UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 | ||||

For the fiscal year ended June 30, 2022

OR

☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15 (d) OF THE EXCHANGE ACT OF 1934 | ||||

For the transition period from ____________________ to _____________________

Commission file number 001-33365

Cantaloupe, Inc.

____________________________________________________________________________________________

(Exact name of registrant as specified in its charter)

| Pennsylvania | 23-2679963 | |||||||

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |||||||

| 100 Deerfield Lane, | Suite 300, | Malvern, | Pennsylvania | 19355 | |||||||||||||

| (Address of principal executive offices) | (Zip Code) | ||||||||||||||||

(610) 989‑0340

____________________________________________________________________________________________

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

| Title of Each Class | Trading Symbol | Name Of Each Exchange On Which Registered | ||||||

| Common Stock, no par value | CTLP | The NASDAQ Stock Market LLC | ||||||

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☑ No ☐

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files) Yes ☑ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer”, “accelerated filer”, “smaller reporting company,” and “emerging growth company” in Rule 12b‑2 of the Exchange Act.

| Large accelerated filer | ☐ | Accelerated filer | ☑ | ||||||||

| Non-accelerated filer (Do not check if a smaller reporting company) | ☐ | Smaller reporting company | ☐ | ||||||||

| Emerging growth company | ☐ | ||||||||||

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☑

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b‑2 of the Act). Yes ☐ No ☑

The aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant computed by reference to the price at which the common equity was last sold as of the last business day of the registrant’s most recently completed second fiscal quarter, December 31, 2021, was $513.2 million.

As of October 14, 2022, there were 71,218,130 outstanding shares of Common Stock, no par value.

Selected portions of the registrant’s definitive proxy statement on Schedule 14A for the registrant’s 2023 annual meeting of stockholders, which will be filed with the Securities and Exchange Commission within 120 days of June 30, 2022, are incorporated by reference into Part III of this Annual Report on Form 10-K.

CANTALOUPE, INC.

TABLE OF CONTENTS

2

PART I

In this Annual Report on Form 10-K, or Annual Report, and unless otherwise indicated, the terms "Cantaloupe", the "Company", "CTLP", "we", "us", "our", "our company" and "our business" refer to Cantaloupe, Inc., formerly known as USA Technologies, Inc.

The following discussion should be read in conjunction with our consolidated financial statements and related notes included elsewhere in this Annual Report. Due to rounding, figures in tables may not sum exactly.

FORWARD-LOOKING STATEMENTS

This Form 10‑K contains certain forward-looking statements within the meaning of Section 21E of the Securities Exchange Act of 1934, as amended, regarding, among other things, the anticipated financial and operating results of Cantaloupe, Inc. For this purpose, forward-looking statements are any statements contained herein that are not statements of historical fact and include, but are not limited to, those preceded by or that include the words, “estimate,” “could,” “should,” “would,” “likely,” “may,” “will,” “plan,” “intend,” “believes,” “expects,” “anticipates,” “projected,” or similar expressions. Those statements are subject to known and unknown risks, uncertainties and other factors that could cause the actual results to differ materially from those contemplated by the statements. The forward-looking information is based on various factors and was derived using numerous assumptions. Important factors that could cause the Company’s actual results to differ materially from those projected include, for example:

•general economic, market or business conditions unrelated to our operating performance, including the impact of the ongoing COVID-19 pandemic, global supply chain disruptions, and inflationary pressures;

•potential mutations of COVID-19 and the efficacy of vaccines and treatment developments and their deployment;

•failure to comply with the financial covenants in the Amended JPMorgan Credit Facility (as defined below);

•our ability to raise funds in the future through sales of securities or debt financing in order to sustain operations in the normal course of business or if an unexpected or unusual event were to occur;

•our ability to compete with our competitors and increase market share;

•whether our current or future customers purchase, lease, rent or utilize ePort devices, Seed’s software solutions or our other products in the future at levels currently anticipated;

•whether our customers continue to utilize the Company’s transaction processing and related services, as our customer agreements are generally cancellable by the customer on thirty to sixty days’ notice;

•our ability to satisfy our trade obligations included in accounts payable and accrued expenses;

•the incurrence by us of any unanticipated or unusual non-operating expenses, which may require us to divert our cash resources from achieving our business plan;

•our ability to predict or estimate our future quarterly or annual revenue and expenses given the developing and unpredictable market for our products;

•our ability to integrate acquired companies into our current products and services structure;

•our ability to retain key customers from whom a significant portion of our revenue is derived;

•the ability of a key customer to reduce or delay purchasing products from us;

•our ability to obtain widespread commercial acceptance of our products and service offerings;

•whether any patents issued to us will provide any competitive advantages or adequate protection for our products, or would be challenged, invalidated or circumvented by others;

•our ability to operate without infringing the intellectual property rights of others;

•the ability of our products and services to avoid disruptions to our systems or unauthorized hacking or credit card fraud;

•geopolitical conflicts, such as the ongoing conflict between Russia and Ukraine;

•whether we will experience material weaknesses in our internal controls over financial reporting in the future, and are not able to accurately or timely report our financial condition or results of operations;

3

•the ability to remain in compliance with the continued listing standards of the Nasdaq Global Select Market (“Nasdaq”) and continue to remain as a member of the US Small-Cap Russell 2000®;

•whether our suppliers would increase their prices, reduce their output or change their terms of sale; and

•the risks associated with the currently pending investigation, potential litigation or possible regulatory action arising from the 2019 Investigation (as defined below) and its findings, from the failure to timely file our periodic reports with the Securities and Exchange Commission, from the restatement of the affected financial statements, from allegations related to the registration statement for the follow-on public offering, or from potential litigation or other claims arising from these events.

Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance, or achievements. Actual results or business conditions may differ materially from those projected or suggested in forward-looking statements as a result of various factors including, but not limited to, those described above and in Part I, Item 1A, “Risk Factors” of this Form 10‑K. We cannot assure you that we have identified all the factors that create uncertainties. Moreover, new risks emerge from time to time and it is not possible for our management to predict all risks, nor can we assess the impact of all risks on our business or the extent to which any risk, or combination of risks, may cause actual results to differ from those contained in any forward-looking statements. Readers should not place undue reliance on forward-looking statements.

Any forward-looking statement made by us in this Form 10‑K speaks only as of the date of this Form 10‑K. Unless required by law, we undertake no obligation to publicly revise any forward-looking statement to reflect circumstances or events after the date of this Form 10‑K or to reflect the occurrence of unanticipated events.

4

Item 1. Business.

OVERVIEW

Cantaloupe, Inc., previously known as USA Technologies, Inc., is organized under the laws of the Commonwealth of Pennsylvania. We are a digital payments and software services company that provides end-to-end technology solutions for the unattended retail market. We are transforming the unattended retail world by offering a single platform for self-service commerce which includes integrated payments processing and software solutions that handle inventory management, pre-kitting, route logistics, warehouse and back-office management. Our enterprise-wide platform is designed to increase consumer engagement and sales revenue through digital payments, digital advertising and customer loyalty programs, while providing retailers with control and visibility over their operations and inventory. As a result, customers ranging from vending machine companies to operators of micro-markets, car wash, electric vehicle charging stations, commercial laundry, kiosks, amusements and more, can run their businesses more proactively, predictably, and competitively.

