Exhibit (a)(1)(A)

OFFER TO PURCHASE FOR CASH

8,669,029 ORDINARY SHARES

OF

MAGAL SECURITY SYSTEMS LTD.

AT

$2.95 NET PER SHARE

by

FIMI OPPORTUNITY V, L.P.

FIMI ISRAEL OPPORTUNITY FIVE, LIMITED PARTNERSHIP

|

THE INITIAL OFFER PERIOD AND WITHDRAWAL RIGHTS WILL EXPIRE AT 10:00 A.M., NEW YORK TIME, ON JUNE 22, 2020, UNLESS THE OFFER IS EXTENDED.

|

We, FIMI Opportunity V, L.P, a limited partnership organized under the laws of the State of Delaware and FIMI Israel Opportunity Five, Limited Partnership, a limited partnership organized under the

laws of the State of Israel (collectively, “FIMI”), are offering to purchase 8,669,029 ordinary shares, NIS 1.0 par value per share, of Magal Security Systems Ltd., (“Magal” and “Magal Shares”,

respectively), at the price of $2.95 per Magal share, net to you (subject to withholding taxes, as applicable), in cash, without interest. Based on the Annual Report on Form 20-F filed by Magal on April 23, 2020, as of December 31, 2019, there was a

total of 23,153,985 Magal Shares issued and outstanding.

THE OFFER IS CONDITIONED UPON, AMONG OTHER THINGS, THE FOLLOWING:

|

(I)

|

AT LEAST 1,200,000 MAGAL SHARES (CURRENTLY REPRESENTING APPROXIMATELY 5.2% OF THE ISSUED AND OUTSTANDING SHARES AND VOTING POWER OF MAGAL), ARE VALIDLY TENDERED AND NOT PROPERLY WITHDRAWN PRIOR TO THE

COMPLETION OF THE INITIAL OFFER PERIOD (AS DEFINED BELOW);

|

|

(II)

|

IN ACCORDANCE WITH ISRAELI LAW, AT THE COMPLETION OF THE INITIAL OFFER PERIOD, THE AGGREGATE NUMBER OF MAGAL SHARES VALIDLY TENDERED AND NOT PROPERLY WITHDRAWN IS GREATER THAN THE AGGREGATE NUMBER OF MAGAL

SHARES REPRESENTED BY NOTICES OF OBJECTION TO THE CONSUMMATION OF THE OFFER; AND

|

|

(III)

|

THE ISRAEL COMPETITION AUTHORITY SHALL HAVE APPROVED THE PURCHASE OF THE MAGAL SHARES PURSUANT TO THIS OFFER TO PURCHASE.

|

THE OFFER IS ALSO SUBJECT TO CERTAIN OTHER CONDITIONS CONTAINED IN THIS OFFER TO PURCHASE. SEE SECTION 11, WHICH SETS FORTH IN FULL THE CONDITIONS OF THE OFFER.

THE OFFER IS NOT CONDITIONED ON THE AVAILABILITY OF FINANCING OR THE APPROVAL OF THE BOARD OF DIRECTORS OF THE COMPANY.

IF MORE THAN 8,669,029 MAGAL SHARES IN THE AGGREGATE ARE VALIDLY TENDERED AND NOT PROPERLY WITHDRAWN, WE WILL PURCHASE A PRO RATA NUMBER OF MAGAL SHARES FROM ALL TENDERING SHAREHOLDERS, SO THAT WE

WOULD PURCHASE NO MORE THAN 8,669,029 MAGAL SHARES.

THE INITIAL PERIOD OF THE OFFER WILL EXPIRE AT 10:00 A.M., NEW YORK TIME ON JUNE 22, 2020, UNLESS THE INITIAL PERIOD OF THE OFFER IS EXTENDED. WE REFER TO THIS PERIOD, AS MAY BE EXTENDED, AS THE

INITIAL OFFER PERIOD. UPON THE TERMS AND SUBJECT TO THE CONDITIONS OF THE OFFER, IF PRIOR TO THE COMPLETION OF THE INITIAL OFFER PERIOD, ALL THE CONDITIONS OF THE OFFER ARE SATISFIED OR, SUBJECT TO APPLICABLE LAW, WAIVED BY US, WE WILL PROVIDE YOU

WITH AN ADDITIONAL FOUR CALENDAR-DAY PERIOD, UNTIL 10:00 A.M., NEW YORK TIME ON JUNE 26, 2020, DURING WHICH YOU MAY TENDER YOUR MAGAL SHARES. WE REFER TO THIS ADDITIONAL PERIOD AS THE ADDITIONAL OFFER PERIOD. THE EXPIRATION OF THE ADDITIONAL OFFER

PERIOD WILL CHANGE IF WE DECIDE TO EXTEND THE INITIAL OFFER PERIOD. SEE SECTION 1 AND SECTION 11.

The Magal Shares are listed on the Nasdaq Global Select Market, or Nasdaq, under the ticker symbol “MAGS”. On May 21, 2020, the last trading day before we announced our intention to commence the offer,

the closing sale price of the Magal Shares was $3.00 on Nasdaq. We encourage you to obtain current market quotations for the Magal Shares before deciding whether to tender your Magal Shares. See Section 6.

The Information Agent for the Offer is:

D.F. KING & CO., INC.

May 22, 2020

IMPORTANT

The offer is subject both to U.S. federal securities laws and the Israeli Companies Law, 5759-1999 (the “Israeli Companies Law”).

The offer has not been approved or disapproved by the Securities and Exchange Commission (“SEC”), any state securities commission, or the Israel Securities Authority (“ISA”), nor has the

SEC, any state securities commission or the ISA passed upon the fairness or merits of the offer or upon the accuracy or adequacy of the information contained in this offer to purchase. Any representation to the contrary is a criminal offense.

We have not authorized any person to make any recommendation on our behalf as to whether you should or should not tender your Magal Shares in the offer. You should rely

only on the information contained in this offer to purchase and the other related documents delivered to you or to which we have referred you. We have not authorized any person to give any information or to make any representation in connection

with the offer, other than those contained in this offer to purchase and the other related documents delivered to you or to which we have referred you. If anyone makes any recommendation or representation to you or gives you any information, you

must not rely on that recommendation, representation or information as having been authorized by us.

Holders of Magal Shares should tender their Magal Shares to American Stock Transfer & Trust Company LLC, the Depositary, pursuant to the applicable instructions in Section 3.

For the address and telephone number of our Depositary, see the back cover of this offer to purchase.

Upon the terms and subject to the conditions of the offer (including any terms and conditions of any extension or amendment), subject to proration, we will accept for payment and pay for the Magal

Shares that are validly tendered and not properly withdrawn prior to 10:00 a.m., New York time, on June 22, 2020, unless we extend the period of time during which the initial period of the offer is open. This period, as may be extended, is referred

to as the Initial Offer Period, and the date of completion of the Initial Offer Period is referred to as the Initial Completion Date. We will publicly announce in accordance with applicable law, and in any event issue a press release by 9:00 a.m.,

New York time, on the U.S. business day following the Initial Completion Date, stating whether or not the conditions of the offer have been satisfied or, subject to applicable law, waived by us. As required by Israeli law, if the conditions of the

offer are satisfied or, subject to applicable law, waived by us, then if, with respect to each Magal Share owned by you,

|

•

|

you have not yet responded to the offer,

|

|

•

|

you have notified us of your objection to the offer, or

|

|

•

|

you have validly tendered such Magal Share but have properly withdrawn your tender during the Initial Offer Period,

|

then you will be afforded an additional four calendar-day period, until 10:00 a.m., New York time, on June 26, 2020, during which you may tender each such Magal Share. We refer to this additional period as the Additional

Offer Period. The date of completion of the Additional Offer Period will change if we decide to extend the Initial Offer Period. Magal Shares tendered during the Initial Offer Period may be withdrawn at any time

prior to 10:00 a.m., New York time, on the Initial Completion Date, but not during the Additional Offer Period. See Section 1, Section 4 and Section 11.

Any questions and requests for assistance may be directed to D.F. King & Co., Inc., our Information Agent, at its address and telephone number set forth on

the back cover of this offer to purchase.

