UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

For the quarterly period ended June 30, 2023

OR

For the transition period from __________ to __________.

Commission File Number: 001-38002

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||||||||

| (Address of principal executive offices) | (Zip Code) | |||||||||||||

Registrant’s telephone number, including area code: (786 ) 209-3368

Securities registered pursuant to Section 12(b) of the Securities Exchange Act of 1934:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

The NASDAQ Stock Market LLC | ||||||||

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

Smaller reporting company ☐ Emerging Growth Company ☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No x

Indicate the number of shares outstanding of each of the issuer's classes of common stock, as of the latest practicable date.

| Class | Outstanding at June 30, 2023 | |||||||

| Common stock, par value $0.004 per share | ||||||||

| INDEX | ||||||||

| PART I. - FINANCIAL INFORMATION | Page No. | |||||||

| Item 1. | Financial Statements (Unaudited) | |||||||

Consolidated Statements of Operations - Three months ended June 30, 2023 and June 30, 2022 | ||||||||

Consolidated Statements of Operations - Six months ended June 30, 2023 and June 30, 2022 | ||||||||

Consolidated Statements of Comprehensive Income - Three months ended June 30, 2023 and June 30, 2022 | ||||||||

Consolidated Statements of Comprehensive Income - Six months ended June 30, 2023 and June 30, 2022 | ||||||||

Consolidated Balance Sheets - June 30, 2023 and December 31, 2022 | ||||||||

Consolidated Statements of Cash Flows - Six months ended June 30, 2023 and June 30, 2022 | ||||||||

| Notes to Consolidated Financial Statements | ||||||||

| Item 2. | Management's Discussion and Analysis of Financial Condition and Results of Operations | |||||||

| Item 3. | Quantitative and Qualitative Disclosures About Market Risk | |||||||

| Item 4. | Controls and Procedures | |||||||

| PART II. - OTHER INFORMATION | ||||||||

| Item 1. | Legal Proceedings | |||||||

| Item 1A. | Risk Factors | |||||||

| Item 5. | Other Information | |||||||

| Item 6. | Exhibits | |||||||

| SIGNATURES | ||||||||

1

PART I - FINANCIAL INFORMATION

Item 1. Financial Statements (Unaudited)

LAUREATE EDUCATION, INC. AND SUBSIDIARIES

Consolidated Statements of Operations

IN THOUSANDS, except per share amounts

| For the three months ended June 30, | 2023 | 2022 | |||||||||

| (Unaudited) | (Unaudited) | ||||||||||

| Revenues | $ | $ | |||||||||

| Costs and expenses: | |||||||||||

| Direct costs | |||||||||||

| General and administrative expenses | |||||||||||

| Loss on impairment of assets | |||||||||||

| Operating income | |||||||||||

| Interest income | |||||||||||

| Interest expense | ( | ( | |||||||||

| Other (expense) income, net | ( | ||||||||||

| Foreign currency exchange loss, net | ( | ( | |||||||||

| Gain on disposal of subsidiaries, net | |||||||||||

| Income from continuing operations before income taxes and equity in net loss of affiliates | |||||||||||

| Income tax expense | ( | ( | |||||||||

| Equity in net loss of affiliates, net of tax | ( | ||||||||||

| Income from continuing operations | |||||||||||

(Loss) income from discontinued operations, net of tax of $ | ( | ||||||||||

| Net income | |||||||||||

| Net income attributable to noncontrolling interests | ( | ( | |||||||||

| Net income attributable to Laureate Education, Inc. | $ | $ | |||||||||

| Basic earnings (loss) per share: | |||||||||||

| Income from continuing operations | $ | $ | |||||||||

| (Loss) income from discontinued operations | ( | ||||||||||

| Basic earnings per share | $ | $ | |||||||||

| Diluted earnings (loss) per share: | |||||||||||

| Income from continuing operations | $ | $ | |||||||||

| (Loss) income from discontinued operations | ( | ||||||||||

| Diluted earnings per share | $ | $ | |||||||||

2

LAUREATE EDUCATION, INC. AND SUBSIDIARIES

Consolidated Statements of Operations

IN THOUSANDS, except per share amounts

| For the six months ended June 30, | 2023 | 2022 | |||||||||

| (Unaudited) | (Unaudited) | ||||||||||

| Revenues | $ | $ | |||||||||

| Costs and expenses: | |||||||||||

| Direct costs | |||||||||||

| General and administrative expenses | |||||||||||

| Loss on impairment of assets | |||||||||||

| Operating income | |||||||||||

| Interest income | |||||||||||

| Interest expense | ( | ( | |||||||||

| Other income (expense), net | ( | ||||||||||

| Foreign currency exchange loss, net | ( | ( | |||||||||

| Gain on disposal of subsidiaries, net | |||||||||||

| Income from continuing operations before income taxes and equity in net (loss) income of affiliates | |||||||||||

| Income tax expense | ( | ( | |||||||||

| Equity in net (loss) income of affiliates, net of tax | ( | ||||||||||

| Income (loss) from continuing operations | ( | ||||||||||

(Loss) income from discontinued operations, net of tax of $ | ( | ||||||||||

| Net income (loss) | ( | ||||||||||

| Net loss attributable to noncontrolling interests | |||||||||||

| Net income (loss) attributable to Laureate Education, Inc. | $ | $ | ( | ||||||||

| Basic and diluted earnings (loss) per share: | |||||||||||

| Income (loss) from continuing operations | $ | $ | ( | ||||||||

| (Loss) income from discontinued operations | ( | ||||||||||

| Basic and diluted earnings per share | $ | $ | |||||||||

The accompanying notes are an integral part of these consolidated financial statements.

3

LAUREATE EDUCATION, INC. AND SUBSIDIARIES

Consolidated Statements of Comprehensive Income

IN THOUSANDS

| For the three months ended June 30, | 2023 | 2022 | |||||||||

| (Unaudited) | (Unaudited) | ||||||||||

| Net income | $ | $ | |||||||||

| Other comprehensive income: | |||||||||||

Foreign currency translation adjustment, net of tax of $ | |||||||||||

| Total other comprehensive income | |||||||||||

| Comprehensive income | |||||||||||

| Net comprehensive income attributable to noncontrolling interests | ( | ( | |||||||||

| Comprehensive income attributable to Laureate Education, Inc. | $ | $ | |||||||||

The accompanying notes are an integral part of these consolidated financial statements.

4

LAUREATE EDUCATION, INC. AND SUBSIDIARIES

Consolidated Statements of Comprehensive Income

IN THOUSANDS

| For the six months ended June 30, | 2023 | 2022 | |||||||||

| (Unaudited) | (Unaudited) | ||||||||||

| Net income (loss) | $ | $ | ( | ||||||||

| Other comprehensive income: | |||||||||||

Foreign currency translation adjustment, net of tax of $ | |||||||||||

Minimum pension liability adjustment, net of tax of $ | |||||||||||

| Total other comprehensive income | |||||||||||

| Comprehensive income | |||||||||||

| Net comprehensive loss attributable to noncontrolling interests | |||||||||||

| Comprehensive income attributable to Laureate Education, Inc. | $ | $ | |||||||||

The accompanying notes are an integral part of these consolidated financial statements.

5

LAUREATE EDUCATION, INC. AND SUBSIDIARIES

Consolidated Balance Sheets

IN THOUSANDS, except per share amounts

| June 30, 2023 | December 31, 2022 | ||||||||||

| Assets | (Unaudited) | ||||||||||

| Current assets: | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Restricted cash | |||||||||||

| Receivables: | |||||||||||

| Accounts and notes receivable | |||||||||||

| Other receivables | |||||||||||

| Allowance for doubtful accounts | ( | ( | |||||||||

| Receivables, net | |||||||||||

| Income tax receivable | |||||||||||

| Prepaid expenses and other current assets | |||||||||||

| Current assets held for sale | |||||||||||

| Total current assets | |||||||||||

| Property and equipment: | |||||||||||

| Land | |||||||||||

| Buildings | |||||||||||

| Furniture, equipment and software | |||||||||||

| Leasehold improvements | |||||||||||

| Construction in-progress | |||||||||||

| Accumulated depreciation and amortization | ( | ( | |||||||||

| Property and equipment, net | |||||||||||

| Operating lease right-of-use assets, net | |||||||||||

| Goodwill | |||||||||||

| Tradenames, net | |||||||||||

| Deferred costs, net | |||||||||||

| Deferred income taxes | |||||||||||

| Other assets | |||||||||||

| Long-term assets held for sale | |||||||||||

| Total assets | $ | $ | |||||||||

The accompanying notes are an integral part of these consolidated financial statements.

