|

File Nos. 333-104602 and 811-07876 |

||||||

|

|

||||||

|

|

||||||

|

As filed with the Securities and Exchange Commission on December 28, 2020. |

||||||

|

|

||||||

|

SECURITIES AND EXCHANGE COMMISSION |

||||||

|

Washington, DC 20549 |

||||||

|

FORM N-1A |

||||||

|

|

||||||

|

|

||||||

|

|

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 |

|

[X] |

|

||

|

|

|

|

|

|

||

|

|

|

|

|

|

||

|

|

Pre-Effective Amendment No. |

|

|

|

||

|

|

|

|

|

|

||

|

|

Post-Effective Amendment No. |

29 |

|

[X] |

|

|

|

|

|

|

|

|

||

|

|

and/or |

|

|

|

||

|

|

|

|

|

|

||

|

|

REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 |

|

[X] |

|

||

|

|

|

|

|

|

||

|

|

Amendment No. |

33 |

|

[X] |

|

|

|

|

|

|||||

|

Templeton China World Fund |

|

|||||

|

(Exact Name of Registrant as Specified in Charter) |

|

|||||

|

|

|

|||||

|

300 S.E. 2nd Street, Fort Lauderdale, Florida 33301-1923 |

|

|||||

|

(Address of Principal Executive Offices) (Zip Code) |

|

|||||

|

|

|

|||||

|

(954) 527-7500 (Registrant's Telephone Number, Including Area Code) |

|

|||||

|

|

|

|||||

|

Craig S. Tyle, One Franklin Parkway, San Mateo, CA 94403-1906 |

|

|||||

|

(Name and Address of Agent for Service of Process) |

|

|||||

|

|

|

|||||

|

It is proposed that this filing will become effective (check appropriate box) |

|

|||||

|

|

|

|||||

|

|

|

|||||

|

|

[ ] |

immediately upon filing pursuant to paragraph (b) |

|

|||

|

|

|

|

|

|||

|

|

[X] |

on January 1, 2021 pursuant to paragraph (b) |

|

|||

|

|

|

|

|

|||

|

|

[ ] |

60 days after filing pursuant to paragraph (a)(i) |

|

|||

|

|

|

|

|

|||

|

|

[ ] |

on (date) pursuant to paragraph (a)(i) |

|

|||

|

|

|

|

|

|||

|

|

[ ] |

75 days after filing pursuant to paragraph (a)(ii) |

|

|||

|

|

|

|

|

|||

|

|

[ ] |

on (date) pursuant to paragraph (a)(ii) of rule 485 |

|

|||

|

|

||||||

|

|

||||||

|

If appropriate check the following box: |

||||||

|

|

||||||

|

|

[ ] |

This post-effective amendment designates a new effective date for a previously filed post-effective amendment. |

|

|||

|

|

|

|

|

|||

|

Prospectus |

||

|

Templeton January 1, 2021  |

||

|

||

| Class A | Class C | Class R6 | Advisor Class |

| TCWAX | TCWCX | FCWRX | TACWX |

The U.S. Securities and Exchange Commission (SEC) has not approved or disapproved these securities or passed upon the adequacy of this prospectus. Any representation to the contrary is a criminal offense.

188 P 01/21

|

Contents |

||

|

Fund Summary Information about the Fund you should know before investing |

||

|

Investment Goal |

||

|

Fund Details More information on investment policies, practices and risks/financial highlights |

||

|

Investment Goal |

||

|

Your Account Information about sales charges, qualified investors, account transactions and services |

||

|

Choosing a Share Class |

||

|

For More Information Where to learn more about the Fund |

||

Fund Summary

Investment Goal

Long-term capital appreciation.

Fees and Expenses of the Fund

These tables describe the fees and expenses that you may pay if you buy and hold shares of the Fund.

Please note that the tables and examples below do not reflect any transaction fees that may be charged by financial intermediaries, or commissions that a shareholder may be required to pay directly to its financial intermediary when buying or selling Class R6 or Advisor Class shares.

Shareholder Fees (fees paid directly from your investment)

| Class A | Class C | Class R6 | Advisor Class | |

| Maximum Sales Charge (Load) Imposed on Purchases (as percentage of offering price) | ||||

| Maximum Deferred Sales Charge (Load) (as percentage of the lower of original purchase price or sale proceeds) |

1. There is a 1% contingent deferred sales charge that applies to investments of $1 million or more (see "Investments of $1 Million or More" under "Choosing a Share Class") and purchases by certain retirement plans without an initial sales charge on shares sold within 18 months of purchase.

Annual Fund Operating Expenses

(expenses that you pay each year as a percentage of the value of your investment)

| Class A | Class C | Class R6 | Advisor Class | |

| Management fees1 | ||||

| Distribution and service (12b-1) fees | ||||

| Other expenses | ||||

| Acquired fund fees and expenses2 | ||||

| Total annual Fund operating expenses1, 2 | ||||

| Fee waiver and/or expense reimbursement3 | - |

|||

| Total annual Fund operating expenses after fee waiver and/or expense reimbursement1, 2, 3 |

1. Management fees of the Fund have been restated to reflect current fiscal year fees as a result of a decrease in the Fund’s contractual management fee rate effective on July 1, 2020. If the management fees were not restated to reflect such decrease in fees, the amounts shown above would be greater. Consequently, the Fund’s total annual Fund operating expenses differ from the ratio of expenses to average net assets shown in the Financial Highlights.

2. Total annual Fund operating expenses differ from the ratio of expenses to average net assets shown in the Financial Highlights, which reflect the operating expenses of the Fund and do not include acquired fund fees and expenses.

3. The investment manager has contractually agreed to waive or assume certain expenses so that operating expenses (excluding Rule 12b-1 fees, acquired fund fees and expenses and certain non-routine expenses) for each class of the Fund do not exceed 1.60% until December 31, 2021. In addition, the transfer agent has contractually agreed to limit its fees on Class R6 shares to 0.03% until December 31, 2021. During its term, this fee waiver and expense reimbursement agreement may not be terminated or amended without approval of the board of trustees except to add series and classes, to reflect the extension of termination dates or to lower the fee waiver and expense limitation.

Example

This Example is intended to help you compare the cost of investing in the Fund with the cost of investing in other mutual funds. The Example assumes that you invest $10,000 in the Fund for the time periods indicated and then redeem all of your shares at the end of the period. The Example also assumes that your investment has a 5% return each year and that the Fund's operating expenses remain the same. The Example reflects adjustments made to the Fund's operating expenses due to the fee waivers and/or expense reimbursements by management for the 1 Year numbers only. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| 1 Year | 3 Years | 5 Years | 10 Years | |

| Class A | $ |

$ |

$ |

$ |

| Class C | $ |

$ |

$ |

$ |

| Class R6 | $ |

$ |

$ |

$ |

| Advisor Class | $ |

$ |

$ |

$ |

| Class C | $ |

$ |

$ |

$ |

Portfolio Turnover

The Fund pays transaction costs, such as commissions, when it buys and sells securities (or "turns over" its portfolio). A

higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when Fund shares are held

in a taxable account. These costs, which are not reflected in annual Fund operating expenses or in the Example, affect the

Fund's performance. During the most recent fiscal year, the Fund's portfolio turnover rate was

Principal Investment Strategies

- that are organized under the laws of, or with a principal office in, the People's Republic of China (China), Hong Kong or Taiwan; or

- for which the principal trading market is in China, Hong Kong or Taiwan; or

- that derive at least 50% of their revenues from goods or services sold or produced, or have at least 50% of their assets, in China.