TABLE OF CONTENTS

|

SUMMARY TERM SHEET

|

1

|

|

INTRODUCTION

|

6

|

|

FORWARD-LOOKING STATEMENTS

|

8

|

|

BACKGROUND TO THE OFFER

|

9

|

|

Background

|

9

|

|

Purpose of the Offer; Reasons for the Offer

|

9

|

|

Plans for Magal after the Offer; Certain Effects of the Offer

|

10

|

|

Rights of Shareholders Who Do Not Accept the Offer

|

11

|

|

Interest of Persons in the Offer

|

11

|

|

Related Party Transactions

|

11

|

|

THE TENDER OFFER

|

12

|

|

1. TERMS OF THE OFFER; PRORATION; EXPIRATION DATE

|

12

|

|

2. ACCEPTANCE FOR PAYMENT AND PAYMENT

|

14

|

|

3. PROCEDURES FOR TENDERING SHARES OR NOTIFYING US OF YOUR OBJECTION TO THE OFFER

|

15

|

|

4. WITHDRAWAL RIGHTS

|

17

|

|

5. MATERIAL U.S. FEDERAL INCOME TAX AND ISRAELI INCOME TAX CONSEQUENCES

|

18

|

|

6. PRICE RANGE OF THE SHARES ETC.

|

22

|

|

7. EFFECTS OF THE OFFER ON THE MARKET FOR SHARES; REGISTRATION UNDER THE EXCHANGE ACT

|

23

|

|

8. INFORMATION CONCERNING MAGAL

|

24

|

|

9. INFORMATION CONCERNING THE BIDDER GROUP

|

25

|

|

10. SOURCES AND AMOUNT OF FUNDS

|

26

|

|

11. CONDITIONS OF THE OFFER

|

26

|

|

12. LEGAL MATTERS AND REGULATORY APPROVALS

|

28

|

|

13. FEES AND EXPENSES

|

28

|

|

14. MISCELLANEOUS

|

29

|

|

ANNEX A Excerpt of Section 331 of the Israeli Companies Law, 5759-1999

|

30

|

|

ANNEX B Definition of Israeli Resident for Israeli Tax Purposes

|

31

|

|

SCHEDULE I

|

32

|

i

Unless the context otherwise requires, all references in this offer to purchase to

“FIMI,” “us,” “we,” and “our” are to FIMI Opportunity V, L.P, a limited partnership organized under the laws of the State of Delaware and FIMI Israel Opportunity Five, Limited Partnership, a limited partnership organized under the laws of

the State of Israel, all references to “MAGAL” are to Magal Security Systems Ltd., all references to “Nasdaq” are to the Nasdaq Global Select Market, all references to “dollars” or “$” are to United States dollars, all references to “NIS”

are to New Israeli Shekels, and all references to the “Israeli Companies Law” are to the Israeli Companies Law 5759-1999, as amended.

Unless the context otherwise requires, the percentages of the issued and outstanding

Magal Shares and the percentages of the voting power of Magal stated throughout this offer to purchase are based on 23,153,985 shares issued and outstanding as of December 31, 2019 (based on the Annual Report on Form 20-F filed by Magal on

April 23, 2020).

Unless otherwise indicated or the context otherwise requires, for purposes of this offer

to purchase, a “U.S. business day” means any day other than a Saturday, Sunday, U.S. federal holiday or any other day on which the banks in the U.S. are permitted not to be open for business.

SUMMARY TERM SHEET

This summary term sheet is a brief summary of the material provisions of this offer to purchase 8,669,029 ordinary shares of Magal, par value NIS 1.0

per share (which we refer to as Magal Shares) being made by FIMI, and is meant to help you understand the offer. This summary term sheet is not meant to be a substitute for the information contained in the remainder of this offer to purchase,

and the information contained in this summary term sheet is qualified in its entirety by the fuller descriptions and explanations contained in the later pages of this offer to purchase. The following are some of the questions you, as a

shareholder of Magal, may have about us and the offer and answers to those questions. We recommend that you read carefully this entire offer to purchase, the Letter of Transmittal and other related documents delivered to you prior to making

any decision regarding whether to tender your shares.

WHO IS OFFERING TO BUY MY SECURITIES?

|

•

|

We, FIMI Opportunity V, L.P. and FIMI Israel Opportunity Five, Limited Partnership, are limited partnerships that are part of a group of private equity funds known as the FIMI Funds. The FIMI Funds

invest in companies that are predominantly located in Israel or that have significant ties or relations to Israel.

|

|

•

|

We are controlled by our general partner FIMI Five 2012 Ltd., a private company limited by shares, the managing general partner of FIMI, and an entity in a chain of ownership that leads up to Mr. Ishay

Davidi, the founder of the FIMI Funds. This chain of entities consists, in addition to FIMI Five 2012 Ltd., of Shira & Ishay Davidi Management Ltd. See Section 9. Because FIMI

Five 2012 Ltd., Shira & Ishay Davidi Management Ltd. and Ishay Davidi control us and helped to structure our offer, our offer may be deemed to be made on behalf of these

controlling persons, and in this offer to purchase we refer to them and us collectively as our “bidder group.”

|

HOW MANY SHARES ARE SOUGHT IN THIS OFFER?

|

•

|

Subject to certain conditions, we are offering to purchase 8,669,029 Magal Shares, representing approximately 37.4% of the issued and outstanding Magal Shares and of the voting power of Magal. See

Section 1.

|

|

•

|

If more than 8,669,029 shares are validly tendered and not properly withdrawn, we will purchase 8,669,029 shares on a pro rata basis from all shareholders who have validly tendered their shares in the

Initial Offer Period and the Additional Offer Period and have not properly withdrawn their shares before the completion of the Initial Offer Period. The number of shares that we will purchase from each tendering shareholder will be

based on the total number of shares validly tendered by all shareholders in the Initial Offer Period and the Additional Offer Period and not properly withdrawn before the completion of the Initial Offer Period. You may only withdraw

previously tendered shares prior to the completion of the Initial Offer Period. See Section 1 and Section 4.

|

|

•

|

If less than 8,669,029 shares are validly tendered, but at least 1,200,000 shares are validly tendered and not properly withdrawn, we will purchase shares from all shareholders who have validly tendered

their shares in the Initial Offer Period and the Additional Offer Period and have not properly withdrawn their shares before the completion of the Initial Offer Period. You may only withdraw previously tendered shares prior to the

completion of the Initial Offer Period. See Section 1 and Section 4.

|

1

WHY ARE YOU CONDUCTING THIS OFFER?

We are conducting the offer to increase our interest in Magal because we believe in the long-term value and prospects of Magal and in order to comply with the requirements of Israeli law. Under

Israeli law, a purchase of shares of a public company may not be made other than by way of a “special tender offer” meeting certain requirements if, among other things, as a result of the purchase, the purchaser would own or would be deemed to

beneficially own more than 45.0% of the aggregate voting power of the company and no other person owns more than 45.0% of the aggregate voting power of the company. As of May 21, 2020 we beneficially held 9,854,159 Magal Shares, representing

approximately 42.6% of the issued and outstanding Magal Shares. Accordingly, in order for us to purchase additional Magal Shares that would increase our voting power in Magal to more than 45.0%, we are required to conduct the offer as a

“special tender offer” meeting the requirements of Israeli law. See “Background to the Offer – Background” and “Background to the Offer – Purpose of the Offer; Reasons for the Offer.”

HOW MUCH ARE YOU OFFERING TO PAY AND WHAT IS THE FORM OF PAYMENT?

|

•

|

We are offering to pay $2.95 per Magal Share, net to you (subject to withholding taxes, as applicable), in cash, without interest. All shareholders tendering their Magal Shares in the offer will be paid

solely in United States dollars. See “Introduction”, Section 1 and Section 2, and, with respect to withholding taxes, Section 5.

|

WHAT PERCENTAGE OF THE MAGAL SHARES DO YOU CURRENTLY OWN AND HOW MUCH WILL YOU OWN IF THE OFFER IS COMPLETED?

|

•

|

We currently beneficially own 9,854,159 Magal Shares, representing approximately 42.6% of the issued and outstanding Magal Shares.

|

|

•

|

Following the consummation of the offer, (i) if we purchase the maximum number of shares we offer to purchase hereunder, we will beneficially own 18,523,188 Magal Shares, representing approximately 80.0%

of the issued and outstanding Magal Shares, and (ii) if we purchase the minimum number of shares we offer to purchase hereunder, we will beneficially own 11,054,159 Magal Shares, representing approximately 47.8% of the issued and

outstanding Magal Shares.

|

See “Introduction” and Section 11.