We derive the majority of our revenues from subscription and transaction fees resulting from transactions on, as well as connectivity and telemetry services provided by, our ePort® cashless devices, Seed™ software, and our Quick Connect API services. These services include digital payment processing, loyalty programs, inventory management, route logistics optimization, warehouse and accounting management, and intelligent merchandising. Devices operating on the Company’s platform and using our services include those resulting from the sale, finance or a monthly bundled subscription (Cantaloupe ONE program) of our point of sale ("POS") electronic payment devices, telemetry devices or certified payment software or the servicing of similar third-party installed POS terminals or telemetry devices. The majority of ePort customers pay a monthly service fee plus a blended percentage rate on transaction volumes. Transaction fees on volumes processed through the Company’s payment devices, are the most significant driver of the Company’s revenues.

Our customers range from global food service organizations to small businesses that operate primarily in self-serve retail markets including food and beverage vending, micro-markets, amusement and arcade machines, commercial laundry, air/vacuum, car wash, electric vehicle, and various other self-serve kiosk applications as well as equipment developers or manufacturers who incorporate our hardware, software, and services into their product offerings.

THE INDUSTRY

We offer a variety of solutions in unattended retail, which enable the acceptance of digital payments and allow our customers to simplify inventory, analytics, warehouse, logistics, and back-office management. We believe the following industry trends are

5

driving growth in demand for digital payment systems and advanced logistics management in general and more specifically within the markets we serve:

•Increased adoption of cashier-less models via vending machines or self-service kiosks to meet demand for and more use of fast, simple and seamless digital purchase and payment experiences;

•Rising consumer demand for transaction convenience, safety, and security which we have seen in the growth in digital payment adoption, especially contactless payments, in the wake of the COVID-19 pandemic; and

•Ongoing labor challenges drive increased utility of actionable operational business intelligence from new technologies like artificial intelligence and machine learning to drive operational efficiencies and operational transparency through modern, cloud-based logistics and inventory management solutions.

Shift Toward Digital Payments Is Here to Stay.

One lasting impact of COVID-19 was the creation of a ‘new normal’ for businesses and shoppers alike, accelerating the secular shift to self-service commerce. According to “The Visa Back to Business Global Study: 2022 Small Business Outlook” (the "Visa Study"); 73% of small businesses surveyed said that new forms of digital payments are fundamental to their growth. In addition, according to the Visa Study, 41% of consumers surveyed said they either plan to shift to using only digital payments within the next two years, or are already cashless. Lastly, 82% of small businesses surveyed said they will accept digital options in 2022 and nearly half (46%) of consumers surveyed expect to use digital payments more often in 2022, with just 4% saying they will use them less. The acceleration towards digital payments amongst surveyed consumers was primarily driven by benefits such as easier online shopping, personal safety and convenience.

Increasing Consumer Interest in Self-Service Models

Cashier-less stores that minimize or remove human intervention have shifted consumer expectations on retail shopping experiences. A consumer survey of 2,000 people across the United States performed by the Company and CITE Research in 2021 found that 83% of consumers who increased unattended retail usage during the pandemic expect to continue using it at elevated levels when the pandemic was over. And consumers are not just looking for traditional food and beverage offerings through unattended, as 82% of respondents cited an interest in purchasing nontraditional items through vending machines, with the interest significantly increasing since the last survey in 2019. Clothing and health and beauty products had the greatest two-year increase with 70% - 71% of respondents interested in purchasing these items from vending machines in 2021 compared to 55% for clothing and 64% for health and beauty in 2019 respectively.

OUR SOLUTION

We continue to transform the unattended retail market by offering one integrated solution for payments processing, logistics, and back-office management. Our platform is designed to increase consumer engagement and sales revenue through digital payments, digital advertising, and customer loyalty programs, while providing retailers with control and visibility over their operations and inventory. As a result, customers can run their businesses more proactively, predictably, and competitively. We offer customers several different ways to connect and manage their distributed assets. These range from our ePort cashless hardware, Seed platform, and our Quick Connect web services. Our platform is designed to transmit from our customers’ terminal or location payment information for processing, sales, and performance data for asset optimization and reporting to our customers within the Seed platform, as well as third-party software solutions, providing greater control and visibility of their business. Through our platform, we enable customers to easily manage assets, make changes, and push updates all remotely, ensuring they run as efficiently as possible.

PRODUCTS AND SERVICES

Our hardware includes ePort, the Company’s integrated payment device, as well as Yoke POS, the Company’s point-of-sale terminal, which are both currently deployed in self-service, unattended market applications such as vending, micro-markets, amusement, arcade, commercial laundry, air/vacuum, car wash, and others. Our ePort products which come in a variety of styles, facilitates digital payments by capturing payment information and transmitting it to our platform for authorization with

6

the payment system (e.g., credit card processors). Additionally, our ePort devices send sales data into the Seed platform for advanced reporting, including remote asset management. ePort has earned a reputation for quality, reliability, and innovation.

Our Yoke POS product provides a tablet-like experience for consumers to purchase goods through a self-checkout model. Additionally, Yoke POS processes transactions and sends sales data into the Yoke Portal for reporting and kiosk management. We offer a variety of hardware through purchase, finance, or subscription with our new Cantaloupe ONE Platform.

•ePort G11 Cashless Kit, is a 4G LTE digital payment device that enables faster processing and enhanced functionality for payment and consumer engagement applications. It supports functionality that requires higher speeds and large data loads, operates on the AT&T and Verizon networks, and has built-in NFC (contactless) support for mobile payments, traditional credit and debit cards, in addition to EMV-contactless.

•The ePort G10-Chip, is a digital reader that accepts contact EMV (chip cards) and contactless EMV (tap) payment methods, along with other standard forms of digital payments that include credit/debit card, and mobile wallet. The reader functions with the existing G11 telemeter and reports into the Seed platform similar to a G11 Cashless Kit (see below for a description of the Seed platform).

•ePort Engage Series, which includes the ePort Engage and ePort Engage Combo, are the next generation of digital touchscreen devices and provide retailers the ability to captivate consumers in new ways and enables truly frictionless purchasing. The ePort Engage Series offers best-in-class networking, security and interactivity, including acceptance of contact EMV (chip cards) and contactless EMV (tap) payment methods. The devices can be fitted in a range of hardware configurations, including vending, kiosks, amusement, and electric vehicle charging stations

•Yoke POS, is a scalable, cost-friendly point-of-sale solution for any micro market or self-service business. The simplified checkout experience provides consumers with a fast and convenient solution to purchase goods via digital payments or the Yoke loyalty card. The Yoke POS displays unique customer promotions or offers, and loyalty points for Yoke loyalty card members, all at the point-of-sale or directly in the Yoke Pay mobile app.

We offer integrated software services that leverage payment or asset tracking devices in the field to connect into our feature-rich platform for advanced data management, analytics, route scheduling, and other offerings:

•The Seed platform is a cloud-based asset management and optimization solution that provides advanced analytics, dynamic route scheduling, automated pre-kitting, proactive equipment management, intelligent merchandising, inventory management, warehouse purchasing, and accounting management. The Seed platform has a reputation for providing innovative software features and functionality that solve every day customer challenges. It includes Seed Live for sales reporting and asset management, Seed Cashless+ for small business owner advanced management tools, Seed Pro for logistics optimization; Seed Office for back-office management; Seed Markets for integrated micro market management; and Seed Delivery for integrated online ordering and office coffee service ("OCS") optimization.

