UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

/X/ QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended September 30, 2018

OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE

SECURITIES EXCHANGE ACT OF 1934

For the transition period from ______ to ______

Commission file number 1-11840

THE ALLSTATE CORPORATION

(Exact name of registrant as specified in its charter)

Delaware | 36-3871531 | |||

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||

2775 Sanders Road, Northbrook, Illinois | 60062 | ||

(Address of principal executive offices) | (Zip Code) | ||

(847) 402-5000

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes X | No ___ | ||

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files).

Yes X | No ___ | ||

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer | X | Accelerated filer | ____ |

Non-accelerated filer | Smaller reporting company | ____ | |

Emerging growth company | ____ | ||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ____

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes | No X | ||

As of October 15, 2018, the registrant had 344,442,270 common shares, $.01 par value, outstanding.

The Allstate Corporation

Index to Quarterly Report on Form 10-Q

September 30, 2018

Part I Financial Information | Page | |

Condensed Consolidated Statements of Operations for the Three Month and Nine Month Periods Ended September 30, 2018 and 2017 (unaudited) | ||

Condensed Consolidated Statements of Comprehensive Income for the Three Month and Nine Month Periods Ended September 30, 2018 and 2017 (unaudited) | ||

Condensed Consolidated Statements of Financial Position as of September 30, 2018 (unaudited) and December 31, 2017 | ||

Condensed Consolidated Statements of Shareholders’ Equity for the Nine Month Periods Ended September 30, 2018 and 2017 (unaudited) | ||

Condensed Consolidated Statements of Cash Flows for the Nine Month Periods Ended September 30, 2018 and 2017 (unaudited) | ||

Highlights | ||

Property-Liability Operations | ||

| ||

– Allstate brand | ||

– Esurance brand | ||

– Encompass brand | ||

Discontinued Lines and Coverages | ||

Service Businesses | ||

Allstate Life | ||

Allstate Benefits | ||

Allstate Annuities | ||

Part II Other Information | ||

Condensed Consolidated Financial Statements

Part I. Financial Information

Item 1. Financial Statements

The Allstate Corporation and Subsidiaries

Condensed Consolidated Statements of Operations

($ in millions, except per share data) | Three months ended September 30, | Nine months ended September 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | |||||||||||||

(unaudited) | (unaudited) | |||||||||||||||

Revenues | ||||||||||||||||

Property and casualty insurance premiums | $ | 8,595 | $ | 8,121 | $ | 25,341 | $ | 24,098 | ||||||||

Life premiums and contract charges | 612 | 593 | 1,840 | 1,777 | ||||||||||||

Other revenue | 238 | 228 | 682 | 664 | ||||||||||||

Net investment income | 844 | 843 | 2,454 | 2,488 | ||||||||||||

Realized capital gains and losses: | ||||||||||||||||

Total other-than-temporary impairment (“OTTI”) losses | (4 | ) | (26 | ) | (8 | ) | (135 | ) | ||||||||

OTTI losses reclassified (from) to other comprehensive income (“OCI”) | (1 | ) | (2 | ) | (2 | ) | (2 | ) | ||||||||

Net OTTI losses recognized in earnings | (5 | ) | (28 | ) | (10 | ) | (137 | ) | ||||||||

Sales and valuation changes on equity investments and derivatives | 181 | 131 | 27 | 455 | ||||||||||||

Total realized capital gains and losses | 176 | 103 | 17 | 318 | ||||||||||||

Total revenues | 10,465 | 9,888 | 30,334 | 29,345 | ||||||||||||

Costs and expenses | ||||||||||||||||

Property and casualty insurance claims and claims expense | 5,817 | 5,545 | 16,758 | 16,650 | ||||||||||||

Life contract benefits | 498 | 456 | 1,485 | 1,416 | ||||||||||||

Interest credited to contractholder funds | 163 | 174 | 489 | 522 | ||||||||||||

Amortization of deferred policy acquisition costs | 1,317 | 1,200 | 3,886 | 3,545 | ||||||||||||

Operating costs and expenses | 1,534 | 1,446 | 4,296 | 4,065 | ||||||||||||

Restructuring and related charges | 16 | 14 | 65 | 77 | ||||||||||||

Interest expense | 82 | 83 | 251 | 251 | ||||||||||||

Total costs and expenses | 9,427 | 8,918 | 27,230 | 26,526 | ||||||||||||

Gain on disposition of operations | 1 | 1 | 4 | 15 | ||||||||||||

Income from operations before income tax expense | 1,039 | 971 | 3,108 | 2,834 | ||||||||||||

Income tax expense | 169 | 305 | 587 | 894 | ||||||||||||

Net income | 870 | 666 | 2,521 | 1,940 | ||||||||||||

Preferred stock dividends | 37 | 29 | 105 | 87 | ||||||||||||

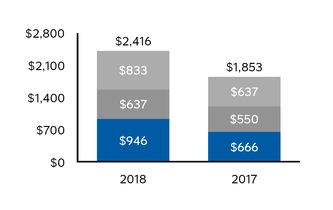

Net income applicable to common shareholders | $ | 833 | $ | 637 | $ | 2,416 | $ | 1,853 | ||||||||

Earnings per common share: | ||||||||||||||||

Net income applicable to common shareholders per common share - Basic | $ | 2.41 | $ | 1.76 | $ | 6.91 | $ | 5.10 | ||||||||

Weighted average common shares - Basic | 346.0 | 361.3 | 349.7 | 363.5 | ||||||||||||

Net income applicable to common shareholders per common share - Diluted | $ | 2.37 | $ | 1.74 | $ | 6.80 | $ | 5.02 | ||||||||

Weighted average common shares - Diluted | 351.7 | 367.1 | 355.4 | 369.1 | ||||||||||||

Cash dividends declared per common share | $ | 0.46 | $ | 0.37 | $ | 1.38 | $ | 1.11 | ||||||||

See notes to condensed consolidated financial statements.

Third Quarter 2018 Form 10-Q 1

Condensed Consolidated Financial Statements

The Allstate Corporation and Subsidiaries

Condensed Consolidated Statements of Comprehensive Income

($ in millions) | Three months ended September 30, | Nine months ended September 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | |||||||||||||

(unaudited) | (unaudited) | |||||||||||||||

Net income | $ | 870 | $ | 666 | $ | 2,521 | $ | 1,940 | ||||||||

Other comprehensive (loss) income, after-tax | ||||||||||||||||

Changes in: | ||||||||||||||||

Unrealized net capital gains and losses | (70 | ) | 125 | (768 | ) | 598 | ||||||||||

Unrealized foreign currency translation adjustments | (14 | ) | 28 | (25 | ) | 36 | ||||||||||

Unrecognized pension and other postretirement benefit cost | 68 | 73 | 113 | 110 | ||||||||||||

Other comprehensive (loss) income, after-tax | (16 | ) | 226 | (680 | ) | 744 | ||||||||||

Comprehensive income | $ | 854 | $ | 892 | $ | 1,841 | $ | 2,684 | ||||||||

See notes to condensed consolidated financial statements.

2  www.allstate.com

www.allstate.com

www.allstate.comCondensed Consolidated Financial Statements

The Allstate Corporation and Subsidiaries

Condensed Consolidated Statements of Financial Position

($ in millions, except par value data) | September 30, 2018 | December 31, 2017 | ||||||

Assets | (unaudited) | |||||||

Investments | ||||||||

Fixed income securities, at fair value (amortized cost $57,618 and $57,525) | $ | 57,663 | $ | 58,992 | ||||

Equity securities, at fair value (cost $5,741 and $5,461) | 6,965 | 6,621 | ||||||

Mortgage loans | 4,592 | 4,534 | ||||||

Limited partnership interests | 7,602 | 6,740 | ||||||

Short-term, at fair value (amortized cost $3,071 and $1,944) | 3,071 | 1,944 | ||||||

Other | 4,075 | 3,972 | ||||||

Total investments | 83,968 | 82,803 | ||||||

Cash | 460 | 617 | ||||||

Premium installment receivables, net | 6,196 | 5,786 | ||||||

Deferred policy acquisition costs | 4,667 | 4,191 | ||||||

Reinsurance recoverables, net | 8,994 | 8,921 | ||||||

Accrued investment income | 616 | 569 | ||||||

Property and equipment, net | 1,032 | 1,072 | ||||||

Goodwill | 2,189 | 2,181 | ||||||

Other assets | 3,061 | 2,838 | ||||||

Separate Accounts | 3,307 | 3,444 | ||||||

Total assets | $ | 114,490 | $ | 112,422 | ||||

Liabilities | ||||||||

Reserve for property and casualty insurance claims and claims expense | $ | 26,939 | $ | 26,325 | ||||

