November 26, 2013

Division of Corporation Finance

United States Securities and Exchange Commission

100 F Street, N.E.

Washington, D.C. 20549

Attn: Jonathan Gottlieb

Re: Blue Valley Ban Corp (the “Company”)

Registration Statement on Form S-1

File No. 333-191058

To the Commission:

On September 11, 2013, the Company submitted a confidential draft registration statement on Form S-1 (the “Draft Registration Statement”). The Company received comments on the Draft Registration Statement from Mr. Todd K. Schiffman of the staff the Securities and Exchange Commission (the “Commission”). On October 28, 2013, the Company filed a registration statement on Form S-1 (the “Registration Statement”) to respond to the comments on the Draft Registration Statement and update certain disclosure. The Company received comments on the Registration Statement from Mr. Todd K. Schiffman of the Commission staff. On November 19, 2013, the Company filed Amendment No. 1 to the Registration Statement ("Amendment ") to respond to the comments. However, a marked copy of the Amendment was inadvertently omitted from the November 19, 2013 EDGAR filing. On November 25, 2013, Jonathan Gottlieb advised that, in order to facilitate the Commision's review of the Amendment, a marked copy should be filed via EDGAR. Therefore, please find below the marked copy of the Amendment.

We look forward to hearing from you soon to discuss any comments you may have on the filing. Please contact the undersigned at (816) 983-8362 or Steve Carman at (816) 983-8153.

As filed with the Securities and Exchange Commission on November 19, 2013

Registration No. 333-191958

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO 1 TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

BLUE VALLEY BAN CORP.

(Exact name of registrant as specified in its charter)

|

Kansas

|

6022

|

48-1070996

|

|

(State or other jurisdiction of incorporation or organization)

|

(Primary Standard Industrial

Classification Code Number)

|

(I.R.S. Employer

Identification No.)

|

11935 Riley

Overland Park, Kansas 66225-6128

(913) 338-1000

|

Agent for Service:

Robert D. Regnier

President and Chief Executive Officer

Blue Valley Ban Corp.

11935 Riley

Overland Park, Kansas 66225-6128

(913) 338-1000

|

Copies of Communications to:

Steven F. Carman, Esq.

Husch Blackwell LLP

4801 Main Street, Suite 1000

Kansas City, Missouri 64112

(816) 983-8000

|

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b2 of the Exchange Act.

| Large accelerated filer | o | Accelerated filer | o | |

| Non-accelerated filer | o | Smaller reporting company | x |

CALCULATION OF REGISTRATION FEE

|

Title of Each Class

of Securities to

be Registered

|

Amount to be

Registered

|

Proposed Offering Price Per Share

|

Proposed Aggregate Offering Price

|

Amount of

Registration Fee

|

|

Nontransferable common

stock subscription rights

|

2,938,871 | ----- | ------ | ----- (1) |

| Common Stock, par value $1.00 per share | 2,000,000 | $5.00 |

$10,000,000 (2)

|

$1,288.00 (3) |

|

|

(1)

|

The nontransferable subscription rights are being issued without consideration. Pursuant to Rule 457(g) under the Securities Act of 1933, as amended, no separate registration fee is required because the rights are being registered in the same registration statement as the securities to be offered pursuant thereto.

|

|

|

(2)

|

Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended. In no event will the aggregate maximum offering price of all securities issued pursuant to this registration statement exceed $10,000,000.

|

|

|

(3)

|

Previously Paid.

|

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any state where the offer or sale is not permitted.

Subject to completion, dated November 19, 2013

PRELIMINARY PROSPECTUS

Minimum of 1,000,000 and maximum of 2,000,000 Shares of Common Stock

Issuable upon the exercise of Nontransferable Subscription Rights at $5.00 per share

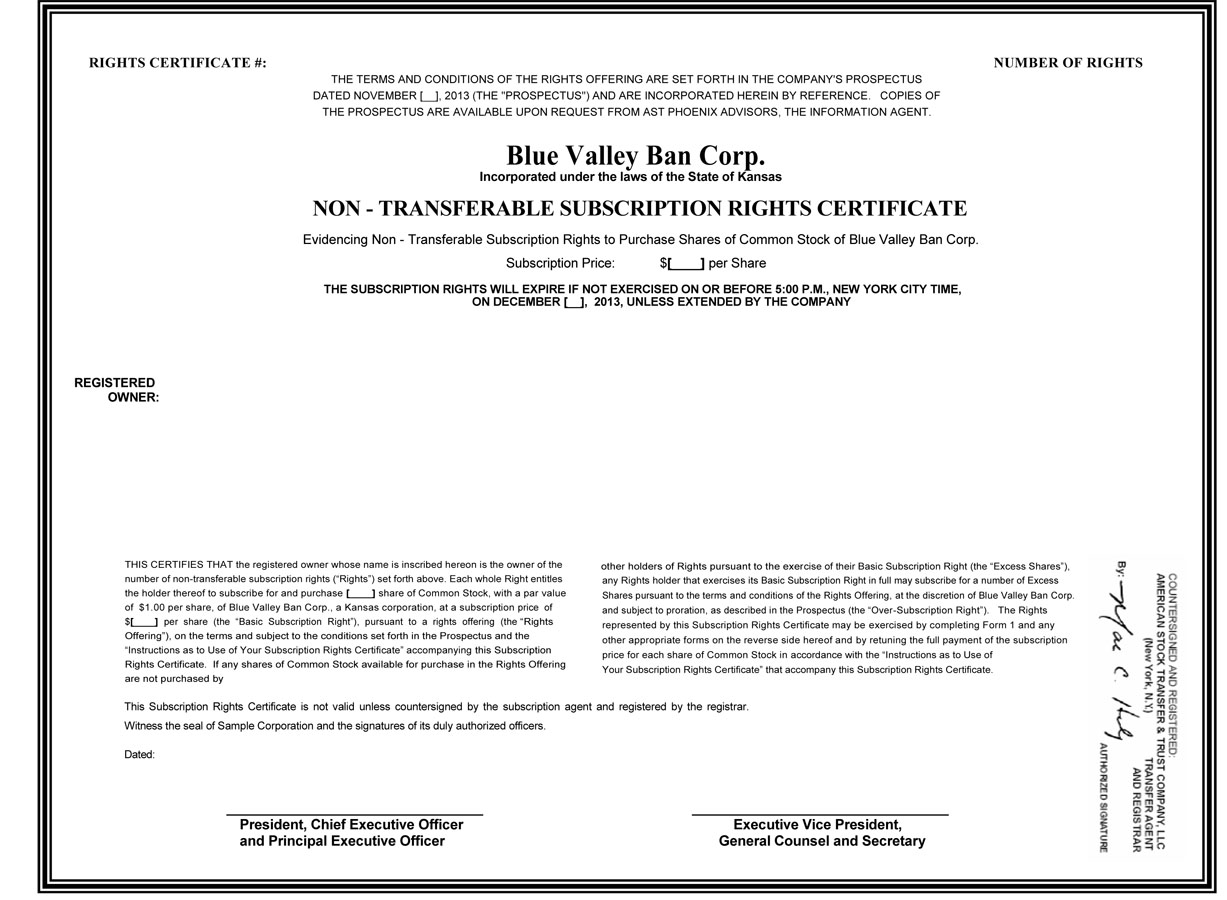

We are distributing to holders of our outstanding common stock, at no charge, non-transferable subscription rights to purchase up to an aggregate of 2,000,000 shares of our common stock at a cash subscription price of $5.00 per share. We must receive minimum gross proceeds of $5.0 million in the aggregate to complete the rights offering. The rights offering is subject to a limit of $10.0 million in gross proceeds.

