|

December 2023 Pricing Supplement No. 24 Registration Statement No. 333-275587 Dated December 6, 2023 Filed pursuant to Rule 424(b)(2) |

Fixed to Floating Rate Notes due 2033

Based on the Secured Overnight Financing Rate (SOFR)

(Using a Daily Compounding Calculation Method)

During the floating interest rate period (as defined below), the interest rate on the notes will be based on the Secured Overnight Financing Rate (“SOFR”), compounded daily over a quarterly interest payment period in accordance with the specific formula described under “Description of Debt Securities—SOFR Debt Securities” in the accompanying prospectus. We refer to this compounded SOFR rate as the base rate. Interest will accrue and be payable on the notes quarterly, in arrears, (i) from the original issue date to December 8, 2026: at a rate of 6.00% per annum and (ii) from December 8, 2026 to maturity: at a variable rate per annum equal to the base rate plus 1.50%, subject to the minimum interest rate of 2.00% per annum and the maximum interest rate of 7.00% per annum, as determined on the interest payment period end-date for the relevant interest payment period (or the rate cut-off date for the final interest payment period).

SOFR has been identified by the Federal Reserve Bank of New York’s Alternative Reference Rates Committee as its recommended alternative to U.S. dollar LIBOR for certain financial contracts and is intended to be a broad measure of the cost of borrowing cash overnight collateralized by U.S. Treasury securities. For a description of SOFR, see “Secured Overnight Financing Rate” below. Publication of SOFR began on April 3, 2018 and it therefore has a very limited history. Any failure of SOFR to gain market acceptance could adversely affect the notes. For further discussion of risks related to the notes, including these and other risks related to the fact that the base rate is determined by reference to SOFR, see “Risk Factors” beginning on page 6.

All payments are subject to the credit risk of Morgan Stanley. If Morgan Stanley defaults on its obligations, you could lose some or all of your investment. These securities are not secured obligations and you will not have any security interest in, or otherwise have any access to, any underlying reference asset or assets.

| FINAL TERMS | |||

| Issuer: | Morgan Stanley | ||

| Aggregate principal amount: | $1,661,000 | ||

| Issue price: | $1,000 per note | ||

| Stated principal amount: | $1,000 per note | ||

| Pricing date: | December 6, 2023 | ||

| Original issue date: | December 8, 2023 (2 business days after the pricing date) | ||

| Maturity date: | December 8, 2033. See “—Interest payment period end-dates” and “—Interest payment dates” below. | ||

| Interest accrual date: | December 8, 2023 | ||

| Payment at maturity: | The payment at maturity per note will be the stated principal amount plus accrued and unpaid interest, if any | ||

| Base rate: | The Secured Overnight Financing Rate (compounded daily over a quarterly interest payment period in accordance with the specific formula described in the accompanying prospectus) (“compounded SOFR”). As further described in the accompanying prospectus, (i) in determining the base rate for a U.S. government securities business day, the base rate generally will be the rate in respect of such day that is provided on the following U.S. government securities business day and (ii) in determining the base rate for any other day, such as a Saturday, Sunday or holiday, the base rate generally will be the rate in respect of the immediately preceding U.S. government securities business day that is provided on the following U.S. government securities business day. Please see “Description of Debt Securities—SOFR Debt Securities” in the accompanying prospectus. | ||

| Interest rate: |

From and including the original issue date to but excluding December 8, 2026 (the “fixed interest rate period”): 6.00% per annum From and including December 8, 2026 to but excluding the maturity date (the “floating interest rate period”): Base rate plus 1.50%; subject to the minimum interest rate and the maximum interest rate. See “Description of Debt Securities—Floating Rate Debt Securities” in the accompanying prospectus, subject to and as modified by “Description of Debt Securities—SOFR Debt Securities” in the accompanying prospectus. The level of the base rate applicable to each interest payment period during the floating interest rate period will be determined on the interest payment period end-date for such interest payment period (or the rate cut-off date for the final interest payment period). Interest for each interest payment period during the floating interest rate period is subject to the minimum interest rate of 2.00% per annum and the maximum interest rate of 7.00% per annum. | ||

| Index maturity: | Daily | ||

| Index currency: | U.S. dollars | ||

| Interest payment periods: |

During the fixed interest rate period: Quarterly During the floating interest rate period: Quarterly. With respect to an interest payment date during the floating interest rate period, the period from and including the second most recent interest payment period end-date (or from and including December 8, 2026 in the case of the first interest payment period during the floating interest rate period) to but excluding the immediately preceding interest payment period end-date; provided that (i) the interest payment period with respect to the final interest payment date (i.e., the maturity date) will be the period from and including the second-to-last interest payment period end-date to but excluding the maturity date (the final interest payment period end-date) and (ii) with respect to such final interest payment period, the level of SOFR for each calendar day in the period from and including the rate cut-off date to but excluding the maturity date shall be the level of SOFR in respect of such rate cut-off date. | ||

