paragraph (b) |

| ¨ | 60 days after filing pursuant to paragraph (a)(1) |

| ¨ | on pursuant to paragraph (a)(1) |

| ¨ | 75 days after filing pursuant to paragraph (a)(2) |

| ¨ | on pursuant to paragraph (a)(2) of rule 485. |

If appropriate, check the following box:

| ¨ | this post-effective amendment designates a new effective date for a previously filed post-effective amendment. |

Table of Contents

Matthews Asia Funds | Prospectus

April 30, 2015 | matthewsasia.com

The U.S. Securities and Exchange Commission (the “SEC”) has not approved or disapproved the Funds. Also, the SEC has not passed upon the adequacy or accuracy of this prospectus. Anyone who informs you otherwise is committing a crime.

Table of Contents

matthewsasia.com

Contents

| 1 | ||||

| 4 | ||||

| 7 | ||||

| 10 | ||||

| 13 | ||||

| 16 | ||||

| 19 | ||||

| 22 | ||||

| 26 | ||||

| 29 | ||||

| 32 | ||||

| 35 | ||||

| 38 | ||||

| 41 | ||||

| 45 | ||||

| 58 | ||||

| 58 | ||||

| 58 | ||||

| 61 | ||||

| 70 | ||||

| 76 | ||||

| 76 | ||||

| 76 | ||||

| 79 | ||||

| 79 | ||||

| 79 | ||||

| 80 | ||||

| 82 | ||||

| 85 | ||||

| 86 | ||||

| 86 | ||||

Please read this document carefully before you make any investment decision. If you have any questions, do not hesitate to contact a Matthews Asia Funds representative at 800.789.ASIA (2742) or visit matthewsasia.com.

Please keep this prospectus with your other account documents for future reference.

Table of Contents

| MATTHEWS ASIAN GROWTH AND INCOME FUND | 1 |

Table of Contents

| 2 | matthewsasia.com | 800.789.ASIA |

Table of Contents

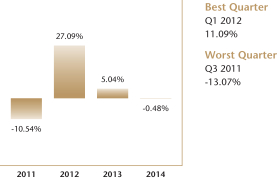

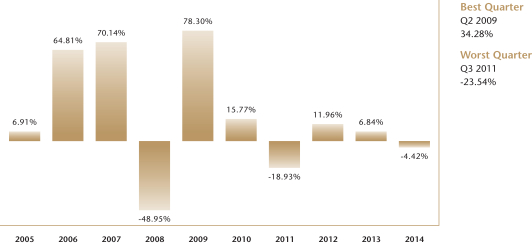

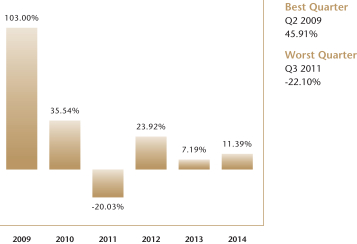

Past Performance

The bar chart below shows the Fund’s performance for each full calendar year since its inception and how it has varied from year to year, reflective of the Fund’s volatility and some indication of risk. Also shown are the best and worst quarters for this time period. The table below shows the Fund’s performance over certain periods of time, along with performance of its benchmark index. The index performance does not take into consideration fees, expenses or taxes. The information presented below is past performance, before and after taxes, and is not a prediction of future results. Both the bar chart and performance table assume reinvestment of all dividends and distributions. For the Fund’s most recent month-end performance, please visit matthewsasia.com or call 800.789.ASIA (2742).

ANNUAL RETURNS FOR YEARS ENDED 12/31

AVERAGE ANNUAL TOTAL RETURNS FOR PERIODS ENDED DECEMBER 31, 2014

| 1 year | Since Inception (10/29/10) |

|||||||

| Matthews Asian Growth and Income Fund |

||||||||

| Return before taxes |

-0.48% | 4.84% | ||||||

| Return after taxes on distributions1 |

-1.52% | 3.80% | ||||||

| Return after taxes on distributions and sale of Fund shares1 |

0.57% | 3.79% | ||||||

| MSCI All Country Asia Ex Japan Index |

||||||||

| (reflects no deduction for fees, expenses or taxes) | 5.11% | 3.39% | ||||||

| 1 | After-tax returns are calculated using the highest historical individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts. |

Investment Advisor

Matthews International Capital Management, LLC (“Matthews”)

Portfolio Managers

Lead Manager: Robert Horrocks, PhD, is Chief Investment Officer at Matthews and has been a Portfolio Manager of the Asian Growth and Income Fund since 2009.

Lead Manager: Kenneth Lowe, CFA, has been a Portfolio Manager of the Asian Growth and Income Fund since 2011.

For important information about the Purchase and Sale of Fund Shares; Taxes; and Payments to Broker-Dealers and Other Financial Intermediaries, please turn to page 44.

| MATTHEWS ASIAN GROWTH AND INCOME FUND | 3 |

Table of Contents

| 4 | matthewsasia.com | 800.789.ASIA |

Table of Contents

| MATTHEWS ASIA DIVIDEND FUND | 5 |

Table of Contents

Risks Associated with Medium-Size Companies: Medium-size companies may be subject to a number of risks not associated with larger, more established companies, potentially making their stock prices more volatile and increasing the risk of loss.

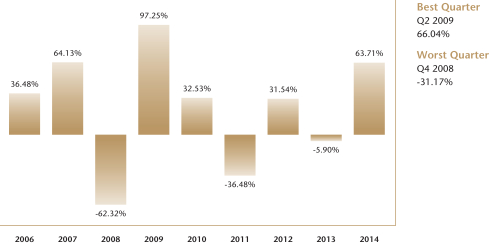

Past Performance

The bar chart below shows the Fund’s performance for each full calendar year since its inception and how it has varied from year to year, reflective of the Fund’s volatility and some indication of risk. Also shown are the best and worst quarters for this time period. The table below shows the Fund’s performance over certain periods of time, along with performance of its benchmark index. The index performance does not take into consideration fees, expenses or taxes. The information presented below is past performance, before and after taxes, and is not a prediction of future results. Both the bar chart and performance table assume reinvestment of all dividends and distributions. For the Fund’s most recent month-end performance, please visit matthewsasia.com or call 800.789.ASIA (2742).

ANNUAL RETURNS FOR YEARS ENDED 12/31

AVERAGE ANNUAL TOTAL RETURNS FOR PERIODS ENDED DECEMBER 31, 2014

| 1 year | Since Inception (10/29/10) |

|||||||

| Matthews Asia Dividend Fund |

||||||||

| Return before taxes |

-0.18% | 5.60% | ||||||

| Return after taxes on distributions1 |

-0.43% | 4.84% | ||||||

| Return after taxes on distributions and sale of Fund shares1 |

0.33% | 4.38% | ||||||

| MSCI All Country Asia Pacific Index |

||||||||

| (reflects no deduction for fees, expenses or taxes) | 0.29% | 4.37% | ||||||

| 1 | After-tax returns are calculated using the highest historical individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts. |

Investment Advisor

Matthews International Capital Management, LLC (“Matthews”)

Portfolio Managers

Lead Manager: Yu Zhang, CFA, has been a Portfolio Manager of the Asia Dividend Fund since 2011.

Lead Manager: Robert Horrocks, PhD, is Chief Investment Officer at Matthews and has been a Portfolio Manager of the Asia Dividend Fund since 2013.

Co-Manager: Vivek Tanneeru has been a Portfolio Manager of the Asia Dividend Fund since 2014.

For important information about the Purchase and Sale of Fund Shares; Taxes; and Payments to Broker-Dealers and Other Financial Intermediaries, please turn to page 44.

| 6 | matthewsasia.com | 800.789.ASIA |

Table of Contents

| MATTHEWS CHINA DIVIDEND FUND | 7 |

Table of Contents

| 8 | matthewsasia.com | 800.789.ASIA |

Table of Contents

adversely impact affected industries or companies. China’s economy, particularly its export-oriented industries, may be adversely impacted by trade or political disputes with China’s major trading partners, including the U.S. In addition, as its consumer class emerges, China’s domestically oriented industries may be especially sensitive to changes in government policy and investment cycles.

Hong Kong: If China were to exert its authority so as to alter the economic, political or legal structures or the existing social policy of Hong Kong, investor and business confidence in Hong Kong could be negatively affected, which in turn could negatively affect markets and business performance and have an adverse effect on the Fund’s investments.

Taiwan: Although the relationship between China and Taiwan has been improving, there is the potential for future political or economic disturbances that may have an adverse impact on the values of investments in either China or Taiwan, or make investments in China and Taiwan impractical or impossible.

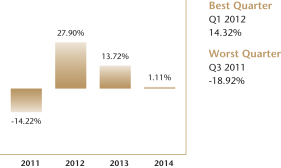

Past Performance

The bar chart below shows the Fund’s performance for each full calendar year since its inception and how it has varied from year to year, reflective of the Fund’s volatility and some indication of risk. Also shown are the best and worst quarters for this time period. The table below shows the Fund’s performance over certain periods of time, along with performance of its benchmark index. The index performance does not take into consideration fees, expenses or taxes. The information presented below is past performance, before and after taxes, and is not a prediction of future results. Both the bar chart and performance table assume reinvestment of all dividends and distributions. For the Fund’s most recent month-end performance, please visit matthewsasia.com or call 800.789.ASIA (2742).

