August 8, 2011

Mr. William H. Thompson

Accounting Branch Chief

Division of Corporate Finance

U.S. Securities and Exchange Commission

100 F Street, NE

Washington, D.C. 20549

RE:

PPL Corporation, PPL Electric Utilities Corporation,

PPL Energy Supply, LLC

Form 10-K for Fiscal Year Ended December 31, 2010

Filed February 28, 2011

Form 10-Q for Fiscal Quarter Ended March 31, 2011

Filed May 6, 2011

File Nos. 1-11459, 1-00905 and 1-32944

PPL Corporation

Definitive Proxy Statement on Schedule 14A

Filed April 6, 2011

File No. 1-11459

Dear Mr. Thompson:

In response to your letter dated July 19, 2011, regarding the above-referenced filings, PPL Corporation (PPL), PPL Electric Utilities Corporation (PPL Electric) and PPL Energy Supply, LLC (PPL Energy Supply) are providing the following information in response to your comments. References to the "Company," "we," "us" and "our" in this letter are references to PPL, PPL Electric and PPL Energy Supply specifically or, if the context requires, to PPL and its subsidiaries, collectively. Each of your comments has been reprinted in bold type and is followed by the response of the Registrants.

We propose to address the Staff’s comments in all future filings with the Commission, without amending the Registrants’ Form 10-K for the year ended December 31, 2010, which we also refer to as the "2010 Form 10-K" throughout this letter, or Form 10-Q for the quarter ended March 31, 2011. We have, where applicable, addressed the comments in our recently filed quarterly reports on Form 10-Q/A for the quarter ended June 30, 2011, filed on August 8, 2011, which we also refer to as the “Second Quarter 10-Q” throughout this letter. Examples of revised disclosures are also included within this letter. Capitalized terms used and not otherwise defined in this letter are used as defined in the Second Quarter 10-Q.

Form 10-K for Fiscal Year Ended December 31, 2010

General

|

1.

|

Please include page numbers in all future filings filed with the Commission and uploaded to EDGAR.

|

We included page numbers in the Second Quarter 10-Q and will include page numbers in all future filings filed with the Commission and uploaded to EDGAR.

Item 1. Business, page 1

2. Please briefly describe the business of each of your material subsidiaries. In this regard, we note your disclosure that PPL Energy Supply distributed its interest in PPL Global to PPL Energy Funding “to better align PPL’s organizational structure with the manner in which it manages its businesses and reports segment information.” Please describe the business done by PPL Energy Funding, with a view towards describing to investors how transferring your interest in PPL Global to PPL Energy Funding better aligns your organizational structure with your reporting segments. See Item 101(a) of Regulation S-K and provide us with your proposed disclosure.

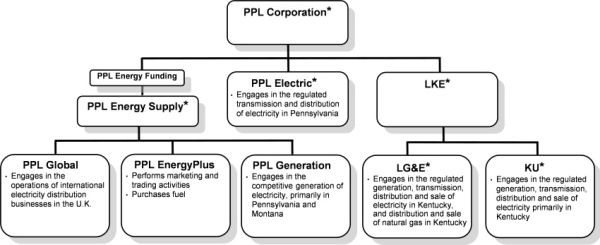

As depicted in the organization chart included in Item 1 of our 2010 Form 10-K, similar to the one shown below, PPL’s material (principal) subsidiaries at December 31, 2010 were:

|

·

|

PPL Energy Supply and its principal subsidiaries (PPL Global, PPL EnergyPlus and PPL Generation),

|

|

·

|

PPL Electric, and

|

|

·

|

LKE and its principal subsidiaries (LG&E and KU).

|

PPL Energy Funding, which has been added to the organization charts below for illustrative purposes, is the parent holding company of PPL Energy Supply and has no material operations other than those conducted by its direct subsidiary PPL Energy Supply and PPL Energy Supply’s subsidiaries. As such, we do not consider PPL Energy Funding to be a principal subsidiary for purposes of describing our business.

2

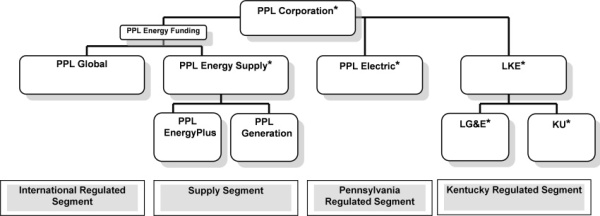

As of December 31, 2010, prior to the distribution of PPL Global, PPL's principal subsidiaries are shown below (* denotes an SEC registrant – LKE, LG&E and KU became SEC registrants effective June 1, 2011). PPL Energy Funding is shown only for illustrative purposes.

As indicated in our disclosures in the 2010 Form 10-K, in January 2011, PPL Energy Supply distributed its 100% membership interest in PPL Global to its parent, PPL Energy Funding, to better align PPL's organizational structure with the manner in which it manages its businesses and reports segment information in its consolidated financial statements. The distribution separated the U.S.-based competitive energy marketing and supply business from the U.K.-based regulated electricity distribution business. The following chart depicts the organizational structure subsequent to this distribution and illustrates how PPL’s principal subsidiaries align with its reportable segments. After distributing PPL Global to its parent, PPL Energy Supply and its subsidiaries’ operations are entirely within the Supply segment.

3

Subsequent to the distribution of PPL Global, PPL's principal subsidiaries are shown below (* denotes an SEC registrant – LKE, LG&E and KU became SEC registrants effective June 1, 2011). PPL Energy Funding is shown only for illustrative purposes.

Subsequent to the distribution, each of our principal subsidiaries and each of our SEC registrants, with the exception of PPL, operates entirely within a single segment. We believe this organizational structure is easier for our investors to understand and better aligns with how we manage our business by segment.

We have added to the “Overview” section of PPL’s Management’s Discussion and Analysis in the Second Quarter 10-Q, disclosures consistent with those described above, as well as an updated organization chart.

PPL Acquisition, page 3

3. We note your disclosure that, as part of the settlement approved by the KPSC, LG&E and KU made a commitment that no base rate increases would take effect before January 1, 2013, but that LG&E and KU may seek approval for “the deferral of ‘extraordinary and uncontrollable costs.’” Please provide additional detail about what may constitute “extraordinary and uncontrollable costs” and describe the process by which you would seek such approval, including the persons or entities that have the authority to grant or reject such a request. In this regard, we note your disclosure in your Form 8-K filed on May 25, 2011 that LG&E and KU expect to seek cost recovery for $2.5 billion in environmental upgrades, and that the impact of these upgrades on customers is estimated at an increase of 2.3% in 2012. Please provide us with your proposed disclosure.

