UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

_________________________

FORM 6-K

_________________________

Report of Foreign Private Issuer

Pursuant to Rule 13a-16 or 15d-16 of

the Securities Exchange Act of 1934

For the quarterly period ended March 31, 2019

Commission file number 1- 12874

_________________________

TEEKAY CORPORATION

(Exact name of Registrant as specified in its charter)

_________________________

4th Floor, Belvedere Building

69 Pitts Bay Road

Hamilton, HM 08, Bermuda

(Address of principal executive office)

_________________________

Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F. |

Form 20-F ý Form 40- F ¨ |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1). |

Yes ¨ No ý |

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7). |

Yes ¨ No ý |

Page 1

TEEKAY CORPORATION AND SUBSIDIARIES

REPORT ON FORM 6-K FOR THE QUARTERLY PERIOD ENDED MARCH 31, 2019

INDEX

PAGE | |

Page 2

ITEM 1 - FINANCIAL STATEMENTS

TEEKAY CORPORATION AND SUBSIDIARIES

UNAUDITED CONSOLIDATED STATEMENTS OF LOSS

(in thousands of U.S. Dollars, except share and per share amounts)

Three Months Ended March 31, | |||||

2019 | 2018 | ||||

$ | $ | ||||

Revenues (note 3) | 481,213 | 394,022 | |||

Voyage expenses | (103,123 | ) | (85,877 | ) | |

Vessel operating expenses | (156,992 | ) | (157,935 | ) | |

Time-charter hire expenses (note 6) | (29,838 | ) | (19,411 | ) | |

Depreciation and amortization | (72,107 | ) | (67,311 | ) | |

General and administrative expenses | (22,972 | ) | (24,183 | ) | |

Asset impairments (note 7) | (3,328 | ) | (18,662 | ) | |

Restructuring charges (note 13) | (8,621 | ) | (2,138 | ) | |

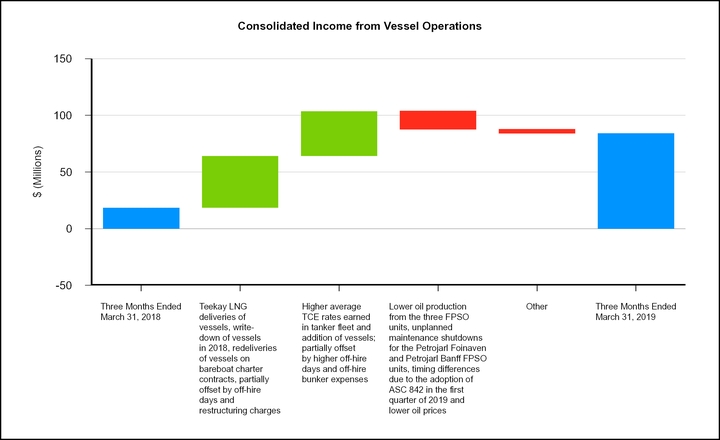

Income from vessel operations | 84,232 | 18,505 | |||

Interest expense | (73,671 | ) | (54,625 | ) | |

Interest income | 2,689 | 1,677 | |||

Realized and unrealized (losses) gains on non-designated derivative instruments (note 15) | (5,423 | ) | 9,426 | ||

Equity (loss) income (note 4) | (61,653 | ) | 27,117 | ||

Foreign exchange (loss) gain (notes 9 and 15) | (2,630 | ) | 22 | ||

Loss on deconsolidation of Teekay Offshore (note 4) | — | (7,070 | ) | ||

Other income (loss) | 28 | (915 | ) | ||

Loss before income taxes | (56,428 | ) | (5,863 | ) | |

Income tax expense (note 16) | (5,036 | ) | (4,117 | ) | |

Net loss | (61,464 | ) | (9,980 | ) | |

Net income attributable to non-controlling interests | (22,793 | ) | (10,575 | ) | |

Net loss attributable to the shareholders of Teekay Corporation | (84,257 | ) | (20,555 | ) | |

Per common share of Teekay Corporation (note 17) | |||||

• Basic and diluted loss attributable to shareholders of Teekay Corporation | (0.84 | ) | (0.21 | ) | |

Weighted average number of common shares outstanding (note 17) | |||||

• Basic and diluted | 100,520,421 | 97,333,503 | |||

The accompanying notes are an integral part of the unaudited consolidated financial statements.

Page 3

TEEKAY CORPORATION AND SUBSIDIARIES

UNAUDITED CONSOLIDATED STATEMENTS OF COMPREHENSIVE (LOSS) INCOME

(in thousands of U.S. Dollars)

Three Months Ended March 31, | |||||

2019 | 2018 | ||||

$ | $ | ||||

Net loss | (61,464 | ) | (9,980 | ) | |

Other comprehensive (loss) income: | |||||

Other comprehensive (loss) income before reclassifications | |||||

Unrealized (loss) gain on qualifying cash flow hedging instruments | (21,509 | ) | 2,622 | ||

Pension adjustments, net of taxes | (87 | ) | 195 | ||

Foreign exchange loss on currency translation | — | (377 | ) | ||

Amounts reclassified from accumulated other comprehensive (loss) income relating to: | |||||

Realized (gain) loss on qualifying cash flow hedging instruments | |||||

To interest expense (note 15) | (251 | ) | 250 | ||

To equity income | (500 | ) | (77 | ) | |

Loss on deconsolidation of Teekay Offshore (note 4) | — | 7,720 | |||

Other comprehensive (loss) income | (22,347 | ) | 10,333 | ||

Comprehensive (loss) income | (83,811 | ) | 353 | ||

Comprehensive income attributable to non-controlling interests | (7,693 | ) | (12,574 | ) | |

Comprehensive loss attributable to shareholders of Teekay Corporation | (91,504 | ) | (12,221 | ) | |

The accompanying notes are an integral part of the unaudited consolidated financial statements.

Page 4

TEEKAY CORPORATION AND SUBSIDIARIES

UNAUDITED CONSOLIDATED BALANCE SHEETS

(in thousands of U.S. Dollars, except share amounts)

As at March 31, 2019 | As at December 31, 2018 | ||||

$ | $ | ||||

ASSETS | |||||

Current | |||||

Cash and cash equivalents (note 9) | 410,724 | 424,169 | |||

Restricted cash – current (note 18) | 47,424 | 40,493 | |||

Accounts receivable, including non-trade of $9,512 (2018 – $7,883) and related party balance of $32,791 (2018 – $57,062) | 119,825 | 174,031 | |||

Accrued revenue | 55,180 | 20,249 | |||

Prepaid expenses and other (notes 3 and 15) | 97,822 | 69,882 | |||

Current portion of loans to equity-accounted investments (note 4) | 153,409 | 169,197 | |||

Total current assets | 884,384 | 898,021 | |||

Restricted cash – non-current (note 18) | 38,155 | 40,977 | |||

Vessels and equipment (note 9) | |||||

At cost, less accumulated depreciation of $1,307,855 (2018 – $1,270,460) | 3,326,468 | 3,362,937 | |||

Vessels related to finance leases, at cost, less accumulated amortization of $191,550 (2018 – $178,178) (note 6) | 2,233,989 | 2,067,254 | |||

Operating lease right-of-use assets (notes 2 and 6) | 173,945 | — | |||

Advances on newbuilding contracts | — | 86,942 | |||

Total vessels and equipment | 5,734,402 | 5,517,133 | |||

Net investment in direct financing leases – non-current (note 6) | 558,857 | 562,528 | |||

Investment in and loans to equity-accounted investments (notes 4 and 11a) | 1,106,572 | 1,193,741 | |||

Goodwill, intangibles and other non-current assets (note 15) | 159,115 | 179,270 | |||

Total assets | 8,481,485 | 8,391,670 | |||

LIABILITIES AND EQUITY | |||||

Current | |||||

Accounts payable, accrued liabilities and other (notes 8, 13 and 15) | 268,897 | 254,380 | |||

Loans from equity-accounted investments | 64,406 | 75,292 | |||

Current portion of derivative liabilities (note 15) | 12,940 | 12,205 | |||

Current portion of long-term debt (note 9) | 517,957 | 242,137 | |||

Current obligations related to finance leases (note 6) | 85,706 | 102,115 | |||

Current portion of operating lease liabilities (notes 2 and 6) | 59,291 | — | |||

Total current liabilities | 1,009,197 | 686,129 | |||

Long-term debt (note 9) | 2,710,534 | 3,077,386 | |||

Long-term obligations related to finance leases (note 6) | 1,700,034 | 1,571,730 | |||

Long-term operating lease liabilities (notes 2 and 6) | 102,188 | — | |||

Derivative liabilities (note 15) | 62,304 | 56,352 | |||

Other long-term liabilities (note 16) | 141,138 | 133,045 | |||

Total liabilities | 5,725,395 | 5,524,642 | |||

Commitments and contingencies (notes 6, 9, 11, and 15) | |||||

Equity | |||||

Common stock and additional paid-in capital ($0.001 par value; 725,000,000 shares authorized; 100,699,409 shares outstanding and issued (2018 – 100,435,210)) (note 10) | 1,048,623 | 1,045,659 | |||

Accumulated deficit | (321,905 | ) | (234,395 | ) | |

Non-controlling interest | 2,040,496 | 2,058,037 | |||

Accumulated other comprehensive loss | (11,124 | ) | (2,273 | ) | |

Total equity | 2,756,090 | 2,867,028 | |||

Total liabilities and equity | 8,481,485 | 8,391,670 | |||

The accompanying notes are an integral part of the unaudited consolidated financial statements.

