EX-99.1

Exhibit 99.1

Eldorado Gold Corporation

Annual Information Form

in respect of the

Year-Ended

December 31, 2017

DATED MARCH 29, 2018

About this Annual Information Form

Throughout this annual information form (AIF), references to “we”, “us”, “our”, “Eldorado” and the

“Company” mean Eldorado Gold Corporation and its subsidiaries. References to “Eldorado Gold” mean Eldorado Gold Corporation only. References to “this year” means 2017.

For all other defined technical and other terms, please refer to our Glossary section on page 156.

All dollar amounts are in United States dollars unless stated otherwise.

Except as otherwise noted, the information in this AIF is as of December 31, 2017. We prepare the financial statements referred to in the AIF in

accordance with International Financial Reporting Standards (IFRS) as issued by the International Accounting Standards Board, and file the AIF with appropriate regulatory authorities in Canada and the United States. Information on our website is not

part of this AIF, or incorporated by reference. Filings on SEDAR are also not part of this AIF or incorporated by reference, except as specifically stated.

You can find more information about Eldorado Gold, including information about executive and director compensation and indebtedness, principal holders of

our securities, and securities authorized for issue under equity compensation plans (such as our incentive stock option plan and performance share unit plan, among others), in our most recent management proxy circular and on SEDAR (www.sedar.com)

under the name Eldorado Gold Corporation. For additional financial information, you should also read our audited consolidated financial statements (2017 FS) and management’s discussion and analysis (MD&A) for the year ended

December 31, 2017. You can find these documents and additional information about the Company filed under our name on SEDAR (www.sedar.com), or you can ask us for a copy by writing to:

Eldorado Gold Corporation

Corporate Secretary

1188 – 550 Burrard Street

Vancouver, BC V6C 2B5

3

Table of Contents

|

|

|

|

|

| About this Annual Information Form |

|

|

3 |

|

|

|

| Forward-looking information and risks |

|

|

5 |

|

|

|

| About Eldorado Gold |

|

|

8 |

|

|

|

| Other offices: |

|

|

9 |

|

|

|

| Key milestones in our recent history |

|

|

11 |

|

|

|

| About our business |

|

|

16 |

|

|

|

| An overview of our business |

|

|

17 |

|

|

|

| How we measure our costs |

|

|

21 |

|

|

|

| Corporate Social Responsibility |

|

|

23 |

|

|

|

| Our Workforce |

|

|

23 |

|

|

|

| Operating Responsibly |

|

|

23 |

|

|

|

| Ethical Business |

|

|

26 |

|

|

|

| Health and Safety |

|

|

26 |

|

|

|

| Environmental |

|

|

28 |

|

|

|

| Human Rights |

|

|

29 |

|

|

|

| Sustainability Reporting |

|

|

30 |

|

|

|

| Material Properties |

|

|

32 |

|

|

|

| Kişladağ |

|

|

32 |

|

|

|

| Efemçukuru |

|

|

40 |

|

|

|

| Olympias |

|

|

46 |

|

|

|

| Skouries |

|

|

54 |

|

|

|

| Lamaque |

|

|

62 |

|

|

|

| Non-Material Properties |

|

|

69 |

|

|

|

| Stratoni |

|

|

69 |

|

|

|

| Tocantinzinho |

|

|

71 |

|

|

|

| Certej |

|

|

74 |

|

|

|

| Perama Hill |

|

|

77 |

|

|

|

| Sapes Project |

|

|

80 |

|

|

|

| Vila Nova |

|

|

82 |

|

|

|

| Mineral reserves and resources |

|

|

83 |

|

|

|

| Year-end 2017 mineral reserve and mineral

resource tabulations |

|

|

83 |

|

|

|

| Risk factors in our business |

|

|

93 |

|

|

|

| Investor information |

|

|

133 |

|

|

|

| Governance |

|

|

138 |

|

4

|

|

|

|

|

| Terms of Reference |

|

|

150 |

|

|

|

| I. ROLE |

|

|

150 |

|

|

|

| II. RESPONSIBILITIES |

|

|

150 |

|

|

|

| III. COMPOSITION |

|

|

154 |

|

|

|

| IV. MEETINGS AND PROCEDURES |

|

|

154 |

|

|

|

| Glossary |

|

|

156 |

|

Forward-looking information and risks

This document includes statements and information about what we expect to happen in the future. When we discuss our strategy, plans, goals, outlook,

including expected production, projected cash costs, planned capital and exploration expenditures, our expectation as to our future financial and operating performance, including future cash flow, estimated cash costs, resources and reserves,

expected metallurgical recoveries, price of gold and other commodities, and our proposed exploration, development, construction, permitting and operating plans and priorities, related timelines and schedules, results of litigation and arbitration

proceedings and other things that have not yet happened in this review, we are making statements considered to be forward-looking information or forward-looking statements under Canadian and United States securities laws. We refer to them in this

AIF as forward-looking information.

Key things to understand about the forward-looking information in this AIF:

It typically includes words and phrases about the future, such as plan, expect, forecast, intend, anticipate, believe, estimate, budget, continue,

projected, scheduled, may, could, would, might, will, as well as the negative of or variations of these words and phrases.

It is provided to help

you understand our current views and can change significantly; it may not be appropriate for other purposes.

It is based on a number of assumptions,

estimates and opinions that may prove to be incorrect, including the geopolitical, economic, permitting and legal climate in which we operate, the future price of gold and other commodities, exchange rates, anticipated costs and expenses,

production, mineral reserves and resources, metallurgical recoveries, the impact of acquisitions, dispositions, suspensions or delays on our business and the ability to achieve our goals.

It is inherently subject to known and unknown risks, uncertainties and other factors. Actual results and events may be significantly different from what

we currently expect due to the risks detailed under “Risks factors in our business” of this AIF, which includes a discussion of material, and other risks that could cause actual results to differ significantly from our current expectations

and risks associated with our business, including the following risks:

| |

● |

|

title, permitting and licensing risks, including the risks of obtaining and maintaining the validity and enforceability

of necessary permits and licenses, the timing of obtaining and renewing such permits and licenses, and risks of defective title to mineral property; |

| |

● |

|

risks of operating in foreign countries in which we currently or may in the future conduct business, including controls,

laws, |

| |

|

regulations, changes in mining regimes or governments, and political or economic developments; |

| |

● |

|

volatility of global and local economic climate and geopolitical risks; |

| |

● |

|

regulatory restrictions, including environmental regulatory restrictions and liability, including actual costs of

reclamation; |

5

| |

● |

|

changes in law and regulatory requirements or policies, including permitting, foreign investment, environmental, tax and

health and safety laws and regulations; |

| |

● |

|

competition for mineral properties and merger and acquisition targets; |

| |

● |

|

environmental risks, including use and transport of regulated substances; |

| |

● |

|

infrastructure, water, energy, equipment and other input availability and durability, and their cost and impact on

capital and operating costs, exploration, development and production schedules; |

| |

● |

|

perceptions of the local people about foreign companies operating on their land; |

| |

● |

|

ability to maintain positive relationships with the communities in which we operate and potential loss of reputation;

|

| |

● |

|

community and non-governmental actions and regulatory risks, including the

possibility of a shutdown at any of our operations; |

| |

● |

|

risks of not meeting production and cost targets or estimates; |

| |

● |

|

subjectivity of estimating mineral reserves and resources and the reliance on available data and assumptions and

judgments used in interpretation of such data and depletion of grades or quantities of mineral reserves; |

| |

● |

|

the loss of key employees and our ability to attract and retain qualified personnel; |

| |

● |

|

employee health and safety risks, and potential human rights risks related to our environmental impacts, economic and