•Add-on software services within the Seed platform include Remote Price Change ("RPC"), HIVERY Enhance, and integration with e-commerce partners Tech2Success and Supply Wizards. RPC saves customers time and money by enabling them to manage prices for products in their machines remotely through Seed. With the HIVERY Enhance integration, customers on Seed Pro and Seed Office can receive powerful new product recommendations and targeted space-to-sales optimization with HIVERY’s artificial intelligence and machine learning technology. Our e-commerce integration partners, Tech2Success and Supply Wizards, enable customers to integrate their online stores to Seed for inventory and warehouse management. RPC and HIVERY Enhance are the latest innovations for unattended retail through our Seed suite of services.

•The Yoke Portal is our web-based kiosk management solution for Yoke POS that gives customers complete access and control over their micro market locations and kiosks. Additionally, within the Yoke Portal customers can customize promotions and loyalty programs per location, creating new ways to engage consumers at the point-of-sale or via the Yoke Pay app.

•Quick Connect is a web service that allows a client application to securely interface with the Company’s payment processing and asset managing services.

•Additional services include loyalty programs, campus card integrations, digital ad-management, and data warehouse services.

7

We support our offerings through a number of professional services and back-office functions:

•Professional Services. For our larger customers we offer a variety of professional services to get them onto and use the platform easily and seamlessly. Services include planning, project management, deployment, installation support, Seed implementation, and marketing and performance evaluation.

•Network Infrastructure. Our services and platforms operate on a combination of proprietary and third-party technologies and are supported by geographically diverse teams.

•Card Processing Services. Through our existing relationships with card processors and card associations, we provide merchant account and terminal ID set up, pre-negotiated discounted fees on small ticket purchases, and direct electronic funds transfers to our customers’ bank accounts for all settled card transactions as well as ensure compliance with processing protocols.

•Customer/Consumer Services. We support our services by providing help desk support, repairs, and replacement services. All inbound consumer billing inquiries are handled through a 24‑hour help desk, thereby reducing our customers’ exposure to consumer billing inquiries and potential chargebacks. We provide remote maintenance updates and enhancements to software, settings, and features to ePort card readers via wireless connections.

COMPETITION

The unattended retail industry is highly competitive with service providers ranging from well-established enterprises to early stage companies within the financial technology and software services industries. The markets for Cantaloupe’s products and services are characterized by evolving industry standards, aggressive pricing, continuous innovation, and changing consumer trends. Many of the company’s competitors are challenging Cantaloupe’s industry leading position, particularly when it comes to pricing, emulating products, services, and marketing, as well as addressing consumer trends. However, we believe we have competitive strengths that position us favorably.

Consumers are expecting more from their shopping experience, with access to buy what they want, when they want, with the ability to pay with any shape or form of digital currency. This has led to a multitude of new devices on the market to enable a more engaging experience at the POS. In addition, micro markets are becoming one of the largest growth sectors in the convenience services industry, with large competitors owning a majority of the current market share. While we believe we have a strong competitive offering that positions us favorably in software services for unattended retail, competitors are entering the market with modernized back-end systems that are focused on the user interface along with real-life product planogram possibilities.

8

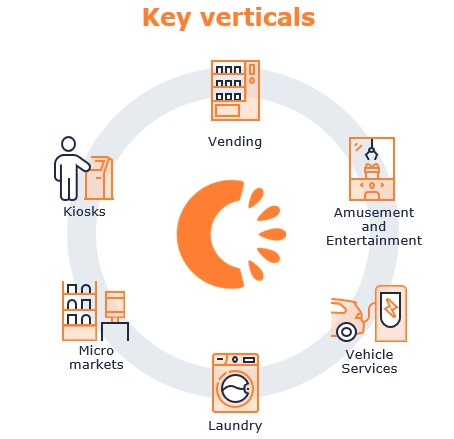

MARKETS WE SERVE

While the below key verticals represent only a fraction of our total market potential, as described below, these are the areas where we have gained the most traction to date.

Vending. According to the 2020 Census of the Convenience Services Industry (conducted biannually), a study conducted by the NAMA Foundation and research firm Technomic, the US Convenience Services Industry, which consists of vending machines, micro markets, OCS and pantry services, represented total annual revenues of approximately $16 billion in 2020 compared to total annual revenues of approximately $27 billion in 2019, reflecting a reduction of approximately $11 billion and 40%. This was due to the impact of the coronavirus pandemic. The Convenience Services Industry is expected to be 64% larger in 2022 compared to 2020, and operators expect a full recovery to 2019 industry levels (pre-pandemic levels) by 2022-2023. In 2020, 80% of the Convenience Services Industry's total annual revenues came from the Vending vertical while Micro Markets, OCS and Pantry Services verticals represented approximately 12%, 7% and 1% of total annual revenues respectively.

Micro Markets and Kiosks. According to the Automatic Merchandiser’s State of the Industry Annual Report published in July 2022, the vending and micro market business operators surveyed indicated that the number of micro market locations served increased 70% in 2021. This demonstrates that while COVID-19 impacted growth and new location placements in 2020, micro markets continued to experience a significant level of growth coming out of the pandemic. We believe the desire to diversify product offerings to employees, while giving them their own convenience store with a micro market, will continue to increase. Our primary opportunity in the micro markets vertical is providing a fully integrated solution to our customers which includes a point-of-sale platform and leveraging the Seed Markets offering to optimize our customers payments and logistics services including integrated route scheduling, warehouse pre-picking, and reporting. While micro markets continue to grow in the traditional vending and food service industry, self-service kiosks are also on the rise. According to the 2022 Kiosk Marketplace Census Report, the 2021 Zebra Technologies’ Global Shopper Study found that nearly half (47%) of shoppers used retail self-checkouts, a 7% year-on-year increase, and 91% of these said they will continue using the technology.

Vehicle Services. Our primary opportunities in the vehicle services markets relate to businesses that provide air, vacuum, car wash, electric car charging and parking services. In these sectors we can provide customers with cashless payment terminals, payment processing, telemetry services for data and connectivity services, as well as software solutions to improve business

9

optimization. Currently, we partner with a leader in the air vending services by equipping their machines with our cashless acceptance devices.

Amusement and Entertainment. Our current customers and primary opportunities in the amusement and entertainment markets are typically classified as “street/route business,” which are standalone businesses that are open to the general public and that offer card/coin-operated games such as claw machines, amusement park machines (i.e. body dryers), bowling alleys and bar entertainment (e.g. digital music machines and dart machines). Currently, we partner with one of the largest independent claw machine providers to enable them with cashless acceptance devices and payment processing.

Laundry. Our primary opportunities in laundry consist of the coin-operated commercial laundry and multi-housing laundry markets. Currently, our joint solution with an industry leader competes with hardware manufacturers, who provide joint solutions to their customers in partnership with payment processors, and with at least one competitor who provides an integrated hardware and payment processing solution.

OUR GROWTH OPPORTUNITY

Our primary objective is to continue to enhance our position as a leading provider of technology that enables electronic payment transactions, advanced logistics management, and value-added services primarily at small-ticket, self-service retail locations such as vending, kiosks, electric vehicle charging. commercial laundry, and other similar markets. We plan to execute our growth strategy organically and through strategic acquisitions. Key elements of our strategy are to:

Maximize Growth in Existing Customers/Partners. Our current customers have seen the benefits of our products and services and we believe they continue to represent the largest opportunity to scale recurring revenue and connections, through the addition of new products and services, as well as expanding our footprint of current product offerings. We are continuously enhancing our solutions and services with additional features and functionality that create add-on service offerings to existing customers such as RPC, HIVERY Enhance integration and Yoke POS. We believe our continued innovation will lead to further adoption of Cantaloupe’s solutions and services in the unattended POS payments market.

