UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-07139

Fidelity Hereford Street Trust

(Exact name of registrant as specified in charter)

245 Summer St., Boston, MA 02210

(Address of principal executive offices) (Zip code)

Cynthia Lo Bessette, Secretary

245 Summer St.

Boston, Massachusetts 02210

(Name and address of agent for service)

Registrant's telephone number, including area code:

617-563-7000

Date of fiscal year end: | April 30 |

Date of reporting period: | October 31, 2020 |

Item 1.

Reports to Stockholders

Fidelity® Treasury Only Money Market Fund

Semi-Annual Report

October 31, 2020

See the inside front cover for important information about access to your fund’s shareholder reports.

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of a fund’s shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from the fund or from your financial intermediary, such as a financial advisor, broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from a fund electronically, by contacting your financial intermediary. For Fidelity customers, visit Fidelity's web site or call Fidelity using the contact information listed below.

You may elect to receive all future reports in paper free of charge. If you wish to continue receiving paper copies of your shareholder reports, you may contact your financial intermediary or, if you are a Fidelity customer, visit Fidelity’s website, or call Fidelity at the applicable toll-free number listed below. Your election to receive reports in paper will apply to all funds held with the fund complex/your financial intermediary.

| Account Type | Website | Phone Number |

| Brokerage, Mutual Fund, or Annuity Contracts: | fidelity.com/mailpreferences | 1-800-343-3548 |

| Employer Provided Retirement Accounts: | netbenefits.fidelity.com/preferences (choose 'no' under Required Disclosures to continue to print) | 1-800-343-0860 |

| Advisor Sold Accounts Serviced Through Your Financial Intermediary: | Contact Your Financial Intermediary | Your Financial Intermediary's phone number |

| Advisor Sold Accounts Serviced by Fidelity: | institutional.fidelity.com | 1-877-208-0098 |

Contents

|

Board Approval of Investment Advisory Contracts and Management Fees |

To view a fund's proxy voting guidelines and proxy voting record for the 12-month period ended June 30, visit http://www.fidelity.com/proxyvotingresults or visit the Securities and Exchange Commission's (SEC) web site at http://www.sec.gov.

You may also call 1-800-544-8544 to request a free copy of the proxy voting guidelines.

Standard & Poor's, S&P and S&P 500 are registered service marks of The McGraw-Hill Companies, Inc. and have been licensed for use by Fidelity Distributors Corporation.

Other third-party marks appearing herein are the property of their respective owners.

All other marks appearing herein are registered or unregistered trademarks or service marks of FMR LLC or an affiliated company. © 2020 FMR LLC. All rights reserved.

This report and the financial statements contained herein are submitted for the general information of the shareholders of the Fund. This report is not authorized for distribution to prospective investors in the Fund unless preceded or accompanied by an effective prospectus.

A fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-PORT. Forms N-PORT are available on the SEC’s web site at http://www.sec.gov. A fund's Forms N-PORT may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information regarding the operation of the SEC's Public Reference Room may be obtained by calling 1-800-SEC-0330.

For a complete list of a fund's portfolio holdings, view the most recent holdings listing, semiannual report, or annual report on Fidelity's web site at http://www.fidelity.com, http://www.institutional.fidelity.com, or http://www.401k.com, as applicable.

NOT FDIC INSURED •MAY LOSE VALUE •NO BANK GUARANTEE

Neither the Fund nor Fidelity Distributors Corporation is a bank.

Note to Shareholders:

Early in 2020, the outbreak and spread of a new coronavirus emerged as a public health emergency that had a major influence on financial markets, primarily based on its impact on the global economy and the outlook for corporate earnings. The virus causes a respiratory disease known as COVID-19. On March 11, the World Health Organization declared the COVID-19 outbreak a pandemic, citing sustained risk of further global spread.

In the weeks following, as the crisis worsened, we witnessed an escalating human tragedy with wide-scale social and economic consequences from coronavirus-containment measures. The outbreak of COVID-19 prompted a number of measures to limit the spread, including travel and border restrictions, quarantines, and restrictions on large gatherings. In turn, these resulted in lower consumer activity, diminished demand for a wide range of products and services, disruption in manufacturing and supply chains, and – given the wide variability in outcomes regarding the outbreak – significant market uncertainty and volatility. Amid the turmoil, global governments and central banks took unprecedented action to help support consumers, businesses, and the broader economies, and to limit disruption to financial systems.

The situation continues to unfold, and the extent and duration of its impact on financial markets and the economy remain highly uncertain. Extreme events such as the coronavirus crisis are “exogenous shocks” that can have significant adverse effects on mutual funds and their investments. Although multiple asset classes may be affected by market disruption, the duration and impact may not be the same for all types of assets.

Fidelity is committed to helping you stay informed amid news about COVID-19 and during increased market volatility, and we’re taking extra steps to be responsive to customer needs. We encourage you to visit our websites, where we offer ongoing updates, commentary, and analysis on the markets and our funds.

Investment Summary/Performance (Unaudited)

Effective Maturity Diversification as of October 31, 2020

| Days | % of fund's investments 10/31/20 |

| 1 - 7 | 29.3 |

| 8 - 30 | 16.0 |

| 31 - 60 | 19.4 |

| 61 - 90 | 10.7 |

| 91 - 180 | 24.6 |

Effective maturity is determined in accordance with the requirements of Rule 2a-7 under the Investment Company Act of 1940.

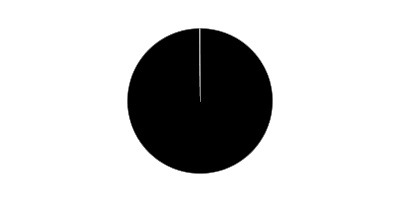

Asset Allocation (% of fund's net assets)

| As of October 31, 2020 | ||

| U.S. Treasury Debt | 98.6% | |

| Net Other Assets (Liabilities) | 1.4% | |

Current 7-Day Yields

| 10/31/20 | |

| Fidelity® Treasury Only Money Market Fund | 0.01% |

Yield refers to the income paid by the Fund over a given period. Yield for money market funds is usually for seven-day periods, as it is here, though it is expressed as an annual percentage rate. Past performance is no guarantee of future results. Yield will vary and it's possible to lose money investing in the Fund. A portion of the Fund's expenses was reimbursed and/or waived. Absent such reimbursements and/or waivers the yield for the period ending October 31, 2020, the most recent period shown in the table, would have been (.27)%.

Schedule of Investments October 31, 2020 (Unaudited)

Showing Percentage of Net Assets

| U.S. Treasury Debt - 98.6% | ||||

| Yield(a) | Principal Amount (000s) | Value (000s) | ||

| U.S. Treasury Obligations - 98.6% | ||||

| U.S. Treasury Bills | ||||

| 11/3/20 to 4/22/21 | 0.05 to 0.19% | $3,418,919 | $3,418,273 | |

| U.S. Treasury Notes | ||||

| 11/15/20 to 7/31/22 | 0.09 to 0.69 (b) | 905,977 | 906,537 | |

| TOTAL U.S. TREASURY DEBT | ||||

| (Cost $4,324,810) | 4,324,810 | |||

| TOTAL INVESTMENT IN SECURITIES - 98.6% | ||||

| (Cost $4,324,810) | 4,324,810 | |||

| NET OTHER ASSETS (LIABILITIES) - 1.4% | 60,217 | |||

| NET ASSETS - 100% | $4,385,027 |

The date shown for securities represents the date when principal payments must be paid, taking into account any call options exercised by the issuer and any permissible maturity shortening features other than interest rate resets.

Legend

(a) Yield represents either the annualized yield at the date of purchase, or the stated coupon rate, or, for floating and adjustable rate securities, the rate at period end.

(b) Coupon rates for floating and adjustable rate securities reflect the rates in effect at period end.

Investment Valuation

All investments are categorized as Level 2 under the Fair Value Hierarchy. The inputs or methodology used for valuing securities may not be an indication of the risk associated with investing in those securities. For more information on valuation inputs please refer to the Investment Valuation section in the accompanying Notes to Financial Statements.

See accompanying notes which are an integral part of the financial statements.

Financial Statements

Statement of Assets and Liabilities

| Amounts in thousands (except per-share amount) | October 31, 2020 (Unaudited) | |

| Assets | ||

| Investment in securities, at value — See accompanying schedule: Unaffiliated issuers (cost $4,324,810) | $4,324,810 | |

| Receivable for investments sold | 146,402 | |

| Receivable for fund shares sold | 12,290 | |

| Interest receivable | 1,542 | |

| Total assets | 4,485,044 | |

| Liabilities | ||

| Payable for investments purchased | $89,982 | |

| Payable for fund shares redeemed | 9,525 | |

| Distributions payable | 3 | |

| Accrued management fee | 507 | |

| Total liabilities | 100,017 | |

| Net Assets | $4,385,027 | |

| Net Assets consist of: | ||

| Paid in capital | $4,385,012 | |

| Total accumulated earnings (loss) | 15 | |

| Net Assets | $4,385,027 | |

| Net Asset Value, offering price and redemption price per share ($4,385,027 ÷ 4,384,151 shares) | $1.00 |

See accompanying notes which are an integral part of the financial statements.

