UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

For the fiscal year ended December 31 , 2022

OR

For the transition period from __________ to __________.

Commission File Number: 001-38002

(Exact name of registrant as specified in its charter)

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||||||||

| (Address of principal executive offices) | (Zip Code) | |||||||||||||

Registrant’s telephone number, including area code: (786) 209-3368

Securities registered pursuant to Section 12(b) of the Securities Exchange Act of 1934:

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered | ||||||

The NASDAQ Stock Market LLC | ||||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☒ No ☐

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting company, or an emerging growth company. See the definitions of "large accelerated filer," "accelerated filer," "smaller reporting company," and "emerging growth company" in Rule 12b-2 of the Exchange Act.

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C.7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of June 30, 2022 (the last business day of the registrant's most recently completed second fiscal quarter), the aggregate market value of the common stock held by non-affiliates of the registrant was $1.241 billion (based on the closing price of the registrant's common stock on that date as reported on the Nasdaq Global Select Market).

Indicate the number of shares outstanding of each of the issuer's classes of common stock, as of the latest practicable date.

| Class | Outstanding at January 31, 2023 | |||||||

| Common stock, par value $0.004 per share | ||||||||

Documents Incorporated by Reference

| Index | |||||||||||

| Page No. | |||||||||||

| Part I | |||||||||||

| Item 1. | Business | ||||||||||

| Item 1A. | Risk Factors | ||||||||||

| Item 1B. | Unresolved Staff Comments | ||||||||||

| Item 2. | Properties | ||||||||||

| Item 3. | Legal Proceedings | ||||||||||

| Item 4. | Mine Safety Disclosures | ||||||||||

| Part II | |||||||||||

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | ||||||||||

| Item 6. | [Reserved] | ||||||||||

| Item 7. | Management's Discussion and Analysis of Financial Condition and Results of Operations | ||||||||||

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | ||||||||||

| Item 8. | Financial Statements and Supplementary Data | ||||||||||

| Item 9. | Changes in and Disagreements With Accountants on Accounting and Financial Disclosure | ||||||||||

| Item 9A. | Controls and Procedures | ||||||||||

| Item 9B. | Other Information | ||||||||||

| Item 9C. | Disclosure Regarding Foreign Jurisdictions that Prevent Inspections | ||||||||||

| Part III | |||||||||||

| Item 10. | Directors, Executive Officers and Corporate Governance | ||||||||||

| Item 11. | Executive Compensation | ||||||||||

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | ||||||||||

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | ||||||||||

| Item 14. | Principal Accountant Fees and Services | ||||||||||

| Part IV | |||||||||||

| Item 15. | Exhibits and Financial Statement Schedules | ||||||||||

| Item 16. | Form 10-K Summary | ||||||||||

| Signatures | |||||||||||

As used in this Annual Report on Form 10‑K (this “Form 10‑K”), unless otherwise stated or the context otherwise requires, references to “we,” “us,” “our,” the “Company,” “Laureate” and similar references refer collectively to Laureate Education, Inc. and its subsidiaries.

1

Trademarks and Tradenames

LAUREATE, LAUREATE INTERNATIONAL UNIVERSITIES and the leaf symbol are trademarks of Laureate Education, Inc. in the United States and other countries. This Form 10‑K also includes other trademarks of Laureate and trademarks of other persons, which are properties of their respective owners.

Industry and Market Data

We obtained the industry, market and competitive position data used throughout this Form 10‑K from our own internal estimates and research, as well as from industry publications and research, surveys and studies conducted by third‑party sources.

Industry publications, studies and surveys generally state that they have been obtained from sources believed to be reliable, although they do not guarantee the accuracy or completeness of such information. We have not independently verified industry, market and competitive position data from third‑party sources. While we believe that our internal business estimates and research are reliable and the market definitions are appropriate, neither such estimates or research nor these definitions have been verified by any independent source.

Forward‑Looking Statements

This Form 10‑K contains “forward‑looking statements” within the meaning of the federal securities laws, which involve risks and uncertainties. You can identify forward‑looking statements because they contain words such as “believes,” “expects,” “may,” “will,” “should,” “seeks,” “approximately,” “intends,” “plans,” “estimates” or “anticipates” or similar expressions that concern our strategy, plans or intentions. All statements we make relating to estimated and projected earnings, costs, expenditures, cash flows, growth rates and financial results, and all statements we make relating to our current growth strategy and other future plans, strategies or transactions that may be identified, explored or implemented and any litigation or dispute resulting from any completed transaction are forward-looking statements. In addition, we, through our senior management, from time to time make forward‑looking public statements concerning our expected future operations and performance and other developments. All of these forward‑looking statements are subject to risks and uncertainties that may change at any time, including with respect to our current growth strategy and the impact of any completed divestiture or separation transaction on our remaining businesses. Accordingly, our actual results may differ materially from those we expected. We derive most of our forward‑looking statements from our operating budgets and forecasts, which are based upon many detailed assumptions. While we believe that our assumptions are reasonable, we caution that it is very difficult to predict the impact of known factors, and, of course, it is impossible for us to anticipate all factors that could affect our actual results. Important factors that could cause actual results to differ materially from our expectations, including, without limitation, in conjunction with the forward‑looking statements and risk factors included in this Form 10‑K, are disclosed under various sections throughout this Form 10‑K, including, but not limited to, Item 1—Business, Item 1A—Risk Factors, and Item 7—Management’s Discussion and Analysis of Financial Condition and Results of Operations. All subsequent written and oral forward‑looking statements attributable to us, or persons acting on our behalf, are expressly qualified in their entirety by the factors discussed in this Form 10‑K. Some of the factors that we believe could affect our results include:

•the risks associated with operating our portfolio of degree-granting higher education institutions in Mexico and Peru, including complex business, political, legal, regulatory, tax and economic risks;

•our ability to maintain and, subsequently, increase tuition rates and student enrollments in our institutions;

•our ability to effectively manage the growth of our business and increase our operating leverage;

•the risks associated with maintaining the value of our brands and our reputation;

•the effect of existing international and U.S. laws and regulations governing our business or changes to those laws and regulations or in their application to our business;

•changes in the political, economic and business climate in the markets in which we operate;

•risks of downturns in general economic conditions and in the educational services and education technology industries that could, among other things, impair our goodwill and intangible assets;

•possible increased competition from other educational service providers;

2

•market acceptance of new service offerings by us or our competitors and our ability to predict and respond to changes in the markets for our educational services;

•the effect of greater than anticipated tax liabilities;

•the effect on our business and results of operations from fluctuations in the value of foreign currencies;

•the fluctuations in revenues due to seasonality;

•the risks associated with disruptions to our computer networks and other cybersecurity incidents, including misappropriation of personal or proprietary information;

•the risks and uncertainties associated with an epidemic, pandemic or other public health emergency, such as the global coronavirus (COVID-19) pandemic, including, but not limited to, effects on student enrollment, tuition pricing, and collections in future periods;

•the risks associated with protests, strikes or natural or other disasters;

•our ability to attract and retain key personnel;

•our ability to maintain proper and effective internal controls necessary to produce accurate financial statements on a timely basis;

•the risks associated with indebtedness and disruptions to credit and equity markets;

•our focus on a specific public benefit purpose and producing a positive effect for society may negatively influence our financial performance; and

•the future trading prices of our common stock and the impact of any securities analysts’ reports on these prices.