6

LAUREATE EDUCATION, INC. AND SUBSIDIARIES

Consolidated Balance Sheets (continued)

IN THOUSANDS, except per share amounts

| June 30, 2023 | December 31, 2022 | ||||||||||

| Liabilities and stockholders' equity | (Unaudited) | ||||||||||

| Current liabilities: | |||||||||||

| Accounts payable | $ | $ | |||||||||

| Accrued expenses | |||||||||||

| Accrued compensation and benefits | |||||||||||

| Deferred revenue and student deposits | |||||||||||

| Current portion of operating leases | |||||||||||

| Current portion of long-term debt and finance leases | |||||||||||

| Income taxes payable | |||||||||||

| Other current liabilities | |||||||||||

| Current liabilities held for sale | |||||||||||

| Total current liabilities | |||||||||||

| Long-term operating leases, less current portion | |||||||||||

| Long-term debt and finance leases, less current portion | |||||||||||

| Deferred compensation | |||||||||||

| Income taxes payable | |||||||||||

| Deferred income taxes | |||||||||||

| Other long-term liabilities | |||||||||||

| Long-term liabilities held for sale | |||||||||||

| Total liabilities | |||||||||||

| Redeemable equity | |||||||||||

| Stockholders' equity: | |||||||||||

Preferred stock, par value $ | |||||||||||

Common stock, par value $ | |||||||||||

| Additional paid-in capital | |||||||||||

| Retained earnings | |||||||||||

| Accumulated other comprehensive loss | ( | ( | |||||||||

Treasury stock at cost ( | ( | ||||||||||

| Total Laureate Education, Inc. stockholders' equity | |||||||||||

| Noncontrolling interests | ( | ( | |||||||||

| Total stockholders' equity | |||||||||||

| Total liabilities and stockholders' equity | $ | $ | |||||||||

The accompanying notes are an integral part of these consolidated financial statements.

7

LAUREATE EDUCATION, INC. AND SUBSIDIARIES

Consolidated Statements of Cash Flows

IN THOUSANDS

| For the six months ended June 30, | 2023 | 2022 | |||||||||

| Cash flows from operating activities | (Unaudited) | (Unaudited) | |||||||||

| Net income (loss) | $ | $ | ( | ||||||||

| Adjustments to reconcile net income to net cash provided by operating activities: | |||||||||||

| Depreciation and amortization | |||||||||||

| Amortization of operating lease right-of-use assets | |||||||||||

| Loss on impairment of assets | |||||||||||

| Loss (gain) on sales and disposal of subsidiaries and property and equipment, net | ( | ||||||||||

| Non-cash interest expense | |||||||||||

| Non-cash share-based compensation expense | |||||||||||

| Bad debt expense | |||||||||||

| Deferred income taxes | ( | ||||||||||

| Unrealized foreign currency exchange loss | |||||||||||

| Other, net | ( | ( | |||||||||

| Changes in operating assets and liabilities: | |||||||||||

| Receivables | ( | ( | |||||||||

| Prepaid expenses and other assets | ( | ( | |||||||||

| Accounts payable and accrued expenses | ( | ||||||||||

| Income tax receivable/payable, net | ( | ||||||||||

| Deferred revenue and other liabilities | ( | ( | |||||||||

| Net cash provided by operating activities | |||||||||||

| Cash flows from investing activities | |||||||||||

| Purchase of property and equipment | ( | ( | |||||||||

| Expenditures for deferred costs | ( | ||||||||||

| Receipts from sales of discontinued operations and property and equipment | |||||||||||

| Net cash (used in) provided by investing activities | ( | ||||||||||

| Cash flows from financing activities | |||||||||||

| Proceeds from issuance of long-term debt, net of original issue discount | |||||||||||

| Payments on long-term debt | ( | ( | |||||||||

| Payment of dividend equivalent rights for vested share-based awards | ( | ( | |||||||||

| Payments to purchase noncontrolling interests | ( | ||||||||||

| Proceeds from exercise of stock options | |||||||||||

| Withholding of shares to satisfy tax withholding for vested stock awards and exercised stock options | ( | ( | |||||||||

| Payments to repurchase common stock | ( | ||||||||||

| Net cash used in financing activities | ( | ( | |||||||||

| Effects of exchange rate changes on Cash and cash equivalents and Restricted cash | |||||||||||

| Change in cash included in current assets held for sale | ( | ||||||||||

| Net change in Cash and cash equivalents and Restricted cash | ( | ||||||||||

| Cash and cash equivalents and Restricted cash at beginning of period | |||||||||||

| Cash and cash equivalents and Restricted cash at end of period | $ | $ | |||||||||

The accompanying notes are an integral part of these consolidated financial statements.

8

Laureate Education, Inc. and Subsidiaries

Notes to Consolidated Financial Statements

(Dollars and shares in thousands)

Note 1. Description of Business

Laureate Education, Inc. and subsidiaries (hereinafter Laureate, we, us, our, or the Company) provide higher education programs and services to students through licensed universities and higher education institutions (institutions). Laureate's programs are provided through institutions that are campus-based and through electronically distributed educational programs (online). We are domiciled in Delaware as a public benefit corporation, a demonstration of our long-term commitment to our mission to benefit our students and society. The Company completed its initial public offering (IPO) on February 6, 2017, and its shares are listed on the Nasdaq Global Select Market under the symbol “LAUR.”

Note 2. Revenue

Revenue Recognition

Laureate's revenues primarily consist of tuition and educational service revenues. We also generate other revenues from student fees and other education-related activities. These other revenues are less material to our overall financial results and have a tendency to trend with tuition revenues. Revenues are recognized when control of the promised goods or services is transferred to our customers in an amount that reflects the consideration we expect to be entitled to in exchange for those goods or services. These revenues are recognized net of scholarships and other discounts, refunds and waivers. Laureate's institutions have various billing and academic cycles.

We determine revenue recognition through the five-step model prescribed by ASC Topic 606, Revenue from Contracts with Customers, as follows:

•Identification of the contract, or contracts, with a customer;

•Identification of the performance obligations in the contract;

•Determination of the transaction price;

•Allocation of the transaction price to the performance obligations in the contract; and

•Recognition of revenue when, or as, we satisfy a performance obligation.

We assess collectibility on a portfolio basis prior to recording revenue. Generally, students cannot re-enroll for the next academic session without satisfactory resolution of any past-due amounts. If a student withdraws from an institution, Laureate's obligation to issue a refund depends on the refund policy at that institution and the timing of the student's withdrawal. Generally, our refund obligations are reduced over the course of the academic term. We record refunds as a reduction of deferred revenue as applicable.

9

The following table shows the components of Revenues by reportable segment and as a percentage of total revenue for the three months ended June 30, 2023 and 2022:

| Mexico | Peru | Corporate(1) | Total | ||||||||||||||

| 2023 | |||||||||||||||||

| Tuition and educational services | $ | $ | $ | $ | % | ||||||||||||

| Other | ( | % | |||||||||||||||

| Gross revenue | ( | % | |||||||||||||||

| Less: Discounts / waivers / scholarships | ( | ( | ( | ( | % | ||||||||||||

| Total | $ | $ | $ | ( | $ | % | |||||||||||

| 2022 | |||||||||||||||||

| Tuition and educational services | $ | $ | $ | $ | % | ||||||||||||

| Other | % | ||||||||||||||||

| Gross revenue | % | ||||||||||||||||

| Less: Discounts / waivers / scholarships | ( | ( | ( | ( | % | ||||||||||||

| Total | $ | $ | $ | $ | % | ||||||||||||

(1) Includes the elimination of inter-segment revenues.

The following table shows the components of Revenues by reportable segment and as a percentage of total revenue for the six months ended June 30, 2023 and 2022:

| Mexico | Peru | Corporate(1) | Total | ||||||||||||||

| 2023 | |||||||||||||||||

| Tuition and educational services | $ | $ | $ | $ | % | ||||||||||||

| Other | ( | % | |||||||||||||||

| Gross revenue | ( | % | |||||||||||||||

| Less: Discounts / waivers / scholarships | ( | ( | ( | ( | % | ||||||||||||

| Total | $ | $ | $ | ( | $ | % | |||||||||||

| 2022 | |||||||||||||||||

| Tuition and educational services | $ | $ | $ | $ | % | ||||||||||||

| Other | % | ||||||||||||||||

| Gross revenue | % | ||||||||||||||||

| Less: Discounts / waivers / scholarships | ( | ( | ( | ( | % | ||||||||||||

| Total | $ | $ | $ | $ | % | ||||||||||||

(1) Includes the elimination of inter-segment revenues.