| Interest payment period end-dates: | With respect to the floating interest rate period, the 8th of each March, June, September and December, commencing March 2027 and ending on the maturity date; provided that if any scheduled interest payment period end-date, other than the maturity date, falls on a day that is not a business day, it will be postponed to the following business day. If the scheduled final interest payment period end-date for the notes (i.e., the maturity date) falls on a day that is not a business day, the payment of principal and interest will be made on the next succeeding business day, but interest on that payment will not accrue during the period from and after the scheduled final interest payment period end-date. | ||

| Interest payment dates: |

During the fixed interest rate period: Each March 8, June 8, September 8 and December 8, commencing March 8, 2024 to and including December 8, 2026; provided that if any such day is not a business day, that interest payment will be made on the next succeeding business day and no adjustment will be made to any interest payment made on that succeeding business day. During the floating interest rate period: The second business day following each interest payment period end-date; provided that the interest payment date with respect to the final interest payment period will be the maturity date. If the scheduled maturity date falls on a day that is not a business day, the payment of principal and interest will be made on the next succeeding business day, but interest on that payment will not accrue during the period from and after the scheduled maturity date. | ||

| Rate cut-off date: | The second U.S. government securities business day prior to the maturity date | ||

| Business day: | New York | ||

| Day-count convention: | 30/360 (Bond Basis) | ||

| Minimum interest rate: | 2.00% per annum during the floating interest rate period | ||

| Maximum interest rate: | 7.00% per annum during the floating interest rate period | ||

| Estimated value on the pricing date: | $980.80 per note. See “The Notes” on page 3. | ||

| Commissions and issue price: | Price to public | Agent’s commissions(1) | Proceeds to issuer(2) |

| Per note | $1,000 | $17.50 | $992.50 |

| Total | $1,661,000 | $29,067.50 | $1,631,932.50 |

| (1) | Selected dealers and their financial advisors will collectively receive from the agent, MS & Co., a fixed sales commission of $17.50 for each note they sell. See “Supplemental Information Concerning Plan of Distribution; Conflicts of Interest.” For additional information, see “Plan of Distribution (Conflicts of Interest)” in the accompanying prospectus supplement. |

| (2) | See “Use of Proceeds and Hedging” on page 9. |

The notes involve risks not associated with an investment in ordinary debt securities. See “Risk Factors” beginning on page 6.

The Securities and Exchange Commission and state securities regulators have not approved or disapproved these securities, or determined if this pricing supplement or the accompanying prospectus supplement and prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

You should read this document together with the

related prospectus supplement and prospectus,

each of which can be accessed via the hyperlinks below.

| Prospectus Supplement dated November 16, 2023 | Prospectus dated November 16, 2023 |

The notes are not deposits or savings accounts and are not insured by the Federal Deposit Insurance Corporation or any other governmental agency or instrumentality, nor are they obligations of, or guaranteed by, a bank.

Fixed to Floating Rate Notes due 2033

Based on the Secured Overnight Financing Rate (SOFR)

(Using a Daily Compounding Calculation Method)

| Terms continued from previous page: | |

| Redemption: | Not applicable |

| Specified currency: | U.S. dollars |

| No listing: | The notes will not be listed on any securities exchange. |

| CUSIP / ISIN: | 61761J5W5 / US61761J5W51 |

| Book-entry or certificated note: | Book-entry |

| Business day: | New York |

| Agent: | Morgan Stanley & Co. LLC (“MS & Co.”), a wholly owned subsidiary of Morgan Stanley. See “Supplemental Information Concerning Plan of Distribution; Conflicts of Interest.” |

| Calculation agent: |

Morgan Stanley Capital Services LLC. All determinations made by the calculation agent will be at the sole discretion of the calculation agent and will, in the absence of manifest error, be conclusive for all purposes and binding on you, the trustee and us. All determinations related to the base rate will be made by the calculation agent. All percentages used in or resulting from any calculation of the rate of interest on the notes will be rounded, if necessary, to the nearest one hundred-thousandth of a percentage point, with 0.000005% rounded up to 0.00001%, and all U.S. dollar amounts used in or resulting from these calculations on the notes will be rounded to the nearest cent, with one-half cent rounded upward. Because the calculation agent is our affiliate, the economic interests of the calculation agent and its affiliates may be adverse to your interests as an investor in the notes, including with respect to certain determinations and judgments that the calculation agent must make in determining the payment that you will receive on each interest payment date and at maturity. Please see “Description of Debt Securities—SOFR Debt Securities” in the accompanying prospectus. The calculation agent is obligated to carry out its duties and functions as calculation agent in good faith and using its reasonable judgment. |

| Trustee: | The Bank of New York Mellon |

| December 2023 | Page 2 |

Fixed to Floating Rate Notes due 2033

Based on the Secured Overnight Financing Rate (SOFR)

