UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934

Date of report (Date of earliest event reported): August 17, 2020

FLUSHING FINANCIAL CORPORATION

(Exact name of registrant as specified in its charter)

| Delaware | 001-33013 | 11-3209278 | ||

| (State or other jurisdiction of incorporation or organization) |

(Commission File No.) |

(IRS Employer Identification No.) |

220 RXR Plaza, Uniondale, NY 11556

(Address of principal executive offices, including zip code)

(718) 961-5400

(Registrant’s telephone number, including area code)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions:

| ☒ | Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

| ☐ | Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

| ☐ | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| ☐ | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 140.13e-4(c)) |

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class |

Trading Symbol(s) |

Name of each exchange | ||

| Common Stock, $0.01 par value | FFIC | The Nasdaq Stock Market LLC |

Indicate by check mark whether the registrant is an emerging growth company as defined in Rule 405 of the Securities Act of 1933 (17 CFR 230.405) or Rule 12b-2 of the Securities Exchange Act of 1934 (17 CFR 240.12b-2).

Emerging growth company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Item 7.01 Regulation FD Disclosure

On August 17, 2020, Flushing Financial Corporation, a Delaware corporation (“Flushing Financial”), issued a press release, a copy of which is attached hereto as Exhibit 99.1 and is incorporated herein by reference.

On August 17, 2020, Flushing Financial posted a new corporate presentation (the “Corporate Presentation”) on its Investor Relations website at www.flushingbank.com. The Corporate Presentation, attached to this Current Report on Form 8-K as Exhibit 99.2 and incorporated herein by reference, updates previously filed presentations and provides an overview of Flushing Financial’s strategy and performance. The preceding information, as well as Exhibit 99.2 to this Current Report on Form 8-K, shall not be deemed “filed” for purposes of Section 18 of the Securities Exchange Act of 1934, as amended (the “Exchange Act”), or otherwise subject to the liabilities of that Section, or incorporated by reference into any filing under the Securities Act of 1933, as amended, or the Exchange Act, except as shall be expressly set forth by specific reference in such filing.

Item 9.01 Financial Statements and Exhibits

(d) Exhibits. The following exhibits are filed with this Current Report on Form 8-K:

| Exhibit No. |

Description | |

| 99.1 | Press Release, dated August 17, 2020 | |

| 99.2 | Investor Presentation, dated August 17, 2020 | |

| 104 | Cover Page Interactive File (the cover page tags are embedded within the Inline XBRL document) | |

Cautionary Notes on Forward-Looking Statements

This report contains “forward-looking statements” within the meaning of the federal securities laws, including Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These forward-looking statements may include: management plans relating to the proposed transaction; the expected timing of the completion of the proposed transaction; the ability to complete the proposed transaction; the ability to obtain any required regulatory, shareholder or other approvals; any statements of the plans and objectives of management for future operations, products or services, including the execution of integration plans relating to the proposed transaction; any statements of expectation or belief; projections related to certain financial metrics; and any statements of assumptions underlying any of the foregoing. Forward-looking statements are typically identified by words such as “believe,” “expect,” “anticipate,” “intend,” “seek,” “plan,” “may,” “will,” “should,” “could,” “would,” “target,” “outlook,” “estimate,” “forecast,” “project” and other similar words and expressions or negatives of these words. Forward-looking statements are subject to numerous assumptions, risks and uncertainties, which change over time and are beyond our control. Forward-looking statements speak only as of the date they are made. Neither Flushing Financial nor Empire assumes any duty and does not undertake to update any forward-looking statements. Because forward-looking statements are by their nature, to different degrees, uncertain and subject to assumptions, actual results or future events could differ, possibly materially, from those that Flushing Financial or Empire anticipated in its forward-looking statements, and future results could differ materially from historical performance. Factors that could cause or contribute to such differences include, but are not limited to, those included under Item 1A “Risk Factors” in Flushing Financial’s Annual Report on Form 10-K as of December 31, 2019 and those disclosed in Flushing Financial’s other periodic reports filed with the SEC, as well as the possibility that the expected benefits of the proposed transaction may not materialize in the timeframe expected or at all, or may be more costly to achieve; that the proposed transaction may not be timely completed, if at all; that prior to the completion of the proposed transaction or thereafter, Flushing Financial’s and Empire’s respective businesses may not perform as expected due to transaction-related uncertainty or other factors; that the parties are unable to successfully implement integration strategies related to the proposed transaction; that required regulatory, shareholder or other approvals are not obtained or other customary closing conditions are not satisfied in a timely manner or at all; reputational risks and the reaction of the companies’ shareholders, customers, employees and other constituents to the proposed transaction; diversion of management time on merger-related matters; and the impact of the novel coronavirus (COVID-19) and other infectious illness outbreaks that may arise in the future, which has created significant uncertainties in U.S. and global markets. These risks, as well as other risks associated with the proposed transaction, are more fully discussed in the proxy statement/prospectus that is included in the registration statement on Form S-4 filed with the SEC in connection with the proposed transaction, as amended and supplemented from time to time. While the list of factors presented here and the list of factors presented in the registration statement on Form S-4 are, considered representative, no such list should be considered to be a complete statement of all potential risks and uncertainties. Unlisted factors may present significant additional obstacles to the realization of forward looking statements. For any forward-looking statements made in this press release or in any documents, Flushing Financial and Empire claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

Additional Information about the Proposed Transaction

In connection with the proposed transaction, Flushing Financial filed a registration statement on Form S-4 with the SEC, and Flushing Financial’s registration statement, as amended, was declared effective by the SEC on January 17, 2020. A definitive proxy statement/prospectus was first mailed to Empire shareholders on or about January 21, 2020. Flushing Financial intends to file a supplement to the registration statement with the SEC that will include a supplemental proxy statement of Empire with respect to the Supplemental Shareholder Meeting and a prospectus of Flushing Financial, and Flushing Financial will file other documents regarding the proposed transaction with the SEC. Flushing Financial may file other documents with the SEC regarding the proposed transaction. Before making any voting or investment decision, investors and shareholders of Flushing Financial and Empire are urged to carefully read the entire registration statement, proxy statement and prospectus when they become available and any other relevant documents filed with the SEC, as well as any amendments or supplements to those documents, because they will contain important information about the proposed transaction. A supplemental proxy statement will be sent to Empire shareholders seeking the required shareholder approvals. When available, copies of the registration statement, the proxy statement and the prospectus, as they may be amended or supplemented from time to time, may be obtained free of charge from the SEC’s website at www.sec.gov, from Flushing Financial by sending a written request to Susan K. Cullen, Senior Executive Vice President and Chief Financial Officer, Flushing Financial Corporation, at 220 RXR Plaza, Uniondale, New York 11556, telephone (718) 961-5400, or from Empire by sending a written request to William Franz, Senior Vice President, Director of Marketing and Investor Relations, Empire Bancorp, Inc., 1707 Veterans Highway, Islandia, NY 11749, or calling (631) 348-4444.

Investors and shareholders are also urged to carefully review and consider Flushing Financial’s public filings with the SEC, including but not limited to its Annual Reports on Form 10-K, Current Reports on Form 8-K, Quarterly Reports on Form 10-Q and proxy statements. The documents filed by Flushing Financial with the SEC may be obtained free of charge from the SEC’s website at www.sec.gov or through a link on Flushing Financial’s website at www.flushingbank.com. These documents may also be obtained free of charge from Flushing Financial by sending a written request to Susan K. Cullen, Senior Executive Vice President and Chief Financial Officer, Flushing Financial Corporation, at 220 RXR Plaza, Uniondale, New York 11556, telephone (718) 961-5400.

Participants in the Solicitation

Flushing Financial, Empire and certain of their respective directors and executive officers, under the SEC’s rules, may be deemed to be participants in the solicitation of proxies of Empire’s shareholders in connection with the proposed transaction. Information about the directors and executive officers of Flushing Financial and their ownership of Flushing Financial common stock is set forth in the proxy statement for Flushing Financial’s 2020 Annual Meeting of Stockholders filed with the SEC on April 16, 2020. Information about the directors and executive officers of Empire is available on Empire’s website at empirenb.com. Additional information regarding the interests of those participants and other persons who may be deemed participants in the solicitation of proxies from Empire’s shareholders in connection with the proposed transaction may be obtained by reading the proxy statement and prospectus regarding the proposed transaction when they become available. Once available, free copies of the proxy statement and prospectus (as amended and supplemented from time to time) may be obtained as described in the preceding paragraph.

No Offer or Solicitation

This communication is not intended to and shall not constitute an offer to sell or the solicitation of an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote of approval, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offer of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act of 1933, as amended.

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| FLUSHING FINANCIAL CORPORATION | ||||

| /s/ Susan K. Cullen | ||||

| Date: August 17, 2020 | Susan K. Cullen | |||

| Senior Executive Vice President and Chief Financial Officer | ||||

Exhibit 99.1

CONTACT:

Susan K. Cullen

Senior Executive Vice President and Chief Financial Officer

Flushing Financial Corporation

(718) 961-5400

FOR IMMEDIATE RELEASE

FLUSHING FINANCIAL CORPORATION TO HOLD VIRTUAL MEETINGS WITH INSTITUTIONAL INVESTORS

UNIONDALE, NY – August 17, 2020—Flushing Financial Corporation (the “Company”) (Nasdaq: FFIC), the parent holding company for Flushing Bank (the “Bank”), today announced that John R. Buran, the Company’s President and Chief Executive Officer and Susan K. Cullen, the Company’s Senior Executive Vice President and Chief Financial Officer, will be meeting virtually with institutional investors on August 24 and August 26, 2020.

| WHO | Flushing Financial Corporation, with $7.2 billion in consolidated assets, is the holding company for Flushing Bank®, a New York State—chartered commercial bank insured by the Federal Deposit Insurance Corporation. The Bank serves consumers, businesses, professionals, corporate clients, and public entities by offering a full complement of deposit, loan, equipment finance, and cash management services through its banking offices located in Queens, Brooklyn, Manhattan, and on Long Island. As a leader in real estate lending, the Bank’s experienced lending team creates mortgage solutions for real estate owners and property managers both within and outside the New York City metropolitan area. Flushing Bank is an Equal Housing Lender. The Bank also operates an online banking division consisting of iGObanking.com®, which offers competitively priced deposit products to consumers nationwide, and BankPurely®, an eco-friendly, healthier lifestyle community brand. | |

| WHAT | Meetings with institutional investors held virtually on August 24 and August 26, 2020. | |

| PRESENTATION | The presentation will focus on the Company’s performance and its strategic operating objectives. The presentation will be available on the Company’s website, www.flushingbank.com, on August 17, 2020. | |

| RECENT NEWS | • August 17, 2020- Flushing Financial Corporation and Empire Bancorp Inc. Agree to Complete Their Merger Under Extended Time Frame.