You are receiving this prospectus because you held shares of our common stock as of the close of business on October 29, 2013, the record date for this rights offering. We have granted you one right for each share of our common stock that you owned on the record date. You may purchase one share of our common stock for every 1.4694 rights granted to you. If you exercise your rights in full, you may also exercise an oversubscription right to purchase (at the same subscription price) additional shares of common stock that may remain unsubscribed at the expiration of the rights offering

The rights will expire if they are not exercised and paid in full (including final clearance of any checks) by 5:00 p.m., Eastern Time on _______, unless we extend the rights offering in our sole discretion.

We are an “emerging growth company” as the term is used in the Jumpstart Our Business Startups Act of 2012 and, as such, may elect to comply with certain reduced public company reporting requirements for future filings.

Shares of our common stock are quoted on the OTCQB under the trading symbol “BVBC.” On November ____, 2013, the closing sales price for our common stock was ______ per share.

OFFERING SUMMARY

| Per Share | Total | |||||

| Minimum | Maximum | Minimum | Maximum | |||||

| Subscription Price | $5.000 | $5.000 | $5.00 | $5.00 | ||||

|

Estimated Expenses

|

$0.350 | $0.175 | $350,000.00 | $350,000.0 | ||||

| Proceeds to us | $4.650 | $4.825 | $4,650,000.00 | $9,650,000.00 |

Investing in our common stock involves a high degree of risk. We urge you to carefully read the “Risk Factors” section beginning on page 6 of this prospectus before determining whether to exercise your subscription rights.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The shares of our common stock are not deposits or savings accounts or other obligations of any bank or savings association, and are not insured by the Federal Deposit Insurance Corporation or any other governmental agency.

The date of this prospectus is _______, 2013.

|

About This Prospectus

|

ii

|

|||

|

Cautionary Note regarding Forward-Looking Statements

|

ii

|

|||

|

Questions and Answers About The Rights Offering

|

iv

|

|||

|

Prospectus Summary

|

1

|

|||

|

Use of Proceeds

|

5

|

|||

|

Risk Factors

|

6

|

|||

|

The Rights Offering

|

14

|

|||

|

The Company

|

18

|

|||

|

Capitalization

|

35

|

|||

|

Selected Consolidated Financial Data

|

36

|

|||

|

Market Price and Dividends on Our Common Stock

|

38

|

|||

|

Dividends

|

38

|

|||

|

Dilution

|

38

|

|||

|

Material U.S. Federal Income Tax Consequences

|

39

|

|||

|

Plan of Distribution

|

41

|

|||

|

Description of Securities To Be Registered

|

42

|

|||

|

Management’s Discussion and Analysis Of Financial Condition and Results of Operations

|

47

|

|||

|

Management

|

79

|

|||

|

Beneficial Ownership Table

|

82

|

|||

|

Certain Relationships and Related Party Transactions

|

84

|

|||

|

Indemnification of Directors, Officers, and Employees

|

84

|

|||

|

Executive Compensation

|

85

|

|||

|

Legal Matters

|

89

|

|||

|

Experts

|

89

|

|||

|

Index to Financial Statements

|

F-1

|

i

ABOUT THIS PROSPECTUS

You should rely only on the information provided in this prospectus. We have not authorized anyone to provide you with any different information. The information contained in this prospectus is accurate only as of the date on the front cover of this prospectus regardless of the time of delivery of this prospectus or any exercise of the subscription rights.

The distribution of this prospectus and the rights offering and sale of shares of our common shares in certain jurisdictions may be restricted by law. This prospectus does not constitute an offer of, or a solicitation of an offer to buy, any shares of common stock in any jurisdiction in which such offer or solicitation is not permitted. No action is being taken in any jurisdiction outside the United States to permit an offering of the common shares or possession or distribution of this prospectus in that jurisdiction. Persons who come into possession of this prospectus in jurisdictions outside the United States are required to inform themselves about and to observe any restrictions as to this offering and the distribution of this prospectus applicable to those jurisdictions.

In this prospectus, all references to the “we,” “us,” “our,” “Company” and “Blue Valley” refer to Blue Valley Ban Corp., unless the context otherwise requires or where otherwise indicated. References to the “Bank” refer to the Company’s primary wholly-owned subsidiary, Bank of Blue Valley.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements. These forward-looking statements are subject to a number of risks and uncertainties, many of which are beyond our control. All statements, other than statements of historical fact, contained in this prospectus, including statements regarding future events, our future financial performance, business strategy and plans and objectives of management for future operations, are forward-looking statements. We have attempted to identify forward-looking statements by terminology including “anticipates,” “believes,” “can,” “continue,” “could,” “estimates,” “expects,” “intends,” “may,” “plans,” “potential,” “predicts,” “should” or “will” or the negative of these terms or other comparable terminology.

Although we do not make forward-looking statements unless we believe we have a reasonable basis for doing so, we cannot guarantee their accuracy. These statements are only predictions and involve known and unknown risks, uncertainties and other factors, including the risks outlined under “Risk Factors” or referenced elsewhere in this prospectus, which may cause our or our industry’s actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements. Moreover, we operate in a very competitive and rapidly changing environment. New risks emerge from time to time, and it is not possible for us to predict all risk factors. Nor can we address the impact of all factors on our business or the extent to which any factor, or combination of factors, may cause our actual results to differ materially from those contained in any forward-looking statements.

The factors impacting these risks and uncertainties include, but are not limited to:

|

•

|

general economic conditions, either nationally or locally in some or all of the areas in which we do business, or conditions in the securities or real estate markets or the banking industry may be less favorable than we currently anticipate;

|

||

|

•

|

the timing and occurrence or non-occurrence of events may be subject to circumstances beyond our control;

|

|

•

|

there may be increases in competitive pressure among financial institutions or from non-financial institutions;

|

ii

|

•

|

changes in the interest rate environment could adversely affect our results of operations and financial condition;

|

|

•

|

changes in accounting principles, policies or guidelines;

|

|

•

|

legislative or regulatory changes may adversely affect our business;

|

|

•

|

changes in management’s estimate of the adequacy of the allowance for loan losses;

|

|

•

|

litigation or matters before regulatory agencies, whether currently existing or commencing in the future, may delay the occurrence or non-occurrence of events longer than we anticipate;

|

|

•

|

changes in deposit flows, loan demand or real estate values may adversely affect our business;

|

|

•

|

the Company’s non-payment of dividends and accrued interest on its trust preferred securities or fixed rate cumulative preferred stock;

|

||

|

•

|

technological changes may be more difficult or expensive than we anticipate; and

|

|

•

|

success or consumption of new business initiatives may be more difficult or expensive than we anticipate.

|

You should not place undue reliance on any forward-looking statement, each of which applies only as of the date of this prospectus. Before you invest in our common stock, you should be aware that the occurrence of the events described in the section entitled “Risk Factors” and elsewhere in this prospectus, could negatively affect our business, operating results, financial condition and stock price. Except as required by law, we undertake no obligation to update or revise publicly any of the forward-looking statements after the date of this prospectus to conform our statements to actual results or changed expectations.

iii

QUESTIONS AND ANSWERS ABOUT THE RIGHTS OFFERING

The following are examples of what we anticipate will be common questions about the rights offering. The answers are based on selected information from this prospectus and may not contain all of the information that is important to you. This prospectus includes specific terms of the rights offering, as well as information regarding our business, including potential risks related to the rights offering and our common stock. We encourage you to read this prospectus in its entirety.