(Using a Daily Compounding Calculation Method)

The Notes

The notes are debt securities of Morgan Stanley. From the original issue date until December 8, 2026, interest on the notes will accrue and be payable quarterly, in arrears, at 6.00% per annum, and thereafter, during the floating interest rate period, interest on the notes will accrue and be payable quarterly, in arrears, at a variable rate per annum equal to the base rate plus 1.50%, subject to the minimum interest rate of 2.00% per annum and the maximum interest rate of 7.00% per annum, as determined on the interest payment period end-date for the relevant interest payment period (or the rate cut-off date for the final interest payment period). The base rate is SOFR, compounded daily over a quarterly interest payment period, as further described under “Description of Debt Securities—SOFR Debt Securities” in the accompanying prospectus.

We describe the basic features of the notes in the section of the accompanying prospectus supplement called “Description of Notes,” subject to and as modified by the provisions described herein. In addition, we describe the basic features of the notes during the fixed interest rate period in the section of the accompanying prospectus called “Description of Debt Securities—Fixed Rate Debt Securities” and during the floating interest rate period in the section of the accompanying prospectus called “Description of Debt Securities—Floating Rate Debt Securities,” in each case subject to and as modified by the provisions described herein.

We describe how interest is calculated, accrued and paid during the fixed interest rate period under “Description of Debt Securities—Fixed Rate Debt Securities” in the accompanying prospectus. We describe how interest is paid during the floating interest rate period under “Description of Debt Securities—Floating Rate Debt Securities” in the accompanying prospectus, subject to and as modified by the provisions described under “Description of Debt Securities—SOFR Debt Securities” in the accompanying prospectus with respect to the compounding method used to calculate accrued interest during the floating interest rate period and the application of the spread to such method.

All payments on the notes are subject to the credit risk of Morgan Stanley.

The stated principal amount and issue price of each note is $1,000. This price includes costs associated with issuing, selling, structuring and hedging the notes, which are borne by you, and, consequently, the estimated value of the notes on the pricing date is less than the issue price. We estimate that the value of each note on the pricing date is $980.80.

What goes into the estimated value on the pricing date?

In valuing the notes on the pricing date, we take into account that the notes comprise both a debt component and a performance-based component linked to SOFR. The estimated value of the notes is determined using our own pricing and valuation models, market inputs and assumptions relating to SOFR, instruments based on SOFR, volatility and other factors including current and expected interest rates, as well as an interest rate related to our secondary market credit spread, which is the implied interest rate at which our conventional fixed rate debt trades in the secondary market.

What determines the economic terms of the notes?

In determining the economic terms of the notes, including the interest rate, the spread, the minimum interest rate and the maximum interest rate applicable to each interest payment period during the floating interest rate period, we use an internal funding rate, which is likely to be lower than our secondary market credit spreads and therefore advantageous to us. If the issuing, selling, structuring and hedging costs borne by you were lower or if the internal funding rate were higher, one or more of the economic terms of the securities would be more favorable to you.

What is the relationship between the estimated value on the pricing date and the secondary market price of the notes?

The price at which MS & Co. purchases the notes in the secondary market, absent changes in market conditions, including those related to interest rates and SOFR, may vary from, and be lower than, the estimated value on the pricing date, because the secondary market price takes into account our secondary market credit spread as well as the bid-offer spread that MS & Co. would charge in a secondary market transaction of this type, the costs of unwinding the related hedging transactions and other factors.

MS & Co. may, but is not obligated to, make a market in the notes and, if it once chooses to make a market, may cease doing so at any time.

| December 2023 | Page 3 |

Fixed to Floating Rate Notes due 2033

Based on the Secured Overnight Financing Rate (SOFR)

(Using a Daily Compounding Calculation Method)

Secured Overnight Financing Rate

SOFR is published by the New York Federal Reserve and is intended to be a broad measure of the cost of borrowing cash overnight collateralized by U.S. Treasury securities. The New York Federal Reserve reports that SOFR includes all trades in the Broad General Collateral Rate and bilateral Treasury repurchase agreement (repo) transactions cleared through the delivery-versus-payment service offered by the Fixed Income Clearing Corporation (the “FICC”), a subsidiary of the Depository Trust and Clearing Corporation (“DTCC”), and SOFR is filtered by the New York Federal Reserve to remove some (but not all) of the foregoing transactions considered to be “specials.” According to the New York Federal Reserve, “specials” are repos for specific-issue collateral, which take place at cash-lending rates below those for general collateral repos because cash providers are willing to accept a lesser return on their cash in order to obtain a particular security.

