485BPOS3/31/20230000908406false2.585.860.033.564.571.409.047.960.5315.192.296.230.412.723.541.268.588.250.5613.7011.802.134.8817.296.982.0112.677.996.5311.206.091.395.5813.975.953.3213.215.864.4511.820.417.296.001.659.779.142.5510.330.010.010.010.100.591.541.820.400.011.350.210.530.841.921.411.333.954.021.024.172.281.730.503.250.730.074.775.066.303.900.815.442.800.255.235.442.045.820.010.010.010.030.441.411.790.290.011.2600009084062023-08-012023-08-010000908406ck0000908406:InvestmentTrustProspectusMemberck0000908406:S000014384Member2023-08-012023-08-010000908406ck0000908406:InvestmentTrustProspectusMemberck0000908406:C000039168Memberck0000908406:S000014384Member2023-08-012023-08-010000908406ck0000908406:InvestmentTrustProspectusMemberck0000908406:C000189691Memberck0000908406:S000014384Member2023-08-012023-08-010000908406ck0000908406:InvestmentTrustProspectusMemberck0000908406:C000039170Memberck0000908406:S000014384Member2023-08-012023-08-010000908406ck0000908406:InvestmentTrustProspectusMemberck0000908406:C000039172Memberck0000908406:S000014384Member2023-08-012023-08-010000908406ck0000908406:C000039173Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:S000014384Member2023-08-012023-08-010000908406ck0000908406:C000039169Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:S000014384Member2023-08-012023-08-010000908406ck0000908406:C000222299Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:S000014384Member2023-08-012023-08-01iso4217:USDxbrli:pure0000908406ck0000908406:InvestmentTrustProspectusMemberrr:AfterTaxesOnDistributionsMemberck0000908406:C000039168Memberck0000908406:S000014384Member2023-08-012023-08-010000908406ck0000908406:InvestmentTrustProspectusMemberck0000908406:C000039168Memberrr:AfterTaxesOnDistributionsAndSalesMemberck0000908406:S000014384Member2023-08-012023-08-010000908406ck0000908406:BloombergUSAggregateBondIndexMemberck0000908406:InvestmentTrustProspectusMemberck0000908406:S000014384Member2023-08-012023-08-010000908406ck0000908406:S000006579Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000006579Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:C000017955Member2023-08-012023-08-010000908406ck0000908406:S000006579Memberck0000908406:C000017957Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000006579Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:C000189684Member2023-08-012023-08-010000908406ck0000908406:C000017956Memberck0000908406:S000006579Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000006579Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:C000017960Member2023-08-012023-08-010000908406ck0000908406:S000006579Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:C000017961Member2023-08-012023-08-010000908406ck0000908406:S000006579Memberck0000908406:C000189686Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000006579Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:C000131613Member2023-08-012023-08-010000908406ck0000908406:C000237256Memberck0000908406:S000006579Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000006579Memberck0000908406:C000017957Memberck0000908406:InvestmentTrustProspectusMemberrr:AfterTaxesOnDistributionsMember2023-08-012023-08-010000908406ck0000908406:S000006579Memberck0000908406:C000017957Memberck0000908406:InvestmentTrustProspectusMemberrr:AfterTaxesOnDistributionsAndSalesMember2023-08-012023-08-010000908406ck0000908406:S000006579Memberck0000908406:BloombergUSAggregateBondIndexMemberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000058290Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000058290Memberck0000908406:C000191071Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000058290Memberck0000908406:C000191072Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000058290Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:C000191073Member2023-08-012023-08-010000908406ck0000908406:S000058290Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:C000191074Member2023-08-012023-08-010000908406ck0000908406:S000058290Memberck0000908406:C000191075Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000058290Memberck0000908406:C000191076Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000058290Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:C000237257Member2023-08-012023-08-010000908406ck0000908406:S000058290Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:C000191073Memberrr:AfterTaxesOnDistributionsMember2023-08-012023-08-010000908406ck0000908406:S000058290Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:C000191073Memberrr:AfterTaxesOnDistributionsAndSalesMember2023-08-012023-08-010000908406ck0000908406:S000058290Memberck0000908406:ICEBofAUSHighYieldConstrainedIndexIndexMemberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:InvestmentTrustProspectusMemberck0000908406:S000006580Member2023-08-012023-08-010000908406ck0000908406:InvestmentTrustProspectusMemberck0000908406:C000017962Memberck0000908406:S000006580Member2023-08-012023-08-010000908406ck0000908406:InvestmentTrustProspectusMemberck0000908406:C000189687Memberck0000908406:S000006580Member2023-08-012023-08-010000908406ck0000908406:InvestmentTrustProspectusMemberck0000908406:C000189688Memberck0000908406:S000006580Member2023-08-012023-08-010000908406ck0000908406:InvestmentTrustProspectusMemberck0000908406:C000017963Memberck0000908406:S000006580Member2023-08-012023-08-010000908406ck0000908406:C000017967Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:S000006580Member2023-08-012023-08-010000908406ck0000908406:C000017968Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:S000006580Member2023-08-012023-08-010000908406ck0000908406:C000017964Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:S000006580Member2023-08-012023-08-010000908406ck0000908406:C000131614Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:S000006580Member2023-08-012023-08-010000908406ck0000908406:InvestmentTrustProspectusMemberck0000908406:C000017962Memberrr:AfterTaxesOnDistributionsMemberck0000908406:S000006580Member2023-08-012023-08-010000908406ck0000908406:InvestmentTrustProspectusMemberck0000908406:C000017962Memberck0000908406:S000006580Memberrr:AfterTaxesOnDistributionsAndSalesMember2023-08-012023-08-010000908406ck0000908406:BloombergUSHighYield2IssuerCappedBondIndexMemberck0000908406:InvestmentTrustProspectusMemberck0000908406:S000006580Member2023-08-012023-08-010000908406ck0000908406:InvestmentTrustProspectusMemberck0000908406:S000046094Member2023-08-012023-08-010000908406ck0000908406:C000144171Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:S000046094Member2023-08-012023-08-010000908406ck0000908406:InvestmentTrustProspectusMemberck0000908406:S000046094Memberck0000908406:C000189695Member2023-08-012023-08-010000908406ck0000908406:InvestmentTrustProspectusMemberck0000908406:C000189696Memberck0000908406:S000046094Member2023-08-012023-08-010000908406ck0000908406:InvestmentTrustProspectusMemberck0000908406:S000046094Memberck0000908406:C000144173Member2023-08-012023-08-010000908406ck0000908406:InvestmentTrustProspectusMemberck0000908406:S000046094Memberck0000908406:C000144168Member2023-08-012023-08-010000908406ck0000908406:C000144169Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:S000046094Member2023-08-012023-08-010000908406ck0000908406:InvestmentTrustProspectusMemberck0000908406:S000046094Memberck0000908406:C000144172Member2023-08-012023-08-010000908406ck0000908406:InvestmentTrustProspectusMemberck0000908406:S000046094Memberck0000908406:C000144170Member2023-08-012023-08-010000908406ck0000908406:C000144171Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:S000046094Memberrr:AfterTaxesOnDistributionsMember2023-08-012023-08-010000908406ck0000908406:C000144171Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:S000046094Memberrr:AfterTaxesOnDistributionsAndSalesMember2023-08-012023-08-010000908406ck0000908406:BloombergUSAggregateBondIndexMemberck0000908406:InvestmentTrustProspectusMemberck0000908406:S000046094Member2023-08-012023-08-010000908406ck0000908406:S000006583Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000006583Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:C000017976Member2023-08-012023-08-010000908406ck0000908406:S000006583Memberck0000908406:C000017977Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000006583Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:C000017980Member2023-08-012023-08-010000908406ck0000908406:InvestmentTrustProspectusMemberck0000908406:S000014385Member2023-08-012023-08-010000908406ck0000908406:C000039177Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:S000014385Member2023-08-012023-08-010000908406ck0000908406:InvestmentTrustProspectusMemberck0000908406:S000014385Memberck0000908406:C000189692Member2023-08-012023-08-010000908406ck0000908406:InvestmentTrustProspectusMemberck0000908406:C000039179Memberck0000908406:S000014385Member2023-08-012023-08-010000908406ck0000908406:C000039175Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:S000014385Member2023-08-012023-08-010000908406ck0000908406:C000039176Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:S000014385Member2023-08-012023-08-010000908406ck0000908406:InvestmentTrustProspectusMemberck0000908406:C000039178Memberck0000908406:S000014385Member2023-08-012023-08-010000908406ck0000908406:C000194393Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:S000014385Member2023-08-012023-08-010000908406ck0000908406:C000224786Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:S000014385Member2023-08-012023-08-010000908406ck0000908406:C000039177Memberck0000908406:InvestmentTrustProspectusMemberrr:AfterTaxesOnDistributionsMemberck0000908406:S000014385Member2023-08-012023-08-010000908406ck0000908406:C000039177Memberck0000908406:InvestmentTrustProspectusMemberrr:AfterTaxesOnDistributionsAndSalesMemberck0000908406:S000014385Member2023-08-012023-08-010000908406ck0000908406:BloombergUS13YearGovernmentCreditBondIndexIndexMemberck0000908406:InvestmentTrustProspectusMemberck0000908406:S000014385Member2023-08-012023-08-010000908406ck0000908406:S000006581Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000006581Memberck0000908406:C000017969Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000006581Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:C000189689Member2023-08-012023-08-010000908406ck0000908406:S000006581Memberck0000908406:C000189690Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:C000017971Memberck0000908406:S000006581Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000006581Memberck0000908406:C000017973Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000006581Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:C000017974Member2023-08-012023-08-010000908406ck0000908406:S000006581Memberck0000908406:C000017970Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000006581Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:C000131615Member2023-08-012023-08-010000908406ck0000908406:S000006581Memberck0000908406:C000194391Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000006581Memberck0000908406:C000017969Memberck0000908406:InvestmentTrustProspectusMemberrr:AfterTaxesOnDistributionsMember2023-08-012023-08-010000908406ck0000908406:S000006581Memberck0000908406:C000017969Memberck0000908406:InvestmentTrustProspectusMemberrr:AfterTaxesOnDistributionsAndSalesMember2023-08-012023-08-010000908406ck0000908406:S000006581Memberck0000908406:BloombergUS15YearTreasuryInflationProtectedSecuritiesTIPSIndexIndexMemberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000046093Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000046093Memberck0000908406:C000144162Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000046093Memberck0000908406:C000189693Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000046093Memberck0000908406:C000189694Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000046093Memberck0000908406:C000144164Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000046093Memberck0000908406:C000144165Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000046093Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:C000144166Member2023-08-012023-08-010000908406ck0000908406:S000046093Memberck0000908406:C000144163Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000046093Memberck0000908406:C000144167Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000046093Memberck0000908406:C000144162Memberck0000908406:InvestmentTrustProspectusMemberrr:AfterTaxesOnDistributionsMember2023-08-012023-08-010000908406ck0000908406:S000046093Memberck0000908406:C000144162Memberck0000908406:InvestmentTrustProspectusMemberrr:AfterTaxesOnDistributionsAndSalesMember2023-08-012023-08-010000908406ck0000908406:S000046093Memberck0000908406:BloombergUS13YearGovernmentCreditBondIndexIndexMemberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000006582Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000006582Memberck0000908406:C000017975Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000006582Memberck0000908406:C000162988Memberck0000908406:InvestmentTrustProspectusMember2023-08-012023-08-010000908406ck0000908406:S000006582Memberck0000908406:InvestmentTrustProspectusMemberck0000908406:C000162989Member2023-08-012023-08-01