Statement of Operations

| Amounts in thousands | Six months ended October 31, 2020 (Unaudited) | |

| Investment Income | ||

| Interest | $4,701 | |

| Expenses | ||

| Management fee | $9,686 | |

| Independent trustees' fees and expenses | 8 | |

| Total expenses before reductions | 9,694 | |

| Expense reductions | (5,226) | |

| Total expenses after reductions | 4,468 | |

| Net investment income (loss) | 233 | |

| Realized and Unrealized Gain (Loss) | ||

| Net realized gain (loss) on: | ||

| Investment securities: | ||

| Unaffiliated issuers | 3 | |

| Total net realized gain (loss) | 3 | |

| Net increase in net assets resulting from operations | $236 |

See accompanying notes which are an integral part of the financial statements.

Statement of Changes in Net Assets

| Amounts in thousands | Six months ended October 31, 2020 (Unaudited) | Year ended April 30, 2020 |

| Increase (Decrease) in Net Assets | ||

| Operations | ||

| Net investment income (loss) | $233 | $40,343 |

| Net realized gain (loss) | 3 | 5 |

| Net increase in net assets resulting from operations | 236 | 40,348 |

| Distributions to shareholders | (233) | (40,347) |

| Share transactions | ||

| Proceeds from sales of shares | 801,018 | 4,322,438 |

| Reinvestment of distributions | 211 | 37,205 |

| Cost of shares redeemed | (1,461,544) | (2,137,693) |

| Net increase (decrease) in net assets and shares resulting from share transactions | (660,315) | 2,221,950 |

| Total increase (decrease) in net assets | (660,312) | 2,221,951 |

| Net Assets | ||

| Beginning of period | 5,045,339 | 2,823,388 |

| End of period | $4,385,027 | $5,045,339 |

| Other Information | ||

| Shares | ||

| Sold | 801,018 | 4,322,438 |

| Issued in reinvestment of distributions | 211 | 37,205 |

| Redeemed | (1,461,544) | (2,137,693) |

| Net increase (decrease) | (660,315) | 2,221,950 |

See accompanying notes which are an integral part of the financial statements.

Financial Highlights

Fidelity Treasury Only Money Market Fund

| Six months ended (Unaudited) October 31, | Years endedApril 30, | |||||

| 2020 | 2020 | 2019 | 2018 | 2017 | 2016 | |

| Selected Per–Share Data | ||||||

| Net asset value, beginning of period | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 |

| Income from Investment Operations | ||||||

| Net investment income (loss) | –A | .014 | .018 | .008 | –A | –A |

| Net realized and unrealized gain (loss)A | – | – | – | – | – | – |

| Total from investment operations | –A | .014 | .018 | .008 | –A | –A |

| Distributions from net investment income | –A | (.014) | (.018) | (.008) | –A | –A |

| Total distributions | –A | (.014) | (.018) | (.008) | –A | –A |

| Net asset value, end of period | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 |

| Total ReturnB,C | .01% | 1.39% | 1.79% | .77% | .07% | .01% |

| Ratios to Average Net AssetsD | ||||||

| Expenses before reductions | .42%E | .42% | .42% | .42% | .42% | .42% |

| Expenses net of fee waivers, if any | .19%E | .42% | .42% | .42% | .38% | .16% |

| Expenses net of all reductions | .19%E | .42% | .42% | .42% | .38% | .16% |

| Net investment income (loss) | .01%E | 1.27% | 1.76% | .76% | .06% | .01% |

| Supplemental Data | ||||||

| Net assets, end of period (in millions) | $4,385 | $5,045 | $2,823 | $3,173 | $3,720 | $4,437 |

A Amount represents less than $.0005 per share.

B Total returns for periods of less than one year are not annualized.

C Total returns would have been lower if certain expenses had not been reduced during the applicable periods shown.

D Expense ratios reflect operating expenses of the class. Expenses before reductions do not reflect amounts reimbursed, waived, or reduced through arrangements with the investment advisor, brokerage services, or other offset arrangements, if applicable, and do not represent the amount paid by the class during periods when reimbursements, waivers or reductions occur.

E Annualized

See accompanying notes which are an integral part of the financial statements.

Notes to Financial Statements (Unaudited)

For the period ended October 31, 2020

(Amounts in thousands except percentages)

1. Organization.

Fidelity Treasury Only Money Market Fund (the Fund) is a fund of Fidelity Hereford Street Trust (the Trust) and is authorized to issue an unlimited number of shares. Share transactions on the Statement of Changes in Net Assets may contain exchanges between affiliated funds. The Trust is registered under the Investment Company Act of 1940, as amended (the 1940 Act), as an open-end management investment company organized as a Delaware statutory trust.

2. Significant Accounting Policies.

The Fund is an investment company and applies the accounting and reporting guidance of the Financial Accounting Standards Board (FASB) Accounting Standards Codification Topic 946 Financial Services – Investment Companies. The financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America (GAAP), which require management to make certain estimates and assumptions at the date of the financial statements. Actual results could differ from those estimates. Subsequent events, if any, through the date that the financial statements were issued have been evaluated in the preparation of the financial statements. The following summarizes the significant accounting policies of the Fund:

Investment Valuation. The Fund categorizes the inputs to valuation techniques used to value its investments into a disclosure hierarchy consisting of three levels as shown below:

- Level 1 – quoted prices in active markets for identical investments

- Level 2 – other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, etc.)

- Level 3 – unobservable inputs (including the Fund's own assumptions based on the best information available)

As permitted by compliance with certain conditions under Rule 2a-7 of the 1940 Act, securities are valued at amortized cost, which approximates fair value. The amortized cost of an instrument is determined by valuing it at its original cost and thereafter amortizing any discount or premium from its face value at a constant rate until maturity. Securities held by a money market fund are generally high quality and liquid; however, they are reflected as Level 2 because the inputs used to determine fair value are not quoted prices in an active market.

Investment Transactions and Income. The net asset value per share for processing shareholder transactions is calculated as of the close of business of the New York Stock Exchange (NYSE), normally 4:00 p.m. Eastern time. Security transactions are accounted for as of trade date. Gains and losses on securities sold are determined on the basis of identified cost. Interest income is accrued as earned and includes coupon interest and amortization of premium and accretion of discount on debt securities as applicable.

Expenses. Expenses directly attributable to a fund are charged to that fund. Expenses attributable to more than one fund are allocated among the respective funds on the basis of relative net assets or other appropriate methods. Expense estimates are accrued in the period to which they relate and adjustments are made when actual amounts are known.

Income Tax Information and Distributions to Shareholders. Each year, the Fund intends to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code, including distributing substantially all of its taxable income and realized gains. As a result, no provision for U.S. Federal income taxes is required. The Fund files a U.S. federal tax return, in addition to state and local tax returns as required. The Fund's federal income tax returns are subject to examination by the Internal Revenue Service (IRS) for a period of three fiscal years after they are filed. State and local tax returns may be subject to examination for an additional fiscal year depending on the jurisdiction.

Distributions are declared and recorded daily and paid monthly from net investment income. Distributions from realized gains, if any, are declared and recorded on the ex-dividend date. Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from GAAP.

Capital accounts within the financial statements are adjusted for permanent book-tax differences. These adjustments have no impact on net assets or the results of operations. Capital accounts are not adjusted for temporary book-tax differences which will reverse in a subsequent period.

Book-tax differences are primarily due to losses deferred due to wash sales.

As of period end, the cost and unrealized appreciation (depreciation) in securities for federal income tax purposes were as follows:

| Gross unrealized appreciation | $– |

| Gross unrealized depreciation | – |

| Net unrealized appreciation (depreciation) | $– |

| Tax cost | $4,324,810 |

3. Fees and Other Transactions with Affiliates.

Management Fee. Fidelity Management & Research Company LLC (the investment adviser) and its affiliates provide the Fund with investment management related services for which the Fund pays a monthly management fee that is based on an annual rate of .42% of the Fund's average net assets. Under the management contract, the investment adviser pays all other expenses, except the compensation of the independent Trustees and certain other expenses such as interest expense. The management fee is reduced by an amount equal to the fees and expenses paid by the Fund to the independent Trustees.

Interfund Trades. Funds may purchase from or sell securities to other Fidelity Funds under procedures adopted by the Board. The procedures have been designed to ensure these interfund trades are executed in accordance with Rule 17a-7 of the 1940 Act.

4. Expense Reductions.

The investment adviser or its affiliates voluntarily agreed to waive certain fees in order to avoid a negative yield. Such arrangements may be discontinued by the investment adviser at any time. For the period, the amount of the waiver was $5,213.

In addition, through arrangements with the Fund's custodian, credits realized as a result of certain uninvested cash balances were used to reduce the Fund's expenses by $13.

5. Other.

The Fund's organizational documents provide former and current trustees and officers with a limited indemnification against liabilities arising in connection with the performance of their duties to the Fund. In the normal course of business, the Fund may also enter into contracts that provide general indemnifications. The Fund's maximum exposure under these arrangements is unknown as this would be dependent on future claims that may be made against the Fund. The risk of material loss from such claims is considered remote.

6. Coronavirus (COVID-19) Pandemic.

An outbreak of COVID-19 first detected in China during December 2019 has since spread globally and was declared a pandemic by the World Health Organization during March 2020. Developments that disrupt global economies and financial markets, such as the COVID-19 pandemic, may magnify factors that affect the Fund's performance.

