UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-Q

(Mark One)

|

x

|

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the quarterly period ended December 31, 2014

or

|

o

|

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

|

For the transition period from ___________ to __________

Commission file number: 001-15543

________________________

PALATIN TECHNOLOGIES, INC.

(Exact name of registrant as specified in its charter)

|

Delaware

|

95-4078884

|

|

|

(State or other jurisdiction of

incorporation or organization)

|

(I.R.S. Employer Identification No.)

|

|

|

4B Cedar Brook Drive

Cranbury, New Jersey

|

08512

|

|

|

(Address of principal executive offices)

|

(Zip Code)

|

(609) 495-2200

(Registrant's telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes xNo o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer o Accelerated filer o

Non-accelerated filer o Smaller reporting company x

(Do not check if a smaller reporting company)

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes oNo x

As of February 10, 2015, 41,540,161 shares of the registrant's common stock, par value $.01 per share, were outstanding.

PALATIN TECHNOLOGIES, INC.

Table of Contents

|

Page

|

|

|

PART I – FINANCIAL INFORMATION

|

|

|

Item 1. Financial Statements (Unaudited)

|

2 |

|

Consolidated Balance Sheets as of December 31, 2014 and June 30, 2014

|

2

|

|

Consolidated Statements of Operations for the Three and Six Months Ended December 31, 2014 and 2013

|

3

|

|

Consolidated Statements of Cash Flows for the Six Months Ended December 31, 2014 and 2013

|

4

|

|

Notes to Consolidated Financial Statements

|

5

|

|

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations

|

11

|

|

Item 3. Quantitative and Qualitative Disclosures About Market Risk

|

16

|

|

Item 4. Controls and Procedures

|

16

|

|

PART II – OTHER INFORMATION

|

|

|

Item 1. Legal Proceedings

|

17

|

|

Item 1A. Risk Factors

|

17

|

|

Item 2. Unregistered Sales of Equity Securities and Use of Proceeds

|

20

|

|

Item 3. Defaults Upon Senior Securities

|

20

|

|

Item 4. Mine Safety Disclosures

|

20

|

|

Item 5. Other Information

|

20

|

|

Item 6. Exhibits

|

20

|

PART I - FINANCIAL INFORMATION

Item 1. Financial Statements.

|

PALATIN TECHNOLOGIES, INC.

|

||||||||

|

and Subsidiary

|

||||||||

|

Consolidated Balance Sheets

|

||||||||

|

(unaudited)

|

||||||||

|

December 31, 2014

|

June 30, 2014

|

|||||||

|

ASSETS

|

||||||||

|

Current assets:

|

||||||||

|

Cash and cash equivalents

|

$ | 42,694,472 | $ | 12,184,605 | ||||

|

Accounts receivable

|

3,035,400 | - | ||||||

|

Prepaid expenses and other current assets

|

1,484,703 | 156,393 | ||||||

|

Total current assets

|

47,214,575 | 12,340,998 | ||||||

|

Property and equipment, net

|

185,563 | 160,748 | ||||||

|

Other assets

|

190,835 | 57,308 | ||||||

|

Total assets

|

$ | 47,590,973 | $ | 12,559,054 | ||||

|

LIABILITIES AND STOCKHOLDERS’ EQUITY

|

||||||||

|

Current liabilities:

|

||||||||

|

Accounts payable

|

$ | 1,914,038 | $ | 261,280 | ||||

|

Accrued expenses

|

3,183,027 | 1,508,958 | ||||||

|

Capital lease obligations

|

25,128 | - | ||||||

|

Deferred revenue

|

- | 1,000,000 | ||||||

|

Total current liabilities

|

5,122,193 | 2,770,238 | ||||||

|

Notes payable, net of discount

|

9,734,509 | - | ||||||

|

Capital lease obligations

|

54,872 | - | ||||||

|

Other non-current libilities

|

4,348 | - | ||||||

|

Total liabilities

|

14,915,922 | 2,770,238 | ||||||

|

Stockholders’ equity:

|

||||||||

|

Preferred stock of $0.01 par value – authorized 10,000,000 shares;

|

||||||||

|

Series A Convertible; issued and outstanding 4,697 shares as of December 31, 2014 and June 30, 2014, respectively

|

47 | 47 | ||||||

|

Common stock of $0.01 par value – authorized 300,000,000 shares;

|

||||||||

|

issued and outstanding 41,540,161 shares as of December 31, 2014 and 39,416,595 as of June 30, 2014, respectively

|

415,401 | 394,166 | ||||||

|

Additional paid-in capital

|

302,721,894 | 283,428,356 | ||||||

|

Accumulated deficit

|

(270,462,291 | ) | (274,033,753 | ) | ||||

|

Total stockholders’ equity

|

32,675,051 | 9,788,816 | ||||||

|

Total liabilities and stockholders’ equity

|

$ | 47,590,973 | $ | 12,559,054 | ||||

The accompanying notes are an integral part of these consolidated financial statements.

2

|

PALATIN TECHNOLOGIES, INC.

|

||||||||||||||||

|

and Subsidiary

|

||||||||||||||||

|

Consolidated Statements of Operations

|

||||||||||||||||

|

(unaudited)

|

||||||||||||||||

|

Three Months Ended December 31,

|

Six Months Ended December 31,

|

|||||||||||||||

|

2014

|

2013

|

2014

|

2013

|

|||||||||||||

|

REVENUES:

|

||||||||||||||||

|

Contract revenue

|

$ | 8,019,415 | $ | - | $ | 12,951,730 | $ | - | ||||||||

|

OPERATING EXPENSES:

|

||||||||||||||||

|

Research and development

|

4,273,571 | 2,630,368 | 7,197,537 | 6,079,508 | ||||||||||||

|

General and administrative

|

1,423,206 | 980,070 | 2,537,667 | 2,023,580 | ||||||||||||

|

Total operating expenses

|

5,696,777 | 3,610,438 | 9,735,204 | 8,103,088 | ||||||||||||

|

Income (loss) from operations

|

2,322,638 | (3,610,438 | ) | 3,216,526 | (8,103,088 | ) | ||||||||||

|

OTHER INCOME (EXPENSE):

|

||||||||||||||||

|

Investment income

|

6,199 | 4,931 | 9,998 | 10,250 | ||||||||||||

|

Interest expense

|

(31,857 | ) | (954 | ) | (33,587 | ) | (2,805 | ) | ||||||||

|

Foreign exchange transaction loss

|

(51,700 | ) | - | (152,983 | ) | - | ||||||||||

|

Total other (expense) income, net

|

(77,358 | ) | 3,977 | (176,572 | ) | 7,445 | ||||||||||

|

Income (loss) before income taxes

|

2,245,280 | (3,606,461 | ) | 3,039,954 | (8,095,643 | ) | ||||||||||

|

Income tax benefit

|

531,508 | - | 531,508 | - | ||||||||||||

|

NET INCOME (LOSS)

|

$ | 2,776,788 | $ | (3,606,461 | ) | $ | 3,571,462 | $ | (8,095,643 | ) | ||||||

|

Basic net income (loss) per common share

|

$ | 0.03 | $ | (0.03 | ) | $ | 0.03 | $ | (0.08 | ) | ||||||

|

Diluted net income (loss) per common share

|

$ | 0.03 | $ | (0.03 | ) | $ | 0.03 | $ | (0.08 | ) | ||||||

|

Weighted average number of common shares outstanding used in computing basic net income (loss) per common share

|

109,314,460 | 106,668,186 | 108,134,179 | 106,638,953 | ||||||||||||

|

Weighted average number of common shares outstanding used in computing diluted net income (loss) per common share

|

109,815,718 | 106,668,186 | 108,888,313 | 106,638,953 | ||||||||||||

The accompanying notes are an integral part of these consolidated financial statements.