As Filed with the U.S. Securities and Exchange Commission on July 28, 2023

1933 Act File No. 033-65170

1940 Act File No. 811-07822

| | | | | |

UNITED STATES SECURITIES AND EXCHANGE COMMISSION WASHINGTON, D.C. 20549 |

__________________ |

FORM N-1A |

__________________ |

| | |

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933 | x |

| |

| Pre-Effective Amendment No. | ☐ |

| |

| Post-Effective Amendment No. 83 | x |

| |

| and/or |

| |

REGISTRATION STATEMENT UNDER THE INVESTMENT COMPANY ACT OF 1940 | x |

| | |

| Amendment No. 84 | x |

| (Check appropriate box or boxes.) |

__________________ |

American Century Investment Trust (Exact Name of Registrant as Specified in Charter) |

__________________ |

4500 MAIN STREET, KANSAS CITY, MISSOURI 64111 (Address of Principal Executive Offices)(Zip Code) |

REGISTRANT’S TELEPHONE NUMBER, INCLUDING AREA CODE: (816) 531-5575 |

JOHN PAK 4500 MAIN STREET, KANSAS CITY, MISSOURI 64111 (Name and Address of Agent for Service) |

| Approximate Date of Proposed Public Offering: August 1, 2023 | |

| |

| It is proposed that this filing will become effective (check appropriate box) |

| | | | | |

| ☐ | immediately upon filing pursuant to paragraph (b) |

| x | on August 1, 2023, at 8:30 AM (Central) pursuant to paragraph (b) |

| ☐ | 60 days after filing pursuant to paragraph (a)(1) |

| ☐ | on (date) pursuant to paragraph (a)(1) |

| ☐ | 75 days after filing pursuant to paragraph (a)(2) |

| ☐ | on (date) pursuant to paragraph (a)(2) of rule 485 |

| | |

| If appropriate, check the following box: |

| ☐ | this post-effective amendment designates a new effective date for a previously filed post-effective amendment. |

August 1, 2023

American Century Investments

Prospectus

Core Plus Fund

Investor Class (ACCNX)

I Class (ACCTX)

A Class (ACCQX)

C Class (ACCKX)

R Class (ACCPX)

R5 Class (ACCUX)

G Class (ACCYX)

| | | | | |

The Securities and Exchange Commission has not approved or disapproved these securities or passed upon the adequacy of this prospectus. Any representation to the contrary is a criminal offense. | |

Table of Contents

| | | | | |

Fund Summary | 2 | |

| Investment Objective | 2 | |

| Fees and Expenses | 2 | |

| Principal Investment Strategies | 3 | |

| Principal Risks | 3 | |

| Fund Performance | 4 | |

| Portfolio Management | 5 | |

| Purchase and Sale of Fund Shares | 6 | |

| Tax Information | 6 | |

| Payments to Broker-Dealers and Other Financial Intermediaries | 6 | |

Objectives, Strategies and Risks | 7 | |

Management | 10 | |

Investing Directly with American Century Investments | 12 | |

Investing Through a Financial Intermediary | 14 | |

Additional Policies Affecting Your Investment | 19 | |

Share Price and Distributions | 23 | |

Taxes | 25 | |

Multiple Class Information | 27 | |

Financial Highlights | 28 | |

| |

| Appendix A | A-1 |

©2023 American Century Proprietary Holdings, Inc. All rights reserved.

Fund Summary

Investment Objective

The fund seeks to maximize total return. As a secondary objective, the fund seeks a high level of income.

Fees and Expenses

The following table describes the fees and expenses you may pay if you buy, hold and sell shares of the fund. You may pay other fees, such as brokerage commissions and other fees to financial intermediaries, which are not reflected in the tables and examples below. You may qualify for sales charge discounts if you and your family invest, or agree to invest in the future, at least $100,000 in American Century Investments funds. More information about these and other discounts is available from your financial professional and in Calculation of Sales Charges on page 14 of the fund’s prospectus, Appendix A of the fund’s prospectus and Sales Charges in Appendix B of the statement of additional information.

| | | | | | | | | | | | | | | | | | | | | | | |

Shareholder Fees (fees paid directly from your investment) | | |

| | Investor | I | A | C | R | R5 | G |

Maximum Sales Charge (Load) Imposed on

Purchases (as a percentage of offering price) | None | None | 4.50% | None | None | None | None |

Maximum Deferred Sales Charge (Load) (as a

percentage of the lower of the original offering price or redemption proceeds when redeemed within one year of purchase) | None | None | None¹ | 1.00% | None | None | None |

Maximum Annual Account Maintenance Fee

(waived if eligible investments total at least $10,000) | $25 | None | None | None | None | None | None |

| | | | | | | | | | | | | | | | | | | | | | | |

Annual Fund Operating Expenses (expenses that you pay each year as a percentage of the value of your investment) |

| | Investor | I | A | C | R | R5 | G |

| Management Fee | 0.54% | 0.44% | 0.54% | 0.54% | 0.54% | 0.34% | 0.34% |

| Distribution and Service (12b-1) Fees | None | None | 0.25% | 1.00% | 0.50% | None | None |

| Other Expenses | 0.01% | 0.01% | 0.01% | 0.01% | 0.01% | 0.01% | 0.01% |

| Total Annual Fund Operating Expenses | 0.55% | 0.45% | 0.80% | 1.55% | 1.05% | 0.35% | 0.35% |

| Fee Waiver | None | None | None | None | None | None | 0.34%² |

| Total Annual Fund Operating Expenses After Fee Waiver | 0.55% | 0.45% | 0.80% | 1.55% | 1.05% | 0.35% | 0.01% |

1 Purchases of $1 million or more may be subject to a contingent deferred sales charge of 1.00% if the shares are redeemed within one year of the date of the purchase.