The written settlement agreement in the Kentucky Public Service Commission (KPSC) proceeding included three specific exceptions to the base-rate “stay-out” commitment described above. One exception is for “the deferral of extraordinary and uncontrollable costs,” and the agreement lists ice or wind storm costs as an example thereof. A second exception allows for the operation of any “cost-recovery surcharge mechanisms,” and the agreement lists environmental cost recovery (ECR), demand-side management (DSM) and fuel cost recovery

4

(FAC) as examples thereof. Finally, the agreement contains a third exception preserving rights to an existing Kentucky statute allowing emergency rate relief under certain circumstances to avoid material impairment or damage to utilities’ credit or operations. Approval requests relating to these various exceptions would all be made to the KPSC under standard administrative and procedural structures, including rights of public intervention and hearing, applicable to such matters under existing KPSC practice.

In Note 6 to the Financial Statements in the Second Quarter 10-Q, we revised our disclosure to include the text below. This disclosure is similar to language previously used in Item 1 of the 2010 Form 10-K. During the remainder of the base-rate “stay out” period, we will continue to include disclosure similar to that below in Form 10-K’s or Form 10-Q’s, where applicable, filed with the Commission.

PPL's Acquisition of LKE

In September 2010, the KPSC approved a settlement agreement among PPL and all of the intervening parties to PPL's joint application to the KPSC for approval of its acquisition of ownership and control of LKE, LG&E and KU. In the settlement agreement, the parties agreed that LG&E and KU would commit that no base rate increases would take effect before January 1, 2013. Under the terms of the settlement, LG&E and KU retain the right to seek KPSC approval for the deferral of "extraordinary and uncontrollable costs," such as significant storm restoration costs, if incurred. Additionally, interim rate adjustments will continue to be permissible during that period for existing recovery mechanisms such as the ECR and DSM.

Item 1A. Risk Factors, page 17

4. Please delete the language in the second and third sentences in which you state that other unknown or immaterial risks may also impair your business operations. All material risks should be described in your disclosure. If risks are not deemed material, you should not reference them.

We omitted the language in the referenced sentences in the Second Quarter 10-Q and will omit such language in all future filings.

Risks Specific to Pennsylvania Regulated Segment, page 21

We could be subject to higher costs and/or penalties . . ., page 22

5. Please remove your statement that you expect to meet the requirements set forth in this risk factor, as it mitigates the point of the risk factor. Please provide us with your proposed disclosure.

To the extent this risk factor continues to be part of our disclosure, in future filings we will omit this mitigating statement. The proposed disclosure of the Pennsylvania Conservation and Energy Efficiency Programs risk, which could be included in future filings, is set forth below:

We could be subject to higher costs and/or penalties related to Pennsylvania Conservation and Energy Efficiency Programs.

5

Act 129 became effective in October 2008. This law created requirements for energy efficiency and conservation programs and for the use of smart metering technology, imposed new PLR electricity supply procurement rules, provided remedies for market misconduct, and made changes to the existing Alternative Energy Portfolio Standard. The law also requires electric utilities to meet specified goals for reduction in customer electricity usage and peak demand by specified dates (2011 and 2013). Utilities not meeting these requirements of Act 129 are subject to significant penalties that cannot be recovered in rates. Numerous factors outside of our control, including the levels of customers’ electricity usage, could prevent compliance with these requirements and result in penalties to us.

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations, page 33

6. We note your statements throughout this filing that you expect to grow your regulated businesses and that you expect that 50% of your net income in 2011 will be provided by your regulated businesses. We also note your recent acquisitions of LG&E, KU, Central Networks East and Central Networks Limited. Please provide an analysis regarding these acquisitions and the growth of your regulated businesses, with a view towards describing to investors how your reported financial information may not necessarily be indicative of future results. See Instruction 3 to Item 303(a) of Regulation S-K.

The acquisitions of E.ON U.S. LLC (subsequently renamed LG&E and KU Energy LLC, “LKE”) on November 1, 2010 and Central Networks East and Central Networks Limited (subsequently renamed WPD Midlands) on April 1, 2011, have substantially impacted PPL’s business and significantly increased the relative portion of PPL’s assets and expected earnings from regulated operations.

The impact of the LKE acquisition on anticipated 2011 earnings was described in Management’s Discussion and Analysis in PPL’s 2010 Form 10-K. We also provided pro forma information for 2010 and 2009 in Note 10 to the Financial Statements to show what the impact on revenues and net income would have been had LKE’s results been fully reflected in those periods. Additionally, the required pro forma financial statements were filed on Form 8-K/A on January 14, 2011.

The acquisition of WPD Midlands further increased the regulated portion of PPL’s business. In the Second Quarter 10-Q, we provided pro forma information for the three and six months ended June 30, 2011 and 2010 in Note 8 to the Financial Statements to show what the impact on revenues and net income would have been had the results of WPD Midlands and LKE been fully reflected in those periods. Also, the required pro forma financial statements were filed on Form 8-K on April 11, 2011.

6

We also enhanced our disclosure in Management’s Discussion and Analysis in the Second Quarter 10-Q, to better present the impact of both acquisitions on PPL’s results of operations, and to describe to investors that the results reported in previous periods are not comparable with, or indicative of, post-acquisition results. Please refer to Attachment A for the disclosure we included in the “Overview” section of PPL’s Management’s Discussion and Analysis in the Second Quarter 10-Q.

Results of Operations, page 35

7. Please expand your discussion under results of operations for all periods to quantify the material factors, or any multiple factors, you cite as impacting a single financial statement line item. For example, you disclose that U.K. utility revenues increased in 2010 primarily due to price increases, which were partially offset by a lower regulatory recovery, without quantifying the impact attributable to each component. See Item 303(a)(3) of Regulation S-K. Additionally, we note several instances where you identify a change in a financial statement line item and refer readers to other portions of your Form 10-K, often to the notes to the financial statements, for a discussion of the line item and any year-to-year changes to such items. To the extent that information elsewhere in your filing is necessary to provide an understanding as to your results of operations, financial condition or liquidity, please consider the benefit to investors of including this information and management’s analysis of this information in this section of your filing, rather than presenting such information in a fragmented manner throughout the filing. See Commission Statement about Management’s Discussion & Analysis of Financial Condition and Results of Operations, Part II, SEC Release No. 33-8056 and provide us with your proposed disclosure.

