UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-K

| (Mark One) | ||||||||

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||

| For the fiscal year ended | ||||||||

| OR | ||||||||

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||||||

| For the transition period from ______________ to ______________ | ||||||||

Commission file number 1-12626

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. employer identification no.) | |||||||

| (Address of principal executive offices) | (Zip Code) | |||||||

Registrant's telephone number, including area code: (423 ) 229-2000

Securities registered pursuant to Section 12(b) of the Act:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||||||||

Securities registered pursuant to Section 12(g) of the Act: None

1

| No | |||||||||||||||||||||||

| Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. | ☒ | ☐ | |||||||||||||||||||||

| Yes | |||||||||||||||||||||||

| Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. | ☐ | ☒ | |||||||||||||||||||||

| No | |||||||||||||||||||||||

| Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. | ☒ | ☐ | |||||||||||||||||||||

| No | |||||||||||||||||||||||

| Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). | ☒ | ☐ | |||||||||||||||||||||

| Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer", "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act. | |||||||||||||||||||||||

| ☒ | Accelerated filer | ☐ | |||||||||||||||||||||

| Non-accelerated filer | ☐ | Smaller reporting company | |||||||||||||||||||||

| Emerging growth company | |||||||||||||||||||||||

| If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. | ☐ | ||||||||||||||||||||||

| Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. | |||||||||||||||||||||||

| Yes | No | ||||||||||||||||||||||

| Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). | ☒ | ||||||||||||||||||||||

The aggregate market value (based upon the $69.64 closing price on the New York Stock Exchange on June 30, 2020) of the 135,107,969 shares of common equity held by non-affiliates as of December 31, 2020 was $9,408,918,961 using beneficial ownership rules adopted pursuant to Section 13 of the Securities Exchange Act of 1934 to exclude common stock that may be deemed beneficially owned as of December 31, 2020 by Eastman Chemical Company's directors and executive officers and charitable foundation, some of whom might not be held to be affiliates upon judicial determination. A total of 135,861,854 shares of common stock of the registrant were outstanding at December 31, 2020.

DOCUMENTS INCORPORATED BY REFERENCE

2

FORWARD-LOOKING STATEMENTS

Certain statements made or incorporated by reference in this Annual Report are "forward-looking statements" within the meaning of the Private Securities Litigation Reform Act (Section 27A of the Securities Act of 1933, as amended and Section 21E of the Securities and Exchange Act of 1934, as amended). Forward-looking statements are all statements, other than statements of historical fact, that may be made by Eastman Chemical Company ("Eastman" or the "Company") from time to time. In some cases, you can identify forward-looking statements by terminology such as "anticipates", "believes", "estimates", "expects", "intends", "may", "plans", "projects", "forecasts", "will", "would", and similar expressions or expressions of the negative of these terms. Forward-looking statements may relate to, among other things, such matters as planned and expected capacity increases and utilization; anticipated capital spending; expected depreciation and amortization; environmental matters and opportunities (including potential risks associated with physical impacts of climate change and related voluntary and regulatory carbon requirements); exposure to, and effects of hedging of, raw material and energy prices and costs; foreign currencies and interest rates; disruption or interruption of operations and of raw material or energy supply; global and regional economic, political, and business conditions; competition; growth opportunities; supply and demand, volume, price, cost, margin and sales; pending and future legal proceedings; earnings, cash flow, dividends, stock repurchases and other expected financial results, events, decisions, and conditions; expectations, strategies, and plans for individual assets and products, businesses, and operating segments, as well as for the whole of Eastman; cash sources and requirements and uses of available cash; financing plans and activities; pension expenses and funding; credit ratings; anticipated and other future restructuring, acquisition, divestiture, and consolidation activities; cost reduction and control efforts and targets; the timing and costs of, benefits from the integration of, and expected business and financial performance of acquired businesses as well as the subsequent impairment assessments of acquired long-lived assets; strategic, technology, and product innovation initiatives and development, production, commercialization and acceptance of new products, services and technologies and related costs; asset, business, and product portfolio changes; and expected tax rates and interest costs.

Forward-looking statements are based upon certain underlying assumptions as of the date such statements were made. Such assumptions are based upon internal estimates and other analyses of current market conditions and trends, management expectations, plans, and strategies, economic conditions, and other factors. Forward-looking statements and the assumptions underlying them are necessarily subject to risks and uncertainties inherent in projecting future conditions and results. Actual results could differ materially from expectations expressed in the forward-looking statements if one or more of the underlying assumptions and expectations proves to be inaccurate or is unrealized. The known material factors, risks, and uncertainties that could cause actual results to differ materially from those in the forward-looking statements are identified and discussed under "Management's Discussion and Analysis of Financial Condition and Results of Operations - Risk Factors" in Part II, Item 7 of this Annual Report. Other factors, risks or uncertainties of which management is not aware, or presently deems immaterial, could also cause actual results to differ materially from those in the forward-looking statements.

The Company cautions you not to place undue reliance on forward-looking statements, which speak only as of the date such statements are made. Except as may be required by law, the Company undertakes no obligation to update or alter these forward-looking statements, whether as a result of new information, future events, or otherwise. Investors are advised, however, to consult any further public Company disclosures (such as filings with the Securities and Exchange Commission, Company press releases, or pre-noticed public investor presentations) on related subjects.

3

TABLE OF CONTENTS

| ITEM | PAGE | |||||||

PART I

| 1. | ||||||||

| 1A. | ||||||||

| 1B. | ||||||||

| 2. | ||||||||

| 3. | ||||||||

| 4. | ||||||||

PART II

| 5. | ||||||||

| 6. | ||||||||

| 7. | ||||||||

| 7A. | ||||||||

| 8. | ||||||||

| 9. | ||||||||

| 9A. | ||||||||

| 9B. | ||||||||

PART III

| 10. | ||||||||

| 11. | ||||||||

| 12. | ||||||||

| 13. | ||||||||

| 14. | ||||||||

PART IV

SIGNATURES

4

PART I

| ITEM 1. BUSINESS | ||

| Page | |||||

5

| CORPORATE OVERVIEW | ||

Eastman Chemical Company ("Eastman" or the "Company") is a global specialty materials company that produces a broad range of products found in items people use every day. Eastman began business in 1920 for the purpose of producing chemicals for Eastman Kodak Company's photographic business and became a public company, incorporated in Delaware, on December 31, 1993. Eastman has 47 manufacturing facilities and has equity interests in three manufacturing joint ventures in 14 countries that supply products to customers throughout the world. See Item 2. "Properties" of this Annual Report on Form 10-K (this "Annual Report"). The Company's headquarters and largest manufacturing facility are located in Kingsport, Tennessee. With a robust portfolio of specialty businesses, Eastman works with customers to deliver innovative products and solutions with commitment to safety and sustainability. Eastman's businesses are managed and reported in four operating segments: Additives & Functional Products, Advanced Materials, Chemical Intermediates, and Fibers. See "Business Segments".

In the first years as a stand-alone company, Eastman was diversified between commodity and more specialty chemical businesses. Beginning in 2004, the Company refocused its strategy and changed its businesses and portfolio of products, first by the divestiture and discontinuance of under-performing assets and commodity businesses and initiatives (including divestiture in 2004 of resins, inks, and monomers product lines, divestiture in 2006 of the polyethylene business, and divestiture from 2007 to 2010 of the polyethylene terephthalate ("PET") assets and business). The Company then pursued growth through the development and acquisition of more specialty businesses and product lines by inorganic acquisition and integration (including the acquisition of Solutia, Inc., a global leader in performance materials and specialty chemicals, in 2012, and Taminco Corporation, a global specialty chemical company, in 2014) and organic development and commercialization of new and enhanced technologies and products.