Shareholder Expense Example

As a shareholder, you incur two types of costs: (1) transaction costs, which may include sales charges (loads) on purchase payments or redemption proceeds, as applicable and (2) ongoing costs, which generally include management fees, distribution and/or service (12b-1) fees and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in a fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (May 1, 2020 to October 31, 2020).

Actual Expenses

The first line of the accompanying table provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000.00 (for example, an $8,600 account value divided by $1,000.00 = 8.6), then multiply the result by the number in the first line for a class/Fund under the heading entitled "Expenses Paid During Period" to estimate the expenses you paid on your account during this period. If any fund is a shareholder of any underlying mutual funds or exchange-traded funds (ETFs) (the Underlying Funds), such fund indirectly bears its proportional share of the expenses of the Underlying Funds in addition to the direct expenses incurred presented in the table. These fees and expenses are not included in the annualized expense ratio used to calculate the expense estimate in the table below.

Hypothetical Example for Comparison Purposes

The second line of the accompanying table provides information about hypothetical account values and hypothetical expenses based on the actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. If any fund is a shareholder of any Underlying Funds, such fund indirectly bears its proportional share of the expenses of the Underlying Funds in addition to the direct expenses as presented in the table. These fees and expenses are not included in the annualized expense ratio used to calculate the expense estimate in the table below.

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transaction costs. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds.

| Annualized Expense Ratio-A | Beginning Account Value May 1, 2020 | Ending Account Value October 31, 2020 | Expenses Paid During Period-B May 1, 2020 to October 31, 2020 |

|

| Fidelity Treasury Only Money Market Fund | .19% | |||

| Actual | $1,000.00 | $1,000.10 | $.96** | |

| Hypothetical-C | $1,000.00 | $1,024.25 | $.97** |

A Annualized expense ratio reflects expenses net of applicable fee waivers.

B Expenses are equal to the annualized expense ratio, multiplied by the average account value over the period, multiplied by 184/ 365 (to reflect the one-half year period). The fees and expenses of any Underlying Funds are not included in each annualized expense ratio.

C 5% return per year before expenses

** If certain fees were not voluntarily waived by the investment adviser or its affiliates during the period, the annualized expense ratio would have been .42% and the expenses paid in the actual and hypothetical examples above would have been $2.12 and $2.14, respectively.