We revised our disclosures in Management’s Discussion and Analysis in the Second Quarter 10-Q to provide additional quantification when explaining changes in financial statement line items to provide investors with the relevant impacts of factors affecting components of income from continuing operations.

For example, please refer to Attachment B, which shows a disclosure we provided in the “Overview” section of PPL’s Management’s Discussion and Analysis in the Second Quarter 10-Q, which was revised from prior disclosures based on the Staff’s comments.

As this is just one example, please refer to our Second Quarter 10-Q to see the full breadth of our changes.

We also reduced the extent of the use of cross-references in Management’s Discussion and Analysis to enhance the investors’ understanding by providing more information in a single location, rather than directing the investors to other sections within the document.

We will continue to provide additional quantification and rely less on the use of cross-references in our filings for future periods.

7

Item 8. Financial Statements and Supplementary Data, page 118

Notes to Consolidated Financial Statements, page 135

Note 1: Summary of Significant Accounting Policies, page 135

Goodwill and Other Intangible Assets, page 144

8. We understand that you are a net purchaser of RECs or do not create any RECs through generation. Please confirm or clarify our understanding. In addition, please tell us whether you maintain two separate cost pools for RECs and emission allowances or tell us otherwise how you are able to segregate the cost basis of credits that may have no basis from those that have a cost basis. In this regard, tell us whether you are a net purchaser or seller of emission allowances. If you sell RECs and/or emission allowances, please tell us your revenue recognition policy upon receipt or transfer of such credits or allowances. Please finally explain to us the basis in GAAP for classifying RECs and emission allowances as intangible assets as opposed to some other asset. If based on a FERC chart of accounts, please tell us the specific account which classification is made. We may have further comment.

RECs and emission allowances are intangible assets with different characteristics and are accounted for separately. A REC represents the rights to the environmental, social, and other non-power qualities of renewable electricity generation. A REC, and its associated attributes and benefits, often referred to as “green” attributes, can be sold separately from the underlying physical electricity associated with a renewable energy generation source. An emission allowance authorizes the owner to emit one ton of a specified pollutant during a given vintage year. Emission allowances of the same type and vintage year designation are homogeneous and may be remitted by any party to cover its emissions from any generation facility.

RECs

We enter into agreements to buy and/or sell RECs and also create RECs through our renewable energy generation facilities. As such, in any given quarter, we may be a net purchaser or seller, depending on our contractual obligations to purchase or deliver RECs and our renewable energy generation facilities production of RECs during the period. Homogeneous pools of RECs are maintained by state, vintage year, and class. The carrying value of RECs created from our renewable energy generation facilities is initially recorded at zero value and is not segregated from the carrying value of those RECs purchased and initially recorded based on their purchase price. When RECs are consumed to satisfy our obligation to deliver RECs to meet a state’s Renewable Portfolio Standard Obligations or when RECs are sold to third parties, they are removed from the applicable intangible asset pool at their weighted-average carrying value. Since the economic benefits of RECs are not diminished until they are consumed, RECs are not amortized; rather, they are expensed when consumed or a gain or loss is recognized when sold.

8

Emission allowances

We are allocated emission allowances by states based on our generation facilities’ historical emissions experience, and have purchased emission allowances generally when we believed we would need more allowances for our planned generation than those allocated to us. We are a net purchaser of nitrogen oxide emission allowances. Historically, we had been a net purchaser of sulfur dioxide (SO2) emission allowances, but since our installation of scrubbers at certain of our coal-fired power plants, we currently have more SO2 emission allowances than will be required to comply with current environmental regulations. Homogeneous pools of emission allowances are maintained by type of allowance, vintage year and legal entity and are further segregated as “held for consumption” versus “held for sale.” The only allowances we currently have in the “held for sale” asset pool are SO2 emission allowances due to our current excess quantity of SO2 emission allowances. The carrying value of allocated emission allowances is initially recorded at zero value and is not segregated from the carrying value of those allowances initially recorded based on their purchase price. When consumed or sold, emission allowances are removed from the applicable intangible asset pool at their weighted-average carrying value. Since the economic benefits of emission allowances are not diminished until they are consumed, emission allowances are not amortized; rather, they are expensed when consumed or a gain or loss is recognized when sold.

Revenue recognition

Revenue is not recognized upon receipt of RECs or emission allowances. Gains and losses on the separate sale/transfer of RECs and emission allowances are recognized when realized/earned and collectability is reasonably assured, which generally is when title has been transferred to the buyer.

Classification as intangible assets

The FASB and the IASB currently have a joint project on their agenda to provide comprehensive guidance on the accounting issues that arise related to emissions trading schemes. No definitive guidance has been issued by the FASB or the IASB on the proper accounting for RECs or emission allowances, which in practice has resulted in application of either an intangible asset accounting model or an inventory accounting model. Therefore, we believe that selection of either the intangible asset accounting model or the inventory accounting model is an accounting policy election that should be consistently applied. We classify RECs and emission allowances as intangible assets because we believe they lack physical substance and therefore meet the definition of intangible assets, which is defined in the ASC Master Glossary as, “Assets (not including financial assets) that lack physical substance.” Since our RECs and emission allowances are not held exclusively by our businesses that are public utilities, we did not look to the FERC’s Uniform System of Accounts prescribed for Public Utilities to determine our accounting policy for these assets for U.S. GAAP purposes. As this is a significant accounting policy election for us, we disclosed our policy in our 2010 Form 10-K within the “Goodwill and Other Intangible Assets” section of Summary of Significant Accounting Policies. The disclosure indicates:

9

PPL and its subsidiaries account for emission allowances as intangible assets. Since the economic benefits of emission allowances are not diminished until they are consumed, emission allowances are not amortized; rather, they are expensed when consumed. Such expense is included in "Fuel" on the Statements of Income. Gains and losses on the sale of emission allowances are included in "Other operation and maintenance" on the Statements of Income.

PPL and its subsidiaries also account for RECs as intangible assets, and the associated costs are not expensed until the credits are consumed. Such expense is included in "Energy purchases" on the Statements of Income. Gains and losses on the sale of RECs are included in "Other operation and maintenance" on the Statements of Income.

Note 15: Contingencies and Commitments, page 206

Legal Matters, page 208

9. We note the disclosure in several locations of your document that you “cannot predict the outcome” related to certain legal matters. If you conclude that you cannot estimate a range of reasonably possible losses on any of the matters disclosed or in the aggregate, please disclose this fact in your next Form 10-Q in accordance with ASC 450. In addition, for those matters where you are unable to estimate the possible loss or range of loss, please supplementally provide an explanation of the procedures you undertake on a quarterly basis to attempt to develop a range of reasonably possible loss for disclosure. Please refer to ASC 450-20-50.

