UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM

(Mark One)

or

For the transition period from to

Commission file number

|

(Exact name of registrant as specified in charter) |

| ||

(State or other jurisdiction of incorporation or organization) |

| (I.R.S. Employer Identification No.) |

|

|

|

| ||

(Address of principal executive offices) |

| (Zip Code) |

Registrant's telephone number, including area code (

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | Trading symbol | Name of exchange on which registered |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

YES ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company" and “emerging growth company” in Rule 12b-2 of the Exchange Act:

Large accelerated filer | ☐ | ☒ | |

Accelerated filer | ☐ | Smaller reporting company | |

|

| Emerging growth company |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

YES

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

YES

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report.

YES ☐ NO ☒

The aggregate market value of the voting and non-voting common stock held by non-affiliates of the registrant as of the last business day of the registrant's most recently completed second fiscal quarter, based upon the closing sale price of the registrant's common stock on June 30, 2022 as reported on NYSE American, was approximately $

There were

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the definitive Proxy Statement for the Registrant’s Annual Meeting of Shareholders, which is expected to be filed by April 30, 2023, have been incorporated by reference into Part III of this Annual Report on Form 10-K.

TABLE OF CONTENTS

| 2 |

| Table of Contents |

PART I

This Annual Report on Form 10-K contains statements that constitute "forward-looking statements" within the meaning of section 27A of the Securities Act of 1933 and section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). These statements can be identified by the fact that they do not relate strictly to historical information and include the words "expects", "believes", "anticipates", "plans", "may", "will", "intend", "estimate", "continue" or other similar expressions. These forward-looking statements are subject to various risks and uncertainties that could cause actual results to differ materially from those currently anticipated. These risks and uncertainties include, but are not limited to, items discussed below in Item 1A "Risk Factors" in this Annual Report on Form 10-K. Forward-looking statements speak only as of the date made. We undertake no obligation to publicly release or update forward-looking statements, whether as a result of new information, future events or otherwise. You are, however, advised to consult any further disclosures we make on related subjects in our quarterly reports on Form 10-Q and any current reports made on Form 8-K to the United States Securities and Exchange Commission (the "SEC").

Item 1. Business

Business and Company Formation

Solitario Zinc Corp. (“Solitario” or the “Company”) is an exploration stage company as defined by rules issued by the SEC. Solitario was incorporated in the State of Colorado on November 15, 1984 as a wholly owned subsidiary of Crown Resources Corporation ("Crown"). In July 1994, Solitario became a publicly traded company on the Toronto Stock Exchange (the "TSX") through its initial public offering. Solitario has been actively involved in mineral exploration since 1993. Solitario’s primary business is to acquire exploration mineral properties and/or discover economic deposits on its mineral properties and advance these deposits, either on its own or through joint ventures, up to the development stage of the project. At that point, or sometime prior to that point, Solitario would likely attempt to sell its mineral properties, pursue their development either on its own or through a joint venture with a partner that has expertise in mining operations, or create a royalty with a third party that continues to advance the property. Solitario has never developed a property. Solitario’s primary focus is on the acquisition and exploration of precious metal, zinc and other base metal exploration mineral properties. In addition to focusing on its mineral exploration properties and the evaluation of mineral properties for acquisition, Solitario also evaluates potential strategic transactions as a means to acquire an interest in new precious and base metal properties and assets with exploration potential or other potential corporate transactions that Solitario determines to be favorable to Solitario.

Solitario has recorded revenue in the past from the sale of mineral properties, including the sale of certain mineral royalties. Revenues and / or proceeds from the sale or joint venture of properties or assets, although significant when they occur, have not been a consistent annual source of cash and would only occur in the future, if at all, on an infrequent basis.

Solitario currently considers its Golden Crest project in South Dakota, its carried interest in the Florida Canyon project in Peru, and its interest in the Lik project in Alaska to be its core mineral property assets. Nexa Resources, Ltd. (“Nexa”), Solitario’s joint venture partner at Florida Canyon, is continuing the furtherance of the Florida Canyon project and Solitario is monitoring the progress at Florida Canyon. Solitario is working with its 50% joint venture partner, Teck American Inc., a wholly owned subsidiary of Teck Resources Limited (both companies are referred to in this Annual Report as “Teck”) at its Lik project. Teck completed a drilling program and conducted mapping and ground gravity geophysical activities at the Lik project during 2022. Solitario is conducting mineral exploration on its Golden Crest project on its own.

As of December 31, 2022, Solitario anticipates using its cash and short-term investments, in part, to further fund the exploration of its Golden Crest, Florida Canyon, and Lik projects and to potentially acquire additional mineral property assets. The fluctuations in precious metal and other commodity prices contribute to a challenging environment for mineral exploration and development, which has created opportunities as well as challenges for the potential acquisition of early-stage and advanced mineral exploration projects or other related assets on potentially attractive terms.

Human Capital Management

As of December 31, 2022, Solitario had three full-time employees and three part-time seasonal employees. In addition, we use consultants and contractors with specific skills to assist with exploration activities, administration, due diligence, environmental and regulatory compliance, corporate governance, and asset and operations management.

Our compensation programs are designed to align compensation of our employees with Solitario’s corporate objectives and performance and are designed to provide incentives to attract, retain and motivate our employees and contractors to achieve their highest potential over both the short-term and long-term.

| 3 |

| Table of Contents |

The health and safety of our employees and others is a priority in how we manage and operate our business. Overall oversite of the operations is the responsibility of Solitario’s Chief Executive Officer and the Board of Directors. Officers and employees are required to review Solitario’s Code of Business Conduct and Ethics and acknowledge their understanding of the content and intent to comply on a periodic basis.

Solitario values the diversity and talents of its employees working together to achieve corporate goals and personal and professional goals and objectives. We seek to cultivate a culture that is sensitive to the importance of diversity and inclusion in the workplace and are committed to continuous improvement in these areas.

Environmental, Social and Governance

Solitario has a long history of committed environmental, social and responsible governance (“ESG”) of its business. ESG issues are important to Solitario’s investors, employees, and stakeholders, including communities in which we work. Solitario pledges to operate our business in a manner that supports environmental and social initiatives and responsible corporate governance. We work closely with our employees, government agencies, local communities and other stakeholders in the areas where we operate to include their interests and concerns to arrive at environmentally sound and socially responsible outcomes related to all of our operations. We believe our joint venture partners not only value the importance of ESG issues in the conduct of their activities on our projects but are also industry leaders on these important issues.

Risks and Uncertainties

Solitario faces risks related to health epidemics and other outbreaks of communicable diseases, which could significantly disrupt its operations and may materially and adversely affect its business and financial conditions.