The equity securities in which the Fund invests are primarily common stock. The Fund also invests in American, Global and European Depositary Receipts. China companies may be any size across the entire market capitalization spectrum, including midsize companies and smaller, newly organized and relatively unseasoned issuers. In addition to the Fund's main investments, the Fund may invest up to 20% of its net assets in securities that do not qualify as China company securities, but whose issuers, in the judgment of the investment manager, are expected to benefit from developments in the economy of China, Hong Kong or Taiwan. The Fund is a "non-diversified" fund, which means it generally invests a greater proportion of its assets in the securities of one or more issuers and invests overall in a smaller number of issuers than a diversified fund.

When choosing equity investments for the Fund, the investment manager applies a fundamental research, value-oriented, long-term approach, focusing on the market price of a company’s securities relative to the investment manager’s evaluation of the company’s long-term earnings, asset value and cash flow potential. The investment manager also considers a company’s profit and loss outlook, balance sheet strength, cash flow trends and asset value in relation to the current price of the company's securities.

Principal Risks

You could lose money by investing in the Fund. Mutual fund shares are not deposits or obligations of, or guaranteed or endorsed by, any bank, and are not insured by the Federal Deposit Insurance Corporation, the Federal Reserve Board, or any other agency of the U.S. government.

Foreign Securities (non-U.S.) Investing in foreign securities typically involves more risks than investing in U.S. securities, and includes risks associated with: (i) internal and external political and economic developments – e.g., the political, economic and social policies and structures of some foreign countries may be less stable and more volatile than those in the U.S. or some foreign countries may be subject to trading restrictions or economic sanctions; (ii) trading practices – e.g., government supervision and regulation of foreign securities and currency markets, trading systems and brokers may be less than in the U.S.; (iii) availability of information – e.g., foreign issuers may not be subject to the same disclosure, accounting and financial reporting standards and practices as U.S. issuers; (iv) limited markets – e.g., the securities of certain foreign issuers may be less liquid (harder to sell) and more volatile; and (v) currency exchange rate fluctuations and policies. The risks of foreign investments may be greater in developing or emerging market countries.

There are special risks associated with investments in China, Hong Kong and Taiwan, including exposure to currency fluctuations, less liquidity, expropriation, confiscatory taxation, nationalization and exchange control regulations (including currency blockage). Inflation and rapid fluctuations in inflation and interest rates have had, and may continue to have, negative effects on the economy and securities markets of China, Hong Kong and Taiwan. In addition, investments in Taiwan and Hong Kong could be adversely affected by their respective political and economic relationship with China. China, Hong Kong and Taiwan are deemed by the investment manager to be emerging markets countries, which means an investment in these countries has more heightened risks than general foreign investing due to a lack of established legal, political, business and social frameworks in these countries to support securities markets as well as the possibility for more widespread corruption and fraud. In addition, the standards for environmental, social and corporate governance matters in China, Hong Kong and Taiwan tend to be lower than such standards in more developed economies.

Trade disputes and the imposition of tariffs on goods and services can affect the economies of countries in which the Fund invests, particularly those countries with large export sectors, as well as the global economy. Trade disputes can result in increased costs of production and reduced profitability for non-export-dependent companies that rely on imports to the extent a country engages in retaliatory tariffs. Trade disputes may also lead to increased currency exchange rate volatility.

Region Focus Because the Fund invests its assets primarily in companies in a specific region, the Fund is subject to greater risks of adverse developments in that region and/or the surrounding regions than a fund that is more broadly diversified geographically. Political, social or economic disruptions in the region, even in countries in which the Fund is not invested, may adversely affect the value of investments held by the Fund.

Emerging Markets The Fund’s investments in securities of issuers in emerging market countries are subject to all of the risks of foreign investing generally, and have additional heightened risks due to a lack of established legal, political, business and social frameworks to support securities markets, including: delays in settling portfolio securities transactions; currency and capital controls; greater sensitivity to interest rate changes; pervasiveness of corruption and crime; currency exchange rate volatility; and inflation, deflation or currency devaluation.

Market The market values of securities or other investments owned by the Fund will go up or down, sometimes rapidly or unpredictably. The market value of a security or other investment may be reduced by market activity or other results of supply and demand unrelated to the issuer. This is a basic risk associated with all investments. When there are more sellers than buyers, prices tend to fall. Likewise, when there are more buyers than sellers, prices tend to rise.

The current global outbreak of the novel strain of coronavirus, COVID-19, has resulted in market closures and dislocations, extreme volatility, liquidity constraints and increased trading costs. Efforts to contain the spread of COVID-19 have resulted in global travel restrictions and disruptions of healthcare systems, business operations and supply chains, layoffs, reduced consumer demand, defaults and credit ratings downgrades, and other significant economic impacts. The effects of COVID-19 have impacted global economic activity across many industries and may heighten other pre-existing political, social and economic risks, locally or globally. The full impact of the COVID-19 pandemic is unpredictable and may adversely affect the Fund’s performance.

Stock prices tend to go up and down more dramatically than those of debt securities. A slower-growth or recessionary economic environment could have an adverse effect on the prices of the various stocks held by the Fund.

Small and Mid Capitalization Companies Securities issued by small and mid capitalization companies may be more volatile in price than those of larger companies and may involve additional risks. Such risks may include greater sensitivity to economic conditions, less certain growth prospects, lack of depth of management and funds for growth and development, and limited or less developed product lines and markets. In addition, small and mid capitalization companies may be particularly affected by interest rate increases, as they may find it more difficult to borrow money to continue or expand operations, or may have difficulty in repaying any loans.

Non-Diversification

Management The Fund is subject to management risk because it is an actively managed investment portfolio. The Fund's investment manager applies investment techniques and risk analyses in making investment decisions for the Fund, but there can be no guarantee that these decisions will produce the desired results.

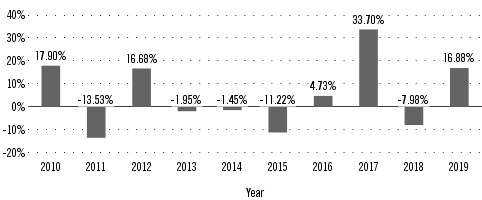

Performance

Class A Annual Total Returns

| - |

||

Average Annual Total Returns

(figures reflect sales charges)

For the periods ended December 31, 2019

| 1 Year | 5 Years | 10 Years | |

| Templeton China World Fund - Class A | |||

| Templeton China World Fund - Class C | |||

| Templeton China World Fund - Class R6 | |||

| Templeton China World Fund - Advisor Class | |||

| MSCI China Index-NR (index reflects no deduction for fees, expenses or taxes but are net of dividend tax withholding)2 | |||

| MSCI China Index (index reflects no deduction for fees, expenses or taxes) |

1. Since inception May 1, 2013.

2. The MSCI China Index-NR is replacing the MSCI China Index as the Fund's benchmark because the investment manager believes the MSCI China Index-NR provides a more consistent basis for comparison relative to the Fund's peers.

The figures in the average annual total returns table above reflect the Class A maximum front-end sales charge of 5.50%. Prior to September 10, 2018, Class A shares were subject to a maximum front-end sales charge of 5.75%. If the prior maximum front-end sales charge of 5.75% was reflected, performance for Class A in the average annual total returns table would be lower.

The after-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor's tax situation and may differ from those shown. After-tax returns are not relevant to investors who hold their Fund shares through tax-deferred arrangements, such as 401(k) plans or individual retirement accounts. After-tax returns are shown only for Class A and after-tax returns for other classes will vary.

Investment Manager

Templeton Asset Management Ltd. (Asset Management)

Portfolio Managers

Michael Lai, CFA Portfolio Manager of Asset Management and portfolio manager of the Fund since 2019.

Eric Mok Portfolio Manager of Asset Management and portfolio manager of the Fund since February 2020.