3

|

PALATIN TECHNOLOGIES, INC.

|

||||||||

|

and Subsidiary

|

||||||||

|

Consolidated Statements of Cash Flows

|

||||||||

|

(unaudited)

|

||||||||

|

Six Months Ended December 31,

|

||||||||

|

2014

|

2013

|

|||||||

|

CASH FLOWS FROM OPERATING ACTIVITIES:

|

||||||||

|

Net income (loss)

|

$ | 3,571,462 | $ | (8,095,643 | ) | |||

|

Adjustments to reconcile net income (loss) to net cash

|

||||||||

|

provided by (used in) operating activities:

|

||||||||

|

Depreciation and amortization

|

55,185 | 56,568 | ||||||

|

Non-cash interest expense

|

8,486 | - | ||||||

|

Other

|

- | (346 | ) | |||||

|

Stock-based compensation

|

512,390 | 405,629 | ||||||

|

Changes in operating assets and liabilities:

|

||||||||

|

Accounts receivable

|

(3,035,400 | ) | - | |||||

|

Prepaid expenses and other assets

|

(1,255,646 | ) | 32,470 | |||||

|

Accounts payable

|

1,152,758 | (47,734 | ) | |||||

|

Accrued expenses

|

1,412,699 | 456,398 | ||||||

|

Deferred revenue

|

(1,000,000 | ) | 1,000,000 | |||||

|

Net cash provided by (used in) operating activities

|

1,421,934 | (6,192,658 | ) | |||||

|

CASH FLOWS FROM INVESTING ACTIVITIES:

|

||||||||

|

Proceeds from maturity of investments

|

- | 3,750,000 | ||||||

|

Purchases of property and equipment

|

- | (6,239 | ) | |||||

|

Net cash provided by investing activities

|

- | 3,743,761 | ||||||

|

CASH FLOWS FROM FINANCING ACTIVITIES:

|

||||||||

|

Payments on capital lease obligations

|

- | (11,794 | ) | |||||

|

Payment of withholding taxes related to restricted

|

||||||||

|

stock units

|

(122,067 | ) | (25,214 | ) | ||||

|

Proceeds from sale of common stock and

|

||||||||

|

warrants, net of costs

|

19,348,000 | - | ||||||

|

Proceeds from the issuance of notes payable

|

||||||||

|

and warrants

|

10,000,000 | - | ||||||

|

Payment of debt issuance costs

|

(138,000 | ) | - | |||||

|

Net cash provided by (used in) financing activities

|

29,087,933 | (37,008 | ) | |||||

|

NET INCREASE (DECREASE) IN CASH

|

||||||||

|

AND CASH EQUIVALENTS

|

30,509,867 | (2,485,905 | ) | |||||

|

CASH AND CASH EQUIVALENTS, beginning of period

|

12,184,605 | 19,167,632 | ||||||

|

CASH AND CASH EQUIVALENTS, end of period

|

$ | 42,694,472 | $ | 16,681,727 | ||||

|

SUPPLEMENTAL CASH FLOW INFORMATION:

|

||||||||

|

Cash paid for interest

|

$ | 2,601 | $ | 2,805 | ||||

|

Interest accrued on long-term debt

|

22,500 | - | ||||||

|

Equipment acquired under capital lease

|

80,000 | - | ||||||

|

Non-cash equity financing costs in accounts payable

|

490,000 | - | ||||||

|

Non-cash equity financing costs in accrued expenses

|

285,000 | - | ||||||

|

Non-cash debt financing costs in accounts payable

|

10,000 | - | ||||||

|

Non-cash debt financing costs in accrued expenses

|

60,000 | - | ||||||

|

Issuance of warrants in connection with debt financing

|

267,820 | - | ||||||

The accompanying notes are an integral part of these consolidated financial statements.

4

(1) ORGANIZATION:

Nature of Business – Palatin Technologies, Inc. (Palatin or the Company) is a biopharmaceutical company developing targeted, receptor-specific peptide therapeutics for the treatment of diseases with significant unmet medical need and commercial potential. Palatin’s programs are based on molecules that modulate the activity of the melanocortin and natriuretic peptide receptor systems. The melanocortin system is involved in a large and diverse number of physiologic functions, and therapeutic agents modulating this system may have the potential to treat a variety of conditions and diseases, including sexual dysfunction, obesity and related disorders, cachexia (wasting syndrome) and inflammation-related diseases. The natriuretic peptide receptor system has numerous cardiovascular functions, and therapeutic agents modulating this system may be useful in treatment of acute asthma, heart failure, hypertension and other cardiovascular diseases.

The Company’s primary product in development is bremelanotide for the treatment of female sexual dysfunction (FSD). The Company also has drug candidates or development programs for obesity, erectile dysfunction, cardiovascular diseases, pulmonary diseases, inflammatory diseases and dermatologic diseases. The Company has a license, co-development and commercialization agreement with Gedeon Richter Plc. (Gedeon Richter) to commercialize bremelanotide for FSD in Europe and selected countries, and an exclusive global research collaboration and license agreement with AstraZeneca AB (AstraZeneca) to commercialize compounds that target melanocortin receptors for the treatment of obesity, diabetes and related metabolic syndrome.

Key elements of the Company’s business strategy include using its technology and expertise to develop and commercialize innovative therapeutic products; entering into alliances and partnerships with pharmaceutical companies to facilitate the development, manufacture, marketing, sale and distribution of product candidates that the Company is developing; and partially funding its product candidate development programs with the cash flow generated from research collaboration and license agreements and any potential future agreements with third parties.

Business Risk and Liquidity – The Company has incurred cumulative negative cash flows from operations since its inception, and has expended, and expects to continue to expend in the future, substantial funds to complete its planned product development efforts. As shown in the accompanying consolidated financial statements, the Company has an accumulated deficit as of December 31, 2014 of $270.5 million and despite reporting net income for the three and six months ended December 31, 2014 of $2.8 million and $3.6 million, respectively, the Company anticipates incurring additional losses in the future as a result of spending on its development programs. To achieve profitability, if ever, the Company, alone or with others, must successfully develop and commercialize its technologies and proposed products, conduct successful preclinical studies and clinical trials, obtain required regulatory approvals and successfully manufacture and market such technologies and proposed products. The time required to reach profitability is highly uncertain, and there can be no assurance that the Company will be able to achieve profitability on a sustained basis, if at all.

As discussed in Note 9, on December 23, 2014, the Company closed a $20.0 million private placement of 2,050,000 shares of common stock and Series C 2014 warrants to purchase 24,949,325 shares of common stock. The Company also concurrently closed a $10.0 million venture loan led by Horizon Technology Finance Corporation (Horizon), as discussed in Note 8.

During December 2014, the Company initiated its Phase 3 Reconnect Study with bremelanotide for the treatment of FSD, which triggered a development milestone payment of €2.5 million (approximately $3 million) due from Gedeon Richter, which was recorded as license revenue for the three months ended December 31, 2014 and as an account receivable as of December 31, 2014. In addition, $4.9 million of license revenue, which was previously recorded as deferred revenue, was recognized as license revenue in the three months ended December 31, 2014 upon the initiation of the Phase 3 clinical trials when such portion became non-refundable per the agreement, as discussed in Note 6.

As of December 31, 2014, the Company’s cash and cash equivalents were $42.7 million and accounts receivable were $3.0 million. The Company intends to utilize existing capital resources for general corporate purposes and working capital, including the Phase 3 clinical trial program with bremelanotide for FSD and preclinical and clinical development of our other product candidates and programs, including PL-3994 and melanocortin receptor-1 and melanocortin receptor-4 programs. Management believes that the Phase 3 clinical trial program with bremelanotide, including regulatory filings for product approval, will cost at least $80.0 million.