WHAT IS THE MARKET VALUE OF MY MAGAL SHARES AS OF A RECENT DATE?

|

•

|

On May 21, 2020, the last trading day before we announced our intention to commence the offer, the closing sale price of the Magal Shares on Nasdaq was $3.00. The price we are offering to pay is less than

the closing price of Magal Shares on Nasdaq on May 21, 2020. We recommend that you obtain a recent quotation for your Magal Shares prior to deciding whether or not to tender your Magal Shares. See Section 6.

|

DO YOU HAVE THE FINANCIAL RESOURCES TO PAY THE PURCHASE PRICE IN THE OFFER?

|

•

|

Yes. We possess all of the necessary funds to consummate the offer from cash on hand. The offer is not conditioned on the availability of financing.

|

IS YOUR FINANCIAL CONDITION RELEVANT TO MY DECISION ON WHETHER TO TENDER IN THE OFFER?

|

•

|

We do not believe that our financial statements are material to your decision whether to tender Magal Shares and accept the offer because: (i) the offer consideration consists solely of cash; (ii) the

offer is not subject to any financing condition; and (iii) we are already a controlling shareholder of Magal. While we do not believe that our financial condition is material to the decision of a holder of Magal Shares whether to

tender Magal Shares and accept the offer, certain selected financial information of FIMI is provided in Section 10.

|

CAN I OBJECT TO THE OFFER?

|

•

|

Yes. Pursuant to Israeli law, you may object to the offer. If you want to notify us of your objection to the offer you must complete and sign the accompanying Notice of Objection and deliver it prior to

the completion of the Initial Offer Period on June 22, 2020 (as may be extended) by following the applicable procedures and instructions described in Section 3. Under Israeli law, since following the consummation of the offer we will

be beneficial owners of more than 45.0% of the voting power of Magal, the aggregate number of Magal Shares validly tendered pursuant to the offer and not properly withdrawn at the completion of the Initial Offer Period must exceed the

aggregate number of Magal Shares represented by Notices of Objection to the offer. This is one of the conditions of the offer, and if it is not met, we will be prohibited from purchasing any Magal Shares tendered pursuant to the

offer.

|

2

See the answer to the question “What are the most significant conditions of the offer?” below, “Background to the Offer – Rights of Shareholders Who Do Not Accept the Offer,”

Section 3 and Section 11.

WHAT ARE THE MOST SIGNIFICANT CONDITIONS OF THE OFFER?

|

•

|

At least 1,200,000 Magal Shares (currently representing 5.2% of the issued and outstanding shares and voting power of Magal), must be validly tendered and not properly withdrawn prior to the completion

of the Initial Offer Period;

|

|

•

|

At the completion of the Initial Offer Period, the aggregate number of Magal Shares validly tendered pursuant to the offer and not properly withdrawn (excluding Magal Shares held by us or our affiliates -

see “Rights of Shareholders Who Do Not Accept the Offer”) must be greater than the aggregate number of Magal Shares represented by Notices of Objection to the offer; and

|

|

•

|

The Competition Authority of the State of Israel shall have approved the purchase of the Magal Shares pursuant to this offer.

|

The offer is not conditioned on the availability of financing or the approval of the board of directors of Magal.

See “Background to the Offer – Rights of Shareholders Who Do Not Accept the Offer” and Section 11, which sets forth in full the conditions of the offer and describes those conditions of the offer

that may be waived by us.

WHAT WILL HAPPEN IF THE CONDITIONS OF THE OFFER ARE NOT SATISFIED?

|

•

|

If any condition is not satisfied, we may elect not to purchase, or may be prohibited from purchasing, any Magal Shares tendered pursuant to the offer, or, subject to applicable law, we may waive such

conditions. See “Introduction”, Section 1 and Section 11.

|

HOW LONG DO I HAVE TO DECIDE WHETHER TO ACCEPT THE OFFER AND TENDER MY SHARES?

|

•

|

You may tender your Magal Shares until 10:00 a.m., New York time, on June 22, 2020 (as may be extended). We refer to this period, as may be extended, as the Initial Offer Period, and the date of

completion of the Initial Offer Period is referred to as the Initial Completion Date.

|

|

•

|

We will publicly announce in accordance with applicable law, and in any event issue a press release by 9:00 a.m., New York time, on the U.S. business day following the Initial Completion Date, stating

whether or not the conditions of the offer have been satisfied or, subject to applicable law, waived by us. As required by Israeli law, if the conditions of the offer are satisfied or, subject to applicable law, waived by us, then if,

with respect to each Magal Share owned by you,

|

|

•

|

you have not yet responded to the offer,

|

|

•

|

you have notified us of your objection to the offer, or

|

|

•

|

you have validly tendered such Magal Share but have properly withdrawn your tender during the Initial Offer Period,

|

you will be afforded an additional four calendar-day period following the Initial Completion Date, until 10:00 a.m., New York time, on June 26, 2020, during which you may

tender each such Magal Share. We refer to this additional period as the Additional Offer Period and the date of expiration of the Additional Offer Period is referred to as the Final Expiration Date. The Final Expiration Date will change if we

decide to extend the Initial Offer Period.

See “Introduction,” Section 1, Section 3 and Section 11.

3

HOW DO I TENDER MY MAGAL SHARES AND TO WHICH DEPOSITARY SHOULD I TENDER?

|

•

|

All holders of Magal Shares should tender their Magal Shares to the Depositary by following the applicable procedures and instructions described in Section 3.

|

CAN I TENDER MY MAGAL SHARES USING A GUARANTEED DELIVERY PROCEDURE?

|

•

|

No. You may only tender your Magal Shares by following the applicable procedures and instructions described in Section 3.

|

WHEN CAN I WITHDRAW THE MAGAL SHARES I TENDERED PURSUANT TO THE OFFER?

|

•

|

You may withdraw any previously tendered Magal Shares at any time prior to the completion of the Initial Offer Period, but not during the Additional Offer Period. In addition, under U.S. law, tendered

Magal Shares may be withdrawn at any time after 60 days from the date of the commencement of the offer if the Magal Shares have not yet been accepted for payment by us. See Section 1 and Section 4.

|

WHEN WILL YOU PAY FOR THE MAGAL SHARES TENDERED IN THE OFFER?

|

•

|

All of the Magal Shares validly tendered pursuant to the offer and not properly withdrawn will be paid for following the Final Expiration Date, subject to proration. We expect to make such payment,

including in the event that proration of tendered Magal Shares is required, within four U.S. business days following the Final Expiration Date. See Section 1, Section 2 and Section 11.

|

CAN THE OFFER BE EXTENDED, AND UNDER WHAT CIRCUMSTANCES?

|

•

|

We have the right, in our sole discretion, to extend the Initial Offer Period, subject to applicable law. In addition, in certain circumstances, we may be required by law to extend the Initial Offer

Period. See Section 1.

|

HOW WILL I BE NOTIFIED IF THE OFFER IS EXTENDED?

|

•

|

If we decide to extend the Initial Offer Period, we will inform the Depositary and the Information Agent of that fact. We will also publicly announce the new Initial Completion Date in accordance with

applicable law, and in any event issue a press release to this effect no later than 9:00 a.m., New York time, on the first U.S. business day following the day on which we decide to extend the Initial Offer Period. See Section 1.

|

HAS MAGAL OR ITS BOARD OF DIRECTORS ADOPTED A POSITION ON THE OFFER?

|

•

|

Under applicable U.S. law, no later than ten U.S. business days from the date of this offer to purchase, Magal is required to publish, send or give to you a statement disclosing that it either recommends

acceptance or rejection of the offer, expresses no opinion and remains neutral toward the offer, or is unable to take a position with respect to the offer.

|

|

•

|

Under Israeli law, Magal’s board of directors is required to express its opinion to the shareholders on the advisability of the offer. Magal’s board of directors may refrain from expressing an opinion if

it cannot do so, as long as it gives the reasons for not providing an opinion.

|

As of the date of this offer to purchase, Magal’s board of directors has not made any recommendation regarding acceptance or rejection of the offer or expressed an opinion

regarding the advisability of the offer.

ARE THERE ANY CONFLICTS OF INTEREST IN THE OFFER?

Yes.

|

•

|

FIMI’s beneficial ownership of approximately 42.6% of the issued and outstanding Magal Shares as of May 21, 2020 is deemed to exert control over Magal.

|

|

•

|

FIMI has invested, and in the future may invest, in other companies that operate in the same industry as, and may compete with, Magal.

|

4

|

•

|

Gillon Beck, a senior partner in FIMI, serves as a director and an Executive Chairman of Magal’s board of directors. Gillon Beck is also a member of the board of directors of FIMI Five 2012 Ltd. Ron

Ben-Haim, a partner in FIMI, is also a member of Magal’s board of directors. Messrs. Beck and Ben-Haim do not control FIMI.

|

See “Background to the Offer – Purpose of the Offer; Reasons for the Offer” and “Background to the Offer – Interest of Persons in the Offer”.