We caution you that the foregoing list of important factors may not contain all of the material factors that are important to you. In addition, in light of these risks and uncertainties, the matters referred to in the forward‑looking statements contained in this Form 10‑K may not in fact occur. We undertake no obligation to publicly update or revise any forward‑looking statement as a result of new information, future events or otherwise, except as otherwise required by law.

3

Part I

Item 1. Business

Our continuing operations include Mexico and Peru. Unless otherwise indicated, the information in or incorporated by reference into this Form 10-K, including our segment information, relates only to our continuing operations.

General

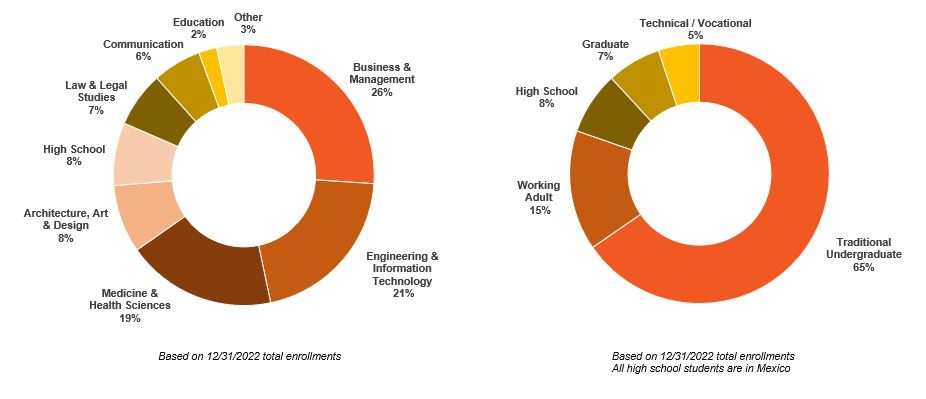

We operate a portfolio of degree-granting higher education institutions in Mexico and Peru. These institutions, which we collectively refer to as the Laureate International Universities network, are leading brands in their respective markets and offer a broad range of undergraduate and graduate degrees through campus-based, online and hybrid programs. Collectively, we have approximately 423,000 students enrolled at five institutions with over 50 campuses as of December 31, 2022. Our institutions in Mexico and Peru operate within scaled country networks, which provide advantages in terms of shared infrastructure, technology, curricula and operational best practices. More than 80% of our students are enrolled in programs of four or more years in duration. As of December 31, 2022, a vast majority of our students were enrolled at traditional, campus-based institutions offering multi-year degrees, similar to leading private and public higher education institutions in developed markets such as the United States and Europe.

Our programs are designed with a distinct emphasis on applied, professional-oriented content for growing career fields and are focused on academic disciplines that we believe offer strong employment opportunities and high earnings potential for our students. We continually and proactively adapt our curriculum to the needs of the market. In particular, we emphasize science, technology, engineering and math (STEM) and business disciplines, areas in which we believe that there is large and growing demand, especially in developing countries. Students pursuing degrees in Medicine & Health Sciences, Engineering & Information Technology and Business & Management, our three largest disciplines, constitute over 70% of our total post-secondary enrollments. We believe that the work of our graduates in these disciplines creates a positive impact on the communities we serve and strengthens our institutions’ reputations within their respective markets. Our focus on private-pay and our track record for delivering high-quality outcomes to our students, while stressing affordability and accessibility, has been a key reason for our long record of success.

We believe that the higher education markets in Mexico and Peru present an attractive long-term opportunity, primarily because of the large and growing imbalance between the supply and demand for affordable, quality higher education in those markets. We believe that the combination of the projected growth in the middle class, limited government resources dedicated to higher education, and a clear value proposition demonstrated by the higher earnings potential afforded by higher education creates substantial opportunities for high-quality private institutions to meet this growing and unmet demand. By offering high-quality, outcome-focused education, we believe that we enable students to prosper and thrive in the dynamic and evolving knowledge economy.

In many developing markets, traditional higher education students (defined as 18-24 year olds) have historically been served by public universities, which have limited capacity and are often underfunded, resulting in an inability to meet growing student demands and employer requirements. In addition, in many of these same markets, non-traditional students, such as working adults and distance learners, have limited options for pursuing higher education. With strong brands and highly reputed institutions in Mexico and Peru, we believe that we are uniquely positioned to address these market opportunities.

4

| Country | Institution | Enrollment at December 31, 2022 | Market Segment | QS Stars™ Overall University Rating | Ratings/Rankings | ||||||||||||

| Mexico | Universidad del Valle de México (UVM) | 103,700 | Premium/ Traditional | «««« | •Ranked Top 10 university in Mexico | ||||||||||||

•5-Star rated by QS Stars™ in categories of Employability & Inclusiveness | |||||||||||||||||

| Mexico | Universidad Tecnológica de México (UNITEC) | 119,100 | Value/Teaching | ««« | •Largest private university in Mexico | ||||||||||||

•5-Stars rated by QS Stars™ in categories of Employability & Inclusiveness | |||||||||||||||||

| Peru | Universidad Peruana de Ciencias Aplicadas (UPC) | 69,000 | Premium/Traditional | «««« | •Ranked Top 5 university in Peru | ||||||||||||

•5-Star rated by QS Stars™ in categories of Employability & Inclusiveness | |||||||||||||||||

| Peru | Universidad Privada del Norte (UPN) | 112,100 | Value/Teaching | «««« | •3rd largest private university in Peru | ||||||||||||

•5-Stars rated by QS Stars™ in categories of Employability & Inclusiveness | |||||||||||||||||

| Peru | CIBERTEC | 19,100 | Tech/Voc | N/A | •2nd largest private tech/voc institute in Peru | ||||||||||||

Sources: QS Stars™, Guía Universitaria (UVM), AmericaEconomia (UPC)

Our institutions in Mexico and Peru offer traditional higher education students a private education alternative, with multiple brands and price points in each market and innovative programs and strong career-driven outcomes. Additionally, through targeted programs and multiple teaching modalities, we are able to serve the differentiated needs of non-traditional students in these markets.

Our program and level of study mix for 2022 was as follows:

5

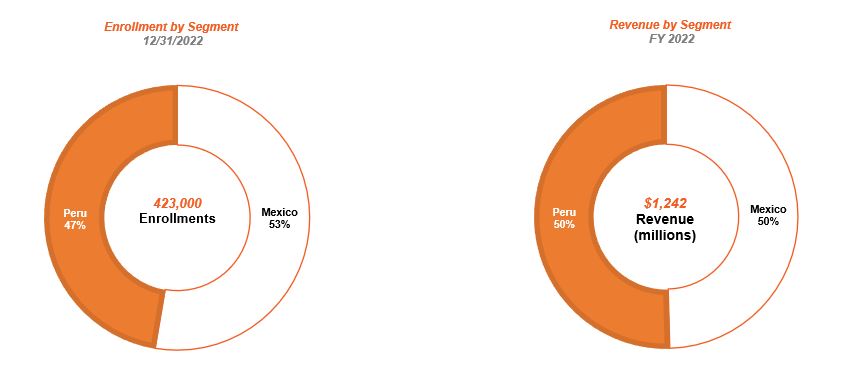

Our Segments

We have two reportable segments, which are summarized in the charts below. The following information for our segments is presented as of December 31, 2022.

