UNITED STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM 10 - Q

☑

QUARTERLY

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE

ACT OF 1934

For the

quarterly period ended September 30, 2019

or

☐

TRANSITION

REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE

ACT OF 1934

For the

transition period from ___________ to __________

Commission

file number: 001-15543

PALATIN TECHNOLOGIES, INC.

(Exact

name of registrant as specified in its charter)

|

Delaware

|

|

95-4078884

|

|

(State

or other jurisdiction of

incorporation

or organization)

|

|

(I.R.S.

Employer Identification No.)

|

|

|

|

|

|

4B Cedar Brook Drive

Cranbury, New Jersey

|

|

08512

|

|

(Address

of principal executive offices)

|

|

(Zip

Code)

|

(609) 495-2200

(Registrant’s

telephone number, including area code)

Securities

registered pursuant to Section 12(b) of the Act:

|

Title of Each Class

|

Trading Symbol

|

Name of Each Exchange

on Which Registered

|

|

Common

Stock, par value $.01 per share

|

PTN

|

NYSE

American

|

Indicate

by check mark whether the registrant (1) has filed all reports

required to be filed by Section 13 or 15(d) of the Securities

Exchange Act of 1934, as amended during the preceding 12 months (or

for such shorter period that the registrant was required to file

such reports), and (2) has been subject to such filing requirements

for the past 90 days.

Yes

☑ No ☐

Indicate

by check mark whether the registrant has submitted electronically,

every Interactive Data File required to be submitted pursuant to

Rule 405 of Regulation S-T

(§232.405 of this chapter) during the preceding 12

months (or for such shorter period that the registrant was required

to submit such files). Yes ☑ No ☐

Indicate

by check mark whether the registrant is a large accelerated filer,

an accelerated filer, a non-accelerated filer, a smaller reporting

company, or an emerging growth company. See the definitions of

“large accelerated filer,” “accelerated

filer,” “smaller reporting company,” and

“emerging growth company” in Rule 12b-2 of the Exchange

Act:

|

Large

accelerated filer

|

☐

|

Accelerated

filer

|

☑

|

|

Non-accelerated

filer

|

☐

|

Smaller

reporting company

|

☑

|

|

Emerging

growth company

|

☐

|

|

|

If an

emerging growth company, indicate by check mark if the registrant

has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided

pursuant to Section 7(a)(2)(B) of the Exchange Act.

☐

Indicate

by check mark whether the registrant is a shell company (as defined

in Rule 12b-2 of the Exchange Act). Yes ☐ No

☑

Indicate

the number of shares outstanding of each of the registrant’s

classes of common stock, as of the latest practicable date

(November 8, 2019): 229,116,104

|

|

Page

|

|

|

|

|

|

|

|

1

|

|

|

2

|

|

|

3

|

|

|

4

|

|

|

5

|

|

|

17

|

|

|

20

|

|

|

20

|

|

|

|

|

|

21

|

|

|

21

|

|

|

21

|

|

|

21

|

|

|

21

|

|

|

21

|

|

|

22

|

|

|

|

|

|

23

|

|

i

Special Note Regarding Forward-Looking Statements

In this

Quarterly Report on Form 10-Q (this “Quarterly Report”)

references to “we,” “our,”

“us,” the “Company” or

“Palatin” means Palatin Technologies, Inc. and its

subsidiary.

Statements

in this Quarterly Report, as well as oral statements that may be

made by us or by our officers, directors, or employees acting on

our behalf, that are not historical facts constitute

“forward-looking statements,” which are made pursuant

to the safe harbor provisions of Section 21E of the Securities

Exchange Act of 1934 (the “Exchange Act”). The

forward-looking statements in this Quarterly Report do not

constitute guarantees of future performance. Investors are

cautioned that statements that are not strictly historical facts

contained in this Quarterly Report, including, without limitation,

the following are forward looking statements:

●

our ability, and

the ability of our licensees, to successfully commercialize

Vyleesi™ (the trade name for bremelanotide) for the treatment

of premenopausal women with acquired, generalized hypoactive sexual

desire disorder (“HSDD”) or obtain approvals in

countries other than the United States;

●

estimates of our

expenses, future revenue and capital requirements;

●

our ability to

achieve revenues from the sale of our product candidates, and to

achieve and maintain profitability;

●

our ability to

advance product candidates into, and successfully complete,

clinical trials;

●

the initiation,

timing, progress and results of future preclinical studies and

clinical trials, and our research and development

programs;

●

our expectations

regarding performance of our exclusive licensees of Vyleesi™

for the treatment of premenopausal women with HSDD, which is a type

of female sexual dysfunction (“FSD”),

including:

o

AMAG

Pharmaceuticals, Inc. (“AMAG”) for North

America,

o

Shanghai Fosun

Pharmaceutical Industrial Development Co. Ltd.

(“Fosun”), a subsidiary of Shanghai Fosun

Pharmaceutical (Group) Co., Ltd., for the territories of the

People’s Republic of China, Taiwan, Hong Kong S.A.R. and

Macau S.A.R. (collectively, “China”), and

o

Kwangdong

Pharmaceutical Co., Ltd. (“Kwangdong”) for the Republic

of Korea (“Korea”);

●

our expectation

regarding the timing of regulatory submissions and approvals of

Vyleesi for HSDD in jurisdictions outside the United

States;

●

our expectations

regarding the potential market size and market acceptance for

Vyleesi for HSDD and our other product candidates, if approved for

commercial use;

●

our expectations

regarding the clinical efficacy and utility of our melanocortin

agonist product candidates for treatment of inflammatory and

autoimmune related diseases and disorders, including ocular

indications;

●

our ability to

compete with other products and technologies treating the same or

similar indications as our product candidates;

●

the ability of our

third-party collaborators to timely carry out their duties under

their agreements with us;

●

the ability of our

contract manufacturers to perform their manufacturing activities

for us in compliance with applicable regulations;

●

our ability to

recognize the potential value of our licensing arrangements with

third parties;

●

our ability to

obtain adequate reimbursement from Medicare, Medicaid, private

insurers and other healthcare payers;

●

our ability to

maintain product liability insurance at a reasonable cost or in

sufficient amounts, if at all;

●

the performance and

retention of our management team, senior staff professionals, and

third-party contractors and consultants;

●

the scope of

protection we are able to establish and maintain for intellectual

property rights covering our product candidates and technology in

the United States and throughout the world;

●

our compliance with

federal and state laws and regulations;

●

the timing and

costs associated with obtaining regulatory approval for our product

candidates;

●

our ability to

obtain additional financing on terms acceptable to us, or to

all;

●

the impact of

fluctuations in foreign exchange rates;

●

the impact of

legislative or regulatory healthcare reforms in the United

States;

●

our ability to

adapt to changes in global economic conditions as well as competing

products and technologies; and

●

our ability to

remain listed on the NYSE American stock exchange.

Such

forward-looking statements involve risks, uncertainties and other

factors that could cause our actual results to be materially

different from historical results or from any results expressed or

implied by such forward-looking statements. Our future operating

results are subject to risks and uncertainties and are dependent

upon many factors, including, without limitation, the risks

identified under the caption “Risk Factors” and

elsewhere in this Quarterly Report, and any of those made in our

other reports filed with the U.S. Securities and Exchange

Commission (the “SEC”). Except as required by law, we

do not intend, and undertake no obligation, to publicly update

forward-looking statements to reflect events or circumstances after

the date of this document or to reflect the occurrence of

unanticipated events.