Purchase and Sale of Fund Shares

You may purchase or redeem shares of the Fund on any business day online through our website at franklintempleton.com, by mail (Franklin Templeton Investor Services, P.O. Box 33030, St. Petersburg, FL 33733-8030), or by telephone at (800) 632-2301. For Class A and C, the minimum initial purchase for most accounts is $1,000 (or $25 under an automatic investment plan). Class R6 and Advisor Class are only available to certain qualified investors and the minimum initial investment will vary depending on the type of qualified investor, as described under "Your Account — Choosing a Share Class — Qualified Investors — Class R6" and "— Advisor Class" in the Fund's prospectus. There is no minimum investment for subsequent purchases.

Taxes

The Fund’s distributions are generally taxable to you as ordinary income, capital gains, or some combination of both, unless you are investing through a tax-deferred arrangement, such as a 401(k) plan or an individual retirement account, in which case your distributions would generally be taxed when withdrawn from the tax-deferred account.

Payments to Broker-Dealers and

Other Financial Intermediaries

If you purchase shares of the Fund through a broker-dealer or other financial intermediary (such as a bank), the Fund and its related companies may pay the intermediary for the sale of Fund shares and related services. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your salesperson to recommend the Fund over another investment. Ask your financial advisor or visit your financial intermediary's website for more information.

Fund Details

Investment Goal

The Fund's investment goal is long-term capital appreciation.

Principal Investment Policies and Practices

Under normal market conditions, the Fund invests at least 80% of its net assets in securities of "China companies," as defined below. Shareholders will be given at least 60 days' advance notice of any change to this 80% policy.

For purposes of the Fund's investments, China companies are those:

- that are organized under the laws of, or with a principal office in, the People's Republic of China (China), Hong Kong or Taiwan; or

- for which the principal trading market is in China, Hong Kong or Taiwan; or

- that derive at least 50% of their revenues from goods or services sold or produced, or have at least 50% of their assets, in China.

China companies may be smaller, newly organized and relatively unseasoned companies. The Fund invests predominantly in the equity securities of China companies. An equity security represents a proportionate share of the ownership of a company; its value is based on the success of the company's business, any income paid to stockholders, the value of the company's assets, and general market conditions. Common stocks, preferred stocks and convertible securities are examples of equity securities. Convertible securities generally are debt securities or preferred stock that may be converted into common stock after certain time periods or under certain circumstances. The Fund may invest in convertible securities without regard to the ratings assigned by ratings services. The Fund also invests in American, Global and European Depositary Receipts. These are certificates typically issued by a bank or trust company that give their holders the right to receive securities issued by a foreign or domestic company.

In addition to the Fund's main investments, the Fund may invest up to 20% of its net assets in securities that do not qualify as China company securities, but whose issuers, in the judgment of the investment manager, are expected to benefit from developments in the economy of China, Hong Kong or Taiwan. The Fund may also invest up to 20% of its net assets in debt obligations of China companies, which may be lower-rated, or unrated and of comparable quality, when consistent with the Fund's investment goal. The Fund may also invest up to 10% of its total assets in exchange-traded funds to obtain exposure to all or a portion of stocks in certain markets and for cash management purposes.

The Fund is a non-diversified fund, which means it may invest a greater proportion of its assets in a single issuer compared to a diversified fund. As a matter of non-fundamental policy the Fund may not invest more than 15% of its total assets in the securities of any one issuer. The Fund may from time to time focus its investments in particular industries or sectors.

When choosing equity investments for this Fund, the investment manager applies a fundamental research, value-oriented, long-term approach, focusing on the market price of a company's securities relative to the investment manager's evaluation of the company's long-term earnings, asset value and cash flow potential. The investment manager also considers a company's profit and loss outlook, balance sheet strength, cash flow trends and asset value in relation to the current price. The analysis considers the company's corporate governance behavior as well as its position in its sector, the economic framework and political environment.

The investment manager may consider selling an equity security when it believes the security has become overvalued due to either its price appreciation or changes in the company's fundamentals, or when the investment manager believes another security is a more attractive investment opportunity.

Temporary Investments

When the investment manager believes market or economic conditions are unfavorable for investors, the investment manager may invest up to 100% of the Fund's assets in a temporary defensive manner by holding all or a substantial portion of its assets in cash, cash equivalents or other high quality short-term investments. Temporary defensive investments generally may include short-term and medium-term debt securities rated, at the time of investment, A or higher by Moody's Investors Service (Moody's) or Standard & Poor's (S&P®) or, if unrated, determined to be of comparable quality. The investment manager also may invest in these types of securities or hold cash while looking for suitable investment opportunities or to maintain liquidity. In these circumstances, the Fund may be unable to achieve its investment goal.

Principal Risks

Foreign Securities (non-U.S.)

Investing in foreign securities typically involves more risks than investing in U.S. securities. Certain of these risks also may apply to securities of U.S. companies with significant foreign operations.

China companies. There are special risks associated with investments in China, Hong Kong and Taiwan, including exposure to currency fluctuations, less liquidity, expropriation, confiscatory taxation, nationalization and exchange control regulations (including currency blockage). Inflation and rapid fluctuations in inflation and interest rates have had, and may continue to have, negative effects on the economy and securities markets of China, Hong Kong and Taiwan. In addition, investments in Taiwan and Hong Kong could be adversely affected by their respective political and economic relationship with China. China, Hong Kong and Taiwan are deemed by the investment manager to be emerging markets countries, which means an investment in these countries has more heightened risks than general foreign investing due to a lack of established legal, political, business and social frameworks in these countries to support securities markets as well as the possibility for more widespread corruption and fraud. In addition, the standards for environmental, social and corporate governance matters in China, Hong Kong and Taiwan tend to be lower than such standards in more developed economies.

China has committed by treaty to preserve Hong Kong’s autonomy and its economic, political and social freedoms for fifty years from the July 1, 1997 transfer of sovereignty from Great Britain to China. In recent years, political tensions within Hong Kong have risen. Such increased political tensions could have potential impacts on the political and legal structures in Hong Kong. They could also affect investor and business confidence in Hong Kong, which in turn could affect markets and business results.

Political and economic developments. The political, economic and social policies or structures of some foreign countries may be less stable and more volatile than those in the United States. Investments in these countries may be subject to greater risks of internal and external conflicts, expropriation, nationalization of assets, foreign exchange controls (such as suspension of the ability to transfer currency from a given country), restrictions on removal of assets, political or social instability, military action or unrest, diplomatic developments, currency devaluations, foreign ownership limitations, and substantial, punitive or confiscatory tax increases. It is possible that a government may take over the assets or operations of a company or impose restrictions on the exchange or export of currency or other assets. Some countries also may have different legal systems that may make it difficult or expensive for the Fund to vote proxies, exercise shareholder rights, and pursue legal remedies with respect to its foreign investments. Diplomatic and political developments could affect the economies, industries, and securities and currency markets of the countries in which the Fund is invested. These developments include rapid and adverse political changes; social instability; regional conflicts; sanctions imposed by the United States, other nations or other governmental entities, including supranational entities; terrorism; and war. In addition, such developments could contribute to the devaluation of a country’s currency, a downgrade in the credit ratings of issuers in such country, or a decline in the value and liquidity of securities of issuers in that country. An imposition of sanctions upon certain issuers in a country could result in an immediate freeze of that issuer’s securities, impairing the ability of the Fund to buy, sell, receive or deliver those securities. These factors would affect the value of the Fund’s investments and are extremely difficult, if not impossible, to predict and take into account with respect to the Fund's investments.

Trading practices. Brokerage commissions, withholding taxes, custodial fees, and other fees generally are higher in foreign markets. The policies and procedures followed by foreign stock exchanges, currency markets, trading systems and brokers may differ from those applicable in the United States, with possibly negative consequences to the Fund. The procedures and rules governing foreign trading, settlement and custody (holding of the Fund's assets) also may result in losses or delays in payment, delivery or recovery of money or other property. Foreign government supervision and regulation of foreign securities and currency markets and trading systems may be less than or different from government supervision in the United States, and may increase the Fund's regulatory and compliance burden and/or decrease the Fund's investor rights and protections.