Solitario’s business could be adversely impacted by the on-going effects of the coronavirus (“COVID-19”) or other epidemics or pandemics. Solitario continues to evaluate the effects of COVID-19 on its operations and at times during the pandemic took pro-active steps to address the impacts on its operations, including at times reducing costs, in response to the economic uncertainty associated with potential risks from COVID-19. These prior cost reductions included implementing salary reductions and evaluating and reducing certain planned 2021 exploration programs through our joint venture partners at the Florida Canyon and Lik exploration projects. Certain of Solitario’s joint venture partners have, from time to time, modified plans with respect to the projects in which Solitario holds an interest in response to the COVID-19 pandemic. Also, Solitario has evaluated the potential impacts on its ability to access future traditional funding sources on the same or reasonably similar terms as in past periods. Solitario will continue to monitor the effects of COVID-19 on its operations, financial condition, and liquidity. However, the extent to which the COVID-19 pandemic or other epidemics or pandemics ultimately impacts Solitario’s business, including our exploration and other activities and the market for our securities, will depend on future developments, which are highly uncertain and cannot be predicted at this time, and include the duration, severity and scope of new outbreaks and governmental actions taken to contain or treat any such outbreak.

Corporate Structure

Solitario Zinc Corp. [Colorado]

- Golden Crest Project [South Dakota]

- Zazu Metals Corporation. [Canada] (100%)

- Zazu Metals (AK) Corp. [Alaska] (100%)

- Lik Project (50%)

- Minera Chambara, S.A. [Peru] (85%)

- Chambara Project

- Minera Solitario Peru, S.A. [Peru] (100%)

- Minera Bongará, S.A. [Peru] (39%)

- Florida Canyon Project

- Minera Soloco, S.A. [Peru] (100%)

Mineral Exploration Properties

We hold a 50% operating interest in the Lik zinc-lead-silver property in northwest Alaska, which is estimated to contain a large tonnage, high-grade deposit potentially mineable by open-pit methods. Teck is a 50% partner with Solitario in the Lik deposit, with Teck acting as the project manager from 2018 through 2023. In late 2021 Solitario engaged Gustavson & Associates to complete a S-K 1300 Technical Report Summary on the Lik project (the “S-K 1300 Lik TRS”) which was completed in March 2022. A Preliminary Economic Assessment (“PEA”) was completed on the Lik deposit in 2014.

| 4 |

| Table of Contents |

Solitario also has a 39% interest in the advanced, high-grade, Florida Canyon zinc project located in northern Peru. The project has a significant mineral resource and Solitario is fully carried to production by its joint venture partner Nexa, formerly Votorantim Metais Holdings, SA (“Votorantim”) and Compañía Minera Milpo S.A.A. (“Milpo”). Nexa is one of the largest zinc producers in Peru. In late 2021 Solitario engaged Gustavson & Associates to complete a S-K 1300 Technical Report Summary on the Florida Canyon Project (the “S-K 1300 Florida Canyon TRS”)which was completed in March 2022. Solitario and Nexa completed a PEA on the Florida Canyon deposit in August 2017. Except for the 2018-2019 drilling program for which Solitario voluntarily funded $1,580,000 of the 39-hole 17,033-meter drilling program, Nexa has funded 100% of project expenditures since the inception of the Florida Canyon joint venture in 2006. Nexa will increase its ownership to a 70% interest in the project from its current ownership of 61%, by continuing to solely fund all project expenditures and committing to place the project into production based upon a positive feasibility study. After earning 70%, and at the request of Solitario, in the event Nexa makes the decision to develop the Florida Canyon project, Nexa has agreed to finance Solitario's 30% participating interest for any development costs through a future loan facility to Solitario. Solitario would then repay the loan facility through 50% of its net cash flow distributions from the project.

During 2021 Solitario entered into a lease agreement (the “Golden Crest Agreement”) whereby Solitario acquired exclusive exploration rights in certain claims (the “GC Claims”) in the Black Hills region of South Dakota. The GC Claims are part of Solitario’s Golden Crest project. Terms of the Golden Crest Agreement include scheduled payments by Solitario to the underlying owner of $65,000 (paid upon signing) and an obligation to pay the underlying owner $60,000 at the first anniversary date which was paid in June 2022. Solitario recorded an initial acquisition cost of $125,000 during 2021 related to these required payments. In addition, to continue the lease, Solitario has agreed to pay, at its option, the underlying owner escalating annual payments that over five years total $340,000 and annual payments of $150,000 thereafter, which will be expensed as paid. Solitario has agreed to pay the underlying owner an additional success fee of $1.00 per ounce of gold in the event Solitario files a 43-101 qualified resource of up to 1.5 million ounces of gold or a maximum of $1,500,000. Solitario has agreed to escalating work commitments, at Solitario’s option, on the GC Claims and a related area of interest around the GC Claims totaling $3,000,000 during the first five years of the lease, with the first-year minimum expenditures totaling $200,000 ending June 2022. Solitario has exceeded the minimum exploration expenditures required in 2022. The term of the Golden Crest Agreement is for twenty years and is automatically extended as long as Solitario is performing any exploration, development or mining activities on the GC Claims. The underlying owner retained a 2.0% Net Smelter Return royalty. Solitario will have the option, but not the obligation, to reduce the Net Smelter Return royalty to 1.0% by paying the owner $1,000,000.

In addition, Solitario staked additional mineral claims, including some claims included in the area of interest of the GC Claims and claims not related to the GC Claims, as part of the Golden Crest project. As of December 31, 2022, Solitario has incurred costs for staking, filing fees, legal and other costs totaling $1,035,000 capitalized as initial acquisition costs related to claims on the Golden Crest project.

At December 31, 2022, Solitario also holds an 85% interest in the Chambara exploration project in Peru. Nexa holds the remaining 15%.

We conduct exploration and property evaluation activities in Peru and in the United States in Alaska and South Dakota either on our own using contract geologists, or through joint ventures operated by our partners.

Our exploration activities and those of our joint venture partners are carried out on a property-by-property basis. These activities may include prospecting, geologic mapping, sampling, geophysics and drilling. When we determine that this work indicates a project may not be economically feasible or contain sufficient geologic or economic potential, we may impair or completely write-off the property. A significant factor in the success or failure of our activities is the price of commodities. For example, when the price of zinc or other commodities is down, we may determine that the value of our mineral exploration properties decreases; however, during such down markets it may also become easier and less expensive to locate and acquire new mineral exploration properties.

We have recorded revenue in the past from the sale of mineral properties and assets, joint venture property payments and the sale of royalties. Proceeds from the sale or joint venture of properties and royalty sales, although potentially significant when they occur, have not been a consistent source of cash and may only occur in the future, if at all, on an infrequent basis. Accordingly, while we conduct exploration activities on our projects, we need to maintain and replenish our capital resources. Historically, we have met our need for capital through (i) the sale of our investments in, and interest on, our short-term treasury notes and bank certificates of deposit (“CDs”); (ii) issuances of common stock; (iii) sales of our shares of common stock of Vendetta Mining Corp. (“Vendetta”), Vox Royalty Corp. (“Vox”) and Kinross Gold Corporation (“Kinross”); (iv) sales of covered call options on common stock of Kinross we hold; and (v) sale of mineral property interests and assets. In certain cases, we have reduced our exposure to the costs of our exploration activities through the use of joint ventures.

| 5 |

| Table of Contents |

We operate in one segment: mineral exploration. We currently conduct exploration activities in Peru, Alaska and South Dakota and evaluate properties for potential acquisition and evaluation of strategic corporate opportunities throughout North and South America. As of March 15, 2023, we had three full-time employees located in the United States and no full-time employees outside of the United States. We utilize contract managers, geologists, administrators and part-time laborers to execute our Latin American and North American project work and acquisition evaluations.