Capitalize on the Emerging Contactless, EMV, NFC, and Growing Mobile Payments Trends. With more than 90% of our digital connected base enabled to accept NFC payments (including mobile wallets), we believe that continued consumer preference towards contactless payments, including mobile wallets like Apple Pay, Google Pay and Samsung Pay, represent a significant opportunity for the Company to further drive adoption in the current markets as well as new unattended kiosk applications in which we can provide services and solutions. Through innovation we’ll seek to offer consumers more ways to pay leveraging digital wallets such as pay with crypto, or other digital-like applications.

Expand into Micro Markets. With the Company’s Yoke’s POS platform, we will continue to penetrate into the growing vertical of micro markets both in near-vending channels as well as small business retail. Self-service or self-checkout is on the rise and with our seamlessly integrated offering or standalone solution of Yoke POS, we believe we are positioned well to deliver a scalable micro market solution for businesses of all kinds. We plan to differentiate ourselves by providing a single platform to manage consumer and operational aspects of micro markets, while also integrating multiple service providers for flexibility and ultimate ease to our customers.

Further Penetrate Attractive Adjacent Markets. We plan to continue to introduce our turn-key solutions and services to various adjacent markets such as the small business retail market to enable self-checkout solutions, along with other key growth verticals like electric car charging where we’ll leverage our expertise in digital payment solutions and telemetry services for data and asset management services. We plan to leverage the Seed platform to extend route optimization tools into other verticals where static schedules are not optimal for service visits. In addition, Seed Pro’s patented dynamic route scheduling capabilities can support optimal servicing and decreased operational costs.

Capitalize on Opportunities in International Markets. We are currently focused on the U.S. and Canadian markets for our ePort devices, Yoke POS terminals, and the Seed platform, but will seek to establish a presence in unattended retail markets to provide electronic payments and logistics optimization outside of the U.S. and Canada. In order to do so, we have dedicated sales resources to spearhead international opportunities, starting with Latin America, and Europe.

Comprehensive Service and Support. In addition to its industry-leading ePort digital payments system, Yoke POS terminal, Seed logistics software, the Company seeks to provide its customers with a comprehensive platform designed to encourage optimal return on investment through business planning and performance optimization; acceptance of crypto payments, and a

10

loyalty and rewards program for consumer engagement; sales data and machine alerts; DEX data transmission; and the ability to extend digital payments capabilities and the full suite of services across multiple aspects of an operator’s business including the micro-markets contract food industry, online and mobile payments.

SALES AND MARKETING

Our sales strategy includes both direct sales and channel development, depending on the particular dynamics of each of our markets. Our direct sale efforts are supported by both inside and external sales team members, which are aligned to serve our enterprise and our small- and medium-business (SMB) customers and prospects. In order to expand our sales reach, we have agreements with resellers in select market segments. Our marketing strategy includes advertising and outreach initiatives designed to build brand awareness, position our company’s thought leadership within unattended retail, make clear our competitive strengths, and prove the value of our products and services to our opportunity markets. Activities include creating a vibrant company and product presence on the web, digital advertising, Search Engine Optimization ("SEO"), and social media; the use of direct mail and email campaigns; educational and instructional online training sessions; content curation through blogs, whitepapers, guides, podcasts, and joint industry studies; advertising in vertically-oriented trade publications; participating in industry tradeshows and events; and working closely with customers and key strategic partners on co-marketing opportunities that drive customer and consumer adoption of our services.

As of June 30, 2022, we are marketing and selling our products primarily through our full and part-time sales and marketing staff consisting of 44 people.

IMPORTANT RELATIONSHIPS

Our most important relationships are with our almost 24,000 customers, which are governed by services agreements that provide for terms and conditions of purchase, rental, subscription or lease of the devices, licensing of our solutions, and processing services. Under the terms, we typically collect our fees from settled funds, including activation fees, monthly service fees, and transaction processing fees. Our relationships with certain large customers are governed by customized terms and conditions contained within individually negotiated services agreements.

We maintain broad and long-standing relationships with card industry associations, including our listing on the Visa Global Registry of Service Providers. From time to time, we enter into short-term incentive and promotional agreements with the card industry counterparties.

We maintain close relationships with domestic wireless telecommunications carriers and with which we have long-term bespoke pricing and support terms.

We have long-term agreements with our payment processors, each of which is seamlessly integrated with our products and customers.

We have established reseller relationships with select solution providers for add-on features and services within our traditional offerings

As part of our strategy to expand our sales reach while optimizing resources, we have agreements with select resellers within the industries we serve.

Lastly, we have a number of key technology vendors supporting our network environment and technology, our product development and our product offerings.

MANUFACTURING AND SUPPLY CHAIN

We utilize independent third-party manufacturing partners to produce the substantial majority of our hardware products that we market and sell to our customers. Production by our manufacturing partners is performed in accordance with our product specifications, quality control and compliance standards. For the years ended June 30, 2022 and June 30, 2021 our manufacturing activities principally took place in the United States and Mexico.

Our internal processes center around quality assurance of materials and testing of finished goods received from our contract manufacturers.

11

As supply chains worldwide continue to recover from COVID-19-related disruptions, the technology industry has experienced delays within supply chain. We have not experienced significant disruptions to date; however we are continually monitoring and evaluating manufacturing partners to accommodate our expected growth and minimize potential risks of disruption within our supply chain operations.

TRADEMARKS, PROPRIETARY INFORMATION, AND PATENTS

The Company owns US federal and foreign registrations for the following trademarks and service marks: Because Machines Can’t Cry For Help®, Blue Light Sequence (design only)Business Express®, Cantaloupe circle logo (design only), Cantaloupe Systems®, Cantaloupe Systems & design (Cantaloupe circle logo), CM2iQ®, COMPUVEND®, EnergyMiser®, ePort®, ePort Connect®, ePort Mobile & design, eSuds®, Intelligent Vending®, Routemaster®, Seed®, Seed & design, Seed Office®, SnackMiser®, TransAct®, USA Technologies®, USA Technologies & design, USALIVE®, VendingMiser®, VendPro®, VM2iQ®, Warehouse Master®, and YOKE®.

Much of the technology developed or to be developed by the Company is subject to trade secret protection. To reduce the risk of loss of trade secret protection through disclosure, the Company has entered into confidentiality agreements with its key employees.

From the incorporation of our Company in 1992, through June 30, 2022, 136 patents have been granted to the Company or its subsidiaries. Of the 136 patents, 50 are still in force at June 30, 2022. Our patents expire between 2022 and 2038.

ACTIVE DEVICES AND ACTIVE CUSTOMERS

In order to present meaningful information on our business, we report Active Devices and Active Customers. Active Devices are devices that have communicated with us or have had a transaction in the last twelve months. Included in the number of Active Devices are devices that communicate through other devices that communicate or transact with us. A self-service retail location that utilizes an ePort cashless payment device as well as Seed management services constitutes only one device. We define Active Customers as all customers with at least one active device

We had 23,991 Active Customers and 1.14 million Active Devices connected to our service as of June 30, 2022 compared to 19,834 Active Customers and 1.09 million Active Customers as of June 30, 2021.