Our Industry

We operate higher education institutions in Mexico and Peru. These markets are characterized by what we believe is a significant imbalance between supply and demand. The demand for higher education is large and growing and is fueled by several demographic and economic factors, including a growing middle class, global growth in services and technology-related industries and recognition of the significant personal and economic benefits gained by graduates of higher education institutions. At the same time, the respective Mexican and Peruvian governments often have limited resources to devote to higher education, resulting in a diminished ability by the public sector to meet growing demand, and creating opportunities for private education providers to enter these markets and deliver high-quality education. As a result, the private sector plays a large and growing role in higher education.

Favorable industry dynamics in Mexico and Peru driving growth in the higher education sector include the following:

Large, Growing and Underpenetrated Population of Qualified Higher Education Students. In many countries, including throughout Latin America and other developing regions, there is growing demand for higher education based on favorable demographics, increasing secondary completion rates and increasing higher education participation rates, resulting in continued growth in higher education enrollments. While global participation rates have increased for traditional higher education students (defined as 18-24 year olds), the market for higher education in Mexico and Peru is still significantly underpenetrated, at approximately 34% and 52%, respectively, as compared to approximately 62% in the United States.

Strong Economic Incentives for Higher Education. According to data from the Organization for Economic Co-operation and Development (“OECD”), in countries that are members of the OECD, the earnings from employment for younger adults (25-34 years) and older adults (45-54 years) completing higher education were approximately 39% and 75% higher, respectively, than those of younger and older adults with only an upper secondary education. We believe that the cumulative impact of favorable demographic and socio-economic trends, coupled with the superior earnings potential of higher education graduates, will continue to expand the market for private higher education.

Increasing Role of the Private Sector in Higher Education. In both Mexico and Peru, the private sector plays a meaningful role in higher education, bridging supply and demand imbalances created by a lack of capacity at public universities. In Mexico, private education providers constitute 36% of the total higher-education market (42% in states in which we have operations). In Peru, private education providers constitute 73% of the total higher-education market. In addition to capacity limitations, we believe that limited public resources, and the corresponding policy reforms to make higher education systems less dependent on the financial and operational support of local governments, have resulted in increased enrollments in private institutions relative to public institutions.

6

Increasing Demand for Online Offerings. We believe that increasing student demand, new instruction methodologies designed for the online medium, and growing employer and regulatory acceptance of degrees obtained through online and hybrid modalities will continue to drive online learning in Mexico and Peru. Moreover, increasing the percentage of courses taught online in a hybrid educational model has significant cost and capital efficiency benefits, as a greater number of students can be accommodated in existing physical campus space.

Our Strengths and Competitive Advantages

We believe that our key competitive strengths that will enable us to execute our strategy include the following:

Scaled Platform Institutions Across Country Networks. Our scale within the countries in which we operate facilitates distinct advantages for our students and allows us to leverage our operating model across multiple brands in Mexico and Peru.

Our in-country networks facilitate competitive advantages related to:

•Curricula and Programs. We are able to leverage our curricula and resources, allowing for the rapid deployment of new programs. Increasing amounts of our curricula are being standardized, allowing us to lower the cost of program development by reusing and sharing content, while improving the quality of our programs.

•Best Practices. Through collaboration across our institutions, best practices for key operational processes, such as digital marketing, data science/AI, scheduling, retention management, market research, campus design, faculty training, student services and recruitment, are identified and then rolled out to all of our institutions.

•Unified Systems. Our scale also permits increased investment in unified technology systems and an opportunity to leverage standardization of processes, centralization of common services (such as information technology, finance and procurement) and intellectual property, and implementing a common operating model and platform for content development, digital campus experiences, student services, recruitment and administrative services within each country. These systems provide data and insights on a scale that we believe will allow us to improve student experience, retention rates and outcomes, while also enabling a more efficient and lower cost educational delivery model.

Leading Online Technology. Our commitment to digital teaching and learning has been manifested through significant investments in core technologies, as well as in human resources, training and development activities. These investments have been instrumental in establishing a deep level of expertise in online education, facilitating the design and delivery of high quality, effective and differentiated online courses in the markets in which we operate.

Long-Standing and Respected University Brands. We believe that we have established a reputation for providing high-quality higher education, and our institutions are among the most respected higher education brands in their local markets. Our institutions have long-established histories and are ranked among the best in their respective countries.

In addition, many of our institutions and programs have earned the highest accreditation available, which provides us with a strong competitive advantage in local markets. For example, medical school licenses are often the most difficult to obtain and are only granted to institutions that meet rigorous standards. Throughout Mexico and Peru we operate 13 medical and seven dental schools. We believe that the establishment of our medical and dental schools further validates the quality of our institutions and programs and increases brand awareness.

Commitment to Academic Quality. We offer high-quality undergraduate, graduate and specialized programs in a wide range of disciplines that generate strong interest from students and provide attractive employment prospects. We focus on programs that prepare our students to become employed in high demand professions. Our curriculum development process includes employer surveys and ongoing research into business trends to determine the skills and knowledge base that will be required by those employers in the future. This information results in timely curriculum upgrades, which helps ensure that our graduates acquire the skills that will make them marketable to employers. We also are committed to continually evaluating our institutions to ensure we are providing the highest quality education to our students. External assessment methodologies, such as QS Stars™, allows us to identify key areas for improvement in order to drive a culture of quality and continual innovation at our institutions.

7

Attractive Financial Model.

•Private Pay Model. Essentially all of our revenues for 2022 were generated from private pay sources, as there are no material government-sponsored student loan programs in Mexico or Peru. We believe that students’ and families’ willingness to allocate personal resources to fund higher education at our institutions validates our strong value proposition.

•Revenue Visibility Enhanced by Program Length and Strong Retention. The length of our programs provides us with a high degree of revenue visibility. The majority of the academic programs offered by our institutions last between four and five years, and more than 80% of our students were enrolled in programs of at least four years or more in duration as of December 31, 2022. Additionally, we actively monitor and manage student retention because of the impact it has on student outcomes and our financial results. Our historical annual student retention rate, which we define as the proportion of prior year students returning in the current year (excluding graduating students), was 79% on average over the last five years. Given our high degree of revenue visibility, we are able to make attractive capital investments and execute other strategic initiatives to help drive sustainable growth in our business.

•Attractive Margin Profile with Significant Operating Leverage. Our scale within each country provides significant advantages, enabling us to operate efficiently with attractive margin levels. We focus on optimizing our operations at the country level through our in-county networks.