Palatin

Technologies® is a registered trademark of Palatin

Technologies, Inc. Vyleesi™ is a trademark of AMAG

Pharmaceuticals, Inc. in North America and of Palatin Technologies,

Inc. elsewhere in the world.

ii

PART I – FINANCIAL

INFORMATION

Item 1. Financial Statements.

|

PALATIN TECHNOLOGIES, INC.

|

||

|

and

Subsidiary

|

||

|

Consolidated

Balance Sheets

|

||

|

(unaudited)

|

||

|

|

|

|

|

|

September

30,

2019

|

June

30,

2019

|

|

ASSETS

|

|

|

|

Current

assets:

|

|

|

|

Cash and cash

equivalents

|

$96,698,232

|

$43,510,422

|

|

Accounts

receivable

|

97,379

|

60,265,970

|

|

Prepaid expenses

and other current assets

|

597,853

|

637,289

|

|

Total current

assets

|

97,393,464

|

104,413,681

|

|

|

|

|

|

Property and

equipment, net

|

186,166

|

141,539

|

|

Right-of-use

assets

|

213,065

|

-

|

|

Other

assets

|

179,916

|

179,916

|

|

Total

assets

|

$97,972,611

|

$104,735,136

|

|

|

|

|

|

LIABILITIES

AND STOCKHOLDERS’ EQUITY

|

|

|

|

Current

liabilities:

|

|

|

|

Accounts

payable

|

$57,823

|

$504,787

|

|

Accrued

expenses

|

1,579,460

|

2,848,692

|

|

Notes payable, net

of discount

|

-

|

332,896

|

|

Other current

liabilities

|

213,065

|

499,517

|

|

Total

liabilities

|

1,850,348

|

4,185,892

|

|

|

|

|

|

Stockholders’

equity:

|

|

|

|

Preferred stock of

$0.01 par value – authorized 10,000,000 shares; shares issued

and outstanding designated as follows:

|

|

|

|

Series A

Convertible: authorized 264,000 shares: issued and outstanding

4,030 shares as of September 30, 2019 and June 30,

2019

|

40

|

40

|

|

Common stock of

$0.01 par value – authorized 300,000,000 shares:

|

|

|

|

issued and

outstanding 227,697,257 shares as of September 30, 2019 and

226,815,363 shares as of June 30, 2019

|

2,276,973

|

2,268,154

|

|

Additional paid-in

capital

|

394,119,078

|

394,053,929

|

|

Accumulated

deficit

|

(300,273,828)

|

(295,772,879)

|

|

Total

stockholders’ equity

|

96,122,263

|

100,549,244

|

|

Total liabilities

and stockholders’ equity

|

$97,972,611

|

$104,735,136

|

The

accompanying notes are an integral part of these consolidated

financial statements.

1

|

PALATIN TECHNOLOGIES, INC.

|

||

|

and

Subsidiary

|

||

|

Consolidated

Statements of Operations

|

||

|

(unaudited)

|

||

|

|

|

|

|

|

Three Months

Ended September 30

|

|

|

|

2019

|

2018

|

|

|

|

|

|

REVENUES

|

|

|

|

License and

contract

|

$97,379

|

$34,505

|

|

|

|

|

|

OPERATING

EXPENSES

|

|

|

|

Research and

development

|

3,127,489

|

3,622,691

|

|

General and

administrative

|

1,832,442

|

2,040,582

|

|

Total operating

expenses

|

4,959,931

|

5,663,273

|

|

|

|

|

|

Loss from

operations

|

(4,862,552)

|

(5,628,768)

|

|

|

|

|

|

OTHER INCOME

(EXPENSE)

|

|

|

|

Investment

income

|

370,654

|

153,583

|

|

Interest

expense

|

(9,051)

|

(206,871)

|

|

Total other income

(expense), net

|

361,603

|

(53,288)

|

|

|

|

|

|

NET

LOSS

|

$(4,500,949)

|

$(5,682,056)

|

|

|

|

|

|

Basic net loss per

common share

|

$(0.02)

|

$(0.03)

|

|

|

|

|

|

Diluted net loss

per common share

|

$(0.02)

|

$(0.03)

|

|

|

|

|

|

Weighted average

number of common shares outstanding used in computing basic net

loss per common share

|

233,113,241

|

205,009,278

|

|

|

|

|

|

Weighted average

number of common shares outstanding used in computing diluted net

loss per common share

|

233,113,241

|

205,009,278

|

The

accompanying notes are an integral part of these consolidated

financial statements.

2

|

PALATIN TECHNOLOGIES, INC.

|

||||||||

|

and Subsidiary

|

||||||||

|

Consolidated Statements of Stockholders’ Equity

|

||||||||

|

(unaudited)

|

|

|

|

|

|

|

Additional

|

|

|

|

|

Preferred

Stock

|

Common

Stock

|

Paid-in

|

Accumulated

|

|

||

|

|

Shares

|

Amount

|

Shares

|

Amount

|

Capital

|

Deficit

|

Total

|

|

Balance, June 30,

2019

|

4,030

|

$40

|

226,815,363

|

$2,268,154

|

$394,053,929

|

$(295,772,879)

|

$100,549,244

|

|

Stock-based

compensation

|

-

|

-

|

224,000

|

2,240

|

825,495

|

-

|

827,735

|

|

Sale of common stock , net of

costs

|

-

|

-

|

657,894

|

6,579

|

573,151

|

-

|

579,730

|

|

Warrant

repurchase

|

-

|

-

|

-

|

-

|

(1,333,497)

|

-

|

(1,333,497)

|

|

Net loss

|

-

|

-

|

-

|

-

|

-

|

(4,500,949)

|

(4,500,949)

|

|

Balance, September 30,

2019

|

4,030

|

$40

|

227,697,257

|

$2,276,973

|

$394,119,078

|

$(300,273,828)

|

$96,122,263

|

|

|

|

|

Additional

|

|

|

||

|

|

Preferred

Stock

|

Common

Stock

|

Paid-in

|

Accumulated

|

|

||

|

|

Shares

|

Amount

|

Shares

|

Amount

|

Capital

|

Deficit

|

Total

|

|

Balance, June 30,

2018

|

4,030

|

$40

|

200,554,205

|

$2,005,542

|

$357,005,233

|

$(332,045,906)

|

$26,964,909

|

|

Cumulative effect of accounting

change

|

-

|

-

|

-

|

-

|

-

|

500,000

|

500,000

|

|

Stock-based

compensation

|

-

|

-

|

319,817

|

3,198

|

1,230,387

|

-

|

1,233,585

|

|

Sale of common stock , net of

costs

|

-

|

-

|

2,225,145

|

22,251

|

2,200,196

|

-

|

2,222,447

|

|

Withholding taxes related to

restricted stock units

|

-

|

-

|

(67,038)

|

(670)

|

(65,322)

|

-

|

(65,992)

|

|

Net loss

|

-

|

-

|

-

|

-

|

-

|

(5,682,056)

|

(5,682,056)

|

|

Balance, September 30,

2018

|

4,030

|

$40

|

203,032,129

|

$2,030,321

|

$360,370,494

|

$(337,227,962)

|

$25,172,893

|

The

accompanying notes are an integral part of these consolidated

financial statements.