PPL and its subsidiaries are involved in legal proceedings, claims and litigation in the ordinary course of business. The ultimate outcome of these matters is ordinarily difficult to anticipate, and any such evaluation is only made more uncertain when proceedings are in their early stages, where claimants seek large or unspecified damages, and in matters involving numerous parties or complex issues. In such situations, we generally cannot reasonably estimate the potential loss or range of losses without being unduly speculative until some definitive event has occurred in the course of the matter.

We have revised our disclosures of “Legal Matters” in Note 10 to the Financial Statements in the Second Quarter 10-Q to address disclosures where we had previously indicated that we “cannot predict the outcome” of particular legal contingencies. See Attachment C for our disclosure of “Legal Matters” in the Second Quarter 10-Q. The disclosures are underscored to show revisions from our 2010 Form 10-K in response to the comment by the Staff and to reflect recent developments in these matters. Updates to these disclosures include:

|

·

|

Trimble County Unit 2 Construction:

|

We clarified that the impact would be to the capital cost of the project, as opposed to a loss that would impact the income statement. Accordingly, this contingency is not a loss contingency under ASC 450-20. As such, there is no probable loss or range of losses to record or disclose, but we note that we are unable to predict the impact on the cost of this capital project.

10

|

·

|

Trimble County Unit 2 Transmission:

|

In March 2011, the Kentucky Supreme Court issued an order which closed this matter.

|

·

|

Spent Nuclear Fuel Litigation:

|

This matter was not disclosed in the notes to the financial statements in the 2010 Form 10-K, given the status at the time of this gain contingency. (However, PPL’s suit against the U.S. Department of Energy was disclosed in the 2010 Form 10-K, in Item 1, “Business-Background.”) In May 2011, PPL and the DOE executed a settlement agreement, the terms and impact of which are provided in the Second Quarter 10-Q disclosure, which updated the disclosure of this matter provided in the notes to the financial statements in the Form 10-Q for the period ended March 31, 2011.

|

·

|

Montana Hydroelectric Litigation:

|

In the penultimate paragraph of this disclosure, we disclose the estimated loss that was recorded in the first quarter of 2010, following the Montana Supreme Court decision that upheld the 2008 decision by the Montana District Court, at which point the loss was deemed “probable” by PPL’s management. The last paragraph provides a procedural update regarding PPL’s petition to the U.S. Supreme Court. We note that while we cannot predict the outcome of this matter, we do not expect to incur any material losses beyond the estimated losses recorded.

|

·

|

PJM/MISO Billing Dispute:

|

This disclosure has been updated to note that in June 2011 the FERC issued an order approving the settlement which closed this matter.

We will also make revisions in response to the Staff’s comment in our disclosures of “Legal Matters” in all future filings, and whenever we conclude that we cannot estimate a range of reasonably possible losses on any of the legal matters disclosed we will provide disclosure of this fact in accordance with ASC 450-20.

In response to the second part of the Staff’s comment, PPL has procedures for complying with the requirements of ASC 450-20 as it relates to establishing reasonably possible losses or ranges of losses for all loss contingencies. With respect to legal contingencies, prior to the end of each reporting period the Controller’s Department convenes meetings with the Legal Department at which all significant legal contingencies are reviewed. In these meetings, the status of legal contingencies is presented by the appropriate attorney from the Legal Department to address information necessary under ASC 450-20. Outside counsel may be consulted to the extent they are involved in a legal matter. As part of this process, management evaluates whether events have transpired during the quarter that are sufficient to establish or revise a reasonable estimate of the loss, or range of loss, with respect to the legal contingencies. After convening similar meetings with appropriate parties to assess other contingencies (e.g., environmental matters), the Controller’s Department conducts an overall review of loss contingencies in advance of its quarterly financial close. The outcomes of these procedures regarding the necessary accruals and required disclosures are then reflected in our quarterly periodic filings.

11

We believe these procedures provide adequate assurance that our accounting treatment and disclosures of loss contingencies are in compliance with ASC 450-20.

Item 9A. Controls and Procedures, page 260

10. We note that the acquisition of LG&E and KU Energy LLC (LKE) has been excluded from your assessment of internal controls over financial reporting as of the year ended December 31, 2010. Please tell us what consideration you gave to disclosing any changes in internal control over financial reporting related to the acquisition that occurred during the quarter ended December 31, 2010. In this regard, notwithstanding management's exclusion of LKE’s internal controls from its annual assessment, you must disclose any material change to your internal control over financial reporting due to the acquisition. Refer to Questions 3 and 7 of Frequently Asked Questions (revised September 24, 2007) on Management’s Report on Internal Control Financial Reporting and Certification of Disclosure in Exchange Act Periodic Reports found here: http://www.sec.gov/info/accountants/controlfaq.htm.

PPL considered the relative significance of the LKE acquisition to PPL’s consolidated financial statements. PPL also considered that it was acquiring a sizable company that would continue to operate most of its own existing systems, processes and internal controls over financial reporting and that PPL would enhance and extend its existing internal controls and procedures to mitigate financial reporting risks related to the acquired businesses. Specifically, we reviewed certain controls at the acquired companies that mitigated risk of material misstatement of financial statement balances and compared those to similar controls at PPL. At the time of our 2010 Form10-K filing, we were still evaluating other operational and internal control changes. Based on these factors, the acquisition of LKE was deemed to be a material change to PPL’s internal control over financial reporting.

Accordingly, in Item 9A, paragraph (a), of the 2010 Form 10-K, PPL disclosed the relative significance of the acquisition on PPL’s consolidated net income (5.0%, reflecting two months of LKE’s earnings) and on its consolidated total assets (32.6%) and consolidated net assets (47.3%) at December 31, 2010. The acquisition of LKE was disclosed as a material change in PPL’s internal control over financial reporting in paragraph (b). The disclosure in paragraph (b) referenced paragraph (a), which also noted that PPL was evaluating changes to processes, information technology systems and other components of internal control over financial reporting as part of its ongoing integration activities.

In the Second Quarter 10-Q, PPL disclosed in Item 4 that its acquisition of Western Power Distribution East Midlands plc and Western Power Distribution West Midlands plc on April 1, 2011 also had a material impact on PPL’s internal control over financial reporting. Please refer to Attachment D for the Item 4 disclosure provided in the Second Quarter 10-Q, which we believe addresses the Staff’s comments.

