ITEM 1B. |

UNRESOLVED STAFF COMMENTS |

None.

ITEM 2. |

PROPERTIES |

We own certain of our branch offices, as well as our headquarters on Long Island and certain other back-office buildings in New York, Ohio, and Florida. We also utilize other branch and back-office locations in those states, and in New Jersey and Arizona, under various lease and license agreements that expire at various times. (See Note 7, “Leases” in Item 8, “Financial Statements and Supplementary Data.”) We believe that our facilities are adequate to meet our present and immediately foreseeable needs.

ITEM 3. |

LEGAL PROCEEDINGS |

The Company is involved in various legal actions arising in the ordinary course of its business. All such actions in the aggregate involve amounts that are believed by management to be immaterial to the financial condition and results of operations of the Company.

ITEM 4. |

MINE SAFETY DISCLOSURES |

Not applicable.

31

PART II

ITEM 5. |

MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS, AND ISSUER PURCHASES OF EQUITY SECURITIES |

The common stock of New York Community Bancorp, Inc. trades on the New York Stock Exchange (the “NYSE”) under the symbol “NYCB.”

At December 31, 2019, the number of outstanding shares was 467,346,781 and the number of registered owners was approximately 11,042. The latter figure does not include those investors whose shares were held for them by a bank or broker at that date.

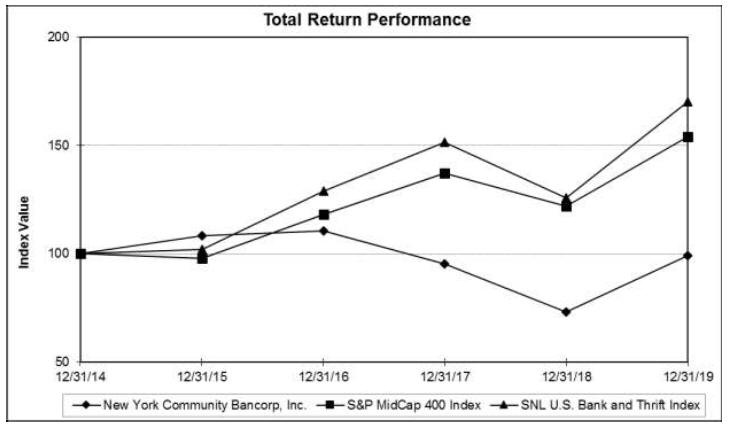

Stock Performance Graph

The following graph compares the cumulative total return on the Company’s stock in the five years ended December 31, 2019 with the cumulative total returns on a broad market index (the S&P

Mid-Cap

400 Index) and a peer group index (the SNL U.S. Bank and Thrift Index) during the same time. The S&P Mid-Cap

400 Index was chosen as the broad market index in connection with the Company’s trading activity on the NYSE; the SNL U.S. Bank and Thrift Index currently is comprised of 386 bank and thrift institutions, including the Company. S&P Global Market Intelligence provided us with the data for both indices.The performance graph is being furnished solely to accompany this report pursuant to Item 201(e) of Regulation

S-K,

and is not being filed for purposes of Section 18 of the Securities Exchange Act of 1934, as amended, and is not to be incorporated by reference into any filing of the Company, whether made before or after the date hereof, regardless of any general incorporation language in such filing.The cumulative total returns are based on the assumption that $100.00 was invested in each of the three investments on December 31, 2014 and that all dividends paid since that date were reinvested. Such returns are based on historical results and are not intended to suggest future performance.

Comparison of

5-Year

Cumulative Total Return Among New York Community Bancorp, Inc.,

S&P

Mid-Cap

400 Index, and SNL U.S. Bank and Thrift Index

32

ASSUMES $100 INVESTED ON DECEMBER 31, 2014

ASSUMES DIVIDEND REINVESTED

FISCAL YEAR ENDING DECEMBER 31, 2019

| 12/31/2014 |

12/31/2015 |

12/31/2016 |

12/31/2017 |

12/31/2018 |

12/31/2019 |

|||||||||||||||||||

| New York Community Bancorp, Inc. |

$ | 100.00 |

$ | 108.22 |

$ | 110.55 |

$ | 95.20 |

$ | 73.09 |

$ | 98.99 |

||||||||||||

| S&P Mid-Cap 400 Index |

$ | 100.00 |

$ | 97.82 |

$ | 118.11 |

$ | 137.30 |

$ | 122.08 |

$ | 154.07 |

||||||||||||

| SNL U.S. Bank and Thrift Index |

$ | 100.00 |

$ | 102.02 |

$ | 128.80 |

$ | 151.45 |

$ | 125.81 |

$ | 170.04 |

||||||||||||

33

Share Repurchases

Shares Repurchased Pursuant to the Company’s Stock-Based Incentive Plans

Participants in the Company’s stock-based incentive plans may have shares of common stock withheld to fulfill the income tax obligations that arise in connection with their exercise of stock options and the vesting of their stock awards. Shares that are withheld for this purpose are repurchased pursuant to the terms of the applicable stock-based incentive plan, rather than pursuant to the share repurchase program authorized by the Board of Directors described below.