• August 3, 2020- Flushing Financial Corporation and Empire Bancorp, Inc. Announce Continued Merger Discussions.

• July 21, 2020- Flushing Financial Corporation Reports Record Net Interest Income Net Interest Margin Expansion Driven by Ability to Significantly Reduce Funding Costs. | |

“Safe Harbor” Statement under the Private Securities Litigation Reform Act of 1995: Statements in this Press Release relating to plans, strategies, economic performance and trends, projections of results of specific activities or investments and other statements that are not descriptions of historical facts may be forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995, Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Forward-looking information is inherently subject to risks and uncertainties, and actual results could differ materially from those currently anticipated due to a number of factors, which include, but are not limited to, risk factors discussed in the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2019 and in other documents filed by the Company with the Securities and Exchange Commission from time to time. Forward-looking statements may be identified by terms such as “may”, “will”, “should”, “could”, “expects”, “plans”, “intends”, “anticipates”, “believes”, “estimates”, “predicts”, “forecasts”, “goals”, “potential” or “continue” or similar terms or the negative of these terms. Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. The Company has no obligation to update these forward-looking statements.

Additional information on Flushing Financial Corporation may be obtained by visiting the Company’s website at http://www.flushingbank.com.

# # #

Exhibit 99.2 Investor Presentation August 17, 2020 contact: susan.cullen@flushingbank.com | phone: 718.961.5400 | website: www.flushingbank.comExhibit 99.2 Investor Presentation August 17, 2020 contact: susan.cullen@flushingbank.com | phone: 718.961.5400 | website: www.flushingbank.com

Cautionary Notes on Forward-Looking Statements and Additional Information This communication contains “forward-looking statements” within the meaning of the federal securities laws, including Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These forward-looking statements may include: management plans relating to the proposed transaction; the expected timing of the completion of the proposed transaction; the ability to complete the proposed transaction; the ability to obtain any required regulatory, shareholder or other approvals; any statements of the plans and objectives of management for future operations, products or services, including the execution of integration plans relating to the proposed transaction; any statements of expectation or belief; projections related to certain financial metrics; and any statements of assumptions underlying any of the foregoing. Forward-looking statements are typically identified by words such as “believe,” “expect,” “anticipate,” “intend,” “seek,” “plan,” “may,” “will,” “should,” “could,” “would,” “target,” “outlook,” “estimate,” “forecast,” “project” and other similar words and expressions or negatives of these words. Forward-looking statements are subject to numerous assumptions, risks and uncertainties, which change over time and are beyond our control. Forward-looking statements speak only as of the date they are made. Neither Flushing Financial Corporation (“Flushing”) nor Empire Bancorp, Inc. (“Empire”) assumes any duty and does not undertake to update any forward-looking statements. Because forward-looking statements are by their nature, to different degrees, uncertain and subject to assumptions, actual results or future events could differ, possibly materially, from those that Flushing or Empire anticipated in its forward-looking statements, and future results could differ materially from historical performance. Factors that could cause or contribute to such differences include, but are not limited to, those included under Item 1A “Risk Factors” in Flushing’s Annual Report on Form 10-K and those disclosed in Flushing’s other periodic reports filed with the Securities and Exchange Commission (the “SEC”), as well as the possibility that the expected benefits of the proposed transaction may not materialize in the timeframe expected or at all, or may be more costly to achieve; that the proposed transaction may not be timely completed, if at all; that prior to the completion of the proposed transaction or thereafter, Flushing’s and Empire’s respective businesses may not perform as expected due to transaction-related uncertainty or other factors; that the parties are unable to successfully implement integration strategies related to the proposed transaction; that required regulatory, shareholder or other approvals are not obtained or other customary closing conditions are not satisfied in a timely manner or at all; reputational risks and the reaction of the companies’ shareholders, customers, employees and other constituents to the proposed transaction; diversion of management time on merger-related matters; and the impact of the novel coronavirus (COVID-19) and other infectious illness outbreaks that may arise in the future, which has created significant uncertainties in U.S. and global markets. These risks, as well as other risks associated with the proposed transaction, are more fully discussed in the proxy statement/prospectus that is included in the registration statement on Form S-4 filed with the SEC in connection with the proposed transaction, as amended and supplemented from time to time. While the list of factors presented here and the list of factors presented in the registration statement on Form S-4 are, considered representative, no such list should be considered a complete statement of all potential risks and uncertainties. Unlisted factors may present significant additional obstacles to the realization of forward looking statements. For any forward-looking statements made in this press release or in any documents, Flushing and Empire claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995. Annualized, pro forma, projected and estimated numbers are used for illustrative purposes only, are not forecasts and may not reflect actual results. In connection with the proposed transaction, Flushing filed a registration statement on Form S-4 with the SEC, which included a proxy statement of Empire and a prospectus of Flushing, was declared effective by the SEC on January 17, 2020. Flushing intends to file a supplement to the registration statement that will include a supplemental proxy statement and prospectus. Flushing has filed and may file other documents regarding the proposed transaction with the SEC. Before making any voting or investment decision, investors and shareholders of Flushing and Empire are urged to carefully read the entire registration statement, proxy statement and prospectus when they become available and any other relevant documents filed with the SEC, as well as any amendments or supplements to those documents, because they will contain important information about the proposed transaction. A supplemental proxy statement will be sent to Empire shareholders seeking the required shareholder approvals. When available, copies of the registration statement, the proxy statement and the prospectus, as they may be amended from time to time, may be obtained free of charge from the SEC’s website at www.sec.gov, from Flushing by sending a written request to Susan K. Cullen, Senior Executive Vice President and Chief Financial Officer, Flushing Financial Corporation, at 220 RXR Plaza, Uniondale, New York 11556, telephone (718) 961-5400, or from Empire by sending a written request to William Franz, Senior Vice President, Director of Marketing and Investor Relations, Empire Bancorp, Inc., 1707 Veterans Highway, Islandia, NY 11749, or calling (631) 348-4444. Investors and shareholders are also urged to carefully review and consider Flushing’s public filings with the SEC, including but not limited to its Annual Reports on Form 10-K, Current Reports on Form 8-K, Quarterly Reports on Form 10-Q and proxy statements. The documents filed by Flushing with the SEC may be obtained free of charge from the SEC’s website at www.sec.gov or through a link on Flushing’s website at www.flushingbank.com. These documents may also be obtained free of charge from Flushing by sending a written request to Susan K. Cullen, Senior Executive Vice President and Chief Financial Officer, Flushing Financial Corporation, at 220 RXR Plaza, Uniondale, New York 11556, telephone (718) 961-5400. Flushing, Empire and certain of their respective directors and executive officers, under the SEC’s rules, may be deemed to be participants in the solicitation of proxies of Empire’s shareholders in connection with the proposed transaction. Information about the directors and executive officers of Flushing and their ownership of Flushing common stock is set forth in the proxy statement for Flushing’s 2020 Annual Meeting of Stockholders filed with the SEC on April 16, 2020. Information about the directors and executive officers of Empire is available on Empire’s website at www.empirenb.com. Additional information regarding the interests of those participants and other persons who may be deemed participants in the solicitation of proxies from Empire’s shareholders in connection with the proposed transaction may be obtained by reading the proxy statement and prospectus regarding the proposed transaction when it becomes available. Once available, free copies of the proxy statement and prospectus may be obtained as described in the preceding paragraph. This communication is not intended to and shall not constitute an offer to sell or the solicitation of an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote of approval, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offer of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act of 1933, as amended. 2Cautionary Notes on Forward-Looking Statements and Additional Information This communication contains “forward-looking statements” within the meaning of the federal securities laws, including Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These forward-looking statements may include: management plans relating to the proposed transaction; the expected timing of the completion of the proposed transaction; the ability to complete the proposed transaction; the ability to obtain any required regulatory, shareholder or other approvals; any statements of the plans and objectives of management for future operations, products or services, including the execution of integration plans relating to the proposed transaction; any statements of expectation or belief; projections related to certain financial metrics; and any statements of assumptions underlying any of the foregoing. Forward-looking statements are typically identified by words such as “believe,” “expect,” “anticipate,” “intend,” “seek,” “plan,” “may,” “will,” “should,” “could,” “would,” “target,” “outlook,” “estimate,” “forecast,” “project” and other similar words and expressions or negatives of these words. Forward-looking statements are subject to numerous assumptions, risks and uncertainties, which change over time and are beyond our control. Forward-looking statements speak only as of the date they are made. Neither Flushing Financial Corporation (“Flushing”) nor Empire Bancorp, Inc. (“Empire”) assumes any duty and does not undertake to update any forward-looking statements. Because forward-looking statements are by their nature, to different degrees, uncertain and subject to assumptions, actual results or future events could differ, possibly materially, from those that Flushing or Empire anticipated in its forward-looking statements, and future results could differ materially from historical performance. Factors that could cause or contribute to such differences include, but are not limited to, those included under Item 1A “Risk Factors” in Flushing’s Annual Report on Form 10-K and those disclosed in Flushing’s other periodic reports filed with the Securities and Exchange Commission (the “SEC”), as well as the possibility that the expected benefits of the proposed transaction may not materialize in the timeframe expected or at all, or may be more costly to achieve; that the proposed transaction may not be timely completed, if at all; that prior to the completion of the proposed transaction or thereafter, Flushing’s and Empire’s respective businesses may not perform as expected due to transaction-related uncertainty or other factors; that the parties are unable to successfully implement integration strategies related to the proposed transaction; that required regulatory, shareholder or other approvals are not obtained or other customary closing conditions are not satisfied in a timely manner or at all; reputational risks and the reaction of the companies’ shareholders, customers, employees and other constituents to the proposed transaction; diversion of management time on merger-related matters; and the impact of the novel coronavirus (COVID-19) and other infectious illness outbreaks that may arise in the future, which has created significant uncertainties in U.S. and global markets. These risks, as well as other risks associated with the proposed transaction, are more fully discussed in the proxy statement/prospectus that is included in the registration statement on Form S-4 filed with the SEC in connection with the proposed transaction, as amended and supplemented from time to time. While the list of factors presented here and the list of factors presented in the registration statement on Form S-4 are, considered representative, no such list should be considered a complete statement of all potential risks and uncertainties. Unlisted factors may present significant additional obstacles to the realization of forward looking statements. For any forward-looking statements made in this press release or in any documents, Flushing and Empire claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995. Annualized, pro forma, projected and estimated numbers are used for illustrative purposes only, are not forecasts and may not reflect actual results. In connection with the proposed transaction, Flushing filed a registration statement on Form S-4 with the SEC, which included a proxy statement of Empire and a prospectus of Flushing, was declared effective by the SEC on January 17, 2020. Flushing intends to file a supplement to the registration statement that will include a supplemental proxy statement and prospectus. Flushing has filed and may file other documents regarding the proposed transaction with the SEC. Before making any voting or investment decision, investors and shareholders of Flushing and Empire are urged to carefully read the entire registration statement, proxy statement and prospectus when they become available and any other relevant documents filed with the SEC, as well as any amendments or supplements to those documents, because they will contain important information about the proposed transaction. A supplemental proxy statement will be sent to Empire shareholders seeking the required shareholder approvals. When available, copies of the registration statement, the proxy statement and the prospectus, as they may be amended from time to time, may be obtained free of charge from the SEC’s website at www.sec.gov, from Flushing by sending a written request to Susan K. Cullen, Senior Executive Vice President and Chief Financial Officer, Flushing Financial Corporation, at 220 RXR Plaza, Uniondale, New York 11556, telephone (718) 961-5400, or from Empire by sending a written request to William Franz, Senior Vice President, Director of Marketing and Investor Relations, Empire Bancorp, Inc., 1707 Veterans Highway, Islandia, NY 11749, or calling (631) 348-4444. Investors and shareholders are also urged to carefully review and consider Flushing’s public filings with the SEC, including but not limited to its Annual Reports on Form 10-K, Current Reports on Form 8-K, Quarterly Reports on Form 10-Q and proxy statements. The documents filed by Flushing with the SEC may be obtained free of charge from the SEC’s website at www.sec.gov or through a link on Flushing’s website at www.flushingbank.com. These documents may also be obtained free of charge from Flushing by sending a written request to Susan K. Cullen, Senior Executive Vice President and Chief Financial Officer, Flushing Financial Corporation, at 220 RXR Plaza, Uniondale, New York 11556, telephone (718) 961-5400. Flushing, Empire and certain of their respective directors and executive officers, under the SEC’s rules, may be deemed to be participants in the solicitation of proxies of Empire’s shareholders in connection with the proposed transaction. Information about the directors and executive officers of Flushing and their ownership of Flushing common stock is set forth in the proxy statement for Flushing’s 2020 Annual Meeting of Stockholders filed with the SEC on April 16, 2020. Information about the directors and executive officers of Empire is available on Empire’s website at www.empirenb.com. Additional information regarding the interests of those participants and other persons who may be deemed participants in the solicitation of proxies from Empire’s shareholders in connection with the proposed transaction may be obtained by reading the proxy statement and prospectus regarding the proposed transaction when it becomes available. Once available, free copies of the proxy statement and prospectus may be obtained as described in the preceding paragraph. This communication is not intended to and shall not constitute an offer to sell or the solicitation of an offer to sell or the solicitation of an offer to buy any securities or a solicitation of any vote of approval, nor shall there be any sale of securities in any jurisdiction in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such jurisdiction. No offer of securities shall be made except by means of a prospectus meeting the requirements of Section 10 of the Securities Act of 1933, as amended. 2

