Ohio Valley Banc Corp.

The management of Ohio Valley Banc Corp. (the Company) is responsible for establishing and maintaining adequate internal control over financial reporting as defined in Rules 13a-15(f) and 15d-15(f) under the Securities

Exchange Act of 1934. The Company's internal control over financial reporting is designed to provide reasonable assurance regarding the reliability of financial reporting and the preparation of financial statements for external purposes in accordance

with generally accepted accounting principles. The Company's internal control over financial reporting includes those policies and procedures that: (i) pertain to the maintenance of records that, in reasonable detail, accurately and fairly reflect

the transactions and dispositions of the assets of the Company; (ii) provide reasonable assurance that transactions are recorded as necessary to permit preparation of financial statements in accordance with generally accepted accounting principles,

and that receipts and expenditures of the Company are being made only in accordance with authorizations of management and directors of the Company; and (iii) provide reasonable assurance regarding prevention or timely detection of unauthorized

acquisition, use or disposition of the Company's assets that could have a material effect on the financial statements.

The system of internal control over financial reporting as it relates to the consolidated financial statements is evaluated for effectiveness by management. Because of its inherent limitations, internal control over

financial reporting may not prevent or detect misstatements. Also, projections of any evaluation of effectiveness to future periods are subject to the risk that controls may become inadequate because of changes in conditions, or that the degree of

compliance with the policies or procedures may deteriorate.

Management assessed Ohio Valley Banc Corp.’s system of internal control over financial reporting as of December 31, 2021, in relation to criteria for effective internal control over financial reporting as described in

the 2013 “Internal Control Integrated Framework,” issued by the Committee of Sponsoring Organizations of the Treadway Commission (COSO). Based on this assessment, management concluded that, as of December 31, 2021, its system of internal control over

financial reporting is effective and meets the criteria of the “Internal Control Integrated Framework.”

Crowe LLP, independent registered public accounting firm, has not issued an integrated audit report on Ohio Valley Banc Corp.’s internal control over financial reporting.

OHIO VALLEY BANC CORP.

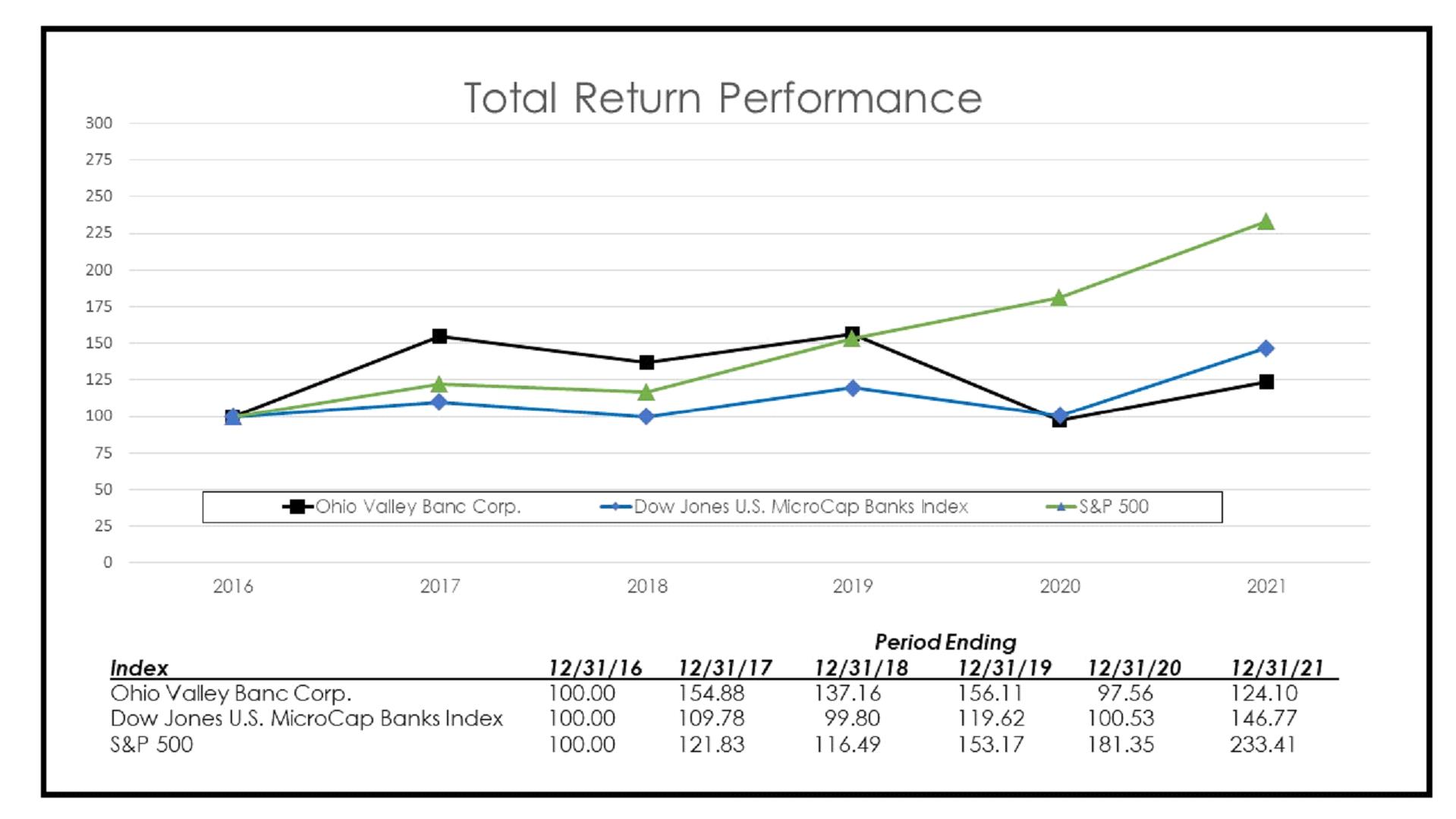

The following graph sets forth a comparison of five-year cumulative total returns among the Company's common shares (indicated “Ohio Valley Banc Corp.” on the Performance Graph), the S & P 500

Index (indicated “S & P 500” on the Performance Graph), and Dow Jones U.S. MicroCap Banks Index (indicated “Dow Jones U.S. MicroCap Banks Index” on the Performance Graph) for fiscal years indicated. Information reflected on the graph assumes an

investment of $100 on December 31, 2016, in the common shares of each of the Company, the S & P 500 Index, and the Dow Jones U.S. MicroCap Banks Index. Cumulative total return assumes reinvestment of dividends. The Dow Jones U.S. MicroCap Banks

Index represents the stock performance of 163 banks located throughout the United States, including the Company, within the respective market capitalization range as selected by Dow Jones. The Dow Jones U.S. MicroCap Banks Index was selected as a

replacement peer index for the SNL $1 Billion-$5 Billion Bank Asset-Size Index due to the latter no longer being published.

FORWARD LOOKING STATEMENTS

Certain statements contained in this report and other publicly available documents incorporated herein by reference constitute "forward looking statements" within the meaning

of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Act of 1934, as amended (the “Exchange Act”), and as defined in the Private Securities Litigation Reform Act of 1995. Such statements are often, but not

always, identified by the use of such words as “believes,” “anticipates,” “expects,” “intends,” “plan,” “goal,” “seek,” “project,” “estimate,” “strategy,” “future,” “likely,” “may,” “should,” “will,” and other similar expressions. Such statements

involve various important assumptions, risks, uncertainties, and other factors, many of which are beyond our control, particularly with regard to developments related to the Coronavirus (“COVID-19”) pandemic, and which could cause actual results to

differ materially from those expressed in such forward looking statements. These factors include, but are not limited to: the effects of COVID-19 on our business, operations, customers and capital position; higher default rates on loans made to

our customers related to COVID-19 and its impact on our customers’ operations and financial condition; the impact of COVID-19 on local, national and global economic conditions; unexpected changes in interest rates or disruptions in the mortgage

market; the effects of various governmental responses to COVID-19; changes in political, economic or other factors, such as inflation rates, recessionary or expansive trends, taxes, the effects of implementation of legislation and the continuing

economic uncertainty in various parts of the world; competitive pressures; fluctuations in interest rates; the level of defaults and prepayment on loans made by the Company; unanticipated litigation, claims, or assessments; fluctuations in the cost

of obtaining funds to make loans; and regulatory changes. Additional detailed information concerning such factors is available in the Company’s filings with the Securities and Exchange Commission, under the Exchange Act, including the disclosure

under the heading “Item 1A. Risk Factors” of Part I of the Company’s Annual Report on Form 10-K for the fiscal year ended December 31, 2021. Readers are cautioned not to place undue reliance on such forward looking statements, which speak only as

of the date hereof. The Company undertakes no obligation and disclaims any intention to republish revised or updated forward looking statements, whether as a result of new information, unanticipated future events or otherwise.

ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The purpose of this discussion is to provide an analysis of the financial condition and results of operations of Ohio Valley Banc Corp. (“Ohio Valley” or the “Company”) that is

not otherwise apparent from the audited consolidated financial statements included in this report. The accompanying consolidated financial information has been prepared by management in conformity with U.S. generally accepted accounting principles

(“US GAAP”) and is consistent with that reported in the consolidated financial statements. Reference should be made to those statements and the selected financial data presented elsewhere in this report for an understanding of the following tables

and related discussion. All dollars are reported in thousands, except share and per share data.

BUSINESS OVERVIEW:

The Company is primarily engaged in commercial and retail banking through its wholly-owned subsidiary, The Ohio Valley Bank Company (the “Bank”), offering a blend of commercial and consumer banking

services within southeastern Ohio, as well as western West Virginia. The banking services offered by the Bank include the acceptance of deposits in checking, savings, time and money market accounts; the making and servicing of personal,

commercial, floor plan and student loans; the making of construction and real estate loans; and credit card services. The Bank also offers individual retirement accounts, safe deposit boxes, wire transfers and other standard banking products and

services. Ohio Valley also has a subsidiary that engages in consumer lending generally to individuals with higher credit risk history, Loan Central, Inc. (“Loan Central”); a subsidiary insurance agency that facilitates the receipt of insurance

commissions, Ohio Valley Financial Services Agency, LLC; and a limited purpose property and casualty insurance company, OVBC Captive, Inc. (the “Captive”). The Bank has two wholly-owned subsidiaries, Race Day Mortgage, Inc. ("Race Day"), an online

consumer direct mortgage company, and Ohio Valley REO, LLC, an entity to which the Bank transfers certain real estate acquired by the Bank through foreclosure for sale.

In January 2020, the Bank began offering Tax Refund Advance Loans (“TALs”) to Loan Central tax customers. A TAL represents a short-term loan offered by the Bank to tax preparation customers of

Loan Central. Previously, Loan Central offered and originated tax refund anticipation loans that represented a large composition of its annual earnings. However, new Ohio laws that became effective in April 2019 placed numerous restrictions on

short-term and small loans extended by certain non-bank lenders in Ohio. As a result, Loan Central is no longer able to directly offer the service to its tax preparation customers, but it is able to do so through the Bank. After Loan Central

prepares a customer’s tax return, the customer is offered the opportunity to have immediate access to a portion of the anticipated tax refund by entering into a TAL with the Bank. As part of the process, the tax customer completes a loan

application and authorizes the expected tax refund to be deposited with the Bank once it is issued by the IRS. Once the Bank receives the tax refund, the refund is used to repay the TAL and Loan Central’s tax preparation fees, then the remainder

of the refund is remitted to Loan Central’s tax customer.

IMPACT of COVID-19:

COVID-19 has caused significant disruption in the United States and international economies and financial markets. The primary markets served by the Company in southeastern

Ohio and western West Virginia were significantly impacted by COVID-19, which has changed the way we live and work. The continued effects of COVID-19 on the economy, supply chains, financial markets, unemployment levels, businesses and our

customers is unknown and unpredictable.

On March 27, 2020, the Coronavirus Aid, Relief, and Economic Security Act ("CARES Act") was signed into law. The CARES Act provided assistance to small businesses through the

establishment of the Paycheck Protection Program ("PPP"). The PPP provided small businesses with funds to use for payroll and certain other expenses. The funds were provided in the form of loans that would be fully forgiven if certain criteria were

met. In 2021, Congress amended the PPP by extending the authority of the Small Business Administration (“SBA”) to guarantee loans and the ability of PPP lenders to disburse PPP loans until May 31, 2021. The Company supported its clients who

experienced financial hardship due to COVID-19 through participation in the PPP, assistance with expedited deposits of CARES Act stimulus payments, and loan modifications, as needed.

RESULTS OF OPERATIONS:

SUMMARY

2021 v. 2020

Ohio Valley generated net income of $11,732 for 2021, an increase of $1,473, or 14.4%, from 2020. Earnings per share were $2.45 for 2021, an increase of 14.5% from 2020. The

increase in net income and earnings per share for 2021 was impacted by higher net interest income and lower provision expense, which collectively contributed to a $4,430 increase in earnings from 2020. For 2021, the Company finished with negative

provision expense of $419, compared to $2,980 in provision expense for 2020. The decrease in provision expense was largely due to a decrease in net loan charge offs during 2021 and the establishment of an economic risk factor for the pandemic

during the first quarter of 2020 that was less impactful in 2021. Net interest income increased 2.6% in 2021 largely due to growth in average earning assets, partially offset by a decrease in the fully tax-equivalent net interest income as a

percentage of average earning assets (“net interest margin”). Average earnings assets increased 13.0% coming from growth in loans, investment securities and interest-bearing deposits with banks. The positive impact from earning asset growth was

partially offset by net interest margin compression in relation to aggressive rate cuts by the Federal Reserve in response to the pandemic during 2020. The positive contributions from higher net interest income and lower provision expense were

partially offset by lower noninterest income and higher noninterest expense, which collectively contributed to a $2,721 decrease in earnings from 2020. Contributing to lower noninterest income were realized losses of $1,066 from the sale of

lower-yielding securities during 2021 and the receipt of $2,000 during 2020 from a litigation settlement with a third-party. Partially offsetting these negative factors within noninterest income was growth in debit/credit card interchange income

and electronic refund check/electronic refund deposit (“ERC/ERD”) fees during 2021. The increase in noninterest expenses during 2021 came mostly from higher software, data processing, marketing and FDIC costs.

The Company’s net interest income in 2021 was $41,013, representing an increase of $1,031, or 2.6%, from 2020. Impacting net interest income growth was average earning assets,

which were up $131,943 during 2021, as compared to 2020. The growth came largely from increases in interest-bearing deposits with banks and investment securities, which were up $57,860 and $43,836, over 2020, respectively. Interest-bearing

deposits were impacted by higher balances maintained at the Federal Reserve Bank (“FRB”) driven by heightened deposit balances related to stimulus payments received by customers. A portion of the deposit increase was invested in the securities

portfolio during 2021. Average loans also grew $30,247 during 2021, largely impacted by higher commercial loan balances. In general, commercial loan demand has been positive in the Company’s market areas, particularly in the counties of Pike and

Athens in Ohio and Cabell County in West Virginia. Furthermore, the Company participated in the PPP to assist various businesses in our market areas during the pandemic. The loan fees earned in association with the PPP loans during 2021 contributed

to a $587 increase in total loan fees, which also had a positive impact to net interest income. Partially offsetting the positive impacts from average earning asset growth and loan fee increases was the decrease in net interest margin in relation

to the decrease in market rates. In March 2020, the Federal Reserve took action to reduce interest rates by 150 basis points in response to COVID-19. This action led to a sustained low-rate interest environment, which contributed to lower earning

asset yields during the remainder of 2020 and all of 2021. Interest-bearing costs were reduced during those periods, but not to the same magnitude as earning assets due to a lagging effect associated with time deposits and certain other

interest-bearing deposits being at or near their interest rate floors. Furthermore, the change in asset mix during 2020 and 2021 into more PPP loans and elevated deposits at the Federal Reserve had a dilutive effect on the net interest margin, with

PPP loans carrying a 1.0% interest rate and the rate on balances maintained at the Federal Reserve below 25 basis points. As a result, the Company’s net interest margin finished at 3.61% during the year ended December 31, 2021, a decrease of 36

basis points from a 3.97% net interest margin during the same period in 2020.