Shares Repurchased Pursuant to the Board of Directors’ Share Repurchase Authorization

On October 23, 2018, the Board of Directors authorized the repurchase of up to $300 million of the Company’s common stock. Under said authorization, shares may be repurchased on the open market or in privately negotiated transactions.

Shares that are repurchased pursuant to the Board of Directors’ authorization, and those that are repurchased pursuant to the Company’s stock-based incentive plans, are held in our Treasury account and may be used for various corporate purposes, including, but not limited to, merger transactions and the vesting of restricted stock awards.

As indicated in the table below, during the twelve months ended December 31, 2019, the Company allocated 769,111 shares or $8.1 million toward the repurchase of shares tied to its stock-based incentive plans. Also, during the first quarter of the year, the Company repurchased $67.1 million or 7.1 million shares of its common stock under its authorized share repurchase program, leaving $72.1 million remaining under the repurchase authorization at December 31, 2019.

| (dollars in thousands, except per share data) |

||||||||||||

| Period |

Total Shares of Common Stock Repurchased |

Average Price Paid per Common Share |

Total Allocation |

|||||||||

| First Quarter 2019 |

7,816,228 |

$ 9.57 |

$ | 74,788 |

||||||||

| Second Quarter 2019 |

3,485 |

11.14 |

39 |

|||||||||

| Third Quarter 2019 |

31,059 |

11.10 |

345 |

|||||||||

| Fourth Quarter 2019: |

||||||||||||

| October |

232 |

13.02 |

3 |

|||||||||

| November |

3,018 |

12.02 |

36 |

|||||||||

| December |

829 |

10.53 |

9 |

|||||||||

| Total Fourth Quarter 2019 |

4,079 |

11.78 |

48 |

|||||||||

| 2019 Total |

7,854,851 |

9.58 |

$ | 75,220 |

||||||||

34

ITEM 6. |

SELECTED FINANCIAL DATA |

| At or For the Years Ended December 31, |

||||||||||||||||||||

| (dollars in thousands, except share data) |

2019 |

2018 |

2017 |

2016 |

2015 |

|||||||||||||||

| EARNINGS SUMMARY: |

||||||||||||||||||||

| Net interest income (1) |

$ | 957,400 |

$ | 1,030,995 |

$ | 1,130,003 |

$ | 1,287,382 |

$ | 408,075 |

||||||||||

| Provision for (recovery of) losses on non-covered loans |

7,105 |

18,256 |

60,943 |

11,874 |

(3,334 |

) | ||||||||||||||

| Recovery of losses on covered loans |

— |

— |

(23,701 |

) | (7,694 |

) | (11,670 |

) | ||||||||||||

| Non-interest income |

84,230 |

91,558 |

216,880 |

145,572 |

210,763 |

|||||||||||||||

| Non-interest expense: |

||||||||||||||||||||

| Operating expenses (2) |

511,218 |

546,628 |

641,218 |

638,109 |

615,600 |

|||||||||||||||

| Amortization of core deposit intangibles |

— |

— |

208 |

2,391 |

5,344 |

|||||||||||||||

| Debt repositioning charge |

— |

— |

— |

— |

141,209 |

|||||||||||||||

| Merger-related expenses |

— |

— |

— |

11,146 |

3,702 |

|||||||||||||||

| Total non-interest expense |

511,218 |

546,628 |

641,426 |

651,646 |

765,855 |

|||||||||||||||

| Income tax expense (benefit) |

128,264 |

135,252 |

202,014 |

281,727 |

(84,857 |

) | ||||||||||||||

| Net income (loss) (3) |

395,043 |

422,417 |

466,201 |

495,401 |

(47,156 |

) | ||||||||||||||

| Basic earnings (loss) per common share (3) |

$ | 0.77 |

$ | 0.79 |

$ | 0.90 |

$ | 1.01 |

$ | (0.11 |

) | |||||||||

| Diluted earnings (loss) per common share (3) |

0.77 |

0.79 |

0.90 |

1.01 |

(0.11 |

) | ||||||||||||||