Reserve for life-contingent contract benefits | 12,214 | 12,549 | ||||||

Contractholder funds | 18,650 | 19,434 | ||||||

Unearned premiums | 14,408 | 13,473 | ||||||

Claim payments outstanding | 904 | 875 | ||||||

Deferred income taxes | 660 | 782 | ||||||

Other liabilities and accrued expenses | 7,325 | 6,639 | ||||||

Long-term debt | 6,450 | 6,350 | ||||||

Separate Accounts | 3,307 | 3,444 | ||||||

Total liabilities | 90,857 | 89,871 | ||||||

Commitments and Contingent Liabilities (Note 12) | ||||||||

Shareholders’ equity | ||||||||

Preferred stock and additional capital paid-in, $1 par value, 25 million shares authorized, 95.2 thousand and 72.2 thousand shares issued and outstanding, $2,380 and $1,805 aggregate liquidation preference | 2,303 | 1,746 | ||||||

Common stock, $.01 par value, 2.0 billion shares authorized and 900 million issued, 345 million and 355 million shares outstanding | 9 | 9 | ||||||

Additional capital paid-in | 3,441 | 3,313 | ||||||

Retained income | 46,178 | 43,162 | ||||||

Deferred Employee Stock Ownership Plan (“ESOP”) expense | (3 | ) | (3 | ) | ||||

Treasury stock, at cost (555 million and 545 million shares) | (27,011 | ) | (25,982 | ) | ||||

Accumulated other comprehensive income: | ||||||||

Unrealized net capital gains and losses: | ||||||||

Unrealized net capital gains and losses on fixed income securities with OTTI | 86 | 85 | ||||||

Other unrealized net capital gains and losses | (53 | ) | 1,981 | |||||

Unrealized adjustment to DAC, DSI and insurance reserves | (49 | ) | (404 | ) | ||||

Total unrealized net capital gains and losses | (16 | ) | 1,662 | |||||

Unrealized foreign currency translation adjustments | (34 | ) | (9 | ) | ||||

Unrecognized pension and other postretirement benefit cost | (1,234 | ) | (1,347 | ) | ||||

Total accumulated other comprehensive income (“AOCI”) | (1,284 | ) | 306 | |||||

Total shareholders’ equity | 23,633 | 22,551 | ||||||

Total liabilities and shareholders’ equity | $ | 114,490 | $ | 112,422 | ||||

See notes to condensed consolidated financial statements.

Third Quarter 2018 Form 10-Q 3

Condensed Consolidated Financial Statements

The Allstate Corporate and Subsidiaries

Condensed Consolidated Statements of Shareholders’ Equity

($ in millions) | Nine months ended September 30, | |||||||

2018 | 2017 | |||||||

(unaudited) | ||||||||

Preferred stock par value | $ | — | $ | — | ||||

Preferred stock additional capital paid-in | ||||||||

Balance, beginning of period | 1,746 | 1,746 | ||||||

Preferred stock issuance | 557 | — | ||||||

Balance, end of period | 2,303 | 1,746 | ||||||

Common stock par value | 9 | 9 | ||||||

Common stock additional capital paid-in | ||||||||

Balance, beginning of period | 3,313 | 3,303 | ||||||

Forward contract on accelerated share repurchase agreement | 45 | — | ||||||

Equity incentive plans activity | 83 | 27 | ||||||

Balance, end of period | 3,441 | 3,330 | ||||||

Retained income | ||||||||

Balance, beginning of period | 43,162 | 40,678 | ||||||

Cumulative effect of change in accounting principle | 1,088 | — | ||||||

Net income | 2,521 | 1,940 | ||||||

Dividends on common stock | (488 | ) | (406 | ) | ||||

Dividends on preferred stock | (105 | ) | (87 | ) | ||||

Balance, end of period | 46,178 | 42,125 | ||||||

Deferred ESOP expense | (3 | ) | (6 | ) | ||||

Treasury stock | ||||||||

Balance, beginning of period | (25,982 | ) | (24,741 | ) | ||||

Shares acquired | (1,117 | ) | (845 | ) | ||||

Shares reissued under equity incentive plans, net | 88 | 173 | ||||||

Balance, end of period | (27,011 | ) | (25,413 | ) | ||||

Accumulated other comprehensive income | ||||||||

Balance, beginning of period | 306 | (416 | ) | |||||

Cumulative effect of change in accounting principle | (910 | ) | — | |||||

Change in unrealized net capital gains and losses | (768 | ) | 598 | |||||

Change in unrealized foreign currency translation adjustments | (25 | ) | 36 | |||||

Change in unrecognized pension and other postretirement benefit cost | 113 | 110 | ||||||

Balance, end of period | (1,284 | ) | 328 | |||||

Total shareholders’ equity | $ | 23,633 | $ | 22,119 | ||||

See notes to condensed consolidated financial statements.

4 www.allstate.com

www.allstate.comCondensed Consolidated Financial Statements

The Allstate Corporation and Subsidiaries

Condensed Consolidated Statements of Cash Flows

($ in millions) | Nine months ended September 30, | |||||||

2018 | 2017 | |||||||

Cash flows from operating activities | (unaudited) | |||||||

Net income | $ | 2,521 | $ | 1,940 | ||||

Adjustments to reconcile net income to net cash provided by operating activities: | ||||||||

Depreciation, amortization and other non-cash items | 376 | 358 | ||||||

Realized capital gains and losses | (17 | ) | (318 | ) | ||||

Gain on disposition of operations | (4 | ) | (15 | ) | ||||

Interest credited to contractholder funds | 489 | 522 | ||||||

Changes in: | ||||||||

Policy benefits and other insurance reserves | 90 | 1,276 | ||||||

Unearned premiums | 785 | 525 | ||||||

Deferred policy acquisition costs | (203 | ) | (176 | ) | ||||

Premium installment receivables, net | (422 | ) | (267 | ) | ||||

Reinsurance recoverables, net | (103 | ) | (1,017 | ) | ||||

Income taxes | (227 | ) | 119 | |||||

Other operating assets and liabilities | 533 | 267 | ||||||

Net cash provided by operating activities | 3,818 | 3,214 | ||||||

Cash flows from investing activities | ||||||||

Proceeds from sales | ||||||||

Fixed income securities | 26,223 | 19,508 | ||||||

Equity securities | 4,637 | 5,179 | ||||||

Limited partnership interests | 490 | 767 | ||||||

Other investments | 234 | 170 | ||||||

Investment collections | ||||||||

Fixed income securities | 2,388 | 3,038 | ||||||

Mortgage loans | 378 | 477 | ||||||

Other investments | 370 | 458 | ||||||

Investment purchases | ||||||||

Fixed income securities | (29,049 | ) | (23,935 | ) | ||||

Equity securities | (4,791 | ) | (5,296 | ) | ||||

Limited partnership interests | (1,317 | ) | (1,082 | ) | ||||

Mortgage loans | (435 | ) | (311 | ) | ||||

Other investments | (686 | ) | (700 | ) | ||||

Change in short-term investments, net | (665 | ) | 2,257 | |||||

Change in other investments, net | (28 | ) | (28 | ) | ||||

Purchases of property and equipment, net | (195 | ) | (216 | ) | ||||

Acquisition of operations | (10 | ) | (1,356 | ) | ||||

Net cash used in investing activities | (2,456 | ) | (1,070 | ) | ||||

Cash flows from financing activities | ||||||||

Proceeds from issuance of long-term debt | 498 | — | ||||||

Redemption and repayment of long-term debt | (401 | ) | — | |||||

Proceeds from issuance of preferred stock | 557 | — | ||||||

Contractholder fund deposits | 756 | 767 | ||||||

Contractholder fund withdrawals | (1,474 | ) | (1,416 | ) | ||||

Dividends paid on common stock | (455 | ) | (391 | ) | ||||

Dividends paid on preferred stock | (97 | ) | (87 | ) | ||||

Treasury stock purchases | (1,062 | ) | (848 | ) | ||||

Shares reissued under equity incentive plans, net | 66 | 132 | ||||||

Other | 93 | (47 | ) | |||||

Net cash used in financing activities | (1,519 | ) | (1,890 | ) | ||||

Net (decrease) increase in cash | (157 | ) | 254 | |||||

Cash at beginning of period | 617 | 436 | ||||||

Cash at end of period | $ | 460 | $ | 690 | ||||

See notes to condensed consolidated financial statements.

Third Quarter 2018 Form 10-Q 5

Notes to Condensed Consolidated Financial Statements

The Allstate Corporation and Subsidiaries

Notes to Condensed Consolidated Financial Statements

(Unaudited)

Note 1 | General |

Basis of presentation

The accompanying condensed consolidated financial statements include the accounts of The Allstate Corporation (the “Corporation”) and its wholly owned subsidiaries, primarily Allstate Insurance Company (“AIC”), a property and casualty insurance company with various property and casualty and life and investment subsidiaries, including Allstate Life Insurance Company (“ALIC”) (collectively referred to as the “Company” or “Allstate”). These condensed consolidated financial statements have been prepared in conformity with accounting principles generally accepted in the United States of America (“GAAP”).

The condensed consolidated financial statements and notes as of September 30, 2018 and for the three month and nine month periods ended September 30, 2018 and 2017 are unaudited. The condensed consolidated financial statements reflect all adjustments (consisting only of normal recurring accruals) which are, in the opinion of management, necessary for the fair presentation of the financial position, results of operations and cash flows for the interim periods. These condensed consolidated financial statements and notes should be read in conjunction with the consolidated financial statements and notes thereto included in the Company’s annual report on Form 10-K for the year ended December 31, 2017. The results of operations for the interim periods should not be considered indicative of results to be expected for the full year. All significant intercompany accounts and transactions have been eliminated.