12

Definitive Proxy Statement on Schedule 14A

Nominees for Directors, page 7

11. Please briefly describe the specific experience, qualifications, attributes or skills that led to your conclusion that each nominee for director should serve as such, in light of your business and structure. See Item 401(e) of Regulation S-K and provide us with your proposed disclosure.

PPL respectfully directs the Staff’s attention to the introductory text on page 7 of PPL’s definitive proxy statement on Schedule 14A filed on April 6, 2011 (Proxy Statement), which refers readers to the discussion under the caption “Director Nomination Process” beginning on page 16 of the Proxy Statement for information concerning the specific experience, qualifications, attributes and/or skills that led the Compensation, Governance and Nominating Committee (CGNC) and the Board of Directors to determine that each nominee should serve as a director, in light of PPL’s business and structure. These specific criteria are discussed on page 17 of the Proxy Statement, with the relevant text reproduced below:

When considering whether the Board’s directors and nominees have the experience, qualifications, attributes and skills, taken as a whole, to enable the Board to satisfy its oversight responsibilities effectively in light of the Company’s business and structure, the Board focused primarily on the information discussed in each of the Board members’ or nominees’ biographical information set forth on pages 7 to 10. In particular, in connection with the nominations of each director for election as directors at the 2011 Annual Meeting of Shareowners, the Board considered their contributions to the company’s success during their previous years of Board service. With regards to Dr. Bernthal, the Board considered his service with the U.S. Nuclear Regulatory Commission and his governmental and leadership experience. For Mr. Conway, the Board considered his general business background and his leadership expertise as a CEO of a publicly traded company. With regards to Mr. Deaver, the Board considered his engineering and general business background, as well as his senior executive experience. For Mr. Elliott, the Board considered his broad experience in the financial services industry, and his accounting and risk management expertise. With regards to Ms. Goeser, the Board considered her leadership and business experience in a variety of industry positions. For Mr. Graham, the Board considered his international construction and development experience, as well as his leadership skills from serving as a CEO of a publicly traded company. With regards to Dr. Heydt, the Board considered his business experience and leadership expertise from serving as CEO of a large healthcare system. For Mr. Miller, the Board considered his operating and nuclear experience, as well as his leadership skills. With regards to Mr. Rogerson, the Board considered his general business background and his leadership expertise as a CEO of several publicly traded companies. With regards to Ms. von Althann, the Board considered her financial and risk management experience, as well as

13

senior management experience. With regards to Mr. Williamson, the Board considered his general business, finance and legal background.

PPL will include similar disclosure in its future proxy statement filings with the Commission.

Transactions with Related Persons, page 26

12. Please describe the standards applied by the independent disinterested members of your board of directors in determining whether to ratify related-party transactions. See Item 404(b)(1)(ii) of Regulation S-K and provide us with your proposed disclosure.

In its future proxy statement filings with the Commission, PPL will include the following language describing the standards applied by the independent disinterested members of its Board of Directors in determining whether to ratify related-party transactions, consistent with the Company’s related-person transaction policy.

In connection with the review and approval or ratification of a related-person transaction, the Compensation, Governance and Nominating Committee, or CGNC, will consider the relevant facts and circumstances, including:

|

·

|

the approximate dollar value of the amount involved in the transaction, and all the material facts as to the related person’s direct or indirect interest in, or relationship to, the related-person transaction;

|

|

·

|

whether the related-person transaction complies with the terms of the Company’s agreements governing its material outstanding indebtedness that limit or restrict PPL’s ability to enter into a related-person transaction;

|

|

·

|

whether the related-person transaction will be required to be disclosed in PPL’s applicable filings under the Securities Act of 1933, as amended, or the Securities Exchange Act of 1934, as amended; and

|

|

·

|

whether the related-person transaction constitutes a “personal loan” for purposes of Section 402 of the Sarbanes-Oxley Act of 2002.

|

In addition, in connection with any approval or ratification of a related-person transaction involving a non-employee director or nominee for director, the CGNC will consider whether such transaction would compromise such director’s status as: (1) an independent director under the New York Stock Exchange Listing Standards or PPL’s categorical independence standards, (2) an “outside director” under Section 162(m) of the Internal Revenue Code or a “non-employee director” under Rule 16b-3 under the Securities Exchange Act of 1934, as amended, if such non-employee director serves on the CGNC, or (3) an independent director under Rule 10A-3 under the Securities Exchange Act of 1934, as amended, if such non-employee director serves on the Audit Committee of the Board.

14

Executive Compensation, page 28

Base Salary, page 33

13. We note your disclosure that prior to the closing of the LKE acquisition your compensation committee ratified Mr. Stafferi’s base-salary as previously set by

E. ON AG. If true, please confirm that Mr. Stafferi’s base salary going forward will be based on his 2010 compensation as set by E. ON AG and disclose how you will make adjustments to his base salary going forward, including how you will determine the PPL Competitive Range applicable to his position.

As disclosed on page 33 of the Proxy Statement, PPL’s CGNC meets in January of each year in order to review base salary levels for all executive officers, which includes Mr. Staffieri for purposes of 2011 and future years. The CGNC will evaluate Mr. Staffieri’s future base salary in the same manner as it evaluates the base salary levels for other named executive officers, consistent with the terms of Mr. Staffieri’s employment agreement and the purchase and sale agreement. PPL respectfully directs the Staff’s attention to page 30 of the Proxy Statement, which discusses the acquisition of E.ON U.S. LLC. While the CGNC will consider the competitive compensation range for Mr. Staffieri based on his level and position, the Company agreed in its purchase and sale agreement with E.ON AG to continue, for 24 months, specified components of the executive compensation program in place for the E.ON U.S. LLC, now known as LG&E and KU Energy LLC, or LKE, executives on terms materially no less favorable in the aggregate than those executives’ then-current terms, including each executive’s annual base salary. As with the other named executive officers, any decisions made by the CGNC for 2011 will be disclosed in the proxy statement to be filed in 2012. The Company cannot predict what decisions the CGNC will make for its named executive officers from year-to-year.

Proxy Card

14. With respect to proposal four, please revise to clarify that shareholders are voting for or against, or abstaining from voting on, the approval of executive compensation and not an advisory vote on executive compensation.

In its future proxy statement filings with the Commission, PPL will clarify on its proxy card that shareholders are, on an advisory basis, voting for or against, or abstaining from voting on, the approval of executive compensation.