A large number of companies are engaged in the acquisition, exploration and development of mineral properties, many of which have substantially greater technical and financial resources than we have and, accordingly, we may be at a disadvantage in being able to compete effectively for the acquisition, exploration and development of mineral properties. We are not aware of any single competitor or group of competitors that dominate the exploration and development of mineral properties. In acquiring mineral properties for exploration and development, we rely on the experience, technical expertise and knowledge of our employees, contractors and advisors, which is limited by the size of our company compared to many of our competitors who may have greater resources, including more employees or employees with more specialized knowledge and experience.

Governmental Regulations

Mineral development and exploration activities are subject to various national, state/provincial, and local laws and regulations, which govern prospecting, development, mining, production, exports, taxes, labor standards, occupational health, waste disposal, protection of the environment, mine safety, hazardous substances and other matters. Similarly, if any of our properties are developed and/or mined those activities are also subject to significant governmental regulation and oversight. We are required to obtain licenses, permits and other authorizations in order to conduct our exploration programs.

Environmental Regulations

Our current and planned activities are subject to various national and local laws and regulations governing protection of the environment. These laws are continually changing and, in general, are becoming more restrictive. We are required to conduct our operations in compliance with applicable laws and regulations. Changes to current local, state or federal laws and regulations in each jurisdiction in which we conduct our exploration activities could, in the future, require additional capital expenditures and increased operating and/or reclamation costs. We have reviewed and considered current federal legislation relating to climate change and do not believe it to currently have a material effect on our operations. Future changes in U.S. federal or state laws or regulations could have a material adverse effect upon us and our results of operations. Although we are unable to predict what additional legislation, if any, might be proposed or enacted, additional regulatory requirements could impact the economics of our projects. During 2022, we had no material environmental incidents or known non-compliance with any applicable environmental regulations.

Financial Information about Geographic Areas

Included in the consolidated balance sheets at December 31, 2022 and 2021, are total assets of $31,000 and $19,000, respectively, related to Solitario's operations located outside of the United States.

Available Information

We file our Annual Report on Form 10-K, our quarterly reports on Form 10-Q, current reports on Form 8-K, and any amendments to those reports electronically with the SEC. The SEC maintains a website (http://www.sec.gov) that contains periodic reports, proxy and information statements and other information regarding registrants, including the Company, that file electronically with the SEC.

Paper copies of our Annual Report to Shareholders, our Annual Report on Form 10-K, our quarterly reports on Form 10-Q, current reports on Form 8-K, and any amendments to those reports are available free of charge by writing to Solitario at its address on the front of this Annual Report on Form 10-K. In addition, electronic versions of the reports we file with the SEC are available on our website, www.solitarioxr.com, as soon as practicable, after filing with the SEC.

Item 1A. Risk Factors

In addition to considering the other information in this Annual Report on Form 10-K, you should consider carefully the following factors. The risks described below are the significant risks we face and include all material risks of which we are aware. Additional risks not presently known to us or risks that we currently consider immaterial may also adversely affect our business.

| 6 |

| Table of Contents |

Risks Related to Our Business and Industry

Our mineral exploration activities involve a high degree of risk, and a significant portion of our business model envisions the sale or joint venture of mineral properties. If we are unable to sell or joint venture these properties, the money spent on acquisition and exploration of our mineral properties may never be recovered and we could incur an impairment of our investments in our projects.

The exploration for mineral deposits involves significant financial and other risks over an extended period of time. Few properties that are explored are ultimately developed into producing mines. Major expenditures are required to determine if any of our mineral properties may have the potential to be commercially viable, be salable or joint ventured. From time to time, we may acquire a mineral property asset and later determine to abandon that project for various reasons, and as a result costs incurred to acquire the asset, and any costs incurred for initial exploration efforts will be lost. Moreover, significant expenses and risks, including drilling and determining the feasibility of a project, are required prior to the establishment of reserves. It is impossible to ensure that the current or proposed exploration programs on properties in which we have an interest will be commercially viable or that we will be able to sell, joint venture or develop our properties. Whether a mineral deposit will be commercially viable depends on a number of factors, some of which are the particular attributes of the deposit, such as its size and grade, costs and efficiency of the recovery methods that can be employed, proximity to infrastructure, commodity prices, financing costs and governmental regulations, including regulations relating to prices, taxes, royalties, infrastructure, land use, importing and exporting of mineral products and environmental protection.

We believe the data obtained from our own exploration activities or our partners' activities to be reliable; however, the nature of exploration of mineral properties and analysis of geological information is often subjective, and data and conclusions are subject to uncertainty. Even if exploration activities determine that a project is commercially viable, it is impossible to ensure that such determination will result in a profitable sale of the project or development either on our own or by a joint venture in the future and that such project will result in profitable commercial mining operations. If we determine that capitalized costs associated with any of our mineral interests are not likely to be recovered, we would incur an impairment of our investment in such property interest. All of these factors may result in losses in relation to amounts spent, which are not recoverable. We have experienced losses of this type from time to time in the past and may record mineral property impairments in the future.

We have no reported mineral reserves as defined by SEC rules, and our current projects and assets or any projects we may acquire are not likely to offer the opportunity for near term revenues or sale proceeds. If we are unsuccessful in identifying mineral reserves in the future, we may not be able to realize any profit from our property interests.

None of our current projects have reported mineral reserves as those terms are used in SEC rules. Any mineral reserves on these projects will only come from extensive additional exploration, engineering and evaluation of existing or future mineral properties. The lack of reserves on these mineral properties could prohibit us from any near-term sale or joint venture of our mineral properties and we would not be able to realize any proceeds and or profit from our interests in such mineral properties, which could materially adversely affect our financial position or results of operations.

We have mineral resources reported on our Florida Canyon and Lik projects upon which we do not exercise 100% control. The potential for reported mineral reserves on these projects is dependent on additional geologic work and economic evaluation which our joint venture partners may or may not conduct, and there can be no assurance that if such activities are performed that these will result in a positive feasibility or other study to allow the mineral resources to be upgraded to mineral reserves as defined by SEC rules, and as a result we may not be able to sell or otherwise realize any profit from our property interests in the Florida Canyon or Lik projects.