The New York Federal Reserve reports that SOFR is calculated as a volume-weighted median of transaction-level tri-party repo data collected from The Bank of New York Mellon as well as General Collateral Finance Repo transaction data and data on bilateral Treasury repo transactions cleared through the FICC’s delivery-versus-payment service. The New York Federal Reserve also notes that it obtains information from DTCC Solutions LLC, an affiliate of DTCC.

If data for a given market segment were unavailable for any day, then the most recently available data for that segment would be utilized, with the rates on each transaction from that day adjusted to account for any change in the level of market rates in that segment over the intervening period. SOFR would be calculated from this adjusted prior day’s data for segments where current data were unavailable, and unadjusted data for any segments where data were available. To determine the change in the level of market rates over the intervening period for the missing market segment, the New York Federal Reserve would use information collected through a daily survey conducted by its Trading Desk of primary dealers’ repo borrowing activity. Such daily survey would include information reported by Morgan Stanley & Co. LLC, a wholly owned subsidiary of Morgan Stanley, as a primary dealer.

The New York Federal Reserve notes on its publication page for SOFR that use of SOFR is subject to important limitations, indemnification obligations and disclaimers, including that the New York Federal Reserve may alter the methods of calculation, publication schedule, rate revision practices or availability of SOFR at any time without notice.

Each U.S. Government Securities Business Day, the New York Federal Reserve publishes SOFR on its website at approximately 8:00 a.m., New York City time. If errors are discovered in the transaction data provided by The Bank of New York Mellon or DTCC Solutions LLC, or in the calculation process, subsequent to the initial publication of SOFR but on that same day, SOFR and the accompanying summary statistics may be republished at approximately 2:30 p.m., New York City time. Additionally, if transaction data from The Bank of New York Mellon or DTCC Solutions LLC had previously not been available in time for publication, but became available later in the day, the affected rate or rates may be republished at around this time. Rate revisions will only be effected on the same day as initial publication and will only be republished if the change in the rate exceeds one basis point. Any time a rate is revised, a footnote to the New York Federal Reserve’s publication would indicate the revision. This revision threshold will be reviewed periodically by the New York Federal Reserve and may be changed based on market conditions.

Because SOFR is published by the New York Federal Reserve based on data received from other sources, we have no control over its determination, calculation or publication. See “Risk Factors” below.

The information contained in this section “Secured Overnight Financing Rate” is based upon the New York Federal Reserve’s Website and other U.S. government sources.

| December 2023 | Page 4 |

Fixed to Floating Rate Notes due 2033

Based on the Secured Overnight Financing Rate (SOFR)

(Using a Daily Compounding Calculation Method)

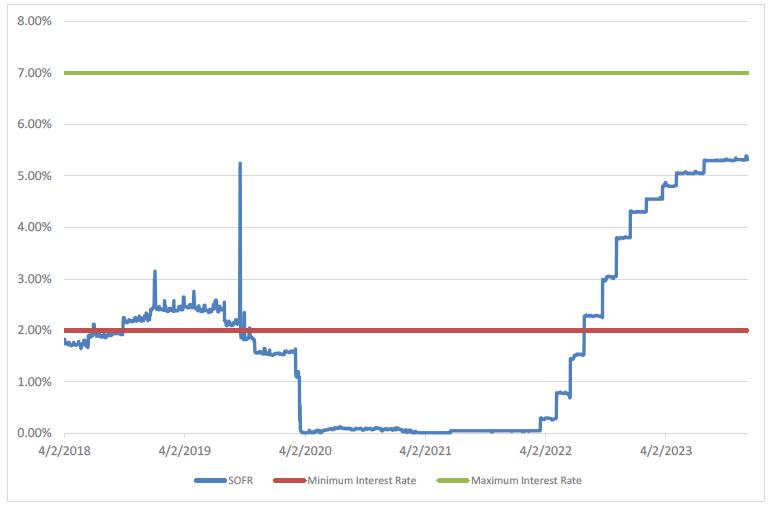

Historical Information

The following graph sets forth the historical percentage levels of SOFR as published by the New York Federal Reserve for the period from April 2, 2018 to December 6, 2023. The historical levels of SOFR should not be taken as an indication of its future performance and no assurance can be given as to the level of SOFR or the base rate on any day during the term of the notes. In addition, the historical levels of SOFR do not reflect the daily compounding calculation method used to calculate the base rate. We obtained the information in the graph below from Bloomberg Financial Markets, without independent verification.