Form 10-Q for the Fiscal Period Ended March 31, 2011

15. Please apply the above comments to this filing and to subsequent filings as applicable.

As indicated above, we propose to address the Staff’s comments in all future filings with the Commission, without amending the Registrants’ Form 10-Q for the quarter ended March 31, 2011. We have, as indicated, addressed the above comments in our recently filed Second Quarter 10-Q.

15

PPL, PPL Electric and PPL Energy Supply each acknowledge that: (1) it is responsible for the adequacy and accuracy of the disclosure in its filings, (2) staff comments or changes to disclosure in response to staff comments do not foreclose the Commission from taking any action with respect to the filing, and (3) it may not assert staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States.

If you have any additional questions or need further clarification, please call me at (610)-774-3621.

Sincerely,

/s/ Vincent Sorgi

Vincent Sorgi

Vice President and Controller

PPL Corporation

PPL Electric Utilities Corporation

PPL Energy Supply, LLC

cc: Mr. J.H. Miller

Mr. W.H. Spence

Mr. P.A. Farr

Mr. R.J. Grey

16

Attachment A

Supplement to Question 6

We included the following disclosure in the “Overview” section of PPL’s Management’s Discussion and Analysis in the Second Quarter 10-Q (dollars are in millions):

Business Strategy

PPL's overall strategy is to achieve stable, long-term growth in its regulated electricity delivery businesses through efficient operations and strong customer and regulatory relations, and disciplined growth in energy supply margins while mitigating volatility in both cash flows and earnings. In pursuing this strategy, PPL acquired LKE in November 2010 and WPD Midlands in April 2011. These acquisitions have reduced PPL's overall business risk profile and reapportioned the mix of PPL's regulated and competitive businesses by increasing the regulated portion of its business and enhancing rate-regulated growth opportunities as the regulated businesses make investments to improve infrastructure and customer reliability.

The increase in regulated assets is expected to provide earnings stability through regulated returns and the ability to recover costs of capital investments, in contrast to the competitive energy supply business where earnings and cash flows are subject to commodity market volatility. Following the LKE and WPD Midlands acquisitions, approximately 70% of PPL's assets are in its regulated businesses. The pro forma impacts of the acquisitions of LKE and WPD Midlands on PPL's income from continuing operations (after income taxes) for the six months ended June 30 are as follows:

|

|

|

2011

|

|

2010

|

||||||||||||

|

|

|

Pro forma

|

|

|

Actual

|

|

|

Pro forma

|

|

|

Actual

|

|

||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Regulated

|

|

$

|

510

|

62%

|

|

$

|

393

|

56%

|

|

$

|

387

|

70%

|

|

$

|

184

|

52%

|

|

Competitive

|

|

|

310

|

38%

|

|

|

310

|

44%

|

|

|

167

|

30%

|

|

|

167

|

48%

|

|

|

|

$

|

820

|

|

|

$

|

703

|

|

|

$

|

554

|

|

|

$

|

351

|

|

|

Note:

|

Pro forma and actual amounts exclude non-recurring adjustments identified in Note 8 to the Financial Statements.

|

Accordingly, results for periods prior to the acquisitions of LKE and WPD Midlands are not comparable with, or indicative of, results for periods subsequent to the acquisitions.

17

Attachment B

Supplement to Question 7

We included the following disclosure in "Results of Operations" – "Utility Revenues" in Management’s Discussion and Analysis in the Second Quarter 10-Q (dollars are in millions):

|

Changes in utility revenues for the periods ended June 30, 2011 compared with 2010 were attributable to:

|

|||||||||

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Three Months

|

|

Six Months

|

||

|

Domestic:

|

|

|

|

|

|

|

|||

|

|

PPL Electric

|

|

|

|

|

|

|

||

|

|

|

Decrease in energy revenue due to customers selecting alternative suppliers (a)

|

|

$

|

(106)

|

|

$

|

(388)

|

|

|

|

|

Price increase related to the distribution rate case effective January 1, 2011

|

|

|

14

|

|

|

38

|

|

|

|

|

Other

|

|

|

8

|

|

|

9

|

|

|

|

|

Total

|

|

|

(84)

|

|

|

(341)

|

|

|

|

LKE (b)

|

|

|

638

|

|

|

1,404

|

||

|

|

|

|

|

|

|

|

|

|

|

|

|

Total Domestic

|

|

|

554

|

|

|

1,063

|

||

|

|

|

|

|

|

|

|

|

|

|

|

U.K.:

|

|

|

|

|

|

|

|||

|

|

PPL WW

|

|

|

|

|

|

|

||

|

|

|

Price increases effective April 1, 2011 and 2010

|

|

|

20

|

|

|

22

|

|

|

|

|

Change in recovery of allowed revenues (c)

|

|

|

3

|

|

|

12

|

|

|

|

|

Foreign currency exchange rates

|

|

|

16

|

|

|

13

|

|

|

|

|

Other

|

|

|

(8)

|

|

|

(3)

|

|

|

|

|

Total PPL WW

|

|

|

31

|

|

|

44

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

WPD Midlands (b)

|

|

|

207

|

|

|

207

|

||

|

|

Total U.K.

|

|

|

238

|

|

|

251

|

||

|

Total

|

|

$

|

792

|

|

$

|

1,314

|

|||

|

(a)

|

In 2011, customers continued to select alternative suppliers to provide their energy needs. This decrease in energy revenue has a minimal impact on earnings as the cost of providing this energy is passed through to the customer with no additional mark-up. These revenues are offset with purchases in Pennsylvania Gross Delivery Margins.

|

|

(b)

|

There are no comparable amounts in the 2010 periods as LKE was acquired in November 2010 and WPD Midlands was acquired in April 2011.

|

|

(c)

|

The six month period was higher due to a $12 million charge recorded in the first quarter of 2010 reflecting the impact on regulatory allowed revenues, primarily resulting from changes in the network electricity line loss assumptions. Such charges were insignificant in the first quarter of 2011.

|

18

Attachment C

Supplement to Question 9

We included the following disclosure of “Legal Matters” in the Second Quarter 10-Q. The disclosures are underscored to show revisions from our 2010 Form 10-K, in response to the comment by the Staff and to reflect developments in these matters. Updates to these disclosures include:

Legal Matters

(PPL, PPL Energy Supply and PPL Electric)

PPL and its subsidiaries are involved in legal proceedings, claims and litigation in the ordinary course of business.