|

Q:

|

What is the rights offering?

|

|

A:

|

The rights offering is a distribution to holders of our common stock, at no charge, of nontransferable rights to purchase shares of our common stock based on your ownership of common stock as of October 29, 2013, the record date. You may purchase one whole share of our common stock at $5.00 per share for every 1.4694 rights granted to you.

|

|

Q:

|

What is a subscription right?

|

|

A:

|

A subscription right is the right to purchase a portion of a share of our common stock. Because we have 2,938,871 shares of common stock outstanding and we are targeting the sale of a maximum of 2,000,000 shares in connection with this rights offering, each subscription right carries with it a basic subscription right to purchase 0.6805 of a share of our common stock. Each subscription right also includes an oversubscription right to purchase additional shares of our common stock.

|

|

Q:

|

Why do I need to exercise 1.4694 rights to purchase one share of common stock?

|

|

A:

|

As of October 29, 2013 we had outstanding 2,938,871 shares of our common stock. By granting one right for each share of common stock, we have granted an aggregate of 2,938,871 rights. As a result, because we are targeting the sale of a maximum of 2,000,000 shares of common stock in this rights offering, you must exercise 1.4694 rights to acquire one share.

|

|

Q:

|

What is the basic subscription right?

|

|

A:

|

Each whole subscription right entitles you to purchase 0.6805 of a share of our common stock at the subscription price of $5.00 per share. We have granted to you, as a stockholder of record on the record date, a subscription right for each share of our common stock you owned at that time. Fractional shares of our common stock resulting from the exercise of the basic subscription right will be eliminated by rounding down to the nearest whole share, with the total subscription payment being adjusted accordingly. For example, if you owned 1,000 shares of our common stock on the record date, your basic subscription right would permit the purchase of 680 shares (1,000 purchase rights / 1.4694 = 680.55, with fractional shares rounded down to the nearest whole number). You may exercise all or a portion of your basic subscription right, or you may choose not to exercise any subscription rights at all. However, if you exercise less than your full basic subscription right , you will not be entitled to purchase shares under your oversubscription right.

|

|

If you hold your shares in the name of a custodian bank, broker, dealer or other nominee, you will not receive a rights certificate. Instead, the Depository Trust Company, or DTC, will issue the appropriate number of subscription rights to your nominee record holder based on the shares of our common stock that you own at the record date. If you are not contacted by your nominee, you should contact your nominee as soon as possible.

|

iv

|

Q:

|

What is the oversubscription right?

|

||

|

A:

|

If any holders of subscription rights do not fully exercise their basic subscription rights as of the expiration time of the rights offering, we will permit stockholders who do fully exercise their basic subscription rights to subscribe for additional shares of our common stock at the same subscription price per share, on the pro rata basis described below, rounded down to the nearest whole share number. This oversubscription right will be available only to stockholders who exercise their basic subscription rights in full. We may elect, in our sole discretion, to honor some or all of the oversubscription rights.

|

||

|

If oversubscription requests exceed the number of shares of common stock we elect to sell, we will allocate the available shares of common stock among stockholders who oversubscribed by multiplying the number of shares requested by each stockholder through the exercise of their oversubscription rights by a fraction that equals (x) the number of shares we elect to issue through oversubscription rights divided by (y) the total number of shares requested by all subscribers through the exercise of their oversubscription rights. As described above for the basic subscription right, we will not issue fractional shares through the exercise of oversubscription rights.

|

|||

|

Q:

|

How many shares may I purchase if I exercise my subscription rights?

|

||

|

A:

|

The number of shares of common stock you can purchase under your basic subscription rights will depend on the number of subscription rights you receive. You will receive one basic subscription right for each share of our common stock you hold on the record date. Each basic subscription right entitles you to purchase 0.6805 of a share of our common stock at the subscription price of $5.00 per share.

|

||

|

Upon exercising your subscription rights, you may request to subscribe for additional shares on your subscription rights certificate. However, the actual number of shares for which you will be entitled to subscribe under your oversubscription rights will not be determinable until after the expiration time of the rights offering and the pro rata allocation.

|

|||

|

Q:

|

What if there is an insufficient number of shares to satisfy the oversubscription requests?

|

||

|

A:

|

If there is an insufficient number of shares to fully satisfy the oversubscription requests of rightsholders, each subscription rightsholder who exercised his or her oversubscription right will receive a pro rata number of the shares we elect to sell, rounded down to the nearest whole share number, as described above. Any excess subscription payments will be returned, without interest or deduction, promptly after the expiration of this rights offering.

|

||

|

Q:

|

Am I required to participate in the rights offering?

|

||

|

A:

|

No

|

||

|

Q:

|

Why are we conducting the rights offering?

|

||

|

A:

|

We are conducting the rights offering to improve our earnings by eliminating double interest and compounding interest. We will achieve this goal by bringing current all previously accrued and unpaid dividends on our Subordinated Debentures, with any additional proceeds to be used for general corporate purposes. Our Board of Directors has chosen to raise capital through a rights offering to give our stockholders the opportunity to limit ownership dilution from a capital raise by allowing our current stockholders to purchase additional shares of our common stock. We cannot determine the amount of dilution that a stockholder will experience or whether the rights offering will be successful. See the section of this prospectus captioned “Use of Proceeds,” for more details.

|

v

|

Q:

|

Will the Company be issuing fractional shares of common stock?

|

||

|

A:

|

No. You may not purchase fractional shares of common stock pursuant to the exercise of subscription rights. We will accept any subscription indicating a purchase of fractional shares by rounding down to the nearest whole share number and promptly refunding without interest any payment received for a fractional share.

|

||

|

Q:

|

If I wish to exercise my rights, do I have to exercise all of my rights?

|

||

|

A:

|

No. You may exercise some or all of your rights. However, if you subscribe for fewer than all the shares represented by your basic subscription rights, your remaining rights are non-transferable and will expire at the expiration time of the rights offering. You may not sell your remaining rights. In addition, you may only participate in the oversubscription portion of this rights offering if you exercise your basic subscription rights in full.

|

||

|

Q:

|

How long will the rights offering remain open?

|

||

|

A:

|

The rights offering will commence on ______________, 2013. The rights offering will remain open for [16] days after commencement, and the rights will expire at 5:00 p.m., Eastern Time, on _______, 2013 unless we extend the rights offering. We reserve the right to extend the rights offering at our discretion for a period not to exceed 45 additional days beyond ______, 2013, in which event the term “expiration time” will mean the latest date and time to which the rights offering has been extended. We will make a public announcement of any extension by issuing a press release prior to 9:00 a.m., Eastern Time, on the next business day after the previously scheduled expiration time. In addition, if the commencement of the rights offering is delayed, the expiration time of the rights offering will be similarly delayed. In that event, we will notify you by issuing a press release.

|

||

|

Q:

|

When must I exercise my oversubscription rights?

|

||

|

A:

|

You must exercise your oversubscription rights when you exercise your basic subscription rights in full. However, the number of shares for which you will be able to purchase by exercise of your oversubscription rights cannot be determined until after the expiration time of the rights offering period.

|

||

|

Q:

|

What happens if I choose not to exercise my subscription rights?

|

||

|

A:

|

You will retain your current number of shares of our common stock held by you even if you do not exercise your subscription rights. If you choose not to exercise your subscription rights, upon completion of the offering the percentage of our capital stock held by you will decrease, however, the magnitude of the reduction will depend upon the extent to which other rightsholders subscribe in the rights offering.