Eastman currently uses an innovation-driven growth model which consists of leveraging world class scalable technology platforms, delivering differentiated application development capabilities, and relentlessly engaging the market. The Company's world class technology platforms form the foundation of sustainable growth by differentiated products through significant scale advantages in research and development ("R&D") and advantaged global market access. Differentiated application development converts market complexity into opportunities for growth and accelerates innovation by enabling a deeper understanding of the value of Eastman's products and how they perform within customers' and end-user products. Key areas of application development include molecular recycling technologies, thermoplastic conversion, functional films, coatings formulations, rubber additive formulations, adhesives formulations, nonwovens and textiles, and animal nutrition. The Company engages the market by working directly with customers and downstream users, targeting attractive niche markets, and leveraging disruptive macro trends. Management believes that these elements of the Company's innovation-driven growth model, combined with disciplined portfolio management and balanced capital deployment, is transforming Eastman to a global specialty materials company that enhances the quality of life in a material way. To facilitate Eastman's transformation to a global specialty materials company, management is changing the Company's business and operations to improve cost structure, increase investment in growth, and strengthen execution capabilities, including specific initiatives during 2020 and currently to transform operations, work processes and systems, and business structure alignment, scale, and integration.

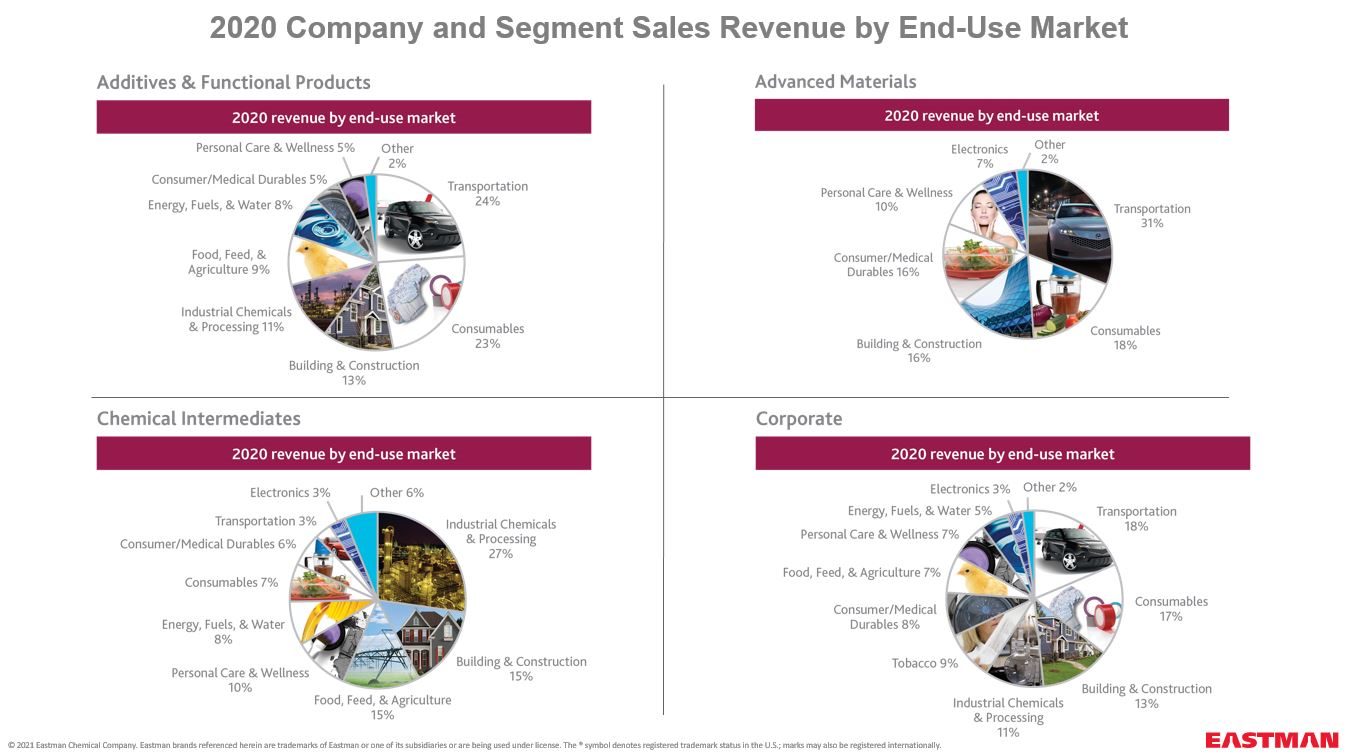

In 2020, the Company reported sales revenue of $8.5 billion, earnings before interest and taxes ("EBIT") of $741 million, and net earnings of $478 million. Diluted earnings per share were $3.50. Net cash provided by operating activities was $1.5 billion and "free cash flow" (cash provided by or used in operating activities less the amount of net capital expenditures) was $1.1 billion. Excluding non-core and unusual items, adjusted EBIT was $1.2 billion and adjusted diluted earnings per share were $6.15. See "Management's Discussion and Analysis of Financial Condition and Results of Operations" in Part II, Item 7 of this Annual Report for reconciliation of financial measures under accounting principles generally accepted in the United States ("GAAP") to non-GAAP financial measures, description of excluded items, and related information. For Company sales revenue by end-market, see Exhibit 99.01 "2020 Company and Segment Sales Revenue by End-Use Market" of this Annual Report. Approximately 60 percent of 2020 sales revenue was generated from outside the United States and Canada region. For additional information regarding sales by customer location and by segment, see Note 19, "Segment and Regional Sales Information", to the Company's consolidated financial statements in Part II, Item 8, and "Management's Discussion and Analysis of Financial Condition and Results of Operations - Summary by Operating Segment", "Sales by Customer Location", and "Risk Factors" in Part II, Item 7 of this Annual Report.

6

BUSINESS STRATEGY

Eastman's objective is to be a global specialty materials company that enhances the quality of life in a material way with consistent, sustainable earnings growth and strong cash flow. Integral to the Company's strategy for growth is leveraging its heritage expertise and innovation within its cellulose and acetyl, olefins, polyester, and alkylamine chemistries. For each of these "streams", the Company has developed and acquired a combination of assets and technologies that combine scale and integration across multiple manufacturing units and sites as a competitive advantage. Management uses an innovation-driven growth model which consists of leveraging world class scalable technology platforms, delivering differentiated application development, and relentlessly engaging the market. The Company sells differentiated products into diverse markets and geographic regions and engages the market by collaborating and co-innovating with customers and downstream users in existing and new niche markets to creatively solve problems. Management believes that this innovation-driven growth model will result in consistent financial results by leveraging the Company's proven technology capabilities to improve product mix, increasing emphasis on specialty businesses, and sustaining and expanding leadership in attractive niche markets. A consistent increase in earnings is expected to result from both organic growth initiatives and strategic inorganic initiatives.

Innovation

Management is pursuing specific opportunities to leverage Eastman's innovation-driven growth model for continued near-term and long-term greater than end-market growth by both sustaining the Company's leadership in existing markets and expanding into new markets. Recently developed, introduced, or commercialized innovation products, applications, and technologies include the following:

•As described below under "Circular Economy and Sustainability", commercialization of two molecular recycling technologies, carbon renewal technology and polyester renewal technology. These technologies are being used for production of multiple products with commercial sales in various markets leveraging our polyester and acetyl streams.

•Eastman Tritan™ Renew copolyester based on polyester renewal technology which transforms single-use polyester waste into basic building blocks that are then used to make durable, high performance materials.

•Naia™ Renew, a fiber product for the apparel market developed from proprietary cellulose ester technology.

•Saflex™ E series, an enhanced acoustic interlayer product, formulated to dampen sound, particularly in the high frequency range, and provides improved performance compared to traditional acoustic interlayers.

•Tetrashield™ performance polyester resins based on proprietary monomer technology with improved performance and sustainability features for packaging, industrial, and automotive coatings end-users.

•Paint protection films ongoing innovation and new product line additions, including faster adhering films and black paint protection films, and expansion of our service offerings, including the launch of Eastman CORE (trademark and patent pending), a differentiated analytics-based software platform that provides high performance paint protection films and window films product customers and end-users access to digital service and automotive film patterns to improve customer experience and accelerate category development.

•Impera™ tire additives performance resins that enable tire manufacturers to improve the safety and handling of tires, balance tire performance and fuel economy needs, and achieve superior levels of tack for tire construction.