2 The advisor has agreed to waive the G Class’s management fee in its entirety. The advisor expects this waiver to remain in effect permanently and cannot terminate it without the approval of the Board of Trustees.

Example

The example below is intended to help you compare the costs of investing in the fund with the costs of investing in other mutual funds. The example assumes that you invest $10,000 in the fund for the time periods indicated and then redeem all of your shares at the end of those periods and that you earn a 5% return each year. The example also assumes that the fund’s operating expenses remain the same, except that it reflects the rate and duration of any fee waivers noted in the table above. Although your actual costs may be higher or lower, based on these assumptions your costs would be:

| | | | | | | | | | | | | | |

| | 1 year | 3 years | 5 years | 10 years |

| Investor Class | $56 | $177 | $308 | $690 |

| I Class | $46 | $145 | $252 | $567 |

| A Class | $528 | $694 | $875 | $1,396 |

| C Class | $158 | $490 | $845 | $1,643 |

| R Class | $107 | $335 | $580 | $1,282 |

| R5 Class | $36 | $113 | $197 | $444 |

| G Class | $1 | $3 | $6 | $13 |

Portfolio Turnover

The fund pays transaction costs, such as commissions, when it buys and sells securities (or “turns over” its portfolio). A higher portfolio turnover rate may indicate higher transaction costs and may result in higher taxes when fund shares are held in a taxable account. These costs, which are not reflected in annual fund operating expenses or in the example, affect the fund’s performance. During the most recent fiscal year, the fund’s portfolio turnover rate was 174% of the average value of its portfolio.

Principal Investment Strategies

The fund invests in debt securities such as notes, bonds, commercial paper, mortgage- or asset-backed securities, collateralized loan obligations, collateralized mortgage obligations, and U.S. Treasury securities. These securities may be payable in U.S. or foreign currencies.

The fund invests at least 65% of its assets in investment-grade, non-money market debt securities. An investment-grade security is one that has been rated by a nationally recognized statistical rating organization in its top four credit quality categories or determined by the advisor to be of comparable credit quality. The fund may invest up to 35% of its assets in high-yield debt securities. A high-yield security, or junk bond, is one that has been rated below the four highest categories used by a nationally recognized statistical rating organization, or determined by the investment advisor to be of similar quality. The fund may also invest in securities issued by companies that are located in emerging market countries—emerging market securities.

The fund may invest in non-dollar denominated debt securities. The weighted average maturity of the fund’s portfolio must be 3½ years or longer.

The fund may invest in securities issued or guaranteed by the U.S. Treasury and certain U.S. government agencies or instrumentalities such as the Government National Mortgage Association (Ginnie Mae). Ginnie Mae is supported by the full faith and credit of the U.S. government. Securities issued or guaranteed by other U.S. government agencies or instrumentalities, such as the Federal National Mortgage Association (Fannie Mae), the Federal Home Loan Mortgage Corporation (Freddie Mac), and the Federal Home Loan Bank (FHLB) are not guaranteed by the U.S. Treasury or supported by the full faith and credit of the U.S. government. However, they are authorized to borrow from the U.S. Treasury to meet their obligations.

In addition to the debt securities described above, the fund may also invest in bank loans.

The fund also may invest in derivative instruments provided that such investments are in keeping with the fund’s investment objectives. Such derivative instruments may include options, futures contracts, options on futures contracts, and swaps (including credit default swaps). The fund may use foreign currency exchange contracts to shift investment exposure from one currency into another for hedging purposes or to enhance returns.

The portfolio managers select securities using an approach that integrates macroeconomic inputs, technical analysis of the relative value among various sectors, and fundamental research on individual securities. The macroeconomic framework provides interest rate and duration guidelines for the fund by analyzing economic activity, inflation, and monetary policy. Portfolio managers select individual securities using in-depth fundamental analysis designed to provide a detailed understanding of the credit worthiness of a security and its related market. As the market environment and investment opportunities change, portfolio managers buy and sell securities to meet the fund’s evolving sector allocations and credit quality standards.

The fund may engage in active and frequent trading of portfolio securities to achieve its principal investment strategies. This may cause higher transaction costs and may affect performance. It may also result in the realization and distribution of capital gains.

Principal Risks

•Interest Rate Risk – Investments in debt securities are sensitive to interest rate changes. Generally, the value of debt securities and the funds that hold them decline as interest rates rise. This fund is more susceptible to interest rate changes than funds that have a shorter-weighted average maturity, such as money market and short-term bond funds. A period of rising interest rates may negatively affect the fund’s performance.

•Credit Risk – The inability or perceived inability of a security’s issuer to make interest and principal payments may cause the value of the security to decrease. As a result the fund’s share price could also decrease. Changes in the credit rating of a debt security held by the fund could have a similar effect.

•High-Yield Risk – Issuers of high-yield securities are more vulnerable to real or perceived economic changes (such as an economic downturn or a prolonged period of rising interest rates), political changes or adverse developments specific to an issuer. These factors may be more likely to cause an issuer of low quality bonds to default on its obligations.

•Liquidity Risk – During periods of market turbulence or unusually low trading activity, to meet redemptions it may be necessary for the fund to sell securities at prices that could have an adverse effect on the fund’s price. Changing regulatory and market conditions, including increases in interest rates and credit spreads may adversely affect the liquidity of the fund’s investments.

•Prepayment and Extension Risk – The fund may invest in debt securities backed by mortgages or other assets. If these underlying assets are prepaid, the fund may benefit less from declining interest rates than funds of similar maturity that invest less heavily in mortgage- and asset-backed securities. Conversely, an issuer may exercise its right to pay principal on an obligation held by the fund later than expected (extend the obligation) especially in periods of rising interest rates. These events may lengthen the maturity and potentially reduce the value of these securities.

•Collateralized Obligations Risk – Collateralized obligations, such as collateralized loan obligations (CLOs), are subject to credit, interest rate, valuation, and prepayment and extension risks. These securities also are subject to risk of default on the underlying asset, particularly during periods of economic downturn. The market value of collateralized obligations may be affected by, among other things, changes in the market value of the underlying assets held by the collateralized obligations, changes in the distributions on the underlying assets, defaults and recoveries on the underlying assets, capital gains and losses on the underlying assets, prepayments on underlying assets, and prices and interest rates of underlying assets. Some of the collateralized obligations in which the fund invests may be covenant-lite loans. Covenant-lite loans contain fewer or less restrictive constraints on the borrower. The fund may have fewer rights against a borrower and an accompanying greater risk of loss when it invests in covenant-lite loans.

•Foreign Securities Risk – Foreign securities are generally riskier than U.S. securities. Political events (such as civil unrest, national elections and imposition of exchange controls), social and economic events (such as labor strikes and rising inflation), natural disasters and public health emergencies occurring in a country where the fund invests could cause the fund’s investments in that country to experience losses. Securities of foreign issuers may be less liquid, more volatile and harder to value than U.S. securities.

•Currency Risk – Because the fund may invest in securities denominated in foreign currencies, the fund could experience gains or losses based solely on changes in the exchange rate between foreign currencies and the U.S. dollar.

•Emerging Markets Risk – Investing in emerging market countries generally is also riskier than investing in foreign developed countries. Emerging market countries may have unstable governments and/or economies that are subject to sudden change, and significant volatility in their financial markets. These countries also may lack the legal, business and social framework to support securities markets.

•Derivatives Risk – The use of derivative instruments involves risks different from, or possibly greater than, the risks associated with investing directly in securities and other traditional instruments. Derivatives are subject to a number of risks, including liquidity, interest rate, market, credit, and correlation risk. Derivatives used for hedging or risk management may not operate as intended, may expose the fund to other risks, and may be insufficient to protect the fund from the risks they were intended to hedge.

•Bank Loan Risk – The market for bank loans may not be highly liquid and the fund may have difficulty selling them. Bank loans may not be considered securities, thus the fund may not be afforded anti-fraud protections available under the federal securities laws. In connection with purchasing loan participations, the fund generally will have no right to enforce compliance by borrowers with loan terms nor any set off rights, and the fund may not benefit directly from any posted collateral. As a result, the fund may be subject to the credit risk of both the borrower and the lender selling the participation. Bank loan transactions may take more than seven days to settle, meaning that proceeds would be unavailable to make additional investments or meet redemptions.

•Market Risk – The value of securities owned by the fund may go up and down, sometimes rapidly or unpredictably. Market risks, including political, regulatory, economic and social developments, can affect the value of the fund’s investments. Natural disasters, public health emergencies, war, terrorism and other unforeseeable events may lead to increased market volatility and may have adverse long-term effects on world economies and markets generally.