3

|

PALATIN

TECHNOLOGIES, INC.

|

||

|

and

Subsidiary

|

||

|

Consolidated Statements of Cash Flows

|

||

|

(unaudited)

|

||

|

|

|

|

|

|

Three Months

Ended September 30,

|

|

|

|

2019

|

2018

|

|

CASH FLOWS FROM

OPERATING ACTIVITIES:

|

|

|

|

Net

loss

|

$(4,500,949)

|

$(5,682,056)

|

|

Adjustments

to reconcile net loss to net cash

|

|

|

|

provided

by (used in) operating activities:

|

|

|

|

Depreciation and

amortization

|

18,253

|

14,045

|

|

Non-cash interest

expense

|

438

|

23,581

|

|

Decrease in

right-of-use asset

|

72,113

|

-

|

|

Stock-based

compensation

|

827,735

|

1,233,585

|

|

Changes in

operating assets and liabilities:

|

|

|

|

Accounts

receivable

|

60,168,591

|

(104,189)

|

|

Prepaid expenses

and other assets

|

39,436

|

93,049

|

|

Accounts

payable

|

(446,964)

|

(1,058,542)

|

|

Accrued

expenses

|

(1,269,232)

|

(82,688)

|

|

Operating lease

liability

|

(72,113)

|

-

|

|

Other non-current

liabilities

|

-

|

25,653

|

|

Net cash provided

by (used in) operating activities

|

54,837,308

|

(5,537,562)

|

|

|

|

|

|

CASH FLOWS FROM

INVESTING ACTIVITIES:

|

|

|

|

Purchases of

property and equipment

|

(62,880)

|

-

|

|

Net cash used in

investing activities

|

(62,880)

|

-

|

|

|

|

|

|

CASH FLOWS FROM

FINANCING ACTIVITIES:

|

|

|

|

Payment of

withholding taxes related to restricted

|

|

|

|

stock

units

|

-

|

(65,992)

|

|

Payment on notes

payable obligations

|

(832,851)

|

(2,000,000)

|

|

Warrant

repurchase

|

(1,333,497)

|

-

|

|

Proceeds from the

sale of common stock,

|

|

|

|

net of

costs

|

579,730

|

2,222,447

|

|

Net cash (used in)

provided by financing activities

|

(1,586,618)

|

156,455

|

|

|

|

|

|

NET INCREASE

(DECREASE) IN CASH AND CASH EQUIVALENTS

|

53,187,810

|

(5,381,107)

|

|

|

|

|

|

CASH AND CASH

EQUIVALENTS, beginning of period

|

43,510,422

|

38,000,171

|

|

|

|

|

|

CASH AND CASH

EQUIVALENTS, end of period

|

$96,698,232

|

$32,619,064

|

|

|

|

|

|

SUPPLEMENTAL CASH

FLOW INFORMATION:

|

|

|

|

Cash paid for

interest

|

$8,132

|

$157,636

|

|

Cash paid for

income taxes

|

-

|

-

|

The

accompanying notes are an integral part of these consolidated

financial statements.

4

PALATIN TECHNOLOGIES, INC.

and Subsidiary

Notes to Consolidated Financial Statements

(unaudited)

(1)

ORGANIZATION

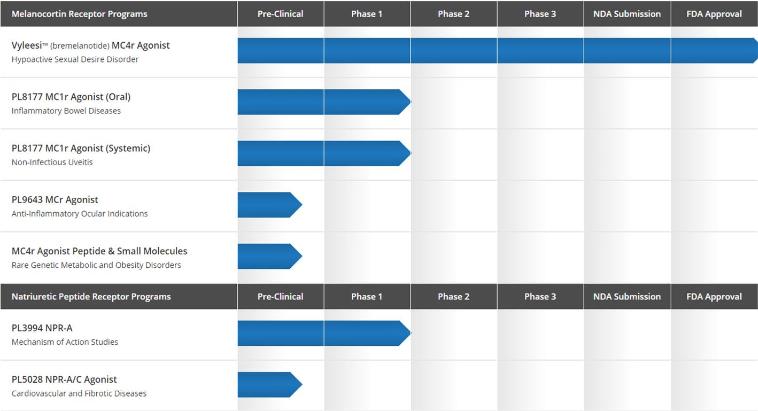

Nature of Business - Palatin Technologies, Inc.

(“Palatin” or the “Company”) is a

specialized biopharmaceutical company developing first-in-class

medicines based on molecules that modulate the activity of the

melanocortin and natriuretic peptide receptor systems. The

Company’s product candidates are targeted, receptor-specific

therapeutics for the treatment of diseases with significant unmet

medical need and commercial potential.

Melanocortin Receptor System. The melanocortin receptor

(“MCr”) system is hormone driven, with effects on food

intake, metabolism, sexual function, inflammation and immune system

responses. There are five melanocortin receptors, MC1r through

MC5r. Modulation of these receptors, through use of

receptor-specific agonists, which activate receptor function, or

receptor-specific antagonists, which block receptor function, can

have significant pharmacological effects.

The

Company’s lead product, Vyleesi™, was approved by the

U.S. Food and Drug Administration (“FDA”) in June 2019

and is being marketed in North America by AMAG Pharmaceuticals,

Inc. (“AMAG”) for the treatment of hypoactive sexual

desire disorder (“HSDD”) in premenopausal

women.

The

Company’s new product development activities focus primarily

on MC1r agonists, with potential to treat inflammatory and

autoimmune diseases such as dry eye disease, which is also known as

keratoconjunctivitis sicca, uveitis, diabetic retinopathy and

inflammatory bowel disease. The Company believes that the MC1r

agonist peptides in development have broad anti-inflammatory

effects and appear to utilize mechanisms engaged by the endogenous

melanocortin system in regulation of the immune system and

resolution of inflammatory responses. The Company is also

developing peptides that are active at more than one melanocortin

receptor, and MC4r peptide and small molecule agonists with

potential utility in obesity and metabolic-related disorders,

including rare disease and orphan indications.

Natriuretic Peptide Receptor System. The natriuretic peptide

receptor (“NPR”) system regulates cardiovascular

functions, and therapeutic agents modulating this system have

potential to treat cardiovascular and fibrotic diseases. The

Company has designed and is developing potential NPR candidate

drugs selective for one or more different natriuretic peptide

receptors, including natriuretic peptide receptor-A

(“NPR-A”), natriuretic peptide receptor B

(“NPR-B”), and natriuretic peptide receptor C

(“NPR-C”).

Business Risk and Liquidity – Since inception, the

Company has incurred negative cash flows from operations, and has

expended, and expects to continue to expend, substantial funds to

complete its planned product development efforts. As shown in the

accompanying consolidated financial statements, the Company had an

accumulated deficit as of September 30, 2019 of $300,273,828 and a

net loss for the three months ended September 30, 2019 of

$4,500,949, and the Company anticipates incurring significant

expenses in the future as a result of spending on its development

programs and will require substantial additional financing or

revenues to continue to fund its planned developmental activities.

To achieve sustained profitability, if ever, the Company, alone or

with others, must successfully develop and commercialize its

technologies and proposed products, conduct successful preclinical

studies and clinical trials, obtain required regulatory approvals

and successfully manufacture and market such technologies and

proposed products. The time required to reach sustained

profitability is highly uncertain, and the Company may never be

able to achieve profitability on a sustained basis, if at

all.

As of

September 30, 2019, the Company’s cash and cash equivalents

were $96,698,232 and current liabilities were $1,850,348.