|

||

|

Q:

|

Will I be charged a sales commission or a fee by the Company if I exercise my subscription rights?

|

||

|

A:

|

No. We will not charge a brokerage commission or a fee to rightsholders for exercising their subscription rights. However, if you exercise your subscription rights through a broker or nominee, then you will be responsible for any transaction fees charged by your broker or nominee.

|

||

|

Q:

|

What is the Board of Directors’ recommendation regarding whether I should exercise my rights in the rights offering?

|

||

|

A:

|

Our Board of Directors is not making any recommendation as to whether you should exercise your subscription rights. You are urged to make your decision based on your own assessment of our business and the rights offering.

|

||

vi

|

Q:

|

Are there any conditions to completing the rights offering?

|

||

|

A:

|

Yes. We must sell the minimum offering amount of at least $5.0 million (1,000,000 shares) of common stock for the rights offering to be completed.

|

||

|

Q:

|

If the rights offering is not completed, will my subscription payment be refunded to me?

|

||

|

A:

|

Yes. The subscription agent will hold all funds it receives in escrow until completion of the rights offering. If the rights offering is not completed, the subscription agent will return promptly, without interest, all subscription payments. We reserve the right to terminate the offering at any time if, due to market conditions or otherwise, the Board of Directors deems it advisable not to proceed with the rights offering.

|

||

|

Q:

|

Will our directors and executive officers participate in the rights offering?

|

||

|

A:

|

We expect that certain of our directors and executive officers, and certain of the directors of our primary wholly-owned subsidiary Bank of Blue Valley (the “Bank”), together with their affiliates, will participate in the rights offering, although they are not obligated to do so. We anticipate that our directors and executive officers, along with the Bank’s directors, and their affiliates, will at a minimum purchase that number of shares of common stock in this rights offering that will allow them to maintain the percentage of our common stock they currently hold and could increase the percentage of our common stock they own. We also expect that certain of our officers and directors will, if necessary, subscribe for additional shares of common stock in the aggregate amount required to raise the minimum gross proceeds. The purchase price paid by them will be the same paid by all other persons who purchase shares of our common stock in the rights offering.

|

||

|

Q:

|

How was the subscription price established?

|

||

|

A:

|

In determining the subscription price, our Board of Directors considered a number of factors, including: the price at which our stockholders might be willing to participate in the rights offering, historical and current trading prices for our common stock, the need for liquidity and capital, potential market conditions, and the desire to provide an opportunity to our stockholders to participate in the rights offering on a pro rata basis. In conjunction with its review of these factors, our Board of Directors also reviewed our history and prospects, including our past and present earnings, our prospects for future earnings, our current financial condition and regulatory status. The subscription price is not necessarily related to our book value, net worth or any other established criteria of value and may or may not be considered the fair value of our common stock. You should not assume or expect that, after this offering, our shares of common stock will trade at or above the $5.00 per share purchase price.

|

||

|

Q:

|

What is the role of KBW in the rights offering?

|

||

|

A:

|

We have entered into an agreement with Keefe, Bruyette & Woods, Inc. (“KBW”) pursuant to which KBW is acting as our financial advisor in connection with the rights offering. We have agreed to pay certain fees to, and expenses of, KBW.

|

||

|

Q:

|

Is exercising my subscription rights risky?

|

||

|

A:

|

Yes. Investing in our securities involves risks. Exercising your rights should be considered as carefully as any other equity investment. Some of the risks include the following:

|

||

|

•

|

You may not revoke your subscription rights once you exercise them and so you could be committed to buying shares above the prevailing market value of our common stock.

|

||

vii

|

•

|

If you do not act promptly and follow subscription instructions, then we may reject your exercise of subscription rights.

|

||

|

•

|

For a more complete discussion of the risks associated with an investment in our common stock, you should carefully review the section captioned “Risk Factors”.

|

||

|

Q:

|

May I transfer my subscription rights if I do not want to purchase any shares?

|

||

|

A:

|

No. Your subscription rights are not transferable.

|

||

|

Q:

|

Is there a minimum subscription required to complete the rights offering?

|

||

|

A:

|

There is no individual minimum purchase requirement in the rights offering. However, we will not complete the rights offering unless we receive aggregate subscriptions of at least $5.0 million (1,000,000 shares) of common stock in the rights offering.

|

||

|

Q:

|

Is there a limit to how much common stock will be issued in the rights offering?

|

||

|

A:

|

We will accept subscriptions for a maximum of $10.0 million (2,000,000 shares) of common stock in the rights offering

|

||

|

Q:

|

How many shares will be outstanding after the rights offering?

|

||

|

A:

|

There were 2,938,871 shares of our common stock outstanding as of October 29, 2013. If the maximum number of shares are sold in the rights offering we expect there will be 4,938,000 shares of our common stock outstanding. If the minimum number of shares are sold in the rights offering, we expect there will be 3,938,000 shares of our common stock outstanding.

|

||

|

Q:

|

After I exercise my subscription rights, can I change my mind and cancel my purchase?

|

||

|

A:

|

No. All exercises of subscription rights are irrevocable.

|

||

|

Q:

|

What are the federal income tax consequences of receiving or exercising my subscription rights as a holder of common stock?

|

||

|

A:

|

A holder of common stock will not recognize income or loss for federal income tax purposes in connection with the receipt or exercise of subscription rights in the rights offering. We urge you to consult your own tax adviser with respect to the particular tax consequences of the rights offering or any related share purchases by you. See section captioned, “Material U.S. Federal Income Tax Consequences,” for more details.

|

||

|

Q:

|

To whom should I send my forms and payment?

|

||

|

A:

|

If your shares are held in the name of a broker, or other nominee holder, then you should send your subscription documents, subscription rights certificate, notices of guaranteed delivery, and subscription payment to that record holder. If you are the record holder, then you should send your subscription documents and subscription payment to American Stock Transfer & Trust Company, LLC at:

By Mail, By Hand, or By Overnight Courier

American Stock Transfer & Trust Company, LLC

Operations Center

Attn: Reorganization Department

6201 15th Avenue

Brooklyn, NY 11219

|

||

viii

|

You are solely responsible for completing delivery to the subscription agent of your subscription documents, and subscription payment. We urge you to allow sufficient time for delivery of your subscription documents and subscription payment to the subscription agent so that they are received by the subscription agent by 5:00 p.m., Eastern Time, on _________, 2013.

|

|||

|

If you send a payment that is insufficient to purchase the number of shares you requested, or if the number of shares you requested is not specified in the forms, the payment received will be applied to exercise your subscription rights to the fullest extent possible based on the amount of the payment received, subject to our decision to sell shares under the oversubscription right and the elimination of fractional shares. Any excess subscription payments received by the subscription agent will be returned, without interest, as soon as practicable following the expiration of the rights offering.

|

|||

|

Q:

|

What form of payment is required to purchase the shares of our common stock?

|

||

|

A:

|

As described in the subscription rights certificate, payments submitted to the subscription agent must be made in full United States currency by:

|

||

|

•

|

personal or certified check to American Stock Transfer & Trust Company, LLC, drawn upon a United States bank; or

|

||

|

•

|

wire transfer of immediately available funds to accounts maintained by American Stock Transfer & Trust Company, LLC

|

||

|

Q:

|

What should I do if I want to participate in the rights offering but my shares are held in the name of my broker, custodian bank, or other nominee?

|

||

|

A:

|

If you hold shares of our common stock through a broker, custodian bank, or other nominee, then we will ask your broker, custodian bank, or other nominee to notify you of the rights offering. If you wish to exercise your subscription rights, then you will need to have your broker, custodian bank, or other nominee act for you.

|

||

|

Q:

|

When will I receive my new shares?

|

||

|

A:

|

If you purchase stock in the rights offering by submitting a subscription rights certificate and payment, we will mail you a stock certificate representing your new shares as soon as practicable after the expiration of the rights offering; however, we will not be able to begin calculations for any oversubscription pro rata allocations and adjustments until approximately three days after the expiration time of the rights offering, which is the latest date for our stockholders to deliver the subscription rights certificate according to the guaranteed delivery procedures. If your shares are held by your nominee, and you participate in the rights offering, you will not receive a stock certificate for your new shares. Your nominee will be credited with the shares of common stock you purchase in the rights offering as soon as practicable after the expiration of the rights offering.

|

||

|

Q:

|

What should I do if I have other questions?

|

||

|

A:

|

If you have questions or need assistance about the procedure for exercising your rights, including the procedure if you have lost your rights certificate, please contact, AST Phoenix Advisors, which is acting as our information agent, at:

|

||

ix

By Telephone

(866) 796-1285

(From 9:00 a.m. to 10:00 p.m., Eastern Time, Monday through Friday)

By Mail

AST Phoenix Advisors

6201 15th Avenue

Brooklyn, NY 11219

|

You may also contact Bob Regnier, our President and Chief Executive Officer, at (913) 234-2240 or Mark Fortino our Chief Financial Officer, at (913) 234-2345 from 7:00 a.m. to 6:00 p.m., Central Time, Monday through Friday, if you have any questions.

|

x

|

PROSPECTUS SUMMARY

This summary highlights information contained elsewhere in this prospectus or incorporated herein. Because this is a summary, it does not contain all the information that may be important to you. For a more complete understanding, you should carefully read the more detailed information set out in this prospectus, especially the “Risk Factors” section, as well as the financial statements and the related notes to those statements included elsewhere in this prospectus.

The Company

Blue Valley, a Kansas corporation, is a bank holding company organized in 1989. The Bank, the Company’s primary wholly-owned subsidiary, was also organized in 1989 to provide banking services to closely-held businesses and their owners, professionals and residents in Johnson County, Kansas, a high growth, demographically attractive area within the Kansas City, Missouri — Kansas Metropolitan Statistical Area (the “Kansas City MSA”). The focus of Blue Valley has been to take advantage of the current and anticipated growth in our market area as well as to serve the needs of small and mid-sized commercial customers. We believe that these customers are underserved as a result of banking consolidation in the industry generally and within our market specifically. We are an emerging growth company as defined in the Jumpstart Our Business Startups Act of 2012, or JOBS Act and, as such, may elect to comply with certain reduced public company reporting requirements for future filings. We will remain an emerging growth company until the earlier of (1) the last day of the fiscal year (a) following the fifth anniversary of the completion of this offering, (b) in which we have total annual gross revenue of at least $1.0 billion, or (c) in which we are deemed to be a large accelerated filer, which means the market value of our common stock that is held by non-affiliates exceeds $700 million as of the prior June 30th, or (2) the date on which we have issued more than $1.0 billion in non-convertible debt securities during the prior three-year period.

The Bank operates a total of five banking center locations in Johnson County, Kansas, including our main office, which includes a lobby banking center in Overland Park, as well as full-service offices in Leawood, Lenexa, Olathe, and Shawnee, Kansas.

The Company’s lending activities are focused on commercial, commercial real estate, construction, home equity and residential real estate lending. In addition, the Bank infrequently engages in lease financing and provides consumer lending. The Company strives to identify, develop and maintain diversified lines of business that provide acceptable risk-adjusted returns.

The Company seeks to develop lines of business that diversify the Bank’s revenue sources, increase the Bank’s non-interest income and offer additional value-added services to the Bank’s customers. We develop these new or existing lines of business while monitoring related risk factors. In addition to fees generated in conjunction with lending activities, the Bank derives non-interest income by providing mortgage origination, deposit and cash management services, as well as trust and investment brokerage services.

In addition to the Bank, the Company has two wholly-owned subsidiaries, BVBC Capital Trust II and BVBC Capital Trust III, which issued the Subordinated Debentures.

We experienced losses from the third quarter of 2008 through the second quarter of 2012. During that period, the book value of our common stock decreased from $19.97 on December 31, 2008 to $6.20 on June 30, 2012. A significant portion of this decline in the book value per common share was attributable to the valuation allowance recorded in 2011 for our deferred tax asset. The subsequent decline in the book value per common share to $4.94 as of September 30, 2013 is primarily attributable to the accrual of dividends on our Fixed Rate Cumulative Preferred Stock and unrealized losses in our Securities Available for Sale portfolio resulting from increases in market interest rates.

On December 5, 2008, we issued and sold 21,750 shares of Fixed Rate Cumulative Preferred Stock, along with a ten year warrant to purchase 111,083 shares of our common stock for $29.37 per share, for a total cash price of $21.75 million to the United States Department of Treasury (the “Treasury”). The Fixed Rate Cumulative Preferred Stock is now held by third party investors unaffiliated with the U.S. government.

1

|

|||

|

The Board of Directors of the Company and the Bank entered into a written agreement with the Federal Reserve Bank of Kansas City as of November 4, 2009. This agreement was a result of an examination that was completed by the regulators in May 2009, and related primarily to the Bank’s asset quality. Under the terms of the agreement, the Company and the Bank agreed, among other things, to submit an enhanced written plan to strengthen credit risk management practices and improve the Bank’s position on past due loans, classified loans, and other real estate owned; review and revise its allowance for loan and lease loss methodology and maintain an adequate allowance for loan loss; maintain sufficient capital at the Company and Bank level; and improve the Bank’s earnings and overall condition. The Company and Bank also agreed not to increase or guarantee any debt, purchase or redeem any shares of stock or declare or pay any dividends without prior written approval from the Federal Reserve Bank. The Company and the Bank substantially complied with all terms of the written agreement.

As a result of a November 12, 2012 regulatory examination, which noted the improved financial condition of the Company and the Bank, satisfactory risk management processes, and senior management oversight, as well as full compliance with all actionable provisions of the Written Agreement, the Federal Reserve Bank of Kansas City terminated the November 4, 2009 Written Agreement and, effective January 11, 2013, replaced it with a Memorandum of Understanding (“MOU”). The MOU’s purpose is to maintain the financial soundness of the Company and the Bank, and provides, among other things, the Company and the Bank will continue to work on improvement of asset quality, maintain an adequate allowance for loan losses, maintain adequate capital, improve earnings, and not declare or pay any dividends or increase or guarantee any debt without prior written approval from the Federal Reserve Bank and the Office of the State Banking Commissioner of Kansas (“OSBC”).

Under the MOU, prior regulatory approval is currently required before the payment of any dividends by the Bank. In prior years, the Company has relied on dividends from the Bank to assist in making debt service and dividend payments. There is no assurance that the Company will resume paying dividends on its common stock. Even if the Company resumes paying dividends, future payment of cash dividends on its common stock, if any, will be subject to the prior payment of all unpaid dividends and deferred distributions on the Fixed Rate Cumulative Preferred Stock. All dividends are declared and paid at the discretion of the Company’s Board of Directors and are dependent upon our liquidity, financial condition, results of operations, capital requirements and such other factors as our Board of Directors may deem relevant.