Availability of information. Foreign issuers may not be subject to the same disclosure, accounting, auditing and financial reporting standards and practices as U.S. issuers. Thus, there may be less information publicly available about foreign issuers than about most U.S. issuers. In addition, information provided by foreign issuers may be less timely or less reliable than information provided by U.S. issuers.

Currency exchange rates. Foreign securities may be issued and traded in foreign currencies. As a result, their market values in U.S. dollars may be affected by changes in exchange rates between such foreign currencies and the U.S. dollar, as well as between currencies of countries other than the U.S. For example, if the value of the U.S. dollar goes up compared to a foreign currency, an investment traded in that foreign currency will go down in value because it will be worth fewer U.S. dollars. The Fund accrues additional expenses when engaging in currency exchange transactions, and valuation of the Fund's foreign securities may be subject to greater risk because both the currency (relative to the U.S. dollar) and the security must be considered.

Limited markets. Certain foreign securities may be less liquid (harder to sell) and their prices may be more volatile than many U.S. securities. Illiquidity tends to be greater, and valuation of the Fund's foreign securities may be more difficult, due to the infrequent trading and/or delayed reporting of quotes and sales.

Trade disputes. The economies of foreign countries dependent on large export sectors may be adversely affected by trade disputes with key trading partners and escalating tariffs imposed on goods and services produced by such countries. A national economic slowdown in the export sector may also affect companies that are not heavily dependent on exports. To the extent a country engages in retaliatory tariffs, a company that relies on imported parts to produce its own goods may experience increased costs of production or reduced profitability, which may affect consumers, investors and the domestic economy. Trade disputes and retaliatory actions may include embargoes and other trade limitations, which may trigger a significant reduction in international trade and impact the global economy. Trade disputes may also lead to increased currency exchange rate volatility, which can adversely affect the prices of Fund securities valued in US dollars. The potential threat of trade disputes may also negatively affect investor confidence in the markets generally and investment growth.

Regional. Adverse conditions in a certain region or country can adversely affect securities of issuers in other countries whose economies appear to be unrelated. Because the Fund invests a significant portion of its assets in a specific geographic region or a particular country, the Fund will generally have more exposure to the specific regional or country economic risks. In the event of economic or political turmoil or a deterioration of diplomatic relations in a region or country where a substantial portion of the Fund's assets are invested, the Fund may experience substantial illiquidity or reduction in the value of the Fund's investments.

Emerging market countries. The Fund's investments in securities of issuers in emerging market countries are subject to all of the risks of foreign investing generally, and have additional heightened risks due to a lack of established legal, political, business and social frameworks to support securities markets. Some of the additional significant risks include:

- less social, political and economic stability;

- a higher possibility of the devaluation of a country’s currency, a downgrade in the credit ratings of issuers in such country, or a decline in the value and liquidity of securities of issuers in that country if the United States, other nations or other governmental entities (including supranational entities) impose sanctions on issuers that limit or restrict foreign investment, the movement of assets or other economic activity in the country due to political, military or regional conflicts or due to terrorism or war;

- smaller securities markets with low or non-existent trading volume and greater illiquidity and price volatility;

- more restrictive national policies on foreign investment, including restrictions on investment in issuers or industries deemed sensitive to national interests;

- less transparent and established taxation policies;

- less developed regulatory or legal structures governing private and foreign investment or allowing for judicial redress for injury to private property, such as bankruptcy;

- less familiarity with a capital market structure or market-oriented economy and more widespread corruption and fraud;

- less financial sophistication, creditworthiness and/or resources possessed by, and less government regulation of, the financial institutions and issuers with which the Fund transacts;

- less government supervision and regulation of business and industry practices, stock exchanges, brokers and listed companies than in the U.S.;

- greater concentration in a few industries resulting in greater vulnerability to regional and global trade conditions;

- higher rates of inflation and more rapid and extreme fluctuations in inflation rates;

- greater sensitivity to interest rate changes (for example, a higher interest rate environment can make it more difficult for emerging market governments to service their existing debt);

- increased volatility in currency exchange rates and potential for currency devaluations and/or currency controls;

- greater debt burdens relative to the size of the economy;

- more delays in settling portfolio transactions and heightened risk of loss from share registration and custody practices; and

- less assurance that when favorable economic developments occur, they will not be slowed or reversed by unanticipated economic, political or social events in such countries.

Because of the above factors, the Fund's investments in emerging market countries may be subject to greater price volatility and illiquidity than investments in developed markets.

The definition of emerging market countries or companies as used in this prospectus may differ from the definition of the same terms as used in other Franklin Templeton fund prospectuses.

Focus

The greater the Fund's exposure to any single type of investment – including investment in a given industry, sector, region, country, issuer, or type of security – the greater the losses the Fund may experience upon any single economic, market, business, political, regulatory, or other occurrence. As a result, there may be more fluctuation in the price of the Fund's shares.

Market

The market values of securities or other investments owned by the Fund will go up or down, sometimes rapidly or unpredictably. The Fund’s investments may decline in value due to factors affecting individual issuers (such as the results of supply and demand), or sectors within the securities markets. The value of a security or other investment also may go up or down due to general market conditions that are not specifically related to a particular issuer, such as real or perceived adverse economic conditions, changes in interest rates or exchange rates, or adverse investor sentiment generally. In addition, unexpected events and their aftermaths, such as the spread of diseases; natural, environmental or man-made disasters; financial, political or social disruptions; terrorism and war; and other tragedies or catastrophes, can cause investor fear and panic, which can adversely affect the economies of many companies, sectors, nations, regions and the market in general, in ways that cannot necessarily be foreseen. During a general downturn in the securities markets, multiple asset classes may decline in value. When markets perform well, there can be no assurance that securities or other investments held by the Fund will participate in or otherwise benefit from the advance.

The current global outbreak of the novel strain of coronavirus, COVID-19, has resulted in market closures and dislocations, extreme volatility, liquidity constraints and increased trading costs. Efforts to contain the spread of COVID-19 have resulted in global travel restrictions and disruptions of healthcare systems, business operations and supply chains, layoffs, reduced consumer demand, defaults and credit ratings downgrades, and other significant economic impacts. The effects of the COVID-19 pandemic have impacted global economic activity across many industries and may heighten other pre-existing political, social and economic risks, locally or globally. The full impact of the COVID-19 pandemic, and other epidemics and pandemics that may arise in the future, on national and global economies, individual companies and the financial markets is unpredictable, may result in a high degree of uncertainty for potentially extended periods of time and may adversely affect the Fund’s performance.

Stock prices tend to go up and down more dramatically than those of debt securities. A slower-growth or recessionary economic environment could have an adverse effect on the prices of the various stocks held by the Fund.

Small and Mid Capitalization Companies

While small and mid capitalization companies may offer substantial opportunities for capital growth, they also may involve more risks than larger capitalization companies. Historically, small and mid capitalization company securities have been more volatile in price than larger company securities, especially over the short term. Among the reasons for the greater price volatility are the less certain growth prospects of small and mid capitalization companies, the lower degree of liquidity in the markets for such securities, and the greater sensitivity of small and mid capitalization companies to changing economic conditions.

In addition, small and mid capitalization companies may be less seasoned and newly organized, lack depth of management, be unable to generate funds necessary for growth or development, have limited product lines or be developing or marketing new products or services for which markets are not yet established and may never become established. Small and mid capitalization companies may be particularly affected by interest rate increases, as they may find it more difficult to borrow money to continue or expand operations, or may have difficulty in repaying loans, particularly those with floating interest rates.