Page 5

TEEKAY CORPORATION AND SUBSIDIARIES

UNAUDITED CONSOLIDATED STATEMENTS OF CASH FLOWS

(in thousands of U.S. Dollars)

Three Months Ended March 31, | |||||

2019 | 2018 | ||||

$ | $ | ||||

Cash, cash equivalents and restricted cash provided by (used for) | |||||

OPERATING ACTIVITIES | |||||

Net loss | (61,464 | ) | (9,980 | ) | |

Non-cash and non-operating items: | |||||

Depreciation and amortization | 72,107 | 67,311 | |||

Unrealized loss (gain) on derivative instruments (note 15) | 5,642 | (37,309 | ) | ||

Asset impairments (note 7) | 3,328 | 18,662 | |||

Loss on deconsolidation of Teekay Offshore (note 4) | — | 7,070 | |||

Equity loss (income), net of dividends received | 68,661 | (26,369 | ) | ||

Income tax expense | 5,036 | 4,117 | |||

Foreign exchange (gain) loss | (3,051 | ) | 23,622 | ||

Other | 10,287 | 6,075 | |||

Direct financing lease payments received | 3,025 | — | |||

Change in operating assets and liabilities | 16,295 | (11,635 | ) | ||

Expenditures for dry docking | (14,712 | ) | (8,454 | ) | |

Net operating cash flow | 105,154 | 33,110 | |||

FINANCING ACTIVITIES | |||||

Proceeds from issuance of long-term debt, net of issuance costs | 138,082 | 263,920 | |||

Prepayments of long-term debt | (176,581 | ) | (237,824 | ) | |

Scheduled repayments of long-term debt (note 9) | (54,877 | ) | (64,501 | ) | |

Proceeds from financing related to sale-leaseback of vessels | 158,680 | 126,273 | |||

Repayments of obligations related to finance leases | (23,199 | ) | (15,246 | ) | |

Net proceeds from equity issuances of Teekay Corporation (note 10) | — | 103,696 | |||

Repurchase of Teekay LNG common units | (9,497 | ) | — | ||

Distributions paid from subsidiaries to non-controlling interests | (13,892 | ) | (19,824 | ) | |

Cash dividends paid | (5,523 | ) | (5,514 | ) | |

Other financing activities | (24 | ) | (524 | ) | |

Net financing cash flow | 13,169 | 150,456 | |||

INVESTING ACTIVITIES | |||||

Expenditures for vessels and equipment | (124,540 | ) | (168,287 | ) | |

Proceeds from sale of equity-accounted investments | — | 54,438 | |||

Investment in equity-accounted investments | (2,864 | ) | (19,604 | ) | |

Cash of transferred subsidiaries on sale, net of proceeds received (note 4) | — | (25,254 | ) | ||

Other investing activities | (255 | ) | 2,358 | ||

Net investing cash flow | (127,659 | ) | (156,349 | ) | |

(Decrease) increase in cash, cash equivalents and restricted cash | (9,336 | ) | 27,217 | ||

Cash, cash equivalents and restricted cash, beginning of the period | 505,639 | 552,174 | |||

Cash, cash equivalents and restricted cash, end of the period | 496,303 | 579,391 | |||

Supplemental cash flow information (note 18) | |||||

The accompanying notes are an integral part of the unaudited consolidated financial statements.

Page 6

TEEKAY CORPORATION AND SUBSIDIARIES

UNAUDITED CONSOLIDATED STATEMENT OF CHANGES IN TOTAL EQUITY

(in thousands of U.S. Dollars, except share amounts)

TOTAL EQUITY | |||||||||||||||||

Thousands of Shares of Common Stock Outstanding # | Common Stock and Additional Paid-in Capital $ | Accumulated Deficit $ | Accumulated Other Compre- hensive (Loss) Income $ | Non- controlling Interests $ | Total $ | ||||||||||||

Balance as at December 31, 2018 | 100,435 | 1,045,659 | (234,395 | ) | (2,273 | ) | 2,058,037 | 2,867,028 | |||||||||

Net (loss) income | — | — | (84,257 | ) | — | 22,793 | (61,464 | ) | |||||||||

Other comprehensive loss | — | — | — | (7,247 | ) | (15,100 | ) | (22,347 | ) | ||||||||

Dividends declared: | |||||||||||||||||

Common stock ($0.055 per share) | — | — | (5,385 | ) | — | — | (5,385 | ) | |||||||||

Other dividends | — | — | — | — | (13,892 | ) | (13,892 | ) | |||||||||

Employee stock compensation and other (note 10) | 264 | 2,964 | — | — | — | 2,964 | |||||||||||

Change in accounting policy (note 2) | — | — | 606 | (1,604 | ) | (1,993 | ) | (2,991 | ) | ||||||||

Changes to non-controlling interest from equity contributions and other (note 2) | — | — | 1,526 | — | (9,349 | ) | (7,823 | ) | |||||||||

Balance as at March 31, 2019 | 100,699 | 1,048,623 | (321,905 | ) | (11,124 | ) | 2,040,496 | 2,756,090 | |||||||||

TOTAL EQUITY | |||||||||||||||||

Thousands of Shares of Common Stock Outstanding # | Common Stock and Additional Paid-in Capital $ | Accumulated Deficit $ | Accumulated Other Compre- hensive (Loss) Income $ | Non- controlling Interests $ | Total $ | ||||||||||||

Balance as at December 31, 2017 | 89,127 | 919,078 | (135,892 | ) | (5,995 | ) | 2,102,465 | 2,879,656 | |||||||||

Net (loss) income | — | — | (20,555 | ) | — | 10,575 | (9,980 | ) | |||||||||

Other comprehensive income | — | — | — | 8,334 | 1,999 | 10,333 | |||||||||||

Dividends declared: | |||||||||||||||||

Common stock ($0.055 per share) | — | — | (5,445 | ) | — | — | (5,445 | ) | |||||||||

Other dividends | — | — | — | — | (19,824 | ) | (19,824 | ) | |||||||||

Employee stock compensation and other (note 10) | 180 | 4,430 | — | — | — | 4,430 | |||||||||||

Proceeds from equity offerings, net of offering costs (note 10) | 11,127 | 103,696 | — | — | — | 103,696 | |||||||||||

Equity component of convertible notes (note 9) | — | 16,099 | — | — | — | 16,099 | |||||||||||

Changes to non-controlling interest from equity contributions and other | — | — | 1,988 | 99 | 3,059 | 5,146 | |||||||||||

Balance as at March 31, 2018 | 100,434 | 1,043,303 | (159,904 | ) | 2,438 | 2,098,274 | 2,984,111 | ||||||||||

The accompanying notes are an integral part of the unaudited consolidated financial statements.

Page 7

TEEKAY CORPORATION AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share and per share data)

1. | Basis of Presentation |

The unaudited interim consolidated financial statements have been prepared in accordance with United States generally accepted accounting principles (or GAAP). They include the accounts of Teekay Corporation (or Teekay), which is incorporated under the laws of the Republic of the Marshall Islands, its wholly-owned or controlled subsidiaries and any variable interest entities (or VIEs) of which it is the primary beneficiary (collectively, the Company).

Certain of Teekay’s significant non-wholly owned subsidiaries are consolidated in these financial statements even though Teekay owns less than a 50% ownership interest in the subsidiaries. These significant subsidiaries include the publicly-traded subsidiaries Teekay LNG Partners L.P. (or Teekay LNG) and Teekay Tankers Ltd. (or Teekay Tankers).

Certain information and footnote disclosures required by GAAP for complete annual financial statements have been omitted from these unaudited interim consolidated financial statements and, therefore, these financial statements should be read in conjunction with the Company’s audited consolidated financial statements for the year ended December 31, 2018, included in the Company’s Annual Report on Form 20-F, filed with the U.S. Securities and Exchange Commission (or SEC) on April 1, 2019. In the opinion of management, these unaudited interim consolidated financial statements reflect all adjustments, consisting of a normal recurring nature, necessary to present fairly, in all material respects, the Company’s consolidated financial position, results of operations, cash flows and changes in total equity for the interim periods presented. The results of operations for the three months ended March 31, 2019, are not necessarily indicative of those for a full fiscal year. Significant intercompany balances and transactions have been eliminated upon consolidation.