Experienced Executive Leadership Team John Buran Maria Grasso Susan Cullen Francis Korzekwinski Michael Bingold President SEVP, COO, SEVP, CFO, SEVP, Chief of SEVP, Chief Retail and and CEO Corporate Secretary Treasurer Real Estate Client Development Officer FFIC: 19 years FFIC: 14 years FFIC: 5 years FFIC: 26 years FFIC: 7 years Industry: 43 years Industry: 34 years Industry: 29 years Industry: 30 years Industry: 37 years Vincent Giovinco Jeoung Jin Theresa Kelly Patricia Mezeul EVP, Commercial Real EVP, Residential and EVP, Business EVP, Director of Estate Lending Banking Banking Government Banking FFIC: 1 year FFIC: 22 years FFIC: 14 years FFIC: 12 years Industry: 23 years Industry: 24 years Industry: 36 years Industry: 40 years 3Experienced Executive Leadership Team John Buran Maria Grasso Susan Cullen Francis Korzekwinski Michael Bingold President SEVP, COO, SEVP, CFO, SEVP, Chief of SEVP, Chief Retail and and CEO Corporate Secretary Treasurer Real Estate Client Development Officer FFIC: 19 years FFIC: 14 years FFIC: 5 years FFIC: 26 years FFIC: 7 years Industry: 43 years Industry: 34 years Industry: 29 years Industry: 30 years Industry: 37 years Vincent Giovinco Jeoung Jin Theresa Kelly Patricia Mezeul EVP, Commercial Real EVP, Residential and EVP, Business EVP, Director of Estate Lending Banking Banking Government Banking FFIC: 1 year FFIC: 22 years FFIC: 14 years FFIC: 12 years Industry: 23 years Industry: 24 years Industry: 36 years Industry: 40 years 3

Summary of Strategic Objectives Increase Core Deposits, with an Manage Net Loan Growth and Enhance Core Earnings Power by Emphasis on Non-Interest Focus on Yield with an Emphasis Improving Scalability and Bearing DDA, and Continue to on Assets with the Best Risk- Efficiency Through Executional Improve Funding Mix Adjusted Returns Excellence Profitable Growth and Expansion through New Distribution Manage Credit Risk Remain Well Capitalized Channels and Business Lines 4Summary of Strategic Objectives Increase Core Deposits, with an Manage Net Loan Growth and Enhance Core Earnings Power by Emphasis on Non-Interest Focus on Yield with an Emphasis Improving Scalability and Bearing DDA, and Continue to on Assets with the Best Risk- Efficiency Through Executional Improve Funding Mix Adjusted Returns Excellence Profitable Growth and Expansion through New Distribution Manage Credit Risk Remain Well Capitalized Channels and Business Lines 4

Key Messages Exceeding Customer Enhancing Earnings Strengthening Our Maintaining Our Strong Expectations Power Commercial Bank Risk Management Balance Sheet Philosophy § Committed to being the § Manage yield through loan § Focus on the origination of § Remain well capitalized at preeminent community portfolio mix C&I loans while remaining all times financial services company nimble and responsive to § Manage cost of funds§ Maintain sufficient sources in our multicultural market industry shifts of liquid assets and area § Improve scalability and § Shift funding sources to contingency funding efficiency of operating § Competitive strength as a core deposits from CDs and expense base§ Strong cyber and physical commercial real estate borrowings security measures to lender § Continue to add key talent safeguard Company and § Broad array of products and with commercial expertise customer assets and services delivered through information customers’ preferred § Adequate loan loss reserve channels § Conservative underwriting § Strong presence in our standards ethnic communities, particularly the Asian community in Queens § Staff branches and lending units with seasoned, multi- lingual professionals 5Key Messages Exceeding Customer Enhancing Earnings Strengthening Our Maintaining Our Strong Expectations Power Commercial Bank Risk Management Balance Sheet Philosophy § Committed to being the § Manage yield through loan § Focus on the origination of § Remain well capitalized at preeminent community portfolio mix C&I loans while remaining all times financial services company nimble and responsive to § Manage cost of funds§ Maintain sufficient sources in our multicultural market industry shifts of liquid assets and area § Improve scalability and § Shift funding sources to contingency funding efficiency of operating § Competitive strength as a core deposits from CDs and expense base§ Strong cyber and physical commercial real estate borrowings security measures to lender § Continue to add key talent safeguard Company and § Broad array of products and with commercial expertise customer assets and services delivered through information customers’ preferred § Adequate loan loss reserve channels § Conservative underwriting § Strong presence in our standards ethnic communities, particularly the Asian community in Queens § Staff branches and lending units with seasoned, multi- lingual professionals 5