Our Florida Canyon and Lik projects have reported mineral resources in accordance with SEC rules. However, these resources may never be upgraded to mineral reserves without significant additional geologic work, including additional drilling, economic and environmental analysis, and the completion of a feasibility or other study to demonstrate the mineral potential and economic viability of these projects. To a significant degree, the completion of this work and a feasibility or other appropriate study is dependent on our joint venture partners desire to do so, over which we have limited influence. In addition, there is no assurance that if such work and studies are undertaken and completed, that either or both of these projects will be determined to be economically viable. The lack of reserves on these mineral properties could prohibit us from any near-term sale or joint venture of such mineral properties and we would not be able to realize any proceeds and or profit from our interests in such mineral properties, which could materially adversely affect our financial position or results of operations.

| 7 |

| Table of Contents |

Our Golden Crest project is an early-stage exploration project with no mineral resources or mineral reserves as defined by SEC rules. There can be no assurance that additional geologic work will result in reported mineral resources or mineral reserves in the future. If we are unsuccessful in identifying mineral reserves in the future, we may not be able to sell or otherwise realize any profit from our property interests.

Our Golden Crest project, which was acquired during 2021, has no reported mineral resources or mineral reserves as defined by SEC rules. We have conducted limited geologic activities at the Golden Crest project consisting primarily of soil and rock sampling. Additional geologic, environmental, and economic work would be required to allow us to report mineral resources at the Golden Crest project, including drilling and completion of a preliminary economic study. Furthermore, significant additional work would be required to prepare a feasibility or other study to allow us to report mineral reserves at the Golden Crest project. There can be no assurance that if such work is completed that the results would allow us to report either mineral resources or mineral reserves in the future. The lack of mineral resources or mineral reserves at the Golden Crest project could prohibit us from any near-term sale or joint venture of our interest in the Golden Crest project and we may not be able to realize any proceeds and or profit from our interests in the Golden Crest project, which could materially adversely affect our financial position or results of operations.

Mineral exploration activities are inherently dangerous and could cause us to incur significant unexpected costs, including legal liability for loss of life, damage to property and environmental damage, any of which could materially adversely affect our financial position or results of operations.

Mining exploration operations are subject to the hazards and risks normally related to exploration of a mineral deposit, including, but not limited to mapping and sampling, drilling, road building, trenching, assaying and analyzing rock samples, transportation over primitive roads or via small contract aircraft or helicopters and severe weather conditions. Any of the hazards of mineral exploration could result in damage to life or property, and environmental damage, and possible legal liability for such damage. Any of these risks could cause us to incur significant unexpected costs that could have a material adverse effect on our financial condition and ability to finance our exploration and development activities.

Our operations outside of the United States of America may be adversely affected by factors outside of our control, such as changing political, local and economic conditions, any of which could materially adversely affect our financial position or results of operations.

Our mineral properties located in Peru consist primarily of mineral concessions granted by national governmental agencies and are held 100% by us or in conjunction with our joint venture partners, or under lease, option or purchase agreements. Currently a portion of our mineral properties are located in Peru and we have previously held mineral properties and royalties on non-producing exploration properties in Peru, Mexico, Argentina, Bolivia and Brazil. Our current exploration activities and mineral properties located outside of the United States are subject to the laws of Peru (and any other countries in which we may conduct business). Exploration and potential development activities in other countries where we may conduct exploration are potentially subject to political and economic risks, including:

| · | cancellation or renegotiation of contracts; |

| · | disadvantages of competing against companies from countries that are not subject to U.S. laws and regulations, including the U.S. Foreign Corrupt Practices Act (“FCPA”); |

| · | changes in foreign laws or regulations; |

| · | changes in tax laws; |

| · | royalty and tax increases or claims by governmental entities, including retroactive claims; |

| · | expropriation or nationalization of property; |

| · | currency fluctuations (particularly related to a change in the U.S. dollar compared to local currencies); |

| · | foreign exchange controls; |

| · | restrictions on the ability for us to hold U.S. dollars or other foreign currencies in offshore bank accounts; |

| · | import and export regulations; |

| · | environmental controls; |

| · | risks of loss due to community opposition to our activities, civil strife, acts of war, guerrilla activities, insurrection and terrorism; and |

| · | other risks arising out of foreign sovereignty over the areas in which our exploration activities are conducted. |

Accordingly, our current exploration activities outside of the United States may be substantially affected by factors beyond our control, any of which could materially adversely affect the value of certain of our assets or results of operations. Furthermore, in the event of a dispute arising from such activities, we would likely be subject to the exclusive jurisdiction of courts outside of the United States or may not be successful in subjecting persons to the jurisdictions of the courts in the United States, which could adversely affect the outcome of a dispute.

| 8 |

| Table of Contents |

We may not have sufficient funding for exploration and development, which may impair our results of operations and growth potential.

The capital required for exploration and development of mineral properties is substantial. In the past we have financed operations through public and private sales of our common stock, the sale of interests in mineral properties (including the sale of our interest in the former Mt. Hamilton project in 2015), the utilization of joint venture arrangements with third parties (generally providing that the third party will obtain a specified percentage of our interest in a certain property or a subsidiary owning a property in exchange for the expenditure of a specified amount), the sale of other assets including short-term investments, the sale of marketable equity securities we hold, and funds from the issuance of long-term debt. We expect to need to raise additional capital, or enter into new joint venture arrangements, in order to fund our obligations with respect to our properties and our exploration activities required to determine whether mineral deposits on our projects are commercially viable. New financing or acceptable joint venture partners may or may not be available on a basis that is acceptable to us. The inability to obtain new financing or joint venture partners on acceptable terms may prohibit us from continued exploration or development of our existing mineral properties or any new mineral property assets we may acquire. Without the successful sale or future development of our mineral properties through joint ventures, or on our own, we will not be able to realize any profit from our interests in such properties, which could have a material adverse effect on our financial position or results of operations.

A large number of companies are engaged in the exploration and development or sale of mineral properties, many of which have substantially greater technical and financial resources than us and, accordingly, we may be unable to compete effectively which could have a material adverse effect on our financial position, prospects, or results of operations.

We are at a disadvantage with respect to many of our competitors in the acquisition, exploration and development or sale of mineral property assets and mining projects. Our competitors with greater financial resources than us are better able to withstand the uncertainties and fluctuations associated with sustained downturns in the market and to acquire high quality exploration and mining properties when market conditions are favorable. In addition, we compete with other companies in the mineral properties sector to attract and retain key executives and other personnel with technical skills and experience in the mineral exploration business. There can be no assurance that we will continue to retain skilled and experienced employees or to acquire additional exploration projects. The realization of any of these risks from competitors could have a material adverse effect on our financial position or results of operations.

The title to our mineral properties may be defective or challenged which could have a material adverse effect on our financial position or results of operations.

In connection with the acquisition of our mineral properties, we conduct limited reviews of title and related matters, and obtain certain representations regarding ownership. These limited reviews and representations do not necessarily preclude third parties from challenging our title and, furthermore, our title may be defective. Consequently, there can be no assurance that we hold good and marketable title to all of our mineral interests. Additionally, we have to make annual filings with various government agencies on all of our mineral properties. If we, or our joint venture partners, fail to make such filings, or improperly document such filings, the validity of our title to a mineral property could be lost or challenged. If any of our mineral interests were challenged, we could incur significant costs in defending such a challenge. These costs or an adverse ruling with regards to any challenge of our titles could have a material adverse effect on our financial position or results of operations.