Management intends to utilize existing capital resources for

general corporate purposes and working capital, including

preclinical and clinical development of the Company’s MC1r

and MC4r peptide programs and natriuretic peptide program, and

development of other portfolio products.

Management

believes that the Company’s existing capital resources will

be adequate to fund the Company’s planned operations through

at least calendar year 2021. The Company will need additional

funding to complete required clinical trials for its other product

candidates and, assuming those clinical trials are successful, as

to which there can be no assurance, to complete submission of

required applications to the FDA. If the Company is unable to

obtain approval or otherwise advance in the FDA approval process,

the Company’s ability to sustain its operations could be

materially adversely affected.

5

PALATIN TECHNOLOGIES, INC.

and Subsidiary

Notes to Consolidated Financial Statements

(unaudited)

The

Company may seek the additional capital necessary to fund its

operations through public or private equity offerings,

collaboration agreements, debt financings or licensing

arrangements. Additional capital that is required by the Company

may not be available on reasonable terms, or at all.

Concentrations – Concentrations in the Company’s

assets and operations subject it to certain related risks.

Financial instruments that subject the Company to concentrations of

credit risk primarily consist of cash and cash equivalents. The

Company’s cash and cash equivalents are primarily invested in

one money market account sponsored by a large financial

institution. For the three months ended September 30, 2019, the

Company reported $97,379 in revenue related to a license agreement

with AMAG for Vyleesi for North America (“AMAG License

Agreement”) (Note 5). For the three months ended September

30, 2018, the Company reported $34,505 in revenue related to the

AMAG License Agreement.

(2)

BASIS

OF PRESENTATION

The

accompanying unaudited consolidated financial statements have been

prepared in accordance with accounting principles generally

accepted in the United States of America (“U.S. GAAP”)

for interim financial information and with the instructions to Form

10-Q. Accordingly, they do not include all of the information and

footnote disclosures required to be presented for complete

financial statements. In the opinion of management, these

consolidated financial statements contain all adjustments

(consisting of normal recurring adjustments) considered necessary

for fair presentation. The results of operations for the three

months ended September 30, 2019 may not necessarily be indicative

of the results of operations expected for the full

year.

The

accompanying unaudited consolidated financial statements should be

read in conjunction with the audited consolidated financial

statements and notes thereto included in the Company’s Annual

Report on Form 10-K for the year ended June 30, 2019, filed with

the Securities and Exchange Commission (“SEC”), which

includes consolidated financial statements as of June 30, 2019 and

2018 and for each of the fiscal years in the three-year period

ended June 30, 2019.

(3)

SUMMARY

OF SIGNIFICANT ACCOUNTING POLICIES

Principles of Consolidation – The consolidated

financial statements include the accounts of Palatin and its

wholly-owned inactive subsidiary. All intercompany accounts and

transactions have been eliminated in consolidation.

Use of Estimates – The preparation of consolidated

financial statements in conformity with U.S. GAAP requires

management to make estimates and assumptions that affect the

reported amounts of assets and liabilities and disclosure of

contingent assets and liabilities at the date of the consolidated

financial statements and the reported amounts of revenues and

expenses during the reporting period. Actual results could differ

from those estimates.

Cash and Cash Equivalents – Cash and cash equivalents

include cash on hand, cash in banks and all highly liquid

investments with a purchased maturity of less than three months.

Cash equivalents consist of $96,520,597 and $43,381,556 in a money

market account at September 30, 2019 and June 30, 2019,

respectively.

Fair Value of Financial Instruments – The

Company’s financial instruments consist primarily of cash

equivalents, accounts receivable and accounts payable. Management

believes that the carrying values of cash equivalents, accounts

receivable and accounts payable are representative of their

respective fair values based on the short-term nature of these

instruments.

Credit Risk – Financial instruments which potentially

subject the Company to concentrations of credit risk consist

principally of cash and cash equivalents. Total cash and cash

equivalent balances have exceeded balances insured by the Federal

Depository Insurance Company (“FDIC”).

Property and Equipment – Property and equipment

consists of office and laboratory equipment, office furniture and

leasehold improvements and includes assets acquired under capital

leases. Property and equipment are recorded at cost. Depreciation

is recognized using the straight-line method over the estimated

useful lives of the related assets, generally five years for

laboratory and computer equipment, seven years for office furniture

and equipment and the lesser of the term of the lease or the useful

life for leasehold improvements. Amortization of assets acquired

under capital leases is included in depreciation expense.

Maintenance and repairs are expensed as incurred while expenditures

that extend the useful life of an asset are capitalized.

Accumulated depreciation and amortization was $2,406,896 and

$2,388,644 as of September 30, 2019 and June 30, 2019,

respectively.

6

PALATIN TECHNOLOGIES, INC.

and Subsidiary

Notes to Consolidated Financial Statements

(unaudited)

Impairment of Long-Lived Assets – The Company reviews

its long-lived assets for impairment whenever events or changes in

circumstances indicate that the carrying amount of the assets may

not be fully recoverable. To determine recoverability of a

long-lived asset, management evaluates whether the estimated future

undiscounted net cash flows from the asset are less than its

carrying amount. If impairment is indicated, the long-lived asset

would be written down to fair value. Fair value is determined by an

evaluation of available price information at which assets could be

bought or sold, including quoted market prices, if available, or

the present value of the estimated future cash flows based on

reasonable and supportable assumptions.

Revenue Recognition – In

May 2014, the Financial Accounting Standards Board

(“FASB”) issued Accounting Standards Update

(“ASU”) No. 2014-09, Revenue from Contracts with

Customers (“ASC Topic

606”), which, along with amendments from 2015 and 2016

requires an entity to recognize the amount of revenue to which it

expects to be entitled for the transfer of promised goods or

services to customers. ASC Topic 606 replaced most existing revenue

recognition guidance in U.S. GAAP when it became

effective.

On July 1, 2018, the Company adopted ASC Topic 606 using the

modified retrospective approach, a practical expedient permitted

under ASC Topic 606, and applied this approach only to contracts

that were not completed as of July 1, 2018.

For

licenses of intellectual property, the Company assesses, at

contract inception, whether the intellectual property is distinct

from other performance obligations identified in the arrangement.

If the licensing of intellectual property is determined to be

distinct, revenue is recognized for nonrefundable, upfront license

fees when the license is transferred to the customer and the

customer can use and benefit from the license. If the licensing of

intellectual property is determined not to be distinct, then the

license will be bundled with other promises in the arrangement into

one performance obligation. The Company needs to determine if the

bundled performance obligation is satisfied over time or at a point

in time. If the Company concludes that the nonrefundable, upfront

license fees will be recognized over time, the Company will need to

assess the appropriate method of measuring proportional

performance.

Regulatory

milestone payments are excluded from the transaction price due to

the inability to estimate the probability of reversal. Revenue

relating to achievement of these milestones is recognized in the

period in which the milestone is achieved.

Sales-based

royalty and milestone payments resulting from customer contracts

solely or predominately for the license of intellectual property

will only be recognized upon occurrence of the underlying sale or

achievement of the sales milestone and such sales-based royalties

and milestone payments are recognized in the same period

earned.

The Company recognizes revenue for reimbursements of research and

development costs under collaboration agreements as the services

are performed. The Company records these reimbursements as revenue

and not as a reduction of research and development expenses as the

Company is the principal in the research and development activities

based upon its control of such activities, which is considered part

of its ordinary activities.

