Exhibit 10.1

EXECUTION COPY

CAPACITY PURCHASE AGREEMENT

between

AMERICAN AIRLINES, INC.

AND

AIR WISCONSIN AIRLINES LLC

EFFECTIVE AS OF AUGUST 19, 2022

TABLE OF CONTENTS

| ARTICLE I. DEFINITIONS |

1 | |||||

| ARTICLE II. CAPACITY PURCHASE, REVENUES AND OTHER SERVICES |

1 | |||||

| 2.01 |

Capacity Purchase | 1 | ||||

| 2.02 |

Flight Related Revenues | 2 | ||||

| 2.03 |

Non-Revenue Pass Travel | 3 | ||||

| 2.04 |

Ground Handling | 3 | ||||

| ARTICLE III. USE OF COVERED AIRCRAFT |

3 | |||||

| 3.01 |

Use of Covered Aircraft | 3 | ||||

| 3.02 |

Additional Aircraft; Spare Aircraft; Aircraft Substitution; Neutral Livery Aircraft | 4 | ||||

| 3.03 |

Aircraft Unavailability | 5 | ||||

| 3.04 |

Supportability Commitment | 6 | ||||

| 3.05 |

Flight Designator Codes and Codeshare Term | 6 | ||||

| 3.06 |

Flight Dispatch | 7 | ||||

| 3.07 |

Maintenance of Supported Aircraft | 7 | ||||

| 3.08 |

Compliance with Other Terms of Related Agreements | 9 | ||||

| 3.09 |

Event of Loss | 9 | ||||

| ARTICLE IV. SERVICE STANDARDS, PERFORMANCE MEASUREMENT AND TRAINING |

9 | |||||

| 4.01 |

Crews and Other Personnel | 9 | ||||

| 4.02 |

Governmental Regulations | 9 | ||||

| 4.03 |

Quality of Service | 10 | ||||

| 4.04 |

Access and Use of American Systems | 12 | ||||

| 4.05 |

Data Security | 13 | ||||

| 4.06 |

Processing and Adjudicating Customer or Passenger Complaints | 14 | ||||

| 4.07 |

Right to Inspect Aircraft and Service Conditions | 15 | ||||

| 4.08 |

Controllable Cancellation Codes and Controllable On Time Departure Codes | 16 | ||||

| 4.09 |

Catering Products and Catering Services | 16 | ||||

| ARTICLE V. SAFETY |

16 | |||||

| 5.01 |

Incidents or Accidents | 16 | ||||

| 5.02 |

Accident Reports | 17 | ||||

| 5.03 |

International Air Transport Association Operational Safety Audit | 17 | ||||

| 5.04 |

Emergency Assistance Agreement | 17 | ||||

| ARTICLE VI. OTHER OBLIGATIONS OF CONTRACTOR |

17 | |||||

| 6.01 |

FAA or DOT Certification Suspension or Revocation | 17 | ||||

| 6.02 |

Fuel Efficiency Program | 17 | ||||

| 6.03 |

Use of Approved Marks and Copyrights | 18 | ||||

| 6.04 |

Ownership and Use of Data | 20 | ||||

| 6.05 |

American’s AAdvantage® Program | 21 | ||||

| 6.06 |

Periodic Reports | 21 | ||||

| 6.07 |

Intentionally Omitted | 22 | ||||

| 6.08 |

Liquor Licenses for Covered Aircraft | 22 | ||||

| 6.09 |

Intentionally Omitted | 22 | ||||

| 6.10 |

Eagle Partnership Manuals | 22 | ||||

| 6.11 |

Review of Insurance Coverage | 22 | ||||

| 6.12 |

Intentionally Omitted | 23 | ||||

i

| 6.13 |

Intentionally Omitted | 23 | ||||

| 6.14 |

Late Reduced Crew Estimates | 23 | ||||

| 6.15 |

Unsupported Aircraft | 24 | ||||

| 6.16 |

Resource Allocation | 25 | ||||

| 6.17 |

Actions during a Force Majeure Event or Labor Dispute | 25 | ||||

| ARTICLE VII. CONTRACTOR’S COMPENSATION |

26 | |||||

| 7.01 |

Base and Incentive Payments | 26 | ||||

| 7.02 |

Costs and Expenses | 26 | ||||

| 7.03 |

Cost Savings | 26 | ||||

| ARTICLE VIII. USE OF FACILITIES |

26 | |||||

| 8.01 |

Facilities | 26 | ||||

| 8.02 |

Conditions of Use for American Facilities | 27 | ||||

| 8.03 |

Replacement and Termination of Facilities Use | 27 | ||||

| 8.04 |

Facilities Related Insurance | 27 | ||||

| 8.05 |

Subleases | 27 | ||||

| ARTICLE IX. REPRESENTATIONS, WARRANTIES AND ACKNOWLEDGEMENTS |

28 | |||||

| 9.01 |

Contractor’s Representations and Warranties | 28 | ||||

| 9.02 |

American Representations and Warranties | 29 | ||||

| ARTICLE X. INSURANCE |

29 | |||||

| 10.01 |

Minimum Insurance Coverage | 29 | ||||

| 10.02 |

Endorsements | 31 | ||||

| ARTICLE XI. INDEMNIFICATION |

32 | |||||

| 11.01 |

Contractor’s Indemnification of American Indemnified Parties | 32 | ||||

| 11.02 |

American’s Indemnification of Contractor Indemnified Parties | 33 | ||||

| 11.03 |

Procedure for Indemnification Claims | 33 | ||||

| 11.04 |

Employer’s Liability and Workers’ Compensation | 36 | ||||

| ARTICLE XII. TERM AND TERMINATION |

36 | |||||

| 12.01 |

Term | 36 | ||||

| 12.02 |

Termination and Withdrawal Rights | 36 | ||||

| ARTICLE XIII. INTENTIONALLY OMITTED |

41 | |||||

| 13.01 |

Intentionally Omitted | 41 | ||||

| ARTICLE XIV. MISCELLANEOUS |

41 | |||||

| 14.01 |

Notices | 41 | ||||

| 14.02 |

Binding Effect and Assignment | 43 | ||||

| 14.03 |

Amendment and Modification | 43 | ||||

| 14.04 |

Waiver | 43 | ||||

| 14.05 |

Interpretation | 43 | ||||

| 14.06 |

Confidentiality and Public Communications | 44 | ||||

| 14.07 |

Cooperation with Respect to Reporting | 45 | ||||

| 14.08 |

Right of Set-off | 45 | ||||

| 14.09 |

Counterparts | 46 | ||||

| 14.10 |

Severability | 46 | ||||

| 14.11 |

Governing Law | 46 | ||||

| 14.12 |

Entire Agreement; Conflicts with this Agreement | 46 | ||||

| 14.13 |

Remedies Cumulative | 46 | ||||

| 14.14 |

Further Assurances | 46 | ||||

| 14.15 |

No Third Party Beneficiaries | 47 | ||||

ii

| 14.16 |

Relationship of the Parties | 47 | ||||

| 14.17 |

Jurisdiction | 47 | ||||

| 14.18 |

Waiver of Jury Trial | 48 | ||||

| 14.19 |

Limitation on Damages | 48 | ||||

| 14.20 |

Equitable Remedies | 49 | ||||

| 14.21 |

Survival of Certain Obligations | 49 |

SCHEDULES AND EXHIBITS

| SCHEDULE 1: |

COVERED AIRCRAFT | |

| SCHEDULE 2: |

SCHEDULING AND OPERATING RESTRICTIONS ON COVERED AIRCRAFT | |

| SCHEDULE 3: |

PASS THROUGH COSTS, CONTROLLABLE COSTS AND AMERICAN ABSORBED EXPENSES | |

| SCHEDULE 4: |

FUEL EFFICIENCY PROGRAM | |

| SCHEDULE 5: |

COMPENSATION AND BONUSES AND REBATES | |

| SCHEDULE 6: |

INTENTIONALLY OMITTED | |

| SCHEDULE 7: |

ACCOUNTING AND AUDITING PROCEDURES AND PAYMENT TERMS | |

| SCHEDULE 8: |

CONTROLLABLE CANCELLATION CODES | |

| SCHEDULE 9: |

CONTROLLABLE ON TIME DEPARTURE CODES | |

| SCHEDULE 10: |

INTENTIONALLY OMITTED | |

| SCHEDULE 11: |

AMERICAN FACILITIES | |

| SCHEDULE 12: |

INTERIOR DESIGN OF COVERED AIRCRAFT (INCLUDING LAYOUT FOR PASSENGER ACCOMMODATION) | |

| EXHIBIT A: |

DEFINITIONS | |

| EXHIBIT B: |

STANDARDS OF SERVICE | |

| EXHIBIT C: |

TRAINING | |

| EXHIBIT D: |

AMERICAN’S SECURITY POLICIES AND PROCEDURES | |

| EXHIBIT E: |

STANDARDS OF FACILITIES USE | |

| EXHIBIT F: |

CREW FORECAST TEMPLATE | |

iii

CAPACITY PURCHASE AGREEMENT

This CAPACITY PURCHASE AGREEMENT (as amended, modified or supplemented from time to time, this “Agreement”), is effective as of August 19, 2022 (the “Effective Date”), between AMERICAN AIRLINES, INC., a Delaware corporation (together with its successors and permitted assigns, “American”) and AIR WISCONSIN AIRLINES LLC, a Delaware limited liability company (together with its permitted successors and assigns, “Contractor”).