•Redemption Risk – The fund may need to sell securities at times it would not otherwise do so in order to meet shareholder redemption requests. Selling securities to meet such redemptions may cause the fund to experience a loss, increase the fund’s transaction costs or have tax consequences. To the extent that a large shareholder (including a fund of funds or 529 college savings plan) invests in the fund, the fund may experience relatively large redemptions as such shareholder reallocates its assets.

•Principal Loss – At any given time your shares may be worth less than the price you paid for them. In other words, it is possible to lose money by investing in the fund.

An investment in the fund is not a bank deposit, and it is not insured or guaranteed by the Federal Deposit Insurance Corporation (FDIC) or any other government agency.

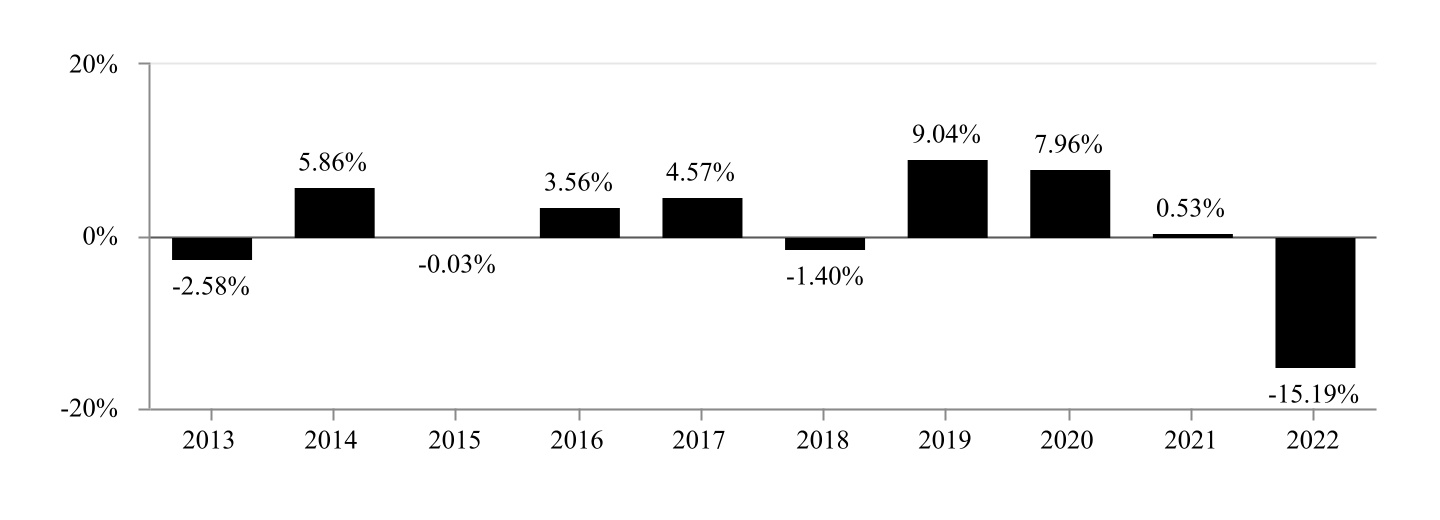

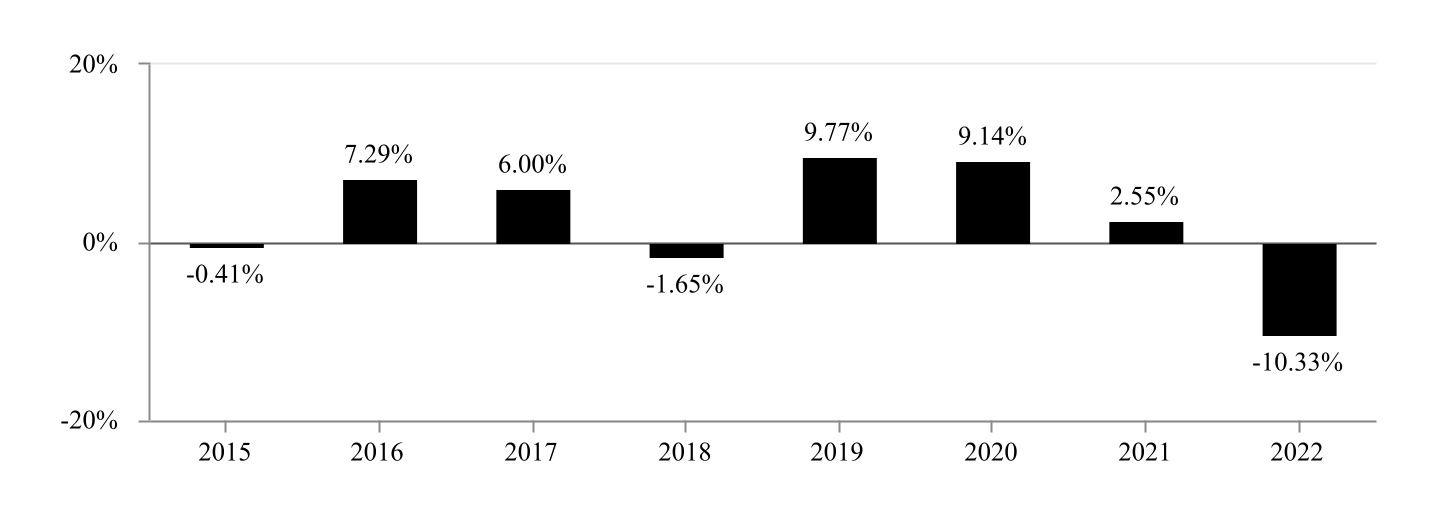

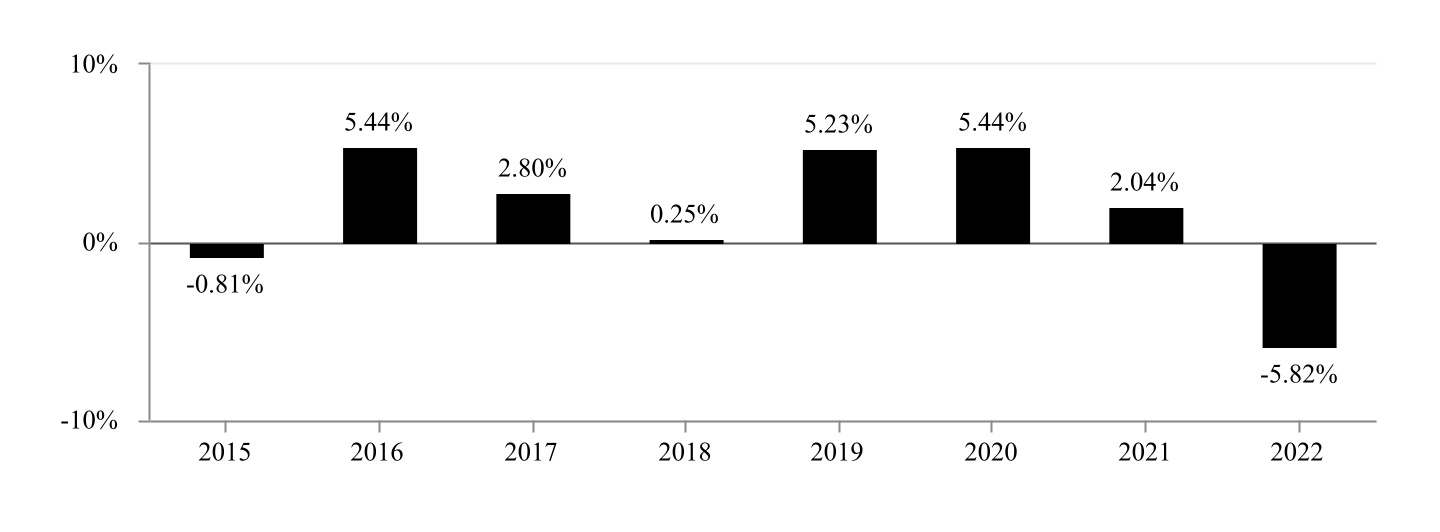

Fund Performance

The following bar chart and table provide some indication of the risks of investing in the fund. The bar chart shows changes in the fund’s performance from year to year for Investor Class shares. The table shows how the fund’s average annual returns for the periods shown compared with those of a broad measure of market performance. The fund’s past performance (before and after taxes) is not necessarily an indication of how the fund will perform in the future. For current performance information, including yields, please visit americancentury.com.

Sales charges and account fees, if applicable, are not reflected in the bar chart. If those charges were included, returns would be less than those shown.