ANNUAL RETURNS FOR YEARS ENDED 12/31

AVERAGE ANNUAL TOTAL RETURNS FOR PERIODS ENDED DECEMBER 31, 2014

| 1 year | Since Inception (10/29/10) |

|||||||

| Matthews China Dividend Fund |

||||||||

| Return before taxes |

1.11% | 6.70% | ||||||

| Return after taxes on distributions1 |

-0.25% | 5.62% | ||||||

| Return after taxes on distributions and sale of Fund shares1 |

0.93% | 4.94% | ||||||

| MSCI China Index |

||||||||

| (reflects no deduction for fees, expenses or taxes) | 8.26% | 2.26% | ||||||

| 1 | After-tax returns are calculated using the highest historical individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts. |

Investment Advisor

Matthews International Capital Management, LLC (“Matthews”)

Portfolio Managers

Lead Manager: Yu Zhang, CFA, has been a Portfolio Manager of the China Dividend Fund since 2012.

Co-Manager: Sherwood Zhang, CFA, has been a Portfolio Manager of the China Dividend Fund since 2014.

For important information about the Purchase and Sale of Fund Shares; Taxes; and Payments to Broker-Dealers and Other Financial Intermediaries, please turn to page 44.

| MATTHEWS CHINA DIVIDEND FUND | 9 |

Table of Contents

| 10 | matthewsasia.com | 800.789.ASIA |

Table of Contents

| MATTHEWS ASIA FOCUS FUND | 11 |

Table of Contents

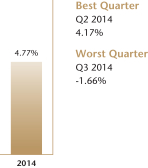

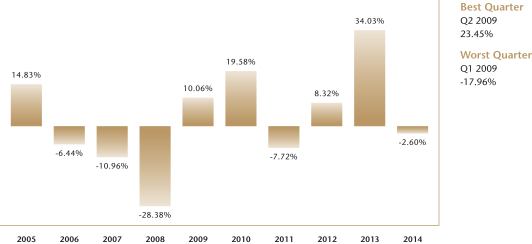

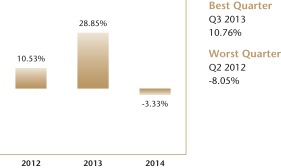

Past Performance

The bar chart below shows the Fund’s performance for each full calendar year since its inception and how it has varied from year to year, reflective of the Fund’s volatility and some indication of risk. Also shown are the best and worst quarters for this time period. The table below shows the Fund’s performance over certain periods of time, along with performance of its benchmark index. The index performance does not take into consideration fees, expenses or taxes. The information presented below is past performance, before and after taxes, and is not a prediction of future results. Both the bar chart and performance table assume reinvestment of all dividends and distributions. For the Fund’s most recent month-end performance, please visit matthewsasia.com or call 800.789.ASIA (2742).

ANNUAL RETURN FOR YEAR ENDED 12/31

AVERAGE ANNUAL TOTAL RETURNS FOR PERIODS ENDED DECEMBER 31, 2014

| 1 year | Since Inception (4/30/13) |

|||||||

| Matthews Asia Focus Fund |

||||||||

| Return before taxes |

4.77% | 1.29% | ||||||

| Return after taxes on distributions1 |

4.62% | 1.08% | ||||||

| Return after taxes on distributions and sale of Fund shares1 |

2.91% | 1.01% | ||||||

| MSCI All Country Asia Ex Japan |

||||||||

| (reflects no deduction for fees, expenses or taxes) | 5.11% | 4.24% | ||||||

| 1 | After-tax returns are calculated using the highest historical individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts. |

Investment Advisor

Matthews International Capital Management, LLC (“Matthews”)

Portfolio Managers

Lead Manager: Kenneth Lowe, CFA, has been a Portfolio Manager of the Asia Focus Fund since its inception in 2013.

Co-Manager: Michael J. Oh, CFA, has been a Portfolio Manager of the Asia Focus Fund since its inception in 2013.

Co-Manager: Sharat Shroff, CFA, has been a Portfolio Manager of the Asia Focus Fund since its inception in 2013.

For important information about the Purchase and Sale of Fund Shares; Taxes; and Payments to Broker-Dealers and Other Financial Intermediaries, please turn to page 44.

| 12 | matthewsasia.com | 800.789.ASIA |

Table of Contents

| MATTHEWS ASIA GROWTH FUND | 13 |

Table of Contents

| 14 | matthewsasia.com | 800.789.ASIA |

Table of Contents

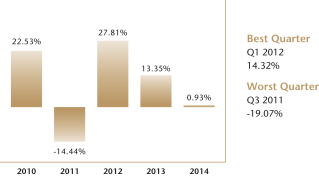

Past Performance

The bar chart below shows the Fund’s performance for each full calendar year since its inception and how it has varied from year to year, reflective of the Fund’s volatility and some indication of risk. Also shown are the best and worst quarters for this time period. The table below shows the Fund’s performance over certain periods of time, along with performance of its benchmark index. The index performance does not take into consideration fees, expenses or taxes. The information presented below is past performance, before and after taxes, and is not a prediction of future results. Both the bar chart and performance table assume reinvestment of all dividends and distributions. For the Fund’s most recent month-end performance, please visit matthewsasia.com or call 800.789.ASIA (2742).

ANNUAL RETURNS FOR YEARS ENDED 12/31

AVERAGE ANNUAL TOTAL RETURNS FOR PERIODS ENDED DECEMBER 31, 2014

| 1 year | Since Inception (10/29/10) |

|||||||

| Matthews Asia Growth Fund |

||||||||

| Return before taxes |

1.63% | 6.19% | ||||||

| Return after taxes on distributions1 |

1.02% | 5.74% | ||||||

| Return after taxes on distributions and sale of Fund shares1 |

1.16% | 4.73% | ||||||

| MSCI All Country Asia Pacific Index |

||||||||

| (reflects no deduction for fees, expenses or taxes) | 0.29% | 4.37% | ||||||

| 1 | After-tax returns are calculated using the highest historical individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts. |

Investment Advisor

Matthews International Capital Management, LLC (“Matthews”)

Portfolio Managers

Lead Manager: Taizo Ishida has been a Portfolio Manager of the Asia Growth Fund since 2007.

Co-Manager: Sharat Shroff, CFA, has been a Portfolio Manager of the Asia Growth Fund since 2007.

For important information about the Purchase and Sale of Fund Shares; Taxes; and Payments to Broker-Dealers and Other Financial Intermediaries, please turn to page 44.

| MATTHEWS ASIA GROWTH FUND | 15 |

Table of Contents

| 16 | matthewsasia.com | 800.789.ASIA |

Table of Contents

| MATTHEWS PACIFIC TIGER FUND | 17 |

Table of Contents

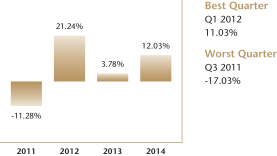

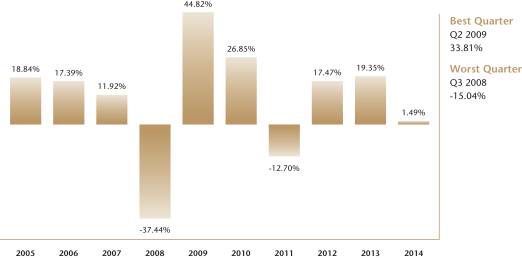

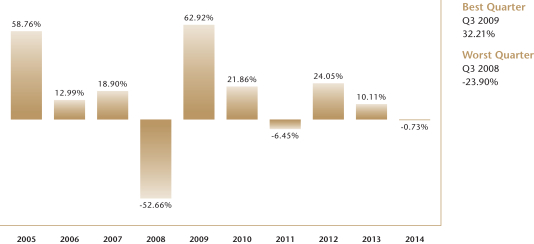

Past Performance

The bar chart below shows the Fund’s performance for each full calendar year since its inception and how it has varied from year to year, reflective of the Fund’s volatility and some indication of risk. Also shown are the best and worst quarters for this time period. The table below shows the Fund’s performance over certain periods of time, along with performance of its benchmark index. The index performance does not take into consideration fees, expenses or taxes. The information presented below is past performance, before and after taxes, and is not a prediction of future results. Both the bar chart and performance table assume reinvestment of all dividends and distributions. For the Fund’s most recent month-end performance, please visit matthewsasia.com or call 800.789.ASIA (2742).

ANNUAL RETURNS FOR YEARS ENDED 12/31

AVERAGE ANNUAL TOTAL RETURNS FOR PERIODS ENDED DECEMBER 31, 2014

| 1 year | Since Inception (10/29/10) |

|||||||

| Matthews Pacific Tiger Fund |

||||||||

| Return before taxes |

12.03% | 5.67% | ||||||

| Return after taxes on distributions1 |

10.79% | 5.29% | ||||||

| Return after taxes on distributions and sale of Fund shares1 |

8.02% | 4.58% | ||||||

| MSCI All Country Asia Ex Japan Index |

||||||||

| (reflects no deduction for fees, expenses or taxes) | 5.11% | 3.39% | ||||||

| 1 | After-tax returns are calculated using the highest historical individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts. |

Investment Advisor

Matthews International Capital Management, LLC (“Matthews”)

Portfolio Managers

Lead Manager: Sharat Shroff, CFA, has been a Portfolio Manager of the Pacific Tiger Fund since 2008.

Co-Manager: Richard Gao has been a Portfolio Manager of the Pacific Tiger Fund since 2006.

Co-Manager: In-Bok Song has been a Portfolio Manager of the Pacific Tiger Fund since 2014.

Co-Manager: Rahul Gupta has been a Portfolio Manager of the Pacific Tiger Fund since 2015.