HUMAN CAPITAL MANAGEMENT

As of June 30, 2022, the Company had 225 full-time employees compared to 181 full-time employees as of June 30, 2021. This represents a headcount increase of approximately 24% over prior year. Headcount growth has occurred primarily in our Sales, Customer Support and Technology departments. The headcount increase aligns with the Company's overall objectives to reduce general and administrative expenses and utilize savings to invest in innovative technologies and products, increase marketing spend to penetrate new and existing customers with our products and services and provide highest levels of customer service. We believe our ability to attract and retain qualified employees in all areas of our business is critical to our future success and growth. We seek employees who share a passion for our technology and its ability to improve our customers’ businesses.

We believe our ability to attract and retain the most qualified candidates in all areas of our business is critical to our future success and growth, and we strive for a well-balanced and diverse workforce. In addition to standard Company-wide Compliance trainings, we prioritize and continue to invest in helping our employees grow professionally in their career. We offer a combination of interactive professional development trainings, access to on demand online courses through our learning management System, and group learning programs.

We offer our employees wages and benefit packages that we believe are competitive with others throughout our industry. In addition to salaries, we provide benefits that include a 401(k) retirement savings plan, healthcare and insurance benefits, health savings and flexible spending accounts, tuition reimbursement, paid time off, as well as other benefits including access to mental health benefits, and a paid parental leave policy.

We continue to prioritize the health and safety of our employees through the COVID-19 pandemic. We continue to regularly adapt and review and policies and procedures established at the beginning of COVID-19 and communicate updates regularly internally to our employees. We have kept in place the additional safety measures for employees continuing critical on-site work at either the Company or customers’ locations and offer flexible remote or hybrid working arrangements. We have taken, and will continue to take, actions in accordance with the applicable local guidance, such as the guidance provided by the

12

Centers for Disease Control and Prevention in the United States, to protect our employees so they can safely and effectively perform their work duties.

Annually we request our employees to complete a Company-wide employee engagement survey. The survey is facilitated internally through our Human Resources department. The survey reflects questions to gauge employee sentiments toward current trends and issues including company direction and strategy, communication by management, individual development, team culture, and overall satisfaction. With the information provided by the annual engagement survey, leadership is provided key insights and valuable feedback which we continue to implement in our Company-wide action plans with the intent to focus on key areas to prioritize, enhance, and drive continued increase in employee engagement, learning and development, and professional growth for our employees.

AVAILABLE INFORMATION

The public may access any materials the Company files with the Securities and Exchange Commission (“SEC”), including our annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, proxy statements for our annual stockholder meetings, and amendments to those reports, through the SEC’s Interactive Data Electronic Applications system at http://www.sec.gov. These reports are also available free of charge on our website, www.cantaloupe.com, as soon as reasonably practicable after we electronically file the material with the SEC. In addition, our website includes, among other things, charters of the various committees of our Board of Directors and our code of business conduct and ethics applicable to all employees, officers and directors. Within the time period required by the SEC, we will post on our website any amendment to the code of business conduct and ethics and any waiver applicable to any executive officer, director or senior financial officer. We use our website as a means of disclosing material non-public information and for complying with our disclosure obligations under Regulation FD. Accordingly, investors should monitor our website, in addition to following our press releases, SEC filings and public conference calls and webcasts.

13

Item 1A. Risk Factors.

The risks and uncertainties describe below are not the only ones we face. There may be other unknown or unpredictable economic, business, competitive, regulatory or other factors that could have material adverse effects on our future results. The occurrence of any of these risks could materially adversely affect our business, financial condition, results of operations and cash flows. Accordingly, you should carefully consider the following risk factors, as well as other information contained in or incorporated by reference in this Annual Report.

Summary

You should read this summary together with the more detailed description of each risk factor contained below. Our business operations are subject to numerous risks and uncertainties, including those outside of our control, that could cause our actual results to be harmed, including risks regarding the following:

Risks related to our business and our industry:

•General economic, market or business conditions unrelated to our operating performance, including global supply chain disruptions and inflationary pressures could adversely affect our business and results of operations.

•We have a history of losses since inception and if we continue to incur losses, the price of our shares can be expected to fall.

•The COVID-19 pandemic has and may continue to significantly and adversely impact our business.

•Impacts of widespread inflation could negatively affect our industry.

•If we are not able to implement successful enhancements and new features for our products and services, our business could be materially and adversely affected.

•Substantially all of the network service contracts with our customers are terminable for any or no reason upon thirty to sixty days’ advance notice.

•We may not successfully implement our go-to-market strategy which may adversely affect growth and profitability.

•We engage in the outsourcing of engineering work, including outsourcing of software work overseas.

•Our ability to commercially manage the transition from the 3G network could lead to competitive disadvantage in the marketplace.

•The loss of one or more of our key customers could significantly reduce our revenues, results of operations, and increase net losses.

•Increases in card association and debit network interchange fees could increase our operating costs or otherwise adversely affect our operations.

•Our efforts to expand into international markets may not be successful; our products and services may not gain traction in new markets; managing international operations may be challenging or may fail.

•Geopolitical conflicts, including the conflict between Russia and Ukraine, may adversely affect our business and results of operations.

Operational and liquidity:

•We depend on our key personnel and, if they leave us, or if we are unable to attract highly skilled personnel, our business could be adversely affected.

•Disruptions to our systems, breaches in the security of transactions involving our products or services, or failure of our processing systems could adversely affect our reputation, business and results of operations.

14

•The termination of our relationships with certain third-party suppliers upon whom we rely for services that are critical to our products could adversely affect our business and delay achievement of our business plan.

•We rely on other card payment processors, and if they fail or no longer agree to provide their services or we fail to operate in compliance with the requirements of those relationships, our customer relationships could be adversely affected, and we could lose business.

•Disruptions at other participants in the financial system could prevent us from delivering our cashless payment services.

•Any increase in chargebacks not paid by our customers may adversely affect our results of operations, financial condition and cash flows.

•Our dependence on proprietary technology and limited ability to protect our intellectual property may adversely affect our ability to compete.

•We may require additional financing or find it necessary to raise capital to sustain our operations and without it we may not be able to achieve our business plan.

•Failure to comply with any of the financial covenants under the Company’s credit agreement could result in an event of default which may accelerate our outstanding indebtedness or other obligations and have a material adverse impact on our business, liquidity position and financial position.

•We may not fully realize the benefits of acquisitions, it may take longer than we anticipate for us to achieve those benefits, they may be difficult to integrate, may disrupt our business, or divert management attention and may adversely affect our financial condition.

Legal, regulatory, and compliance risks:

•We are subject to laws and regulations that affect the products, services and markets in which we operate. Failure by us to comply with these laws or regulations would have an adverse effect on our business, financial condition, or results of operations.

•The accounting review of our previously issued financial statements and the audits of prior fiscal years have been time-consuming and expensive, has resulted in claims and lawsuits , and may result in additional expense and/or litigation.

•Matters relating to or arising from the restatement and the 2019 Investigation, including adverse publicity and potential concerns from our customers, and enforcement proceedings could continue to have an adverse effect on our business and financial condition.

•Remaining regulatory matters may require significant time and attention, result in substantial expenses and lead to adverse publicity.

•We and certain of our former officers and directors could be subject to future claims and lawsuits, which could require significant additional management time and attention, result in significant additional legal expenses or result in government enforcement actions.

•Failure to maintain effective systems of internal control over financial reporting and disclosure controls and procedures could cause a loss of confidence in our financial reporting and adversely affect the trading price of our common stock.

Risks related to our common stock:

•Director and officer liability is limited and shareholders may have limited rights to recover against directors for breach of fiduciary duty.

•An active trading market for our common stock may not be maintained.

15

•If securities and/or industry analysts fail to continue publishing research about our business, if they change their recommendations adversely, or if our results of operations do not meet their expectations, our stock price and trading volume could decline.

•There is a risk that we may be dropped from inclusion in the Russell 2000® Index which could result in a decline in the price of our stock.

•Upon certain fundamental transactions involving the Company, such as a merger or sale of substantially all of our assets, we may be required to distribute the liquidation preference then due to the holders of our Series A Preferred Stock which would reduce the amount of the distributions otherwise to be made to the holders of our common stock in connection with such transactions.

16

Risks related to our business and our industry

General economic, market or business conditions unrelated to our operating performance, including global supply chain disruptions and inflationary pressures could adversely affect our business and results of operations.

The global payments technology industry depends heavily on the overall level of consumer, business and government spending. We are exposed to general economic conditions that affect consumer confidence, spending, and discretionary income and changes in consumer purchasing habits. A sustained deterioration in general economic conditions in the markets in which we operate, supply chain disruptions, inflationary pressure or interest rate fluctuations, may adversely affect our financial performance by reducing the number or active devices, active customers and total number of transactions using our payment solutions.

A downturn in the economy and other adverse economic trends may accelerate the timing, or increase the impact of, risks to our financial performance. These trends could include the following:

•low levels of consumer and business confidence typically associated with recessionary environments may result in decreased spending by consumers;

•high unemployment may result in decreased spending by consumers;

•budgetary concerns in the United States and other countries could affect sovereign credit ratings, and impact consumer confidence and spending;

•supply chain disruptions may result in decreased spending by consumers whose ability to provide goods and services is materially impacted;

•supply chain disruptions could impact our ability to purchase devices for existing or prospective customers;

•current and potential future inflationary pressures may adversely impact spending by consumers;

•emerging market economies tend to be more sensitive to adverse economic trends than the more established markets we serve;

In addition, climate-related events, including extreme weather events and natural disasters and their effect on critical infrastructure in the U.S. or internationally, could have similar adverse effects on our customers and our operations.

Furthermore, shareholders, customers and other stakeholders have begun to consider how corporations are addressing environmental, social and governance (“ESG”) issues. Government regulators, investors, customers and the general public are increasingly focused on ESG practices and disclosures, and views about ESG are diverse and rapidly changing. These shifts in investing priorities may result in adverse effects on the trading price of our common stock if investors determine that the Company has not made sufficient progress on ESG matters. We could also face potential negative ESG-related publicity in traditional media or social media if shareholders or other stakeholders determine that we have not adequately considered or addressed ESG matters.

We have a history of losses since inception and if we continue to incur losses, the price of our shares can be expected to fall.

We experienced losses from inception through June 30, 2012, and from fiscal year 2015 through fiscal year 2022. For fiscal years 2022, 2021, and 2020, we incurred a net loss of $1.7 million, $8.7 million, and $40.6 million, respectively. In light of our recent history of losses as well as the length of our history of losses, profitability in the foreseeable future is not assured. Until we achieve profitability, we will be required to use our cash and cash equivalents on hand and may raise capital to meet cash flow requirements including the issuance of common stock or debt financing. Additionally, if we continue to incur losses in the future, the price of our common stock can be expected to fall.

The coronavirus disease 2019 (“COVID-19”) pandemic has and may continue to significantly and adversely impact our business.

The global spread of the COVID-19 pandemic has created significant volatility, uncertainty and economic disruption on our business. Electronic payment transaction volume within unattended markets decreased significantly at the onset of the

17

pandemic, as government authorities imposed forced closure of non-essential businesses and social distancing protocols, significantly reducing foot traffic to distributed assets containing our electronic payment solutions and reducing discretionary spending by consumers.

As a result of COVID-19, the technology industry is experiencing disruptions within its supply chain. We have experienced, and may continue to experience delays in securing the components and finished goods of our hardware products that we market and sell to our customers. Supply chain delays could cause shortages of our hardware products, which could negatively affect our ability to retain and acquire customers and could adversely impact our financial results.

The extent to which the COVID-19 pandemic continues to impact our business, operations and financial results will depend on numerous evolving factors that we are not able to accurately predict, including: the duration and scope of the pandemic; potential mutations of COVID-19; the efficacy of vaccines and treatment developments and their deployment; governmental, business and individuals’ actions that have been and continue to be taken in response to the pandemic; and the impact of the pandemic on economic activity and actions taken in response. Furthermore, even as containment measures are lifted there can be no assurance as to whether further measures will be implemented, or the time required to sustain operations and sales at pre-pandemic levels. There may also be increased marketplace consolidation as companies are challenged to respond to the continued evolving conditions of COVID-19.

A sustained or recurring downturn could result in a decrease in the fair value of our goodwill or other intangible assets, causing them to exceed their carrying value. This may require us to recognize an impairment to those assets. Further, the COVID-19 pandemic could decrease consumer spending, adversely affect demand for our technology and services, cause one or more of our customers and partners to file for bankruptcy protection or go out of business, cause one or more of our customers to fail to renew, terminate, or renegotiate their contracts, affect the ability of our sales team to travel to potential customers, impact expected spending from new customers and negatively impact collections of accounts receivable, all of which could adversely affect our business, results of operations and financial condition. In response to the outbreak, we agreed to concessions on price and/or payment terms with certain customers who have been negatively impacted by the COVID-19 pandemic, and may negotiate additional concessions on price and/or payment terms.

It is not possible for us to predict the future impact of the pandemic and its effects on our business, results of operations or financial condition at this time.

The impact of inflation could negatively affect our business, our industry, and our customer base.

Our own costs, including labor, hardware, services, technology providers, and other variable expenses could be severely impacted by severe, widespread or continuing inflation. Our customer base includes many small businesses, some of which operate on tight margins. Our customers may not successfully navigate a rising cost environment, causing collection issues or bankruptcies. Inflation could seriously erode the discretionary buying decisions of consumers, impacting size of purchases or volumes at our unattended points of sale.

If we are not able to implement successful enhancements and new features for our products and services, our business could be materially and adversely affected.

Our success depends on our ability to develop new products and services to address the rapidly evolving market for cashless payments and cloud and mobile solutions for the self-service retail markets. Rapid and significant technological changes continue to confront the industries in which we operate, including developments in proximity payment devices. These new services and technologies may be superior to, impair, or render obsolete the products and services we currently offer or the technologies we currently use to provide them. Incorporating new technologies into our products and services may require substantial expenditures and take considerable time, and we may not be successful in realizing a return on these development efforts in a timely manner or at all. There can be no assurance that any new products or services we develop and offer to our customers will achieve significant commercial acceptance. Our ability to develop new products and services may be inhibited by industry-wide standards, payment card networks, existing and future laws and regulations, resistance to change from our customers, challenges of integration with a wide variety of legacy end-point machines, or third parties’ intellectual property rights. If we are unable to provide enhancements and new features for our products and services or to develop new products and services that achieve market acceptance or that keep pace with rapid technological developments and evolving industry standards, our business would be materially and adversely affected.