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the amounts reported in the financial statements and accompanying notes. Actual results could differ from those estimates. It is possible that the amounts recorded as derivative assets and liabilities could vary by material amounts prior to their settlement.

2. Recent Accounting Pronouncements

In February 2016, the Financial Accounting Standards Board (or FASB) issued Accounting Standards Update 2016-02, Leases (or ASU 2016-02). ASU 2016-02 establishes a right-of-use model that requires a lessee to record a right-of-use asset and a lease liability on the balance sheet for all leases with terms longer than 12 months. For lessees, leases will be classified as either finance or operating, with classification affecting the pattern of expense recognition in the income statement. ASU 2016-02 requires lessors to classify leases as a sales-type, direct financing, or operating lease. A lease is a sales-type lease if any one of five criteria are met, each of which indicate that the lease, in effect, transfers control of the underlying asset to the lessee. If none of those five criteria are met, but two additional criteria are both met, indicating that the lessor has transferred substantially all of the risks and benefits of the underlying asset to the lessee and a third party, the lease is a direct financing lease. All leases that are not sales-type leases or direct financing leases are operating leases. ASU 2016-02 became effective for the Company on January 1, 2019. FASB issued an additional accounting standards update in July 2018 that made further amendments to accounting for leases, including allowing the use of a transition approach whereby a cumulative effect adjustment is made as of the effective date, with no retrospective effect and providing an optional practical expedient to lessors not to separate lease and non-lease components of a contract if certain criteria are met. The Company has elected to use this new optional transitional approach. To determine the cumulative effect adjustment, the Company has not reassessed lease classification, initial direct costs for any existing leases, or whether any expired or existing contracts are or contain leases. The Company identified the following differences:

• | The adoption of ASU 2016-02 resulted in a change in the accounting method for the lease portion of the daily charter hire for the chartered-in vessels by the Company and the Company's equity-accounted joint ventures accounted for as operating leases with firm periods of greater than one year, as well as a small number of office leases. On January 1, 2019, a right-of-use asset relating to vessels of $170.0 million and a lease liability of $170.0 million were recognized, equal to the present value of future minimum lease payments. On March 31, 2019, the right-of-use asset relating to vessels was $161.5 million and the lease liability was $161.5 million. The carrying value of the Company's chartered-in vessels has also been reclassified from other non-current assets ($12.9 million – March 31, 2019 and $13.7 million – January 1, 2019) and from other long-term liabilities ($0.4 million – March 31, 2019 and $0.9 million – January 1, 2019) to the right-of-use asset. In addition, on March 31, 2019 the right-of-use asset relating to office leases was $7.6 million and is presented in other non-current assets. The lease liability relating to office leases, presented in accounts payable, accrued liabilities and other and other long-term liabilities, was $7.7 million, and $0.1 million was reflected as a foreign exchange loss. Under ASU 2016-02, the Company and the Company's equity-accounted joint ventures recognize a right-of-use asset and a lease liability on the balance sheet for these charters and office leases based on the present value of future minimum lease payments, whereas previously no right-of-use asset or lease liability was recognized. This has the result of increasing the Company's and its equity-accounted joint ventures' assets and liabilities. The pattern of expense recognition of chartered-in vessels and office leases is expected to remain substantially unchanged, unless the right-of-use asset becomes impaired. |

• | The adoption of ASU 2016-02 results in the recognition of revenue from the reimbursement of scheduled dry-dock expenditures, where such charter contract is accounted for as an operating lease, occurring upon completion of the scheduled dry-dock, instead of ratably over the period between the previous scheduled dry-dock and the next scheduled dry-dock. This change decreased investment in and loans to equity-accounted investments by $3.0 million, and total equity by $3.0 million as at March 31, 2019. The cumulative decrease to opening equity as at January 1, 2019 was $3.0 million. |

Page 8

TEEKAY CORPORATION AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share and per share data)

• | The adoption of ASU 2016-02 results in direct financing lease payments received being presented as an operating cash inflow instead of an investing cash inflow in the consolidated statement of cash flows. Direct financing lease payments received during the three months ended March 31, 2019 and March 31, 2018 were $3.0 million and $2.4 million, respectively. |

• | The adoption of ASU 2016-02 results in sale and leaseback transactions where the seller lessee has a fixed price repurchase option or other situations where the leaseback would be classified as a finance lease being accounted for as a failed sale of the vessel and a failed purchase of the vessel by the buyer lessor. Prior to the adoption of ASU 2016-02 such transactions were accounted for as a completed sale and a completed purchase. Consequently, for such transactions the Company does not derecognize the vessel sold and continues to depreciate the vessel as if it were the legal owner. Proceeds received from the sale of the vessel are recognized as a financial liability and bareboat charter hire payments made by the Company to the lessor are allocated between interest expense and principal repayments on the financial liability. The adoption of ASU 2016-02 has resulted in the sale and leaseback of the Yamal Spirit during the first quarter of 2019 being accounted for as a failed sale and unlike the eight sale-leaseback transactions entered in prior years, the Company is not considered as holding a variable interest in the buyer lessor entity and thus does not consolidate the buyer lessor entity (see Note 6). |

The Company's floating production, storage and offloading (or FPSO) contracts, time charters and voyage charters include both a lease component, consisting of the lease of the vessel, and a non-lease component, consisting of the operation of the vessel for the customer. The Company has elected not to separate the non-lease component from the lease component for all such charters, where the lease component is classified as an operating lease, and to account for the combined component as an operating lease in accordance with Accounting Standards Codification (or ASC) 842 Leases.

In August 2017, the FASB issued Accounting Standards Update 2017-12, Derivatives and Hedging - Targeted Improvements to Accounting for Hedging Activities (or ASU 2017-12). ASU 2017-12 eliminates the requirement to separately measure and report hedge ineffectiveness and generally requires, for qualifying hedges, the entire change in the fair value of a hedging instrument to be presented in the same income statement line as the hedged item. The guidance also modifies the accounting for components excluded from the assessment of hedge effectiveness, eases documentation and assessment requirements and modifies certain disclosure requirements. ASU 2017-12 became effective for the Company on January 1, 2019. This change decreased accumulated other comprehensive (loss) income by $4.8 million as at January 1, 2019, and correspondingly increased opening equity as at January 1, 2019 by $4.8 million.

In June 2016, the FASB issued Accounting Standards Update 2016-13, Financial Instruments - Credit Losses: Measurement of Credit Losses on Financial Instruments (or ASU 2016-13). ASU 2016-13 replaces the incurred loss impairment methodology with a methodology that reflects expected credit losses and requires consideration of a broader range of reasonable and supportable information to inform credit loss estimates. This update is effective for the Company on January 1, 2020, with a modified-retrospective approach. The Company is currently evaluating the effect of adopting this new guidance.

3. Revenues

The Company’s primary source of revenue is chartering its vessels and offshore units to its customers. The Company utilizes four primary forms of contracts, consisting of time-charter contracts, voyage charter contracts, bareboat charter contracts and contracts for FPSO units. The Company also generates revenue from the management and operation of vessels owned by third parties and by equity-accounted investments as well as providing corporate management services to such entities. For a description of these contracts, see "Item 18 - Financial Statements: Note 2" in the Company’s Annual Report on Form 20-F for the year ended December 31, 2018.

Revenue Table

The following tables contain the Company’s revenue for the three months ended March 31, 2019 and 2018, by contract type, by segment and by business lines within segments.

Three Months Ended March 31, 2019 | ||||||||||||||

Teekay LNG Liquefied Gas Carriers | Teekay LNG Conventional Tankers | Teekay Tankers Conventional Tankers | Teekay Parent Offshore Production | Teekay Parent Other | Eliminations and Other | Total | ||||||||

$ | $ | $ | $ | $ | $ | $ | ||||||||

Time charters | 130,775 | 2,762 | 3,410 | — | 6,269 | — | 143,216 | |||||||

Voyage charters | 9,160 | — | 216,417 | — | — | — | 225,577 | |||||||

Bareboat charters | 6,062 | — | — | — | — | — | 6,062 | |||||||

FPSO contracts | — | — | — | 49,438 | — | — | 49,438 | |||||||

Management fees and other | 985 | — | 12,674 | — | 44,390 | (1,129 | ) | 56,920 | ||||||

146,982 | 2,762 | 232,501 | 49,438 | 50,659 | (1,129 | ) | 481,213 | |||||||

Page 9

TEEKAY CORPORATION AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share and per share data)

Three Months Ended March 31, 2018 | ||||||||||||||

Teekay LNG Liquefied Gas Carriers | Teekay LNG Conven-tional Tankers | Teekay Tankers Conven-tional Tankers | Teekay Parent Offshore Production | Teekay Parent Other | Eliminations and Other | Total | ||||||||

$ | $ | $ | $ | $ | $ | $ | ||||||||

Time charters | 93,459 | 5,398 | 22,110 | — | 13,094 | (7,979 | ) | 126,082 | ||||||

Voyage charters | 3,623 | 4,751 | 135,642 | — | — | — | 144,016 | |||||||

Bareboat charters | 5,377 | — | — | — | — | — | 5,377 | |||||||

FPSO contracts | — | — | — | 65,970 | — | — | 65,970 | |||||||

Management fees and other | 2,590 | 108 | 10,713 | — | 38,850 | 316 | 52,577 | |||||||

105,049 | 10,257 | 168,465 | 65,970 | 51,944 | (7,663 | ) | 394,022 | |||||||

The following table contains the Company's total revenue for the three months ended March 31, 2019 and 2018, by contracts or components of contracts accounted for as leases and those not accounted for as leases.