Management believes that the Company’s existing capital resources will be adequate to fund its currently planned operations through the quarter ending March 31, 2016.

Concentrations – Concentrations in the Company’s assets and operations subject it to certain related risks. Financial instruments that subject the Company to concentrations of credit risk primarily consist of cash and cash equivalents. The Company’s cash and cash equivalents are primarily in one money market fund sponsored by a large financial institution. For the three and six months ended December 31, 2014, 100% of revenues were from Gedeon Richter. For the three and six months ended December 31, 2013, the Company had no revenues.

5

(2) BASIS OF PRESENTATION:

The accompanying unaudited consolidated financial statements have been prepared in accordance with U.S. generally accepted accounting principles for interim financial information and with the instructions to Form 10-Q. Accordingly, they do not include all of the information and footnote disclosures required to be presented for complete financial statements. In the opinion of management, these consolidated financial statements contain all adjustments (consisting of normal recurring adjustments) considered necessary for fair presentation. The results of operations for the three and six months ended December 31, 2014 may not necessarily be indicative of the results of operations expected for the full year, except that the Company expects to incur a significant loss for the fiscal year ending June 30, 2015.

The accompanying consolidated financial statements should be read in conjunction with the audited consolidated financial statements and notes thereto included in the Company’s annual report on Form 10-K for the year ended June 30, 2014, filed with the Securities and Exchange Commission (SEC), which includes consolidated financial statements as of June 30, 2014 and 2013 and for each of the fiscal years in the three-year period ended June 30, 2014.

(3) SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES:

Principles of Consolidation – The consolidated financial statements include the accounts of Palatin and its wholly-owned inactive subsidiary. All significant intercompany accounts and transactions have been eliminated in consolidation.

Use of Estimates – The preparation of consolidated financial statements in conformity with U.S. generally accepted accounting principles (GAAP) requires management to make estimates and assumptions that affect the reported amount of assets and liabilities and disclosure of contingent assets and liabilities at the date of the consolidated financial statements and the reported amounts of revenues and expenses during the reporting period. Actual results could differ from those estimates.

Cash and Cash Equivalents – Cash and cash equivalents include cash on hand, cash in banks and all highly liquid investments with a purchased maturity of less than three months. Cash equivalents consist of $40,036,076 and $9,495,656 in a money market fund at December 31, 2014 and June 30, 2014, respectively.

Fair Value of Financial Instruments – The Company’s financial instruments consist primarily of cash equivalents, accounts receivable, accounts payable, and notes payable. Management believes that the carrying value of current assets and current liabilities are representative of their respective fair values based on the short-term nature of these instruments. Management believes that the carrying amount of its notes payable approximates fair value based on the terms of the notes.

Property and Equipment – Property and equipment consists of office and laboratory equipment, office furniture and leasehold improvements and includes assets acquired under capital leases. Property and equipment are recorded at cost. Depreciation is recognized using the straight-line method over the estimated useful lives of the related assets, generally five years for laboratory and computer equipment, seven years for office furniture and equipment and the lesser of the term of the lease or the useful life for leasehold improvements. Amortization of assets acquired under capital leases is included in depreciation expense. Maintenance and repairs are expensed as incurred while expenditures that extend the useful life of an asset are capitalized.

Impairment of Long-Lived Assets – The Company reviews its long-lived assets for impairment whenever events or changes in circumstances indicate that the carrying amount of the assets may not be fully recoverable. To determine recoverability of a long-lived asset, management evaluates whether the estimated future undiscounted net cash flows from the asset are less than its carrying amount. If impairment is indicated, the long-lived asset would be written down to fair value. Fair value is determined by an evaluation of available price information at which assets could be bought or sold, including quoted market prices if available, or the present value of the estimated future cash flows based on reasonable and supportable assumptions.

Deferred Rent – The Company’s operating leases provide for rent increases over the terms of the leases. Deferred rent consists of the difference between periodic rent payments and the amount recognized as rent expense on a straight-line basis, as well as tenant allowances for leasehold improvements. Rent expenses are being recognized ratably over the terms of the leases.

Revenue Recognition – Under our license, co-development and commercialization agreement with Gedeon Richter (Note 6), we may be entitled to receive consideration in the form of license fees, regulatory milestone payments, sales milestone payments, and royalties.

Revenue resulting from license fees is recognized upon delivery of the license for the portion of the license fee payment that is non-contingent and non-refundable, if the license has standalone value. Revenue resulting from the achievement of development milestones is recorded in accordance with the accounting guidance for the milestone method of revenue recognition. Revenue resulting from the achievement of sales milestone events is recognized when the milestone is achieved. Revenue from royalties is recorded when earned.

Research and Development Costs – The costs of research and development activities are charged to expense as incurred, including the cost of equipment for which there is no alternative future use.

Accrued Expenses – Third parties perform a significant portion of our development activities. We review the activities performed under significant contracts each quarter and accrue expenses and the amount of any reimbursement to be received from our collaborators based upon the estimated amount of work completed. Estimating the value or stage of completion of certain services requires judgment based on available information.

6

Stock-Based Compensation – The Company charges to expense the fair value of stock options and other equity awards granted. The Company determines the value of stock options utilizing the Black-Scholes option pricing model. Compensation costs for share-based awards with pro rata vesting are allocated to periods on a straight-line basis.

Income Taxes – The Company and its subsidiary file consolidated federal and separate-company state income tax returns. Income taxes are accounted for under the asset and liability method. Deferred tax assets and liabilities are recognized for the future tax consequences attributable to differences between the financial statement carrying amounts of assets and liabilities and their respective tax basis and operating loss and tax credit carryforwards. Deferred tax assets and liabilities are measured using enacted tax rates expected to apply to taxable income in the years in which those temporary differences or operating loss and tax credit carryforwards are expected to be recovered or settled. The effect on deferred tax assets and liabilities of a change in tax rates is recognized in the period that includes the enactment date. The Company has recorded a valuation allowance against its deferred tax assets based on the history of losses incurred.

During the three and six months ended December 31, 2014, the Company sold New Jersey state net operating loss (NJ NOL) carryforwards, which resulted in the recognition of $531,508 in tax benefits.

Net Income (Loss) per Common Share – Basic and diluted earnings per common share (EPS) are calculated in accordance with the provisions of Financial Accounting Standards Board (FASB) Accounting Standards Codification (ASC) Topic 260, “Earnings per Share,” which includes guidance pertaining to the warrants, issued in connection with the July 3, 2012 and December 23, 2014 private placement offerings, that are exercisable for nominal consideration and, therefore, are to be considered in the computation of basic and diluted net income (loss) per common share. The Series A 2012 warrants to purchase up to 31,988,151 shares of common stock were exercisable starting at July 3, 2012 and, therefore, are included in the weighted average number of common shares outstanding used in computing basic and diluted net income (loss) per common share starting on July 3, 2012.

The Series B 2012 warrants to purchase up to 35,488,380 shares of common stock were considered contingently issuable shares and were not included in computing basic net loss per common share until the Company received stockholder approval for the increase in authorized underlying common stock on September 27, 2012. For diluted EPS, contingently issuable shares are to be included in the calculation as of the beginning of the period in which the conditions were satisfied, unless the effect would be anti-dilutive. The Series B 2012 warrants have been excluded from the calculation of diluted net loss per common share during the period from July 3, 2012 until September 27, 2012 as the impact would be anti-dilutive.

The Series C 2014 warrants to purchase up to 24,949,325 shares of common stock were exercisable starting at December 23, 2014 and, therefore, are included in the weighted average number of common shares outstanding used in computing basic and diluted net income (loss) per common share starting on December 23, 2014.