•Regalite™ UltraPure Platform, a class of tackifying hydrocarbon adhesives resins with enhanced features addressing hygiene end-use product consumer odor, volatile organic compounds, and trace chemicals concerns.

Circular Economy and Sustainability

Central to Eastman's innovation-driven growth model is our dedication to enhance the quality of life in a material way with an ongoing commitment to our sustainability strategy to create more value than the resources used by innovating to deliver consumer choices that will sustain and protect our world.

7

The Company's long history of technical expertise in chemical processes and polymer science position it to provide innovative solutions to some of the world's most complex problems, contributing to development of a more "circular economy" - an economic system in which resource input and waste generation, emissions, and energy usage are reduced by slowing, closing, and narrowing energy and material loops through long-lasting design, maintenance, repair, reuse, remanufacturing, refurbishing, recycling, and upcycling. The Company's sustainable innovation initiatives include mechanical recycling, biodegradation, molecular recycling, and strategic collaborations with end-user markets. In 2019, the Company announced the use of its unique platform of solutions to address the challenges of plastic waste in the environment with advanced circular recycling, or molecular recycling, including carbon renewal and polyester renewal technologies. Together, these technologies can recycle multiple kinds of plastic waste, including polyester carpet and textiles. These technologies reduce plastic waste and lower greenhouse gas emissions compared to traditional processes. Eastman's scale and integration provides a unique opportunity to accelerate the use of these advanced circular recycling technologies and make a meaningful positive impact on the environment.

Management approaches sustainability as a source of competitive strength by focusing its innovation strategy on opportunities where disruptive macro trends align with the Company's differentiated technology platforms and applications development capabilities to develop innovative products, applications, and technologies that enable customers' development and sales of sustainable products. Eastman's sustainability-related growth initiatives include targeted products utilizing technology that enhance end-use product durability, material usage, recyclability, and health and safety impact characteristics to reduce unnecessary waste, pollution, and greenhouse gas emissions associated with climate change. These efforts include collaboration and communication with stakeholders, including policymakers and other interested parties, to include the concepts of molecular recycling and mass balance accounting (an accepted and certified protocol that documents and tracks recycled content through complex manufacturing systems). Eastman has committed to reduce greenhouse gas emissions by one-third by 2030 in order to achieve carbon neutrality by 2050, and to innovate to provide products that enable energy savings and greenhouse gas emissions reductions to customers and end-users.

Examples of Eastman sustainable solutions within identified disruptive macro trends include:

•circular economy: molecular recycling technology including carbon renewal and polyester renewal technologies, including Tritan™ Renew coployesters, Acetate Renew cellulose esters, Trēva™ Renew cellulose esters, Cristal™ Renew copolyesters, Naia™ Renew cellulosic yarn, and the announcement in January 2021 of a planned methanolysis manufacturing plant;

•health and wellness: Tritan™ copolyester, Tetrashield™ performance polyester resins, and Vestera™ cellulosic fiber;

•natural resource efficiency: Saflex™ Q series advanced acoustic interlayers, Impera™ high performance resins for tires, and Treva™ proprietary engineering bioplastic;

•feeding a growing population: Eastman organic acids, Enhanz™ feed additive, and Banguard™ crop protectant; and

•emerging middle class: Saflex™ and head-up display ("HUD") acoustic interlayers, Regalite™ hydrocarbon resins, and Naia™ cellulosic yarn.

The Company leverages core competencies in polyesters, cellulose esters, thermoplastic processing, textile capability, and in-house application expertise for use in a wide range of applications to provide sustainable solutions to markets which are in search of new and improved products.

FINANCIAL STRATEGY

In its management of the Company's businesses and growth initiatives, management is committed to maintaining a strong financial position with appropriate financial flexibility and liquidity. Management believes maintaining a financial profile that supports an investment grade credit rating is important to its long-term strategy and financial flexibility. The Company employs a disciplined and balanced approach to capital allocation and deployment of cash. The priorities for uses of available cash include payment of the quarterly dividend, repayment of debt, funding targeted growth opportunities, and repurchasing shares. Management expects that the combination of continued strong cash flow generation, a strong balance sheet, and sufficient liquidity will continue to provide flexibility to pursue growth initiatives.

8

| BUSINESS SEGMENTS | ||

The Company's products and operations are managed and reported in four operating segments: Additives & Functional Products ("AFP"), Advanced Materials ("AM"), Chemical Intermediates ("CI"), and Fibers. This organizational structure is based on the management of the strategies, operating models, and sales channels that the various businesses employ and supports the Company's continued transformation towards a global specialty materials company. For segment sales revenue and earnings and segment product lines revenues, see Note 19, "Segment and Regional Sales Information", to the Company's consolidated financial statements in Part II, Item 8 and "Management's Discussion and Analysis of Financial Condition and Results of Operations - Summary by Operating Segment" in Part II, Item 7 of this Annual Report. For identification of manufacturing facilities by segment, see Item 2, "Properties" of this Annual Report.

ADDITIVES & FUNCTIONAL PRODUCTS SEGMENT

Overview

In the AFP segment, the Company manufactures materials for products in the transportation, consumables, building and construction, animal nutrition, crop protection, energy, personal and home care, and other markets. Key technology platforms in this segment are cellulose esters, polyester polymers, insoluble sulfur, hydrocarbon resins, alkylamine derivatives, and propylene derivatives.

The AFP segment's sales growth is typically above annual industrial production growth due to innovation and enhanced commercial execution with sales to a robust set of end-markets. The segment is focused on producing high-value additives that provide critical functionality but which comprise a small percentage of total customer product cost. The segment principally competes on the differentiated performance characteristics of its products and through leveraging its strong customer base and long-standing customer relationships to promote substantial recurring business and product development. A critical element of the AFP segment's success is its close formulation collaboration with customers through advantaged application development capability.

9

Principal Products

| Product | Description | Principal Competitors | Key Raw Materials | End-Use Applications | ||||||||||

| Adhesives Resins | ||||||||||||||

Piccotac™ Regalite™ Eastotac™ Eastoflex™ Aerafin™ | hydrocarbon resins and rosin resins mainly for hot-melt and pressure sensitive adhesives | Exxon Mobil Corporation Kolon Industries, Inc. Evonik Industries | C9 resin oil piperylene gum rosin propylene | consumables (resins used in hygiene and packaging adhesives) building and construction (resins for construction adhesives and interior flooring) | ||||||||||

| Animal Nutrition | ||||||||||||||

Organic acids and derivatives Choline chloride Enhanz™ | organic acid-based solutions | BASF SE Perstorp Holding AB Luxi Chemical Group Feicheng Acid Chemicals | formic acid ethylene oxide propane heavy fuel oil | gut health solutions preservation industrial applications | ||||||||||

| Care Chemicals | ||||||||||||||

Alkylamine derivatives Organic acids and derivatives Cellulose esters Banguard™ | amine derivative-based building blocks for production of flocculants intermediates for surfactants metam-based soil fumigants thiram and ziram-based fungicides plant growth regulator | BASF SE Dow Inc. Huntsman Corporation Corteva, Inc. Argo-Kanesho Co., Ltd. Bayer AG | alkylamines ammonia alcohols ethylene oxide CS2 caustic soda | water treatment personal and home care pharmaceuticals agriculture crop protection | ||||||||||

| Coatings and Inks Additives | ||||||||||||||

Polymers cellulosics Tetrashield™ polyesters polyolefins Additives and Solvents Texanol™ Optifilm™ ketones esters glycol ethers oxo alcohols EastaPure™ electronic chemicals | specialty coalescents, specialty solvents, and commodity solvents paint additives and specialty polymers | BASF SE Dow Inc. Oxea Celanese Corporation Alternative Technologies | wood pulp propane propylene | building and construction (architectural coatings) transportation (OEM) and refinish coatings durable goods (wood, industrial coatings and applications) consumables (graphic arts, inks, and packaging) electronics | ||||||||||