March 31, 2019 | March 31, 2018 | |||||

Lease revenue | ||||||

Lease revenue from lease payments of operating leases | 393,761 | 318,617 | ||||

Interest income on lease receivables | 12,794 | 9,960 | ||||

Variable lease payments – cost reimbursements (1) | 12,008 | 8,862 | ||||

Variable lease payments – other (2) | 205 | (134 | ) | |||

418,768 | 337,305 | |||||

Non-lease revenue | ||||||

Non-lease revenue – related to sales-type or direct financing leases | 5,525 | 4,140 | ||||

Management fees and other income | 56,920 | 52,577 | ||||

62,445 | 56,717 | |||||

Total | 481,213 | 394,022 | ||||

(1) | Reimbursement for vessel operating expenditures and drydocking expenditures received from the Company's customers relating to such costs incurred by the Company to operate the vessel for the customer. |

(2) | Compensation from time-charter contracts based on spot market rates in excess of a base daily hire amount, production tariffs, which are based on the volume of oil produced, the price of oil, as well as other monthly or annual operational performance measures. |

Operating Leases

As at March 31, 2019, the minimum scheduled future rentals to be received by the Company in each of the next five years for the lease and non-lease elements related to time-charters, bareboat charters and FPSO contracts that were accounted for as operating leases were approximately $506.9 million (remainder of 2019), $551.5 million (2020), $487.6 million (2021), $411.3 million (2022) and $320.0 million (2023).

As at December 31, 2018, the minimum scheduled future rentals to be received by the Company in each of the next five years for the lease and non-lease elements related to time-charters, bareboat charters and FPSO contracts that were accounted for as operating leases were approximately $630.8 million (2019), $524.6 million (2020), $457.5 million (2021), $382.0 million (2022) and $291.8 million (2023).

Minimum scheduled future revenues should not be construed to reflect total charter hire revenues for any of the years. Minimum scheduled future revenues do not include revenue generated from new contracts entered into after March 31, 2019 or after December 31, 2018, as applicable, revenue from unexercised option periods of contracts that existed on March 31, 2019 or on December 31, 2018, as applicable, revenue from vessels in the Company’s equity-accounted investments, or variable or contingent revenues accounted for under ASC 842 Leases. In addition, minimum scheduled future operating lease revenues presented in this paragraph have been reduced by estimated off-hire time for any periodic maintenance. The amounts may vary given unscheduled future events such as vessel maintenance.

The net carrying amount of the vessels employed on time-charter contracts, bareboat charter contracts and FPSO contracts that have been accounted for as operating leases at March 31, 2019, was $3.6 billion (December 31, 2018 – $3.4 billion). At March 31, 2019, the cost and accumulated depreciation of such vessels were $4.5 billion (December 31, 2018 – $4.3 billion) and $0.9 billion (December 31, 2018 – $0.8 billion), respectively.

Page 10

TEEKAY CORPORATION AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share and per share data)

Net Investment in Direct Financing Leases

Teekay LNG's time-charter contracts accounted for as direct financing leases contain both a lease component (lease of the vessel) and a non-lease component (operation of the vessel). Teekay LNG has allocated the contract consideration between the lease component and non-lease component on a relative standalone selling price basis. The standalone selling price of the non-lease component has been determined using a cost-plus approach, whereby Teekay LNG estimates the cost to operate the vessel using cost benchmarking studies prepared by a third party, when available, or internal estimates when not available, plus a profit margin. The standalone selling price of the lease component has been determined using an adjusted market approach, whereby Teekay LNG calculates a rate excluding the operating component based on a market time-charter rate from published broker estimates, when available, or internal estimates when not available. Given that there are no observable standalone selling prices for either of these two components, judgment is required in determining the standalone selling price of each component.

Teekay LNG has three liquefied natural gas (or LNG) carriers, excluding vessels in its equity-accounted joint ventures, which are accounted for as direct financing leases. For a description of Teekay LNG's LNG carriers accounted for as direct financing leases, see "Item 18 - Financial Statements: Note 2" to the Company's Annual Report on Form 20-F for the year ended December 31, 2018. The following table lists the components of Teekay LNG's net investments in direct financing leases:

March 31, 2019 | December 31, 2018 | ||||

$ | $ | ||||

Total minimum lease payments to be received | 880,978 | 897,130 | |||

Estimated unguaranteed residual value of leased properties | 291,098 | 291,098 | |||

Initial direct costs and other | 320 | 329 | |||

Less unearned revenue | (600,600 | ) | (613,394 | ) | |

Total | 571,796 | 575,163 | |||

Less current portion | (12,939 | ) | (12,635 | ) | |

Long-term portion | 558,857 | 562,528 | |||

As at March 31, 2019, estimated minimum lease payments to be received by Teekay LNG related to its direct financing leases in each of the next five years are approximately $48.3 million (2019), $64.3 million (2020), $64.2 million (2021), $64.2 million (2022), $64.0 million (2023) and an aggregate of $576.0 million thereafter. The leases are scheduled to end between 2029 and 2039.

As at December 31, 2018, estimated minimum lease payments to be received by Teekay LNG related to its direct financing leases in each of the next five years are approximately $64.2 million (2019), $64.3 million (2020), $64.2 million (2021), $64.2 million (2022), $64.0 million (2023) and an aggregate of $576.2 million thereafter. The leases are scheduled to end between 2029 and 2039.

Contract Liabilities

The Company enters into certain customer contracts that result in situations where the customer will pay consideration upfront for performance to be provided in the following month or months. These receipts are contract liabilities and are presented as deferred revenue until performance is provided. As at March 31, 2019, December 31, 2018, March 31, 2018 and on transition to ASC 606 on January 1, 2018, there were contract liabilities of $22.4 million, $26.4 million, $22.3 million and $29.5 million respectively. During each of the three months ended March 31, 2019 and 2018, the Company recognized $26.4 million of revenue that was included in the contract liability balance as at the beginning of such three-month periods.

4. Related Party Transactions

Teekay Offshore was a related party of Teekay as at March 31, 2019. On September 25, 2017, Teekay, Teekay Offshore and Brookfield Business Partners L.P. (or Brookfield) completed a strategic partnership (or the 2017 Brookfield Transaction), which resulted in the deconsolidation of Teekay Offshore as of that date. On April 29, 2019, Teekay entered into an agreement to sell to Brookfield all of the Company’s remaining interests in Teekay Offshore (or the 2019 Brookfield Transaction), which included the Company’s 49% general partner interest, common units, warrants, and an outstanding $25 million loan from the Company to Teekay Offshore (described below), for total proceeds of $100 million in cash. The 2019 Brookfield Transaction was completed in May 2019.

The Company accounted for its investment in Teekay Offshore's general partner and common units under the equity method of accounting. Based on the 2019 Brookfield Transaction, the Company has remeasured its investment in Teekay Offshore to fair value at March 31, 2019 based on the Teekay Offshore publicly-traded unit price at that date, resulting in a write-down of $64.9 million reflected in the Company's consolidated statements of loss, included in equity loss, for the three months ended March 31, 2019. The Company expects to recognize a loss on sale of approximately $10.0 million with respect to the completion of the 2019 Brookfield Transaction in the second quarter of 2019.

As at March 31, 2019, Teekay had advanced $67.2 million to Teekay Offshore (December 31, 2018 – $83.1 million) and Teekay Offshore had advanced $40.1 million to Teekay (December 31, 2018 – $59.3 million). Such amounts are included in current portion of loans to equity-accounted investments and loans from equity-accounted investments, respectively, on the consolidated balance sheets.

Page 11

TEEKAY CORPORATION AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share and per share data)

In March 2018, Teekay Offshore entered into a loan agreement for a $125.0 million senior unsecured revolving credit facility, of which up to $25.0 million was provided by Teekay and up to $100.0 million was provided by Brookfield. The facility is scheduled to mature in October 2019. As at March 31, 2019, Teekay had advanced $25.0 million to Teekay Offshore under this facility, which is included in the $67.2 million recorded in current portion of loans to equity-accounted investments in the consolidated balance sheets. Teekay’s $25.0 million loan to Teekay Offshore was among the assets sold by Teekay to Brookfield in the 2019 Brookfield Transaction.