Adopted accounting standards

Recognition and Measurement of Financial Assets and Financial Liabilities

Effective January 1, 2018, the Company adopted new Financial Accounting Standards Board (“FASB”) guidance requiring equity investments, including equity securities and limited partnership interests not accounted for under the equity method of accounting or that do not result in consolidation to be measured at fair value with changes in fair value recognized in net income. The guidance clarifies that an entity should evaluate the realizability of deferred tax assets related to available-for-sale fixed income securities in combination with the entity’s other deferred tax assets. The Company’s adoption of the new FASB guidance included adoption of the relevant elements of Technical Corrections and Improvements to Financial Instruments, issued in February 2018.

Upon adoption of the new guidance on January 1, 2018, $1.16 billion of pre-tax unrealized net capital gains for equity securities were reclassified from AOCI to retained income. The after-tax change in accounting for equity securities did not affect the Company’s total shareholders’ equity and the unrealized net capital

gains of $910 million, reclassified to retained income will never be recognized in net income.

Upon adoption of the new guidance on January 1, 2018, the carrying value of cost method limited partnership interests increased $224 million, pre-tax, to fair value. The after-tax cumulative-effect increase in retained income of $177 million increased the Company’s shareholders’ equity but will never be recognized in net income thereby negatively impacting calculations of returns on equity.

Revenue from Contracts with Customers

Effective January 1, 2018, the Company adopted new FASB guidance which revises the criteria for revenue recognition. Insurance contracts are excluded from the scope of the new guidance. The Company’s principal activities impacted by the new guidance are those related to the issuance of protection plans for consumer products and automobiles and service contracts that provide roadside assistance. Under the guidance, the transaction price is attributed to underlying performance obligations in the contract and revenue is recognized as the entity satisfies performance obligations and transfers control of a good or service to the customer. Incremental costs of obtaining a contract may be capitalized and amortized to the extent the entity expects to recover those costs.

Adoption of the guidance on January 1, 2018 under the modified retrospective approach resulted in the recognition of an immaterial after-tax net cumulative effect increase to the beginning balance of retained income. In addition to the net cumulative effect, the Company also recorded in the statement of financial position an increase of approximately $160 million pre-tax in unearned premiums with a corresponding $160 million pre-tax increase in deferred policy acquisition costs (“DAC”) for protection plans sold directly to retailers for which SquareTrade Holding Company, Inc. (“SquareTrade”) is deemed to be the principal in the transaction. This impact offsets fully and did not impact retained income at the date of adoption.

Presentation of Net Periodic Pension and Postretirement Benefits Costs

Effective January 1, 2018, the Company adopted new FASB guidance requiring identification, on the statement of operations or in disclosures, the line items in which the components of net periodic pension and postretirement benefits costs are presented. The new guidance permits only the service cost component to be eligible for capitalization where applicable. The adoption had no impact on the Company’s results of operations or financial position.

Goodwill Impairment

In January 2017, the FASB issued guidance to simplify the accounting for goodwill impairment which

6 www.allstate.com

www.allstate.comNotes to Condensed Consolidated Financial Statements

removes the second step of the goodwill impairment test that requires a hypothetical purchase price allocation. Under the new guidance, goodwill impairment will be measured and recognized as the amount by which a reporting unit’s carrying value, including goodwill, exceeds its fair value, not to exceed the carrying amount of goodwill allocated to the reporting unit. The revised guidance does not affect a reporting entity’s ability to first assess qualitative factors by reporting unit to determine whether to perform the quantitative goodwill impairment test. The guidance is to be applied on a prospective basis, with the effects, if any, recognized in net income in the period of adoption. The Company elected to early adopt the new guidance as of January 1, 2018. The adoption had no impact on the Company’s results of operations or financial position.

Changes to significant accounting policies

Investments

Changes were made to the Company’s Significant Accounting Policies upon adoption of new FASB guidance related to the recognition and measurement of financial assets. Equity securities primarily include common stocks, exchange traded and mutual funds, non-redeemable preferred stocks and real estate investment trust equity investments. Equity securities are carried at fair value. Equity securities without readily determinable or estimable fair values are measured using the measurement alternative of cost less impairment, if any, and adjustments resulting from observable price changes in orderly transactions for the identical or similar investment of the same issuer. The periodic change in fair value of equity securities is recognized within realized capital gains and losses on the Condensed Consolidated Statements of Operations effective January 1, 2018.

Investments in limited partnership interests include interests in private equity funds, real estate funds and other funds. Where the Company’s interest is so minor that it exercises virtually no influence over operating and financial policies, investments in limited partnership interests purchased prior to January 1, 2018 are accounted for at fair value primarily utilizing the net asset value (“NAV”) as a practical expedient to determine fair value. All other investments in limited partnership interests, including those purchased subsequent to January 1, 2018, are accounted for in accordance with the equity method of accounting (“EMA”).

Investment income from limited partnership interests carried at fair value is recognized based upon the changes in fair value of the investee’s equity primarily determined using NAV. Income from EMA limited partnership interests is recognized based on the Company’s share of the partnerships’ earnings. Income from EMA limited partnership interests is generally recognized on a three month delay due to the availability of the related financial statements from investees.

Recognition of Revenue

Revenues related to protection plans, other contracts (primarily finance and insurance products) and roadside assistance are deferred and earned over the term of the contract in a manner that recognizes revenue as obligations under the contracts are performed. Revenues from these products are classified as premiums as the products are backed by insurance. Protection plans and finance and insurance premiums are recognized using a cost-based incurrence method. Roadside assistance premiums are recognized evenly over the term of the contract as performance obligations are fulfilled.

Tax Reform

On December 22, 2017, Public Law 115-97, known as the Tax Cuts and Jobs Act of 2017 (“Tax Legislation”) became effective, permanently reducing the U.S. corporate income tax rate from 35% to 21% beginning January 1, 2018. As a result, the corporate tax rate is not comparable between periods. During 2017, the Company revalued its deferred tax assets and liabilities and recorded liabilities related to the transition to the modified territorial system for international taxation. The impact of the Tax Legislation was adjusted from the Company’s preliminary estimate due to, among other things, changes in interpretations and assumptions the Company previously made, guidance that was issued and actions the Company took as a result of the Tax Legislation. During the third quarter of 2018, the Company recorded a reduction of $31 million to income tax expense related to these provisional amounts. The Company may make adjustments to these provisional amounts as additional information becomes available and future guidance is issued by the Internal Revenue Service.

Pending accounting standards

Accounting for Leases

In February 2016, the FASB issued guidance revising the accounting for leases. Under the new guidance, lessees will be required to recognize a right-of-use (“ROU”) asset and lease liability for all leases other than those with a term less than one year. The lease liability will be equal to the present value of lease payments. A ROU asset will be based on the lease liability adjusted for qualifying initial direct costs. The Company currently estimates that the recognition of the ROU asset and lease liability will result in an increase in both total assets and liabilities in the Condensed Consolidated Statement of Financial Position of approximately $525 million. The new guidance requires sellers in a sale-leaseback transaction to recognize the entire gain from the sale of an underlying asset at the time the sale is recognized rather than over the leaseback term. The carrying value of unrecognized gains on sale-leaseback transactions executed prior to January 1, 2019 are approximately $20 million, after-tax, and will be recorded as an increase to retained income.

The expense of operating leases under the new guidance will be recognized in the income statement on a straight-line basis by adjusting the amortization of

Third Quarter 2018 Form 10-Q 7

Notes to Condensed Consolidated Financial Statements

the ROU asset to produce a straight-line expense when combined with the interest expense on the lease liability. For finance leases, the expense components are computed separately and produce greater up-front expense compared to operating leases as interest expense on the lease liability is higher in early years and the ROU asset is amortized on a straight-line basis. Lease classification will be based on criteria similar to those currently applied. The accounting model for lessors will be similar to the current model with modifications to reflect definition changes for components such as initial direct costs. Lessors will continue to classify leases as operating, direct financing, or sales-type. The guidance is effective for reporting periods beginning after December 15, 2018, and will be implemented using the optional transition method that allows application of the transition provisions at the adoption date instead of the earliest date presented.

Measurement of Credit Losses on Financial Instruments

In June 2016, the FASB issued guidance which revises the credit loss recognition criteria for certain financial assets measured at amortized cost, including reinsurance recoverables. The new guidance replaces the existing incurred loss recognition model with an expected loss recognition model. The objective of the expected credit loss model is for the reporting entity to recognize its estimate of expected credit losses for affected financial assets in a valuation allowance deducted from the amortized cost basis of the related financial assets that results in presenting the net carrying value of the financial assets at the amount expected to be collected. The reporting entity must consider all relevant information available when estimating expected credit losses, including details about past events, current conditions, and reasonable and supportable forecasts over the life of an asset. Financial assets may be evaluated individually or on a pooled basis when they share similar risk characteristics. The measurement of credit losses for available-for-sale debt securities measured at fair value is not affected except that credit losses recognized are limited to the amount by which fair value is below amortized cost and the carrying value adjustment is recognized through a valuation allowance and not as a direct write-down. The guidance is effective for reporting periods beginning after December 15, 2019, and for most affected instruments must be adopted using a modified retrospective approach, with a cumulative effect adjustment recorded to beginning retained income. The Company is in the process of evaluating the impact of adoption.