WHAT ARE THE TAX CONSEQUENCES OF THE OFFER?

|

•

|

The receipt of cash for Magal Shares accepted for payment by us from tendering shareholders who are “United States persons” for United States federal income tax purposes will be treated as a taxable

transaction for United States federal income tax purposes.

|

|

•

|

The receipt of cash for Magal Shares accepted for payment by us from tendering shareholders generally will be a taxable transaction for Israeli income tax purposes for both Israeli residents and non-Israeli

residents, unless a specific exemption is available or a tax treaty between Israel and the shareholder’s country of residence provides otherwise.

|

|

•

|

We have obtained an approval from the Israeli Tax Authority with respect to the Israeli withholding tax rates applicable to shareholders as a result of the sale of Magal Shares pursuant to the offer. The

approval provides, among other things, that (1) tendering shareholders who acquired their Magal Shares after Magal’s initial public offering on Nasdaq in 1993 and who certify that they are not, and at the date of purchase of their

Shares were not Israeli residents (and, in the case of a corporation, that no Israeli residents (x) hold 25.0% or more of the means to control such corporation or (y) are the beneficiaries of, or are entitled to, 25.0% or more of the

revenues or profits of such corporation, whether directly or indirectly), will not be subject to Israeli withholding tax, and (2) payments to be made to tendering shareholders who acquired their Magal Shares after Magal’s initial public

offering on Nasdaq in 1993 and who hold their Magal Shares through an Israeli broker or Israeli financial institution will be made by us without any Israeli withholding at source, and the relevant Israeli broker or Israeli financial

institution will withhold Israeli tax, if any, as required by Israeli law. The approval does not address shareholders who are not described in clauses (1) and (2) above, and therefore they will be subject to Israeli withholding tax at

the applicable rate of the gross proceeds payable to them pursuant to the offer as prescribed by Israeli tax law.

|

|

•

|

We recommend that you seek professional advice from your own advisors concerning the tax consequences applicable to your particular situation. See Section 5.

|

WILL THE OFFER RESULT IN THE DELISTING OF THE MAGAL SHARES?

|

•

|

No. Magal Shares will continue to trade on Nasdaq following completion of the offer. See Section 7.

|

WITH WHOM MAY I TALK IF I HAVE QUESTIONS ABOUT THE OFFER?

|

•

|

You can call D.F. King & Co., Inc., our Information Agent in the United States, at (212) 269-5550 (banks and brokers) or Toll Free at (800) 814-2879, during its normal business hours. See the back

cover of this offer to purchase.

|

5

INTRODUCTION

We, FIMI Opportunity V, L.P, a limited partnership organized under the laws of the State of Delaware and FIMI Israel Opportunity Five, Limited Partnership, a limited partnership organized under the

laws of the State of Israel (collectively, “FIMI”), hereby offer to purchase 8,669,029 ordinary shares, par value NIS 1.0 per share, of Magal Security Systems Ltd., or Magal Shares, at a price of $2.95 per share, net to you (subject to

withholding taxes, as applicable), in cash, without interest. The offer is subject to the terms and conditions set forth in this offer to purchase, the Letter of Transmittal and the other related documents delivered to you.

Magal Shares are listed on the Nasdaq Global Select Market, or Nasdaq, under the ticker symbol “MAGS”. Based on the Annual Report on Form 20-F filed by Magal on April 23, 2020, as of December 31, 2019,

there was a total of 23,153,985 Magal Shares issued and outstanding. As of the date of this offer to purchase, we beneficially own 9,854,159 Magal Shares, representing approximately 42.6% of the issued and outstanding Magal Shares. As a result, (i)

if we purchase the maximum amount of Magal Shares we offer to purchase hereunder, we would beneficially own 18,523,188 Magal Shares, representing approximately 80.0% of the issued and outstanding Magal Shares, and (ii) if we purchase the minimum

amount of Magal Shares we offer to purchase hereunder, we would beneficially own 11,054,159 Magal Shares, representing approximately 47.8% of the issued and outstanding Magal Shares.

FIMI is part of a group of private equity funds known as the FIMI Funds. The FIMI Funds invest in companies that are predominantly located in Israel or that have significant ties or relations to Israel.

We are controlled by our general partner, FIMI Five 2012 Ltd., and an entity in a chain of ownership that leads up to Ishay Davidi, the founder of the FIMI Funds. This entity is Shira & Ishay Davidi Management Ltd. Because FIMI Five 2012 Ltd., Shira & Ishay Davidi Management Ltd. and Ishay Davidi control us and helped

structure our offer, our offer may be deemed to be made on behalf of these controlling persons, and in this offer to purchase we refer to them and us collectively as our “bidder group.”

Gillon Beck, a senior partner in FIMI, serves as a director and an Executive Chairman of Magal’s board of directors. Gillon Beck is also a member of the board of directors of FIMI Five 2012 Ltd. Ron

Ben-Haim, a partner in FIMI, is also a member of Magal’s board of directors. Messrs. Beck and Ben-Haim do not control FIMI.

The initial period of the offer will be completed at 10:00 a.m., New York time, on June 22, 2020. We refer to this period, as may be extended, as the Initial Offer Period, and the date of completion of

the Initial Offer Period is referred to as the Initial Completion Date. We will publicly announce in accordance with applicable law, and in any event issue a press release by 9:00 a.m., New York time, on the U.S. business day following the Initial

Completion Date, stating whether or not the conditions of the offer have been satisfied or, subject to applicable law, waived by us. As required by Israeli law, if the conditions of the offer have been satisfied or, subject to applicable law, waived

by us, then if, with respect to each Magal Share owned by you, (a) you have not yet responded to the offer, (b) you have notified us of your objection to the offer, or (c) you have validly tendered such Magal Share but have properly withdrawn your

tender during the Initial Offer Period, then you will be afforded an additional four calendar-day period, until 10:00 a.m., New York time, on June 26, 2020, during which you may tender each such Magal Share. We refer to this additional period as the

Additional Offer Period and the date of expiration of the Additional Offer Period is referred to as the Final Expiration Date. The Final Expiration Date will change if we decide to extend the Initial Offer Period.

We have applied to the SEC for exemptive relief from Rule 14d-7(a) to provide for the four-day additional offering

period without withdrawal rights, and no-action relief by the staff of the SEC from Rule 14e-1(c) to permit payment within four U.S. business days following the Final Expiration Date.

If you are a record owner of Magal Shares and tender directly to American Stock Transfer & Trust Company LLC, the Depositary, you generally will not be obligated to pay brokerage fees or

commissions, service fees or commissions or, except as set forth in the Letter of Transmittal, share transfer taxes with respect to the sale of your Magal Shares in the offer. If you hold your Magal Shares through a bank or broker, we recommend that

you check whether they charge any service or other fees.

We will pay the fees and expenses of the Depositary in connection with the offer. The Depositary will act as agent for tendering shareholders for the purpose of receiving payment from us and

transmitting payments to tendering shareholders whose Magal Shares are accepted for payment. We will also pay the fees and expenses of D.F. King & Co., Inc., our Information Agent, who will facilitate and answer questions concerning the offer

during their respective normal business hours.

6

The offer is conditioned on at least 1,200,000 Magal Shares (currently representing 5.2% of the issued and outstanding shares and voting power of Magal), being validly tendered and not properly

withdrawn, and we may terminate the offer if the total number of Magal Shares validly tendered and not properly withdrawn prior to 10:00 a.m., New York time, on the Initial Completion Date is less than 1,200,000. Certain other conditions to the

consummation of the offer are described in Section 11. We reserve the right (subject to applicable law and the rules of the United States Securities and Exchange Commission, or the SEC) to amend or, other than the conditions set forth in clause (a)

and clauses (c) and (d) of Section 11, waive any one or more of the terms and conditions of the offer. However, if any of these conditions is not satisfied, we may elect not to purchase, or may be prohibited from purchasing any Magal Shares tendered

pursuant to the offer. The offer is not conditioned on the availability of financing or the approval of the board of directors of Magal. See Section 1, Section 10 and Section 11.

Under applicable U.S. law, no later than ten U.S. business days from the date of this offer to purchase, Magal is required to publish, send or give to you a statement

disclosing that it either recommends acceptance or rejection of the offer, expresses no opinion and remains neutral toward the offer, or is unable to take a position with respect to the offer. Under Israeli law, Magal’s board of directors is

required to express its opinion to the shareholders on the advisability of the offer. Magal’s board of directors may refrain from expressing an opinion if it cannot do so, as long as it gives the reasons for not providing an opinion. As of the date

of this offer to purchase Magal’s board of directors has not made such a statement. Mr. Beck and Mr. Ben-Haim intend to abstain from voting on the offer in their capacities as directors of Magal, because their interests with regard to the offer as

directors of Magal may be deemed to conflict with their interests with regard to the offer as executive officers of FIMI.

This offer to purchase, the Letter of Transmittal and the other related documents delivered to you contain important information which should be read carefully before any decision is made with respect

to the offer.