10

| Product | Description | Principal Competitors | Key Raw Materials | End-Use Applications | ||||||||||

| Specialty Fluids | ||||||||||||||

Therminol™ Turbo oils Skydrol™ SkyKleen™ Marlotherm™ | heat transfer and aviation fluids | Dow Inc. Exxon Mobil Corporation | benzene phosphorous neo-polyol esters | industrial chemicals and processing (heat transfer fluids for chemical processes) renewable energy commercial aviation | ||||||||||

| Tire Additives | ||||||||||||||

Crystex™ | insoluble sulfur rubber additive | Oriental Carbon & Chemicals Limited Shikoku Chemicals Corporation | sulfur naphthenic process oil | transportation (tire manufacturing) other rubber products (such as hoses, belts, seals, and footwear) | ||||||||||

Santoflex™ | antidegradant rubber additive | Jiangsu Sinorgchem Technology Co., Ltd. Kumho Petrochemical Co., Ltd. Lanxess AG | nitrobenzene aniline methyl isobutyl ketone | transportation (tire manufacturing) other rubber products (such as hoses, belts, seals, and footwear) | ||||||||||

Impera™ | performance resins | Cray Valley Hydrocarbon Specialty Chemicals Exxon Mobil Corporation Kolon Industries, Inc. | alpha methylstyrene piperylene styrene | transportation (tire manufacturing) | ||||||||||

Strategy

Management applies Eastman's innovation-driven growth model in the AFP segment by leveraging proprietary technologies for the continued development of innovative product offerings and focusing growth efforts on further expanding end-markets such as transportation, building and construction, consumables, industrial applications, animal nutrition, care chemicals, and energy. Management believes that the ability to leverage the AFP segment's research, differentiated application development, and production capabilities across multiple markets uniquely positions it to meet evolving needs to improve the quality and performance of its customers' products. For example, Eastman Bisphenol A ("BPA") -non intent (BPA-NI) Tetrashield™ protective resins enable metal packaging coatings formulation with a unique balance of durability and flexibility and allows the coating to stay intact even with hard-to-hold foods and beverages. Such protective resins can also be used in protective coatings, industrial coatings and automotive coatings. The Company is also developing new technologies such as ultrapure tackifier for hot-melt adhesives, sustainable solvents and hydrocarbon resins for tires to address identified customer and end-user desired features.

Eastman's global manufacturing presence is a key element of the AFP segment's growth strategy. For example, the AFP segment expects to capitalize on industrial growth in Asia from its manufacturing capacity expansion in Kuantan, Malaysia and cellulose ester products sourced from the Company's low-cost cellulose and acetyl manufacturing stream in North America.

11

In 2020, the AFP segment:

•completed a Dimethylethanolamine ("DMAE") manufacturing capacity expansion in China in response to growing demand for stricter regulation of sustainable water treatment. In addition, the Company decided to significantly increase capacity to produce tertiary amines at its Ghent, Belgium, facility to meet growing demand for hand sanitizers and other household cleaning products;

•advanced growth and innovation of Tetrashield™ , resins that enable low-VOC formulations and eliminate energy-intensive manufacturing steps, by working with key customers and other brands through the value chain;

•completed process improvements of Eastoflex amorphous polyolefin ("APO") polymers manufacturing capacity in Longview, Texas to support product line growth and innovation; and

•entered into a global customer supply agreement to meet a growing demand for products in the animal nutrition industry, expanding the Company's gut health solutions offerings.

Eastman is pursuing specific opportunities in the AFP segment to leverage its innovation-driven growth model to create greater than end-market growth by both sustaining the Company's leadership in existing markets and expanding into new markets. Examples of recent product innovation within the AFP segment include Tetrashield™ performance polyester resins based on proprietary monomer technology, Impera™ high performance resins for tires, Regalite™ UltraPure Platform addressing consumer concerns associated with odor, volatile organic compounds and trace chemicals in the hygiene industry, Aerafin™ polymer developed from proprietary olefin technology, and care chemicals alkylamine derivatives including state-of-the-art water treatment solutions.

In response to market and business conditions, management continues to evaluate strategic alternatives for certain businesses and product lines within the AFP segment, including certain adhesives resins, tire additives, and animal nutrition products constituting approximately one-third of segment revenue. In 2020, the Company recognized charges related to the closures of an animal nutrition manufacturing facility in first quarter and a tire additives manufacturing facility in second quarter, both in Asia Pacific. AFP segment strategic alternatives being considered include restructuring and cost management actions, partnerships or other arrangements with third-parties, and divestitures.

ADVANCED MATERIALS SEGMENT

Overview

In the AM segment, the Company produces and markets polymers, films, and plastics with differentiated performance properties for value-added end-uses in transportation, consumables, building and construction, durable goods, and health and wellness markets. Key technology platforms for this segment include cellulose esters, copolyesters, and polyvinyl butyral ("PVB") and polyester films.

Eastman's technical, application development, and market development capabilities enable the AM segment to modify its polymers, films, and plastics to control and customize their final properties for development of new applications with enhanced functionality. For example, Tritan™ copolyesters are a leading solution for food contact applications due to their performance and processing attributes and BPA free properties. The Saflex™ Q Series product line is a leading acoustic solution for architectural and automotive applications. The Company also maintains a leading solar control technology position in the window films market through the use of high performance sputter coatings which enhance solar heat rejection while maintaining superior optical properties. The segment principally competes on differentiated technology and application development capabilities. Management believes the AM segment's competitive advantages also include long-term customer relationships, vertical integration and scale in manufacturing, and leading market positions.

12

Principal Products

| Product | Description | Principal Competitors | Key Raw Materials | End-Use Applications | ||||||||||

| Advanced Interlayers | ||||||||||||||

Saflex™ Saflex™ Q Series Saflex™ ST Saflex™ E Series | standard PVB sheet premium PVB sheet | Sekisui Chemical Co., Ltd. Kuraray Co., Ltd. Kingboard (Fo Gang) Specialty Resins Limited Chang Chun Petrochemical Co., Ltd. | polyvinyl alcohol vinyl acetate monomer butyraldehyde 2-ethyl hexanol ethanol triethylene glycol | transportation (automotive safety glass, automotive acoustic glass, and HUD) building and construction (PVB for architectural interlayers) | ||||||||||

| Performance Films | ||||||||||||||

LLumar™ Flexvue™ SunTek™ V-KOOL™ Gila™ | window films and protective films products for aftermarket applied films | 3M Company Saint-Gobain S.A. XPEL, Inc. | polyethylene terephthalate film aliphatic thermoplastic polyurethane film | transportation (automotive after- market window films and paint protection films) building and construction (residential and commercial window films) health and wellness (medical) | ||||||||||

| Specialty Plastics | ||||||||||||||

Tritan™ copolyester Eastar™ copolyesters Spectar™ copolyester Embrace™ copolyester Visualize™ Eastman Aspira™ family of resins Treva™ | standard copolyesters premium copolyesters cellulose esters | Covestro AG Trinseo S.A. Evonik Industries AG Saudi Basic Industries Corporation Mitsubishi Chemical Corporation S.K. Chemical Industries Sichuan Push Acetati Company Limited Daicel Chemical Industries Ltd. | paraxylene ethylene glycol cellulose purified terephthalic acid waste plastics and textiles | consumables (consumer packaging, cosmetics packaging, in-store fixtures and displays) durable goods (consumer housewares and appliances) health and wellness (medical) electronics (displays) | ||||||||||

Strategy

Management applies Eastman's innovation-driven growth model in the AM segment by leveraging innovation and technology platforms to develop new and multi-generational products and applications to accelerate AM segment growth and leverage its manufacturing capacity. The segment continues to expand its portfolio of higher margin products in attractive end-markets. Through Eastman's advantaged asset position and expertise in applications development, management believes that the AM segment is well positioned for continued future growth. The advanced interlayers product lines, including acoustic and HUD sheet interlayer products, leverage Eastman's global presence to supply industry leading innovations to automotive and architectural end-markets by collaborating with global and large regional customers. In the automotive end-market, the performance films product line has industry leading technologies, recognized brands, and what management believes is one of the largest distribution and dealer networks which, when combined, position Eastman for further growth, particularly in leading automotive markets such as North America and Asia. The segment's product portfolio is aligned with underlying energy efficiency trends in both automotive and architectural markets. Additionally, the AM segment is positioned to benefit from recent Eastman polyesters and acetyl streams sustainability innovations by leveraging advanced circular recycling technology to enable various waste plastics to be recycled into specialty plastics products marketed and sold under the "Renew" product designation. See "Corporate Overview - Business Strategy - Circular Economy and Sustainability".