Non-Diversification

The Fund is a "non-diversified" fund. It generally invests a greater portion of its assets in the securities of one or more issuers and invests overall in a smaller number of issuers than a diversified fund. The Fund may be more sensitive to a single economic, business, political, regulatory or other occurrence than a more diversified fund might be, which may negatively impact the Fund's performance and result in greater fluctuation in the value of the Fund's shares.

Exchange Traded Funds (ETFs)

The Fund's investments in ETFs may subject the Fund to additional risks than if the Fund would have invested directly in the ETFs’ underlying securities. These risks include the possibility that an ETF may experience a lack of liquidity that can result in greater volatility than its underlying securities; an ETF may trade at a premium or discount to its net asset value; or, if an index ETF, an ETF may not replicate exactly the performance of the benchmark index it seeks to track. In addition, investing in an ETF may also be more costly than if a Fund had owned the underlying securities directly. The Fund, and indirectly, shareholders of the Fund, bear a proportionate share of the ETF's expenses, which include management and advisory fees and other expenses. In addition, the Fund pays brokerage commissions in connection with the purchase and sale of shares of ETFs.

Interest Rate

Interest rate changes can be sudden and unpredictable, and are influenced by a number of factors, including government policy, monetary policy, inflation expectations, perceptions of risk, and supply of and demand for bonds. Changes in government or central bank policy, including changes in tax policy or changes in a central bank’s implementation of specific policy goals, may have a substantial impact on interest rates. There can be no guarantee that any particular government or central bank policy will be continued, discontinued or changed, nor that any such policy will have the desired effect on interest rates. Debt securities generally tend to lose market value when interest rates rise and increase in value when interest rates fall. A rise in interest rates also has the potential to cause investors to rapidly sell fixed income securities. A substantial increase in interest rates may also have an adverse impact on the liquidity of a debt security, especially those with longer maturities or durations. Securities with longer maturities or durations or lower coupons or that make little (or no) interest payments before maturity tend to be more sensitive to interest rate changes.

Credit

The Fund could lose money on a debt security if the issuer or borrower is unable or fails to meet its obligations, including failing to make interest payments and/or to repay principal when due. Changes in an issuer's financial strength, the market's perception of the issuer's financial strength or an issuer's or security's credit rating, which reflects a third party's assessment of the credit risk presented by a particular issuer or security, may affect debt securities' values. The Fund may incur substantial losses on debt securities that are inaccurately perceived to present a different amount of credit risk by the market, the investment manager or the rating agencies than such securities actually do.

High-Yield Debt Securities

Issuers of lower-rated or “high-yield” debt securities (also known as “junk bonds”) are not as strong financially as those issuing higher credit quality debt securities. High-yield debt securities are generally considered predominantly speculative by the applicable rating agencies as their issuers are more likely to encounter financial difficulties because they may be more highly leveraged, or because of other considerations. In addition, high yield debt securities generally are more vulnerable to changes in the relevant economy, such as a recession or a sustained period of rising interest rates, that could affect their ability to make interest and principal payments when due. The prices of high-yield debt securities generally fluctuate more than those of higher credit quality. High-yield debt securities are generally more illiquid (harder to sell) and harder to value.

Management

The Fund is actively managed and could experience losses (realized and unrealized) if the investment manager's judgment about markets, interest rates or the attractiveness, relative values, liquidity, or potential appreciation of particular investments made for the Fund's portfolio prove to be incorrect. There can be no guarantee that these techniques or the investment manager's investment decisions will produce the desired results. Additionally, legislative, regulatory, or tax developments may affect the investment techniques available to the investment manager in connection with managing the Fund and may also adversely affect the ability of the Fund to achieve its investment goal.

More detailed information about the Fund and its policies and risks can be found in the Fund's Statement of Additional Information (SAI).

A description of the Fund's policies and procedures regarding the release of portfolio holdings information is also available in the Fund's SAI. Portfolio holdings information can be viewed online at franklintempleton.com.

Management

Templeton Asset Management Ltd. (Asset Management), whose principal office is 7 Temasek Boulevard, Suntec Tower One, #38-03, Singapore 038987, is the Fund's investment manager. Asset Management has a branch office in Hong Kong. Asset Management is an indirect subsidiary of Franklin Resources, Inc. Together, Asset Management and its affiliates manage as of November 30, 2020, over $1.46 trillion in assets, and have been in the investment management business since 1947.

The Fund is managed by a team of dedicated professionals focused on investments in developing or emerging markets. The portfolio managers of the team are as follows:

Michael Lai, CFA Portfolio Manager of Asset Management

Mr. Lai has been lead portfolio manager of the Fund since 2019. He has primary responsibility for the investments of the Fund. He has final authority over all aspects of the Fund's investment portfolio, including but not limited to, purchases and sales of individual securities, portfolio risk assessment, and the management of daily cash balances in accordance with anticipated investment management requirements. The degree to which he may perform these functions, and the nature of these functions, may change from time to time. He joined Franklin Templeton in August 2019. Prior to joining Franklin Templeton, he was lead portfolio manager of GAM Investments’ (GAM) China equity strategy since its inception in 2007. He also headed GAM’s Asian equity team in Hong Kong and was lead portfolio manager of GAM’s Asian strategy and co-manager for additional strategies.

Eric Mok Portfolio Manager of Asset Management

Mr. Mok has been a portfolio manager of the Fund since February 2020, providing research and advice on the purchases and sales of individual securities, and portfolio risk assessment. He joined Franklin Templeton in 1998.

CFA® and Chartered Financial Analyst® are trademarks owned by CFA Institute.

The Fund’s SAI provides additional information about portfolio manager compensation, other accounts that they manage and their ownership of Fund shares.

The Fund pays Asset Management a fee for managing the Fund's assets. For the fiscal year ended August 31, 2020, Asset Management agreed to reduce its fees to reflect reduced services resulting from the Fund's investment in a Franklin Templeton money fund. In addition, Asset Management has agreed to waive its fees or to assume as its own certain expenses otherwise payable by the Fund so that common expenses (i.e., a combination of investment management fees and other expenses, but excluding the Rule 12b-1 fees and acquired fund fees and expenses) for each class of the Fund do not exceed 1.60% (other than certain non-routine expenses or costs, including those relating to litigation, indemnification, reorganizations and liquidations) until December 31, 2021. In addition, the transfer agent has contractually agreed to limit its fees on Class R6 shares to 0.03% until December 31, 2021. The management fees before and after such waiver for the fiscal year ended August 31, 2020 were 1.24% and 1.23%, respectively.

Effective July 1, 2020, the Fund’s investment management fee was reduced, as approved by the board of trustees. Prior to July 1, 2020, the Fund paid the investment manager a fee equal to an annual rate based on the Fund’s average weekly net assets, as listed below:

- 1.25%, up to and including $1 billion;

- 1.20%, over $1 billion, up to and including $5 billion;

- 1.15%, over $5 billion, up to and including $10 billion;

- 1.10%, over $10 billion, up to and including $15 billion;

- 1.05%, over $15 billion, up to and including $20 billion; and

- 1.00%, over $20 billion.

Effective July 1, 2020, the Fund pays the investment manager a fee equal to an annual rate based on the Fund’s average weekly net assets, as listed below:

- 1.20%, up to and including $4 billion;

- 1.15%, over $4 billion, up to and including $10 billion;

- 1.10%, over $10 billion, up to and including $15 billion;

- 1.05%, over $15 billion, up to and including $20 billion; and

- 1.00%, over $20 billion.