Our Strategy

Our mission is to deliver affordable, high-quality education to prepare students for successful careers and lifelong achievement, while building pride, trust, and respect in our communities. To achieve our mission, we execute a strategy enabled by the following initiatives:

Integration of Campus-Based Operations in Mexico and Peru. Our institutions in Mexico and Peru serve approximately 423,000 students in a relatively homogenous operating environment, creating a unique opportunity to harvest the benefits of scale. We believe that by implementing best practices within each country we will enable closer collaboration and facilitate innovation and improved student experiences. We believe that this unification will enable us to be more nimble in our day-to-day operations and will allow us to extract valuable insights from more data across our network. Further, we believe that integration will enable further innovation and efficiency in our academic model and operations, and allow us to expand our market share.

Leverage and Expand Existing Portfolio. We will continue to focus on opportunities to expand our programs and the type of students that we serve, as well as our capacity in our markets to meet local demand, leveraging our existing platform to execute on attractive organic growth opportunities. In particular, we intend to add new programs and course offerings, expand target student demographics and, where appropriate, increase capacity at existing campuses and through hybrid online opportunities, open new campuses and enter new cities in existing markets. We believe that these initiatives will drive growth and provide an attractive return on capital.

•Add New Programs and Course Offerings. We will continue to develop new programs and course offerings to address the changing needs in the markets. New programs and course offerings enable us to provide a high-quality education that we believe is desired by students and prospective employers. In addition, we have a comprehensive suite of current program offerings, all of which are not currently offered in each campus in which we operate. We intend to lift and shift many of those current programs to the campuses where they are not currently being offered, with a particular focus on our health sciences vertical.

•Expand Target Student Demographics. We use sophisticated analytical techniques to identify opportunities to provide quality education to new or underserved student populations where market demand is not being met, such as non-traditional students (e.g., working adults, life-long learners) who may value flexible scheduling options, as well as traditional students. Our ability to provide quality education to these underserved markets has provided additional growth opportunities to our network and we intend to leverage our management capabilities and local knowledge to further capitalize on these opportunities in new and existing markets.

8

•Increase Capacity at Existing and New Campus Locations. We will continue to make demand-driven investments in additional capacity throughout our network by expanding existing campuses and opening new campuses, including in new cities. We employ a highly analytical process based on economic and demographic trends, and demand data for the local market to determine when and where to expand capacity. When opening a new campus or expanding existing facilities, we use best practices that we have developed over more than the past decade to cost-effectively expedite the opening and development of that location.

Expand Online and Hybrid Education Programs. We intend to increase the number of our students that receive their education through fully online or hybrid programs to meet the growing demands of students. Our online initiative is designed to not only provide students with access to innovative programs and modern digital experiences, but also to diversify our offerings, increase our enrollments and expand our digital solutions in a capital efficient manner, leveraging current infrastructure and improving classroom utilization.

The percentage of student credit hours taken online in our campus-based institutions was approximately 27% for 2019. During most of 2020 and 2021, due to the COVID-19 pandemic, all of our students were effectively transitioned to an online learning environment, at scale. In 2022, our students, faculty and staff were able to safely return to campus and fully transitioned to blended learning modalities by the second half of the year. As we return to face-to-face operations at our campuses, we are targeting to have 40% to 60% percent of our student credit hours taken online going forward. With a common learning management system implemented across our universities, we believe that we have the expertise to continue to expand online and hybrid offerings to meet the growing demand for this market opportunity, allowing us to differentiate ourselves further from our competitors.

We continue to accelerate the advancement of online education programs and technology-enabled solutions that deliver high-quality differentiated student experiences for our institutions at scale.

Our strategy for the online opportunity includes the following components:

•Hybrid Online Programs. Traditional 18-24 year old students attending campus-based institutions are increasingly seeking digital learning experiences that are blended with in-person learning. We provide those students with a hybrid learning experience, mixing face-to-face classroom experience with technology through our online platform, which we believe improves the student experience by providing them with a wide range of online courses, interactive discussions, virtual experiences, digital resources, and simulations that enhance their learning experiences both within and outside the classroom.

•Fully Online Programs. Many students require flexible learning modules to accommodate work and personal responsibilities. Often, these students are working adults who are looking to either complete an undergraduate or post-graduate degree, or who want to gain a credential to accelerate or change careers. Our fully online programs provide students with a high-quality curriculum experience to achieve their goals.

Our Segments and Institutions

Laureate offers its educational services through two reportable segments: Mexico and Peru.

We determine our segments based on information utilized by our chief operating decision maker to allocate resources and assess performance. See Note 6, Business and Geographic Segment Information, in our consolidated financial statements for financial information regarding our operating segments and financial information about geographic areas; see also “Item 7—Management’s Discussion and Analysis of Financial Condition and Results of Operations—Results of Operations—Segment Results” and “—Overview—Factors Affecting Comparability—Seasonality” in this Form 10-K.

9

The following table presents information about the institutions as of December 31, 2022:

Reportable Segment (Enrollment) | Higher Education Institution | Year Joined Laureate Network | Year Founded | |||||||||||||||||

Mexico | Universidad del Valle de México (UVM) | 2000 | 1960 | |||||||||||||||||

| (222,800) | Universidad Tecnológica de México (UNITEC) | 2008 | 1966 | |||||||||||||||||

Peru | Universidad Peruana de Ciencias Aplicadas (UPC) | 2004 | 1994 | |||||||||||||||||

| (200,200) | CIBERTEC | 2004 | 1983 | |||||||||||||||||

| Universidad Privada del Norte (UPN) | 2007 | 1994 | ||||||||||||||||||

Competition

We face competition in both of our reportable segments. We believe that competition focuses on price, educational quality, reputation, brand positioning, location and facilities.

The market for higher education in Mexico and Peru is highly fragmented and marked by large numbers of local competitors. The target demographics are primarily 18- to 24-year-olds in the countries in which we compete. Public institutions tend to be less expensive, if not free, but limited in capacity. The top public universities in these market are selective, and many of the other public universities are less focused on practical programs aligned around career opportunities. This creates market demand for private educational providers. We compete with other private higher education institutions on the basis of price, educational quality, reputation and location. We believe that we compare favorably with competitors because of our focus on quality, professional-oriented curriculum and the competitive advantages provided by our network. There are a number of private and public institutions in both of the countries in which we operate, and it is difficult to predict how the markets will evolve and how many competitors there will be in the future. We expect competition to increase as the Mexican and Peruvian markets continue to develop.

See “Item 1A—Risk Factors—Risks Relating to Our Business—The higher education market is very competitive, and we may not be able to compete effectively.”

Intellectual Property

We currently own, or have filed applications for, trademark registrations for the word “Laureate,” for “Laureate International Universities” and for the Laureate leaf logo in the trademark offices of all jurisdictions in which we operate institutions of higher learning. We have also registered or filed applications in the applicable jurisdictions in which we operate for the trademarks “Laureate Online International” and “Laureate Online Education.” In addition, we have the rights to trade names, logos and other intellectual property specific to most of our higher education institutions, in the countries in which those institutions operate.

Human Capital

At Laureate Education, Inc., we employ approximately 35,000 people (including approximately 22,000 academic staff) and are committed to promoting a culture that is strengthened by its diversity, enriched through collaboration, and built upon a foundation of continuous learning and development.