RECITALS:

WHEREAS, American and Contractor desire to establish the terms by which Contractor will provide Regional Airline Services utilizing certain regional aircraft on behalf of American;

WHEREAS, American holds a certificate of public convenience and necessity issued pursuant to certain federal transportation statutes authorizing it to engage in air transportation of persons, property and mail, and is a major air carrier providing scheduled domestic and international air transportation;

WHEREAS, Contractor holds a certificate of public convenience and necessity issued pursuant to certain federal transportation statutes authorizing it to engage in air transportation of persons, property and mail, and is a regional air carrier providing scheduled air transportation;

WHEREAS, Contractor is willing to provide, on behalf of American under American’s brands, the Regional Airline Services with respect to the Covered Aircraft as set forth herein, and American and Contractor desire to establish the terms by which Contractor will provide such Regional Airline Services; and

WHEREAS, all references to specific Schedules and Exhibits in this Agreement shall be those certain Schedules and Exhibits attached hereto, which shall be deemed incorporated herein by reference and a part of this Agreement for all purposes.

NOW, THEREFORE, for and in consideration of the mutual covenants and agreements herein contained, American, on the one hand, and Contractor, on the other hand, agree as follows:

ARTICLE I.

DEFINITIONS

Capitalized terms used in this Agreement (including, unless otherwise defined therein, in the Schedules and Exhibits to this Agreement) shall have the meanings set forth on Exhibit A hereto.

ARTICLE II.

CAPACITY PURCHASE, REVENUES AND OTHER SERVICES

2.01 Capacity Purchase. Subject to the terms and conditions of this Agreement and the Related Agreements, American shall purchase during the Term hereof all of the capacity of the Covered Aircraft and Contractor shall provide all of the capacity of each Covered Aircraft and shall operate, in accordance with the terms and conditions hereof, Regional Airline Services between various U.S. domestic city-pairs and between various U.S.-Canadian city-pairs as specified by American pursuant to Section 2.01(b). Contractor shall use the Covered Aircraft, solely for, or as directed by, American in connection with Regional Airline Services and, without limiting the foregoing, in accordance with the following:

(a) Fares, Rules and Seat Inventory. American shall in its sole discretion establish and publish all fares, fare rules, related tariff rules, and other similar information for all seats on the Covered Aircraft. Contractor shall not publish any fares, fare rules, related tariff rules (other than as prepared or authorized by American), or other similar information for the Covered Aircraft. In addition, American shall have complete and exclusive control in its sole discretion with respect to the Covered Aircraft relating to all (i) seat inventories, including all positive space and “space available” non-revenue seating, and pass travel policies, subject to Section 2.03, and (ii) revenue management decisions, including pricing, overbooking levels, discount seat levels and allocation of seats among various fare categories.

(b) Flight Schedules. American shall have the right to schedule all CAATS (pursuant to the scheduling procedures set forth on Schedule 2) and Contractor shall operate the CAATS according to such schedule. Subject to the terms and conditions hereof, American shall in its sole discretion establish and publish all schedules for the CAATS, including determining the city pairs served, frequencies and timing of scheduled arrivals and departures of Scheduled Flights; provided that unless otherwise provided for in this Agreement, all such schedules shall be subject to the scheduling procedures set forth on Schedule 2. In no event shall American schedule a Covered Aircraft that is a Spare Aircraft, a Covered Aircraft in Heavy Maintenance or an Unsupported Aircraft to operate a Scheduled Flight. American shall not schedule any flight to a foreign jurisdiction, other than Canada, without Contractor’s prior written consent.

(c) Hubs. Subject to the implementation of Covered Aircraft pursuant to Section 3.01(a) and Schedule 1 and without limiting Section 6.15, the operations for no fewer than [***] CAATS shall be principally based at, and each such CAATS shall operate primarily from, Chicago O’Hare airport (“ORD”). If American intends to have more than [***] CAATS be principally based at, and operate primarily from, another airport where Parent provides airline services [***], then such other airport shall also be deemed a “Hub” hereunder; provided that American delivers Notice of such intention to Contractor at least [***] in advance of the first date that such other airport is intended to be used as a Hub hereunder and during such [***] period, Contractor shall identify any requirements for American Facilities (including crew rooms or line maintenance facilities) that are necessary for Contractor to provide the Regional Airline Services from such new Hub. In the event that a new Hub is added following the Effective Date, Contractor shall take all action necessary to relocate the applicable number of CAATS to such new Hub. Contractor’s costs and expenses in relocating CAATS to be principally based at a new Hub shall be [***] as provided in Schedule 3 and the costs and expenses of the American Facilities for Contractor’s use of the Regional Airline Services will be [***].

2.02 Flight Related Revenues. Contractor acknowledges and agrees that American shall be entitled to and shall receive all revenues (including any consideration received from any interline and non-revenue travel agreements) resulting from the sale or issuance of passenger tickets associated with the Covered Aircraft and all other sources of revenue associated with the operation of the Covered Aircraft, including revenues relating to (a) any tickets sold under the designator code of a Third Party (such as an American codeshare partner); (b) transportation of cargo or mail; (c) ancillary passenger service charges, including any baggage charges, food, beverage (including revenues relating to the sale of beer, wine, liquor or any other alcoholic beverages), unaccompanied minor fees and duty free services; (d) guarantees, incentive payments or cost abatements from Governmental Authorities or other Third Parties in connection with scheduling flights to an airport or locality; (e) ticket change fees; and (f) pass travel and other non-revenue or reduced rate travel charges. All such revenues shall be the sole property of, and shall belong to, American, and if received by Contractor, shall be promptly remitted by Contractor to American. American shall perform all revenue accounting and management functions in connection with all such revenues. The Parties hereto acknowledge and agree that all flight related revenue to which American is entitled hereunder (including under this Section 2.02) is independent of the non-exclusive license of Approved Marks set forth in Section 6.03(b) hereof.

2

2.03 Non-Revenue Pass Travel. American shall have the sole right and option to implement and oversee all pass travel and other non-revenue or reduced rate travel on any Scheduled Flight in accordance with its policies and procedures as in effect and adopted by American from time to time, in its sole discretion.

2.04 Ground Handling. American shall provide, or arrange for another Person to provide, all ground handling and related services with respect to the operation of the Covered Aircraft, including, but not limited to: (a) all gate and ticket counter check in activities, (b) all baggage handling, (c) all cargo handling, if any, (d) all passenger enplaning/deplaning services, including but not limited to sky cap, if any, and wheel chair services, (e) all aircraft loading/unloading services, including but not limited to airside busing (as necessary), (f) all passenger ticketing, (g) all aircraft cabin cleaning and related cleaning supplies, other than routine cabin straightening between Scheduled Flights, (h) all jet bridge maintenance (where applicable), (i) all security functions, (j) all janitorial services in connection with ground handling and related services with respect to the operation of the Covered Aircraft, and (k) all deicing services. In connection therewith, American shall select in its reasonable discretion any Person to perform such services with respect to the operation of the Covered Aircraft without the consent or approval of Contractor.

ARTICLE III.