(PPL)

Trimble County Unit 2 Construction

In June 2006, LG&E and KU entered into a construction contract regarding the TC2 project. The contract is generally in the form of a turnkey agreement for the design, engineering, procurement, construction, commissioning, testing and delivery of the project, according to designated specifications, terms and conditions. The contract price and its components are subject to a number of potential adjustments which may serve to increase or decrease the ultimate construction price. During 2009 and 2010, LG&E and KU received several contractual notices from the TC2 construction contractor asserting historical force majeure and excusable event claims for a number of adjustments to the contract price, construction schedule, commercial operations date, liquidated damages or other relevant provisions. In September 2010, LG&E, KU and the construction contractor agreed to a settlement to resolve the force majeure and excusable event claims occurring through July 2010, under the TC2 construction contract, which settlement provided for a limited, negotiated extension of the contractual commercial operations date and/or relief from liquidated damage calculations. With limited exceptions, LG&E and KU took care, custody and control of TC2 in January 2011. LG&E and KU and the contractor have agreed to certain amendments to the construction agreement whereby the contractor will complete certain actions relating to identifying and completing any necessary modifications to allow operation of TC2 on all fuels in accordance with initial specifications prior to certain dates, and amending the provisions relating to liquidated damages. The remaining issues are still under discussion with the contractor. PPL, LKE, LG&E and KU cannot currently predict the outcome of this matter or the potential impact on the capital costs of this project.

Trimble County Unit 2 Transmission

LG&E's and KU's Certificate of Public Convenience and Necessity (CCN) and condemnation rights relating to a transmission line associated with the TC2 construction have been challenged by certain property owners in Hardin County, Kentucky. Certain proceedings relating to CCN challenges and federal historic preservation permit requirements have concluded with outcomes in LG&E's and KU's favor. With respect to the remaining issues in dispute, during 2008 KU obtained various successful rulings at the Hardin County Circuit Court confirming its condemnation rights. In August 2008, several landowners appealed such rulings to the Kentucky Court of Appeals. In May 2010, the Kentucky Court of Appeals issued an Order affirming the Hardin Circuit Court's finding that KU had the right to condemn easements on the properties. In May 2010, the landowners filed a petition for reconsideration with the Kentucky Court of Appeals. In July 2010, the Kentucky Court of Appeals denied that petition. In August 2010, the landowners filed for discretionary review of that denial by the Kentucky Supreme Court. In March 2011, the Kentucky Supreme Court issued an order declining the discretionary review request, thus closing this matter.

19

(PPL and PPL Energy Supply)

Spent Nuclear Fuel Litigation

Federal law requires the U.S. government to provide for the permanent disposal of commercial spent nuclear fuel, but there is no definitive date by which a repository will be operational. As a result, it was necessary to expand Susquehanna's on-site spent fuel storage capacity. To support this expansion, PPL Susquehanna contracted for the design and construction of a spent fuel storage facility employing dry cask fuel storage technology. The facility is modular, so that additional storage capacity can be added as needed. The facility began receiving spent nuclear fuel in 1999. PPL Susquehanna estimates that there is sufficient storage capacity in the spent nuclear fuel pools and the on-site dry cask storage facility at Susquehanna to accommodate spent fuel discharged through approximately 2017 under current operating conditions. If necessary, on-site dry cask storage capability can be expanded, assuming appropriate regulatory approvals are obtained, such that, together, the spent fuel pools and the expanded dry fuel storage facilities will accommodate all of the spent fuel expected to be discharged through the current licensed life of each unit, 2042 for Unit 1 and 2044 for Unit 2.

In 1996, the U.S. Court of Appeals for the District of Columbia Circuit (D.C. Circuit Court) ruled that the Nuclear Waste Policy Act imposed on the DOE an unconditional obligation to begin accepting spent nuclear fuel on or before January 31, 1998. In 1997, the D.C. Circuit Court ruled that the contracts between the utilities and the DOE provide a potentially adequate remedy if the DOE failed to begin accepting spent nuclear fuel by January 31, 1998. The DOE did not, in fact, begin to accept spent nuclear fuel by that date. The DOE continues to contest claims that its breach of contract resulted in recoverable damages. In January 2004, PPL Susquehanna filed suit in the U.S. Court of Federal Claims for unspecified damages suffered as a result of the DOE's breach of its contract to accept and dispose of spent nuclear fuel. In May 2011, the parties entered into a settlement agreement which resolved all claims of PPL Susquehanna through December 2013. Under the settlement agreement, PPL Susquehanna received approximately $50 million for its share of claims to recover costs to store spent nuclear fuel at the Susquehanna station through September 30, 2009, and will be eligible to receive payment of annual claims for allowed costs, as set forth in the settlement agreement, that are incurred thereafter through the December 31, 2013 termination date of the settlement agreement. In exchange, PPL Susquehanna has waived any claims against the United States government for costs paid or injuries sustained related to storing spent nuclear fuel at PPL Susquehanna through December 31, 2013.

Montana Hydroelectric Litigation

In November 2004, PPL Montana, Avista Corporation (Avista) and PacifiCorp commenced an action for declaratory judgment in Montana First Judicial District Court seeking a determination that no lease payments or other compensation for their hydroelectric facilities' use and occupancy of certain riverbeds in Montana can be collected by the State of Montana. This lawsuit followed dismissal on jurisdictional grounds of an earlier federal lawsuit seeking such compensation in the U.S. District Court of Montana. The federal lawsuit alleged that the beds of Montana's navigable rivers became state-owned trust property upon Montana's admission to statehood, and that the use of them should, under a 1931 regulatory scheme enacted after all but one of the hydroelectric facilities in question were constructed, trigger lease payments for use of land beneath. In July 2006, the Montana state court approved a stipulation by the State of Montana that it was not seeking compensation for the period prior to PPL Montana's December 1999 acquisition of the hydroelectric facilities.

Following a number of adverse trial court rulings, in 2007 Pacificorp and Avista each entered into settlement agreements with the State of Montana providing, in pertinent part, that each company would make prospective lease payments for use of the State's navigable riverbeds (subject to certain future adjustments), resolving the State's claims for past and future compensation.

20

Following an October 2007 trial of this matter on damages, in June 2008, the Montana District Court awarded the State retroactive compensation of approximately $35 million for the 2000-2006 period and approximately $6 million for 2007 compensation. Those unpaid amounts continue to accrue interest at 10% per year. The Montana District Court also deferred determination of compensation for 2008 and future years to the Montana State Land Board. In October 2008, PPL Montana appealed the decision to the Montana Supreme Court, requesting a stay of judgment and a stay of the Land Board's authority to assess compensation for 2008 and future periods.