The Company recorded negative provision expense of $419 during 2021, representing a decrease of $3,399 compared to 2020. The decrease in provision expense was largely impacted

by the economic effects of the COVID-19 pandemic, which resulted in a higher general allocation of the allowance for loan losses during the first quarter of 2020. Based on declining economic conditions and increasing unemployment levels, management

increased general reserves by $2,315 to reflect higher anticipated losses due to COVID-19. Further impacting lower provision expense in 2021 was a $1,332 decrease in net charge-offs on loans that had not been specifically allocated for, primarily

from the consumer and residential real estate loan portfolios.

The Company’s noninterest income decreased $1,574, or 13.8%, from 2020. The year-to-date decrease in noninterest income was largely impacted by proceeds of $2,000 received in a

litigation settlement with a third-party. The proceeds were paid to the Bank as part of a settlement agreement signed during the first quarter of 2020. The settlement agreement was related to the previously disclosed litigation the Bank filed

against a third-party tax software product provider for early termination of its tax processing contract. As part of the settlement agreement, the Bank is processing a certain amount of tax items, which started in 2021 and will end in 2025. As a

result, the Bank recognized $675 in ERC/ERD income during 2021, which partially offset the impact of the non-recurring litigation settlement proceeds in 2020. Further contributing to the decrease in noninterest income for 2021 were losses of

$1,066 realized on the sale of $48,732 in lower-yielding investment securities during the fourth quarter of 2021. The proceeds from the sale were reinvested into similar higher-yielding securities, which are expected to increase future income. As

was anticipated, mortgage banking income decreased $400 during 2021, primarily due to the 2020 heightened refinancing volume that subsided in 2021. Partially offsetting decreases in noninterest income was an increase of $613 in interchange income

on debit and credit card transactions as customers increased spending during 2021.

The Company’s noninterest expenses during 2021 increased $1,147, or 3.2%, from 2020. This increase was impacted by various items including higher software, data processing,

marketing and FDIC costs. Software expense increased $404 in relation to the purchase of software to enhance the platform used for the loan origination process, as well as to process PPP loans. Data processing expense increased $236 due to higher

debit and credit card transaction volume impacted by heightened consumer spending. Marketing expense increased $213 due to resuming select marketing campaigns in 2021 that had been limited in 2020 due to COVID-19 restrictions on lobby access. FDIC

insurance costs were up $161 primarily due to assessment credits received from the FDIC in 2020 that were not received in 2021.

The Company’s provision for income taxes increased $236 during 2021, largely due to the changes in taxable income affected by the factors mentioned above.

NET INTEREST INCOME

The most significant portion of the Company's revenue, net interest income, results from properly managing the spread between interest income on earning assets and interest

expense incurred on interest-bearing liabilities. The Company earns interest and dividend income from loans, investment securities and short-term investments while incurring interest expense on interest-bearing deposits and short- and long-term

borrowings. Net interest income is affected by changes in both the average volume and mix of assets and liabilities and the level of interest rates for financial instruments. Changes in net interest income are measured by net interest margin and

net interest spread. Net interest margin is expressed as the percentage of net interest income to average interest-earning assets. Net interest spread is the difference between the average yield earned on interest-earning assets and the average

rate paid on interest-bearing liabilities. Both of these are reported on a fully tax-equivalent (“FTE”) basis. Net interest margin exceeds the net interest rate spread because noninterest-bearing sources of funds, principally noninterest-bearing

demand deposits and stockholders' equity, also support interest-earning assets. The following is a discussion of changes in interest-earning assets, interest-bearing liabilities and the associated impact on interest income and interest expense for

the two years ended December 31, 2021 and 2020. Tables I and II have been prepared to summarize the significant changes outlined in this analysis.

Net interest income in 2021 totaled $41,491 on an FTE basis, up $1,069, or 2.6%, from 2020. This positive change reflects a 13.0% increase in average earning assets partially

offset by the net effect of a 65 basis point decrease in earning asset yield less a 41 basis point decrease in average interest-bearing liability cost. The increase in average earning assets came mostly from interest-bearing balances with banks and

securities, which increased 74.0% and 34.4% during 2021, respectively, as compared to the same period in 2020. Average loans also increased 3.7% over the same time period. The average earning asset yield during 2021 was impacted by the FRB’s

action to lower rates by 150 basis points in March 2020. Market rate decreases during 2020 had a corresponding impact to lower average deposit costs during 2021, primarily within time, savings and money market deposits. The net interest margin

decrease of 36 basis points reflected a 41 basis point positive impact from lower funding costs that was completely offset by a 65 basis point negative impact from the mix and yield on earning assets and a 12 basis point negative impact from the

use of noninterest-bearing funding (i.e., demand deposits and shareholders’ equity).

Net interest income increased in 2021 primarily due to the increase in average volume of earning assets plus the decrease in average cost of interest-bearing liabilities,

partially offset by the decrease in average yield on earning assets. The volume increase in average earning assets was responsible for increasing FTE interest income by $2,445 during 2021 compared to 2020, while the decrease in average

interest-bearing liability costs contributed to a $2,416 reduction in interest expense during the same period. These positive impacts were partially offset by lower average earning asset yields, which decreased FTE interest income by $3,868 during

2021 compared to 2020. The increase in average earning assets for 2021 was largely impacted by interest-bearing balances with other banks. The average volume on interest-bearing balances with other banks contributed to $136 in interest income

growth during 2021, primarily from excess deposits within the Federal Reserve clearing account. Balances within interest-bearing deposits with banks are driven primarily by the Company’s interest-bearing Federal Reserve clearing account. The

Company utilizes its interest-bearing Federal Reserve clearing account to manage excess funds, as well as to assist in funding earning asset growth. The impact of COVID-19 continued to generate higher levels of excess funds within the clearing

account during 2021, which included customer deposits of stimulus monies from various government relief programs. The volume increase in the Bank’s Federal Reserve clearing account during 2021 led to a $57,860, or 74.0%, increase in average

interest-bearing balances with other banks during 2021 compared to 2020, and also led to a higher composition of average interest-bearing balances with other banks, finishing at 11.8% of average earning assets in 2021, as compared to 7.7% in 2020.

The action of the FRB to reduce rates by 150 basis points in March 2020 had an immediate effect on reducing the interest income generated by the Company’s Federal Reserve clearing account. The clearing account interest rate was adjusted down to

0.25% in March 2020, and has been fluctuating at or below 0.25% since that time. As a result, the average yield factor on interest-bearing balances with other banks continued to have a negative impact on earnings, decreasing interest income by $215

in 2021, as compared to a $1,285 decrease in interest income during 2020.

Average securities of $171,157 at year-end 2021 represented a 34.4% increase from the $127,321 in average securities at year-end 2020. The significant surge in deposits during

2021 was a result of various government stimulus programs that produced heightened levels of excess liquidity. The Company utilized a portion of these excess funds to purchase investment securities. Average taxable securities in 2021 increased

37.6% over the prior year, particularly from purchases of U.S. Government, Agency and Agency mortgage-backed securities. As a result, the composition of average taxable securities grew to 14.1% of average earning assets at year-end 2021, as

compared to 11.6% at year-end 2020. Average tax exempt securities were down 6.3% from the prior year, largely related to maturities of state and municipal investments. As a result, the composition of average state and municipal investments trended

down to 0.8% of average earning assets at year-end 2021, as compared to 0.9% at year-end 2020. Management continues to focus on generating loan growth as loans provide the greatest return to the Company. Management also maintains securities at a

dollar level adequate enough to provide ample liquidity and cover pledging requirements.