Distributions and Taxes

Income and Capital Gain Distributions

As a regulated investment company, the Fund generally pays no federal income tax on the income and gains it distributes to you. The Fund intends to pay income dividends at least annually from its net investment income. Capital gains, if any, may be paid at least annually. The Fund may distribute income dividends and capital gains more frequently, if necessary, in order to reduce or eliminate federal excise or income taxes on the Fund. The amount of any distribution will vary, and there is no guarantee the Fund will pay either income dividends or capital gain distributions. Your income dividends and capital gain distributions will be automatically reinvested in additional shares at net asset value (NAV) unless you elect to receive them in cash.

Annual statements. After the close of each calendar year, you will receive tax information from the Fund with respect to the federal income tax treatment of the Fund’s distributions and any taxable sales or exchanges of Fund shares occurring during the prior calendar year. If the Fund finds it necessary to reclassify its distributions or adjust the cost basis of any covered shares sold or exchanged after you receive your tax information, the Fund will send you revised tax information. Distributions declared in December to shareholders of record in such month and paid in January are taxable as if they were paid in December. Additional tax information about the Fund’s distributions is available at franklintempleton.com.

Avoid "buying a dividend." At the time you purchase your Fund shares, the Fund’s net asset value may reflect undistributed income, undistributed capital gains, or net unrealized appreciation in the value of the portfolio securities held by the Fund. For taxable investors, a subsequent distribution to you of such amounts, although constituting a return of your investment, would be taxable. Buying shares in the Fund just before it declares an income dividend or capital gain distribution is sometimes known as “buying a dividend.”

Tax Considerations

If you are a taxable investor, Fund distributions are generally taxable to you as ordinary income, capital gains or some combination of both. This is the case whether you reinvest your distributions in additional Fund shares or receive them in cash.

Dividend income. Income dividends are generally subject to tax at ordinary rates. Income dividends reported by the Fund to shareholders as qualified dividend income may be subject to tax by individuals at reduced long-term capital gains tax rates provided certain holding period requirements are met. A return-of-capital distribution is generally not taxable but will reduce the cost basis of your shares, and will result in a higher capital gain or a lower capital loss when you later sell your shares.

Capital gains. Fund distributions of short-term capital gains are also subject to tax at ordinary rates. Fund distributions of long-term capital gains are taxable at the reduced long-term capital gains rates no matter how long you have owned your Fund shares. For single individuals with taxable income not in excess of $40,400 in 2021 ($80,800 for married individuals filing jointly), the long-term capital gains tax rate is 0%. For single individuals and joint filers with taxable income in excess of these amounts but not more than $445,850 or $501,600, respectively, the long-term capital gains tax rate is 15%. The rate is 20% for single individuals with taxable income in excess of $445,850 and married individuals filing jointly with taxable income in excess of $501,600. An additional 3.8% Medicare tax may also be imposed as discussed below.

Sales of Fund shares. When you sell your shares in the Fund, or exchange them for shares of a different Franklin Templeton fund, you will generally recognize a taxable capital gain or loss. If you have owned your Fund shares for more than one year, any net long-term capital gains will qualify for the reduced rates of taxation on long-term capital gains. An exchange of your shares in one class of the Fund for shares of another class of the same Fund is not taxable and no gain or loss will be reported on the transaction.

Cost basis reporting. If you acquire shares in the Fund on or after January 1, 2012, generally referred to as “covered shares," and sell or exchange them after that date, the Fund is generally required to report cost basis information to you and the IRS annually. The Fund will compute the cost basis of your covered shares using the average cost method, the Fund’s “default method,” unless you contact the Fund to select a different method, or choose to specifically identify your shares at the time of each sale or exchange. If your account is held by your financial advisor or other broker-dealer, that firm may select a different default method. In these cases, please contact the firm to obtain information with respect to the available methods and elections for your account. Shareholders should carefully review the cost basis information provided by the Fund and make any additional basis, holding period or other adjustments that are required when reporting these amounts on their federal and state income tax returns. Additional information about cost basis reporting is available at franklintempleton.com/costbasis.

Medicare tax. An additional 3.8% Medicare tax is imposed on certain net investment income (including ordinary dividends and capital gain distributions received from the Fund and net gains from redemptions or other taxable dispositions of Fund shares) of U.S. individuals, estates and trusts to the extent that such person’s “modified adjusted gross income” (in the case of an individual) or “adjusted gross income” (in the case of an estate or trust) exceeds a threshold amount. Any liability for this additional Medicare tax is reported on, and paid with, your federal income tax return.

Backup withholding. A shareholder may be subject to backup withholding on any distributions of income, capital gains, or proceeds from the sale or exchange of Fund shares if the shareholder has provided either an incorrect tax identification number or no number at all, is subject to backup withholding by the IRS for failure to properly report payments of interest or dividends, has failed to certify that the shareholder is not subject to backup withholding, or has not certified that the shareholder is a U.S. person (including a U.S. resident alien). The backup withholding rate is currently 24%. State backup withholding may also apply.

State, local and foreign taxes. Distributions of ordinary income and capital gains, and gains from the sale of your Fund shares, are generally subject to state and local taxes. If the Fund qualifies, it may elect to pass through to you as a foreign tax credit or deduction any foreign taxes that it pays on its investments.

Non-U.S. investors. Non-U.S. investors may be subject to U.S. withholding tax at 30% or a lower treaty rate on Fund dividends of ordinary income. Non-U.S. investors may be subject to U.S. estate tax on the value of their shares. They are subject to special U.S. tax certification requirements to avoid backup withholding, claim any exemptions from withholding and claim any treaty benefits. Exemptions from U.S. withholding tax are generally provided for capital gains realized on the sale of Fund shares, capital gain dividends paid by the Fund from net long-term capital gains, short-term capital gain dividends paid by the Fund from net short-term capital gains and interest-related dividends paid by the Fund from its qualified net interest income from U.S. sources. However, notwithstanding such exemptions from U.S. withholding tax at source, any such dividends and distributions of income and capital gains will be subject to backup withholding at a rate of 24% if you fail to properly certify that you are not a U.S. person.

Other reporting and withholding requirements. Payments to a shareholder that is either a foreign financial institution or a non-financial foreign entity within the meaning of the Foreign Account Tax Compliance Act (FATCA) may be subject to a 30% withholding tax on income dividends paid by the Fund. The FATCA withholding tax generally can be avoided by such foreign entity if it provides the Fund, and in some cases, the IRS, information concerning the ownership of certain foreign financial accounts or other appropriate certifications or documentation concerning its status under FATCA. The Fund may be required to report certain shareholder account information to the IRS, non-U.S. taxing authorities or other parties to comply with FATCA.

Other tax information. This discussion of "Distributions and Taxes" is for general information only and is not tax advice. You should consult your own tax advisor regarding your particular circumstances, and about any federal, state, local and foreign tax consequences before making an investment in the Fund. Additional information about the tax consequences of investing in the Fund may be found in the SAI.