The following table is a reconciliation of net income (loss) and the shares used in calculating basic and diluted net income (loss) per common share for the three and six months ended December 31, 2014 and 2013:

|

Three Months Ended December 31,

|

Six Months Ended December 31,

|

|||||||||||||||

|

2014

|

2013

|

2014

|

2013

|

|||||||||||||

|

Numerator:

|

||||||||||||||||

|

Net income (loss)

|

$ | 2,776,788 | $ | (3,606,461 | ) | $ | 3,571,462 | $ | (8,095,643 | ) | ||||||

|

Denominator:

|

||||||||||||||||

|

Weighted average common shares outstanding - Basic

|

109,314,460 | 106,668,186 | 108,134,179 | 106,638,953 | ||||||||||||

|

Effect of dilutive shares:

|

||||||||||||||||

|

Common stock equivalents arising from stock options and warrants

|

346,867 | - | 560,572 | - | ||||||||||||

|

Restriced stock units

|

154,391 | - | 193,562 | - | ||||||||||||

|

Weighted average common shares outstanding - Diluted

|

109,815,718 | 106,668,186 | 108,888,313 | 106,638,953 | ||||||||||||

|

Net income (loss) per common share:

|

||||||||||||||||

|

Basic

|

$ | 0.03 | $ | (0.03 | ) | $ | 0.03 | $ | (0.08 | ) | ||||||

|

Diluted

|

$ | 0.03 | $ | (0.03 | ) | $ | 0.03 | $ | (0.08 | ) | ||||||

For the periods ended December 31, 2014 and 2013, common shares issuable upon conversion of Series A Convertible Preferred Stock, the exercise of outstanding options and warrants (excluding the Series A 2012, Series B 2012 and Series C 2014 warrants issued in connection with the July 3, 2012 and December 23, 2014 private placement offerings as such warrants are already included in weighted average number of common shares outstanding used in computing basic net income (loss) per common share since they are exercisable for nominal consideration), and the vesting of restricted stock units amounted to an aggregate of 29,378,689 and 28,657,356 shares, respectively, and are excluded in the weighted average number of common shares outstanding used in computing basic net income (loss) per common share. For the three and six months ended December 31, 2014, an additional 501,258 and 754,134, respectively, of common shares have been included in the computation of diluted EPS using the treasury stock method. However, for the three and six months ended December 31, 2013, no additional common shares were added in the computation of diluted EPS because to do so would have been anti-dilutive for these periods.

7

(4) NEW AND RECENTLY ADOPTED ACCOUNTING PRONOUNCEMENTS:

In August 2014, the FASB issued ASU No. 2014-15, “Presentation of Financial Statements-Going Concern: Disclosures of Uncertainties about an Entity’s Ability to Continue as a Going Concern.” The amendments in this update provide guidance in GAAP about management's responsibility to evaluate whether there is substantial doubt about an entity's ability to continue as a going concern and to provide related footnote disclosures. In doing so, the amendments should reduce diversity in the timing and content of footnote disclosures. The new standard is effective for the Company for its fiscal year ending June 30, 2017. The Company is evaluating the effect of the standard, if any, on its financial statements.

In May 2014, the FASB issued ASU No. 2014-09, “Revenue from Contracts with Customers,” which requires an entity to recognize the amount of revenue to which it expects to be entitled for the transfer of promised goods or services to customers. The ASU will replace most existing revenue recognition guidance in U.S. GAAP when it becomes effective. The new standard is effective for the Company on July 1, 2017. Early application is not permitted. The standard permits the use of either the retrospective or cumulative effect transition method. The Company is evaluating the effect that ASU 2014-09 will have on its consolidated financial statements and related disclosures. The Company has not yet determined the effect of the standard on its ongoing financial reporting.

(5) AGREEMENT WITH ASTRAZENECA:

In January 2007, the Company entered into an exclusive global research collaboration and license agreement with AstraZeneca to discover, develop and commercialize compounds that target melanocortin receptors for the treatment of obesity, diabetes and related metabolic syndrome. In June 2008, the license agreement was amended to include additional compounds and associated intellectual property developed by the Company. In December 2008, the license agreement was further amended to include additional compounds and associated intellectual property developed by the Company and extended the research collaboration for an additional year through January 2010. In September 2009, the license agreement was further amended to modify royalty rates and milestone payments. The collaboration is based on the Company’s melanocortin receptor obesity program and includes access to compound libraries, core technologies and expertise in melanocortin receptor drug discovery and development. As part of the September 2009 amendment to the research collaboration and license agreement, the Company agreed to conduct additional studies on the effects of melanocortin receptor specific compounds on food intake, obesity and other metabolic parameters.

In December 2009 and 2008, the Company also entered into clinical trial sponsored research agreements with AstraZeneca, under which the Company agreed to conduct studies of the effects of melanocortin receptor specific compounds on food intake, obesity and other metabolic parameters. Under the terms of these clinical trial agreements, AstraZeneca paid the Company $5,000,000 as of March 31, 2009 upon achieving certain objectives and paid all costs associated with these studies.

The Company received an up-front payment of $10,000,000 from AstraZeneca on execution of the research collaboration and license agreement. Under the September 2009 amendment the Company was paid an additional $5,000,000 in consideration of reduction of future milestones and royalties and providing specific materials to AstraZeneca. The Company is now eligible for milestone payments totaling up to $145,250,000, with up to $85,250,000 contingent on development and regulatory milestones and the balance contingent on achievement of sales targets. In addition, the Company is eligible to receive mid to high single digit royalties on sales of any approved products. AstraZeneca assumed responsibility for product commercialization, product discovery and development costs, with both companies contributing scientific expertise in the research collaboration. The Company provided research services to AstraZeneca through January 2010, the expiration of the research collaboration portion of the research collaboration and license agreement, at a contractual rate per full-time-equivalent employee.

AstraZeneca is evaluating its program and next steps. No assurance can be given that AstraZeneca will continue to develop compounds that target melanocortin receptors for the treatment of obesity, diabetes and related metabolic syndrome, or that AstraZeneca will be successful in developing any such compound.

(6) AGREEMENT WITH GEDEON RICHTER:

In August 2014, the Company entered into a license, co-development and commercialization agreement with Gedeon Richter on bremelanotide for FSD in Europe and selected countries. The Company has the potential to receive up to €80 million ($97.1 million as of December 31, 2014) in regulatory and sales related milestones, and will receive low double-digit royalties on net sales in the licensed territory. Under the agreement, the Company will contribute, with Gedeon Richter, to the costs of co-development activities for obtaining regulatory approval in Europe. Gedeon Richter will exclusively market bremelanotide for FSD in the licensed territory, and will be responsible for all sales, marketing and commercial activities, including associated costs, in the licensed territory. The agreement remains in effect as long as Gedeon Richter is selling bremelanotide on which a royalty is owed. The agreement may be terminated by either party upon notice in the event of a material breach or insolvency. In the event Gedeon Richter terminates the agreement because the Company breached the agreement or is insolvent, Gedeon Richter’s license becomes fully paid-up, royalty free, perpetual and irrevocable. In the event that the Company terminates the agreement because Gedeon Richter breached the agreement or is insolvent, upon timely request, all regulatory approvals for bremelanotide in the licensed territory will be transferred to the Company or its designee.

8

The Company views the delivery of the license for bremelanotide as a revenue generating activity that is part of its ongoing and central operations. The other elements of the agreement with Gedeon Richter are considered non-revenue activities associated with the collaborative arrangement. The Company believes the license has standalone value from the other elements of the collaborative arrangement because it conveys all of the rights necessary to develop and commercialize bremelanotide in the licensed territory.