The Company has also agreed at the request of the Federal Reserve Bank of Kansas City to defer interest payments and not pay dividends on the Subordinated Debentures without prior regulatory approval in an effort to preserve capital. As a result, the Company has deferred the payment of quarterly interest related to the Subordinated Debentures issued by BVBC Capital Trust III since March 31, 2009 and the payment of quarterly interest related to the Subordinated Debentures issued by BVBC Capital Trust II since April 24, 2009. As of October 31, 2013, the Company has deferred 19 scheduled quarterly interest payments on the Subordinated Debentures issued by BVBC Capital Trust III and 19 scheduled quarterly interest payments on the Subordinated Debentures issued by BVBC Capital Trust II. As of September 30, 2013 and December 31, 2012, the Company had accrued $3.9 million and $3.2 million, respectively, for interest on the Subordinated Debentures. The Company requested and has been granted prior approval from the Federal Reserve Bank of Kansas City to use the proceeds from this offering to pay the deferred interest due on the Subordinated Debentures issued by BVBC Capital Trust II and BVBC Capital Trust III. This will improve our earnings by eliminating double interest and compounding interest on these debentures. See the section of this prospectus captioned “Use of Proceeds,” for more details.

In addition, at the request of the Federal Reserve Bank of Kansas City, the Company has deferred the payment of quarterly dividends on the Fixed Rate Cumulative Preferred Stock since May 15, 2009. The Fixed Rate Cumulative Preferred Stock carries a 5% per year cumulative preferred dividend rate, payable quarterly . The dividend rate increases to 9% beginning with the May 15, 2014 quarterly payment, which will cause our quarterly dividend to increase from $271,875 to $493,375. Dividends compound if they accrue and are not paid. Failure by the Company to pay dividends on the Fixed Rate Cumulative Preferred Stock is not an event of default. However, a failure to pay a total of six preferred share dividends, whether or not consecutive, gives the holders of the Fixed Rate Cumulative Preferred Stock the right to elect two directors to the Company’s Board of Directors. That right continues until the Company pays all dividends in arrears. As of October 31, 2013, the Company has deferred 18 dividend payments. In 2012, the holder of the Fixed Rate Cumulative Preferred Stock elected James L. Gegg to serve on the Company’s Board of Directors. This board seat was terminated in 2013 upon completion of the auction of our Fixed Rate Cumulative Preferred Stock by the Treasury to private investors, almost all of whom we have been advised have

|

|||

| 2 | |||

|

waived their right to elect directors. In recognition of Mr. Gegg’s valuable contributions, the Board of Directors subsequently appointed Mr. Gegg to fill a vacancy on the Board. As of September 30, 2013 and December 31, 2012, the Company had accrued $5.5 million and $4.5 million, respectively, for dividends and interest on the Fixed Rate Cumulative Preferred Stock.

Our principal executive offices are located at 11935 Riley, Overland Park, Kansas 66225-6128, and our telephone number is (913) 338-1000. Our website address is http://www.bankbv.com. Information included or referred to on our website is not incorporated by reference in or otherwise a part of this prospectus.

|

||||

|

The Rights Offering

|

||||

| Securities Offered By Us: |

We are distributing to you, at no charge, a non-transferable subscription right for each share of our common stock that you owned as of 5:00 p.m., Eastern Time, on October 29, 2013, the record date, either as a holder of record or, in the case of shares held of record by custodian banks, brokers, dealers, or other nominees on your behalf, as a beneficial owner of such shares. If the rights offering is fully subscribed, the gross proceeds from the rights offering will be $10.0 million.

|

|||

| Subscription Price: | $5.00 per share | |||

| Minimum Offering: | The rights offering is conditioned upon the receipt of minimum gross proceeds of $5.0 million. | |||

| Maximum Offering: | The rights offering is subject to a limit of $10.0 million in gross proceeds, including any oversubscription rights that we, in our sole discretion, elect to honor. | |||

| Common Stock to be Outstanding Immediately After This Offering: | Assuming no options are exercised prior to the expiration of the rights offering and assuming the minimum or maximum number of shares are sold in the rights offering, we expect approximately 3,938,000 or 4,938,000 shares of our common stock will be outstanding, respectively, immediately after completion of the rights offering. | |||

| Record Date: | 5:00 p.m. Eastern Time on October 29, 2013. | |||

| Basic Rights of Common Stockholders: | As a common stockholder, you are entitled to receive a subscription right for each whole share of our common stock you owned on the record date. For each basic subscription right you hold, you may purchase 0.6805 shares of our common stock. | |||

|

Oversubscription Right:

|

In the event that you purchase all of the shares of our common stock available to you pursuant to your basic subscription rights, you may also choose to purchase a portion of any shares of our common stock that our other stockholders do not purchase through the exercise of their basic subscription rights. The number of shares of our common stock that you purchase pursuant to this oversubscription right will be determined on a pro rata basis and will be subject to our decision to honor, in our sole discretion, the oversubscription rights.

|

|||

| Nontransferability: | You may not transfer your subscription rights. | |||

| Irrevocability: | Once you submit a subscription, you may not revoke it. | |||

| Best Efforts Offering: | We are offering the shares on a best efforts basis. This means there is no guarantee that we will be able to sell all or any of the shares offered. We intend to pay no commissions on shares we sell in this offering. However, we have reserved the right to retain brokers or sales agents to assist us in selling the shares, if we deem it necessary. | |||

|

3

|

||||

| No Recommendation: | Our Board of Directors is making no recommendation as to whether you should subscribe for shares pursuant to either your basic right or your oversubscription right. | |||

|

Board and Executive Officer Commitment:

|

We expect that certain of our directors and executive officers, and certain of the directors of the Bank, together with their affiliates, will participate in the rights offering, although they are not required to do so. The purchase price paid by them will be the same paid by all other persons who purchase shares of our common stock in the rights offering. We also expect that certain of our officers and directors will, if necessary, subscribe for additional shares of common stock in the aggregate amount required to raise the minimum gross proceeds.

|

|||

|

Use Of Proceeds:

|

We intend to use the first $4.1 million of net proceeds of the rights offering to bring current all previously accrued and unpaid dividends on the Subordinated Debentures. This will improve our earnings by eliminating double interest and compounding interest currently being paid on the Subordinated Debentures. We intend to use any remaining proceeds for general corporate purposes. See the section of this prospectus captioned “Use of Proceeds” for further details.

|

|||

|

Fees and Expenses:

|

We will pay the fees and expenses of the rights offering, estimated to be approximately $350,000.

|

|||

|

Risk Factors:

|

See the section of this prospectus captioned “Risk Factors” on page 6 and other information included in this prospectus for a discussion of certain factors that you should carefully consider before making a decision to invest in our common stock.

|

|||

|

Expiration Date:

|

The offering will terminate on _________, 2013 , unless extended by our Board of Directors for up to an additional 45 days.

|

|||

|

Subscription Agent and Information Agent:

|

We have retained American Stock Transfer & Trust Company, LLC to act as the subscription agent and AST Phoenix Advisors to as as the information agent for the rights offering. The process for you to follow in communicating with American Stock Transfer & Trust Company, LLC and AST Phoenix Advisors is set forth in the section of this prospectus captioned “QUESTIONS AND ANSWERS ABOUT THE RIGHTS OFFERING”.

|

|||

|

4

|

||||

USE OF PROCEEDS

Assuming the sale of the minimum or maximum number of shares in the rights offering, we estimate that the aggregate net proceeds from the rights offering, after deducting estimated offering expenses of approximately $350,000, will be approximately $4.65 million or $9.65 million, respectively. If we sell more than the minimum but less than the maximum number of shares, our net proceeds will be somewhere between $4.65 million and $9.65 million. We intend to use the first $4.1 million of net proceeds to bring current all previously accrued and unpaid dividends on the Subordinated Debentures. This will improve our earnings by eliminating double interest and compounding interest currently being paid on the Subordinated Debentures. We intend to use any remaining proceeds for general corporate purposes.