Until December 31, 2017, Teekay and its wholly-owned subsidiaries directly and indirectly provided substantially all of Teekay Offshore’s ship management, commercial, technical, strategic, business development and administrative service needs. On January 1, 2018, as part of the 2017 Brookfield Transaction, Teekay Offshore acquired a 100% ownership interest in seven subsidiaries (or the Transferred Subsidiaries) of Teekay at carrying value. The Company recognized a loss of $7.1 million for the three months ended March 31, 2018 related to the sale of the Transferred Subsidiaries and the resultant release of accumulated pension losses from accumulated other comprehensive income, which is recorded in loss on deconsolidation of Teekay Offshore on the Company's consolidated statements of loss. Specifically, the Transferred Subsidiaries provided ship management, commercial, technical, strategic, business development and administrative services to Teekay Offshore, primarily related to Teekay Offshore's FPSO units, shuttle tankers and floating storage and offtake (or FSO) units.

Subsequent to their transfer to Teekay Offshore, the Transferred Subsidiaries continue to provide ship management, commercial, technical, strategic, business development and administrative services to Teekay, primarily related to Teekay's FPSO units. Teekay and certain of its subsidiaries, other than the Transferred Subsidiaries, continue to provide certain other ship management, commercial, technical, strategic and administrative services to Teekay Offshore.

Revenues received by the Company for services provided to Teekay Offshore for the three months ended March 31, 2019 and March 31, 2018 were $5.3 million and $6.5 million, respectively, which were recorded in revenues on the Company's consolidated statements of loss. Fees paid by the Company to Teekay Offshore for services provided by Teekay Offshore to the Company for the three months ended March 31, 2019 and March 31, 2018 were $6.3 million and $6.5 million, respectively, which were recorded in vessel operating expenses and general and administrative expenses on the Company's consolidated statements of loss.

As at March 31, 2019, two shuttle tankers and three FSO units of Teekay Offshore were employed on long-term time-charter-out or bareboat contracts to subsidiaries of Teekay. Time-charter hire expenses paid by the Company to Teekay Offshore for the three months ended March 31, 2019 and March 31, 2018 were $14.7 million and $14.0 million, respectively.

In September 2018, Teekay LNG entered into an agreement with its 52%-owned joint venture with Marubeni Corporation (or the Teekay LNG-Marubeni Joint Venture) to charter in one of Teekay LNG-Marubeni Joint Venture's LNG carriers, the Magellan Spirit, for a period of two years at a fixed-rate. Time-charter hire expense for the three months ended March 31, 2019 was $5.6 million.

The Company provides ship management and corporate services to certain of its equity-accounted joint ventures that own and operate LNG carriers on long-term charters. In addition, the Company is reimbursed for costs incurred by the Company for its seafarers operating these LNG carriers. During the three months ended March 31, 2019 and March 31, 2018, the Company earned $15.8 million and $12.6 million, respectively, of fees pursuant to these management agreements and reimbursement of costs.

5. Segment Reporting

The Company’s segments are described in "Item 18 - Financial Statements: Note 3" to the Company’s Annual Report on Form 20-F for the year ended December 31, 2018. The Company allocates capital and assesses performance from the separate perspectives of its two publicly-traded subsidiaries Teekay LNG and Teekay Tankers (together, the Controlled Daughter Entities), Teekay and its remaining subsidiaries (or Teekay Parent), and, prior to the completion of the 2019 Brookfield Transaction, its equity-accounted investment in Teekay Offshore, as well as from the perspective of the Company's lines of business. The primary focus of the Company’s organizational structure, internal reporting and allocation of resources by the chief operating decision maker is on the Controlled Daughter Entities, Teekay Parent and, prior to the completion of the 2019 Brookfield Transaction, its equity-accounted investment in Teekay Offshore, (the Legal Entity approach), and its segments are presented accordingly on this basis. The Company (which excludes Teekay Offshore) has three primary lines of business: (1) offshore production (FPSO units), (2) LNG and liquefied petroleum gas (or LPG) carriers, and (3) conventional tankers. The Company manages these businesses for the benefit of all stakeholders. The Company incorporates the primary lines of business within its segments, as in certain cases there is more than one line of business in each Controlled Daughter Entity and the Company believes this information allows a better understanding of the Company’s performance and prospects for future net cash flows.

Page 12

TEEKAY CORPORATION AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share and per share data)

The following table includes the Company’s revenues by segment for the three months ended March 31, 2019 and 2018:

Revenues | ||||

Three Months Ended March 31, | ||||

2019 | 2018 | |||

$ | $ | |||

Teekay LNG | ||||

Liquefied Gas Carriers(1) | 146,982 | 105,049 | ||

Conventional Tankers | 2,762 | 10,257 | ||

149,744 | 115,306 | |||

Teekay Tankers | ||||

Conventional Tankers(1) | 232,501 | 168,465 | ||

Teekay Parent | ||||

Offshore Production | 49,438 | 65,970 | ||

Other | 50,659 | 51,944 | ||

100,097 | 117,914 | |||

Eliminations and other | (1,129 | ) | (7,663 | ) |

481,213 | 394,022 | |||

(1) | The amounts in the table below represent revenue earned by each segment from other segments within the group. During 2019, Teekay Tankers' ship-to-ship transfer business provided operational and maintenance services to Teekay LNG Bahrain Operations L.L.C., an entity wholly-owned by Teekay LNG, for the LNG receiving and regasification terminal in Bahrain. During 2018, certain vessels were chartered by Teekay LNG to Teekay Parent. Such intersegment revenue for the three months ended March 31, 2019 and 2018 is as follows: |

Three Months Ended March 31, | ||||

2019 | 2018 | |||

$ | $ | |||

Teekay LNG - Liquefied Gas Carriers | — | 7,979 | ||

Teekay Tankers - Conventional Tankers | 1,129 | — | ||

1,129 | 7,979 | |||

The following table includes the Company’s income (loss) from vessel operations by segment for the three months ended March 31, 2019 and 2018:

Income (loss) from Vessel Operations(1) | ||||

Three Months Ended March 31, | ||||

2019 | 2018 | |||

$ | $ | |||

Teekay LNG | ||||

Liquefied Gas Carriers | 70,443 | 44,545 | ||

Conventional Tankers | (1,082 | ) | (19,403 | ) |

69,361 | 25,142 | |||

Teekay Tankers | ||||

Conventional Tankers | 32,097 | (8,421 | ) | |

Teekay Parent | ||||

Offshore Production | (12,557 | ) | 6,882 | |

Other | (4,669 | ) | (5,098 | ) |

(17,226 | ) | 1,784 | ||

84,232 | 18,505 | |||

(1) | Includes direct general and administrative expenses and indirect general and administrative expenses (allocated to each segment based on estimated use of corporate resources). |

Page 13

TEEKAY CORPORATION AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share and per share data)

As at March 31, 2019 and 2018, the Company accounted for its investment in Teekay Offshore's general partner and common units using the equity method, and recognized an equity loss of $68.0 million in respect of Teekay Offshore for the three months ended March 31, 2019 and equity income of $0.7 million for the three months ended March 31, 2018.

A reconciliation of total segment assets to total assets presented in the accompanying unaudited consolidated balance sheets is as follows:

March 31, 2019 | December 31, 2018 | |||

$ | $ | |||

Teekay LNG – Liquefied Gas Carriers | 5,289,549 | 5,162,756 | ||

Teekay LNG – Conventional Tankers | 13,557 | 36,701 | ||

Teekay Tankers – Conventional Tankers | 2,127,741 | 2,106,169 | ||

Teekay Parent – Offshore Production | 374,959 | 311,550 | ||

Teekay Parent – Conventional Tankers | 3,056 | 13,056 | ||

Teekay Parent – Other | 83,793 | 25,224 | ||

Teekay Offshore | 151,140 | 233,225 | ||

Cash and cash equivalents | 410,724 | 424,169 | ||

Other assets not allocated | 49,104 | 99,024 | ||

Eliminations | (22,138 | ) | (20,204 | ) |

Consolidated total assets | 8,481,485 | 8,391,670 | ||

6. Leases

Obligations Related to Finance Leases

March 31, 2019 | December 31, 2018 | ||||

$ | $ | ||||

Teekay LNG | |||||

LNG Carriers | 1,415,987 | 1,274,569 | |||

Suezmax Tanker | — | 23,987 | |||

Teekay Tankers | |||||

Suezmax Tankers | 162,979 | 165,145 | |||

Aframax Tankers | 180,932 | 184,021 | |||

LR2 Product Tanker | 25,842 | 26,123 | |||

Total obligations related to finance leases | 1,785,740 | 1,673,845 | |||

Less current portion | (85,706 | ) | (102,115 | ) | |

Long-term obligations related to finance leases | 1,700,034 | 1,571,730 | |||

Teekay LNG

As at March 31, 2019, Teekay LNG was a party to finance leases on nine LNG carriers. Upon delivery of these nine LNG carriers between February 2016 and January 2019, Teekay LNG sold these vessels to third parties (or Lessors) and leased them back under 10- to 15-year bareboat charter contracts ending in 2026 through to 2034. At the inception of these leases, the weighted-average interest rate implicit in these leases was 5.2%. The bareboat charter contracts are presented as obligations related to finance leases on the Company's consolidated balance sheets and have purchase obligations at the end of the lease terms.