Flushing Financial Corporate Profile (NASDAQ: FFIC) 2Q20 Key Statistics Balance Sheet Footprint 1 • Deposits primarily $7.2B $6.0B $5.1B $0.6B from 20 branches Assets Gross Loans Deposits Equity in multi-cultural neighborhoods and our online Queens division, Performance Brooklyn Nassau consisting of ® iGObanking.com 0.57% 7.39% 7.29% $18.3MM $10.3MM ® and BankPurely Core Core Dividend GAAP Core 2 ROAA ROAE Yield Earnings Earnings Strong Franchise and Track Record of Focus on Strategic Diverse Business Mix Outperformance Opportunities § Leading community bank in greater § Of the 69 publicly traded banks in § Improved customer experience and New York City area Flushing’s markets in 1995, only 11 cost control as we deploy the remain, with FFIC ranked 5th overall Universal Banker model in branches § Diversified loan portfolio with focus 3 on a total return basis on commercial business loans, multi-§ Optimizing funding mix through family mortgages and commercial § Record GAAP net interest income internet banks and Asian initiatives real estate totaling $48.7MM § Proactively managing balance sheet § Current and historical strong credit § Loan pipeline remains strong at to optimize NIM and capital positions $310.8MM § Acquisition of Empire Bancorp. Inc. 1 2 3 Includes mortgagors‘ escrow deposits. Calculated using 6/30/2020 closing price of $11.52. Through 6/30/2020. 6Flushing Financial Corporate Profile (NASDAQ: FFIC) 2Q20 Key Statistics Balance Sheet Footprint 1 • Deposits primarily $7.2B $6.0B $5.1B $0.6B from 20 branches Assets Gross Loans Deposits Equity in multi-cultural neighborhoods and our online Queens division, Performance Brooklyn Nassau consisting of ® iGObanking.com 0.57% 7.39% 7.29% $18.3MM $10.3MM ® and BankPurely Core Core Dividend GAAP Core 2 ROAA ROAE Yield Earnings Earnings Strong Franchise and Track Record of Focus on Strategic Diverse Business Mix Outperformance Opportunities § Leading community bank in greater § Of the 69 publicly traded banks in § Improved customer experience and New York City area Flushing’s markets in 1995, only 11 cost control as we deploy the remain, with FFIC ranked 5th overall Universal Banker model in branches § Diversified loan portfolio with focus 3 on a total return basis on commercial business loans, multi-§ Optimizing funding mix through family mortgages and commercial § Record GAAP net interest income internet banks and Asian initiatives real estate totaling $48.7MM § Proactively managing balance sheet § Current and historical strong credit § Loan pipeline remains strong at to optimize NIM and capital positions $310.8MM § Acquisition of Empire Bancorp. Inc. 1 2 3 Includes mortgagors‘ escrow deposits. Calculated using 6/30/2020 closing price of $11.52. Through 6/30/2020. 6

Proven Track Record of Steady Organic Growth Total Assets ($B) $8.0 $7.2 $7.0 $6.0 $5.0 $4.0 $3.0 $2.0 $0.7 $1.0 $- Stockholder’s Equity ($B) $0.7 $0.6 $0.6 $0.5 $0.4 $0.3 $0.2 $0.1 $0.1 $- Note: Acquisitions of Atlantic Liberty Financial Corp in 2006 (assets and deposits acquired of $180MM and $107MM); New York Federal Savings Bank in 1997 7 (assets and deposits acquired of $84MM and $51MM).Proven Track Record of Steady Organic Growth Total Assets ($B) $8.0 $7.2 $7.0 $6.0 $5.0 $4.0 $3.0 $2.0 $0.7 $1.0 $- Stockholder’s Equity ($B) $0.7 $0.6 $0.6 $0.5 $0.4 $0.3 $0.2 $0.1 $0.1 $- Note: Acquisitions of Atlantic Liberty Financial Corp in 2006 (assets and deposits acquired of $180MM and $107MM); New York Federal Savings Bank in 1997 7 (assets and deposits acquired of $84MM and $51MM).

Proven Track Record of Steady Organic Growth Total Gross Loans ($B) $6.0 $6.0 $5.0 $4.0 $3.0 $2.0 $1.0 $0.3 $- Total Deposits ($B) $6.0 1 $5.1 $5.0 $4.0 $3.0 $2.0 $0.6 $1.0 $- Note: Acquisitions of Atlantic Liberty Financial Corp in 2006 (assets and deposits acquired of $180MM and $107MM); New York Federal Savings Bank in 1997 1 8 (assets and deposits acquired of $84MM and $51MM). Includes mortgagors’ escrow deposits.Proven Track Record of Steady Organic Growth Total Gross Loans ($B) $6.0 $6.0 $5.0 $4.0 $3.0 $2.0 $1.0 $0.3 $- Total Deposits ($B) $6.0 1 $5.1 $5.0 $4.0 $3.0 $2.0 $0.6 $1.0 $- Note: Acquisitions of Atlantic Liberty Financial Corp in 2006 (assets and deposits acquired of $180MM and $107MM); New York Federal Savings Bank in 1997 1 8 (assets and deposits acquired of $84MM and $51MM). Includes mortgagors’ escrow deposits.

Strong Asian Banking Market Focus § Asian Bank within Flushing Bank § New branch opened in Hicksville, NY in 4Q19 to expand our focus on the Asian population to the Long Island market § Relocated branch to Bayside Queens in 4Q19 § Loans in the Asian communities total over 1 $650MM with deposits exceeding $900MM § Flushing deposits in Asian branch footprint increased 18% from June 30, 2018 to June 30, 2 2019 while the market size decreased § Multilingual branch staff serves our diverse customer base in the New York City market area § Growth aided by the Asian Advisory Board 1 2 2Q20 includes Bayside and Hicksville branches. FDIC data. 9Strong Asian Banking Market Focus § Asian Bank within Flushing Bank § New branch opened in Hicksville, NY in 4Q19 to expand our focus on the Asian population to the Long Island market § Relocated branch to Bayside Queens in 4Q19 § Loans in the Asian communities total over 1 $650MM with deposits exceeding $900MM § Flushing deposits in Asian branch footprint increased 18% from June 30, 2018 to June 30, 2 2019 while the market size decreased § Multilingual branch staff serves our diverse customer base in the New York City market area § Growth aided by the Asian Advisory Board 1 2 2Q20 includes Bayside and Hicksville branches. FDIC data. 9