For important information about the Purchase and Sale of Fund Shares; Taxes; and Payments to Broker-Dealers and Other Financial Intermediaries, please turn to page 44.

| 18 | matthewsasia.com | 800.789.ASIA |

Table of Contents

| MATTHEWS ASIA ESG FUND | 19 |

Table of Contents

| 20 | matthewsasia.com | 800.789.ASIA |

Table of Contents

Volatility: The smaller size and lower levels of liquidity in emerging markets, as well as other factors, may result in changes in the prices of Asian securities that are more volatile than those of companies in more developed regions. This volatility can cause the price of the Fund’s shares (NAV) to go up or down dramatically. Because of this volatility, it is recommended that you invest in the Fund only for the long term (at least five years).

Responsible Investing Risk: The Fund’s consideration of ESG factors in making its investment decisions may affect the Fund’s exposure to certain issuers, industries, sectors, regions or countries and may impact the Fund’s relative investment performance—positively or negatively—depending on whether such investments are in or out of favor in the market. Although an investment by the Fund in a company may satisfy one or more ESG standards in the view of the portfolio managers, that same company may also fail to satisfy other ESG standards, in some cases even egregiously.

Convertible Securities: The Fund may invest in convertible preferred stocks, and convertible bonds and debentures. The risks of convertible bonds and debentures include repayment risk and interest rate risk. Many Asian convertible securities are not rated by rating agencies like Moody’s Investors Service, Inc. (“Moody’s”), Standard and Poor’s Corporation (“S&P”) and Fitch Inc. (“Fitch”), or, if they are rated, they may be rated below investment grade (these are referred to as “junk bonds,” which are primarily speculative securities, and include unrated securities, regardless of quality), which may have a greater risk of default. Investments in convertible securities may also subject the Fund to currency risk and risks associated with foreign exchange rate. Convertible securities may trade less frequently and in lower volumes, making it difficult for the Fund to value those securities.

Interest Rate Risk: Fixed-income securities may decline in value because of changes in interest rates. Bond prices generally rise when interest rates decline and generally decline when interest rates rise.

High Yield Securities Risk: High yield securities or unrated securities of similar credit quality (commonly known as “junk bonds”) are more likely to default than higher rated securities. These securities typically entail greater potential price volatility and are considered predominantly speculative. They may also be more susceptible to adverse economic and competitive industry conditions than higher-rated securities.

Risks Associated with Smaller and Medium-Size Companies: Smaller and medium-size companies may be subject to a number of risks not associated with larger, more established companies, potentially making their stock prices more volatile and increasing the risk of loss.

Past Performance

The Fund is new and does not have a full calendar year of performance or financial information to present. Once it has been in operation for a full calendar year, performance (including total return) and financial information will be presented. The Fund’s primary benchmark index is MSCI All Country Asia Ex Japan Index.

Investment Advisor

Matthews International Capital Management, LLC (“Matthews”)

Portfolio Managers

Lead Manager: Vivek Tanneeru has been a Portfolio Manager of the Matthews Asia ESG Fund since its inception in 2015.

Co-Manager: Winnie Chwang has been a Portfolio Manager of the Matthews Asia ESG Fund since its inception in 2015.

For important information about the Purchase and Sale of Fund Shares; Taxes; and Payments to Broker-Dealers and Other Financial Intermediaries, please turn to page 44.

| MATTHEWS ASIA ESG FUND | 21 |

Table of Contents

| 22 | matthewsasia.com | 800.789.ASIA |

Table of Contents

| MATTHEWS EMERGING ASIA FUND | 23 |

Table of Contents

Risks Associated with Smaller Companies: Smaller companies may offer substantial opportunities for capital growth; they also involve substantial risks, and investments in smaller companies may be considered speculative. Such companies often have limited product lines, markets or financial resources. Smaller companies may be more dependent on one or few key persons and may lack depth of management. Larger portions of their stock may be held by a small number of investors (including founders and management) than is typical of larger companies. Credit may be more difficult to obtain (and on less advantageous terms) than for larger companies. As a result, the influence of creditors (and the impact of financial or operating restrictions associated with debt financing) may be greater than in larger or more established companies. The Fund may have more difficulty obtaining information about smaller companies, making it more difficult to evaluate the impact of market, economic, regulatory and other factors on them. Informational difficulties may also make valuing or disposing of their securities more difficult than it would for larger companies. Securities of smaller companies may trade less frequently and in lesser volume than more widely held securities and the securities of such companies generally are subject to more abrupt or erratic price movements than more widely held or larger, more established companies or the market indices in general. The value of securities of smaller companies may react differently to political, market and economic developments than the markets as a whole or than other types of stocks.

Risks Associated with Micro-Cap Companies: Investments in micro-cap companies are subject to the same types of risks described above for investments in smaller companies, but the likelihood of losses from such risks is even greater for micro-cap companies.

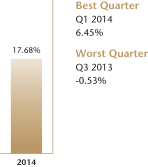

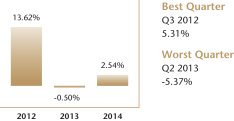

Past Performance

The bar chart below shows the Fund’s performance for each full calendar year since its inception and how it has varied from year to year, reflective of the Fund’s volatility and some indication of risk. Also shown are the best and worst quarters for this time period. The table below shows the Fund’s performance over certain periods of time, along with performance of its benchmark index. The index performance does not take into consideration fees, expenses or taxes. The information presented below is past performance, before and after taxes, and is not a prediction of future results. Both the bar chart and performance table assume reinvestment of all dividends and distributions. For the Fund’s most recent month-end performance, please visit matthewsasia.com or call 800.789.ASIA (2742).

ANNUAL RETURN FOR YEAR ENDED 12/31

AVERAGE ANNUAL TOTAL RETURNS FOR PERIODS ENDED DECEMBER 31, 2014

| 1 year | Since Inception (4/30/13) |

|||||||

| Matthews Emerging Asia Fund |

||||||||

| Return before taxes |

17.68% | 9.87% | ||||||

| Return after taxes on distributions1 |

17.59% | 9.85% | ||||||

| Return after taxes on distributions and sale of Fund shares1 |

10.24% | 7.66% | ||||||

| MSCI Emerging Markets Asia Index |

||||||||

| (reflects no deduction for fees, expenses or taxes) | 5.27% | 4.43% | ||||||

| 1 | After-tax returns are calculated using the highest historical individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts. |

| 24 | matthewsasia.com | 800.789.ASIA |

Table of Contents

Investment Advisor

Matthews International Capital Management, LLC (“Matthews”)

Portfolio Managers

Lead Manager: Taizo Ishida has been a Portfolio Manager of the Emerging Asia Fund since its inception in 2013.

Co-Manager: Robert Harvey, CFA, has been a Portfolio Manager of the Emerging Asia Fund since its inception in 2013.

For important information about the Purchase and Sale of Fund Shares; Taxes; and Payments to Broker-Dealers and Other Financial Intermediaries, please turn to page 44.

| MATTHEWS EMERGING ASIA FUND | 25 |

Table of Contents

| 26 | matthewsasia.com | 800.789.ASIA |

Table of Contents

| MATTHEWS CHINA FUND | 27 |

Table of Contents

Past Performance

The bar chart below shows the Fund’s performance for each full calendar year since its inception and how it has varied from year to year, reflective of the Fund’s volatility and some indication of risk. Also shown are the best and worst quarters for this time period. The table below shows the Fund’s performance over certain periods of time, along with performance of its benchmark index. The index performance does not take into consideration fees, expenses or taxes. The information presented below is past performance, before and after taxes, and is not a prediction of future results. Both the bar chart and performance table assume reinvestment of all dividends and distributions. For the Fund’s most recent month-end performance, please visit matthewsasia.com or call 800.789.ASIA (2742).

ANNUAL RETURNS FOR YEARS ENDED 12/31

AVERAGE ANNUAL TOTAL RETURNS FOR PERIODS ENDED DECEMBER 31, 2014

| 1 year | Since Inception (10/29/10) |

|||||||

| Matthews China Fund |

||||||||

| Return before taxes |

-4.22% | -2.02% | ||||||

| Return after taxes on distributions1 |

-4.71% | -3.17% | ||||||

| Return after taxes on distributions and sale of Fund shares1 |

-2.11% | -1.37% | ||||||

| MSCI China Index |

||||||||

| (reflects no deduction for fees, expenses or taxes) | 8.26% | 2.26% | ||||||

| 1 | After-tax returns are calculated using the highest historical individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts. |

Investment Advisor

Matthews International Capital Management, LLC (“Matthews”)

Portfolio Managers

Lead Manager: Richard Gao has been a Portfolio Manager of the China Fund since 1999.

Co-Manager: Henry Zhang, CFA, has been a Portfolio Manager of the China Fund since 2010.

Co-Manager: Winnie Chwang has been a Portfolio Manager of the China Fund since 2014.

Co-Manager: Andrew Mattock, CFA, has been a Portfolio Manager of the China Fund since 2015.