USE OF COVERED AIRCRAFT

3.01 Use of Covered Aircraft.

(a) Implementation Date. Contractor shall implement Covered Aircraft pursuant to the Implementation Schedule set forth on Schedule 1 attached hereto. The date on which a Covered Aircraft is scheduled to be implemented (as set forth in Schedule 1) and any date that an aircraft becomes a Covered Aircraft pursuant to Contractor’s substitution rights in Section 3.02(d) is referred to herein as such aircraft’s “Implementation Date”); provided that if a Covered Aircraft commences operating Regional Airline Services under this Agreement at an earlier date in accordance with the remainder of this Section 3.01(a), then such earlier date will be deemed to be such Covered Aircraft’s Implementation Date. By delivering written Notice to American as provided below, Contractor may request an earlier Implementation Date than the applicable date set forth on Schedule 1 for one or more Covered Aircraft (each, an “Early Implementation Date”), and American shall accept Contractor’s implementation of such Covered Aircraft upon the corresponding Early Implementation Date so long as: (i) Contractor delivers such Notice to American at least [***] prior to the first [***] in which such Early Implementation Date(s) is to occur; (ii) each such aircraft being, as of the applicable Early Implementation Date, airworthy and in substantially the same condition, configuration and livery requirements as other Covered Aircraft; and (iii) solely with respect to any proposed early implementation that Contractor proposes to occur prior to [***], American having determined, in its reasonable and good faith discretion, that, using commercially reasonable efforts, American will be able to complete all required information technology tasks, personnel training, and station readiness tasks in order to accommodate implementation for such aircraft as of the proposed early implementation date; provided that, in each case (i)-(iii), no such consent will be required to implement a Covered Aircraft pursuant to Contractor’s substitution right set forth in Section 3.02(d).

3

(b) Use for Regional Airline Services. Except as otherwise permitted in this Agreement or as American may otherwise Consent in its reasonable discretion, the Covered Aircraft (i) may only be used by Contractor to provide Regional Airline Services, and (ii) subject to Sections 3.01(c) and 3.01(d), may not be used by Contractor for any other purpose, including flight operations for any other airline or flight operations or activities on Contractor’s own behalf. Contractor shall operate international flights to and from Canada as may be scheduled by American in its sole discretion, subject to the operational limitations of the Covered Aircraft and obtaining necessary DOT and foreign approvals and required operating authorities and licenses, with the Base Compensation, Pass Through Costs and other amounts to be paid to Contractor as set forth on Schedules 3 and 5 hereof, and according to the scheduling requirements as set forth on Schedule 2 hereof.

(c) Ad Hoc Charter Flights. If requested by American upon reasonable prior Notice to Contractor, and subject to Schedule 2 and the other terms of this Agreement, Contractor shall use CAATS for charter flights (which for all purposes of this Agreement shall include any reasonable repositioning flights related to such charter flights) not included in the applicable Final Schedule for the month of such flight and American shall specify the terms of such use; provided that the compensation for such charter flights shall be as provided in Schedule 3.

(d) Maintenance/Ferry Flights. Contractor shall be entitled to use Covered Aircraft for the purpose of Maintenance/Ferry Flights.

(e) CRJ-700. If Contractor provides Notice to American of its desire to use CRJ-700 aircraft in connection with the provision of Regional Airline Services, then the Parties shall discuss in good faith whether such aircraft may be added to the terms of this Agreement; provided that neither Party shall be obligated to add such aircraft to the terms of this Agreement or any other capacity purchase agreement with American, unless mutually agreed.

3.02 Additional Aircraft; Spare Aircraft; Aircraft Substitution; Neutral Livery Aircraft.

(a) Additional Aircraft. Subject to Section 12.02(d)(iv), at any time and from time to time during the Term, if (i) Contractor has sufficient crew to operate any CRJ-200 aircraft, that is then-currently not a Covered Aircraft, at a minimum average daily block hour utilization of [***] block hours per [***] per Supportable CAATS during any [***] and (ii) the number of Covered Aircraft equals the number of Supported Aircraft for such [***], then Contractor may provide and make available to American, and American shall accept, such aircraft as additional Covered Aircraft for an Aircraft Term that will commence beginning as of the start of such [***] and will conclude as of the [***] anniversary of the final day of the Transition Period (each aircraft, an “Additional Aircraft”). The Notice provided by Contractor to American under this Section 3.02(a) will be provided together with the Initial Crew Max and shall specify the number of Additional Aircraft, each Implementation Date and the time at which such Additional Aircraft will be made available at a Hub for Regional Airline Services. Such Additional Aircraft shall be airworthy and in substantially the same condition, configuration and livery requirements as the then-existing Supported Aircraft. Contractor shall take all requisite action to obtain all FAA, DOT, TSA and other certifications, permits, licenses, certificates, exemptions, approvals and plans required by Governmental Authorities, along with any insurance required pursuant to the terms hereof, necessary to enable Contractor to provide Regional Airline Services and operate the Additional Aircraft prior to it being placed in service and shall otherwise cause the Additional Aircraft to meet the terms and conditions for “Supported Aircraft” as specified under this Agreement.

(b) Maximum Number of Covered Aircraft. In no event shall the total aggregate number of Covered Aircraft under this Agreement exceed sixty (60) Covered Aircraft, unless otherwise Consented to by American.

4

(c) Spare Aircraft. Notwithstanding anything in this Agreement to the contrary, (i) [***] Supported Aircraft, at any time that there are fewer than [***] CAATS, or (ii) [***] Supported Aircraft, at any time there are [***] or more CAATS, will not be scheduled for Scheduled Flights, but will instead be spare aircraft to be used as substitutes when necessary or required for any other Covered Aircraft (“Spare Aircraft”). The specific identity of Supported Aircraft designated at any time as Spare Aircraft shall be within the sole control of Contractor. For clarity, Spare Aircraft are Covered Aircraft and Supported Aircraft for all purposes of this Agreement. The Spare Aircraft shall also be available at American’s written request, subject to Contractor’s Consent (which shall not be unreasonably withheld) and the terms and conditions of this Agreement, to operate any flight as designated by American on behalf of American or any of its Affiliates, and in such case (x) Contractor shall receive compensation for [***] for each such flight and (y) such flight shall count towards any calculation of Controllable On Time Departures and Controllable Completion Rate, in all cases, as if such flight were a Scheduled Flight; provided, however, that if American requests that Contractor utilize a Spare Aircraft to operate any flight as designated by American on behalf of American or any of its Affiliates, and a Scheduled Flight is delayed or cancelled as a direct result of the unavailability of such Spare Aircraft, then such delay or cancellation shall be deemed an Uncontrollable Delay or an Uncontrollable Cancellation, as applicable.

(d) Aircraft Substitution and Removal. Upon not less than [***] prior Notice to American, Contractor may, in its sole discretion, remove a Covered Aircraft from this Agreement and substitute such Covered Aircraft with another CRJ-200 aircraft in American livery and configuration. Schedule 1 shall be deemed amended to reflect the substitution on the effective date provided in such Notice. Such Notice of substitution shall identify by tail number both the Covered Aircraft being removed and the aircraft that will substitute-in for such Covered Aircraft (if any). Each such aircraft that is substituted-in shall be covered by Contractor’s FAA approved maintenance program and shall otherwise meet the requirements applicable to Covered Aircraft in this Agreement. Upon such substitution, the removed aircraft shall cease to be a Covered Aircraft under this Agreement, and any substituted-in aircraft shall be a Covered Aircraft for all purposes of this Agreement (which substituted-in aircraft will have the same Aircraft Term as the removed aircraft). [***]

(e) Neutral Livery Aircraft. Contractor shall have the right at any time, without American’s prior consent, to operate any Scheduled Flight with any CRJ-200 regional jet that (i) is not a Covered Aircraft, (ii) is in neutral livery or Contractor’s branded livery, (iii) is covered by Contractor’s FAA approved maintenance program and (iv) otherwise meets the requirements applicable to Covered Aircraft in this Agreement (each, a “Neutral Livery Aircraft”); provided that (A) Contractor must provide American with prior Notice of the tail numbers of any Neutral Livery Aircraft and (B) in no event shall more than [***] Neutral Livery Aircraft be used to operate Scheduled Flights in any [***] without American’s prior written consent. The Block Hour Rate, Departure Rate and any Pass Through Costs and American Absorbed Expenses attributable to Neutral Livery Aircraft provided by Contractor for Regional Airline Services will be payable by American with respect to each such Neutral Livery Aircraft. [***]

3.03 Aircraft Unavailability.

(a) Other Operator. American shall have the right and option at its sole discretion to cause an operator other than Contractor to operate a Scheduled Flight. If American determines that an operator other than Contractor will operate a Scheduled Flight, then it shall provide prior notice to Contractor thereof (but failure to provide such notice shall not prejudice or impact American’s rights under this Section 3.03(a), and American shall not have any liability for any failure to provide such notice).