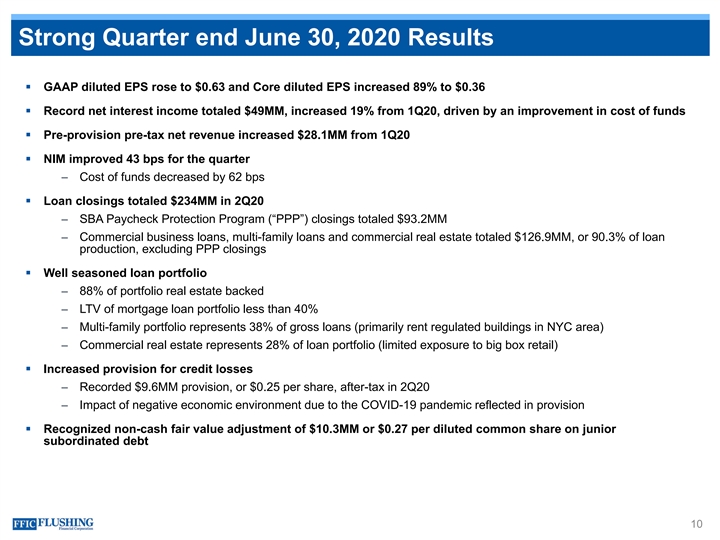

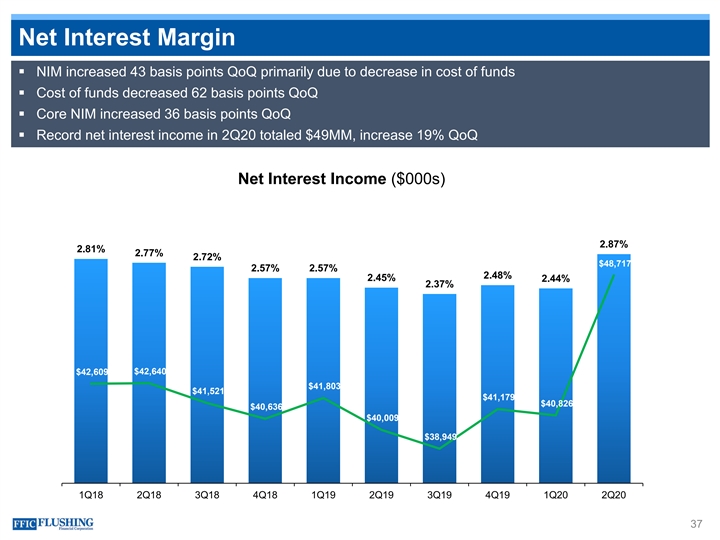

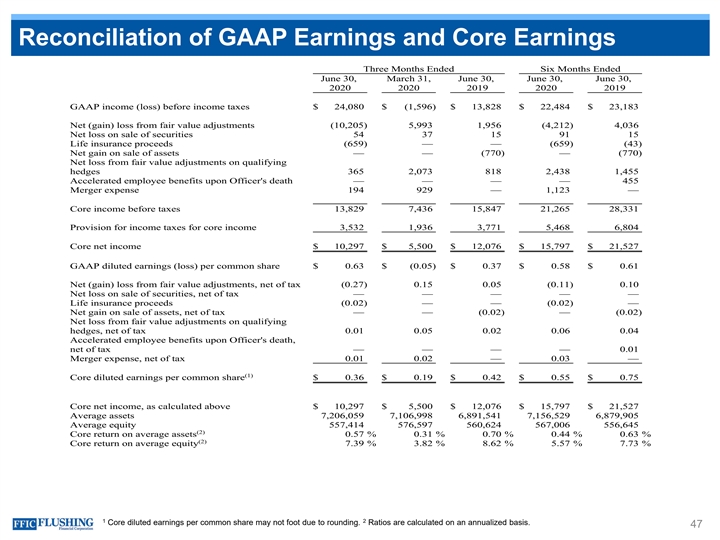

Strong Quarter end June 30, 2020 Results § GAAP diluted EPS rose to $0.63 and Core diluted EPS increased 89% to $0.36 § Record net interest income totaled $49MM, increased 19% from 1Q20, driven by an improvement in cost of funds § Pre-provision pre-tax net revenue increased $28.1MM from 1Q20 § NIM improved 43 bps for the quarter – Cost of funds decreased by 62 bps § Loan closings totaled $234MM in 2Q20 – SBA Paycheck Protection Program (“PPP”) closings totaled $93.2MM – Commercial business loans, multi-family loans and commercial real estate totaled $126.9MM, or 90.3% of loan production, excluding PPP closings § Well seasoned loan portfolio – 88% of portfolio real estate backed – LTV of mortgage loan portfolio less than 40% – Multi-family portfolio represents 38% of gross loans (primarily rent regulated buildings in NYC area) – Commercial real estate represents 28% of loan portfolio (limited exposure to big box retail) § Increased provision for credit losses – Recorded $9.6MM provision, or $0.25 per share, after-tax in 2Q20 – Impact of negative economic environment due to the COVID-19 pandemic reflected in provision § Recognized non-cash fair value adjustment of $10.3MM or $0.27 per diluted common share on junior subordinated debt 10Strong Quarter end June 30, 2020 Results § GAAP diluted EPS rose to $0.63 and Core diluted EPS increased 89% to $0.36 § Record net interest income totaled $49MM, increased 19% from 1Q20, driven by an improvement in cost of funds § Pre-provision pre-tax net revenue increased $28.1MM from 1Q20 § NIM improved 43 bps for the quarter – Cost of funds decreased by 62 bps § Loan closings totaled $234MM in 2Q20 – SBA Paycheck Protection Program (“PPP”) closings totaled $93.2MM – Commercial business loans, multi-family loans and commercial real estate totaled $126.9MM, or 90.3% of loan production, excluding PPP closings § Well seasoned loan portfolio – 88% of portfolio real estate backed – LTV of mortgage loan portfolio less than 40% – Multi-family portfolio represents 38% of gross loans (primarily rent regulated buildings in NYC area) – Commercial real estate represents 28% of loan portfolio (limited exposure to big box retail) § Increased provision for credit losses – Recorded $9.6MM provision, or $0.25 per share, after-tax in 2Q20 – Impact of negative economic environment due to the COVID-19 pandemic reflected in provision § Recognized non-cash fair value adjustment of $10.3MM or $0.27 per diluted common share on junior subordinated debt 10

Empire Bank Acquisition 11Empire Bank Acquisition 11

Empire Bank Acquisition nd § Combined entity will be Long Island’s 2 largest bank by deposit share among regional and community 1 financial institutions • Expands Flushing’s presence across Long Island with entrance into Suffolk County Compelling • Meets Flushing's strategic objectives by improving cost of deposits and lowering loan-to-deposit Strategic ratio Rationale • Expands business opportunities through Flushing’s enhanced technological capabilities § Increased size and geographic reach enhances operating leverage and profitability § 20% accretive in 2021 Positive 2 § Tangible book value dilution of 7.2% at close, with an earnback of 3.4 years Financial Impact 3 § Pro forma efficiency ratio improves ~300bps to 52% Seamless § Empire’s asset base is 15% relative to Flushing, allowing for a manageable integration process Integration § Empire’s current credit conditions are similar to what Flushing is experiencing Execution 1 Based on aggregate deposit market share for Kings, Queens, Nassau & Suffolk counties for community banks <$20 billion in assets 2 Using cross-over method. Calculated as time period at which Flushing’s pro forma tangible book value per share equals Flushing’s stand-alone tangible book value per share 3 Based on pro forma core non-interest expenses for the quarter ended June 30, 2020 including fully phased-in cost savings Source: Company reports, S&P Global Market Intelligence 12Empire Bank Acquisition nd § Combined entity will be Long Island’s 2 largest bank by deposit share among regional and community 1 financial institutions • Expands Flushing’s presence across Long Island with entrance into Suffolk County Compelling • Meets Flushing's strategic objectives by improving cost of deposits and lowering loan-to-deposit Strategic ratio Rationale • Expands business opportunities through Flushing’s enhanced technological capabilities § Increased size and geographic reach enhances operating leverage and profitability § 20% accretive in 2021 Positive 2 § Tangible book value dilution of 7.2% at close, with an earnback of 3.4 years Financial Impact 3 § Pro forma efficiency ratio improves ~300bps to 52% Seamless § Empire’s asset base is 15% relative to Flushing, allowing for a manageable integration process Integration § Empire’s current credit conditions are similar to what Flushing is experiencing Execution 1 Based on aggregate deposit market share for Kings, Queens, Nassau & Suffolk counties for community banks <$20 billion in assets 2 Using cross-over method. Calculated as time period at which Flushing’s pro forma tangible book value per share equals Flushing’s stand-alone tangible book value per share 3 Based on pro forma core non-interest expenses for the quarter ended June 30, 2020 including fully phased-in cost savings Source: Company reports, S&P Global Market Intelligence 12

Cost Saves Drive Additional Accretion Cost Savings Breakdown 2021E ~20% EPS Accretion by Responsibility Centers ($MM) ~$63 Internal 2 ~$7 Cost savings audit Marketing 1% 7% 1 3 ~$7 EMPK standalone ~$48 Finance 9% Executive 12% 1 Non- FFIC standalone ~$48 revenue staffing 59% IT 12% 4 FFIC 2021E standalone 2021E pro forma 5 Pre-Tax Cost Savings: ~$9.2MM Share count 28.9MM 31.4MM 1 Based on FFIC management guidance for standalone 2021E earnings 2 Represents fully-phased in cost savings of ~50% of EMPK’s cost base, after-tax 3 Represents EMPK’s projected standalone income 4 Does not include effects of purchase accounting adjustments or the implementation of CECL 5 Incremental shares based on 0.6548x fixed exchange ratio for 50% of transaction consideration at announcement Note: Assumes a 21% tax rate Source: Company reports, S&P Global Market Intelligence 13Cost Saves Drive Additional Accretion Cost Savings Breakdown 2021E ~20% EPS Accretion by Responsibility Centers ($MM) ~$63 Internal 2 ~$7 Cost savings audit Marketing 1% 7% 1 3 ~$7 EMPK standalone ~$48 Finance 9% Executive 12% 1 Non- FFIC standalone ~$48 revenue staffing 59% IT 12% 4 FFIC 2021E standalone 2021E pro forma 5 Pre-Tax Cost Savings: ~$9.2MM Share count 28.9MM 31.4MM 1 Based on FFIC management guidance for standalone 2021E earnings 2 Represents fully-phased in cost savings of ~50% of EMPK’s cost base, after-tax 3 Represents EMPK’s projected standalone income 4 Does not include effects of purchase accounting adjustments or the implementation of CECL 5 Incremental shares based on 0.6548x fixed exchange ratio for 50% of transaction consideration at announcement Note: Assumes a 21% tax rate Source: Company reports, S&P Global Market Intelligence 13

Combination Creates a Leading Long Island Franchise 1 1 Median Household Income ($MM) # of Businesses $119.2 20 Branches 74,963 73,116 $103.8 $96.1 4 Branches $66.0 Suffolk New York Nassau Queens Nassau Suffolk Nassau Suffolk Flushing U.S. Average County County Current County County Kings Markets 2 Pro Forma Financial Highlights ($MM) 3 3 Lowers Flushing’s cost of deposits and $8,215 $5,983 improves loan-to-deposit ratio Assets Deposits ü 3 3 Enhances core earnings power and $6,681 110.9% provides significant cost savings Loans / deposits Gross Loans ü opportunities Expands Flushing’s geographic presence 0.76% $375 4 5 into Suffolk County ROAA Market cap ü 1 Demographic data as of the quarter ended June 30, 2019 2 Based on Flushing’s estimates for the combined entity without merger adjustments 3 Pro forma data as of the quarter ended June 30, 2020, including net deferred fees / costs 4 Based on 2021 estimated projections 5 Based on Flushing’s closing price on August 13, 2020 multiplied by pro forma diluted outstanding shares of Flushing after giving effect to the transaction Source: Company reports, S&P Global Market Intelligence 14Combination Creates a Leading Long Island Franchise 1 1 Median Household Income ($MM) # of Businesses $119.2 20 Branches 74,963 73,116 $103.8 $96.1 4 Branches $66.0 Suffolk New York Nassau Queens Nassau Suffolk Nassau Suffolk Flushing U.S. Average County County Current County County Kings Markets 2 Pro Forma Financial Highlights ($MM) 3 3 Lowers Flushing’s cost of deposits and $8,215 $5,983 improves loan-to-deposit ratio Assets Deposits ü 3 3 Enhances core earnings power and $6,681 110.9% provides significant cost savings Loans / deposits Gross Loans ü opportunities Expands Flushing’s geographic presence 0.76% $375 4 5 into Suffolk County ROAA Market cap ü 1 Demographic data as of the quarter ended June 30, 2019 2 Based on Flushing’s estimates for the combined entity without merger adjustments 3 Pro forma data as of the quarter ended June 30, 2020, including net deferred fees / costs 4 Based on 2021 estimated projections 5 Based on Flushing’s closing price on August 13, 2020 multiplied by pro forma diluted outstanding shares of Flushing after giving effect to the transaction Source: Company reports, S&P Global Market Intelligence 14