All of our contract assets are considered accounts receivable and are included within the Accounts and notes receivable balance in the accompanying Consolidated Balance Sheets. Total accounts receivable from our contracts with students were $186,729 and $133,105 as of June 30, 2023 and December 31, 2022, respectively. The increase in the contract assets balance at June 30, 2023 compared to December 31, 2022 was primarily driven by enrollment cycles. The first and third calendar quarters generally coincide with the primary and secondary intakes for our larger institutions. All contract asset amounts are classified as current.

10

Note 3. Assets Held for Sale

During the second quarter of 2023, two of the Company’s subsidiaries that operate K-12 educational programs in Mexico met the criteria for classification as held for sale under ASC 360-10-45-9, “Long-Lived Assets Classified as Held for Sale.” The sale of the K-12 campuses is intended to allow the Mexico segment to focus on its core business. The assets and liabilities of this disposal group are recorded at the lower of their carrying values or their estimated fair values less costs to sell. The planned sale of this disposal group does not represent a strategic shift and therefore does not qualify for presentation as a discontinued operation in the Consolidated Financial Statements. The carrying amounts of the major classes of assets and liabilities that were classified as held for sale are presented in the following table:

| June 30, 2023 | December 31, 2022 | ||||||||||

| Assets Held for Sale | |||||||||||

| Cash and cash equivalents | $ | $ | |||||||||

| Receivables, net | |||||||||||

| Property and equipment, net | |||||||||||

| Operating lease right-of-use assets, net | |||||||||||

| Other assets | |||||||||||

| Total assets held for sale | $ | $ | |||||||||

| Liabilities Held for Sale | |||||||||||

| Deferred revenue and student deposits | $ | ||||||||||

| Operating leases, including current portion | |||||||||||

| Long-term debt, including current portion | |||||||||||

| Other liabilities | |||||||||||

| Total liabilities held for sale | $ | $ | |||||||||

The long-term debt balance represents a finance lease for property.

Note 4. Business and Geographic Segment Information

Laureate’s educational services are offered through two reportable segments: Mexico and Peru. Laureate determines its segments based on information utilized by the chief operating decision maker to allocate resources and assess performance.

Our segments generate revenues by providing an education that emphasizes profession-oriented fields of study with undergraduate and graduate degrees in a wide range of disciplines. Our educational offerings utilize campus-based, online and hybrid (a combination of online and in-classroom) courses and programs to deliver their curriculum. The Mexico and Peru markets are characterized by what we believe is a significant imbalance between supply and demand. The demand for higher education is large and growing and is fueled by several demographic and economic factors, including a growing middle class, global growth in services and technology-related industries and recognition of the significant personal and economic benefits gained by graduates of higher education institutions. The target demographics are primarily 18- to 24-year-olds in both countries in which we compete. We compete with other private higher education institutions on the basis of price, educational quality, reputation and location. We believe that we compare favorably with competitors because of our focus on quality, professional-oriented curriculum and the competitive advantages provided by our network. There are a number of private and public institutions in both countries in which we operate, and it is difficult to predict how the markets will evolve and how many competitors there will be in the future. We expect competition to increase as the Mexican and Peruvian markets mature.

11

Essentially all of our revenues were generated from private pay sources as there are no material government-sponsored loan programs in Mexico or Peru. Specifics related to both of our reportable segments are discussed below.

In Mexico, the private sector plays a meaningful role in higher education, bridging supply and demand imbalances created by a lack of capacity at public universities. Laureate owns two nationally licensed institutions and is present throughout the country with a footprint of over 35 campuses. Students in our Mexican institutions typically finance their own education.

In Peru, private universities are increasingly providing the capacity to meet growing demand in the higher-education market. Laureate owns three institutions in Peru, with a footprint of 19 campuses.

Inter-segment transactions are accounted for in a similar manner as third-party transactions and are eliminated in consolidation. The Corporate amounts presented in the following tables include corporate charges that were not allocated to our reportable segments and adjustments to eliminate inter-segment items.

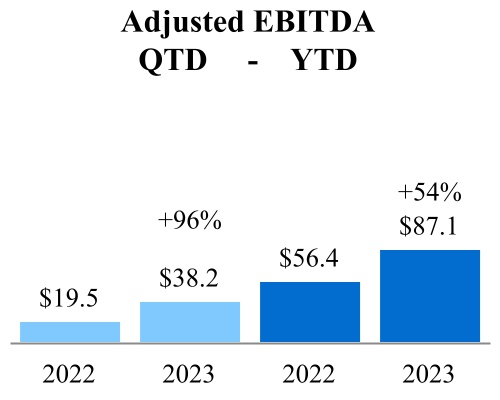

We evaluate segment performance based on Adjusted EBITDA, which is a non-GAAP performance measure defined as Income from continuing operations before income taxes and equity in net income of affiliates, adding back the following items: Gain on disposal of subsidiaries, net, Foreign currency exchange loss, net, Other (expense) income, net, Interest expense, Interest income, Depreciation and amortization expense, Loss on impairment of assets, Share-based compensation expense and expenses related to our Excellence-in-Process (EiP) initiative. Our EiP initiative was completed as of December 31, 2021, except for certain EiP expenses related to the completion of programs that began in prior periods. EiP was an enterprise-wide initiative to optimize and standardize Laureate’s processes, creating vertical integration of procurement, information technology, finance, accounting and human resources. It included the establishment of regional shared services organizations (SSOs), as well as improvements to the Company's system of internal controls over financial reporting. The EiP initiative also included other back- and mid-office areas, as well as certain student-facing activities, expenses associated with streamlining the organizational structure, an enterprise-wide program aimed at revenue growth, and certain non-recurring costs that were incurred in connection with previous dispositions.

Adjusted EBITDA is a key measure used by our management and Board of Directors to understand and evaluate our core operating performance and trends, to prepare and approve our annual budget and to develop short- and long-term operational plans. In particular, the exclusion of certain expenses in calculating Adjusted EBITDA can provide a useful measure for period-to-period comparisons of our core business. Additionally, Adjusted EBITDA is a key financial measure used by the compensation committee of our Board of Directors and our Chief Executive Officer in connection with the payment of incentive compensation to our executive officers and other members of our management team. Accordingly, we believe that Adjusted EBITDA provides useful information to investors and others in understanding and evaluating our operating results in the same manner as our management and Board of Directors. We use total assets as the measure of assets for reportable segments.

12

The following tables provide financial information for our reportable segments, including a reconciliation of Adjusted EBITDA to Income from continuing operations before income taxes and equity in net income of affiliates, as reported in the Consolidated Statements of Operations:

| For the three months ended | For the six months ended | ||||||||||||||||||||||

| June 30, | June 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| Revenues | |||||||||||||||||||||||

| Mexico | $ | $ | $ | $ | |||||||||||||||||||

| Peru | |||||||||||||||||||||||

| Corporate | ( | ( | |||||||||||||||||||||

| Total Revenues | $ | $ | $ | $ | |||||||||||||||||||

| Adjusted EBITDA of reportable segments | |||||||||||||||||||||||

| Mexico | $ | $ | $ | $ | |||||||||||||||||||

| Peru | |||||||||||||||||||||||

| Total Adjusted EBITDA of reportable segments | |||||||||||||||||||||||

| Reconciling items: | |||||||||||||||||||||||

| Corporate | ( | ( | ( | ( | |||||||||||||||||||

| Depreciation and amortization expense | ( | ( | ( | ( | |||||||||||||||||||

| Loss on impairment of assets | ( | ( | ( | ||||||||||||||||||||

| Share-based compensation expense | ( | ( | ( | ( | |||||||||||||||||||

| EiP expenses | ( | ( | |||||||||||||||||||||

| Operating income | |||||||||||||||||||||||

| Interest income | |||||||||||||||||||||||

| Interest expense | ( | ( | ( | ( | |||||||||||||||||||

| Other (expense) income, net | ( | ( | |||||||||||||||||||||

| Foreign currency loss, net | ( | ( | ( | ( | |||||||||||||||||||

| Gain on disposal of subsidiaries, net | |||||||||||||||||||||||

| Income from continuing operations before income taxes and equity in net income of affiliates | $ | $ | $ | $ | |||||||||||||||||||

| June 30, 2023 | December 31, 2022 | ||||||||||

| Assets | |||||||||||

| Mexico | $ | $ | |||||||||

| Peru | |||||||||||

| Corporate | |||||||||||

| Total assets | $ | $ | |||||||||

Note 5. Goodwill

The change in the net carrying amount of Goodwill from December 31, 2022 through June 30, 2023 was composed of the following items:

| Mexico | Peru | Total | |||||||||

| Balance at December 31, 2022 | $ | $ | $ | ||||||||

| Currency translation adjustments | |||||||||||

| Balance at June 30, 2023 | $ | $ | $ | ||||||||

13

Note 6. Debt

Outstanding long-term debt was as follows:

| June 30, 2023 | December 31, 2022 | ||||||||||

| Senior long-term debt: | |||||||||||

| Senior Secured Credit Facility (stated maturity date October 7, 2024) | $ | $ | |||||||||

| Other debt: | |||||||||||

| Lines of credit | |||||||||||

| Notes payable and other debt | |||||||||||

| Total senior and other debt | |||||||||||

| Finance lease obligations and sale-leaseback financings | |||||||||||

| Total long-term debt and finance leases | |||||||||||

| Less: total unamortized deferred financing costs | |||||||||||

| Less: current portion of long-term debt and finance leases | |||||||||||

| Long-term debt and finance leases, less current portion | $ | $ | |||||||||

Senior Secured Credit Facility

Under our Third Amended and Restated Credit Agreement (the Third A&R Credit Agreement), the Company maintains a revolving credit facility (the Senior Secured Credit Facility) that has a borrowing capacity of $410,000 and a maturity date of October 7, 2024. As of June 30, 2023 and December 31, 2022, the Senior Secured Credit Facility had a total outstanding balance of $88,000 and $100,000 , respectively.

Estimated Fair Value of Debt

As of June 30, 2023 and December 31, 2022, the estimated fair value of our debt approximated its carrying value.

Certain Covenants

As of June 30, 2023, our Third A&R Credit Agreement contained certain negative covenants including, among others: (1) limitations on additional indebtedness; (2) limitations on dividends; (3) limitations on asset sales, including the sale of ownership interests in subsidiaries and sale-leaseback transactions; and (4) limitations on liens, guarantees, loans or investments. The Third A&R Credit Agreement provides, solely with respect to the revolving credit facility, that the Company shall not permit its Consolidated Senior Secured Debt to Consolidated EBITDA ratio, as defined in the Third A&R Credit Agreement, to exceed 3.50 x as of the last day of each quarter commencing with the quarter ending December 31, 2019 and thereafter. The agreement also provides that if (i) the Company’s Consolidated Total Debt to Consolidated EBITDA ratio, as defined in the Third A&R Credit Agreement, is not greater than 4.75 x as of such date and (ii) less than 25 % of the revolving credit facility is utilized as of that date, then such financial covenant shall not apply. As of June 30, 2023, these conditions were satisfied and, therefore, we were not subject to the leverage ratio covenant. In addition, indebtedness at some of our locations contain financial maintenance covenants. We were in compliance with these covenants as of June 30, 2023.

Note 7. Leases

Laureate conducts a significant portion of its operations at leased facilities, including many of Laureate's higher education facilities and other office locations. In accordance with ASC Topic 842, “Leases,” Laureate analyzes each lease agreement to determine whether it should be classified as a finance lease or an operating lease.

Finance Leases

Our finance lease agreements are for property and equipment. The lease assets are included within buildings as well as furniture, equipment and software, and the related lease liability is included within debt and finance leases on the Consolidated Balance Sheets.

14

Operating Leases

Our operating lease agreements are primarily for real estate space and are included within operating lease right-of-use (ROU) assets and operating lease liabilities on the Consolidated Balance Sheets. The terms of our operating leases vary and generally contain renewal options. Certain of these operating leases provide for increasing rent over the term of the lease. Laureate also leases certain equipment under noncancellable operating leases, which are typically for terms of 60 months or less.

ROU assets represent our right to use an underlying asset for the lease term, and lease liabilities represent our obligation to make lease payments arising from the lease. ROU assets and lease liabilities are recognized at the commencement date of the lease based on the present value of lease payments over the lease term. Our variable lease payments consist of non-lease services related to the lease. Variable lease payments are excluded from the ROU assets and lease liabilities and are recognized in the period in which the obligation for those payments is incurred. As most of our leases do not provide an implicit rate, we use our incremental borrowing rate based on the information available at the commencement date in determining the present value of lease payments. Many of our lease agreements include options to extend the lease, which we do not include in our minimum lease terms unless they are reasonably certain to be exercised. Rental expense for lease payments related to operating leases is recognized on a straight-line basis over the lease term. On occasion, Laureate has entered into sublease agreements for certain leased office space; however, the sublease income from these agreements is immaterial.

Note 8. Commitments and Contingencies

Loss Contingencies

Laureate is subject to legal actions arising in the ordinary course of its business. In management's opinion, we have adequate legal defenses, insurance coverage and/or accrued liabilities with respect to the eventuality of such actions. We do not believe that any settlement would have a material impact on our Consolidated Financial Statements.

Income Tax Contingencies

As of June 30, 2023 and December 31, 2022, Laureate had recorded cumulative liabilities for income tax contingencies of $132,552 and $130,323 , respectively.

Non-Income Tax Loss Contingencies

Laureate has accrued liabilities for certain civil actions against our institutions, a portion of which existed prior to our acquisition of these entities. Laureate intends to vigorously defend against these matters. As of June 30, 2023 and December 31, 2022, approximately $12,700 and $11,400 , respectively, of loss contingencies were included in Other long-term liabilities and Other current liabilities on the Consolidated Balance Sheets.

We have also identified certain loss contingencies that we have assessed as being reasonably possible of loss, but not probable of loss, and could have an adverse effect on the Company’s results of operations if the outcomes are unfavorable. In the aggregate, we estimate that the reasonably possible loss for these unrecorded contingencies could be up to approximately $18,300 if the outcomes were unfavorable.

Guarantees

In connection with a loan agreement entered into by a Laureate subsidiary in Peru, all of the shares of Universidad Privada del Norte, one of our universities, were pledged to the third-party lender as a guarantee of the payment obligations under the loan.

During the first quarter of 2021, one of our Peruvian institutions issued a bank guarantee in order to appeal a preliminary tax assessment received related to tax audits of 2014 and 2015. As of June 30, 2023 and December 31, 2022, the amount of the guarantee was $7,428 and $7,076 , respectively.

15

Note 9. Stockholders’ Equity

The components of net changes in stockholders’ equity for the fiscal quarters of 2023 are as follows:

| Laureate Education, Inc. Stockholders | ||||||||||||||||||||||||||

| Common stock | Additional paid-in capital | Retained earnings | Accumulated other comprehensive loss | Treasury stock at cost | Non-controlling interests | Total stockholders’ equity | ||||||||||||||||||||

| Shares | Amount | |||||||||||||||||||||||||

| Balance at December 31, 2022 | $ | $ | $ | $ | ( | $ | ( | $ | ( | $ | ||||||||||||||||

| Non-cash share-based compensation | — | — | — | — | — | — | ||||||||||||||||||||

| Exercise of stock options and vesting of restricted stock units, net of shares withheld to satisfy tax withholding | ( | — | — | — | — | ( | ||||||||||||||||||||

| Equitable adjustments to stock-based awards | — | — | ( | — | — | — | — | ( | ||||||||||||||||||

| Change in noncontrolling interests | — | — | — | — | — | ( | ( | |||||||||||||||||||

| Net loss | — | — | — | ( | — | — | ( | ( | ||||||||||||||||||

Foreign currency translation adjustment, net of tax of $ | — | — | — | — | — | |||||||||||||||||||||

| Balance at March 31, 2023 | $ | $ | $ | $ | ( | $ | ( | $ | ( | $ | ||||||||||||||||

| Non-cash share-based compensation | — | — | — | — | — | — | ||||||||||||||||||||

| Retirement of treasury stock | — | ( | ( | — | — | — | ||||||||||||||||||||

| Exercise of stock options and vesting of restricted stock units, net of shares withheld to satisfy tax withholding | — | — | — | — | — | |||||||||||||||||||||

| Equitable adjustments to stock-based awards | — | — | — | — | — | — | ||||||||||||||||||||

| Net income | — | — | — | — | — | |||||||||||||||||||||

Foreign currency translation adjustment, net of tax of $ | — | — | — | — | — | ( | ||||||||||||||||||||

| Balance at June 30, 2023 | $ | $ | $ | $ | ( | $ | $ | ( | $ | |||||||||||||||||

Retirement of Treasury Stock

On May 24, 2023, the Company’s Board of Directors approved the retirement of all outstanding shares of treasury stock, which totaled 73,766 shares. The Company recorded the purchases of treasury stock at cost as a separate component within stockholders’ equity in the Consolidated Balance Sheets. Upon retirement of treasury stock, the Company allocates the excess of the purchase price over par value to additional paid-in capital, subject to certain limitations.

16

| Laureate Education, Inc. Stockholders | ||||||||||||||||||||||||||

Common stock | Additional paid-in capital | Retained earnings (accumulated deficit) | Accumulated other comprehensive loss | Treasury stock at cost | Non-controlling interests | Total stockholders’ equity | ||||||||||||||||||||

| Shares | Amount | |||||||||||||||||||||||||

| Balance at December 31, 2021 | $ | $ | $ | $ | ( | $ | ( | $ | ( | $ | ||||||||||||||||

| Non-cash share-based compensation | — | — | — | — | — | — | ||||||||||||||||||||

| Purchase of treasury stock at cost | ( | — | — | — | — | ( | — | ( | ||||||||||||||||||

| Exercise of stock options and vesting of restricted stock units, net of shares withheld to satisfy tax withholding | — | — | — | — | ||||||||||||||||||||||

| Equitable adjustments to stock-based awards | — | — | ( | — | — | — | ( | |||||||||||||||||||

| Net loss | — | — | — | ( | — | — | ( | ( | ||||||||||||||||||

Foreign currency translation adjustment, net of tax of $ | — | — | — | — | — | |||||||||||||||||||||

Minimum pension liability adjustment, net of tax of $ | — | — | — | — | — | — | ||||||||||||||||||||

| Balance at March 31, 2022 | $ | $ | $ | ( | $ | ( | $ | ( | $ | ( | $ | |||||||||||||||

| Non-cash share-based compensation | — | — | — | — | — | — | ||||||||||||||||||||

| Purchase of treasury stock at cost | ( | — | — | — | — | ( | — | ( | ||||||||||||||||||

| Exercise of stock options and vesting of restricted stock units, net of shares withheld to satisfy tax withholding | ( | — | — | — | — | ( | ||||||||||||||||||||

| Equitable adjustments to stock-based awards | — | — | ( | — | — | — | — | ( | ||||||||||||||||||

| Change in noncontrolling interests | — | — | — | — | — | ( | ||||||||||||||||||||

| Reclassification of redeemable equity to non-redeemable equity | — | — | — | — | — | — | ||||||||||||||||||||

| Net income | — | — | — | — | — | |||||||||||||||||||||

Foreign currency translation adjustment, net of tax of $ | — | — | — | — | — | |||||||||||||||||||||

| Balance at June 30, 2022 | $ | $ | $ | $ | ( | $ | ( | $ | ( | $ | ||||||||||||||||

Share-based Compensation Expense

During the six months ended June 30, 2023 and 2022, the Company recorded share-based compensation expense for restricted stock unit awards of $3,100 and $5,122 , respectively.

Accumulated Other Comprehensive Income (Loss)

Accumulated other comprehensive income (loss) (AOCI) in our Consolidated Balance Sheets includes the accumulated translation adjustments arising from translation of foreign subsidiaries’ financial statements, the unrealized gain on a derivative designated as an effective net investment hedge, and the accumulated net gains or losses that are not recognized as components of net periodic benefit cost for our minimum pension liability. The AOCI related to the net investment hedge will be deferred from earnings until the sale or liquidation of the hedged investee. The components of these balances were as follows:

| June 30, 2023 | December 31, 2022 | ||||||||||||||||||||||

| Laureate Education, Inc. | Noncontrolling Interests | Total | Laureate Education, Inc. | Noncontrolling Interests | Total | ||||||||||||||||||

| Foreign currency translation adjustment | $ | ( | $ | $ | ( | $ | ( | $ | $ | ( | |||||||||||||

| Unrealized gain on derivatives | |||||||||||||||||||||||

| Minimum pension liability adjustment | ( | ( | ( | ( | |||||||||||||||||||

| Accumulated other comprehensive loss | $ | ( | $ | $ | ( | $ | ( | $ | $ | ( | |||||||||||||

17

Note 10. Income Taxes

Laureate's income tax provisions for all periods consist of federal, state and foreign income taxes. The tax provisions for the six months ended June 30, 2023 and 2022 are based on estimated full-year effective tax rates, adjusted for discrete income tax items related specifically to the interim periods. Laureate has operations in multiple countries at various statutory tax rates and other operations that are loss-making entities for which it is not more likely than not that a tax benefit will be realized on the loss.

For the six months ended June 30, 2023, the Company recognized income tax expense of $67,663 , as compared to $119,933 in the prior year period.

Income tax expense for the six months ended June 30, 2023 was attributable to pretax income, the jurisdictional mix of earnings, and pretax losses for which the Company cannot recognize a tax benefit.

Income tax expense for the six months ended June 30, 2022 was in part driven by discrete tax expense of approximately $32,500 that was recorded for income tax reserves related to the application of the high-tax exception to global intangible low-taxed income. In addition, income tax expense for the six months ended June 30, 2022 was attributable to pretax income, the jurisdictional mix of earnings and pretax losses for which the Company cannot recognize a tax benefit, the tax effect of stock options that expired unexercised, and additional valuation allowance.

18

Note 11. Earnings (Loss) Per Share

Laureate computes basic earnings per share (EPS) by dividing income available to common shareholders by the weighted average number of common shares outstanding for the reporting period. Diluted EPS reflects the potential dilution that would occur if share-based compensation awards were exercised or converted into common stock. To calculate the diluted EPS, the basic weighted average number of shares is increased by the dilutive effect of stock options, restricted stock units, and any other share-based compensation arrangements determined using the treasury stock method.

The following tables summarize the computations of basic and diluted earnings (loss) per share:

| For the three months ended June 30, | 2023 | 2022 | |||||||||

| Numerator used in basic and diluted earnings (loss) per common share for continuing operations: | |||||||||||

| Income from continuing operations | $ | $ | |||||||||

| Income attributable to noncontrolling interests | ( | ( | |||||||||

| Net income from continuing operations for basic and diluted earnings per share | $ | $ | |||||||||

| Numerator used in basic and diluted earnings (loss) per common share for discontinued operations: | |||||||||||

| Net (loss) income from discontinued operations for basic and diluted earnings (loss) per share | $ | ( | $ | ||||||||

| Denominator used in basic and diluted earnings (loss) per common share: | |||||||||||

| Basic weighted average shares outstanding | |||||||||||

| Dilutive effect of stock options | |||||||||||

| Dilutive effect of restricted stock units | |||||||||||

| Diluted weighted average shares outstanding | |||||||||||

| Basic earnings (loss) per share: | |||||||||||

| Income from continuing operations | $ | $ | |||||||||

| (Loss) income from discontinued operations | ( | ||||||||||

| Basic earnings per share | $ | $ | |||||||||

| Diluted earnings (loss) per share: | |||||||||||

| Income from continuing operations | $ | $ | |||||||||

| (Loss) income from discontinued operations | ( | ||||||||||

| Diluted earnings per share | $ | $ | |||||||||

19

| For the six months ended June 30, | 2023 | 2022 | |||||||||

| Numerator used in basic and diluted earnings (loss) per common share for continuing operations: | |||||||||||

| Income (loss) from continuing operations | $ | $ | ( | ||||||||

| Loss attributable to noncontrolling interests | |||||||||||

| Net income (loss) from continuing operations for basic and diluted earnings (loss) per share | $ | $ | ( | ||||||||

| Numerator used in basic and diluted earnings (loss) per common share for discontinued operations: | |||||||||||

| Net (loss) income from discontinued operations for basic and diluted (loss) earnings per share | $ | ( | $ | ||||||||

| Denominator used in basic and diluted earnings (loss) per common share: | |||||||||||

| Basic weighted average shares outstanding | |||||||||||

| Dilutive effect of stock options | |||||||||||

| Dilutive effect of restricted stock units | |||||||||||

| Diluted weighted average shares outstanding | |||||||||||

| Basic and diluted earnings (loss) per share: | |||||||||||

| Income (loss) from continuing operations | $ | $ | ( | ||||||||

| (Loss) income from discontinued operations | ( | ||||||||||

| Basic and diluted earnings per share | $ | $ | |||||||||

The following table summarizes the number of stock options and restricted stock units that were excluded from the diluted EPS calculations because the effect would have been antidilutive:

| For the three months ended June 30, | For the six months ended June 30, | ||||||||||||||||||||||

| 2023 | 2022 | 2023 | 2022 | ||||||||||||||||||||

| Stock options | |||||||||||||||||||||||

| Restricted stock units | |||||||||||||||||||||||

Note 12. Legal and Regulatory Matters

Laureate is subject to legal proceedings arising in the ordinary course of business. In management’s opinion, we have adequate legal defenses, insurance coverage, and/or accrued liabilities with respect to the eventuality of these actions. Management believes that any settlement would not have a material impact on Laureate’s financial position, results of operations, or cash flows.