Net interest income was negatively impacted by loans, particularly with the decrease in average yield. The decrease in short-term rates in March 2020 had a direct impact on the

repricing of a portion of the Company’s loan portfolio that contributed to lower earnings in 2021. This decreased the average loan yield by 32 basis points to 5.05% at year-end 2021, as compared to 5.37% at year-end 2020, which caused FTE interest

income to decrease by $2,639 during 2021. Partially offsetting the effects from loan yields was a $30,247, or 3.7%, increase in average loans, which contributed to $1,587 in additional FTE interest income during 2021 compared to 2020. This growth

came predominantly from the commercial real estate and commercial and industrial loan segments. This was due to positive loan demand occurring within the Company’s primary market areas, particularly Athens and Pike counties in Ohio and Cabell

County in West Virginia. While the Company experienced origination increases of government-guaranteed PPP loans in 2020, and to a smaller extent in early 2021, the payoffs of those loans were experienced during the second half of 2021, causing an

average balance decrease in PPP loans in 2021 compared to 2020. While average loans increased in 2021, interest-bearing deposits with other banks and investment securities experienced more accelerated growth in 2021. As a result, the Company’s

average loan composition decreased to 73.3% of average earning assets at year-end 2021, as compared to 79.8% for 2020.

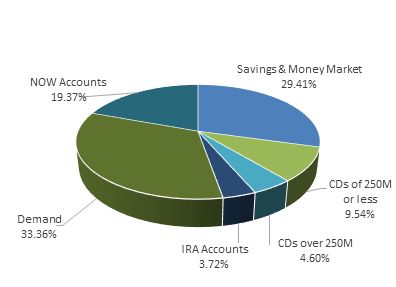

Net interest income was positively impacted by a decline in the average cost of interest-bearing liabilities, particularly with the Company’s time deposits, during 2021. The

short-term rate decrease from 2020 had a direct impact in lowering CD rate offerings. However, there was a lagging effect to the impact that this market rate decrease had on reducing time deposit expense. As CD rates have repriced downward, the

Company benefited from lower interest expense only to the extent that new CDs at lower rates were issued. As CDs continued to rollover into lower rates during the second half of 2020 and all of 2021, a greater reduction to interest expense on time

deposits was recognized. As a result, the average cost of time deposits decreased 74 basis points from 1.75% in 2020 to 1.01% in 2021, which contributed to a $1,483 decrease in interest expense for the year. This is compared to a $427 decrease in

interest expense during 2020. Lower CD rates have also generated less consumer demand for CD products. As a result, the average time deposit segment decreased $11,337, or 5.4%, during 2021, which led to a decrease in the composition of average

time deposits from 30.8% of interest-bearing liabilities at year-end 2020 to 26.9% at year-end 2021.

Lower interest rates also had a significant impact on core deposit segments that include negotiable order of withdrawal (“NOW”), savings and money market accounts. Interest

expense was significantly impacted by a decrease in the average costs of this core group of interest-bearing liabilities, particularly savings and money market accounts. This is largely due to the short-term rate cuts made by the FRB in March 2020

that influenced the repricing of various deposit products into 2021. These repricing efforts in a lower rate environment have contributed to lower average costs in 2021. This includes the rate reduction associated with the Company’s prime

investment deposit account, which contributed to a $542 decrease in money market interest expense during 2021. As a result, the average cost of savings and money market accounts decreased from 0.36% in 2020 to 0.09% in 2021, which led to a $794

decrease in interest expense during 2021. Conversely, customer deposits continued to increase during 2021 within these core deposit segments impacted by stimulus relief monies and a consumer preference to preserve these customer deposit proceeds

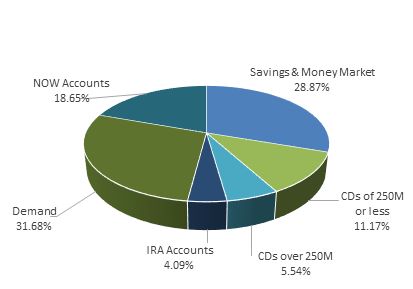

during the pandemic. As a result, average balances during 2021 increased 19.5% within NOW accounts and 15.7% within savings and money market accounts, altogether representing 68.5% of average interest-bearing liabilities in 2021, as compared to

63.4% in 2020.

In addition, the Company’s average other borrowings and subordinated debentures collectively decreased $5,852, or 14.5%, during 2021. The decrease was related to the principal

repayments applied to various FHLB advances. Borrowings and subordinated debentures continue to represent the smallest composition of average interest-bearing liabilities, finishing at 4.6% and 5.9% at the end of 2021 and 2020, respectively.

Total interest and fee income on average earning assets decreased $1,423, or 3.1%, during 2021, and $4,133, or 8.1%, during 2020. The decreases in earnings were largely the

result of a decline in market rates during the second half of 2019 and in March 2020 partially offset by loan fee increases during 2021. The Company’s interest and fees from its consumer loan portfolio decreased $376, or 3.6%, during 2021. The

decrease was primarily the result of lower consumer loan yields and a decrease in average automobile loans. As a result, consumer loan interest decreased $358 and consumer loan fees decreased $18 during 2021. During 2020, consumer loan interest and

fees decreased $1,726, or 14.3%. The decrease was also impacted by lower consumer yields, as well as a decrease in average automobile and home equity loan balances, which contributed to an $804 decrease in consumer loan interest during 2020.

Consumer loan fees also decreased $922 during 2020. The decrease was primarily due to a change in the Company’s business model with Loan Central that was necessary to comply with new regulations, which resulted in Loan Central not assessing any

loan fees for tax refund loan advances during 2020. Rather, Loan Central began assessing a fee for preparing a tax return in combination with a reduced loan fee. The fee income for preparing the tax return was recorded as noninterest income.

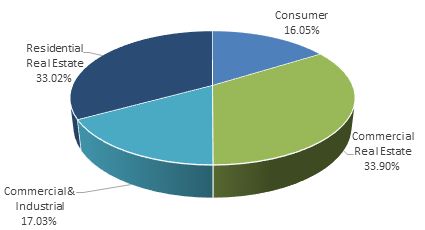

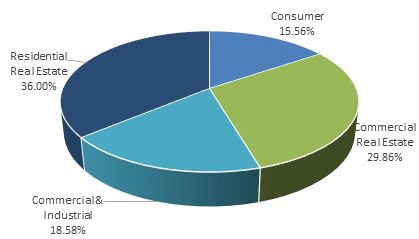

The Company’s interest and fees from its commercial loan portfolio increased $1,387, or 7.0%, during 2021. The increase was impacted by higher average commercial

loan balances that completely offset the negative impact of lower commercial loan yields. Commercial loan demand was successful in generating an average balance increase of 14.0% within the Company’s commercial real estate and commercial and

industrial portfolios. Balance increases were driven by a $48,035 increase in average commercial loans from the Company’s Pike and Athens counties in Ohio and Cabell County in West Virginia. Further impacting commercial revenue during 2021 was a

$728 increase in loan fees. The Company has participated in the PPP since 2020 as part of the government’s relief program for businesses impacted by COVID-19. These originations began in the second quarter of 2020, with another round added during

the first quarter of 2021. The majority of PPP loan originations from both rounds had paid off by year-end 2021. This resulted in the income recognition of $1,184 in PPP loan fees from the SBA during 2021, an increase of $479 in PPP fees over

2020. During 2020, the Company’s commercial loan interest and fees decreased by $157, or 0.8%. The decrease was impacted by lower commercial loan yields that completely offset the positive impacts of higher average commercial loan balances and

higher commercial loan fees during 2020. Commercial loan yields were negatively impacted by the low rate environment in 2020. Average commercial loans grew by 17.2% and came primarily from $35,141 in PPP loan originations. Loan fees of $1,175

were collected from the SBA during this first round of PPP loans in 2020, of which, $705 were recorded to fee income. While PPP loans contributed to higher commercial loan balances in 2020, they also had a dilutive effect on loan yields

as a result of the 1% interest rate associated with each loan.