Board Approval of Investment Advisory Contracts and Management Fees

Fidelity Treasury Only Money Market Fund

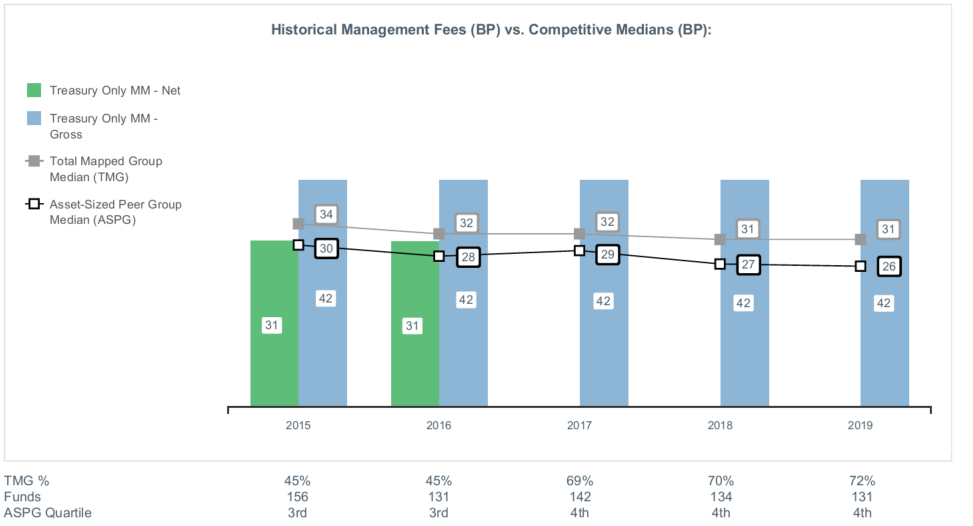

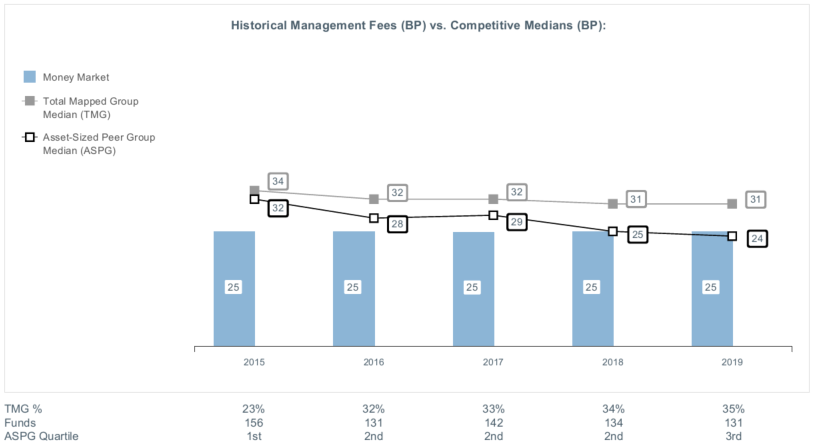

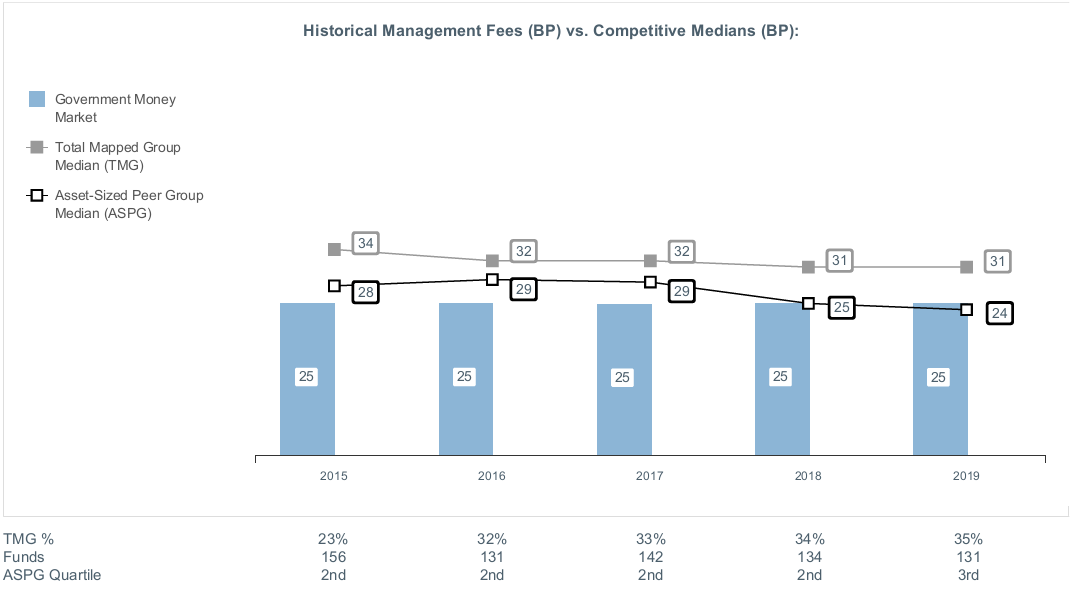

Each year, the Board of Trustees, including the Independent Trustees (together, the Board), votes on the renewal of the management contract with Fidelity Management & Research Company LLC (FMR) and the sub-advisory agreements (together, the Advisory Contracts) for the fund. FMR and the sub-advisers are referred to herein as the Investment Advisers. The Board, assisted by the advice of fund counsel and Independent Trustees' counsel, requests and considers a broad range of information relevant to the renewal of the Advisory Contracts throughout the year.The Board meets regularly and, at each of its meetings, covers an extensive agenda of topics and materials and considers factors that are relevant to its annual consideration of the renewal of the fund's Advisory Contracts, including the services and support provided to the fund and its shareholders. The Board has established four standing committees (Committees) — Operations, Audit, Fair Valuation, and Governance and Nominating — each composed of and chaired by Independent Trustees with varying backgrounds, to which the Board has assigned specific subject matter responsibilities in order to enhance effective decision-making by the Board. The Operations Committee, of which all of the Independent Trustees are members, meets regularly throughout the year and considers, among other matters, information specifically related to the annual consideration of the renewal of the fund's Advisory Contracts. The Board, acting directly and through its Committees, requests and receives information concerning the annual consideration of the renewal of the fund's Advisory Contracts. The Board also meets as needed to review matters specifically related to the Board's annual consideration of the renewal of the Advisory Contracts. Members of the Board may also meet with trustees of other Fidelity funds through joint ad hoc committees to discuss certain matters relevant to all of the Fidelity funds.At its September 2020 meeting, the Board unanimously determined to renew the fund's Advisory Contracts. In reaching its determination, the Board considered all factors it believed relevant, including (i) the nature, extent, and quality of the services provided to the fund and its shareholders (including the investment performance of the fund); (ii) the competitiveness of the fund's management fee and total expense ratio relative to peer funds; (iii) the total costs of the services provided by and the profits realized by Fidelity from its relationships with the fund; and (iv) the extent to which, if any, economies of scale exist and are realized as the fund grows, and whether any economies of scale are appropriately shared with fund shareholders.In considering whether to renew the Advisory Contracts for the fund, the Board reached a determination, with the assistance of fund counsel and Independent Trustees' counsel and through the exercise of its business judgment, that the renewal of the Advisory Contracts was in the best interests of the fund and its shareholders and that the compensation payable under the Advisory Contracts was fair and reasonable. The Board's decision to renew the Advisory Contracts was not based on any single factor, but rather was based on a comprehensive consideration of all the information provided to the Board at its meetings throughout the year. The Board, in reaching its determination to renew the Advisory Contracts, was aware that shareholders of the fund have a broad range of investment choices available to them, including a wide choice among funds offered by Fidelity's competitors, and that the fund's shareholders, who have the opportunity to review and weigh the disclosure provided by the fund in its prospectus and other public disclosures, have chosen to invest in this fund, which is part of the Fidelity family of funds. Nature, Extent, and Quality of Services Provided. The Board considered Fidelity's staffing as it relates to the fund, including the backgrounds of investment personnel of Fidelity, and also considered the fund's investment objective, strategies, and related investment philosophy. The Independent Trustees also had discussions with senior management of Fidelity's investment operations and investment groups. The Board considered the structure of the investment personnel compensation program and whether this structure provides appropriate incentives to act in the best interests of the fund. Additionally, the Board considered the portfolio managers' investments, if any, in the funds that they manage. Resources Dedicated to Investment Management and Support Services. The Board reviewed the general qualifications and capabilities of Fidelity's investment staff, including its size, education, experience, and resources, as well as Fidelity's approach to recruiting, managing, and compensating investment personnel. The Board noted that Fidelity has continued to increase the resources devoted to non-U.S. offices, including expansion of Fidelity's global investment organization. The Board also noted that Fidelity's analysts have extensive resources, tools and capabilities that allow them to conduct sophisticated quantitative and fundamental analysis, as well as credit analysis of issuers, counterparties and guarantors. Further, the Board considered that Fidelity's investment professionals have sufficient access to global information and data so as to provide competitive investment results over time, and that those professionals also have access to sophisticated tools that permit them to assess portfolio construction and risk and performance attribution characteristics continuously, as well as to transmit new information and research conclusions rapidly around the world. Additionally, in its deliberations, the Board considered Fidelity's trading, risk management, compliance, and technology and operations capabilities and resources, which are integral parts of the investment management process. The Board also considered Fidelity's investments in business continuity planning, and its success in continuously providing services to the fund notwithstanding the severe disruptions caused by the COVID-19 pandemic. Shareholder and Administrative Services. The Board considered (i) the nature, extent, quality, and cost of advisory, administrative, and shareholder services performed by the Investment Advisers and their affiliates under the Advisory Contracts and under separate agreements covering transfer agency and pricing and bookkeeping services for the fund; (ii) the nature and extent of the supervision of third party service providers, principally custodians, subcustodians, and pricing vendors; and (iii) the resources devoted to, and the record of compliance with, the fund's compliance policies and procedures.The Board noted that the growth of fund assets over time across the complex allows Fidelity to reinvest in the development of services designed to enhance the value and convenience of the Fidelity funds as investment vehicles. These services include 24-hour access to account information and market information over the Internet and through telephone representatives, investor education materials and asset allocation tools, and the expanded availability of Fidelity Investor Centers. Investment in a Large Fund Family. The Board considered the benefits to shareholders of investing in a Fidelity fund, including the benefits of investing in a fund that is part of a large family of funds offering a variety of investment disciplines and providing a large variety of mutual fund investor services. The Board noted that Fidelity had taken, or had made recommendations that resulted in the Fidelity funds taking, a number of actions over the previous year that benefited particular funds, including: (i) continuing to dedicate additional resources to Fidelity's investment research process, which includes meetings with management of issuers of securities in which the funds invest, and to the support of the senior management team that oversees asset management; (ii) continuing efforts to enhance Fidelity's global research capabilities; (iii) launching new funds and ETFs with innovative structures, strategies and pricing and making other enhancements to meet client needs; (iv) launching new share classes of existing funds; (v) eliminating purchase minimums and broadening eligibility requirements for certain funds and share classes; (vi) reducing management fees and total expenses for certain target date funds or classes and index funds; (vii) lowering expenses for certain funds and classes by implementing or lowering expense caps; (viii) rationalizing product lines and gaining increased efficiencies from fund mergers, liquidations, and share class consolidations; (ix) continuing to develop, acquire and implement systems and technology to improve services to the funds and shareholders, strengthen information security, and increase efficiency; and (x) continuing to implement enhancements to further strengthen Fidelity's product line to increase investors' probability of success in achieving their investment goals, including retirement income goals. Investment Performance. The Board considered whether the fund has operated in accordance with its investment objective, as well as its record of compliance with its investment restrictions and its performance history.The Board took into account discussions that occur at Board meetings throughout the year with representatives of the Investment Advisers about fund investment performance. In this regard the Board noted that as part of regularly scheduled fund reviews and other reports to the Board on fund performance, the Board considers annualized return information for the fund for different time periods, measured against an appropriate peer group of funds with similar objectives (peer group).In addition to reviewing absolute and relative fund performance, the Independent Trustees periodically consider the appropriateness of fund performance metrics in evaluating the results achieved. In general, the Independent Trustees believe that fund performance should be evaluated based on gross performance (before fees and expenses but after transaction costs) compared to the gross performance of appropriate peer groups, over appropriate time periods that may include full market cycles, taking into account relevant factors including the following: general market conditions; expectations for interest rate levels and credit conditions; issuer-specific information including credit quality; the fund's market value NAV over time and its resilience under various stressed conditions; and fund cash flows and other factors. The Independent Trustees generally give greater weight to fund performance over longer time periods than over shorter time periods.The Board recognizes that in interest rate environments where many competitors waive fees to maintain a minimum yield, relative money market fund performance on a net basis (after fees and expenses) may not be particularly meaningful due to miniscule performance differences among competitor funds. Depending on the circumstances, the Independent Trustees may be satisfied with a fund's performance notwithstanding that it lags its peer group for certain periods.The Independent Trustees recognize that shareholders evaluate performance on a net basis over their own holding periods, for which one-, three-, and five-year periods are often used as a proxy. For this reason, the performance information reviewed by the Board also included net cumulative calendar year total return information for the fund and an appropriate peer group for the most recent one-, three-, and five-year periods. The Independent Trustees recognize that shareholders who are not investing through a tax-advantaged retirement account also consider tax consequences in evaluating performance.Based on its review, the Board concluded that the nature, extent, and quality of services provided to the fund under the Advisory Contracts should continue to benefit the shareholders of the fund. Competitiveness of Management Fee and Total Expense Ratio. The Board considered the fund's management fee and total expense ratio compared to "mapped groups" of competitive funds and classes created for the purpose of facilitating the Trustees' competitive analysis of management fees and total expenses. Fidelity creates "mapped groups" by combining similar Lipper investment objective categories that have comparable investment mandates. Combining Lipper investment objective categories aids the Board's management fee and total expense ratio comparisons by broadening the competitive group used for comparison. Management Fee. The Board considered two proprietary management fee comparisons for the 12-month periods shown in basis points (BP) in the chart below. The group of Lipper funds used by the Board for management fee comparisons is referred to below as the "Total Mapped Group" and is broader than the Lipper peer group used by the Board for performance comparisons. The Total Mapped Group comparison focuses on a fund's standing in terms of gross management fees before expense reimbursements or caps relative to the total universe of funds with comparable investment mandates, regardless of whether their management fee structures also are comparable. Funds with comparable investment mandates offer exposure to similar types of securities. Funds with comparable management fee structures have similar management fee contractual arrangements (e.g., flat rate charged for advisory services, all-inclusive fee rate, etc.). "TMG %" represents the percentage of funds in the Total Mapped Group that had management fees that were lower than the fund's. For example, a hypothetical TMG % of 20% would mean that 80% of the funds in the Total Mapped Group had higher, and 20% had lower, management fees than the fund. The fund's actual TMG %s and the number of funds in the Total Mapped Group are in the chart below. The "Asset-Sized Peer Group" (ASPG) comparison focuses on a fund's standing relative to a subset of non-Fidelity funds within the Total Mapped Group that are similar in size and management fee structure. For example, if a fund is in the first quartile of the ASPG, the fund's management fee ranks in the least expensive or lowest 25% of funds in the ASPG. The ASPG represents at least 15% of the funds in the Total Mapped Group with comparable asset size and management fee structures, subject to a minimum of 50 funds (or all funds in the Total Mapped Group if fewer than 50). Additional information, such as the ASPG quartile in which the fund's management fee rate ranked, is also included in the chart and was considered by the Board. Because the vast majority of competitor funds' management fees do not cover non-management expenses, in prior years, the fund was compared on the basis of a hypothetical "net management fee," which was derived by subtracting payments made by Fidelity for non-management expenses (including transfer agent fees, pricing and bookkeeping fees, and fees paid to non-affiliated custodians) from the fund's all-inclusive fee. Given the fund's competitive management fee rate, Fidelity no longer calculates a hypothetical net management fee for the fund and, as a result, the chart does not include a hypothetical net management fee for periods after 2016.Fidelity Treasury Only Money Market Fund

![]()

TMM-SANN-1220

1.538317.123

Fidelity® Money Market Fund

Semi-Annual Report

October 31, 2020

See the inside front cover for important information about access to your fund’s shareholder reports.