The AM segment expects to continue to improve its product mix from increased sales of premium products, including Tritan™ copolyester, Visualize™ material, Saflex™ Q acoustic series, Saflex™ HUD interlayer products, LLumar™, V-KOOL™, and SunTek™ window and protective films.

13

In 2020, the AM segment:

•commercialized polyester renewal technology with multiple products in various markets including the adoption of Tritan™ Renew in durable goods end-markets;

•commercialized carbon renewal technology with multiple products in various markets including the adoption of Acetate Renew in the premium eyewear end-market;

•continued circular economy advancements (including the January 2021 announced methanolysis advanced plastic-to-plastic molecular recycling manufacturing facility);

•continued the growth of Tritan™ copolyester in the durable goods and health and wellness markets, supported by continued market and application development

•continued to expand portfolio of differentiated next generation products for both automotive and architectural interlayer films products; and

•developed and launched Eastman CORE (trademark and patent pending) digital product data analytics software for accessory sales management and installation of automotive window and paint protection films products.

Eastman is pursuing specific opportunities in its AM segment to leverage its innovation-driven growth model to create greater than end-market growth by both sustaining the Company's leadership in existing markets and expanding into new markets.

CHEMICAL INTERMEDIATES SEGMENT

Overview

Eastman leverages large scale and vertical integration from the cellulose and acetyl, olefins, and alkylamines streams to support the Company's specialty operating segments with advantaged cost positions. The CI segment sells excess intermediates beyond the Company's internal specialty needs into markets such as industrial chemicals and processing, building and construction, health and wellness, and agrochemicals. Key technology platforms include acetyls, oxos, plasticizers, polyesters, and alkylamines.

The CI segment product lines benefit from competitive cost positions primarily resulting from the use of and access to lower cost raw materials, and the Company's scale, technology, and operational excellence. Examples include coal used in the production of cellulose and acetyl stream product lines, feedstocks used in the production of olefin derivative product lines such as oxo alcohols and plasticizers, and ammonia and methanol used to manufacture methylamines. The CI segment also provides superior reliability to customers through its backward integration into readily available raw materials, such as propane, ethane, coal, and propylene. In addition to a competitive cost position, the plasticizers business expects to continue to benefit from the growth in relative use of non-phthalate rather than phthalate plasticizers in the United States, Canada, and Europe.

Several CI segment product lines are affected by cyclicality, most notably olefin and acetyl-based products. See "Eastman Chemical Company General Information - Manufacturing Streams". This cyclicality is caused by periods of supply and demand imbalance, when either incremental capacity additions are not offset by corresponding increases in demand, or when demand exceeds existing supply. While management continues to take steps to reduce the impact of the trough of these cycles, future results are expected to occasionally fluctuate due to both general economic conditions and industry supply and demand.

14

Principal Products

| Product | Description | Principal Competitors | Key Raw Materials | End-Use Applications | ||||||||||

| Functional Amines | ||||||||||||||

| Alkylamines | methylamines and salts higher amines and solvents | BASF SE US Amines Limited Oxea GmbH Belle Chemical Company | methanol ammonia acetone ethanol butanol | agrochemicals energy consumables water treatment animal nutrition industrial intermediates | ||||||||||

| Intermediates | ||||||||||||||

Oxo alcohols and derivatives Acetic acid and derivatives Acetic anhydride Ethylene Glycol ethers Esters | Olefin derivatives, acetyl derivatives, ethylene, commodity solvents | Lyondell Bassell, BASF SE Dow Inc. Oxea BP plc Celanese Corporation Lonza Ineos Group Holdings S.A. Indorama Ventures Public Company Limited | propane ethane propylene coal natural gas paraxylene metaxylene | industrial chemicals and processing building and construction (paint and coating applications, construction chemicals, building materials) pharmaceuticals and agriculture health and wellness packaging | ||||||||||

| Plasticizers | ||||||||||||||

Eastman 168™ DOP Benzoflex™ TXIB™ Effusion™ | primary non- phthalate and phthalate plasticizers and a range of niche non- phthalate plasticizers | BASF SE Exxon Mobil Corporation LG Chem, Ltd. Emerald Performance Materials | propane propylene paraxylene | building and construction (non-phthalate plasticizers used in interior surfaces) consumables (food packaging, packaging adhesives, and glove applications) health and wellness (medical devices) | ||||||||||

Strategy

To maintain and enhance its status as a low-cost producer and optimize earnings, the CI segment continuously focuses on cost control, operational efficiency, and capacity utilization. This includes focusing on products used internally by other operating segments, thereby supporting growth in specialty product lines throughout the Company, and also external licensing opportunities. Through the CI segment, the Company has leveraged the advantage of its highly integrated manufacturing facilities. The Kingsport, Tennessee manufacturing facility allows for the production of acetic anhydride and other acetyl derivatives from coal rather than natural gas or other petroleum feedstocks. At the Longview, Texas manufacturing site, Eastman uses its proprietary oxo technology in one of the world's largest single-site oxo butyraldehyde manufacturing facilities to produce a wide range of alcohols and other derivative products utilizing local propane and ethane supplies and purchased propylene. The Pace, Florida manufacturing facility, which uses ammonia and methanol feedstocks, is one of the world's largest methylamine production site in the world. These integrated facilities, combined with large scale production processes and a continuous focus on additional process improvements, allow the CI segment product lines to remain cost competitive and, for some products, cost-advantaged as compared to competitors. Use of refinery-grade propylene ("RGP") in the feedstock mix of the olefin cracking units at the Longview, Texas manufacturing site reduces the amount of other purchased feedstocks, resulting in a decrease in ethylene production and excess ethylene sales while maintaining historical levels of propylene production and providing flexibility to reduce participation in the merchant ethylene market while retaining a cost-advantaged integrated propylene position to support specialty derivatives throughout the Company.

15

In 2020, the CI segment announced a strategic project for site optimization and recognized revenue and earnings from licensing of innovative technologies. Under a site optimization project with Gulf Coast Ammonia ("GCA") and Air Products, Inc., GCA leases a portion of Eastman's Texas City, Texas site and will build and own a new world-scale ammonia production plant. In 2018, the Company and Johnson Matthey announced that Eastman's proprietary technology for the production of mono ethylene glycol ("MEG") from coal had been selected by Inner Mongolia Jiutai New Material (Jiutai) for its planned 1,000,000 tonnes per annum ethylene glycol facility. The Company recognized revenue and earnings from the MEG technology license in 2020. In addition, production of certain products at the Singapore manufacturing site discontinued as of December 31, 2020 with the site to be shut down in 2021.

FIBERS SEGMENT

Overview

In the Fibers segment, Eastman manufactures and sells acetate tow and triacetin plasticizers for use in filtration media, primarily cigarette filters; natural (undyed), cellulosic fibers and yarn for use in apparel, home furnishings, and industrial fabrics; nonwovens for use in filtration and friction media, used primarily in transportation, industrial, and agricultural markets; and cellulose acetate flake and acetyl raw materials for other acetate fiber producers. Eastman is one of the world's two largest suppliers of acetate tow and has been a market leader in the manufacture and sale of acetate tow since it began production in the early 1950s. The Company is the world's largest producer of acetate yarn and has been in this business for over 85 years.

The 10 largest Fibers segment customers accounted for approximately 70 percent of the segment's 2020 sales revenue, and include multinational as well as regional cigarette producers, fabric manufacturers, and other acetate fiber producers.

The Company's long history and experience in fibers markets are reflected in the Fibers segment's operating expertise, both within the Company and in support of its customers' processes. The Fibers segment's knowledge of the industry and of customers' processes allows it to assist its customers in maximizing their processing efficiencies, promoting repeat sales, and developing mutually beneficial, long-term customer relationships.