Our institutions are subject to uncertain and varying laws and regulations, and any changes to these laws or regulations or their application to us may materially adversely affect our business, financial condition and results of operations. Except as set forth below, there have been no material changes to the laws and regulations affecting our higher education institutions that are described in our Annual Report on Form 10-K for the year ended December 31, 2022.

Peru Regulation

Superintendencia Nacional de Educación Superior Universitaria (“SUNEDU”), the regulatory agency that supervises university standards and quality in Peru, is currently reviewing all regulations applicable to universities, with new regulations expected to be announced during 2023. This follows the appointment of new members to the board of SUNEDU in the first quarter of 2023 in connection with the implementation of the July 2022 law that modified SUNEDU’s board representation and authority.

On March 30, 2023, Cibertec, the Company’s technical-vocational institute, was granted a higher education colleges license for a six-year period. This license will now allow Cibertec to offer four-year programs for professional bachelor degrees.

20

Note 13. Supplemental Cash Flow Information

Reconciliation of Cash and cash equivalents and Restricted cash

The following table provides a reconciliation of cash, cash equivalents and restricted cash reported within the Consolidated Balance Sheets, as well as the June 30, 2022 balance. The June 30, 2023 and June 30, 2022 balances sum to the amounts shown in the Consolidated Statements of Cash Flows for the six months ended June 30, 2023 and 2022:

| June 30, 2023 | June 30, 2022 | December 31, 2022 | ||||||||||||

| Cash and cash equivalents | $ | $ | $ | |||||||||||

| Restricted cash | ||||||||||||||

| Total Cash and cash equivalents and Restricted cash shown in the Consolidated Statements of Cash Flows | $ | $ | $ | |||||||||||

Restricted cash represents cash that is not immediately available for use in current operations.

21

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

Forward-Looking Statements

This Quarterly Report on Form 10-Q (this Form 10-Q) contains “forward‑looking statements” within the meaning of the federal securities laws, which involve risks and uncertainties. You can identify forward‑looking statements because they contain words such as “believes,” “expects,” “may,” “will,” “should,” “seeks,” “approximately,” “intends,” “plans,” “estimates” or “anticipates” or similar expressions that concern our strategy, plans or intentions. All statements we make relating to estimated and projected earnings, costs, expenditures, cash flows, growth rates and financial results, and all statements we make relating to our current growth strategy and other future plans, strategies or transactions that may be identified, explored or implemented and any litigation or dispute resulting from any completed transaction are forward-looking statements. In addition, we, through our senior management, from time to time make forward‑looking public statements concerning our expected future operations and performance and other developments. All of these forward‑looking statements are subject to risks and uncertainties that may change at any time, including with respect to our current growth strategy and the impact of any completed divestiture or separation transaction on our remaining businesses. Accordingly, our actual results may differ materially from those we expected. We derive most of our forward‑looking statements from our operating budgets and forecasts, which are based upon many detailed assumptions. While we believe that our assumptions are reasonable, we caution that it is very difficult to predict the impact of known factors, and, of course, it is impossible for us to anticipate all factors that could affect our actual results. Important factors that could cause actual results to differ materially from our expectations, including, without limitation, in conjunction with the forward-looking statements and risk factor included in this Form 10-Q, are disclosed in “Item 1—Business,” and “Item 1A—Risk Factors” of our Annual Report on Form 10-K for the fiscal year ended December 31, 2022 (the 2022 Form 10-K). Some of the factors that we believe could affect our results include:

•the risks associated with operating our portfolio of degree-granting higher education institutions in Mexico and Peru, including complex business, political, legal, regulatory, tax and economic risks;

•our ability to maintain and, subsequently, increase tuition rates and student enrollments in our institutions;

•our ability to effectively manage the growth of our business and increase our operating leverage;

•the risks associated with maintaining the value of our brands and our reputation;

•the effect of existing international and U.S. laws and regulations governing our business or changes to those laws and regulations or in their application to our business;

•changes in the political, economic and business climate in the markets in which we operate;

•risks of downturns in general economic conditions and in the educational services and education technology industries that could, among other things, impair our goodwill and intangible assets;

•possible increased competition from other educational service providers;

•market acceptance of new service offerings by us or our competitors and our ability to predict and respond to changes in the markets for our educational services;

•the effect of greater than anticipated tax liabilities;

•the effect on our business and results of operations from fluctuations in the value of foreign currencies;

•the fluctuations in revenues due to seasonality;

•the risks associated with disruptions to our computer networks and other cybersecurity incidents, including misappropriation of personal or proprietary information;

•the risks and uncertainties associated with an epidemic, pandemic or other public health emergency, such as the global coronavirus (COVID-19) pandemic, including, but not limited to, effects on student enrollment, tuition pricing, and collections in future periods;

•the risks associated with protests, strikes or natural or other disasters;

•our ability to attract and retain key personnel;

•our ability to maintain proper and effective internal controls necessary to produce accurate financial statements on a timely basis;

•the risks associated with indebtedness and disruptions to credit and equity markets;

•our focus on a specific public benefit purpose and producing a positive effect for society may negatively influence our financial performance; and

22

•the future trading prices of our common stock and the impact of any securities analysts’ reports on these prices.

We caution you that the foregoing list of important factors may not contain all of the material factors that are important to you. In addition, in light of these risks and uncertainties, the matters referred to in the forward-looking statements contained in this Form 10-Q may not in fact occur. We undertake no obligation to publicly update or revise any forward-looking statement as a result of new information, future events or otherwise, except as otherwise required by law.

Introduction

This Management’s Discussion and Analysis of Financial Condition and Results of Operations (the MD&A) is provided to assist readers of the financial statements in understanding the results of operations, financial condition and cash flows of Laureate Education, Inc. This MD&A should be read in conjunction with the consolidated financial statements and related notes included elsewhere in this Form 10-Q. The consolidated financial statements included elsewhere in this Form 10-Q are presented in U.S. dollars (USD) rounded to the nearest thousand, with the amounts in MD&A rounded to the nearest tenth of a million. Therefore, discrepancies in the tables between totals and the sums of the amounts listed may occur due to such rounding. Our MD&A is presented in the following sections:

•Overview;

•Results of Operations;

•Liquidity and Capital Resources;

•Critical Accounting Policies and Estimates; and

•Recently Adopted Accounting Standards.

Overview

Our Business

We operate a portfolio of degree-granting higher education institutions in Mexico and Peru. Collectively, we have approximately 424,400 students enrolled at five institutions in these two countries. We believe that the higher education markets in Mexico and Peru present an attractive long-term opportunity, primarily because of the large and growing imbalance between the supply and demand for affordable, quality higher education in those markets. We believe that the combination of the projected growth in the middle class, limited government resources dedicated to higher education, and a clear value proposition demonstrated by the higher earnings potential afforded by higher education, creates substantial opportunities for high-quality private institutions to meet this growing and unmet demand. By offering high-quality, outcome-focused education, we believe that we enable students to prosper and thrive in the dynamic and evolving knowledge economy. We have two reportable segments as described below. We group our institutions by geography in Mexico and Peru for reporting purposes.