social disruption, security incidents, land acquisition, indigenous peoples, access to remedy and our supply chain; |

| |

● |

|

labour disputes, labour shortages and risks associated with unionized labour; |

| |

● |

|

risks related to natural disasters and climate change |

| |

● |

|

prices for energy inputs, labour, material costs, supplies and services (including shipping) remaining consistent with

expectations |

| |

● |

|

speculative and uncertain nature of gold and other mineral exploration; |

| |

● |

|

discrepancies between actual and estimated production, mineral reserves and resources and metallurgical recoveries;

|

| |

● |

|

failure, security breaches or disruption of our information technology systems; |

| |

● |

|

development, mining and operational risks, including timing, hazards and losses that are uninsured or uninsurable;

|

| |

● |

|

impact on operations of compliance and non-compliance with General Data

Protection Regulation |

| |

● |

|

increased capital requirements and the ability to obtain financing; |

| |

● |

|

share capital dilution and share price volatility; |

| |

● |

|

risks associated with maintaining substantial levels of indebtedness, including potential financial constraints on

operations, interest rate risk and credit rating risk; |

| |

● |

|

gold and other metal price volatility and the impact of any related hedging activities; |

| |

● |

|

currency exchange fluctuations and the impact of any related hedging activities; |

| |

● |

|

taxation, including change in tax laws and interpretations of tax laws; |

| |

● |

|

financial reporting risks |

| |

● |

|

the impact of acquisitions, dispositions, monetization, mergers, other business combinations or transactions, including

effect of changes in our portfolio of projects on our current and future operations, capital requirements, and financial condition and ability to complete such transactions; |

| |

● |

|

the risks that the integration of acquired businesses may take longer than expected, the anticipated benefits of the

integration may be less than estimated or the costs of acquisition may be higher than anticipated; |

| |

● |

|

risk associated with co-ownership (including joint ventures);

|

| |

● |

|

litigation and arbitration risks, including the uncertainties inherent in current and future legal challenges we are, or

may become, a party to; and |

| |

● |

|

impact on operations of compliance and non-compliance with anti-corruption,

anti-bribery and sanction laws. |

6

The reader is directed to the discussion set out under the heading “Risk factors in our business”

for a full discussion of these risks and uncertainties.

Although we believe that the expectations reflected in the forward-looking information

contained herein are reasonable and we have attempted to identify important factors that could cause actual results to differ materially from those contained in the forward-looking information, there may be other factors that cause actual results to

differ materially from those which are anticipated, estimated or intended.

Forward-looking information is not a guarantee of future performance and

actual results and future events could materially differ from those anticipated in such statements and information.

We will not necessarily update

this information unless we are required to do so by applicable securities laws.

All forward-looking information in this AIF is qualified by these

cautionary statements.

Reporting mineral reserves and resources

There are material differences between the standards and terms used for reporting mineral reserves and resources in Canada, and the US. While the terms

mineral resource, measured mineral resource, indicated mineral resource and inferred mineral resource are defined by the Canadian Institute of Mining, Metallurgy and Petroleum (CIM), and the CIM Definition Standards on Mineral Resources and Mineral

Reserves adopted by the CIM Council, and must be disclosed according to Canadian securities regulations, the US Securities and Exchange Commission (SEC) does not recognize them under SEC Industry Guide 7 and they are not normally permitted to be

used in reports and registration statements filed with the SEC.

Investors should not assume that:

| |

● |

|

any or all of a measured, indicated or inferred mineral resource will ever be upgraded to a higher category or to

mineral reserves; or |

| |

● |

|

any or all of an indicated or inferred mineral resource exists or is economically feasible to mine.

|

Mineral resources which are not mineral reserves do not have demonstrated economic viability.

Under the securities regulations adopted by the Canadian Securities Administrators (CSA), estimates of inferred mineral resources generally cannot be

used as the basis of feasibility or prefeasibility studies.

Information about our mineral deposits may not be comparable to similar information made

public by US domestic mining companies, including information prepared according to SEC Industry Guide 7.

Except as otherwise noted, Paul Skayman,

FAusIMM, our Chief Operating Officer, is the “Qualified Person” under NI 43-101 responsible for preparing or supervising the preparation of, or approving the scientific or technical information

contained in this AIF for all our properties.

7

About Eldorado Gold

Eldorado Gold owns and operates mines around the world, primarily gold mines, but also a silver-lead-zinc mine and an iron ore mine. Its activities

involve all facets of the mining industry, including exploration, discovery, acquisition, financing, development, production and reclamation. Our business is currently focused in Turkey Greece, Canada Brazil, Romania and Serbia. Eldorado Gold is

governed by the Canada Business Corporations Act (CBCA) and is headquartered in Vancouver, BC.

Each operation has a general manager and operates as

a decentralized business unit within the Company. We manage exploration properties, merger and acquisition strategies, corporate financing, global tax planning, regulatory compliance, commodity price and currency risk management programs, investor

relations, engineering for capital projects and general corporate matters centrally, at our head office in Vancouver. Our risk management program is developed by senior management and monitored by the Board of Directors.

Properties as of March 29, 2018

|

|

|

|

Operating gold mines:

|

|

Other Operating Mines and

Development projects: |

|

● Kişladağ, in Turkey

(100%) ● Efemçukuru, in

Turkey (100%) ● Olympias, in

Greece (95%) |

|

● Stratoni, in Greece (95%),

silver-lead-zinc mine ● Lamaque,

in Canada (100%) development project Skouries, in Greece (95%) development project, currently moving into care and maintenance

● Perama Hill, in Greece (100%)

development project, currently on care and maintenance status

● Certej, in Romania (80.5%)

development project

● Tocantinzinho, in Brazil (100%)

development project ● Sapes, in

Greece (100%) development project currently on care and maintenance status ● Vila Nova, in Brazil (100%), iron ore mine, currently on care and maintenance status |

Kişladağ, Efemçukuru, Olympias, Skouries and Lamaque are material properties for the purposes of NI 43-101. The term Kassandra Mines is used throughout this AIF to reference the Stratoni and Olympias mine and Skouries project. The Stratoni mine consists of two deposits; Mavres Petres, which is still being mined,

and Madem Lakkos, which was mined out previously.

Eldorado Gold Corporation

Head office:

Suite 1188 – 550 Burrard Street

Vancouver, British Columbia, V6C 2B5

Telephone: 604.687.4018

Facsimile: 604.687.4026

Website:

www.eldoradogold.com

Eldorado Gold Corporation

Registered office:

Suite 2900 – 550 Burrard Street

Vancouver, British Columbia, V6C 0A3

8

Other offices:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Turkey |

|

Brazil |

|

Greece |

|

Barbados |

|

Romania |

|

Netherlands |

|

Canada |

|

Serbia |

|

● Ankara

● Usak

● Izmir

● Canakkale |

|

● Belo Horizonte

● Macapa |

|

● Athens

● Alexandropoulos

● Stratoni

● Sapes |

|

● Bridgetown |

|

● Deva |

|

● Amsterdam |

|

● Val-d’Or |

|

● Belgrade |

9

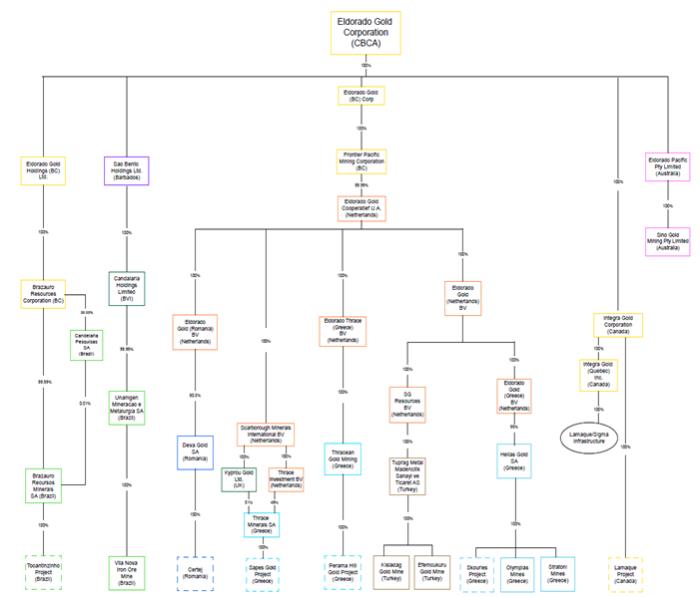

Our corporate structure is illustrated in the chart below (other than those subsidiaries permitted to be

excluded under Section 3.2 of 51-102F2).