Financial Highlights

The Financial Highlights present the Fund's financial performance for the past five years or since its inception. Certain information reflects financial results for a single Fund share. The total returns represent the rate that an investor would have earned or lost on an investment in the Fund assuming reinvestment of dividends and capital gains. This information has been audited by PricewaterhouseCoopers LLP, an independent registered public accounting firm, whose report, along with the Fund's financial statements, are included in the annual report, which is available upon request.

| Class A | Year Ended August 31, | ||||

| 2020 | 2019 | 2018 | 2017 | 2016 | |

| Per share operating performance (for a share outstanding throughout the year) |

|||||

| Net asset value, beginning of year | $ 18.01 | $ 22.42 | $ 23.49 | $ 21.51 | $ 26.19 |

| Income from investment operations:a | |||||

| Net investment income (loss)b | -0.07 | 0.14 | 0.29c | 0.15 | 0.17 |

| Net realized and unrealized gains (losses) | 5.95 | -1.76 | 1.29 | 4.59 | 2.19 |

| Total from investment operations | 5.88 | -1.62 | 1.58 | 4.74 | 2.36 |

| Less distributions from: | |||||

| Net investment income | -0.13 | -0.30 | -0.25 | -0.19 | -0.46 |

| Net realized gains | -3.05 | -2.49 | -2.40 | -2.57 | -6.58 |

| Total distributions | -3.18 | -2.79 | -2.65 | -2.76 | -7.04 |

| Net asset value, end of year | $ 20.71 | $ 18.01 | $ 22.42 | $ 23.49 | $ 21.51 |

| Total returnd | 36.80% | -6.46% | 7.26% | 26.00% | 11.19% |

| Ratios to average net assets | |||||

| Expenses before waiver and payments by affiliates | 1.86% | 1.87% | 1.85% | 1.94% | 1.91% |

| Expenses net of waiver and payments by affiliates | 1.85% | 1.83% | 1.85%e | 1.94%e, f | 1.91%e, f |

| Net investment income (loss) | -0.39% | 0.76% | 1.26%c | 0.71% | 0.77% |

| Supplemental data | |||||

| Net assets, end of year (000’s) | $ 164,145 | $ 146,709 | $ 178,315 | $ 188,885 | $ 186,850 |

| Portfolio turnover rate | 59.87% | 5.69% | 12.15% | 7.92% | 3.87% |

a. The amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations in the annual report for the period due to the timing of sales and repurchases of the Fund’s shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

b. Based on average daily shares outstanding.

c. Net investment income per share includes approximately $0.10 per share related to income received in the form of special dividends in connection with certain Fund holdings. Excluding this amount, the ratio of net investment income to average net assets would have been 0.83%.

d. Total return does not reflect sales commissions or contingent deferred sales charges, if applicable.

e. Benefit of waiver and payments by affiliates rounds to less than 0.01%.

f. Benefit of expense reduction rounds to less than 0.01%.

| Class C | Year Ended August 31, | ||||

| 2020 | 2019 | 2018 | 2017 | 2016 | |

| Per share operating performance (for a share outstanding throughout the year) |

|||||

| Net asset value, beginning of year | $ 17.91 | $ 22.13 | $ 23.12 | $ 21.18 | $ 25.76 |

| Income from investment operations:a | |||||

| Net investment income (loss)b | -0.20 | -—c | 0.10d | -0.03 | —c |

| Net realized and unrealized gains (losses) | 5.91 | -1.72 | 1.31 | 4.54 | 2.17 |

| Total from investment operations | 5.71 | -1.72 | 1.41 | 4.51 | 2.17 |

| Less distributions from: | |||||

| Net investment income | — | -0.01 | -—c | — | -0.17 |

| Net realized gains | -3.05 | -2.49 | -2.40 | -2.57 | -6.58 |

| Total distributions | -3.05 | -2.50 | -2.40 | -2.57 | -6.75 |

| Net asset value, end of year | $ 20.57 | $ 17.91 | $ 22.13 | $ 23.12 | $ 21.18 |

| Total returne | 35.80% | -7.16% | 6.52% | 24.97% | 10.41% |

| Ratios to average net assets | |||||

| Expenses before waiver and payments by affiliates | 2.61% | 2.62% | 2.60% | 2.69% | 2.66% |

| Expenses net of waiver and payments by affiliates | 2.60% | 2.58% | 2.60%f | 2.69%f, g | 2.66%f, g |

| Net investment income (loss) | -1.15% | 0.01%h | 0.51%d | -0.04% | 0.02% |

| Supplemental data | |||||

| Net assets, end of year (000’s) | $ 12,376 | $ 15,744 | $ 36,678 | $ 42,577 | $ 48,769 |

| Portfolio turnover rate | 59.87% | 5.69% | 12.15% | 7.92% | 3.87% |

a. The amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations in the annual report for the period due to the timing of sales and repurchases of the Fund’s shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

b. Based on average daily shares outstanding.

c. Amount rounds to less than $0.01 per share.

d. Net investment income per share includes approximately $0.10 per share related to income received in the form of special dividends in connection with certain Fund holdings. Excluding this amount, the ratio of net investment income to average net assets would have been 0.08%.

e. Total return does not reflect sales commissions or contingent deferred sales charges, if applicable.

f. Benefit of waiver and payments by affiliates rounds to less than 0.01%.

g. Benefit of expense reduction rounds to less than 0.01%.

h. Ratio is calculated based on the Fund level net investment income, as reflected in the Statement of Operations in the annual report, and adjusted for class specific expenses. The amount may not correlate with the per share amount due to the timing of income earned and/or fluctuating fair value of the investments of the Fund in relation to the timing of sales and repurchases of Fund shares.

| Class R6 | Year Ended August 31, | ||||

| 2020 | 2019 | 2018 | 2017 | 2016 | |

| Per share operating performance (for a share outstanding throughout the year) |

|||||

| Net asset value, beginning of year | $ 18.14 | $ 22.55 | $ 23.66 | $ 21.68 | $ 26.41 |

| Income from investment operations:a | |||||

| Net investment incomeb | 0.01 | 0.26 | 0.45c | 0.27 | 0.31 |

| Net realized and unrealized gains (losses) | 5.99 | -1.81 | 1.25 | 4.59 | 2.18 |

| Total from investment operations | 6.00 | -1.55 | 1.70 | 4.86 | 2.49 |

| Less distributions from: | |||||

| Net investment income | -0.21 | -0.37 | -0.41 | -0.31 | -0.64 |

| Net realized gains | -3.05 | -2.49 | -2.40 | -2.57 | -6.58 |

| Total distributions | -3.26 | -2.86 | -2.81 | -2.88 | -7.22 |

| Net asset value, end of year | $ 20.88 | $ 18.14 | $ 22.55 | $ 23.66 | $ 21.68 |

| Total return | 37.42% | -6.08% | 7.75% | 26.62% | 11.76% |

| Ratios to average net assets | |||||

| Expenses before waiver and payments by affiliates | 1.56% | 1.57% | 1.50% | 1.49% | 1.45% |

| Expenses net of waiver and payments by affiliates | 1.42% | 1.42% | 1.42% | 1.44%d | 1.42%d |

| Net investment income | 0.05% | 1.17% | 1.69%c | 1.21% | 1.26% |

| Supplemental data | |||||

| Net assets, end of year (000’s) | $ 3,437 | $ 3,395 | $ 3,412 | $ 1,213 | $ 720 |

| Portfolio turnover rate | 59.87% | 5.69% | 12.15% | 7.92% | 3.87% |

a. The amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations in the annual report for the period due to the timing of sales and repurchases of the Fund’s shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

b. Based on average daily shares outstanding.

c. Net investment income per share includes approximately $0.10 per share related to income received in the form of special dividends in connection with certain Fund holdings. Excluding this amount, the ratio of net investment income to average net assets would have been 1.26%.

d. Benefit of expense reduction rounds to less than 0.01%.