Accounting for Hedging Activities

In August 2017, the FASB issued amendments intended to better align hedge accounting with an organization’s risk management activities. The amendments expand hedge accounting for nonfinancial and financial risk components and revise the measurement methodologies to better align with an organization’s risk management activities. Separate presentation of hedge ineffectiveness is eliminated to provide greater transparency of the full impact of

hedging by requiring presentation of the results of the hedged item and hedging instrument in a single financial statement line item. In addition, the amendments are designed to reduce complexity by simplifying the manner in which assessments of hedge effectiveness may be performed. The guidance is effective for reporting periods beginning after December 15, 2018. The presentation and disclosure guidance is effective on a prospective basis. The impact of adoption is not expected to be material to the Company’s results of operations or financial position.

Changes to the Disclosure Requirements for Deferred Benefit Plans

In August 2018, the FASB issued amendments to modify certain disclosure requirements for defined benefit plans. Disclosure additions relate to the weighted-average interest crediting rates for cash balance plans and other plans with interest crediting rates and explanations for significant gains and losses related to changes in the benefit obligation for the period. Disclosures to be removed include those that identify amounts that are expected to be reclassified out of AOCI and into the income statement in the coming year and the anticipated impact of a one-percentage point change in assumed health care cost trend rate on service and interest cost and on the accumulated benefit obligation. The amendments are effective for annual reporting periods beginning after December 15, 2020. The impacts of adoption are to the Company’s disclosures only.

Accounting for Long-Duration Insurance Contracts

In August 2018, the FASB issued guidance revising the accounting for certain long-duration insurance contracts. The new guidance changes the measurement of the Company’s reserves for traditional life, life-contingent immediate annuities and certain voluntary accident and health insurance products.

Under the new guidance, measurement assumptions, including those for mortality, morbidity and policy terminations, will be required to be reviewed and updated at least annually. The effect of updating measurement assumptions other than the discount rate are required to be determined on a retrospective basis and reported in net income. In addition, cash flows under the new guidance are required to be discounted using an upper-medium grade fixed income instrument yield that is updated through OCI at each reporting date. These changes will replace current GAAP, which utilizes assumptions set at policy issuance until such time as the assumptions result in reserves that are deficient when compared to reserves computed using current assumptions. When this occurs under current GAAP, premium deficiency reserves are recognized by unlocking reserve assumptions to eliminate a reserve deficiency.

The new guidance requires DAC and other capitalized balances currently amortized in proportion to premiums or gross profits to be amortized on a constant level basis over the expected term for all long-duration insurance contracts. DAC will not be subject to loss recognition testing but rather will be

8 www.allstate.com

www.allstate.comNotes to Condensed Consolidated Financial Statements

reduced when actual experience exceeds expected experience (i.e. as a result of unexpected contract terminations). The new guidance will no longer require adjustments to DAC and deferred sales inducement costs (“DSI”) related to unrealized gains and losses.

Market risk benefit product features are required to be measured at fair value with changes in fair value recorded in net income with the exception of changes in the fair value attributable to a change in the instrument’s credit risk, which are required to be recognized in OCI. Substantially all of the Company’s market risk benefits are reinsured and therefore these impacts are not expected to be material to the Company.

The guidance is to be included in the comparable financial statements issued in reporting periods beginning after December 15, 2020, thereby requiring restatement of prior periods presented. Early adoption is permitted. The new guidance will be applied to affected contracts and DAC on the basis of existing carrying amounts at the earliest period presented or the new guidance may be applied retrospectively using actual historical experience as of contract inception. The guidance for market risk benefits is required to be adopted retrospectively.

The Company is evaluating the anticipated impacts of applying the new guidance to both retained income and AOCI. While the requirements of the new guidance represent a material change from existing GAAP, the underlying economics of the business and related cash flows are unchanged. The Company has

not completed an evaluation of the specific impacts of adopting the new guidance, but anticipates the financial statement impact of migrating from existing GAAP to that required by the new guidance to be material, largely attributed to the impact of transitioning from an original investment-based discount rate to one based on an upper-medium grade fixed income investment yield and updates to mortality assumptions that had previously been locked in at issuance. The Company expects the most significant impacts will occur in the run-off annuity segment. The revised accounting for DAC will be applied prospectively using the new model and any DAC effects existing in AOCI as a result of applying existing GAAP at the date of adoption will be reversed.

Other revenue presentation

Concurrent with the adoption of new FASB guidance on revenue from contracts with customers and the Company’s objective of providing more information related to revenues for our Service Businesses, the Company revised the presentation of total revenue to include other revenue. Previously, components of other revenue were presented within operating costs and expenses and primarily represent fees collected from policyholders relating to premium installment payments, commissions on sales of non-proprietary products, fee-based services and other revenue transactions. Other revenue is recognized when performance obligations are fulfilled. Prior periods have been reclassified to conform to current separate presentation of other revenue.

Note 2 | Earnings per Common Share |

Basic earnings per common share is computed using the weighted average number of common shares outstanding, including vested unissued participating restricted stock units. Diluted earnings per common share is computed using the weighted average number

of common and dilutive potential common shares outstanding. For the Company, dilutive potential common shares consist of outstanding stock options and unvested non-participating restricted stock units and contingently issuable performance stock awards.

Computation of basic and diluted earnings per common share | ||||||||||||||||

($ in millions, except per share data) | Three months ended September 30, | Nine months ended September 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | |||||||||||||

Numerator: | ||||||||||||||||

Net income | $ | 870 | $ | 666 | $ | 2,521 | $ | 1,940 | ||||||||

Less: Preferred stock dividends | 37 | 29 | 105 | 87 | ||||||||||||

Net income applicable to common shareholders (1) | $ | 833 | $ | 637 | $ | 2,416 | $ | 1,853 | ||||||||

Denominator: | ||||||||||||||||

Weighted average common shares outstanding | 346.0 | 361.3 | 349.7 | 363.5 | ||||||||||||

Effect of dilutive potential common shares: | ||||||||||||||||

Stock options | 3.8 | 4.4 | 3.8 | 4.3 | ||||||||||||

Restricted stock units (non-participating) and performance stock awards | 1.9 | 1.4 | 1.9 | 1.3 | ||||||||||||

Weighted average common and dilutive potential common shares outstanding | 351.7 | 367.1 | 355.4 | 369.1 | ||||||||||||

Earnings per common share - Basic | $ | 2.41 | $ | 1.76 | $ | 6.91 | $ | 5.10 | ||||||||

Earnings per common share - Diluted | $ | 2.37 | $ | 1.74 | $ | 6.80 | $ | 5.02 | ||||||||

(1) | Net income applicable to common shareholders is net income less preferred stock dividends. |

Third Quarter 2018 Form 10-Q 9

Notes to Condensed Consolidated Financial Statements

The effect of dilutive potential common shares does not include the effect of options with an anti-dilutive effect on earnings per common share because their exercise prices exceed the average market price of Allstate common shares during the period or for which the unrecognized compensation cost would have an anti-dilutive effect.

Options to purchase 2.3 million and 0.2 million Allstate common shares, with exercise prices ranging from $84.93 to $102.84 and $78.35 to $93.93, were outstanding for the three month periods ended

September 30, 2018 and 2017, respectively, but were not included in the computation of diluted earnings per common share in those periods. Options to purchase 1.9 million and 2.5 million Allstate common shares, with exercise prices ranging from $84.93 to $102.84 and $74.03 to $93.93, were outstanding for the nine month periods ended September 30, 2018 and 2017, respectively, but were not included in the computation of diluted earnings per common share in those periods.

Note 3 | Acquisitions |

On January 3, 2017, the Company acquired SquareTrade, a consumer product protection plan provider that distributes through many of America’s major retailers and Europe’s mobile operators, for $1.4 billion in cash. SquareTrade provides protection plans covering a variety of consumer electronics and appliances. This acquisition broadened Allstate’s unique product offerings to better meet consumers’ needs.

In connection with the SquareTrade acquisition, the Company recorded goodwill of $1.10 billion, commissions paid to retailers (reported in deferred policy acquisition costs) of $66 million, other intangible assets (reported in other assets) of $555 million, contractual liability insurance policy premium expenses (reported in other assets) of $205 million, unearned premiums of $389 million and net deferred income tax liability of $138 million. These amounts reflect re-measurement adjustments to the fair value of the opening balance sheet assets and liabilities.

Of the $555 million assigned to other intangible assets, $465 million was attributable to acquired customer relationships and $69 million was assigned to

the SquareTrade trade name which is considered to have an indefinite useful life. The amortization expense of intangible assets was $20 million and $23 million for the three months ended September 30, 2018 and 2017, respectively, and was $61 million and $69 million for the nine months ended September 30, 2018 and 2017, respectively.