Subsidiaries

We abbreviate

and refer to our subsidiaries as follows:

| |

● |

|

Brazauro Recursos Minerais S.A. (Brazauro) |

| |

● |

|

Deva Gold S.A. (Deva Gold) |

| |

● |

|

Hellas Gold S.A. (Hellas Gold) |

| |

● |

|

Integra Gold Corp.(Integra) |

| |

● |

|

Thracean Gold Mining S.A. (Thracean) |

| |

● |

|

Thrace Minerals S.A. (Thrace Minerals) |

| |

● |

|

Tuprag Metal Madencilik Sanayi ve Ticaret AS (Tuprag) |

10

Key milestones in our recent history

|

|

|

|

|

|

|

| 2015 |

|

|

|

2016 |

|

2017 |

|

● Published the Feasibility Study on Certej Project,

Romania ● Published the Feasibility Study on

Tocantinzinho Project, Brazil ● Received the

Project Permit Approval for the Eastern Dragon Project, China

● Amended Stratoni silver stream agreement with

Silver Wheaton ● Suspended operations at

Kassandra Mines for 6 weeks due to permitting issues with the government |

|

|

|

● Completed the sale of the 4 Chinese mineral assets to China National Gold and a subsidiary of Yintai Resources for a combined value of approximately $900M

● Suspended operations at Skouries based on the

action of the Ministry of Energy and Environment (MOE) in January 2016 and restarted the operations in May 2016 |

|

● Reconfigured pit design at Kişladağ and

decided to indefinitely defer expansion ● George

Burns appointed President and CEO in April

● Completed acquisition of Integra, commenced pre-feasibility work (including test mining), and advanced construction of the Lamaque mine and refurbishment of the associated Sigma mill

● Hellas Gold entered into arbitration proceedings

with the Greek Government, which are expected to conclude on or before April 6, 2018 ● Announced intention to move the Skouries project into care and maintenance due to continued permitting delays. The Skouries project is expected to be fully ramped down in H1

2018 ● Announced the reconfiguration of

the Board of Directors with retirement of Paul Wright in December 2017 and Jonathan Rubenstein in January 2018 and the appointment of George Albino as the new Board Chair.

● Olympias Phase II completed commissioning and

achieved commercial production in December |

In 2015, we published the feasibility study on the Certej project in Romania and on the Tocantinzinho project in Brazil.

In addition, we amended the Stratoni silver stream agreement with Silver Wheaton.

Operations at the Kassandra Mines were suspended for six weeks due to permitting delays by the government.

11

China

On April 26, 2016, Eldorado Gold reached an

agreement to sell and on September 6, 2016 completed the sale of its 82% interest in the Jinfeng mine to a wholly-owned subsidiary of China National Gold Group (CNG) for $300M in cash, subject to certain closing adjustments. On May 16,

2016 Eldorado Gold reached an agreement to sell and on November 22, 2016 completed the sale of its interest in the White Mountain mine, the Tanjianshan mine and the Eastern Dragon development project (the “Yintai operations”) to an

affiliate of Yintai Resources Co. Ltd. (Yintai) for $600M in cash, subject to certain closing adjustments.

The results from operations for our China

business have, together with restated comparatives, been presented as discontinued operations within the Consolidated Income Statements and the Consolidated Statements of Cash Flows in Eldorado Gold’s December 31, 2016 financial results.

The discontinued operations include the results of Jinfeng up to September 6, 2016 and of White Mountain, Tanjianshan and Eastern Dragon up to November 22, 2016.

Greece

In early 2016, we made significant changes to our

investment plans in Greece. In order to complete the construction and development of the Kassandra Mines we require the approval of various routine permits and licenses from a number of government agencies, predominantly under the direction of the

MOE.

As a result of routine permits being delayed, we suspended construction and development activities at Skouries in January 11, 2016.

Subsequently, we received the building permit for the Skouries processing plant. Activity at Skouries started up again on May 9, 2016. Skouries construction continued and was on track for a start up date in 2019.

On March 22, 2016, the Company was granted the installation permit in order to complete construction of the metallurgical plant required for Phase

II of Olympias. At year end 2016, Olympias Phase II was well advanced and commissioning commenced in Q2 of 2017.

In July 2017, Eldorado Gold completed the acquisition of Integra and commenced pre-feasibility work

(including test mining), and advanced construction of the Lamaque mine and refurbishment of the associated Sigma mill.

In September 2017, Hellas

Gold entered into arbitration proceedings with the Greek Government, which is expected to conclude on or before April 6, 2018. For more information on the Greek Arbitration, please refer to “Olympias –

Hellas Gold Litigation – Arbitration” on page 50.

In January 2017, Eldorado Gold announced the indefinite deferral of the

Kişladağ expansion from 12.5 Mtpa to 20 Mtpa. Eldorado Gold then reduced Kişladağ guidance mid-year due to concerns around the leach pad performance. Eldorado Gold identified a potential

issue with the leach pad chemistry and subsequently increased the cyanide addition levels. In October, 2017, Eldorado Gold reported lower metallurgical recoveries for sections of the orebody that were being mined, which subsequently caused a write

down of 40,000 ounces of gold from inventory. Testwork continues on the metallurgical performance of the remaining material along with a pre-feasibility study around milling. In March 2018, Eldorado Gold

announced the results of a pre-feasibility study regarding Kişladağ and its intention to proceed with a staged approach to the construction of a mill to treat all of the remaining economic ore at

Kişladağ. This pre-feasibility study confirmed that the mill option could provide robust returns, increased annual gold production and continuity of the Kişladağ operation until 2030.

In November 2017, Eldorado Gold announced its intention to move the Skouries project into care and maintenance due to continued permitting delays.

The Skouries project is expected to be fully ramped down in H1 2018. At the end of March 2018, Eldorado Gold announced the results of an updated technical report in respect of Skouries.

12

The Company continued exploration success at Lamaque (Canada), Bolcana (Romania), Efemçukuru

(Turkey), and Stratoni (Greece), with a total of 114,900 meters of drilling completed. At the end of March, 2018, Eldorado Gold announced the results of a pre-feasibility study in respect of Lamaque

Olympias Phase II completed commissioning and achieved commercial production on December 31, 2017.

In April 2017, George Burns was appointed President and CEO. Ross Cory retired from the Board in April, as he did not stand for re-election at the 2017 AGM. The Company announced the reconfiguration of the Board of Directors with retirement of Paul Wright in December 2017 and Jonathan Rubenstein in January 2018 and the

appointment of George Albino as the new Board Chair. The Board was reduced to eight directors (from 10) as well as reduced individual director and overall Board compensation. Jason Cho was promoted to Executive Vice President, Strategy and Corporate

Development effective as of November 1, 2017.