In August 2013, the Company received an initial payment of $1.0 million from Gedeon Richter as a non-refundable option fee on the license, co-development and commercialization agreement, and in September 2014, the Company received €6.7 ($8.8 million) on execution of the definitive agreement. During the six months ended December 31, 2014, the upfront payment of €7.5 million ($9.8 million) was recorded as license revenue in the consolidated statements of operations, of which $4.9 million was recorded in the three months ended September 30, 2014 for the non-refundable and non-contingent portion of the license fee and $4.9 million was recorded in the three months ended December 31, 2014 upon the initiation of the Phase 3 clinical trials when such portion became non-refundable per the agreement. During the three months ended December 31, 2014, the Company recorded revenue related to a milestone payment due of €2.5 million ($3.1 million) upon the initiation of the Company’s Phase 3 clinical trial program in the United States, which the Company initiated in December 2014.

As a result of fluctuations in the conversion rates between the Euro and the U.S. Dollar between the transaction dates and the settlement dates, the Company has recorded a foreign exchange loss of $51,700 and $152,983 for the three and six months ended December 31, 2014, respectively.

(7) FAIR VALUE MEASUREMENTS:

The fair value of cash equivalents and short-term investments are classified using a hierarchy prioritized based on inputs. Level 1 inputs are quoted prices (unadjusted) in active markets for identical assets or liabilities. Level 2 inputs are quoted prices for similar assets and liabilities in active markets or inputs that are observable for the asset or liability, either directly or indirectly through market corroboration, for substantially the full term of the financial instrument. Level 3 inputs are unobservable inputs based on management’s own assumptions used to measure assets and liabilities at fair value. A financial asset or liability’s classification within the hierarchy is determined based on the lowest level input that is significant to the fair value measurement.

The following table provides the assets carried at fair value:

|

Carrying Value

|

Quoted prices in

active markets

(Level 1)

|

Other quoted/observable inputs (Level 2)

|

Significant unobservable inputs

(Level 3)

|

|||||||||||||

|

December 31, 2014:

|

|

|

|

|||||||||||||

|

Money Market Fund

|

$ | 40,036,076 | $ | 40,036,076 | $ | - | $ | - | ||||||||

|

June 30, 2014:

|

||||||||||||||||

|

Money Market Fund

|

$ | 9,495,656 | $ | 9,495,656 | $ | - | $ | - | ||||||||

(8) NOTES PAYABLE:

Notes payable consist of the following:

|

December 31, 2014

|

||||

|

Notes payable under venture loan

|

$ | 10,000,000 | ||

|

Less unamortized related debt discount

|

(265,491 | ) | ||

|

Notes payable, net of discount

|

$ | 9,734,509 | ||

9

On December 23, 2014, the Company closed on a $10.0 million venture loan which was led by Horizon. The debt facility is a four year senior secured term loan that bears interest at a floating coupon rate of one-month LIBOR (floor of 0.50%) plus 8.50%, and provides for interest-only payments for the first eighteen months followed by monthly payments of principal payments of $333,333 plus accrued interest through January 1, 2019. The lenders also received five-year immediately exercisable Series D 2014 warrants to purchase 666,666 shares of common stock exercisable at an exercise price of $0.75 per share. The Company recorded a debt discount of $267,820 equal to the fair value of these warrants at issuance, which is being amortized to interest expense over the term of the related debt. This debt discount is offset against the note payable balance and included in additional paid-in capital on the Company’s balance sheet at December 31, 2014. In addition, a final incremental payment equal to $500,000 is due on January 1, 2019, or upon early repayment of the loan. This final incremental payment is being accreted to interest expense over the term of the related debt. The Company incurred $208,000 of costs in connection with the Loan Agreement. These costs were capitalized as deferred financing costs and are being amortized to interest expense over the term of the related debt. In addition, if the Company repays all or a portion of the loan prior to the applicable maturity date, it will pay the lenders a prepayment penalty fee, based on a percentage of the then outstanding principal balance, equal to 3% if the prepayment occurs on or before 18 months after the funding date thereof or 1% if the prepayment occurs more than 18 months after, but on or before 30 months after, the funding date.

The Company’s obligations under the Loan Agreement are secured by a first priority security interest in substantially all of its assets other than its intellectual property. The Company also has agreed to specified limitations on pledging or otherwise encumbering its intellectual property assets.

The Loan Agreement includes customary affirmative and restrictive covenants, but does not include any covenants to attain or maintain certain financial metrics, and also includes customary events of default, including payment defaults, breaches of covenants, change of control and a material adverse change default. Upon the occurrence of an event of default and following any applicable cure periods, a default interest rate of an additional 5% may be applied to the outstanding loan balances, and the lenders may declare all outstanding obligations immediately due and payable and take such other actions as set forth in the Loan Agreement.

(9) STOCKHOLDERS’ EQUITY:

Common Stock Transactions – On December 23, 2014, the Company closed on a private placement offering in which the Company sold, for aggregate proceeds of $20.0 million, 2,050,000 shares of its common stock and Series C 2014 warrants to purchase up to 24,949,325 shares of common stock. Funds under the management of QVT Financial LP (QVT) invested $10 million and an unrelated accredited investment fund invested $10 million. The funds paid $0.75 for each share of common stock and $0.74 for each Series C 2014 warrant, resulting in gross proceeds to Palatin of $20 million, with net proceeds, after deducting estimated offering expenses, of approximately $18.6 million. The Series C 2014 warrants, which may be exercised on a cashless basis, are exercisable immediately upon issuance at an initial exercise price of $0.01 per share and expire on the tenth anniversary of the date of issuance. The Series C 2014 warrants are subject to limitation on exercise if QVT and its affiliates would beneficially own more than 9.99% (4.99% for the other accredited investment fund holder) of the total number of Palatin’s shares of common stock following such exercise.

The purchase agreement for the private placement provides that the purchasers have certain rights until the earlier of approval of bremelanotide for FSD by the U.S. Food and Drug Administration and December 23, 2018, including rights of first refusal and participation in any subsequent equity or debt financing. The purchase agreement also contains certain restrictive covenants so long as the funds continue to hold specified amounts of warrants or beneficially own specified amounts of the outstanding shares of common stock.

Stock Options – In June 2014, the Company granted 325,000 options to its executive officers, 143,400 options to its employees and 135,000 options to its non-employee directors under the Company’s 2011 Stock Incentive Plan. The Company is amortizing the fair value of these options of $265,726, $117,247 and $97,530, respectively, over the vesting period. The Company recognized $46,523 and $93,046 of stock-based compensation expense related to these options during the three and six months ended December 31, 2014, respectively.

In June 2013, the Company granted 525,000 options to its executive officers, 394,300 options to its employees and 270,000 options to its non-employee directors under the Company’s 2011 Stock Incentive Plan. The Company is amortizing the fair value of these options of $287,000, $204,000 and $148,000, respectively, over the vesting period. The Company recognized $23,882 and $47,763 of stock-based compensation expense related to these options during the three and six months ended December 31, 2014, respectively, and $67,155 and $133,353 during the three and six months ended December 31, 2013, respectively.

In July 2012, the Company granted 285,000 options to its executive officers, 182,500 options to its employees and 112,500 options to its non-employee directors under the Company’s 2011 Stock Incentive Plan. The Company is amortizing the fair value of these options of $182,000, $108,000 and $72,000, respectively, over the vesting period. The Company recognized $14,096 and $28,192 of stock-based compensation expense related to these options during the three and six months ended December 31, 2014, respectively, and $17,638 and $34,778 for the three and six months ended December 31, 2013, respectively.