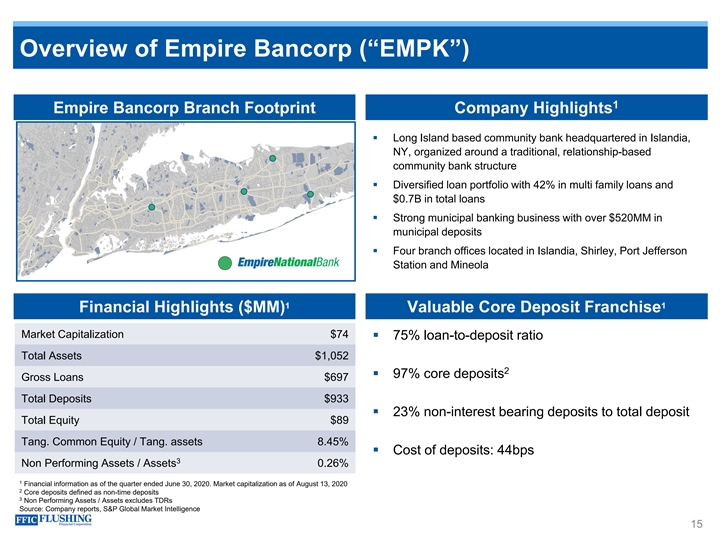

Overview of Empire Bancorp (“EMPK”) 1 Empire Bancorp Branch Footprint Company Highlights § Long Island based community bank headquartered in Islandia, NY, organized around a traditional, relationship-based community bank structure § Diversified loan portfolio with 42% in multi family loans and $0.7B in total loans § Strong municipal banking business with over $520MM in municipal deposits § Four branch offices located in Islandia, Shirley, Port Jefferson Station and Mineola 1 1 Financial Highlights ($MM) Valuable Core Deposit Franchise Market Capitalization $74 § 75% loan-to-deposit ratio Total Assets $1,052 2 § 97% core deposits Gross Loans $697 Total Deposits $933 § 23% non-interest bearing deposits to total deposit Total Equity $89 Tang. Common Equity / Tang. assets 8.45% § Cost of deposits: 44bps 3 Non Performing Assets / Assets 0.26% 1 Financial information as of the quarter ended June 30, 2020. Market capitalization as of August 13, 2020 2 Core deposits defined as non-time deposits 3 Non Performing Assets / Assets excludes TDRs Source: Company reports, S&P Global Market Intelligence 15Overview of Empire Bancorp (“EMPK”) 1 Empire Bancorp Branch Footprint Company Highlights § Long Island based community bank headquartered in Islandia, NY, organized around a traditional, relationship-based community bank structure § Diversified loan portfolio with 42% in multi family loans and $0.7B in total loans § Strong municipal banking business with over $520MM in municipal deposits § Four branch offices located in Islandia, Shirley, Port Jefferson Station and Mineola 1 1 Financial Highlights ($MM) Valuable Core Deposit Franchise Market Capitalization $74 § 75% loan-to-deposit ratio Total Assets $1,052 2 § 97% core deposits Gross Loans $697 Total Deposits $933 § 23% non-interest bearing deposits to total deposit Total Equity $89 Tang. Common Equity / Tang. assets 8.45% § Cost of deposits: 44bps 3 Non Performing Assets / Assets 0.26% 1 Financial information as of the quarter ended June 30, 2020. Market capitalization as of August 13, 2020 2 Core deposits defined as non-time deposits 3 Non Performing Assets / Assets excludes TDRs Source: Company reports, S&P Global Market Intelligence 15

Expansion into Suffolk County Suffolk New York Nassau Queens 1 Long Island Regional Banks Deposits Kings ($B) Apple Financial Holdings $6.1 $5.4 Pro Forma Flushing 2 Pro Forma Geographic Footprint $4.5 New York City 3 $2.4B 16 Dime Bancorp $4.5 Deposits Branches Ridgewood Savings Bank $3.7 Nassau County 3 $2.7B 5 Bridge Bancorp $3.7 Deposits Branches First of Long Island $3.3 Suffolk County Maspeth FSLA $0.9B 3 $1.2 Deposits Branches Cathay General Bancorp $1.0 1 Aggregate deposit market share for Kings, Queens, Nassau & Suffolk counties for community banks <$20 billion in assets 2 FFIC and EMPK values as of June 30, 2020 3 Dime Bancorp and Bridge Bancorp announced an agreement to merge on July 1, 2020 Source: S&P Global Market Intelligence. Data as of June 30, 2019 $0.0 $1.0 $2.0 $3.0 $4.0 $5.0 $6.0 $7.0 16Expansion into Suffolk County Suffolk New York Nassau Queens 1 Long Island Regional Banks Deposits Kings ($B) Apple Financial Holdings $6.1 $5.4 Pro Forma Flushing 2 Pro Forma Geographic Footprint $4.5 New York City 3 $2.4B 16 Dime Bancorp $4.5 Deposits Branches Ridgewood Savings Bank $3.7 Nassau County 3 $2.7B 5 Bridge Bancorp $3.7 Deposits Branches First of Long Island $3.3 Suffolk County Maspeth FSLA $0.9B 3 $1.2 Deposits Branches Cathay General Bancorp $1.0 1 Aggregate deposit market share for Kings, Queens, Nassau & Suffolk counties for community banks <$20 billion in assets 2 FFIC and EMPK values as of June 30, 2020 3 Dime Bancorp and Bridge Bancorp announced an agreement to merge on July 1, 2020 Source: S&P Global Market Intelligence. Data as of June 30, 2019 $0.0 $1.0 $2.0 $3.0 $4.0 $5.0 $6.0 $7.0 16

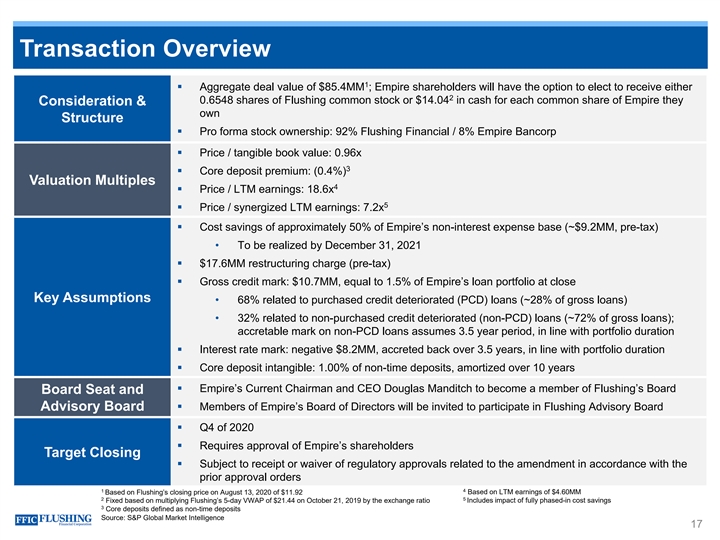

Transaction Overview 1 § Aggregate deal value of $85.4MM ; Empire shareholders will have the option to elect to receive either 2 0.6548 shares of Flushing common stock or $14.04 in cash for each common share of Empire they Consideration & own Structure § Pro forma stock ownership: 92% Flushing Financial / 8% Empire Bancorp § Price / tangible book value: 0.96x 3 § Core deposit premium: (0.4%) Valuation Multiples 4 § Price / LTM earnings: 18.6x 5 § Price / synergized LTM earnings: 7.2x § Cost savings of approximately 50% of Empire’s non-interest expense base (~$9.2MM, pre-tax) • To be realized by December 31, 2021 § $17.6MM restructuring charge (pre-tax) § Gross credit mark: $10.7MM, equal to 1.5% of Empire’s loan portfolio at close Key Assumptions • 68% related to purchased credit deteriorated (PCD) loans (~28% of gross loans) • 32% related to non-purchased credit deteriorated (non-PCD) loans (~72% of gross loans); accretable mark on non-PCD loans assumes 3.5 year period, in line with portfolio duration § Interest rate mark: negative $8.2MM, accreted back over 3.5 years, in line with portfolio duration § Core deposit intangible: 1.00% of non-time deposits, amortized over 10 years § Empire’s Current Chairman and CEO Douglas Manditch to become a member of Flushing’s Board Board Seat and § Members of Empire’s Board of Directors will be invited to participate in Flushing Advisory Board Advisory Board § Q4 of 2020 § Requires approval of Empire’s shareholders Target Closing § Subject to receipt or waiver of regulatory approvals related to the amendment in accordance with the prior approval orders 4 1 Based on LTM earnings of $4.60MM Based on Flushing’s closing price on August 13, 2020 of $11.92 2 5 Fixed based on multiplying Flushing’s 5-day VWAP of $21.44 on October 21, 2019 by the exchange ratio Includes impact of fully phased-in cost savings 3 Core deposits defined as non-time deposits Source: S&P Global Market Intelligence 17Transaction Overview 1 § Aggregate deal value of $85.4MM ; Empire shareholders will have the option to elect to receive either 2 0.6548 shares of Flushing common stock or $14.04 in cash for each common share of Empire they Consideration & own Structure § Pro forma stock ownership: 92% Flushing Financial / 8% Empire Bancorp § Price / tangible book value: 0.96x 3 § Core deposit premium: (0.4%) Valuation Multiples 4 § Price / LTM earnings: 18.6x 5 § Price / synergized LTM earnings: 7.2x § Cost savings of approximately 50% of Empire’s non-interest expense base (~$9.2MM, pre-tax) • To be realized by December 31, 2021 § $17.6MM restructuring charge (pre-tax) § Gross credit mark: $10.7MM, equal to 1.5% of Empire’s loan portfolio at close Key Assumptions • 68% related to purchased credit deteriorated (PCD) loans (~28% of gross loans) • 32% related to non-purchased credit deteriorated (non-PCD) loans (~72% of gross loans); accretable mark on non-PCD loans assumes 3.5 year period, in line with portfolio duration § Interest rate mark: negative $8.2MM, accreted back over 3.5 years, in line with portfolio duration § Core deposit intangible: 1.00% of non-time deposits, amortized over 10 years § Empire’s Current Chairman and CEO Douglas Manditch to become a member of Flushing’s Board Board Seat and § Members of Empire’s Board of Directors will be invited to participate in Flushing Advisory Board Advisory Board § Q4 of 2020 § Requires approval of Empire’s shareholders Target Closing § Subject to receipt or waiver of regulatory approvals related to the amendment in accordance with the prior approval orders 4 1 Based on LTM earnings of $4.60MM Based on Flushing’s closing price on August 13, 2020 of $11.92 2 5 Fixed based on multiplying Flushing’s 5-day VWAP of $21.44 on October 21, 2019 by the exchange ratio Includes impact of fully phased-in cost savings 3 Core deposits defined as non-time deposits Source: S&P Global Market Intelligence 17