Our workforce proudly serves a population of approximately 423,000 students across Mexico and Peru and is focused on delivering academic quality and a market-leading student experience, while ensuring the highest standards of accountability, governance, and reporting.

Leading an international workforce requires a combination of universal standards, expectations, and protocols, along with a deep understanding of local culture and context. Regardless of geography, we establish and maintain the highest degree of ethical conduct, compliance, and transparency, and design and implement initiatives to promote engagement, performance, and collaboration.

10

In 2022, some of our company-wide initiatives included:

Ethics and Compliance

•The launch of a revised Code of Conduct, which sets out principles of integrity and ethical behavior, and our responsibilities to each other, our students, suppliers, stockholders, and the public. The Code covers such topics as accurate records, proper use of assets and information, conflicts of interest, and bribery and corruption.

•Company-wide Ethics communication campaigns targeting all employees, including live, interactive town-halls.

•Ongoing mandatory training for all employees, in all geographies.

Employee Engagement Benchmarking

•We conducted a comprehensive employee engagement survey, with an overall response rate of 79%, and an overall engagement score well above the median within higher education.

•Our overall engagement score combines net promoter score, pride in the company, intention to stay, and discretionary effort to go above and beyond. Specific areas of strength, company-wide, included productivity, engagement, and inclusion. The survey also revealed areas in which we can improve, and a series of targeted actions are being developed for 2023.

Recognizing the Impact of our People

•Through the expertise, passion, and commitment of our people, we are making a positive impact within and beyond communities across Mexico, Peru, and the United States. In 2022 we published our 2021 Impact Report which recognizes and celebrates the impact our people are creating. The report is available on our website at laureate.net. We plan to continue these efforts with publication of our 2022 Impact Report later this year. Information contained on our website is not incorporated by reference herein and is not a part of this Annual Report on Form 10-K.

Diversity and Inclusion

•We are committed to strengthening our commitment to Diversity and Inclusion across our company. In 2022, we established a Diversity and Equity Committee across both our universities in Mexico, and in Peru, we improved gender diversity in senior leadership by more than 20%.

Our History

Since making our first investment in global higher education in 1999, we have focused on expanding access to differentiated higher education and learning opportunities to traditionally underserved areas of the world. In August 2007, we were acquired in a leveraged buyout by a consortium of investment funds and other investors. On February 6, 2017, we consummated our initial public offering and shares of our common stock began trading on the Nasdaq under the symbol “LAUR”.

Public Benefit Corporation Status

In October 2015, we redomiciled in Delaware as a public benefit corporation as a demonstration of our long-term commitment to our mission to benefit our students and society. Public benefit corporations are intended to produce a public benefit and to operate in a responsible and sustainable manner. Under Delaware law, public benefit corporations are required to identify in their certificate of incorporation the public benefit or benefits they will promote and their directors have a duty to manage the affairs of the corporation in a manner that balances the pecuniary interests of the stockholders, the best interests of those materially affected by the corporation’s conduct, and the specific public benefit or public benefits identified in the public benefit corporation’s certificate of incorporation. Public benefit corporations organized in Delaware also are required to assess their benefit performance internally and to disclose publicly at least biennially a report detailing their success in meeting their benefit objectives.

Our public benefit, as provided in our amended and restated certificate of incorporation, is to produce a positive effect (or a reduction of negative effects) for society and persons by offering diverse education programs delivered online and on premises operated in the communities that we serve. By doing so, we believe that we provide greater access to cost-effective, high-quality higher education that enables more students to achieve their academic and career aspirations. Our operations are outside the United States, where there is a large and growing imbalance between the supply and demand for quality higher education. Our stated public benefit is firmly rooted in our company mission and our belief that when our students succeed, countries

11

prosper and societies benefit. Becoming a public benefit corporation underscores our commitment to our purpose and our stakeholders, including students, regulators, employers, local communities and stockholders.

Available Information

Our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports are available free of charge through the “Financials” portion of our investor relations website at http://investors.laureate.net and on the SEC's website at www.sec.gov as soon as reasonably practical after they are filed with the SEC. Various corporate governance documents, including our Audit Committee Charter, Compensation Committee Charter, Nominating and Corporate Governance Committee Charter, Corporate Governance Guidelines and Code of Conduct and Ethics are available without charge through the “Leadership and Governance” portion of our investor relations website, listed above. In addition, we may use our website as a distribution channel of material company information, and we also webcast our earnings calls via our investor relations website.

Industry Regulation

Mexican Regulation

Mexican law provides that private entities are entitled to render education services in accordance with applicable legal provisions. These provisions regulate the education services rendered by the federal government, the states and private entities and contain guidelines for the allocation of the higher education role among the federal government, the states and the municipalities, including their respective economic contributions, in order to jointly participate in the development and coordination of higher education.

There are three levels of regulation in Mexico: federal, state and municipal. The federal authority is the Federal Ministry of Public Education (Secretaría de Educación Pública). Each of the 31 states and Mexico City has the right to establish a local Ministry of Education, and each municipality of each state may establish a municipal education authority that only has authority to advertise and promote educational services and/or activities.

Some functions are exclusive to the Federal Ministry of Education, such as the establishment of study plans and programs for Basic and Mid-Superior education services. There are also concurrent functions, such as the granting and withdrawal of governmental recognition of validity of studies (Reconocimiento de Validez Oficial de Estudios) (“REVOEs”).

The General Law on Education (Ley General de Educación) in Mexico classifies studies in the following three categories: (i) Basic Education, which includes pre-school (kindergarten), elementary school and junior high school (secundaria); (ii) Mid-Superior Education, which includes high school (preparatoria) and equivalent studies, as well as professional education that does not consider preparatoria as a prerequisite; and (iii) Superior Education, which includes the studies taught after preparatoria, including undergraduate school (licenciatura), specialties (especialidades), master’s studies, doctorate studies and studies for teachers (educación normal).

The REVOEs are issued either by the Federal Ministry of Education under the General Law on Education or by any of the state Ministries of Education under the applicable state law. REVOEs are granted for each program taught at each campus. If there is a change in the program or in the campus at which it is taught, the entity will need to get a new REVOE.

The Federal Ministry of Education has issued a set of general resolutions (Acuerdos) that regulate the general requirements for obtaining REVOEs. The main Acuerdos are (i) Acuerdo 243, issued on May 27, 1998, which sets the general guidelines for obtaining an Authorization or REVOE; (ii) Acuerdo 17/11/17, issued on November 10, 2017, which sets the procedures related to REVOEs for Superior Education studies; and (iii) Acuerdo 18/11/18, issued on November 27, 2018, which defines the different levels, models and educational options at Superior Education. The Federal Ministry of Education recommends to the local Ministries of Education the adoption and inclusion of the provisions contained in Acuerdo 243 and Acuerdo 17/11/17 in the local Law on Education and other applicable local laws and regulations.

Depending on each state, other requirements may apply; for example, in certain states, private institutions that provide educational services with REVOEs need to be registered with the corresponding local authorities.