Subsequent event On October 5, 2018, the Company acquired InfoArmor, Inc. (“InfoArmor”), a leading provider of identity protection in the employee benefits market, for $525 million in cash. InfoArmor primarily offers identity protection to employees and their family members through voluntary benefit programs at over 1,400 firms, including more than 100 of the Fortune 500 companies. Due to the limited time since the closing date, the Company is currently evaluating the allocation of the purchase price and is unable to provide amounts recognized as of the closing date for the major classes of assets acquired and liabilities assumed. The Company will include this information in its annual report on Form 10-K for the year ended December 31, 2018.

10 www.allstate.com

www.allstate.comNotes to Condensed Consolidated Financial Statements

Note 4 | Reportable Segments |

Reportable segments revenue information | ||||||||||||||||

($ in millions) | Three months ended September 30, | Nine months ended September 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | |||||||||||||

Property-Liability | ||||||||||||||||

Insurance premiums | ||||||||||||||||

Auto | $ | 5,798 | $ | 5,501 | $ | 17,094 | $ | 16,327 | ||||||||

Homeowners | 1,891 | 1,832 | 5,603 | 5,462 | ||||||||||||

Other personal lines | 455 | 439 | 1,354 | 1,306 | ||||||||||||

Commercial lines | 176 | 124 | 477 | 367 | ||||||||||||

Allstate Protection | 8,320 | 7,896 | 24,528 | 23,462 | ||||||||||||

Discontinued Lines and Coverages | — | — | — | — | ||||||||||||

Total property-liability insurance premiums | 8,320 | 7,896 | 24,528 | 23,462 | ||||||||||||

Other revenue | 192 | 185 | 550 | 533 | ||||||||||||

Net investment income | 410 | 368 | 1,100 | 1,063 | ||||||||||||

Realized capital gains and losses | 126 | 82 | 16 | 302 | ||||||||||||

Total Property-Liability | 9,048 | 8,531 | 26,194 | 25,360 | ||||||||||||

Service Businesses | ||||||||||||||||

Consumer product protection plans | 125 | 78 | 369 | 207 | ||||||||||||

Roadside assistance | 66 | 69 | 198 | 204 | ||||||||||||

Finance and insurance products | 84 | 78 | 246 | 225 | ||||||||||||

Intersegment premiums and service fees (1) | 31 | 26 | 89 | 82 | ||||||||||||

Other revenue | 16 | 17 | 48 | 50 | ||||||||||||

Net investment income | 7 | 4 | 18 | 11 | ||||||||||||

Realized capital gains and losses | — | — | (6 | ) | — | |||||||||||

Total Service Businesses | 329 | 272 | 962 | 779 | ||||||||||||

Allstate Life | ||||||||||||||||

Traditional life insurance premiums | 149 | 141 | 443 | 420 | ||||||||||||

Accident and health insurance premiums | — | — | 1 | 1 | ||||||||||||

Interest-sensitive life insurance contract charges | 173 | 175 | 531 | 535 | ||||||||||||

Other revenue | 30 | 26 | 84 | 81 | ||||||||||||

Net investment income | 128 | 119 | 380 | 362 | ||||||||||||

Realized capital gains and losses | (3 | ) | 2 | (9 | ) | 4 | ||||||||||

Total Allstate Life | 477 | 463 | 1,430 | 1,403 | ||||||||||||

Allstate Benefits | ||||||||||||||||

Traditional life insurance premiums | 13 | 12 | 32 | 30 | ||||||||||||

Accident and health insurance premiums | 246 | 232 | 739 | 696 | ||||||||||||

Interest-sensitive life insurance contract charges | 26 | 29 | 83 | 85 | ||||||||||||

Net investment income | 19 | 18 | 57 | 54 | ||||||||||||

Realized capital gains and losses | 2 | 1 | — | 1 | ||||||||||||

Total Allstate Benefits | 306 | 292 | 911 | 866 | ||||||||||||

Allstate Annuities | ||||||||||||||||

Fixed annuities contract charges | 5 | 4 | 11 | 10 | ||||||||||||

Net investment income | 260 | 324 | 843 | 967 | ||||||||||||

Realized capital gains and losses | 51 | 18 | 28 | 11 | ||||||||||||

Total Allstate Annuities | 316 | 346 | 882 | 988 | ||||||||||||

Corporate and Other | ||||||||||||||||

Net investment income | 20 | 10 | 56 | 31 | ||||||||||||

Realized capital gains and losses | — | — | (12 | ) | — | |||||||||||

Total Corporate and Other | 20 | 10 | 44 | 31 | ||||||||||||

Intersegment eliminations (1) | (31 | ) | (26 | ) | (89 | ) | (82 | ) | ||||||||

Consolidated revenues | $ | 10,465 | $ | 9,888 | $ | 30,334 | $ | 29,345 | ||||||||

(1) Intersegment insurance premiums and service fees are primarily related to Arity and Allstate Roadside Services and are eliminated in the condensed consolidated financial statements.

Third Quarter 2018 Form 10-Q 11

Notes to Condensed Consolidated Financial Statements

Reportable segments financial performance | ||||||||||||||||

Three months ended September 30, | Nine months ended September 30, | |||||||||||||||

($ in millions) | 2018 | 2017 | 2018 | 2017 | ||||||||||||

Property-Liability | ||||||||||||||||

Allstate Protection | $ | 553 | $ | 572 | $ | 1,934 | $ | 1,392 | ||||||||

Discontinued Lines and Coverages | (80 | ) | (88 | ) | (86 | ) | (95 | ) | ||||||||

Total underwriting income | 473 | 484 | 1,848 | 1,297 | ||||||||||||

Net investment income | 410 | 368 | 1,100 | 1,063 | ||||||||||||

Income tax expense on operations | (178 | ) | (271 | ) | (603 | ) | (746 | ) | ||||||||

Realized capital gains and losses, after-tax | 103 | 54 | 16 | 199 | ||||||||||||

Gain on disposition of operations, after-tax | — | 1 | — | 7 | ||||||||||||

Tax Legislation expense | (3 | ) | — | (3 | ) | — | ||||||||||

Property-Liability net income applicable to common shareholders | 805 | 636 | 2,358 | 1,820 | ||||||||||||

Service Businesses | ||||||||||||||||

Adjusted net income (loss) | — | (17 | ) | (4 | ) | (35 | ) | |||||||||

Realized capital gains and losses, after-tax | (1 | ) | — | (5 | ) | — | ||||||||||

Amortization of purchased intangible assets, after-tax | (16 | ) | (15 | ) | (48 | ) | (45 | ) | ||||||||

Tax Legislation expense | (4 | ) | — | (4 | ) | — | ||||||||||

Service Businesses net loss applicable to common shareholders | (21 | ) | (32 | ) | (61 | ) | (80 | ) | ||||||||

Allstate Life | ||||||||||||||||

Adjusted net income | 74 | 74 | 221 | 196 | ||||||||||||

Realized capital gains and losses, after-tax | (3 | ) | 1 | (7 | ) | 2 | ||||||||||

DAC and DSI amortization related to realized capital gains and losses, after-tax | (1 | ) | (2 | ) | (6 | ) | (8 | ) | ||||||||

Tax Legislation expense | (16 | ) | — | (16 | ) | — | ||||||||||

Allstate Life net income applicable to common shareholders | 54 | 73 | 192 | 190 | ||||||||||||

Allstate Benefits | ||||||||||||||||

Adjusted net income | 32 | 28 | 94 | 75 | ||||||||||||

Realized capital gains and losses, after-tax | 2 | 1 | — | 1 | ||||||||||||

Allstate Benefits net income applicable to common shareholders | 34 | 29 | 94 | 76 | ||||||||||||

Allstate Annuities | ||||||||||||||||

Adjusted net income | 20 | 55 | 99 | 149 | ||||||||||||

Realized capital gains and losses, after-tax | 40 | 11 | 22 | 6 | ||||||||||||

Valuation changes on embedded derivatives not hedged, after-tax | 1 | (1 | ) | 5 | (2 | ) | ||||||||||

Gain on disposition of operations, after-tax | 1 | 1 | 3 | 3 | ||||||||||||

Tax Legislation benefit | 69 | — | 69 | — | ||||||||||||

Allstate Annuities net income applicable to common shareholders | 131 | 66 | 198 | 156 | ||||||||||||

Corporate and Other | ||||||||||||||||

Adjusted net loss | (155 | ) | (134 | ) | (340 | ) | (295 | ) | ||||||||

Realized capital gains and losses, after-tax | — | — | (10 | ) | — | |||||||||||

Business combination expenses, after-tax | — | (1 | ) | — | (14 | ) | ||||||||||

Tax Legislation expense | (15 | ) | — | (15 | ) | — | ||||||||||

Corporate and Other net loss applicable to common shareholders | (170 | ) | (135 | ) | (365 | ) | (309 | ) | ||||||||