*The green line in the graph above represents the maximum interest rate of 7.00% per annum, and the red line represents the minimum interest rate of 2.00% per annum, in each case, applicable to each interest payment period during the floating interest rate period.

You should note that publication of SOFR began on April 3, 2018 and it therefore has a very limited history. Among other things, SOFR and, therefore, the base rate may not increase or decrease over the term of the notes in accordance with the trends depicted in the graph above and the size and frequency of any fluctuations in SOFR and, therefore, the base rate over the term of the notes, which we refer to as volatility, may be significantly different from the volatility of SOFR depicted in the graph above. See “Risk Factors—SOFR-Related Risks—SOFR Has a Very Limited History; the Future Performance of SOFR Cannot be Predicted Based on Historical Performance” in the accompanying prospectus.

| December 2023 | Page 5 |

Fixed to Floating Rate Notes due 2033

Based on the Secured Overnight Financing Rate (SOFR)

(Using a Daily Compounding Calculation Method)

Risk Factors

The notes involve risks not associated with an investment in ordinary floating rate notes. An investment in the notes entails significant risks not associated with similar investments in a conventional debt security, including, but not limited to, fluctuations in SOFR, and other events that are difficult to predict and beyond the issuer’s control. This section describes the material risks relating to the notes. For a complete list of risk factors, please see the accompanying prospectus supplement and prospectus. Investors should consult their financial and legal advisers as to the risks entailed by an investment in the notes and the suitability of the notes in light of their particular circumstances.

Risks Relating to an Investment in the Notes

| § | The amount of interest payable on the notes for each interest payment period during the floating interest rate period is capped. The interest rate on the notes for each interest payment period during the floating interest rate period is capped at the maximum interest rate of 7.00% per annum. |

| § | Investors are subject to our credit risk, and any actual or anticipated changes to our credit ratings or credit spreads may adversely affect the market value of the notes. Investors are dependent on our ability to pay all amounts due on the notes on interest payment dates and at maturity and therefore investors are subject to our credit risk and to changes in the market’s view of our creditworthiness. The notes are not guaranteed by any other entity. If we default on our obligations under the notes, your investment would be at risk and you could lose some or all of your investment. As a result, the market value of the notes prior to maturity will be affected by changes in the market’s view of our creditworthiness. Any actual or anticipated decline in our credit ratings or increase in the credit spreads charged by the market for taking our credit risk is likely to adversely affect the value of the notes. |

| § | The rate we are willing to pay for securities of this type, maturity and issuance size is likely to be lower than the rate implied by our secondary market credit spreads and advantageous to us. Both the lower rate and the inclusion of costs associated with issuing, selling, structuring and hedging the notes in the original issue price reduce the economic terms of the notes, cause the estimated value of the notes to be less than the original issue price and will adversely affect secondary market prices. Assuming no change in market conditions or any other relevant factors, the prices, if any, at which dealers, including MS & Co., are willing to purchase the notes in secondary market transactions will likely be significantly lower than the original issue price, because secondary market prices will exclude the issuing, selling, structuring and hedging-related costs that are included in the original issue price and borne by you and because the secondary market prices will reflect our secondary market credit spreads and the bid-offer spread that any dealer would charge in a secondary market transaction of this type, the costs of unwinding the related hedging transactions as well as other factors. |

The inclusion of the costs of issuing, selling, structuring and hedging the notes in the original issue price and the lower rate we are willing to pay as issuer make the economic terms of the notes less favorable to you than they otherwise would be.

| § | The estimated value of the notes is determined by reference to our pricing and valuation models, which may differ from those of other dealers and is not a maximum or minimum secondary market price. These pricing and valuation models are proprietary and rely in part on subjective views of certain market inputs and certain assumptions about future events, which may prove to be incorrect. As a result, because there is no market-standard way to value these types of securities, our models may yield a higher estimated value of the notes than those generated by others, including other dealers in the market, if they attempted to value the notes. In addition, the estimated value on the pricing date does not represent a minimum or maximum price at which dealers, including MS & Co., would be willing to purchase your notes in the secondary market (if any exists) at any time. The value of your notes at any time after the date of this pricing supplement will vary based on many factors that cannot be predicted with accuracy, including our creditworthiness and changes in market conditions. |

| § | The notes will not be listed on any securities exchange and secondary trading may be limited. The notes will not be listed on any securities exchange. Therefore, there may be little or no secondary market for the notes. MS & Co. may, but is not obligated to, make a market in the notes and, if it once chooses to make a market, may cease doing so at any time. When it does make a market, it will generally do so for transactions of routine secondary market size at prices based on its estimate of the current value of the notes, taking into account its bid/offer spread, our credit spreads, market volatility, the notional size of the proposed sale, the cost of unwinding any related hedging positions, the time remaining to maturity and the likelihood that it will be able to resell the notes. Even if there is a secondary market, it may not provide enough liquidity |

| December 2023 | Page 6 |

Fixed to Floating Rate Notes due 2033

Based on the Secured Overnight Financing Rate (SOFR)