7

FORWARD-LOOKING STATEMENTS

This offer to purchase, the Letter of Transmittal and the other related documents delivered to you and/or incorporated by reference herein include “forward-looking statements” that are not purely historical

regarding our intentions, hopes, beliefs, expectations and strategies for the future, including, without limitation:

|

•

|

statements regarding the public float of Magal Shares following consummation of the offer;

|

|

•

|

statements regarding whether the Magal Shares will continue to be “margin securities” following consummation of the offer;

|

|

•

|

statements regarding whether the Magal Shares will continue to be traded on Nasdaq or registered under the United States Securities Exchange Act of 1934, as amended, following consummation of the offer;

|

|

•

|

statements regarding the plans, objectives or expectations regarding the future operations or status of us or Magal; and

|

|

•

|

any statement of assumptions underlying any of the foregoing.

|

Forward-looking statements that are based on various assumptions (some of which are beyond our control) may be identified by the use of forward-looking terminology, such as “may,” “can be,” “will,” “expects,”

“anticipates,” “intends,” “believes,” “believe in the value,” and similar words and phrases. Such forward-looking statements are inherently subject to known and unknown risks and uncertainties. Actual results could differ materially from those set

forth in forward-looking statements due to a variety of factors, including, but not limited to:

|

•

|

changes in domestic and foreign economic and market conditions;

|

|

•

|

changes in the ownership of Magal Shares, particularly any substantial accumulations by persons who are not affiliated with us;

|

|

•

|

uncertainty as to the completion of the offer; and

|

|

•

|

the risk factors detailed in Magal’s most recent annual report on Form 20-F and its other filings with the SEC.

|

See Section 9 of this offer to purchase for a discussion of certain information relating to us. Except as may be required by law, we do not undertake, and specifically disclaim, any obligation to publicly release

the results of any revisions which may be made to any forward-looking statements to reflect the occurrence of anticipated or unanticipated events or circumstances after the date of such forward-looking statements.

You should assume that the information appearing in this offer to purchase is accurate as of the date on the front cover of this offer to purchase only.

8

BACKGROUND TO THE OFFER

Background

We originally made an investment in Magal on October 1, 2014 by purchasing a total of 6,461,290 Magal Shares from Ki Corporation.

On September 30, 2016, we purchased 3,392,869 additional Magal Shares, pursuant to a rights offering initiated by Magal on September 7, 2016.

In the ordinary course of our business, we from time to time review the performance of our investments and consider possible strategies for enhancing value. As part of our ongoing review of our investment in

Magal, we explore, from time to time, the possibilities of acquiring additional Magal Shares.

In March 2020, Mr. Davidi, Mr. Beck and Mr. Ben-Haim, together with other members of our management, began considering the possibility of purchasing additional Magal Shares. In connection therewith, we conducted

an analysis of the legal requirements relating to the purchase of Magal Shares and the tender offer requirements. The analysis was made with the assistance of Israeli and U.S. legal counsel.

Under Israeli law, a purchase of the shares of a public company may not be made other than by way of a “special tender offer” meeting certain requirements, if, among other things, as a result of the

purchase, the purchaser would own or would be deemed to own more than 45.0% of the aggregate voting power of the company and no other person owns more than 45.0% of the voting power.

Accordingly, due to the fact that under Israeli law we are obligated to initiate a “special tender offer” in order to own more than 45% of Magal’s issued and outstanding share capital, we decided to

initiate a public “special tender offer” pursuant to Israeli law, to acquire a minimum of 1,200,000 and up to 8,669,029 Magal Shares at a price of $2.95 per Magal Share.

In addition, we, with the assistance of Israeli and U.S. legal counsel, applied to the SEC for relief from certain provisions of the U.S. securities laws to enable us to structure a tender offer that would comply

with applicable law and regulations in both the U.S. and Israel. We have requested from the Israeli Tax Authority, or the ITA, an approval with respect to the Israeli withholding tax rates applicable to the offer.

On May 21, 2020, we received

the exemptive relief and no-action relief that we requested from the SEC.

On May 18, 2020, we received from the ITA an approval with respect to the Israeli withholding tax rates applicable to sales of shares pursuant to the offer.

Purpose of the Offer; Reasons for the Offer

Our bidder group’s purpose for the offer is for FIMI to increase its beneficial ownership of the issued and outstanding Magal Shares from its current level of approximately 42.6% up to approximately 80.0%. This

is because each member of our bidder group believes in the long-term value and prospects of Magal. Although not required under the federal securities laws, we are conducting the offer in order to comply with the requirements of Israeli law. According

to Israeli law, we are not permitted to acquire additional Magal Shares if such acquisition would result in our percentage ownership of the voting power of Magal exceeding 45.0%, other than by means of a special tender offer.

Plans for Magal after the Offer; Certain Effects of the Offer

Except as otherwise described below or elsewhere in this offer to purchase, none of the members of our bidder group, and to the best of our knowledge none of the other persons listed in Schedule I to this

offer to purchase, has any current plans, proposals or negotiations that relate to or would result in the following:

|

•

|

an extraordinary corporate transaction, merger, reorganization or liquidation involving Magal or any of its subsidiaries;

|

9

|

•

|

a purchase, sale or transfer of a material amount of the assets of Magal or any of its subsidiaries;

|

|

•

|

any change in the present board of directors and management of Magal (including any plan or proposal to change the number or term of directors or to fill any existing vacancy on the board or to change any

material term of the employment contract of any executive officer);

|

|

•

|

any other material change in Magal’s corporate structure or business;

|

|

•

|

a delisting of the Magal Shares from Nasdaq; or

|

|

•

|

the Magal Shares becoming eligible for termination of registration under the United States Securities Exchange Act of 1934, as amended, or the Exchange Act.

|

We expect that from time to time there may be significant developments or transactions involving our portfolio companies (including Magal) or their securities, or offers, proposals or discussions related thereto,

which may involve acquisitions or sales by us of our holdings in such entities (including Magal) or acquisitions or sales of securities, assets or business operations by such entities.

We intend to review our investment in Magal, its performance and market conditions periodically and consider possible

strategies for enhancing value and take such actions with respect to our investment as we deem appropriate in light of the circumstances existing from time to time. Such actions could include, among other things, additional purchases of

Magal Shares pursuant to one or more open-market purchase programs, through private transactions or through tender offers or otherwise, subject to applicable U.S. and Israeli law. Future purchases may be on the same terms or on terms that are more or

less favorable to Magal’s shareholders than the terms of the offer. Any possible future purchases will depend on many factors, including the results of the offer, the market price of Magal Shares, our business and financial position, and general

economic and market conditions. In addition, following the consummation of the offer, we may also determine to dispose of our Magal Shares, in whole or in part, at any time and from time to time, subject to applicable laws. Any such decision would be

based on our assessment of a number of different factors, including, without limitation, the business, prospects and affairs of Magal, the market for the Magal Shares, the condition of the securities markets, general economic and industry conditions

and other opportunities available to us.

We may exercise our controlling influence in Magal to cause Magal to change its current dividend policy and declare a distribution of dividends to Magal’s shareholders,

from time to time, subject to the requirements and limitations set forth in the Israeli Companies Law.

Under Israeli law, if a shareholder owns or is deemed to beneficially own in excess of 45.0% of the voting power of a company, such shareholder may purchase shares in the open market or through private

transactions, and not solely by means of a tender offer, provided such shareholder does not beneficially own more than 90% of the voting power of such company. Accordingly, following the consummation of the offer, we may purchase Magal Shares in the

open market or through private transactions, and not solely by means of a tender offer, subject to the applicable laws.

However, under Israeli law, if the offer is accepted, we, our controlling shareholders and any company under our or their control, are prohibited from conducting an additional tender

offer for Magal Shares and from merging with Magal within 12 months after the date of this offer to purchase.

Rights of Shareholders Who Do Not Accept the Offer

You will have no appraisal or similar rights with respect to the offer. Under Section 331 of the Israeli Companies Law, you may respond to the offer by accepting the offer or notifying us of your

objection to the offer. Alternatively, you may simply not respond to the offer and not tender your Magal Shares. It is a condition to the offer that, at the completion of the Initial Offer Period, the aggregate number of Magal Shares validly tendered

pursuant to the offer and not properly withdrawn is greater than the aggregate number of Magal Shares represented by Notices of Objection. As required by Section 331(c) of the Israeli Companies Law, in making this calculation, the votes of a holder

of a controlling interest in the offeror, a holder who has a personal interest in the acceptance of the special tender offer, a holder of a control block in the company, or any person acting on their behalf or on behalf of the offeror, including

their relatives and companies under their control, shall not be taken into account.

An excerpt of Section 331 of the Israeli Companies Law is attached as Annex A.

10

Please see Section 3 for instructions on how to notify us of your objection to the offer.

Interests of Persons in the Offer

Gillon Beck, a senior partner in FIMI, serves as a director and an Executive Chairman of Magal’s board of directors. Gillon Beck is also a member of the board of directors of FIMI Five 2012 Ltd. Ron

Ben-Haim, a partner in FIMI is also a member of Magal’s board of directors. Messrs. Beck and Ben-Haim do not control FIMI.

Related Party Transactions

On September 30, 2016, we purchased 3,392,869 Magal Shares, pursuant to a rights offering initiated by Magal on September 7, 2016, including through an exercise of over-subscription rights for a total

subscription price of $13,096,478.20.

Except as set forth in this offer to purchase, none of the members of our bidder group, nor any of the other persons listed in Schedule I to this offer to purchase, have had any transaction during the

past two years with Magal or any of its executive officers, directors or affiliates that is required to be described in this offer to purchase under applicable law. Except as set forth in this offer to purchase, there have been no negotiations,

transactions or material contacts during the past two years between any of the members of our bidder group, or any of the other persons listed in Schedule I to this offer to purchase, on the one hand, and Magal and its affiliates, on the

other hand, concerning a merger, consolidation or acquisition, tender offer, exchange offer or other acquisitions of Magal’s securities, an election of Magal’s directors or a sale or other transfer of a material amount of the assets of Magal.

11

THE TENDER OFFER

YOU SHOULD READ THIS OFFER TO PURCHASE, THE LETTER OF TRANSMITTAL AND THE OTHER RELATED DOCUMENTS DELIVERED TO YOU CAREFULLY BEFORE YOU MAKE ANY DECISION WITH RESPECT TO THE OFFER.

1. TERMS OF THE OFFER; PRORATION; EXPIRATION DATE.

The offer is being made to all of Magal’s shareholders. Upon the terms and subject to the conditions of the offer (including any terms and conditions of any extension or amendment), subject to

proration, we will accept for payment and pay for Magal Shares, that are validly tendered and not properly withdrawn in accordance with Section 4 prior to 10:00 a.m., New York time, on June 22, 2020, unless we extend the period of time during which

the initial period of the offer is open. We refer to this period, as may be extended (as described below), as the Initial Offer Period, and the date of completion of the Initial Offer Period is referred to as the Initial Completion Date.

We will publicly announce in accordance with applicable law, and in any event issue a press release by 9:00 a.m., New York time, on the U.S. business day following the Initial Completion Date, stating whether

or not the conditions of the offer have been satisfied or, subject to applicable law, waived by us. Under Israeli law, if the conditions of the offer have been satisfied or, subject to applicable law, waived by us, then the shareholders who have,

with respect to each Magal Share owned by them,

|

•

|

not responded to the offer,

|

|

•

|

notified us of their objection to the offer, or

|

|

•

|

validly tendered such Magal Share but have properly withdrawn their tender during the Initial Offer Period,

|

will be entitled to tender each such Magal Share during an additional four calendar-day period commencing at the completion of the Initial Offer Period. We refer to this period as the Additional Offer Period and to the

expiration of such period as the Final Expiration Date. Shares tendered during the Initial Offer Period may be withdrawn at any time prior to 10:00 a.m., New York time, on the Initial Completion Date, but not during

the Additional Offer Period. In this respect, we recommend that you read Section 4 and Section 11 of this offer to purchase.

Subject to proration, we will also accept for payment and pay for all Magal Shares validly tendered and not properly withdrawn in accordance with Section 4 prior to 10:00 a.m., New York time, on the Final

Expiration Date. We expect to make such payment, including in the event that proration of tendered Magal Shares is required, within four U.S. business days following the Final Expiration Date.

No fractional Magal Shares will be purchased by us in the offer.

Conditions of the offer include, among other things, that:

|

•

|

prior to 10:00 a.m., New York time, on the Initial Completion Date, there shall have been validly tendered and not properly withdrawn at least 8,669,029 Magal Shares (currently representing 5.2% of the issued

and outstanding shares and voting power of Magal);

|

|

•

|

as required by Israeli law, at 10:00 a.m., New York time, on the Initial Completion Date, the aggregate number of Magal Shares validly tendered pursuant to the offer and not properly withdrawn (excluding the

Magal Shares held by us or our affiliates – see “Rights of Shareholders Who Do Not Accept the Offer”) is greater than the aggregate number of Magal Shares represented by Notices of Objection to the

offer; and

|

|

•

|

The Israel Competition Authority shall have approved the purchase of the Magal Shares pursuant to this offer.

|

The offer is also subject to certain other conditions set forth in Section 11. If any of these conditions is not satisfied, we may elect not to purchase, or may be prohibited from purchasing, any

Magal Shares tendered pursuant to the offer. The offer is not conditioned on the availability of financing or the approval of the board of directors of Magal. See Section 11, which sets forth in full the conditions of the offer and specifies those

conditions of the offer that are waivable by us.

If more than 8,669,029 Magal Shares are validly tendered and not properly withdrawn prior to 10:00 a.m., New York time, on the Final Expiration Date, we will purchase 8,669,029 Magal Shares on a pro rata basis

from all tendering shareholders who have validly tendered their shares in the Initial Offer Period and the Additional Offer Period and have not properly withdrawn their shares before the completion of the Initial Offer Period. The number of Magal

Shares that we will purchase from each tendering shareholder will be based on the total number of Magal Shares validly tendered by all shareholders prior to 10:00 a.m., New York time, on the Final Expiration Date and not properly withdrawn before the

completion of the Initial Offer Period. The proration factor, if any, will be calculated by dividing (x) 8,669,029 Magal Shares, the number of Magal Shares that we are offering to purchase, by (y) the aggregate number of Magal Shares validly tendered

pursuant to the offer and not properly withdrawn.

12

We will publicly announce in accordance with applicable law and in any event issue a press release by 9:00 a.m., New York time, on the U.S. business day following the Initial Completion Date, stating whether the

conditions of the offer have been satisfied or, subject to applicable law, waived by us. Promptly following the Final Expiration Date, we will announce the results of the offer and the proration factor, if any. If we are unable to promptly determine

the proration factor, we will announce the preliminary results. We will pay for all Magal Shares accepted for payment pursuant to the offer promptly following the calculation of the proration factor. We expect to make such payment within four U.S.

business days following the Final Expiration Date.

Under Israeli law, once we announce, following the completion of the Initial Offer Period, that the offer has been accepted, or, in other words, that all the conditions of the offer have been satisfied or,

subject to applicable law, waived by us, no further conditions of the offer would apply and we will become irrevocably bound to purchase the Magal Shares validly tendered pursuant to the offer and not properly withdrawn prior to 10:00 a.m., New York

time, on the Final Expiration Date (subject to proration, if any).

Subject to applicable laws and regulations, if any condition has not been satisfied as of the Initial Completion Date, we may decide to:

|

•

|

extend the Initial Offer Period and, subject to applicable withdrawal rights until the Initial Completion Date, retain all tendered Magal Shares until the Final Expiration Date;

|

|

•

|

if the only conditions that have not been satisfied are one or more of the conditions set forth in clause (b) of Section 11, waive such condition(s) and, subject to proration, accept for payment and pay for all

Magal Shares validly tendered and not properly withdrawn prior to 10:00 a.m., New York time, on the Final Expiration Date by no later than four business days following the Final Expiration Date; or

|

|

•

|

terminate the offer and not accept for payment or pay for any Magal Shares and promptly return all tendered Magal Shares to tendering shareholders.

|

In the event that we extend the Initial Offer Period, we will inform the Depositary and the Information Agent of that fact. We will also issue a press release announcing a new Initial Completion Date

no later than 9:00 a.m., New York time, on the first U.S. business day following the day on which we decide to extend the Initial Offer Period.

Without limiting the manner in which we may choose to make any public announcement, subject to applicable law (including Rule 14e-1(d) and Rule 14d-4(d) under the Exchange Act, which require that material changes

be promptly disseminated to holders of Magal shares in a manner reasonably designed to inform such holders of such changes), we currently intend to make announcements regarding the offer by distributing a press release to “PR Newswire” and publishing

the aforesaid notices in a daily newspaper with national circulation in the United States.

If we make a material change in the terms of the offer (as may be permitted under applicable law) or in the information concerning the offer, or if we waive a material condition to the offer (if

permitted pursuant to the Exchange Act and the rules of the SEC), we will extend the Initial Offer Period to the extent required by the Exchange Act and the rules of the SEC.

This offer to purchase, the Letter of Transmittal and the other related documents to be furnished will be mailed to the record holders of Magal Shares whose names appear as of the date of this offer to purchase

on Magal’s shareholder list. They will also be furnished to brokers, dealers, commercial banks, trust companies and similar persons whose names, or the names of whose nominees, appear as of the date of this offer to purchase on the shareholder list

or, if applicable, who are listed as of the date of this offer to purchase as participants in a clearing agency’s security position listing, for subsequent transmittal to beneficial owners of Magal Shares.