Consolidated net income applicable to common shareholders | $ | 833 | $ | 637 | $ | 2,416 | $ | 1,853 | ||||||||

12 www.allstate.com

www.allstate.comNotes to Condensed Consolidated Financial Statements

Note 5 | Investments |

Amortized cost, gross unrealized gains and losses and fair value for fixed income securities | ||||||||||||||||

($ in millions) | Amortized cost | Gross unrealized | Fair value | |||||||||||||

Gains | Losses | |||||||||||||||

September 30, 2018 | ||||||||||||||||

U.S. government and agencies | $ | 3,142 | $ | 36 | $ | (27 | ) | $ | 3,151 | |||||||

Municipal | 9,316 | 204 | (105 | ) | 9,415 | |||||||||||

Corporate | 42,828 | 557 | (723 | ) | 42,662 | |||||||||||

Foreign government | 854 | 12 | (12 | ) | 854 | |||||||||||

Asset-backed securities (“ABS”) | 979 | 8 | (8 | ) | 979 | |||||||||||

Residential mortgage-backed securities (“RMBS”) | 404 | 98 | (2 | ) | 500 | |||||||||||

Commercial mortgage-backed securities (“CMBS”) | 74 | 7 | (1 | ) | 80 | |||||||||||

Redeemable preferred stock | 21 | 1 | — | 22 | ||||||||||||

Total fixed income securities | $ | 57,618 | $ | 923 | $ | (878 | ) | $ | 57,663 | |||||||

December 31, 2017 | ||||||||||||||||

U.S. government and agencies | $ | 3,580 | $ | 56 | $ | (20 | ) | $ | 3,616 | |||||||

Municipal | 8,053 | 311 | (36 | ) | 8,328 | |||||||||||

Corporate | 42,996 | 1,234 | (204 | ) | 44,026 | |||||||||||

Foreign government | 1,005 | 27 | (11 | ) | 1,021 | |||||||||||

ABS | 1,266 | 13 | (7 | ) | 1,272 | |||||||||||

RMBS | 480 | 101 | (3 | ) | 578 | |||||||||||

CMBS | 124 | 6 | (2 | ) | 128 | |||||||||||

Redeemable preferred stock | 21 | 2 | — | 23 | ||||||||||||

Total fixed income securities | $ | 57,525 | $ | 1,750 | $ | (283 | ) | $ | 58,992 | |||||||

Scheduled maturities for fixed income securities | ||||||||

($ in millions) | As of September 30, 2018 | |||||||

Amortized cost | Fair value | |||||||

Due in one year or less | $ | 4,038 | $ | 4,042 | ||||

Due after one year through five years | 28,963 | 28,812 | ||||||

Due after five years through ten years | 16,216 | 15,987 | ||||||

Due after ten years | 6,944 | 7,263 | ||||||

56,161 | 56,104 | |||||||

ABS, RMBS and CMBS | 1,457 | 1,559 | ||||||

Total | $ | 57,618 | $ | 57,663 | ||||

Actual maturities may differ from those scheduled as a result of calls and make-whole payments by the issuers. ABS, RMBS and CMBS are shown separately because of the potential for prepayment of principal prior to contractual maturity dates.

Net investment income | ||||||||||||||||

($ in millions) | Three months ended September 30, | Nine months ended September 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | |||||||||||||

Fixed income securities | $ | 527 | $ | 519 | $ | 1,544 | $ | 1,564 | ||||||||

Equity securities | 35 | 37 | 130 | 130 | ||||||||||||

Mortgage loans | 52 | 52 | 163 | 157 | ||||||||||||

Limited partnership interests (1)(2) | 210 | 223 | 563 | 596 | ||||||||||||

Short-term investments | 19 | 9 | 50 | 21 | ||||||||||||

Other | 71 | 58 | 205 | 174 | ||||||||||||

Investment income, before expense | 914 | 898 | 2,655 | 2,642 | ||||||||||||

Investment expense | (70 | ) | (55 | ) | (201 | ) | (154 | ) | ||||||||

Net investment income | $ | 844 | $ | 843 | $ | 2,454 | $ | 2,488 | ||||||||

(1) | Due to the adoption of the recognition and measurement accounting standard, limited partnerships previously reported using the cost method are now reported at fair value with changes in fair value recognized in net investment income. |

(2) | Includes net investment income of $135 million and $381 million for EMA limited partnership interests and $75 million and $182 million for limited partnership interests carried at fair value for the three and nine months ended September 30, 2018, respectively. |

Third Quarter 2018 Form 10-Q 13

Notes to Condensed Consolidated Financial Statements

Realized capital gains and losses by asset type | ||||||||||||||||

($ in millions) | Three months ended September 30, | Nine months ended September 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | |||||||||||||

Fixed income securities | $ | (30 | ) | $ | 41 | $ | (153 | ) | $ | 78 | ||||||

Equity securities | 223 | 57 | 204 | 182 | ||||||||||||

Mortgage loans | — | 1 | 2 | 1 | ||||||||||||

Limited partnership interests | (23 | ) | 21 | (56 | ) | 92 | ||||||||||

Derivatives | 5 | (17 | ) | 20 | (40 | ) | ||||||||||

Other | 1 | — | — | 5 | ||||||||||||

Realized capital gains and losses | $ | 176 | $ | 103 | $ | 17 | $ | 318 | ||||||||

Realized capital gains and losses by transaction type | ||||||||||||||||

($ in millions) | Three months ended September 30, | Nine months ended September 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | |||||||||||||

Impairment write-downs (1) | $ | (5 | ) | $ | (23 | ) | $ | (10 | ) | $ | (94 | ) | ||||

Change in intent write-downs (1) | — | (5 | ) | — | (43 | ) | ||||||||||

Net OTTI losses recognized in earnings | (5 | ) | (28 | ) | (10 | ) | (137 | ) | ||||||||

Sales (1) | (22 | ) | 148 | (139 | ) | 495 | ||||||||||

Valuation of equity investments (1) | 198 | — | 149 | — | ||||||||||||

Valuation and settlements of derivative instruments | 5 | (17 | ) | 17 | (40 | ) | ||||||||||

Realized capital gains and losses | $ | 176 | $ | 103 | $ | 17 | $ | 318 | ||||||||

(1) | Due to the adoption of the recognition and measurement accounting standard, equity securities are reported at fair value with changes in fair value recognized in valuation of equity investments and are no longer included in impairment write-downs, change in intent write-downs and sales. |

Gross gains of $21 million and gross losses of $48 million were realized on sales of fixed income securities during the three months ended September 30, 2018. Gross gains of $145 million and gross losses of $36 million were realized on sales of fixed income and equity securities during the three months ended September 30, 2017.

Gross gains of $95 million and gross losses of $242 million were realized on sales of fixed income securities during the nine months ended September 30, 2018. Gross gains of $521 million and gross losses of $161 million were realized on sales of fixed income and equity securities during the nine months ended September 30, 2017.

Valuation changes included in net income for investments still held as of September 30, 2018 | ||||||||

($ in millions) | Three months ended September 30, 2018 | Nine months ended September 30, 2018 | ||||||

Equity securities (1) | $ | 234 | $ | 321 | ||||

Limited partnership interests carried at fair value (1) | 75 | 181 | ||||||

Total valuation changes | $ | 309 | $ | 502 | ||||

(1) | Investments held at the end of a prior quarter that were sold in the current quarter are not included in the year-to-date amounts shown in the table above; therefore, the sum of the quarterly amounts may not equal the year-to-date amount. |

14 www.allstate.com

www.allstate.comNotes to Condensed Consolidated Financial Statements

OTTI losses by asset type | ||||||||||||||||||||||||

($ in millions) | Three months ended September 30, 2018 | Three months ended September 30, 2017 | ||||||||||||||||||||||

Gross | Included in OCI | Net | Gross | Included in OCI | Net | |||||||||||||||||||

Fixed income securities: | ||||||||||||||||||||||||

Municipal | $ | — | $ | — | $ | — | $ | — | $ | — | $ | — | ||||||||||||

ABS | — | (1 | ) | (1 | ) | — | (1 | ) | (1 | ) | ||||||||||||||

RMBS | — | — | — | — | — | — | ||||||||||||||||||

CMBS | (2 | ) | — | (2 | ) | (1 | ) | (1 | ) | (2 | ) | |||||||||||||

Total fixed income securities | (2 | ) | (1 | ) | (3 | ) | (1 | ) | (2 | ) | (3 | ) | ||||||||||||

Equity securities (1) | — | — | — | (8 | ) | — | (8 | ) | ||||||||||||||||

Mortgage loans | — | — | — | (1 | ) | — | (1 | ) | ||||||||||||||||

Limited partnership interests (1) | (2 | ) | — | (2 | ) | (16 | ) | — | (16 | ) | ||||||||||||||

Other | — | — | — | — | — | — | ||||||||||||||||||

OTTI losses | $ | (4 | ) | $ | (1 | ) | $ | (5 | ) | $ | (26 | ) | $ | (2 | ) | $ | (28 | ) | ||||||

Nine months ended September 30, 2018 | Nine months ended September 30, 2017 | |||||||||||||||||||||||