(Using a Daily Compounding Calculation Method)

to allow you to trade or sell the notes easily. Since other broker-dealers may not participate significantly in the secondary market for the notes, the price at which you may be able to trade your notes is likely to depend on the price, if any, at which MS & Co. is willing to transact. If, at any time, MS & Co. were to cease making a market in the notes, it is likely that there would be no secondary market for the notes. Accordingly, you should be willing to hold your notes to maturity.

| § | Morgan Stanley & Co. LLC, which is a subsidiary of the issuer, has determined the estimated value on the pricing date. MS & Co. has determined the estimated value of the notes on the pricing date. |

SOFR-Related Risks

| § | The interest rate on the notes during the floating interest rate period is based on a daily compounded SOFR rate, which is relatively new in the marketplace. For each interest payment period during the floating interest rate period, the interest rate on the notes is based on a daily compounded SOFR rate calculated using the specific formula described in the accompanying prospectus, not the SOFR rate published on or in respect of a particular date during such interest payment period or an average of SOFR rates during such period. For this and other reasons, the interest rate on the notes during any interest payment period within the floating interest rate period will not be the same as the interest rate on other SOFR-linked investments that use an alternative basis to determine the applicable interest rate. Further, if the SOFR rate in respect of a particular date during an interest payment period within the floating interest rate period is negative, the portion of the accrued interest compounding factor specifically attributable to such date will be less than one, resulting in a reduction to the accrued interest compounding factor used to calculate the interest payable on the notes on the interest payment date for such interest payment period. |

In addition, very limited market precedent exists for securities that use SOFR as the interest rate and the method for calculating an interest rate based upon SOFR in those precedents varies. Accordingly, the specific formula for the daily compounded SOFR rate used in the notes may not be widely adopted by other market participants, if at all. If the market adopts a different calculation method, that would likely adversely affect the market value of such notes.

| § | The amount of interest payable with respect to each interest payment period during the floating interest rate period will be determined near the end of the interest payment period. The level of the base rate applicable to each interest payment period during the floating interest rate period and, therefore, the amount of interest payable with respect to such interest payment period will be determined on the interest payment period end-date for such interest payment period (or the rate cut-off date for the final interest payment period). Because each such date is near the end of such interest payment period, you will not know the amount of interest payable with respect to each such interest payment period until shortly prior to the related interest payment date and it may be difficult for you to reliably estimate the amount of interest that will be payable on each such interest payment date. |

| § | The price at which the notes may be sold prior to maturity will depend on a number of factors and may be substantially less than the amount for which they were originally purchased. Some of these factors include, but are not limited to: (i) actual or anticipated changes in the level of SOFR, (ii) volatility of the level of SOFR, (iii) changes in interest and yield rates, (iv) any actual or anticipated changes in our credit ratings or credit spreads and (v) the time remaining to maturity of such notes. Generally, the longer the time remaining to maturity and the more tailored the exposure, the more the market price of the notes will be affected by the other factors described in the preceding sentence. This can lead to significant adverse changes in the market price of securities like the notes. Depending on the actual or anticipated level of SOFR, the market value of the notes is expected to decrease and you may receive substantially less than 100% of the issue price if you are able to sell your notes prior to maturity. |

| § | The issuer, its subsidiaries or affiliates may publish research that could affect the market value of the notes. They also expect to hedge the issuer’s obligations under such notes. The issuer or one or more of its affiliates may, at present or in the future, publish research reports with respect to movements in interest rates generally, or the LIBOR transition or SOFR specifically. This research is modified from time to time without notice to you and may express opinions or provide recommendations that are inconsistent with purchasing or holding the notes. Any of these activities may affect the market value of such notes. In addition, the issuer’s subsidiaries expect to hedge the issuer’s obligations under the notes and they may realize a profit from that expected hedging activity even if investors do not receive a favorable investment return under the terms of such notes or in any secondary market transaction. |

| December 2023 | Page 7 |

Fixed to Floating Rate Notes due 2033

Based on the Secured Overnight Financing Rate (SOFR)