5

(b) Compensation. If an operator other than Contractor operates a Scheduled Flight due to a Covered Aircraft not being available to operate such Scheduled Flight, then Contractor shall not receive the compensation from American in respect of Block Hours or departures for such Scheduled Flight. If an operator other than Contractor operates a Scheduled Flight and a Supported Aircraft was available to operate such Scheduled Flight, then Contractor shall receive all of the compensation from American for such Scheduled Flight it would have received as if it had operated such Scheduled Flight (including, but not limited to Block Hours and departures), and for purposes of calculating the performance metrics set forth in Schedule 5, such Scheduled Flight shall be deemed to have departed and been completed on time.

(c) Controllable On Time Departures and/or Controllable Completion Rate. If a Covered Aircraft is not available to operate a Scheduled Flight, and American is able to locate an operator other than Contractor to operate such flight, and that flight is canceled or delayed, then that flight shall count as a “Scheduled Flight” for purposes of any calculation of Controllable On Time Departures and/or Controllable Completion Rate as if such flight was provided by Contractor. For the avoidance of doubt, if that flight is not canceled or delayed, then it shall not count towards the calculation of Controllable On Time Departures and/or Controllable Completion Rate.

3.04 Supportability Commitment.

(a) Contractor Commitment. Except as otherwise Consented to by American in its sole discretion, Contractor shall not operate aircraft in FAR Part 121 passenger operations for another carrier unless and until the Implementation Date for the [***] Covered Aircraft has occurred (the “Commitment Threshold”), provided that the foregoing will apply only during the period beginning as of the end of the Transition Period and ending upon the date of the first Notice of termination pursuant to Article XII; provided further that if American Withdraws a Covered Aircraft pursuant to this Agreement (other than pursuant to Section 12.02(c)(ii)), then the Commitment Threshold shall be decreased by one for each Withdrawn aircraft as of the date of Withdrawal.

(b) Contractor Code Flight Restrictions. Notwithstanding anything herein to the contrary, and except as otherwise Consented to by American in its sole discretion, during the Term, Contractor shall not operate any FAR Part 121 passenger flights under its own flight designator code into or out of any Hub.

3.05 Flight Designator Codes and Codeshare Term.

(a) All Scheduled Flights shall be operated under the name “American Eagle” or such other name, incorporating an Approved Mark, as may be determined by American in its sole discretion and specified by American to Contractor, from time to time.

(b) All Scheduled Flights shall be identified by an “AA*” flight designator code (or such other flight designator codes as may be assigned by American in its sole discretion), as appropriate, in: (i) American, Contractor, and Third Party computer reservations systems, including Internet reservation systems; (ii) American timetables; (iii) airport flight information displays; and (iv) passenger tickets and like media distributed to or accessed by travel agents, other airlines or the public (all Scheduled Flights that display the “AA*” flight designator code or such other flight designator codes as may be assigned by American from time to time in its sole discretion are referred to herein as “AA Flights”).

6

(c) To the extent Contractor subsequently discloses or identifies the AA Flights to the public as flights operated by Contractor, Contractor shall do so only in the following ways: (i) a symbol and/or text may be used in timetables and computer reservation systems indicating that AA Flights are operated by Contractor; (ii) to the extent reasonable and necessary, messages on airport flight information displays may identify Contractor as the operator of flights shown as AA Flights; and (iii) in any other manner prescribed and/or required by any laws, rules or regulations of a Governmental Authority.

(d) In all cases, the conditions of carriage with regard to passengers on AA Flights will be between a passenger and American.

(e) Contractor agrees to operate all Scheduled Flights using the American flight designator code and flight numbers assigned by American, or such other flight designator codes and flight numbers as may be assigned by American (to accommodate, for example, an American codeshare partner). American shall have the exclusive right to determine which other airlines (“Codeshare Airlines”), if any, may place their two-letter designator codes on flights operated by Contractor with Covered Aircraft and to enter into agreements with such Codeshare Airlines with respect thereto. Contractor will cooperate with American and any Codeshare Airlines, as reasonably requested by American and at American’s expense, with respect thereto (including, without limitation, making necessary governmental filings and entering into reasonably acceptable agreements with such Codeshare Airlines).

3.06 Flight Dispatch. Contractor shall be solely responsible for, and American shall have no obligations or duties with respect to, the Dispatch of Scheduled Flights, any charter flights pursuant to Section 3.01(c), or any Maintenance/Ferry Flights; provided that Contractor shall coordinate such Dispatch for Scheduled Flights and charter flights hereunder with American’s systems operation control and pursuant to Schedule 2. Contractor shall provide information to American that American may reasonably request from time to time regarding Scheduled Flights, including any changes in scheduling of a Scheduled Flight, Dispatch entries, and data for textual flight plans.

3.07 Maintenance of Supported Aircraft.

(a) Generally. Contractor shall cause the Supported Aircraft to be maintained, inspected, serviced, repaired, overhauled and tested: (i) in accordance with this Agreement and Contractor’s FAA-approved Part 121 maintenance program, and (ii) so as to keep the Supported Aircraft (A) in full conformity with all manufacturers’ manuals, instructions, AD mandatory service bulletins, technical data and recommendations and in airworthy condition under FAA and customary industry practice, (B) in such condition as may be necessary to enable the FAA airworthiness certificate of the Supported Aircraft to be issued and, at all times, maintained in good standing, and (C) in such condition as may be necessary to enable Contractor to provide the flights as contemplated by this Agreement. Without limiting the generality of this Section 3.07(a), Contractor shall ensure the Supported Aircraft, each engine installed thereon and all parts at any time used in connection therewith shall at all times be duly certified as being airworthy in accordance with applicable law. All material modifications requested by American in accordance with this Agreement or required by an applicable Governmental Authority (other than Heavy Maintenance) shall be coordinated as may be agreed to by the Parties.

7

(b) Line Maintenance. All Line Maintenance on the Supported Aircraft shall, to the extent reasonably practicable, be performed at a maintenance facility or station in a location that is reasonably acceptable to American from time to time during the Term hereof; it being understood that the initial designations for such maintenance facilities and stations shall be as set forth on Schedule 2.

(c) Heavy Maintenance. On or prior to each [***] during the Term, Contractor shall deliver to American a forecast stating (i) the approximate date that each such Covered Aircraft is to be removed for Heavy Maintenance during the upcoming [***] period, and (ii) the number of Covered Aircraft that Contractor will maintain throughout such [***] period. Contractor shall provide American with prompt Notice of any changes to such schedule. In addition to the annual Notice described above in this Section 3.07(c), Contractor shall also deliver Notice to American (A) at least [***] prior to any Supported Aircraft needing to be removed from providing Scheduled Flights for purposes of accomplishing scheduled Heavy Maintenance and Notify American of any changes to such schedule; and (B) no later than [***] following request from American, detailed reports regarding scheduled and completed maintenance operations(including Heavy Maintenance) of any Covered Aircraft. Pursuant to Section 3.02(d), Contractor will have the right to substitute out any aircraft that is not available due to Heavy Maintenance and American shall not include in the Final Schedule any aircraft that is not available due to Heavy Maintenance.

(d) Painting Covered Aircraft. Contractor shall repaint each Covered Aircraft (A) no later than [***] following its Implementation Date, and (B) from time to time as reasonably requested by American in order to maintain an acceptable exterior appearance or repair damage to the exterior of a Covered Aircraft. Any such repainting request by American shall include American’s required support and changes to the operating schedule to permit Contractor to remove such Covered Aircraft from service to accommodate such repainting. Painting of any Covered Aircraft must be approved in advance by American, which approval shall not be unreasonably withheld.

(e) Cabin Maintenance and Exterior Cleaning. Without limiting the requirements set forth in Section 4.03(e), with respect to interior cabin maintenance and exterior cleaning of the Supported Aircraft, Contractor shall, [***], comply with the following standards and replacement schedule:

(i) An extensive interior cleaning shall take place every [***];

(ii) Carpets shall be cleaned every [***] and shall be removed and replaced as needed in conjunction with every Heavy Maintenance check;

(iii) Seat coverings shall be conditioned every [***] in conjunction with every other extensive interior cleaning and inspected and replaced as needed in conjunction with every Heavy Maintenance check;

(iv) Seat bottom cushions shall be replaced at least every [***] and back cushions for seats shall be replaced as needed in conjunction with Heavy Maintenance checks;

(v) The galley and lavatory floor laminate shall be [***];

(vi) The exterior shall be dry washed every [***], provided that the APU exhaust will be washed [***]; and

8

(vii) The exterior of the engines and the wings shall be dry washed [***].

(f) In connection with any improvements or modifications to any Covered Aircraft required by an airworthiness directive, Contractor (taken together with its Affiliates) shall not discriminate against such Covered Aircraft with regard to efforts to satisfy the requirements of such airworthiness directives, including the method and date of compliance, and shall satisfy all such requirements, including by using or applying any efforts used or applied by Contractor or its Affiliates with regard to any other aircraft owned or operated by Contractor or any of its Affiliates. In connection with any grounding order which relates to any of the Covered Aircraft, Contractor shall not discriminate against such Covered Aircraft with regard to efforts to satisfy the applicable requirements to lift such grounding order, including using or applying any efforts used or applied by Contractor or its Affiliates with regard to other aircraft owned or operated by Contractor or its Affiliates, and shall satisfy such requirements.

3.08 Compliance with Other Terms of Related Agreements. Upon execution, each Related Agreement will be automatically incorporated into this Agreement. In the event of a conflict between the provisions of a Related Agreement and any provisions of this Agreement, the provisions of this Agreement will prevail, unless otherwise expressly set forth in the applicable Related Agreement.

3.09 Event of Loss. If an Event of Loss has occurred with respect to any Covered Aircraft, then (a) Contractor shall Notify American of such Event of Loss, (b) such Covered Aircraft shall no longer be a Covered Aircraft under this Agreement effective as of the date such Event of Loss occurs, (c) Contractor shall have the right to substitute another aircraft for such Covered Aircraft, as provided in Section 3.02(d), and (d) American shall have no obligation to pay any amounts to Contractor related to such Covered Aircraft to the extent otherwise subject to payment or reimbursement as set forth herein unless such amounts accrued hereunder before such Event of Loss. Contractor shall, upon request from American, promptly provide all additional documentation reasonably requested by American with respect to such Event of Loss.

ARTICLE IV.

SERVICE STANDARDS, PERFORMANCE MEASUREMENT AND TRAINING

4.01 Crews and Other Personnel. Contractor shall provide all crews (flight and cabin) and maintenance personnel necessary to operate all Scheduled Flights and for all aspects (personnel and other) of Dispatch and operational control of such flights; provided, however, that Contractor’s inability to provide crew for any Scheduled Flight resulting in Unsupported Aircraft shall not in and of itself constitute a breach of this Agreement or any Related Agreement, and American’s exclusive remedies for Unsupported Aircraft shall be pursuant to Section 6.15(a) and 12.02(c)(ii).

4.02 Governmental Regulations. Contractor has and shall maintain at all times all FAA, DOT, TSA and other certifications, permits, licenses (including licenses to sell or dispense beer, wine, liquor or any other alcoholic beverages), certificates, exemptions, approvals and plans required by Governmental Authorities necessary to enable Contractor to provide Regional Airline Services, along with any insurance required pursuant to the terms hereof, to maintain the airworthiness of the Supported Aircraft and to operate the Supported Aircraft. All Regional Airline Services and all other operations and services undertaken by Contractor pursuant to this Agreement shall be conducted, operated and provided by Contractor in compliance with all laws, rules, requirements and regulations of all applicable Governmental Authorities, including those relating to airport security, the use and transportation of Hazardous Materials and dangerous goods, environmental rules and regulations, crew qualifications, crew training and crew hours, and the carriage of persons with disabilities. To the extent American subsequently elects or is required to include the Supported Aircraft in an EAS Program, Contractor agrees to assist American [***] in its compliance with the program. Without limiting Section 3.07(a), all Covered Aircraft shall be operated and maintained by Contractor in compliance with all laws, regulations and governmental requirements, Contractor’s own operations manuals and maintenance manuals and procedures, and all applicable equipment manufacturers’ manuals and instructions.

9

4.03 Quality of Service.

(a) Procedures and Performance Standards. Without limiting this Section 4.03(a) or Section 4.07, at all times, Contractor shall provide Regional Airline Services to American in accordance with the written procedures and performance standards relating to customer experience approved by American and applicable to [***] (collectively, “Other Regional Carriers”) from time to time in its sole discretion and provided to Contractor, including but not limited to those certain Standards of Service set forth on Exhibit B hereto [***]. The Standards of Service set forth on Exhibit B hereto may be amended or changed by American from time to time upon [***] prior Notice to Contractor; provided, however that (i) [***] and (ii) no advance Notice to Contractor of a change is required for American to modify the in-flight service sample on Schedule 1 to Exhibit B or the cabin condition sample on Schedule 2 to Exhibit B each of which may be modified at any time by American in its sole discretion. Contractor shall be responsible for all crew and other employee conduct, appearance and training policies (as set forth on Exhibit C), aircraft cleaning (including the timing thereof so long as the standards are met), standards and adequate staffing levels in order to comply in all material respects with such procedures and meet such standards, including without limitation in respect of customer complaint response (subject to Section 4.06) and any handling of irregular operations, all of which shall be handled in a professional, businesslike and courteous manner. Without limiting Section 3.07 or Section 4.03(a), Contractor shall cause its crews to conduct routine clean up and straightening of Covered Aircraft between Scheduled Flights.

(b) Contractor’s Representative Uniforms. Contractor shall require all of its respective personnel and any of its respective Contractor Agents providing Regional Airline Services in job classifications requiring direct public contact to wear uniforms and accessories furnished by Contractor that are of colors and styles approved by American from time to time. Contractor shall not alter or change such uniforms and accessories without the prior written Consent of American. If, after the Effective Date, American determines, in its sole discretion, that such uniforms and accessories should be materially altered or changed, then American shall provide Contractor with Notice of such alterations or changes. In the event that American decides to implement such alterations or changes, Contractor shall implement such alterations or changes.

(c) In Flight Services. Contractor shall comply with the catering requirements set forth on Exhibit B hereto. Contractor shall also coordinate all in-flight services relating to the Regional Airline Services with the in-flight services department of American or any Person designated by American to ensure consistency and quality of Contractor’s in-flight service, including non-safety related functions such as in-flight marketing announcements, meal and beverage presentation and delivery, and provisioning and usage of passenger amenity kits. Contractor shall sell beer, wine, liquor and any other alcoholic beverages on Scheduled Flights. Contractor agrees that such in-flight sales shall be conducted as directed by American from time to time. Contractor shall implement any suggestions made by American’s in-flight services department. All in-flight services on the Covered Aircraft shall be provided on a cashless basis on devices provided by American. Contractor must provide Notice to American of any threatened catering related fines or penalties that could result in a liability to American in accordance with Section IV of Schedule 3 within [***] after receipt of such notification and allow for the involvement of American in the resolution process of such issue so that both Parties can work to minimize any fines to American.

10

(d) Communication of Scheduled Flight Information. Contractor shall provide as promptly as possible to American through ACARS, accurate and timely updates of planned and Actual Departure and arrival times of Scheduled Flights (including updates of irregularities), any changes in scheduling of a Scheduled Flight, Dispatch entries, data for textual flight plans, FOQA data (excluding any FOQA data that is not directly or indirectly related to fuel usage on Covered Aircraft), data for textual flight plans, and all other information related thereto as may be requested by American from time to time and as specified by American from time to time; provided that with respect to any FOQA data, the foregoing requirements will not apply to the extent such delivery of FOQA data to American is restricted by any of Contractor’s collective bargaining agreements.

(e) Aircraft Livery; Refurbishment and Design Costs.

(i) Cabin Condition as of Implementation Date. Contractor shall cause the interior and cabin condition of each Covered Aircraft to comply with the Interior Design requirements set forth on Schedule 12 and be in a condition that would result in a passing score for a Cabin Condition Compliance Check (as determined by American in accordance with Schedule 2 to Exhibit B). At least [***] prior to the Implementation Date for a Covered Aircraft, Contractor shall permit American to inspect such Covered Aircraft’s interior. If such Covered Aircraft’s interior does not meet the Interior Design requirements set forth on Schedule 12 or is not in a condition that would result in a passing score for a Cabin Condition Compliance Check, then American shall Notify Contractor of the applicable deficiencies and Contractor shall correct such deficiencies prior to such Covered Aircraft’s Implementation Date (and if such deficiencies are not corrected on or prior to such date, then such aircraft shall not become a Covered Aircraft until American provides its approval). Any cost and expense related to preparing or correcting each Covered Aircraft’s interior and cabin condition to meet American’s approval pursuant to this Section 4.03(e)(i) shall be [***].

(ii) Interior Design.

(A) Interior Design Generally. At all times during the Term, all Covered Aircraft (including Spare Aircraft) shall satisfy the Interior Design requirements set forth on Schedule 12 including the layout for passenger accommodation set forth therein (as such Schedule 12 may be subsequently modified by American in its sole discretion upon Notice to Contractor, in which case Schedule 12 shall automatically be deemed to be amended, modified and restated to reflect such modifications); provided that the initial Interior Design and branding requirements shall be mutually agreed upon by the Parties and included on Schedule 12 at least [***] prior to the Implementation Date for the first Covered Aircraft. Without the prior Consent of American (such Consent not to be unreasonably withheld), Contractor may not materially alter the Interior Design of the Covered Aircraft.

(B) Changes to Interior Design and Branding. If American determines that the interior design or branding of a Covered Aircraft should be altered or changed, then American shall provide Contractor with Notice of such alteration or change and within [***] following such Notice, Contractor shall provide American with a [***] estimate of the out-of-pocket costs and expenses to Contractor attributable to such alteration or change, so that American may determine whether to implement such alteration or change. In the event that American determines that it shall implement such alteration or change, it shall

11

provide Notice thereof to Contractor and Contractor shall use commercially reasonable efforts to implement such alteration or change by no later than [***] following such Notice, unless a longer time period is Consented to by American (acting reasonably under the circumstances) and such reasonable and documented out-of-pocket costs and expenses [***] (and to the extent actually incurred by Contractor) shall be [***].

(iii) Exterior Livery. Contractor shall maintain all Covered Aircraft in an exterior livery Consented to by American as provided below.

(A) Exterior Livery On Implementation Date. Contractor will have the right to implement any Covered Aircraft in neutral livery; provided that, by no later than the conclusion of the [***] period following the Implementation Date for a Covered Aircraft, Contractor shall cause the exterior livery of such Covered Aircraft to be painted in the colors and design approved by American. Contractor shall provide American with a [***] estimate of the out-of-pocket costs and expenses to Contractor attributable to such exterior livery painting. Such reasonable and documented out-of-pocket costs and expenses in an amount that [***].

(B) Exterior Livery Changes After Implementation Date. If, after the Implementation Date for a Covered Aircraft, American determines that the exterior livery of such Covered Aircraft should be altered or changed in any material respect, then American shall provide Contractor with Notice of such alterations or changes and within at least [***] following such Notice, Contractor shall provide American with a [***] estimate of the out-of-pocket costs and expenses to Contractor attributable to such alterations or changes, so that American may determine whether to implement such alterations or changes. In the event that American determines that it shall implement such alterations or changes, it shall provide Notice thereof to Contractor and Contractor shall implement such alterations or changes no later than [***] following the delivery of such Notice, and such reasonable and documented out-of-pocket costs and expenses in an amount that [***].

4.04 Access and Use of American Systems.

(a) Systems Access. American may provide Contractor with access to American Systems as determined by American to be necessary or appropriate for Contractor to provide the Regional Airline Services.

(b) Use of Systems. Contractor shall maintain connections to any American Systems provided to Contractor by American, and will be responsible for using any other systems, including ACARS and FOQA, that are necessary or appropriate for Contractor to provide Regional Airline Services. Neither Contractor nor Contractor Agents shall access or use any American System for any purpose other than to provide Regional Airline Services.

(c) Systems Support. Contractor shall be responsible for the maintenance and performance of any connections that Contractor uses to access or interface with the American Systems (for clarity, Contractor is not otherwise responsible for the performance or costs of American Systems). Additionally, American may require Contractor to install and operate certain support programs on Contractor’s equipment that American requires for American’s internal reporting systems. The costs and expenses incurred by Contractor in connection with its use of American Systems under this Section 4.04(c) will be [***] as set forth in Section I(O) of Schedule 3.

12

(d) IT Access to Operational Data. During the Term, Contractor shall provide all core operational integration data that is available for collection by Contractor as reasonably requested by American, including real-time flight movement, flight release updates and fuel slips, Contractor Employee Data for purpose of provisioning user accounts and providing flight privileges, crew movement deadhead booking requirements, weight and balance system integration for paperless closeout, and unscheduled daily aircraft out of service and Minimum Equipment List data with respect to customer-facing issues. In addition, by no later than the Implementation Date for the [***] Covered Aircraft, except to the extent such provision is restricted by any of Contractor’s collective bargaining agreements, Contractor shall use commercially reasonable efforts to provide all operational and analytics data reasonably requested by American to be used for American’s decision support tools, including but not limited to IOC Tools such as “HEAT,” “Crew Recovery” and “Diversion Planner,” crew scheduling data, including operating crew details per flight, crew duty periods and legalities, and any IROPS requirements that American utilizes to provides solutions to cancels and/or recovery of the operation.

4.05 Data Security.

(a) Safeguards. Where Contractor stores or Processes American Data, Contractor shall and shall cause its Contractor Agents to establish and maintain a secure environment for all American Data and any hardware and software (including servers, network and data components) to be provided or used by Contractor or its Contractor Agents to store or Process American Data. Contractor represents, warrants and covenants that the security measures it takes in performance of its obligations under this Agreement are, and will at all times remain, consistent with the following (collectively referred to herein as “Security Best Practices”): (i) the security requirements, obligations, specifications and event reporting procedures set forth on Exhibit D, including, without limitation, the Security Requirements, and (ii) any security requirements, obligations, specifications and/or event reporting procedures required by American in writing from time to time. Failure by Contractor to comply with Security Best Practices in fulfilling its obligations hereunder shall constitute a breach of this Agreement. Contractor shall contractually require any Contractor Agent with access to American Data to adhere to such Security Best Practices as applicable to their access to the American Data.

(b) Notice of Breach. If Contractor or any Contractor Agent discovers or is notified of a breach or potential breach of security relating to the American Data, then Contractor shall immediately (i) provide Notice to American of such breach or potential breach, and (ii) if the applicable American Data was in the possession of Contractor or any Contractor Agent at the time of such breach or potential breach, Contractor (A) shall investigate and remediate with American’s assistance the effects of the breach or potential breach (such remediation to include restoring data to the last data back-up), and (B) shall provide American with assurance satisfactory to American that the likelihood of a recurrence of such breach or potential breach has been appropriately reduced.

13

(c) Disaster Recovery.

(i) Contractor shall maintain a disaster recovery plan designed to (A) continue all Contractor business operations that are critical to the operation and functionality of, and American’s and authorized users’ access to, the Application, and (B) permit Contractor to comply with this Agreement, in each case, notwithstanding a Crisis (a “Disaster Recovery Plan”). Contractor shall at least [***] per calendar year review, test and modify its Disaster Recovery Plan to ensure it is consistent with the guidelines and standards of the airline industry as such guidelines and standards evolve. Contractor shall provide American with the results of tests Contractor conducts on its Disaster Recovery Plan within [***] of such tests.

(ii) Contractor shall, as part of its Disaster Recovery Plan, host and operate the Application (“Backup Facility”) that (A) is at a hardened data center facility in the U.S. that is geographically remote from its Primary Facility, (B) other than location, is otherwise identical in all respects to the Primary Facility, (C) has hardware, software, network connectivity, power supplies, backup generators, and other similar equipment and services that operate independently of the Primary Facility, (D) has fully current backups of all American Data stored at the Primary Facility, and (E) has the ability to provide access to the version of the Application currently in use at the Primary Facility in accordance with this Agreement during a Crisis. Contractor shall provide a recovery time objective and recovery point objective of no more than [***] immediately following such Crisis, and at all times thereafter, American’s access to the Application will be uninterrupted.

(iii) In the event of a Crisis, Contractor shall promptly implement its Disaster Recovery Plan. The occurrence of a Crisis does not relieve Contractor of its obligation to implement its Disaster Recovery Plan.

(iv) Contractor agrees that American has the right to have a third party audit or access to a third party audit of Contractor’s Disaster Recovery Plan and testing results. If there is a deficiency or material weakness revealed in the audit findings in any IT security audit undertaken by or on behalf of American hereunder or if Contractor otherwise fails to demonstrate successful Disaster Recovery testing and Contractor fails to cure any such deficiency, weakness or non-compliance within [***] following the date of Notice thereof from American and American reasonably determines that such deficiency, weakness or non-compliance could have a negative impact on American, then Contractor shall [***] continuing until the date such deficiency, weakness or non-compliance is cured in all material respects.