Calendar Year Total Returns

Highest Performance Quarter (2Q 2020): 4.64% Lowest Performance Quarter (1Q 2022): -6.24%

As of June 30, 2023, the most recent calendar quarter end, the fund’s Investor Class year-to-date return was 1.84%.

| | | | | | | | | | | | | | | | | |

Average Annual Total Returns For the calendar year ended December 31, 2022 | 1 year | 5 years | 10 years | Since Inception | Inception Date |

Investor Class Return Before Taxes | -15.19% | -0.21% | 1.00% | — | 11/30/2006 |

| Return After Taxes on Distributions | -16.18% | -1.39% | -0.23% | — | 11/30/2006 |

| Return After Taxes on Distributions and Sale of Fund Shares | -8.97% | -0.60% | 0.26% | — | 11/30/2006 |

I Class1 Return Before Taxes | -15.11% | -0.09% | 1.10% | — | 04/10/2017 |

A Class Return Before Taxes | -19.21% | -1.37% | 0.29% | — | 11/30/2006 |

C Class2 Return Before Taxes | -16.04% | -1.18% | 0.15% | — | 11/30/2006 |

R Class Return Before Taxes | -15.62% | -0.71% | 0.50% | — | 11/30/2006 |

R5 Class Return Before Taxes | -14.95% | 0.01% | 1.20% | — | 11/30/2006 |

G Class Return Before Taxes | -14.75% | — | — | -5.93% | 11/04/2020 |

Bloomberg U.S. Aggregate Bond Index (reflects no deduction for fees, expenses or taxes) | -13.01% | 0.02% | 1.06% | — | — |

1 Historical performance for the I Class prior to its inception is based on the performance of R5 Class shares. I Class performance has been adjusted to reflect differences in expenses between classes, if applicable.

2 C Class shares automatically convert to A Class shares after approximately eight years. All returns for periods greater than eight years reflect this conversion.

The after-tax returns are shown only for Investor Class shares. After-tax returns for other share classes will vary. After-tax returns are calculated using the historical highest individual federal marginal income tax rates and do not reflect the impact of state and local taxes. Actual after-tax returns depend on an investor’s tax situation and may differ from those shown. After-tax returns are not relevant to investors who hold their fund shares through tax-deferred arrangements, such as 401(k) plans or IRAs.

Portfolio Management

Investment Advisor

American Century Investment Management, Inc.

Portfolio Managers

Robert V. Gahagan, Senior Vice President and Senior Portfolio Manager, has served on teams managing fixed-income investments since joining the advisor in 1983.

Charles Tan, Senior Vice President and Co-Chief Investment Officer, Global Fixed Income, has served on teams managing fixed-income investments since joining the advisor in 2018.

Peter Van Gelderen, Vice President and Senior Portfolio Manager, has served on teams managing fixed-income investments since joining the advisor in 2021.

Jason Greenblath, Vice President and Senior Portfolio Manager, has served on teams managing fixed-income investments since joining the advisor in 2019.

Jeffrey L. Houston, CFA, Vice President and Senior Portfolio Manager, has served on teams managing fixed-income investments since joining the advisor in 1990.

Purchase and Sale of Fund Shares

You may purchase or redeem shares of the fund on any business day through our website at americancentury.com, in person (at one of our Investor Centers), by mail (American Century Investments, P.O. Box 419200, Kansas City, MO 64141-6200), by telephone at 1-800-345-2021 (Investor Services Representative) or 1-800-345-3533 (Business, Not-For-Profit and Employer-Sponsored Retirement Plans), or through a financial intermediary. Shares may be purchased and redemption proceeds received by electronic bank transfer, by check or by wire.

Unless otherwise specified below, the minimum initial investment amount to open an account is $2,500 ($1,000 for Coverdell Education Savings Accounts and IRAs). However, American Century Investments will waive the fund minimum if you make an initial investment of at least $500 and continue to make automatic investments of at least $100 a month until reaching the fund minimum. Investors opening accounts through financial intermediaries may open an account with $250 for the Investor, A, C and R Classes, but the financial intermediaries may require their clients to meet different investment minimums. The minimum may be waived for broker-dealer sponsored wrap program accounts, fee based accounts, and accounts through bank/trust and wealth management advisory organizations.

The minimum initial investment amount for the I Class is generally $5 million ($3 million for endowments and foundations), but the minimum may be waived if you have an aggregate investment in the American Century family of funds of $10 million or more ($5 million for endowments and foundations). This includes accounts held directly with American Century and those held through a financial intermediary.

There is no minimum initial investment amount for R5 Class shares.

For the Investor, A, C, R and R5 Classes, there is no minimum initial investment amount for certain employer-sponsored retirement plans, however, financial intermediaries or plan recordkeepers may require plans to meet different minimums. Employer-sponsored retirement plans are not eligible to purchase I Class shares.

There is a $50 minimum for subsequent purchases, except that there is no subsequent purchase minimum for financial intermediaries or employer-sponsored retirement plans.

G Class shares are available for purchase by other funds offered by American Century Investments for which it charges a management fee. In its sole discretion, American Century Investments may also make G Class shares available for purchase by other institutional clients for which American Century Investments provides investment management services for a fee pursuant to an investment advisory agreement. Currently, eligible clients are limited to commingled investment trusts or other pooled investment vehicles that utilize a target date or other asset allocation investment strategy for which American Century Investments provides asset allocation or glide path investment management services for a fee. G Class shares do not have a minimum purchase amount.

Tax Information

Fund distributions are generally taxable as ordinary income or capital gains, unless you are investing through a tax-deferred account such as a 401(k) or individual retirement account (in which case you may be taxed upon withdrawal of your investment from such account).

Payments to Broker-Dealers and Other Financial Intermediaries

If you purchase the fund through a broker-dealer or other financial intermediary (such as a bank, insurance company, plan sponsor or financial professional), the fund and its related companies may pay the intermediary for the sale of fund shares and related services for investments in all classes except G Class. These payments may create a conflict of interest by influencing the broker-dealer or other intermediary and your salesperson to recommend the fund over another investment. Ask your salesperson or visit your financial intermediary’s website for more information.

Objectives, Strategies and Risks

What are the fund’s investment objectives?

The fund seeks to maximize total return. As a secondary objective, the fund seeks a high level of income.

What are the fund’s principal investment strategies?

The fund invests in debt securities including corporate bonds and notes, government securities, collateralized loan obligations, collateralized mortgage obligations, and securities backed by mortgages or other assets. These securities may be payable in U.S. or foreign currencies.

The fund invests at least 65% of its assets in investment-grade, non-money market debt securities. The fund may invest up to 35% of its assets in high-yield debt securities. A high-yield security is one that has been rated below the four highest categories used by a nationally recognized statistical rating organization, or determined by the investment advisor to be of similar quality. The fund may also invest in securities issued by companies that are located in emerging market countries—emerging market securities.

The fund may invest in non-dollar denominated debt securities.

The weighted average maturity of the fund’s portfolio must be 3½ years or longer. Within this maturity limit, the portfolio managers may shorten the portfolio’s maturity during periods of rising interest rates in order to reduce the effect of bond price declines on the fund’s value. When interest rates are falling and bond prices are rising, they may lengthen the portfolio’s maturity. Like most loans, debt securities eventually must be repaid or refinanced at some date. This date is called the maturity date. The number of days left to a debt security’s maturity date is called the remaining maturity. The longer a debt security’s remaining maturity, generally the more sensitive its price is to changes in interest rates. Because a bond fund will own many debt securities, the portfolio managers calculate the average of the remaining maturities of all the debt securities the fund owns to evaluate the interest rate sensitivity of the entire portfolio. This average is weighted according to the size of the fund’s individual holdings and is called the weighted average maturity.

The fund may invest in securities issued or guaranteed by the U.S. Treasury and certain U.S. government agencies or instrumentalities such as the Government National Mortgage Association (Ginnie Mae). Ginnie Mae is supported by the full faith and credit of the U.S. government. Securities issued or guaranteed by other U.S. government agencies or instrumentalities, such as the Federal National Mortgage Association (Fannie Mae), the Federal Home Loan Mortgage Corporation (Freddie Mac), and the Federal Home Loan Bank (FHLB) are not guaranteed by the U.S. Treasury or supported by the full faith and credit of the U.S. government. However, they are authorized to borrow from the U.S. Treasury to meet their obligations.

In addition to the debt securities described above, the fund may invest in bank loans, loan participations and loan assignments.

The fund also may invest in derivative instruments provided that such investments are in keeping with the fund’s investment objectives. Such derivative instruments may include options, futures contracts, options on futures contracts, and swaps (including credit default swaps). The fund may use foreign currency exchange contracts to shift investment exposure from one currency into another for hedging purposes or to enhance returns.

The fund may engage in active and frequent trading of portfolio securities to achieve its principal investment strategies. A higher portfolio turnover rate may indicate higher transaction costs and may affect the fund’s performance. Higher portfolio turnover also may result in the realization and distribution of capital gains, including short-term capital gains.

In the event of adverse market, economic, political or other conditions, the fund may take temporary defensive positions that are inconsistent with the fund’s principal investment strategies. To the extent the fund assumes a defensive position, it may not achieve its investment objective.

The portfolio managers select securities using an approach that integrates macroeconomic inputs, technical analysis of the relative value among various sectors, and fundamental research on individual securities. The macroeconomic framework provides interest rate and duration guidelines for the fund by analyzing economic activity, inflation, and monetary policy. Portfolio managers select individual securities using in-depth fundamental analysis designed to provide a detailed understanding of the credit worthiness of a security and its related market. As the market environment and investment opportunities change, sector exposures shift to those sectors that the process identifies as offering better relative yield and capital appreciation potential. The portfolio managers utilize the process on an ongoing basis to buy securities that fit the fund’s evolving sector allocations and credit quality standards and sell those securities that do not.

A description of the policies and procedures with respect to the disclosure of the fund’s portfolio securities is available in the statement of additional information.

What are the principal risks of investing in the fund?

When interest rates change, the fund’s share value will be affected. Generally, when interest rates rise, the fund’s share value will decline. The opposite is true when interest rates decline. The degree to which interest rate changes affect the fund’s performance varies and is related to the weighted average maturity of the fund. For example, when interest rates rise, you can expect the share value of a long-term bond fund to fall more than that of a short-term bond fund. When rates fall, the opposite is true. Interest rate risk is generally higher for Core Plus than for funds that have shorter-weighted average maturities, such as money market and short-term bond funds. A period of rising interest rates may negatively affect the fund’s performance.

Debt securities, even investment-grade debt securities, are subject to credit risk. Credit risk is the risk that the inability or perceived inability of the issuer to make interest and principal payments will cause the value of the securities to decrease. As a result the fund’s share price could also decrease. A high credit rating indicates a high degree of confidence by the rating organization that the issuer will be able to withstand adverse business, financial or economic conditions and make interest and principal payments on time. A lower credit rating indicates a greater risk of non-payment. Changes in the credit rating of a debt security held by the fund could have a similar effect. The fund’s credit quality restrictions apply at the time of purchase; the fund will not necessarily sell securities if they are downgraded by a rating agency.

Most of the securities purchased by the fund are quality debt securities at the time of purchase. The fund, however, may invest part of its assets in securities rated in the lowest investment-grade category, and up to 35% of its assets in high-yield debt securities, including so-called junk bonds, which are rated in the fifth category or below. As a result, the fund may have increased credit risk. Although their securities are considered investment-grade, issuers of securities rated in the lowest investment-grade category (and securities of similar quality) are more likely to have problems making interest and principal payments than issuers of higher-rated securities. Issuers of high-yield securities (and securities of similar quality) are even more vulnerable to real or perceived economic changes (such as an economic downturn or a prolonged period of rising interest rates), political changes or adverse developments specific to the issuer. In addition, lower-rated securities may be unsecured or subordinated to other obligations of the issuer. These factors may be more likely to cause an issuer of low-quality debt securities to default on its obligation to pay the interest and principal due under its securities.

The fund may also be subject to liquidity risk. The chance that a fund will have difficulty selling its debt securities is called liquidity risk. During periods of market turbulence or unusually low trading activity, in order to meet redemptions it may be necessary for the fund to sell securities at prices that could have an adverse effect on the fund’s price. The market for lower-quality debt securities is generally even less liquid than the market for higher-quality securities. Adverse publicity and investor perceptions, as well as new and proposed laws, also may have a greater negative impact on the market for lower-quality securities. Changing regulatory and market conditions, including increases in interest rates and credit spreads may adversely affect the liquidity of the fund’s investments.

The fund may invest in debt securities backed by mortgages or assets such as auto loan, home equity loan or student loan receivables. These underlying obligations may be prepaid, as when a homeowner refinances a mortgage to take advantage of declining interest rates. If so, the fund must reinvest prepayments at current rates, which may be less than the rate of the prepaid mortgage. Because of this prepayment risk, the fund may benefit less from declining interest rates than funds of similar maturity that invest less heavily in mortgage- and asset-backed securities. Conversely, an issuer may exercise its right to pay principal on an obligation held by the fund later than expected (extend the obligation) especially in periods of rising interest rates. These events may lengthen the maturity and potentially reduce the value of these securities.

In addition, to the extent the fund invests in loan participations and loan assignments, it may be exposed to restrictions on transfer, the inability or unwillingness of assignor(s) on whom it relies to demand and receive loan payments, the risks of being a lender, and the general risks of investing in debt securities.

Collateralized debt obligations (CDOs), collateralized mortgage obligations (CMOs) and collateralized loan obligations (CLOs) are subject to credit, interest rate, valuation, prepayment and extension risks. These securities also are subject to risk of default on the underlying asset, particularly during periods of economic downturn. The risks of an investment in a CDO depend largely on the type of the collateral securities and the class of the debt obligation in which the fund invests. The market value of CLO securities may be affected by, among other things, changes in the market value of the underlying assets held by the CLO, changes in the distributions on the underlying assets, defaults and recoveries on the underlying assets, capital gains and losses on the underlying assets, prepayments on underlying assets and the availability, and prices and interest rates of underlying assets. Lower rated tranches of such debt are subject to a higher risk of total loss and deferral or nonpayment of interest than the more senior tranches to which they are subordinated. Some of the collateralized obligations in which the fund invests may be covenant-lite loans. Covenant-lite loans contain fewer or less restrictive constraints on the borrower. Generally, the lender is not allowed to monitor the borrower’s performance, declare default, or force borrowers into bankruptcy. In this type of loan, lenders rely on restrictive covenants to prevent a company from engaging in specified actions such as taking on additional debt. Generally, such covenants are precipitated only by an affirmative breach by the borrower, as opposed to a decline in the borrower’s financial condition. Thus, the fund may have fewer rights against a borrower and an accompanying greater risk of loss when it invests in covenant-lite loans.

The fund may invest in the securities of foreign companies, which are generally riskier than U.S. securities. As a result, the fund may be subject to foreign risk, meaning that political events (such as civil unrest, national elections and imposition of exchange controls), social and economic events (such as labor strikes and rising inflation), natural disasters and public health emergencies occurring in a country where the fund invests could cause the fund’s investments in that country to experience losses. In addition, foreign securities can have reduced availability of public information, and the lack of uniform financial reporting and regulatory practices similar to those that apply to U.S. issuers. For these and other reasons, securities of foreign companies are often more volatile, less liquid and harder to value than those of U.S. issuers.

In addition, investments in foreign countries are subject to currency risk, meaning that because a portion of the fund’s investments may be denominated in foreign currencies, the fund could experience gains or losses based solely on changes in the exchange rate between foreign currencies and the U.S. dollar.

Investing in securities of companies located in emerging market countries generally is also riskier than investing in securities of companies located in foreign developed countries. Emerging market countries may have unstable governments and/or economies that are subject to sudden change. These changes may be magnified by the countries’ emergent financial markets, resulting in significant volatility to investments in these countries. These countries also may lack the legal, business and social framework to support securities markets.

The use of derivative instruments involves risks different from, or possibly greater than, the risks associated with investing directly in securities and other traditional instruments. Derivatives are subject to a number of risks, including liquidity, interest rate, market, and credit risk. They also involve the risk of mispricing or improper valuation, the risk that changes in the value of the derivative may not correlate perfectly with the underlying asset, rate or index, and the risk of default or bankruptcy of the other party to the instrument. Gains or losses involving some futures, options, and other derivatives may be substantial — in part because a relatively small price movement in these securities may result in an immediate and substantial gain or loss for the fund.

Futures contracts may experience potentially dramatic price changes (losses) and imperfect correlations between the price of the contract and the underlying security, index or currency which will increase the volatility of the fund and may involve a small investment of cash relative to the magnitude of the risk assumed.

Swap agreements are agreements to exchange the return generated by one instrument for the return generated by another instrument (or index). Swap agreements subject a fund to the risk that the counterparty to the transaction may not meet its obligations. The fund also bears the risk of loss of the amount expected to be received under a swap agreement in the event of the default or bankruptcy of a counterparty. Interest rate swaps could result in losses if interest rate changes are not correctly anticipated by the fund. Credit default swaps could result in losses if the fund does not correctly evaluate the creditworthiness of the issuer on which the credit default swap is based.