Teekay LNG consolidates eight of the nine Lessors for financial reporting purposes as variable interest entities. Teekay LNG understands that these vessels and lease operations are the only assets and operations of the Lessors. Teekay LNG operates the vessels during the lease term and as a result, is considered to be, under GAAP, the Lessor's primary beneficiary.

The liabilities of the eight Lessors are loans and are non-recourse to Teekay LNG. The amounts funded to the eight Lessors in order to purchase the vessels materially match the funding to be paid by Teekay LNG's subsidiaries under the sale-leaseback transactions. As a result, the amounts due by Teekay LNG's subsidiaries to the eight Lessors have been included in obligations related to finance leases as representing the Lessors' loans.

Page 14

TEEKAY CORPORATION AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share and per share data)

During January 2019, Teekay LNG sold the Yamal Spirit and leased it back for a period of 15 years, with an option granted to Teekay LNG to extend the lease term by an additional five years. Teekay LNG is required to purchase the vessel at the end of the lease term. Subsequent to the adoption of ASU 2016-02 on January 1, 2019, sale and leaseback transactions where the lessee has a purchase obligation are treated as a failed sale. Consequently, Teekay LNG has not derecognized the vessel and continues to depreciate the asset as if Teekay LNG was the legal owner. Proceeds received from the sale are set up as a financial liability and bareboat charter hire payments made by Teekay LNG to the Lessor are allocated between interest expense and principal repayments on the financial liability.

The obligations of Teekay LNG under the bareboat charter contracts for the nine LNG carriers are guaranteed by Teekay LNG. In addition, the guarantee agreements require Teekay LNG to maintain minimum levels of tangible net worth and aggregate liquidity, and not to exceed a maximum amount of leverage. As at March 31, 2019, Teekay LNG was in compliance with all covenants in respect of the obligations related to its finance leases.

As at March 31, 2019 and December 31, 2018, the remaining commitments related to the financial liabilities of these nine LNG carriers (December 31, 2018 – eight LNG carriers) including the amounts to be paid for the related purchase obligations, approximated $1.9 billion (December 31, 2018 – $1.7 billion), including imputed interest of $513.2 million (December 31, 2018 – $435.3 million), repayable for the remainder of 2019 through 2034, as indicated below:

Commitments | ||||||

At March 31, 2019 | At December 31, 2018 | |||||

Year | $ | $ | ||||

Remainder of 2019 | 101,700 | 119,517 | ||||

2020 | 134,915 | 118,685 | ||||

2021 | 133,542 | 117,772 | ||||

2022 | 132,312 | 116,978 | ||||

2023 | 131,237 | 116,338 | ||||

Thereafter | 1,295,440 | 1,120,670 | ||||

As at December 31, 2018, Teekay LNG was a party, as lessee, to a finance lease on one Suezmax tanker, the Toledo Spirit. As at December 31, 2018, the remaining commitments related to the finance lease for the Suezmax tanker, including the related purchase obligation, approximated $24.2 million, including imputed interest of $0.2 million, repayable in 2019. In January 2019, the charterer, who is also the owner, sold the Toledo Spirit to a third party which resulted in Teekay LNG returning the vessel to its owner and the obligation related to finance lease concurrently being extinguished.

Teekay Tankers

In November 2018, Teekay Tankers completed an $84.7 million sale-leaseback financing transaction with a financial institution relating to four of Teekay Tankers' vessels, consisting of two Aframax tankers, one Suezmax tanker and one Long Range 2 (or LR2) product tanker, the Explorer Spirit, Navigator Spirit, Pinnacle Spirit and Trysil Spirit.

In September 2018, Teekay Tankers completed a $156.6 million sale-leaseback financing transaction with a financial institution relating to six of its Aframax tankers, the Blackcomb Spirit, Emerald Spirit, Garibaldi Spirit, Peak Spirit, Tarbet Spirit and Whistler Spirit.

In July 2017, Teekay Tankers completed a $153.0 million sale-leaseback financing transaction with a financial institution relating to four of its Suezmax tankers, the Athens Spirit, the Beijing Spirit, the Moscow Spirit and the Sydney Spirit.

Under these arrangements, Teekay Tankers transferred the vessels to subsidiaries of the financial institutions (or collectively, the Lessors), and leased the vessels back from the Lessors on bareboat charters ranging from nine- to 12-year terms. Teekay Tankers has the option to purchase each of the 14 tankers at various times starting between July 2020 and November 2021 until the end of their respective lease terms. Teekay Tankers is also obligated to purchase six of the Aframax vessels upon expiration of their respective bareboat charters.

Teekay Tankers understands that these vessels and lease operations are the only assets and operations of the Lessors. Teekay Tankers operates the vessels during the lease terms, and as a result, is considered to be the Lessor's primary beneficiary and therefore Teekay Tankers consolidates the Lessors for financial reporting purposes.

The liabilities of the Lessors are loans that are non-recourse to Teekay Tankers. The amounts funded to the Lessors in order to purchase the vessels materially match the funding to be paid by Teekay Tankers' subsidiaries under these leaseback transactions. As a result, the amounts due by Teekay Tankers' subsidiaries to the Lessors have been included in obligations related to finance leases as representing the Lessors' loans.

The bareboat charters related to each of these vessels require that Teekay Tankers maintain minimum liquidity (cash, cash equivalents and undrawn committed revolving credit lines with at least six months to maturity) of $35.0 million and at least 5.0% of Teekay Tankers' consolidated debt and obligations related to finance leases (excluding applicable security deposits reflected in restricted cash – non-current on the Company's consolidated balance sheets).

Page 15

TEEKAY CORPORATION AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share and per share data)

Four of the bareboat charters require Teekay Tankers to maintain, for each vessel, a hull coverage ratio of 90% of the total outstanding principal balance during the first three years of the lease period and 100% of the total outstanding principal balance thereafter. As at March 31, 2019, this ratio was approximately 110% (December 31, 2018 – 101%).

Six of the bareboat charters require Teekay Tankers to maintain, for each vessel, a hull coverage ratio of 75% of the total outstanding principal balance during the first year of the lease period, 78% for the second year, 80% for the following two years and 90% of the total outstanding principal balance thereafter. As at March 31, 2019, this ratio was approximately 92% (December 31, 2018 – 91%).

The remaining four bareboat charters also require Teekay Tankers to maintain, for each vessel, a hull overage ratio of 100% of the total outstanding principal balance. As at March 31, 2019, this ratio was approximately 131% (December 31, 2018 – 122%).

Such requirements are assessed annually with reference to vessel valuations compiled by one or more agreed upon third parties. As at March 31, 2019, Teekay Tankers was in compliance with all covenants in respect of its obligations related to finance leases.

As at March 31, 2019 and December 31, 2018, the total remaining commitments related to the financial liabilities of Teekay Tankers' Suezmax, Aframax and LR2 product tankers, including the amounts to be paid for the related purchase obligations, approximated $544.7 million (December 31, 2018 – $557.1 million), including imputed interest of $174.9 million (December 31, 2018 – $181.8 million), repayable from 2019 through 2030, as indicated below:

Commitments | ||||||

At March 31, 2019 | At December 31, 2018 | |||||

Year | $ | $ | ||||

Remainder of 2019 | 35,613 | 47,962 | ||||

2020 | 47,373 | 47,373 | ||||

2021 | 47,237 | 47,237 | ||||

2022 | 47,230 | 47,230 | ||||

2023 | 47,222 | 47,222 | ||||

Thereafter | 319,981 | 320,064 | ||||

Operating Lease Liabilities

The Company charters-in vessels from other vessel owners on time-charter-in and bareboat charter contracts, whereby the vessel owner provides use of the vessel to the Company, and, in the case of time-charter-in contracts, also operates the vessel for the Company. A time-charter-in contract is typically for a fixed period of time, although in certain cases the Company may have the option to extend the charter. The Company typically pays the owner a daily hire rate that is fixed over the duration of the charter. The Company is generally not required to pay the daily hire rate for time-charters during periods the vessel is not able to operate.