Dawn Moss, Executive Vice President, Administration, retired from Eldorado’s management team at the end of February 2018.

Timothy Garvin joined Eldorado as Executive Vice President and General Counsel on February 20, 2018.

Fabiana Chubbs, Chief Financial Officer will leave the Company at the end of April 2018.

13

Corporate

Senior Credit

Facility

On October 12, 2011, Eldorado Gold entered into a $280M revolving credit facility, maturing October 12, 2015, with a

syndicate of lenders. The credit facility (Amended Facility) was amended and restated as of November 23, 2012, and subsequently amended by a first amendment made April 30, 2013 and a second amendment made August 25, 2015. The

principal amount of the Amended Facility was increased by $95M to $375M and the maturity was extended from October 12, 2015 to November 23, 2016 (the “Maturity Date”).

On June 10, 2016, Eldorado Gold amended and restated the Amended Facility (Senior Credit Facility) to $250M with the option to increase the

principal amount by an additional $100M through an accordion feature. The Maturity Date was extended to June 13, 2020. The Senior Credit Facility is secured by the shares of S.G Resources and Tuprag.

The Senior Credit Facility contains covenants that restrict, among other things, the ability of Eldorado Gold and its material subsidiaries to incur

unsecured indebtedness exceeding $150M; incur certain permitted unsecured indebtedness exceeding $850M (inclusive of the Indenture) provided certain conditions are met; and incur certain permitted secured indebtedness exceeding $200M provided

certain conditions are met. The Senior Credit Facility also contains restrictions for making distributions in certain circumstances; selling material assets (other than the China assets that were disposed of in 2016); and conducting business other

than that which relates to the mining industry. Significant financial covenants include a maximum Net Debt to EBITDA ratio of 3.5:1 and a minimum EBITDA to Interest ratio of 3:1. Eldorado Gold was in compliance with the Senior Credit Facility

covenants as at December 31, 2017.

Loan interest is set at the Canadian Prime Rate, Base Rate or LIBOR Rate, in each case plus the applicable

margin, which margin is dependent on the net leverage ratio.

The Senior Credit Facility’s intended use is for Eldorado Gold to manage working

capital and for general corporate purposes. No amounts were drawn down under the Senior Credit Facility as of December 31, 2017.

Management

In December 2017, Eldorado Gold announced the resignation of Paul Wright effective December 31, 2017.

The Board of Directors

In December 2017, Eldorado Gold

announced the resignation of Jonathan Rubenstein effective January 1, 2018 from the Board of Directors. The Company also announced the appointment of Dr. George Albino as chair of the Board of Directors. Ross Cory retired from the Board on

April 27, 2017, as he did not stand for re-election at our AGM.

Recent property acquisitions, dispositions and reorganizations

The following discussion is a summary of our recent significant acquisitions and dispositions since January 1, 2015.

Acquisition of Integra:

On July 10, 2017, Eldorado Gold

completed the acquisition of Integra by way of plan of arrangement (Arrangement) originally announced on May 15, 2017. The Arrangement was approved by the shareholders of Integra at its special shareholder meeting on July 4,

2017 and received approval from the Supreme Court of British Columbia on July 7, 2017.

Pursuant to the Arrangement, Integra

shareholders collectively received, for all the issued common shares of Integra that Eldorado did not already own, approximately CDN$129M cash and 77M common shares of Eldorado

14

Gold (representing approximately 10% of the total issued common shares of Eldorado Gold, post-completion of the Arrangement).

Disposition of China Operations:

The transaction between Sino

Gold Mining Pty Limited (Sino Gold), a wholly owned subsidiary of the Company, as seller, and China National Gold Group Hong Kong Limited, a wholly owned subsidiary of CNG, as buyer, of all of the outstanding shares of Sino Mining Guizhou Pty Ltd.

and, indirectly, all of Eldorado Gold’s interest in the CNG Operations, for a price of $300M (subject to certain closing adjustments) in cash and on terms and conditions typical for such transactions, closed September 6, 2016, and has

fully completed, including finalization of all closing adjustments.

The transaction between Sino Gold, as seller, and Shanghai Shengwei Mining

Investment Co., Ltd., a wholly owned subsidiary of Yintai, Ltd., as buyer, of all of the shares held by Sino Gold in each of Sino Gold BMZ Limited, TJS Limited and Sino Gold Tenya Hong Kong Limited and indirectly, all of Eldorado

Gold’s respective interests in the White Mountain and Tanjianshan mines and the Eastern Dragon development project, for a price of $600M (subject to certain closing adjustments) in cash and on terms and conditions generally customary for such

transactions, closed November 22, 2016.

As a result of such dispositions, we no longer have any business operations in China.

Material Reorganization

From time to time, we may reorganize

our business, including winding up non-material subsidiaries, and transferring ownership of subsidiaries from one subsidiary to another. The sale of our interests in the CNG Operations and the Yintai

operations in 2016 resulted in the indirect sale of 11 subsidiaries and the acquisition of Integra in 2017 resulted in the indirect acquisition of two subsidiaries. See page 9 for our current corporate organizational chart.

15

About our business

Eldorado is a global gold and base metals producer. We believe our international expertise in mining, finance and project development places us in a

strong position to grow in value and deliver good returns for our stakeholders as we create and pursue new opportunities.

We are focused on building

a successful and profitable, intermediate gold company. Our strategy is to actively manage our portfolio of projects, including pursuing growth opportunities by discovering deposits through grassroots exploration and acquiring advanced

exploration, development or low-cost production assets with a focus on the regions where we already have a presence.

From time to time, we may evaluate and re-align our business objectives, including considering suspension or

delay of projects or disposition of assets.

Our success to date stems from a commitment to the following four strategic priorities.

1. Quality Assets

Our business is based on a portfolio of

long-life, low-cost assets in prospective jurisdictions. We believe that the quality of our asset base allows us to achieve long-term growth with solid margins and enhance our ability to generate free cash

flows and earnings per share.

2. Operational Excellence

We invest in new technologies and training our people in order to increase productivity, reduce risk and operate to guidance year-on-year.

3. Capital Discipline

Capital discipline underpins every business decision we make. Eldorado Gold considers all competing uses of cash and prioritize capital for sustaining

it’s operations and developing it’s key projects.

4. Accountability

We are committed to doing business honestly, respecting our neighbours, minimizing our environmental impacts and keeping our people safe. Operating this

way is essential to the sustainability of our business.

Industry factors that affect our results

Gold market and price

Gold is used mainly for product

fabrication and investment. It is traded on international markets. The London AM price for gold on December 31, 2017 was $1,296.50 per ounce.

Foreign

currency exposure

All of our revenues from gold sales are denominated in US dollars, while the majority of our operating costs are denominated

in the local currencies of the countries we operate in. We monitor the economic environment, including foreign exchange rates, in these countries on an ongoing basis.

The table below shows the foreign exchange losses (gains in brackets) recorded in the last three financial years:

|

|

|

| As of December 31*: |

| 2017 |

|

($2,382,000) |

| 2016 |

|

$2,708,000 |

| 2015 |

|

$15,044,000 |

*Losses from previous years were restated to exclude discontinued operations.

Hedging

16

We monitor and consider the selective use of a variety of hedging techniques to mitigate the impact of

downturns in the various metals and currency markets.

As of the date of this AIF, we do not have any material long-term gold or currency hedges.

However, between November 2017 and January 2018, Eldorado entered into a series of zero-cost Asian-style collars to hedge the price of certain base metal production at our Stratoni and Olympias mines. The

collars protect the price of lead and zinc production within a pre-defined price band. The commodity reference price is based on monthly averages as traded on the London Mercantile Exchange (LME) and are

quoted in USD.