4.06 Processing and Adjudicating Customer or Passenger Complaints. Subject to Contractor’s rights under Section 11.03(a) and Section 11.03(a)(i) with respect to claims subject to Contractor’s indemnification obligations under Section 11.01, (a) American shall process and adjudicate all customer or passenger complaints related to this Agreement and the Regional Airline Services and Contractor shall provide reasonable assistance to American in processing and adjudicating such customer or passenger complaints in such manner as American may reasonably determine; (b) to the extent information regarding the complaint is not requested by American, Contractor may provide information regarding such complaint, but American is under no obligation to consider such information in American’s processing, adjudicating, disposition or handling of such complaint; and (c) American shall have complete and exclusive control of the method of processing and adjudicating such customer or passenger complaints and any final disposition or handling of any customer or passenger complaint shall be in American’s sole discretion and, without limiting American’s rights under Section 11.01 [***]. For clarity, to the extent that any customer or passenger complaint arises out of a circumstance for which Contractor is required to indemnify American pursuant to Section 11.01, the terms and conditions set forth in Section 11.03(a) and Section 11.03(a)(i) will apply. Contractor shall promptly notify American’s customer service department of any customer service complaints related to the Regional Airline Services that are directly received by Contractor.

14

4.07 Right to Inspect Aircraft and Service Conditions.

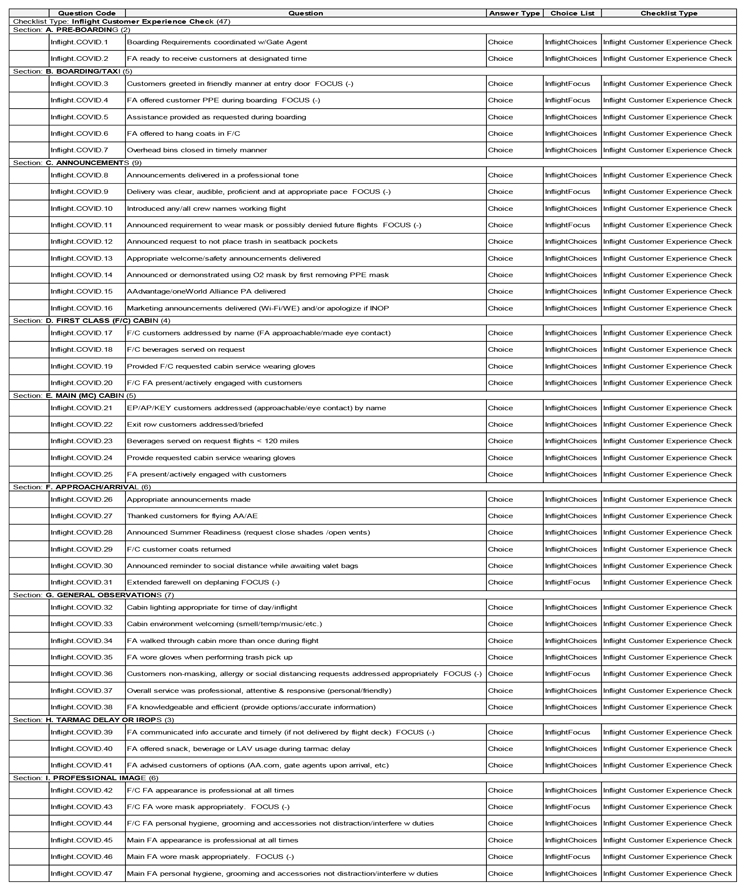

(a) Checks. Without limiting Section 4.03(a) and the rights set forth on Schedule 7, American shall have the right and option, in its sole discretion from time to time, to perform quality checks on Contractor’s in-flight service performance for Scheduled Flights (each such check an “Inflight Customer Experience Check”) and the condition of the cabin of the Covered Aircraft (each such check a “Cabin Condition Compliance Check”) to ensure the service performance of such Covered Aircraft meet the Standards of Service and the aircraft condition standards and actions as required in Section 4.03, Exhibit B and elsewhere in this Agreement, and such other service and condition standards that may be developed by American from time to time in its sole discretion in accordance with this Agreement [***]. In performing an Inflight Customer Experience Check or Cabin Condition Compliance Check, American shall use the in-flight service sample described on Schedule 1 to Exhibit B, and the cabin condition sample described on Schedule 2 to Exhibit B, respectively; [***]. The conditions giving rise to an unsatisfactory score for any Inflight Customer Experience Check or a failing score for any Cabin Condition Compliance Check shall be as stated on Schedules 1 and 2 to Exhibit B, respectively.

(b) Unsatisfactory Inflight Customer Experience Check. If there is an unsatisfactory score (as determined by American in accordance with Schedule 1 to Exhibit B) for an Inflight Customer Experience Check, then Contractor shall pay to American [***] for each unsatisfactory score in accordance with Section IV of Schedule 7. Such amount shall be taken into account for purposes of the next applicable reconciliation of amounts due to American pursuant to Section III of Schedule 5.

(c) Cabin Condition Compliance Check Failure. If there is a failing score (as determined by American in accordance with Schedule 2 to Exhibit B) for a Cabin Condition Compliance Check, then American shall provide prompt Notice of such failure to Contractor. No sooner than [***] after Contractor’s receipt of such Notice, American may conduct a second Cabin Condition Compliance Check on the same Covered Aircraft that resulted in the failing score. If the second Cabin Condition Compliance Check also results in a failing score, Contractor shall pay to American [***] (in accordance with the wiring instructions set forth in Section IV of Schedule 7) until such time as Contractor is able to demonstrate to American’s satisfaction that it has remedied all conditions giving rise to such failing scores. Such amount shall be taken into account for purposes of the next applicable reconciliation of amounts due to American pursuant to Section III of Schedule 5.

(d) Intentionally Omitted.

(e) Remedies Cumulative. It is further agreed and understood between the Parties, that American’s rights and remedies as provided in this Section 4.07 shall not impair and shall not be deemed to limit, amend, modify or supplant any other rights or remedies American shall have hereunder or under applicable law, including, but not limited to, American’s rights and remedies as provided in Section 4.03, any of the other subsections of this Section 4.07 and Section 12.02 hereof (including, without limitation, rights and remedies available upon the occurrence of a Material Breach) and Exhibit B attached hereto. In no event shall American be required to elect between available remedies with respect to any Inflight Customer Experience Check or Cabin Condition Compliance Check; it being understood that American shall have the right to have all of the remedies related thereto be cumulative and non-exclusive.

15

4.08 Controllable Cancellation Codes and Controllable On Time Departure Codes.

(a) Change to Codes. In the event the codes set forth in American’s Delay Code Handbook and/or Cancel Code Handbook (or any successor handbooks thereto) are amended, restated or modified in any way, or American determines that any code set forth therein shall be deemed a Controllable On Time Departure code or Uncontrollable Cancellation code, then such amendment, restatement, modification or determination (each a “Code Change”) shall automatically be deemed to amend, modify or restate the applicable codes set forth on Schedule 8 (Controllable Cancellation Codes) and Schedule 9 (Controllable On Time Departure Codes) without any action by American or Contractor; it being understood that American shall promptly provide Notice to Contractor of any such Code Change.

(b) Change to Controllable On Time Departures or Controllable Completion Rate. If a Code Change occurs, then the Parties shall meet to discuss and agree upon any relevant adjustments to the Controllable Completion Rate Bonus Threshold, Controllable Completion Rate Service Level Threshold, Controllable On Time Departure Bonus Threshold, Controllable On Time Departures Service Level Threshold and the termination thresholds set forth in Section 12.02(c)(i) in order to maintain the status quo with respect to Contractor’s ability to achieve the applicable threshold following such Code Change; provided that if no mutual agreement is reached between the Parties within [***] of such Code Change, then American will have the right, acting reasonably and in good faith, to make reasonable adjustments to the foregoing thresholds as a result of such Code Change. Any such adjustment shall take effect as of the [***] following delivery of a Notice from American to Contractor thereof, and Schedule 5 of this Agreement shall automatically be deemed to be amended to reflect the Parties’ agreement. For the avoidance of doubt, any adjustments to the foregoing thresholds as a result of a Code Change will be implemented on a forward-looking basis, and no retroactive adjustments will be made with respect to Bonuses or Rebates related thereto that were assessed prior to such Code Change.

(c) Data for Performance Measurements. American shall use American’s own data when determining Contractor’s performance under this Agreement, including Likelihood to Recommend Factor, Controllable On Time Departures and Controllable Completion Rate and shall not discriminate against Contractor with respect to any such determination as compared to any Other Regional Carrier. Upon Contractor’s reasonable request, American shall provide to Contractor reasonably detailed supporting information used by American to determine Contractor’s Likelihood to Recommend Factor, Controllable On Time Departures and Controllable Completion Rate performance under this Agreement (to the extent that American is not restricted from providing such information due to confidentiality and related obligations) and Contractor reserves the right to dispute American’s determination.