The Company has determined that all of its time-charter-in contracts contain both a lease component (lease of the vessel) and a non-lease component (operation of the vessel). The Company has allocated the contract consideration between the lease component and non-lease component on a relative standalone selling price basis. The standalone selling price of the non-lease component has been determined using a cost-plus approach, whereby the Company estimates the cost to operate the vessel using cost benchmarking studies prepared by a third party, when available, or internal estimates when not available, plus a profit margin. The standalone selling price of the lease component has been determined using an adjusted market approach, whereby the Company calculates a rate excluding the operating component based on a market time-charter rate information from published broker estimates, when available, or internal estimates when not available. Given that there are no observable standalone selling prices for either of these two components, judgment is required in determining the standalone selling price of each component. The discount rate of the lease is determined using the Company’s incremental borrowing rate, which is based on the fixed interest rate the Company could obtain when entering into a secured loan facility of similar terms for an amount equal to the total minimum lease payments. The bareboat charter contracts contain only a lease component.

With respect to time-charter-in and bareboat charter contracts with an original term of more than one year, for the three months ended March 31, 2019, the Company incurred $25.1 million of time-charter and bareboat hire expense related to these time-charter and bareboat charter contracts, of which $17.3 million was allocable to the lease component and $7.8 million was allocable to the non-lease component. The $17.3 million allocable to the lease component approximates the cash paid for the amounts included in lease liabilities and is reflected as a reduction in operating cash flows for the three months ended March 31, 2019. Two of Teekay Tankers' time-charter-in contracts each have an option to extend the charter for an additional one-year term. Since it is not reasonably certain that Teekay Tankers will exercise the options, the lease components of the options are not recognized as part of the right-of-use assets and lease liabilities. As at March 31, 2019, the weighted-average remaining lease term and weighted-average discount rate for these time-charter-in and bareboat charter contracts were 3.0 years and 6.5%, respectively.

Page 16

TEEKAY CORPORATION AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share and per share data)

The Company has elected to recognize the lease payments of short-term leases in its consolidated statements of loss on a straight-line basis over the lease term and variable lease payments in the period in which the obligation for those payments is incurred, which is consistent with the recognition of payment for the non-lease component. The Company considers as short-term leases those with an original term of one year or less, excluding leases with an option to extend the lease for greater than one year or an option to purchase the underlying asset where the lessee is deemed reasonably certain to exercise the applicable option. For the three months ended March 31, 2019, the Company incurred $4.3 million of time-charter hire expense related to time-charter-in contracts classified as short-term leases.

During the three months ended March 31, 2019, Teekay Tankers chartered in two LR2 vessels each for a period of 24 months, which resulted in the Company recognizing a right-of-use asset of $14.7 million on the lease commencement date. In addition, Teekay Tankers has the option to extend each of these charters by an additional 12 months.

A maturity analysis of the Company’s operating lease liabilities from time-charter-in and bareboat charter contracts (excluding short-term leases) at March 31, 2019 is as follows:

Lease Commitment | Non-Lease Commitment | Total Commitment | |||||||

Year | $ | $ | $ | ||||||

Payments | |||||||||

April to December 2019 | 51,484 | 24,831 | 76,315 | ||||||

2020 | 59,777 | 31,054 | 90,831 | ||||||

2021 | 37,002 | 15,858 | 52,860 | ||||||

2022 | 16,146 | 3,971 | 20,117 | ||||||

2023 | 9,227 | — | 9,227 | ||||||

Thereafter | 5,713 | — | 5,713 | ||||||

Total payments | 179,349 | 75,714 | 255,063 | ||||||

Less: imputed interest | (17,870 | ) | |||||||

Carrying value of operating lease liabilities | 161,479 | ||||||||

As at March 31, 2019, minimum commitments to be incurred by the Company under short-term time-charter-in contracts were approximately $10.5 million (remainder of 2019) and $0.6 million (2020).

As at December 31, 2018, minimum commitments to be incurred by the Company under vessel operating leases by which the Company charters-in vessels were approximately $116.3 million (2019), $90.4 million (2020), $53.4 million (2021), $9.1 million (2022), $9.1 million (2023) and $5.6 million thereafter.

7. Asset Impairments

The Company's write-downs generally consist of those vessels approaching the end of their useful lives as well as other vessels it strategically sells to reduce exposure to a certain vessel class.

The following table contains the write-downs for the three months ended March 31, 2019 and 2018:

Asset Impairments | ||||||||||

Three Months Ended March 31, | ||||||||||

Segment | Asset Type | Completion of Sale Date | 2019 $ | 2018 $ | ||||||

Teekay Parent Segment - Offshore Production (1) | FPSO | N/A | (3,328 | ) | — | |||||

Teekay LNG Segment – Conventional Tankers (2) | Handymax | N/A | — | (13,000 | ) | |||||

Teekay LNG Segment – Conventional Tankers (3) | 2 Suezmaxes | Oct/Dec-2018 | — | (5,662 | ) | |||||

Total | (3,328 | ) | (18,662 | ) | ||||||

(1) | In March 2019, the Company took an impairment charge in respect of certain of its FPSO-related assets. |

(2) | In March 2018, the carrying value of the Alexander Spirit conventional tanker was written down to its estimated fair value, using an appraised value, as a result of changes in the Company's expectations of the vessel's future opportunities once its current charter contract ends in 2019. |

(3) | In June and August 2017, the charterer for the European Spirit and African Spirit Suezmax tankers gave formal notices to Teekay LNG that it will not exercise its one-year extension option under the charter contracts and redelivered the tankers in August 2017 and November 2017, respectively. Upon receiving these notifications, Teekay LNG commenced marketing the vessels for sale. Based on second-hand market comparable values at the time, Teekay LNG wrote down the vessels to their estimated resale values and they were presented as held for sale on the consolidated balance sheets as at December 31, 2017. During the three months ended March 31, 2018, the Partnership recorded a further write-down of the vessels to their estimated resale value as at March 31, 2018. In the fourth quarter of 2018, Teekay LNG sold the European Spirit and African Spirit for net proceeds of $15.7 million and $12.8 million, respectively, using the net proceeds from the sales primarily to repay its existing term loans associated with the vessels. |

Page 17

TEEKAY CORPORATION AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share and per share data)

8. Accounts Payable, Accrued Liabilities and Other

March 31, 2019 | December 31, 2018 | ||||

$ | $ | ||||

Accounts payable | 61,946 | 31,201 | |||

Accrued liabilities | |||||

Voyage and vessel expenses | 100,192 | 98,135 | |||

Interest | 33,461 | 47,731 | |||

Payroll and related liabilities | 37,997 | 41,275 | |||

Deferred revenues and gains – current | 26,339 | 30,108 | |||

In-process revenue contracts – current | 5,933 | 5,930 | |||

Office lease liability (note 2) | 3,029 | — | |||

268,897 | 254,380 | ||||

9. Long-Term Debt

March 31, 2019 | December 31, 2018 | ||||

$ | $ | ||||

Revolving Credit Facilities | 587,997 | 642,997 | |||

Senior Notes (8.5%) due January 15, 2020 | 497,657 | 508,577 | |||

Convertible Senior Notes (5%) due January 15, 2023 | 125,000 | 125,000 | |||

Norwegian Kroner-denominated Bonds due through August 2023 | 353,553 | 352,973 | |||

U.S. Dollar-denominated Term Loans due through 2030 | 1,512,153 | 1,536,499 | |||

Euro-denominated Term Loans due through 2024 | 187,301 | 193,781 | |||

Other U.S. Dollar-denominated loan | 3,300 | 3,300 | |||

Total principal | 3,266,961 | 3,363,127 | |||

Less unamortized discount and debt issuance costs | (38,470 | ) | (43,604 | ) | |

Total debt | 3,228,491 | 3,319,523 | |||

Less current portion | (517,957 | ) | (242,137 | ) | |

Long-term portion | 2,710,534 | 3,077,386 | |||

As of March 31, 2019, the Company had five revolving credit facilities (or the Revolvers) available, which, as at such date, provided for aggregate borrowings of up to $1.0 billion, of which $0.4 billion was undrawn. Interest payments are based on LIBOR plus margins; the margins ranged between 1.40% and 3.95% at March 31, 2019 and at December 31, 2018. The aggregate amount available under the Revolvers is scheduled to decrease by $23.9 million (remainder of 2019), $408.0 million (2020), $333.9 million (2021) and $192.0 million (2022). The Revolvers are collateralized by first-priority mortgages granted on 38 of the Company’s vessels, together with other related security, and include a guarantee from Teekay or its subsidiaries for all but one of the Revolvers' outstanding amounts. Included in other related security are 25.2 million common units in Teekay LNG, 40.3 million Class A common shares in Teekay Tankers and, prior to the 2019 Brookfield Transaction, 56.6 million common units in Teekay Offshore, to secure a $150 million credit facility.