The precise amounts and timing of the application of the net proceeds from this offering depend upon many factors, including, but not limited to, the amount of any such proceeds and actual funding requirements. Until the proceeds are used, the Company may invest the proceeds, depending on its cash flow requirements, in short- and long-term investments, including, but not limited to treasury bills, commercial paper, certificates of deposit, securities issued by U.S. government agencies, money market funds, repurchase agreements and other similar investments.

5

RISK FACTORS

Investing in our common stock involves a high degree of risk. In addition to the following risk factors and other information contained in this prospectus, including the matters under the caption “Cautionary Note Regarding Forward-Looking Statements” and “Management’s Discussion and Analysis of Financial Condition,” you should carefully consider the risks described below before deciding whether to invest in our common stock. If any of the following risks actually occur, our business, financial condition, operating results and prospects would suffer. In that case, the trading price of our common stock would likely decline and you might lose all or part of your investment. The risks described below are not the only ones we face. Additional risks that we currently do not know about or that we currently believe to be immaterial may also impair our operations and business results.

Risks Related to the Rights Offering

The subscription price determined for this rights offering is not necessarily an indication of our value.

The subscription price per share was arbitrarily set by our Board of Directors after consideration of a number of factors, including: the price at which our stockholders might be willing to participate in the rights offering, historical and current trading prices for our common stock, the need for liquidity and capital, potential market conditions, and the desire to provide an opportunity to our stockholders to participate in the rights offering on a pro rata basis. In conjunction with its review of these factors, our Board of Directors also reviewed our history and prospects, including our past and present earnings, our prospects for future earnings, our current financial condition and regulatory status. The subscription price does not necessarily bear any relationship to the book value of our assets, past operations, cash flows, income, financial condition or any other established criteria for value. You should not consider the subscription price as an indication of the value of our common stock.

Because our management will have broad discretion over the use of the net proceeds from the rights offering, you may not agree with how we use the proceeds, and we may not invest the proceeds effectively.

We intend to use the proceeds of the rights offering to improve our earnings by eliminating double interest and compounding interest. We will achieve this goal by bringing current all previously accrued and unpaid dividends on our Subordinated Debentures, with any additional proceeds to be used for general corporate purposes. Our management will, however, have broad discretion in the application of the proceeds from the rights offering. Because of the number and variability of factors that will determine our use of the proceeds from the rights offering, their ultimate use may vary substantially from our currently intended use. Moreover, our management may use the proceeds for corporate purposes that may not increase our market value or make us profitable. In addition, it may take us some time to deploy the proceeds from this offering effectively in accordance with our intended uses. Management’s failure to utilize the proceeds effectively could have an adverse effect on our business, financial condition and results of operations.

All exercises of subscription rights are irrevocable, even if the market price of our common stock declines below the subscription price you have paid.

Once you exercise your subscription rights, you may not revoke them. It is possible that the market price of our common stock will decline after you elect to exercise your subscription rights. If you exercise your subscription rights and, afterwards, the public trading market price of our common stock decreases below the subscription price, you will have committed to buying shares of our common stock at a price above the prevailing market price and could have an immediate unrealized loss.

The subscription rights are not transferable and there is no market for the subscription rights.

You may not sell, give away or otherwise transfer your subscription rights. The subscription rights are only transferable by operation of law. Because the subscription rights are otherwise non-transferable, there is no market or other means for you to directly realize any value associated with the subscription rights. You must exercise the subscription rights and acquire additional shares of our common stock to realize any value from your subscription rights.

6

If you do not exercise your subscription rights, your percentage ownership in the Company will be diluted.

Assuming we sell the maximum amount of common stock issuable in connection with the rights offering, we will issue approximately 2,000,000 shares. If you choose not to exercise your subscription rights prior to the expiration of the rights offering, your relative ownership interest in our common stock will be diluted.

We may cancel the rights offering at any time prior to the expiration of the rights offering, and neither we nor the subscription agent will have any obligation to you except to return your exercise payments.

We may, in our sole discretion, decide not to continue with the rights offering or cancel the rights offering prior to the expiration of the rights offering. If the rights offering is cancelled, all subscription payments that the subscription agent has received will be returned, without interest, as soon as practicable.

If you do not act promptly and follow the subscription instructions, we may reject your exercise of subscription rights.

If you desire to purchase shares in the rights offering, you must act promptly to ensure that the subscription agent actually receives all required forms and payments before the expiration of the rights offering at [__] p.m., Eastern Time, on _________, 2013. If you are beneficial owner of shares, you must act promptly to ensure that your broker, custodian bank or other nominee holder acts for you and that all required forms and payments are actually received by the subscription agent before the expiration of the rights offering. We are not responsible if your broker, or other nominee holder, fails to ensure that the subscription agent receives all required forms and payments before the expiration of the rights offering. If you fail to complete and sign the required subscription forms, send an incorrect payment amount, or otherwise fail to follow the subscription procedures that apply to the exercise of your subscription rights prior to the expiration of the rights offering, the subscription agent may reject your subscription or accept it only to the extent of the payment received. Neither we nor our subscription agent undertake any responsibility to contact you concerning an incomplete or incorrect subscription form or payment, nor are we under any obligation to correct such forms or payment. We have the sole discretion to determine whether a subscription exercise properly complies with the subscription procedures.

If we do not generate the desired level of capital from the rights offering, we may try to raise additional capital and can give no assurance as to what the cost of that capital may be.

If we do not complete the rights offering or raise sufficient capital in the rights offering, we may have to sell additional securities in order to generate the desired capital. We may seek to raise additional capital through additional offerings of our common stock, preferred stock, securities convertible into common stock, or rights to acquire such securities or our common stock. The issuance of any additional shares of common stock or convertible securities in a subsequent offering could be substantially dilutive to stockholders of our common stock. Dilution is the difference between what you pay for your stock and the net tangible book value per share immediately after the additional shares are sold by us. Holders of our shares of common stock have no preemptive rights as a matter of law that entitle them to purchase their pro-rata share of any offering or shares of any class or series. The market price of our common stock could decline as a result of additional sales of shares of our common stock or the perception that such sales could occur.

New investors also may have rights, preferences, and privileges that are senior to, and that could adversely affect, our then current stockholders. For example, preferred stock would be senior to shares of our common stock.

We cannot predict or estimate the amount, timing, or nature of our future offerings. Thus, our stockholders bear the risk of our future offerings diluting their stock holdings, adversely affecting their rights as stockholders, and/or reducing the market price of our common stock.

7

You will not receive any interest on funds submitted by you to the Subscription Agent in the event all or a portion of such funds are returned to you for any reason.

Funds delivered to and held by the subscription agent will be held in escrow in a segregated, non-interest bearing account. As a result, no interest will be earned on such funds while they are held pending the expiration of the rights offering. Any funds returned to you in the event of the cancellation of the rights offering, overpayment of the subscription price in connection with the basic subscription right or over-subscription privilege or otherwise will be returned to you without interest thereon.

Our position for U.S. federal income tax consequences on the receipt of the subscription rights may not be sustained by the Internal Revenue Service.

A risk exists as to the value, if any, of the subscription right. If the value is more than 15% of the value of the common stock, or you elect to allocate basis to the subscription right, a risk exists that the IRS may challenge the value of the subscription right, which could affect the amount of gain or loss recognized on the sale of particular shares of our common stock owned by you. The Company has not sought any third party appraisal for guidance on the value of the subscription rights.