In March 2010, the Montana Supreme Court substantially affirmed the June 2008 Montana District Court decision. As a result, in the first quarter of 2010, PPL Montana recorded a pre-tax charge of $56 million ($34 million after tax or $0.08 per share, basic and diluted, for PPL), representing estimated rental compensation for the first quarter of 2010 and prior years, including interest. Rental compensation was estimated for periods subsequent to 2007, although such estimated amounts may differ from amounts ultimately determined by the Montana State Land Board. The portion of the pre-tax charge that related to prior years totaled $54 million ($32 million after tax). The pre-tax charge recorded on the Statement of Income was $49 million in "Other operation and maintenance" and $7 million in "Interest Expense." PPL Montana continues to accrue interest expense for the prior years and rent expense for the current year. PPL Montana's total loss accrual at June 30, 2011 was $81 million.

In August 2010, PPL Montana filed a petition for a writ of certiorari with the U.S. Supreme Court requesting the Court's review of this matter. In June 2011, the Supreme Court granted PPL Montana's petition. This matter will be briefed on its merits, with oral argument likely to occur in late November or early December 2011 and a decision likely to be rendered by the Court by June 30, 2012. The stay of the judgment granted during the proceedings before the Montana Supreme Court has been extended by agreement with the State of Montana, to cover the anticipated period of the proceeding before the U.S. Supreme Court. PPL and PPL Energy Supply cannot predict the outcome of this matter, but do not expect to incur material losses beyond the estimated losses recorded.

PJM/MISO Billing Dispute (PPL, PPL Energy Supply and PPL Electric)

In 2009, PJM reported that it had discovered a modeling error in the market-to-market power flow calculations between PJM and MISO. The error was a result of incorrect modeling of certain generation resources that have an impact on power flows across the PJM/MISO border. Informal settlement discussions on this issue terminated in March 2010. Also in March 2010, MISO filed two complaints with the FERC concerning the modeling error and related matters with a demand for $130 million of principal plus interest. In April 2010, PJM filed answers to the complaints and filed a related complaint against MISO. In its answers and complaint, PJM denies that any compensation is due to MISO and seeks recovery in excess of $25 million from MISO for alleged violations by MISO regarding market-to-market power flow calculations. PPL participates in markets in both PJM and MISO. In June 2010, the FERC ordered the complaints to be consolidated and set for settlement discussions, followed by hearings if the discussions are unsuccessful. In January 2011, the parties to this dispute filed a settlement with the FERC under which no compensation would be paid to either PJM or MISO and providing for certain improvements in how the calculations are administered going forward. The settlement was contested by several parties and in June 2011 the FERC issued an order approving the contested settlement, which order has become final and is not subject to rehearing and appeal.

21

Attachment D

Supplement to Question 10

We included the following Item 4 disclosure in the Second Quarter 10-Q:

Item 4. Controls and Procedures

PPL Corporation; PPL Energy Supply LLC; PPL Electric Utilities Corporation; LG&E and KU Energy LLC; Louisville Gas and Electric Company; and Kentucky Utilities Company

(a) Evaluation of disclosure controls and procedures.

The registrants' principal executive officers and principal financial officers, based on their evaluation of the registrants' disclosure controls and procedures (as defined in Rules 13a-15(e) and 15d-15(e) of the Securities Exchange Act of 1934) have concluded that, as of June 30, 2011, the registrants' disclosure controls and procedures are effective to ensure that material information relating to the registrants and their consolidated subsidiaries is recorded, processed, summarized and reported within the time periods specified by the SEC's rules and forms, particularly during the period for which this quarterly report has been prepared. The aforementioned principal officers have concluded that the disclosure controls and procedures are also effective to ensure that information required to be disclosed in reports filed under the Exchange Act is accumulated and communicated to management, including the principal executive and principal financial officers, to allow for timely decisions regarding required disclosure.

PPL Corporation

PPL acquired Western Power Distribution East Midlands plc and Western Power Distribution West Midlands plc ("WPD Midlands") on April 1, 2011. These companies are included in PPL's 2011 financial statements as of the date of the acquisition. On a pro forma basis, WPD Midlands would have accounted for approximately 16% of PPL's net income for the six months ended June 30, 2011. WPD Midlands represented 21% and 27% of PPL's consolidated total assets and net assets at June 30, 2011. The internal control over financial reporting of WPD Midlands were excluded from a formal evaluation of effectiveness of PPL Corporation's disclosure controls and procedures. This decision was based upon the significance of these companies to PPL, and the timing of integration efforts underway to transition WPD Midlands' processes, information technology systems and other components of internal control over financial reporting to the internal control structure of PPL. PPL has expanded its consolidation and disclosure controls and procedures to include the acquired companies, and PPL continues to assess the current internal control over financial reporting at WPD Midlands. Risks related to the increased account balances are partially mitigated by PPL's expanded controls and PPL's existing policy of consolidating foreign subsidiaries on a one-month lag, which provided management additional time for review and analysis of WPD Midlands' results and their incorporation into PPL's consolidated financial statements.

(b) Change in internal control over financial reporting.

PPL Corporation

PPL's principal executive officer and principal financial officer have concluded that the WPD Midlands acquisition created a material change to its internal control over financial reporting. WPD Midlands is a significant subsidiary for PPL that will continue to operate under its pre-acquisition internal control over financial reporting for the remainder of 2011. PPL is transitioning the processes, information technology systems and other components of internal control over financial reporting of WPD Midlands to the internal control structure of PPL. PPL has expanded its consolidation and disclosure controls and procedures related to its foreign activities to include the acquired companies, and PPL continues to assess the current internal control over financial reporting at WPD Midlands. Risks related to the increased account balances are partially mitigated by PPL's expanded controls and PPL's existing policy of consolidating foreign subsidiaries on a one-month lag, which provided management additional time for

22

review and analysis of WPD Midlands' results and their incorporation into PPL's consolidated financial statements. The aforementioned principal executive officer and principal financial officer have concluded that there were no other changes in the registrant's internal control over financial reporting during the registrant's second fiscal quarter that have materially affected, or are reasonably likely to materially affect, the registrant's internal control over financial reporting.

PPL Energy Supply LLC; PPL Electric Utilities Corporation; LG&E and KU Energy LLC; Louisville Gas and Electric Company; and Kentucky Utilities Company

The registrants' principal executive officers and principal financial officers have concluded that there were no changes in the registrants' internal control over financial reporting during the registrants' second fiscal quarter that have materially affected, or are reasonably likely to materially affect the registrants' internal control over financial reporting.

23