Pro Forma Deposit Mix Reduction in Cost of Deposits Empire National Bank Pro Forma Flushing Bank 13% 12% 19% 3% 22% 23% 74% 66% 68% MMDA/Savings, and other Non-interest bearing CDs Total deposits: $5.1B Total deposits: $0.9B Total deposits: $6.0B Cost of total deposits: 0.79% Cost of total deposits: 0.44% Cost of total deposits: 0.74% Loan-to-deposit 117% 74% 111% ratio (%) Note: Data represents bank level entity reporting data Source: S&P Global Market Intelligence. Data as of the quarter ended June 30, 2020 18Pro Forma Deposit Mix Reduction in Cost of Deposits Empire National Bank Pro Forma Flushing Bank 13% 12% 19% 3% 22% 23% 74% 66% 68% MMDA/Savings, and other Non-interest bearing CDs Total deposits: $5.1B Total deposits: $0.9B Total deposits: $6.0B Cost of total deposits: 0.79% Cost of total deposits: 0.44% Cost of total deposits: 0.74% Loan-to-deposit 117% 74% 111% ratio (%) Note: Data represents bank level entity reporting data Source: S&P Global Market Intelligence. Data as of the quarter ended June 30, 2020 18

Pro Forma Balance Sheet Increases Loan Yield Empire National Bank Pro Forma Flushing Bank 2% 6% 2% 6% 3% 9% 14% 14% 39% 38% 42% 21% 13% 13% 12% 13% 27% 26% Multi-family CRE Investor 1-4 Family C&I CRE Owner-occupied Other Total loans: $6.0B Total loans: $0.7B Total loans: $6.7B Yield on loans: 4.07% Yield on loans: 4.41% Yield on loans: 4.11% Note: Data represents bank level entity reporting data Source: S&P Global Market Intelligence. Data as of the quarter ended June 30, 2020 19Pro Forma Balance Sheet Increases Loan Yield Empire National Bank Pro Forma Flushing Bank 2% 6% 2% 6% 3% 9% 14% 14% 39% 38% 42% 21% 13% 13% 12% 13% 27% 26% Multi-family CRE Investor 1-4 Family C&I CRE Owner-occupied Other Total loans: $6.0B Total loans: $0.7B Total loans: $6.7B Yield on loans: 4.07% Yield on loans: 4.41% Yield on loans: 4.11% Note: Data represents bank level entity reporting data Source: S&P Global Market Intelligence. Data as of the quarter ended June 30, 2020 19

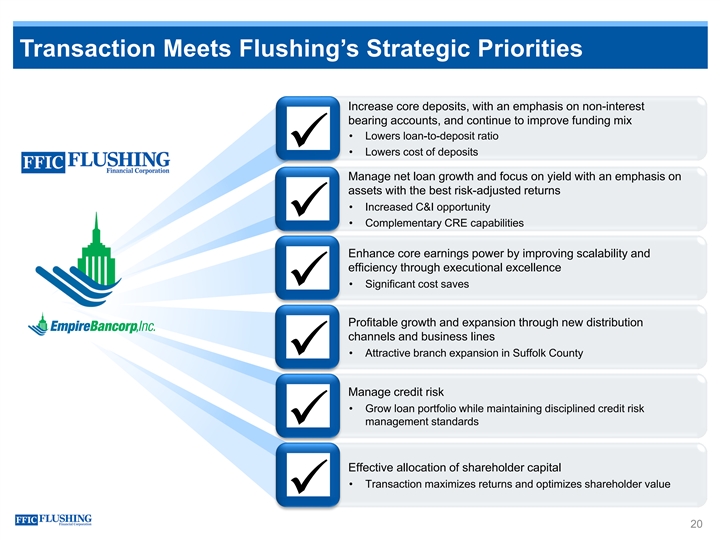

Transaction Meets Flushing’s Strategic Priorities Increase core deposits, with an emphasis on non-interest bearing accounts, and continue to improve funding mix • Lowers loan-to-deposit ratio ü • Lowers cost of deposits Manage net loan growth and focus on yield with an emphasis on assets with the best risk-adjusted returns • Increased C&I opportunity ü • Complementary CRE capabilities Enhance core earnings power by improving scalability and efficiency through executional excellence • Significant cost saves ü ü Profitable growth and expansion through new distribution channels and business lines • Attractive branch expansion in Suffolk County ü Manage credit risk • Grow loan portfolio while maintaining disciplined credit risk management standards ü Effective allocation of shareholder capital • Transaction maximizes returns and optimizes shareholder value ü 20Transaction Meets Flushing’s Strategic Priorities Increase core deposits, with an emphasis on non-interest bearing accounts, and continue to improve funding mix • Lowers loan-to-deposit ratio ü • Lowers cost of deposits Manage net loan growth and focus on yield with an emphasis on assets with the best risk-adjusted returns • Increased C&I opportunity ü • Complementary CRE capabilities Enhance core earnings power by improving scalability and efficiency through executional excellence • Significant cost saves ü ü Profitable growth and expansion through new distribution channels and business lines • Attractive branch expansion in Suffolk County ü Manage credit risk • Grow loan portfolio while maintaining disciplined credit risk management standards ü Effective allocation of shareholder capital • Transaction maximizes returns and optimizes shareholder value ü 20

COVID-19 and Credit 21COVID-19 and Credit 21

Adaptability and Flexibility in COVID-19 Environment TEAM MEMBERS CUSTOMERS COMMUNITIES § Safety and health of § SBA PPP loan closings § Delivering food to hospitals employees is our top priority $93.2MM at June 30, 2020 in support of healthcare workers on the frontlines in our § 85% of back office staff § Active loan forbearances communities working remotely on any given with outstanding balance of day; capability for nearly all ~$1.3B (as of 6/30/2020)§ Set up appointment banking employees to work remotely to service clients without the § 37 Forbearances totaling need to overcrowd branches § Granted additional PTO and $91.9MM completed deferral, and practice social distancing expanded paid family leave resumed making payments and medical leave benefits § Waiving ATM fees for § Enhanced digital capabilities adhering to government customers and non-customers through recent improvement of regulations mobile and on-line banking§ Waiving late fees on loans § No furloughs; no job § 19% of retail account § Participating in State of New discontinuances; no pay openings in second quarter York Main Street Lending decreases were completed online Program § Participating in FHLBNY Small Business Recovery Grant Consistent with Our History of Supporting Communities, Customers and Employees with Superior Customer Service, Flushing is Committed to Providing Flexibility to All that We Serve in this Time of Need 22Adaptability and Flexibility in COVID-19 Environment TEAM MEMBERS CUSTOMERS COMMUNITIES § Safety and health of § SBA PPP loan closings § Delivering food to hospitals employees is our top priority $93.2MM at June 30, 2020 in support of healthcare workers on the frontlines in our § 85% of back office staff § Active loan forbearances communities working remotely on any given with outstanding balance of day; capability for nearly all ~$1.3B (as of 6/30/2020)§ Set up appointment banking employees to work remotely to service clients without the § 37 Forbearances totaling need to overcrowd branches § Granted additional PTO and $91.9MM completed deferral, and practice social distancing expanded paid family leave resumed making payments and medical leave benefits § Waiving ATM fees for § Enhanced digital capabilities adhering to government customers and non-customers through recent improvement of regulations mobile and on-line banking§ Waiving late fees on loans § No furloughs; no job § 19% of retail account § Participating in State of New discontinuances; no pay openings in second quarter York Main Street Lending decreases were completed online Program § Participating in FHLBNY Small Business Recovery Grant Consistent with Our History of Supporting Communities, Customers and Employees with Superior Customer Service, Flushing is Committed to Providing Flexibility to All that We Serve in this Time of Need 22

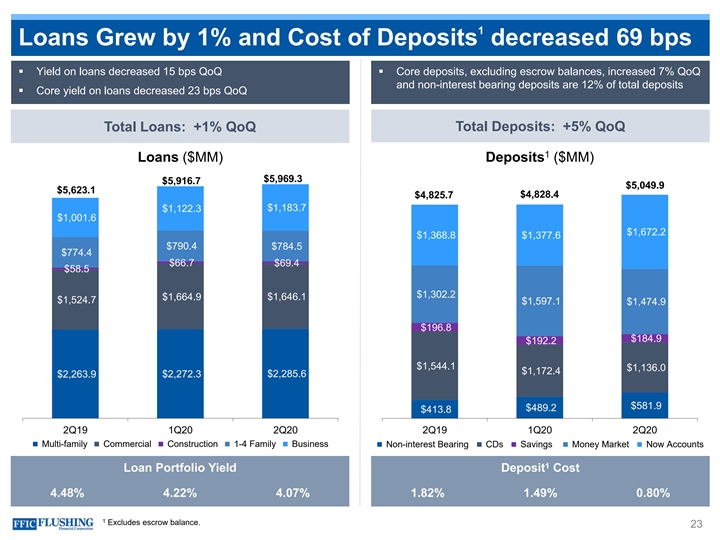

1 Loans Grew by 1% and Cost of Deposits decreased 69 bps § Yield on loans decreased 15 bps QoQ§ Core deposits, excluding escrow balances, increased 7% QoQ and non-interest bearing deposits are 12% of total deposits § Core yield on loans decreased 23 bps QoQ Total Deposits: +5% QoQ Total Loans: +1% QoQ 1 Loans ($MM) Deposits ($MM) $5,969.3 $5,916.7 $5,049.9 $5,623.1 $4,825.7 $4,828.4 $1,183.7 $1,122.3 $1,001.6 $1,672.2 $1,368.8 $1,377.6 $790.4 $784.5 $774.4 $66.7 $69.4 $58.5 $1,302.2 $1,664.9 $1,646.1 $1,524.7 $1,597.1 $1,474.9 $196.8 $184.9 $192.2 $1,544.1 $1,136.0 $1,172.4 $2,272.3 $2,285.6 $2,263.9 $581.9 $489.2 $413.8 2Q19 1Q20 2Q20 2Q19 1Q20 2Q20 Multi-family Commercial Construction 1-4 Family Business Non-interest Bearing CDs Savings Money Market Now Accounts 1 Loan Portfolio Yield Deposit Cost 4.48% 4.22% 4.07% 1.82% 1.49% 0.80% 1 Excludes escrow balance. 231 Loans Grew by 1% and Cost of Deposits decreased 69 bps § Yield on loans decreased 15 bps QoQ§ Core deposits, excluding escrow balances, increased 7% QoQ and non-interest bearing deposits are 12% of total deposits § Core yield on loans decreased 23 bps QoQ Total Deposits: +5% QoQ Total Loans: +1% QoQ 1 Loans ($MM) Deposits ($MM) $5,969.3 $5,916.7 $5,049.9 $5,623.1 $4,825.7 $4,828.4 $1,183.7 $1,122.3 $1,001.6 $1,672.2 $1,368.8 $1,377.6 $790.4 $784.5 $774.4 $66.7 $69.4 $58.5 $1,302.2 $1,664.9 $1,646.1 $1,524.7 $1,597.1 $1,474.9 $196.8 $184.9 $192.2 $1,544.1 $1,136.0 $1,172.4 $2,272.3 $2,285.6 $2,263.9 $581.9 $489.2 $413.8 2Q19 1Q20 2Q20 2Q19 1Q20 2Q20 Multi-family Commercial Construction 1-4 Family Business Non-interest Bearing CDs Savings Money Market Now Accounts 1 Loan Portfolio Yield Deposit Cost 4.48% 4.22% 4.07% 1.82% 1.49% 0.80% 1 Excludes escrow balance. 23