Occurrence of events for which we are not insured or have limited insurance coverage may materially adversely affect our business.

Mineral exploration is subject to risks of human injury, environmental liability and loss of assets. We maintain limited insurance coverage to protect ourselves against certain risks related to loss of assets for equipment in our operations and limited corporate liability coverage; however, we have elected not to have insurance for other risks because of the high premiums associated with insuring those risks or for various other reasons including those risks where insurance may not be available. There are additional risks in connection with investments in parts of the world where civil unrest, war, nationalist movements, political violence or economic crisis are possible. These countries may also pose heightened risks of expropriation of assets, business interruption, increased taxation and a unilateral modification of concessions and contracts. We do not maintain insurance against political risk. Occurrence of events for which we are not insured or have limited insurance coverage could have a material adverse effect on our financial position or results of operations.

Normal weather variations as well as severe or violent storms could materially affect our operations due to damage or delays caused by such weather.

Our exploration activities (and those of our joint venture partners) are subject to normal seasonal weather conditions that often hamper and may temporarily prevent exploration or development activities. There is a risk that unexpectedly harsh weather or violent storms could affect areas where our projects are located and we or our joint venture partners conduct these activities. Delays or damage caused by severe weather could materially affect our operations or our financial position.

| 9 |

| Table of Contents |

Our operations could be negatively affected by existing laws as well as potential changes in laws and regulatory requirements to which we are subject, including regulation of mineral exploration and ownership, environmental regulations and taxation.

The exploration and development of mineral properties is subject to federal, state, provincial and local laws and regulations in the countries in which they are located in a variety of ways, including regulation of mineral exploration and land ownership, environmental regulation and taxation. These laws and regulations, as well as future interpretation of or changes to existing laws and regulations, may require substantial increases in capital and operating costs to us and delays, interruptions, or a termination of operations.

In the United States and the other countries in which we operate or own assets, in order to obtain permits for exploration or potential future development of mineral properties, environmental regulations generally require a description of the existing environment, including but not limited to natural, archeological and socio-economic environments, at the project site and in the region; an interpretation of the nature and magnitude of potential environmental impacts that might result from such activities; and a description and evaluation of the effectiveness of the operational measures planned to mitigate the environmental impacts. The expenditures to obtain exploration permits to conduct our exploration activities may be material to our total exploration cost.

The laws and regulations in all the countries in which we operate, or own assets are continually changing and are generally becoming more restrictive, especially environmental laws and regulations. As part of our ongoing exploration activities, we have made expenditures to comply with such laws and regulations, but such expenditures could substantially increase our costs to achieve compliance in the future. Delays in obtaining or failure to obtain government permits and approvals or significant changes in regulation could have a material adverse effect on our exploration activities, our ability to locate economic mineral deposits, and our potential to sell, joint venture or eventually develop our properties, which could have a material adverse effect on our financial position or results of operations.

Our operations are subject to permitting requirements which could require us to delay, suspend or terminate our operations on our mining properties.

Our exploration operations, including any exploration drilling programs and other exploration activities, require permits from various state and federal governments, including permits for the use of water and for drilling exploration holes. We may be unable to obtain these permits in a timely manner, on reasonable terms or on terms that provide us sufficient resources to explore or develop our properties in any way. Even if we are able to obtain such permits, the time required by the permitting process can be significant. If we cannot obtain or maintain the necessary permits, or if there is a delay in receiving these permits, our timetable and business plan for exploration of our properties will be adversely affected, which may in turn adversely affect our results of operations, financial condition, cash flows and market price of our securities.

Due to increased activity levels of non-governmental environmental groups, native American, aboriginal, and local groups targeting the mining industry, the potential for the government or process instituted by these local groups, to delay the issuance of permits or impose new requirements or conditions upon mining operations may be increased. Any changes in government policies may be costly to comply with and may delay mining operations. Future changes in such laws and regulations, if any, may adversely affect our operations, make them prohibitively expensive, or prohibit them altogether. If our interests are materially adversely affected as a result of a violation of applicable laws, regulations, permitting requirements or a change in applicable law or regulations, it would have a significant negative impact on the value of our company and could have a significant impact on our stock price.

Our business could be negatively affected by changing climate and climate change laws.

A number of governments, including the United States, have introduced or are moving to introduce climate change legislation and treaties at the international, national, state/provincial and local levels. Regulations relating to emission levels (such as carbon taxes) and energy efficiency are becoming more stringent. If the current regulatory trend continues, this may result in increased costs at some or all of our project locations. In addition, the physical risks of climate change may also have an adverse effect on our operations and properties. Some of the countries in which we own or have owned mineral property assets have implemented, and are developing, laws and regulations related to climate change and greenhouse gas emissions.

Legislation and increased regulation and requirements regarding climate change could impose increased costs or limit our ability, or our joint venture partners’ ability, to effectively advance our projects, including impacting our suppliers through increased energy, capital equipment, environmental monitoring and reporting and other costs to comply with such regulations.

| 10 |

| Table of Contents |

Our business is dependent on the market price of certain commodities, particularly gold and zinc, and currency exchange rates over which we have no control.

Our operations are significantly affected by changes in the market price of commodities since the evaluation of whether a mineral deposit is commercially viable is heavily dependent upon the market price of the commodities related to any specific project. Because our core assets are currently in zinc and gold related projects, the spot price of zinc and gold is particularly important to the value of our assets and future prospects. The price of commodities also affects the value of exploration projects we own or may wish to acquire or joint venture. These commodity prices fluctuate on a daily basis and are affected by numerous factors beyond our control. The supply and demand for commodities, the level of interest rates, the rate of inflation, investment decisions by large holders of these commodities, including governmental reserves, and stability of exchange rates can all cause significant fluctuations in prices. Currency exchange rates relative to the United States dollar can affect the cost of doing business in a foreign country in United States dollar terms, which is our functional currency. Consequently, the cost of conducting exploration in the countries where we operate, accounted for in United States dollars, can fluctuate based upon changes in currency exchange rates and may be higher than we anticipate in terms of United States dollars because of a decrease in the relative strength of the United States dollar to currencies of the countries where we operate. We currently do not hedge against currency or commodity fluctuations. The prices of commodities as well as currency exchange rates have fluctuated widely and future significant price declines in commodities or changes in currency exchange rates could have a material adverse effect on our financial position or results of operations.

Our business is dependent on key executives and the loss of any of our key executives could adversely affect our business, future operations and financial condition.

We are dependent on the services of key executives, including our Chief Executive Officer, Christopher E. Herald, our Chief Operating Officer, Walter H. Hunt, and our Chief Financial Officer, James R. Maronick. All those officers have many years of experience and an extensive background with Solitario and in the mining industry in general. We may not be able to replace that experience and knowledge with other individuals. We do not have "Key-Man" life insurance policies on any of our key executives. The loss of these persons or our inability to attract and retain additional highly skilled employees may adversely affect our business, future operations and financial condition.