Development milestone payments are generally due 30 business days

after the milestone is achieved. Sales milestone payments are

generally due 45 business days after the calendar year in which the

sales milestone is achieved. Royalty payments are generally due on

a quarterly basis 20 business days after being

invoiced.

Research and Development Costs – The costs of research

and development activities are charged to expense as incurred,

including the cost of equipment for which there is no alternative

future use.

Accrued Expenses – Third parties perform a significant

portion of the Company’s development activities. The Company

reviews the activities performed under all contracts each quarter

and accrues expenses and the amount of any reimbursement to be

received from its collaborators based upon the estimated amount of

work completed. Estimating the value or stage of completion of

certain services requires judgment based on available information.

If the Company does not identify services performed for it but not

billed by the service-provider, or if it underestimates or

overestimates the value of services performed as of a given date,

reported expenses will be understated or overstated.

7

PALATIN TECHNOLOGIES, INC.

and Subsidiary

Notes to Consolidated Financial Statements

(unaudited)

Stock-Based Compensation – The Company charges to

expense the fair value of stock options and other equity awards

granted. Compensation costs for stock-based awards with time-based

vesting are determined using the quoted market price of the

Company’s common stock on the date of grant or for stock

options, the value determined utilizing the Black-Scholes option

pricing model, and are recognized on a straight-line basis, while

awards containing a market condition are valued using multifactor

Monte Carlo simulations. Compensation costs for awards containing a

performance condition are determined using the quoted price of the

Company’s common stock on the date of grant or for stock

options, the value is determined utilizing the Black Scholes option

pricing model, and are recognized based on the probability of

achievement of the performance condition over the service period.

Forfeitures are recognized as they occur.

Income Taxes – The Company and its subsidiary file

consolidated federal and separate-company state income tax returns.

Income taxes are accounted for under the asset and liability

method. Deferred tax assets and liabilities are recognized for the

future tax consequences attributable to differences between the

financial statement carrying amounts of assets and liabilities and

their respective tax basis and operating loss and tax credit

carryforwards. Deferred tax assets and liabilities are measured

using enacted tax rates expected to apply to taxable income in the

years in which those temporary differences or operating loss and

tax credit carryforwards are expected to be recovered or settled.

The effect on deferred tax assets and liabilities of a change in

tax rates is recognized in the period that includes the enactment

date. The Company has recorded and continues to maintain a full

valuation allowance against its deferred tax assets based on the

history of losses incurred and lack of experience projecting future

sales-based royalty and milestone payments.

Net Loss per Common Share - Basic and diluted earnings per

common share (“EPS”) are calculated in accordance with

the provisions of FASB Accounting Standards Codification

(“ASC”) Topic 260, Earnings per Share.

For the

three months ended September 30, 2019 and 2018, no additional

common shares were added to the computation of diluted EPS because

to do so would have been anti-dilutive. The potential number of

common shares excluded from diluted EPS during the three months

ended September 30, 2019 and 2018 was 37,497,717 and 41,454,308

respectively.

Included

in the weighted average common shares used in computing basic and

diluted net loss per common share are 5,978,150 and 3,347,999

vested restricted stock units that had not been issued as of

September 30, 2019 and 2018, respectively, due to a provision in

the restricted stock unit agreements to delay

delivery.

(4)

NEW

AND RECENTLY ADOPTED ACCOUNTING PRONOUNCEMENTS

In November 2018, the FASB issued ASU No. 2018-18,

Collaborative

Arrangements (Topic 808): Clarifying the Interaction between Topic

808 and Topic 606. This

update provides clarification on the interaction between Revenue

Recognition (Topic 606) and Collaborative Arrangements (Topic 808),

including the alignment of unit of account guidance between the two

topics. The

guidance is effective for public entities for fiscal years

beginning after December 15, 2019, and for interim periods within

those fiscal years, with early adoption permitted. The

guidance is applicable to the Company beginning July 1, 2020. The

Company is currently evaluating the potential effects of this

guidance on its consolidated financial

statements.

In June

2016, the FASB issued ASU No. 2016-13, Financial Instruments - Credit Losses:

Measurement of Credit Losses on Financial Instruments, which

requires measurement and recognition of expected credit losses for

financial assets held at the reporting date based on historical

experience, current conditions, and reasonable and supportable

forecasts. This is different from the current guidance as this will

require immediate recognition of estimated credit losses expected

to occur over the remaining life of many financial assets. The new

guidance will be effective for the Company on July 1, 2020. The

Company is currently evaluating the effect that ASU No. 2016-13

will have on its consolidated financial statements and related

disclosures.

8

PALATIN TECHNOLOGIES, INC.

and Subsidiary

Notes to Consolidated Financial Statements

(unaudited)

On July

1, 2019, the Company adopted the requirements of ASU No.2016-02,

Leases (“Topic

842”). The objective of this ASU, along with several related

ASUs issued subsequently, is to increase transparency and

comparability between organizations that enter into lease

agreements. For lessees, the key difference of the new standard

from the previous guidance (“Topic 840”) is the

recognition of a right-of-use (“ROU”) asset and lease

liability on the balance sheet. The most significant change is the

requirement to recognize ROU assets and lease liabilities for

leases classified as operating leases. The standard requires

disclosures to meet the objective of enabling users of financial

statements to assess the amount, timing, and uncertainty of cash

flows arising from leases. As part of the transition to the new

standard, the Company elected to measure and recognize leases that

existed at July 1, 2019 using a modified retrospective approach,

including the option to not restate comparative periods. For leases

existing at the effective date, the Company elected the package of

three transition practical expedients and therefore did not

reassess whether an arrangement is or contains a lease, did not

reassess lease classification, and did not reassess what qualifies

as an initial direct cost. Additionally, the Company elected, as

practical expedients, not separating lease and non-lease components

for all of its leases and the short-term lease recognition

exemption for all of its leases that qualify. The Company did not

elect the use of the hindsight practical expedient. The adoption of

Topic 842 resulted in the recognition of an operating ROU asset and

operating lease liability of $225,134 as of July 1, 2019. The

adoption did not have a material impact on the consolidated

statements of operations, stockholder’s equity and cash flows

for the three months ended September 30, 2019.

At

lease inception, the Company determines whether an arrangement is

or contains a lease. Operating leases are included in operating

lease ROU assets, current operating lease liabilities, and

noncurrent operating lease liabilities in the consolidated

financial statements. ROU assets represent the Company’s

right to use leased assets over the term of the lease. Lease

liabilities represent the Company’s contractual obligation to

make lease payments over the lease term. For operating leases, ROU

assets and lease liabilities are recognized at the commencement

date. The lease liability is measured as the present value of the

lease payments over the lease term. The Company uses the rate

implicit in the lease if it is determinable. When the rate implicit

in the lease is not determinable, the Company uses an estimate

based on a hypothetical rate provided by a third party as the

Company currently does not have issued debt. Operating ROU assets

are calculated as the present value of the remaining lease payments

plus unamortized initial direct costs plus any prepayments less any

unamortized lease incentives received. Lease terms may include

renewal or extension options to the extent they are reasonably

certain to be exercised. The assessment of whether renewal or

extension options are reasonably certain to be exercised is made at

lease commencement. Factors considered in determining whether an

option is reasonably certain of exercise include, but are not

limited to, the value of any leasehold improvements, the value of

renewal rates compared to market rates, and the presence of factors

that would cause incremental costs to the Company if the option

were not exercised. Lease expense is recognized on a straight-line

basis over the lease term. The Company has elected not to recognize

an ROU asset and obligation for leases with an initial term of

twelve months or less. The expense associated with short term

leases is included in general and administrative expense in the

statement of operations. To the extent a lease arrangement includes

both lease and non-lease components, the Company has elected to

account for the components as a single lease

component.