The Company's fully integrated fibers manufacturing process employs unique technology that allows it to use a broad range of high-purity wood pulps for which the Company has dependable sources of supply.

Contributing to profitability in the Fibers segment is the limited number of competitors and significant barriers to entry. These barriers include, but are not limited to, high capital costs for integrated manufacturing facilities.

The Fibers segment's competitive strengths include a reputation for high-quality products, technical expertise, large scale vertically-integrated processes, reliability of supply, internally produced acetate flake supply for Fibers segment's products, a reputation for customer service excellence, and a customer base characterized by strategic long-term customer and end-user relationships. The Company continues to capitalize and build on these strengths to further improve the strategic position of its Fibers segment. In response to challenging acetate tow market conditions, including additional industry capacity and lower capacity utilization rates, the Company has taken actions in recent years expected to stabilize segment earnings, including the establishment of long-term acetate tow customer arrangements and agreements, development of innovative textile and nonwoven applications, and repurposing manufacturing capacity from acetate tow to new products.

16

Principal Products

| Product | Description | Principal Competitors | Key Raw Materials | End-Use Applications | ||||||||||

| Acetate Tow | ||||||||||||||

Estron™ | cellulose acetate tow | Celanese Corporation Cerdia International Daicel Corporation | wood pulp methanol high sulfur coal | filtration media (primarily cigarette filters) | ||||||||||

| Acetate Yarn and Fiber | ||||||||||||||

Naia™ Estron™ | natural (undyed) acetate yarn solution dyed acetate yarn staple fiber | UAB Dirbtinis Pluostas Lenzing AG Aditya Birla Group | wood pulp methanol high sulfur coal waste plastics and textiles | consumables (apparel, home furnishings, and industrial fabrics) health and wellness (medical tape) | ||||||||||

| Acetyl Chemical Products | ||||||||||||||

Estrobond™ | triacetin cellulose acetate flake acetic acid acetic anhydride | Jiangsu Ruijia Chemistry Co., Ltd. Polynt SpA Daicel Corporation Celanese Corporation Cerdia International | wood pulp methanol high sulfur coal | filtration media (primarily cigarette filters) | ||||||||||

| Nonwovens | ||||||||||||||

Nonwovens Vestera™ Cellulosic Fiber | wetlaid nonwoven media specialty and engineered papers cellulose acetate fiber | Hollingsworth and Vose Company Lydall, Inc. BorgWarner Inc. Lenzing AG | natural and synthetic fibers inorganic and metallic additives resins | filtration and friction media for transportation industrial agriculture and mining aerospace markets personal hygiene consumables | ||||||||||

Strategy

Management applies the innovation-driven growth model to the Fibers segment by leveraging its strong customer relationships and industry knowledge to maintain a leading industry position in the global market. The segment benefits from a state-of-the-art, world class, acetate flake production facility at the Kingsport, Tennessee site, which is supplied from Eastman's vertically integrated coal gasification facility and is the largest and most integrated acetate tow site in the world. The Fibers segment also expects to benefit from Eastman’s recently developed carbon renewal technology, which enables the substitution of fossil fuel feedstock with waste plastics and textiles. Products using this technology are marketed and sold under the "Renew" product designation. See "Corporate Overview - Business Strategy - Circular Economy and Sustainability". Eastman's global acetate tow capacity is approximately 150,000 metric tons, not including the Company's participation in an acetate tow joint venture manufacturing facility in China. The Company supplies 100 percent of the acetate flake raw material to the China manufacturing joint venture from the Company's manufacturing facility in Kingsport, Tennessee, which the Company recognizes in sales revenue. The Company recognizes earnings in the joint venture through its equity investment, reported in "Other (income) charges, net" in the Consolidated Statements of Earnings, Comprehensive Income and Retained Earnings in Part II, Item 8 of this Annual Report. The Company's focus on innovation has resulted in repurposing some of its acetate tow manufacturing capacity to fibers products for textiles and nonwovens markets, resulting in increased capacity utilization and lower acetate tow costs.

To meet customers' evolving needs and further improve the Fibers segment's manufacturing process efficiencies, the Company makes use of its capabilities in fibers technology to maintain a strong focus on incremental product and process improvements.

17

The Fibers segment R&D efforts focus on serving existing customers, leveraging proprietary cellulose ester and spinning technology for differentiated application development in new markets, optimizing asset productivity, and working with suppliers to reduce costs. For acetate tow, these efforts are assisting customers in the effective use of the Fibers segment's products and customers' product development efforts. For other products, management is applying the Company's innovation-driven growth model to leverage its fibers technology and expertise to focus on innovative growth in the textiles and nonwovens markets. Examples of recent product innovation within the Fibers segment include Naia™ yarn for the apparel market developed from Eastman's proprietary cellulose ester technology; and Vestera™ wood pulp-based alternative for the nonwoven industry used in personal hygiene applications.

In 2019 the Company acquired Industrias del Acetato de Celulosa. S.A. ("INACSA"), a cellulosic yarn business in LA Batllòria, Spain as a targeted addition to the Fibers segment's acetate yarn business.

| EASTMAN CHEMICAL COMPANY GENERAL INFORMATION | ||

Seasonality

Eastman's earnings are typically higher in the second and third quarters, and cash flows from operations are typically highest in the second half of the year due to seasonal demand based on general economic activity in the Company's key markets as described in "Business Segments". Results in all segments except Fibers are typically weaker in the fourth quarter due to seasonal downturns in key markets.

The coatings and inks additives product line of the AFP segment and the intermediates product line of the CI segment are impacted by the cyclicality of key end products and markets, while other operating segments and product lines are more sensitive to global economic conditions. Eastman is exposed to consumer discretionary end-markets, particularly in the AM and AFP segments, and changes in global consumer spending impact the results in these segments. Supply and demand dynamics determine profitability at different stages of business cycles and global economic conditions affect the length of each cycle.

Sales, Marketing, and Distribution

Eastman markets and sells products primarily through a global marketing and sales organization which has a presence in the United States and approximately 30 other countries selling into more than 100 countries around the world. The Company focuses its market engagement on attractive niche markets, leveraging disruptive macro trends, and market activation throughout the value chain with both customers and downstream users. Eastman's strategy is to target industries and markets where the Company can leverage its application development expertise to develop product offerings to provide differentiated value that address current and future customer and market needs. The Company's strategic marketing approach and capabilities leverage the Company's insights about trends, markets, and customers to drive development of specialty products. Through a highly skilled and specialized sales force that is capable of providing differentiated product solutions, Eastman strives to be the preferred supplier in the Company's targeted markets.

The Company's products are also marketed through indirect channels, which include dealers and contract representatives. Sales outside the United States tend to be made more frequently through dealers and contract representatives than sales in the United States. The combination of direct and indirect sales channels, including sales online through its Customer Center website, allows Eastman to reliably serve customers throughout the world.

The Company's products are shipped to customers and to downstream users directly from Eastman manufacturing plants and distribution centers worldwide.

18

Research and Development

Management applies its innovation-driven growth model to leverage the Company's world class scalable technology platforms that provide a competitive advantage and the foundation for sustainable earnings growth. The Company's R&D strategy for sustainable growth through innovation includes multi-generational product development for specialty products, faster and more differentiated product development by leveraging global application development capabilities, and the creation of value through integration of multiple technology platforms. The Company's innovation strategy is guided by the need to provide practical solutions to sustainability macro-drivers that will improve the quality of life globally through material solutions. This strategy has been accelerated by enhancements of global differentiated application development capabilities that position Eastman as a strategic element of customers' success within attractive niche markets. See examples of recent product and technology innovations in "Corporate Overview - Business Strategy - Innovation".

Eastman manages certain growth initiatives and costs at the corporate level, including certain R&D costs not allocated to any one operating segment. The Company uses a stage-gating process, which is a disciplined decision-making framework for evaluating targeted opportunities, with a number of projects at various stages of development. As projects meet milestones, additional amounts are spent on those projects. The Company continues to explore and invest in R&D initiatives such as high-performance materials and opportunities created by disruptive macro trends including sustainability and development of a more "circular economy". See "Corporate Overview - Business Strategy - Circular Economy and Sustainability".