With respect to Lead, the collar protects the Company at a minimum price of $2,300 per tonne. It also caps or limits the price

per the schedule below. Similarly, for Zinc, the minimum price is $2,850 per tonne and the cap or limits are also per the schedule below. The contracts have monthly maturities for the calendar 2018 year, with the final contract maturing on

December 31, 2018.

Should the price of each metal average below the floor, the Company will benefit from the hedge position and the

counterparty will have a settlement owing to us. Inversely, if the average monthly price exceeds the limit or cap then the Company will have a settlement owing to the counterparty. The hedge covers 15,336 tonnes of lead and 25,416 tonnes

of zinc. A summary of the positions is as follows:

|

|

|

|

|

|

|

|

|

| Metal |

|

Hedged

Amount

(tonnes) |

|

PUT

($/T) |

|

CALL

($/T) |

|

Maturity |

| Lead |

|

7,668 |

|

$2,300 |

|

$2,625 |

|

Jan 2018 – June 2018 |

| Lead |

|

7,668 |

|

$2,300 |

|

$2,735 |

|

Jul 2018

– Dec 2018 |

| Zinc |

|

12,708 |

|

$2,850 |

|

$3,470 |

|

Jan 2018

– Jun 2018 |

| Zinc |

|

12,708 |

|

$2,850 |

|

$3,600 |

|

Jul 2018

– Dec 2018 |

As of December 31, 2017, the net mark-to-market value

of the hedge contracts was $837,000, representing a loss to the Company.

An overview of our business

Below we describe each stage of the mining life cycle and the role of our dedicated teams at each phase.

|

|

|

| Exploration |

|

Eldorado’s exploration and corporate development teams actively look for potential new assets within our focus jurisdictions and in new regions.

They assess early and advanced stage exploration projects and conduct near-mine and grassroots exploration programs with the primary goal of adding value through discovery by increasing our mineral resources and reserves. Our exploration programs

are focused primarily in the countries in which we operate: Brazil, Canada, Greece, Romania, Serbia, and Turkey. During grassroots exploration, our

exploration teams visit prospective areas to conduct geological surveys and sampling, often partnering with other companies to benefit from their local knowledge and experience. If results indicate a possible mineralized deposit, we drill

exploration holes to determine whether economically viable concentrations of metals may exist. |

| Evaluation and Development |

|

During the

evaluation and development stage, our engineering, technical services and metallurgy teams conduct feasibility studies to determine:

● the optimal mining methods and

mineral recovery processes for each project, |

17

|

|

|

| |

|

● the required infrastructure,

● the best placement and design of

facilities, based on thorough impact and mitigation assessments, and

● the required mine monitoring,

closure and reclamation plans. These studies give us a picture of the capital costs required for development and the longer-term economics of the

project. We are then able to decide if a capital investment makes economic sense, in order to make a construction decision. |

| Construction |

|

Once the

project Environmental Impact Assessment (EIA) (also known as an Environmental Impact Study (EIS)) and other relevant permits are approved by government authorities, and we have received board approval to proceed, our capital projects team can begin

construction. Explicit requirements described in each EIA guide our activities and help us manage any social and environmental risks. This

construction phase requires the greatest input of capital and resources over a project’s life cycle, and through this phase we can add significant value to local economies through local job growth and procurement. |

| Mining and Processing |

|

During

production, our operations team and site personnel are responsible for mining and extracting ore from our underground mines (Efemçukuru, Olympias, Lamaque, Stratoni) and open pit mines (Kişladağ). The ore is processed on-site to produce a concentrate or doré. Any leftover materials generated by our mining activities, which typically include topsoil, waste rock and tailings, are either placed

on-site in engineered facilities for storage and treatment, or reused elsewhere on-site as part of construction activities, rehabilitation, or as underground backfill.

Rigorous environmental monitoring – to test air, water and soil quality, and noise, blast vibration and dust levels – enables us to comply with environmental regulations and our operating licenses and permits. |

| Reclamation and Closure |

|

Restoring the

land so it is compatible with the surrounding landscape is a priority for us and our communities. How we conduct our rehabilitation in one jurisdiction impacts how we are welcomed in another. Therefore, prior to and throughout a mine’s

operation, our operations teams develop and continuously enhance plans for the mine’s future closure in order to:

● Protect public health and

safety, ● Eliminate environmental

damage, ● Return the land to its

original condition, or an acceptable and productive alternative, and

● Provide for long-term social and

economic benefits. |

| Refining and Sales |

|

We produce

gold, silver, lead and zinc. Our in-country marketing teams are responsible for finding downstream smelters and refineries and establishing long-term working relationships and purchase agreements. These

agreements outline the terms and conditions of payment for our products, and specify parameters and penalties for the quantity, quality and chemical composition of our doré and concentrate.

The gold doré produced at Kişladağ is refined to market delivery standards at gold refineries in Turkey and sold at the spot price on

the Istanbul Gold Exchange. Contracts are also in place for the sale of concentrates from Greece and Turkey. These include gold concentrates from

Efemçukuru and Olympias as well as lead/silver and zinc concentrates from Stratoni and Olympias in Greece. These concentrates are sold under contract and are paid for at prevailing spot prices for the contained metals.

Gold doré will be produced at Lamaque and will be sold to local refineries. |

18

Except as otherwise noted, Paul Skayman, FAusIMM, Eldorado Gold’s Chief Operating Officer, is the

Qualified Person under NI 43-101 responsible for preparing or supervising the preparation of, or approving the scientific or technical information contained in this AIF for all our properties.

19

Production and costs

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| |

|

|

|

|

|

|

|

|

|

2017

|

|

|

| |

|

2017 |

|

2016* |

|

Change |

|

First

quarter |

|

Second

quarter |

|

Third

quarter |

|

Fourth quarter |

| Total |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Gold ounces produced

(including gold from tailings retreatment and pre commercial production at Olympias)** |

|

292,971 |

|

312,299 |

|

(193,222) |

|

75,172 |

|

63,692 |

|

70,053 |

|

83,886 |

| Cash operating costs ($ per

ounce) |

|

509 |

|

487 |

|

70 |

|

466 |

|

484 |

|

508 |

|

577 |

| Total cash cost ($ per

ounce) |

|

534 |

|

502 |

|

87 |

|

483 |

|

502 |

|

548 |

|

603 |

| All in sustaining cost ($

per ounce) |

|

922 |

|

829 |

|

(93) |

|

791 |

|

846 |

|

925 |

|

1,104 |

| Realized price ($ per ounce

sold) |

|

1,262 |

|

1,249 |

|

13 |

|

1,222 |

|

1,262 |

|

1,290 |

|

1,280 |

| CONTINUING OPERATIONS:

Kişladağ |

| Gold ounces

produced |

|

171,358 |

|

211,161 |

|

(39,803) |

|

52,644 |

|

38,456 |

|

35.902 |

|

44,356 |

| Tonnes to pad

|

|

13,061,861 |

|

16,565,254 |

|

(3,503,393) |

|

3,227,406 |

|

3,288,604 |

|

3,212,861 |

|

3,332,990 |

| Grade (grams per tonne) |

|

1.03 |

|

0.80 |

|

0.23 |

|

1.13 |

|

0.82 |

|

1.17 |

|

1.02 |

| Cash operating costs ($ per

ounce) |

|

500 |

|

474 |

|

(26) |

|

446 |

|

464 |

|

491 |

|

604 |

| Total cash cost ($ per

ounce) |

|

522 |

|

488 |

|

(34) |

|

464 |

|

478 |

|

528 |

|

626 |

|

Efemçukuru |

| Gold ounces

produced |

|

96,080 |

|

98,364 |

|

(2,452) |

|

22.528 |

|

23,406 |

|

24,905 |

|

25,295 |

| Tonnes milled

|

|

481,649 |

|

476,528 |

|

5,121 |

|

115,794 |

|

120,044 |

|

121,759 |

|

119,135 |

| Grade (grams per tonne) |

|

7.01 |

|

7.40 |

|

(0.39) |

|

6.77 |

|

6.95 |

|

7.20 |

|

7.46 |

| Cash operating costs ($ per

ounce) |

|

524 |

|

514 |

|

(10) |

|

515 |

|

509 |

|

529 |

|

525 |

| Total cash cost ($ per

ounce) |

|

556 |

|

530 |

|

(26) |

|

531 |

|

521 |

|

572 |

|

559 |

|

Lamaque |

| Ounces produced

|

|

7,061 |

|

0 |

|

7,061 |

|

0 |

|

0 |

|

0 |

|

0 |

| Cash operating costs

($/ounce) |

|

0 |

|

0 |

|

0 |

|

0 |

|

0 |

|

0 |

|

0 |

| Sustaining capex

|

|

0 |

|

0 |

|

0 |

|

0 |

|

0 |

|

0 |

|

0 |

|

Olympias** |

|

Gold ounces produced (pre-commercial) |

|

18,472 |

|

2,774 |

|

15,698 |

|

0 |

|

2,052 |

|

9,246 |

|

7,174 |

| Tonnes Milled

|

|

141,236 |

|

87,350 |

|

53,886 |

|

0 |

|

20,550 |

|

62,099 |

|

58,587 |

| Grade (grams per tonne) |

|

7.45 |

|

2.47 |

|

4.98 |

|

0 |

|

7.35 |

|

8.32 |

|

6.64 |

|

Stratoni |

| Lead/zinc concentrate tonnes sold

|

|

41,693 |

|

42,655 |

|

(962) |

|

14,835 |

|

8,351 |

|

7,400 |

|

11,107 |

|

DISCONTINUED OPERATIONS:

Tanjianshan

|

| Gold ounces

produced |

|

|

|

49,266 |

|

(49,266) |

|

0 |

|

0 |

|

0 |

|

0 |

| Tonnes milled

|

|

|

|

869,964 |

|

(869,964) |

|

0 |

|

0 |

|

0 |

|

0 |

| Grade (grams per tonne) |

|

|

|

1.90 |

|

(1.90) |

|

0 |

|

0 |

|

0 |

|

0 |

| Cash operating costs ($ per

ounce) |

|

|

|

819 |

|

819 |

|

0 |

|

0 |

|

0 |

|

0 |

20

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Total cash cost ($ per

ounce) |

|

|

|

970 |

|

970 |

|

0 |

|

0 |

|

0 |

|

0 |

|

Jinfeng |

| Gold ounces

produced |

|

|

|

68,195 |

|

(68,195) |

|

0 |

|

0 |

|

0 |

|

0 |

| Tonnes milled

|

|

|

|

766,697 |

|

(766,697) |

|

0 |

|

0 |

|

0 |

|

0 |

| Grade (grams per tonne)

|

|

|

|

3.32 |

|

(3.32) |

|

0 |

|

0 |

|

0 |

|

0 |

| Cash operating costs ($ per

ounce) |

|

|

|

705 |

|

(705) |

|

0 |

|

0 |

|

0 |

|

0 |

| Total cash cost ($ per

ounce) |

|

|

|

791 |

|

(791) |

|

0 |

|

0 |

|

0 |

|

0 |

|

White Mountain |

| Gold ounces

produced |

|

|

|

56,265 |

|

(56,265) |

|

0 |

|

0 |

|

0 |

|

0 |

| Tonnes milled

|

|

|

|

717,145 |

|

(717,145) |

|

0 |

|

0 |

|

0 |

|

0 |

| Grade (grams per tonne) |

|

|

|

2.78 |

|

(2.78) |

|

0 |

|

0 |

|

0 |

|

0 |

| Cash operating costs ($ per

ounce) |

|

|

|

731 |

|

(731) |

|

0 |

|

0 |

|

0 |

|

0 |

| Total cash cost ($ per

ounce) |

|

|

|

773 |

|

(773) |

|

0 |

|

0 |

|

0 |

|

0 |

*Production totals for 2016 include both continuing and discontinued operations. For more information on our discontinued operations

(Tanjianshan, Jinfeng and White Mountain), please see our prior AIF.

**Olympias for 2017 is Pre-commercial production.

| |

● |

|

We calculate cash operating costs according to the Gold Institute Standard. |

| |

● |

|

Total cash cost is cash operating costs plus royalties, and production taxes. |

| |

● |

|

Cash operating costs and total cash cost and all-in sustaining costs are non-IFRS measures. See page 10 of our MD&A and below for more information. |

| |

● |

|

AISC (All-in sustaining costs) are calculated by taking total cash costs and

adding sustaining capital expenditure, corporate administrative expenses, exploration and evaluation costs, and reclamation cost accretion. Eldorado Gold began reporting AISC in 2014. |

How we measure our costs

The following

are non-IFRS measures, which we believe provide a better indication of our cash flow from operations and may be meaningful in evaluating our past performance or future prospects. It is not meant to be a

substitute for cash flow from operations (or operating activities), which we calculate according to IFRS.

Since there is no standard method for

calculating non-IFRS measures, they are not a reliable way to compare us against other companies. Non-IFRS measures should be used with other performance measures

prepared in accordance with IFRS.

Costs are calculated using the standard developed by the Gold Institute, a worldwide association of suppliers of

gold and gold products including leading North American gold producers.

The Gold Institute stopped operating in 2002, but its standard is still

widely used in North America to report cash costs of production. Adoption of the standard is voluntary, so you may not be able to compare the costs reported here to those reported by other companies.

Cash operating costs (C1)

Cash operating costs include the

costs of operating the site, including mining, processing and administration. They do not include royalties and production taxes, amortization, reclamation costs, financing costs or capital development (initial and sustaining) or exploration costs.

Cash operating costs are divided by ounces sold to arrive at cash operating cost per ounce.

21

Total cash cost

Total cash cost is cash operating costs, plus royalties and production taxes.

All-in Sustaining Cost

AISC is calculated by taking total cash costs and adding sustaining capital expenditures, corporate administrative expenses, exploration and evaluation

costs, and reclamation cost accretion. Sustaining capital expenditures are defined as those expenditures which do not increase annual gold ounce production at a mine site and exclude all expenditures at our projects and certain expenditures at our

operating sites which are deemed expansionary in nature. Certain other cash expenditures, including tax payments, dividends and financing costs are not included. The Company believes that this measure represents the total costs of producing gold

from current operations, and provides the Company and other stakeholders of the Company with additional information on the Company’s operational performance and ability to generate cash flows. The Company reports this measure on a gold ounces

sold basis. Please refer to our management’s discussion and analysis (MD&A) for the year ended December 31, 2017. You can find these documents and additional information about the Company filed under our name on SEDAR (www.sedar.com).

22

Corporate Social Responsibility

For us, being a responsible corporate citizen means making a positive impact in the areas where we operate by protecting the environment, providing a

safe and respectful workplace for our employees and contractors, and investing in infrastructure, economic development, health and education in the communities around our operations so that we can enhance the lives of those who work and live there

beyond the life of the mine.

Over the past twenty-two years, we have operated mines in Mexico, Brazil,

Turkey, Greece and China. We continue to operate in Turkey, operate and develop our projects in Greece, and maintain progress towards developing our existing projects in Canada, Brazil and Romania. We are also exploring in Serbia. We are proud of

our record of implementing industry best practices that minimize environmental impacts while maximizing long-term social and economic benefits.