| Dividends paid per common share |

0.68 |

0.68 |

0.68 |

0.68 |

1.00 |

|||||||||||||||

| SELECTED RATIOS: |

||||||||||||||||||||

| Return on average assets (3) |

0.76 |

% | 0.84 |

% | 0.96 |

% | 1.00 |

% | (0.10 |

)% | ||||||||||

| Return on average common stockholders’ equity (3) |

5.88 |

6.20 |

7.12 |

8.19 |

(0.81 |

) | ||||||||||||||

| Average common stockholders’ equity to average assets |

11.82 |

12.51 |

12.76 |

12.28 |

11.90 |

|||||||||||||||

| Operating expenses to average assets (2) |

0.98 |

1.09 |

1.32 |

1.29 |

1.26 |

|||||||||||||||

| Efficiency ratio (1)(2) |

49.08 |

48.70 |

47.61 |

44.53 |

99.48 |

|||||||||||||||

| Net interest rate spread (1) |

1.79 |

2.06 |

2.47 |

2.85 |

0.69 |

|||||||||||||||

| Net interest margin (1) |

2.02 |

2.25 |

2.59 |

2.93 |

0.94 |

|||||||||||||||

| Dividend payout ratio |

88.31 |

86.08 |

75.56 |

67.33 |

— |

|||||||||||||||

| BALANCE SHEET SUMMARY: |

||||||||||||||||||||

| Total assets |

$ | 53,640,821 |

$ | 51,899,376 |

$ | 49,124,195 |

$ | 48,926,555 |

$ | 50,317,796 |

||||||||||

| Loans, net of allowance for loan losses |

41,746,517 |

40,006,088 |

38,265,183 |

39,308,016 |

38,011,995 |

|||||||||||||||

| Allowance for losses on non-covered loans |

147,638 |

159,820 |

158,046 |

158,290 |

147,124 |

|||||||||||||||

| Allowance for losses on covered loans |

— |

— |

— |

23,701 |

31,395 |

|||||||||||||||

| Securities |

5,885,887 |

5,644,071 |

3,531,427 |

3,817,057 |

6,173,645 |

|||||||||||||||

| Deposits |

31,657,132 |

30,764,430 |

29,102,163 |

28,887,903 |

28,426,758 |

|||||||||||||||

| Borrowed funds |

14,557,593 |

14,207,866 |

12,913,679 |

13,673,379 |

15,748,405 |

|||||||||||||||

| Common stockholders’ equity |

6,208,854 |

6,152,395 |

6,292,536 |

6,123,991 |

5,934,696 |

|||||||||||||||

| Common shares outstanding |

467,346,781 |

473,536,604 |

488,490,352 |

487,056,676 |

484,943,308 |

|||||||||||||||

| Book value per common share |

$ | 13.29 |

$ | 12.99 |

$ | 12.88 |

$ | 12.57 |

$ | 12.24 |

||||||||||

| Common stockholders’ equity to total assets |

11.57 |

% | 11.85 |

% | 12.81 |

% | 12.52 |

% | 11.79 |

% | ||||||||||

| ASSET QUALITY RATIOS (excluding covered assets and non-covered purchased credit-impaired loans): |

||||||||||||||||||||

| Non-performing non-covered loans to total non-covered loans |

0.15 |

% | 0.11 |

% | 0.19 |

% | 0.15 |

% | 0.13 |

% | ||||||||||

| Non-performing non-covered assets to total non-covered assets |

0.14 |

0.11 |

0.18 |

0.14 |

0.13 |

|||||||||||||||

| Allowance for losses on non-covered loans to non-performing non-covered loans |

241.07 |

351.21 |

214.50 |

277.19 |

310.08 |

|||||||||||||||

| Allowance for losses on non-covered loans to total non-covered loans |

0.35 |

0.40 |

0.41 |

0.42 |

0.41 |

|||||||||||||||

| Net charge-offs (recoveries) to average loans (4) |

0.05 |

0.04 |

0.16 |

0.00 |

(0.02 |

) | ||||||||||||||

(1) |

The 2015 amount reflects the impact of a $773.8 million debt repositioning charge recorded as interest expense in the fourth quarter of the year. |

(2) |

The 2015 amount includes state and local non-income taxes of $5.4 million resulting from the debt repositioning charge. |

(3) |

The 2015 amount reflects the $546.8 million after-tax impact of the debt repositioning charge recorded as interest expense and non-interest expense, combined. |

(4) |

Average loans include covered loans. |

35