For important information about the Purchase and Sale of Fund Shares; Taxes; and Payments to Broker-Dealers and Other Financial Intermediaries, please turn to page 44.

| 28 | matthewsasia.com | 800.789.ASIA |

Table of Contents

| MATTHEWS INDIA FUND | 29 |

Table of Contents

| 30 | matthewsasia.com | 800.789.ASIA |

Table of Contents

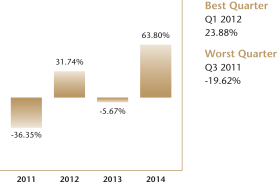

Past Performance

The bar chart below shows the Fund’s performance for each full calendar year since its inception and how it has varied from year to year, reflective of the Fund’s volatility and some indication of risk. Also shown are the best and worst quarters for this time period. The table below shows the Fund’s performance over certain periods of time, along with performance of its benchmark index. The index performance does not take into consideration fees, expenses or taxes. The information presented below is past performance, before and after taxes, and is not a prediction of future results. Both the bar chart and performance table assume reinvestment of all dividends and distributions. For the Fund’s most recent month-end performance, please visit matthewsasia.com or call 800.789.ASIA (2742).

ANNUAL RETURNS FOR YEARS ENDED 12/31

AVERAGE ANNUAL TOTAL RETURNS FOR PERIODS ENDED DECEMBER 31, 2014

| 1 year | Since Inception (10/29/10) |

|||||||

| Matthews India Fund |

||||||||

| Return before taxes |

63.80% | 5.89% | ||||||

| Return after taxes on distributions1 |

63.47% | 5.62% | ||||||

| Return after taxes on distributions and sale of Fund shares1 |

36.38% | 4.56% | ||||||

| S&P Bombay Stock Exchange 100 Index |

||||||||

| (reflects no deduction for fees, expenses or taxes) | 31.40% | 0.34% | ||||||

| 1 | After-tax returns are calculated using the highest historical individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts. |

Investment Advisor

Matthews International Capital Management, LLC (“Matthews”)

Portfolio Managers

Lead Manager: Sunil Asnani has been a Portfolio Manager of the India Fund since 2010.

Co-Manager: Sharat Shroff, CFA, has been a Portfolio Manager of the India Fund since 2006.

For important information about the Purchase and Sale of Fund Shares; Taxes; and Payments to Broker-Dealers and Other Financial Intermediaries, please turn to page 44.

| MATTHEWS INDIA FUND | 31 |

Table of Contents

| 32 | matthewsasia.com | 800.789.ASIA |

Table of Contents

| MATTHEWS JAPAN FUND | 33 |

Table of Contents

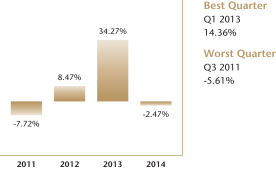

Past Performance

The bar chart below shows the Fund’s performance for each full calendar year since its inception and how it has varied from year to year, reflective of the Fund’s volatility and some indication of risk. Also shown are the best and worst quarters for this time period. The table below shows the Fund’s performance over certain periods of time, along with performance of its benchmark index. The index performance does not take into consideration fees, expenses or taxes. The information presented below is past performance, before and after taxes, and is not a prediction of future results. Both the bar chart and performance table assume reinvestment of all dividends and distributions. For the Fund’s most recent month-end performance, please visit matthewsasia.com or call 800.789.ASIA (2742).

ANNUAL RETURNS FOR YEARS ENDED 12/31

AVERAGE ANNUAL TOTAL RETURNS FOR PERIODS ENDED DECEMBER 31, 2014

| 1 year | Since Inception (10/29/10) |

|||||||

| Matthews Japan Fund |

||||||||

| Return before taxes |

-2.47% | 9.45% | ||||||

| Return after taxes on distributions1 |

-2.57% | 8.96% | ||||||

| Return after taxes on distributions and sale of Fund shares1 |

-1.25% | 7.37% | ||||||

| MSCI Japan Index |

||||||||

| (reflects no deduction for fees, expenses or taxes) | -3.72% | 5.55% | ||||||

| 1 | After-tax returns are calculated using the highest historical individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts. |

Investment Advisor

Matthews International Capital Management, LLC (“Matthews”)

Portfolio Managers

Lead Manager: Kenichi Amaki has been a Portfolio Manager of the Japan Fund since 2010.

Co-Manager: Taizo Ishida has been a Portfolio Manager of the Japan Fund since 2006.

For important information about the Purchase and Sale of Fund Shares; Taxes; and Payments to Broker-Dealers and Other Financial Intermediaries, please turn to page 44.

| 34 | matthewsasia.com | 800.789.ASIA |

Table of Contents

| MATTHEWS KOREA FUND | 35 |

Table of Contents

| 36 | matthewsasia.com | 800.789.ASIA |

Table of Contents

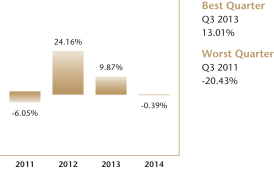

Past Performance

The bar chart below shows the Fund’s performance for each full calendar year since its inception and how it has varied from year to year, reflective of the Fund’s volatility and some indication of risk. Also shown are the best and worst quarters for this time period. The table below shows the Fund’s performance over certain periods of time, along with performance of its benchmark index. The index performance does not take into consideration fees, expenses or taxes. The information presented below is past performance, before and after taxes, and is not a prediction of future results. Both the bar chart and performance table assume reinvestment of all dividends and distributions. For the Fund’s most recent month-end performance, please visit matthewsasia.com or call 800.789.ASIA (2742).

ANNUAL RETURNS FOR YEARS ENDED 12/31

AVERAGE ANNUAL TOTAL RETURNS FOR PERIODS ENDED DECEMBER 31, 2014

| 1 year | Since Inception (10/29/10) |

|||||||

| Matthews Korea Fund |

||||||||

| Return before taxes |

-0.39% | 8.13% | ||||||

| Return after taxes on distributions1 |

-1.41% | 7.40% | ||||||

| Return after taxes on distributions and sale of Fund shares1 |

0.59% | 6.54% | ||||||

| Korea Composite Stock Price Index2 |

||||||||

| (reflects no deduction for fees, expenses or taxes) | -7.25% | 2.52% | ||||||

| 1 | After-tax returns are calculated using the highest historical individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts. |

| 2 | Korea Composite Stock Price Index performance data may be readjusted periodically by the Korea Exchange due to certain factors, including the declaration of dividends. |

Investment Advisor

Matthews International Capital Management, LLC (“Matthews”)

Portfolio Managers

Lead Manager: Michael J. Oh, CFA, has been a Portfolio Manager of the Korea Fund since 2007.

Co-Manager: Michael Han, CFA, has been a Portfolio Manager of the Korea Fund since 2008.

For important information about the Purchase and Sale of Fund Shares; Taxes; and Payments to Broker-Dealers and Other Financial Intermediaries, please turn to page 44.

| MATTHEWS KOREA FUND | 37 |

Table of Contents

| 38 | matthewsasia.com | 800.789.ASIA |

Table of Contents

| MATTHEWS ASIA SMALL COMPANIES FUND | 39 |

Table of Contents

Past Performance

The bar chart below shows the Fund’s performance for each full calendar year since its inception and how it has varied from year to year, reflective of the Fund’s volatility and some indication of risk. Also shown are the best and worst quarters for this time period. The table below shows the Fund’s performance over certain periods of time, along with performance of its benchmark index. The index performance does not take into consideration fees, expenses or taxes. The information presented below is past performance, before and after taxes, and is not a prediction of future results. Both the bar chart and performance table assume reinvestment of all dividends and distributions. For the Fund’s most recent month-end performance, please visit matthewsasia.com or call 800.789.ASIA (2742).

ANNUAL RETURN FOR YEAR ENDED 12/31

AVERAGE ANNUAL TOTAL RETURNS FOR PERIODS ENDED DECEMBER 31, 2014

| 1 year | Since Inception (4/30/13) |

|||||||

| Matthews Asia Small Companies Fund |

||||||||

| Return before taxes |

11.65% | 6.90% | ||||||

| Return after taxes on distributions1 |

11.61% | 6.81% | ||||||

| Return after taxes on distributions and sale of Fund shares1 |

6.83% | 5.38% | ||||||

| MSCI All Country Asia Ex Japan Small Cap Index |

||||||||

| (reflects no deduction for fees, expenses or taxes) | 2.56% | 0.66% | ||||||

| 1 | After-tax returns are calculated using the highest historical individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts. |

Investment Advisor

Matthews International Capital Management, LLC (“Matthews”)

Portfolio Managers

Lead Manager: Lydia So, CFA, has been a Portfolio Manager of the Asia Small Companies Fund since its inception in 2008.

Co-Manager: Kenichi Amaki has been a Portfolio Manager of the Asia Small Companies Fund since 2013.

Co-Manager: Beini Zhou, CFA, has been a Portfolio Manager of the Asia Small Companies Fund since 2014.

For important information about the Purchase and Sale of Fund Shares; Taxes; and Payments to Broker-Dealers and Other Financial Intermediaries, please turn to page 44.

| 40 | matthewsasia.com | 800.789.ASIA |

Table of Contents

| MATTHEWS ASIA SCIENCE AND TECHNOLOGY FUND | 41 |

Table of Contents

| 42 | matthewsasia.com | 800.789.ASIA |

Table of Contents

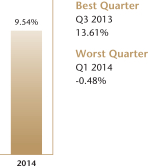

Past Performance

The bar chart below shows the Fund’s performance for each full calendar year since its inception and how it has varied from year to year, reflective of the Fund’s volatility and some indication of risk. Also shown are the best and worst quarters for this time period. The table below shows the Fund’s performance over certain periods of time, along with performance of its benchmark index and an index of Asian equities tracking a range of technology stocks. The index performance does not take into consideration fees, expenses or taxes. The information presented below is past performance, before and after taxes, and is not a prediction of future results. Both the bar chart and performance table assume reinvestment of all dividends and distributions. For the Fund’s most recent month-end performance, please visit matthewsasia.com or call 800.789.ASIA (2742).