Our Workforce

At the end of 2017, we

directly employed 4,951 employees and contractors worldwide, with the majority of our employees residing in local communities near our operations.

We have permanent employees and contractors in nine countries. We also engage a number of contractors to work on specific projects. The table below shows

the number of personnel working at our operations by country at December 31, 2017.

|

|

|

|

|

|

|

| |

|

Employees

|

|

Contractors

|

|

Total

|

| Turkey |

|

1,271 |

|

661 |

|

1,932 |

| Brazil |

|

56 |

|

115 |

|

171 |

| Greece |

|

1,088 |

|

1,191 |

|

2,279 |

| Canada |

|

139 |

|

96 |

|

235 |

| Romania |

|

263 |

|

53 |

|

316 |

| Barbados |

|

1 |

|

0 |

|

1 |

| Serbia |

|

9 |

|

0 |

|

9 |

| Netherlands |

|

6 |

|

0 |

|

6 |

| China |

|

0 |

|

2 |

|

2 |

| Total |

|

2,833 |

|

2,118 |

|

4,951 |

The majority of our employees are unionized, with employment terms and conditions negotiated through collective

bargaining agreements. In 2017, we renewed each of our agreements in Greece, Romania and Brazil, while our agreement in Turkey is valid until December 31, 2018. Approximately 72% of our employees at our mines in Turkey, Greece, Brazil, Canada

and Romania were covered by collective bargaining agreements in 2017.

Generally, we believe we have good relations with both our unionized and non-unionized employees and are committed to resolving employee relations matters promptly and to mutually beneficial outcomes.

Operating Responsibly

The “About our Business” section of this AIF describes each stage of the mining life cycle,

from exploration through to mine closure. Below we provide a brief overview of some of the additional activities we undertake as part of being a responsible operator and respectful neighbour.

Exploration

During exploration, while we conduct geological

surveys, drilling and sampling to determine the existence and location of an ore deposit, we first engage directly with local communities. Through this interaction, we seek to understand their social and environmental concerns and consider these as

part of our exploration programs and

23

potential mine development plans. Where possible, we hire local residents and local contractors to assist us in conducting our exploration fieldwork. We also assess community needs so that we can

plan future initiatives and investments. During exploration, we also conduct environmental baseline studies as part of our mine impact assessments.

Evaluation

and Development

During the evaluation and development stage, we complete feasibility studies that outline the economics, optimal mining methods

and mineral recovery processes for the project, including environmental and closure considerations. We conduct extensive environmental testing and studies to establish baseline data and characteristics for air, water, soil and biodiversity. All this

information becomes part of an EIA, also referred to as an Environmental Impact Study (EIS) that must be completed and approved by the relevant government authorities before a project can be developed. Sustainability criteria are built into the EIA,

and throughout the environmental permitting process we engage and consult with local communities, businesses and government to obtain input and commentary. This research and dialogue helps Eldorado develop innovative solutions for the social and

environmental challenges of our projects, including, but not limited to, dust and air emissions, water and energy use, noise and waste. Infrastructure development initiatives – such as initiatives for improving roads, building sewage systems

and drilling water wells – may also commence, subject to both project and local community needs.

Construction

We make it a priority to hire locally. We also train and instruct our employees and contractors in leading environmental, health and safety practices,

procedures and controls. Based on dialogue with local communities and businesses, we identify gaps in skills and capacity, provide on-the-job training and, where

possible, work with local technical schools and universities to enhance their mining-specific and trades programs so that local residents and businesses have the skills and training necessary for employment with us.

Mining and Processing

All of our mining operations are

required to comply with the more stringent of local or international environmental standards. We implement the practices described in our applicable EIA or EIS and permits to mitigate known potential environmental impacts throughout the life of a

mine.

Beyond adherence to our permits and licenses, we add value during the production phase through a commitment to local employment and

procurement, operational excellence, local investment and community engagement. New equipment and technologies, continuous improvement projects, low accident rates, a commitment to environmental stewardship and effective controls and procedures

combine to deliver productivity benefits. Frequent consultation with local communities and businesses helps identify where we can create new opportunities for sustainable economic development within the framework of our Code of Business

Conduct & Ethics and Anti-Bribery & Anti-Corruption Policy (ABC).

Consultation with local communities continues throughout the

mining and processing cycle. As part of our commitment to protecting the environment, we maintain extensive environmental monitoring programs, the results of which are shared with relevant government agencies and independent government and academic

groups. We also regularly audit our operations to determine whether each site is operating within environmental limits. We monitor air, water (surface and ground) and soil quality, as well as noise, blast vibration and dust levels both on the mine

site and surrounding areas. We are sensitive to the potential impacts of our operations on local communities and have robust programs to mitigate any such effects. We also implement programs to preserve biodiversity at and near our operations. All

types of mine waste, including hazardous wastes, are stored and disposed of with consideration for their potential environmental impacts.

Water use

is strictly controlled across all of our sites to reduce overall water consumption, and we recycle as much water as is possible. Process tailings are discharged into specially constructed storage facilities, which are lined if required, and water

from tailings is recycled through the mining process or, if being discharged, treated and tested

24

to meet regulated limits before release. Measures are also in place to safeguard our tailings storage areas in the case of heavier than usual rainfall.

We employ 4,951 employees and contractors worldwide, the majority of whom are from the local communities near our operations. Less than 1% of our

employees across the Company, including our operations and projects, are expatriates. We pay locally competitive salaries and benefits to our employees and contractors.

To provide a healthy and safe work environment, our workforce is trained on a regular and ongoing basis. These training programs are designed to minimize

accidents and occupational illnesses.

Since the life of any mine is limited, we encourage and work with local communities to create new

opportunities for long-term economic development. For example, we have supported the creation of local companies such as a vineyard management company at Efemçukuru, a plant nursery business at Olympias, and transport services companies at

both Kişladağ and Efemçukuru. This ultimately benefits local communities and helps to provide opportunity for local residents, including those not directly associated with mining operations, beyond the life of the mine.

In 2017, Efemçukuru worked on a number of underground efficiency projects reliant on technology. These were all completed utilizing in-house information technology (IT) and underground personnel, in partnership with Izmir-based technology companies. These projects include the new Pitram control

center, underground personnel tracking, fixed plant management system and most recently, the underground traffic management system. This has the benefit of upgrading employee skills and lowering costs and includes local back up service and

development. Importantly, it has developed strong relationships with the local Aegean (Izmir) based IT companies, which is critical to mine system development in the future.

Reclamation, Care and Maintenance and Closure

Prior to and

throughout a mine’s operation, we conduct research to establish best practices for mine reclamation and closure. Whenever possible, remediation and reclamation will begin in parallel with other work being carried out across the mine. For

example, at Kişladağ, cover systems for capping the leach pad and rock dumps have been designed and are implemented as work is completed on those areas. Topsoil removed from mining and construction areas is stored for later use in all

reclamation activities. We also investigate different plants, shrubs and tree species suitable for local propagation in studies that are typically done in onsite greenhouses.

Sometimes it is necessary to place a mine site or development project under care and maintenance, whereby we temporarily close the site when there is the

potential to recommence operations at a later date. This may occur when a mine or development project is considered temporarily unviable (e.g. current economic conditions or resource prices) or expected permits have not been issued. During care and

maintenance, such as at Eldorado’s Vila Nova mine production and construction activities are stopped but the site is managed so that it remains in a safe and stable condition. Environmental management of risks such as mine tailings, hazardous

materials storage and water continue to be managed, while idle plants and machinery are maintained. Care and maintenance does not reduce our environmental or safety requirements. Skouries is moving towards care and maintenance due to the Greek

government delays in the issuing required permits. It is expected that Skouries will be in full care and maintenance by mid-2018.