10

Stock options granted to the Company’s executive officers and employees vest over a 48 month period, while stock options granted to its non-employee directors vest over a 12 month period.

Restricted Stock Units – In June 2014, the Company granted 325,000 restricted stock units to its executive officers, 143,400 restricted stock units to its employees and 135,000 restricted stock units to its non-employee directors under the Company’s 2011 Stock Incentive Plan. The Company is amortizing the fair value of these restricted stock units of $331,500, $146,268 and $137,700, respectively, over the vesting period. Restricted stock units granted to the Company’s executive officers, employees and non-employee directors in 2014 vest over 24 months, 48 months and 12 months, respectively. The Company recognized $115,627 and $231,253 of stock-based compensation expense related to these restricted stock units during the three and six months ended December 31, 2014, respectively.

In June 2013, the Company granted 420,000 restricted stock units to its executive officers and 115,000 restricted stock units to its employees under the Company’s 2011 Stock Incentive Plan. The Company is amortizing the fair value of these restricted stock units of $260,000 and $71,000, respectively, over the 24 month vesting period ending June 2015. The Company recognized $18,794 and $37,587 of stock-based compensation expense related to these restricted stock units during the three and six months ended December 31, 2014, respectively, and $62,194 and $124,388 during the three and six months ended December 31, 2013, respectively.

In July 2012, the Company granted 222,500 restricted stock units to its executive officers under the Company’s 2011 Stock Incentive Plan. The Company has amortized the fair value of these restricted stock units of $160,000 over the 24 months ended July 2014. The Company recognized $10,012 and $23,685 for the three and six months ended December 31, 2013, respectively.

Stock-based compensation cost for the three and six months ended December 31, 2014 for stock options and equity-based instruments issued other than the stock options and restricted stock units described above was $40,997 and $74,549, respectively, and $44,994 and $89,425 for the three and six months ended December 31, 2013, respectively.

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations.

The following discussion and analysis should be read in conjunction with the consolidated financial statements and notes to the consolidated financial statements filed as part of this report and the audited consolidated financial statements and notes thereto included in our annual report on Form 10-K for the year ended June 30, 2014.

Statements in this quarterly report on Form 10-Q, as well as oral statements that may be made by us or by our officers, directors, or employees acting on our behalf, that are not historical facts constitute “forward-looking statements”, which are made pursuant to the safe harbor provisions of Section 21E of the Securities Exchange Act of 1934, as amended (the Exchange Act). The forward-looking statements in this quarterly report on Form 10-Q do not constitute guarantees of future performance. Investors are cautioned that statements that are not strictly historical statements contained in this quarterly report on Form 10-Q, including, without limitation, the following are forward looking statements:

|

●

|

estimates of our expenses, future revenue, capital requirements;

|

|

●

|

our ability to obtain additional financing on terms acceptable to us, or at all;

|

|

●

|

our ability to advance product candidates into, and successfully complete, clinical trials;

|

|

●

|

the initiation, timing, progress and results of future preclinical studies and clinical trials, and our research and development programs;

|

|

●

|

the timing or likelihood of regulatory filings and approvals;

|

|

●

|

our expectations regarding the results and the timing of results in our Phase 3 clinical trials of bremelanotide for FSD;

|

11

|

●

|

our expectation regarding the timing of our regulatory submissions for approval of bremelanotide for FSD in the United States and Europe;

|

|

●

|

the potential for commercialization of bremelanotide for FSD and other product candidates, if approved, by us;

|

|

●

|

our expectations regarding the potential market size and market acceptance for bremelanotide for FSD and our other product candidates, if approved for commercial use;

|

|

●

|

our ability to compete with other products and technologies similar to our product candidates;

|

|

●

|

the ability of our third-party collaborators to timely carry out their duties under their agreements with us;

|

|

●

|

the ability of our contract manufacturers to perform their manufacturing activities for us in compliance with applicable regulations;

|

|

●

|

our ability to recognize the potential value of our licensing arrangements with third parties;

|

|

●

|

the potential to achieve revenues from the sale of our product candidates;

|

|

●

|

our ability to obtain adequate reimbursement from Medicare, Medicaid, private insurers and other healthcare payers;

|

|

●

|

our ability to maintain product liability insurance at a reasonable cost or in sufficient amounts, if at all;

|

|

●

|

the retention of key management, employees and third-party contractors;

|

|

●

|

the scope of protection we are able to establish and maintain for intellectual property rights covering our product candidates and technology;

|

|

●

|

our compliance with federal and state laws and regulations;

|

|

●

|

the timing and costs associated with obtaining regulatory approval for our product candidates;

|

|

●

|

the impact of legislative or regulatory healthcare reforms in the United States;

|

|

●

|

our ability to adapt to changes in global economic conditions; and

|

|

●

|

our ability to remain listed on the NYSE MKT.

|

12

Such forward-looking statements involve known and unknown risks, uncertainties and other factors that could cause our actual results to be materially different from historical results or from any results expressed or implied by such forward-looking statements. Our future operating results are subject to risks and uncertainties and are dependent upon many factors, including, without limitation, the risks identified in this report, in our annual report on Form 10-K for the year ended June 30, 2014, and in our other Securities and Exchange Commission (SEC) filings.

We expect to incur losses in the future as a result of spending on our planned development programs and results may fluctuate significantly from quarter to quarter.

In this quarterly report on Form 10-Q, references to “we”, “our”, “us” or “Palatin” means Palatin Technologies, Inc. and its subsidiary.

Critical Accounting Policies and Estimates

Our significant accounting policies, which are described in the notes to our consolidated financial statements included in this report and in our annual report on Form 10-K for the year ended June 30, 2014, have not changed as of December 31, 2014. We believe that our accounting policies and estimates relating to revenue recognition, accrued expenses and stock-based compensation are the most critical.

Overview

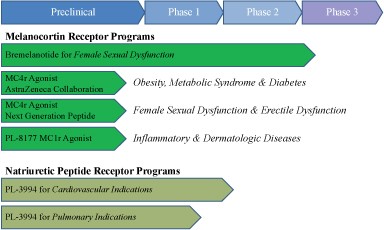

We are a biopharmaceutical company developing targeted, receptor-specific peptide therapeutics for the treatment of diseases with significant unmet medical need and commercial potential. Our programs are based on molecules that modulate the activity of the melanocortin and natriuretic peptide receptor systems. Our primary product in clinical development is a combination drug-device product for the delivery of bremelanotide for the treatment of female sexual dysfunction, or FSD. In addition, we have drug candidates or development programs for obesity, erectile dysfunction, cardiovascular diseases, pulmonary diseases, inflammatory diseases and dermatologic diseases.

The following drug development programs are actively under development:

|

●

|

Bremelanotide, an on-demand subcutaneous injectable peptide melanocortin receptor agonist, for treatment of FSD in premenopausal women. Bremelanotide, which is a melanocortin agonist (a compound which binds to a cell receptor and activates a response), is a synthetic peptide analog of the naturally occurring hormone alpha-MSH (melanocyte-stimulating hormone). The novel mechanism of action involves activating endogenous melanocortin hormone pathways involved in sexual arousal response. Phase 3 clinical trials were initiated in December 2014;

|

|

●

|

Melanocortin receptor-4, or MC4r, compounds for treatment of obesity and diabetes in collaboration with AstraZeneca pursuant to our research collaboration and license agreement. Results of our studies involving MC4r peptides suggest that certain of these peptides may have significant commercial potential for treatment of conditions responsive to MC4r activation, including FSD, erectile dysfunction, obesity and diabetes;

|

|

●

|

PL-3994, a peptide mimetic natriuretic peptide receptor A, or NPR-A, agonist, for treatment of cardiovascular and pulmonary indications. PL-3994 is our lead natriuretic peptide receptor product candidate, and is a synthetic mimetic of the neuropeptide hormone ANP. PL-3994 is in development for treatment of heart failure, acute exacerbations of asthma and refractory hypertension; and

|

|

●

|

Melanocortin receptor-1, or MC1r, agonist peptides, for treatment of inflammatory and dermatologic disease indications. Our MC1r peptide drug candidates are highly specific, with substantially greater binding and efficacy at MC1r than at other melanocortin receptors. We have selected one of our MC1r peptide drug candidates, designated PL-8177, as a clinical trial candidate.

|

The following chart shows the status of our drug development programs.