(Using a Daily Compounding Calculation Method)

| § | The calculation agent, which is a subsidiary of the issuer, (or, if applicable, we or our designee) will make determinations with respect to the notes. The calculation agent will make certain determinations with respect to the notes as further described in the accompanying prospectus. In addition, if a Benchmark Transition event and its related Benchmark Replacement Date have occurred, we or our designee will make certain determinations with respect to the notes in our or our designee’s sole discretion as further described under “Description of Debt Securities—SOFR Debt Securities—Determination of SOFR” in the accompanying prospectus. Any of these determinations may adversely affect the payout to investors. Moreover, certain determinations may require the exercise of discretion and the making of subjective judgments, such as with respect to the base rate or the occurrence or non-occurrence of a Benchmark Transition Event and any Benchmark Replacement Conforming Changes. These potentially subjective determinations may adversely affect the payout to you on the notes. For further information regarding these types of determinations, see “Description of Debt Securities—SOFR Debt Securities” in the accompanying prospectus. |

| § | In determining the base rate for the final interest payment period in the floating interest rate period, the level of SOFR for any day from and including the rate cut-off date to but excluding the maturity date will be the level of SOFR in respect of such rate cut-off date. For the final interest payment period, because the level of SOFR for any day from and including the rate cut-off date to but excluding the maturity date will be the level of SOFR in respect of such rate cut-off date, you will not receive the benefit of any increase in the level in respect of SOFR beyond the level for such date in connection with the determination of the interest payable with respect to such interest payment period, which could adversely impact the amount of interest payable with respect to that interest payment period. |

| December 2023 | Page 8 |

Fixed to Floating Rate Notes due 2033

Based on the Secured Overnight Financing Rate (SOFR)

(Using a Daily Compounding Calculation Method)

Use of Proceeds and Hedging

The proceeds we receive from the sale of the notes will be used for general corporate purposes. We will receive, in aggregate, $1,000 per note issued, because, when we enter into hedging transactions in order to meet our obligations under the notes, our hedging counterparty will reimburse the cost of the agent’s commissions. The costs of the notes borne by you and described on page 3 above comprise the agent’s commissions and the cost of issuing, structuring and hedging the notes.

Supplemental Information Concerning Plan of Distribution; Conflicts of Interest

Morgan Stanley or one of our affiliates will pay varying discounts and commissions to dealers, including Morgan Stanley Smith Barney LLC (“Morgan Stanley Wealth Management”) and their financial advisors, of up to $17.50 per note depending on market conditions. The agent may distribute the notes through Morgan Stanley Wealth Management, as selected dealer, or other dealers, which may include Morgan Stanley & Co. International plc (“MSIP”) and Bank Morgan Stanley AG. Morgan Stanley Wealth Management, MSIP and Bank Morgan Stanley AG are affiliates of Morgan Stanley.

MS & Co. is our wholly owned subsidiary and it and other subsidiaries of ours expect to make a profit by selling, structuring and, when applicable, hedging the notes.

MS & Co. will conduct this offering in compliance with the requirements of FINRA Rule 5121 of the Financial Industry Regulatory Authority, Inc., which is commonly referred to as FINRA, regarding a FINRA member firm’s distribution of the securities of an affiliate and related conflicts of interest. MS & Co. or any of our other affiliates may not make sales in this offering to any discretionary account.

Acceleration Amount in Case of an Event of Default

In case an event of default with respect to the notes shall have occurred and be continuing, the amount declared due and payable per note upon any acceleration of the notes shall be determined by the calculation agent, after consultation with us, and shall be an amount in cash equal to the stated principal amount plus accrued and unpaid interest calculated as if the date of such acceleration were the maturity date, final interest payment period end-date (if applicable) and final interest payment date.

Validity of the Notes

In the opinion of Davis Polk & Wardwell LLP, as special counsel to Morgan Stanley, when the notes offered by this pricing supplement have been executed and issued by Morgan Stanley, authenticated by the trustee pursuant to the Senior Debt Indenture and delivered against payment as contemplated herein, such notes will be valid and binding obligations of Morgan Stanley, enforceable in accordance with their terms, subject to applicable bankruptcy, insolvency and similar laws affecting creditors’ rights generally, concepts of reasonableness and equitable principles of general applicability (including, without limitation, concepts of good faith, fair dealing and the lack of bad faith), provided that such counsel expresses no opinion as to the effect of fraudulent conveyance, fraudulent transfer or similar provision of applicable law on the conclusions expressed above. This opinion is given as of the date hereof and is limited to the laws of the State of New York and the General Corporation Law of the State of Delaware. In addition, this opinion is subject to customary assumptions about the trustee’s authorization, execution and delivery of the Senior Debt Indenture and its authentication of the notes and the validity, binding nature and enforceability of the Senior Debt Indenture with respect to the trustee, all as stated in the letter of such counsel dated November 16, 2023, which is Exhibit 5-a to the Registration Statement on Form S-3 filed by Morgan Stanley on November 16, 2023.

| December 2023 | Page 9 |

Fixed to Floating Rate Notes due 2033

Based on the Secured Overnight Financing Rate (SOFR)

(Using a Daily Compounding Calculation Method)

Tax Considerations

In the opinion of our counsel, Davis Polk & Wardwell LLP, the notes should be treated as “variable rate debt instruments” for U.S. federal tax purposes, and the remainder of this discussion assumes this treatment is correct.