Manufacturing Streams

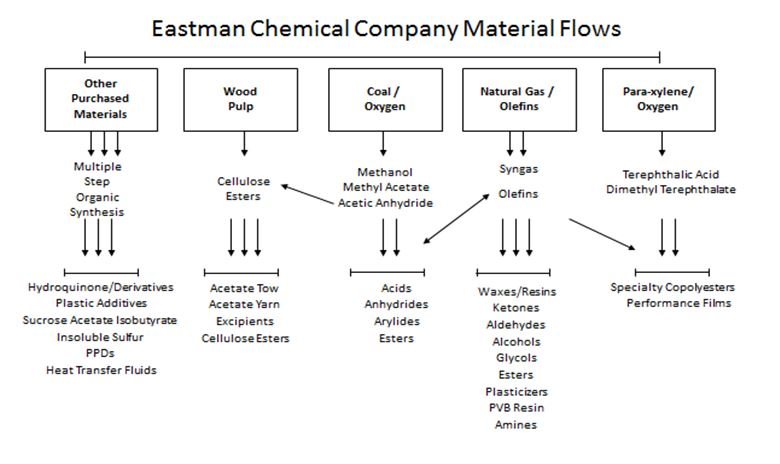

Integral to Eastman's strategy for growth is leveraging its heritage expertise and innovation in cellulose and acetyl, olefins, polyester, and alkylamine chemistries in key markets, including transportation, building and construction, consumables, filtration media, and agriculture. For each of these chemistries, Eastman has developed and acquired a combination of assets and technologies that are operated within four manufacturing "streams", combining scale and integration across multiple manufacturing units and sites as a competitive advantage.

•In the cellulose and acetyl stream, the Company begins with gasification of fossil fuels with oxygen. The resulting synthesis gas is converted into acetic acid and acetic anhydride. Cellulose derivative manufacturing at the Company begins with natural polymers, sourced from managed forests, which, when combined with acetyl and olefin chemicals, provide differentiated product lines. Through a new recycling innovation, carbon renewal technology is now enabling the recycling of complex plastics to the basic building blocks of Eastman's cellulosic product stream. The major end-markets for products from the cellulose and acetyl stream include coatings, displays, thermoplastics, and filtration media.

•In the olefins stream, the Company begins primarily with propane and ethane, which are thermally "cracked" (the process whereby hydrocarbon molecules are broken down and rearranged) into ethylene and propylene in three cracking units at its site in Longview, Texas. As a result of modifications completed in 2018, these units also offer flexibility to use RGP as a diversified feedstock to minimize the impact of olefins spread volatility. The Company purchases some additional propylene to supplement cracking unit production. Propylene derivative products are used in a variety of items such as paints and coatings, automotive safety glass, and non-phthalate plasticizers. Ethylene derivative products are converted for end-uses in the food industry, health and beauty products, detergents, and automotive products.

•In the polyester stream, the Company begins with paraxylene and glycol feedstocks, converting them through a series of intermediate materials to ultimately produce copolyesters. Eastman can add specialty monomers to copolyesters to provide clear, tough, chemically resistant product characteristics. As a result, the Company's copolyesters effectively compete with materials such as polycarbonate and acrylic. The polyester stream is now leveraging polyester renewal technology to enable various waste plastics to be recycled into high quality, specialty copolyester products.

•In the alkylamines stream, the Company begins with ammonia and alcohol feedstocks to produce methylamines and higher alkylamines, which can then be further converted into alkylamine derivatives. The Company's alkylamines products are primarily used in agriculture, water treatment, consumables, animal nutrition, and oil and gas end-markets.

The Company leverages its expertise and innovation in cellulose and acetyl, olefins, polyester, and alkylamine chemistries and technologies to meet demand and create new uses and opportunities for the Company's products in key markets. Through integration and optimization across these streams, the Company is able to create unique and differentiated products that have a performance advantage over competitive materials.

19

Sources and Availability of Raw Materials and Energy

Eastman purchases a majority of its key raw materials and energy through different contract mechanisms, generally of one to three years in initial duration with renewal or cancellation options for each party. Most of these agreements do not require the Company to purchase materials or energy if its operations are reduced or idle. The cost of raw materials and energy is generally based on market price at the time of purchase; however, from time to time Eastman uses derivative financial instruments for certain key raw materials to mitigate the impact of market price fluctuations. Key raw materials include propane, propylene, paraxylene, methanol, cellulose, fatty alcohol, polyvinyl alcohol, and a wide variety of precursors for specialty organic chemicals. Key purchased energy sources include natural gas, coal, and electricity. The Company has multiple suppliers for most key raw materials and energy and uses quality management principles, such as the establishment of long-term relationships with suppliers and ongoing performance assessments and benchmarking, as part of its supplier selection process. When appropriate, the Company purchases raw materials from a single source supplier to maximize quality and reduce cost and has contingency plans to minimize the potential impact of any supply disruptions from single source suppliers.

While temporary shortages of raw materials and energy may occasionally occur, these items are generally sufficiently available to cover current and projected requirements. However, their continuous availability and cost are subject to unscheduled plant interruptions occurring during periods of high demand, domestic and world market conditions, changes in government regulation, the ongoing COVID-19 coronavirus global pandemic ("COVID-19"), natural disasters, war or other outbreak of hostilities or terrorism or other political factors, or breakdown or degradation of transportation infrastructure. Eastman's operations or products have in the past, and may in the future, be adversely affected by these factors. See "Management's Discussion and Analysis of Financial Condition and Results of Operations - Risk Factors" in Part II, Item 7 of this Annual Report. The Company's raw material and energy costs as a percent of total cost of operations were approximately 35 percent in 2020. For additional information about raw materials, see Exhibit 99.02 "Product and Raw Material Information" of this Annual Report.

Intellectual Property, Trademarks, and Licensing

While Eastman's intellectual property portfolio is an important Company asset which it expands and vigorously protects globally through a combination of patents, trademarks, copyrights, and trade secrets, neither its business as a whole nor any particular operating segment is materially dependent upon any one particular patent, trademark, copyright, or trade secret. As a producer of a broad range of advanced materials, specialty additives, chemicals, and fibers, Eastman owns over 800 active United States patents and more than 1,500 active foreign patents, expiring at various times over several years, and owns over 5,300 active worldwide trademark applications and registrations. Eastman continues to actively protect its intellectual property. As the laws of many countries do not protect intellectual property to the same extent as the laws of the United States, Eastman cannot ensure that it will be able to adequately protect its intellectual property assets outside the United States. See "Management's Discussion and Analysis of Financial Condition and Results of Operations - Risk Factors" in Part II, Item 7 of this Annual Report.

The Company pursues opportunities to license proprietary technology to third parties where it has determined competitive impact to its businesses will be minimal. These arrangements typically are structured to require payments at significant project milestones such as signing, completion of design, and start-up.

Information Security

The Company employs information systems to support its business, enable Company transformation, and deploy digital services. The Company utilizes a risk-based, multi-layered information security approach following the U.S. National Institute of Standards and Technology Cybersecurity Framework, including dedicated security operations center monitoring; network-based and host-based protections; a Privacy Council focused upon adherence to privacy regulations; privilege access management controls; annual and on-going information security training and targeted exercises for employees and third-parties; encryption of data, backup, recovery, and testing; regular internal and external assessments against information security best practices; and benchmarking utilizing external third parties. As with other manufacturing companies, the Company from time to time experiences attempted cyber-attacks of its information systems. None of these attempts has resulted in a material adverse impact on the Company's operations or financial results, any penalties or settlements. Management, including the Chief Information Officer ("CIO"), reviews information security performance and recent cybersecurity industry trends at least quarterly, and at least annually reviews information security strategy with executive management. See "Management's Discussion and Analysis of Financial Condition and Results of Operations – Risk Factors" in Part II, Item 7 of this Annual Report.