The Company’s 8.5% senior unsecured notes are due January 15, 2020 with an original aggregate principal amount of $450 million (the Original Notes). The Original Notes issued on January 27, 2010 were sold at a price equal to 99.2% of par. During 2014, the Company repurchased $57.3 million of the Original Notes. In November 2015, the Company issued an aggregate principal amount of $200 million of the Company’s 8.5% senior unsecured notes due on January 15, 2020 (or the Additional Notes) at 99.01% of face value, plus accrued interest from July 15, 2015. The Additional Notes are an additional issuance of the Company's Original Notes (collectively referred to as the 2020 Notes). The Additional Notes were issued under the same indenture governing the Original Notes, and are fungible with the Original Notes. The discount on the 2020 Notes is accreted through the maturity date of the notes using the effective interest rate of 8.67% per year. During 2018, the Company repurchased $84.1 million in aggregate principal amount of the 2020 Notes. During the first quarter of 2019, the Company repurchased an additional $10.9 million in aggregate principal amount of the 2020 Notes. In April 2019, the Company commenced a cash tender offer to purchase any and all of its outstanding 2020 Notes. In May 2019, the Company completed the cash tender offer and purchased $460.9 million in aggregate principal amount of the 2020 Notes and issued $250.0 million in aggregate principal amount of 9.25% senior secured notes due November 2022 (or the 2022 Notes) (see Note 19) for net proceeds of approximately $241 million. Accordingly, $241 million of the 2020 Notes have been classified as long-term debt as at March 31, 2019.

The 2020 Notes rank equally in right of payment with all of Teekay's existing and future senior unsecured debt and senior to any future subordinated debt of Teekay. The 2020 Notes are not guaranteed by any of Teekay's subsidiaries and effectively rank behind all existing and future secured debt of Teekay and other liabilities of its subsidiaries.

Page 18

TEEKAY CORPORATION AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share and per share data)

The Company may redeem the 2020 Notes in whole or in part at any time before their maturity date at a redemption price equal to the greater of (i) 100% of the principal amount of the 2020 Notes to be redeemed and (ii) the sum of the present values of the remaining scheduled payments of principal and interest on the 2020 Notes to be redeemed (excluding accrued interest), discounted to the redemption date on a semi-annual basis, at the treasury yield plus 50 basis points, plus accrued and unpaid interest to the redemption date.

On January 26, 2018, Teekay Parent completed a private offering of $125.0 million in aggregate principal amount of 5% Convertible Senior Notes due January 15, 2023 (the Convertible Notes). The Convertible Notes are convertible into Teekay’s common stock, initially at a rate of 85.4701 shares of common stock per $1,000 principal amount of Convertible Notes. This represents an initial effective conversion price of $11.70 per share of common stock. The initial conversion price represents a premium of 20% to the concurrent common stock offering price of $9.75 per share. The conversion rate is subject to customary adjustments for, among other things, payments of dividends by Teekay Parent beyond the current quarterly dividend of $0.055 per share of common stock. On issuance of the Convertible Notes, $104.6 million of the net proceeds was reflected in long-term debt, including unamortized discount, and is being accreted to $125.0 million over its five-year term through interest expense. The remaining amount of the net proceeds of $16.1 million was allocated to the conversion feature and reflected in additional paid-in capital.

Teekay LNG has a total of Norwegian Kroner (or NOK) 3.1 billion in senior unsecured bonds issued in the Norwegian bond market at March 31, 2019 that mature through August 2023. As of March 31, 2019, the total carrying amount of the senior unsecured bonds was $353.6 million. The bonds are listed on the Oslo Stock Exchange. The interest payments on the bonds are based on NIBOR plus a margin, which ranges from 3.70% to 6.00%. The Company entered into cross currency rate swaps to swap all interest and principal payments of the bonds into U.S. Dollars, with the interest payments fixed at rates ranging from 5.92% to 7.89%, and the transfer of the principal amount fixed at $382.5 million upon maturity in exchange for NOK 3.1 billion (see Note 15).

As of March 31, 2019, the Company had 11 U.S. Dollar-denominated term loans outstanding, which totaled $1.5 billion in aggregate principal amount (December 31, 2018 – $1.5 billion). Interest payments on the term loans are based on LIBOR plus a margin, of which two of the term loans have additional tranches with a weighted average fixed rate of 4.62%. At March 31, 2019 and December 31, 2018, the margins ranged between 0.30% and 3.50%. All but one of the term loans, which is repayable on demand, require payments in quarterly or semi-annual installments commencing three or six months after delivery of each newbuilding vessel financed thereby, and nine of the term loans have balloon or bullet repayments due at maturity. The term loans are collateralized by first-priority mortgages on 24 (December 31, 2018 – 24) of the Company’s vessels, together with certain other security.

Teekay LNG has two Euro-denominated term loans outstanding, which, as at March 31, 2019, totaled 167.0 million Euros ($187.3 million) (December 31, 2018 – 169.0 million Euros ($193.8 million)). Teekay LNG is servicing the loans with funds generated by two Euro-denominated, long-term time-charter contracts. Interest payments on the loans are based on EURIBOR plus a margin. At March 31, 2019 and December 31, 2018, the margins ranged between 0.60% and 1.95%. The Euro-denominated term loans reduce in monthly and semi-annual payments with varying maturities through 2024, are collateralized by first-priority mortgages on two of Teekay LNG's vessels, together with certain other security, and are guaranteed by Teekay LNG and one of its subsidiaries.

Both Euro-denominated term loans and NOK-denominated bonds are revalued at the end of each period using the then-prevailing U.S. Dollar exchange rate. Due primarily to the revaluation of the Company’s NOK-denominated bonds, the Company’s Euro-denominated term loans and restricted cash, and the change in the valuation of the Company’s cross currency swaps, the Company recognized a foreign exchange loss of $2.6 million (2018 – gain of $0.02 million) during the three months ended March 31, 2019.

The weighted-average interest rate on the Company’s aggregate long-term debt as at March 31, 2019 was 5.2% (December 31, 2018 – 5.1%). This rate does not include the effect of the Company’s interest rate swap agreements (see Note 15).

Teekay has guaranteed obligations pursuant to certain credit facilities of Teekay Tankers. As at March 31, 2019, the aggregate outstanding balance on such credit facilities was $161.1 million.

The aggregate annual long-term debt principal repayments required to be made by the Company subsequent to March 31, 2019, after giving effect to the 2020 Notes repurchased and the 2022 Notes issued by Teekay Parent in May 2019, are $207.8 million (remainder of 2019), $937.9 million (2020), $837.1 million (2021), $419.1 million (2022), $337.1 million (2023) and $528.0 million (thereafter).

The Company’s long-term debt agreements generally provide for maintenance of minimum consolidated financial covenants and five loan agreements require the maintenance of vessel market value to loan ratios. As at March 31, 2019, these ratios ranged from 133% to 210% compared to their minimum required ratios of 115% to 135%. The vessel values used in these ratios are the appraised values provided by third parties where available, or prepared by the Company based on second-hand sale and purchase market data. Changes in the LNG/LPG carrier and conventional tanker markets could negatively affect the Company's compliance with these ratios.

Page 19

TEEKAY CORPORATION AND SUBSIDIARIES

NOTES TO THE UNAUDITED CONSOLIDATED FINANCIAL STATEMENTS

(all tabular amounts stated in thousands of U.S. Dollars, other than share and per share data)

Two of Teekay Tankers’ term loans require Teekay Parent and Teekay Tankers collectively to maintain the greater of (a) free cash (cash and cash equivalents) of at least $100.0 million for one of the term loans and $50.0 million for the other and (b) an aggregate of free cash and undrawn committed revolving credit lines with at least six months to maturity of at least 7.5% for one of the term loans and 5.0% for the other, of their total debt. In addition, certain loan agreements require Teekay Tankers to maintain minimum liquidity (cash, cash equivalents and undrawn committed revolving credit lines with at least six months to maturity) of $35.0 million and at least 5.0% of Teekay Tankers' total consolidated debt. Certain loan agreements require Teekay LNG to maintain a minimum level of tangible net worth, and minimum liquidity (cash, cash equivalents and undrawn committed revolving credit lines with at least six months to maturity) of $35.0 million, and not to exceed a maximum level of financial leverage.

As at March 31, 2019, the Company was in compliance with all covenants under its credit facilities and other long-term debt.

10. Capital Stock

The authorized capital stock of Teekay at March 31, 2019 and December 31, 2018 was 25 million shares of preferred stock, with a par value of $1 per share, and 725 million shares of common stock, with a par value of $0.001 per share. As at March 31, 2019, Teekay had no shares of preferred stock issued.

In April 2019, Teekay implemented a continuous offering program (or COP) under which Teekay may issue shares of its common stock, at market prices up to a maximum aggregate amount of $63.0 million.

During the three months ended March 31, 2018, Teekay completed a public offering of 10.0 million common shares priced at $9.75 per share, raising net proceeds of approximately $93.0 million, issued 1.1 million shares of common stock as part of a COP initiated in 2016 generating net proceeds of $10.7 million, and issued 0.2 million shares of common stock pursuant to stock options, restricted stock units and restricted stock awards.