Acuerdo 17/11/17 regulates in detail the provisions contained under the General Law on Education to grant REVOEs for Superior Education studies, regarding faculty, plans and programs of studies, inspection visits, procedures, etc. Acuerdo 17/11/17 also provides that private institutions that provide Superior Education services in accordance with presidential decrees or secretarial resolutions (acuerdos secretariales) issued specifically to them may maintain the obligations provided to them

12

thereunder and may function under the simplified provisions of Acuerdo 17/11/17. Currently, Universidad Tecnológica de México, S.C. and Universidad del Valle de México, S.C. have secretarial resolutions that were issued in their favor before the issuance of Acuerdo 17/11/17. The obligations contained in these secretarial resolutions generally conform to the obligations provided under Acuerdo 17/11/17.

The regulatory authorities are entitled to conduct inspection visits to the facilities of educational institutions to verify compliance with applicable legal provisions. Failure to comply with applicable legal provisions may result in the imposition of fines, the cancellation of the applicable REVOE and the closure of the education facilities.

Private institutions with REVOEs are required to grant a minimum percentage of scholarships to students. Acuerdo 17/11/17 requires private institutions to grant scholarships to at least five percent of the total students registered during each academic term. Scholarships consist, in whole or in part, of payment of the registration and tuition fees established by the educational institution.

Private entities may also obtain the recognition of validity of their programs from the National Autonomous University of Mexico (Universidad Nacional Autónoma de México or “UNAM”). The General Regulations of Incorporation and Validation of Studies issued by UNAM provide that programs followed in private entities may be “incorporated” to UNAM in order for UNAM to recognize their validity.

The UNAM regulations also require private entities incorporated to UNAM to grant scholarships to at least five percent of the total students registered at such entity. The students entitled to have this benefit will be selected by UNAM. Some of our high school programs and one of our medical programs are incorporated to UNAM.

A new higher education bill was enacted in April 2021, and expected secondary provisions for this bill have not yet been added to the legislative agenda. No foreseeable material changes are expected to impact the business as a result of this bill and the expected secondary provisions.

Peruvian Regulation

We operate three post-secondary education institutions in Peru, two of which are universities and one of which is a technical-vocational institute. Peruvian law provides that universities and technical-vocational institutes can be operated as public or private entities, and that the private entities may be organized for profit. The Ministry of Education (“MINEDU”) has overall responsibility for the national education system.

In 2014, the Peruvian Congress enacted a new law (the “University Law”) to regulate the establishment, operation, monitoring and closure of universities and to promote continuous improvement of quality at Peruvian universities. The University Law created a new agency, the Superintendencia Nacional de Educación Superior Universitaria (“SUNEDU”), which is responsible for carrying out the governmental role in university regulation, including ensuring quality. While institutional autonomy is still recognized, and universities are permitted to create their own internal governance rules and determine their own academic, management and economic systems, including curriculum design and entrance and graduation requirements, all of these matters are now subject to review and evaluation by SUNEDU through its periodic review of universities as part of a license renewal process.

Under the University Law, university licenses are granted for specific time periods but are renewable, and are granted by SUNEDU. Universities have to demonstrate to SUNEDU that they comply with, at a minimum, certain Basic Quality Conditions (“BQCs”) (i.e., that they have specified academic goals and that the degrees granted and plans of study are aligned with those goals; that their academic offerings are compatible with their planning goals (e.g., there is sufficient labor demand for careers offered); that there are only two regular semesters of studies per year; that they have appropriate infrastructure and equipment; that they engage in research; that they have a sufficient supply of qualified teachers, at least 25% of whom will need to be full-time; that they supply adequate basic complementary educational services (e.g., medical and psychological services and sports activities); that they provide appropriate placement office services; and that they have transparency of institutional information). Both UPC and UPN had their licenses renewed in 2017, in each case for a period of six years, extended one additional year due to COVID-19.

SUNEDU allows for the educational services to be provided by three modalities: (i) face-to-face learning (with a maximum of 20% virtual credits), (ii) hybrid learning (with 20% to 70% of the total credits of the academic program allowed to be taken virtually) and (iii) virtual learning (credits taken virtually cannot exceed 80% of the total credits of undergraduate academic programs, with the exception of programs that are specially designed for an adult population over 24 years old - (WA programs)). In December 2022, SUNEDU modified the possibility of having WA programs 100% virtual learning, leaving

13

only the possibility of reaching 80% of virtuality. It does not apply to previously approved programs, as the case of UPC and UPN, which must be adapted to the new percentage at the time of re-licensing.

In January 2023, the Constitutional Court declared constitutional Law 31520 that was passed in July 2022, which modified the composition of the SUNEDU Board of Directors and reduced its powers for the approval of new careers, schools and faculties. We are awaiting the appointment of the new members of SUNEDU.

Technical-vocational institutes are regulated by the MINEDU, which grants operating licenses for six years, after which the Ministry conducts a revalidation process. Since 2016, a new law regarding technical-vocational institutes (the “Institutes Law”) was enacted. The Institutes Law created two types of institutes: Higher Education Institutes (“Institutes”) which are dedicated to technical careers and Higher Education Colleges (“Colleges”) which are devoted to technical careers related to education, as well as science and information technology. Colleges grant Technical Bachelor Degrees and Professional Technical Degrees. Institutes and Colleges are subject to a mandatory license granted by the MINEDU, based on an evaluation to determine compliance with BQCs. BQCs include: an appropriate institutional management guaranteeing a proper relation with the educational model of the institution; appropriate academic management and proper program studies aligned with the MINEDU norms; appropriate infrastructure and equipment to develop educational activities; adequate teachers and staff which, at a minimum, should consist of 20% full-time staff; and appropriate financial and economic provisions. Unlike licenses, quality accreditation is voluntary, except for certain careers for which it might be mandatory as determined by law. Such accreditation will be taken into consideration for access to public grants for scholarships and research, among other things. Private Institutes and Colleges may be organized as for-profit or not-for-profit entities under Peruvian law. According to the schedule determined by the regulations, in 2018, Cibertec was granted a license by the MINEDU for a five-year period. In November 2022, Cibertec’s license renewal was submitted, with a request for a renewal period of six years.

14

Item 1A. Risk Factors

Risk Factors

In addition to the information set forth in this Form 10-K and our other filings with the SEC, you should carefully consider the following risks and uncertainties, which could materially adversely affect our business, financial condition, results of operations and cash flows. The risks identified below are not all encompassing but should be considered in establishing an opinion of our future operations. The situation continues to evolve, and additional impacts may arise of which we are not currently aware.

Risks Relating to Our Business

We operate a portfolio of degree-granting higher education institutions in Mexico and Peru and are subject to complex business, economic, legal, political, tax and foreign currency risks, which risks may be difficult to adequately address.

Our portfolio, which is composed of five institutions, operates in Mexico and Peru, each of which is subject to complex business, economic, legal, political, tax and foreign currency risks. We may have difficulty managing and administering our operations in multiple countries, and we may need to expend additional funds to, among other things, staff key management positions, obtain additional information technology infrastructure and successfully implement relevant course and program offerings for each market, which may materially adversely affect our business, financial condition and results of operations.