Assets Held for Sale

As discussed in Note 3, Assets Held for Sale, of our consolidated financial statements included elsewhere in this Quarterly Report on Form 10-Q, the Company has undertaken a process to sell two of our subsidiaries in Mexico that operate K-12 educational programs. As such, these subsidiaries are classified as assets held for sale as of June 30, 2023. The planned sale does not represent a strategic shift and therefore does not qualify for presentation as a discontinued operation in the consolidated financial statements. The completion of the sale is not expected to have a material effect on our financial results.

Our Segments

Our segments generate revenues by providing an education that emphasizes profession-oriented fields of study with undergraduate and graduate degrees in a wide range of disciplines. Our educational offerings utilize campus-based, online and hybrid (a combination of online and in-classroom) courses and programs to deliver their curriculum. The Mexico and Peru markets are characterized by what we believe is a significant imbalance between supply and demand. The demand for higher education is large and growing and is fueled by several demographic and economic factors, including a growing middle class, global growth in services and technology-related industries and recognition of the significant personal and economic benefits gained by graduates of higher education institutions. The target demographics are primarily 18- to 24-year-olds in both countries in which we compete. We compete with other private higher education institutions on the basis of price, educational quality, reputation and location. We believe that we compare favorably with competitors because of our focus on quality, professional-oriented curriculum and the competitive advantages provided by our network. There are a number of private and

23

public institutions in both countries in which we operate, and it is difficult to predict how the markets will evolve and how many competitors there will be in the future. We expect competition to increase as the Mexican and Peruvian markets mature. Essentially all of our revenues were generated from private pay sources as there are no material government-sponsored loan programs in Mexico or Peru. Specifics related to both of our reportable segments are discussed below:

•Private education providers in Mexico constitute approximately 36% of the total higher-education market. The private sector plays a meaningful role in higher education, bridging supply and demand imbalances created by a lack of capacity at public universities. Laureate owns two nationally licensed institutions and is present throughout the country with a footprint of over 35 campuses. Students in our Mexican institutions typically finance their own education.

•In Peru, private universities are increasingly providing the capacity to meet growing demand and constitute approximately 73% of the total higher-education market. Laureate owns three institutions in Peru, with a footprint of 19 campuses.

Corporate is a non-operating business unit whose purpose is to support operations. Its departments are responsible for establishing operational policies and internal control standards, implementing strategic initiatives, and monitoring compliance with policies and controls throughout our operations. Our Corporate segment provides financial, human resource, information technology, insurance, legal, and tax compliance services. The Corporate segment also contains the eliminations of inter-segment revenues and expenses.

The following information for our reportable segments is presented as of June 30, 2023:

| Institutions | Enrollment | 2023 YTD Revenues ($ in millions) | % Contribution to 2023 YTD Revenues | |||||||||||

| Mexico | 2 | 205,100 | $ | 374.1 | 52 | % | ||||||||

| Peru | 3 | 219,300 | 339.2 | 48 | % | |||||||||

| Total | 5 | 424,400 | $ | 713.3 | 100 | % | ||||||||

Challenges

Our operations are outside of the United States and are subject to complex business, economic, legal, regulatory, political, tax and foreign currency risks, which may be difficult to adequately address. As a result, we face risks that are inherent in international operations, including: fluctuations in exchange rates, possible currency devaluations, inflation and hyper-inflation; price controls and foreign currency exchange restrictions; potential economic and political instability in both countries in which we operate; expropriation of assets by local governments; key political elections and changes in government policies; multiple and possibly overlapping and conflicting tax laws; and compliance with a wide variety of foreign laws. See “Item 1A—Risk Factors—Risks Relating to Our Business—We operate a portfolio of degree-granting higher education institutions in Mexico and Peru and are subject to complex business, economic, legal, political, tax and foreign currency risks, which risks may be difficult to adequately address,” in our 2022 Form 10-K. We plan to grow our operations organically by: 1) adding new programs and course offerings, including online and hybrid offerings; 2) expanding target student demographics; and 3) increasing capacity at existing and new campus locations. Our success in growing our business will depend on the ability to anticipate and effectively manage these and other risks related to operating in various countries.

Regulatory Environment and Other Matters

Our business is subject to varying laws and regulations based on the requirements of local jurisdictions. These laws and regulations are subject to updates and changes. We cannot predict the form of the rules that ultimately may be adopted in the future or what effects they might have on our business, financial condition, results of operations and cash flows. We will continue to develop and implement necessary changes that enable us to comply with such laws and regulations. See also “Item 1A—Risk Factors—Risks Relating to Our Business—Our institutions are subject to uncertain and varying laws and regulations, and any changes to these laws or regulations or their application to us may materially adversely affect our business, financial condition and results of operations,” and “Item 1—Business—Industry Regulation” in our 2022 Form 10-K for a detailed discussion of our different regulatory environments.

24

Key Business Metric

Enrollment

Enrollment is our lead revenue indicator and represents our most important non-financial metric. We define “enrollment” as the number of students registered in a course on the last day of the enrollment reporting period. New enrollments provide an indication of future revenue trends. Total enrollment is a function of continuing student enrollments, new student enrollments and enrollments from acquisitions, offset by graduations, attrition and enrollment decreases due to dispositions. Attrition is defined as a student leaving the institution before completion of the program. To minimize attrition, we have implemented programs that involve assisting students in remedial education, mentoring, counseling and student financing.

Each of our institutions has an enrollment cycle that varies by geographic region and academic program. Each institution has a “Primary Intake” period during each academic year in which the majority of the enrollment occurs. Each institution also has a smaller “Secondary Intake” period. Our Peruvian institutions have their Primary Intake during the first calendar quarter and a Secondary Intake during the third calendar quarter. Institutions in our Mexico segment have their Primary Intake during the third calendar quarter and a Secondary Intake during the first calendar quarter. Our institutions in Peru are generally out of session in January, February and July, while institutions in Mexico are generally out of session in May through July. Revenues are recognized when classes are in session.

Principal Components of Income Statement

Revenues

The majority of our revenue is derived from tuition and educational services. The amount of tuition generated in a given period depends on the price per credit hour and the total credit hours or price per program taken by the enrolled student population. The price per credit hour varies by program, by market and by degree level. Additionally, varying levels of discounts and scholarships are offered depending on market-specific dynamics and individual achievements of our students. Revenues are recognized net of scholarships and other discounts, refunds and waivers. In addition to tuition revenues, we generate other revenues from student fees and other education-related activities. These other revenues are less material to our overall financial results and have a tendency to trend with tuition revenues. The main drivers of changes in revenues between periods are student enrollment and price. We continually monitor market conditions and carefully adjust our tuition rates to meet local demand levels. We proactively seek the best price and content combinations to remain competitive in all the markets in which we operate.

Direct Costs

Our direct costs include labor and operating costs associated with the delivery of services to our students, including the cost of wages, payroll taxes and benefits, depreciation and amortization, rent, utilities, bad debt expenses, and marketing and promotional costs to grow future enrollments. In general, a significant portion of our direct costs tend to be variable in nature and trend with enrollment, and management continues to monitor and improve the efficiency of instructional delivery.

General and Administrative Expenses

Our general and administrative expenses primarily consist of costs associated with corporate departments, including executive management, finance, legal, business development and other departments that do not provide direct operational services.

Factors Affecting Comparability

Foreign Exchange

While the USD is our reporting currency, our institutions are located in Mexico and Peru and operate in other functional currencies, namely the Mexican peso and Peruvian nuevo sol. We monitor the impact of foreign currency movements and the correlation between the local currency and the USD. Our revenues and expenses are generally denominated in local currency. The principal foreign exchange exposure is the risk related to the translation of revenues and expenses incurred in each country from the local currency into USD. See “Item 1A—Risk Factors—Risks Relating to Our Business—Our reported revenues and earnings may be negatively affected by the strengthening of the U.S. dollar and currency exchange rates” in our 2022 Form 10-K. In order to provide a framework for assessing how our business performed excluding the effects of foreign currency fluctuations, we present organic constant currency in our segment results, which is calculated using the change from prior-year

25

average foreign exchange rates to current-year average foreign exchange rates, as applied to local-currency operating results for the current year, and then excludes the impact of other items, as described in the segments’ results.