4.09 Catering Products and Catering Services. American shall provide, or arrange for another Person to provide, all Catering Products and Catering Services for Scheduled Flights of Covered Aircraft (excluding any Maintenance/Ferry Flights).

ARTICLE V.

SAFETY

5.01 Incidents or Accidents. Contractor shall promptly notify American’s System Operations Control/Flight Dispatch Office of any Accident or Incident that could reasonably be expected to result in a complaint or claim by passengers or an investigation by a Governmental Authority involving any Covered Aircraft occurring during Contractor’s provision of Regional Airline Services, including those that result in any injury or death to persons or damage to property. To the extent Contractor is involved in any such Accident or Incident, it shall furnish in writing to American detail concerning the same and shall cooperate with American [***] in any appropriate internal or external investigation. Contractor shall provide

16

American with notification of any security breach (regardless of level). Contractor shall maintain an emergency response plan in accordance with the applicable provisions of the Aviation Disaster Family Assistance Act of 1996 and any amendments or regulations relating thereto. Contractor shall promptly inform American in writing of any material modifications to such plan. American shall manage the customer response efforts on behalf of Contractor in the case of an Accident or Incident involving Regional Airline Services or the Covered Aircraft, including responding to an Accident or Incident and providing necessary assistance and services to the family members of passengers and Contractor shall fully cooperate in such efforts [***]. Prior to the Implementation Date of the first Covered Aircraft hereunder, Contractor and American shall enter into an Emergency Assistance Agreement as mutually agreed upon by the Parties (the “Emergency Assistance Agreement”).

5.02 Accident Reports. Contractor shall promptly furnish to American a copy of every written report and plan that Contractor prepares, whether such report is filed with the FAA, NTSB or any other Governmental Authority, relating to any Accident or Incident involving any Covered Aircraft or Regional Airline Services when such Accident or Incident is claimed to have resulted in the death or injury to any person or the loss of, damage to or destruction of any property. Contractor shall also provide prompt Notice to American of all irregularities involving any Scheduled Flights (including, without limitation, irregularities that result in any injury to or death of persons or material damage to property, but excluding common issues such as weather events) as soon as such information is available and shall furnish to American in writing detail regarding such irregularity. Each Party shall [***] to maintain communications with systems related to Accident and Incident reporting related to the Regional Airline Services.

5.03 International Air Transport Association Operational Safety Audit. Without limiting any other provisions of this Agreement, Contractor shall comply with the safety standards set forth by the International Air Transport Association Operational Safety Audit, and upon Notice from American from time to time, Contractor agrees to provide American with evidence in a form reasonably satisfactory to American of such compliance.

5.04 Emergency Assistance Agreement. The foregoing provisions of this Article V shall in no way be deemed to limit, restrict or amend any of the obligations of Contractor pursuant to the Emergency Assistance Agreement.

ARTICLE VI.

OTHER OBLIGATIONS OF CONTRACTOR

6.01 FAA or DOT Certification Suspension or Revocation. If Contractor discovers or is notified of the suspension or revocation, or potential suspension or revocation, of an FAA or DOT certification used in connection with the Scheduled Flights or Covered Aircraft, then Contractor shall immediately deliver Notice to American of such suspension or revocation.

6.02 Fuel Efficiency Program. Without limiting the obligations of Contractor pursuant to the terms hereof, Contractor shall promptly adopt and adhere to a “Fuel Efficiency Program” as described on Schedule 4, as such Schedule 4 may be subsequently amended in writing from time to time by American, as long as (i) Contractor’s adoption or adherence to such Fuel Efficiency Program does not materially and adversely impact the safety of Regional Airline Services under FAA operational specifications, or other regulatory constraints, or the airworthiness of the Covered Aircraft and (ii) [***]. American may also elect, upon [***] Notice to Contractor, to incorporate performance goals and rebates with respect to Contractor’s compliance with such Fuel Efficiency Program, so long as such goals and rebates apply generally to all other regional aircraft operators that provide passenger flight services for American (other than American’s wholly owned subsidiaries), and Contractor shall cooperate with American in good faith to implement and perform its obligations in accordance with such changes to the Fuel Efficiency Program.

17

6.03 Use of Approved Marks and Copyrights.

(a) Ownership of Marks. Contractor acknowledges and agrees that American, Parent and/or one of their respective Affiliates, as the case may be, is the sole worldwide owner or licensee of the Marks.

(b) License to Use Approved Marks. Subject to the terms and conditions of this Agreement, including service quality requirements set forth in Section 4.03, Contractor is hereby granted the [***] right and license to use the Approved Marks solely as specified by American from time to time and solely for Contractor to perform its obligations, including by operating the Regional Airline Services, as specified in this Agreement.

(c) Restrictions on Use. Contractor shall not use the Marks in any manner other than as permitted by this Agreement. Contractor shall only use the Approved Marks in a manner consistent with American’s quality standards, as they may exist from time to time, and shall not utilize the Marks in any manner that would diminish their value or harm the reputation of American, Parent or any of their respective Affiliates. All goodwill associated with Contractor’s use of the Approved Marks will inure solely to the benefit of the owner of such Marks. Upon termination of this Agreement, Contractor will immediately cease use of the Approved Marks, unless otherwise authorized in another agreement with American, Parent or one of their Affiliates. Under no circumstance will Contractor: (i) use or display any of the Marks that Contractor obtained from a source other than the American Airlines Brand Center Website; (ii) alter the Marks in any way; or (iii) transfer, sell, or give away to a Third Party any products bearing the Approved Marks that do not meet American’s quality standards. Contractor agrees that it shall in no way contest or deny the validity of, or the right or title of American, Parent and/or one of their Affiliates, as the case may be, in or to the Marks, and shall not encourage or assist others directly or indirectly to do so, whether during the Term or thereafter. Contractor shall not use or register any domain name that is identical to or similar to any of the Marks without first receiving American’s prior Consent. American may inspect Contractor’s use of the Approved Marks at any time to ensure Contractor’s use of such Approved Marks is consistent with this Agreement. Upon written request from American from time to time, Contractor agrees to provide American with reports setting forth Contractor’s use of the Approved Marks.

(d) Marking. For all uses of Approved Marks, Contractor and its respective Affiliates shall affix proper trademark or service mark notice: the symbol ® for registered trademarks or service marks, or the symbols ™ or SM for unregistered trademarks or service marks, and where requested by American, a statement that the Approved Mark “is a (registered, if applicable) trademark (or service mark, if applicable) of American Airlines, Inc. (or Parent or any of their Affiliates, if applicable) and is being used by Contractor under license from American Airlines, Inc. (or Parent or any of their Affiliates, if applicable).”

(e) Additional Approved Marks. Contractor has no right or permission to use any of the Marks, other than the Approved Marks, without first receiving American’s express Consent to do so. If Contractor receives American’s Consent to use any additional Marks, then such Marks will then be considered Approved Marks.

(f) New Marks. American has the right to amend the Approved Marks list at any time. If American removes a Mark from the Approved Mark list, Contractor must cease all use of the Mark within a time period to be determined in American’s sole discretion. Similarly, if American adopts a new Mark that it desires Contractor to use in connection with the performance and operation of Regional Airline Services, it will notify Contractor in writing and specify a deadline by which Contractor must incorporate and use the new Mark, and Contractor shall incorporate and use the new Mark by such deadline [***].

18

(g) Further Assurances. At American’s request, Contractor agrees to cooperate with American, Parent and their Affiliates in connection with applications and other filings to create, register, maintain, or otherwise perfect American’s, Parent’s and their Affiliates’ rights in Marks, at [***]. Upon termination of this Agreement, Contractor agrees to do everything necessary to effect cancellation of the recordation, if any, of Contractor as a recorded licensee of the Marks.

(h) License and Use of American’s Copyrights. American grants to Contractor a [***] right and license to reproduce, display, perform, distribute and prepare derivative works of American’s Copyrights solely as specified by American from time to time and solely in connection with the performance and operation of Regional Airline Services in accordance with this Agreement. Any reproductions shall include the notice “Reproduced with permission of American Airlines, Inc. © [date] American Airlines, Inc.” Contractor agrees it will not materially alter works subject to American’s Copyrights without American’s Consent. All derivative works of American’s Copyrights created by or for Contractor shall be the sole and exclusive property of American, and Contractor hereby assigns, and upon creation shall be deemed to have automatically assigned, all right, title and interest in and to such derivative works to American, including all copyright and other proprietary rights therein.