Our business model relies significantly on other companies to joint venture our projects and we anticipate continuing this practice in the future. Therefore, our results are subject to the additional risks associated with the financial condition, operational expertise and corporate priorities of our joint venture partners.

The success of projects held under joint ventures that are not operated by us are substantially dependent on the joint venture partner, over which we have limited or no control. Our Florida Canyon project and our Lik project are joint ventured with other mining companies that manage the exploration activities on the projects. We are the minority-interest party at Florida Canyon and a 50% partner at the Lik project. Although our joint venture agreements provide certain voting rights and other minority-interest safeguards, the majority partner and/or operator not only manages operations, but controls most decisions, including budgets and scope and pace of exploration and other activities. Consequently, we are highly dependent on the operational expertise and financial condition of our joint venture partners, as well as their corporate priorities. For instance, even though our joint venture property may be highly prospective for exploration success, or economically viable based on feasibility studies, our partner may decide not to fund the further exploration or development of our project based on their respective financial condition or other corporate priorities. Therefore, our results are subject to the additional risks associated with the financial condition, operational expertise and corporate priorities of our joint venture partners, which could have a material adverse effect on our financial position or results of operations. Our Lik project requires unanimous consent by the joint venture partners for annual budgets in excess of $1.0 million. Consequently, exploration of the Lik project could be delayed without the unanimous consent of both parties to certain proposed actions or transactions.

We may look to joint venture with another mining company in the future to explore, develop and/or operate our current or future projects; therefore, in the future, our results may become subject to additional risks associated with development and production of our foreign mining projects.

Neither we, nor our joint venture partners are currently involved in mining development or mining operations at any of our properties. In order to realize a profit from our mineral interests we have to: (1) sell our properties or interests outright at a profit; (2) form a joint venture for the project with a larger mining company with greater resources, both technical and financial, to further develop and/or operate a project; (3) develop and operate such projects at a profit on our own; or (4) create and retain a royalty interest in a property with a third party that agrees to advance the property toward development and mining. In the future, if our exploration results show sufficient promise in a future project, not currently under joint venture, we may either look to form a joint venture with another mining company to develop and/or operate the project or sell the property outright and retain partial ownership or a retained royalty based on the success of such project. Therefore, in the future, our results may become subject to the additional risks associated with development and production of mining projects in general.

| 11 |

| Table of Contents |

In the future, we may attempt to acquire a new property, or another company and the acquisition may require a substantial amount of capital or the issuance of our capital stock to complete. Acquisition costs may never be recovered due to changing market conditions, or our own miscalculation concerning the recoverability of our acquisition investment. Such an occurrence could adversely affect our business, future operations and financial condition.

We have evaluated a wide variety of acquisition opportunities involving mineral properties and companies for acquisition and we anticipate evaluating potential acquisition opportunities in the future. Some of these opportunities may require a substantial amount of capital or the issuance of our capital stock to successfully acquire. As many of these opportunities do not have reliable feasibility-level studies, we may have to rely on our own estimates for investment analysis. Such estimates, by their very nature, contain substantial uncertainty. In addition, economic assumptions, such as future costs and commodity prices, also contain significant uncertainty. Consequently, if we are successful in acquiring any new opportunities and our estimates prove to be in error, either through miscalculations or changing market conditions, this could have a material adverse effect on our financial position or results of operations.

Failure to comply with the FCPA could subject us to penalties and other adverse consequences.

As a Colorado corporation, we are subject to the FCPA and similar worldwide anti-bribery laws, which generally prohibit United States companies and their intermediaries from engaging in bribery or other improper payments to foreign officials for the purpose of obtaining or retaining business. Foreign companies, including some that may compete with us, are not subject to U.S. laws and regulations, including the FCPA, and therefore our exploration, and potential future development, production and mine closure activities are subject to the disadvantage of competing against companies from countries that are not subject to these prohibitions.

In addition, we could be adversely affected by violations of the FCPA and similar anti-bribery laws in other jurisdictions. Corruption, extortion, bribery, pay-offs, theft and other fraudulent practices may occur from time-to-time in the countries outside of the United States in which we operate. Certain of our mineral properties are located in countries that may have experienced governmental corruption to some degree and, in certain circumstances, strict compliance with anti-bribery laws may conflict with local customs and practices. Our policies mandate compliance with the FCPA and other anti-bribery laws; however, we cannot assure you that our internal controls and procedures always will protect us from the reckless or criminal acts committed by our employees or agents. We can make no assurance that our employees or other agents will not engage in such conduct for which we might be held responsible. If our employees or other agents are found to have engaged in such practices or we are found to be liable for FCPA violations, we could suffer severe criminal or civil penalties or other sanctions and other consequences that may have a material adverse effect on our business, financial condition and results of operations.

Risks Related to Our Common Stock

The market for shares of our common stock has limited liquidity and the market price of our common stock has fluctuated and may decline.

An investment in our common stock involves a high degree of risk. The liquidity of our shares, or the ability of a shareholder to buy or sell our common stock, may be significantly limited for various unforeseeable periods. The average combined daily volume of our shares traded on the NYSE American and the TSX during 2022 was approximately 148,000 shares. The market price of our shares of common stock has historically fluctuated within a wide range. The price of our common stock may be affected by many factors, including an adverse change in our business, a decline in the price of zinc or other commodity prices, negative news on our projects, negative investment sentiment for mining and commodity equities and general economic trends.

We have a history of losses and if we do not operate profitably in the future it could have a material adverse effect on our financial position or results of operations and the trading price of our common stock would likely decline.

We have reported losses in 26 of our 29 years of operations. We can provide no assurance that we will be able to operate profitably in the future or begin to generate significant and consistent sources of revenues or cash flows from operations. We have had net income in only three years in our history; (i) during 2015, as a result of the sale of our former Mt. Hamilton project; (ii) during 2003, as a result of a $5,438,000 gain on a derivative instrument related to our investment in certain Crown warrants and (iii) during 2000, when we sold our former Yanacocha property. We cannot predict when, if ever, we will be profitable again or able to begin generating consistent revenues or cash flows from our operations or assets. If we do not operate profitably or identify and execute on outside sources of funding, we may be unable to fund our current or contemplated exploration activities, acquire new assets, or otherwise further our business plan.

| 12 |

| Table of Contents |

We have never paid, and do not intend to pay cash dividends and, consequently, the ability to achieve a return on any investment in our common stock will depend on appreciation in the price of our common stock.

We have never paid cash dividends on any of our capital stock, and we currently intend to retain future earnings, if any, to fund the development and growth of our business. Therefore, a holder of our stock is not likely to receive any dividends on our common stock for the foreseeable future. Since we do not intend to pay dividends, the ability to receive a return on an investment in our common stock will depend on any future appreciation in the market value of our common stock. There is no guarantee that our common stock will appreciate or even maintain the price at which it was purchased.

Issuances of our stock in the future could dilute existing shareholders and adversely affect the market price of our common stock.