Investments in bank loans, loans made by banks or other financial intermediaries to borrowers, require the fund to depend primarily upon the creditworthiness of the borrower for payment of principal and interest, exposing the fund to the credit risk of both the financial institution and the underlying borrower. The market for bank loans may not be highly liquid and the fund may have difficulty selling them. In connection with purchasing participations, the fund generally will have no right to enforce compliance by the borrower with the terms of the loan agreement, nor any rights with respect to any funds acquired by other lenders through set-off against the borrower, and the fund may not directly benefit from any collateral supporting the loan in which it has purchased the participation. In addition, transactions in bank loans may take more than seven days to settle. As a result, the proceeds from the sale of bank loans may not be readily available to make additional investments or to meet the fund’s redemption obligations. Some bank loan interests may not be considered securities or registered under the Securities Act of 1933 and therefore not afforded the protections of the federal securities laws.

The value of securities owned by the fund may go up and down, sometimes rapidly or unpredictably, due to factors affecting securities markets generally, particular industries, real or perceived adverse economic conditions or investor sentiment generally. Market risks, including political, regulatory, economic and social developments, can affect the value of the fund’s investments. Natural disasters, public health emergencies, war, terrorism and other unforeseeable events may lead to increased market volatility and may have adverse long-term effects on world economies and markets generally.

The fund may need to sell securities at times it would not otherwise do so in order to meet shareholder redemption requests. The fund could experience a loss when selling securities, particularly if the redemption requests are unusually large or frequent, occur in times of overall market turmoil or declining pricing for the securities sold or when the securities the fund wishes to sell are illiquid. Selling securities to meet such redemption requests also may increase transaction costs or have tax consequences. To the extent that a large shareholder (including a 529 college savings plan) invests in the fund, the fund may experience relatively large redemptions as such shareholder reallocates its assets. Although the advisor seeks to minimize the impact of such transactions where possible, the fund’s performance may be adversely affected.

The fund’s share value will fluctuate, and at any given time your shares may be worth less than the price you paid for them. As a result, it is possible to lose money by investing in the fund. In general, funds that have higher potential income have higher potential loss.

Management

Who manages the fund?

The Board of Trustees, investment advisor and fund management team play key roles in the management of the fund.

The Board of Trustees

The Board of Trustees is responsible for overseeing the advisor’s management and operations of the fund pursuant to the management agreement. In performing their duties, Board members receive detailed information about the fund and its advisor regularly throughout the year, and meet at least quarterly with management of the advisor to review reports about fund operations. The trustees’ role is to provide oversight and not to provide day-to-day management. More than three-fourths of the trustees are independent of the fund’s advisor. They are not employees, directors or officers of, and have no financial interest in, the advisor or any of its affiliated companies (other than as shareholders of American Century Investments funds), and they do not have any other affiliations, positions or relationships that would cause them to be considered “interested persons” under the Investment Company Act of 1940.

The Investment Advisor

The fund’s investment advisor is American Century Investment Management, Inc. (the advisor). The advisor has been managing mutual funds since 1958 and is headquartered at 4500 Main Street, Kansas City, Missouri 64111.

The advisor is responsible for managing the investment portfolio of the fund and directing the purchase and sale of its investment securities. The advisor also arranges for transfer agency, custody and all other services necessary for the fund to operate.

For the services it provides to the classes of the fund other than G Class, the advisor receives a unified management fee based on a percentage of the daily net assets of each class of shares of the fund. The management fee is calculated daily and paid monthly in arrears. Out of the fund’s fee, the advisor pays all expenses of managing and operating the fund except brokerage expenses, taxes, interest, fees and expenses of the independent trustees (including legal counsel fees), extraordinary expenses, and expenses incurred in connection with the provision of shareholder services and distribution services under a plan adopted pursuant to Rule 12b-1 under the Investment Company Act of 1940. The difference in unified management fees among the classes is a result of their separate arrangements for non-Rule 12b-1 shareholder services. It is not the result of any difference in advisory or custodial fees or other expenses related to the management of the fund’s assets, which do not vary by class. For all classes other than the G Class, the advisor may pay unaffiliated third parties who provide recordkeeping and administrative services that would otherwise be performed by an affiliate of the advisor.

The percentage rate used to calculate the management fee for each class of shares of the fund is determined daily using a two-component formula that takes into account (i) the daily net assets of certain accounts managed by the advisor that are in the same broad investment category as the fund (the Category Fee) and (ii) the assets of all funds in the American Century Investments family of funds that have the same investment advisor and distributor as the fund (the Complex Fee). For purposes of determining the Category Fee and Complex Fee, the assets of funds managed by the advisor that invest exclusively in the shares of other funds (funds of funds) are not included. The statement of additional information contains detailed information about the calculation of the management fee.

The G Class is subject to a contractual management fee that the advisor waives in its entirety. However, the advisor does receive a management fee from funds or client advisory accounts that invest in the G Class.

| | | | | | | | | | | | | | | | | | | | | | | |

| Management Fees Paid by the Fund to the Advisor as a Percentage of Average Net Assets for the Fiscal Year Ended March 31, 2023 | Investor

Class | I

Class | A

Class | C

Class | R

Class | R5

Class | G

Class |

| Core Plus | 0.54% | 0.44% | 0.54% | 0.54% | 0.54% | 0.34% | 0.00% |

A discussion regarding the basis for the Board of Trustees’ approval of the fund’s investment advisory agreement with the advisor available in the fund’s semiannual report to shareholders dated September 30, 2022.

The Fund Management Team

The advisor uses teams of portfolio managers and analysts, organized by broad investment categories such as money markets, corporate bonds, government bonds and municipal bonds, in its management of fixed-income funds. Designated portfolio managers serve on the firm’s Global Fixed Income Investment Committee, which is responsible for periodically adjusting the fund’s dynamic investment parameters based on economic and market conditions. All portfolio managers listed below are responsible for security selection and portfolio construction for the fund within these parameters, as well as compliance with stated investment objectives and cash flow monitoring. Other members of the investment team provide research and analytical support but generally do not make day-to-day investment decisions for the fund.

The individuals listed below are jointly and primarily responsible for the day-to-day management of the fund described in this prospectus.

Robert V. Gahagan (Global Fixed Income Investment Committee Representative)

Mr. Gahagan, Senior Vice President and Senior Portfolio Manager, has served on teams managing fixed-income investments since joining the advisor in 1983. He has a bachelor’s degree in economics and an MBA from the University of Missouri – Kansas City.

Charles Tan (Global Fixed Income Investment Committee Representative)

Mr. Tan, Senior Vice President and Co-Chief Investment Officer, Global Fixed Income, has served on teams managing fixed-income investments since joining the advisor in 2018. Prior to joining American Century, Mr. Tan worked at Aberdeen Standard Investments as head of North American fixed income from 2015 to 2018 and head of U.S. credit and as a senior portfolio manager from 2005 to 2015. He has a bachelor’s degree in economics from University of International Business and Economics, Beijing and an MBA from Bucknell University.

Peter Van Gelderen (Global Fixed Income Investment Committee Representative)

Mr. Van Gelderen, Vice President and Senior Portfolio Manager, has served on teams managing fixed-income investments since joining the advisor in 2021. Prior to joining American Century, Mr. Van Gelderen was most recently co-head of the structured credit group at Guggenheim Partners from 2013 to 2021. He has a bachelor of arts degree from Duke University and a juris doctorate from Georgetown University Law Center.

Jason Greenblath (Global Fixed Income Investment Committee Representative)

Mr. Greenblath, Vice President and Senior Portfolio Manager, has served on teams managing fixed-income investments since joining the advisor in 2019. Prior to joining American Century, Mr. Greenblath worked at Aberdeen Standard Investments as head of U.S. investment grade credit from 2018 to 2019, head of U.S. investment grade credit research from 2014 to 2018 and as a portfolio manager from 2012 to 2018. He has a bachelor’s degree in finance from Pennsylvania State University.

Jeffrey L. Houston

Mr. Houston, Vice President and Senior Portfolio Manager, has served on teams managing fixed-income investments since joining the advisor in 1990. He has a bachelor’s degree in history and political science from the University of Delaware and a master’s degree of public administration from Syracuse University. He is a CFA charterholder.

The statement of additional information provides additional information about the accounts managed by the portfolio managers, the structure of their compensation, and their ownership of fund securities.

Fundamental Investment Policies

Shareholders must approve any change to the fundamental investment policies contained in the statement of additional information, as well as any change to the investment objective of the fund. The Board of Trustees and/or the advisor may change any other policies or investment strategies described in this prospectus or otherwise used in the operation of the fund at any time, subject to applicable notice provisions.