ANNUAL RETURN FOR YEAR ENDED 12/31

AVERAGE ANNUAL TOTAL RETURNS FOR PERIODS ENDED DECEMBER 31, 2014

| 1 year | Since Inception (4/30/13) |

|||||||

| Matthews Asia Science and Technology Fund |

||||||||

| Return before taxes |

9.54% | 20.68% | ||||||

| Return after taxes on distributions1 |

9.25% | 20.51% | ||||||

| Return after taxes on distributions and sale of Fund shares1 |

5.70% | 16.07% | ||||||

| MSCI All Country Asia Index (reflects no deduction for fees, expenses or taxes) |

0.84% | 2.48% | ||||||

| MSCI All Country Asia Information Technology Index |

||||||||

| (reflects no deduction for fees, expenses or taxes) | 8.19% | 11.50% | ||||||

| 1 | After-tax returns are calculated using the highest historical individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns shown are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts. |

Investment Advisor

Matthews International Capital Management, LLC (“Matthews”)

Portfolio Managers

Lead Manager: Michael J. Oh, CFA, has been a Portfolio Manager of the Asia Science and Technology Fund since 2006.

Co-Manager: Lydia So, CFA, has been a Portfolio Manager of the Asia Science and Technology Fund since 2008.

For important information about the Purchase and Sale of Fund Shares; Taxes; and Payments to Broker-Dealers and Other Financial Intermediaries, please turn to page 44.

| MATTHEWS ASIA SCIENCE AND TECHNOLOGY FUND | 43 |

Table of Contents

Important Information

Purchase and Sale of Fund Shares

You may purchase and sell Fund shares directly through the Fund’s transfer agent by calling 800.789.ASIA (2742) or online at matthewsasia.com. Fund shares may also be purchased and sold through various securities brokers and benefit plan administrators or their sub-agents. You may purchase and redeem Fund shares by electronic bank transfer, check, or wire. The minimum initial and subsequent investment amounts for various types of accounts offered by the Fund are shown below.

| Minimum Initial Investment | Subsequent Investments | |

| $3,000,000 | $100 |

Minimum amount may be lower for purchases through certain financial intermediaries and different minimums may apply for retirement plans and other arrangements subject to criteria set by Matthews.

Tax Information

The Fund’s distributions are taxable, and will be taxed as ordinary income or capital gains, unless you are investing through a tax-deferred arrangement, such as a 401(k) plan or an individual retirement account. Tax-deferred arrangements may be taxed later upon withdrawal from those accounts.

Payments to Broker-Dealers and Other Financial Intermediaries

If you purchase Fund shares through a broker-dealer or other financial intermediary (such as a bank), Matthews may pay the intermediary for the sale of Fund shares and related services. Shareholders who purchase or hold Fund shares through an intermediary may inquire about such payments from that intermediary. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your salesperson to recommend the Fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

| 44 | matthewsasia.com | 800.789.ASIA |

Table of Contents

The financial highlights tables are intended to help you understand the Funds’ financial performance for the past 5 years or, if shorter, the period of the applicable Funds’ operations. Certain information reflects financial results for a single Fund share. The total returns in the tables represent the rate that an investor would have earned (or lost) on an investment in a Fund (assuming reinvestment of all dividends and distributions). This information has been audited by PricewaterhouseCoopers, LLP, the Funds’ independent registered public accounting firm, whose report, along with the Funds’ financial statements, are included in the Funds’ annual report, which is available upon request.

Matthews Asian Growth and Income Fund

The table below sets forth financial data for a share of beneficial interest outstanding throughout each period presented.

| Year Ended Dec. 31, |

Period Ended Dec. 31, 20101 |

|||||||||||||||||||

| 2014 | 2013 | 2012 | 2011 | |||||||||||||||||

| Net Asset Value, beginning of period | $18.90 | $18.60 | $15.06 | $18.04 | $18.13 | |||||||||||||||

| Income (loss) from investment operations: | ||||||||||||||||||||

| Net investment income (loss)2 |

0.42 | 0.44 | 0.45 | 0.52 | 0.07 | |||||||||||||||

| Net realized gain (loss) and unrealized appreciation/ |

(0.50) | 0.48 | 3.58 | (2.39) | 0.37 | |||||||||||||||

| Total from investment operations |

(0.08) | 0.92 | 4.03 | (1.87) | 0.44 | |||||||||||||||

| Less distributions from: | ||||||||||||||||||||

| Net investment income |

(0.38) | (0.50) | (0.49) | (0.50) | (0.29) | |||||||||||||||

| Net realized gains on investments |

(0.44) | (0.12) | — | (0.61) | (0.24) | |||||||||||||||

| Total distributions |

(0.82) | (0.62) | (0.49) | (1.11) | (0.53) | |||||||||||||||

| Paid-in capital from redemption fees | — | 3 | — | 3 | — | 3 | — | 3 | — | |||||||||||

| Net Asset Value, end of period | $18.00 | $18.90 | $18.60 | $15.06 | $18.04 | |||||||||||||||

| Total return* |

(0.48%) | 5.04% | 27.09% | (10.54%) | 2.49% | 4 | ||||||||||||||

| *The total return represents the rate that an investor would have earned (or lost) on an investment in the Fund assuming reinvestment of all dividends and distributions. | ||||||||||||||||||||

| RATIOS/SUPPLEMENTAL DATA | ||||||||||||||||||||

| Net assets, end of period (in 000s) | $1,182,690 | $1,120,218 | $856,876 | $531,493 | $128,417 | |||||||||||||||

| Ratio of expenses to average net assets before any reimbursement or waiver or recapture of expenses by Advisor and Administrator | 0.92% | 0.93% | 0.97% | 0.99% | 0.93% | 5 | ||||||||||||||

| Ratio of expenses to average net assets after any reimbursement or waiver or recapture of expenses by Advisor and Administrator | 0.92% | 0.93% | 0.97% | 0.99% | 0.93% | 5 | ||||||||||||||

| Ratio of net investment income (loss) to average net assets | 2.19% | 2.30% | 2.69% | 3.05% | 2.46% | 5 | ||||||||||||||

| Portfolio turnover6 | 16.79% | 15.27% | 17.43% | 16.54% | 19.84% | 4 | ||||||||||||||

1 Institutional Shares commenced operations on October 29, 2010.

2 Calculated using the average daily shares method.

3 Less than $0.01 per share.

4 Not annualized.

5 Annualized.

6 The portfolio turnover rate is calculated on the Fund as a whole without distinguishing between classes of shares issued.

| FINANCIAL HIGHLIGHTS | 45 |

Table of Contents

Matthews Asia Dividend Fund

The table below sets forth financial data for a share of beneficial interest outstanding throughout each period presented.

| Year Ended Dec. 31, | Period Ended Dec. 31, 20102 |

|||||||||||||||||||

| 20141 | 2013 | 2012 | 2011 | |||||||||||||||||

| Net Asset Value, beginning of period | $15.59 | $14.57 | $12.48 | $14.33 | $14.13 | |||||||||||||||

| Income (loss) from investment operations: | ||||||||||||||||||||

| Net investment income (loss)3 |

0.32 | 0.34 | 0.37 | 0.41 | 0.09 | |||||||||||||||

| Net realized gain (loss) and unrealized appreciation/ |

(0.33) | 1.30 | 2.29 | (1.82) | 0.32 | |||||||||||||||

| Total from investment operations |

(0.01) | 1.64 | 2.66 | (1.41) | 0.41 | |||||||||||||||

| Less distributions from: | ||||||||||||||||||||

| Net investment income |

(0.25) | (0.62) | (0.57) | (0.38) | (0.17) | |||||||||||||||

| Return of capital |

(0.07) | — | — | — | — | |||||||||||||||

| Net realized gains on investments |

— | — | — | (0.06) | (0.04) | |||||||||||||||

| Total distributions |

(0.32) | (0.62) | (0.57) | (0.44) | (0.21) | |||||||||||||||

| Paid-in capital from redemption fees4 | — | — | — | — | — | |||||||||||||||

| Net Asset Value, end of period | $15.26 | $15.59 | $14.57 | $12.48 | $14.33 | |||||||||||||||

| Total return* |

(0.18%) | 11.43% | 21.70% | (9.93%) | 2.95% | 5 | ||||||||||||||

| *The total return represents the rate that an investor would have earned (or lost) on an investment in the Fund assuming reinvestment of all dividends and distributions. | ||||||||||||||||||||

| RATIOS/SUPPLEMENTAL DATA | ||||||||||||||||||||

| Net assets, end of period (in 000s) | $2,107,371 | $2,124,214 | $922,561 | $344,502 | $48,293 | |||||||||||||||

| Ratio of expenses to average net assets before any reimbursement, waiver or recapture of expenses by Advisor and Administrator | 0.93% | 0.93% | 0.97% | 1.00% | 1.02% | 6 | ||||||||||||||

| Ratio of expenses to average net assets after any reimbursement, waiver or recapture of expenses by Advisor and Administrator | 0.93% | 0.93% | 0.97% | 1.00% | 1.02% | 6 | ||||||||||||||

| Ratio of net investment income (loss) to average net assets | 2.02% | 2.17% | 2.72% | 3.03% | 3.86% | 6 | ||||||||||||||

| Portfolio turnover7 | 20.06% | 14.06% | 9.17% | 16.48% | 10.48% | 5 | ||||||||||||||