13

We are developing subcutaneously administered bremelanotide for the treatment of FSD in premenopausal women. Bremelanotide, which is a melanocortin agonist, is a synthetic peptide analog of the naturally occurring hormone alpha-MSH. The novel mechanism of action involves activating endogenous melanocortin hormone pathways involved in sexual arousal response. We have completed a Phase 2B clinical trial and meetings with the U.S. Food and Drug Administration (FDA), and started patient enrollment in the Phase 3 clinical trials in December 2014. The Phase 3 studies, which will be conducted in North America, will utilize a single-dose autoinjector intended for commercialization. It is anticipated that the Phase 3 program will take at least fifteen to eighteen months from initiation of patient dosing through database lock. Following database lock, clinical trial data will be analyzed and, assuming the data supports approval of bremelanotide for FSD, a New Drug Application (NDA) will be submitted to FDA. There can be no assurance that the Phase 3 data will support approval of bremelanotide for FSD or that the FDA will approve an NDA for bremelanotide.

Key elements of our business strategy include:

|

●

|

Using our technology and expertise to develop and commercialize products in our active drug development programs;

|

|

●

|

Entering into strategic alliances and partnerships with pharmaceutical companies to facilitate the development, manufacture, marketing, sale and distribution of product candidates that we are developing;

|

|

●

|

Partially funding our product development programs with the cash flow generated from research collaboration and license agreements and any potential future agreements with third parties; and

|

|

●

|

Completing development and seeking regulatory approval of bremelanotide for FSD and our other product candidates.

|

We incorporated in Delaware in 1986 and commenced operations in the biopharmaceutical area in 1996. Our corporate offices are located at 4B Cedar Brook Drive, Cranbury, New Jersey 08512 and our telephone number is (609) 495-2200. We maintain an Internet site at http://www.palatin.com, where among other things, we make available free of charge on and through this website our Forms 3, 4 and 5, proxy statements, annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d), Section 14A and Section 16 of the Exchange Act as soon as reasonably practicable after we electronically file such material with, or furnish it to, the SEC. Our website and the information contained in it or connected to it are not incorporated into this quarterly report on Form 10-Q.

14

Results of Operations

Three and Six Months Ended December 31, 2014 Compared to the Three and Six Months Ended December 31, 2013

Revenue – For the three and six months ended December 31, 2014, we recognized $8.0 million and $12.9 million, respectively, in revenue pursuant to our license, co-development and commercialization agreement with Gedeon Richter. We recognized no revenue for the three and six months ended December 31, 2013.

In August 2014, we entered into a license, co-development and commercialization agreement with Gedeon Richter, which provided for $9.8 million in upfront payments. The non-refundable portion of the upfront payment, $4.9 million, was recorded as revenue in the three months ended September 30, 2014 and the remaining balance was recorded as revenue in the three months ended December 31, 2014, which became non-refundable upon initiation of our Phase 3 clinical trial program in the United States. We also recognized $3.1 million in the three months ended December 31, 2014 relating to the milestone payment due upon initiation of our Phase 3 clinical trial program in the United States, which was initiated in December 2014.

Research and Development – Research and development expenses were $4.3 million and $7.2 million, respectively, for the three and six months ended December 31, 2014 compared to $2.6 million and $6.1 million, respectively, for the three and six months ended December 31, 2013. These costs primarily relate to our bremelanotide Phase 3 clinical trial program.

Research and development expenses related to our bremelanotide, PL-3994, peptide melanocortin agonist, obesity and other preclinical programs were $3.7 million and $6.1 million, respectively, for the three and six months ended December 31, 2014 compared to $1.9 million and $4.7 million, respectively, for the three and six months ended December 31, 2013. Spending to date has been primarily related to our bremelanotide for the treatment of FSD program. We initiated the pivotal Phase 3 studies of bremelanotide in December 2014. The amount of such spending and the nature of future development activities are dependent on a number of factors, including primarily the availability of funds to support future development activities, success of our clinical trials and preclinical and discovery programs, and our ability to progress compounds in addition to bremelanotide and PL-3994 into human clinical trials.

The amounts of project spending above exclude general research and development spending, which consists mainly of compensation and related costs, and which were $0.6 million and $1.1 million, respectively, for the three and six months ended December 31, 2014 compared to $0.7 million and $1.4 million, respectively, for the three and six months ended December 31, 2013.

Cumulative spending from inception to December 31, 2014 is approximately $178.8 million for our bremelanotide program and approximately $122.3 million on all our other programs (which include PL-3994, other melanocortin receptor agonists, obesity, other discovery programs and terminated programs). Due to various risk factors described in our periodic filings with the SEC, including the difficulty in currently estimating the costs and timing of future Phase 1 clinical trials and larger-scale Phase 2 and Phase 3 clinical trials for any product under development, we cannot predict with reasonable certainty when, if ever, a program will advance to the next stage of development or be successfully completed, or when, if ever, net cash inflows will be generated.

General and Administrative – General and administrative expenses, which consist mainly of compensation and related costs, were $1.4 million and $2.5 million, respectively, for the three and six months ended December 31, 2014 compared to $1.0 million and $2.0 million, respectively, for the three and six months ended December 31, 2013.

15

Liquidity and Capital Resources

Since inception, we have incurred net operating losses, primarily related to spending on our research and development programs. We have financed our net operating losses primarily through debt and equity financings and amounts received under collaborative agreements.

Our product candidates are at various stages of development and will require significant further research, development and testing and some may never be successfully developed or commercialized. We may experience uncertainties, delays, difficulties and expenses commonly experienced by early stage biopharmaceutical companies, which may include unanticipated problems and additional costs relating to:

|

●

|

the development and testing of products in animals and humans;

|

|

●

|

product approval or clearance;

|

|

●

|

regulatory compliance;

|

|

●

|

good manufacturing practices (GMPs);

|

|

●

|

intellectual property rights;

|

|

●

|

product introduction;

|

|

●

|

marketing, sales and competition; and

|

|

●

|

obtaining sufficient capital.

|

Failure to enter into collaboration agreements and obtain timely regulatory approval for our product candidates and indications would impact our ability to increase revenues and could make it more difficult to attract investment capital for funding our operations. Any of these possibilities could materially and adversely affect our operations and require us to curtail or cease certain programs.

During the six months ended December 31, 2014, cash provided by operating activities was $1.4 million, compared to cash used for operating activities of $6.2 million for the six months ended December 31, 2013. The difference for the six months ended December 31, 2014 and 2013 was primarily attributable to the upfront payment relating to the license, co-development and commercialization agreement with Gedeon Richter. Our periodic accounts payable and accrued expenses balances will continue to be highly dependent on the timing of our operating costs.

During the six months ended December 31, 2014, there were no investing activities. During the six months ended December 31, 2013, net cash provided by investing activities was $3.7 million, consisting of proceeds from the maturity of short-term investments offset by $6,239 used for capital expenditures.