(5)

AGREEMENT

WITH AMAG

On

January 8, 2017, the Company entered into the AMAG License

Agreement. Under the terms of the AMAG License Agreement, the

Company granted to AMAG (i) an exclusive license in all countries

of North America (the “Territory”), with the right to

grant sub-licenses, to research, develop and commercialize products

containing Vyleesi (each a “Product”, and collectively,

“Products”), (ii) a non-exclusive license in the

Territory, with the right to grant sub-licenses, to manufacture the

Products, and (iii) a non-exclusive license in all countries

outside the Territory, with the right to grant sub-licenses, to

research, develop and manufacture (but not commercialize) the

Products.

Following

the satisfaction of certain conditions to closing, the license

agreement became effective on February 2, 2017. On that date, AMAG

paid the Company $60,000,000 as a one-time initial payment.

Pursuant to the terms of and subject to the conditions in the AMAG

License Agreement, AMAG was required to reimburse the Company up to

an aggregate amount of $25,000,000 for reasonable, documented,

direct out-of-pocket expenses incurred by the Company following

February 2, 2017, in connection with the development and regulatory

activities necessary to file a New Drug Application

(“NDA”) for Vyleesi for HSDD in the United States

related to Palatin’s development obligations.

The

Company determined there was no stand-alone value for the license,

and that the license and the reimbursable direct out-of-pocket

expenses, pursuant to the terms of the License Agreement,

represented a combined unit of accounting which totaled

$85,000,000. The Company recognized revenue of the combined unit of

accounting over the arrangement using the input-based proportional

method as the Company completed its development obligations. During

the three months ended September 30, 2019 and 2018, license and

contract revenue included additional billings for AMAG related

Vyleesi costs of $97,379 and $34,505.

9

PALATIN TECHNOLOGIES, INC.

and Subsidiary

Notes to Consolidated Financial Statements

(unaudited)

On June

4, 2018, the FDA accepted the Vyleesi NDA for filing. The

FDA’s acceptance triggered a $20,000,000 milestone payment to

Palatin from AMAG. As a result, the Company recognized $20,000,000

in revenue related to regulatory milestones in fiscal 2018. On June

21, 2019, the FDA granted approval of Vyleesi for use in the United

States. The FDA’s approval triggered a $60,000,000 milestone

payment to Palatin from AMAG. As a result, the Company recognized

$60,000,000 in revenue related to regulatory milestones in fiscal

2019. In addition, pursuant to the terms of and subject to the

conditions in the AMAG License Agreement, the Company is eligible

to receive from AMAG up to $300,000,000 in sales milestone payments

based on achievement of certain annual net sales for all Products

in the Territory.

AMAG is

also obligated to pay the Company tiered royalties on annual net

sales of Products, on a product-by-product basis, in the Territory

ranging from the high single-digits to the low double-digits. The

royalties will expire on a product-by-product and

country-by-country basis upon the latest to occur of (i) the

earliest date on which there are no valid claims of the

Company’s patent rights covering such Product in such

country, (ii) the expiration of the regulatory exclusivity period

for such Product in such country and (iii) ten years following the

first commercial sale of such Product in such country. Such

royalties are subject to reductions in the event that:

(a) AMAG must license additional third-party intellectual

property in order to develop, manufacture or commercialize a

Product, or (b) generic competition occurs with respect to a

Product in a given country, subject to an aggregate cap on such

deductions of royalties otherwise payable to the Company. After the

expiration of the applicable royalties for any Product in a given

country, the license for such Product in such country will become a

fully paid-up, royalty-free, perpetual and irrevocable

license.

The

Company engaged Greenhill & Co. LLC (“Greenhill”)

as the Company’s sole financial advisor in connection with a

potential transaction with respect to Vyleesi. Under the

engagement agreement with Greenhill, the Company is obligated to

pay Greenhill a fee equal to 2% of all proceeds and consideration,

as defined, paid or to be paid to the Company by AMAG in connection

with the AMAG License Agreement, subject to a minimum fee of

$2,500,000. The minimum fee of $2,500,000, less a credit of $50,000

for an advisory fee previously paid by the Company, was paid to

Greenhill and recorded as an expense upon the closing of the

licensing transaction. This amount is credited toward amounts that

were and will become due to Greenhill in the future, provided that

the aggregate fee payable to Greenhill will not be less than 2% of

all proceeds and consideration, as defined, paid or to be paid to

the Company by AMAG in connection with the AMAG License Agreement.

The Company will generally pay Greenhill 2% of all future proceeds

and consideration paid to the Company by AMAG in connection with

the AMAG License Agreement, including milestone and royalty

payments. The Company also reimbursed Greenhill $7,263 for certain

expenses incurred in connection with its advisory

services.

Pursuant

to the AMAG License Agreement, the Company has assigned to AMAG the

Company’s manufacturing and supply agreements with Catalent

Belgium S.A. to perform fill, finish and packaging of

Vyleesi.

(6)

AGREEMENT

WITH FOSUN:

On

September 6, 2017, the Company entered into a license agreement

with Fosun (“Fosun License Agreement”) for exclusive

rights to commercialize Vyleesi in China. Under the terms of the

agreement, the Company received $4,500,000 in October 2017, which

consisted of an upfront payment of $5,000,000 less $500,000 that

was withheld in accordance with tax withholding requirements in the

Chinese Territories and recorded as an expense during the year

ended June 30, 2018. The Company will receive a $7,500,000

milestone payment when regulatory approval in China is obtained,

provided that a commercial supply agreement for Vyleesi has been

entered into. Palatin has the potential to receive up to

$92,500,000 in additional sales related milestone payments and high

single-digit to low double-digit royalties on net sales in the

licensed territory. All development, regulatory, sales, marketing,

and commercial activities and associated costs in the licensed

territory will be the sole responsibility of Fosun.

(7)

AGREEMENT

WITH KWANGDONG:

On

November 21, 2017, the Company entered into a license agreement with Kwangdong

(“Kwangdong License Agreement”) for exclusive

rights to commercialize Vyleesi in Korea.

10

PALATIN TECHNOLOGIES, INC.

and Subsidiary

Notes to Consolidated Financial Statements

(unaudited)

Under

the terms of the agreement, the Company received $417,500 in

December 2017, consisting of an upfront payment of $500,000, less

$82,500, which was withheld in accordance with tax withholding

requirements in Korea and recorded as an expense during the year

ended June 30, 2018. Based upon certain refund provisions, the

upfront payment was recorded as non-current deferred revenue at

December 31, 2017. On July 1, 2018, in

conjunction with the adoption of ASC Topic 606, a one-time

transition of adjustment of $500,000 was recorded to the opening

balance of accumulated deficit as the Company determined a

significant revenue reversal would not occur in a future

period. The Company will receive a $3,000,000 milestone

payment based on the first commercial sale in Korea. Palatin has

the potential to receive up to $37,500,000 in additional sales

related milestone payments and mid-single-digit to low double-digit

royalties on net sales in the licensed territory. All development,

regulatory, sales, marketing, and commercial activities and

associated costs in the licensed territory will be the sole

responsibility of Kwangdong.