Additional challenges associated with the conduct of our business overseas that may materially adversely affect our operating results include:

•difficulty in staffing and managing foreign operations as a result of distance, language, legal and other differences;

•our presence solely in Latin America presents risks relating to regional economic pressures;

•each of our institutions is subject to unique business risks and challenges, including competitive pressures and diverse pricing environments at the local level;

•difficulty maintaining quality standards consistent with our brands and with local accreditation requirements;

•potential economic and political instability in the countries in which we operate, including student unrest;

•fluctuations in exchange rates, possible currency devaluations, inflation and hyperinflation;

•difficulty selecting, monitoring and controlling partners outside of the United States;

•compliance with a wide variety of foreign laws and regulations;

•expropriation of assets by governments;

•difficulty protecting our intellectual property rights overseas due to, among other reasons, the uncertainty of laws and enforcement in certain countries relating to the protection of intellectual property rights;

•lower levels of availability or use of the Internet, through which our online programs are delivered;

•limitations on the repatriation and investment of funds and foreign currency exchange restrictions; and

•acts of terrorism, public health risks, crime and natural disasters, particularly in areas in which we have significant operations.

Our success in operating our business will depend, in part, on our ability to anticipate and effectively manage these and other risks related to operating in multiple countries. Any failure by us to effectively manage the challenges associated with our operations could materially adversely affect our business, financial condition and results of operations.

15

If we cannot maintain student enrollments in our institutions and maintain tuition levels, our results of operations may be materially adversely affected.

Our strategy for growth and profitability depends, in part, upon maintaining and, subsequently, increasing student enrollments in our institutions and maintaining tuition levels. Attrition rates are often due to factors outside our control. Students sometimes face financial, personal or family constraints that require them to drop out of school. They also are affected by economic and social factors prevalent in their countries. In some markets in which we operate, transfers between universities are not common and, as a result, we are less likely to fill spaces of students who drop out. In addition, our ability to attract and retain students may require us to discount tuition from published levels and may prevent us from increasing tuition levels at a rate consistent with inflation and increases in our costs. If we are unable to control the rate of student attrition, our overall enrollment levels are likely to decline, which could materially adversely affect our business, financial condition and results of operations. If we are unable to charge tuition rates that are both competitive and cover our rising expenses, our business, financial condition, cash flows and results of operations may be materially adversely affected. In addition, student enrollment may be negatively affected by our reputation and any negative publicity related to us.

Our success depends substantially on the value of the local brands of each of our institutions, each of which may be materially adversely affected by changes in current and prospective students’ perception of our reputation and the use of social media.

Each of our institutions has worked hard to establish the value of its individual brand. Brand value may be severely damaged, even by isolated incidents, particularly if the incidents receive considerable negative publicity. There has been a marked increase in use of social media platforms and other forms of Internet-based communications that allow individuals access to a broad audience of interested persons. We believe that students and prospective employers value readily available information about our institutions and often act on such information without further investigation or authentication, and without regard to its accuracy. In addition, some of our institutions use the Laureate name in promoting their institutions. Social media platforms and devices immediately publish the content their subscribers and participants post, often without filters or checks on the accuracy of the content posted. Information concerning our company and our institutions may be posted on such platforms and devices at any time. Information posted may be materially adverse to our interests, it may be inaccurate, and it may harm our performance, prospects and business.

Our reputation may be negatively influenced by the actions of other for-profit and private institutions.

Allegations against the post-secondary for-profit and private education sectors may affect general public perceptions of for-profit and private educational institutions, including our institutions and us, in a negative manner. Adverse media coverage regarding other for-profit or private educational institutions or regarding us directly or indirectly could damage our reputation, reduce student demand for our programs, materially adversely affect our revenues and operating profit or result in increased regulatory scrutiny.

Growing our online academic programs could be difficult for us.

Despite our success in effectively transitioning all of our students to an online learning environment shortly after COVID-19 was declared a global pandemic in March 2020, the expansion of our existing online programs and the creation of new online academic programs may not be accepted by students or employers, or by government regulators or accreditation agencies. In addition, our efforts may be materially adversely affected by increased competition in the online education market or because of problems with the performance or reliability of our online program infrastructure.

Our success depends, in part, on the effectiveness of our marketing and advertising programs in recruiting new students.

In order to maintain and increase our revenues and margins, we must continue to develop our admissions programs and attract new students in a cost-effective manner. The level of marketing and advertising and types of strategies used are affected by the specific geographic markets, regulatory compliance requirements and the specific individual nature of each institution and its students. The complexity of these marketing efforts contributes to their cost. If we are unable to advertise and market our institutions and programs successfully, our ability to attract and enroll new students could be materially adversely affected and, consequently, our financial performance could suffer. We use marketing tools such as the Internet, radio, television and print media advertising to promote our institutions and programs. Our representatives also make presentations at upper secondary schools. In order to maintain our growth, we will need to attract a larger percentage of students in existing markets and increase our addressable market by adding locations in new markets and rolling out new academic programs. Any failure to accomplish this may have a material adverse effect on our future growth.

16

If we do not effectively manage our growth and business, our results of operations may be materially adversely affected.

There is no assurance that we will be able to maintain or accelerate the current growth rate, effectively manage expanding operations, build expansion capacity, or achieve planned growth on a timely or profitable basis. If our revenue growth is less than projected, the costs incurred for these additions and upgrades could have a material adverse effect on our business, financial condition and results of operations.

Our institutions are subject to uncertain and varying laws and regulations, and any changes to these laws or regulations or their application to us may materially adversely affect our business, financial condition and results of operations.

Higher education is regulated to varying degrees and in different ways in each of the countries in which we operate an institution. In general, our institutions must have licenses, approvals, authorizations, or accreditations from various governmental authorities and accrediting bodies. These licenses, approvals, authorizations, and accreditations must be renewed periodically, usually after an evaluation of the institution by the relevant governmental authorities or accrediting bodies. These periodic evaluations could result in limitations, restrictions, conditions, or withdrawal of such licenses, approvals, authorizations or accreditations, which could have a material adverse effect on our business, financial condition and results of operations. Once licensed, approved, authorized or accredited, some of our institutions may need approvals for new campuses or to add new degree programs.

All of these regulations and their applicable interpretations are subject to change. Moreover, regulatory agencies may scrutinize our institutions because they are owned or controlled by a U.S.-based for-profit corporation. Changes in applicable regulations may cause a material adverse effect on our business, financial condition and results of operations.

The higher education market is very competitive, and we may not be able to compete effectively.

Higher education markets around the world are highly fragmented and are very competitive and dynamic. Our institutions compete with traditional public and private colleges and universities and other proprietary institutions, including those that offer online professional-oriented programs. In each of the countries in which we operate a private institution, our primary competitors are public and other private universities, some of which are larger, more widely known and have more established reputations than our institutions. Some of our competitors in both the public and private sectors may have greater financial and other resources than we have and have operated in their markets for many years. Other competitors may include large, well-capitalized companies that may pursue a strategy similar to ours of acquiring or establishing for-profit institutions. Public institutions receive substantial government subsidies, and public and private not-for-profit institutions have access to government and foundation grants, tax-deductible contributions and other financial resources generally not available to for-profit institutions. Accordingly, public and private not-for-profit institutions may have instructional and support resources superior to those in the for-profit sector, and public institutions can offer substantially lower tuition prices or other advantages that we cannot match.