Beginning on January 1, 2021, as permitted by regulations adopted by the Securities and Exchange Commission, paper copies of a fund’s shareholder reports will no longer be sent by mail, unless you specifically request paper copies of the reports from the fund or from your financial intermediary, such as a financial advisor, broker-dealer or bank. Instead, the reports will be made available on a website, and you will be notified by mail each time a report is posted and provided with a website link to access the report.

If you already elected to receive shareholder reports electronically, you will not be affected by this change and you need not take any action. You may elect to receive shareholder reports and other communications from a fund electronically, by contacting your financial intermediary. For Fidelity customers, visit Fidelity's web site or call Fidelity using the contact information listed below.

You may elect to receive all future reports in paper free of charge. If you wish to continue receiving paper copies of your shareholder reports, you may contact your financial intermediary or, if you are a Fidelity customer, visit Fidelity’s website, or call Fidelity at the applicable toll-free number listed below. Your election to receive reports in paper will apply to all funds held with the fund complex/your financial intermediary.

| Account Type | Website | Phone Number |

| Brokerage, Mutual Fund, or Annuity Contracts: | fidelity.com/mailpreferences | 1-800-343-3548 |

| Employer Provided Retirement Accounts: | netbenefits.fidelity.com/preferences (choose 'no' under Required Disclosures to continue to print) | 1-800-343-0860 |

| Advisor Sold Accounts Serviced Through Your Financial Intermediary: | Contact Your Financial Intermediary | Your Financial Intermediary's phone number |

| Advisor Sold Accounts Serviced by Fidelity: | institutional.fidelity.com | 1-877-208-0098 |

Contents

|

Board Approval of Investment Advisory Contracts and Management Fees |

To view a fund's proxy voting guidelines and proxy voting record for the 12-month period ended June 30, visit http://www.fidelity.com/proxyvotingresults or visit the Securities and Exchange Commission's (SEC) web site at http://www.sec.gov.

You may also call 1-800-544-8544 to request a free copy of the proxy voting guidelines.

Standard & Poor's, S&P and S&P 500 are registered service marks of The McGraw-Hill Companies, Inc. and have been licensed for use by Fidelity Distributors Corporation.

Other third-party marks appearing herein are the property of their respective owners.

All other marks appearing herein are registered or unregistered trademarks or service marks of FMR LLC or an affiliated company. © 2020 FMR LLC. All rights reserved.

This report and the financial statements contained herein are submitted for the general information of the shareholders of the Fund. This report is not authorized for distribution to prospective investors in the Fund unless preceded or accompanied by an effective prospectus.

A fund files its complete schedule of portfolio holdings with the SEC for the first and third quarters of each fiscal year on Form N-PORT. Forms N-PORT are available on the SEC’s web site at http://www.sec.gov. A fund's Forms N-PORT may be reviewed and copied at the SEC’s Public Reference Room in Washington, DC. Information regarding the operation of the SEC's Public Reference Room may be obtained by calling 1-800-SEC-0330.

For a complete list of a fund's portfolio holdings, view the most recent holdings listing, semiannual report, or annual report on Fidelity's web site at http://www.fidelity.com, http://www.institutional.fidelity.com, or http://www.401k.com, as applicable.

NOT FDIC INSURED •MAY LOSE VALUE •NO BANK GUARANTEE

Neither the Fund nor Fidelity Distributors Corporation is a bank.

Note to Shareholders:

Early in 2020, the outbreak and spread of a new coronavirus emerged as a public health emergency that had a major influence on financial markets, primarily based on its impact on the global economy and the outlook for corporate earnings. The virus causes a respiratory disease known as COVID-19. On March 11, the World Health Organization declared the COVID-19 outbreak a pandemic, citing sustained risk of further global spread.

In the weeks following, as the crisis worsened, we witnessed an escalating human tragedy with wide-scale social and economic consequences from coronavirus-containment measures. The outbreak of COVID-19 prompted a number of measures to limit the spread, including travel and border restrictions, quarantines, and restrictions on large gatherings. In turn, these resulted in lower consumer activity, diminished demand for a wide range of products and services, disruption in manufacturing and supply chains, and – given the wide variability in outcomes regarding the outbreak – significant market uncertainty and volatility. Amid the turmoil, global governments and central banks took unprecedented action to help support consumers, businesses, and the broader economies, and to limit disruption to financial systems.

The situation continues to unfold, and the extent and duration of its impact on financial markets and the economy remain highly uncertain. Extreme events such as the coronavirus crisis are “exogenous shocks” that can have significant adverse effects on mutual funds and their investments. Although multiple asset classes may be affected by market disruption, the duration and impact may not be the same for all types of assets.

Fidelity is committed to helping you stay informed amid news about COVID-19 and during increased market volatility, and we’re taking extra steps to be responsive to customer needs. We encourage you to visit our websites, where we offer ongoing updates, commentary, and analysis on the markets and our funds.

Investment Summary/Performance (Unaudited)

Effective Maturity Diversification as of October 31, 2020

| Days | % of fund's investments 10/31/20 |

| 1 - 7 | 18.1 |

| 8 - 30 | 18.9 |

| 31 - 60 | 23.4 |

| 61 - 90 | 15.0 |

| 91 - 180 | 24.2 |

| > 180 | 0.4 |

Effective maturity is determined in accordance with the requirements of Rule 2a-7 under the Investment Company Act of 1940.

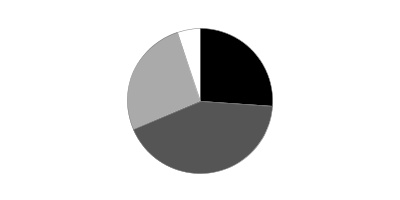

Asset Allocation (% of fund's net assets)

| As of October 31, 2020 | ||

| Certificates of Deposit | 16.5% | |

| Commercial Paper | 28.5% | |

| Variable Rate Demand Notes (VRDNs) | 0.1% | |

| U.S. Treasury Debt | 37.8% | |

| Non-Negotiable Time Deposit | 8.3% | |

| Other Instruments | 0.3% | |

| Interfund Loans | 0.1% | |

| Repurchase Agreements | 8.6% | |

| Net Other Assets (Liabilities)* | (0.2)% | |

* Short-Term Investments and Net Other Assets (Liabilities) are not included in the pie chart

Current 7-Day Yields

| 10/30/20 | |

| Fidelity® Money Market Fund | 0.01% |

| Premium Class | 0.01% |

Yield refers to the income paid by the Fund over a given period. Yield for money market funds is usually for seven-day periods, as it is here, though it is expressed as an annual percentage rate. Past performance is no guarantee of future results. Yield will vary and it's possible to lose money investing in the Fund. A portion of the Fund's expenses was reimbursed and/or waived. Absent such reimbursements and/or waivers the yield for the period ending October 31, 2020, the most recent period shown in the table, would have been (.22)% for Fidelity Money Market Fund Class and (.15)% for Premium Class.

Schedule of Investments October 31, 2020 (Unaudited)