CONSOLIDATED AVERAGE BALANCE SHEET & ANALYSIS OF NET INTEREST INCOME

|

|

December 31

|

|

|

Table I

|

|

2021

|

|

|

2020

|

|

|

(dollars in thousands)

|

|

Average Balance

|

|

|

Income/

Expense

|

|

|

Yield/

Average

|

|

|

Average Balance

|

|

|

Income/

Expense

|

|

|

Yield/

Average

|

|

|

Assets

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest-earning assets:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest-bearing balances with banks

|

|

$

|

136,071

|

|

|

$

|

195

|

|

|

|

0.14

|

%

|

|

$

|

78,211

|

|

|

$

|

274

|

|

|

|

0.35

|

%

|

|

Securities:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Taxable

|

|

|

162,511

|

|

|

|

2,179

|

|

|

|

1.34

|

|

|

|

118,090

|

|

|

|

2,409

|

|

|

|

2.04

|

|

|

Tax exempt

|

|

|

8,646

|

|

|

|

297

|

|

|

|

3.44

|

|

|

|

9,231

|

|

|

|

359

|

|

|

|

3.90

|

|

|

Loans

|

|

|

841,681

|

|

|

|

42,519

|

|

|

|

5.05

|

|

|

|

811,434

|

|

|

|

43,571

|

|

|

|

5.37

|

|

|

Total interest-earning assets

|

|

|

1,148,909

|

|

|

|

45,190

|

|

|

|

3.93

|

%

|

|

|

1,016,966

|

|

|

|

46,613

|

|

|

|

4.58

|

%

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Noninterest-earning assets:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Cash and due from banks

|

|

|

14,739

|

|

|

|

|

|

|

|

|

|

|

|

13,619

|

|

|

|

|

|

|

|

|

|

|

Other nonearning assets

|

|

|

77,254

|

|

|

|

|

|

|

|

|

|

|

|

73,395

|

|

|

|

|

|

|

|

|

|

|

Allowance for loan losses

|

|

|

(7,101

|

)

|

|

|

|

|

|

|

|

|

|

|

(7,789

|

)

|

|

|

|

|

|

|

|

|

|

Total noninterest-earning assets

|

|

|

84,892

|

|

|

|

|

|

|

|

|

|

|

|

79,225

|

|

|

|

|

|

|

|

|

|

|

Total assets

|

|

$

|

1,233,801

|

|

|

|

|

|

|

|

|

|

|

$

|

1,096,191

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Liabilities and Shareholders’ Equity

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest-bearing liabilities:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NOW accounts

|

|

$

|

211,636

|

|

|

$

|

680

|

|

|

|

0.32

|

%

|

|

$

|

177,170

|

|

|

$

|

618

|

|

|

|

0.35

|

%

|

|

Savings and money market

|

|

|

299,129

|

|

|

|

265

|

|

|

|

0.09

|

|

|

|

258,434

|

|

|

|

932

|

|

|

|

0.36

|

|

|

Time deposits

|

|

|

200,572

|

|

|

|

2,032

|

|

|

|

1.01

|

|

|

|

211,909

|

|

|

|

3,704

|

|

|

|

1.75

|

|

|

Other borrowed money

|

|

|

26,064

|

|

|

|

564

|

|

|

|

2.16

|

|

|

|

31,916

|

|

|

|

729

|

|

|

|

2.28

|

|

|

Subordinated debentures

|

|

|

8,500

|

|

|

|

158

|

|

|

|

1.86

|

|

|

|

8,500

|

|

|

|

208

|

|

|

|

2.44

|

|

|

Total int.-bearing liabilities

|

|

|

745,901

|

|

|

|

3,699

|

|

|

|

0.49

|

%

|

|

|

687,929

|

|

|

|

6,191

|

|

|

|

0.90

|

%

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Noninterest-bearing liabilities:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Demand deposit accounts

|

|

|

331,027

|

|

|

|

|

|

|

|

|

|

|

|

258,802

|

|

|

|

|

|

|

|

|

|

|

Other liabilities

|

|

|

18,042

|

|

|

|

|

|

|

|

|

|

|

|

18,422

|

|

|

|

|

|

|

|

|

|

|

Total noninterest-bearing liabilities

|

|

|

349,069

|

|

|

|

|

|

|

|

|

|

|

|

277,224

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Shareholders’ equity

|

|

|

138,831

|

|

|

|

|

|

|

|

|

|

|

|

131,038

|

|

|

|

|

|

|

|

|

|

|

Total liabilities and shareholders’ equity

|

|

$

|

1,233,801

|

|

|

|

|

|

|

|

|

|

|

$

|

1,096,191

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Net interest earnings

|

|

|

|

|

|

$

|

41,491

|

|

|

|

|

|

|

|

|

|

|

$

|

40,422

|

|

|

|

|

|

|

Net interest margin

|

|

|

|

|

|

|

|

|

|

|

3.61

|

%

|

|

|

|

|

|

|

|

|

|

|

3.97

|

%

|

|

Net interest rate spread

|

|

|

|

|

|

|

|

|

|

|

3.44

|

%

|

|

|

|

|

|

|

|

|

|

|

3.68

|

%

|

|

Average interest-bearing liabilities to average earning assets

|

|

|

|

|

|

|

|

|

|

|

64.92

|

%

|

|

|

|

|

|

|

|

|

|

|

67.65

|

%

|

Fully taxable equivalent yields are reported for tax exempt securities and loans and calculated assuming a 21% tax rate, net of nondeductible interest expense. Tax-equivalent

adjustments for securities during the years ended December 31, 2021 and 2020 totaled $61 and $73, respectively. Tax-equivalent adjustments for loans during the years ended December 31, 2021 and 2020 totaled $417 and $367, respectively. Average

balances are computed on an average daily basis. The average balance for available for sale securities includes the market value adjustment. However, the calculated yield is based on the securities’ amortized cost. Average loan balances include

nonaccruing loans. Loan income includes cash received on nonaccruing loans.

|

RATE VOLUME ANALYSIS OF CHANGES IN INTEREST INCOME & EXPENSE

|

|

Table II

|

|

(dollars in thousands)

|

|

2021

|

|

|

2020

|

|

|

|

|

Increase (Decrease)

From Previous Year Due to

|

|

|

Increase (Decrease)

From Previous Year Due to

|

|

|

|

|

Volume

|

|

|

Yield/Rate

|

|

|

Total

|

|

|

Volume

|

|

|

Yield/Rate

|

|

|

Total

|

|

|

Interest income

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest-bearing balances with banks

|

|

$

|

136

|

|

|

$

|

(215

|

)

|

|

$

|

(79

|

)

|

|

$

|

287

|

|

|

$

|

(1,285

|

)

|

|

$

|

(998

|

)

|

|

Securities:

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Taxable

|

|

|

744

|

|

|

|

(974

|

)

|

|

|

(230

|

)

|

|

|

14

|

|

|

|

(540

|

)

|

|

|

(526

|

)

|

|

Tax exempt

|

|

|

(22

|

)

|

|

|

(40

|

)

|

|

|

(62

|

)

|

|

|

(64

|

)

|

|

|

(9

|

)

|

|

|

(73

|

)

|

|

Loans

|

|

|

1,587

|

|

|

|

(2,639

|

)

|

|

|

(1,052

|

)

|

|

|

2,048

|

|

|

|

(4,584

|

)

|

|

|

(2,536

|

)

|

|

Total interest income

|

|

|

2,445

|

|

|

|

(3,868

|

)

|

|

|

(1,423

|

)

|

|

|

2,285

|

|

|

|

(6,418

|

)

|

|

|

(4,133

|

)