Seasonality

Our institutions have a summer break during which classes are generally not in session and minimal revenues are recognized. In addition to the timing of summer breaks, holidays such as Easter also have an impact on our academic calendar. Operating expenses, however, do not fully correlate to the enrollment and revenue cycles, as the institutions continue to incur expenses during summer breaks. Given the geographic diversity of our institutions and differences in timing of summer breaks, our second and fourth quarters are stronger revenue quarters as the majority of our institutions are in session for most of these respective quarters. Our first and third fiscal quarters are weaker revenue quarters because our institutions have summer breaks for some portion of one of these two quarters. However, our primary enrollment intakes occur during the first and third quarters. Due to this seasonality, revenues and profits in any one quarter are not necessarily indicative of results in subsequent quarters and may not be correlated to new enrollment in any one quarter. Additionally, seasonality may be affected due to other events that could change the academic calendar at our institutions. See “Item 1A—Risk Factors—Risks Relating to Our Business—We experience seasonal fluctuations in our results of operations” in our 2022 Form 10-K.

Income Tax Expense

Our consolidated income tax provision is derived based on the combined impact of federal, state and foreign income taxes. Also, discrete items can arise in the course of our operations that can further impact the Company’s effective tax rate for the period. Our tax rate fluctuates from period to period due to changes in the mix of earnings between our tax-paying entities and our loss-making entities for which it is not 'more likely than not' that a tax benefit will be realized on the loss. See “Item 1A—Risk Factors—Risks Relating to Our Business—We may have exposure to greater-than-anticipated tax liabilities” in our 2022 Form 10-K.

The Organization for Economic Co-operation and Development (OECD) has proposed changes to numerous long-standing tax principles. These proposals, if finalized and adopted by its member countries, will likely increase tax uncertainty, and may adversely affect our provision for income taxes. The Company will continue to monitor regulatory developments to assess potential impacts to the Company.

Results of Operations

The following discussion of the results of our operations is organized as follows:

•Summary Comparison of Consolidated Results;

•Non-GAAP Financial Measure; and

•Segment Results.

26

Comparison of Consolidated Results for the Three Months Ended June 30, 2023 and 2022

| % Change | |||||||||||||||||

| Better/(Worse) | |||||||||||||||||

| (in millions) | 2023 | 2022 | 2023 vs. 2022 | ||||||||||||||

| Revenues | $ | 462.1 | $ | 385.4 | 20 | % | |||||||||||

| Direct costs | 294.0 | 242.8 | (21) | % | |||||||||||||

| General and administrative expenses | 12.0 | 15.9 | 25 | % | |||||||||||||

| Loss on impairment of assets | 1.6 | — | nm | ||||||||||||||

| Operating income | 154.5 | 126.6 | 22 | % | |||||||||||||

| Interest expense, net of interest income | (4.1) | (2.5) | (64) | % | |||||||||||||

| Other non-operating expense | (32.5) | (12.8) | (154) | % | |||||||||||||

| Income from continuing operations before income taxes | 117.8 | 111.4 | 6 | % | |||||||||||||

| Income tax expense | (57.5) | (72.0) | 20 | % | |||||||||||||

| Income from continuing operations | 60.4 | 39.4 | 53 | % | |||||||||||||

| (Loss) income from discontinued operations, net of tax | (4.0) | 4.1 | (198) | % | |||||||||||||

| Net income | 56.3 | 43.6 | 29 | % | |||||||||||||

| Net income attributable to noncontrolling interests | (0.1) | (0.1) | — | % | |||||||||||||

| Net income attributable to Laureate Education, Inc. | $ | 56.2 | $ | 43.4 | 29 | % | |||||||||||

nm - percentage changes not meaningful

Comparison of Consolidated Results for the Three Months Ended June 30, 2023 to the Three Months Ended June 30, 2022

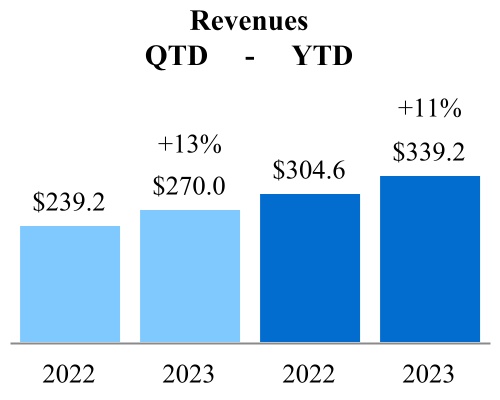

Revenues increased by $76.7 million to $462.1 million for the three months ended June 30, 2023 (the 2023 fiscal quarter) from $385.4 million for the three months ended June 30, 2022 (the 2022 fiscal quarter). This increase in revenues was attributable to: (1) higher average total organic enrollment at our institutions during the 2023 fiscal quarter, which increased revenues by $28.2 million compared to the 2022 fiscal quarter; (2) the effect of changes in tuition rates and enrollments in programs at varying price points (product mix), pricing and timing, which increased revenues by $25.7 million compared to the 2022 fiscal quarter; and (3) the effect of a net change in foreign currency exchange rates, which increased revenues by $24.5 million, mainly due to the strengthening of the Mexican peso against the USD compared to the 2022 fiscal quarter. These increases in revenues were partially offset by other Corporate and Eliminations changes, which accounted for a decrease in revenues of $1.7 million.

Direct costs and general and administrative expenses combined increased by $47.3 million to $306.0 million for the 2023 fiscal quarter from $258.7 million for the 2022 fiscal quarter. The increase in direct costs was primarily driven by the effect of operational changes, which increased costs by $31.0 million, primarily due to the result of higher enrollment at our institutions, as well as return-to-campus expenses. In addition, the effect of a net change in foreign currency exchange rates increased costs by $19.7 million, mainly due to the strengthening of the Mexican peso against the USD compared to the 2022 fiscal quarter. These increases in direct costs were partially offset by a decrease of $3.4 million in Corporate and Eliminations expenses.

Operating income increased by $27.9 million to $154.5 million for the 2023 fiscal quarter from $126.6 million for the 2022 fiscal quarter. The increase in operating income was mainly driven by higher operating income at both our Peru and Mexico segments, which was primarily attributable to higher revenues compared to the 2022 fiscal quarter.

Interest expense, net of interest income increased by $1.6 million to $4.1 million for the 2023 fiscal quarter from $2.5 million for the 2022 fiscal quarter. The increase in interest expense was primarily attributable to higher average debt balances compared to the 2022 fiscal quarter.

Other non-operating expense increased by $19.7 million to $32.5 million for the 2023 fiscal quarter from $12.8 million for the 2022 fiscal quarter. This increase was attributable to: (1) a higher loss on foreign currency exchange of $17.9 million during the 2022 fiscal quarter, mainly related to intercompany loan arrangements; (2) the year-over-year effect of a gain on disposal of subsidiaries of $1.5 million during the 2022 fiscal quarter, which was primarily attributable to the release of accumulated foreign currency translation gains upon liquidation of certain subsidiaries; and (3) the year-over-year change in other non-operating expense of $0.3 million.

27

Income tax expense decreased by $14.5 million to $57.5 million for the 2023 fiscal quarter from $72.0 million for the 2022 fiscal quarter. This decrease was primarily attributable to a change in the mix of pre-tax earnings among jurisdictions.

(Loss) income from discontinued operations, net of tax changed by $8.1 million to a loss of $(4.0) million for the 2023 fiscal quarter from income of $4.1 million for the 2022 fiscal quarter. This change was primarily attributable to changes in estimates during the 2023 fiscal quarter regarding the realizability of certain receivables from previous divestitures, combined with the year-over-year impact of a gain recognized during the 2022 fiscal quarter upon completion of the transfer of certain leases related to our former operations in Chile.

Summary Comparison of Consolidated Results

Comparison of Consolidated Results for the Six Months Ended June 30, 2023 and 2022

| % Change | |||||||||||||||||

| Better/(Worse) | |||||||||||||||||

| (in millions) | 2023 | 2022 | 2023 vs. 2022 | ||||||||||||||

| Revenues | $ | 713.3 | $ | 594.9 | 20 | % | |||||||||||

| Direct costs | 519.3 | 425.7 | (22) | % | |||||||||||||

| General and administrative expenses | 22.3 | 33.4 | 33 | % | |||||||||||||

| Loss on impairment of assets | 1.6 | 0.1 | nm | ||||||||||||||

| Operating income | 170.1 | 135.7 | 25 | % | |||||||||||||

| Interest expense, net of interest income | (8.0) | (4.2) | (90) | % | |||||||||||||

| Other non-operating expense | (60.9) | (17.6) | nm | ||||||||||||||