In addition, because our products and services are designed to operate with a variety of systems, infrastructures, and devices, we need to continuously modify and enhance our products and services to keep pace with changes in mobile, software,

18

communication, and database technologies. We may not be successful in either developing these modifications and enhancements or in bringing them to market in a timely and cost-effective manner. Any failure of our products and services to continue to operate effectively with third-party infrastructures and technologies could reduce the demand for our products and services, result in dissatisfaction of our customers, and materially and adversely affect our business.

Substantially all of the service contracts with our customers are terminable for any or no reason upon thirty to sixty days’ advance notice.

Substantially all of our customers may terminate their services with us for any or no reason upon providing us with thirty to sixty- days’ advance notice. Accordingly, consistent demand for and satisfaction with our products by our customers is critical to our financial condition and future success. Problems, outages, defects, or other issues with our products or services or competition in the marketplace could cause us to lose a substantial number of our customers with minimal notice. If a substantial number of our customers were to exercise their termination rights, it would result in a material adverse effect to our business, operating results, and financial condition.

We may not successfully implement our go-to-market strategy which may adversely affect growth and profitability.

Our current core business is highly concentrated among several large customers in the vending industry. We have made inroads into other adjacent markets including micro-markets, laundry, gaming, entertainment, vehicle services, and other commercial payments applications and continued expansion into these markets is a substantial piece of our potential future growth prospects. Changing technology, customer preferences, and competitor actions may limit our ability to successfully grow and expand beyond our core business.

We face significant risks to our business when we engage in the outsourcing of engineering work, including outsourcing of software work overseas, which, if not properly managed, could result in the loss of valuable intellectual property and increased costs due to inefficient and poor work product, which could harm our business, including our financial results, reputation, and brand.

We may, from time-to-time, outsource engineering work related to the design, development, and operations of our products and services, typically to save money and gain access to additional engineering resources. We have worked, and expect to work in the future, with companies located in jurisdictions outside of the U.S., including, but not limited to Ukraine, Columbia, and India. If we are unable to properly manage and oversee the outsourcing of engineering and other work to third parties located internationally that operate under different laws and regulations than those in the U.S., we could suffer the loss of valuable intellectual property, or the loss of the ability to claim such intellectual property, including patents and trade names. Additionally, instead of saving money, we could in fact incur significant additional costs because of inefficient engineering services and poor work product. As a result, our business would be harmed, including our financial results, reputation, and brand.

Our ability to commercially manage the transition from the 3G network could lead to competitive disadvantage in the marketplace.

Our transition away from the 3G wireless network is nearing completion as the cellular service providers phase these networks out in North America through the end of the 2022 calendar year. This transition has and will continue to affect many of our active devices and has required significant customer retention programs and resources to ensure that our existing customer base is properly transitioned to the new platform. This change affects our industry and will also lead to changes with our competitors and their customers. Our ability to successfully transition the remaining impacted devices and provide the new platform for our existing and new customers is critical to our strategy, our network and to the competitive landscape in the marketplace.

The loss of one or more of our key customers could significantly reduce our revenues, results of operations, and increase net losses.

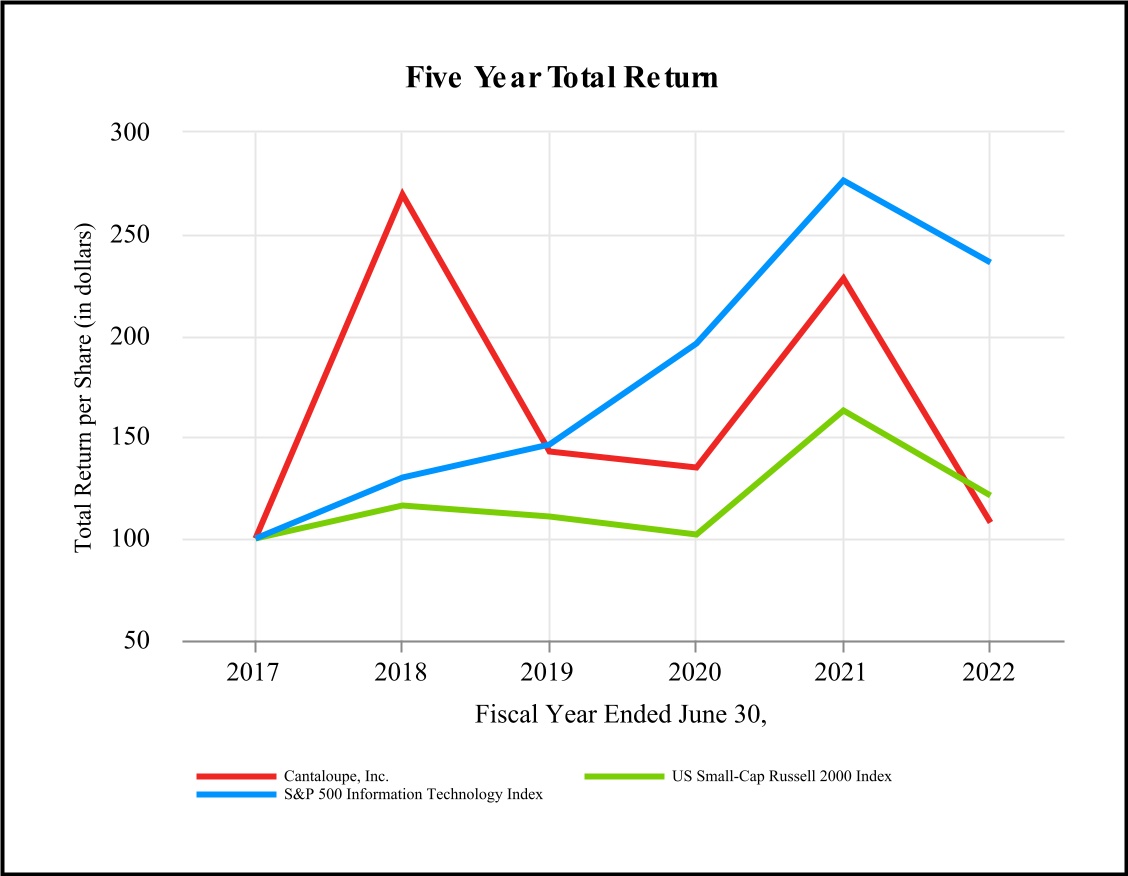

We have derived, and believe we will continue to derive, a significant portion of our revenues from one large customer or a limited number of large customers. Customer concentrations for the years ended June 30, 2022, 2021 and 2020 were as follows:

| For the year ended June 30, | ||||||||||||||||||||

| Single customer | 2022 | 2021 | 2020 | |||||||||||||||||

| Total revenue | 14 | % | 16 | % | 16 | % | ||||||||||||||

19

The loss of such customers could materially adversely affect our revenues. Additionally, a major customer in one year may not purchase any of our products or services in another year, which may negatively affect our financial performance. We have offered, and may in the future offer, discounts to our large customers to incentivize them to continue to utilize our products and services. If we are required to sell products to any of our large customers at reduced prices or unfavorable terms, our revenue and earnings could be materially adversely affected. Further, there is no assurance that our customers will continue to utilize our transaction processing and related services as our customer agreements are generally cancellable by the customer on thirty to sixty days’ notice.

Increases in card association and debit network interchange fees could increase our operating costs or otherwise adversely affect our operations.

We are obligated to pay interchange fees and other network fees set by the bankcard networks to the card issuing bank and the bankcard networks for each transaction we process through our network. From time to time, card associations and debit networks increase the organization and/or processing fees, known as interchange fees that they charge. Under our processing agreements with our customers, we are permitted to pass along these fee increases to our customers through corresponding increases in our processing fees. Passing along such increases could result in some of our customers canceling their contracts with us. Consequently, it is possible that competitive pressures will result in our Company absorbing some or all of the increases in the future, which would increase our operating costs, reduce our gross profit and adversely affect our business.

We are expending significant resources into certain international initiatives. Our efforts may fail, adversely affecting our results.

As we expand into international markets, we may not be successful, or our plans may be delayed. Our Company is inexperienced in managing international operations. Our products will need to be localized in some cases and if our localization efforts fail or are delayed or our products and services do not gain traction in new markets, our business could be adversely affected.

Geopolitical conflicts, including the conflict between Russia and Ukraine, may adversely affect our business and results of operations.

While we do not currently have employees, customers or corporate offices in impacted areas, we have worked, and expect to work in the future, with companies located in jurisdictions outside of the U.S., including, but not limited to Ukraine. In addition, we are focused on international expansion. As a result, our operations and international expansion efforts could be impacted by economic, political and other conditions resulting from the current conflict between Russia and Ukraine, which could, among other things, lead to a reduction in consumer, government or corporate spending, international sanctions, embargoes, heightened inflation, volatility in global financial markets, increased cyber disruptions or attacks, higher supply chain costs and increased tensions between the United States and countries in which we operate, which could result in charges related to the recoverability of assets, including financial assets, long-lived assets and goodwill and other losses, and could adversely affect our financial position and results of operations. To the extent the invasion of Ukraine by Russia adversely affects our business, it may also have the effect of heightening many other risks disclosed in this Form 10-K, any of which could have a material adverse effect on our business and results of operations.

Operational and liquidity

We depend on our key personnel and, if they leave us, or if we are unable to attract highly skilled personnel, our business could be adversely affected.

Our success and future growth also depends, to a significant degree, on the skills and continued services of our management team. Further, due to the complexity of the work required to make needed improvements within the Company, it may be difficult for us to retain existing senior management and new hires, sales personnel, and development and engineering personnel critical to our ability to execute our business plan, which could result in harm to key customer relationships, loss of key information, expertise or know-how and unanticipated recruitment and training costs. We may experience a loss of productivity due to the departure of key personnel and the associated loss of institutional knowledge, or while new personnel integrate into our business and transition into their respective roles. Our future success also depends on our ability to attract and motivate highly skilled technical, managerial, sales, marketing and customer service personnel, including members of our management team. The labor market has been very challenging this fiscal year, with several key functions and departments experiencing high turnover. These changes are disruptive and expensive. Continued turnover could prevent us from achieving,

20

or significantly delay achievement, of our business and operational goals and could adversely affect our business and results of operations.

Disruptions to our systems, breaches in the security of transactions involving our products or services, or failure of our processing systems could adversely affect our reputation, business and results of operations.

We rely on information technology and other systems to transmit financial information of consumers making cashless transactions and to provide accounting and inventory management services to our customers. As such, the information we transmit and/or maintain is exposed to the ever-evolving threat of compromised security, in the form of a risk of potential breach, system failure, computer virus, cyber-attack or unauthorized or fraudulent use by consumers, customers, company employees, or employees of third party vendors. A cybersecurity breach could result in disclosure of confidential information and intellectual property, or cause operational disruptions and compromised data. We may be unable to anticipate or prevent techniques to obtain unauthorized access or to sabotage systems because they change frequently and often are not detected until after an incident has occurred.

In addition, our processing systems may experience errors, interruptions, delays or damage from a number of causes, including, but not limited to, power outages, hardware, software and network failures, internal design, manual or usage errors, terrorism, workplace violence or wrongdoing, catastrophic events, climate-related events such as natural disasters and severe weather conditions. The steps we take to deter and mitigate these risks, including annual validation of our compliance with the Payment Card Industry Data Security Standard, may not be successful, and any resulting compromise or loss of data or systems could adversely impact the marketplace acceptance of our products and services, and could result in significant remedial expenses to not only assess and repair any damage to our systems, but also to reimburse customers for losses that occur from service interruptions or the fraudulent use of confidential data. Additionally, we could become subject to significant fines, litigation, and loss of reputation, potentially impacting our financial results.

In addition, following an acquisition, we take steps to ensure our data and system security protection measures cover the acquired business as part of our integration process. As such, there may be a period of increased cybersecurity risk during the period between closing an acquisition and the completion of our data and system security integration.

The termination of our relationships with certain third-party suppliers upon whom we rely for services that are critical to our products could adversely affect our business and delay achievement of our business plan.

The operation of our networked devices depends upon the capacity, reliability and security of services provided to us by our wireless telecommunication services providers, equipment manufacturers and other suppliers. In addition, if we terminate relationships with our current telecommunications service providers and other third-party suppliers, we may have to replace hardware that is part of our existing ePort or Seed products that are already installed in the marketplace. This could significantly harm our reputation and could cause us to lose customers and revenues.

We rely on other card payment processors, and if they fail or no longer agree to provide their services or we fail to operate in compliance with the requirements of those relationships, our customer relationships could be adversely affected, and we could lose business.

We rely on agreements with other large payment processing organizations, primarily Fiserv Inc., JPMorgan Chase & Co., and Global Payments, Inc. to enable us to provide card authorization, data capture and transmission, settlement and merchant accounting services for the customers we serve. The termination by our card processing providers of their arrangements with us or their failure to perform their services efficiently and effectively would adversely affect our relationships with the customers whose accounts we serve and may cause those customers to terminate their processing agreements with us.

Further, substantially all of the cashless payment transactions handled by our network involve Visa U.S.A. Inc. (“Visa”) or MasterCard International Incorporated ("MasterCard"). If we fail to comply with the applicable standards or requirements of the Visa and MasterCard card associations relating to security, Visa or MasterCard could suspend or terminate our registration with them. The termination of our registration with them or any changes in the Visa or MasterCard rules that would impair our registration with them could require us to stop providing cashless payment services through our network. In such event, our business plan and/or competitive advantages in the market place would be materially adversely affected.

Disruptions at other participants in the financial system could prevent us from delivering our cashless payment services.

The operations and systems of many participants in the financial system are interconnected. Many of the transactions that involve our cashless payment services rely on multiple participants in the financial system to accurately move funds and

21

communicate information to the next participant in the transaction chain. A disruption for any reason at one of the participants in the financial system could impact our ability to cause funds to be moved in a manner to successfully deliver our services. Although we work with other participants to avoid any disruptions, there is no assurance that such efforts will be effective. Such a disruption could lead to the inability for us to deliver services, reputational damage, lost customers and lost revenue, loss of customers’ confidence, as well as additional costs, all of which could have a material adverse effect on our revenues, profitability, financial condition, and future growth.

Any increase in chargebacks not paid by our customers may adversely affect our results of operations, financial condition and cash flows.