Showing Percentage of Net Assets

| Certificate of Deposit - 16.5% | ||||

| Yield(a) | Principal Amount (000s) | Value (000s) | ||

| New York Branch, Yankee Dollar, Foreign Banks - 16.5% | ||||

| Bank of Montreal | ||||

| 11/17/20 to 5/3/21 | 0.17 to 0.32 (b)% | $1,543,600 | $1,543,600 | |

| Bank of Tokyo-Mitsubishi UFJ Ltd. | ||||

| 11/12/20 to 11/25/20 | 0.23 to 0.25 | 941,000 | 941,000 | |

| Bayerische Landesbank | ||||

| 11/13/20 | 0.20 | 212,000 | 212,000 | |

| Landesbank Baden-Wuerttemberg New York Branch | ||||

| 11/2/20 | 0.21 | 427,000 | 427,000 | |

| Mitsubishi UFJ Trust & Banking Corp. | ||||

| 11/3/20 to 2/2/21 | 0.18 to 0.33 | 268,000 | 268,000 | |

| Mizuho Corporate Bank Ltd. | ||||

| 11/3/20 to 1/21/21 | 0.20 to 0.23 | 1,445,000 | 1,445,001 | |

| Sumitomo Mitsui Banking Corp. | ||||

| 11/9/20 to 2/23/21 | 0.20 to 0.28 (b) | 1,596,000 | 1,596,000 | |

| Sumitomo Mitsui Trust Bank Ltd. | ||||

| 11/13/20 to 12/18/20 | 0.18 to 0.21 | 1,446,000 | 1,446,000 | |

| UBS AG | ||||

| 1/6/21 | 0.23 | 119,000 | 119,287 | |

| TOTAL CERTIFICATE OF DEPOSIT | ||||

| (Cost $7,997,888) | 7,997,888 | |||

| Financial Company Commercial Paper - 28.4% | ||||

| Bank of Nova Scotia | ||||

| 11/13/20 to 2/19/21 | 0.25 to 0.27 (b) | 296,000 | 295,903 | |

| BPCE SA | ||||

| 11/19/20 to 2/8/21 | 0.20 to 0.22 | 1,967,000 | 1,966,334 | |

| Caisse d'Amort de la Dette Sociale | ||||

| 3/4/21 to 3/9/21 | 0.20 to 0.21 (c) | 773,000 | 772,459 | |

| Canadian Imperial Bank of Commerce | ||||

| 3/10/21 | 0.21 | 203,000 | 202,847 | |

| Citigroup Global Markets, Inc. | ||||

| 12/4/20 to 3/1/21 | 0.20 | 854,000 | 853,596 | |

| Credit Suisse AG | ||||

| 2/23/21 to 2/25/21 | 0.22 | 507,000 | 506,644 | |

| Federation des caisses Desjardin | ||||

| 12/21/20 to 4/8/21 | 0.20 to 0.30 | 637,000 | 636,592 | |

| Lloyds Bank PLC | ||||

| 11/16/20 to 11/27/20 | 0.23 | 765,000 | 764,894 | |

| Mitsubishi UFJ Trust & Banking Corp. | ||||

| 11/2/20 to 2/26/21 | 0.18 to 0.23 | 685,819 | 685,507 | |

| Mizuho Bank Ltd. Singapore Branch | ||||

| 11/4/20 to 1/22/21 | 0.22 to 0.25 | 349,000 | 348,933 | |

| Mizuho Corporate Bank Ltd. | ||||

| 1/12/21 | 0.20 | 65,000 | 64,974 | |

| National Bank of Canada | ||||

| 2/9/21 to 4/20/21 | 0.19 to 0.21 | 1,198,000 | 1,197,019 | |

| PSP Capital, Inc. | ||||

| 3/1/21 | 0.20 (c) | 80,000 | 79,947 | |

| Sumitomo Mitsui Banking Corp. | ||||

| 2/1/21 | 0.21 | 76,000 | 75,959 | |

| Sumitomo Mitsui Trust Bank Ltd. | ||||

| 11/5/20 to 2/10/21 | 0.20 to 0.24 | 956,180 | 955,881 | |

| Svenska Handelsbanken AB | ||||

| 3/9/21 to 4/13/21 | 0.20 to 0.21 | 1,012,725 | 1,011,885 | |

| The Toronto-Dominion Bank | ||||

| 11/10/20 to 3/15/21 | 0.20 to 0.26 (b) | 1,914,600 | 1,913,433 | |

| Toyota Motor Credit Corp. | ||||

| 3/18/21 to 3/30/21 | 0.26 | 295,000 | 294,695 | |

| UBS AG London Branch | ||||

| 12/29/20 to 4/21/21 | 0.23 to 0.29 (b) | 1,133,100 | 1,132,406 | |

| TOTAL FINANCIAL COMPANY COMMERCIAL PAPER | ||||

| (Cost $13,759,908) | 13,759,908 | |||

| Asset Backed Commercial Paper - 0.1% | ||||

| Manhattan Asset Funding Co. LLC (Liquidity Facility Sumitomo Mitsui Banking Corp.) | ||||

| 11/30/20 | ||||

| (Cost $44,993) | 0.20 | 45,000 | 44,993 | |

| U.S. Treasury Debt - 37.8% | ||||

| U.S. Treasury Obligations - 37.8% | ||||

| U.S. Treasury Bills | ||||

| 11/3/20 to 2/18/21 | 0.10 to 0.19 | 18,252,085 | 18,249,307 | |

| U.S. Treasury Notes | ||||

| 10/31/21 | 0.40 (b)(d) | 84,000 | 84,016 | |

| TOTAL U.S. TREASURY DEBT | ||||

| (Cost $18,333,323) | 18,333,323 | |||

| Other Instrument - 0.3% | ||||

| Master Notes - 0.3% | ||||

| Toyota Motor Credit Corp. | ||||

| 11/6/20 | ||||

| (Cost $162,000) | 0.34 (b)(d)(e) | 162,000 | 162,000 | |

| Variable Rate Demand Note - 0.1% | ||||

| Florida - 0.1% | ||||

| Florida Timber Fin. III LLC Taxable, LOC Wells Fargo Bank NA, VRDN | ||||

| 11/6/20 | 0.15 (b) | 40,000 | 40,000 | |

| Wisconsin - 0.0% | ||||

| Green Bay Redev. Auth. (Green Bay Packaging, Inc. Proj.) Series 2019, 0.17% 11/6/20, LOC Wells Fargo Bank NA, VRDN | ||||

| 11/6/20 | 0.17 (b)(c)(f) | 15,600 | 15,600 | |

| TOTAL VARIABLE RATE DEMAND NOTE | ||||

| (Cost $55,600) | 55,600 | |||

| Non-Negotiable Time Deposit - 8.3% | ||||

| Time Deposits - 8.3% | ||||

| Barclays Bank PLC | ||||

| 11/2/20 | 0.18 | 2,009,646 | 2,009,646 | |

| Credit Agricole CIB | ||||

| 11/2/20 to 11/5/20 | 0.15 | 1,399,636 | 1,399,636 | |

| Landesbank Hessen-Thuringen London Branch | ||||

| 11/2/20 to 11/5/20 | 0.15 | 635,000 | 635,000 | |

| TOTAL NON-NEGOTIABLE TIME DEPOSIT | ||||

| (Cost $4,044,282) | 4,044,282 | |||

| Interfund Loans - 0.1% | ||||

| With: | ||||

| Fidelity Small Cap Index Fund, at 0.34% due, 11/2/20(g) | 10,577 | 10,577 | ||

| Fidelity Total International Index Fund, at 0.34% due, 11/2/20(g) | 33,621 | 33,621 | ||

| TOTAL INTERFUND LOANS | ||||

| (Cost $44,198) | 44,198 |

| Other Repurchase Agreement - 8.6% | |||

| Maturity Amount (000s) | Value (000s) | ||

| Other Repurchase Agreement - 8.6% | |||

| With: | |||

| BMO Capital Markets Corp. at: | |||

| 0.23%, dated 10/30/20 due 11/2/20 (Collateralized by Corporate Obligations valued at $93,452,601, 0.90% - 6.50%, 6/8/23 - 2/12/67) | $89,002 | $89,000 | |

| 0.33%, dated 10/30/20 due 11/2/20 (Collateralized by Equity Securities valued at $143,644,137) | 133,004 | 133,000 | |

| 0.36%, dated 10/30/20 due 11/2/20 (Collateralized by Corporate Obligations valued at $143,497,543, 3.40% - 10.50%, 11/15/21 - 6/21/29) | 133,004 | 133,000 | |

| BNP Paribas Prime Brokerage, Inc. at: | |||

| 0.38%, dated 10/30/20 due 11/2/20 (Collateralized by Equity Securities valued at $421,213,351) | 390,012 | 390,000 | |

| 0.6%, dated 10/15/20 due 12/4/20 (Collateralized by Equity Securities valued at $233,313,483)(b)(d)(h) | 216,180 | 216,000 | |

| BofA Securities, Inc. at: | |||

| 0.73%, dated 10/19/20 due 2/2/21 (Collateralized by Corporate Obligations valued at $116,673,113, 0.00% - 1.00%, 9/15/24 - 8/15/26) | 108,276 | 108,000 | |

| 0.78%, dated 10/30/20 due 2/2/21 (Collateralized by Corporate Obligations valued at $116,647,582, 0.00% - 1.25%, 12/15/23 - 6/15/25) | 108,421 | 108,000 | |

| Citigroup Global Markets, Inc. at: | |||

| 0.59%, dated 8/11/20 due 12/4/20 (Collateralized by Corporate Obligations valued at $71,434,192, 0.21% - 7.83%, 10/26/22 - 5/11/63)(b)(d)(h) | 66,124 | 66,000 | |

| 0.67%, dated: | |||

| 8/19/20 due 11/17/20 (Collateralized by U.S. Treasury Obligations valued at $45,439,614, 0.13% - 7.00%, 12/31/21 - 2/5/25) | 44,074 | 44,000 | |

| 8/31/20 due 11/30/20 (Collateralized by Corporate Obligations valued at $47,674,192, 0.29% - 5.19%, 10/26/22 - 4/26/50) | 44,075 | 44,000 | |

| 0.71%, dated 9/24/20 due 1/22/21 (Collateralized by Corporate Obligations valued at $94,114,192, 0.00% - 6.28%, 10/26/22 - 10/12/52) | 87,206 | 87,000 | |

| Deutsche Bank AG at 0.58%, dated 10/30/20 due 11/2/20 (Collateralized by Municipal Bond Obligations valued at $228,445,462, 0.50% - 6.25%, 10/1/22 - 7/1/40) | 217,010 | 217,000 | |

| J.P. Morgan Securities, LLC at: | |||

| 0.38%, dated: | |||

| 10/16/20 due 12/4/20 (Collateralized by Equity Securities valued at $233,321,861)(b)(d)(h) | 216,112 | 216,000 | |

| 10/21/20 due 12/4/20 (Collateralized by Corporate Obligations valued at $233,309,549, 0.00% - 5.00%, 6/1/22 - 8/15/28)(b)(d)(h) | 216,100 | 216,000 | |

| 0.43%, dated: | |||

| 10/16/20 due 12/4/20 (Collateralized by Corporate Obligations valued at $256,422,288, 0.00% - 6.75%, 9/15/21 - 5/15/38)(b)(d)(h) | 238,139 | 238,000 | |