Composition of Our CRE and C&I Portfolios § C&I closings totaled $153MM § Mortgage loan closings total $81MM § At June 30, 2020 the pipeline totaled $311MM at an average rate of 3.81% 1 C&I CRE 2% 3% Real Estate Collateral 6% $488.1MM 12% 13% 3% 2% 4% 10% 8% 3% 4% $1,094.6MM $3,931.6MM 9% Total Portfolio 7% 8% Total Portfolio 58% 8% 7% 7% 8% 6% 12% § Hotels: 12%§ Medical: 10% § Auto/Marine Transportation: 9%§ Airlines: 8% § Entertainment: 8%§ Financing Company: 6% § Multi-Family: 58%§ General Commercial: 12% § Manufacturers: 7%§ Retail Services: 7% § CRE – Shopping Center: 8%§ CRE – Strip Mall: 8% § Construction Related: 7%§ Restaurants/Bars/Food Service: 4% § CRE – Single Tenant: 3%§ Office: 6% § Real Estate Related: 3%§ Professional Services: 4% § Commercial Special Use: 3%§ Industrial: 2% § School / Child Care: 2%§ Other: 13% 1 24 Excludes $93.2MM in SBA PPP loansComposition of Our CRE and C&I Portfolios § C&I closings totaled $153MM § Mortgage loan closings total $81MM § At June 30, 2020 the pipeline totaled $311MM at an average rate of 3.81% 1 C&I CRE 2% 3% Real Estate Collateral 6% $488.1MM 12% 13% 3% 2% 4% 10% 8% 3% 4% $1,094.6MM $3,931.6MM 9% Total Portfolio 7% 8% Total Portfolio 58% 8% 7% 7% 8% 6% 12% § Hotels: 12%§ Medical: 10% § Auto/Marine Transportation: 9%§ Airlines: 8% § Entertainment: 8%§ Financing Company: 6% § Multi-Family: 58%§ General Commercial: 12% § Manufacturers: 7%§ Retail Services: 7% § CRE – Shopping Center: 8%§ CRE – Strip Mall: 8% § Construction Related: 7%§ Restaurants/Bars/Food Service: 4% § CRE – Single Tenant: 3%§ Office: 6% § Real Estate Related: 3%§ Professional Services: 4% § Commercial Special Use: 3%§ Industrial: 2% § School / Child Care: 2%§ Other: 13% 1 24 Excludes $93.2MM in SBA PPP loans

Outstanding Loans in Forbearance § Forbearances are primarily backed by mortgages § Forbearances are either deferral of principal and interest, principal, or escrow or combination thereof § Repayment of deferred principal and interest is generally not due until loan maturity As of 6/30/20 ($MM) $728.3 $308.6 $114.6 $37.7 $24.4 $21.2 $14.8 $16.1 $12.4 Restaurants & Hotels Travel & Leisure Retail Services CRE Retail Transportation Contractors Schools & Child Less Risky Catering Halls Outlets Care Exposures 25Outstanding Loans in Forbearance § Forbearances are primarily backed by mortgages § Forbearances are either deferral of principal and interest, principal, or escrow or combination thereof § Repayment of deferred principal and interest is generally not due until loan maturity As of 6/30/20 ($MM) $728.3 $308.6 $114.6 $37.7 $24.4 $21.2 $14.8 $16.1 $12.4 Restaurants & Hotels Travel & Leisure Retail Services CRE Retail Transportation Contractors Schools & Child Less Risky Catering Halls Outlets Care Exposures 25

COVID-19 Impact on Retail § FB portfolio stabilizing as many tenants were able to operate at some capacity during lockdown – Limited exposure to national chains – Gradual opening of New York economy allowed more business to operate § Shopping centers and local strip malls began to recover in Phases 2 and 3 – Our portfolio remains driven by essential needs tenancy less affected by on-line retail – Landlords willing to work with tenants to reopen businesses and providing modified lease terms – Properties largely located in populated neighborhoods – Tenancy of typical center generally longer-term tenants at or below market rental terms § Recently inspected 42% of Retail Outlet properties across the portfolio – Stores largely open for business – Customer traffic appears to be returning § All properties appeared to be well maintained and stores appeared to be well stocked 26COVID-19 Impact on Retail § FB portfolio stabilizing as many tenants were able to operate at some capacity during lockdown – Limited exposure to national chains – Gradual opening of New York economy allowed more business to operate § Shopping centers and local strip malls began to recover in Phases 2 and 3 – Our portfolio remains driven by essential needs tenancy less affected by on-line retail – Landlords willing to work with tenants to reopen businesses and providing modified lease terms – Properties largely located in populated neighborhoods – Tenancy of typical center generally longer-term tenants at or below market rental terms § Recently inspected 42% of Retail Outlet properties across the portfolio – Stores largely open for business – Customer traffic appears to be returning § All properties appeared to be well maintained and stores appeared to be well stocked 26

Forbearance Process § Independent team monitors progress of loans granted forbearance during COVID-19 § Focused on the following: – Maintaining customer contact – Site visits – Follow up for current financial data – Review regular reporting to assess rent collection activity – Evaluate loan performance and make recommendations on need for assistance – Provide reporting and tracking of assistance plans due to expire § Results to date – As of July 10, 2020, of the expiring forbearances with an outstanding balance of $146.3MM, $91.9MM have returned to regularly scheduled payment – Site inspections performed on loans secured by retail properties with total exposure of $286MM § Overall results indicate that borrowers are working with tenants to stabilize operations – Concessions in form of moderately reduced rents during early months of pandemic – Granting of extended lease terms in order to recover past due rent – Delinquent rents are collected over time with borrowers paying current rents 27Forbearance Process § Independent team monitors progress of loans granted forbearance during COVID-19 § Focused on the following: – Maintaining customer contact – Site visits – Follow up for current financial data – Review regular reporting to assess rent collection activity – Evaluate loan performance and make recommendations on need for assistance – Provide reporting and tracking of assistance plans due to expire § Results to date – As of July 10, 2020, of the expiring forbearances with an outstanding balance of $146.3MM, $91.9MM have returned to regularly scheduled payment – Site inspections performed on loans secured by retail properties with total exposure of $286MM § Overall results indicate that borrowers are working with tenants to stabilize operations – Concessions in form of moderately reduced rents during early months of pandemic – Granting of extended lease terms in order to recover past due rent – Delinquent rents are collected over time with borrowers paying current rents 27

Credit Quality 2Q20 Highlights § Non-performing loans totaled $20.2MM, an increase of 20.5% QoQ and 28.6% YoY § Loan-to-value ratio on real estate dependent loans as of June 30, 2020 totaled 38.1% § Average loan-to-value for non-performing loans collateralized by real estate at June 30, 2020 was 30.3% Non-performing Loans ($000s) Net Charge-offs ($000s) $1,149 $20,188 $1,007 $979 $16,752 $15,702 2Q19 1Q20 2Q20 2Q19 1Q20 2Q20 Non-Performing Loans as a % of Gross Loans Charge-offs as a % of Average Loans 0.28% 0.28% 0.34% 0.07% 0.08% 0.07% 28Credit Quality 2Q20 Highlights § Non-performing loans totaled $20.2MM, an increase of 20.5% QoQ and 28.6% YoY § Loan-to-value ratio on real estate dependent loans as of June 30, 2020 totaled 38.1% § Average loan-to-value for non-performing loans collateralized by real estate at June 30, 2020 was 30.3% Non-performing Loans ($000s) Net Charge-offs ($000s) $1,149 $20,188 $1,007 $979 $16,752 $15,702 2Q19 1Q20 2Q20 2Q19 1Q20 2Q20 Non-Performing Loans as a % of Gross Loans Charge-offs as a % of Average Loans 0.28% 0.28% 0.34% 0.07% 0.08% 0.07% 28

Credit Outlook § Strong credit history § Our loan portfolio is 88% collateralized by real estate with an average LTV of 38% § Minimal 90+ delinquencies representing 32 bps of gross loans § Ratio of Classified Assets to Total Capital is 3.5% at June 30, 2020 § Forbearance down 13% from intra-period peak – Of the $146MM of loans expected to return to paying status, 63% have done so through July 17, 2020 – Active forbearances have decreased to $1.3B from peak of $1.5B – Pace of forbearance requests has declined § New York Metro area is beginning to open up – Over 90% of the loan portfolio is situated in the area 29Credit Outlook § Strong credit history § Our loan portfolio is 88% collateralized by real estate with an average LTV of 38% § Minimal 90+ delinquencies representing 32 bps of gross loans § Ratio of Classified Assets to Total Capital is 3.5% at June 30, 2020 § Forbearance down 13% from intra-period peak – Of the $146MM of loans expected to return to paying status, 63% have done so through July 17, 2020 – Active forbearances have decreased to $1.3B from peak of $1.5B – Pace of forbearance requests has declined § New York Metro area is beginning to open up – Over 90% of the loan portfolio is situated in the area 29