Gross | Included in OCI | Net | Gross | Included in OCI | Net | |||||||||||||||||||

Fixed income securities: | ||||||||||||||||||||||||

Municipal | $ | — | $ | — | $ | — | $ | (1 | ) | $ | (2 | ) | $ | (3 | ) | |||||||||

Corporate | — | — | — | (9 | ) | 3 | (6 | ) | ||||||||||||||||

ABS | (1 | ) | (1 | ) | (2 | ) | (1 | ) | (1 | ) | (2 | ) | ||||||||||||

RMBS | (1 | ) | — | (1 | ) | (1 | ) | (3 | ) | (4 | ) | |||||||||||||

CMBS | (2 | ) | (1 | ) | (3 | ) | (9 | ) | 1 | (8 | ) | |||||||||||||

Total fixed income securities | (4 | ) | (2 | ) | (6 | ) | (21 | ) | (2 | ) | (23 | ) | ||||||||||||

Equity securities (1) | — | — | — | (77 | ) | — | (77 | ) | ||||||||||||||||

Mortgage loans | — | — | — | (1 | ) | — | (1 | ) | ||||||||||||||||

Limited partnership interests (1) | (3 | ) | — | (3 | ) | (32 | ) | — | (32 | ) | ||||||||||||||

Other | (1 | ) | — | (1 | ) | (4 | ) | — | (4 | ) | ||||||||||||||

OTTI losses | $ | (8 | ) | $ | (2 | ) | $ | (10 | ) | $ | (135 | ) | $ | (2 | ) | $ | (137 | ) | ||||||

(1) | Due to the adoption of the recognition and measurement accounting standard, equity securities and limited partnerships previously reported using the cost method are now reported at fair value with changes in fair value recognized in net income and are no longer included in the table above. |

The total amount of OTTI losses included in AOCI at the time of impairment for fixed income securities, which were not included in earnings, are presented in the following table. The amounts exclude $195 million and $208 million as of September 30, 2018 and

December 31, 2017, respectively, of net unrealized gains related to changes in valuation of the fixed income securities subsequent to the impairment measurement date.

OTTI losses included in AOCI at the time of impairment for fixed income securities | ||||||||

($ in millions) | September 30, 2018 | December 31, 2017 | ||||||

Municipal | $ | (5 | ) | $ | (5 | ) | ||

ABS | (11 | ) | (15 | ) | ||||

RMBS | (68 | ) | (77 | ) | ||||

CMBS | (3 | ) | (4 | ) | ||||

Total | $ | (87 | ) | $ | (101 | ) | ||

Third Quarter 2018 Form 10-Q 15

Notes to Condensed Consolidated Financial Statements

Rollforward of the cumulative credit losses recognized in earnings for fixed income securities held as of September 30, | ||||||||||||||||

($ in millions) | Three months ended | Nine months ended September 30, | ||||||||||||||

2018 | 2017 | 2018 | 2017 | |||||||||||||

Beginning balance | $ | (206 | ) | $ | (281 | ) | $ | (226 | ) | $ | (318 | ) | ||||

Additional credit loss for securities previously other-than-temporarily impaired | (3 | ) | (3 | ) | (5 | ) | (15 | ) | ||||||||

Additional credit loss for securities not previously other-than-temporarily impaired | — | — | (1 | ) | (8 | ) | ||||||||||

Reduction in credit loss for securities disposed or collected | 4 | 20 | 26 | 76 | ||||||||||||

Change in credit loss due to accretion of increase in cash flows | — | — | 1 | 1 | ||||||||||||

Ending balance | $ | (205 | ) | $ | (264 | ) | $ | (205 | ) | $ | (264 | ) | ||||

The Company uses its best estimate of future cash flows expected to be collected from the fixed income security, discounted at the security’s original or current effective rate, as appropriate, to calculate a recovery value and determine whether a credit loss exists. The determination of cash flow estimates is inherently subjective and methodologies may vary depending on facts and circumstances specific to the security. All reasonably available information relevant to the collectability of the security, including past events, current conditions, and reasonable and supportable assumptions and forecasts, are considered when developing the estimate of cash flows expected to be collected. That information generally includes, but is not limited to, the remaining payment terms of the security, prepayment speeds, foreign exchange rates, the financial condition and future earnings potential of the issue or issuer, expected defaults, expected recoveries, the value of underlying collateral, vintage, geographic concentration of underlying collateral, available reserves or escrows, current subordination levels, third party guarantees and other credit

enhancements. Other information, such as industry analyst reports and forecasts, sector credit ratings, financial condition of the bond insurer for insured fixed income securities, and other market data relevant to the realizability of contractual cash flows, may also be considered. The estimated fair value of collateral will be used to estimate recovery value if the Company determines that the security is dependent on the liquidation of collateral for ultimate settlement. If the estimated recovery value is less than the amortized cost of the security, a credit loss exists and an OTTI for the difference between the estimated recovery value and amortized cost is recorded in earnings. The portion of the unrealized loss related to factors other than credit remains classified in AOCI. If the Company determines that the fixed income security does not have sufficient cash flow or other information to estimate a recovery value for the security, the Company may conclude that the entire decline in fair value is deemed to be credit related and the loss is recorded in earnings.

Unrealized net capital gains and losses included in AOCI | ||||||||||||||||

($ in millions) | Fair value | Gross unrealized | Unrealized net gains (losses) | |||||||||||||

September 30, 2018 | Gains | Losses | ||||||||||||||

Fixed income securities | $ | 57,663 | $ | 923 | $ | (878 | ) | $ | 45 | |||||||

Short-term investments | 3,071 | — | — | — | ||||||||||||

Derivative instruments | — | — | (3 | ) | (3 | ) | ||||||||||

EMA limited partnerships (1) | 2 | |||||||||||||||

Unrealized net capital gains and losses, pre-tax | 44 | |||||||||||||||

Amounts recognized for: | ||||||||||||||||

Insurance reserves (2) | — | |||||||||||||||

DAC and DSI (3) | (62 | ) | ||||||||||||||

Amounts recognized | (62 | ) | ||||||||||||||

Deferred income taxes | 2 | |||||||||||||||

Unrealized net capital gains and losses, after-tax | $ | (16 | ) | |||||||||||||

(1) | Unrealized net capital gains and losses for limited partnership interests represent the Company’s share of EMA limited partnerships’ OCI. Fair value and gross unrealized gains and losses are not applicable. |

(2) | The insurance reserves adjustment represents the amount by which the reserve balance would increase if the net unrealized gains in the applicable product portfolios were realized and reinvested at lower interest rates, resulting in a premium deficiency. This adjustment primarily relates to structured settlement annuities with life contingencies (a type of immediate fixed annuities). |

(3) | The DAC and DSI adjustment balance represents the amount by which the amortization of DAC and DSI would increase or decrease if the unrealized gains or losses in the respective product portfolios were realized. |

16 www.allstate.com

www.allstate.comNotes to Condensed Consolidated Financial Statements

Unrealized net capital gains and losses included in AOCI | ||||||||||||||||

($ in millions) | Fair value | Gross unrealized | Unrealized net gains (losses) | |||||||||||||

December 31, 2017 | Gains | Losses | ||||||||||||||

Fixed income securities | $ | 58,992 | $ | 1,750 | $ | (283 | ) | $ | 1,467 | |||||||

Equity securities | 6,621 | 1,172 | (12 | ) | 1,160 | |||||||||||

Short-term investments | 1,944 | — | — | — | ||||||||||||

Derivative instruments (1) | 2 | 2 | (3 | ) | (1 | ) | ||||||||||

EMA limited partnerships | 1 | |||||||||||||||

Unrealized net capital gains and losses, pre-tax | 2,627 | |||||||||||||||

Amounts recognized for: | ||||||||||||||||

Insurance reserves | (315 | ) | ||||||||||||||

DAC and DSI | (196 | ) | ||||||||||||||

Amounts recognized | (511 | ) | ||||||||||||||

Deferred income taxes | (454 | ) | ||||||||||||||

Unrealized net capital gains and losses, after-tax | $ | 1,662 | ||||||||||||||

(1) Included in the fair value of derivative instruments is $2 million classified as liabilities.

Change in unrealized net capital gains and losses | ||||

($ in millions) | Nine months ended September 30, 2018 | |||

Fixed income securities | $ | (1,422 | ) | |

Equity securities (1) | — | |||

Derivative instruments | (2 | ) | ||

EMA limited partnerships | 1 | |||

Total | (1,423 | ) | ||

Amounts recognized for: | ||||

Insurance reserves | 315 | |||

DAC and DSI | 134 | |||

Amounts recognized | 449 | |||

Deferred income taxes | 206 | |||

Decrease in unrealized net capital gains and losses, after-tax | $ | (768 | ) | |

(1) Upon adoption of the recognition and measurement accounting standard on January 1, 2018, $1.16 billion of pre-tax unrealized net capital gains for equity securities were reclassified from AOCI to retained income. See Note 1 of the condensed consolidated financial statements.