| 10/21/20 due 12/4/20 (Collateralized by Corporate Obligations valued at $226,832,508, 0.00% - 9.38%, 12/14/20 - 8/1/2116)(b)(d)(h) | 216,100 | 216,000 | |

| Mitsubishi UFJ Securities (U.S.A.), Inc. at: | |||

| 0.33%, dated 10/30/20 due 11/2/20 (Collateralized by Equity Securities valued at $82,082,266) | 76,002 | 76,000 | |

| 0.35%, dated 10/27/20 due 11/3/20 (Collateralized by Equity Securities valued at $10,800,638) | 10,001 | 10,000 | |

| 0.6%, dated 10/30/20 due 11/2/20 (Collateralized by Corporate Obligations valued at $9,720,486, 4.00%, 10/15/24) | 9,000 | 9,000 | |

| Mizuho Securities U.S.A., Inc. at 0.47%, dated 10/30/20 due 11/2/20 (Collateralized by Equity Securities valued at $140,325,718) | 130,005 | 130,000 | |

| RBS Securities, Inc. at 0.35%, dated 10/30/20 due 11/2/20 (Collateralized by U.S. Treasury Obligations valued at $111,243,440, 1.38% - 3.63%, 1/15/26 - 2/15/44) | 108,003 | 108,000 | |

| Societe Generale at: | |||

| 0.31%, dated 10/30/20 due 11/2/20 (Collateralized by Corporate Obligations valued at $421,210,881, 0.00% - 13.00%, 2/1/21 - 3/15/43) | 390,010 | 390,000 | |

| 0.33%, dated 10/27/20 due 11/3/20 (Collateralized by Corporate Obligations valued at $140,407,722, 0.00% - 12.50%, 1/26/21 - 2/15/44) | 130,008 | 130,000 | |

| 0.45%, dated 10/30/20 due 11/2/20 (Collateralized by Corporate Obligations valued at $186,789,551, 0.25% - 13.00%, 1/7/21 - 3/26/79) | 173,006 | 173,000 | |

| 0.46%, dated 10/27/20 due 11/3/20 (Collateralized by Corporate Obligations valued at $46,440,924, 0.28% - 11.50%, 11/10/21 - 2/15/51) | 43,004 | 43,000 | |

| Wells Fargo Securities, LLC at: | |||

| 0.48%, dated 10/30/20 due 11/2/20 (Collateralized by Corporate Obligations valued at $46,441,858, 1.75% - 3.50%, 12/1/22 - 7/1/23) | 43,002 | 43,000 | |

| 0.51%, dated: | |||

| 10/29/20 due 11/5/20 (Collateralized by Corporate Obligations valued at $140,407,958, 0.00% - 4.00%, 6/15/21 - 2/15/37) | 130,013 | 130,000 | |

| 10/30/20 due 11/6/20 (Collateralized by Corporate Obligations valued at $46,441,975, 0.00% - 4.25%, 10/1/24 - 9/1/26) | 43,004 | 43,000 | |

| 0.6%, dated 10/23/20 due 11/20/20 (Collateralized by Corporate Obligations valued at $140,423,401, 0.00% - 4.00%, 12/1/24 - 5/1/27) | 130,061 | 130,000 | |

| 0.8%, dated 9/10/20 due 12/9/20 (Collateralized by Corporate Obligations valued at $141,646,633, 0.13% - 5.00%, 1/30/23 - 5/15/30) | 131,262 | 131,000 | |

| 0.91%, dated 8/12/20 due 11/12/20 (Collateralized by Corporate Obligations valued at $119,046,247, 5.75%, 4/1/23) | 110,256 | 110,000 | |

| TOTAL OTHER REPURCHASE AGREEMENT | |||

| (Cost $4,177,000) | 4,177,000 | ||

| TOTAL INVESTMENT IN SECURITIES - 100.2% | |||

| (Cost $48,619,192) | 48,619,192 | ||

| NET OTHER ASSETS (LIABILITIES) - (0.2)% | (95,370) | ||

| NET ASSETS - 100% | $48,523,822 |

Security Type Abbreviations

VRDN – VARIABLE RATE DEMAND NOTE (A debt instrument that is payable upon demand, either daily, weekly or monthly)

The date shown for securities represents the date when principal payments must be paid, taking into account any call options exercised by the issuer and any permissible maturity shortening features other than interest rate resets.

Legend

(a) Yield represents either the annualized yield at the date of purchase, or the stated coupon rate, or, for floating and adjustable rate securities, the rate at period end.

(b) Coupon rates for floating and adjustable rate securities reflect the rates in effect at period end.

(c) Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be resold in transactions exempt from registration, normally to qualified institutional buyers. At the end of the period, the value of these securities amounted to $868,006,000 or 1.8% of net assets.

(d) Coupon is indexed to a floating interest rate which may be multiplied by a specified factor and/or subject to caps or floors.

(e) Restricted securities (including private placements) - Investment in securities not registered under the Securities Act of 1933 (excluding 144A issues). At the end of the period, the value of restricted securities (excluding 144A issues) amounted to $162,000,000 or 0.3% of net assets.

(f) Private activity obligations whose interest is subject to the federal alternative minimum tax for individuals.

(g) Loan is with an affiliated fund.

(h) The maturity amount is based on the rate at period end.

Additional information on each restricted holding is as follows:

| Security | Acquisition Date | Cost |

| Toyota Motor Credit Corp. 0.34%, 11/6/20 | 3/2/20 | $162,000,000 |

Investment Valuation

All investments are categorized as Level 2 under the Fair Value Hierarchy. The inputs or methodology used for valuing securities may not be an indication of the risk associated with investing in those securities. For more information on valuation inputs please refer to the Investment Valuation section in the accompanying Notes to Financial Statements.

See accompanying notes which are an integral part of the financial statements.

Financial Statements

Statement of Assets and Liabilities

| Amounts in thousands (except per-share amounts) | October 31, 2020 (Unaudited) | |

| Assets | ||

| Investment in securities, at value (including repurchase agreements of $4,177,000) — See accompanying schedule: Unaffiliated issuers (cost $48,574,994) | $48,574,994 | |

| Affiliated issuers (cost $44,198) | 44,198 | |

| Total Investment in Securities (cost $48,619,192) | $48,619,192 | |

| Receivable for fund shares sold | 52,777 | |

| Interest receivable | 5,620 | |

| Prepaid expenses | 80 | |

| Receivable from investment adviser for expense reductions | 1,796 | |

| Other receivables | 263 | |

| Total assets | 48,679,728 | |

| Liabilities | ||

| Payable for fund shares redeemed | 145,801 | |

| Distributions payable | 32 | |

| Accrued management fee | 9,278 | |

| Other affiliated payables | 342 | |

| Other payables and accrued expenses | 453 | |

| Total liabilities | 155,906 | |

| Net Assets | $48,523,822 | |

| Net Assets consist of: | ||

| Paid in capital | $48,523,641 | |

| Total accumulated earnings (loss) | 181 | |

| Net Assets | $48,523,822 | |

| Net Asset Value and Maximum Offering Price | ||

| Fidelity Money Market Fund: | ||

| Net Asset Value, offering price and redemption price per share ($5,238,028 ÷ 5,237,906 shares) | $1.00 | |

| Premium Class: | ||

| Net Asset Value, offering price and redemption price per share ($43,285,794 ÷ 43,282,913 shares) | $1.00 |

See accompanying notes which are an integral part of the financial statements.

Statement of Operations

| Amounts in thousands | Six months ended October 31, 2020 (Unaudited) | |

| Investment Income | ||

| Interest (including $60 from affiliated interfund lending) | $91,756 | |

| Expenses | ||

| Management fee | $66,293 | |

| Transfer agent fees | 28,412 | |

| Accounting fees and expenses | 983 | |

| Custodian fees and expenses | 228 | |

| Independent trustees' fees and expenses | 84 | |

| Registration fees | 400 | |

| Audit | 23 | |

| Legal | 18 | |

| Miscellaneous | 99 | |

| Total expenses before reductions | 96,540 | |

| Expense reductions | (25,609) | |

| Total expenses after reductions | 70,931 | |

| Net investment income (loss) | 20,825 | |

| Realized and Unrealized Gain (Loss) | ||

| Net realized gain (loss) on: | ||

| Investment securities: | ||

| Unaffiliated issuers | 1 | |

| Total net realized gain (loss) | 1 | |

| Net increase in net assets resulting from operations | $20,826 |

See accompanying notes which are an integral part of the financial statements.

Statement of Changes in Net Assets

| Amounts in thousands | Six months ended October 31, 2020 (Unaudited) | Year ended April 30, 2020 |

| Increase (Decrease) in Net Assets | ||

| Operations | ||

| Net investment income (loss) | $20,825 | $834,183 |

| Net realized gain (loss) | 1 | 79 |

| Net increase in net assets resulting from operations | 20,826 | 834,262 |

| Distributions to shareholders | (20,827) | (834,183) |

| Share transactions - net increase (decrease) | (6,139,191) | 12,485,517 |

| Total increase (decrease) in net assets | (6,139,192) | 12,485,596 |

| Net Assets | ||

| Beginning of period | 54,663,014 | 42,177,418 |

| End of period | $48,523,822 | $54,663,014 |

See accompanying notes which are an integral part of the financial statements.