We have the authority to issue up to 100,000,000 shares of common stock and 10,000,000 shares of preferred stock, and to issue options and warrants to purchase shares of our common stock without shareholder approval. In addition, during 2021 we put an ATM (“At the Market”) program in place and expect to sell shares of our common stock under that program from time to time. Future issuances of our securities could be at prices substantially below the price paid for our common stock by our current shareholders. In addition, we can issue blocks of our common stock in amounts up to 20% of the then-outstanding shares without further shareholder approval. Sales of a substantial number of shares by the Company in the public market (or otherwise), or the perception that those sales may occur, could cause the market price of our common stock to decline.

General Risk Factors

The outbreak of pandemics, including the coronavirus (COVID-19) may affect our assets, operations and development plans at our projects.

We face risks related to health epidemics and other outbreaks of communicable diseases, which could significantly disrupt our operations and may materially and adversely affect our business and financial conditions.

Our business still could be adversely impacted by the effects of the COVID-19 or other epidemics or pandemics. How these epidemics or pandemics may ultimately impact our business, including our future exploration and other activities and the market for our securities, will depend on future developments, which are highly uncertain and cannot be predicted at this time, and include the duration, severity, and any recurrence of various strains of the outbreak and the actions taken to contain or treat the coronavirus outbreak. In particular travel and other restrictions established to curb the spread of COVID-19, or other pandemic diseases could materially and adversely impact our business including without limitation, planned exploration programs at our Florida Canyon, Lik and Golden Crest projects during 2023 and beyond, employee health, workforce productivity, increased insurance premiums, limitations on travel, labor shortages and the availability of industry experts and personnel, the timing to process drilling and other metallurgical testing, supply chain constraints that impede exploration operations, and other factors that will depend on future developments beyond our control, which may have a material and adverse effect on our business, financial condition and results of operations. There can be no assurance that we will not be impacted by COVID-19 or other pandemic diseases and that we could ultimately see our workforce productivity reduced or incur increased medical costs or insurance premiums as a result of these health risks. The outbreak of additional strains of COVID-19 or other pandemic diseases could create a widespread global health crisis that contributes to volatility in the economy and financial markets that could have an adverse effect on the future demand for precious and base metals and, in turn, our prospects.

A significant portion of our liquid assets consist of U.S. Treasuries and cash held in brokerage accounts. The failure of the financial institutions that issued or hold these financial instruments or our cash could have a material adverse impact on the market price of our common stock and our liquidity and capital resources.

At December 31, 2022, we have invested $3,951,000 in United States Treasury securities (“USTS”) held in a brokerage account, with maturities of between 15 days and 12 months and we have approximately $293,000 of our cash in uninsured deposit accounts and brokerage accounts which are not covered by Federal Deposit Insurance Company insurance. The failure of a financial institution holding these funds and assets could have a material impact on the market price of our common stock and our liquidity and capital resources.

Increased costs could impede our ability to explore sell or develop our current projects.

Capital and operating costs at mining operations are subject to variation due to a number of factors, such as changing ore grade, changing metallurgy, and revisions to mine plans in response to changing commodity prices, additional drilling results and updated geologic interpretations. In addition, costs are affected by the cost of capital, tax and royalty regimes, trade tariffs, the global cost of mining and processing equipment, commodity prices, and foreign exchange rates, as well as the costs of fuel, electricity, operating supplies, and appropriately skilled labor. These costs are at times subject to volatile price movements, including increases that could negatively affect our ongoing exploration efforts and negatively impact our potential for future development or sale of our exploration projects as well as our estimates of mineral resources. This could have a material adverse effect on our business prospects, results of operations, cash flows and financial condition.

| 13 |

| Table of Contents |

We are dependent upon information technology systems, which are subject to disruption, damage, failure and risks associated with implementation and integration.

We are dependent upon information technology systems in the conduct of our operations. Our information technology systems are subject to disruption, damage or failure from a variety of sources, including, without limitation, computer viruses, security breaches, cyber-attacks, natural disasters and defects in design. Cybersecurity incidents, in particular, are evolving and include, but are not limited to, malicious software, attempts to gain unauthorized access to data and other electronic security breaches that could lead to disruptions in systems, theft of assets, unauthorized release of confidential or otherwise protected information and the corruption of data. Various measures have been implemented to manage our risks related to information technology systems and network disruptions. However, given the unpredictability of the timing, nature and scope of information technology disruptions, we could potentially be subject to operational delays, the compromising of confidential or otherwise protected information, loss of assets, including our cash, short-term investments, or marketable equity securities, destruction or corruption of data, security breaches, other manipulation or improper use of our systems and networks or financial losses from remedial actions, any of which could have a material adverse effect on our cash flows, competitive position, financial condition or results of operations.

Item 1B. Unresolved Staff Comments

None

Item 2. Properties

CAUTIONARY NOTE REGARDING DISCLOSURE OF MINERAL PROPERTIES

Mineral Reserves and Resources

We are subject to the reporting requirements of the Exchange Act and applicable Canadian securities laws, and as a result we report our mineral resources according to two different standards. U.S. reporting requirements, are governed by Item 1300 of Regulation S-K (“S-K 1300”), as issued by the SEC. Canadian reporting requirements for disclosure of mineral properties are governed by National Instrument 43-101 Standards of Disclosure for Mineral Projects, as adopted from the definitions provided by the Canadian Institute of Mining, Metallurgy and Petroleum. Both sets of reporting standards have similar goals in terms of conveying an appropriate level of confidence in the disclosures being reported, but the standards generally embody slightly different approaches and definitions.

In our public filings in the U.S. and Canada and in certain other announcements not filed with the SEC, we disclose measured, indicated and inferred resources, each as defined in S-K 1300. The estimation of measured resources and indicated resources involve greater uncertainty as to their existence and economic feasibility than the estimation of proven and probable reserves, and therefore investors are cautioned not to assume that all or any part of measured or indicated resources will ever be converted into S-K 1300-compliant reserves. The estimation of inferred resources involves far greater uncertainty as to their existence and economic viability than the estimation of other categories of resources, and therefore it cannot be assumed that all or any part of inferred resources will ever be upgraded to a higher category. Therefore, investors are cautioned not to assume that all or any part of inferred resources exist, or that they can be mined legally or economically.

Technical Report Summaries and Qualified Persons

The scientific and technical information concerning our mineral projects in this Annual Report on Form 10-K have been reviewed and approved by “qualified persons” under S-K 1300, including our Chief Operating Officer, Walter Hunt. For a description of the key assumptions, parameters and methods used to estimate mineral reserves and mineral resources included in this Annual Report on Form 10-K, as well as data verification procedures and a general discussion of the extent to which the estimates may be affected by any known environmental, permitting, legal, title, taxation, sociopolitical, marketing or other relevant factors, please review the Technical Report Summaries for each of the Company’s material properties which are incorporated by reference into, this Annual Report on Form 10-K.

| 14 |

| Table of Contents |

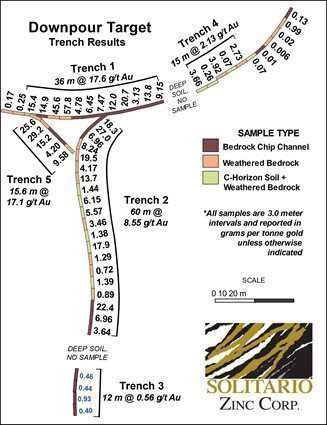

Golden Crest Project (United States)

1. Property Description and Location

(map of Golden Crest project)

The Golden Crest project is in the northern Black Hills of western South Dakota in Lawrence County. A map of the project location is shown above. The Golden Crest project is comprised of 1,707 unpatented lode claims, with an associated area of approximately 33,000 acres. Two hundred forty-one of the claims are leased from Golden Crest II, LLC , a Wyoming limited liability company (“GC LLC”) and 27 unpatented claims (“Easter Claims”) are leased from the Easter Project, LLC, a Wyoming limited liability company. All the remaining claims are owned by Solitario and were staked throughout 2021 and 2022.