13

2. ACCEPTANCE FOR PAYMENT AND PAYMENT.

General. Following the Final Expiration Date and upon the terms and subject to the conditions of the offer (including, if the Initial Offer Period is extended or

the offer is otherwise amended, the terms and conditions of any such extension or amendment), subject to proration, we will accept for payment and, subject to any applicable withholding tax duties, pay for all Magal Shares validly tendered prior to

10:00 a.m., New York time, on the Final Expiration Date and not properly withdrawn in accordance with Section 4. We expect to make such payment, including in the event that proration of tendered Magal Shares is required, within four U.S. business

days following the Final Expiration Date. Please see Section 1.

In all cases, we will pay for Magal Shares validly tendered and accepted for payment pursuant to the offer only after timely receipt by the Depositary of the required documents

to substantiate a valid tender, as set forth in Section 3.

For purposes of the offer, we will be deemed to have purchased Magal Shares that have been validly tendered and not properly withdrawn if and when we give oral or written notice to the Depositary of

our acceptance for payment of Magal Shares pursuant to the offer. Upon the terms and subject to the conditions of the offer, payment for the Magal Shares will be made by the Depositary.

Under no circumstances will interest be paid on the purchase price to be paid, regardless of any extension of the offer or any delay in making payment.

If, pursuant to the terms and conditions of the offer, we do not accept tendered Magal Shares for payment for any reason or if certificates are submitted representing more Magal Shares than are tendered

(including by reason of proration), certificates evidencing unpurchased Magal Shares will be returned to the tendering shareholder (or, in the case of Magal Shares tendered by book-entry transfer pursuant to the procedure set forth in Section 3, the

Magal Shares will be credited to the relevant account), no later than three business days following the expiration, termination or withdrawal of the offer.

Form of Payment. All shareholders tendering their Magal Shares will be paid solely in U.S. dollars.

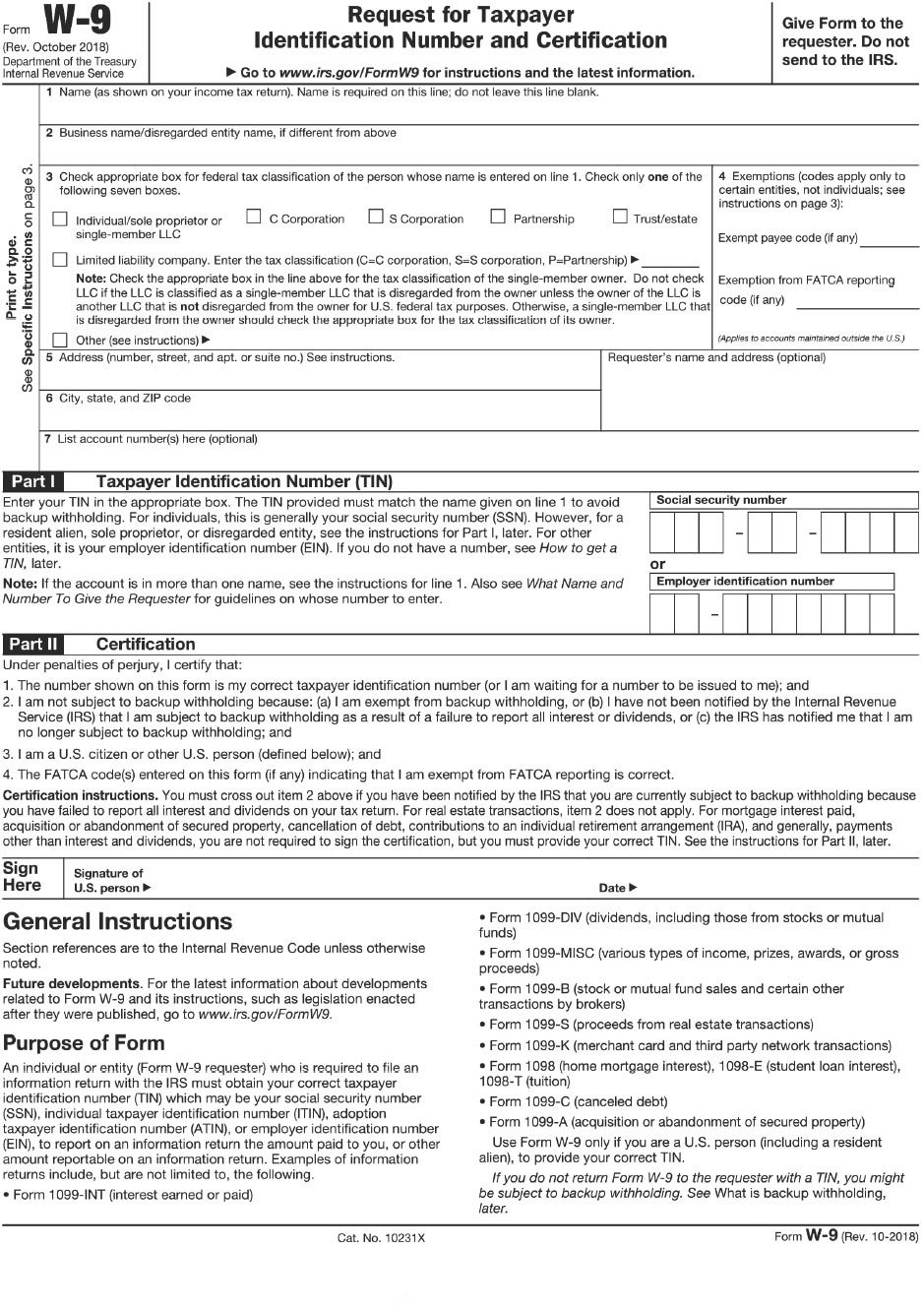

Withholding Tax. Please note that under the “Backup Withholding” provisions of U.S. federal income tax law, the Depositary may be required to withhold tax, at applicable

rates (currently 24.0%), on amounts received by a tendering shareholder or other payee pursuant to the offer. To prevent such withholding from the purchase price received for Magal Shares tendered pursuant to the offer to the Depositary, each

tendering shareholder who does not otherwise establish an exemption from such withholding, must properly complete the Form W-9 included in the Letter of Transmittal. See Section 5.

Also, under the “withholding tax” provisions of Israeli income tax law, the gross proceeds payable to a tendering shareholder in the offer generally will be subject to Israeli withholding tax. However, based on an

approval that we received from the ITA:

(1) tendering shareholders who acquired their Magal Shares after Magal’s initial public offering on Nasdaq in 1993 and who certify that they are not, and at the date of purchase of their Shares were not Israeli

residents (and, in the case of a corporation, that no Israeli resident(s) (x) holds 25.0% or more of the means of control of such corporation or (y) is the beneficiary of, or is entitled to, 25.0% or more of the revenues or profits of such

corporation, whether directly or indirectly), will not be subject to Israeli withholding tax; and

(2) payments to tendering shareholders who acquired their Magal Shares after Magal’s initial public offering on Nasdaq in 1993 and who hold their Magal Shares through an Israeli broker or Israeli financial

institution will be made by us without any Israeli withholding at source, and the relevant Israeli broker or Israeli financial institution will withhold Israeli tax, if any, as required by Israeli law.

The approval does not address shareholders who are not described in clauses (1) and (2) above, and therefore they will be subject to Israeli withholding tax at the applicable rate of the gross proceeds payable

to them pursuant to the offer, as prescribed by Israeli tax law.

See Section 5 and the Letter of Transmittal for instructions on how to prevent us from withholding Israeli income tax from the gross proceeds payable to you (if any) pursuant to the offer.

14

3. PROCEDURES FOR TENDERING SHARES OR NOTIFYING US OF YOUR OBJECTION TO THE OFFER.

Overview

All holders of Magal Shares should tender their Magal Shares to, or object to the offer through, the Depositary pursuant to the instructions described under the caption “Tenders to American Stock Transfer & Trust Company, LLC, our Depositary” below.

You may only tender your Magal Shares or object to the offer by following the procedures described in this Section 3. You may not tender your Magal Shares using a guaranteed

delivery procedure.

Tenders to American Stock Transfer & Trust Company, LLC, our Depositary

Eligibility; Who May Tender to, or Object to the Offer through, the Depositary. All shareholders should tender their Magal Shares to, or object to the offer through, the

Depositary.

Valid Tender. In order for you to validly tender Magal Shares pursuant to the offer, a properly completed and duly executed Letter of Transmittal, together with any

required signature guarantees, or in the case of a book-entry transfer, an agent’s message, and any other documents required by the Letter of Transmittal, must be received by the Depositary at its address set forth on the back cover of this offer to

purchase prior to 10:00 a.m., New York time, on the Initial Completion Date or Final Expiration Date, as applicable. In addition, certificates evidencing tendered Magal Shares must be received by the Depositary at its address or the shares must be

delivered to the Depositary (including an agent’s message if you did not deliver a Letter of Transmittal), in each case prior to 10:00 a.m., New York time, on the Initial Completion Date or Final Expiration Date, as applicable.