1 Consolidated Financial Highlights.

2 Institutional Shares commenced operations on October 29, 2010.

3 Calculated using the average daily shares method.

4 Less than $0.01 per share.

5 Not annualized.

6 Annualized.

7 The portfolio turnover rate is calculated on the Fund as a whole without distinguishing between classes of shares issued.

| 46 | matthewsasia.com | 800.789.ASIA |

Table of Contents

Matthews China Dividend Fund

The table below sets forth financial data for a share of beneficial interest outstanding throughout each period presented.

| Year Ended Dec. 31, |

Period Ended Dec. 31, 20101 |

|||||||||||||||||||

| 2014 | 2013 | 2012 | 2011 | |||||||||||||||||

| Net Asset Value, beginning of period | $13.74 | $12.34 | $10.06 | $12.17 | $11.87 | |||||||||||||||

| Income (loss) from investment operations: | ||||||||||||||||||||

| Net investment income (loss)2 |

0.28 | 0.33 | 0.22 | 0.30 | — | 3 | ||||||||||||||

| Net realized gain (loss) and unrealized appreciation/ |

(0.13) | 1.32 | 2.53 | (2.01) | 0.47 | |||||||||||||||

| Total from investment operations |

0.15 | 1.65 | 2.75 | (1.71) | 0.47 | |||||||||||||||

| Less distributions from: | ||||||||||||||||||||

| Net investment income |

(0.38) | (0.26) | (0.48) | (0.38) | (0.13) | |||||||||||||||

| Net realized gains on investments |

(0.14) | — | — | (0.02) | (0.04) | |||||||||||||||

| Total distributions |

(0.52) | (0.26) | (0.48) | (0.40) | (0.17) | |||||||||||||||

| Paid-in capital from redemption fees | — | 3 | 0.01 | 0.01 | — | 3 | — | |||||||||||||

| Net Asset Value, end of period | $13.37 | $13.74 | $12.34 | $10.06 | $12.17 | |||||||||||||||

| Total return* |

1.11% | 13.72% | 27.90% | (14.22%) | 3.91% | 4 | ||||||||||||||

| *The total return represents the rate that an investor would have earned (or lost) on an investment in the Fund assuming reinvestment of all dividends and distributions. | ||||||||||||||||||||

| RATIOS/SUPPLEMENTAL DATA | ||||||||||||||||||||

| Net assets, end of period (in 000s) | $30,662 | $24,790 | $201 | $12 | $4 | |||||||||||||||

| Ratio of expenses to average net assets | 1.01% | 1.08% | 1.29% | 1.31% | 1.24% | 5 | ||||||||||||||

| Ratio of net investment income (loss) to average net assets | 2.06% | 2.54% | 1.87% | 2.61% | (0.06%) | 5 | ||||||||||||||

| Portfolio turnover6 | 25.43% | 20.52% | 21.40% | 22.31% | 6.84% | 4 | ||||||||||||||

1 Institutional Shares commenced operations on October 29, 2010.

2 Calculated using the average daily shares method.

3 Less than $0.01 per share.

4 Not annualized.

5 Annualized.

6 The portfolio turnover rate is calculated on the Fund as a whole without distinguishing between classes of shares issued.

| FINANCIAL HIGHLIGHTS | 47 |

Table of Contents

Matthews Asia Focus Fund

The table below sets forth financial data for a share of beneficial interest outstanding throughout the period presented.

| Year Ended Dec. 31, 2014 |

Period

Ended Dec. 31, 20131 |

|||||||

| Net Asset Value, beginning of period | $9.66 | $10.00 | ||||||

| Income (loss) from investment operations: | ||||||||

| Net investment income (loss)2 |

0.10 | 0.05 | ||||||

| Net realized gain (loss) and unrealized appreciation/depreciation on investments and foreign currency |

0.36 | (0.30) | ||||||

| Total from investment operations |

0.46 | (0.25) | ||||||

| Less distributions from: | ||||||||

| Net investment income |

(0.08) | (0.09) | ||||||

| Total distributions |

(0.08) | (0.09) | ||||||

| Paid-in capital from redemption fees | — | 3 | — | 3 | ||||

| Net Asset Value, end of period | $10.04 | $9.66 | ||||||

| Total return* |

4.77% | (2.48%) | 4 | |||||

| *The total return represents the rate that an investor would have earned (or lost) on an investment in the Fund assuming reinvestment of all dividends and distributions. | ||||||||

| RATIOS/SUPPLEMENTAL DATA | ||||||||

| Net assets, end of period (in 000s) | $7,148 | $2,118 | ||||||

| Ratio of expenses to average net assets before any reimbursement, waiver or recapture of expenses by Advisor and Administrator | 1.94% | 3.32% | 5 | |||||

| Ratio of expenses to average net assets after any reimbursement, waiver or recapture of expenses by Advisor and Administrator | 1.31% | 1.50% | 5 | |||||

| Ratio of net investment income (loss) to average net assets | 0.96% | 0.79% | 5 | |||||

| Portfolio turnover6 | 24.12% | 16.23% | 4 | |||||

1 Commenced operations on April 30, 2013.

2 Calculated using the average daily shares method.

3 Less than $0.01 per share.

4 Not annualized.

5 Annualized.

6 The portfolio turnover rate is calculated on the Fund as a whole without distinguishing between classes of shares issued.

| 48 | matthewsasia.com | 800.789.ASIA |

Table of Contents

Matthews Asia Growth Fund

The table below sets forth financial data for a share of beneficial interest outstanding throughout each period presented.

| Year Ended Dec. 31, | Period Ended Dec. 31, 20101 |

|||||||||||||||||||

| 2014 | 2013 | 2012 | 2011 | |||||||||||||||||

| Net Asset Value, beginning of period | $21.26 | $18.08 | $15.37 | $17.98 | $17.65 | |||||||||||||||

| Income (loss) from investment operations: | ||||||||||||||||||||

| Net investment income (loss)2 |

0.16 | 0.15 | 0.17 | 0.14 | 0.01 | |||||||||||||||

| Net realized gain (loss) and unrealized appreciation/ |

0.19 | 3.39 | 2.54 | (2.42) | 0.47 | |||||||||||||||

| Total from investment operations |

0.35 | 3.54 | 2.71 | (2.28) | 0.48 | |||||||||||||||

| Less distributions from: | ||||||||||||||||||||

| Net investment income |

(0.42) | (0.36) | — | (0.35) | (0.15) | |||||||||||||||

| Total distributions |

(0.42) | (0.36) | — | (0.35) | (0.15) | |||||||||||||||

| Paid-in capital from redemption fees | — | 3 | — | 3 | — | 3 | 0.02 | — | ||||||||||||

| Net Asset Value, end of period | $21.19 | $21.26 | $18.08 | $15.37 | $17.98 | |||||||||||||||

| Total return* |

1.63% | 19.63% | 17.63% | (12.58%) | 2.76% | 4 | ||||||||||||||

| *The total return represents the rate that an investor would have earned (or lost) on an investment in the Fund assuming reinvestment of all dividends and distributions. | ||||||||||||||||||||

| RATIOS/SUPPLEMENTAL DATA | ||||||||||||||||||||

| Net assets, end of period (in 000s) | $287,262 | $227,852 | $147,142 | $84,302 | $8,853 | |||||||||||||||

| Ratio of expenses to average net assets | 0.91% | 0.93% | 0.98% | 1.03% | 0.99% | 5 | ||||||||||||||

| Ratio of net investment income (loss) to average net assets | 0.74% | 0.73% | 1.02% | 0.84% | 0.37% | 5 | ||||||||||||||

| Portfolio turnover6 | 22.24% | 10.77% | 44.76% | 28.06% | 26.33% | 4 | ||||||||||||||

1 Institutional Shares commenced operations on October 29, 2010.

2 Calculated using the average daily shares method.

3 Less than $0.01 per share.

4 Not annualized.

5 Annualized.

6 The portfolio turnover rate is calculated on the Fund as a whole without distinguishing between classes of shares issued.

| FINANCIAL HIGHLIGHTS | 49 |

Table of Contents

Matthews Pacific Tiger Fund

The table below sets forth financial data for a share of beneficial interest outstanding throughout each period presented.

| Year Ended Dec. 31, | Period Ended Dec. 31, 20101 |

|||||||||||||||||||

| 2014 | 2013 | 2012 | 2011 | |||||||||||||||||

| Net Asset Value, beginning of period | $24.97 | $24.41 | $20.32 | $23.44 | $23.37 | |||||||||||||||

| Income (loss) from investment operations: | ||||||||||||||||||||

| Net investment income (loss)2 |

0.18 | 0.21 | 0.21 | 0.23 | 0.01 | |||||||||||||||

| Net realized gain (loss) and unrealized appreciation/ |

2.82 | 0.71 | 4.10 | (2.87) | 0.15 | |||||||||||||||

| Total from investment operations |

3.00 | 0.92 | 4.31 | (2.64) | 0.16 | |||||||||||||||

| Less distributions from: | ||||||||||||||||||||

| Net investment income |

(0.18) | (0.20) | (0.20) | (0.15) | (0.09) | |||||||||||||||

| Net realized gains on investments |

(1.23) | (0.16) | (0.02) | (0.33) | — | |||||||||||||||

| Total distributions |

(1.41) | (0.36) | (0.22) | (0.48) | (0.09) | |||||||||||||||

| Paid-in capital from redemption fees3 | — | — | — | — | — | |||||||||||||||

| Net Asset Value, end of period | $26.56 | $24.97 | $24.41 | $20.32 | $23.44 | |||||||||||||||

| Total return* |

12.03% | 3.78% | 21.24% | (11.28%) | 0.67% | 4 | ||||||||||||||

| *The total return represents the rate that an investor would have earned (or lost) on an investment in the Fund assuming reinvestment of all dividends and distributions. | ||||||||||||||||||||

| RATIOS/SUPPLEMENTAL DATA | ||||||||||||||||||||

| Net assets, end of period (in 000’s) | $5,049,643 | $4,679,039 | $3,770,568 | $2,029,091 | $540,469 | |||||||||||||||

| Ratio of expenses to average net assets before any reimbursement or waiver or recapture of expenses by Advisor and Administrator | 0.92% | 0.92% | 0.95% | 0.95% | 0.95% | 5 | ||||||||||||||

| Ratio of expenses to average net assets after any reimbursement or waiver or recapture of expenses by Advisor and Administrator | 0.91% | 0.92% | 0.95% | 0.95% | 0.95% | 5 | ||||||||||||||

| Ratio of net investment income (loss) to average net assets | 0.68% | 0.83% | 0.95% | 1.03% | 0.38% | 5 | ||||||||||||||

| Portfolio turnover6 | 11.38% | 7.73% | 6.53% | 10.51% | 11.43% | 4 | ||||||||||||||