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

Interest expense

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

NOW accounts

|

|

|

114

|

|

|

|

(52

|

)

|

|

|

62

|

|

|

|

49

|

|

|

|

31

|

|

|

|

80

|

|

|

Savings and money market

|

|

|

127

|

|

|

|

(794

|

)

|

|

|

(667

|

)

|

|

|

111

|

|

|

|

(469

|

)

|

|

|

(358

|

)

|

|

Time deposits

|

|

|

(189

|

)

|

|

|

(1,483

|

)

|

|

|

(1,672

|

)

|

|

|

(67

|

)

|

|

|

(427

|

)

|

|

|

(494

|

)

|

|

Other borrowed money

|

|

|

(128

|

)

|

|

|

(37

|

)

|

|

|

(165

|

)

|

|

|

(125

|

)

|

|

|

(29

|

)

|

|

|

(154

|

)

|

|

Subordinated debentures

|

|

|

----

|

|

|

|

(50

|

)

|

|

|

(50

|

)

|

|

|

----

|

|

|

|

(148

|

)

|

|

|

(148

|

)

|

|

Total interest expense

|

|

|

(76

|

)

|

|

|

(2,416

|

)

|

|

|

(2,492

|

)

|

|

|

(32

|

)

|

|

|

(1,042

|

)

|

|

|

(1,074

|

)

|

|

Net interest earnings

|

|

$

|

2,521

|

|

|

$

|

(1,452

|

)

|

|

$

|

1,069

|

|

|

$

|

2,317

|

|

|

$

|

(5,376

|

)

|

|

$

|

(3,059

|

)

|

|

The change in interest due to volume and rate is determined as follows: Volume Variance - change in volume multiplied by the previous year's rate; Yield/Rate Variance - change in

rate multiplied by the previous year's volume; Total Variance – change in volume multiplied by the change in rate. The change in interest due to both volume and rate has been allocated tovolume and rate changes in proportion to the

relationship of the absolute dollar amounts of the change in each. The tax exempt securities and loan income is presented on an FTE basis. FTE yield assumes a 21% tax rate, net of related nondeductible interest expense.

|

The Company’s interest and fees from its residential real estate loan portfolio decreased $2,113, or 16.2%, during 2021. The decrease was impacted by lower average balances,

yields and fees on the residential real estate loan portfolio during 2021. Residential real estate loan yields were negatively impacted by a sustained low rate environment in 2021. Lower average residential real estate loan balances in 2021 came

mostly from the Bank’s warehouse lending volume. Warehouse lending consists of a line of credit provided by the Bank to another mortgage lender that makes loans for the purchase of one- to four-family residential real estate properties. The

mortgage lender eventually sells the loans and repays the Bank. As mortgage refinancings reached their peak during the second half of 2020, the volume of warehouse lending balances decreased to zero at June 30, 2021. As a result, average warehouse

lending balances decreased from $25,110 in 2020 to $7,214 in 2021. The sustained low rate environment combined with less mortgage refinancings also contributed to a shift into more long-term fixed-rate mortgages (up $4,284) and less short-term

adjustable-rate mortgages (down $11,044) during 2021. Lower real estate loan fees were the result of fewer loan modifications during 2021. During 2020, residential real estate loan interest and fees decreased by $679, or 5.0%. The change in 2020

was impacted by lower residential real estate loan yields that completely offset higher loan fees. Residential real estate loan yields were negatively impacted by the low rate environment in 2020. The impact of lower loan yields completely offset a

$132 increase in loan fees during 2020. Higher loan fees were largely the result of loan modifications that were generated under the CARES Act. The low interest rate environment in 2020 caused a significant amount of mortgage refinancings to

occur. As a result, the Company experienced a portfolio shift from payoffs and maturities within its long-term fixed-rate mortgages to new short-term adjustable-rate mortgages during 2020. Furthermore, the Company sold a portion of its long-term,

fixed-rate real estate loans to the Federal Home Loan Mortgage Corporation, while retaining the servicing rights for those mortgages. This strategy was successful in generating a significant amount of loan sale and servicing fee revenue within

noninterest income during 2020.

The Company’s interest income from taxable investment securities decreased $230, or 9.6%, in 2021 and $526, or 17.9%, in 2020. For 2021, the Company took

opportunities to reinvest a portion of excess deposits into new U.S. Government, U.S. Government sponsored entity and Agency mortgage-backed securities, which contributed to a $44,421 increase in average taxable securities. However, the positive

impacts from higher average taxable securities was completely offset by a 70 basis point decline in taxable securities yield from 2.04% to 1.34%. This was primarily due to investment purchases and reinvestment of maturities at market rates lower

than the average portfolio yield. For 2020, the decrease in income on taxable securities was heavily influenced by the short-term rate decreases from March 2020 in response to COVID-19.

Total interest expense incurred on the Company’s interest-bearing liabilities decreased $2,492, or 40.3%, during 2021, and $1,074, or 14.8%, during 2020. The decreases in

interest expense during 2021 and 2020 were largely the result of a decline in market rates during March 2020. The Company’s strategy continues to focus on funding earning asset growth with lower cost, core deposit funding sources to further

reduce, or limit growth in, interest expense. With the FRB’s action to reduce short-term rates in 2020, the Bank saw many of its interest-bearing deposit products reprice downward. This led to a decrease in the Company’s weighted average costs from

0.90% at year-end 2020 to 0.49% at year-end 2021. This caused the interest cost on most deposit products to decrease during 2020 and 2021. However, the pace of interest expense savings was slowed during 2020 due to a lag in repricing on deposits.

Given the Company’s asset-sensitivity, decreases in short-term interest rates had a negative impact on net interest income in that interest-earning assets repriced faster than interest-bearing liabilities. This delayed the positive impact that

lower market rates had on reducing deposit expense during most of 2020, particularly with CDs. The Company can only benefit from lower CD interest expense to the extent that new CDs at lower rates could be issued. As CD rates have continued to

reprice downward, the Company has experienced more of an interest expense savings in 2021 than in 2020. The Company’s repricing efforts continued in 2021 with a rate reduction to the Company’s prime investment deposit account, which had a

significant impact in lowering money market expense during 2021. Lower rates on deposits also contributed to less of a consumer demand for CDs in 2020 and 2021, which caused a shift into more NOW, savings and money market balances. This composition

shift from higher-cost CDs to lower-cost NOW, savings and money market accounts helped to reduce the Company’s interest expense during 2020 and 2021.

The Company’s interest expenses were also impacted by other borrowed money and subordinated debentures, which were

down collectively by $215, or 22.9%, during the year ended 2021, and $302, or 24.4% during the year ended 2020. The decreases were primarily from the average balance decrease in FHLB borrowings caused by principal repayments during both 2020 and

2021, and the average cost decrease of subordinated debentures during both periods.

During 2021, the Company’s net interest margin was negatively impacted by the decreasing market rates that contributed to lower earning asset yields. The negative impact from

2020’s interest rate cuts by the FRB materially reduced interest income on earning assets during 2021. The margin was also negatively impacted by a larger amount of excess deposits being maintained at the Federal Reserve yielding below 0.25%.

However, the margin benefited from a larger reduction to interest costs in 2021 due to the lagging effect in CD rates that limited cost savings in 2020. These factors contributed to a decline in the net interest margin from 3.97% in 2020 to 3.61%

in 2021. The Company’s primary focus is to invest its funds into higher-yielding assets, particularly loans, as opportunities arise. However, if loan balances do not continue to expand and remain a larger component of overall earning assets, the

Company will face pressure within its net interest income and margin improvement.

PROVISION EXPENSE

Credit risk is inherent in the business of originating loans. The Company sets aside an allowance for loan losses through charges to income, which are reflected in the

consolidated statement of income as the provision for loan losses. Provision for loan loss is recorded to achieve an allowance for loan losses that is adequate to absorb losses in the Company’s loan portfolio. Management performs, on a quarterly

basis, a detailed analysis of the allowance for loan losses that encompasses loan portfolio composition, loan quality, loan loss experience and other relevant economic factors.