Once a mine site is permanently closed, we conduct further environmental monitoring and reclamation activities, as required by the mine’s EIA and

mine licenses, so that the environment can successfully transition to a productive ecosystem.

All of Eldorado’s mine closure plans address:

| |

● |

|

Decommissioning – dismantling mine infrastructure such as facilities and buildings |

| |

● |

|

Reclamation – rehabilitating and revegetating disturbed areas |

| |

● |

|

Ongoing monitoring – long-term monitoring of environmental parameters |

| |

● |

|

Closure costs – regularly reviewing and updating closure plan costs, and making financial provisions

|

25

Ethical Business

Throughout the lifecycle of our operations, we remain aware of the social, political and economic risks posed by bribery and corruption. These risks may

result in social or financial harm to our business and our stakeholders, and it is our responsibility to operate transparently under the rule of law to mitigate these risks in all of our operating jurisdictions. Eldorado’s Code of Business

Conduct & Ethics (the Code) and ABC policies are intended to directly address these risks and advance ethical business conduct across our operations. The Code of Business Conduct & Ethics and the ABC policies are discussed further

on page 131.

Health and Safety

The

return of our people to their home safely every day is paramount to us. We are committed to the highest health and safety standards, strictly adhere to the most stringent safety regulations and have systems in place to promote a culture of safety.

2017 Safety Performance

We work to maintain a good

safety record by investing in environmental and health and safety training at our operations, and measure our results by tracking the numbers of lost-time incidents (LTIs) and the lost-time incident frequency rate (LTIFR) at each of our sites. In

order to reduce or eliminate LTIs we continue to train our workers and stress the importance of safety at our operations as one of our core values. We hold contractors working for Eldorado to the same high standards as our employees and all of our

safety reporting herein combines employees and contractors.

The table below shows our LTI performance for 2017 for our employees and contractors.

|

|

|

|

|

|

|

|

|

| |

|

|

|

Man hours worked

(million) |

|

LTI |

|

LTIFR |

| Turkey |

|

Kişladağ |

|

2.34 |

|

4 |

|

1.7 |

| |

|

Efemçukuru |

|

1.68 |

|

5 |

|

3.0 |

| Canada |

|

Lamaque* |

|

0.24 |

|

0 |

|

0.0 |

| Brazil |

|

Vila

Nova |

|

0.08 |

|

0 |

|

0.0 |

| |

|

Tocantinzinho |

|

0.24 |

|

0 |

|

0.0 |

| Greece |

|

Stratoni |

|

0.96 |

|

2 |

|

2.1 |

| |

|

Olympias |

|

2.01 |

|

2 |

|

1.0 |

| |

|

Skouries |

|

0.89 |

|

1 |

|

1.1 |

| |

|

Perama

Hill |

|

0.02 |

|

0 |

|

0.0 |

| Romania |

|

Certej |

|

0.62 |

|

1 |

|

1.6 |

| Exploration |

|

Exploration |

|

0.61 |

|

1 |

|

1.6 |

| Total |

|

|

|

9.68 |

|

16 |

|

1.65 |

* In 2017, Eldorado completed the acquisition of Lamaque. The reported man-hours worked, LTIs and

LTIFR reflects the assets safety performance since the date of acquisition.

We had an overall LTIFR of 1.65 this year, a 21% increase from 2016 when

statistics are adjusted to remove man-hours and injuries attributable to Eldorado’s formerly owned Chinese assets. This is the first time the LTIFR has increased in five years. Sadly, we had a fatality

involving a contractor during tree cutting operations at our Skouries project in Greece. Our internal investigation resulted in findings that we acted upon immediately, which included instituting additional administrative control measures and

training to increase hazard awareness all aimed at reducing the likelihood of a similar accident occurring again.

26

In late 2017, we finalised a Global Health and Safety Directive to provide all subsidiaries and operations

of Eldorado a common approach to achieving our vision of creating and sustaining a secure, injury free, healthy environment for all people who enter our workplaces.

Health and Safety Policy

In 2017, Eldorado updated its

Health and Safety Policy. The health and safety of our employees and local stakeholders is a key priority of Eldorado. We are committed to providing our employees with both a safe working environment and the skills necessary to perform their tasks

in a safe manner.

To achieve these goals, Eldorado commits to:

| |

● |

|

Promote safety as a core value within all levels of the organization. |

| |

● |

|

Comply fully with all applicable health and safety laws and regulations while adopting international best practices.

|

| |

● |

|

Promote a culture where all employees and contractors take responsibility for safety, actively take part in training and

recognize the importance of continuous improvement. |

| |

● |

|

Provide adequate resources throughout project life cycles to ensure the risks associated with every task are understood

and mitigated. |

| |

● |

|

Offer wellness programs in order to provide basic medical treatment, including immunizations and medical checkups as an

effort towards illness prevention. |

| |

● |

|

Require all of our contractors, suppliers and partners to conform to our Health and Safety Policy in their business

activities while on our sites. |

| |

● |

|

Adhere to the Company’s Global Health and Safety Directive to ensure consistency with respect to the design and

application of health and safety management systems. |

| |

● |

|

Implement emergency response programs at each mine site to support our activities, employees, visitors and community

members. |

| |

● |

|

Make our Health and Safety Policy accessible to all employees, contractors, stakeholders, business partners and

interested parties to Eldorado. |

This Policy is translated into each of our local languages and posted on notice boards at all of

our operations. A full copy of the Health and Safety Policy is available on our website: (https://www.eldoradogold.com/responsibility/health-and-safety/default.aspx).

Eldorado Gold also has a Sustainability Committee comprising selected members of the Board of Directors. Their task is to oversee and monitor the

environmental, health, safety, community relations, security, human rights and other sustainability policies, practices, programs and performance of the Company.

Safety Management Systems

As part of our commitment to a safe

workplace, we align our safety management systems with best practice frameworks. OHSAS 18001 is a leading framework for occupational health and safety management systems. Efemçukuru achieved OHSAS certification in July 2013 and was

recertified in 2016. Kişladağ achieved certification in December 2015. The Kassandra Mines achieved certification in January 2011 and were recertified in 2014 and 2017. All of the sites mentioned have passed their annual OHSAS surveillance

audits as required to maintain certification.

The Kassandra Mines also achieved certification in 2016 to the ISO 39001 road traffic safety

management systems framework. The objective of ISO 39001 is to reduce death and serious injuries related to road traffic incidents that are within the mines’ influence.

For further information on our safety initiatives please visit the ‘Responsibility’ section of Eldorado Gold’s website (https://www.eldoradogold.com/responsibility/default.aspx).

27

Environmental

All of our projects and operations are expected to comply with local and international environmental standards. We implement best practices described in

our EIAs and EISs and feasibility studies to maintain compliance.

Environmental Policy

In 2017, Eldorado Gold updated its Environmental Policy, which states that the Company is committed to minimizing our impact and protecting all aspects

of the natural environment of the areas in which we work. The Environmental Policy also applies to all contractors working on or for any of our projects or mines. This is a core value of Eldorado Gold and applies to all elements of the mining cycle

including exploration, development, operation and closure.

To address this standard of protection, Eldorado Gold and its subsidiaries will strive

to:

| |

● |

|

Design, develop, operate and decommission facilities in an environmentally sound manner. |

| |

● |

|

Conform to all applicable environmental laws and regulations, frameworks to which we subscribe and international best

practices. |

| |

● |

|

Identify, evaluate, manage and regularly review the potential environmental impacts of our projects from inception

through to closure. |

| |

● |

|