Portfolio monitoring

The Company has a comprehensive portfolio monitoring process to identify and evaluate each fixed income security whose carrying value may be other-than-temporarily impaired.

For each fixed income security in an unrealized loss position, the Company assesses whether management with the appropriate authority has made the decision to sell or whether it is more likely than not the Company will be required to sell the security before recovery of the amortized cost basis for reasons such as liquidity, contractual or regulatory purposes. If a security meets either of these criteria, the security’s decline in fair value is considered other than temporary and is recorded in earnings.

If the Company has not made the decision to sell the fixed income security and it is not more likely than not the Company will be required to sell the fixed income security before recovery of its amortized cost basis, the Company evaluates whether it expects to receive cash flows sufficient to recover the entire amortized cost basis of the security. The Company calculates the estimated recovery value by discounting the best estimate of future cash flows at the security’s original or current effective rate, as appropriate, and

compares this to the amortized cost of the security. If the Company does not expect to receive cash flows sufficient to recover the entire amortized cost basis of the fixed income security, the credit loss component of the impairment is recorded in earnings, with the remaining amount of the unrealized loss related to other factors recognized in OCI.

For fixed income securities managed by third parties, either the Company has contractually retained its decision-making authority as it pertains to selling securities that are in an unrealized loss position or it recognizes any unrealized loss at the end of the period through a charge to earnings.

The Company’s portfolio monitoring process includes a quarterly review of all securities to identify instances where the fair value of a security compared to its amortized cost is below established thresholds. The process also includes the monitoring of other impairment indicators such as ratings, ratings downgrades and payment defaults. The securities identified, in addition to other securities for which the Company may have a concern, are evaluated for potential OTTI using all reasonably available information relevant to the collectability or recovery of the security. Inherent in the Company’s evaluation of

Third Quarter 2018 Form 10-Q 17

Notes to Condensed Consolidated Financial Statements

OTTI for these securities are assumptions and estimates about the financial condition and future earnings potential of the issue or issuer. Some of the factors that may be considered in evaluating whether a decline in fair value is other than temporary are: 1) the financial condition, near-term and long-term prospects of the issue or issuer, including relevant industry specific market conditions and trends, geographic

location and implications of rating agency actions and offering prices; 2) the specific reasons that a security is in an unrealized loss position, including overall market conditions which could affect liquidity; and 3) the length of time and extent to which the fair value has been less than amortized cost.

Gross unrealized losses and fair value by type and length of time held in a continuous unrealized loss position | ||||||||||||||||||||||||||

($ in millions) | Less than 12 months | 12 months or more | Total unrealized losses | |||||||||||||||||||||||

Number of issues | Fair value | Unrealized losses | Number of issues | Fair value | Unrealized losses | |||||||||||||||||||||

September 30, 2018 | ||||||||||||||||||||||||||

Fixed income securities | ||||||||||||||||||||||||||

U.S. government and agencies | 65 | $ | 2,517 | $ | (23 | ) | 26 | $ | 175 | $ | (4 | ) | $ | (27 | ) | |||||||||||

Municipal | 3,192 | 5,600 | (75 | ) | 480 | 667 | (30 | ) | (105 | ) | ||||||||||||||||

Corporate | 1,823 | 24,061 | (500 | ) | 329 | 4,274 | (223 | ) | (723 | ) | ||||||||||||||||

Foreign government | 26 | 166 | (2 | ) | 25 | 432 | (10 | ) | (12 | ) | ||||||||||||||||

ABS | 68 | 442 | (3 | ) | 19 | 107 | (5 | ) | (8 | ) | ||||||||||||||||

RMBS | 97 | 21 | — | 182 | 53 | (2 | ) | (2 | ) | |||||||||||||||||

CMBS | 5 | 18 | — | 3 | 1 | (1 | ) | (1 | ) | |||||||||||||||||

Total fixed income securities | 5,276 | $ | 32,825 | $ | (603 | ) | 1,064 | $ | 5,709 | $ | (275 | ) | $ | (878 | ) | |||||||||||

Investment grade fixed income securities | 4,939 | $ | 30,338 | $ | (529 | ) | 1,015 | $ | 5,461 | $ | (253 | ) | $ | (782 | ) | |||||||||||

Below investment grade fixed income securities | 337 | 2,487 | (74 | ) | 49 | 248 | (22 | ) | (96 | ) | ||||||||||||||||

Total fixed income securities | 5,276 | $ | 32,825 | $ | (603 | ) | 1,064 | $ | 5,709 | $ | (275 | ) | $ | (878 | ) | |||||||||||

December 31, 2017 | ||||||||||||||||||||||||||

Fixed income securities | ||||||||||||||||||||||||||

U.S. government and agencies | 66 | $ | 2,829 | $ | (18 | ) | 18 | $ | 182 | $ | (2 | ) | $ | (20 | ) | |||||||||||

Municipal | 1,756 | 3,143 | (24 | ) | 165 | 349 | (12 | ) | (36 | ) | ||||||||||||||||

Corporate | 781 | 11,616 | (102 | ) | 208 | 3,289 | (102 | ) | (204 | ) | ||||||||||||||||

Foreign government | 45 | 580 | (10 | ) | 5 | 44 | (1 | ) | (11 | ) | ||||||||||||||||

ABS | 57 | 476 | (3 | ) | 9 | 34 | (4 | ) | (7 | ) | ||||||||||||||||

RMBS | 118 | 35 | (1 | ) | 181 | 50 | (2 | ) | (3 | ) | ||||||||||||||||

CMBS | 2 | 1 | — | 6 | 23 | (2 | ) | (2 | ) | |||||||||||||||||

Redeemable preferred stock | 1 | — | — | — | — | — | — | |||||||||||||||||||

Total fixed income securities | 2,826 | 18,680 | (158 | ) | 592 | 3,971 | (125 | ) | (283 | ) | ||||||||||||||||

Equity securities | 127 | 369 | (12 | ) | 2 | — | — | (12 | ) | |||||||||||||||||

Total fixed income and equity securities | 2,953 | $ | 19,049 | $ | (170 | ) | 594 | $ | 3,971 | $ | (125 | ) | $ | (295 | ) | |||||||||||

Investment grade fixed income securities | 2,706 | $ | 17,668 | $ | (134 | ) | 535 | $ | 3,751 | $ | (98 | ) | $ | (232 | ) | |||||||||||

Below investment grade fixed income securities | 120 | 1,012 | (24 | ) | 57 | 220 | (27 | ) | (51 | ) | ||||||||||||||||

Total fixed income securities | 2,826 | $ | 18,680 | $ | (158 | ) | 592 | $ | 3,971 | $ | (125 | ) | $ | (283 | ) | |||||||||||

As of September 30, 2018, $862 million of the $878 million unrealized losses are related to securities with an unrealized loss position less than 20% of amortized cost, the degree of which suggests that these securities do not pose a high risk of being other-than-temporarily impaired. Of the $862 million, $770 million are related to unrealized losses on investment grade fixed income securities. Of the remaining $92 million, $58 million have been in an unrealized loss position for less than 12 months. Investment grade is defined as a security having a rating of Aaa, Aa, A or Baa from Moody’s, a rating of AAA, AA, A or BBB from S&P Global Ratings (“S&P”), a comparable rating from another nationally recognized rating agency, or a comparable internal rating if an externally provided rating is not available. Market prices for certain securities may have credit spreads which imply higher or lower credit quality than the current third party rating. Unrealized

losses on investment grade securities are principally related to an increase in market yields which may include increased risk-free interest rates and/or wider credit spreads since the time of initial purchase. The unrealized losses are expected to reverse as the securities approach maturity.

As of September 30, 2018, the remaining $16 million of unrealized losses are related to securities in unrealized loss positions greater than or equal to 20% of amortized cost. Investment grade fixed income securities comprising $12 million of these unrealized losses were evaluated based on factors such as discounted cash flows and the financial condition and near-term and long-term prospects of the issue or issuer and were determined to have adequate resources to fulfill contractual obligations. Of the $16 million, $4 million are related to below investment

18 www.allstate.com

www.allstate.comNotes to Condensed Consolidated Financial Statements

grade fixed income securities. Of these amounts, $1 million are related to below investment grade fixed income securities that had been in an unrealized loss position greater than or equal to 20% of amortized cost for a period of twelve or more consecutive months as of September 30, 2018.

ABS, RMBS and CMBS in an unrealized loss position were evaluated based on actual and projected collateral losses relative to the securities’ positions in the respective securitization trusts, security specific expectations of cash flows, and credit ratings. This evaluation also takes into consideration credit enhancement, measured in terms of (i) subordination from other classes of securities in the trust that are contractually obligated to absorb losses before the class of security the Company owns, and (ii) the expected impact of other structural features embedded in the securitization trust beneficial to the class of securities the Company owns, such as overcollateralization and excess spread. Municipal bonds in an unrealized loss position were evaluated based on the underlying credit quality of the primary obligor, obligation type and quality of the underlying assets.

As of September 30, 2018, the Company has not made the decision to sell and it is not more likely than not the Company will be required to sell fixed income securities with unrealized losses before recovery of the amortized cost basis.

Limited partnerships