The Company’s provision expense decreased $3,399 from 2020 to 2021 in large part due to the addition of a new risk reserve allocation in March 2020 for COVID-19 that was less

impactful in 2021. The risk factor was necessary to account for the changes in economic conditions resulting from increases in unemployment that would produce higher anticipated losses as a result of COVID-19. Given that the economic scenarios

deteriorated significantly since the pandemic was declared in early March 2020, it was determined the credit risk in the loan portfolio had increased, resulting in the need for an additional reserve for credit loss. As a result, the general reserve

allocation related to COVID-19 totaled $2,315 at December 31, 2020, which had a corresponding impact to provision expense. During 2021, the Company did not experience any significant charge-offs related to COVID-19, but continued to monitor the

related economic effects that the pandemic had on the allowance for loan losses. At December 31, 2021, the general reserve allocation related to COVID-19 totaled $2,633.

Provision expense during 2021 was further impacted by a $1,332, or 83.8%, decrease in net-charge offs on loans that had not already been specifically allocated for in prior

years. Gross charge-offs totaled $1,481 during 2021, a decrease of $1,552 compared to 2020. Lower gross charge-offs during 2021 were experienced primarily within the commercial real estate and consumer loan portfolios.

Excluding the risk factors from COVID-19, the Company also recognized lower provision expense from general allocations during 2021. The Company’s general allocation evaluates

several factors that include: loan volume, average historical loan loss trends, credit risk, regional unemployment conditions, asset quality, and changes in classified and criticized assets. Provision expense decreases arising from general

allocations were mostly impacted by a decrease in the Company’s historical loan loss factor, which trended down from 0.24% at year-end 2020 to 0.18% at year-end 2021. Further contributing to lower provision expense were decreases in loan balances

generally allocated for at December 31, 2021 compared to December 31, 2020, primarily within the residential real estate loan portfolio. The risk associated with the decline in loans generated lower general reserves and a corresponding decrease to

provision expense. Lower provision expense during 2021 also came from decreases in both criticized and classified assets, as well as lower nonperforming loans that yielded less general allocations. Criticized and classified assets within the

commercial loan portfolio collectively decreased $4,610, or 28.2%, from year-end 2020 to year-end 2021. Furthermore, the Company’s nonperforming loans to total loans were 0.56% at year-end 2021, as compared to 0.82% at year-end 2020, while

nonperforming assets to total assets were 0.37% at year-end 2021 and 0.59% at year-end 2020.

Partially offsetting the decreasing effects to provision expense mentioned above were higher specific allocations. Specific allocations of the allowance for loan losses

identify loan impairment by measuring fair value of the underlying collateral and the present value of estimated future cash flows. The provision expense for specific allocations increased $315 during 2021 in large part to unused reserve

allocations from 2020. During the first quarter of 2020, charge-offs of $502 were taken on two commercial real estate properties that contained an $807 specific allocation from the prior year. As a result, $305 of the unused specific reserve was

reversed from the allowance for loan losses. Therefore, provision expense was lowered by $305 in 2020 due to the unused reserve, which had a reverse impact to higher provision expense in 2021.

Management believes that the allowance for loan losses was adequate at December 31, 2021, and reflected probable incurred losses in the portfolio. The allowance for loan

losses was 0.78% of total loans at December 31, 2021, as compared to 0.84% at December 31, 2020. There can be no assurance, however, that adjustments to the allowance for loan losses will not be required in the future. Changes in the

circumstances of particular borrowers, as well as adverse developments in the economy, particularly with respect to COVID-19, could cause further increases in the required allowance for loan losses and require additional provision expense. Asset

quality will continue to remain a key focus, as management continues to stress not just loan growth, but quality in loan underwriting as well. Future provisions to the allowance for loan losses will continue to be based on management’s quarterly

in-depth evaluation that is discussed in further detail below under the caption “Critical Accounting Policies - Allowance for Loan Losses” within this Management’s Discussion and Analysis.

NONINTEREST INCOME

During 2021, total noninterest income decreased $1,574, or 13.8%, as compared to 2020. The decrease in noninterest revenue was primarily impacted by proceeds of $2,000

received in a litigation settlement with a third-party in 2020. During the first quarter of 2020, the Bank entered into a settlement agreement related to the previously disclosed litigation the Bank had filed against a third-party tax software

product provider for breach of contract. Under the settlement agreement, the third-party paid a $2,000 settlement payment to the Bank in March 2020, which was recorded as noninterest income. As part of the settlement agreement, the Bank is

processing a certain amount of tax items, which started in 2021 and will end in 2025. As a result, the Bank recognized $675 in ERC/ERD income during 2021, which helped to partially offset the effects of the settlement proceeds received in 2020.

Noninterest income during 2021 was also impacted by losses of $1,066 realized on the sale of investment securities. During the fourth quarter of 2021, the Company received

proceeds of $47,666 from the sale of thirteen securities totaling $48,732 at a weighted average yield of 0.89%. The lower-yielding securities were replaced with similar securities with a higher weighted average yield of 1.30%. The transaction is

expected to increase future income and have a positive impact to the margin.

Noninterest income was negatively impacted by a decrease in mortgage banking income affected by a lower volume of real estate loans sold to the secondary market in 2021. To

help manage consumer demand for longer-term, fixed-rate real estate mortgages during a low interest rate environment, the Company will sell a portion of the real estate loan volume it originates during that period. The decision to sell long-term

fixed-rate mortgages at lower rates will also help to minimize the interest rate risk exposure to rising rates. Market rates in 2020 were decreased in response to the pandemic, and as a result, the Company experienced a significant increase in the

number of loans sold to the secondary market during that time. This period of significant mortgage refinancings generated more income during 2020 than 2021, which contributed to a $400, or 31.9%, decrease in mortgage banking income during the year

ended December 31, 2021, as compared to the same period in 2020.

Noninterest income was positively impacted in 2021 by an increase in the Company’s interchange income from a higher volume of transactions and new card issuances of its debit

and credit card products. This was largely impacted by the economic stimulus proceeds received by customers due to the COVID-19 pandemic that has increased consumer spending. As a result, debit and credit card interchange income increased $613, or

15.2%, during 2021, as compared to 2020.

Other noninterest income also increased $167, or 21.4%, during 2021, as compared to 2020. This was primarily impacted by the sale of Bank owned property during 2021, which

contributed to a $193 increase in the gains on property sales. The increases were impacted by the sale of vacant land in Lawrence County, Ohio and a branch building in Jackson, Ohio that had been acquired as part of the merger with the Milton

Banking Company in 2016.

Noninterest income was also positively impacted in 2021 by an increase in the Company’s tax preparation fee income, which was up $110, or 17.1%, during the year ended December

31, 2021, as compared to the same period in 2020. As previously discussed, the Company changed its business model in 2020 from assessing TAL fees to assessing tax preparation fees in response to a state law enacted in 2019. By charging for the

tax preparation services, the Company recorded $754 in tax preparation fee income during the year ended December 31, 2021, as compared to $644 during the same period in 2020.

The Company’s remaining noninterest income categories increased $327, or 12.0%, during the year ended 2021 as compared to 2020. This was in large part due to a $179 increase

in service charges on deposits, impacted by a surge in consumer spending during 2021. The Company also experienced an $84 increase in income from bank owned life insurance (“BOLI”) and annuity assets during 2021, in part due to BOLI death benefit

proceeds received in 2021.

NONINTEREST EXPENSE

Management continues to work diligently to minimize noninterest expense. For 2021, total noninterest expense increased $1,147, or 3.2%, as compared to 2020. The Company’s

largest noninterest expense item, salaries and employee benefits, was limited to a $13, or 0.1%, increase during 2021. This minimal change in expense was partly impacted by the costs associated with the severance package payout of an employee from

September 2020 that had a reverse effect in 2021. Expense savings were also impacted by a lower employee base, with the Bank’s average full-time equivalent employee base at 233 employees at year-end 2021 compared to 241 employees at year-end 2020.

This cost savings helped to offset the expenses associated with annual merit increases associated with the improved financial performance achieved in 2021.