Risks Related to Blue Valley

Our operations may be adversely affected if we are unable to maintain and increase our deposit base and secure adequate funding.

We fund our banking and lending activities primarily through demand, savings and time deposits and, to a lesser extent, lines of credit, sale/repurchase facilities from various financial institutions, securities sold under agreement to repurchase and FHLBank borrowings. The success of our business depends in part on our ability to maintain and increase our deposit base and our ability to maintain access to other funding sources. Our inability to obtain funding on favorable terms, on a timely basis, or at all, would adversely affect our operations and financial condition.

The loss of our key personnel could adversely affect our operations.

We are a relatively small organization and depend on the services of all of our employees. Our growth and development to date has depended in a large part on a few key employees who have primary responsibility for maintaining personal relationships with our largest customers. The unexpected loss of services of one or more of these key employees could have a material adverse effect on our operations. Our key employees are Robert D. Regnier, Mark A. Fortino, Bruce A. Easterly, and Bonnie M. McConnaughy. Each of these persons is an officer of the Bank. We do not have written employment or non-compete agreements with any of these key employees; however, if employment was terminated, Mr. Regnier would lose 16,930 Blue Valley Ban Corp. Restricted Stock Awards and Mr. Fortino, Mr. Easterly, and Ms. McConnaughy would each lose 1,600 of Blue Valley Ban Corp. Restricted Stock Awards. We carry bank owned life insurance policies on each of these executive officers.

Changes in interest rates may adversely affect our earnings and cost of funds.

Changes in interest rates affect our operating performance and financial condition in diverse ways. A substantial part of our profitability depends on the difference between the rates we receive on loans and investments and the rates we pay for deposits and other sources of funds. Our net interest spread will depend on many factors that are partly or entirely outside our control, including competition, federal monetary and fiscal policies, and economic conditions generally. Historically, net interest spreads for many financial institutions have widened and narrowed in response to these and other factors, which are often collectively referred to as “interest rate risk.” We try to minimize our exposure to interest rate risk, but are unable to eliminate it. As discussed on page [77], we use an asset/liability modeling system to analyze our current sensitivity to instantaneous and permanent changes in interest rates. The system simulates our asset and liability base and projects future net interest income results under several interest rate assumptions. This allows management to view how changes in interest rates will affect the spread between the yield received on assets and the cost of deposits and borrowed funds. Among other strategies, we attempt to mitigate the risk from increases in interest rates by maintaining a significant level of adjustable rate loans in our portfolio, and

8

attempt to mitigate the risk from declines in interest rates by implementing rate floors for our adjustable rate loan portfolio and managing our level of fixed rate liabilities. As illustrated in the Interest-Rate Sensitivity Analysis on page [78], as of September 30, 2013, approximately 57% of our loan portfolio has variable rates, and approximately 51% of our loan portfolio matures or reprices in 90 days or less. As a result of the number of adjustable rate loans in our portfolio, increases in interest rates will expose us to greater risk of delinquencies and defaults on such loans, which could lead to decreased earnings. In addition, increased interest rates may decrease the number of loans that we originate, which could also lead to decreased earnings.

Because our business is concentrated in the Kansas City MSA, a downturn in the economy of the Kansas City MSA may adversely affect our business.

Our success is dependent to a significant extent upon the general economic conditions in the Kansas City MSA, including Johnson County, Kansas, and, in particular, the conditions for the medium- and small-sized businesses that are the focus of our customer base. Adverse changes in economic conditions in the Kansas City MSA, including Johnson County, Kansas, could impair our ability to collect loans, reduce our growth rate and have a negative effect on our overall financial condition.

If our allowance for loan losses is insufficient to absorb losses in our loan portfolio, it will adversely affect our financial condition and results of operations.

Some borrowers may not repay loans that we make to them. This risk is inherent in the banking business. Like all financial institutions, the Company maintains an allowance for loan losses to absorb probable loan losses in our loan portfolio. The level of the allowance reflects management’s continuing evaluation of industry concentrations, specific credit risks, loan loss experience, current loan portfolio credit quality, economic and regulatory conditions and unidentified losses inherent in the current loan portfolio. However, we cannot predict loan losses with certainty, and we cannot assure you that our allowance will be sufficient to cover our future loan losses. Loan losses in excess of our reserves would have a material adverse effect on our financial condition and results of operations.

In addition, various regulatory agencies, as an integral part of the examination process, periodically review our loan portfolio. These agencies may require us to add to the allowance for loan losses based on their judgments and interpretations of information available to them at the time of their examinations. If these agencies require us to increase our allowance for loan losses, our earnings will be adversely affected in the period in which the increase occurs.

Our concentration of loans secured by real estate may continue to adversely affect our financial condition and results of operations.

As of September 30, 2013, approximately $132.8 million, or 32.69% of our loan portfolio, represented commercial real estate loans and approximately $51.0 million, or 12.54%, of our loan portfolio consisted of residential mortgage loans. A downturn in the real estate market, the deterioration in the value of collateral, and the local and national economic recessions would adversely affect our customers’ ability to sell or refinance real estate and repay their loans. In the event we are required to foreclose on a property securing one of our mortgage loans, or otherwise pursue remedies in order to protect our investment, we may be unable to recover enough value from the collateral to prevent a loss.

We may incur significant costs if we foreclose on environmentally contaminated real estate.

If we foreclose on a defaulted real estate loan to recover our investment, we may be subject to environmental liabilities in connection with the underlying real property. It is also possible that hazardous substances or wastes may be discovered on these properties during our ownership or after they are sold to a third party. If they are discovered on a property that we have acquired through foreclosure or otherwise, we may be required to remove those substances and clean up the property. We may have to pay for the entire cost of any removal and clean-up without the contribution of any other third parties. We may also be liable to tenants and other users of neighboring properties. These costs or liabilities may exceed the fair value of the property. In addition, we may find it difficult or impossible to sell the property prior to or following any environmental clean-up.

9

The Bank is subject to possible future repurchase and indemnification demands on mortgage loans previously sold to investors.

The Bank is subject to possible future repurchase and indemnification demands for future losses realized by investors for alleged breaches of representations and warranties on mortgage loans previously sold to investors. The financial services industry has been materially and adversely impacted by a prolonged period of negative economic conditions , including, but not limited to, high levels of unemployment, declines in asset values, as well as delinquencies and defaults on loans. These defaults on loans include, but are not limited to, possible “strategic defaults” which are characterized by borrowers that appear to have the financial means to meet the debt service requirements of their loans, however, elect not to do so because the value of the assets securing their debts may have declined below the amount of the debt or in consideration of statutory restrictions which impede a lender’s ability to exercise prudent collection efforts or foreclose in an efficient manner. The Company’s consolidated financial statements have been prepared using values and information currently available to the Company; however, there can be no assurance that the impact of these conditions will cease or reverse to mitigate possible risk of future potential losses by the Bank.

If we are not able to compete effectively in the highly competitive banking industry, our business will be adversely affected.

Our business is extremely competitive. Many of our competitors are, or are affiliates of, enterprises that have greater resources, name recognition and market presence than we do. Some of our competitors are not regulated as extensively as we are and, therefore, may have greater flexibility in competing for business. Some of these competitors are subject to similar regulation but have the advantages of established customer bases, higher lending limits, extensive branch networks, numerous ATMs, and more ability to absorb the costs of maintaining technology or other factors.

Blue Valley and the Bank are subject to extensive governmental regulation.