| Advisor Class | Year Ended August 31, | ||||

| 2020 | 2019 | 2018 | 2017 | 2016 | |

| Per share operating performance (for a share outstanding throughout the year) |

|||||

| Net asset value, beginning of year | $ 18.18 | $ 22.60 | $ 23.68 | $ 21.68 | $ 26.39 |

| Income from investment operations:a | |||||

| Net investment income (loss)b | -0.02 | 0.20 | 0.35c | 0.22 | 0.22 |

| Net realized and unrealized gains (losses) | 6.01 | -1.79 | 1.30 | 4.60 | 2.22 |

| Total from investment operations | 5.99 | -1.59 | 1.65 | 4.82 | 2.44 |

| Less distributions from: | |||||

| Net investment income | -0.18 | -0.34 | -0.33 | -0.25 | -0.57 |

| Net realized gains | -3.05 | -2.49 | -2.40 | -2.57 | -6.58 |

| Total distributions | -3.23 | -2.83 | -2.73 | -2.82 | -7.15 |

| Net asset value, end of year | $ 20.94 | $ 18.18 | $ 22.60 | $ 23.68 | $ 21.68 |

| Total return | 37.20% | -6.25% | 7.54% | 26.31% | 11.51% |

| Ratios to average net assets | |||||

| Expenses before waiver and payments by affiliates | 1.61% | 1.62% | 1.60% | 1.69% | 1.66% |

| Expenses net of waiver and payments by affiliates | 1.60% | 1.58% | 1.60%d | 1.69%d, e | 1.66%d, e |

| Net investment income (loss) | -0.12% | 1.01% | 1.51%c | 0.96% | 1.02% |

| Supplemental data | |||||

| Net assets, end of year (000’s) | $ 74,741 | $ 67,189 | $ 79,456 | $ 83,172 | $ 73,504 |

| Portfolio turnover rate | 59.87% | 5.69% | 12.15% | 7.92% | 3.87% |

a. The amount shown for a share outstanding throughout the period may not correlate with the Statement of Operations in the annual report for the period due to the timing of sales and repurchases of the Fund’s shares in relation to income earned and/or fluctuating fair value of the investments of the Fund.

b. Based on average daily shares outstanding.

c. Net investment income per share includes approximately $0.10 per share related to income received in the form of special dividends in connection with certain Fund holdings. Excluding this amount, the ratio of net investment income to average net assets would have been 1.08%.

d. Benefit of waiver and payments by affiliates rounds to less than 0.01%.

e. Benefit of expense reduction rounds to less than 0.01%.

Your Account

Choosing a Share Class

Each class has its own sales charge and expense structure, allowing you to choose the class that best meets your situation. Some share classes may not be offered by certain financial intermediaries. Your financial intermediary or investment representative (financial advisor) can help you decide which class is best for you. Investors may purchase Class C shares only for Fund accounts on which they have appointed an investment representative (financial advisor) of record. Investors who have not appointed an investment representative (financial advisor) to existing Class C share Fund accounts may not make additional purchases to those accounts but may exchange their shares for shares of a Franklin Templeton fund that offers Class C shares. Dividend and capital gain distributions may continue to be reinvested in existing Class C share Fund accounts. These provisions do not apply to Employer Sponsored Retirement Plans.

| Class A | Class C | Class R6 | Advisor Class |

| Initial sales charge of 5.50% or less | No initial sales charge | See "Qualified Investors - Class R6" below | See "Qualified Investors - Advisor Class" below |

| Deferred sales charge of 1% on purchases of $1 million or more sold within 18 months | Deferred sales charge of 1% on shares you sell within 12 months | ||

| Lower annual expenses than Class C due to lower distribution fees | Higher annual expenses than Class A due to higher distribution fees. Automatic conversion to Class A shares after approximately ten years, reducing future annual expenses. |

Class A & C

The availability of certain sales charge waivers and discounts may depend on whether you purchase your shares directly from the Fund or through a financial intermediary. Different intermediaries may impose different sales charges (including potential reductions in or waivers of sales charges) other than those listed below. Such intermediary-specific sales charge variations are described in Appendix A to this prospectus, entitled "Intermediary Sales Charge Discounts and Waivers." Appendix A is incorporated herein by reference (is legally a part of this prospectus).

In all instances, it is the purchaser's responsibility to notify the Fund or the purchaser's financial intermediary at the time of purchase of any relationship or other facts qualifying the purchaser for sales charge waivers or discounts. For waivers and discounts not available through a particular intermediary, shareholders will have to purchase Fund shares directly from the Fund or through another intermediary to receive these waivers or discounts.

| Sales Charges - Class A | ||

| when you invest this amount | the sales charge makes up this % of the offering price1 | which equals this % of your net investment1 |

| Under $50,000 | 5.50 | 5.82 |

| $50,000 but under $100,000 | 4.50 | 4.71 |

| $100,000 but under $250,000 | 3.50 | 3.63 |

| $250,000 but under $500,000 | 2.50 | 2.56 |

| $500,000 but under $1 million | 2.00 | 2.04 |

| $1 million or more | 0.00 | 0.00 |

1. The dollar amount of the sales charge is the difference between the offering price of the shares purchased (which factors in the applicable sales charge in this table) and the net asset value of those shares. Since the offering price is calculated to two decimal places using standard rounding criteria, the number of shares purchased and the dollar amount of the sales charge as a percentage of the offering price and of your net investment may be higher or lower depending on whether there was a downward or upward rounding.

Sales Charge Reductions

Quantity discounts. We offer two ways for you to combine your current purchase of Class A Fund shares with other existing Franklin Templeton fund share holdings that might enable you to qualify for a lower sales charge with your current purchase. You can qualify for a lower sales charge when you reach certain "sales charge breakpoints." This quantity discount information is also available free of charge at franklintempleton.com/quantity-discounts. This web page can also be reached at franklintempleton.com by clicking the "Products & Planning" tab and then choosing "Quantity Discounts for Class A Shares" under "Fund Resources."

1. Cumulative quantity discount - lets you combine certain existing holdings of Franklin Templeton fund shares - referred to as "cumulative quantity discount eligible shares" - with your current purchase of Class A shares to determine if you qualify for a sales charge breakpoint.

Cumulative quantity discount eligible shares are Franklin Templeton fund shares registered to (or held by a financial intermediary for):

- You, individually;

- Your "family member," defined as your spouse or domestic partner, as recognized by applicable state law, and your children under the age of 21;

- You jointly with one or more family members;

- You jointly with another person(s) who is (are) not family members if that other person has not included the value of the jointly-owned shares as cumulative quantity discount eligible shares for purposes of that person’s separate investments in Franklin Templeton fund shares;

- A Coverdell Education Savings account for which you or a family member is the identified responsible person;

- A trustee/custodian of an IRA (which includes a Roth IRA and an employer sponsored IRA such as a SIMPLE IRA) or your non-ERISA covered 403(b) plan account, if the shares are registered/recorded under your or a family member's Social Security number;

- A 529 college savings plan over which you or a family member has investment discretion and control;

- Any entity over which you or a family member has (have) individual or shared authority, as principal, has investment discretion and control (for example, an UGMA/UTMA account for a child on which you or a family member is the custodian, a trust on which you or a family member is the trustee, a business account [not to include retirement plans] for your solely owned business [or the solely owned business of a family member] on which you or a family member is the authorized signer);

- A trust established by you or a family member as grantor.

Franklin Templeton fund shares held through an administrator or trustee/custodian of an Employer Sponsored Retirement Plan (see definition below) such as a 401(k) plan do not qualify for a cumulative quantity discount.

Franklin Templeton fund assets held in multiple Employer Sponsored Retirement Plans may be combined in order to qualify for sales charge breakpoints at the plan level if the plans are sponsored by the same employer.

If you believe there are cumulative quantity discount eligible shares that can be combined with your current purchase to achieve a sales charge breakpoint (for example, shares held in a different broker-dealer’s brokerage account or with a bank or an investment advisor), it is your responsibility to specifically identify those shares to your financial advisor at the time of your purchase (including at the time of any future purchase). It may be necessary for you to provide your financial advisor with information and records (including account statements) of all relevant accounts invested in the Franklin Templeton funds. If you have not designated a financial advisor associated with your Franklin Templeton fund shares, it is your responsibility to specifically identify any cumulative quantity discount eligible shares to the Fund’s transfer agent at the time of any purchase.

If there are cumulative quantity discount eligible shares that would qualify for combining with your current purchase and you do not tell your financial advisor or the Franklin Templeton funds’ transfer agent at the time of any purchase, you may not receive the benefit of a reduced sales charge that might otherwise be available since your financial advisor and the Fund generally will not have that information.