Solitario acquired its interest in the GC Claims in May 2021 by entering into the Golden Crest Agreement with GC LLC. Terms of the Golden Crest Agreement include scheduled payments to the underlying owner of $65,000 paid upon signing and an obligation to pay the underlying owner $60,000 at the first anniversary date. To continue the lease, Solitario has agreed to pay, at its option, the underlying owner escalating annual payments over a five-year period that total $340,000 and annual payments of $150,000 thereafter. Solitario has agreed to pay the underlying owner an additional success fee of $1.00 per ounce of gold in the event Solitario files a 43-101 qualified resource of up to 1.5 million ounces of gold or a maximum of $1,500,000. Solitario has agreed to perform escalating work commitments, at Solitario’s option, on the GC Claims totaling $3,000,000 in work expenditures during the first five years of the lease. Solitario has fulfilled its $600,000 work commitment for the first two years. The term of the Golden Crest Agreement is for twenty years and is automatically extended as long as Solitario is performing any exploration, development or mining activities on the GC Claims. The underlying owner will retain a 2.0% Net Smelter Return royalty. Solitario has the option, but not the obligation, to reduce the Net Smelter Return royalty to 1.0% by paying the underlying owner $1,000,000. GC LLC reserves a three-mile area of interest to its original claim position.

In February of 2022, Solitario entered into a lease agreement (the “Easter Agreement”) whereby Solitario acquired exclusive exploration rights to the Easter Claims in the Black Hills region of South Dakota. The Easter Claims are part of Solitario’s Golden Crest project. Terms of the Easter Agreement include $10,000 paid upon signing, scheduled annual payments to the underlying owner totaling $180,000 through the tenth anniversary, and $30,000 per year thereafter. Solitario has agreed to escalating work commitments, at Solitario’s option, on the Easter Claims totaling $660,000 during the first five years of the lease, with the first year totaling $20,000. All other terms of the Easter Agreement are substantially the same as the Golden Crest Agreement, except there is no area of interest.

Federal maintenance fees and county registration due in 2022 will be approximately $333,000 for all Golden Crest claims currently held by Solitario.

2. Accessibility, Climate, Local Resources, Infrastructure and Physiology

Access to the Golden Crest project by road is by traveling south of the city of Spearfish, SD along several paved and/or gravel roads. US Highway 14A, and US Highway 85 are near the eastern and southern boundaries of the Golden Crest project. Maintained gravel roads extending westward and northward from Highways 14A and 85 as well as numerous unmaintained, numbered secondary United States Forest Service (“USFS”) roads provide additional ingress to the Golden Crest Project.

The Golden Crest Project is in forested highlands with subdued relief separated by steep-sided canyons. Elevations in the immediate area range from approximately 1,500 m to 2000 m. Spearfish Creek, a stream with a perennial flow, is situated east of the property while most other creeks on the property are generally dry in the summer months. Vegetation consists of mixed forest composed of deciduous hardwoods and conifers with sporadic meadows and locally dense underbrush. Stands of timber of commercial value cover the property at higher elevations and are managed by the USFS. Logging activities have been widespread on large portions of the property in the past five to twenty years and are ongoing.

| 15 |

| Table of Contents |

Climate at the Golden Crest project area is temperate, characterized by hot summers, cold winters and pronounced seasonal variation in precipitation and temperatures. Average annual temperature, as measured at the Spearfish weather station, is 55°F with seasonal variation averages highs of 32°F and 80°F in winter and summer respectively. The average amount of annual rainfall is approximately 26 inches along with 44 inches of snowfall (as measured at the Spearfish recording station). Average precipitation is greater at the higher elevations of the property itself. The mineral exploration season is generally from early April to late November.

The closest population center is Spearfish, South Dakota (population 11,500), which represents the largest city in Lawrence County (population: 25,800). Spearfish is located along Interstate Highway 90, linking Rapid City, South Dakota to Gillette, Wyoming. Spearfish supports light industry, ranching and tourism and hosts a small university, Black Hills State University. The nearest towns to the project area are Lead (population 3,000) and the nearby town of Deadwood (population 1,500), which is the county seat of Lawrence County and a major tourism and gaming center for the area. Mining related employment continues to be an important segment of Lawrence County’s economy. The closest regional airport servicing the area is at Rapid City, situated approximately 80 km southeast along Interstate Highway 90. All major commercial and industrial services are available in Rapid City. Other mining services are available in Lead, South Dakota due to the legacy of the Homestake Mining Company (“Homestake”) operations and the currently producing Wharf mine operated by Coeur Mining. Solitario maintains an office in Spearfish, South Dakota.

3. History

The state of South Dakota ranks third among US states for historic gold production, totaling approximately 51 million ounces produced through 2020, most of which came from the world class Homestake Mine in Lead. The first documented gold discovery in the Black Hills was made by prospectors attached to the Custer Expedition of 1874, who discovered placer gold in gravel bars along French Creek near the present site of Custer, South Dakota. The first known lode claims in the Black Hills were located in the spring of 1876 at the head of Gold Run and Deadwood Gulches. Beginning in the 1890’s, hundreds of mines and mining companies sprang to life in the northern Black Hills, clustered within a relatively small area measuring 20 km long by 16 km wide, and centered around the cities of Lead and Deadwood. Collectively this area, known as the Lead Gold District, is one of the richest gold districts in the world. Gold mining has occurred continuously in the district for 145 years, a record unmatched by any other US gold mining district.

Despite the importance of the Lead Gold District among American mining camps, during the last 140 years very little regional exploration has been conducted on the property which comprises the Golden Crest project. Although the Golden Crest project is adjacent to the Lead Gold District, the lack of regional exploration is apparently due to the widespread cover of the gold bearing Precambrian rocks by younger sedimentary formations. The Golden Crest project is within several kilometers of district mines with significant historical production, yet only a handful of prospect pits occur on the property. It is also thought that the subdued topography, soil cover and absence of outcrops of the distinctive Precambrian rocks that host the ore in the main Lead Gold District resulted in the project area being largely overlooked for such a long time. There is no prior documented work on the property with the exception of three exploration core holes drilled by Homestake in 1993-1994, a small cluster of small prospect pits and a very limited stream sediment survey.