Financial Highlights

Fidelity Money Market Fund

| Six months ended (Unaudited) October 31, | Years endedApril 30, | |||||

| 2020 | 2020 | 2019 | 2018 | 2017 | 2016 | |

| Selected Per–Share Data | ||||||

| Net asset value, beginning of period | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 |

| Income from Investment Operations | ||||||

| Net investment income (loss) | –A | .016 | .020 | .011 | .005 | .001 |

| Net realized and unrealized gain (loss)A | – | – | – | – | – | – |

| Total from investment operations | –A | .016 | .020 | .011 | .005 | .001 |

| Distributions from net investment income | –A | (.016) | (.020) | (.011) | (.005) | (.001) |

| Total distributions | –A | (.016) | (.020) | (.011) | (.005) | (.001) |

| Net asset value, end of period | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 |

| Total ReturnB,C | .02% | 1.61% | 2.03% | 1.11% | .52% | .09% |

| Ratios to Average Net AssetsD | ||||||

| Expenses before reductions | .42%E | .42% | .42% | .42% | .42% | .42% |

| Expenses net of fee waivers, if any | .31%E | .42% | .42% | .42% | .42% | .36% |

| Expenses net of all reductions | .31%E | .42% | .42% | .42% | .42% | .36% |

| Net investment income (loss) | .04%E | 1.56% | 2.06% | 1.15% | .55% | .15% |

| Supplemental Data | ||||||

| Net assets, end of period (in millions) | $5,238 | $6,093 | $5,196 | $3,209 | $2,301 | $2,126 |

A Amount represents less than $.0005 per share.

B Total returns for periods of less than one year are not annualized.

C Total returns would have been lower if certain expenses had not been reduced during the applicable periods shown.

D Expense ratios reflect operating expenses of the class. Expenses before reductions do not reflect amounts reimbursed, waived, or reduced through arrangements with the investment adviser, brokerage services, or other offset arrangements, if applicable, and do not represent the amount paid by the class during periods when reimbursements, waivers or reductions occur.

E Annualized

See accompanying notes which are an integral part of the financial statements.

Fidelity Money Market Fund Premium Class

| Six months ended (Unaudited) October 31, | Years endedApril 30, | |||||

| 2020 | 2020 | 2019 | 2018 | 2017 | 2016 | |

| Selected Per–Share Data | ||||||

| Net asset value, beginning of period | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 |

| Income from Investment Operations | ||||||

| Net investment income (loss) | –A | .017 | .021 | .012 | .006 | .002 |

| Net realized and unrealized gain (loss)A | – | – | – | – | – | – |

| Total from investment operations | –A | .017 | .021 | .012 | .006 | .002 |

| Distributions from net investment income | –A | (.017) | (.021) | (.012) | (.006) | (.002) |

| Total distributions | –A | (.017) | (.021) | (.012) | (.006) | (.002) |

| Net asset value, end of period | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 | $1.00 |

| Total ReturnB,C | .04% | 1.73% | 2.16% | 1.23% | .64% | .15% |

| Ratios to Average Net AssetsD | ||||||

| Expenses before reductions | .35%E | .36% | .37% | .37% | .37% | .37% |

| Expenses net of fee waivers, if any | .26%E | .30% | .30% | .30% | .30% | .30% |

| Expenses net of all reductions | .26%E | .30% | .30% | .30% | .30% | .30% |

| Net investment income (loss) | .08%E | 1.68% | 2.18% | 1.27% | .67% | .20% |

| Supplemental Data | ||||||

| Net assets, end of period (in millions) | $43,286 | $48,570 | $36,981 | $15,497 | $7,317 | $3,706 |

A Amount represents less than $.0005 per share.

B Total returns for periods of less than one year are not annualized.

C Total returns would have been lower if certain expenses had not been reduced during the applicable periods shown.

D Expense ratios reflect operating expenses of the class. Expenses before reductions do not reflect amounts reimbursed, waived, or reduced through arrangements with the investment adviser, brokerage services, or other offset arrangements, if applicable, and do not represent the amount paid by the class during periods when reimbursements, waivers or reductions occur.

E Annualized

See accompanying notes which are an integral part of the financial statements.

Notes to Financial Statements (Unaudited)

For the period ended October 31, 2020

(Amounts in thousands except percentages)

1. Organization.

Fidelity Money Market Fund (the Fund) is a fund of Fidelity Hereford Street Trust (the Trust) and is authorized to issue an unlimited number of shares. The Trust is registered under the Investment Company Act of 1940, as amended (the 1940 Act), as an open-end management investment company organized as a Delaware statutory trust. The Fund offers Fidelity Money Market Fund and Premium Class shares, each of which has equal rights as to assets and voting privileges. Each class has exclusive voting rights with respect to matters that affect that class. Shares of the Fund are only available for purchase by retail shareholders.

2. Significant Accounting Policies.

The Fund is an investment company and applies the accounting and reporting guidance of the Financial Accounting Standards Board (FASB) Accounting Standards Codification Topic 946 Financial Services – Investment Companies. The financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America (GAAP), which require management to make certain estimates and assumptions at the date of the financial statements. Actual results could differ from those estimates. Subsequent events, if any, through the date that the financial statements were issued have been evaluated in the preparation of the financial statements. The following summarizes the significant accounting policies of the Fund:

Investment Valuation. The Fund categorizes the inputs to valuation techniques used to value its investments into a disclosure hierarchy consisting of three levels as shown below:

- Level 1 – quoted prices in active markets for identical investments

- Level 2 – other significant observable inputs (including quoted prices for similar investments, interest rates, prepayment speeds, etc.)

- Level 3 – unobservable inputs (including the Fund's own assumptions based on the best information available)

As permitted by compliance with certain conditions under Rule 2a-7 of the 1940 Act, securities are valued at amortized cost, which approximates fair value. The amortized cost of an instrument is determined by valuing it at its original cost and thereafter amortizing any discount or premium from its face value at a constant rate until maturity. Securities held by a money market fund are generally high quality and liquid; however, they are reflected as Level 2 because the inputs used to determine fair value are not quoted prices in an active market.

Investment Transactions and Income. The net asset value per share for processing shareholder transactions is calculated as of the close of business of the New York Stock Exchange (NYSE), normally 4:00 p.m. Eastern time. Security transactions are accounted for as of trade date. Gains and losses on securities sold are determined on the basis of identified cost and include proceeds received from litigation. Interest income is accrued as earned and includes coupon interest and amortization of premium and accretion of discount on debt securities as applicable. The principal amount on inflation-indexed securities is periodically adjusted to the rate of inflation and interest is accrued based on the principal amount. The adjustments to principal due to inflation are reflected as increases or decreases to Interest in the accompanying Statement of Operations.

Class Allocations and Expenses. Investment income, realized and unrealized capital gains and losses, common expenses of the Fund, and certain fund-level expense reductions, if any, are allocated daily on a pro-rata basis to each class based on the relative net assets of each class to the total net assets of the Fund. Each class differs with respect to transfer agent fees incurred. Certain expense reductions may also differ by class. For the reporting period, the allocated portion of income and expenses to each class as a percent of its average net assets may vary due to the timing of recording these transactions in relation to fluctuating net assets of the classes. Expenses directly attributable to a fund are charged to that fund. Expenses attributable to more than one fund are allocated among the respective funds on the basis of relative net assets or other appropriate methods. Expense estimates are accrued in the period to which they relate and adjustments are made when actual amounts are known.

Deferred Trustee Compensation. Under a Deferred Compensation Plan (the Plan) for the Fund, certain independent Trustees have elected to defer receipt of a portion of their annual compensation. Deferred amounts are invested in a cross-section of Fidelity funds, are marked-to-market and remain in the Fund until distributed in accordance with the Plan. The investment of deferred amounts and the offsetting payable to the Trustees of $262 are included in the accompanying Statement of Assets and Liabilities in other receivables and other payables and accrued expenses, respectively.

Income Tax Information and Distributions to Shareholders. Each year, the Fund intends to qualify as a regulated investment company under Subchapter M of the Internal Revenue Code, including distributing substantially all of its taxable income and realized gains. As a result, no provision for U.S. Federal income taxes is required. The Fund files a U.S. federal tax return, in addition to state and local tax returns as required. The Fund's federal income tax returns are subject to examination by the Internal Revenue Service (IRS) for a period of three fiscal years after they are filed. State and local tax returns may be subject to examination for an additional fiscal year depending on the jurisdiction.

Distributions are declared and recorded daily and paid monthly from net investment income. Distributions from realized gains, if any, are declared and recorded on the ex-dividend date. Income and capital gain distributions are declared separately for each class. Income and capital gain distributions are determined in accordance with income tax regulations, which may differ from GAAP.

Capital accounts within the financial statements are adjusted for permanent book-tax differences. These adjustments have no impact on net assets or the results of operations. Capital accounts are not adjusted for temporary book-tax differences which will reverse in a subsequent period.

Book-tax differences are primarily due to deferred trustees compensation.

As of period end, the cost and unrealized appreciation (depreciation) in securities for federal income tax purposes were as follows:

| Gross unrealized appreciation | $– |

| Gross unrealized depreciation | – |

| Net unrealized appreciation (depreciation) | $– |

| Tax cost | $48,619,192 |