During the six months ended December 31, 2014, net cash provided by financing activities was $29.1 million. During the six months ended December 31, 2013, cash used in financing activities of $37,008 consisted of the $25,214 for the payment of withholding taxes related to restricted stock units and payments of $11,794 on capital lease payments. The difference for the six months ended December 31, 2014 and 2013 was primarily related to the closing of a $20.0 million private placement and the closing of a $10.0 million venture loan.

As of December 31, 2014, our cash and cash equivalents were $42.7 million and our current liabilities were $5.1 million. We intend to utilize existing capital resources for general corporate purposes and working capital, including the Phase 3 clinical trial program with bremelanotide for FSD and preclinical and clinical development of our other product candidates and programs, including PL-3994, MC1r, and MC4r programs. Based on our current plan, we believe that the Phase 3 clinical trial program with bremelanotide will cost at least $80.0 million. We initiated patient enrollment in our Phase 3 program in the fourth quarter of calendar 2014. We intend to seek additional capital to support our Phase 3 program through collaborative arrangements on bremelanotide, public or private equity or debt financings, or other sources.

Management believes that our existing capital resources will be adequate to fund its planned operations through the quarter ending March 31, 2016.

We anticipate incurring additional losses over at least the next few years. To achieve profitability, if ever, we, alone or with others, must successfully develop and commercialize our technologies and proposed products, conduct preclinical studies and clinical trials, obtain required regulatory approvals and successfully manufacture and market such technologies and proposed products. The time required to reach profitability is highly uncertain, and we do not know whether we will be able to achieve profitability on a sustained basis, if at all.

Item 3. Quantitative and Qualitative Disclosures About Market Risk.

Not required to be provided by smaller reporting companies.

Item 4. Controls and Procedures.

Our management, with the participation of our Chief Executive Officer and Chief Financial Officer, has evaluated the effectiveness of our disclosure controls and procedures, as defined in Exchange Act Rules 13a-15(e) and 15d-15(e), as of the end of the period covered by this report. Based on that evaluation, our Chief Executive Officer and Chief Financial Officer concluded that our disclosure controls and procedures were effective as of December 31, 2014. There were no changes in our internal control over financial reporting that occurred during our most recent fiscal quarter that materially affected, or that are reasonably likely to materially affect, our internal control over financial reporting.

16

PART II - OTHER INFORMATION

Item 1. Legal Proceedings.

We may be involved, from time to time, in various claims and legal proceedings arising in the ordinary course of our business. We are not currently a party to any claim or legal proceeding.

Item 1A. Risk Factors.

There have been no material changes to our risk factors disclosed in Part II, Item 1A of our quarterly report on Form 10-Q for the quarter ended September 30, 2014 other than as set forth below:

Risks Relating to Our Financial Results and Need for Financing

We will need additional financing, including financing to submit required regulatory applications to the FDA for bremelanotide for FSD and to complete clinical trials for our other product candidates, which may be difficult to obtain.

As of December 31, 2014, we had cash and cash equivalents of $42.7 million, with current liabilities of $5.1 million. We believe we have sufficient currently available working capital to fund our planned operations through the quarter ending March 31, 2016. We will need additional funding to complete our Phase 3 clinical trials of bremelanotide for FSD. We will also need additional funding to complete required clinical trials for our other product candidates and, assuming those clinical trials are successful, as to which there can be no assurance, to complete submission of required regulatory applications to the FDA.

We have initiated Phase 3 clinical trials of bremelanotide for FSD and have started patient enrollment, but we may be required to curtail or delay clinical trial operations unless we have adequate funds to complete Phase 3 clinical trials. We estimate that the Phase 3 program, including regulatory filings for product approval, will cost at least $80.0 million. We will seek funds to support the Phase 3 program through collaborative arrangements on bremelanotide in addition to our agreement with Gedeon Richter, including marketing and distribution partnering agreements, public or private equity or debt financings, and other sources, but such additional funding may not be available on acceptable terms, or at all.

We do not have any source of significant recurring revenue and must depend on financing or partnering to sustain our operations. We may raise additional funds through public or private equity or debt financings, collaborative arrangements on our product candidates, or other sources. However, additional funding may not be available on acceptable terms, or at all. To obtain additional funding, we may need to enter into arrangements that require us to develop only certain of our product candidates or relinquish rights to certain technologies, product candidates and/or potential markets.

If we are unable to raise sufficient additional funds when needed, we may be required to curtail operations significantly, cease clinical trials and decrease staffing levels. We may seek to license, sell or otherwise dispose of our product candidates, technologies and contractual rights on the best possible terms available. Even if we are able to license, sell or otherwise dispose of our product candidates, technologies and contractual rights, it is likely to be on unfavorable terms and for less value than if we had the financial resources to develop or otherwise advance our product candidates, technologies and contractual rights ourselves.

17

Our future capital requirements depend on many factors, including:

|

●

|

the results of our Phase 3 clinical trials for bremelanotide for FSD;

|

|

●

|

the timing of, and the costs involved in, obtaining regulatory approvals for bremelanotide for FSD and our other product candidates;

|

|

●

|

the number and characteristics of any additional product candidates we develop or acquire;

|

|

●

|

the scope, progress, results and costs of researching and developing bremelanotide for FSD, PL-3994 or any future product candidates, and conducting preclinical and clinical trials;

|

|

●

|

the cost of commercialization activities if bremelanotide for FSD, PL-3994 or any future product candidates are approved for sale, including marketing, sales and distribution costs;

|

|

●

|

the cost of manufacturing bremelanotide for FSD, PL-3994 or any future product candidates and any products we successfully commercialize and maintaining our related facilities;

|

|

●

|

our ability to establish and maintain strategic collaborations, licensing or other arrangements and the terms and timing of such arrangements;

|

|

●

|

the degree and rate of market acceptance of any future approved products;

|

|

●

|

the emergence, approval, availability, perceived advantages, relative cost, relative safety and relative efficacy of alternative and competing products or treatments;

|

|

●

|

any product liability or other lawsuits related to our products;

|

|

●

|

the expenses needed to attract and retain skilled personnel;

|

|

●

|

the costs involved in preparing, filing, prosecuting, maintaining, defending and enforcing patent claims, including litigation costs and the outcome of such litigation; and

|

|

●

|

the timing, receipt and amount of sales of, or royalties on, future approved products, if any.

|

Risks Relating to Obligations in Our 2012 and 2014 Private Placements

Under agreements relating to our 2012 and 2014 private placements, we are required to allow purchasers in the 2012 and 2014 private placements to participate in certain future equity and debt financings, which may restrict our ability to raise funds on acceptable terms, or at all.

For six years after our 2012 private placement, unless the purchasers own less than 20% of our outstanding common stock calculated as if the warrants were exercised, and for four years after our 2014 private placement, unless the FDA earlier approves bremelanotide for FSD, the purchasers have the right of first negotiation on any subsequent equity or debt financing. Under our 2012 private placement, if we do not agree to terms of a financing with the purchasers, and negotiate with a third party on a financing, we must offer to sell to the purchasers at least 55% of the financing, and the purchasers may elect to purchase all or a portion of the financing. Under our 2014 private placement, if we do not agree to terms of a financing with the purchasers, depending on pricing of the financing, the purchasers have the right to purchase between 83.5% and all of the financing. We will require significant additional resources and capital for our Phase 3 bremelanotide clinical trial program and other clinical trial programs. The right of first negotiation and right of participation granted to the purchasers in our 2012 and 2014 private placements may make it more difficult to raise additional funding through public or private equity or debt financings or other sources. Such funding may not be available on acceptable terms, or at all.

18

Under agreements relating to our 2012 and 2014 private placements, so long as any Series A 2012, Series B 2012 or Series C 2014 warrants are outstanding, we are required to redeem such warrants at the option of the holders in the event of any takeover, change of control or other fundamental transaction which we permit.