The Company also experienced an increase in software expense during 2021, which was up $404, or 27.8%, over the year ended 2020. The increase was primarily related to the

purchase of software to enhance the platform used for the loan origination process. Software cost increases were also impacted by the use of a portal to process PPP loans during 2021. The loan portal costs were completely offset by the PPP loan

fees that were recorded during 2021.

Data processing expense also increased $236, or 10.9%, during 2021. Higher costs in this category were the direct result of the large volume increase in debit and credit card

transactions, which increased processing costs. Transaction volume can be partly tied to the various stimulus programs offered by the government that benefited the consumer during 2021.

Also contributing to higher noninterest expense were the Company’s marketing costs, which increased $213, or 34.8%, during 2021 compared to 2020. During 2020, COVID-19

significantly disrupted consumer behavior and caused banking center lobbies to be limited or closed. As a result, the opportunities to advertise and promote the brand of the Company were very limited in 2020. The pandemic environment, consisting of

social distancing, self-quarantining and remote working arrangements, slowed many of the marketing goals that were set in 2020, which led to lower expense during that time. The Company resumed its marketing campaigns during 2021, with less of an

impact from the pandemic-related factors of the previous year.

FDIC insurance costs were up $161, or 97.6%, during 2021 compared to 2020. During 2020, the Bank utilized its remaining FDIC credits that were issued in September 2019. The

Bank’s FDIC assessments during the first half of 2020 were reduced by $115 in credits. The Bank fully exhausted all of its credits as of June 30, 2020 and did not recognize any premium expense discounts during the rest of 2020.

Other noninterest expense increased $129, or 2.4%, during 2021 compared to 2020. During the fourth quarter of 2021, the Company redeemed $3,187 in long-term FHLB advances that

had been used to fund fixed rate loans. The specific loans being funded were paid off, which permitted the Company to redeem the advances. By redeeming the advances, a prepayment penalty of $186 was incurred, which contributed to the increase in

other noninterest expense. Also impacting other noninterest expense were various overhead costs from Race Day, including loan expense and consulting fees, being offset by a reduction in the Bank’s customer incentive costs during 2021.

The remaining noninterest expense categories decreased $9, or 0.2%, during the year-ended 2021, as compared to 2020.

The Company's efficiency ratio is defined as noninterest expense as a percentage of fully tax-equivalent net interest income plus noninterest income. The effects from provision

expense are excluded from the efficiency ratio. Management continues to place emphasis on managing its balance sheet mix and interest rate sensitivity as well as developing more innovative ways to generate noninterest revenue. During 2021, the

Company’s asset yields were negatively impacted by market rate reductions related to COVID-19. Growth in average earning assets, higher loan fees, and redeploying excess Federal Reserve Bank balances into securities helped to generate a 2.6%

increase in net interest income. However, this increase was completely offset by a 13.8% decrease in noninterest income, which was impacted by the receipt of $2,000 in litigation proceeds in 2020 and $1,066 in realized losses from the sale of

securities in 2021. This was also combined with a 3.2% increase in overhead costs impacted by higher software, data processing and marketing expenses during 2021. As a result, the Company’s efficiency number increased (regressed) from 69.67% at

December 31, 2020, to 72.59% at December 31, 2021.

PROVISION FOR INCOME TAXES

The provision for income taxes during 2021 totaled $2,284, compared to $2,048 in 2020. The effective tax rates for 2021 and 2020 were 16.3% and 16.6%, respectively. The

decrease in the effective tax rate in 2021 was mostly impacted by additional costs associated with certain nondeductible retirement benefit plans during 2020.

FINANCIAL CONDITION:

CASH AND CASH EQUIVALENTS

The Company’s cash and cash equivalents consist of cash, as well as interest- and non-interest bearing balances due from other banks. The amounts of cash and cash equivalents

fluctuate on a daily basis due to customer activity and liquidity needs. At December 31, 2021, cash and cash equivalents had increased $13,731 to $152,034, compared to $138,303 at December 31, 2020. The increase in cash and cash equivalents came

mostly from higher interest-bearing deposits on hand with correspondent banks. At December 31, 2021, the Company’s interest-bearing Federal Reserve clearing account represented over 89% of cash and cash equivalents. The Company utilizes its

interest-bearing Federal Reserve clearing account to manage excess funds, as well as to assist in funding earning asset growth. The primary factor for the significant influx in clearing account balances was the investment of heightened deposit

balances received during 2021 as a result of the pandemic environment. At December 31, 2021, total deposits increased $66,169 from year-end 2020 in relation to customers receiving stimulus funds from various government programs and their desire to

preserve cash during the uncertain economic environment. Furthermore, several congressional acts led to the extension of the PPP loan program during the first half of 2021. Under the reopened PPP, commercial business customers received loan

proceeds, which helped to generate higher levels of investable deposits during the first quarter of 2021. During the second quarter of 2021, the Company utilized a portion of its clearing account balances and proceeds from the payoffs of PPP loans

to reinvest in higher-yielding investment securities. This redeployment of assets from year-end 2020 into higher-yielding investment securities lowered the dilutive effect that higher clearing account balances was having on the net interest

margin. The interest rate paid on both the required and excess reserve balances of the Federal Reserve Bank account is based on the targeted federal funds rate established by the Federal Open Market Committee. During the first quarter of 2020, the

rate associated with the Company’s Federal Reserve Bank clearing account decreased 150 basis points due to concerns about the impact of COVID-19 on the economy, resulting in a target federal funds rate range of 0% to 0.25%. Although

interest-bearing deposits in the Federal Reserve Bank are the Company's lowest-yielding interest-earning asset, the investment rate is higher than the rate the Company would have received from its investments in federal funds sold. Furthermore,

Federal Reserve balances are guaranteed by the U.S. Government.

As liquidity levels continuously vary based on consumer activities, amounts of cash and cash equivalents can vary widely at any given point in time. The Company’s focus during

periods of heightened liquidity will be to invest excess funds into longer-term, higher-yielding assets, primarily loans, when the opportunities arise. Further information regarding the Company’s liquidity can be found below under the caption

“Liquidity” in this Management’s Discussion and Analysis.

CERTIFICATES OF DEPOSIT IN FINANCIAL INSTITUTIONS

At December 31, 2021, the Company had $2,329 in CDs owned by the Captive, down $171, or 6.8%, from year-end 2020. The deposits on hand at December 31, 2021, consist of ten

certificates with remaining maturity terms ranging from less than 5 months up to 21 months.

SECURITIES

Management's goal in structuring its investment securities portfolio is to maintain a prudent level of liquidity and to provide an acceptable rate of return without sacrificing

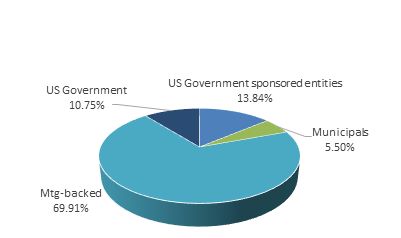

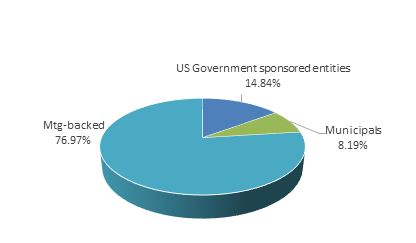

asset quality. During 2021, the balance of total securities increased $64,952, or 53.1%, compared to year-end 2020. The Company’s investment securities portfolio is made up mostly of Agency mortgage-backed securities, representing 69.9% of total

investments at December 31, 2021. During the year ended 2021, the Company utilized a portion of its heightened excess deposits to purchase investment securities with the intent of minimizing the amount of funds being maintained within the

lower-yielding interest-bearing Federal Reserve clearing account. This resulted in $75,231 of new Agency mortgage-backed securities, while receiving principal repayments of $35,976. The monthly repayment of principal has been the primary advantage

of Agency mortgage-backed securities as compared to other types of investment securities, which deliver proceeds upon maturity or at a specified call date. The Company also used excess deposits to purchase $20,224 in U.S. Government securities,