1 Institutional Shares commenced operations on October 29, 2010.

2 Calculated using the average daily shares method.

3 Less than $0.01 per share.

4 Not annualized.

5 Annualized.

6 The portfolio turnover rate is calculated on the Fund as a whole without distinguishing between classes of shares issued.

| 50 | matthewsasia.com | 800.789.ASIA |

Table of Contents

Matthews Emerging Asia Fund

The table below sets forth financial data for a share of beneficial interest outstanding throughout the period presented.

| Year Ended Dec. 31, 2014 |

Period

Ended Dec. 31, 20131 |

|||||||

| Net Asset Value, beginning of period | $9.92 | $10.00 | ||||||

| Income (loss) from investment operations: | ||||||||

| Net investment income (loss)2 |

0.06 | 0.01 | ||||||

| Net realized gain (loss) and unrealized appreciation/depreciation on investments and foreign currency |

1.69 | (0.07) | ||||||

| Total from investment operations |

1.75 | (0.06) | ||||||

| Less distributions from: | ||||||||

| Net investment income |

(0.07) | — | 3 | |||||

| Return of capital |

— | (0.02) | ||||||

| Total distributions |

(0.07) | (0.02) | ||||||

| Paid-in capital from redemption fees | — | 3 | — | 3 | ||||

| Net Asset Value, end of period | $11.60 | $9.92 | ||||||

| Total return* |

17.68% | (0.55%) | 4 | |||||

| *The total return represents the rate that an investor would have earned (or lost) on an investment in the Fund assuming reinvestment of all dividends and distributions. | ||||||||

| RATIOS/SUPPLEMENTAL DATA | ||||||||

| Net assets, end of period (in 000s) | $21,350 | $2,017 | ||||||

| Ratio of expenses to average net assets before any reimbursement, waiver or recapture of expenses by Advisor and Administrator | 1.59% | 2.21% | 5 | |||||

| Ratio of expenses to average net assets after any reimbursement, waiver or recapture of expenses by Advisor and Administrator | 1.33% | 1.75% | 5 | |||||

| Ratio of net investment income (loss) to average net assets | 0.55% | 0.19% | 5 | |||||

| Portfolio turnover6 | 8.21% | 1.66% | 4 | |||||

1 Commenced operations on April 30, 2013.

2 Calculated using the average daily shares method.

3 Less than $0.01 per share.

4 Not annualized.

5 Annualized.

6 The portfolio turnover rate is calculated on the Fund as a whole without distinguishing between classes of shares issued.

| FINANCIAL HIGHLIGHTS | 51 |

Table of Contents

Matthews China Fund

The table below sets forth financial data for a share of beneficial interest outstanding throughout each period presented.

| Year Ended Dec. 31, | Period

Ended Dec. 31, 20102 |

|||||||||||||||||||

| 20141 | 2013 | 2012 | 2011 | |||||||||||||||||

| Net Asset Value, beginning of period | $22.81 | $23.45 | $21.49 | $29.36 | $30.02 | |||||||||||||||

| Income (loss) from investment operations: | ||||||||||||||||||||

| Net investment income (loss)3 |

0.28 | 0.26 | 0.36 | 0.26 | (0.04) | |||||||||||||||

| Net realized gain (loss) and unrealized appreciation/ |

(1.25) | 1.36 | 2.25 | (5.73) | (0.44) | |||||||||||||||

| Total from investment operations |

(0.97) | 1.62 | 2.61 | (5.47) | (0.48) | |||||||||||||||

| Less distributions from: | ||||||||||||||||||||

| Net investment income |

(0.30) | (0.31) | (0.40) | (0.34) | (0.16) | |||||||||||||||

| Net realized gains on investments |

(0.10) | (1.95) | (0.25) | (2.06) | (0.02) | |||||||||||||||

| Total distributions |

(0.40) | (2.26) | (0.65) | (2.40) | (0.18) | |||||||||||||||

| Paid-in capital from redemption fees | — | 4 | — | 4 | — | 4 | — | 4 | — | |||||||||||

| Net Asset Value, end of period | $21.44 | $22.81 | $23.45 | $21.49 | $29.36 | |||||||||||||||

| Total return* |

(4.22%) | 6.97% | 12.22% | (18.80%) | (1.62%) | 5 | ||||||||||||||

| *The total return represents the rate that an investor would have earned (or lost) on an investment in the Fund assuming reinvestment of all dividends and distributions. | ||||||||||||||||||||

| RATIOS/SUPPLEMENTAL DATA | ||||||||||||||||||||

| Net assets, end of period (in 000s) | $52,478 | $117,678 | $390,744 | $288,277 | $41,545 | |||||||||||||||

| Ratio of expenses to average net assets | 0.95% | 0.91% | 0.91% | 0.96% | 0.97% | 6 | ||||||||||||||

| Ratio of net investment income (loss) to average net assets | 1.27% | 1.13% | 1.58% | 0.99% | (0.74%) | 6 | ||||||||||||||

| Portfolio turnover7 | 10.23% | 6.29% | 9.61% | 8.43% | 9.98% | 5 | ||||||||||||||

1 Consolidated Financial Highlights.

2 Institutional Shares commenced operations on October 29, 2010.

3 Calculated using the average daily shares method.

4 Less than $0.01 per share.

5 Not annualized.

6 Annualized.

7 The portfolio turnover rate is calculated on the Fund as a whole without distinguishing between classes of shares issued.

| 52 | matthewsasia.com | 800.789.ASIA |

Table of Contents

Matthews India Fund

The table below sets forth financial data for a share of beneficial interest outstanding throughout each period presented.

| Year Ended Dec. 31, | Period Ended Dec. 31, 20101 |

|||||||||||||||||||

| 2014 | 2013 | 2012 | 2011 | |||||||||||||||||

| Net Asset Value, beginning of period | $16.31 | $17.53 | $13.61 | $21.48 | $22.03 | |||||||||||||||

| Income (loss) from investment operations: | ||||||||||||||||||||

| Net investment income (loss)2 |

0.09 | 0.10 | 0.14 | 0.16 | (0.02) | |||||||||||||||

| Net realized gain (loss) and unrealized appreciation/ |

10.29 | (1.11) | 4.17 | (7.96) | (0.43) | |||||||||||||||

| Total from investment operations |

10.38 | (1.01) | 4.31 | (7.80) | (0.45) | |||||||||||||||

| Less distributions from: | ||||||||||||||||||||

| Net investment income |

(0.08) | (0.21) | (0.12) | (0.07) | (0.10) | |||||||||||||||

| Net realized gains on investments |

(0.14) | (0.01) | (0.27) | — | — | |||||||||||||||

| Total distributions |

(0.22) | (0.22) | (0.39) | (0.07) | (0.10) | |||||||||||||||

| Paid-in capital from redemption fees | 0.02 | 0.01 | — | 3 | — | 3 | — | |||||||||||||

| Net Asset Value, end of period | $26.49 | $16.31 | $17.53 | $13.61 | $21.48 | |||||||||||||||

| Total return* |

63.80% | (5.67%) | 31.74% | (36.35%) | (2.01%) | 4 | ||||||||||||||

| *The total return represents the rate that an investor would have earned (or lost) on an investment in the Fund assuming reinvestment of all dividends and distributions. | ||||||||||||||||||||

| RATIOS/SUPPLEMENTAL DATA | ||||||||||||||||||||

| Net assets, end of period (in 000s) | $109,331 | $3,234 | $36,166 | $26,920 | $48,119 | |||||||||||||||

| Ratio of expenses to average net assets | 0.94% | 0.95% | 0.98% | 0.99% | 0.99% | 5 | ||||||||||||||

| Ratio of net investment income (loss) to average net assets | 0.38% | 0.61% | 0.87% | 0.86% | (0.51%) | 5 | ||||||||||||||

| Portfolio turnover6 | 14.86% | 8.70% | 7.03% | 3.51% | 6.14% | 4 | ||||||||||||||

1 Institutional Shares commenced operations on October 29, 2010.

2 Calculated using the average daily shares method.

3 Less than $0.01 per share.

4 Not annualized.

5 Annualized.

6 The portfolio turnover rate is calculated on the Fund as a whole without distinguishing between classes of shares issued.