The term “agent’s message” means a message, transmitted by The Depository Trust Company, or DTC, to, and received by, the Depositary and forming part of the Book-Entry Confirmation that states that DTC has

received an express acknowledgement from the participant in DTC tendering the Magal Shares that are the subject of the Book-Entry Confirmation, that the participant has received and agrees to be bound by the Letter of Transmittal and that we may

enforce that agreement against that participant.

If certificates evidencing tendered Magal Shares are forwarded to the Depositary in multiple deliveries, a properly completed and duly executed Letter of Transmittal must accompany each delivery. No alternative,

conditional or contingent tenders will be accepted and no fractional Magal Shares will be purchased.

The method of delivery of share certificates and all other required documents, including through DTC, is at your option and risk, and the delivery will be deemed made only when

actually received by the Depositary. If delivery is by mail, registered mail with return receipt requested, properly insured, is recommended. In all cases, sufficient time should be allowed to ensure timely delivery.

Book-Entry Transfer. The Depositary will establish an account with respect to the Magal Shares at DTC for purposes of the offer within two U.S. business days

after the date of this offer to purchase. Any financial institution that is a participant in the system of DTC may make book-entry delivery of Magal Shares by causing DTC to transfer such Magal Shares into the Depositary’s account at DTC in

accordance with DTC’s procedures. However, although delivery of Magal Shares may be effected through book-entry transfer into the Depositary’s account at DTC, the Letter of Transmittal, properly completed and duly executed, with any required

signature guarantees, or an agent’s message, and any other required documents must, in any case, be transmitted to, and received by, the Depositary at its address set forth on the back cover of this offer to purchase prior to 10:00 a.m., New York

time, on the Initial Completion Date or Final Expiration Date, as applicable. Delivery of the documents to DTC or any other party does not constitute delivery to the Depositary.

Signature Guarantees. Signatures on all Letters of Transmittal must be guaranteed by a firm that is a member of the Securities Transfer Agents Medallion Program, or by any

other “eligible guarantor institution,” as that term is defined in Rule 17Ad-15 under the Exchange Act, except in cases where Magal Shares are tendered:

|

•

|

by a registered holder of Magal Shares who has not completed either the box entitled “Special Delivery Instructions” or the box entitled “Special Payment Instructions” on the Letter of Transmittal; or

|

|

•

|

for the account of an eligible guarantor institution.

|

If a share certificate is registered in the name of a person other than the signer of the Letter of Transmittal, or if payment is to be made, or a share certificate not accepted for payment or not tendered is to

be returned, to a person other than the registered holder(s), then the tendered certificate must be endorsed or accompanied by appropriate stock powers, in either case, signed exactly as the name(s) of the registered holder(s) appear on the

certificate, with the signature(s) on the certificate or stock powers guaranteed by an eligible guarantor institution. See Instruction 1 and Instruction 5 to the Letter of Transmittal.

15

Condition to Payment. In all cases, payment for Magal Shares tendered and accepted for payment pursuant to the offer will be made only after timely receipt by the

Depositary of the certificate(s) evidencing Magal Shares, or a timely Book-Entry Confirmation for the delivery of Magal Shares, the Letter of Transmittal, properly completed and duly executed, with any required signature guarantees, or, in the case

of a book-entry transfer, an agent’s message, and any other documents required by the Letter of Transmittal.

The valid tender of Magal Shares pursuant to the applicable procedure described above will constitute a binding agreement between you and us upon the terms and subject to the conditions of the offer.

Appointment. By executing the Letter of Transmittal as set forth above (including delivery by way of an agent’s message), you irrevocably appoint our designees as your

agents, attorneys-in-fact and proxies in the manner set forth in the Letter of Transmittal, each with full power of substitution, to the full extent of your rights with respect to the Magal Shares you tendered. These powers of attorney and proxies

will be considered coupled with an interest in the tendered Magal Shares. The appointment will be effective if, as and when, and only to the extent that, we accept your Magal Shares for payment. Upon our acceptance for payment, all prior powers of

attorney, proxies and consents given by you with respect to such Magal Shares (and any and all Magal Shares or other securities issued or issuable in respect of your Magal Shares) will be revoked, without further action, and no subsequent powers of

attorney or proxies may be given or any subsequent written consent executed by you (and, if given or executed, will not be deemed effective). Our designees will, with respect to the Magal Shares for which the appointment is effective, be empowered to

exercise all of your voting and other rights as they in their sole discretion may deem proper at any annual or special meeting of Magal’s shareholders or any adjournment or postponement of that meeting, by written consent in lieu of any meeting or

otherwise. We reserve the right to require that, in order for Magal Shares to be deemed validly tendered, immediately upon our payment for the Magal Shares, we must be able to exercise full voting rights with respect to the Magal Shares at any

meeting of Magal’s shareholders with a record date subsequent to the consummation of the offer (and at any meeting of Magal’s shareholders with a record date prior to the consummation of the offer if such Magal Shares were held by such tendering

shareholder as of such record date).

Objecting to the Offer. If you want to notify us of your objection to the offer with respect to all or any portion of your Magal Shares, and you hold such Magal

Shares through a broker, dealer, commercial bank, trust company or other nominee, you should request such broker, dealer, commercial bank, trust company or other nominee to provide on your behalf the Notice of Objection to the Depositary prior to

10:00 a.m., New York time, on the Initial Completion Date.

We will disregard any Notices of Objection received by the Depositary after such deadline. In addition, if you submit a Notice of Objection with respect to Magal Shares and

thereafter you deliver a Letter of Transmittal by which you tender those Magal Shares, we will disregard your Notice of Objection. Similarly, if you submit a Letter of Transmittal by which you tender Magal Shares, and thereafter you deliver to us a

Notice of Objection with respect to those Magal Shares, we will disregard your Letter of Transmittal. If you submit a Letter of Transmittal and a Notice of Objection concurrently with respect to the same Magal Shares, we will disregard the Notice of

Objection.

Withdrawing your Objection. You may withdraw a previously submitted Notice of Objection at any time prior to 10:00 a.m., New York time, on the Initial Completion Date. For

a withdrawal to be effective, a written notice of withdrawal must be timely received by the Depositary at its address set forth on the back cover of this offer to purchase. Any notice of withdrawal must specify the name of the person(s) who submitted

the Notice of Objection to be withdrawn and the number of Magal Shares to which the Notice of Objection to be withdrawn relates. Following the withdrawal of a Notice of Objection, a new Notice of Objection may be submitted at any time prior to 10:00

a.m., New York time, on the Initial Completion Date by following the procedures described above.

If, with respect to all or any portion of your Magal Shares, you object to the offer during the Initial Offer Period and the conditions to the offer have been satisfied or, subject to applicable law, waived by

us, you may tender such Magal Shares during the Additional Offer Period. See Section 1 and Section 11.

Determination of Validity. All questions as to the validity, form, eligibility (including time of receipt) and acceptance for payment of any tender of Magal Shares or Notice of

Objection will be determined by us, in our sole discretion. We reserve the absolute right to reject any or all tenders or Notices of Objection that we determine not to be in proper form or, in the case of tenders, the acceptance for payment

of which may be unlawful. A tender of Magal Shares or Notice of Objection will not have been made until all defects and irregularities have been cured or waived. None of us, our affiliates, our assigns, the

Depositary, the Information Agent, our Israeli or U.S. legal counsel or any other person will be under any duty to give notification of any defects or irregularities in tenders of Magal Shares or Notices of Objection or incur any liability for

failure to give any notification.

16

If you tender your Magal Shares pursuant to the applicable procedure described above, it will constitute your acceptance of the terms and conditions of the offer, as well as your representation and warranty to us

that:

|

•

|

you have the full power and authority to tender, sell, assign and transfer the tendered Magal Shares (and any and all Magal Shares or other securities issued or issuable in respect of your Magal Shares); and

|

|

•

|

when we accept your Magal Shares for payment, we will acquire good and unencumbered title to your Magal Shares, free and clear of all liens, restrictions, charges and encumbrances and not subject to any adverse

claims.

|

4. WITHDRAWAL RIGHTS

You may withdraw previously tendered Magal Shares at any time prior to 10:00 a.m., New York time, on the Initial Completion Date, but not during the Additional Offer

Period (see Section 1 and Section 11). In addition, under U.S. law, tendered Magal Shares may be withdrawn at any time after 60 days from the date of the commencement of the offer if the Magal Shares have not yet been accepted for payment

by us. If we extend the Initial Offer Period, delay our acceptance for payment of Magal Shares or are unable to accept Magal Shares for payment pursuant to the offer for any reason, then, without prejudice to our rights under the offer but subject to