If our graduates are unable to obtain professional licenses or certifications required for employment in their chosen fields of study, our reputation may suffer and we may face declining enrollments and revenues or be subject to student litigation.

Certain of our students require or desire professional licenses or certifications after graduation to obtain employment in their chosen fields. Their success in obtaining such licensure depends on several factors, including the individual merits of the student, whether the institution and the program were approved by the relevant government or by a professional association, whether the program from which the student graduated meets all governmental requirements and whether the institution is accredited. If one or more governmental authorities refuses to recognize our graduates for professional licensure in the future based on factors relating to us or our programs, the potential growth of our programs would be negatively affected, which could have a material adverse effect on our business, financial condition and results of operations. In addition, we could be exposed to litigation that would force us to incur legal and other expenses that could have a material adverse effect on our business, financial condition and results of operations.

Our business may be materially adversely affected if we are not able to maintain or improve the content of our existing academic programs or to develop new programs on a timely basis and in a cost-effective manner.

We continually seek to maintain and improve the content of our existing academic programs and develop new programs in order to meet changing market needs. Revisions to our existing academic programs and the development of new programs may not be accepted by existing or prospective students or employers in all instances. If we cannot respond effectively to market changes, our business may be materially adversely affected. Even if we are able to develop acceptable new programs, we may not be able to introduce these new programs as quickly as students or employers require or as quickly as our competitors are

17

able to introduce competing programs. Our efforts to introduce a new academic program may be conditioned or delayed by requirements to obtain foreign, federal, state and accrediting agency approvals. The development of new programs and courses, both conventional and online, is subject to requirements and limitations imposed by the governmental regulatory bodies of the various countries in which our institutions are located. The imposition of restrictions on the initiation of new educational programs by regulatory agencies may delay such expansion plans. If we do not respond adequately to changes in market requirements, our ability to attract and retain students could be impaired and our financial results could suffer.

Establishing new academic programs or modifying existing academic programs also may require us to make investments in specialized personnel and capital expenditures, increase marketing efforts and reallocate resources away from other uses. We may have limited experience with the subject matter of new programs and may need to modify our systems and strategy. If we are unable to increase the number of students, offer new programs in a cost-effective manner or otherwise effectively manage the operations of newly established academic programs, our business, financial condition and results of operations could be materially adversely affected.

Failure to keep pace with changing market needs and technology could harm our ability to attract students.

The success of our institutions depends to a significant extent on the willingness of prospective employers to hire our students upon graduation. Increasingly, employers demand that their employees possess appropriate technological skills and appropriate “soft” skills, such as communication, critical thinking and teamwork skills. These skills can evolve rapidly in a changing economic and technological environment. Accordingly, it is important that our educational programs evolve in response to those economic and technological changes. The expansion of existing academic programs and the development of new programs may not be accepted by current or prospective students or by the employers of our graduates. Students and faculty increasingly rely on personal communication devices and expect that we will be able to adapt our information technology platforms and our educational delivery methods to support these devices and any new technologies that may develop. Even if our institutions are able to develop acceptable new programs and adapt to new technologies, our institutions may not be able to begin offering those new programs and technologies as quickly as required by prospective students and employers or as quickly as our competitors begin offering similar programs. If we are unable to adequately respond to changes in market requirements due to regulatory or financial constraints, unusually rapid technological changes or other factors, our ability to attract and retain students could be impaired, the rates at which our graduates obtain jobs involving their fields of study could suffer and our results of operations and cash flows could be materially adversely affected.

We may have exposure to greater-than-anticipated tax liabilities.

As a multinational corporation, we are subject to income taxes as well as non-income based taxes in the United States and various foreign jurisdictions. The determination of our provision for income taxes and other tax liabilities requires significant judgment, and there are many transactions and calculations where the ultimate tax determination is uncertain. In addition, changes in the valuation of our deferred tax assets and liabilities, or changes in tax laws, regulations and accounting principles, could have a material adverse effect on our future income taxes. We have not recorded deferred tax liabilities for undistributed foreign earnings because our strategy is to reinvest these earnings outside the United States. As circumstances change and if some or all of these undistributed foreign earnings are remitted to the United States, we may be required to recognize deferred tax liabilities on any amounts that we are unable to repatriate in a tax-free manner.

We are subject to regular review and audit by both domestic and foreign tax authorities. Any adverse outcome of such a review or audit could have a negative effect on our operating results and financial condition. We are also subject to non-income based taxes, such as payroll, sales, use, value-added, net worth, property and goods and services taxes, in both the United States and various foreign jurisdictions. We are under regular audit by tax authorities with respect to these non-income based taxes and may have exposure to additional non-income based tax liabilities.

We have also identified certain tax-related contingencies that we have assessed as being reasonably possible of loss, but not probable of loss, and could have an adverse effect on our results of operations if the outcomes are unfavorable.

Although we believe that our estimates are reasonable, the ultimate tax outcome may differ from the amounts recorded in our financial statements and may materially adversely affect our financial results in the period or periods for which such determination is made.

18

Our reported revenues and earnings may be negatively affected by the strengthening of the U.S. dollar and currency exchange rates.

We report revenues, costs and earnings in U.S. dollars, while our institutions generally collect tuition in the local currency. Exchange rates between the U.S. dollar and the local currency in the countries where we operate institutions are likely to fluctuate from period to period. In 2022, essentially all of our revenues originated outside the United States. We translate revenues and other results denominated in foreign currencies into U.S. dollars for our consolidated financial statements. This translation is based on average exchange rates during a reporting period. While the Mexican peso and the Peruvian nuevo sol strengthened against the U.S. dollar in 2022, in recent years, the U.S. dollar has strengthened against many international currencies, including the Mexican peso and Peruvian nuevo sol. As the exchange rate of the U.S. dollar strengthens, our reported international revenues and earnings are reduced because foreign currencies translate into fewer U.S. dollars. For the year ended December 31, 2022, a hypothetical 10% adverse change in average annual foreign currency exchange rates would have decreased our operating income and our Adjusted EBITDA by approximately $35.6 million and $41.3 million, respectively. For more information, see “Item 7A—Quantitative and Qualitative Disclosures About Market Risk—Foreign Currency Exchange Risk.”

To the extent that foreign revenues and expense transactions are not denominated in the local currency and/or to the extent foreign earnings are reinvested in a currency other than their functional currency, we are also subject to the risk of transaction losses. We occasionally enter into foreign exchange forward contracts or other hedging arrangements to reduce the earnings impact of non-functional currency denominated non-trade receivables and debt and to protect the U.S. dollar value of our assets and future cash flows with respect to exchange rate fluctuations. Given the volatility of exchange rates, there is no assurance that we will be able to effectively manage currency transaction and/or translation risks. Therefore, volatility in currency exchange rates may have a material adverse effect on our business, financial condition, results of operations and cash flows.