Investing Directly with American Century Investments

Services Automatically Available to You

Most accounts automatically have access to the services listed under Ways to Manage Your Account when the account is opened. If you have questions about the services that apply to your account type, please call us.

Generally, once your account is established, any registered owner (including those on jointly owned accounts) or any trustee (including those on trust accounts with multiple trustees), or any authorized signer on business accounts with multiple authorized signers, may transact business by any of the methods described below. American Century reserves the right to require all owners or trustees or authorized signers to act together, at our discretion.

Account Maintenance Fee

If you hold Investor Class shares of any American Century Investments mutual fund, or I Class shares of the American Century Diversified Bond Fund, in an American Century Investments account (i.e., not through a financial intermediary or employer-sponsored retirement plan account), we may charge you a $25 annual account maintenance fee if the value of those shares is less than $10,000. We will determine the amount of your total eligible investments once per year, generally the last Friday in October. If the value of those investments is less than $10,000 at that time, we will automatically redeem shares in one of your accounts to pay the $25 fee as soon as administratively possible. Please note that you may incur tax liability as a result of the redemption. In determining your total eligible investment amount, we will include your investments in all personal accounts (including American Century Investments brokerage accounts) registered under your Social Security number.

Personal accounts include individual accounts, joint accounts, UGMA/UTMA accounts, personal trusts, Coverdell Education Savings Accounts, IRAs (including traditional, Roth, Rollover, SEP-, SARSEP- and SIMPLE-IRAs), and certain other retirement accounts. If you have only business, business retirement, employer-sponsored or American Century Investments brokerage accounts, you are currently not subject to this fee, but you may be subject to other fees.

Wire Purchases

Current Investors: If you would like to make a wire purchase into an existing account, your bank will need the following information. (To invest in a new fund, please call us first to set up the new account.)

•American Century Investments bank information: Commerce Bank N.A., Routing No. 101000019, Account No. 2804918

•Your American Century Investments account number and fund name

•Your name

•The contribution year (for IRAs only)

•Dollar amount

New Investors: To make a wire purchase into a new account, please complete an application or call us prior to wiring money.

Ways to Manage Your Account

ONLINE

americancentury.com

Open an account: If you are a current or new investor, you can open an account by completing and submitting our online application. Current investors also can open an account by exchanging shares from another American Century Investments account with an identical registration.

Exchange shares: Exchange shares from another American Century Investments account with an identical registration.

Make additional investments: Make an additional investment into an established American Century Investments account. If we do not have your bank information, you can add it.

Sell shares*: Redeem shares and choose whether the proceeds are electronically transferred to your authorized bank account or sent by check to your address of record.

* Online redemptions up to $25,000 per day per account.

IN PERSON

If you prefer to handle your transactions in person, visit one of our Investor Centers and a representative can help you open an account, make additional investments, and sell or exchange shares.

•4400 Main Street, Kansas City, MO — 8 a.m. to 5 p.m., Monday – Friday

•4917 Town Center Drive, Leawood, KS — 8 a.m. to 5 p.m., Monday – Friday

BY TELEPHONE

Investor Services Representative: 1-800-345-2021

Business, Not-For-Profit and Employer-Sponsored Retirement Plans: 1-800-345-3533

Automated Information Line: 1-800-345-8765

Open an account: If you are a current investor, you can open an account by exchanging shares from another American Century Investments account with an identical registration.

Exchange shares: Call or use our Automated Information Line (available only to Investor Class shareholders).

Make additional investments: Call or use our Automated Information Line if you have authorized us to invest from your bank account. The Automated Information Line is available only to Investor Class shareholders.

Sell shares: Call or use our Automated Information Line. The Automated Information Line redemptions are up to $25,000 per day per account and are available for Investor Class shareholders only.

BY MAIL OR FAX

Mail Address: P.O. Box 419200, Kansas City, MO 64141-6200 — Fax: 1-888-327-1998

Open an account: Send a signed, completed application and check or money order payable to American Century Investments.

Exchange shares: Send written instructions to exchange your shares from one American Century Investments account to another with an identical registration.

Make additional investments: Send your check or money order for at least $50 with an investment slip. If you don’t have an investment slip, include your name, address and account number on your check or money order.

Sell shares: Send written instructions or a redemption form to sell shares. Call a Service Representative to request a form.

AUTOMATICALLY

Open an account: Not available.

Exchange shares: Send written instructions to set up an automatic exchange of your shares from one American Century Investments account to another with an identical registration.

Make additional investments: With the automatic investment service, you can purchase shares on a regular basis. You must invest at least $50 per month per account.

Sell shares: You may sell shares automatically by establishing a systematic redemption plan.

See Additional Policies Affecting Your Investment for more information about investing with us.

Investing Through a Financial Intermediary

The fund may be purchased by participants in employer-sponsored retirement plans or through financial intermediaries that provide various administrative and distribution services.

Financial intermediaries include banks, broker-dealers, insurance companies, plan sponsors and financial professionals.

Although each class of the fund’s shares represents an interest in the same fund, each has a different cost structure, as described below. Which class is right for you depends on many factors, including how long you plan to hold the shares, how much you plan to invest, the fee structure of each class, and how you wish to compensate your financial professional for the services provided to you. Your financial professional can help you choose the option that is most appropriate.

Investor Class

Investor Class shares are available for purchase without sales charges or commissions but may be subject to account or transaction fees if purchased through financial intermediaries. These shares are available to investors in retail brokerage accounts, broker-dealer-sponsored fee-based advisory accounts, other advisory accounts where fees are charged, and employer-sponsored retirement plans.

I Class

I Class shares are available for purchase without sales charges or commissions by endowments, foundations, large institutional investors and financial intermediaries.

A Class

A Class shares are available for purchase through broker-dealers and other financial intermediaries. These shares carry an initial sales charge and an ongoing distribution and service (12b-1) fee that is used to compensate your financial professional. See Calculation of Sales Charges below for commission amounts received by financial professionals on the purchase of A Class shares. The sales charge decreases with the size of the purchase, and may be reduced or eliminated in certain situations. See Reductions and Waivers of Sales Charges for A Class and CDSC Waivers below for a full description of the breakpoints, reductions and waivers that may be available through financial intermediaries in certain types of accounts or products.

C Class

C Class shares are available for purchase through broker-dealers and other financial intermediaries. These shares do not have an initial sales charge but carry an ongoing distribution and service (12b-1) fee. Except as noted below, the commission paid to your financial professional for purchases of C Class shares is 1.00% of the amount invested, and the shares have a contingent deferred sales charge (CDSC) when redeemed within one year of purchase. Your financial professional does not receive the distribution and service (12b-1) fee until the CDSC period has expired (it is retained by the distributor). See CDSC Waivers below for a full description of the waivers that may be available. C Class shares automatically convert to A Class shares 8 years after purchase.

R Class

R Class shares do not carry a sales charge or commission, but they have an ongoing distribution and service (12b-1) fee. R Class shares are available for purchase through certain employer-sponsored retirement plans. R Class shares also may be available for certain other accounts through financial intermediaries who have an agreement with us to offer R Class in certain products. Additionally, IRA accounts in R Class shares established through financial intermediaries prior to August 1, 2006, may make additional purchases. With respect to purchases through financial intermediaries, R Class shares are not available in the following types of employer-sponsored retirement plans: SEP IRAs, SIMPLE IRAs or SARSEPs, except that investors in such plans with accounts in R Class shares established prior to March 1, 2009, may make additional purchases, and certain intermediaries may have agreements with us to offer R Class shares in such plans as described above.

R5 Class

R5 Class shares are available for purchase without sales charges or commissions by participants in certain employer-sponsored retirement plans. R5 Class shares may be purchased or redeemed only through employer-sponsored retirement plans where a financial intermediary provides retirement recordkeeping services to plan participants. Accounts in R5 Class shares opened prior to April 10, 2017 remain eligible for the R5 Class.

Calculation of Sales Charges

The information regarding sales charges provided herein is included free of charge and in a clear and prominent format at americancentury.com in the Investors Using Advisors and Investment Professionals portions of the website. From the description of A or C Class shares, a hyperlink will take you directly to this disclosure.

The availability of the sales charge reductions and waivers discussed below will depend upon whether you purchase your shares directly from the fund or through a financial intermediary. Intermediaries may have different policies and procedures regarding the availability of these reductions or waivers. Please refer to Appendix A for information provided by certain financial intermediaries regarding their sales charge waiver or discount policies that are applicable to investors transacting in fund shares through such financial intermediary.

A Class