(8)

PREPAID

EXPENSES AND OTHER CURRENT ASSETS

Prepaid

expenses and other

current assets consist of the following:

|

|

September

30,

|

June

30,

|

|

|

2019

|

2019

|

|

Clinical study

costs

|

$49,079

|

$61,798

|

|

Insurance

premiums

|

77,856

|

87,937

|

|

Other

|

470,918

|

487,554

|

|

|

$597,853

|

$637,289

|

(9)

FAIR

VALUE MEASUREMENTS

The

fair value of cash equivalents is classified using a hierarchy

prioritized based on inputs. Level 1 inputs are quoted prices

(unadjusted) in active markets for identical assets or liabilities.

Level 2 inputs are quoted prices for similar assets and liabilities

in active markets or inputs that are observable for the asset or

liability, either directly or indirectly through market

corroboration, for substantially the full term of the financial

instrument. Level 3 inputs are unobservable inputs based on

management’s own assumptions used to measure assets and

liabilities at fair value. A financial asset’s or

liability’s classification within the hierarchy is determined

based on the lowest level input that is significant to the fair

value measurement.

The

following table provides the assets carried at fair

value:

|

|

Carrying

Value

|

Quoted prices in

active markets

(Level

1)

|

Other

quoted/observable inputs

(Level

2)

|

Significant

unobservable inputs

(Level

3)

|

|

September 30,

2019:

|

|

|

|

|

|

Money Market

Account

|

$96,520,597

|

$96,520,597

|

$-

|

$-

|

|

June 30,

2019:

|

|

|

|

|

|

Money Market

Account

|

$43,381,556

|

$43,831,556

|

$-

|

$-

|

(10)

LEASES

The

Company has operating leases of office and laboratory space, each

of which expires on June 30, 2020.

11

PALATIN TECHNOLOGIES, INC.

and Subsidiary

Notes to Consolidated Financial Statements

(unaudited)

The

components of lease expense are as follows:

|

Lease

cost

|

Three months

ended

September 30,

2019

|

|

Operating lease

cost

|

$72,113

|

|

Short-term lease

cost

|

8,520

|

|

Total lease

cost

|

$80,633

|

Supplemental

balance sheet information related to leases was as

follows:

|

|

September

30, 2019

|

|

Operating lease ROU

asset and liability

|

$213,065

|

Supplemental

lease term and discount rate information related to leases was as

follows:

|

Weighted -average

remaining lease term (years)

|

0.75

|

|

Weighted -average

discount rate

|

6.25%

|

Supplemental

cash flow information related to leases was as

follows:

|

|

Three months

ended

September 30,

2019

|

|

Cash paid for the

amounts included in the measurement of lease

liabilities:

|

|

|

Operating

cash flows for operating leases

|

$71,838

|

|

Supplemental

non-cash information on lease liabilities arisng from obtaining

right-of-use assets

|

|

|

Right-of-use

assets obtained in exchange for new lease obligation

|

$56,715

|

The

following table summarizes the maturity of the Company’s

operating lease liability as of September 30, 2019:

|

|

September

30,

2019

|

|

Year Ending June

30, 2020

|

$217,519

|

|

Less imputed

interest

|

(4,454)

|

|

Total

|

$213,065

|

As of

June 30, 2019, the Company had $225,120 in future lease payments

for the year ending June 30, 2020 under ASC Topic 840.

12

PALATIN TECHNOLOGIES, INC.

and Subsidiary

Notes to Consolidated Financial Statements

(unaudited)

(11)

ACCRUED

EXPENSES

Accrued

expenses consist of the

following:

|

|

September

30,

|

June

30,

|

|

|

2019

|

2019

|

|

Clinical study

costs

|

$171,878

|

$943,721

|

|

Other research

related expenses

|

1,114,475

|

1,361,414

|

|

Professional

services

|

89,138

|

317,500

|

|

Other

|

203,969

|

226,057

|

|

|

$1,579,460

|

$2,848,692

|

(12)

NOTES PAYABLE:

Notes

payable consist of the following:

|

|

June

30,

|

|

|

2019

|

|

Notes payable under

venture loan

|

$333,333

|

|

Unamortized related

debt discount

|

(295)

|

|

Unamortized debt

issuance costs

|

(142)

|

|

Notes

payable

|

332,896

|

|

|

|

|

Less: current

portion

|

332,896

|

|

|

|

|

Long-term

portion

|

$-

|

On

December 23, 2014, the Company closed on a $10,000,000 venture loan

which was led by Horizon Technology Finance Corporation

(“Horizon”). The debt facility was a four-year senior

secured term loan that bore interest at a floating coupon rate of

one-month LIBOR (floor of 0.50%) plus 8.50%, and provided for

interest-only payments for the first eighteen months followed by

monthly payments of principal of $333,333 plus accrued interest

through January 1, 2019. The lenders also received five-year

immediately exercisable Series D 2014 warrants to purchase 666,666

shares of common stock exercisable at an exercise price of $0.75

per share. The Company recorded a debt discount of $267,820 equal

to the fair value of these warrants at issuance, which was

amortized to interest expense over the term of the related debt.

This debt discount was offset against the note payable balance and

included in additional paid-in capital on the Company’s

balance sheet. In addition, a final incremental payment of $500,000

was due on January 1, 2019, or upon early repayment of the loan.

This final incremental payment was accreted to interest expense

over the term of the related debt and included in other liabilities

on the consolidated balance sheet. The Company incurred $209,367 of

costs in connection with the loan. These costs were capitalized as

deferred financing costs and were offset against the note payable

balance. These debt issuance costs were amortized to interest

expense over the term of the related debt. During the three months

ended December 31, 2018, the loan matured, and on December 31,

2018, the Company made the final incremental payment of

$500,000.

On July

2, 2015, the Company closed on a $10,000,000 venture loan led by

Horizon. The debt facility was a four-year senior secured term loan

that bore interest at a floating coupon rate of one-month LIBOR

(floor of 0.50%) plus 8.50% and provided for interest-only payments

for the first eighteen months followed by monthly payments of

principal of $333,333 plus accrued interest through August 1, 2019.

The lenders also received five-year immediately exercisable Series

G warrants to purchase 549,450 shares of the Company’s common

stock exercisable at an exercise price of $0.91 per share. The

Company recorded a debt discount of $305,196 equal to the fair

value of these warrants at issuance, which were amortized to

interest expense over the term of the related debt. This debt

discount was offset against the note payable balance and was

included in additional paid-in capital on the Company’s

balance sheet. In addition, a final incremental payment of $500,000

was due on August 1, 2019. This final incremental payment was

accreted to interest expense over the term of the related debt and

was included in other current liabilities on the consolidated

balance sheet. The Company incurred $146,115 of costs in connection

with the loan agreement. These costs were capitalized as deferred

financing costs and were offset against the note payable balance.

These debt issuance costs were amortized to interest expense over

the term of the related debt. During the three months ended

September 30, 2019, the loan matured, and on July 31, 2019, the

Company made the final incremental payment of

$500,000.

13

PALATIN TECHNOLOGIES, INC.

and Subsidiary

Notes to Consolidated Financial Statements

(unaudited)

(13)

STOCKHOLDERS’

EQUITY

Financing Transactions – On June 21, 2019 and April 20, 2018, the Company

entered into equity distribution agreements with Canaccord Genuity

LLC (“Canaccord”) (the “2019 Equity Distribution

Agreement” and the “2018 Equity Distribution

Agreement”, respectively), pursuant to which the Company may,

from time to time, sell shares of the Company’s common

stock at market prices by

methods deemed to be an “at-the-market offering” as

defined in Rule 415 promulgated under the Securities Act of 1933,

as amended. The 2018 Equity Distribution Agreement and related

prospectus was limited to sales of up to an aggregate maximum $25.0

million of shares of the Company’s common stock, and the 2019

Equity Distribution Agreement and related prospectus is limited to

sales of up to an aggregate maximum $40.0 million of shares of the

Company’s common stock. The Company pays Canaccord 3.0% of

the gross proceeds as a commission.

For the three months ended September 30, 2019, 657,894 shares of

common stock were sold through Canaccord under the 2019 Equity

Distribution Agreement for net proceeds of $579,730 after payment

of commission fees of $19,940 and other related expenses of

$65,000. From inception of the 2019 Equity Distribution Agreement

through September 30, 2019, a total of 8,222,469 shares of common

Stock were sold for net proceeds of $10,868,566 after payment of

commission fees of $338,152 and other related expenses of $65,000.

For the three months ended September 30, 2018, 2,225,145 shares of

common stock were sold through Canaccord under the 2018 Equity

Distribution Agreement for net proceeds of $2,222,447 after payment

of commission fees of $68,735. From inception of the 2018 Equity

Distribution Agreement through September 30, 2019, a total of

18,504,993 shares of common Stock were sold for net proceeds of

$24,249,997 after payment of commission fees of $750,000, and the

2018 Equity Distribution Agreement is deemed

completed.

Stock Purchase Warrants – On September 13, 2019, the

Company’s Board of Directors approved a plan to offer to

purchase and terminate certain outstanding common stock purchase

warrants through privately negotiated transactions. The purchase

and termination program has no time limit and may be suspended for

periods or discontinued at any time.

During

the three months ended September 30, 2019, the Company entered into

several warrant termination agreements to repurchase and cancel

previously issued Series H and Series J warrants. The Company

repurchased and cancelled 474,045 and 2,866,809 Series H and Series

J warrants, respectively, at an aggregate buyback price of $186,773

and $1,146,724, respectively, plus additional consideration upon

any sale of the Company within six months of the respective

agreement.

Stock Options – For the three months ended September

30, 2019 and 2018, the Company recorded stock-based compensation

related to stock options of $344,160 and $323,703,

respectively.

In July

2018, the terms of certain options were modified to accelerate

vesting and extend the option exercise period. As a result, the

Company recorded additional stock-based compensation of $109,004

during the three months ended September 30, 2018.

14

PALATIN TECHNOLOGIES, INC.

and Subsidiary

Notes to Consolidated Financial Statements

(unaudited)

A

summary of stock option activity is as follows:

|

|

Number of

Shares

|

Weighted

Average

Exercise

Price

|

Weighted Average

Remaining

Term in

Years

|

Aggregate

Intrinsic

Value

|

|

Outstanding - June

30, 2019

|

14,435,650

|

0.85

|

7.3

|

|

|

|

|

|

|

|

|

Granted

|

-

|

-

|

|

|

|

Forfeited

|

-

|

-

|

|

|

|

Exercised

|

-

|

-

|

|

|

|

Expired

|

(77,100)

|

2.72

|

|

|

|

Outstanding -

September 30, 2019

|

14,358,550

|

$0.84

|

7.1

|

$2,402,286

|

|

|

|

|

|

|

|

Exercisable at

September 30, 2019

|

8,461,000

|

$0.76

|

5.9

|

$1,627,979

|

|

|

|

|

|

|

|

Expected to vest at

September 30, 2019

|

5,897,550

|

$0.96

|

8.7

|

$774,907

|

Stock

options granted to the Company’s executive officers and

employees generally vest over a 48-month period, while stock

options granted to its non-employee directors vest over a 12-month

period.

Included

in the options outstanding above are 1,075,000 and 117,500

performance-based options granted in December 2017 to executive

officers and employees, respectively, which vest during a

performance period ending on December 31, 2020, if and upon either

i) as to 100% of the target number of shares upon achievement of a

closing price for the Company’s common stock equal to or

greater than $1.50 per share for 20 consecutive trading days, which

is considered a market condition; or ii) as to thirty percent (30%)

of the target number of shares, upon the acceptance for filing by

the FDA of an NDA for Vyleesi for HSDD in premenopausal women

during the performance period, which is considered a performance

condition; iii) as to fifty percent (50%) of the target number of

shares, upon the approval by the FDA of an NDA for Vyleesi for HSDD

in premenopausal women during the performance period, which is also

considered a performance condition; iv) as to twenty percent (20%)

of the target number of shares, upon entry into a licensing

agreement during the performance period for the commercialization

of Vyleesi for FSD in at least two of the following geographic

areas (a) four or more countries in Europe, (b) Japan, (c) two or

more countries in Central and/or South America, (d) two or more

countries in Asia, excluding Japan and China, and (e) Australia,

which is also considered a performance condition. The fair value of

these options was $602,760. The Company amortized the fair value

over the derived service period of 1.1 years or upon the attainment

of the performance condition. Pursuant to the FDA acceptance of the

NDA filing of Vyleesi, 30% of the target number of options vested

in June 2018 and 50% of the target number of options vested in June

2019 upon FDA approval of Vyleesi.

Restricted Stock Units – For the three months ended

September 30, 2019 and 2018, the Company recorded stock-based

compensation related to restricted stock units of $483,575 and

$800,878, respectively.

A

summary of restricted stock unit activity is as

follows:

|

|

RSU's

|

|

Outstanding at July

1, 2019

|

10,327,833

|

|

Granted

|

-

|

|

Forfeited

|

-

|

|

Vested

|

(224,000)

|

|

Outstanding at

September 30, 2019

|

10,103,833

|

15

PALATIN TECHNOLOGIES, INC.

and Subsidiary

Notes to Consolidated Financial Statements

(unaudited)

Included

in outstanding restricted stock units in the table above are

5,978,150 vested shares that have not been issued as of September

30, 2019 due to a provision in the restricted stock unit agreements

to delay delivery.

Time-based

restricted stock units granted to the Company’s executive

officers, employees and non-employee directors generally vest over

24 months, 48 months and 12 months, respectively.

In June

2019, the Company granted 438,000 performance-based restricted

stock units to its executive officers and 182,725 performance-based

restricted stock units to other employees which vest during a

performance period ending June 24, 2023. The performance-based

restricted stock units vest on performance criteria relating to

advancement of MC1r programs, including initiation of clinical

trials and licensing of Vyleesi in additional countries or

regions.

In

December 2017, the Company granted 1,075,000 performance-based

restricted stock units to its executive officers and 670,000

performance-based restricted stock units to other employees which

vest during a performance period, ending on December 31, 2020, if

and upon either i) as to 100% of the target number of shares upon

achievement of a closing price for the Company’s common stock

equal to or greater than $1.50 per share for 20 consecutive trading

days, which is considered a market condition; or ii) as to thirty

percent (30%) of the target number of shares, upon the acceptance

for filing by the FDA of an NDA for Vyleesi for HSDD in