The notes should be treated as “variable debt instruments” providing for a single fixed rate followed by a single qualified floating rate (“QFR”), as described in the sections of the accompanying prospectus supplement called “United States Federal Taxation—Tax Consequences to U.S. Holders—Notes—Floating Rate Notes—General” and “—Floating Rate Notes that Provide for Multiple Rates.” Unless otherwise stated, the following discussion in this paragraph is based on the treatment of each note as described in the preceding sentence. Under applicable Treasury Regulations, in order to determine the amount of qualified stated interest (“QSI”) and original issue discount (“OID”) in respect of the notes, an equivalent fixed rate debt instrument must be constructed. The equivalent fixed rate debt instrument is constructed in the following manner: (i) first, the initial fixed rate is converted to a QFR that would preserve the fair market value of the notes, and (ii) second, each QFR (including the QFR determined under (i) above) is converted to a fixed rate substitute (which will generally be the value of that QFR as of the issue date of the notes). The rules under “United States Federal Taxation—Tax Consequences to U.S. Holders—Notes—Discount Notes—General” must be applied to the equivalent fixed rate debt instrument to determine the amounts of QSI and OID on the notes. Under this method, the notes may be issued with OID.

A U.S. holder is required to include any QSI in income in accordance with the U.S. holder’s regular method of accounting for U.S. federal income tax purposes. U.S. holders will be required to include OID in income for U.S. federal income tax purposes as it accrues, in accordance with a constant yield method based on a compounding of interest. QSI allocable to an accrual period must be increased (or decreased) by the amount, if any, which the interest actually accrued or paid during an accrual period (including the fixed rate payments made during the initial period) exceeds (or is less than) the interest assumed to be accrued or paid during the accrual period under the equivalent fixed rate debt instrument. For the QSI and the amount of OID (if any) on a note, please contact Morgan Stanley at StructuredNotesTaxInfo@morganstanley.com.

If you are a non-U.S. holder, please read the section of the accompanying prospectus supplement called “United States Federal Taxation—Tax Consequences to Non-U.S. Holders.”

Both U.S. and non-U.S. holders should read the section of the accompanying prospectus supplement entitled “United States Federal Taxation.”

You should consult your tax adviser regarding all aspects of the U.S. federal tax consequences of an investment in the notes, as well as any tax consequences arising under the laws of any state, local or non-U.S. taxing jurisdiction. Moreover, neither this document nor the accompanying prospectus supplement addresses the consequences to taxpayers subject to special tax accounting rules under Section 451(b) of the Internal Revenue Code of 1986, as amended.

The discussion in the preceding paragraphs under “Tax Considerations,” and the discussion contained in the section entitled “United States Federal Taxation” in the accompanying prospectus supplement, insofar as they purport to describe provisions of U.S. federal income tax laws or legal conclusions with respect thereto, constitute the full opinion of Davis Polk & Wardwell LLP regarding the material U.S. federal tax consequences of an investment in the notes.

| December 2023 | Page 10 |

Fixed to Floating Rate Notes due 2033

Based on the Secured Overnight Financing Rate (SOFR)

(Using a Daily Compounding Calculation Method)

Where You Can Find More Information

Morgan Stanley has filed a registration statement (including a prospectus, as supplemented by a prospectus supplement) with the Securities and Exchange Commission, or SEC, for the offering to which this pricing supplement relates. You should read the prospectus in that registration statement, the prospectus supplement and any other documents relating to this offering that Morgan Stanley has filed with the SEC for more complete information about Morgan Stanley and this offering. You may get these documents without cost by visiting EDGAR on the SEC web site at www.sec.gov. Alternatively, Morgan Stanley will arrange to send you the prospectus and the prospectus supplement if you so request by calling toll-free 800-584-6837.

You may access these documents on the SEC web site at.www.sec.gov as follows:

Prospectus Supplement dated November 16, 2023

Prospectus dated November 16, 2023

Terms used but not defined in this pricing supplement are defined in the prospectus supplement or in the prospectus. As used in this pricing supplement, the “Company,” “we,” “us” and “our” refer to Morgan Stanley.

| December 2023 | Page 11 |