| FINANCIAL HIGHLIGHTS | 53 |

Table of Contents

Matthews Japan Fund

The table below sets forth financial data for a share of beneficial interest outstanding throughout each period presented.

| Year Ended Dec. 31, | Period Ended Dec. 31, 20101 |

|||||||||||||||||||

| 2014 | 2013 | 2012 | 2011 | |||||||||||||||||

| Net Asset Value, beginning of period | $16.20 | $12.26 | $11.34 | $12.53 | $11.73 | |||||||||||||||

| Income (loss) from investment operations: | ||||||||||||||||||||

| Net investment income (loss)2 |

0.09 | 0.06 | 0.12 | 0.06 | (0.01) | |||||||||||||||

| Net realized gain (loss) and unrealized appreciation/ |

(0.50) | 4.12 | 0.84 | (1.04) | 1.30 | |||||||||||||||

| Total from investment operations |

(0.41) | 4.18 | 0.96 | (0.98) | 1.29 | |||||||||||||||

| Less distributions from: | ||||||||||||||||||||

| Net investment income |

(0.09) | (0.26) | (0.04) | (0.22) | (0.49) | |||||||||||||||

| Total distributions |

(0.09) | (0.26) | (0.04) | (0.22) | (0.49) | |||||||||||||||

| Paid-in capital from redemption fees | 0.01 | 0.02 | — | 3 | 0.01 | — | ||||||||||||||

| Net Asset Value, end of period | $15.71 | $16.20 | $12.26 | $11.34 | $12.53 | |||||||||||||||

| Total return* |

(2.47%) | 34.27% | 8.47% | (7.72%) | 11.22% | 4 | ||||||||||||||

| *The total return represents the rate that an investor would have earned (or lost) on an investment in the Fund assuming reinvestment of all dividends and distributions. | ||||||||||||||||||||

| RATIOS/SUPPLEMENTAL DATA | ||||||||||||||||||||

| Net assets, end of period (in 000s) | $154,750 | $59,702 | $22,233 | $30,302 | $4 | |||||||||||||||

| Ratio of expenses to average net assets | 0.90% | 0.96% | 1.04% | 1.07% | 1.08% | 5 | ||||||||||||||

| Ratio of net investment income (loss) to average net assets | 0.58% | 0.41% | 0.99% | 0.46% | (0.51%) | 5 | ||||||||||||||

| Portfolio turnover6 | 42.52% | 22.72% | 48.58% | 34.94% | 46.29% | 4 | ||||||||||||||

1 Institutional Shares commenced operations on October 29, 2010.

2 Calculated using the average daily shares method.

3 Less than $0.01 per share.

4 Not annualized.

5 Annualized.

6 The portfolio turnover rate is calculated on the Fund as a whole without distinguishing between classes of shares issued.

| 54 | matthewsasia.com | 800.789.ASIA |

Table of Contents

Matthews Korea Fund

The table below sets forth financial data for a share of beneficial interest outstanding throughout each period presented.

| Year Ended Dec. 31, | Period Ended Dec. 31, 20101 |

|||||||||||||||||||

| 2014 | 2013 | 2012 | 2011 | |||||||||||||||||

| Net Asset Value, beginning of period | $5.96 | $5.67 | $4.61 | $5.14 | $4.84 | |||||||||||||||

| Income (loss) from investment operations: | ||||||||||||||||||||

| Net investment income (loss)2 |

0.05 | — | 3 | — | 3 | 0.17 | 0.03 | |||||||||||||

| Net realized gain (loss) and unrealized appreciation/ |

(0.08) | 0.56 | 1.11 | (0.47) | 0.38 | |||||||||||||||

| Total from investment operations |

(0.03) | 0.56 | 1.11 | (0.30) | 0.41 | |||||||||||||||

| Less distributions from: | ||||||||||||||||||||

| Net investment income |

— | (0.03) | — | (0.01) | — | |||||||||||||||

| Net realized gains on investments |

(0.25) | (0.24) | (0.05) | (0.22) | (0.11) | |||||||||||||||

| Total distributions |

(0.25) | (0.27) | (0.05) | (0.23) | (0.11) | |||||||||||||||

| Paid-in capital from redemption fees | — | 3 | — | 3 | — | 3 | — | 3 | — | |||||||||||

| Net Asset Value, end of period | $5.68 | $5.96 | $5.67 | $4.61 | $5.14 | |||||||||||||||

| Total return* |

(0.39%) | 9.87% | 24.16% | (6.05%) | 8.51% | 4 | ||||||||||||||

| *The total return represents the rate that an investor would have earned (or lost) on an investment in the Fund assuming reinvestment of all dividends and distributions. | ||||||||||||||||||||

| RATIOS/SUPPLEMENTAL DATA | ||||||||||||||||||||

| Net assets, end of period (in 000s) | $91,431 | $12,283 | $8,597 | $15,109 | $4 | |||||||||||||||

| Ratio of expenses to average net assets | 0.93% | 0.97% | 1.00% | 1.07% | 0.91% | 5 | ||||||||||||||

| Ratio of net investment income (loss) to average net assets | 0.87% | (0.03%) | (0.07%) | 3.37% | 3.74% | 5 | ||||||||||||||

| Portfolio turnover6 | 17.37% | 46.20% | 34.84% | 30.13% | 39.05% | 4 | ||||||||||||||

1 Institutional Shares commenced operations on October 29, 2010.

2 Calculated using the average daily shares method.

3 Less than $0.01 per share.

4 Not annualized.

5 Annualized.

6 The portfolio turnover rate is calculated on the Fund as a whole without distinguishing between classes of shares issued.

| FINANCIAL HIGHLIGHTS | 55 |

Table of Contents

Matthews Asia Small Companies Fund

The table below sets forth financial data for a share of beneficial interest outstanding throughout each period presented.

| Year Ended Dec. 31, 2014 |

Period

Ended Dec. 31, 20131 |

|||||||

| Net Asset Value, beginning of period | $19.33 | $19.44 | ||||||

| Income (loss) from investment operations: | ||||||||

| Net investment income (loss)2 |

0.15 | 0.18 | ||||||

| Net realized gain (loss) and unrealized appreciation/depreciation on investments and foreign currency |

2.10 | (0.16) | ||||||

| Total from investment operations |

2.25 | 0.02 | ||||||

| Less distributions from: | ||||||||

| Net investment income |

(0.12) | (0.13) | ||||||

| Net realized gains on investments |

— | — | ||||||

| Total distributions |

(0.12) | (0.13) | ||||||

| Paid-in capital from redemption fees3 | — | — | ||||||

| Net Asset Value, end of period | $21.46 | $19.33 | ||||||

| Total return* |

11.65% | 0.13% | 4 | |||||

| *The total return represents the rate that an investor would have earned (or lost) on an investment in the Fund assuming reinvestment of all dividends and distributions. | ||||||||

| RATIOS/SUPPLEMENTAL DATA | ||||||||

| Net assets, end of period (in 000’s) | $77,168 | $44,769 | ||||||

| Ratio of expenses to average net assets before any reimbursement, waiver or recapture of expenses by Advisor and Administrator | 1.27% | 1.25% | 5 | |||||

| Ratio of expenses to average net assets after any reimbursement, waiver or recapture of expenses by Advisor and Administrator | 1.26% | 1.25% | 5 | |||||

| Ratio of net investment income (loss) to average net assets | 0.70% | 1.39% | 5 | |||||

| Portfolio turnover6 | 21.70% | 37.01% | 4 | |||||

1 Institutional Shares commenced operations on April 30, 2013.

2 Calculated using the average daily shares method.

3 Less than $0.01 per share.

4 Not annualized.

5 Annualized.

6 The portfolio turnover rate is calculated on the Fund as a whole for the entire year without distinguishing between classes of shares issued.

| 56 | matthewsasia.com | 800.789.ASIA |

Table of Contents

Matthews Asia Science and Technology Fund

The table below sets forth financial data for a share of beneficial interest outstanding throughout each period presented.

| Year Ended Dec. 31, 2014 |

Period

Ended Dec. 31, 20131 |

|||||||

| Net Asset Value, beginning of period | $12.58 | $10.09 | ||||||

| Income (loss) from investment operations: | ||||||||

| Net investment income (loss)2 |

0.03 | 0.04 | ||||||

| Net realized gain (loss) and unrealized appreciation/depreciation on investments and foreign currency |

1.17 | 2.48 | ||||||

| Total from investment operations |

1.20 | 2.52 | ||||||

| Less distributions from: | ||||||||

| Net investment income |

(0.09) | (0.03) | ||||||

| Net realized gains on investments |

(0.08) | — | ||||||

| Total distributions |

(0.17) | (0.03) | ||||||

| Paid-in capital from redemption fees3 | — | — | ||||||

| Net Asset Value, end of period | $13.61 | $12.58 | ||||||

| Total return* |

9.54% | 24.99% | 4 | |||||

| *The total return represents the rate that an investor would have earned (or lost) on an investment in the Fund assuming reinvestment of all dividends and distributions. | ||||||||

| RATIOS/SUPPLEMENTAL DATA | ||||||||

| Net assets, end of period (in 000s) | $61,088 | $49,236 | ||||||

| Ratio of expenses to average net assets | 0.95% | 1.00% | 5 | |||||

| Ratio of net investment income (loss) to average net assets | 0.21% | 0.56% | 5 | |||||

| Portfolio turnover6 | 62.99% | 62.04% | 4 | |||||

1 Institutional Shares commenced operations on April 30, 2013.