20

Under the Company's enterprise-wide approach to risk management, cybersecurity and security of Company information is a "high-level" risk that is reported to and overseen by the Audit Committee of the Board of Directors, which consists of five non-employee independent directors, three with information systems experience and one with a Certified Information Privacy Professional (CIPP) certification. The CIO provides an overview of information security performance and recent cybersecurity industry trends to the Audit Committee of the Board of Directors at least six times per year.

Human Capital

Effective attraction, development, and retention of our employees ("human capital"), including workforce and management development, inclusion and diversity initiatives, succession management, corporate culture and leadership quality, morale, and compensation and benefits are vital to the success of Eastman's innovation-driven growth strategy. Management's goal is to continue building a high performing, inclusive culture where everyone is inspired to do their best work. The Compensation and Management Development Committee of the Board of Directors oversees workforce and senior management development and the Board of Directors monitors the culture of the Company and leadership quality, morale, and development.

Eastman places a strong emphasis on the health, safety and well-being of employees — both at work and at home. Eastman's "zero-incident mindset" takes a holistic approach to people and processes by fostering the right behaviors, values, and culture to ensure that employees are operating responsibly, accountably, and safely. For 2020, in addition to annual process and personal safety performance expectations (see "Executive Compensation" in Part III, Item 11 of this Annual Report), this included safety and wellness protocols for protection against the COVID-19 virus for employees returning to the workplace. The Company's focus on well-being also includes physical, emotional, and financial health of employees and their families, with on-site and on-demand resources such as fitness classes, health coaches, and financial counselors.

Increased efforts for more diverse representation in the global employee population of approximately 14,500 people worldwide include commitment to be a manufacturing and chemical industry leader in inclusion and diversity. The Company has committed to achieve gender parity globally and to be an industry leader in racial and ethnic diversity in the United States by 2030; in 2020, business and technical employees were 36 percent female globally and 14 percent racially and ethnically diverse in the United States. The Executive Team, the top employee leadership of the Company, is 13 percent female and 25 percent racially and ethnically diverse (see "Information About our Executive Officers" in Part I of this Annual Report). The non-employee directors of Eastman's Board of Directors are 40 percent female and 20 percent racially and ethnically diverse (see "Directors, Executive Officers and Corporate Governance"— "Election of Directors" in Part III. Item 10 of this Annual Report).

21

Customers

Eastman has an extensive customer base and, while it is not dependent on any one customer, loss of certain top customers could adversely affect the Company until such business is replaced. The top 100 customers accounted for approximately 55 percent of the Company's 2020 sales revenue. No single customer accounted for 10 percent or more of the Company's consolidated sales revenue during 2020.

Compliance With Environmental and Other Government Regulations

The Company is subject to significant and complex governmental laws and regulations, both in the U.S. and internationally, which require and will continue to require significant expenditures to remain in compliance and may, depending on specific facts and circumstances, impact the Company's competitive position. (See "Management's Discussion and Analysis of Financial Condition and Results of Operations - Risk Factors -- Legislative, regulatory, or voluntary actions could increase the Company's future health, safety, and environmental compliance costs." in Part II, Item 7 of this Annual Report.) These include health, safety, and environmental laws and regulations; site security regulations; chemical control laws; laws protecting intellectual property; privacy, data sharing and data protection laws; laws regulating energy generation and distribution, such as utilities, pipelines and co-generation facilities; and customs laws and laws regulating import and export of products and technology. As described below, the most significant capital and other expenditures are for compliance with environmental and health and safety laws. In addition to these regulations, compliance with chemical control laws (including the U.S. Toxic Substances Control Act, the U.S. Federal Insecticide, Fungicide, and Rodenticide Act and similar non-U.S. counterparts, and the Registration, Evaluation, Authorisation and Restriction of Chemicals ("REACH") program in the European Union) and laws protecting intellectual property (see "Intellectual Property, Trademarks, and Licensing") have the most impact on the Company's day-to-day operations and competitive position.

Environmental

The Company is subject to laws, regulations, and legal requirements relating to the use, storage, handling, generation, transportation, emission, discharge, disposal, remediation of, and exposure to, hazardous and non-hazardous substances and wastes in all of the countries in which it does business. These health, safety, and environmental considerations are a priority in the Company's planning for all existing and new products and processes. The Environmental, Safety, and Sustainability Committee of Eastman's Board of Directors oversees the Company's policies and practices concerning health, safety, and the environment and its processes for complying with related laws and regulations and monitors related matters.

The Company's policy is to operate its plants and facilities in compliance with all applicable laws and regulations such that it protects the environment and the health and safety of its employees and the public. The Company intends to continue to make expenditures for environmental protection and improvements in a timely manner consistent with its policies and with available technology. In some cases, applicable environmental regulations such as those adopted under the Clean Air Act, Resource Conservation and Recovery Act, Comprehensive Environmental Response, Compensation, and Liability Act, and related actions of regulatory agencies determine the timing and amount of environmental costs incurred by the Company. Likewise, any new legislation or regulations related to greenhouse gas emissions, energy or climate change, or the repeal of such legislation or regulations, could impact the timing and amount of environmental costs incurred by the Company.

The Company accrues environmental costs when it is probable that the Company has incurred a liability at a contaminated site and the amount can be reasonably estimated. In some instances, the amount cannot be reasonably estimated due to insufficient information, particularly as to the nature and timing of future expenditures. In these cases, the liability is monitored until such time that sufficient information exists. With respect to a contaminated site, the amount accrued reflects liabilities expected to be paid out within approximately 30 years as well as the Company's assumptions about remediation requirements at the contaminated site, the nature of the remedy, the outcome of discussions with regulatory agencies and other potentially responsible parties at multi-party sites, and the number and financial viability of other potentially responsible parties. Changes in the estimates on which the accruals are based, unanticipated government enforcement action, or changes in health, safety, environmental, and chemical control regulations, and testing requirements could result in higher or lower costs.

The Company does not currently expect near term environmental capital expenditures arising from requirements of environmental laws and regulations to materially impact the Company's planned level of annual capital expenditures for environmental control facilities. Other matters concerning health, safety, and the environment are discussed in "Management's Discussion and Analysis of Financial Condition and Results of Operations" in Part II, Item 7 and in Note 1, "Significant Accounting Policies"; Note 12, "Environmental Matters and Asset Retirement Obligations"; and Note 21, "Reserve Rollforwards", to the Company's consolidated financial statements in Part II, Item 8 of this Annual Report.

22

Eastman's cash expenditures related to environmental protection and improvement were $265 million, $244 million, and $274 million in 2020, 2019, and 2018, respectively, and include operating costs associated with environmental protection equipment and facilities, engineering costs, and construction costs. These cash expenditures include environmental capital expenditures of approximately $42 million, $27 million, and $44 million in 2020, 2019, and 2018, respectively.

Health and Safety

Eastman places a strong emphasis on the health, safety and well-being of employees. Eastman's "zero-incident mindset" takes a holistic approach to people and processes by fostering the right behaviors, values, and culture to ensure that employees are operating responsibly, accountably, and safely. See "Human Capital". Under the U.S. Occupational Safety and Health Act of 1970, as administered by the Occupational Safety and Health Administration ("OSHA"), some of the Company's operations are subject to workplace standards under OSHA's Process Safety Management program. From time to time, the Company may incur significant capital expenditures to maintain compliance with the requirements of this program.

Available Information - Securities and Exchange Commission ("SEC") Filings

Eastman makes available free of charge, in the "Investors - SEC Information" section of its Internet website (www.eastman.com), its annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 as soon as reasonably practicable after electronically filing such material with, or furnishing it to, the SEC. The SEC maintains an Internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC at http://www.sec.gov.

23

| ITEM 1A. RISK FACTORS | ||

For identification and discussion of the most significant risks applicable to the Company and its business, see "Management's Discussion and Analysis of Financial Condition and Results of Operations - Risk Factors" in Part II, Item 7 of this Annual Report.

| ITEM 1B. UNRESOLVED STAFF COMMENTS | ||

None.

| INFORMATION ABOUT OUR EXECUTIVE OFFICERS | ||

Certain information about Eastman's executive officers is provided below: