UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

10 - K

☑

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

For the

fiscal year ended June 30, 2016

or

☐

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

For the

transition period from ___________ to __________

Commission file

number: 001-15543

PALATIN TECHNOLOGIES, INC.

(Exact

name of registrant as specified in its charter)

|

Delaware

|

|

95-4078884

|

|

(State

or other jurisdiction of incorporation or

organization)

|

|

(I.R.S.

Employer Identification No.)

|

|

4B Cedar Brook Drive

Cranbury, New Jersey

|

|

08512

|

|

(Address

of principal executive offices)

|

|

(Zip

Code)

|

(609)

495-2200

(Registrant’s

telephone number, including area code)

Securities

registered pursuant to Section 12(b) of the Act:

|

Title of Each Class

|

|

Name of Each Exchange on

Which Registered

|

|

Common

Stock, par value $.01 per share

|

|

NYSE

MKT

|

Securities

registered pursuant to Section 12(g) of the Act: None

Indicate by check

mark if the registrant is a well-known seasoned issuer, as defined

in Rule 405 of the Securities Act. Yes ☐ No

☑

Indicate by check

mark if the registrant is not required to file reports pursuant to

Section 13 or Section 15(d) of the Act. Yes ☐ No

☑

Indicate by check

mark whether the registrant (1) has filed all reports required to

be filed by Section 13 or 15(d) of the Securities Exchange Act of

1934 during the preceding 12 months (or for such shorter period

that the registrant was required to file such reports), and (2) has

been subject to such filing requirements for the past 90

days. Yes ☑ No

☐

Indicate by check

mark whether the registrant has submitted electronically and posted

on its corporate Web site, if any, every Interactive Data File

required to be submitted and posted pursuant to Rule 405 of

Regulation S-T during the preceding 12 months (or for such shorter

period that the registrant was required to submit and post such

files). Yes

☑ No ☐

Indicate by check

mark if disclosure of delinquent filers pursuant to Item 405 of

Regulation S-K is not contained herein, and will not be contained,

to the best of the registrant’s knowledge, in definitive

proxy or information statements incorporated by reference in Part

III of this Form 10-K or any amendment to this Form 10-K.

☐

Indicate by check

mark whether the registrant is a large accelerated filer, an

accelerated filer, a non-accelerated filer, or a smaller reporting

company. See the definitions of “large accelerated

filer,” “accelerated filer” and “smaller

reporting company” in Rule 12b-2 of the Exchange Act. (Check

one):

| Large accelerated filer | ☐ | Accelerated filer | ☐ |

| Non-accelerated filer | ☐ | Smaller reporting company | ☑ |

| (Do not check if a smaller reporting company) |

|

|

|

Indicate by check

mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Exchange Act). Yes ☐ No ☑

State

the aggregate market value of the voting and non-voting common

equity held by non-affiliates, computed by reference to the price

at which the common equity was last sold, or the average bid and

asked price of such common equity, as of the last business day of

the registrant’s most recently completed second fiscal

quarter (December 31, 2015): $44,069,665.

Indicate the number

of shares outstanding of each of the registrant’s classes of

common stock, as of the latest practicable date (September 16,

2016): 85,934,037.

PALATIN TECHNOLOGIES, INC.

Table

of Contents

|

|

Page

|

|

|

PART

I

|

||

|

Item

1.

|

Business

|

1

|

|

|

|

|

|

Item

1A.

|

Risk

Factors

|

18

|

|

|

|

|

|

Item

1B.

|

Unresolved Staff

Comments

|

38

|

|

|

|

|

|

Item

2.

|

Properties

|

38

|

|

|

|

|

|

Item

3.

|

Legal

Proceedings

|

38

|

|

|

|

|

|

Item

4.

|

Mine

Safety Disclosures

|

38

|

|

|

|

|

|

PART

II

|

||

|

|

|

|

|

Item

5.

|

Market

for Registrant’s Common Equity, Related Stockholder Matters

and Issuer Purchases of Equity Securities

|

39

|

|

|

|

|

|

Item

6.

|

Selected Financial

Data

|

39

|

|

|

|

|

|

Item

7.

|

Management’s

Discussion and Analysis of Financial Condition and Results of

Operations

|

39

|

|

|

|

|

|

Item

7A.

|

Quantitative and

Qualitative Disclosures About Market Risk

|

43

|

|

|

|

|

|

Item

8.

|

Financial

Statements and Supplementary Data

|

44

|

|

|

|

|

|

Item

9.

|

Changes

in and Disagreements with Accountants on Accounting and Financial

Disclosure

|

67

|

|

|

|

|

|

Item

9A.

|

Controls and

Procedures

|

67

|

|

|

|

|

|

Item

9B.

|

Other

Information

|

67

|

|

|

||

|

PART

III

|

||

|

|

||

|

Item

10.

|

Directors,

Executive Officers and Corporate Governance

|

68

|

|

|

|

|

|

Item

11.

|

Executive

Compensation

|

72

|

|

|

|

|

|

Item

12.

|

Security Ownership

of Certain Beneficial Owners and Management and Related Stockholder

Matters

|

78

|

|

|

|

|

|

Item

13.

|

Certain

Relationships and Related Transactions, and Director

Independence

|

81

|

|

|

|

|

|

Item

14.

|

Principal

Accountant Fees and Services

|

81

|

|

|

||

|

PART

IV

|

||

|

|

||

|

Item

15.

|

Exhibits, Financial

Statement Schedules

|

82

|

Forward-Looking

Statements

Statements in this

Annual Report on Form 10-K (this Annual Report), as well as oral

statements that may be made by us or by our officers, directors, or

employees acting on our behalf, that are not historical facts

constitute “forward-looking statements,” which are made

pursuant to the safe harbor provisions of Section 21E of the

Securities Exchange Act of 1934, or the Exchange Act. The

forward-looking statements in this Annual Report do not constitute

guarantees of future performance. Investors are cautioned that

statements that are not strictly historical facts contained in this

Annual Report, including, without limitation, those relating to our

current or future financial performance, management’s plans

and objectives for future operations, ability to raise capital or

repay debt, if required, clinical trials and results, uncertainties

associated with product research and development, product plans and

performance, management’s assessment of market factors, as

well as statements regarding our strategy and plans and those of

our strategic partners, constitute forward-looking statements. In

some cases, you can identify forward-looking statements by

terminology such as “believe,” will,”

“may,” “estimate,” “continue,”

“anticipated,” “intend,”

“should,” “plan,” “expect,”

“predict,” “could,”

“potentially,” or the negative of these terms or other

similar expressions. Such forward-looking statements involve

substantial risks, uncertainties and other factors that could cause

our actual results to be materially different from our historical

results or from any results expressed or implied by such

forward-looking statements. Our future operating results are

subject to risks and uncertainties and are dependent upon many

factors, including, without limitation, the risks identified under

the caption “Risk Factors” and elsewhere in this Annual

Report, and any of those made in our other reports filed with the

Securities and Exchange Commission, or the SEC. Except as required

by law, we do not intend, and undertake no obligation, to publicly

update forward-looking statements to reflect events or

circumstances after the date of this document or to reflect the

occurrence of unanticipated events.

In this

Annual Report, references to “we,” “our,”

“us,” the “Company” or

“Palatin” means Palatin Technologies, Inc. and its

subsidiary.

PART

I

Item

1. Business.

Overview

We are

a biopharmaceutical company developing targeted, receptor-specific

peptide therapeutics for the treatment of diseases with significant

unmet medical need and commercial potential. Our programs are based

on molecules that modulate the activity of the melanocortin and

natriuretic peptide receptor systems. Our primary product in

clinical development is bremelanotide for the treatment of

premenopausal women with hypoactive sexual desire disorder, or

HSDD, which is a type of female sexual dysfunction, or FSD, defined

as low desire with associated distress. In addition, we have drug

candidates or development programs for obesity, erectile

dysfunction, cardiovascular diseases, pulmonary diseases,

inflammatory diseases and dermatologic diseases.

The

following drug development programs are actively under

development:

●

Bremelanotide, an

as needed subcutaneous injectable peptide melanocortin receptor

agonist, for treatment of HSDD in premenopausal women.

Bremelanotide, which is a melanocortin agonist, is a synthetic

peptide analog of the naturally occurring hormone alpha-MSH

(melanocyte-stimulating hormone). The novel mechanism of action

involves activating endogenous melanocortin hormone pathways

involved in sexual response. Bremelanotide has completed the

efficacy portion of patient studies in the primary Phase 3 clinical

studies;

●

Melanocortin

receptor-4, or MC4r, compounds for treatment of obesity and

diabetes. Results of our studies involving MC4r peptides suggest

that certain of these peptides may have significant commercial

potential for treatment of conditions responsive to MC4r

activation, including FSD, HSDD, erectile dysfunction or ED,

obesity and diabetes;

●

PL-3994, a

natriuretic peptide receptor-A, or NPR-A, agonist, for treatment of

cardiovascular and pulmonary indications. PL-3994 is our lead

natriuretic peptide receptor product candidate, and is a synthetic

mimetic of the neuropeptide hormone atrial natriuretic peptide, or

ANP. PL-3994 is in development for treatment of heart failure,

acute exacerbations of asthma and refractory hypertension;

and

●

Melanocortin

receptor-1, or MC1r, agonist peptides for treatment of inflammatory

and dermatologic disease indications. Our MC1r peptide drug

candidates are highly specific, with substantially greater binding

and efficacy at MC1r than at other melanocortin receptors. We have

selected one of our MC1r peptide drug candidates, designated

PL-8177, as a clinical trial candidate.

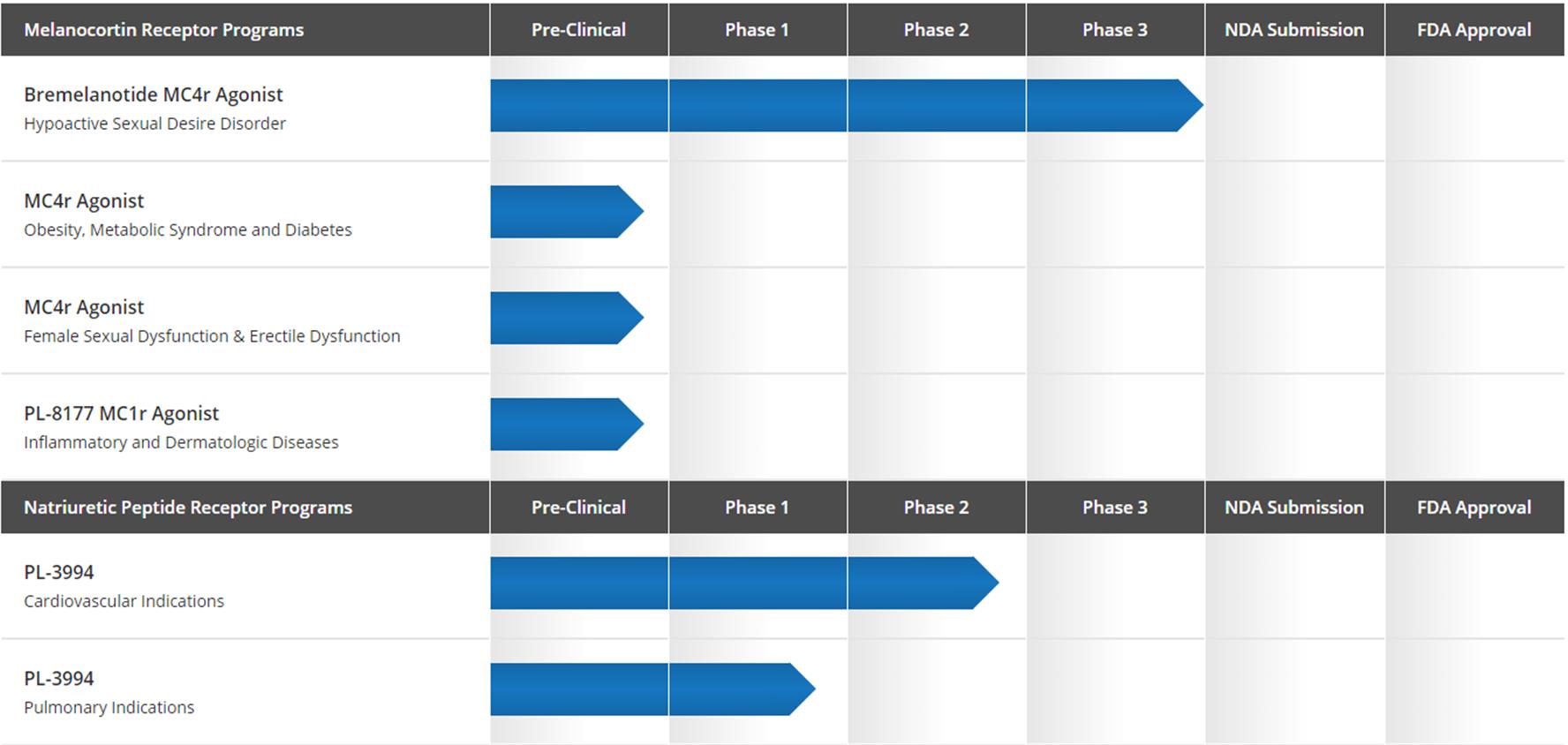

The

following chart illustrates the status of our drug development

programs.

1

Our

Strategy

Key

elements of our business strategy include:

●

Using our

technology and expertise to develop and commercialize products in

our active drug development programs;

●

Entering into

strategic alliances and partnerships with pharmaceutical companies

to facilitate the development, manufacture, marketing, sale and

distribution of product candidates that we are

developing;

●

Partially funding

our product development programs with the cash flow generated from

research collaboration and license agreements and any potential

future agreements with third parties; and

●

Completing

development and seeking regulatory approval of bremelanotide for

HSDD and our other product candidates.

Our

Melanocortin Receptor-Specific Programs

The

melanocortin system is involved in a large and diverse number of

physiologic functions. Therapeutic agents modulating this system

may have the potential to treat a variety of conditions and

diseases, including sexual dysfunction, obesity and related

disorders, pigmentation disorders and inflammation-related

diseases.

Bremelanotide for HSDD. We are

developing subcutaneously administered bremelanotide for the

treatment of HSDD in premenopausal women. HSDD is characterized by

a decrease in sexual desire with significant personal distress or

interpersonal difficulty as a result of the lack of desire.

Bremelanotide is a melanocortin agonist with a mechanism of action

involving activation of endogenous neuronal pathways regulating

sexual arousal and desire responses.

We

initiated patient screening in our Phase 3 clinical study program

of bremelanotide for the treatment of HSDD in premenopausal women,

called the RECONNECT STUDY, in the fourth quarter of calendar 2014,

completed patient enrollment in the fourth quarter of calendar

2015, and completed the last patient visits in the double blind, or

efficacy, portion of the studies in the third quarter of calendar

2016. Topline results are projected early fourth quarter of

calendar 2016. The open-label safety extension portion of the

RECONNECT STUDY is continuing. We cannot assure you that the Phase

3 efficacy data will support approval of bremelanotide for HSDD or

that the U.S. Food and Drug Administration, or FDA, will approve a

new drug application, or NDA, for bremelanotide.

Phase 3 Clinical Program. Prior to

initiating our Phase 3 RECONNECT STUDY clinical program, we reached

preliminary agreement with the FDA on key aspects of the

bremelanotide efficacy Phase 3 pivotal registration studies,

including HSDD patient population, primary and key secondary

efficacy endpoints, general study design, dose selection and safety

monitoring. In addition, the FDA agreed that the Phase 2 data

adequately characterized blood pressure and heart rate signals of

bremelanotide. The FDA also agreed that the intranasal Definitive

QTc study (an electrocardiographic evaluation), the carcinogenicity

studies and the reproductive toxicity studies we conducted were

acceptable for NDA submission.

The

RECONNECT STUDY is being conducted in premenopausal women diagnosed

with HSDD, either with or without arousal difficulties. HSDD is the

single largest specific diagnosis in FSD. We enrolled a combined

total of approximately 1,250 randomized subjects in the two pivotal

efficacy studies, which are double blind placebo-controlled,

randomized parallel group studies. Each study had two arms, one a

1.75 mg bremelanotide dose and one a placebo. The double blind or

efficacy portion of each study consisted of a 24-week treatment

evaluation period, with primary and key secondary endpoints of

satisfying sexual events, or SSEs, the Female Sexual Function

Index, or FSFI, desire subdomain (a 28 day recall), and question 13

of the Female Sexual Distress Scale-Desire/Arousal/Orgasm, or

FSDS-DAO, questionnaire.

The

last patient visits for efficacy portion of the RECONNECT STUDY

were completed in the third quarter of calendar 2016. Patients in

the efficacy portion of the RECONNECT STUDY had the option, after

completion of the randomized portion of the study, to continue in

an open-label safety extension study, in which all patients receive

the 1.75 mg bremelanotide dose. The open-label safety extension

study has enrolled approximately 680 patients. The open-label

safety extension study will continue through the third quarter of

calendar 2017, and the purpose of the extension study is to gather

additional data on the safety of long-term and repeated use of

bremelanotide.

The

analysis of Phase 3 efficacy data is anticipated to be completed in

the fourth quarter of calendar 2016. Assuming we believe that the

Phase 3 data will support approval of bremelanotide for HSDD by

FDA, we will conduct drug interaction and other ancillary studies,

and certain chemistry, manufacturing and controls activities,

required for FDA approval in the fourth quarter of calendar 2016

and first half of calendar 2017. We anticipate submitting an NDA to

FDA for approval of bremelanotide for HSDD in mid-calendar 2017. We

cannot assure you that the Phase 3 data will support approval of

bremelanotide for HSDD or that the FDA will approve an NDA for

bremelanotide.

In the

RECONNECT STUDY patients self-administer bremelanotide with a

single-use autoinjector pen. The bremelanotide single-use

autoinjector pen, intended to be the commercial drug product, does

not have a visible needle, is stored at room temperature and is

easy to use. Women administer bremelanotide by pressing the

autoinjector pen collar against either their thigh or abdomen, and

the autoinjector pen automatically introduces the needle,

administers the dose of bremelanotide under the skin and audibly

signals when the drug has been delivered and the needle is

retracted.

2

Phase 2B Clinical Study Results. The

bremelanotide RECONNECT STUDY was predicated on the results of a

Phase 2B clinical study of bremelanotide. The Phase 2B clinical

study was a multicenter, placebo-controlled, randomized, parallel

group, dose-finding trial testing three dose levels, 0.75 mg, 1.25

mg and 1.75 mg, of subcutaneously administered bremelanotide

against placebo in premenopausal women diagnosed with hypoactive

sexual desire disorder, female sexual arousal disorder or both. The

1.75 mg dose demonstrated clinically meaningful and statistically

significant results for all predefined endpoints and was

well-tolerated. Full data on the Phase 2B clinical study was

presented at the March 2013 annual meeting of the International

Society for the Study of Women’s Sexual Health, and was

published in Women’s

Health, 12:3425-337 (2016).

The

Phase 2B clinical study enrolled 395 premenopausal women across 66

sites within the United States and Canada, with patients randomized

to one of three bremelanotide treatment arms and a placebo arm for

16 weeks of treatment. The objective of the Phase 2B study was to

measure safety and efficacy in premenopausal women with hypoactive

sexual desire disorder, female sexual arousal disorder or both of

bremelanotide compared to placebo. In the Phase 2B study,

subcutaneous doses of bremelanotide and placebo were

self-administered by the patient prior to a sexual encounter. The

primary efficacy endpoint was change from baseline to end of study

in the number of SSEs, with pre-specified analysis of pooled 1.25

and 1.75 mg doses compared to placebo.

In the

Phase 2B clinical study, the primary endpoint data analysis of 327

premenopausal women with hypoactive sexual desire disorder, female

sexual arousal disorder or both showed statistically significant

and clinically meaningful increases in the number of SSEs, and

statistically significant and clinically meaningful improvement in

secondary endpoint measures of overall sexual functioning and

distress related to sexual dysfunction, for women taking

bremelanotide compared to placebo. Satisfying sexual events were

measured with an event log and overall sexual functioning and

distress related to sexual dysfunction were measured using

validated patient reported outcome measurement tools. Bremelanotide

showed a statistically significant increase from baseline in the

number of SSEs compared against placebo at both the 1.75 mg dose

and pooled results of the 1.75 and 1.25 mg doses. The mean increase

in SSEs at 1.75 mg dose levels was 0.8 SSEs per month, from 1.8 to

2.6, with a p value of 0.021 against placebo. For the pooled doses,

the mean increase in SSEs was 0.7 SSEs per month, from 1.6 to 2.4

(a 50% increase), with a p value of 0.018 against placebo. By

contrast, with placebo, the mean change from baseline was from 1.7

to 1.9 (a 12% increase) in SSEs. The 0.75 mg dose demonstrated a

response that was not significant different from

placebo.

The

mean change from baseline in a validated measurement tool of

overall sexual functioning, the FSFI total score, was 4.4 at the

1.75 mg dose level, compared to 1.88 for placebo, with a p value of

0.0021 against placebo. For the pooled doses, the FSFI total score

mean change from baseline was 3.55, compared to 1.88 for placebo,

with a p value of 0.0017 against placebo. The FSFI is a 19-item

questionnaire measuring improvement in arousal, desire and overall

sexual function.

The

mean change from baseline in a validated measurement tool of

distress related to sexual dysfunction, the FSDS-DAO total score,

was -13.1 at the 1.75 mg dose level, compared to -6.8 for placebo,

with a p value of 0.0005 against placebo. For the pooled doses, the

FSDS-DAO total score mean change from baseline was -11.1, compared

to -6.8 for placebo, with a p value of 0.036 against placebo. The

FSDS-DAO is a 15-item questionnaire that measures personal distress

associated with HSDD.

A

significantly higher percentage of women receiving the 1.75 mg

bremelanotide dose – 55% – achieved a clinically

meaningful change from baseline of at least one satisfying sexual

event, compared to 37% of women receiving placebo. In addition,

compared against placebo a significantly higher percentage of women

also achieved a clinically meaningful improvement in sexual

function, as measured by the FSFI (53% vs. 29%), and a clinically

meaningful decrease in distress associated with sexual dysfunction

as measured by the FSDS-DAO (69% vs. 45%).

Using a

validated self-assessment questionnaire of treatment benefit, 79.5%

of blinded patients receiving the 1.75 mg dose of bremelanotide

reported they benefited from taking the drug, compared to 48.4% of

blinded patients receiving placebo.

Bremelanotide was

well-tolerated during the Phase 2B clinical study. The most common

types of treatment-emergent adverse events reported more frequently

in the bremelanotide arms were facial flushing, nausea, emesis and

headache, which were mainly mild-to-moderate in severity. Adverse

events that most commonly led to discontinuation were nausea and

emesis, with less than 3% discontinuation due to an adverse event.

Twenty-six patients, evenly distributed among placebo and active

arms of the Phase 2B clinical study, met the predefined blood

pressure withdrawal criteria. Drug treated patients had

approximately a 2 mm Hg change in blood pressure, predominately

during the first four hours following dosing. No serious adverse

events were attributable to bremelanotide during the

trial.

3

Medical Need — HSDD. Hypoactive

sexual desire disorder, either with or without arousal

difficulties, is the largest single category of FSD. Female sexual

dysfunction is a multifactorial condition that has anatomical,

physiological, medical, psychological and social components, and is

defined as persistent or recurring problems during one or more of

the stages of sexual response with associated distress. HSDD has a

significant impact on a patient’s self-image, relationships

and general well-being. The 2006 PRESIDE (Prevalence of Female

Sexual Problems Associated with Distress and Determinants of

Treatment Seeking) study, a cross-sectional, population-based

survey of 31,581 female adult respondents in the United States

published in 2008 in the journal Obstetrics & Gynecology, found that

approximately 22% of women reported a sexual problem and 11% were

women with HSDD. Based on the number of premenopausal women in the

United States according to the U.S. Census, the presenting market

size of premenopausal women with primary HSDD is at least 5.1

million women.

Subcutaneous Bremelanotide.

Bremelanotide, which is believed to act through activation of

melanocortin receptors in the central nervous system, is a

first-in-class pharmaceutical agent in development as a treatment

of HSDD. Bremelanotide is intended for as needed use and is

self-administered by the patient thirty minutes to one hour prior

to anticipated sexual activity. We selected a simple and

patient-friendly single-use autoinjector pen used in the RECONNECT

STUDY and intended for commercialization of the bremelanotide drug

product.

Partnering. In August 2014, we entered

into a license agreement with Gedeon Richter to co-develop and

commercialize bremelanotide for FSD in the European Union, other

European countries and additional selected countries. We received

€7.5 million ($9.8 million) in total upfront payments from

Gedeon Richter, and a milestone payment of €2.5 million ($3.1

million) upon the initiation of our Phase 3 clinical trial program

in the United States. On September 16, 2015, we entered into a

termination agreement pursuant to which we and Gedeon Richter

agreed to mutually and amicably terminate the license agreement. In

connection with this termination, all rights and licenses to

co-develop and commercialize bremelanotide for FSD indications held

by Gedeon Richter terminated and reverted back to us. Neither we

nor Gedeon Richter have any future material obligations under the

license agreement.

We have

worldwide rights for bremelanotide for FSD, HSDD and all other

indications. We are in active discussions with potential partners

for U.S. marketing and commercialization rights for bremelanotide

for HSDD. We may not be able to enter into suitable agreements with

potential partners on acceptable terms, if at all.

Prior Clinical Trials. We have

completed several Phase 1 clinical studies in which various safety

parameters, including blood pressure effects of subcutaneously

administered bremelanotide, were studied. Based in part on these

studies, our Phase 2B clinical trial assessed the magnitude and

duration of blood pressure effect, and determined that subcutaneous

administration of selected doses of bremelanotide for treatment of

HSDD in premenopausal women provides acceptable control of blood

pressure effects. We have also completed clinical studies involving

an alternative route of administration. Bremelanotide has been

administered in 34 clinical studies involving about 3,000 subjects,

including studies of premenopausal and postmenopausal women with

HSDD and other forms of FSD and men with ED.

MC1r Peptide Agonists. We have conducted

preclinical animal studies with MC1r peptide drug candidates for

inflammatory disease and autoimmune indications. The MC1r is

upregulated in a number of diseases, including inflammatory bowel

disease, nephritis, which is inflammation of the kidneys, and

rheumatoid arthritis, and ocular indications such as uveitis and

dry eye. We believe that MC1r peptides have broad anti-inflammatory

effects and appear to utilize mechanisms engaged by the endogenous

melanocortin system in regulation of the immune system and

resolution of pro-inflammatory responses. MC1r peptides also have

potential application in a number of dermatologic indications,

including vitiligo and erythropoietic protoporphyria.

Our

MC1r peptide drug candidates are highly specific, with

substantially greater binding and efficacy at MC1r than at other

melanocortin receptors. In vitro safety studies have shown that our

MC1r peptide drug candidates have no activity in a wide range of

various receptors, ion channels and kinases. We have selected one

of our MC1r peptide drug candidates, designated PL-8177, as a

clinical trial candidate.

Animal

studies that we have conducted with our MC1r peptide drug

candidates have shown positive results in experimental models of

inflammatory bowel disease, uveitis and nephritis. We are

continuing to conduct studies on a number of different indications.

We have completed preclinical toxicology testing on PL-8177 and

chemistry, controls and manufacturing activities to support Phase 1

studies, and anticipate filing an IND application on

PL-8177.

Next Generation MC4r Peptide and Small Molecule

Agonists. We have developed a series of highly selective

MC4r peptides and are developing orally active small molecules. In

developing these compounds, we examined effectiveness in animal

models of sexual response, obesity and related metabolic signals,

and also determined cardiovascular effects, primarily looking at

changes in blood pressure. Results of these studies suggest that

certain of these compounds may have significant commercial

potential for treatment of conditions responsive to MC4r

activation, including HSDD, FSD, ED, obesity and diabetes. We are

engaged in preclinical activities with these compounds, and are

evaluating potential pharmaceutical applications.

4

We have

selected an internal lead compound for obesity, designated PL-8905,

which has over 100-fold functional selectivity for MC4r over MC1r

with minimal effect on blood pressure and limited central nervous

system penetration. PL-8905 exhibits significant chemical and

metabolic stability.

Obesity. Obesity is a multifactorial

condition with numerous biochemical components relating to satiety

(feeling full), energy utilization and homeostasis. A number of

different metabolic and hormonal pathways are being evaluated by

companies around the world in efforts to develop better treatments

for obesity. Scientific research has established that melanocortin

receptors have a role in eating behavior and energy homeostasis,

and that melanocortin receptor agonists can decrease food intake

and induce weight loss. With a previous partner, we completed

clinical proof-of-concept studies for the MC4r mechanism in

obesity, which met the primary objectives of significant decrease

in food intake and weight loss.

Other Melanocortin Receptor-Specific

Programs. We are continuing drug discovery efforts in the

melanocortin receptor field, primarily developing peptide

compounds, including highly selective MC1r agonists and peptides

specific for MC4r, including both agonists and

antagonists.

Our

Natriuretic Peptide Receptor-Specific Programs

The

natriuretic peptide receptor system has numerous cardiovascular

functions, and therapeutic agents modulating this system may be

useful in treatment of heart failure, acute asthma, other pulmonary

diseases and hypertension. While the therapeutic potential of

modulating this system is well appreciated, development of

therapeutic agents has been difficult due, in part, to the short

biological half-life of native peptide agonists.

We have

designed and are developing candidate drugs that are selective for

different natriuretic peptide receptors, including NPR-A,

natriuretic peptide receptor B, or NPR-B, natriuretic peptide

receptor C, or NPRC, and both NPR-A and NPR-B.

We are

in active discussions with potential partners for marketing and

commercialization rights in the United States and the rest of the

world for PL-3994 and our related candidate drugs. We may not be

able to enter into suitable agreements on acceptable terms with

potential partners, if at all.

PL-3994. PL-3994 is our lead natriuretic

peptide receptor product candidate, and is a synthetic mimetic of

the neuropeptide hormone ANP and an NPR-A agonist. PL-3994 is in

development for treatment of heart failure, acute exacerbations of

asthma and refractory hypertension. PL-3994 activates NPR-A, a

receptor known to play a role in cardiovascular homeostasis.

Consistent with being an NPR-A agonist, PL-3994 increases plasma

cyclic guanosine monophosphate, or cGMP, levels, a pharmacological

response consistent with the effects of endogenous (naturally

produced) natriuretic peptides on cardiovascular function and

smooth muscle relaxation. PL-3994 also decreases activity of the

renin-angiotensin-aldosterone system, or RAAS, a hormone system

that regulates blood pressure and fluid balance. The RAAS system is

frequently over-activated in heart failure patients, leading to

worsening of cardiovascular function.

PL-3994, our lead

product development candidate which is ready for Phase 2 safety and

efficacy studies, is one of a number of natriuretic peptide

receptor agonist compounds we have developed. PL-3994 is a

synthetic molecule incorporating a novel and proprietary amino acid

mimetic structure, and has an extended circulation half-life and

metabolic stability compared to endogenous ANP. Based on the

half-life and pharmacokinetics, we believe that PL-3994 is amenable

to once daily chronic use subcutaneous administration.

PL-3994 for Heart Failure. Heart

failure is an illness in which the heart is unable to pump blood

efficiently, and includes acutely decompensated heart failure with

dyspnea (shortness of breath) at rest or with minimal activity.

Endogenous natriuretic peptides have a number of beneficial

effects, including vasodilation (relaxation of blood vessels),

natriuresis (excretion of sodium) and diuresis (excretion of

fluids).

Patients who have

been admitted to the hospital with an episode of worsening heart

failure have an increased risk of either death or hospital

readmission in the three months following discharge. Up to 15% of

patients die in this period and as many as 30% need to be

readmitted to the hospital. We believe that decreasing mortality

and hospital readmission in patients discharged following

hospitalization for worsening heart failure is a large unmet

medical need for which PL-3994 may be effective. PL-3994 could

potentially be utilized as an adjunct to existing heart failure

medications, and may, if successfully developed, be

self-administered by patients as a subcutaneous injection following

hospital discharge. We believe that PL-3994, through activation of

NPR-A, may, if successful, reduce cardiac hypertrophy (increase in

heart size due to disease), which is an independent risk factor for

cardiovascular morbidity and mortality.

5

According to a

report from the American Heart Association published in 2014 in the

journal Circulation, an

estimated 5.7 million Americans suffer from heart failure, with

870,000 new cases of heart failure diagnosed each year, with

disease incidence expected to increase with the aging of the

American population. Heart failure has tremendous human and

financial costs. The same report estimated that the 2012 total

costs in the United States for heart failure were $30.7 billion,

with heart failure constituting the leading cause of

hospitalization in people over 65 years of age and with over 1

million hospital discharges for heart failure in 2010. Heart

failure is a high mortality disease, with approximately one-half of

heart failure patients dying within five years of initial

diagnosis.

Patient

populations have been identified which have reduced levels of

endogenous active natriuretic peptides, including endogenous active

ANP. The reduced levels have a variety of causes, including

mutations in endogenous natriuretic peptides and in enzymes

necessary to convert natriuretic peptide sequences to their active

form. Patients with reduced levels of endogenous active natriuretic

peptides are reported to have a poor response to current drug

therapies and to have increased rates of cardiac remodeling and

cardiac events.

We

believe that PL-3994 has the potential to treat heart failure with

preserved ejection fraction, or HFpEF, which is a high unmet

medical need with no approved treatment options, heart failure with

reduced ejection fraction, or HFrEF, and patients with reduced

levels of endogenous active natriuretic peptides, such as corin

deficiencies, which is a high unmet medical need in patients with a

poor response to current therapies, with the objective to restore

normal natriuretic peptide function.

We have

planned a repeat dose Phase 2 clinical trial in patients with

HFpEF, HFrEF and corin deficiency to evaluate safety profiles and

symptom relief as well as pharmacokinetic (period to metabolize or

excrete the drug) and pharmacodynamic (period of action or effect

of the drug) endpoints. Analysis will include cardiac imaging and

measurement of left ventricular ejection fraction. Contingent on

adequate available funds, we intend to initiate this trial in the

first half of calendar 2017. Assuming favorable results from this

trial, we have planned a repeat dose Phase 2 proof-of-principle

clinical trial in patients with heart failure, which would involve

treatment for a three- to six-month period, and would evaluate

safety, cardiac function, effects on remodeling, symptom

improvement and hospitalization admission rates. Contingent on

adequate available funds, the proof-of-principle Phase 2 trial will

be initiated following completion of the first repeat dose Phase 2

clinical trial.

PL-3994 for Acute Exacerbations of

Asthma. Research over the past two decades has demonstrated

potent bronchodilator effects with both systemic and inhalation

administration of natriuretic peptides. NPR-A agonism is known to

relax smooth muscles in airways and works through a pathway

independent of the beta-2 adrenergic receptor. Preclinical testing

demonstrated potent airway smooth muscle relaxation in guinea pig

and human tissues using PL-3994, and animal studies in sensitized

guinea pigs have demonstrated a bronchodilator effect with PL-3994

using both subcutaneous and inhalation administration.

Acute

exacerbations of asthma, also called acute severe asthma, is an

ongoing, unremitting asthma episode in which asthma symptoms do not

adequately respond to initial bronchodilator therapy. Inhaled

beta-2 adrenergic receptor agonists, such as albuterol, inhaled

anticholinergic drugs, such as ipratropium, and systemic

corticosteroids are primary treatments for episodes of acute

exacerbations of asthma. Some patients with acute exacerbations of

asthma become unresponsive to beta-2 adrenergic receptor agonists,

significantly limiting treatment options and increasing risk.

Patients who do not respond to initial therapy are at risk of

severe complications. We intend to initially target PL-3994 as a

treatment for those at-risk unresponsive patients.

According to a 2014

report from the National Center for Environmental Health, Asthma

Prevalence in the United States, in 2010 there were 1.8 million

emergency room visits and 439,000 hospitalizations attributed to

asthma. Approximately 25.7 million Americans have

asthma.

Endogenous

natriuretic peptides have a very short half-life, due primarily to

degradation by neutral endopeptidase and clearance through the

natriuretic peptide clearance receptor. PL-3994 is resistant to

neutral endopeptidase and clears from the body much more slowly

than endogenous natriuretic peptides. PL-3994 has a blood-plasma

half-life of at least three hours in humans when administered by

subcutaneous injection, with biological effects seen for over eight

hours post-administration.

Clinical Studies with PL-3994. Human

clinical studies of PL-3994 commenced with a Phase 1 trial, which

concluded in 2008. This was a randomized, double-blind,

placebo-controlled study in 26 healthy volunteers who received

either PL-3994 or a placebo subcutaneously. The evaluations

included safety, tolerability, pharmacokinetics and several

pharmacodynamic endpoints, including levels of cGMP. Dosing

concluded with the successful achievement of the primary endpoint

of the study, a pre-specified reduction in systemic blood pressure.

No volunteer experienced a serious or severe adverse event.

Elevations in plasma cGMP levels, increased diuresis and increased

natriuresis were all observed for several hours after single

subcutaneous doses.

6

Later

in 2008, we conducted a Phase 2A trial in volunteers with

controlled hypertension who were receiving one or more conventional

antihypertensive medications. In this trial, which was a

randomized, double-blind, placebo-controlled, single ascending dose

study in 21 volunteers, the objective was to demonstrate that

PL-3994 can be given safely to patients taking antihypertensive

medications commonly used in heart failure and hypertension

patients. Dosing concluded with the successful achievement of the

primary endpoint of the study, a pre-specified reduction in

systemic blood pressure. No volunteer experienced a serious or

severe adverse event. Elevations in plasma cGMP levels were

observed for several hours after single subcutaneous doses. Based

on the studies to date, PL-3994 is ready for Phase 2 safety and

efficacy studies.

Administration of PL-3994. For heart

failure and refractory hypertension indications we believe that

subcutaneous administration of PL-3994 may be preferable. PL-3994

is well absorbed through the subcutaneous route of administration.

In human studies, the pharmacokinetic and pharmacodynamic

half-lives were on the order of hours, significantly longer than

the comparable half-lives of endogenous natriuretic peptides. We

believe that subcutaneous PL-3994, if successful, will be

appropriate for self-administration by patients, similar to insulin

and other self-administered drugs. For asthma indications we

believe that inhalation administration of PL-3994 may be preferable

to subcutaneous or other systemic administration.

Technologies

We Use

We used

a rational drug design approach to discover and develop proprietary

peptide, peptide mimetic and small molecule agonist compounds,

focusing on melanocortin and natriuretic peptide receptor systems.

Computer-aided drug design models of receptors are optimized based

on experimental results obtained with peptides and small molecules

that we develop. With our approach, we believe we are developing an

advanced understanding of the factors which drive

agonism.

We have

developed a series of proprietary technologies used in our drug

development programs. One technology employs novel amino acid

mimetics in place of selected amino acids. These mimetics provide

the receptor-binding functions of conventional amino acids while

providing structural, functional and physiochemical advantages. The

amino acid mimetic technology is employed in PL-3994, our compound

in development for treatment of heart failure, acute exacerbations

of asthma and refractory hypertension.

Some

compound series have been derived using our proprietary and

patented platform technology, called MIDAS™, or Metal Ion-induced Distinctive Array of Structures. This technology employs

metal ions to fix the three-dimensional configuration of peptides,

forming conformationally rigid molecules that remain folded

specifically in their active state. These MIDAS molecules are

generally simple to synthesize, are chemically and proteolytically

stable, and have the potential to be orally bioavailable. In

addition, MIDAS molecules are information-rich and provide data on

structure-activity relationships that may be used to design small

molecule, non-peptide drugs.

Amount

Spent on Research and Development Activities

Research and

development expenses were approximately $43.1 million for the

fiscal year ended June 30, 2016, or fiscal 2016, $24.6 million for

the fiscal year ended June 30, 2015, or fiscal 2015, and $10.8

million for the fiscal year ended June 30, 2014, or fiscal

2014.

Competition

General. Our products under development

will compete on the basis of quality, performance, cost

effectiveness and application suitability with numerous established

products and technologies. We have many competitors, including

pharmaceutical, biopharmaceutical and biotechnology companies.

Furthermore, there are several well-established products in our

target markets that we will have to compete against. Products using

new technologies which may be competitive with our proposed

products may also be introduced by others. Most of the companies

selling or developing competitive products have financial,

technological, manufacturing and distribution resources

significantly greater than ours and may represent significant

competition for us. In addition, if any of our product candidates

are approved by FDA, they will eventually face competition from

generic versions that will sell at significantly reduced prices, be

preferred by managed care and health insurance payers, and be

eligible for automatic pharmacy substitution even when a prescriber

writes a prescription for our product. The timing and extent of

future generic competition is dependent upon both our intellectual

property rights and the FDA regulatory process, but cannot be

accurately predicted.

The

pharmaceutical and biotechnology industries are characterized by

extensive research efforts and rapid technological change. Many

biopharmaceutical companies have developed or are working to

develop products similar to ours or that address the same markets.

Such companies may succeed in developing technologies and products

that are more effective or less costly than any of those that we

may develop. Such companies may be more successful than us in

developing, manufacturing and marketing products.

7

We

cannot guarantee that we will be able to compete successfully in

the future or that developments by others will not render our

proposed products under development or any future product

candidates obsolete or noncompetitive or that our collaborators or

customers will not choose to use competing technologies or

products.

Bremelanotide for Treatment of HSDD.

There is competition and financial incentive to develop, market and

sell drugs for the treatment of HSDD and other forms of FSD.

Flibanserin, sold under the trade name Addyi®, is the only

drug currently approved in the United States for treatment of HSDD.

Flibanserin, a non-hormonal oral serotonin 5-HT1A agonist, 5-HT2A

antagonist, which requires chronic dosing, was approved by the FDA

on August 18, 2015 for treatment of premenopausal women with HSDD.

The FDA approval included a risk evaluation and mitigation

strategy, or REMS, because of the increased risk of severe

hypotension and syncope due to the interaction between flibanserin

and alcohol, and a Boxed Warning to highlight the risks of severe

hypotension and syncope in patients who drink alcohol during

treatment with flibanserin, in those who also use moderate or

strong CYP3A4 inhibitors, and in those who have liver impairment.

Approval by the FDA followed a positive FDA advisory committee

recommendation in June 2015. We are aware of several other drugs at

various stages of development, most of which are taken on a

chronic, typically once-daily, basis. An oral fixed-dose

combination of two antidepressants, bupropion and trazodone, is

reported to be entering Phase 2 studies in premenopausal women with

HSDD. Another company is developing two different oral fixed-dose

combination drugs, one a combination of sildenafil and testosterone

and the other a combination of testosterone and buspirone

hydrochloride, and has conducted Phase 2 studies. Libigel®, a

testosterone gel, completed two Phase 3 efficacy trials for

treatment of FSD in surgically post-menopausal women, but did not

show statistical separation from placebo in those trials. Intrinsa,

a transdermal testosterone patch, successfully completed a Phase 3

clinical program, but was not approved in the United States based

on potential long-term use safety risks of cancer and

cardiovascular adverse events. There are other companies reported

to be developing new drugs for FSD indications, some of which may

be in clinical trials in the United States or elsewhere. We are not

aware of any company actively developing a melanocortin receptor

agonist drug for HSDD.

PL-3994 for Heart Failure Indications.

Nesiritide (sold under the trade name Natrecor®), a

recombinant human B-type natriuretic peptide drug, is marketed in

the United States by Scios Inc., a Johnson & Johnson company.

Nesiritide is approved for treatment of acutely decompensated

congestive heart failure patients who have dyspnea at rest or with

minimal activity. Other peptide drugs, including carperitide, a

recombinant human atrial natriuretic peptide drug, and ularitide, a

synthetic form of urodilatin, a naturally occurring human

natriuretic peptide related to atrial natriuretic peptide, have

been investigated for treatment of congestive heart failure, but we

are not aware of any active development in the United States. We

are aware of other companies developing intravenously administered

natriuretic peptide drugs, with at least one reported to have

completed Phase 2 clinical trials for acute heart failure. A

combination drug comprised of sacubitril and valsartan developed by

Novartis AG, sold under the trade name Entresto®, inhibits

both the angiotensin II receptor and neprilysin (an enzyme which

inactivates endogenous active natriuretic peptides). This

combination drug, which was approved by the FDA in July 2015,

results in increases of endogenous active ANP levels, and thus has

a mechanism of action with similarities to PL-3994. In a Phase 3

trial, the combination drug was compared to an

angiotensin-converting-enzyme inhibitor, enalapril, in heart

failure patients with reduced ejection fraction. It significantly

improved the rate of death from cardiovascular causes,

significantly reduced hospitalization for heart failure and

significantly improved heart failure symptoms. This combination

drug demonstrated that upregulation of the natriuretic peptide

system in combination with angiotensin-converting-enzyme inhibition

is superior to angiotensin-converting-enzyme inhibition alone, and

thus provides validation of the natriuretic peptide system as a

target for improving outcomes in treating heart failure patients.

In addition, there are a number of approved drugs and drugs in

development for treatment of heart failure through mechanisms or

pathways other than agonism of NPR-A.

PL-3994 for Acute Exacerbations of Asthma

Indications. The asthma market is intensively competitive,

with substantial competition and financial incentive to develop,

market and sell drugs for treatment of asthma, with projected costs

of prescription drugs of $5.9 billion in the United States in 2010.

We are aware of companies developing drugs for the specific

indications of either acute exacerbations of asthma or acute severe

asthma, including at least one company with a drug reported to be

currently in clinical trials. Certain of these drugs under

development work by mechanisms of action different from the

mechanisms of action of currently approved products. In addition, a

number of clinical trials are conducted by hospitals, research

institutes and others exploring various methods and combinations of

drugs to treat acute exacerbations of asthma. There are a number of

drugs and therapies currently used to treat acute exacerbations of

asthma, including administration of oral or intravenous systemic

steroids, use of oxygen or heliox, a mixture of helium and oxygen,

nebulized short-acting beta-2 adrenergic receptor agonists,

intravenous or nebulized anticholinergic agents and, for patients

in or approaching respiratory arrest, intubation and mechanical

ventilation. However, each of these drugs or therapies has

recognized limitations or liabilities, and we believe that there

remains an unmet medical need for a safe and effective treatment

for acute exacerbations of asthma. We are not aware of any other

company actively developing a drug to treat asthma using a

natriuretic peptide receptor pathway.

8

MC4r Peptides for Erectile Dysfunction.

Leading drugs approved for erectile dysfunction, or ED, indications

are PDE-5 inhibitors which target the vascular system, such as

sildenafil (sold under the trade name Viagra®), vardenafil

(sold under the trade name Levitra®) and tadalafil (sold under

the trade name Cialis®). Other drugs approved for ED

indications include alprostadil for injection (sold under the trade

name Caverject Impulse® among others), which is injected

directly into the penis, and alprostadil in urethral suppository

format (sold under the trade name MUSE®). In addition, a

variety of devices, including vacuum devices and surgical penile

implants, have been approved for ED indications. We are aware of a

number of companies developing new drugs for ED indications, some

of which are in clinical trials in the United States and elsewhere.

We are not aware of any company actively developing a melanocortin

receptor agonist drug for ED.

Obesity. There are a number of

FDA-approved drugs and medical devices for the treatment of

obesity, and a large number of products in clinical development by

other companies, including products which target melanocortin

receptors. At least one Phase 2 study has been reported on use of

an MC4r agonist for obesity indications.

MC1r Peptides for Dermatologic and

Inflammatory Disease-Related Indications. Many dermatologic

and inflammatory disease-related indications are treated using

systemic steroids or immunosuppressant drugs, both of which have

side effects which can be dose limiting. There are a large number

of approved biological drugs and biological drugs under development

for treatment of dermatologic and inflammatory disease-related

indications.

Patents

and Proprietary Information

Patent Protection. Our success will

depend in substantial part on our ability to obtain, defend and

enforce patents, maintain trade secrets and operate without

infringing upon the proprietary rights of others, both in the

United States and abroad. We own a number of issued United States

patents and have pending United States patent applications, many

with issued or pending counterpart patents in selected foreign

countries. We seek patent protection for our technologies and

products in the United States and those foreign countries where we

believe patent protection is commercially important.

We own

two issued United States patents claiming the bremelanotide

substance and an issued patent claiming the bremelanotide substance

in each of Australia, Austria, Belgium, Brazil, Canada, Cyprus,

Denmark, Finland, France, Germany, Greece, Hong Kong, Ireland,

Italy, Japan, Korea, Luxembourg, Mexico, Monaco, Netherlands, New

Zealand, Portugal, Spain, Sweden, Switzerland, and the United

Kingdom. The issued United States patents have a term until 2020,

which term may be subject to extension for a maximum period of up

to five years as compensation for patent term lost during drug

development and the FDA regulatory review process, pursuant to the

Drug Price Competition and Patent Term Restoration Act of 1984, or

the Hatch-Waxman Amendments. Whether we will be able to obtain

patent term extensions under the Hatch-Waxman Amendments and the

length of any such extension cannot be determined until the FDA

approves for marketing, if ever, a product in which bremelanotide

is the active ingredient. In addition, the claims of issued patents

covering bremelanotide may not provide meaningful protection.

Further, third parties may challenge the validity or scope of any

issued patent, and under the Hatch-Waxman Amendments, potentially

receive approval of a competing generic version of our product or

products even before a court rules on the validity or infringement

of our patents.

We own

an issued United States patent and pending patent applications in

the United States for methods of treating FSD with bremelanotide,

and related patent applications are pending in Australia, Brazil,

Canada, China, Colombia, Georgia, Hong Kong, India, Indonesia,

Israel, Japan, Korea, Malaysia, Mexico, New Zealand, Philippines,

Singapore, South Africa, Ukraine, Vietnam and before the European

and Eurasian patent offices. The issued United States patent has a

term until 2033. Whether we will be able to obtain a patent term

extension in the United States under the Hatch-Waxman Amendments,

assuming that a relevant patent issues in the United States, and

the length of any such extension, cannot be determined until the

FDA approves for marketing, if ever, a product utilizing

bremelanotide by methods claimed in the patent. Pending

applications in the United States and elsewhere in the world have a

presumptive term, if a patent is issued, until 2033.

We have

patents and patent applications on an alternative class of

melanocortin receptor-specific peptides for treatment of sexual

dysfunction and other indications, including obesity, consisting of

two issued patents in the United States, an issued patent in each

of Australia, Canada, China, Israel, Mexico, New Zealand, Japan and

Russia, and pending patent applications on the same class in

Brazil, India, Korea, and South Africa and before the European

patent office. The presumptive term of the issued patents and

pending patent applications is until 2029. We also have patents and

pending patent applications for a second class of alternative

melanocortin receptor-specific peptides for treatment of sexual

dysfunction and other indications, including obesity, consisting of

issued patents in the United States, Australia, China, Japan,

Mexico, New Zealand, Russia, and South Africa and pending patent

applications on the same class in Brazil, Canada, China, India,

Israel, Korea, and before the European patent office. The

presumptive term of the issued patents and pending patent

applications is until 2030. Until one or more product candidates

covered by a claim of one of these patents and patent applications

are developed for commercialization, which may never occur, we

cannot evaluate the duration of any potential patent term extension

under the Hatch-Waxman Amendments.

9

We own

issued patents in the United States, Mexico, New Zealand, South

Africa and Russia claiming highly selective MC1r agonist peptides

for treatment of inflammation-related diseases and disorders and

related indications, and pending patent applications on two broad

classes of highly selective MC1r agonist peptides in the United

States, Australia, Brazil, Canada, China, India, Israel, Japan,

Korea, and Mexico and before the European patent office. The

presumptive term of the issued patents and pending patent

applications is until 2030. Until one or more product candidates

covered by a claim of one of these patent applications are

developed for commercialization, which may never occur, we cannot

evaluate the duration of any potential patent term extension under

the Hatch-Waxman Amendments.

We own

two issued United States patents claiming the PL-3994 substance and

other natriuretic peptide receptor agonist compounds that we have

developed and an issued United States patent claiming a precursor

molecule to the PL-3994 substance, both of which expire in 2027.

Corresponding patents on the PL-3994 substance and other

natriuretic peptide receptor agonist compounds were issued in

Australia, Austria, Belgium, China, Colombia, Denmark, Finland,

France, Germany, Hong Kong, Hungary, India, Ireland, Israel, Italy,

Japan, Korea, Mexico, Netherlands, Philippines, Russia, South

Africa, Spain, Sweden, Switzerland, and the United Kingdom, with

terms until 2027. Patent applications on the PL-3994 substance and

other natriuretic peptide receptor agonist compounds are pending in

Brazil and Canada, with presumptive terms until 2027. Applications

claiming precursor molecules for the PL-3994 substance and other

compounds have issued in the United States, Australia, China,

France, Germany, Hong Kong, India, Ireland, Israel, Japan, Mexico,

Netherlands, Philippines, Korea, South Africa, Sweden, Switzerland

and the United Kingdom, and expire in 2027. Patent applications on

the precursor molecules are pending in Brazil, Canada, and before

the Eurasian Patent Office, with presumptive terms until 2027. We

also own an issued United States patent claiming use of the PL-3994

substance for treatment of acute asthma and chronic obstructive

pulmonary disease, which expires in 2031. We do not know the full

scope of patent coverage we will obtain, or whether any patents

will issue other than the patents already issued. Until one or more

product candidates covered by a claim of the issued patents or one

of these patent applications are developed for commercialization,

which may never occur, we cannot evaluate the duration of any

potential patent term extension under the Hatch-Waxman

Amendments.

We

additionally have 31 issued United States patents on melanocortin

receptor specific peptides and small molecules, and three issued

United States patents on natriuretic peptide receptor agonist

compounds, but we are not actively developing any product candidate

covered by a claim of any of these patents.

In the

event that a third party has also filed a patent application

relating to an invention we claimed in a patent application, we may

be required to participate in an interference proceeding

adjudicated by the United States Patent and Trademark Office to

determine priority of invention. The possibility of an interference

proceeding could result in substantial uncertainties and cost, even

if the eventual outcome is favorable to us. An adverse outcome

could result in the loss of patent protection for the subject of

the interference, subjecting us to significant liabilities to third

parties, the need to obtain licenses from third parties at

undetermined cost, or requiring us to cease using the

technology.

Future Patent Infringement. We do not

know for certain that our commercial activities will not infringe

upon patents or patent applications of third parties, some of which

may not even have been issued. Although we are not aware of any

valid United States patents which are infringed by bremelanotide or

PL-3994, we cannot exclude the possibility that such patents might

exist or arise in the future. We may be unable to avoid

infringement of any such patents and may have to seek a license,

defend an infringement action, or challenge the validity of such

patents in court. Patent litigation is costly and time consuming.

If such patents are valid and we do not obtain a license under any

such patents, or we are found liable for infringement, we may be

liable for significant monetary damages, may encounter significant

delays in bringing products to market, or may be precluded from

participating in the manufacture, use or sale of products or

methods of treatment covered by such patents.

Proprietary Information. We rely on

proprietary information, such as trade secrets and know-how, which

is not patented. We have taken steps to protect our unpatented

trade secrets and know-how, in part through the use of

confidentiality and intellectual property agreements with our

employees, consultants and certain contractors. If our employees,

scientific consultants, collaborators or licensees develop

inventions or processes independently that may be applicable to our

product candidates, disputes may arise about the ownership of

proprietary rights to those inventions and processes. Such

inventions and processes will not necessarily become our property,

but may remain the property of those persons or their employers.

Protracted and costly litigation could be necessary to enforce and

determine the scope of our proprietary rights.

10

If

trade secrets are breached, our recourse will be solely against the

person who caused the secrecy breach. This might not be an adequate

remedy to us because third parties other than the person who causes

the breach will be free to use the information without

accountability to us. This is an inherent limitation of the law of

trade secret protection.

U.S.

Governmental Regulation of Pharmaceutical Products

General

Regulation by

governmental authorities in the United States and other countries

will continue to significantly impact our research, product

development, manufacturing and marketing of any pharmaceutical

products. The nature and the extent to which regulations apply to

us will vary depending on the nature of any such products. Our

potential pharmaceutical products will require regulatory approval

by governmental agencies prior to commercialization. The products

we are developing are subject to federal regulation in the United

States, principally by the FDA under the Federal Food, Drug, and

Cosmetic Act, or FFDCA, and by state and local governments, as well

as regulatory and other authorities in foreign governments that

include rigorous preclinical and clinical testing and other

approval procedures. Such regulations govern or influence, among

other things, the research, development, testing, manufacture,

safety and efficacy requirements, labeling, storage, recordkeeping,

licensing, advertising, promotion, distribution and export of

products, manufacturing and the manufacturing process. In many

foreign countries, such regulations also govern the prices charged

for products under their respective national social security

systems and availability to consumers.

All

drugs intended for human use are subject to rigorous regulation by

the FDA in the United States and similar regulatory bodies in other

countries. The steps ordinarily required by the FDA before an

innovative new drug product may be marketed in the United States

are similar to steps required in most other countries and include,

but are not limited to:

●

completion of

preclinical laboratory tests, preclinical animal testing and

formulation studies;

●

submission to the

FDA of an IND, which must be in effect before clinical trials may

commence;

●

submission to the

FDA of an NDA that includes preclinical data, clinical trial data

and manufacturing information;

●

payment of

substantial user fees for filing the NDA and other recurring user

fees;

●

FDA review of the

NDA;

●

satisfactory

completion of an FDA pre-approval inspection of the manufacturing

facilities; and

●

FDA approval of the

NDA, including approval of all product labeling.

For

combination products deemed to have a

‘‘drug’’ primary mode of action, primary

review of the product will be conducted by the appropriate division

within the Center for Drug Evaluation and Research, or CDER, but

CDER will consult with the Center for Devices and Radiological

Health, or CDRH, to ensure that the device components of the

product meet all applicable device requirements.

The

research, development and approval process requires substantial

time, effort and financial resources, and approvals may not be

granted on a timely or commercially viable basis, if at

all.

Preclinical testing

includes laboratory evaluations to characterize the product’s

composition, impurities, stability, and mechanism of its

pharmacologic effect, as well as animal studies to assess the

potential safety and efficacy of each product. Preclinical safety

tests must be conducted by laboratories that comply with FDA

regulations regarding Good Laboratory Practices, or GLP, and the

U.S. Department of Agriculture’s Animal Welfare Act.

Violations of these laws and regulations can, in some cases, lead

to invalidation of the tests, requiring such tests to be repeated

and delaying approval of the NDA. The results of the preclinical

tests, together with manufacturing information and analytical data,

are submitted to the FDA as part of an IND and are reviewed by the

FDA before the commencement of human clinical trials. Unless the

FDA objects to an IND by placing the study on clinical hold, the

IND will go into effect 30 days following its receipt by the FDA.

The FDA may authorize trials only on specified terms and may

suspend ongoing clinical trials at any time on various grounds,

including a finding that patients are being exposed to unacceptable

health risks. If the FDA places a study on clinical hold, the

sponsor must resolve all of the FDA’s concerns before the

study may begin or continue. The IND application process may become

extremely costly and substantially delay development of products.

Similar restrictive requirements also apply in other countries.

Additionally, positive results of preclinical tests will not

necessarily indicate positive results in clinical

trials.

Clinical trials

involve the administration of the investigational product to humans

under the supervision of qualified principal investigators. Our

clinical trials must be conducted in accordance with Good Clinical

Practice, or GCP, regulations under protocols submitted to the FDA

as part of an IND. In addition, each clinical trial is approved and

conducted under the auspices of an institutional review board, or

IRB, and requires the patients’ informed consent. An IRB

considers, among other things, ethical factors, the safety of human

subjects, and the possibility of liability of the institutions

conducting the trial. The IRB at each institution at which a

clinical trial is being performed may suspend a clinical trial at

any time for a variety of reasons, including a belief that the test

subjects are being exposed to an unacceptable health risk. As the

sponsor, we can also suspend or terminate a clinical trial at any

time.

11

Clinical trials are

typically conducted in three sequential phases, Phases 1, 2, and 3,

involving an increasing number of human subjects. These phases may

sometimes overlap or be combined. Phase 1 trials are performed in a

small number of healthy human subjects or subjects with the

targeted condition, and involve testing for safety, dosage

tolerance, absorption, distribution, metabolism and excretion.

Phase 2 studies, which may involve up to hundreds of subjects, seek

to identify possible adverse effects and safety risks, preliminary

information related to the efficacy of the product for specific

targeted diseases, dosage tolerance, and optimal dosage. Finally,

Phase 3 trials may involve up to thousands of individuals often at

geographically dispersed clinical trial sites, and are intended to

provide the documentation of effectiveness and important additional

safety data required for approval. Prior to commencing Phase 3

clinical trials many sponsors elect to meet with FDA officials to

discuss the conduct and design of the proposed trial or

trials.

In

addition, federal law requires the listing, on a publicly-available

website, of detailed information on clinical trials for

investigational drugs. Some states have similar or supplemental

clinical trial reporting laws.

Success

in early-stage animal studies and clinical trials does not

necessarily assure success in later-stage clinical trials. Data

obtained from animal studies and clinical activities are not always

conclusive and may be subject to alternative interpretations that

could delay, limit or even prevent regulatory

approval.

All

data obtained from the preclinical studies and clinical trials, in

addition to detailed information on the manufacture and composition

of the product, would be submitted in an NDA to the FDA for review

and approval for the manufacture, marketing and commercial

shipments of any of our products. FDA approval of the NDA is

required before commercial marketing or non-investigational

interstate shipment may begin in the United States. The FDA may

also conduct an audit of the clinical trial data used to support

the NDA.

The FDA

may deny or delay approval of an NDA that does not meet applicable

regulatory criteria. For example the FDA may determine that the

preclinical or clinical data or the manufacturing information does

not adequately establish the safety and efficacy of the drug. The

FDA has substantial discretion in the approval process and may

disagree with an applicant’s interpretation of the data